Embed Size (px)

Citation preview

IX. SYMPOSIUM ZUR ÖKONOMISCHEN ANALYSE DER UNTERNEHMUNG

Managerial versus Financial Transfer Pricing

Jan T. Martini

Session B1

GERMAN ECONOMIC ASSOCIATION OF BUSINESS ADMINISTRATION – GEABA

Einreichung zumIX. Symposium zur ökonomischen Analyse der Unternehmung

GEABA, Universität Augsburg

Managerial versus financial

transfer pricing

Jan Thomas Martini∗

May 2008

Abstract: Transfer prices coordinate managerial decisions in decentralizedfirms. By allocating the group’s profit to its subsididiaries they also servefinancial purposes, including taxation and profit distribution. Given thatboth managerial and financial purposes are commonly served by the sametransfer price, it seems obvious that the optimal transfer price for the groupinduces a trade-off. Based on a model of a decentralized group with asym-metric information and specific investment, this paper shows that this con-clusion does not hold in general. In fact, the group benefits from addinga managerial perspective when transfer pricing solely serves financial pur-poses. A policy of managerial transfer pricing, however, does not necessar-ily benefit from integrating financial aspects. The paper sheds light on theperformance of various transfer pricing policies characterized by differenttypes of decentralization and thereby on the competition of managerial andfinancial objectives in transfer pricing.

Keywords: Transfer Pricing, Decentralization, Management Control, Finan-cial Accounting, Taxation

JEL classification: M41, L22, H25

∗Bielefeld University, Department of Business Administration and Economics, P.O. Box 100131, D–33501Bielefeld, Germany, [email protected]

1 Introduction

Transfer prices are valuations of products and services within a firm and represent acommon and important instrument in management accounting, financial reporting,and taxation.1 Transfer prices essentially perform two tasks, namely coordination andprofit allocation.2

Coordination implies the alignment of delegated decisions with the goals of the de-centralized organization.3 Vertically integrated profit centers are a typical applicationof transfer pricing. The coordinative effect arises because transfer prices value inter-mediates traded between the centers and thus determine their costs and revenues ofsuch internal trade. The role of transfer prices for profit allocation is to quantify a sub-unit’s contribution to firm-wide profit. It is most important for external purposes suchas financial reporting, profit taxation, and profit distribution. Thus, important stake-holders like the shareholders and tax authorities have a vital interest in the allocationof firm-wide profit. Coordination and profit allocation are tightly linked to each other,especially when the firm relies on a single transfer price for internal and external pur-poses. This case of a single set of books, however, is descriptive for business practice.Accordingly, Ernst & Young (2001, p. 6) report that 77 percent of 638 multinational par-ent companies use the same transfer price for both tax and management purposes.4

This paper deals with the optimal focus when setting transfer prices from the firm’sperspective. On the one side, transfer prices may concentrate on management, i.e.,operational efficiency, and thus focus on pre-tax profitability. This approach reflects apolicy aiming at optimal coordination disregarding issues of profit allocation. On theother side, the choice of transfer prices may be driven by financial aspects and thusminimize the organization’s tax burden and profits distributed to minority sharehold-ers. This approach exclusively refers to issues of profit allocation. The third approachis to integrate managerial and financial goals.

The research question seems trivial since the firm apparently should go for that trans-fer price which optimally trades off managerial and financial goals.5 Yet, Ernst & Young(2001, p. 6) report that 21 percent, respectively 26 percent, of 638 multinational parentcompanies primarily base their transfer prices on ”management/operations“, respec-tively on tax considerations. 52 percent use a compromise. Furthermore, these differentperspectives are reflected by the location of the transfer pricing authority within the or-ganization. Accordingly, Ernst & Young (2001, p. 7) find, inter alia, that 65 percent,respectively 29 percent, of the parents relying on a single transfer price place the pri-mary responsibility for setting transfer prices on the tax department, respectively onthe business units leaders.6 This paper draws on the empirical evidence and proposesa model of asymmetric information and delegation which allows to answer the researchquestion in a non-trivial way.

1For instance, Tang (2002, 32) and Tang (1993, 68) find that 88 percent of 95 Fortune 1000 companies and92 percent of 143 Fortune 500 companies use transfer prices.

2See, e.g., Tang (2002, 42) or Anthony and Govindarajan (2000, 201) for functions of (international) trans-fer prices and their empirical prevalence.

3See, e.g., Horngren, Datar, and Foster (2006, ch. 22) or Milgrom and Roberts (1992) for decentralizationand management control.

4Ernst & Young (2003, 17) find a corresponding share of 80 percent.5See, for instance, Baldenius, Melumad, and Reichelstein (2004) for a corresponding model and result.6Respondents were allowed to give multiple answers.

1

The most salient result of the paper is that the performance of a decentralized firm’stransfer pricing system benefits from adding a managerial perspective but that man-agerial transfer prices do not necessarily benefit from adding a financial perspective.Therefore, besides a fully centralized policy, the efficient policies imply either to go onlyfor managerial goals or to go for both managerial and financial goals. Roughly speak-ing, a decentralized organization should not solely put the tax department in charge oftransfer pricing whereas doing without it may be optimal. Moreover, the firm’s opti-mal degree of decentralization decreases, respectively increases, in the optimal weighton financial goals, respectively on managerial goals. The results are mainly driven bythe information asymmetry of the profit center organization so that there is no deci-sion maker who has both the necessary information and the incentive to maximize thegroup’s net profit.

The analysis is based on a model of two vertically integrated subsidiaries of a multi-national group generating a surplus from internal trade due to a specific investmentinto the reduction of production costs. In contrast and as a contribution to the liter-ature this paper explicitly models a situation of asymmetric information in which thegroup responds to the competition of managerial and financial goals by transfer pricingpolicies implying different types and degrees of delegation. Delegation pertains to thetransfer pricing authority as well as to the trade decisions, while the decision on the costreduction investment stays with corporate management. Since the policies respond tothe friction between managerial and financial goals in different ways it is possible toestablish a link between this trade-off and the modes of delegation. In particular, thecomparison of the policies shows for which parameter settings a given policy is thegroup’s best choice. Thereby it is possible to associate the importance of managerialversus financial goals with exogenous parameters such as the tax rates. The main partof the analysis assumes a single set of books. Two sets of books are discussed as anextension.

Related literature is found in the context of transfer pricing for international taxation.While most of the contributions assume centralized firms some consider decentraliza-tion. Nielsen, Raimondos-Møller, and Schjelderup (2006, 2003), Narayanan and Smith(2000), and Schjelderup and Sorgard (1997) concentrate on transfer prices as strategicdevices in oligopolistic markets. Martini, Niemann, and Simons (2007) and Halperinand Srinidhi (1991) identify distortions induced by decentralization and tax regulations.Balachandran and Li (1996) design a mechanism using dual transfer prices. Hyde andChoe (2005) and Baldenius et al. (2004) are based on settings of two sets of books with-out explicitly modeling information asymmetry. Elitzur and Mintz (1996) also have twosets of books but take a public finance perspective when they concentrate on tax com-petition. Smith (2002b) analyzes two sets of books as well as the design of the divisionalperformance measure to disentangle managerial and financial goals.

The next section develops the model. Section 3 motivates the different transfer pric-ing policies and derives the corresponding transfer price and trade decisions. Section 4compares the policies from the group’s perspective. Section 5 extends the model withrespect to a more or less restrictive bandwidth of arm’s length prices and a second set ofbooks. Section 6 summarizes the results and concludes. All proofs are in the appendix.

2

2 Model description

We consider a model of two vertically integrated subsidiaries U and D of a multina-tional group. The upstream subsidiary U produces an intermediate product and sellsit either externally at positive market price r or internally to the group’s downstreamsubsidiary D at transfer price t. D finishes the intermediate and sells the final productat market price r f . In order to focus the analysis on transfer pricing issues, the sub-sidiaries’ production costs and the external markets are such that external trade gener-ates zero contribution margin. Therefore, U’s variable unit costs amount to r and D’svariable unit costs, exclusive of the intermediate’s costs, to r f − r > 0.

