Embed Size (px)

Citation preview

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 1/51

SHAIK.SURESH (20085)

SUSHMITA (20087)UTPAL MANE (20088)

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 2/51

Relating to theresponsibilities of

individual managers.

To evaluatemanagers on

controllable items.

An accounting system thatprovides information . . .

WHAT IS RESPONSIBILITY

ACCOUNTING ?

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 3/51

Decision Making is Pushed Down

Supervisor Supervisor

Middle

Management

Supervisor Supervisor

Middle

Management

Top

Management

DECENTRALIZATION

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 4/51

ADVANTAGES OF DECENTRALIZATION

Promotes betterdecision making.

Allows upper-level management toconcentrate on strategic decisions.

Improvesproductivity.

Developslower-levelmanagers.

Improvesperformanceevaluation.

Advantages

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 5/51

DISADVANTAGES OF DECENTRALIZATION

Upper level management loses some control.

Lack of goal setting.

Duplication of effort.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 6/51

Responsibility Reports

Responsibility

ReportsPrepared for eachindividual who has

control over

revenue or expenseitems

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 7/51

RESPONSIBILITY

REPORTS

Prepare budgets foreach responsibility center.

Prepare timely performance reportscomparing actual amounts with budgeted amounts.

Measure performance ofeach responsibility center.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 8/51

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 9/51

A responsibility center is the point in an organization where the

control over revenue or expense is located, e.g. division,

department or a single machine.

Examples:

A specific store in a chain of grocery stores.

A work-station in a production line manufacturing automobile

batteries

The payroll data processing center within a firm.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 10/51

It is like a small business, and its manager is asked to run

that small business and preserve the interests of the largerorganization.

Goals for the center should be specific and measurable, and

should promote the long terms interests of the organization

and should be compatible with other responsibility center

activities.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 11/51

Example: A courier service (DHL)

Courier operations dispatch trucks to pick up or delivershipments from local terminals.

It could be sent to one or more central terminals andthen sorted and redirected. Success of this service would depend on:

Service commitment to customers (on time, without damage)and controlling costs

Let us suppose that each terminal is treated as aresponsibility center.

How should the company measure the performance ofeach terminal, its mangers, and its employees?

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 12/51

To focus on efficiency: It could measure no. of parcels pickedup, sorted or delivered, per route, per employee, per vehicle, perhour or per shift.

To focus on customer service: It could measure each group’s

contribution to customers proportion of the time the terminal metits deadlines, when terminals are required to sort shipments, whatthe sorting error rate was.

It could also measure customer service : no. of complaintsoperations group receives, average time taken by the operationgroup to respond to complaints, and no. of complaints of poor, orimpolite service.

