Embed Size (px)

Citation preview

Volume X, Issue 2October 2011

Volume X, Issue 2 October 2011

ISSN 0219-8908 Published in October 2011 Economic Policy Group Monetary Authority of Singapore http://www.mas.gov.sg All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanised, photocopying, recording or otherwise, without the prior written permission of the copyright owner except in accordance with the provisions of the Copyright Act (Cap. 63). Application for the copyright owner's written permission to reproduce any part of this publication should be addressed to: Economic Policy Group Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117 Printed by Xpress Print Singapore

Contents Preface i Highlights ii-iii Monetary Policy Statement iv-vi 1 Macroeconomic Developments 1.1 External Developments 2 1.2 Domestic Economy 6 1.3 Macroeconomic Policy 14

Box A: Review of MAS Money Market Operations in FY2010/11 23

2 Wage-Price Dynamics 2.1 Labour Market Conditions 28 2.2 Consumer Price Developments 31

3 Outlook 3.1 External Outlook 38 3.2 Outlook for the Singapore Economy 43

Box B: Global Trade in Services and its Implications for Singapore 53 3.3 Labour Market 57 3.4 Inflation 61

Special Features

Special Feature A: An Overview of the Satellite Model of Singapore 68 Special Feature B: Capital Flow Waves 77

Statistical Appendix 82 List of Selected Publications 92

Monetary Authority of Singapore Economic Policy Group

Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

LIST OF ABBREVIATIONS ACU Asian Currency Unit ASEAN Association of Southeast Asian Nations capex capital expenditures COE Certificate of Entitlement CPF Central Provident Fund CPI consumer price index CSP community, social & personal DLI Domestic Liquidity Indicator EIA Energy Information Administration EPG Economic Policy Group FAO Food and Agriculture Organisation of the United Nations FI Fiscal Impulse GFCF Gross fixed capital formation GST goods and services tax HDB Housing Development Board IMF International Monetary Fund IPI import price index IPO Initial Public Offering m-o-m month-on-month MENA Middle East/North Africa MEQ machinery and equipment MMS Monetary Model of Singapore NIEs newly-industrialised economies NEER nominal effective exchange rate OECD Organisation of Economic Cooperation and Development OPEC Organisation of the Petroleum Exporting Countries PMI Purchasing Managers’ Index q-o-q quarter-on-quarter REER real effective exchange rate SAAR seasonally-adjusted annualised rate SIBOR Singapore interbank offered rate SITC Standard International Trade Classification SOR swap offered rate SMS Satellite Model of Singapore WTO World Trade Organisation WTI West Texas Intermediate y-o-y year-on-year

Preface i

Preface The Macroeconomic Review is published twice a year in conjunction with the release of the MAS Monetary Policy Statement. The Review documents the Economic Policy Group’s (EPG) analysis and assessment of macroeconomic developments in the Singapore economy, and shares with market participants, analysts and the wider public, the basis for the policy decisions conveyed in the Monetary Policy Statement. It also features in-depth studies undertaken by EPG on important economic issues facing Singapore. The Review was edited by Associate Professor Peter Wilson, and continues to feature our collaborations with various academics. We are pleased to have Professor Kristin J. Forbes of MIT and Associate Professor Frank E. Warnock of the University of Virginia write about capital flow waves in Special Feature B of this issue. We are also grateful to Sanjay Kalra, the IMF Resident Representative for Vietnam and Laos, for his collaboration with EPG on Box A which examines the underlying drivers of global trade in services. The data used in the Review were drawn from the following government agencies, unless otherwise stated: BCA, CPF Board, DOS, EDB, HDB, IE Singapore, LTA, MOF, MOM, MTI, STB and URA. The Review may be accessed in PDF format on the MAS website: http://www.mas.gov.sg/publications/macro_review/index.html. The Review may also be purchased at major bookstores, online (http://asp.marketasia.com.sg/Spore/sporeindex.asp), or on an annual subscription basis (details can be found on the last page).

Monetary Authority of Singapore Economic Policy Group

ii Macroeconomic Review, October 2011

Highlights Since the last Review, global economic growth has faltered, with stresses in private and public balance sheets in the crisis-affected countries proving to be more severe, and the deleveraging process more protracted, than previously anticipated. Just as the supply shocks from the political unrest in the Middle East/North Africa (MENA) region and the Tohoku earthquake subsided, the global economy was confronted with fresh uncertainties over US fiscal sustainability and sovereign indebtedness in Europe. Against this backdrop, the Singapore economy recorded a marginal expansion of 1.3% q-o-q SAAR in Q3, with the bulk of this growth coming from pharmaceuticals. Looking ahead, the step-up in uncertainties in recent months has clearly skewed the risks towards the downside, with the outlook for Singapore very much dependent on how economic events in the US and Eurozone unfold. Chapter 1 begins with an overview of recent developments in the external environment and the domestic economy. The supply-chain disruptions from the Tohoku earthquake have largely dissipated, but the retraction in global demand alongside a rapid deterioration of global business and consumer confidence has led to further slowing of the Singapore economy. IT-related activities bore the brunt of the slowdown, partly due to Singapore’s larger exposure to component manufacturing, which generally tends to be more sensitive to changes in final demand. However, the tourism and retail sectors stayed buoyant, owing to continued income growth in the region and domestically. Chapter 2 examines recent trends in the labour market and prices. Notwithstanding the slower pace of employment growth, the labour market has remained tight, causing firms in some sectors to increase hours of work. Some firms responded to the tight labour supply by raising wages, which, coupled with weaker economy-wide labour productivity, has resulted in a further pickup in overall unit labour costs. Correspondingly, domestic price and cost pressures were relatively strong in the first half of the year amidst the high level of resource utilisation in the economy. Headline CPI inflation also rose sharply on a sequential basis, largely due to a rapid increase in accommodation costs and car COE prices. Chapter 3 turns to the prospects for both the external and domestic economies. Broadly, the outlook for the Singapore economy can be characterised by two phases, namely “stalled growth” over the next few quarters, followed by a “modest recovery” probably occurring sometime in the latter half of 2012. The first phase depicts the drag on domestic economic activity due to continued uncertainty and financial volatility in the external environment. Thereafter, if external uncertainties subside, the Singapore economy should experience a more discernible pick-up in activity. However, growth will still be modest, due to structural fragilities in the G3 economies. Accordingly, GDP growth in the Singapore economy could slow to below its potential rate of 3–5% in 2012. At the same time, the gradual narrowing of the positive output gap will have a restraining effect on domestic costs and prices next year, while weak global demand will dampen commodity prices. Also included in Chapter 3 is a box item that examines the underlying drivers of global trade in services. Singapore’s experience in services exports is benchmarked against the global surge in services trade over the last decade. The study shows that Singapore’s export share of modern services (which include financial and ICT services) is low compared to the global average. Coupled with potentially strong regional demand for services imports, there is considerable scope for expansion in these sectors. To complete this Review, we present two special feature items. In Special Feature A, we introduce the Satellite Model of Singapore (SMS), the latest addition to EPG’s suite of models. The SMS is a small quarterly macroeconomic model that provides a satellite view of the Singapore economy, making it more tractable for economic analysis. The SMS is principally used for policy simulations, and is based on core New Keynesian equations for aggregate demand, inflation and the monetary policy reaction function.

Monetary Authority of Singapore Economic Policy Group

Monetary Policy Statement iii

The SMS will complement EPG’s flagship model, the Monetary Model of Singapore (MMS), as essential tools for macroeconomic policy analysis at the MAS. This Review concludes with a Special Feature by Professors Kristin J. Forbes of MIT and Francis E. Warnock of the University of Virginia titled, “Capital Flow Waves”. This feature attempts to better understand the major ebbs and flows of international capital by using a novel approach to define four types of (gross) capital flow episodes—surges, stops, flight, and retrenchment—and differentiate between capital movements initiated by foreigners and residents. Using a probit-like model, they estimate the conditional probability of one of these episodes occurring within the quarter. Their results indicate a significant role for global factors and contagion in driving capital flow episodes, thus pointing to the importance of global institutions and cross-country cooperation in reducing capital flow volatility. In contrast, they find that many domestic factors only have a limited effect on capital flow volatility. This suggests that governments concerned about the effects of capital flow volatility should prioritise strengthening their country’s ability to withstand this volatility rather than trying to reduce it. The next issue of the Review will be released in April 2012.

Economic Policy Group Monetary Authority of Singapore

27 October 2011

Monetary Authority of Singapore Economic Policy Group

iv Macroeconomic Review, October 2011

14 October 2011

Monetary Policy Statement

INTRODUCTION 1. MAS re-centred the S$NEER policy band upwards in April this year, with no change to the slope and width of the band, amidst tight factor markets and strong pressures on domestic costs and prices. This was the third consecutive tightening move since April 2010, aimed at ensuring price stability in the medium term, while keeping growth on a sustainable path.

Chart 1

S$ Nominal Effective Exchange Rate (S$NEER)

Apr Jul Oct Jan Apr Jul Oct

96

100

104

108

112

Inde

x (1

Apr

201

0 =

100)

indicates release of Monetary Policy Statement

Appreciation

Depreciation

2010 2011

2. From April to early September 2011, the S$NEER (Chart 1) had generally appreciated and remained within the upper half of the policy band. This reflected the broad-based weakness in the US$ and investor interest in higher-growth economies. However, the S$NEER has since fallen to the lower half of the band, reflecting a pullback in investor risk appetite on concerns over the deepening debt crisis in the Eurozone and softer growth prospects for Asia. The domestic three-month interbank rate eased further after April, but has increased to 0.44% as of early October.