In the line of Williamson (1985), the group may save on production costs by a specificinvestment. The investment is specific because it exclusively affects variable produc-tion costs of intermediates traded internally, i.e., between U and D. It is either a successor a failure. A successful investment decreases U’s unit costs of producing and D’sunit costs of finishing the intermediate, whereas an investment failure increases thesecosts by the same amount. eu I denotes the magnitude of the symmetric effect on U’scosts where the nonnegative parameter eu reflects the efficacy of the nonnegative in-vestment I chosen at the corporate level.7 The corresponding effect on D’s costs is ed I.The outlay associated with the investment amounts to I2 on the group level and is fullyborne by the subsidiaries. Let au ∈ [0, 1] and ad = 1 − au denote the percentage ofthe investment outlay incurred by U and D, respectively. An example of such an in-vestment is the implementation of information technology aimed at the improvementof the supply chain management as deployed by Wal-Mart.8 Other examples are theredesign of products to better match the subsidiaries’ production technologies on theone hand and the redesign of production processes to better match the traded productson the other hand.

p denotes the probability of a successful investment. It is the realization of a uni-formly distributed random variable P having expectation 1/2 and range [1/2−∆, 1/2 +∆] with ∆ ∈ [0, 1/2].9 The low cost probability p is observed by the subsidiarieswhereas the group’s corporate management C only knows its distribution. Any otherinformation is common knowledge within the group. Note that the range parameter ∆

has two interpretations. First, it is a measure of information asymmetry between cor-porate management and the subsidiaries because it determines the range of possiblerealizations of the low cost probability which is privately observed by the subsidiaries.Second, it is a measure of the group’s cost saving potential. In order to minimize theexpected production costs for given investment it is necessary not to trade internally iffan increase of production costs is expected for internal trade, i.e., iff the low cost prob-ability p is below 1/2. Then the expected cost saving per unit before taxes amounts toE(

P(eu + ed)I − (1 − P)(eu + ed)I : P ≥ 1/2)

· prob(P ≥ 1/2) = ∆(eu + ed)I/2 whichis proportional to ∆. Bringing together both interpretations shows that ∆ is a measureof the value of cost information.

The cost information asymmetry between the subsidiaries and corporate manage-ment provides the argument that corporate management may set up a profit center or-

7The assumption of symmetric upside and downside potentials of the investment is not crucial to theanalysis but simplifies the presentation.

8See Chiles and Dau (2005) for the examples of Wal-Mart and Amazon.com.9The limit case ∆ = 0 can be derived from the following analysis by letting ∆ → 0.

3

ganization and delegate the production and marketing decisions to the subsidiaries.10

It is important that the model’s linear costing and pricing setup is such that the levelof internal trade captures all relevant production and marketing decisions. On the onehand, there is no profit associated with U’s external marketing or D’s external sourcingand marketing. Given the decision contexts of this model, on the other hand, no deci-sion maker would trade internally and then not finish the intermediate and sell it. Notefurther that the optimal internal trade decision is either zero or equals capacity. Nor-malizing both subsidiaries’ capacities to one simplifies the exposition so that q ∈ {0, 1}denotes the volume of internal trade.

Consistent with the information setting, corporate management C has three tasks.First, it decides whether to introduce a profit center organization and to delegate theproduction and marketing decisions to the subsidiaries. The centralized planning policyapplies if C decides not to decentralize these decisions. Second, given delegated prod-uct decisions, C decides on the delegation of the transfer pricing authority. Centralizedtransfer pricing leads to the integrated transfer pricing policy. For delegated transferpricing we consider two options: The managerial transfer pricing policy implies that thesubsidiaries take both the product and the transfer pricing decisions, whereas the finan-cial transfer pricing policy delegates transfer pricing to the tax department T. These fourtransfer pricing regimes form the basis of the analysis and are explained in more detailin Section 3. C’s third task is to budget the cost reduction investment.

These three tasks also represent the first two steps of the model’s time line: 1) Choiceof the transfer pricing policy, 2) budgeting of the investment I, 3) private observation ofthe low cost probability p, 4) choice of the constant unit transfer price t, 5) internal tradedecision q, 6) production and marketing, and 7) preparation of financial statements andfiling of tax declarations, taxation and distribution of profits.

All decision makers are assumed risk neutral. In line with the profit center organiza-tion and the information setting, each subsidiary seeks to maximize its expected profitafter taxes on an a posteriori basis, i.e., given the low cost probability p. The corre-sponding profits before taxes of subsidiaries U and D are denoted by Πu and Πd. Theyread

Πu(I, p, q, t) =(

t − p(r − eu I) − (1 − p)(r + eu I))

q − au I2

=(

t − r + (2p − 1)eu I)

q − au I2

and

Πd(I, p, q, t) =(

r f − t − p(r f − r − ed I) − (1 − p)(r f − r + ed I))

q − ad I2

=(

r − t + (2p − 1)ed I)

q − ad I2.

Both subsidiaries’ profits are given by the a posteriori expected contribution marginfrom internal trade less the subsidiary’s share of the investment outlay. The contri-bution margins consist of two parts: On the one hand, the terms (2p − 1)eu Iq and(2p − 1)ed Iq represent the expected cost reduction effects incurred by U and D, re-spectively. On the other hand, the terms (t − r)q and (r − t)q equal the subsidiaries’

10Other reasons for delegation involve motivation, complexity, and monitoring. See Grabski (1985) inaddition to the references given in footnote 3.

4

contribution margins before cost reduction. Note that the latter terms add to zero sothat they reflect profit shifting between the subsidiaries. For t = r, there is no profitshifting. For t > r, in contrast, some of D’s expected cost reduction is allocated to U viathe transfer price t. For t < r, profit is shifted from U to D. Let τu, τd ∈ [0, 1) denotethe subsidiaries’ profit tax rates. Then, assuming that the investment outlay is fullytax-deductible, the subsidiaries’ objective functions are (1 − τu)Πu and (1 − τd)Πd.

Corporate management maximizes the group’s a priori expected net profit, i.e., thegroup’s expected profit net of profit taxes and profits distributed to minority sharehold-ers without the observation of the low cost probability p. It is given by wu E(Πu) +wd E(Πd) with weights ws ∈

(

(1 − τs)/2, 1 − τs

]

, s ∈ {u, d}, which allow for sub-

sidiaries not fully owned by the group.11 Profit allocation does not play a role forwu = wd. Thus, asymmetric taxation, i.e., τu 6= τd, is neither a necessary nor a suf-ficient condition for the relevance of profit allocation.12

The tax department has the same information as corporate management and min-imizes group taxes and profits distributed to minority shareholders given the tradedecision. The corresponding objective function is (1 − wu) E(Πu) + (1 − wd) E(Πd).For ease of presentation, the following analysis does not point out explicitly whetherexpectations are a priori or a posteriori.

Note that this simple model captures some important features relevant to transferpricing: 1) Cooperation within the integrated group may be more profitable than trad-ing with non-related parties. 2) The subsidiaries have superior information on opera-tions. 3) The trade decisions and the transfer pricing responsibility may be delegated.4) Decentralization is based on profit centers. 5) The group relies on a single set ofbooks.13 6) The allocation of group profit is relevant. Furthermore, the model operateson a constant unit transfer price. With such ‘simple contract’ it is not possible for cor-porate management to engage in the design of a truth-telling mechanism in order toextract the subsidiaries’ superior knowledge.

3 Investments, trade decisions, and transfer prices

This section explains and motivates the four transfer pricing policies and derives theinvestment level, the internal trade decision, and the transfer price applying for each ofthem. Table 1 gives a summary of the decisions.

The analysis focuses on inner solutions for the investment decision. Therefore, weassume that the parameters are such that the investment decisions stated below do notimply negative variable production costs for U and D, i.e., the solutions satisfy eu I ≤ rand ed I ≤ r f − r. Furthermore, we focus on a scenario of a single set of books in whichthe bandwidth of arm’s length prices accepted by external stakeholders is assumedto be given by the interval [r − 2∆eu I, r + 2∆ed I]. See the end of Section 3.1 for moredetails on the bandwidth. Section 5 discusses a less or more restrictive bandwidth andscenarios involving two sets of books.

11It can be shown that linear compensations of subsidiaries’ managements can be integrated into theweights.

12Accordingly, the model is not restricted to multinational groups. However, it is the most intuitive andmost discussed application.

13See Section 5.2 for a relaxation of this assumption.

5

Dec

isio

nC

on

dit

ion

Po

licy

Inv

estm

ent

IT

ran

sfer

pri

cet

wit

hs,

s′∈{

u,d}

,s6=

s′

Man

ager

ial

TP

(wu

+w

d)∆

(eu

+e d

)

8(w

ua u

+w

da d

)r+

(2p−

1)(

wu

+w

d)∆(

e2 d−

e2 u

)

16(w

ua u

+w

da d

)

Fin

anci

alT

Pw

s∆e s

4(w

ua u

+w

da d

)r

ws>

ws′

,e s

′=

0

0r

ws>

ws′

,e s

′>

0∆

(eu

+e d

)

4(a

u+

a d)

rw

u=

wd

Inte

gra

ted

TP

w2 s∆

(eu

+e d

)2

4(w

s(e s

+2

e s′)−

ws′

e s′)(w

ua u

+w

da d

)r+

(wu−

wd)w

2 s∆

2e2 s′

(eu

+e d

)2

2(w

s(e s

+2

e s′ )−

ws′

e s′)2

(wu

a u+

wda d

)w

s≥

ws′

Cen

tral

ized

pla

nn

ing

(ws−

ws′)∆

e s′

wu

a u+

wda d

r+

2(w

u−

wd)∆

2e2 s′

wu

a u+

wda d

ws≥

ws′

Tab

le1:

Su

mm

ary

of

dec

isio

ns

6

3.1 Managerial transfer pricing

The managerial transfer pricing policy implies that the subsidiaries decide on bothtrade and the transfer price. Managerial transfer prices are freely negotiated by thesubsidiaries at date 4, i.e., when they have learned the investment level I chosen bycorporate management at date 2 and the low cost probability p realized at date 3. Sub-sequently, the subsidiaries make the internal trade decision at date 5 for given transferprice. Among the considered policies, managerial transfer pricing is characterized bythe highest degree of decentralization. The idea is to let those decide who have the bestinformation.

