Embed Size (px)

Citation preview

1

Magee Gammon Chartered Accountants

Charity Accounting and

The New SORP Regime

Andy Childs FCA

Disclaimer

• No responsibility for loss occasioned to any person acting or refraining from action as a result of the material in these slides can be accepted by the author or Magee Gammon, its principles or staff.

2

3

Introduction

• Implementing the new SORP(s)

• What has changed

• Where we go next

• Other matters of interest

4

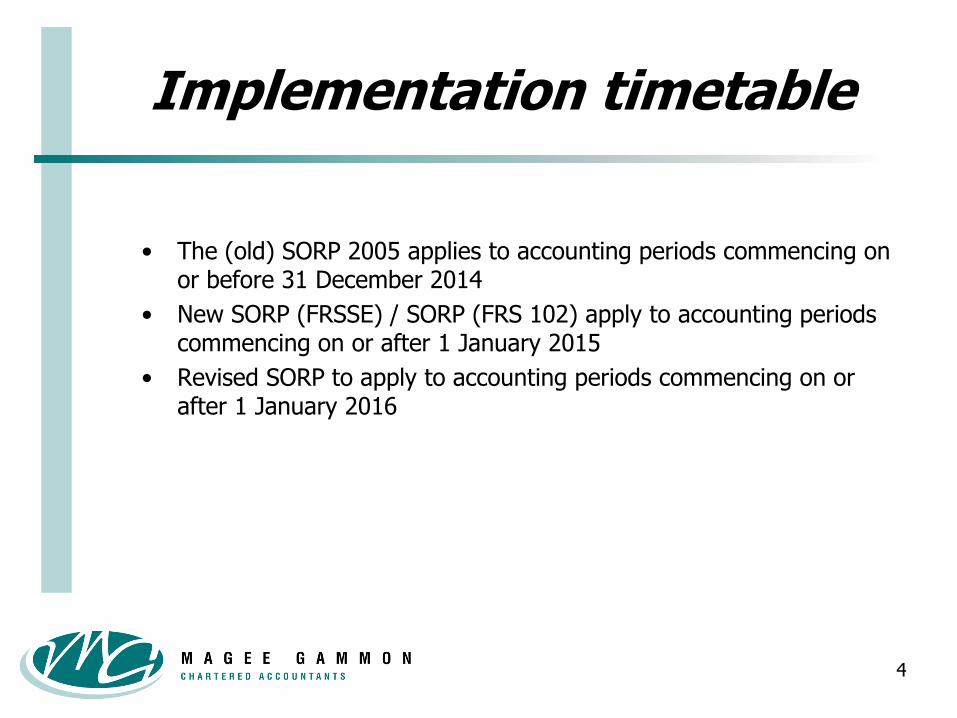

Implementation timetable

• The (old) SORP 2005 applies to accounting periods commencing on or before 31 December 2014

• New SORP (FRSSE) / SORP (FRS 102) apply to accounting periods commencing on or after 1 January 2015

• Revised SORP to apply to accounting periods commencing on or after 1 January 2016

5

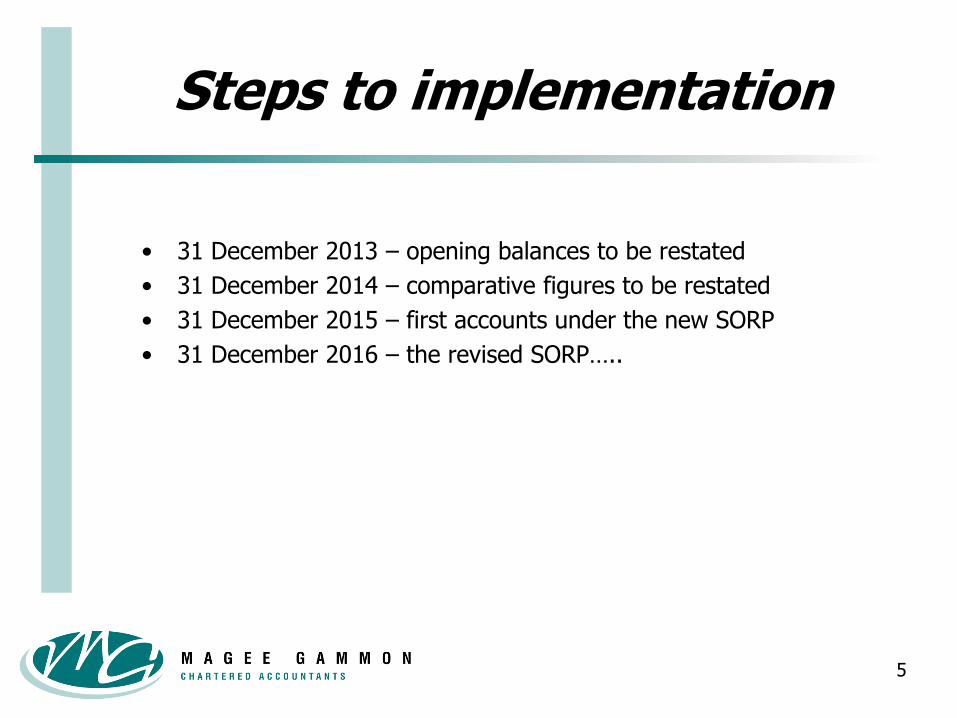

Steps to implementation

• 31 December 2013 – opening balances to be restated

• 31 December 2014 – comparative figures to be restated

• 31 December 2015 – first accounts under the new SORP

• 31 December 2016 – the revised SORP…..

