Embed Size (px)

Citation preview

M&A Salesforce.com & Slack.Inc

Target Price: $23.7 USD Billion

Valuation as of 12 February 2020

Executive Summary

Executive

Summary

Financial

Analysis

Final

RecommendationValuation

4.7 0.9

A Promising Team Collaboration Software Engine

4.7 0.9

Should Salesforce acquire Slack?

YES!

1) The important role of the team collaboration software industryfor the pandemic and post-pandemic work dynamics.

2) The need of both companies to enhance their portfolio ofservices to expand their market share.

3) The cross-crossing customer opportunities expected after theacquisition.

We recommend an acquisition

for 23,7$ Billion

Strategic Rationale

for Acquisition

Main drivers

Financial Analysis

Financial Analysis

Executive

Summary

Financial

Analysis

Final

RecommendationValuation

4.7 0.94.7 0.9-400.00

-200.00

0.00

200.00

400.00

600.00

800.00

1,000.00

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Source: fool.com & Team Assessment

Salesforce’s EBIT over Time

Salesforce presented a 27% CAGR increase in revenues from 2016 to2020….

…Nonetheless, it has always struggled with keeping their OperatingMargins low, compared to its competitors.

Operating Margins for Salesforce & Competitors (2019)

0.00% 8.00% 16.00% 24.00% 32.00%

Salesforce.com

Adobe Inc.

SAP SE

Source: Refinitiv & Team Assessment

Strategic Rationale

for Acquisition

Salesforce

Financial Analysis

Financial

Analysis

Final

RecommendationValuation

4.7 0.94.7 0.9

Source: NASDAQ , Refinitiv & Team Assessment

Salesforce Cash flows from…

In August FY21, Salesforce reported the following… What caused the negative Net Change in Cash (CC&E)? InvestingActivities.

-$3,000.000

-$2,500.000

-$2,000.000

-$1,500.000

-$1,000.000

-$500.000

$0.000

IA With Acquisitions IA Without Acquisitons

Source: NASDAQ , Refinitiv & Team Assessment

Executive

Summary

Strategic Rationale

for Acquisition

All in all, Operating Cash Flows offer a more encompassing measurethat focuses just on the company’s ability to make profits from itsday-to-day business.

Salesforce Investing Activities Including and Excluding Acquisitions

Salesforce

Financial Analysis

Financial

Analysis

Final

RecommendationValuation

4.7 0.9

Slack and Microsoft’s Revenues Growth Rate

Slack currently presents non-reliable historical data for forecastingpurposes, since it is recently new to the public market.

109.7%

81.62%

57.39%

15.38% 16.7%

40%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2018 2019 2020

Slack Technologies Microsoft Teams

Source: Refinitiv, businessofapps.com & Team Assessment

Low levels in EBITDA Margin are due to elevated OperatingExpenses, which account for more than 100% of revenues.

-160.00%

-140.00%

-120.00%

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

2017 2018 2019 2020

EBITDA Margins for Slack

Source: Forbes, Refinitiv & Team Assessment

Executive

Summary

Strategic Rationale

for Acquisition

Slack

Financial Analysis

Financial

Analysis

Final

RecommendationValuation

4.7 0.9

Slack has showed the importance of Cash for tech-companies. Liquidity and Profitability comparisons with Zoom are as following…

Profit Margins for Slack & Zoom

2.67

3.56

0.53

0.70

1.82

2.96

0.420.54

3.28

1.87

0.85 0.83

0.00

0.80

1.60

2.40

3.20

4.00

Zoom Video Slack Tech. Zoom Video Slack Tech.