The analysis of managerial transfer pricing proceeds backwards starting with thetrade decision to determine the profit consequences for a given transfer price. Twocircumstances are fundamental to the analysis of the delegated trade decision: First, atdate 4 the investment outlay is sunk and therefore does not have to be considered in thetrade decision. The investment’s effect on production costs, however, will be reflectedby the trade decision. Second, the internal trade decision is a joint decision of bothsubsidiaries so that both of them have to agree to trade internally.14 The trade decisionunder managerial transfer pricing is given by Proposition 1.

Proposition 1 (Trade decision). Under managerial transfer pricing, the subsidiaries agree oninternal trade, i.e., qm(I, p, t) = 1, iff the transfer price t satisfies t ∈

[

r − (2p − 1)eu I, r +

(2p − 1)ed I]

.

The price interval specified by the proposition reflects that the subsidiaries trade in-ternally as long as they do not expect a loss from internal trade. In other words, thesubsidiaries agree to trade internally iff internal trade is individually rational for bothof them. For instance, U’s after-tax expected contribution margin from internal tradeis nonnegative, i.e., (1 − τu)Πu(I, p, 1, t) ≥ −(1 − τu)au I2, for transfer prices not lowerthan r − (2p − 1)eu I.

Obviously, proportional profit taxes do not play a role in this calculus, nor do minor-ity shares. Therefore the subsidiaries’ trade decision is different from the one corporatemanagement would take if it knew the low cost probability. More precisely, C wouldnot only base its decision on the (weighted) expected cost advantage or disadvantagefrom internal trade but also on the gain or loss from shifting profits between the sub-sidiaries. Therefore, given a sufficiently large gain from profit shifting, corporate man-agement would even find it profitable to trade internally if the expected productioncosts of internal trade exceeded those of external trade.15 The delegation of the internaltrade decision, however, is a viable option due to the subsidiaries’ superior knowledgeof expected production costs.

The following lemma provides further insights into the internal trade decision whichturn out to be helpful for further derivations. The lemma connects the trade decision tothe group’s expected pre-tax cost saving from internal trade which is given by

S(I, p) = (2p − 1)(eu + ed)I.

14Due to the linear setting of the model, the joint decision equally can be interpreted as bilateral ne-gotiations or as one subsidiary setting the quantity and the other accepting or denying the decision.Similarly, the timing of the transfer price and the trade agreement does not play a role either.

15In such cases, C would further benefit from not finishing and marketing the internally traded interme-diate.

7

The lemma uses the definition that an investment is called effective if it affects thegroup’s expected variable production costs, i.e., if I > 0 and eu + ed > 0 hold.

Lemma 1 (Equivalences). Under managerial transfer pricing, the following statements areequivalent: 1) There is a transfer price such that the subsidiaries agree on internal trade, 2) thegroup’s expected pre-tax cost saving from internal trade is nonnegative, and 3) the low costprobability is not less than 1/2 for effective investments.

According to Lemma 1, the subsidiaries only trade if they do not expect a cost in-crease, i.e., p ≥ 1/2. Furthermore, whenever the subsidiaries do not expect a costincrease there is a feasible transfer price they may agree upon. Proposition 2 givesthe symmetric cooperative bargaining solution, i.e., the transfer price allocating the ex-pected pre-tax cost saving from internal trade equally to the subsidiaries.

Proposition 2 (Negotiated transfer price). Under managerial transfer pricing with nonneg-ative expected pre-tax cost saving from internal trade, the subsidiaries agree on transfer pricetm(I, p) = r + (2p − 1)(ed − eu)I/2. For negative expected pre-tax cost saving, the sub-sidiaries do not negotiate.

We first note that the negotiated transfer price tm(I, p) lies within the assumed band-width of arm’s length prices. An intuitive property of the negotiated transfer price isthat it varies with the investment efficacies eu and ed so that an increase (resp. decrease)of ed (resp. eu) increases (resp. decreases) the transfer price. Remember that the low costprobability satisfies p ≥ 1/2 due to Lemma 1, otherwise there would be no expectedcost saving to share and at least one of the subsidiaries would not agree to internaltrade. The idea of this dependency of the transfer price on the investment efficacies isthat any individual benefit from cooperation is shared by both subsidiaries by means ofthe transfer price. Hence, for symmetric subsidiaries, i.e., for eu = ed, the subsidiariesagree on the intermediate’s market price r because U and D expect to get the same ben-efit from the investment. A negative expected pre-tax cost saving from internal tradeimplies that the subsidiaries expect to lose from internal trade. Consequently, they donot negotiate and trade externally. In this case, we set the managerial transfer price tothe intermediate’s market price, i.e., tm(I, p) = r, for compatibility with Proposition 1.

Note that, analogous to the internal trade decision, the pricing agreement does notdepend on taxes or profits distributed to minority shareholders. This is due to the factthat the transfer price cannot shift after-tax profits between the subsidiaries but onlypre-tax profits. In terms of cooperative bargaining theory, this addresses the axiomthat a bargaining solution should covary with positive affine transformations of utility.Here, proportional taxation represents such transformation. Note that the assumptionof after-tax performance measures on the subsidiaries’ level is not in line with Ernst &Young (2001, p. 8) who report that some 75 percent of respondents use pre-tax mea-sures. Due to the irrelevance of taxes, however, the actual choice of the performancemeasure has no effect on the subsidiaries’ decisions.

Putting together Propositions 1 and 2 and Lemma 1 we see that managerial transferpricing realizes any nonnegative expected pre-tax cost saving from internal trade. Sincecorporate management would also realize any nonnegative expected pre-tax cost sav-ing this policy implies the best coordination of the delegated trade decisions. In fact, Cmight find it profitable to realize a negative expected pre-tax cost saving due to a gainfrom profit shifting. But such coordination is not feasible under the considered forms

8

of delegation. In the following, we therefore may speak of coordination to be optimaliff any nonnegative expected pre-tax cost saving from internal trade is realized.

Turning to the investment decision, C’s objective function is given by the expectedweighted sum of the subsidiaries’ expected pre-tax profits given the subsidiaries’ trans-fer pricing agreement tm(I, p) and internal trade decision qm

(

I, p, tm(I, p))

derived inPropositions 1 and 2. The fact that the investment decision is based on C’s expecta-tion of the subsidiaries’ reactions to alternative low cost probabilities reflects the costinformation asymmetry. Exploiting Lemma 1 and the fact that the subsidiaries split theexpected pre-tax cost saving equally leads to the following derivation of C’s objectivefunction:

E

(

∑

s∈{u,d}

wsΠs

(

I, p, qm(·), tm(·))

)

=∑

s∈{u,d}

ws

(

E(

qm(·)S(I, p)/2)

− as I2)

=∑

s∈{u,d}

ws

1/2+∆∫

1/2

S(I, p)

4∆dp − as I2

=∑

s∈{u,d}

ws

(

∆(eu + ed)I/4 − as I2)

. (1)

Apparently, the investment maximizing this objective function trades off the effect onthe group’s expected net cost saving from internal trade to the investment’s net costs.It is given by the following proposition.16

Proposition 3 (Investment). Under managerial transfer pricing, corporate managementchooses investment

Im =(wu + wd)∆(eu + ed)

8(wuau + wdad).

The symmetry of Im in the efficacy parameters eu and ed reflects the equal allocationof the expected pre-tax cost saving to the subsidiaries. Furthermore, corporate manage-ment finds it always profitable to invest unless investments are in vain in the first place,i.e., eu = ed = 0, because the managerial transfer pricing policy exploits the superiorknowledge of the subsidiaries.

Some remarks on the assumed bandwith [r − 2∆eu I, r + 2∆ed I] of arm’s length pricesconclude this subsection. Returning to Proposition 1, we observe that the transfer priceinterval allows for any allocation of the group’s expected pre-tax cost saving from inter-nal trade to the subsidiaries. For any smaller bandwidth the subsidiaries do not fullydispose of the expected cost saving for some low but favorable low cost probability.Since the group’s profit center organization implies individual maximization of after-tax profits and bargaining (effectively) is unrestricted, managerial transfer prices asintroduced above perfectly implement the arm’s length principle as codified amongstothers in Article 9 of the OECD Model Tax Convention.17 Hence, the negotiated transferprice tm(I, p) is the true comparable uncontrolled price (CUP).