6

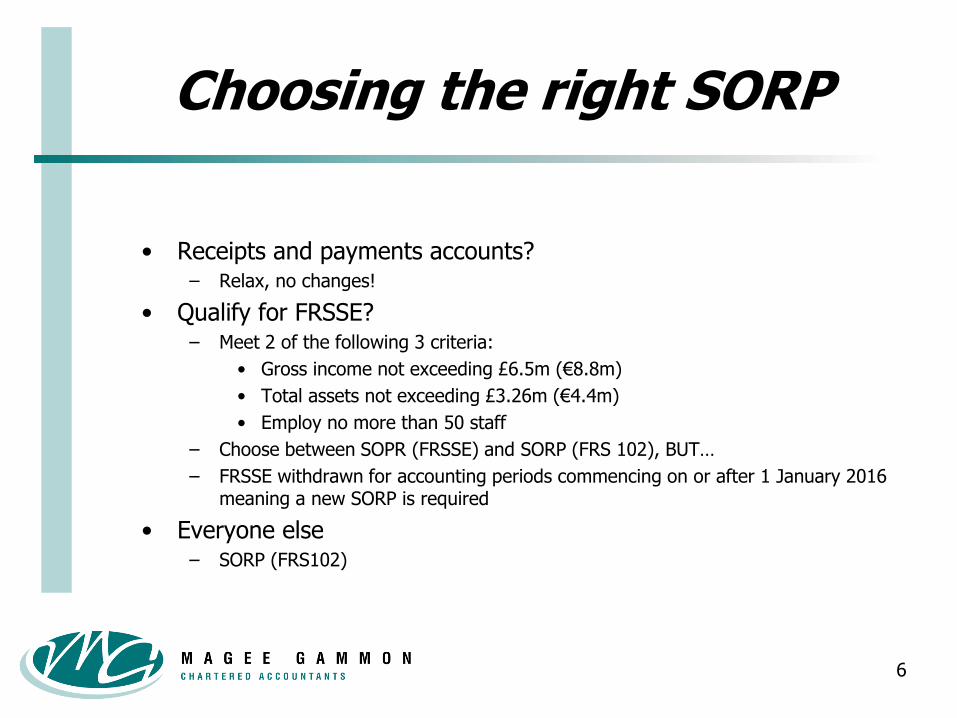

Choosing the right SORP

• Receipts and payments accounts?– Relax, no changes!

• Qualify for FRSSE?– Meet 2 of the following 3 criteria:

• Gross income not exceeding £6.5m (€8.8m)

• Total assets not exceeding £3.26m (€4.4m)

• Employ no more than 50 staff

– Choose between SOPR (FRSSE) and SORP (FRS 102), BUT…

– FRSSE withdrawn for accounting periods commencing on or after 1 January 2016 meaning a new SORP is required

• Everyone else– SORP (FRS102)