Current Ratio Cash Ratio

Zoom Video 2018

Zoom Video 2019Zoom Video 2020

Slack Tech. 2018

Slack Tech. 2018

Slack Tech. 2018

Source: Refinitiv & Team Assessment

Liquidity for Slack & Zoom

Source: Refinitiv & Team Assessment

79.5% 79.7% 81.5% 81.5%

-23.6%

-5.4%

0.0% 3.5%

-139.67%

-82.06%

-35.12%

-90.58%

-150.0%

-100.0%

-50.0%

0.0%

50.0%

100.0%

2017 2018 2019 2020

Zoom's Gross Margin Zoom's Net Margin

Slack's Gross Margin Slack's Net Margin

Executive

Summary

Strategic Rationale

for Acquisition

Slack

Strategic Rationale

Strategic Rationale

Financial

Analysis

Final

RecommendationStrategic Rationale for

AcquisitionValuation

4.7 0.9

Forecasts for Slack

0%

20%

40%

60%

202

2E

202

3E

202

4E

202

5E

202

6E

202

7E

202

8E

202

9E

203

0E

203

1E

Slack without Synergy Slack with Synergy

Growth Projections for

Slack

Source: Grand View Research, Salesforce.com

& Team Assessment

0.0

10.0

20.0

30.0

40.0

50.0

201

9

202

0

202

1

202

2E

202

3E

202

4E

202

5E

202

6E

202

7E

202

8E

202

9E

203

0E

203

1E

Team Collaboration Software Market Size (in billions)

Market Size Expectations

Source: IDC & Team Assessment

The panorama for Slack is positive but incapable of exploiting the potentialgrowth of the market without an acquisition by Salesforce.

• Slack without acquisition:

• If Slack is acquired by Salesforce:

• In the long term, the growth of Slack will most likely converge to the 12,7%market CAGR expected by The Grand View Research.

According to Deloitte:

“Even though the end of the pandemic will suppose the return of manyworkers to a physical space, most CEOs think that around 36% of theiremployees will continue working at home from the beginning of

january 2022 onwards” (Kaiser, Schatsky, & Jones, 2020).

28% CAGR

38% CAGR

First 5 years

Executive

Summary

Strategic Rationale

Financial

Analysis

Final

RecommendationStrategic Rationale for

AcquisitionValuation

4.7 0.9

Forecasts for Salesforce

Growth Projections for

Salesforce

Source: Grand View Research, Salesforce.com

& Team Assessment

Salesforce's biggest challenges for the future is to maintain its leading positionin market share.

• Salesforce without acquisition:

• Salesforce with acquisition:

• In the long term, Salesforce´s growth is expected to converge to the CRMmarket growth ( CAGR of 14,2%) according to The Grand View Research.

19% CAGR

20% CAGR

First 5 years

0%

10%

20%

30%

202

2E

202

3E

202

4E

202

5E

202

6E

202

7E

202

8E

202

9E

203

0E

203

1E

Salesforce without Synergy Salesforce with Synergy

Salesforce acquiring Slack poses a significant opportunity ofgrowth in a highly demanded and rapid changing market.

0.0

50.0

100.0

150.0

200.0

250.0

201

9

202

0

202

1

202

2E

202

3E

202

4E

202

5E

202

6E

202

7E

202

8E

202

9E

203

0E

203

1E

CMR Market Size (in billions)

Market Size Expectations

Source: IDC & Team Assessment

Executive

Summary

Strategic Rationale

Financial

Analysis

Final

RecommendationStrategic Rationale for

AcquisitionValuation

Value drivers for the acquisition

Slack´s trajectory, and key business metrics, shows why it is especially valuable forSalesforce´s future plan of maintaining their lead in the CRM market.

1. Customer Retention:

90% 88% 85% 82% 80%

0%

20%

40%

60%

80%

100%

1 2 3 4 5Years

1 2 Customer Spend:

$1

$9

$0

$2

$4

$6

$8

$10

0 1 2 3 4 5 6

Customer Spend Growth since Year of

Acquisition

Source: Theta Equity Partners & Team Assessment

Retention rate

(Years since newly acquire customer)

3 Low Customer´s Overlap:

Source: (S. Butterfield, December 18, 2020)

Approximately 90% of Slack´s paidcustomers (132,000) are not alreadyon Salesforce.

Most of them are small business.

Layering Slack’s technology onto the Salesforce 360 platform is expected to improve the user interface making it more attractive to its customers.