Assuming that external stakeholders are less informed than corporate management

16The proof of Proposition 3 is omitted since the proposition follows from standard calculus.17See OECD (1999, ch. I, par. 1.5) for further remarks.

9

about the subsidiaries’ bargaining problems at dates 4 and 5, the true CUP is unknownto both corporate management and external stakeholders. In addition to the low costprobability p, it is intuitve that external stakeholders have imperfect information on therange parameter ∆, on the subsidiaries’ bargaining powers, the investment efficacies eu

and ed, or the risk attitudes of the subsidiaries’ managers. They may even lack infor-mation on the kind of interplay, not only on the values, of the mentioned parameters,or on the subsidiaries’ business strategies.18 Thus, the assessment whether a specificprice is at arm’s length typically is a matter of discretion depending on the informationavailable to external stakeholders.19

To gain a better understanding of the assumed bandwidth we generalize the band-width of accepted transfer prices by

[

r + ∆(ed − eu)I/2 −¯δ∆(ed + 3eu)I/2, r + ∆(ed − eu)I/2 + δ̄∆(3ed + eu)I/2

]

(2)

with exogenous paramaters¯δ, δ̄ ≥ 0 representing the degree of discretion admitted

by external stakeholders.20

¯δ = δ̄ = 0 says that external stakeholders only accept

the expected value of the true CUP given equal bargaining powers, i.e., E(

tm(I, P))

.

¯δ = (ed − eu)/(ed + 3eu) < 1 and δ̄ = (ed − eu)/(3ed + eu) < 1 imply that externalstakeholders accept any realization of the true CUP given equal bargaining powers.With

¯δ = δ̄ = 1 external stakeholders additionally accept any distribution of bargain-

ing powers. The setting¯δ, δ̄ > 1 corresponds to cases where external stakeholders are

least strict. Note that, due to the lack of information, external stakeholders have imper-fect information on how the accepted bandwidth actually relates to the subsidiaries’transaction. For instance, external stakeholders holding a high estimation of ∆ may ad-mit

¯δ = δ̄ = 1 even if they are not willing to accept extreme distributions of bargaining

power.Section 3 is based on

¯δ = δ̄ = 1 and thus on an intermediate degree of discretion. The

corresponding bandwidth reads [r − 2∆eu I, r + 2∆ed I]. It consists of all prices such thatany two unrelated parties in the same situation as the subsidiaries would agree to tradewith each other. Hence, the bandwidth corresponds with the price interval given inProposition 1 for p = 1/2 + ∆. This bandwidth is chosen from a modeling perspectivebecause it is the smallest interval such that the trade-off between the managerial andthe financial perspective fully deploys under decentralization. Thus, it is ideal for thestudy of the economic determinants of the group’s policy choice. In Section 5.1, wesketch the effects of a more or less restrictive bandwidth on that choice.

3.2 Financial transfer pricing

The managerial transfer price negotiated by the subsidiaries does not consider taxesand minority shares. The idea of financial transfer pricing is to put a decision maker incharge of the transfer price who accounts for them.21 It is assumed that the tax depart-

18Confer OECD (1999, pp. I-9) for factors determining the comparability of transactions.19Note that discretion typically is not removed when transfer prices are based on empirical data due to

the incompleteness of information and the heterogeneity of the sample.20This approach is in line with previous literature. See, e.g., Smith (2002a). However, note that the explicit

consideration of information asymmetry makes the analysis more involved.21Strictly speaking, this policy would have to be called ’financial and tax transfer pricing‘ as the transfer

price applies to both financial and tax accounting.

10

ment T is such a decision maker. As an alternative, one might think of a joint decisionof the tax department and the CFO. With respect to transfer pricing this policy is theopposite of managerial transfer pricing where transfer prices are set without any con-sideration of taxes and minority shares. In this policy, transfer prices are exclusivelybased on these considerations. Financial and managerial transfer pricing have in com-mon that the production and marketing decisions are delegated to the subsidiaries.Hence, the internal trade decision in Proposition 1 also applies to this policy.

The minimization of payments to tax authorities and minority shareholders for giventrade decision implies a maximal profit shift under the condition that the transfer pricelies in the bandwidth of arm’s length prices. Hence, T’s optimal pricing choice is ex-treme and determined by the relative weights of subsidiaries’ pre-tax profits accordingto

t f (I) =

{

r − 2∆eu I if wu < wd

r + 2∆ed I if wu > wd

.

Note that t f (I) depends on the investment level because the bandwidth of arm’s lengthprices does.

C’s optimal investment choice therefore anticipates both T’s transfer pricing choiceand the subsidiaries’ internal trade decision in reaction to that transfer price. The cor-responding objective function reads

E

∑

s∈{u,d}

wsΠs

(

I, P, qm(

I, P, t f (I))

, t f (I))

.

The following proposition derives C’s and T’s decisions.

Proposition 4 (Investment and transfer price). Under financial transfer pricing with un-equal weights, i.e., wu 6= wd, corporate management’s investment choice is

I f =ws∆es

4(wuau + wdad)

for es′ = 0 and ws > ws′ with s, s′ ∈ {u, d} and s 6= s′. Otherwise corporate management doesnot invest. The transfer price equals the intermediate’s market price, i.e., t f = t f (I f ) = r.

We take the unilateral case eu = 0 and ed > 0 to explore the proposition. When Tvalues U’s pre-tax profit higher than D’s the transfer price equals the right corner ofthe bandwidth of arm’s length prices. For this transfer price, D almost surely deniesinternal trade and no positive expected cost saving is realized. Hence, C does not investand the bandwidth of arm’s length prices collapses into the intermediate’s market price.For wu < wd, the intermediate is priced at the market price which is the left corner of thebandwidth. Both subsidiaries agree to internal trade at this transfer price whenever theexpected cost saving is nonnegative. C’s incentive to invest is to increase this potentialcost saving.

Proposition 4 does not cover the case wu = wd because T has no preferred transferprice if profit allocation does not matter. Consequently, an assumption on T’s decisionbehavior is necessary. We assume that the tax department chooses the intermediate’smarket price r as the transfer price if wu = wd holds.

11

3.3 Integrated transfer pricing

Managerial transfer prices induce optimal coordination of trade with respect to thegroup’s expected pre-tax profit but ignore the group’s payments to tax authorities andminority shareholders. In contrast, financial transfer prices only account for profit al-location but do not consider coordination. The idea of integrated transfer pricing isto find a compromise between the generation of pre-tax profits on the one hand andits allocation to the subsidiaries on the other. Accordingly, C keeps the transfer pric-ing authority. Referring to Ernst & Young (2001, p. 7), one might also think of a jointdecision of the tax department and the controller. The trade decisions stay with thesubsidiaries in order to exploit the subsidiaries’ superior knowledge of expected costs.Consequently, the internal trade decision under managerial transfer pricing given inProposition 1 also applies to this policy.

C’s objective function of the investment and transfer pricing decisions is

E

∑

s∈{u,d}

wsΠs

(

I, P, qm(I, P, t), t)

(3)

where the delegation of the trade decision is reflected by q = qm(I, P, t). Evaluation of(3) yields

E(

(wu−wd)(t−r) + (wueu+wded)(2P−1)I : qm(I, P, t)=1)

· prob(

qm(I, P, t)=1)

− (wuau+wdad)I2 (4)

which is zero in case of no investment because then internal and external trade areequivalent and the only arm’s length price is the intermediate’s market price. Furtherevaluation for unilateral investment effect for D, i.e., eu = 0 and ed > 0, yields

(wu − wd)(t − r)

2∆max

{

∆ −t − r

2ed I, 0

}

+wded I

2∆max

{

∆2 −

(

t − r

2ed I

)2

, 0

}

− (wuau + wdad)I2 (5)

for t ≥ r. For transfer prices below the intermediate’s market price, i.e. for t < r, Udoes not agree to internal trade so that (5) equals the net investment outlays. Expres-sion (5) allows to explore the driving forces of C’s optimal transfer price and investmentchoices.

Two effects have to be taken into account for the transfer price choice. On the onehand, the transfer price determines the extent of profit shifting which exploits theweight differential wu − wd. The according expression (5) of this profit allocation effectis (wu −wd)(t− r). With wu > wd (resp. wu < wd) corporate management wants to shiftprofit to U (resp. D) and therefore prefers high (resp. low) transfer prices. Note that thelowest arm’s length price for eu = 0 is r. On the other hand, the transfer price affects thesubsidiaries’ trade decision. The corresponding expression of this coordination effectin (5) is ∆ − (t − r)/(2ed I). Since the subsidiaries realize any nonnegative expected costsaving from internal trade if the intermediate is priced at the market price, coordinationis optimal for t = r. Any increase of the transfer price increases the probability that D

12

refuses internal trade although the expected pre-tax cost saving from internal trade isnonnegative. For the highest arm’s length price, i.e., for t = r + 2∆ed I, D would onlyagree to internal trade if the low cost probability is maximal, i.e., p = 1/2 + ∆. Theprobability of this event is zero. Hence, managerial and financial goals are complemen-tary for wu < wd and C chooses to value transfers at the market price. For wu > wd, thetwo objectives are competitive and C has to find the optimal trade-off.