7

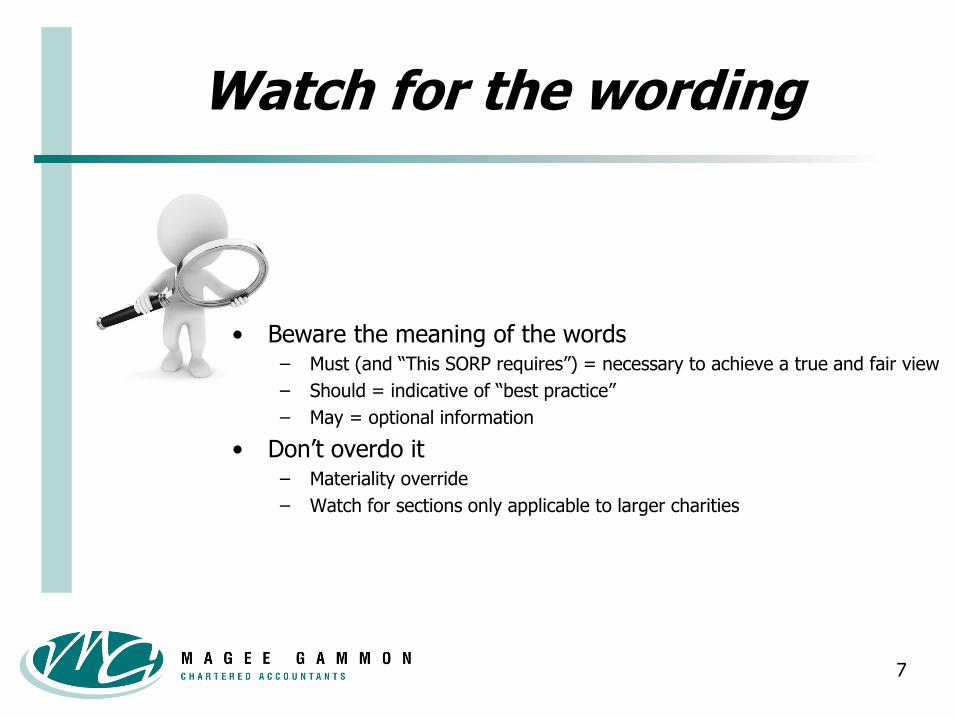

Watch for the wording

• Beware the meaning of the words– Must (and “This SORP requires”) = necessary to achieve a true and fair view

– Should = indicative of “best practice”

– May = optional information

• Don’t overdo it– Materiality override

– Watch for sections only applicable to larger charities

8

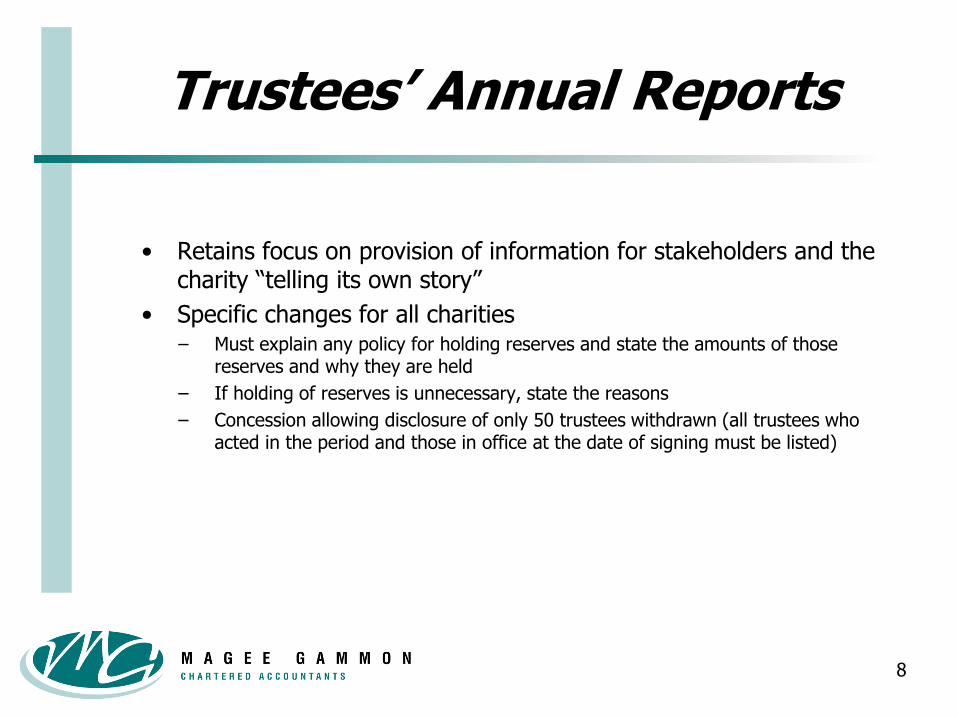

Trustees’ Annual Reports

• Retains focus on provision of information for stakeholders and the charity “telling its own story”

• Specific changes for all charities– Must explain any policy for holding reserves and state the amounts of those

reserves and why they are held

– If holding of reserves is unnecessary, state the reasons

– Concession allowing disclosure of only 50 trustees withdrawn (all trustees who acted in the period and those in office at the date of signing must be listed)