OUTLOOK FOR 2011 AND 2012 3. The Singapore economy has weakened over the last six months, weighed down by supply-side disruptions arising from the earthquake in Japan and, more recently, by faltering global demand. According to the Advance Estimates released by the Ministry of Trade and Industry today, Singapore’s GDP expanded marginally by 1.3% on a quarter-on-quarter seasonally adjusted annualised basis in Q3 2011, following the 6.3% contraction in the preceding quarter. The continued weakness in activity was most evident in electronics-related manufacturing, while sentiment-driven segments of the financial sector were also hit. The biomedical sector however provided support to GDP growth during the quarter.

Monetary Authority of Singapore Economic Policy Group

Monetary Policy Statement v

4. The outlook for the global economy has deteriorated sharply against the backdrop of increased uncertainty in financial markets. The Eurozone economy, faced with an ongoing sovereign debt crisis, will be constrained by fiscal austerity and tightening credit conditions. Private consumption in the US continues to be hampered by the sluggish labour market and anaemic housing prices, while firms remain cautious in their investment spending. With final demand in the advanced economies softening, growth in Asia will slow, notwithstanding some support from domestic demand. At the same time, the global IT industry continues to experience excess supply and could see further correction in output in the coming quarters. Against this backdrop, Singapore’s GDP growth in 2011 is expected to be around 5%. With the weak external environment likely to persist, the Singapore economy will expand more slowly in 2012 and growth could be below its potential rate of 3–5%. 5. The MAS measure of core inflation, which excludes private road transport and accommodation costs, stood at 2.2% in Q2 and the first two months of Q3, compared to 1.9% in Q1 2011. Core inflation better reflects underlying price pressures in the economy and is the most relevant among the range of indicators that MAS monitors for monetary policy. The core inflation over the last two quarters reflected higher global commodity prices compared to a year ago, as well as some pass-through of wage increases arising from the tight labour market. 6. Headline CPI inflation rose from 4.7% in Q2 2011 to 5.6% in July–August. This mainly reflected higher COE premiums and the imputed rental cost of owner-occupied housing, which is the largest component of accommodation costs in the CPI.1/ The core inflation has been significantly lower than headline inflation since the middle of 2010. (Chart 2)

Chart 2 Headline and Core CPI Inflation

2007 2008 2009 2010 2011 Jul-Aug

-2

0

2

4

6

8

0

-2

YO

Y %

Gro

wth

HeadlineInflation

Core Inflation

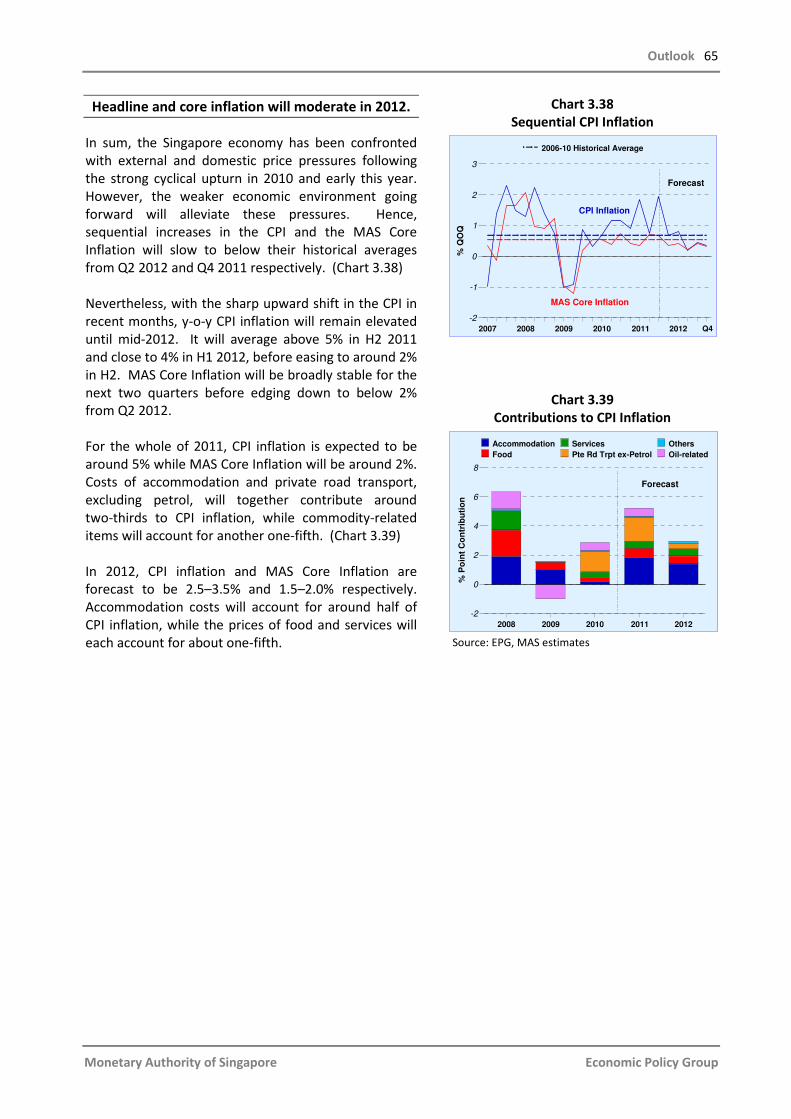

7. The ongoing slowdown in domestic economic activity will reduce tightness in the labour market and alleviate price pressures. Inflationary pressures emanating from abroad should also subside. As a result, core inflation should gradually ease from an estimated 2.3% in Q4 this year to 1.5% at the end of 2012. It is forecast to be around 1.5–2% in 2012, compared to about 2.1% in 2011. 8. The strength in rentals due to a temporary shortage of completed dwellings will, however, cause the imputed rental cost of owner-occupied housing to rise further at a fairly strong pace. Private road transport costs may also remain firm in response to the tight COE supply. As a result, headline inflation will be elevated for the rest of this year before easing, especially in the second half of 2012. For the full year, it is expected to come in at around 5% in 2011 and 2.5–3.5% in 2012.

__________________________________

1/ The CPI accommodation series also includes the costs of actual rented accommodation and minor repairs.

Monetary Authority of Singapore Economic Policy Group

vi Macroeconomic Review, October 2011

MONETARY POLICY 9. Given the stresses and fragility in the advanced economies, the prospects for growth in Singapore’s major trading partners have deteriorated. With the slowdown in demand, growth in the Singapore economy could fall below its potential rate of 3–5%. Thus, core inflation should ease next year, although headline inflation could stay elevated in the near term reflecting the higher imputed rental cost of owner-occupied housing. 10. MAS will continue with the policy of a modest and gradual appreciation of the S$NEER policy band in the period ahead. However, given the expected moderation in core inflation, the slope of the policy band will be reduced, with no change to the width of the band and the level at which it is centred.

Monetary Authority of Singapore Economic Policy Group

Chapter 1 Macroeconomic

Developments

2 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

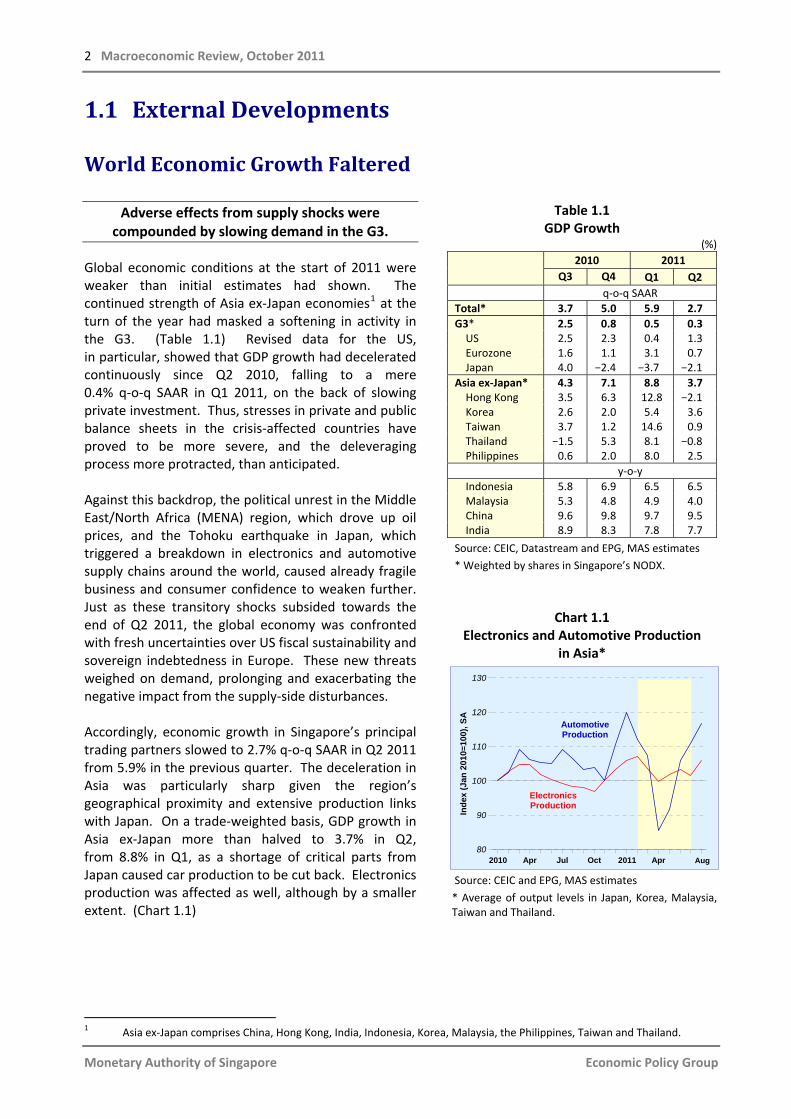

1.1 External Developments

World Economic Growth Faltered

Adverse effects from supply shocks were compounded by slowing demand in the G3.