The investment decision involves three effects. First, the higher the investment thehigher is the cost saving potential and thus the expected pre-tax cost saving from in-ternal trade. The corresponding term in expression (5) is wded I. Second, an increasinginvestment, for given transfer price t > r, decreases the probability that D refuses totrade although the expected pre-tax cost saving is nonnegative. This again refers to thedifference ∆ − (t − r)/(2ed I) in (5). These two effects are complementary and have tobe weighed against the third, namely the investment’s net costs.

The following proposition gives the group’s optimal investment and pricing choicesfor both unilateral and bilateral investment effects.

Proposition 5 (Investment and transfer price). Under integrated transfer pricing, corporatemanagement chooses investment Ii and transfer price ti according to

Ii =w2

s ∆(eu + ed)2

4(

ws(es + 2es′) − ws′es′)

(wuau + wdad)

ti = r +(wu − wd)w2

s ∆2e2

s′(eu + ed)2

2(

ws(es + 2es′) − ws′es′)2

(wuau + wdad)

for ws ≥ ws′ with s, s′ ∈ {u, d} and s 6= s′.

The proposition captures three intuitive properties of integrated transfer prices. First,profit allocation does not play a role for equal weights, i.e., wu = wd, so that the transferprice then solely serves optimal coordination. Second, optimal profit allocation drivesup (resp. down) the transfer price above (resp. below) the market price if C benefitsfrom shifting profits to U (resp. D). Third, the assumed bandwidth of arm’s lengthprices never restricts the transfer price choice because coordination fully deploys withinthe assumed bandwidth and thereby limits profit shifting effectively. Put differently,any extension of the assumed bandwidth of arm’s length prices has no effect on C’sdecisions as given in Proposition 5.

3.4 Centralized planning

The preceding policies all rely on delegation. This section deals with the option tocentralize all considered decisions. Accordingly, in the centralized planning policy cor-porate management takes both the trade decision and the transfer price decision. Thebenefit of a centralized trade decision is that trade does not maximize anymore thegroup’s expected pre-tax profit but the group’s expected net profit due to the decisionmakers’ different objectives. The disadvantage of such a policy is that C’s trade decisionis less informed than the subsidiaries’ decision because it does not react to the realizedlow cost probability.

Obviously, the optimal investment level without internal trade is zero yielding zeroprofit. Therefore, C’s optimization with respect to the investment and the transfer price

13

concentrates on the group’s expected net profit given internal trade which reads

E

∑

s∈{u,d}

wsΠs(I, P, 1, t)

= (wu − wd)(t − r) − (wuau + wdad)I2. (6)

Observe that there is no expected cost saving due to the information asymmetry. Asa consequence, the benefit of internal trade solely relies on profit shifting reflected bythe minuend of the right hand side of expression (6). Proposition 6 gives the optimaldecisions.

Proposition 6 (Investment, transfer price, and internal trade). Under centralized plan-ning, corporate management opts for internal trade, i.e., qc = 1, and chooses investment Ic andtransfer price tc according to

Ic =(ws − ws′)∆es′

wuau + wdadand tc = r +

2(wu − wd)∆2e2

s′

wuau + wdad

for ws ≥ ws′ with s, s′ ∈ {u, d} and s 6= s′.

For equal weights profit shifting has no value and it is not worthwhile to invest.Maximizing the gain from profit shifting for wu 6= wd implies the same transfer pricingdecision as under financial transfer pricing, namely t = t f (I). Thus, the optimal invest-ment level trades off the benefit from extending the bandwidth of arm’s length pricesto its costs. With respect to the investment Ic, the effect on the bandwidth is reflected bythe parameter es′ whereas the cost effect shapes the denominator. The correspondingeffects on the bandwidth can be easily seen from the definition of the transfer price tc.

4 Comparison of policies

The preceding analysis shows that the policies have different strengths and weaknesses.The advantage of managerial transfer pricing is that both the trade and the transferprice decision exploit the subsidiaries’ superior knowledge. This perfectly serves themanagerial goal, i.e., the maximization of the expected pre-tax cost saving from inter-nal trade, but ignores taxation and profit distribution. Financial transfer prices focuson group profitability but ignore the effect on the delegated trade decision. Integratedtransfer prices are also set with respect to the maximization of the group’s expected netprofit while the trade decision still benefits from the subsidiaries’ superior knowledge.Thus, the transfer price incorporates both managerial and financial aspects but the pric-ing decision lacks information. The decisions under the centralized planning policy allaim for the group’s expected net profit but completely do without the subsidiaries’knowledge. This section concentrates on the relative performance of the different poli-cies and identifies conditions of optimality.

The first step to identify C’s optimal policy choice for alternative parameter settingsis to exclude the financial transfer pricing policy.

Lemma 2 (Inefficiency of financial transfer pricing). From the perspective of corporate man-agement, integrated transfer pricing dominates financial transfer pricing.

14

The efficiency result of Lemma 2 states that there is no parameter setting such thatfinancial transfer pricing yields a higher expected net profit of the group than integratedtransfer pricing and that there is some parameter setting such that financial transferpricing actually does worse than integrated transfer pricing. The idea of this result isthat, ceteris paribus, ignoring the coordination effect on the trade decision cannot beoptimal. Thus, it is never detrimental to add a management perspective to financialtransfer pricing. The financial transfer pricing policy therefore will be dropped in thefollowing. Note that the result of the lemma is very robust. In particular, it holds fordifferent degrees of discretion with respect to arm’s length prices.

The second step is Proposition 7 which calculates the expected net profit of the groupfor the remaining policies.22

Proposition 7 (Maximal net profits). The maximal expected net profit of the group reads

(wu + wd)2∆

2(eu + ed)2

64(wuau + wdad)

under managerial transfer pricing,

w4s ∆

2(eu + ed)4

16(wuau + wdad)(ws(es + 2es′) − ws′es′)2

under integrated transfer pricing, and

(wu − wd)2∆

2e2s′

wuau + wdad

under centralized planning for ws ≥ ws′ with s, s′ ∈ {u, d} and s 6= s′.

The following corollary gives a first insight into the relative performance of the poli-cies by considering a knife-edge case where information has no value.23

Corollary 1 (No value of information). When there is no value of information, i.e., ∆ = 0,all policies yield zero expected net profit of the group.

The idea of Corollary 1 is that there neither is a positive expected pre-tax cost savingfrom internal trade nor a gain from profit shifting if cost information has no value.There is no positive expected pre-tax cost saving because with ∆ = 0 the low costprobability always equals 1/2 so that there is no potential for expected cost reductions.Profit shifting does not yield a gain because with ∆ = 0 the bandwidth of arm’s lengthprices collapses into the intermediate’s market price.