Executive

Summary

Valuation

Valuation

Financial

Analysis

Final

RecommendationValuation

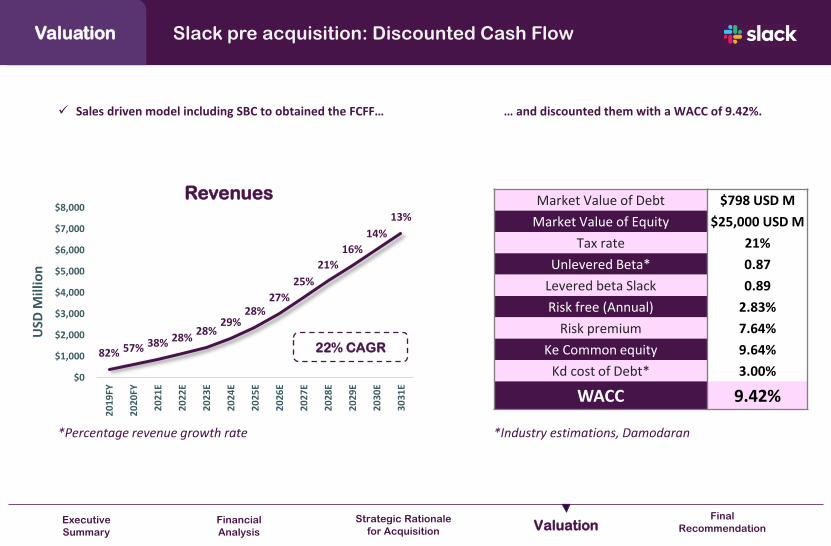

Slack pre acquisition: Discounted Cash Flow

Market Value of Debt $798 USD M

Market Value of Equity $25,000 USD M

Tax rate 21%

Unlevered Beta* 0.87

Levered beta Slack 0.89

Risk free (Annual) 2.83%

Risk premium 7.64%

Ke Common equity 9.64%

Kd cost of Debt* 3.00%

WACC 9.42%

82% 57% 38% 28%28%

29%28%

27%

25%

21%

16%

14%

13%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

20

19FY

20

20FY

20

21E

20

22E

20

23E

20

24E

20

25E

20

26E

20

27E

20

28E

20

29E

20

30E

30

31E

USD

Mill

ion

Revenues

*Percentage revenue growth rate

✓ Sales driven model including SBC to obtained the FCFF…

22% CAGR

… and discounted them with a WACC of 9.42%.

*Industry estimations, Damodaran

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

Financial

Analysis

Final

RecommendationValuation

Slack pre acquisition: Discounted Cash Flow

✓ We decided to include SBC because of ownership dilution. Moreover, use a reinvestment factor of 1.75 following Damodaran’s method.

Team estimations

Management forecasts & Team estimations

Damodaran´s method

In Million USD 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 3031E

Revenues $1,116 $1,432 $1,847 $2,369 $3,009 $3,761 $4,551 $5,279 $6,018 $6,801

Revenues Growth Rate 28.3% 28.3% 29.0% 28.3% 27.0% 25.0% 21.0% 16.0% 14.0% 13.0%

Stock-based compensation (SBC) $77 $99 $127 $163 $208 $260 $314 $364 $415 $469

EBIT Including SBC ($92) ($5) $101 $234 $397 $589 $1,051 $1,219 $1,390 $1,571

EBIT (1- T) Including SBC ($92) ($5) $80 $185 $314 $466 $831 $963 $1,098 $1,241

EBIT (1-T) % of revenues -8.2% -0.4% 4.3% 7.8% 10.4% 12.4% 18.2% 18.2% 18.2% 18.2%

Reinvestments $140 $180 $237 $298 $365 $429 $450 $415 $421 $446

Free Cash Flow to Firm (With SBC) ($232) ($186) ($157) ($112) ($51) $37 $380 $548 $677 $795

FCFF % of revenues -20.8% -13.0% -8.5% -4.7% -1.7% 1.0% 8.4% 10.4% 11.2% 11.7%

Software industry average

PV(Terminal Value) PV(Cash Flows) Perpetual Growth

$6,908 $517 4.53%

Slack Individual DCF

Valuation 7.4 USD Bn

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

Financial

Analysis

Final

RecommendationValuation

Slack pre acquisition: Relative Valuation

02468

1012141618

Text

ura

Co

rp.