Global economic conditions at the start of 2011 were weaker than initial estimates had shown. The continued strength of Asia ex-Japan economies1 at the turn of the year had masked a softening in activity in the G3. (Table 1.1) Revised data for the US, in particular, showed that GDP growth had deceleratedcontinuously since Q2 2010, falling to a mere 0.4% q-o-q SAAR in Q1 2011, on the back of slowing private investment. Thus, stresses in private and public balance sheets in the crisis-affected countries have proved to be more severe, and the deleveraging process more protracted, than anticipated. Against this backdrop, the political unrest in the Middle East/North Africa (MENA) region, which drove up oil prices, and the Tohoku earthquake in Japan, which triggered a breakdown in electronics and automotive supply chains around the world, caused already fragile business and consumer confidence to weaken further. Just as these transitory shocks subsided towards the end of Q2 2011, the global economy was confronted with fresh uncertainties over US fiscal sustainability and sovereign indebtedness in Europe. These new threats weighed on demand, prolonging and exacerbating the negative impact from the supply-side disturbances. Accordingly, economic growth in Singapore’s principal trading partners slowed to 2.7% q-o-q SAAR in Q2 2011 from 5.9% in the previous quarter. The deceleration in Asia was particularly sharp given the region’s geographical proximity and extensive production links with Japan. On a trade-weighted basis, GDP growth in Asia ex-Japan more than halved to 3.7% in Q2, from 8.8% in Q1, as a shortage of critical parts from Japan caused car production to be cut back. Electronics production was affected as well, although by a smaller extent. (Chart 1.1)

Table 1.1 GDP Growth

(%)

2010 2011

Q3 Q4 Q1 Q2 q-o-q SAAR

Total* 3.7 5.0 5.9 2.7 G3* 2.5 0.8 0.5 0.3 US 2.5 2.3 0.4 1.3 Eurozone 1.6 1.1 3.1 0.7 Japan 4.0 −2.4 −3.7 −2.1 Asia ex-Japan* 4.3 7.1 8.8 3.7 Hong Kong 3.5 6.3 12.8 −2.1 Korea 2.6 2.0 5.4 3.6 Taiwan 3.7 1.2 14.6 0.9 Thailand −1.5 5.3 8.1 −0.8 Philippines 0.6 2.0 8.0 2.5

y-o-y Indonesia 5.8 6.9 6.5 6.5 Malaysia 5.3 4.8 4.9 4.0 China 9.6 9.8 9.7 9.5 India 8.9 8.3 7.8 7.7

Source: CEIC, Datastream and EPG, MAS estimates

* Weighted by shares in Singapore’s NODX.

Chart 1.1 Electronics and Automotive Production

in Asia*

Source: CEIC and EPG, MAS estimates

* Average of output levels in Japan, Korea, Malaysia, Taiwan and Thailand.

1 Asia ex-Japan comprises China, Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

2010 Apr Jul Oct 2011 Apr80

90

100

110

120

130

Inde

x (J

an 2

010=

100)

, SA

Automotive Production

Aug

Electronics Production

Macroeconomic Developments 3

Monetary Authority of Singapore Economic Policy Group

US consumption was undermined by a fall in durable goods spending.

In the US, real GDP growth recovered to 1.3% q-o-q SAAR in Q2 2011, after levelling off in the first quarter. (Table 1.1) However, private consumption growth slipped to just 0.7% in the same quarter from 2.1% previously, due to a sharp contraction in durable goods spending. (Chart 1.2) The economy was instead supported by broad-based improvements in investment growth—residential investment and fixed expenditures on structures rose, while equipment and software investment remained firm. In addition, the weak US dollar provided a fillip to exports but this was offset, to some degree, by the moderation in global demand. Apart from higher energy prices, consumption growth was further curtailed by an increase in precautionary savings as households reacted to renewed concerns over the labour market. Non-farm payrolls added only 290,000 workers in the second quarter, compared to 497,000 in the first, as the private sector hired fewer workers, and the public sector continued to shed jobs. Despite slower growth in real disposable incomes, the personal savings rate crept back up to 5.1% in Q2. A lacklustre housing market also weighed on sentiment. Although the overall house price index has stabilised, the dispersion of price changes across the US regions was large and uneven, with increases mostly on the East Coast while property values continued to fall in the Midwest and West Coast. (Chart 1.3)

Growth in the Eurozone and Japan fell in Q2.

The Eurozone economy has fallen to “stall speed”2 as GDP growth tumbled to 0.7% q-o-q SAAR in Q2 2011 from 3.1% in Q1. While the exceptional growth in the first quarter reflected special factors such as the bounce-back in construction activity following a harsh winter, the sharp slowdown in Q2 was due to an abrupt weakening of domestic demand. Notably, private consumption was dragged down by the lagged effects of oil price increases. (Chart 1.4) Moreover, concerns were reignited in April over the debt crisis in Greece on fears that budget slippages could lead to imminent debt restructuring—theconsequences of which could be far-reaching financial

Chart 1.2 US Private Consumption Expenditures

Source: US Bureau of Economic Analysis

Chart 1.3 US House Price Indices by Cities

Source: Case-Shiller (Standard & Poor’s)

* Composite-20 is an aggregate index of the 20 major metropolitan areas in the US listed in the chart.

Chart 1.4 Contribution to Eurozone GDP Growth

Source: Datastream

2 “Stall speed” refers to threshold values of GDP growth below which a recession in the next period is likely.

2010 Q2 Q3 Q4 2011 Q2-10

-5

0

5

10

15

20

-10-10

QO

Q S

AA

R %

Gro

wth

Durable goods Non-durable goods Services

NV-

Las

Vega

sTX

-Dal

las

OR

-Por

tland

OH

-Cle

vela

ndA

Z-Ph

oeni

xM

I-Det

roit

CA

-San

Die

goC

A-L

os A

ngel

esFL

-Tam

paC

A-S

an F

ranc

isD

C-W

ashi

ngto

nC

O-D

enve

rG

A-A

tlant

a

NC

-Cha

rlotte

MA

-Bos

ton

FL-M

iam

iIL

-Chi

cago

NY-

New

Yor

kM

N-M

inne

apol

is

WA

-Sea

ttle

-1.0

-0.5

0.0

0.5

1.0

(Apr

-Jun

201

1)A

vera

ge M

OM

% G

row

th

*Com

posi

te-2

0

2009 Q3 2010 Q3 2011 Q2-15

-10

-5

0

5

QO

Q S

AA

R G

row

th%

Poi

nt C

ontr

ibut

ion

to

Private ConsumptionGovernment ConsumptionGFCF

Net ExportsChange in StocksGDP

4 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

and fiscal contagion across the Eurozone. As a result, retail sales and new car registrations shrank as households, even in the core countries, braced themselves for further belt tightening. At the same time, corporates reduced the pace of investment in the second quarter. Following two quarters of decline, Japan’s real GDP fell again by 2.1% in Q2 on a q-o-q SAAR basis, dragged down by the extensive damage from the earthquake and tsunami. The attendant power shortages caused industrial production and exports to plummet by 14.8% and 18.1% respectively. (Chart 1.5) Not surprisingly, firms held back capital expenditure and consumers became more cautious. Nevertheless, post-quake reconstruction works in the form of public investment spending, which rose by 18.3%, provided some relief.

In Asia ex-Japan, the trade-oriented economies were hit by supply disruptions …

The production stoppages in Japan and anaemic demand from the advanced economies hit GDP growth in the trade-dependent NIE-33 in Q2 2011. However, as anticipated in the April issue of the Review, Taiwan and Korea benefited from the “export substitution” effect arising from overseas customers switching their orders from Japan. (Chart 1.6) These economies have a similar export structure to Japan, in that they ship more consumer and final IT products than components. In contrast, the supply-chain disruptions had a larger impact on the trade of component-producing ASEAN countries such as Thailand and Malaysia, where industrial structures are more complementary to that of Japan. Further, the effects of the common supply shock on growth were aggravated by country-specific factors. In Thailand, negative sentiments arising from uncertainty in the political process weakened consumer spending while implementation delays in infrastructure projects in Malaysia and the Philippines dampened investment.

… while the domestic-oriented economies were relatively resilient.

With the slackening in G3 final demand and a volley of policy tightening measures, China’s economic growth slowed to 9.1% y-o-y in Q3 2011, from 9.5% in Q2 and

Chart 1.5 Japan’s Industrial Production and

Real Exports

Source: CEIC

Chart 1.6 Asian Exports of Final Machinery Goods

Source: World Trade Atlas

Chart 1.7 China’s Money Supply and Loan Growth

Source: CEIC

3 NIE-3 refers to Hong Kong, Korea and Taiwan.

2008 2009 2010 201150

60

70

80

90

100

110

Inde

x (J

an 2

008=

100)

, SA

Real Exports

Aug

Industrial Production

(Mfg)

Mar Apr May Jun2011

80

90

100

110

120

Inde

x (M

ar 2

011=

100)

Malaysia

Taiwan

Korea

Thailand

China

2000 2002 2004 2006 2008 201010

15

20

25

30

35

% Y

OY

(3M

MA

)

Bank Loans

Bank Loans Avg 2000-08 =15.3%

M2

M2 Avg 2000-08 =16.5%

2011Sep

Macroeconomic Developments 5

Monetary Authority of Singapore Economic Policy Group

9.7% in Q1. Concerted moves to rein in excessive credit expansion brought money supply and loan growth back in line with historical norms. (Chart 1.7) Concurrently, industrial production growth moderated to 14.0% y-o-y in Q3 from 14.4% in Q1, amidst rising wages, raw material prices and borrowing costs. However, domestic growth engines, such as fixed investment and retail spending, proved to be resilient. Indonesia expanded at a robust pace of 6.5% in H1 2011, underpinned by strong domestic spending and net exports, which were supported by buoyant commodity prices. (Chart 1.8) Private consumption remained firm, sustained by low interest rates, strong credit growth and higher agricultural earnings. Boosted by public and commodity-based infrastructural expenditures, investment also expanded briskly.

Inflation rose despite softening economic conditions.