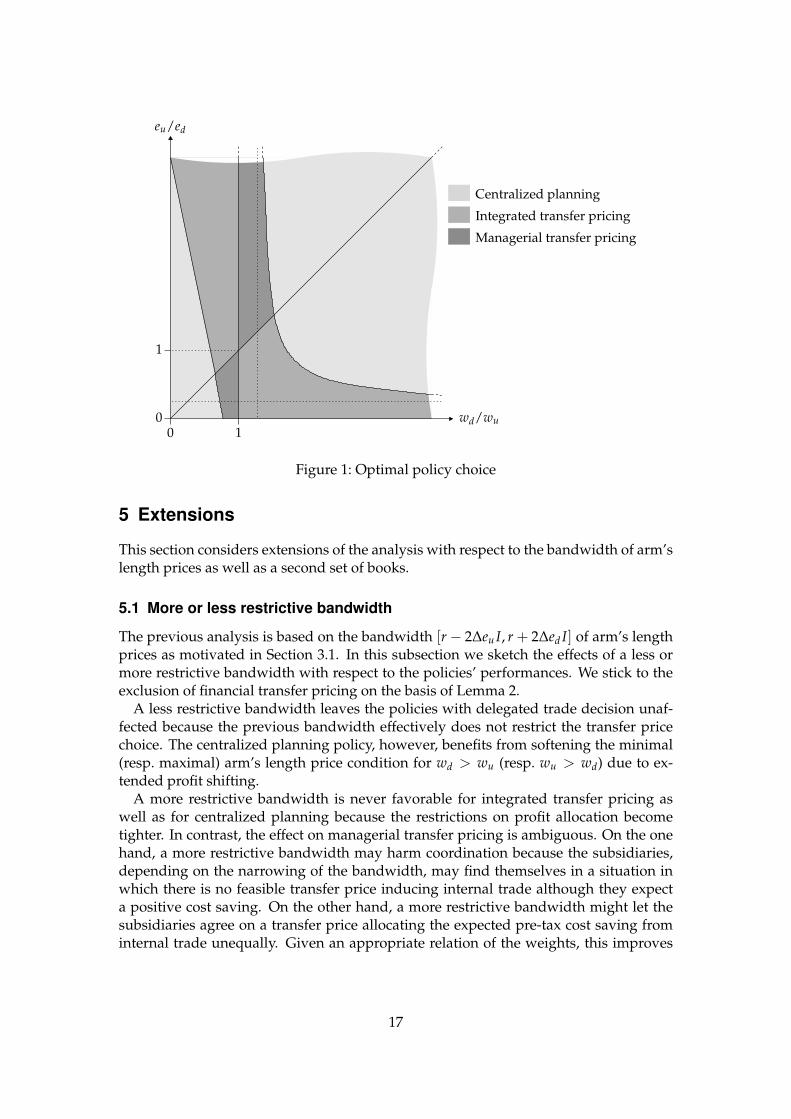

The following corollary describes C’s preference over the policies which is depicted inFigure 1.24 The corollary implicitly shows that a positive value of information actuallyhas no effect on corporate management’s preference. The value of information ratherdetermines the magnitude, not the sign, of the difference in the policies’ expected netprofit.

22The proof of Proposition 7 is omitted since the proposition follows from straight evaluation of thegroup’s objective function for the decisions given in the preceeding propositions.

23The proof of Corollary 1 is omitted since it directly follows from Proposition 7.24The proof of Corollary 2 is omitted since it directly follows from Proposition 7.

15

Corollary 2 (Policy preferences). Corporate management prefers (resp. is indifferent between)1. managerial transfer pricing to (resp. and) integrated transfer pricing iff

(wu − wd)(wded − wueu) > (resp. =) 02. managerial transfer pricing to (resp. and) centralized planning iff

(wu + wd)(eu + ed) > (resp. =) 8(ws − ws′)es′

3. integrated transfer pricing to (resp. and) centralized planning iffw2

s (eu + ed)2

ws(es + 2es′) − ws′es′> (resp. =) 4(ws − ws′)es′

for ∆ > 0 and ws ≥ ws′ with s, s′ ∈ {u, d} and s 6= s′.

An observation from Proposition 7 is that the performance of centralized planningdepends on two factors. On the one hand, the (nonnegative) weight differential ws −ws′

determines C’s marginal benefit of shifting the transfer price below (wu < wd) or above(wu > wd) the intermediate’s market price. On the other hand, the efficacy parameter es′

limits the effective discretion provided by the bandwidth of arm’s length prices, i.e., themaximal extent of an appropriate shift of the transfer price. Both factors are associatedwith profit allocation. Since centralized planning does without the subsidiaries’ in-formation this policy is preferred to the others if the advantage from profit allocationoutweighs the disadvantage of no coordination. From Figure 1 we arrive at the intuitiveconclusion that this is the case if the efficacy parameter es′ is sufficiently large comparedto es.

Managerial and integrated transfer pricing are candidates for optimality whenevermanagerial aspects are important relative to financial aspects. For equal weights profitallocation does not play a role and both policies coincide. It does not surprise that man-agerial transfer pricing is optimal for equal weights since the subsidiaries genericallyagree on internal trade maximizing the group’s expected pre-tax profit. According toProposition 1, however, the same internal trade decision is induced by pricing the in-termediate at the market price. Thus, corporate management also achieves optimalcoordination by means of integrated transfer pricing. For differing weights the transferprices under managerial and integrated transfer pricing serve both managerial and fi-nancial aspects and the policies’ performances differ. As an example, we compare thetwo policies for unilateral investment effect for D, i.e., eu = 0 and ed > 0.

With wd > wu corporate management prefers low transfer prices with respect toprofit allocation. The lowest arm’s length price is the market price for which C bene-fits from optimal coordination. Therefore managerial transfer pricing performs worsethan integrated transfer pricing because the former allocates the group’s (nonnegative)expected pre-tax cost saving from internal trade equally to the subsidiaries whereasthe latter fully allocates it to D. This is an instance where it is advantageous to adda financial perspective to transfer pricing. This is not the case for wu > wd. Underintegrated transfer pricing any profit shift to U comes at the expense of coordination,i.e., a decrease of the expected pre-tax cost saving from internal trade. In order to repli-cate, at least in expectation, the equal cost saving allocation under managerial transferpricing, corporate management suffers from efficiency losses due to suboptimal coor-dination. In contrast, managerial transfer pricing implies optimal coordination. Sincemanagerial transfer pricing prevails for wu > wd, we infer that profit shifting underintegrated transfer pricing is too costly in terms of deteriorated coordination comparedto the equal cost saving allocation and optimal coordination under integrated transferpricing.

16

Centralized planning

Integrated transfer pricing

Managerial transfer pricing

00

wd/wu

1

1

eu/ed

Figure 1: Optimal policy choice

5 Extensions

This section considers extensions of the analysis with respect to the bandwidth of arm’slength prices as well as a second set of books.

5.1 More or less restrictive bandwidth

The previous analysis is based on the bandwidth [r − 2∆eu I, r + 2∆ed I] of arm’s lengthprices as motivated in Section 3.1. In this subsection we sketch the effects of a less ormore restrictive bandwidth with respect to the policies’ performances. We stick to theexclusion of financial transfer pricing on the basis of Lemma 2.

A less restrictive bandwidth leaves the policies with delegated trade decision unaf-fected because the previous bandwidth effectively does not restrict the transfer pricechoice. The centralized planning policy, however, benefits from softening the minimal(resp. maximal) arm’s length price condition for wd > wu (resp. wu > wd) due to ex-tended profit shifting.

A more restrictive bandwidth is never favorable for integrated transfer pricing aswell as for centralized planning because the restrictions on profit allocation becometighter. In contrast, the effect on managerial transfer pricing is ambiguous. On the onehand, a more restrictive bandwidth may harm coordination because the subsidiaries,depending on the narrowing of the bandwidth, may find themselves in a situation inwhich there is no feasible transfer price inducing internal trade although they expecta positive cost saving. On the other hand, a more restrictive bandwidth might let thesubsidiaries agree on a transfer price allocating the expected pre-tax cost saving frominternal trade unequally. Given an appropriate relation of the weights, this improves

17

the performance of managerial transfer pricing due to a more favorable profit alloca-tion. Hence, a group adopting the managerial transfer pricing policy eventually bene-fits from a more restrictive bandwidth of arm’s length prices and thus by less ex-postdiscretion.25

We illustrate the positive effect of a more restrictive bandwidth on the performanceof managerial transfer pricing by concentrating on the low cost probability p = 1/2 + ∆

given a positive investment with an asymmetric effect, i.e., I > 0 and eu 6= ed. For a non-restrictive bandwidth, i.e.,

¯δ, δ̄ ≥ 1 in the bandwidth formulation (2), the subsidiaries

agree on transfer price t = r + ∆(ed − eu)I, trade internally, and share the expectedcost saving equally. Observe that the center of the bandwidth (2), i.e., the expectednegotiated transfer price t = r + ∆(ed − eu)I/2, is above (resp. below) the negotiatedtransfer price for eu > ed (resp. for ed > eu). A restricted bandwidth is representedby

¯δ < 1, δ̄ < 1, or both. The negotiation result for such bandwidth depends on the

specific solution concept.26 For eu > ed (resp. for ed > eu), however, there is a suffi-ciently small

¯δ (resp. δ̄) such that the restricted bandwidth lies above (resp. below) the

freely negotiated transfer price. For such restricted bandwidth, the subsidiaries agree,no matter which solution concept they apply, on some transfer price above (resp. be-low) the freely negotiated one. Thus, the expected pre-tax cost saving is split betweenthe subsidiaries in favor of U (resp. D) which is favorable for corporate management ifthe weights satisfy wu > wd (resp. wd > wu). Consequently, the group’s expected netcost saving from internal trade increases which makes the investment more profitableand increases the performance of managerial transfer pricing.

5.2 Two sets of books

The analysis in Sections 3 and 4 is based on the assumption of a single set of books.When the group employs a second set of books the transfer price for external purposesoptimally would be set in order to minimize group taxes and profits distributed to mi-nority shareholders according to the scenario of financial transfer pricing. The internaltransfer price then is not restricted anymore by a bandwidth of arm’s length prices andis freed from its profit allocation function.