9

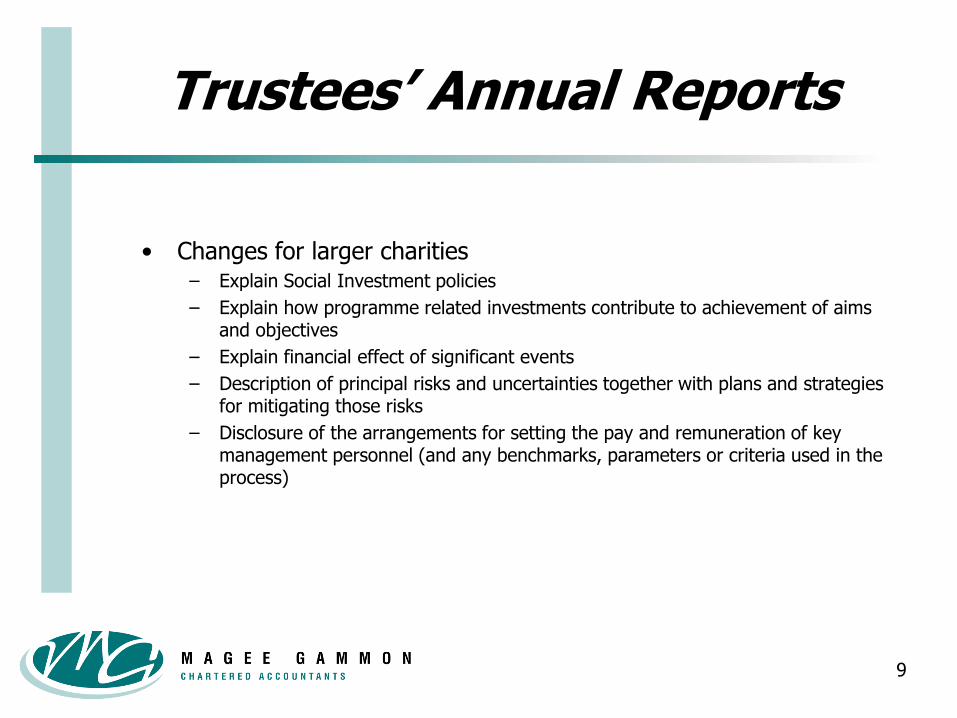

Trustees’ Annual Reports

• Changes for larger charities– Explain Social Investment policies

– Explain how programme related investments contribute to achievement of aims and objectives

– Explain financial effect of significant events

– Description of principal risks and uncertainties together with plans and strategies for mitigating those risks

– Disclosure of the arrangements for setting the pay and remuneration of key management personnel (and any benchmarks, parameters or criteria used in the process)

10

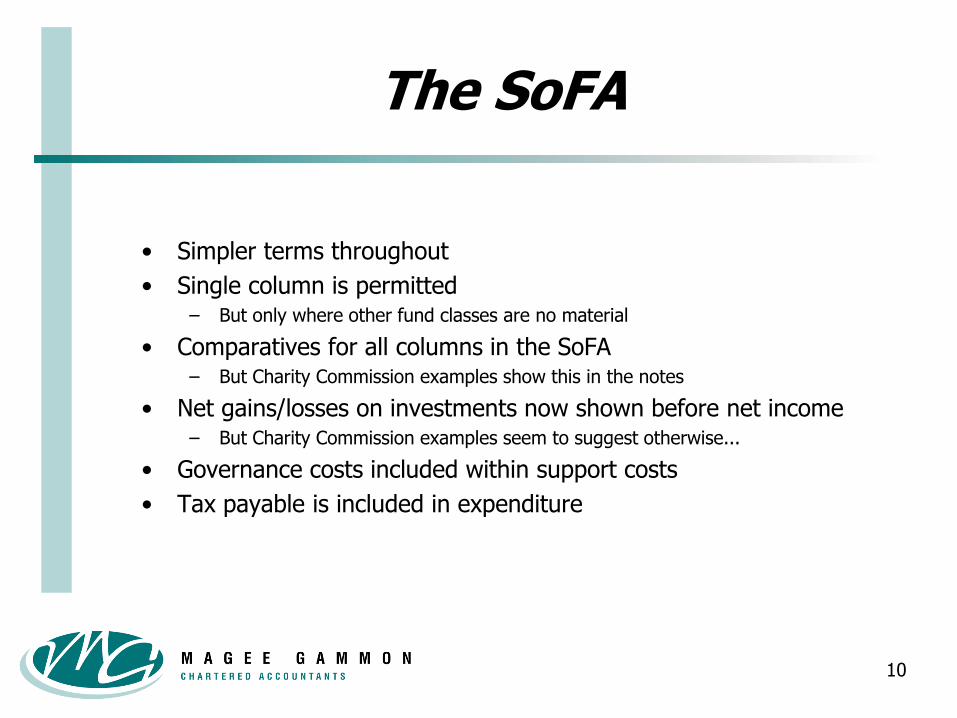

The SoFA

• Simpler terms throughout

• Single column is permitted– But only where other fund classes are no material

• Comparatives for all columns in the SoFA– But Charity Commission examples show this in the notes

• Net gains/losses on investments now shown before net income– But Charity Commission examples seem to suggest otherwise...