In the G3, higher energy prices resulted in headline inflation rising from 1.8% y-o-y in Q1 2011 to 2.5% in Q2. While core inflation increased in the US, it remained relatively subdued in the Eurozone as wage growth was restrained. In Japan, core consumer prices fell by a smaller 0.3% in Q2, following a 0.8% decline in Q1, as deflationary pressures started to dissipate due to energy price increases. (Chart 1.9) Meanwhile, price pressures continued to intensify across Asia ex-Japan, driven largely by higher food and commodity prices, and tight labour markets. Headline CPI inflation in the region rose to 6.1% y-o-y in Q3 2011, from 5.5% in Q1. Nonetheless, there are signs that the upward momentum has slowed and headline rates are starting to stabilise in some countries, particularly Indonesia and Taiwan. Even so, high inflation rates persisted in China and India. (Chart 1.10) The main factor behind the run-up in China has been food price inflation, which exceeded 10% throughout H1 2011 because of weather-related factors and a rise in hog prices. In India, WPI inflation stayed close to double digits during the same period, due partly to higher petroleum prices, increases in the minimum support prices for some agricultural commodities, and strong underlying demand pressures. To curb inflationary pressures, China and India tightened monetary policies several times over the first half of 2011 despite a weakening global outlook.

Chart 1.8 Contribution to Indonesia’s GDP Growth

Source: CEIC

Chart 1.9 G3 Core Inflation

Source: CEIC and Datastream

* Core inflation in Japan only excludes fresh food prices.

Chart 1.10 Asia ex-Japan CPI Inflation*

Source: CEIC and Datastream

* Weighted by 2010 nominal GDP.

** ASEAN-4 refers to Indonesia, Malaysia, the Philippines and Thailand.

2009 Q3 2010 Q3 2011 Q2-5

0

5

10

YOY

Gro

wth

% P

oint

Con

trib

utio

n to

Private ConsumptionGovernment ConsumptionGFCFNet Exports

Change in StocksStatistical DiscrepancyGDP

2009 Jul 2010 Jul 2011-3

-2

-1

0

1

2

3

% Y

OY

Sep

US

Eurozone

Japan*

2007 2008 2009 2010 2011-2

0

2

4

6

8

10

12

% Y

OY

NIE-3

ASEAN-4**

China

India (WPI)

Q3

6 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

1.2 Domestic Economy

Global Headwinds Confronted the Domestic Economy

A series of external shocks buffeted the Singapore economy, weighing on growth.

The domestic economy witnessed significant swings in performance alongside renewed turbulence in the external environment over the last six months. Following the stellar performance at the beginning of the year, GDP contracted on a q-o-q SAAR basis by 6.3% in Q2 2011, a sharp reversal from the 27% expansion in the preceding quarter. (Chart 1.11) The decline was due to a confluence of factors. In mid-March, the calamities in Japan led to supply shortages in cross-border production networks (CPNs) in the region. As a key node of the CPNs, Singapore saw supply-side disruptions in its manufacturing and trade-related activities in the early months of Q2. While production in the region resumed in the latter part of Q2, trade-related services were further hit by sluggish demand in the advanced economies. Higher oil prices, due in part to political unrest in the MENA region, also started to weigh on final demand in Singapore’s key trading partners in Q2. This was compounded by renewed concerns over the sovereign debt situation in the Eurozone. The weakness continued in Q3. Even though the supply-chain disruptions had largely dissipated, the retraction in global demand, alongside the rapid deterioration in global business and consumer confidence, led to a further slowing of domestic economic activity. According to the Advance Estimates, the Singapore economy recorded marginal growth of 1.3% q-o-q SAAR in Q3. Notably, the bulk of the growth support came from pharmaceuticals.4

Chart 1.11 Singapore’s GDP Growth

* Advance Estimates.

4 Pharmaceutical output recorded 33% q-o-q growth in Q3, as firms shifted to a higher value-added product mix during the

quarter.

2008Q3 2009 2010 2011 Q3*-20

-10

0

10

20

30

40

Per C

ent

QOQ SAAR

YOY

Macroeconomic Developments 7

Monetary Authority of Singapore Economic Policy Group

Exhibit A Economic Activity Index

Source: EPG, MAS Estimates

Exhibit A shows EPG’s monthly Economic Activity Index (EAI).5 The EAI reading indicated that output surged at the turn of this year, on a rise in electronics production, and consolidated in the rest of Q1. Following the Japan earthquake in March, the EAI saw a slight dip in April on slower activity, but rebounded subsequently in May. However, the recovery was short-lived and the index contracted over the next few months as a result of renewed weakness in the external environment.

The IT-related activities bore the brunt of the impact …

As Exhibit A shows, the downshift in domestic economic activity was most evident in the trade-related sectors. In the earlier part of Q2, industries such as electronics and chemicals were temporarily affected by the supply-side disruptions in Japan. Growth in these sectors registered sharp double-digit declines in April in the immediate aftermath of the Tohoku quake, but rebounded subsequently in May. (Chart 1.12) However, following the upward blip in May, the IT-related activities saw steep contractions in June, in line with the correction in the global IT industry. (See Chapter 3 for a more detailed discussion of recent developments and prospects for the global IT industry.)

Chart 1.12 Electronics and Petrochemicals Output

5 See the October 2010 issue of the Review for further details on the Economic Activity Index.

Indicators Global Pickup Japan Effect Global Slowdown

EAI ex-PharmaTrade-related IT Non-ITFinancial SvcsTourism

114

116

118

120

122

Inde

x (2

009=

100)

, SA

EAI ex-Pharma

Positive Growth Flat Growth Negative Growth

Global Pickup Japan Effect Global Slowdo

2011Jan Feb Mar Apr May Jun Jul

wn

Aug

Jun Sep Jan Apr Jun

80

90

100

110

120

Inde

x (J

un 2

010=

100)

, SA

Electronics IIP

Petrochemicals IIP

20112010

8 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

The weakness in IT-related activities was broad-based across the IT supply chain, ranging from the upstream precision engineering segment, to midstream components, such as semiconductor chips, and to downstream final products, such as PCs and handsets. (Table 1.2) This had spillover effects on the trade-related services, which fell in Q2 and declined further in July and August. In particular, non-oil re-exports contracted for the third straight month in August, as a result of the deterioration in demand for electronics exports from the US and the Eurozone.

Table 1.2 The Domestic IT Supply Chain

Source: EPG, MAS estimates

… in part due to our larger exposure to component manufacturing.

Singapore’s electronics production fell by a sharp 30% over the last two quarters. This was partly due to the domestic product mix. Singapore’s IT sector is concentrated in component manufacturing, which accounts for a hefty 70% of total electronics output, compared to an average of 44% for the region. In general, the global component manufacturing segment tends to be more sensitive to changes in final demand. During the 2009 recession, for instance, global GDP contracted by 3.4% from its pre-crisis peak over three quarters, while final IT demand suffered a larger 6.7% drop over the same period.6 (Chart 1.13) The latter, in turn, had a magnified impact on the semiconductor segment, which saw global chip sales plunge by 29% from its peak in Q3 2008. Inventoryeffects would also have been at work here. During the global recession, inventory destocking did not occur evenly throughout the supply chain. The brunt of

Chart 1.13 Global GDP and IT Demand during the 2009

Global Recession

Source: EPG, MAS estimates

* Global GDP cyclical peak.

6 Final IT demand is proxied by indicators of final IT demand in the US and China.

SectorsManufacturing

(Non-electronics)Manufacturing (Electronics) Wholesale Air Cargo

Products/ Activities

Precision Engineering

Components Final ProductsProcurement,

Testing & Warehousing

Distribution

Jan-Mar

Apr-May

Jun-Aug

Flat Growth Negative GrowthPositive Growth

P-3 P-2 P-1 Peak* P+1 P+2 P+3 P+4 P+570

80

90

100

110

Inde

x (Q

3 20

08=1

00),

SA

Final IT Demand

Global GDP

Global Chip Sales

Macroeconomic Developments 9

the impact fell on the midstream component makers, who experienced the sharpest cutback in production and inventory drawdown. Thus, the recent global semiconductor inventory overhang has led to a disproportionate impact on markets such as Singapore. By the same token, Singapore should see a stronger rebound in electronics output when the inventory adjustment runs its course and final demand picks up again.

There was also some pullback in activity in the financial services sector.

Besides trade-related activities, there were also some retractions in asset market-related activities. In particular, the financial services sector recorded a mild contraction of 0.2% q-o-q SAAR in Q2, following the 28% expansion in the preceding quarter. (Chart 1.14) Debt-related problems in Europe and the US caused jitters for investors worldwide. This also affected average daily turnover volumes in the domestic stock market, which declined by 24% q-o-q. In addition, insurance activity fell as demand across a number of product lines weakened. Sentiment-sensitive activities in the financial services sector saw a further contraction in Q3 as volatility in global financial markets escalated. Regional equity funds experienced a sharp outflow of US$7.1 billion in August after two months of inflows, as fund managers turned defensive and increased cash holdings. (Chart 1.15) Similarly, domestic equity funds, which track global developments closely, have witnessed consecutive months of outflows since May. Mirroring the 22% fall in the MSCI Asia ex-Japan Index, the local bourse saw a corresponding sell-off, with the STI plunging 14% in Q3, marking its largest decline since Lehman Brothers’ collapse in September 2008. While average daily turnover volumes spiked in August on panic selling, they fell 30% m-o-m in September. (Chart 1.16) Amidst heightened risk aversion, companies in Singapore and the region held back on their fund-raising plans. IPO issuance in Singapore to amounted only $150 million in Q3, compared to the $1.4 billion raised in Q2. In Asia, funds raised through equity markets halved to US$14 billion, fromUS$28 billion in the preceding quarter. Lacklustre fund-raising activities, in turn, translated into lower