Measuring the performance of thecourier-terminal responsibility center

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 13/51

TYPES OF RESPONSIBILITY

CENTERS

Responsibility

Centers

CostCenter

ProfitCenter

InvestmentCenter

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 14/51

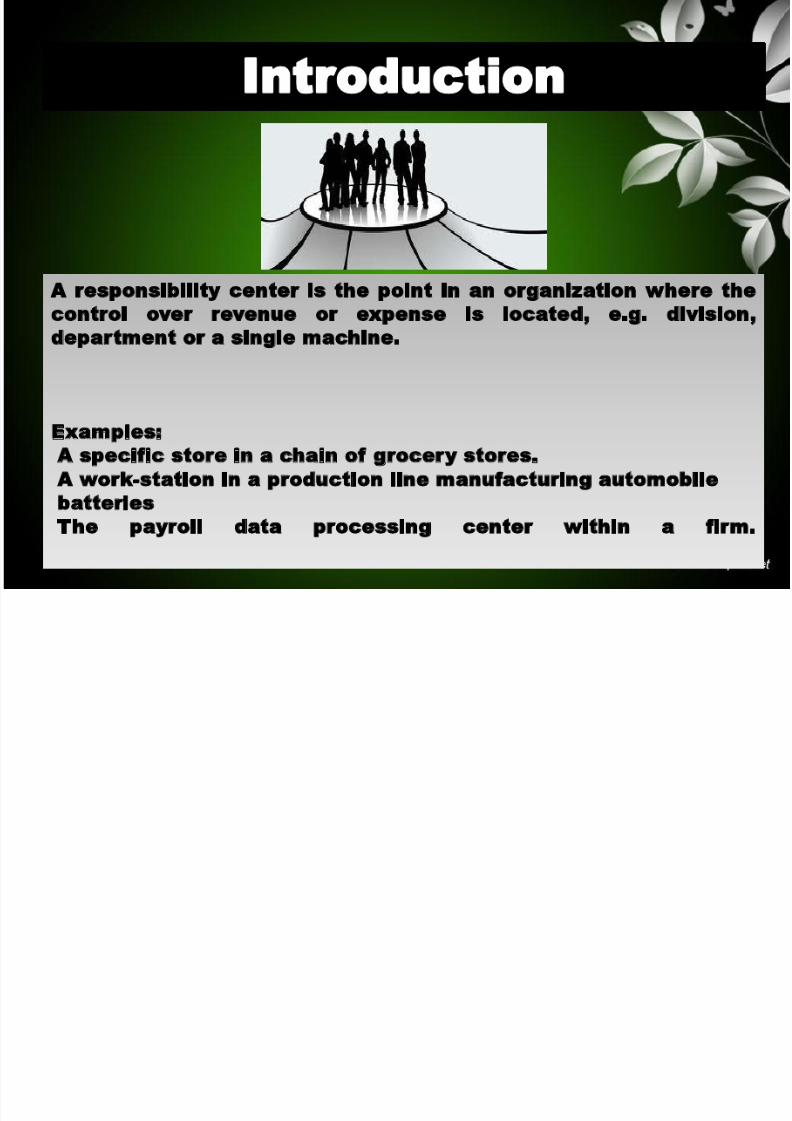

Responsibility centers whose employees control costs,

but do not control their revenues or investment level.

A cost center is evaluated by means of performance

reports (i.e., comparison of actual with standard).