• Governance costs included within support costs

• Tax payable is included in expenditure

11

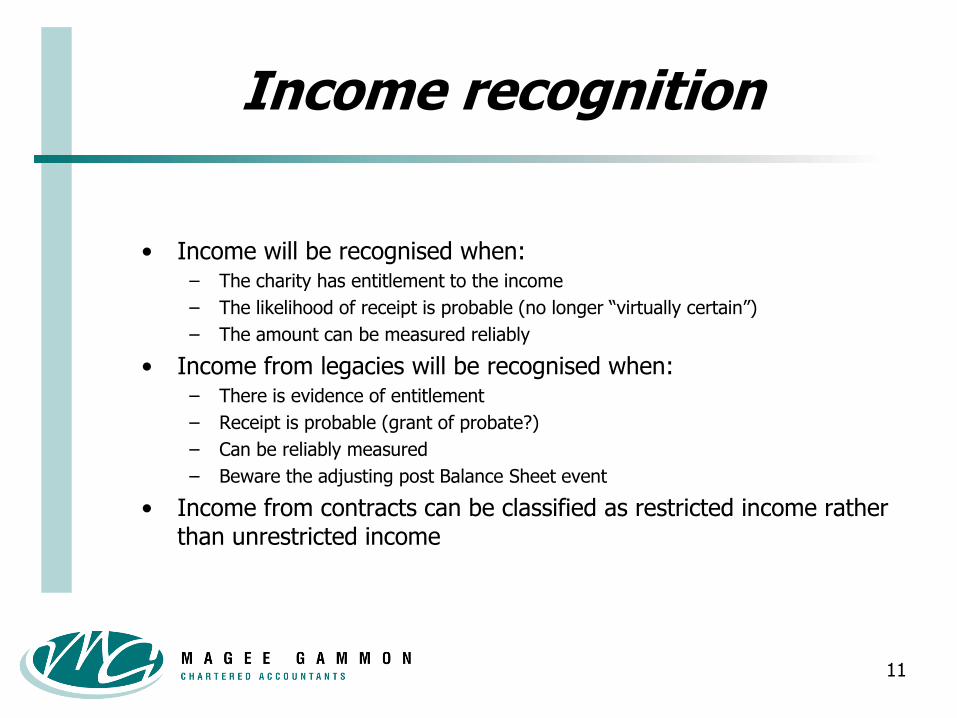

Income recognition

• Income will be recognised when:– The charity has entitlement to the income

– The likelihood of receipt is probable (no longer “virtually certain”)

– The amount can be measured reliably

• Income from legacies will be recognised when:– There is evidence of entitlement

– Receipt is probable (grant of probate?)

– Can be reliably measured

– Beware the adjusting post Balance Sheet event

• Income from contracts can be classified as restricted income rather than unrestricted income

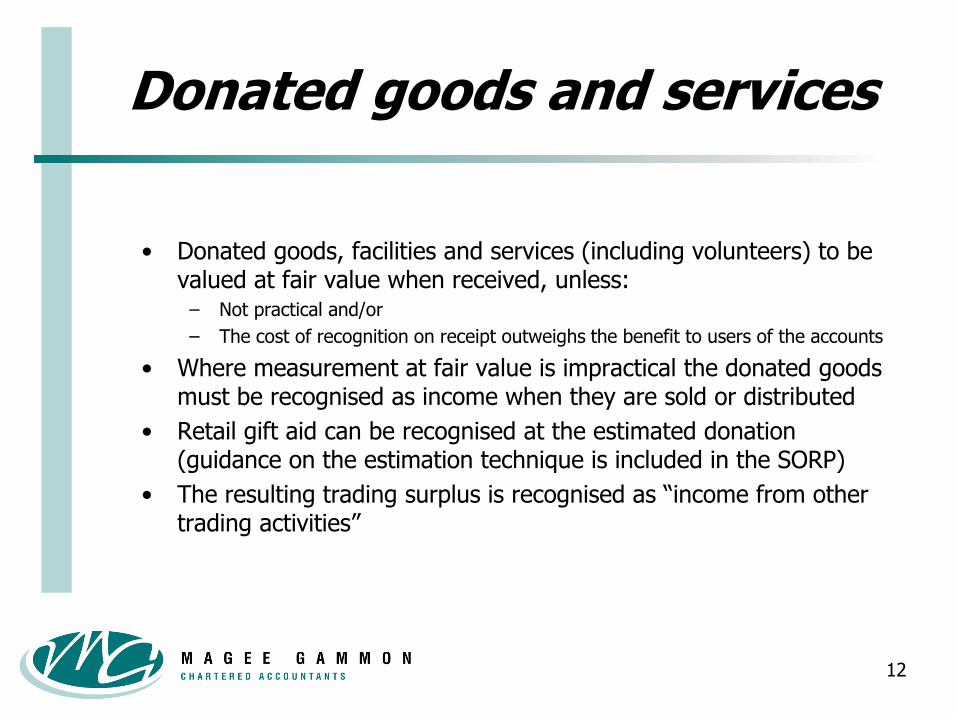

Donated goods and services

• Donated goods, facilities and services (including volunteers) to be valued at fair value when received, unless:

– Not practical and/or

– The cost of recognition on receipt outweighs the benefit to users of the accounts

• Where measurement at fair value is impractical the donated goods must be recognised as income when they are sold or distributed

• Retail gift aid can be recognised at the estimated donation (guidance on the estimation technique is included in the SORP)

• The resulting trading surplus is recognised as “income from other trading activities”

12

Donated goods and services

• Is it material?– Materiality for the SoFA may be different to the Balance Sheet

• Can it be quantified?– Exclusion represents an unadjusted error

• Incomplete records issue?