Chart 1.14 Contribution to Financial Services GDP

Growth

Source: EPG, MAS estimates

Chart 1.15 Fund Flows and Cash Holdings

Source: EPFR Global

Chart 1.16 Stock Market Average Daily Turnover and

Straits Times Index (STI)

Source: SGX

2010 Q2 Q3 Q4 2011 Q2-20

-10

0

10

20

30

40

QO

Q S

AA

R G

row

th%

Poi

nt C

ontr

ibut

ion

to

InsuranceFinancial IntermediationBrokerage & TreasuryAsset Management

Private Banking Others

Financial Services GDP

Jan Feb Mar Apr May Jun Jul Aug2011

-8

-4

0

4

US$

Bill

ion

1.0

1.5

2.0

2.5

% o

f Ass

ets

Man

aged

Asia ex-Japan Equity Funds (LHS)Cash Holdings (RHS)

2010 May Sep 2011 May Sep0.0

0.5

1.0

1.5

2.0

2.5

Bill

ion

2640

2760

2880

3000

3120

3240

Inde

x

Volume, Units (LHS) STI (RHS)

Monetary Authority of Singapore Economic Policy Group

10 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

fees and commissions for domestic financial institutions, with underwriting income falling by a steep 87% q-o-q in Q3, according to data from Bloomberg. In comparison, financial intermediation remained resilient. Domestic non-bank lending continued to expand, recording its ninth sequential quarter of gains in Q2. In particular, business lending growth accelerated to its fastest on record at 12.0% q-o-q, supported by a steady pipeline of loans extended to all sectors. Loan volumes continued to expand in August, albeit at a slower pace of 6.9%. (Chart 1.17) Likewise, offshore lending activities remained firm in Q2 despite a pullback in lending to Europe, supported by demand from Asia and the Americas. However, the continued deterioration in the advanced economies in Q3 took a toll on business confidence. August data showed that loans extended to the Americas contracted by 4.0%, marking the sharpest sequential decline since September 2010. (Chart 1.18)

Domestic-oriented sectors showed signs of softening.

Aided by a firm labour market, the domestic-oriented sectors continued to post steady growth in H1 2011. Excluding motor vehicles, retail sales accelerated further from 1.9% q-o-q SA in Q1 to 2.3% in Q2 on the back of higher merchandise sales. In particular, discretionary expenditure items, such as electronic peripherals, watches and jewellery recorded stronger sales during the quarter. However, growth in non-vehicle retail sales slowed in Q3, declining by 4.6% m-o-m SA in August after rising by 0.9% in the previous two months, reflecting less buoyant consumer sentiment.

Tourist arrivals strengthened despite the global economic turbulence.

The tourism industry was the star performer over the

last six months. Overall visitor arrivals increased 4.9% q-o-q SA in Q2 after rising 5.6% in Q1. Monthly arrivals in July and August remained above 1.14 million visitors on average, even higher than the record levels achieved in Q2. (Chart 1.19) Alongside stable gains from ASEAN, tourists from North Asian markets such as Hong Kong and Taiwan surged. Consequently, hotel occupancy rose to 88% in Q2 and hovered around 86% in July and August, even as

Chart 1.17 Contribution to DBU Business Lending

Chart 1.18 ACU Non-Bank Lending by Region

Chart 1.19 Average Monthly Visitor Arrivals and Hotel

Occupancy

Source: EPG, MAS estimates

2010 Q2 Q3 Q4 2011 Q2 Aug-5

0

5

10

15

% P

oint

Con

trib

utio

n to

QO

Q G

row

th

Trade-relatedBuilding & Construction

Non-bank FIsOthers

Jan Feb Mar Apr May Jun Jul Aug2011

-8

-4

0

4

8M

OM

% G

row

th

East Asia

The Americas

Europe

Overall

2009Q3 2010 Q3 2011

0.6

0.8

1.0

1.2

Mill

ion,

SA

60

70

80

90

%, S

A

Visitor Arrivals (LHS) Occupancy Rate (RHS)

Jul-Aug

Macroeconomic Developments 11

Monetary Authority of Singapore Economic Policy Group

average room rates continued to trend upwards. With corporate demand staying firm, hoteliers continued to report gains in revenues. The resilience shown in the tourism-related industry in recent months underscores its revival in recent years. MTI has estimated that tourism value-added as a share of nominal GDP grew from 3.0% in 2008 to 3.5% in 2010.7 Aside from the decline during the 2009 Global Financial Crisis, visitor inflows have increased steadily over this period, buoyed by regional tourist arrivals. Visitor arrivals from the G3, meanwhile, remained steady, averaging about 2.2 million per annum over the same period.

Shift-share analysis points to the “external effect” as the primary driver of the surge in

Singapore’s visitor arrivals.

To better understand the trend of growing tourism demand, and benchmark Singapore’s performance against regional tourist destinations such as Hong Kong, Malaysia and Thailand, EPG adopted a variant of the shift-share methodology to decompose the growth of visitor arrivals into three factors: the external effect, the competitive effect and the market-mix effect. Singapore’s visitor arrivals grew by an average of 5.1% over the last decade and hit a record high growth of 20.2% in 2010, excluding the rebound in 2004 after the SARS epidemic. (Chart 1.20) The bulk of the growth last year can be attributed to the external effect, reflecting the attractiveness of the region as a tourist destination.8 In fact, the external effect accounted for more than two-thirds of the 20.2% growth in visitor arrivals last year, higher than its average contribution of 10.2% over the decade. Further disaggregation suggests that this was due to intra-Asian travel which, in turn, was facilitated by the proliferation of budget airlines in the region. (Chart 1.21) The competitive effect, which isolates the growth differential in visitor arrivals into Singapore relative to other economies turned positive in 2010 following a decade of weakness. (Chart 1.20) This coincided with a

Chart 1.20 Decomposition of Singapore’s Growth

in Visitor Arrivals

Source: EPG, MAS estimates

Chart 1.21 Decomposition of the External Effect

Source: EPG, MAS estimates

7 Ministry of Trade and Industry (2010), “The Contribution of Tourism to the Singapore Economy”, Economic Survey of

Singapore. 8 The external effect captures the growth of Singapore’s visitor arrivals arising from developments in the external

environment common to Singapore and regional economies including Hong Kong, Malaysia and Thailand.

2000 2002 2004 2006 2008 2010-20

-10

0

10

20

30

40

% P

oint

Con

trib

utio

n to

Gro

wth

External Effect Competitive Effect Market-Mix Effect

1997 1999 2001 2003 2005 20070

20

40

60

80

100

Per C

ent

OthersG3

Rest of AsiaIndia

ChinaASEAN

2010

12 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

series of supply-side expansions to enhance Singapore’stourism infrastructure vis-à-vis the rest of the region, including the opening of the Integrated Resorts in 2010. Notably, Singapore topped the region for its quality of tourism and travel infrastructure in the recent World Economic Forum’s Travel & Tourism Competitiveness Index 2011. The market-mix effect highlights Singapore’s ability to attract tourists from high growth markets. As indicated in Chart 1.20, Singapore had seen a negative market-mix effect last year, due to its reliance on visitor inflows from the ASEAN region, which grew at a slower rate compared to the other emerging markets, such as China and India. (Table 1.3 and Chart 1.22) In comparison, Hong Kong saw positive market-mix effects in 2010 as it has a higher share of mainland tourists.

Table 1.3 Share of Visitor Arrivals from Key Source Markets in 2010

(%)

Source Markets

China India ASEAN

Hong Kong 63 1 1 Malaysia 4 3 77 Singapore 10 7 41 Thailand 7 5 28

Source: EPG, MAS estimates

Chart 1.22 Growth in Tourist Inflows into the Region*

by Source Markets in 2010

Source: EPG, MAS estimates

* The region comprises Hong Kong, Malaysia, Singapore and Thailand.

5

10

15

20

25

30

% Y

OY

China India Rest of Asia

Others ASEAN G3 Total

Macroeconomic Developments 13

Monetary Authority of Singapore Economic Policy Group

The immediate outlook is clouded by significant uncertainties.

Amidst the adverse external environment in recent months, the Singapore economy has seen a sharper downshift in activity compared to the rest of the region. (Chart 1.23) This might be explained by Singapore’s stronger dependence on external trade, extensive global financial linkages, and larger exposure to the more volatile electronics and biomedical manufacturing industries. (Table 1.4) Larger swings in growth numbers are thus not entirely unexpected, especially during periods of global economic and financial stress. Nevertheless, higher volatility has not translated into lower average growth rates for Singapore relative to the rest of the region, as shown in Table 1.5. The immediate outlook is thus characterised by a high degree of uncertainty. In particular, developments in the US and the Eurozone will be critical to Singapore’s economic prospects over the next few quarters. This will be further discussed in Chapter 3.

Chart 1.23 Regional GDP Growth in Q2 2011

Source: CEIC

Table 1.4 Singapore’s Global Exposures Compared to

the Region* in 2010 (% of GDP)

Singapore Regional Average

Total Exports 180 60 Electronics Exports 80 20 Offshore Lending 380 70

Source: BIS, CEIC

* The region comprises China, Hong Kong, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

Table 1.5 Annual GDP Growth (2000s)

Average Rate

(%)

Standard Deviation (% point)

China 10.5 1.8 India 7.6 1.9 Singapore 5.7 5.0 Indonesia 5.2 0.9 Philippines 4.8 1.9 Malaysia 4.7 2.9 Thailand 4.4 3.0 Korea 4.2 2.0 Hong Kong 4.1 3.6 Taiwan 3.9 3.9

Source: CEIC

Singapore

Hong Kong

Thailan

d

Taiwan

Philippines

Korea-8

-6

-4

-2

0

2

4

0

% Q

OQ

SA

AR

14 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

1.3 Macroeconomic Policy

Macroeconomic policy in Singapore plays a countercyclical role, while maintaining

a medium-term orientation.