Examples: Production department in a

manufacturing unit,a dry cleaning business

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 15/51

Input OutputProcess

Control only this

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 16/51

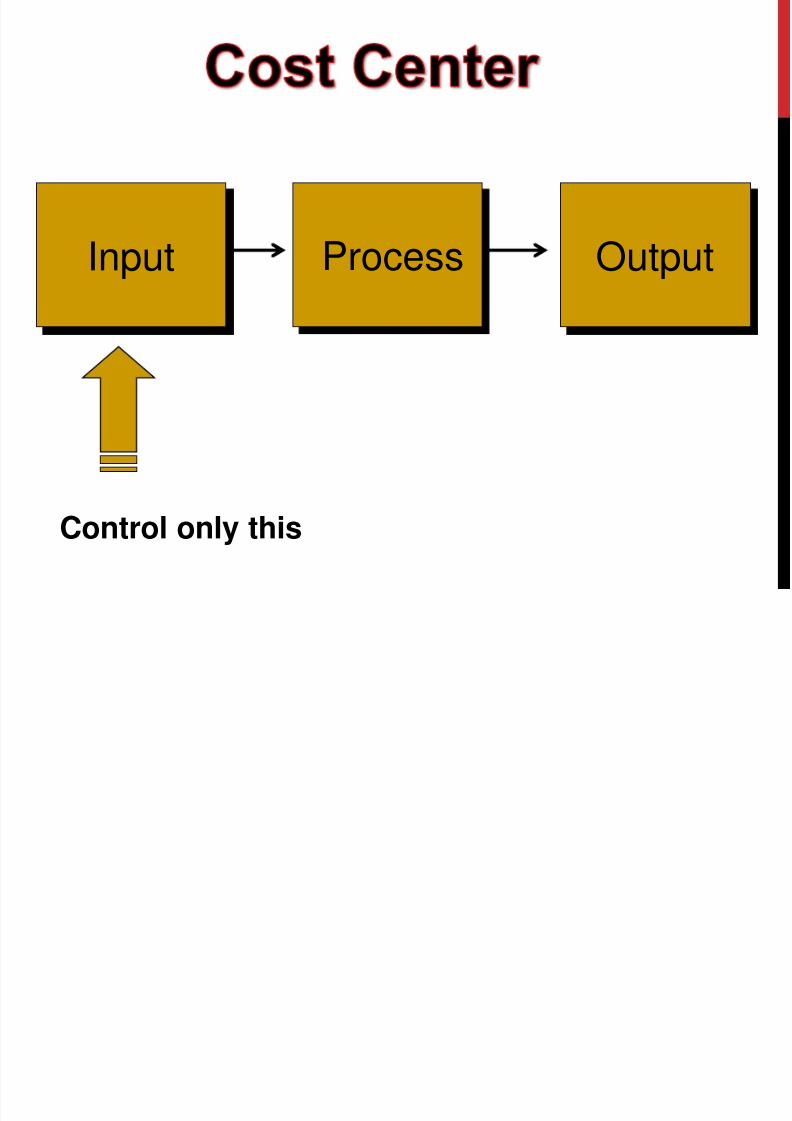

Prod. 1 Prod. 2 Prod. 3 Prod. 4 Total

Units made 245,000 385,000 636,000 1,250,000

Units per batch 500 2,500 1,500 5,000

No. of batches 490 154 424 250

Cost per unit $ 5.40 $3.20 $4.25 $1.45

Cost per batch $325.00 $680.00 $400.00 $135.00

Unit-related costs

(245,000x$5.40)

$1,323,000 $1,232,000 $2,703,000 $1,812,500 $7,070,500

Batch-related costs

(490x$325)

159,250 104,720 169,600 33,750 467,320

Prod.-sustaining

costs

125,000 168,000 256,000 355,000 904,000

Facility costs 1,450,000

Total cost center

costs

$9,891,820

MORTON CARPETS – BUDGETED COST

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 17/51

Prod. 1 Prod. 2 Prod. 3 Prod. 4 Total

Units made2,945,000

345,000 675,000 950,000

Units per batch 600 2,300 1,800 6,000

No. of batches 492 150 375 159

Cost per unit $ 5.43 $3.18 $4.33 $1.40

Cost per batch $335.00 $670.00 $387 $144.00

Unit-related costs $1061,850 $1,097,100 $2,922,750 $1,330,000 $6,951,700

Batch-related costs 164,820 100,500 145,125 22,896 433,341

Prod.-sustaining

costs

133,000 163,000 259,000 362,000 917,,000

Facility costs 1,650,000

Total cost center

costs

$9,952,041

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 18/51

Budget Actual VarianceUnrelated costs

Product 1 1,323,000.00 1,601,850.00 278,850.00

Product 2 1,232,000.00 1,097,100.00 -134,900.00Product 3 2,703,000.00 2,922,750.00 219,750.00Product 4 1,812,500.00 1,330,000.00 -482,500.00

Total 7,070,500.00 6,951,700.00 -118,800.00Batch related costs

Product 1 159,250.00 164,820.00 5,570.00

Product 2 104,720.00 100,500.00 -4,220.00Product 3 169,600.00 145,125.00 -24,475.00Product 4 33,750.00 22,896.00 -10,854.00

Total 467,320.00 433,341.00 -33,979.00Prod. sus. Costs

Product 1 125,000.00 133,000.00 8,000.00

Product 2 168,000.00 163,000.00 -5,000.00Product 3 256,000.00 259,000.00 3,000.00Product 4 355,000.00 362,000.00 7,000.00

Total 904,000.00 917,000.00 13,000.00Fac. Sus. Costs 1,450,000.00 1,650,000.00 200,000.00

Total 9,891,820.00 9,952,041.00 60,221.00

Variance Analysi s

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 19/51

Engineered: Those costs that can be reasonablyassociated with a cost center – direct labor, direct

materials, telephone/electricity consumed, officesupplies.

Discretionary: Where a direct relationship between acost unit and expenses cannot be reasonably made;Management allocates them on a discretionary basis(e.g. depreciation expenses for machines utilized).