However, a second set of books does not make the research topic of this paper ob-solete because the optimal internal transfer price would induce decisions maximizingthe group’s net profit on the part of the subsidiaries and thus indirectly account forprofit allocation. Therefore neither negotiated nor administered internal transfer pricesdo a perfect job. The former imply informed trade decisions that do not maximize thegroup’s expected net profit, whereas the latter aim at the group’s expected net profit butignore the subsidiaries’ superior information. Hence, the idea of the trade-off betweenmanagerial and financial transfer pricing as modeled in this paper remains.27

Note that the model of this paper would have to be extended in order to capture thistrade-off under two sets of books. In the present model with two sets books, corporatemanagement would set the internal transfer price to the intermediate’s market price inorder to induce the subsidiaries to trade internally whenever a nonnegative pre-tax costsaving is expected. Given the delegation of the trade decision, this is optimal for both

25See Smith (2002a) for the effects of ex-post discretion on the decisions of a centralized firm.26The corresponding bargaining problem exhibits the property that utility is not (freely) transferable.27See, e.g., Baldenius et al. (2004) for optimal transfer prices under two sets of books and full information.

18

the group’s expected pre-tax profit and its expected net profit. There are two remediesto this shortcoming. First, the subsidiaries’ optimal trade decision is not binary andreacts more to changes in the transfer price. Second, the sets of transfer prices inducinginternal trade do not all overlap for all low cost probabilities. The remedies’ commonconsequence is that they establish a more effective information asymmetry betweencorporate management and the subsidiaries so that the former is not able to induce itsmost preferred delegated trade decision under partial information.

6 Conclusion

In this paper we examine a multinational group consisting of corporate managementand two subsidiaries organized as profit centers in a setting of asymmetric informationand specific investment. Asymmetric information pertains to the success of a cost re-duction investment which is under the control of corporate management. An expectedcost reduction has to be exploited by an appropriate trade choice. Corporate manage-ment employs a single transfer price for managerial and financial purposes which hasto be at arm’s length. There are four transfer pricing policies available to corporatemanagement.

Under managerial transfer pricing, financial transfer pricing, and integrated transferpricing the trade decision is delegated to the subsidiaries. It is an informed decisiondue the subsidiaries’ superior knowledge, but depends on the transfer price. The firstpolicy additionally delegates the transfer pricing authority to the subsidiaries who ne-gotiate the transfer price. This price is set under full information and serves as thebasis of the bandwidth of arm’s length prices. It is shown that the transfer price maxi-mizes the group’s pre-tax profit so that any expected positive cost saving is exploited.The second policy implies a transfer price decision which is solely driven by financialconsiderations and thus minimizes group taxation and profits distributed to minorityshareholders. The financial focus heavily impairs coordination, i.e., the subsidiaries’trade decision. The third policy allows for a centralized transfer price decision whichis made with respect to the group’s net profit after taxes and profit distribution but suf-fers from incompleteness of information and thus also deteriorates coordination. Thefourth policy of centralized planning delegates neither the transfer price nor the tradedecision. It does not realize any expected cost saving but only relies on profit shifting.

A first result of the comparative analysis is that financial transfer pricing is inferiorto integrated transfer pricing. This result is intuitive because the former policy ignorescoordination. A second, at first sight less intuitive result is that it may be optimal tochoose managerial transfer pricing and thus ignore aspects of profit allocation. Theidea of this result is that the disadvantage of impaired coordination under integratedtransfer pricing outweighs the advantage from a better allocation of profit. Summingup, it is optimal to add a managerial perspective to transfer pricing but the advantageof adding a financial perspective depends on the underlying parameter setting. A thirdresult is illustrated by Figure 2: The more the optimal perspective on transfer pricing isa financial one, i.e., the more important profit allocation, the lower is the optimal degreeof decentralization. For instance, a group with the tax department in charge of transferpricing relies on centralized decision making.

An extension shows that only centralized planning actually may benefit from a lessrestrictive bandwidth of arm’s length transfer prices due to a higher degree of feasible

19

Managerial TP

of centralizationOptimal degreeOptimal degree

of decentralization

Optimal perspective on TP

Optimal policy

Integrated TP

low

high low

high

CentralizedPlanning

financialmanagerial

Figure 2: Transfer pricing perspective and decentralization

profit shifting. As expected, a more restrictive bandwidth does not improve the perfor-mance of integrated transfer pricing but rather harms it. Yet, the effect on the perfor-mance of managerial transfer pricing is ambiguous. Accordingly, this policy benefitsfrom tighter transfer pricing rules if they sufficiently improve profit allocation. Finally,we argue that a second set of books essentially implies the same reasoning as presentedin the course of the analysis when choosing between managerial and integrated transferpricing for internal purposes.

The analysis sheds light on the relative performance of various designs of delegationdiffering in their capabilities to coordinate and to allocate profit. The results may notonly help business practitioners to choose an adequate transfer pricing policy but mayalso be consulted to comment on empirical findings. For instance, Ernst & Young (2001,p. 7) investigate where multinational parent firms using a single transfer price primar-ily locate the responsibility for setting transfer prices. The answer ”BU Leader“ (29 per-cent) easily links to the managerial transfer pricing approach whereas the answer ”TaxDept.“ (65 percent) points at centralized planning. The answer ”Controller“ (29 per-cent) may be interpreted in terms of the integrated transfer pricing policy. The factthat respondents were allowed to give multiple answers indicates that transfer priceauthority may be shared which also relates to an integrated transfer pricing policy.

The paper does not cover administered transfer pricing with prior reporting by thesubsidiaries. Truthful reports would require a more sophisticated management controlsystem and transfer price than the one considered in this paper. Dikolli and Vaysman(2006) elaborate on this topic but do not account for issues of profit allocation.

References

Anthony, R. N., Govindarajan, V., 2000. Management Control Systems, 10th Edition.McGraw-Hill, Boston.

Balachandran, K. R., Li, S.-H., 1996. Effects of differential tax rates on transfer pricing.Journal of Accounting, Auditing and Finance 11 (2), 183–196.

Baldenius, T., Melumad, N. D., Reichelstein, S., July 2004. Integrating managerial andtax objectives in transfer pricing. The Accounting Review 79 (3), 591–615.

Chiles, C. R., Dau, M. T., 2005. An analysis of current supply chain best practices in theretail industry with case studies of wal-mart and amazon.com. Master’s thesis, Mas-

20

sachusetts Institute of Technology, Engineering Systems Division, http://dspace.mit.edu.

Dikolli, S. S., Vaysman, I., 2006. Information technology, organizational design, andtransfer pricing. Journal of Accounting and Economics 41 (1-2), 201–234.

Elitzur, R., Mintz, J., 1996. Transfer pricing rules and corporate tax competition. Journalof Public Economics 60 (3), 401–422.

Ernst & Young, 2001. Transfer Pricing 2001 Global Survey. Ernst & Young International,http://www.ey.com.

Ernst & Young, 2003. Transfer Pricing 2003 Global Survey. Ernst & Young International,http://www.ey.com.

Grabski, S. V., 1985. Transfer pricing in complex organizations: A review and integra-tion of recent empirical and analytical research. Journal of Accounting Literature 4,33–75.

Halperin, R., Srinidhi, B., January 1991. U.S. income tax transfer-pricing rules and re-source allocation: The case of decentralized multinational firms. The Accounting Re-view 66 (1), 141–157.

Horngren, C. T., Datar, S. M., Foster, G., 2006. Cost Accounting: A Managerial Empha-sis, 12th Edition. Prentice Hall, Upper Saddle River (New Jersey).

Hyde, C. E., Choe, C., March 2005. Keeping two sets of books: The relationship be-tween tax and incentive transfer prices. Journal of Economics & Management Strat-egy 14 (1), 165–186.

Martini, J. T., Niemann, R., Simons, D., 2007. Transfer pricing or formula apportion-ment? tax-induced distortions of multinationals’ investment and production deci-sions. CESifo Working Paper 2020.

Milgrom, P. R., Roberts, J., 1992. Economics, Organization and Management. Prentice-Hall, Englewood Cliffs (New Jersey).

Narayanan, V. G., Smith, M., 2000. Impact of competition and taxes on responsibilitycenter organization and transfer prices. Contemporary Accounting Research 17 (3),497–529.

Nielsen, S. B., Raimondos-Møller, P., Schjelderup, G., April 2003. Formula apportion-ment and transfer pricing under oligopolistic competition. Journal of Public Eco-nomic Theory 5 (2), 419–437.

Nielsen, S. B., Raimondos-Møller, P., Schjelderup, G., 2006. Taxes and decision rights inmultinationals. CEPR Discussion Papers 5952.

OECD, October 1999. Transfer Pricing Guidelines for Multinational Enterprises andTax Administrations. Organisation for Economic Co-operation and Development(OECD), Paris.

Rosenmüller, J., 2000. Game Theory: Stochastics, Information, Strategies and Coopera-tion. Kluwer Academic Publishers.