The Singapore economy emerged from recession in Q2 2009, and by Q1 2010, it had recouped all the output lost during the Global Financial Crisis. Price pressures began to build up as resource markets tightened. Given the robust recovery, the authorities began in early 2010 to withdraw the monetary and fiscal stimulus that had been put in place during the crisis. Monetary policy decisions were deliberately calibrated, with the exchange rate providing the effective macroeconomic restraint in order to ensure price stability over the medium term. In April 2010, MAS tightened monetary policy by re-centring the S$NEER policy band upwards and restoring its modest and gradual appreciation path. Monetary policy was tightened further in October via a slightly steeper appreciation of the policy band. The band was also widened slightly to accommodate volatility in international financial markets. Meanwhile, fiscal policy shifted away from the recession relief measures in the FY2009 Budget to more medium term-oriented and productivity-enhancing initiatives. The monetary and fiscal policy stance is proxied by the Domestic Liquidity Indicator (DLI) and the Fiscal Impulse (FI) measure, respectively. 9 Chart 1.24 plots these measures against the output gap. A positive output gap signals that output is above potential, leading to inflationary pressures as the economy faces bottlenecks in meeting demand. Conversely, a negative output gap indicates that the economy is producing below capacity, resulting in the easing of cost and price pressures. Points above the horizontal axis denote a positive output gap and an expansionary policy stance, and vice versa for points below the axis. Movements in the DLI or the FI in the opposite direction to the output gap indicate that macroeconomic policy is countercyclical. It is evident from the chart that the macroeconomic policy stance in Singapore tightened during periods of robust growth, such as recently.

Chart 1.24 DLI, FI and Output Gap

Source: EPG, MAS estimates

9 The DLI reflects changes in the S$NEER and three-month domestic interbank rate. For more details on the methodology

used to calculate the FI measure, see the January 2002 issue of the Review.

1990 1994 1998 2002 2006 2010-4

-2

0

2

4

6

-4

-2

0

2

4

6

% o

f GD

P

Contractionary

% o

f Pot

entia

l GD

P

-1.5

-1.0

-0.5

0.0

0.5

1.0 -4

-2

0

2

4

6

Cha

nge

over

Pre

viou

s Ye

ar Expansionary

% o

f Pot

entia

l GD

P

Contractionary

Expansionary

FI Measure (LHS) Output Gap (RHS)DLI (LHS)

Macroeconomic Developments 15

Monetary Authority of Singapore Economic Policy Group

Monetary Policy

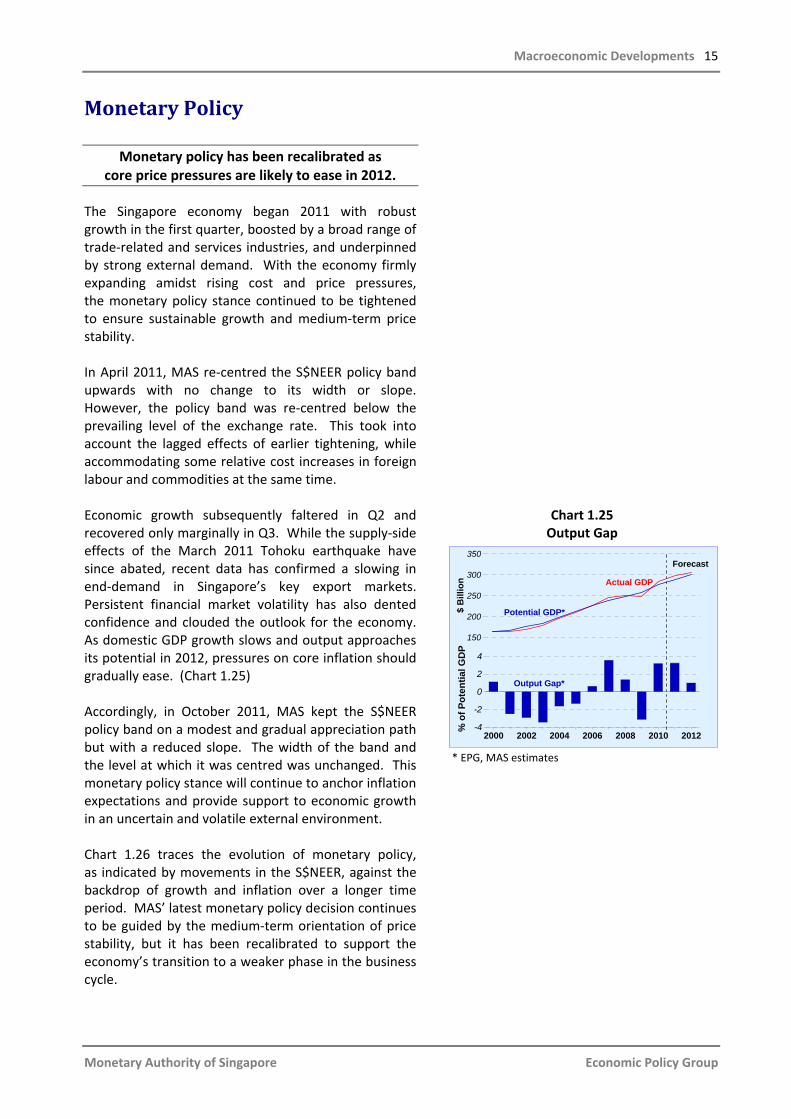

Monetary policy has been recalibrated as core price pressures are likely to ease in 2012.

The Singapore economy began 2011 with robust growth in the first quarter, boosted by a broad range of trade-related and services industries, and underpinned by strong external demand. With the economy firmly expanding amidst rising cost and price pressures, the monetary policy stance continued to be tightened to ensure sustainable growth and medium-term price stability. In April 2011, MAS re-centred the S$NEER policy band upwards with no change to its width or slope. However, the policy band was re-centred below the prevailing level of the exchange rate. This took into account the lagged effects of earlier tightening, while accommodating some relative cost increases in foreign labour and commodities at the same time. Economic growth subsequently faltered in Q2 and recovered only marginally in Q3. While the supply-side effects of the March 2011 Tohoku earthquake have since abated, recent data has confirmed a slowing in end-demand in Singapore’s key export markets. Persistent financial market volatility has also dented confidence and clouded the outlook for the economy. As domestic GDP growth slows and output approaches its potential in 2012, pressures on core inflation should gradually ease. (Chart 1.25) Accordingly, in October 2011, MAS kept the S$NEER policy band on a modest and gradual appreciation path but with a reduced slope. The width of the band and the level at which it was centred was unchanged. This monetary policy stance will continue to anchor inflation expectations and provide support to economic growth in an uncertain and volatile external environment. Chart 1.26 traces the evolution of monetary policy, as indicated by movements in the S$NEER, against the backdrop of growth and inflation over a longer time period. MAS’ latest monetary policy decision continues to be guided by the medium-term orientation of price stability, but it has been recalibrated to support the economy’s transition to a weaker phase in the business cycle.

Chart 1.25 Output Gap

* EPG, MAS estimates

* EPD, internal estimates.2000 2002 2004 2006 2008 2010 2012-4

-2

0

2

4

% o

f Pot

entia

l GD

P 150

200

250

300

350

$ B

illio

n

Potential GDP*

Output Gap*

Actual GDP

Forecast

16 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

Chart 1.26 Key Macroeconomic Variables and Changes in the Monetary Policy Stance

-10

-5

0

5

10

15

20

2004 2005 2006 2007 2008 2009 2010 2011

% Y

OY

Real GDP Growth

-2

0

2

4

6

8

10

% Y

OY

CPI Inflation

IncreaseSlope Slightly Re-

centreRe-

centre

Q3

Reduce Slope

90

95

100

105

110

115

120

125

Inde

x (Q

1 20

04=1

00)

S$NEER

Increase Slope Slightly & Widen

Band Slightly

Modest & Gradual Appreciation

Modest & Gradual AppreciationNeutral

Policy

Maintain

Re-centre

Macroeconomic Developments 17

Monetary Authority of Singapore Economic Policy Group

The S$NEER fluctuated in the upper half of the policy band until mid-September.

Following the April 2011 policy review, the S$NEER mostly fluctuated in the upper half of the exchange rate policy band. (Chart 1.27) Regional currencies appreciated against the US$ between April and August, as Asia, including Singapore, experienced sustained inflows of global liquidity. The S$NEER reached a peak in early September. From mid-September, however, fears of a sovereign debt default in the peripheral Eurozone countries escalated. With risk aversion on the rise, the S$NEER weakened from the upper half of the policy band to the lower half.

The S$REER has strengthened and exceeded its previous peak in the late 1990s.

The Singapore dollar real effective exchange rate (S$REER) is a measure of the S$NEER adjusted for price and cost differentials between Singapore and its trading partners. Using the CPI as the price deflator, the S$REER is estimated to have risen by 3.5% on a sequential basis in H1 2011. (Chart 1.28) This was primarily due to a strengthening of the nominal exchange rate. Nonetheless, relative CPI also contributed to the S$REER appreciation, as domestic consumer prices rose more rapidly than the foreign CPI this year. Moreover, some of the domestic price adjustments were due to the effects of permanent price shifts reflecting higher resource costs. As of Q2 2011, the S$REER was nearly 9% higher than in Q1 2010, before the MAS embarked on the monetary policy tightening cycle. It had also surpassed its historical peak in Q1 1998 by about 2.9%.

Liquidity conditions continued to tighten until August.

From April to August 2011, the DLI was positive, as overall liquidity conditions tightened alongside the modest and gradual appreciation of the S$NEER. (Chart 1.29) Changes in the DLI were almost entirely driven by the exchange rate component over this period, as the three-month domestic interbank rate was quite stable at about 0.44% but fell to 0.31% in August. (Chart 1.30) As at end-September, the interbank rate declined further to 0.25%, while the

Chart 1.27 S$NEER

Chart 1.28

S$NEER, S$REER and Relative CPI

* EPG, MAS estimates.