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 20/51

Motivation of staff who feel committed to the cost centre

Improved monitoring of cost and expenditure

Improved management information on profit ability

Improved monitoring of investment returns

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 21/51

In practice, it may be difficult to allocate costs to aparticular division / centre

Cost centres may add to pressures and stress on staff

Senior managers may be unable to recognise whethera cost centre is running effectively / ineffectively

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 22/51

PROFIT CENTERS

Responsibility ofgenerating revenue andcontrolling costs.

Profit center evaluation

techniques include:Comparison of current year

income with a target or budget.

Relative performanceevaluation compares the center

with other similar profitcenters.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 23/51

CONT…

If performance is poor, it may reflect poor conditions

that no one in the organization could control as well aspoor local conditions.

For this reason, organizations should not evaluate

performance only based on costs and profits, but

Perform detailed evaluations that include quality,

material use, labor use, and service measures that the

local unit can control.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 24/51

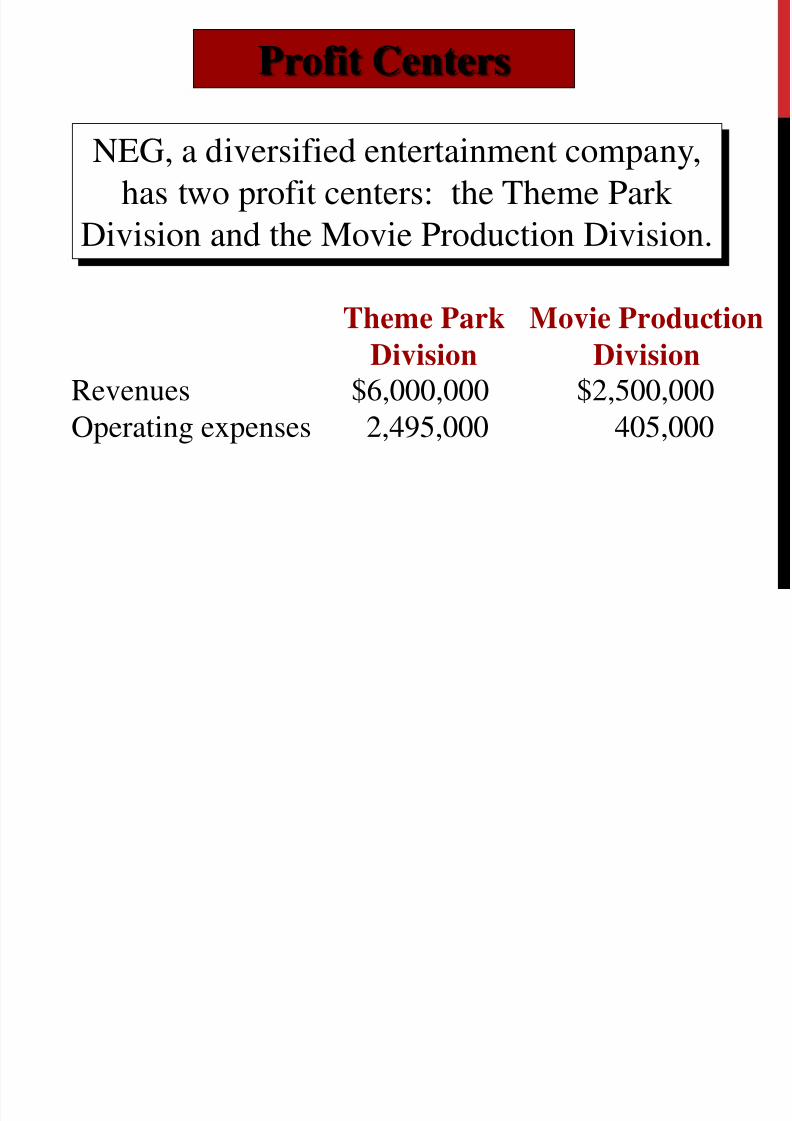

Profit Centers

NEG, a diversified entertainment company,has two profit centers: the Theme Park

Division and the Movie Production Division.