Schjelderup, G., Sorgard, L., 1997. Transfer pricing as a strategic device for decentral-ized multinationals. International Tax and Public Finance 4 (3), 277–290.

Smith, M., January 2002a. Ex ante and ex post discretion over arm’s length transferprices. The Accounting Review 77 (1), 161–184.

Smith, M., 2002b. Tax and incentive trade-offs in multinational transfer pricing. Journalof Accounting, Auditing and Finance 17 (3), 209–236.

Tang, R. Y. W., 1993. Transfer Pricing in the 1990s: Tax and Management Perspectives.Quorum Books, Westport (Connecticut), London.

21

Tang, R. Y. W., 2002. Current trends and corporate cases in transfer pricing. QuorumBooks, Westport (Connecticut).

Williamson, O. E., 1985. The Economic Institutions of Capitalism: Firms, Markets, Re-lational Contracting. The Free Press, New York.

Proofs

Proposition 1

The agreement on internal trade is based on U’s and D’s individual rationality with ex-ternal trade yielding after-tax profits of −(1− τu)au I2 for U and −(1− τd)ad I2 for D. Udoes not benefit from external trade iff (1− τu)Πu(I, p, 1, t) ≥ −(1− τu)au I2. D cooper-ates for (1 − τd)Πd(I, p, 1, t) ≥ −(1 − τd)ad I2. The proposition gives the correspondingtransfer prices such that these two inequalities hold.

Lemma 1

By Proposition 1, the first statement is equivalent to r − (2p − 1)eu I ≤ r + (2p − 1)ed Iwhich is equivalent to (2p− 1)(eu + ed)I ≥ 0. By the definition of S(I, p), this conditioncoincides with the second and the third statement.

Proposition 2

The proof is based on cooperative bargaining theory according to which any bargainingsolution should satisfy the axioms of Pareto efficiency, individual rationality, symme-try, and covariance under positive affine transformations.28 The last axiom allows toconcentrate on expected pre-tax profits.

The status-quo point of negotiations is determined by external trade yielding ex-pected pre-tax profits of

(

Πu(I, p, 0, t), Πd(I, p, 0, t))

=(

− au I2,−ad I2)

. Given a non-negative expected pre-tax cost saving S(I, p), there is a transfer price such that the sub-sidiaries trade internally, see Lemma 1. By Proposition 1, the set of such transfer pricesis[

r − (2p − 1)eu I, r + (2p − 1)ed I]

. The corresponding expected pre-tax profits

{

(

Πu(I, p, 1, t), Πd(I, p, 1, t))

: t ∈[

r − (2p − 1)eu I, r + (2p − 1)ed I]

}

are Pareto efficient and individually rational. In addition, transfer prices t ∈[

r − (2p −

1)eu I, r + (2p − 1)ed I]

allow for any allocation of the cost saving S(I, p) to the sub-sidiaries. Any symmetric bargaining solution allocates this surplus equally to the sub-sidiaries so that

Πu(I, p, 1, t)−(

− au I2)

= Πd(I, p, 1, t)−(

− ad I2)

= S(I, p)/2

holds for the negotiated transfer price. tm(I, p) is the unique transfer price to satisfythis condition. Otherwise, i.e., for negative expected pre-tax cost saving, there is noexpected gain from internal trade, the subsidiaries do not negotiate and trade externallyyielding the status-quo point.

28See, e.g., Rosenmüller (2000, ch. 8) for details.

22

Proposition 4

For unilateral investment effects, the proof concentrates on eu = 0. The case ed = 0can be derived in the same manner. T chooses transfer price t f (I) = r for wu < wd

and t f (I) = r + 2∆ed I for wu > wd to minimize the group’s tax burden and paymentsto minority shareholders for given internal trade and investment. The former pricingchoice is identical to the corresponding case under integrated transfer pricing so thatProposition 5 gives the optimal investment level. Evaluation of (5) for the latter choiceshows that any investment is unprofitable.

Similar to the unilateral case, (7) and (8) show that the pricing choice t f (I) makes anyinvestment in the bilateral case unprofitable for wu 6= wd.

Observe that in any case the transfer price in the optimum is t f = t f (I f ) = r.

Proposition 5

The proof first concentrates on the case of a bilateral investment effect, i.e., eu, ed > 0,from which optimal decisions under unilateral investment effects can be derived. By(3), the expected contribution margin after taxes and profit distribution reads

(wu − wd)(t − r)

2∆max

{

∆ −t − r

2ed I, 0

}

+(wueu + wded)I

2∆max

{

∆2 −

(

t − r

2ed I

)2

, 0

}

(7)

for t ≥ r and

(wd − wu)(r − t)

2∆max

{

∆ −r − t

2eu I, 0

}

+(wueu + wded)I

2∆max

{

∆2 −

(

r − t

2eu I

)2

, 0

}

(8)

for t ≤ r. Since ∆ < (r − t)/(2eu I) for t ≤ r and ∆ < (t − r)/(2ed I) for t ≥ r inducean expected loss and no investment implies zero expected profit for the group, thefollowing search for the optimal transfer price and investment concentrates on ∆ ≥(r − t)/(2eu I) for t ≤ r, ∆ ≥ (t − r)/(2ed I) for t ≥ r, and I > 0.

For wu ≥ wd, the transfer price maximizing (8) for given investment is t = r. Fort ≥ r, expression (7) applies. The first-order condition for the transfer price reads

t = r +2(wu − wd)e2

d∆I

wu(eu + 2ed) − wded.

The first derivative of (7) with respect to I in combination with the marginal net invest-ment costs yields the first-order condition

I =wu(eu + ed)

2(wuau + wdad)∆

(

t − r

2ed I

)2

+wueu + wded

4(wuau + wdad)∆

(

∆2 −

(

t − r

2ed I

)2)

.

The unique solution of these conditions is

Ii =w2

u∆(eu + ed)2

4(

wu(eu + 2ed) − wded

)

(wuau + wdad)

23

and

ti = r +2(wu − wd)∆e2

d Ii

wu(eu + 2ed) − wded= r +

(wu − wd)w2u∆

2e2d(eu + ed)

2

2(

wu(eu + 2ed) − wded

)2(wuau + wdad)

.

(ti, Ii) proves to be the unique global maximizer of (3) for wu ≥ wd taking into accountthat (7) and (8) coincide for t = r and that (7) is strictly concave in (t, I) and tends tozero for I → 0. Due to the symmetry of (7) and (8) the proof for a bilateral investmenteffect with wd ≥ wu is analog to the case wu ≥ wd and can be omitted here.

Also by symmetry, the proof for unilateral investment effects concentrates on eu = 0.Internal trade requires t ≥ r so that the corner solution ti = r maximizes (7) for wd ≥wu. Maximizing the right hand side of (7) less the net investment costs for t = r over Iyields

Ii =wd∆ed

4(wuau + wdad).

The proposition covers this solution. It also covers the solution for wu ≥ wd becausethe maximization of (7) for eu = 0 is a special case of the corresponding optimizationproblem in the case of a bilateral investment effect.

Proposition 6

The maximal net profit of the group for external trade is zero. Therefore, internal tradeis optimal yielding at least zero profit by letting I = 0 and t = r.

Due to the symmetry of the objective function and the bandwidth of arm’s lengthprices it suffices to give the explicit proof for wu ≥ wd. C chooses t = r + 2∆ed I forwu > wd. Then

Ic =(wu − wd)∆ed

wuau + wdad

maximizes (6). The transfer price turns out to be

tc = r + 2∆ed Ic = r +2(wu − wd)∆

2e2d

wuau + wdad.

wu = wd makes any investment unprofitable and reduces the bandwidth of arm’slength prices to t = r. The solution tc = r and Ic = 0 for wu = wd is included inthe above expressions. Similarly, note that it is not necessary to analyze unilateral in-vestment effects separately.

Lemma 2

Under both integrated and financial transfer pricing only the internal trade decisionis delegated. Then the group’s optimization problem is to maximize the objectivefunction (3) with respect to the investment I and the transfer price t under the band-width condition t ∈ [r − 2∆eu I, r + 2∆ed I]. The unique optimal solution

(

Ii, ti)

is re-alized under integrated transfer pricing, see Proposition 5. In contrast, under finan-cial transfer pricing with wu 6= wd, T sets the transfer price to a corner solution, i.e.,t ∈ {r − 2∆eu I, r + 2∆ed I}. Then C maximizes (3) with respect to I. Obviously, the

24

corresponding solution(

I f , t f)

is not optimal iff(

Ii, ti)

is an inner solution, i.e., ti ∈(

r − 2∆eu Ii, r + 2∆ed Ii)

, because(

Ii, ti)

and(

I f , t f)

coincide iff(

Ii, ti)

is a corner so-lution. By assumption, decisions made for wu = wd are the same under fiscal andintegrated transfer pricing.

25