Chart 1.29 Domestic Liquidity Indicator

* EPG, MAS estimates.

Jan Jan Jan Jan Jan

95

100

105

110

115

120

Inde

x (5

Jan

200

7=10

0)

Appreciation

Depreciation

200920082007 2010Oct

2011

1985 1991 1997 2003 2011

60

80

100

120

140

160

80

Inde

x (Q

1 19

85=1

00)

S$REER*

S$NEER

Relative CPI*

Appreciation

Depreciation

Q2

Apr Jul Oct Jan Apr Jul

-0.4

-0.2

0.0

0.2

0.4

0.6

Cha

nge

from

Pre

viou

s Q

uart

er Tightening

Easing

Sep2010

Exchange Rate Changes

InterestRate Changes

DLI*

2011

18 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

S$NEER depreciated sharply. 10 As a result, overall liquidity conditions in the short term eased for the first time since the MAS embarked on the monetary policy tightening cycle in April 2010. Meanwhile, the three-month US$ SIBOR rose from 0.25% in June to 0.37% by end-September. Renewed concerns about financial market stresses in Europe and the US, as well as weaker global growth prospects, led to a shortage of US$ liquidity and higher US$ borrowing costs across international financial markets. As the domestic interbank rate has been falling, the US$-S$ interest rate differential, which has been negative since May 2009, turned positive from late August 2011 to the start of October. In the first week of October, the 3-month domestic interbank rate rose back to 0.44%, given expectations of a looser monetary policy stance in the October policy review. Since US$ interest rates have risen by less, the differential became negative once again. Movements in the 3-month S$ swap offered rate (SOR), which represents the cost of borrowing S$ via a swap out of US$, were similar. The SOR trended down and turned negative in August, reaching a low of −0.70% as expectations of a US$ depreciation against the S$ intensified. When these pressures abated in September, the SOR returned to positive territory and ended the month at 0.19%.

Credit growth picked up in line with low interest rates and sustained economic activity.

The negative SOR rate prompted banks to cease loans pegged to SOR, or introduce new clauses to set a floor for the interest rate. With overall interest rates remaining very low, and given the high levels of activity in the Singapore economy, domestic credit to the private sector continued to expand. (Chart 1.31) Business loan growth was especially robust, and by August, the stock of outstanding loans had risen 39% y-o-y. Loans to a wide range of industries rose, supporting the broad-based expansion in economic activity. Consumer credit growth also remained high at 19% y-o-y in August, as a steady pipeline of housing and other loans this year offset declines in car and share financing loans.

Chart 1.30 Interest and Swap Rates

Chart 1.31 Domestic Credit to the Private Sector

10 As a result of Singapore’s open capital account and the exchange rate-centred monetary policy framework, domestic

interest rates are endogenous, and MAS’ money market operations (MMOs) are not targeted at a specific interest rate level. Instead, MMOs are conducted to ensure there is sufficient liquidity in the banking system to meet banks’ demand for reserve and settlement balances. Box A provides a review of MAS’ MMOs in FY2010/11.

2009 Jul 2010 Jul 2011End of Month

0.00

0.25

0.50

0.75

1.00

1.25

1.50

0.00

% P

er A

nnum

3-month S$ SwapOffered Rate

3-month Domestic Interbank Rate

Sep

3-month US$ SIBOR

2006 2007 2008 2009 2010 2011-10

0

10

20

30

40

YOY

% G

row

th

Domestic Credit to Private Sector

Aug

ConsumerLoans

Business Loans

Macroeconomic Developments 19

Monetary Authority of Singapore Economic Policy Group

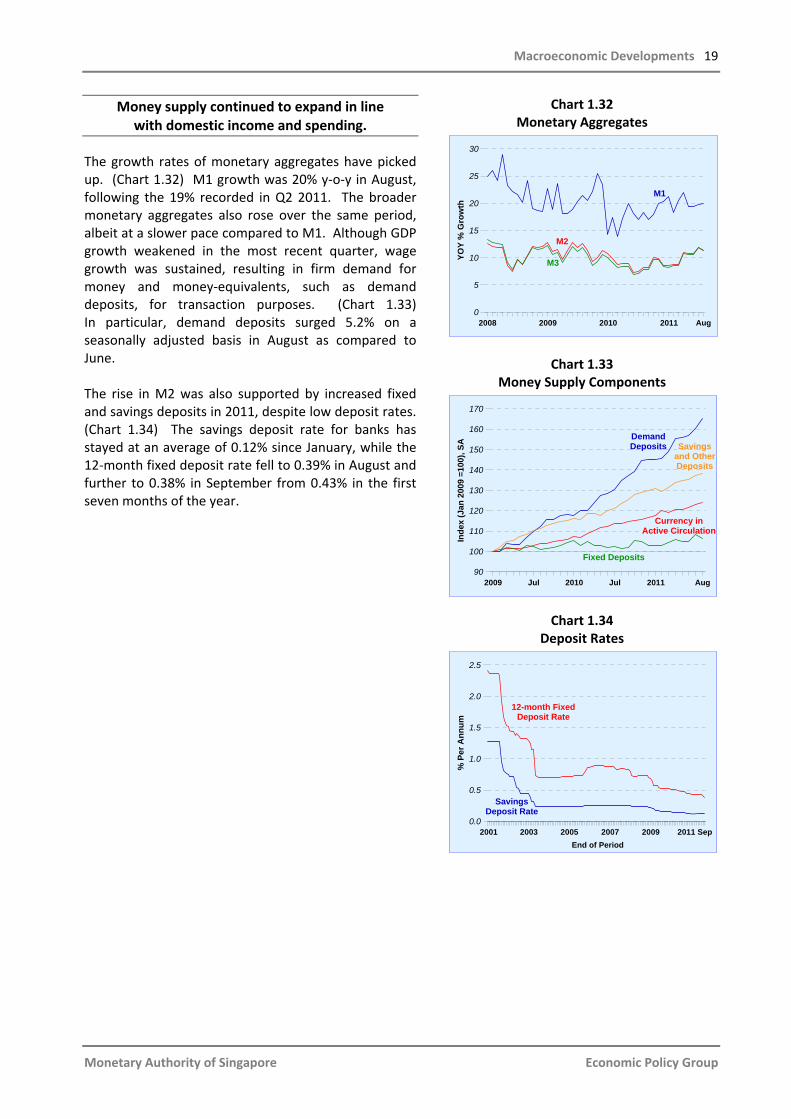

Money supply continued to expand in line with domestic income and spending.

The growth rates of monetary aggregates have picked up. (Chart 1.32) M1 growth was 20% y-o-y in August, following the 19% recorded in Q2 2011. The broader monetary aggregates also rose over the same period, albeit at a slower pace compared to M1. Although GDP growth weakened in the most recent quarter, wage growth was sustained, resulting in firm demand for money and money-equivalents, such as demand deposits, for transaction purposes. (Chart 1.33) In particular, demand deposits surged 5.2% on a seasonally adjusted basis in August as compared to June. The rise in M2 was also supported by increased fixed and savings deposits in 2011, despite low deposit rates. (Chart 1.34) The savings deposit rate for banks has stayed at an average of 0.12% since January, while the 12-month fixed deposit rate fell to 0.39% in August and further to 0.38% in September from 0.43% in the first seven months of the year.

Chart 1.32 Monetary Aggregates

Chart 1.33

Money Supply Components

Chart 1.34

Deposit Rates

2008 2009 2010 2011

0

5

10

15

20

25

30

YOY

% G

row

th

M1

M3

Aug

M2

2009 Jul 2010 Jul 2011

90

100

110

120

130

140

150

160

170

Inde

x (J

an 2

009

=100

), SA

Demand Deposits

Fixed Deposits

Aug

Savingsand OtherDeposits

Currency in Active Circulation

2001 2003 2005 2007 2009 2011 Sep End of Period

0.0

0.5

1.0

1.5

2.0

2.5

% P

er A

nnum

12-month Fixed Deposit Rate

Savings Deposit Rate

20 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

Fiscal Policy

Government operating revenue increased in the first half of 2011 in line with robust economic growth.

Given strong economic growth in 2010 and early this year, the government’s operating revenue increased from $22.3 billion (15.0% of GDP) in H1 2010 to $25.5 billion (15.8% of GDP) in the first half of 2011. Income tax, GST, property-related taxes, as well as fees & charges were the main contributors to this increase. (Chart 1.35) In H1 2011, the government collected $10.5 billion from income taxes, the largest component of operating revenue, $1.1 billion more than in the same period last year. The bulk of the increase was from corporate taxes, notwithstanding the 20% corporate income tax rebate for YA2011. GST, the second largest contributor, also increased by $0.7 billion from a year ago to $4.5 billion in H1 2011. Among the other revenue components, property tax and stamp duty collections rose by $0.5 billion and $0.2 billion, respectively, in H1 2011 due to the increased valuation of private housing amidst a buoyant property market. In particular, with the shift towards a progressive property tax regime from January 2011, all HDB flat owners and a large majority of private property owners would have paid lower property taxes, while only a minority staying in high-end private property paid more.11 The bulk of the increase in non-tax revenue, i.e. fees & charges, was due to receipts from Certificates of Entitlement (COEs). While new car registrations tumbled by about 36% in H1 2011 compared to a year ago, COE premiums for cars surged 79%. (Chart 1.36)

Chart 1.35 Components of Operating Revenue

Chart 1.36 COE Premiums and New Car Registrations

11 Under the progressive property tax system for owner-occupied residential properties, the first $6,000 of Annual Values

(AV) of a property is exempted from tax. The next tier is taxed at 4%, and the balance of AV in excess of $65,000 at 6%. The property tax structure of non-owner occupied residential properties and other properties remains at a flat rate of 10% of AV.