Theme Park

Division

Movie Production

DivisionRevenues $6,000,000 $2,500,000

Operating expenses 2,495,000 405,000

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 25/51

Charging Service Department Coststo Production Divisions

Purchasing Department: $400,000

(Activity base: number of purchase requisitions)Theme Park Division 25,000 purchase requisitions

Movie Production Division: 15,000 purchase requisitions

Total 40,000

$400,000

40,000 purchase requisitions

$10 per purchase

requisition=

Profit Centers

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 26/51

Charging Service Department Coststo Production Divisions

Payroll Accounting: $255,000

(Activity base: number of payroll checks)

$255,000

15,000 payroll checks= $17 per payroll check

Theme Park Division 12,000 payroll checks

Movie Production Division: 3,000 payroll checks

Total 15,000

Profit Centers

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 27/51

Charging Service Department Coststo Production Divisions

Legal Department: $250,000

(Activity base: number of payroll checks)

$250,000

1,000 hours= $250 per hour

Theme Park Division 100 billed hours

Movie Production Division: 900 billed hours

Total 1,000

Profit Centers

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 28/51

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 29/51

Purchasing $250,000 $150,000

Payroll accounting 204,000 51,000

12,000 payroll

checks x $17 per

payroll check

3,000 payroll

checks x $17 per

payroll check

Nova Entertainment Group

Service Department Charges to NEG DivisionsFor the Year Ended December 31, 2006

Theme Movie

Park Production

Service Department Division Division

Profit Centers

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 30/51

Purchasing $250,000 $150,000

Payroll accounting 204,000 51,000

Legal 25,000 225,000

Nova Entertainment Group

Service Department Charges to NEG DivisionsFor the Year Ended December 31, 2006

Theme Movie

Park Production

Service Department Division Division

Profit Centers

100 hours x $250

per hour

900 hours x $250

per hour

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 31/51

Purchasing $250,000 $150,000

Payroll accounting 204,000 51,000

Legal 25,000 225,000

Total service department charges $479,000 $426,000

Nova Entertainment Group

Service Department Charges to NEG DivisionsFor the Year Ended December 31, 2006

Theme Movie

Park Production

Service Department Division Division

Profit Centers

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 32/51

Nova Entertainment Group

Divisional Income StatementsFor the Year Ended December 31, 2006

Theme Park Division Movie Production Division

Income from operations before

service department charges.

Revenues $6,000,000 $2,500,000

Operating expenses 2,495,000 405,000

Income from operations $3,505,000 $2,095,000

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 33/51

Nova Entertainment Group

Divisional Income StatementsFor the Year Ended December 31, 2006

Theme Park Division Movie Production Division

Revenues $6,000,000 $2,500,000

Operating expenses 2,495,000 405,000

Income from operations $3,505,000 $2,095,000Less service dept. charges:

Purchasing $ 250,000 $ 150,000

Payroll accounting 204,000 51,000

Legal 25,000 225,000Total service department

charges $ 479,000 $ 426,000

Income from operations $3,026,000 $1,669,000

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 34/51

PROFIT CENTRE ADVANTAGES

Improves quality of decision Improves speed of decision

Ensures better and safer delegation of authority

Ensures better motivation and evokes commitment

Enhance profit consciousness with every expensemode

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 35/51

Loss of overall control of company

Profit centre could be working towards different or

non- company agendas

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 36/51

USES OF COST AND PROFIT CENTRES

They allow the business to compare performance between departments

/ across products / brands ,etc.

This allows the business to make decisions about underperforming

areas

If a profit centre is identified as doing well businesses may want to

focus on the reasons behind this

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 37/51

CONT….

They allow a more focused study of a firms finances

Benchmarking can take place

Responsibility for a profit / cost centre will motivatethe individual responsible

By placing responsibility with the person involved inthe activity the finances may be run more efficiently

than would be the case if a more remote, senior manager controlled it.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 38/51

WHY OPERATE COST AND PROFIT CENTRES

Financial reasons – they allow to manage and control money. They

allow the business to identify which areas are most profitable

Organisational reasons – helps with the organisation of departments

and resources

Motivational reasons – motivates managers and workers

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 39/51

WHAT IS AN INVESTMENTS

CENTER?