13

Expenditure

• Details of grants to institutions may no longer be made in a separate publication rather than in the notes to the accounts

– But it does permit this information to be provided on a charity’s webpage provided certain criteria are met

• Guidance on accounting for onerous contracts included in the SORP– Provisions may be required if the income stream is less than the expenditure

• Remember the holiday pay accrual– Is it material?

– Align the holiday year?

14

The Balance Sheet

• Format largely unchanged

• Changes in respect of:– Investment properties

– Social Investments

– Heritage assets

– Debtors due after more than one year

– Fund accounting

15

Investment properties

• One-off transitional adjustment for “deemed cost” of property– Increases asset base

– Is a valuation the appropriate use of charity funds?

• Investment properties are measured at cost and subsequently at fair value

– Valuations must be kept up to date (bear in mind type/location of asset)

– Valuations to be made by an independent expert (or disclose if this has not been done)

• Mixed use properties must be apportioned between operational and investment use unless impractical (then treat as tangible fixed asset)

• Property which is let or occupied by another group undertaking must be treated as an investment property

16

Social investment

• New class of investments for “social investment”– Charities (Protection and Social Investment) Bill

• Definition– A social investment is made when a relevant act (i.e. includes guarantees) of a

charity is carried out with a view to both:

a) Directly furthering the charity’s purposes; and

b) Achieving a financial return for the charity (better than spending it?)

• General exclusions– Endowment funds

– Charities established by Charter or legislation

17

Social investment

• What type of investment?– Financial investment

– Programme related investments (exclusively to further charity’s aims)

– Mixed motive investments (further charity’s aims and make financial return)

– Spending/grant making

• Do the trustees have the power to invest?– Is this included in the Governing Document?

• Statutory investment powers for trusts

• Limitation on the statutory investment power

• Express power of investment

• Does investment include Social Investment?

• Can an investment make a negative return?

18

Social investment

• Risk for the trustees– Could be in breach of duty

• Unacceptable private benefit:– Threaten tax reliefs

– Threaten charitable status

– Render transaction ultra vires

– Expose trustees to personal liability

• Trustees must quantify the mission benefit– CC14: “Calculated mission benefit + financial return = justification for social

investment”

• Consider and obtain professional advice

19

Heritage assets

• FRS102 definition adopted

• Explicit link between the objects of the charity and whether or not an asset qualifies as a heritage asset has been removed

• Recognised at cost or valuation with initial recognition of donated assets at fair value (where practicable)

20

Debtors recoverable >1 year

• Debtors recoverable more than 12 months after the year-end must be discounted to present value (if the effect is material)

21

Fund accounting

• Classification of funds is unchanged

• Separate investment revaluation reserve to be included in appropriate fund

• Reserve fund can be separated– Split the free reserves from other reserves

– Cannot create a negative reserve

• Transfers between funds must net to £nil– Removes one-sided transfers as a mechanism for dealing with the acquisition of,

or transfer of, trusts to or from another charity

• The reference to loans from one fund to another fund of the same charity has been removed

22

Financial instruments

• The SORP (FRS102) distinguishes between accounting for ‘basic’ financial assets and liabilities and ‘other’ financial assets and liabilities

• ‘Basic’ financial instruments are identified in the SORP (FRS102)

• If a charity holds ‘other’ financial instruments, refer to FRS102

• Other financial instruments include:– Options

– Forward contracts

– Swaps

– Hedging instruments

– Loan arrangements which includes rights of lender to vary returns unilaterally

• Accounting treatment under FRS102– Measured at fair value (usually the transaction price)

– Subsequent measurement is also at fair value

23

Retirement benefits

• Pension plans under FRS102 but schemes under FRSSE

• Defined benefit plans must follow FRS102

• Multi-employer defined benefit pension plan– Where the charity’s share of an actuarial deficit cannot be identified, these are

treated as defined contribution schemes (no change)

– Where an agreement is in place to make additional contributions based on current and past service of employees a liability must be recognised for the present value of outstanding additional contributions

– The liability for a group scheme must be recognised in (at least) one entity in the group

• FRSSE permits the charity to continue with its existing accounting policy

24

Branches, groups and combinations

• The SORP (FRS102) includes a flow chart to assist identification of which modules apply

• Intangibles– Must be separately identified and valued

• Goodwill– Presumption of 5 year life (unless there is a more reliable estimate)

– What about the estimate made under the old legislation?