Mar

keto

Inc.

Lin

ked

In C

orp

.

De

man

dw

are,

Inc

Net

suit

e In

c.

Cal

lidu

s So

ftw

are

, In

c

Mu

leSo

ft In

c.

Ad

apti

ve In

sigh

ts, I

nc

Ho

rto

nw

ork

s, In

c

Red

Hat

, In

c

Sen

dG

rid

, In

c

Ap

pti

o, I

nc

Min

db

oo

dy,

Inc

The

Ult

imat

e S

oft

war

eG

rou

p, I

nc.

Tab

leu

So

ftw

are

, In

c

Filtered Not Filtered Lineal (Filtered) Lineal (Not Filtered)

NTM Revenue Multiple

• NetSuite acquisition by Oracle

• Tableau acquisition by Salesforce

• Adaptive Insights acquisition by Workday

15,7$ Billion

1,55$ Billion

9,3$ Billion

Source: JP Morgan & Team Assessment

✓ Most of the transactions selected are software as a service companies acquiring other companies to complement the portfolio ofservices offered to their clients and maintain their market relevance.

Slack Individual DCF

Valuation 9.4 USD Bn

8.4 Revenue Multiple

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

Financial

Analysis

Final

RecommendationValuation

4.7 0.9

Slack pre acquisition:

4.7 0.9We issued an ACQUISITION recommendation for Slack

Discounted Cash Flow (FCFF)

75% 25%

M&A Comps

7.9 USD Bn

Slack Company Value

Free Cash Flow to Firm

Sales-driven model Historical transactions

Revenue multiple analysisIncluding Stock-Based

Compensation

Considering both DCF and M&A Comps valuation

Individual value without synergy acquisition

7.4 USD Bn 9.4 USD Bn

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

Financial

Analysis

Final

RecommendationValuation

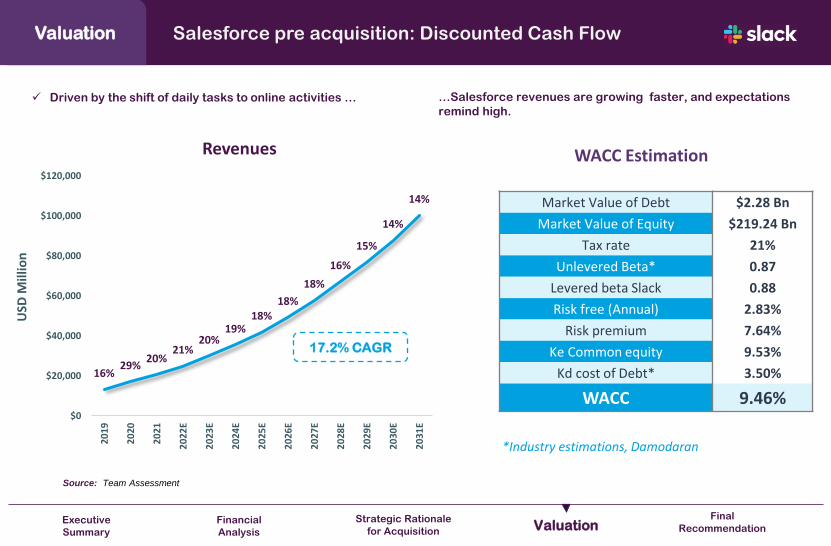

Salesforce pre acquisition: Discounted Cash Flow

✓ Driven by the shift of daily tasks to online activities … …Salesforce revenues are growing faster, and expectations

remind high.