Investment Center

A segment whose managerhas control over costs,

revenues, and investments in

operating assets.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 40/51

Investment CenterA Systems Perspective

Input OutputProcess

Control these

Investment Center

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 41/51

EVALUATION OF INVESTMENT

CENTER…:

An investment center isevaluated by means of theReturn on Investment (ROI) orthe Residual Income (RI) it isable to generate.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 42/51

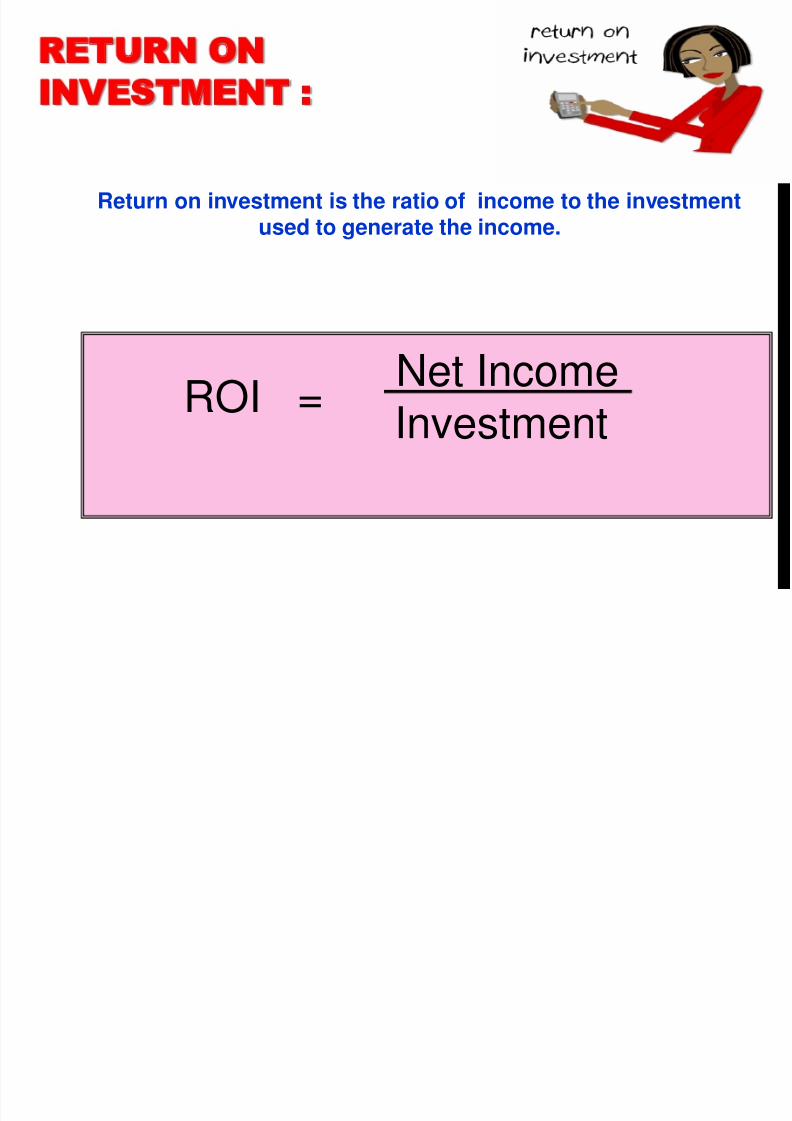

RETURN ON

INVESTMENT :

Return on investment is the ratio of income to the investmentused to generate the income.