Income Taxes

GST

Fees & Charges

Assets Taxes

Stamp Duties

Betting Taxes

Motor Vehicle Taxes

0 4 8 12$ Billion

2010 H1 2011 H1

Customs & Excise Duties

2007 2008 2009 2010 20110

2

4

6

8

10

12

Thou

sand

0

12

24

36

48

60

72

0

$ Th

ousa

nd

Average COE Premiums for

Cars (RHS)

Sep

New Car Registrations

(LHS)

Macroeconomic Developments 21

Monetary Authority of Singapore Economic Policy Group

Operating and development expenditure also rose, but by less than revenue.

Overall government spending rose by $2.0 billion to $24.4 billion (15.1% of GDP) in H1 2011, largely driven by the increase in operating expenditure which accounts for about 75% of total government expenditure. These include expenses on manpower, equipment and supplies, as well as operating grants to statutory boards and aided educational institutions to support their day-to-day operations. Operating expenses were $1.7 billion higher at $18.4 billion (11.4% of GDP), with increases recorded across nearly all ministries. In particular, the Ministryof Education recorded the largest expansion on the back of increased funding to institutions of higher-learning. (Chart 1.37) The Ministry of Health also saw a rise in operating spending stemming from the new initiatives in integrated care, as well as manpower recruitment, retention, and training. Meanwhile, the government spent $6.0 billion (3.7% of GDP) on development items in H1 2011, $0.3 billion more than in the first half of 2010. The bulk of the increase was incurred by the Ministry of National Development to fund home upgrading programmes. (Chart 1.38) In contrast, development expenditure in the healthcare sector fell, given the lull in the construction of new medical facilities. After the completion of the Khoo Teck Puat Hospital last year, spending on major construction projects, such as the Jurong General Hospital, will only ramp up in 2012.

The basic balance remained negative.

Overall, the government recorded a primary surplus of $1.1 billion in H1 2011, compared to a small $55 million deficit recorded in the same period a year ago.12 The basic balance similarly improved by about $1.1 billion, to record a smaller deficit of $1.3 billion.13 (Chart 1.39) While the amount of special transfers disbursed in the first half of this year was almost twice that in H1 2010, the bulk comprised contributions to endowment and trust funds, such as the Singapore

Chart 1.37 Selected Components of Operating Expenditure

Chart 1.38 Selected Components of

Development Expenditure

Chart 1.39 Basic Balance

12 The primary surplus/deficit is defined as operating revenue (excluding net investment income/returns contribution) less

the sum of operating and development expenditure. 13 The basic balance is the primary balance plus special transfers but excluding top-ups to endowment and trust funds.

Education

Health

0 2 4 6$ Billion

8

2010 H1 2011 H1

Security & External Relations

Community Development

NationalDevelopment

Transport

Trade & Industry

Education

Health

0.0 0.5 1.0 1.5 2.0$ Billion

2010 H1 2011 H1

National Development

2000 2002 2004 2006 2008

-10

-5

0

5

10

$ B

illio

n

2011H1

22 Macroeconomic Review, October 2011

Monetary Authority of Singapore Economic Policy Group

Universities Trust Fund14, National Productivity Fund and Eldercare Fund, which have no impact on the basic balance.

The fiscal stance is expected to be mildly contractionary in 2011.

In the FY2011 Budget, the government focused on supply-side measures to generate sustainable and inclusive growth over the longer term. In line with the shift of the economy towards productivity-driven growth, it contained measures to spur the upgrading of the workforce, such as the expansion of the Continuing Education and Training Scheme and top-up to the Lifelong Learning Endowment Fund. Schemes to encourage companies to increase productivity were also enhanced, including higher levies on foreign labour, bigger payouts of Productivity and Innovation Credit, and top-ups to the National Productivity Fund. At the same time, the budget provided substantial support to the economically vulnerable (such as lower-income workers and the elderly) through various long-term programmes. It also included short-term relief measures to help households and businesses cope with rising costs. The FI measure, which provides a useful indication of the initial stimulus to aggregate demand arising from fiscal policy, is forecast to be −1.5% of GDP for CY2011. (Chart 1.40) This indicates a mildly contractionary fiscal policy stance compared to the previous year. It is also slightly more contractionary than the earlier estimate (−0.2%), largely reflecting the higher revenue outturn in H1 2011.

Chart 1.40 Fiscal Impulse Measure

Source: EPG, MAS estimates

14 The Singapore Universities Trust Fund was announced at the National Day Rally in August 2010. The government injected

$2 billion into this Fund in March 2011, and matches three-to-one for new donations to the Fund, and 1.5-to-one for existing programmes.

1990 1996 2002 2008-4

-2

0

2

4

% o

f GD

P

-4

-2

0

2

4

% o

f Pot

entia

l GD

P

Fiscal Impulse Measure (LHS)

2011F

OutputGap (RHS)

Macroeconomic Developments 23

Box A Review of MAS Money Market Operations in FY2010/111/

This box reviews the conduct of MAS’ Money Market Operations (MMOs) in FY2010/11. MAS’ MMOs are undertaken to manage liquidity within the banking system and are distinct from the implementation of exchange rate policy, as explained in the monograph on “Monetary Policy Operations in Singapore” published in April 2007. A brief description of how MMOs are conducted is first provided, followed by a review of banks’ demand for cash balances with MAS, the behaviour of autonomous money market factors in FY2010/11, and an examination of the MMOs conducted during this period. A short introduction to MAS Bills, a new MMO instrument introduced in April 2011 after FY2010/11, completes this box. MMOs in Singapore MAS’ MMOs are aimed at ensuring that there is sufficient liquidity in the banking system to meet banks’ demand for reserve and settlement balances, and are not targeted at any level of interest rate or money supply. This is consistent with the principle underlying the open economy trilemma, i.e. domestic interest rates and the money supply are endogenously determined as a result of Singapore’s open capital account and exchange rate-centred monetary policy. MMOs are conducted daily by the Monetary & Domestic Markets Management Department at MAS. The amount of liquidity in the banking system is estimated by taking into consideration the banking sector’s demand for funds and the net liquidity impact of autonomous money market factors. Money market transactions are then carried out, with market and liquidity conditions monitored throughout the day. Banks’ Demand for Cash Balances Banks hold cash balances with MAS to meet reserve requirements and for settlement purposes. Banks in Singapore are required to maintain with MAS a Minimum Cash Balance (MCB) equivalent to 3% of their liabilities base on a two-week average basis. This forms a base demand for cash balances, which MAS takes into account when conducting MMOs. The demand for reserve balances could, however, vary across periods as banks may use their reserve balances to fulfil other regulatory (e.g. liquid asset) requirements. In FY2010/11, banks’ demand for balances to meet reserve requirements grew as a result of the increase in their liabilities base. (Chart A1) The increase in liabilities base, in turn, reflected the continued rise in bank intermediation activity owing to the robust economic growth in Singapore and across Asia.

Chart A1 Average Reserve Requirements over a Two-week Maintenance Period

Mar Jul Sep Nov Jan Mar

Two-week Maintenance Period Beginning

11.5

12.0

12.5

13.0

13.5

S$ B

illio

n

2010 2011May

____________________________________________________________________

1/ This box is contributed by the Monetary & Domestic Markets Management Department at MAS.

Monetary Authority of Singapore Economic Policy Group

24 Macroeconomic Review, October 2011

MAS also takes into account banks’ demand for settlement balances when planning MMOs, apart from meeting banks’ demand for reserve balances. Since the financial crisis, there has been a tendency for banks to hold slightly more liquidity in the form of central bank reserves compared to the pre-crisis period. Patterns in Banks’ Daily Demand for Cash Balances with MAS Although banks are required to keep an average MCB ratio of 3% over the two-week maintenance period, their daily effective MCB ratios can fluctuate between 2% and 4% of their liability base, giving them more flexibility in their liquidity management. As such, there may be day-to-day variations in banks’ demand for cash balances with MAS within each maintenance period. Chart A2 illustrates the daily fluctuations in cash balances within an average maintenance period in FY2010/11. As the chart suggests, banks typically maintain higher cash balances during the start of a maintenance period so as to avoid being caught short of cash towards the end of the period. The daily cash balances required by the banking system during the last few days of a typical maintenance period are, therefore, lower in general. In addition, banks also tend to keep higher cash balances on Fridays (Days 2 and 9 in Chart A2), on the eve of public holidays, around festive seasons, and towards the end of a month or quarter, to cover their positions.

Chart A2 Daily Effective Cash Balances as % of Liabilities Base over a

Typical Two-week Maintenance Period in FY2010/11

Money Market Factors Liquidity Impact of Autonomous Money Market Factors Chart A3 shows the liquidity impact of each of the autonomous money market factors, which include (i) public sector operations, (ii) currency in circulation, and (iii) Singapore Government Securities (SGS) issuance, redemption and coupon payments, over FY2010/11. Public sector operations include the Government’s and CPF Board’s net transfers of funds between their accounts with MAS and their deposits with commercial banks. In FY2010/11, the liquidity impact of the autonomous money market factors was net contractionary, largely arising from public sector operations. Public sector operations were consistently contractionary throughout the year. SGS issuance and redemption was contractionary in Q4 2010, but mildly expansionary in the other quarters as the amount of redemptions exceeded the issuance size in those quarters. The liquidity impact of currency in circulation was negligible.

Monetary Authority of Singapore Economic Policy Group

1 2 3 4 5 6 7 8 9 10 11 12 13 14Day

2.6

2.8

3.0

3.2

3.4

MA

S as

% o

f Lia

bilit

ies

Bas

eA

ggre

gate

Ban

k B

alan

ces

with Thu Mon Wed

Mon

Fri

Wed

Fri

Macroeconomic Developments 25

Chart A3 Liquidity Impact of Autonomous Money Market Factors

2010 Q2 Q3 Q4 2011 Q1

0

Contractionary (-) : Withdrawal of liquidity from banking system

Expansionary (+) : Injection of liquidity into banking system

Public Sector OperationsCurrency in CirculationSingapore Government Securities