• Merger accounting– Permitted under the SORP but may not be permitted for charitable companies

• Transition– Possibility to restate business combinations prior to transition

– Consideration for transactions in the interim

25

Groups

• Branches– Incorporated charities are specifically excluded from being treated as

branches

• Associates and joint ventures– Must apply equity method for joint ventures

• Charity subsidiaries– New guidance included in the SORP for disclosure required by charities

which are subsidiaries of another entity

• Groups– Control is defined in terms of power and benefit

– Parent company is required to prepare separate

statements (cash flow and SoFA) although these

may not actually need to be filed

26

Related party transactions

• Disclosure required for trustees to apply equally to de-facto trustees

• Trustee expenses include costs reimbursed and costs paid direct to third parties

– FRS102 also requires the total amount of expenses waived by trustees to be disclosed (unless immaterial)

• The number of staff paid £60,000 or more in bands of £10,000

• Additional disclosures under SORP (FRS102)– Aggregate value of unconditional donations made by trustees

– Charity’s contributions to a pension fund for the benefit of employees

– Terms and conditions of transactions with, and the details of any guarantee given or received from, related parties

– Information on the nature, accounting policy and funding of termination payments

– Total amount of employee benefits received by key management personnel

27

Statement of Cash Flows

• Statement of cash flows is required under SOPR (FRS102)

• Direct and indirect method still permitted

• Templates illustrating the indirect method are included in the SORP

• NOT required under SORP (FRSSE)

28

Where we go next

• FRSSE ceases to exist for accounting periods commencing on or after 1 January 2016

• SORP consultation ran for 3 months from 18 June to 18 September 2015

29

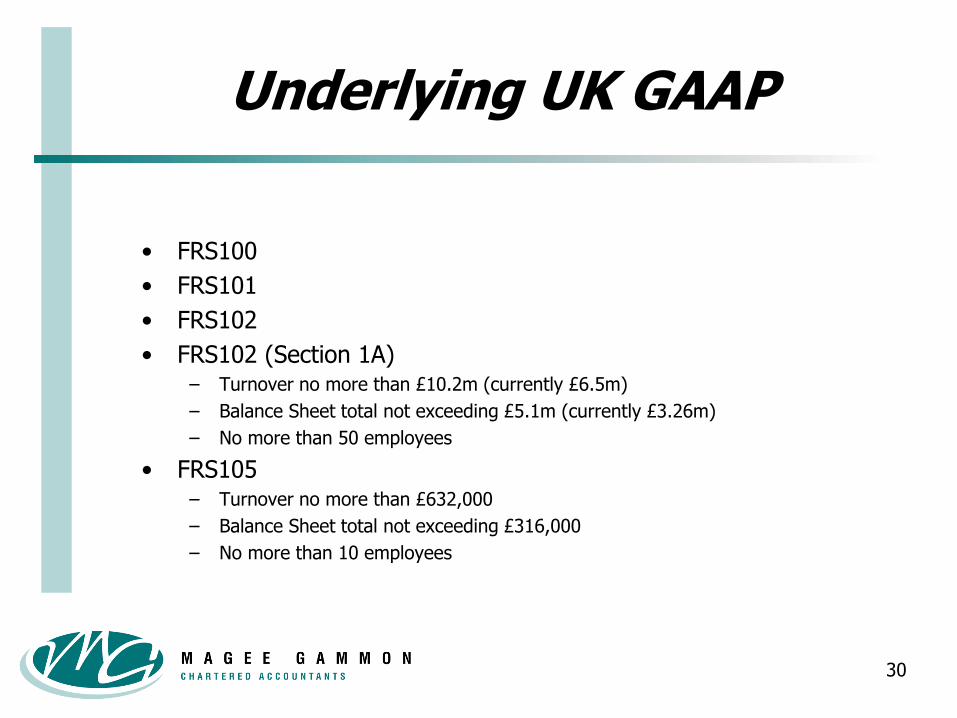

Underlying UK GAAP

• FRS100

• FRS101

• FRS102

• FRS102 (Section 1A)– Turnover no more than £10.2m (currently £6.5m)

– Balance Sheet total not exceeding £5.1m (currently £3.26m)