16%29%

20%21%

20%19%

18%18%

18%

16%

15%

14%

14%

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

20

19

20

20

20

21

20

22E

20

23E

20

24E

20

25E

20

26E

20

27E

20

28E

20

29E

20

30E

20

31E

Revenues

Source: Team Assessment

WACC Estimation

USD

Mill

ion

Market Value of Debt $2.28 Bn

Market Value of Equity $219.24 Bn

Tax rate 21%

Unlevered Beta* 0.87

Levered beta Slack 0.88

Risk free (Annual) 2.83%

Risk premium 7.64%

Ke Common equity 9.53%

Kd cost of Debt* 3.50%

WACC 9.46%

17.2% CAGR

*Industry estimations, Damodaran

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

✓ Achieving higher revenues is Salesforce main objective. Therefore, our model is a sales-driven model

Financial

Analysis

Final

RecommendationValuation

Team estimations

Management forecasts & Team estimations

VP (Terminal Value) VP(FCF)Perpetual Growth

$206,548 $67,907 4.53%

In Million USD 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E

Revenues $24,940 $29,929 $35,465 $41,938 $49,277 $57,900 $67,164 $76,903 $87,862 $100,338

Revenues Growth Rate 21% 20% 19% 18% 18% 18% 16% 15% 14% 14%

EBIT $1,267 $1,673 $2,181 $2,966 $4,007 $5,415 $7,224 $9,512 $12,497 $15,051

EBIT (1-T) $1,001 $1,322 $1,723 $2,343 $3,166 $4,278 $5,707 $7,514 $9,873 $11,890

EBIT (1-T) % of Revenues 4.0% 4.4% 4.9% 5.6% 6.4% 7.4% 8.5% 9.8% 11.2% 11.9%

Depreciation, Depletion & Amortization $2,117 $2,541 $3,011 $3,561 $4,184 $4,916 $5,702 $6,529 $7,459 $8,519

Capital Expenditures $1,284 $1,541 $1,826 $2,160 $2,538 $2,982 $3,459 $3,961 $4,525 $5,167

Change in Non Cash-NetWoring Capital -$2,602 -$2,872 -$3,551 -$4,112 -$4,883 -$5,707 -$6,638 -$7,590 -$8,678 -$9,907

Free Cash Flow (FCF) $4,436 $5,193 $6,459 $7,855 $9,695 $11,919 $14,588 $17,673 $21,485 $25,148

Salesforce Individual

DCF Valuation274.45 USD Bn

Executive

Summary

Strategic Rationale

for Acquisition

Salesforce pre acquisition: Discounted Cash Flow

Valuation

Financial

Analysis

Final

RecommendationValuation

0.9

Salesforce pre acquisition: Relative Valuation

-50

0

50

100

150

200

250

-1 4 9 14 19 24 29 34

EV/E

BIT

DA

EV/Revenues

Salesforce Multiple Prices

Multiple Estimation (Bn) Stock Price

EV/Revenues $254.6 $279.4

EV/EBITDA $78.3 $87.32

P/B $497.1 $541.64

P/S $412.2 $449.1

Median Price $339.4

$ 309.6 Billion

✓ Overall, the market expectations and ongoing crisis increased… …market cap of tech companies, nevertheless Salesforce is

still overpriced relative to its EBITDA

Multiple Analysis Enterprise

Value Ratio

Source: Refinitiv & Team Assessment *Note: Bubbles represent Market Cap

Relative Valuation estimated EV

*Note: Median Price Reduces Overestimation Bias

due to possible Outliers

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

Financial

Analysis

Final

RecommendationValuation

Salesforce pre acquisition

4.70.9 4.70.9

Discounted Cash Flow (FCFF)