ROI =

Net Income

Investment

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 43/51

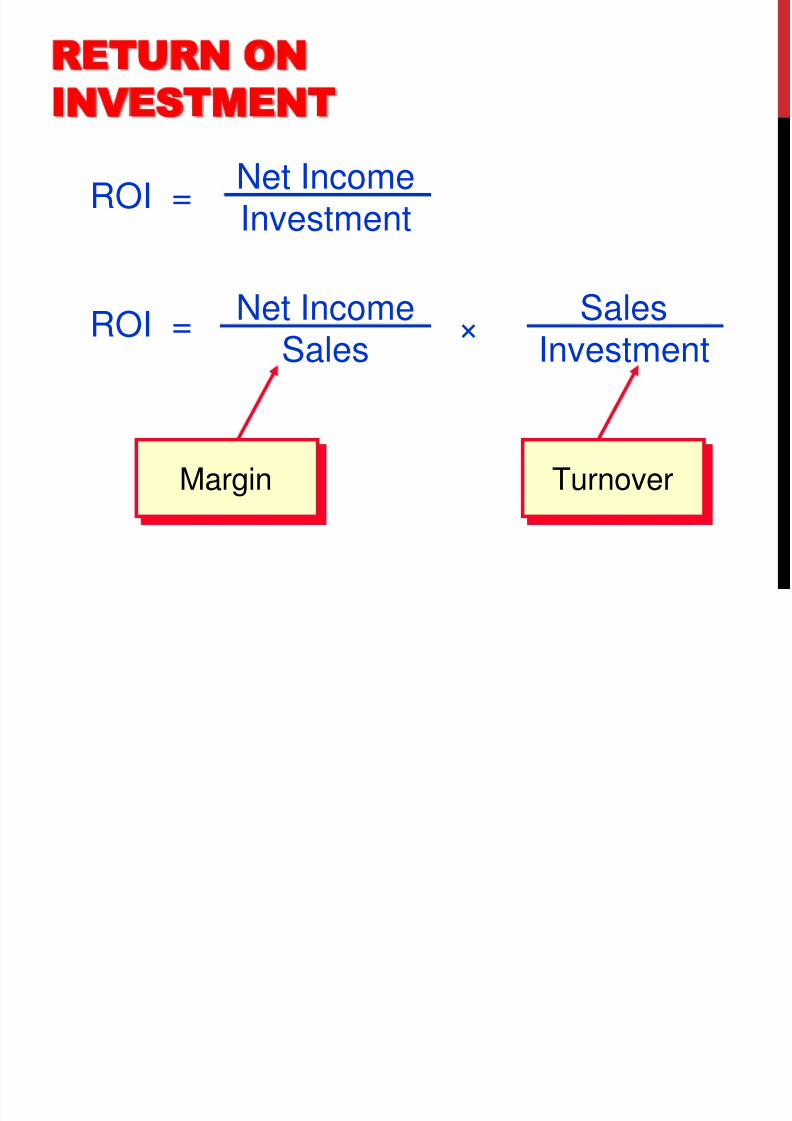

ROI =Net IncomeInvestment

ROI = Net IncomeSales

×Sales

Investment

Margin Turnover

RETURN ON

INVESTMENT

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 44/51

RETURN ON

INVESTMENT

Cola Company reports the following:

Net Income $ 30,000Sales $ 500,000

Investment $ 200,000

Let’s calculate ROI.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 45/51

ROI = 6% × 2.5 = 15%

RETURN ON

INVESTMENT

ROI = Net IncomeSales

×Sales

Investment

ROI = $30,000$500,000

×$500,000$200,000

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 46/51

IMPROVING R0I

Three ways to improve ROI

Increase

Sales

ReduceExpenses

Reduce

Investment

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 47/51

IMPROVING R0I

Cola Company’s manager was able to increase sales to

$600,000 which increased net income to $42,000.

There was no change in investment.

Let’s calculate the new ROI.

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 48/51

Cola Company increased ROI from 15% to 21%.

ROI = 7% × 3 = 21%

ROI = Net IncomeSales

×Sales

Investment

ROI = $42,000$600,000

×$600,000$200,000

IMPROVING R0I

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 49/51

ROI - A MAJOR

DRAWBACK

As division manager at Cola Company,your compensation package includesa salary plus bonus based on your division’s ROI -- the higher your ROI, the bigger your bonus.

The company requires an ROI of 20% on all newinvestments -- your division has been producing anROI of 30%.

You have an opportunity to invest in a new projectthat will produce an ROI of 25%.

As division manager would youinvest in this project?

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 50/51

ROI - A MAJOR DRAWBACK

As division manager,I wouldn’t invest in that project because

it would lower my pay!

I thought we weresupposed to do what

was best for the

company!

8/2/2019 Ma Ppt Final

http://slidepdf.com/reader/full/ma-ppt-final 51/51

THANK YOU ONE & ALL