– No more than 50 employees

• FRS105– Turnover no more than £632,000

– Balance Sheet total not exceeding £316,000

– No more than 10 employees

30

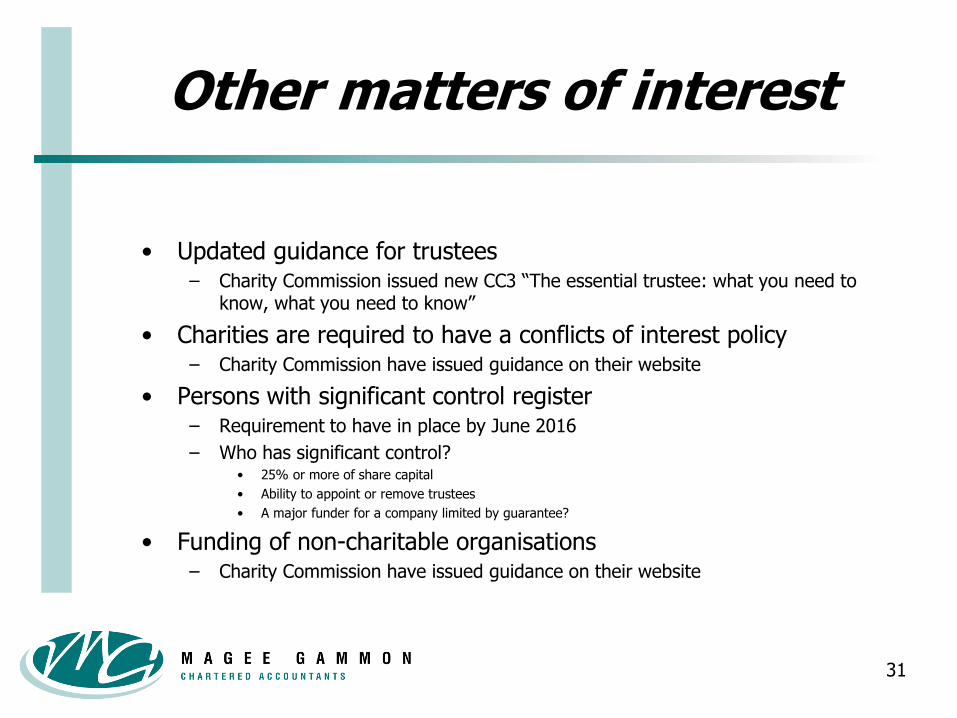

Other matters of interest

• Updated guidance for trustees– Charity Commission issued new CC3 “The essential trustee: what you need to

know, what you need to know”

• Charities are required to have a conflicts of interest policy– Charity Commission have issued guidance on their website

• Persons with significant control register– Requirement to have in place by June 2016

– Who has significant control?• 25% or more of share capital

• Ability to appoint or remove trustees

• A major funder for a company limited by guarantee?

• Funding of non-charitable organisations– Charity Commission have issued guidance on their website

31

Don’t forget

• The wording of gift aid declarations was updated in September 2015

• Charities can continue to use the existing wording until April 2016

• New wording must be used from 6 April 2016

32

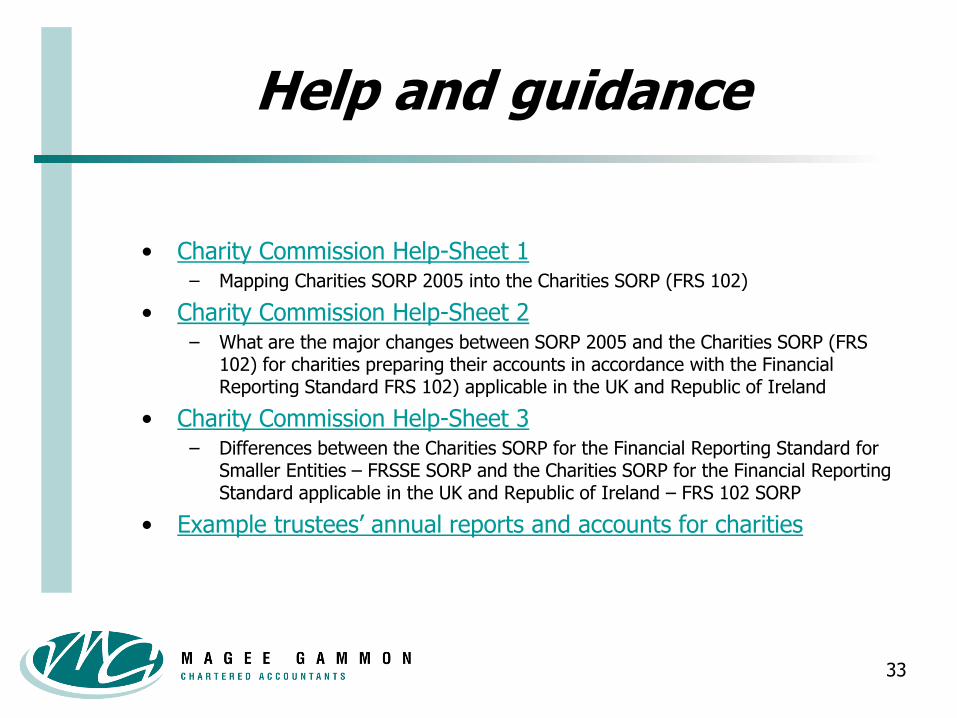

Help and guidance

• Charity Commission Help-Sheet 1– Mapping Charities SORP 2005 into the Charities SORP (FRS 102)

• Charity Commission Help-Sheet 2– What are the major changes between SORP 2005 and the Charities SORP (FRS

102) for charities preparing their accounts in accordance with the Financial Reporting Standard FRS 102) applicable in the UK and Republic of Ireland

• Charity Commission Help-Sheet 3– Differences between the Charities SORP for the Financial Reporting Standard for

Smaller Entities – FRSSE SORP and the Charities SORP for the Financial Reporting Standard applicable in the UK and Republic of Ireland – FRS 102 SORP

• Example trustees’ annual reports and accounts for charities

33

34

Any questions?

If you would like any further advice regarding the new SORP Regime

Please contact Andy Childs FCA

01233 630000

www.mageegammon.com