75% 25%

Relative Valuation

283.25 USD Bn

Salesforce Company Value

Free Cash Flow to Firm

Sales-driven model Historical transactions

Revenue multiple analysisIncluding Historical-Based

forecast

Salesforce will gain Market Share & Relevant customers Acquiring Slack

Executive

Summary

Strategic Rationale

for Acquisition

Valuation

Financial

Analysis

Final

RecommendationValuation

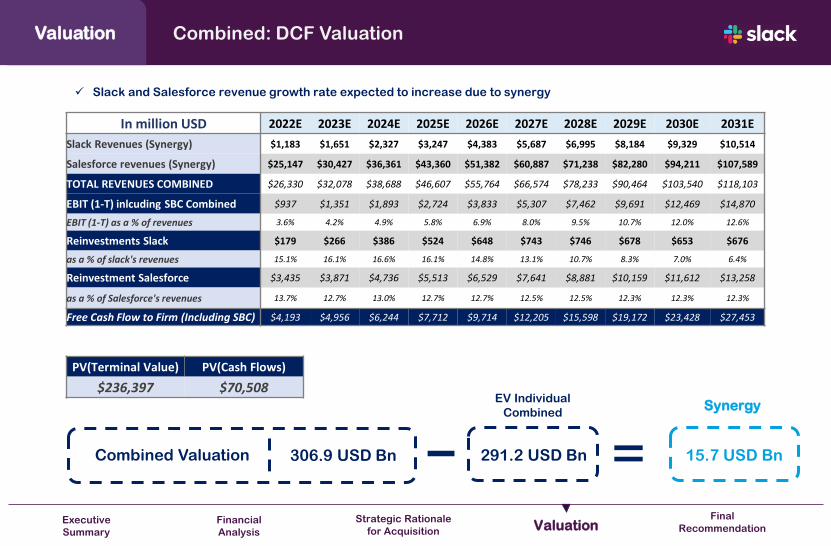

Combined: DCF Valuation

In million USD 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E

Slack Revenues (Synergy) $1,183 $1,651 $2,327 $3,247 $4,383 $5,687 $6,995 $8,184 $9,329 $10,514

Salesforce revenues (Synergy) $25,147 $30,427 $36,361 $43,360 $51,382 $60,887 $71,238 $82,280 $94,211 $107,589

TOTAL REVENUES COMBINED $26,330 $32,078 $38,688 $46,607 $55,764 $66,574 $78,233 $90,464 $103,540 $118,103

EBIT (1-T) inlcuding SBC Combined $937 $1,351 $1,893 $2,724 $3,833 $5,307 $7,462 $9,691 $12,469 $14,870

EBIT (1-T) as a % of revenues 3.6% 4.2% 4.9% 5.8% 6.9% 8.0% 9.5% 10.7% 12.0% 12.6%

Reinvestments Slack $179 $266 $386 $524 $648 $743 $746 $678 $653 $676

as a % of slack's revenues 15.1% 16.1% 16.6% 16.1% 14.8% 13.1% 10.7% 8.3% 7.0% 6.4%

Reinvestment Salesforce $3,435 $3,871 $4,736 $5,513 $6,529 $7,641 $8,881 $10,159 $11,612 $13,258

as a % of Salesforce's revenues 13.7% 12.7% 13.0% 12.7% 12.7% 12.5% 12.5% 12.3% 12.3% 12.3%

Free Cash Flow to Firm (Including SBC) $4,193 $4,956 $6,244 $7,712 $9,714 $12,205 $15,598 $19,172 $23,428 $27,453

✓ Slack and Salesforce revenue growth rate expected to increase due to synergy

PV(Terminal Value) PV(Cash Flows)

$236,397 $70,508

Combined Valuation 306.9 USD Bn 291.2 USD Bn

EV Individual

Combined

15.7 USD Bn

Synergy

Executive

Summary

Strategic Rationale

for Acquisition

Final Recommendation

Final Recommendation

Financial

AnalysisFinal

Recommendation

Strategic Rationale

for AcquisitionValuation

4.7 0.9We issued a BUY recommendation for Slack

Discounted Cash

Flow (FCFF)

75% 25%

M&A Comps

23.7 USD Bn

Slack Company

Value

Free Cash Flow to

Firm

Sales driven model Historical

transactions

Revenue multiple

analysis

15.7 USD Bn

Value of Synergy

Including Stock-Based

Compensation

7.9 USD Bn

Individual value

Executive

Summary

Thank You