Embed Size (px)

Citation preview

MMACROECONOMICSACROECONOMICS

C H A P T E R

Economic Growth II:Technology, Empirics, and Policy

8

CHAPTER 8 Economic Growth II slide 2

Introduction

In the Solow model of Chapter 7, the production technology is held constant. income per capita is constant in the steady state.

Neither point is true in the real world: 1904-2004: U.S. real GDP per person grew by a

factor of 7.6, or 2% per year. examples of technological progress abound

(see next slide).

CHAPTER 8 Economic Growth II slide 3

Technological progress in the Solow model

A new variable: E = labor efficiency

Assume: Technological progress is labor-augmenting: it increases labor efficiency at the exogenous rate g:

Eg

E

CHAPTER 8 Economic Growth II slide 4

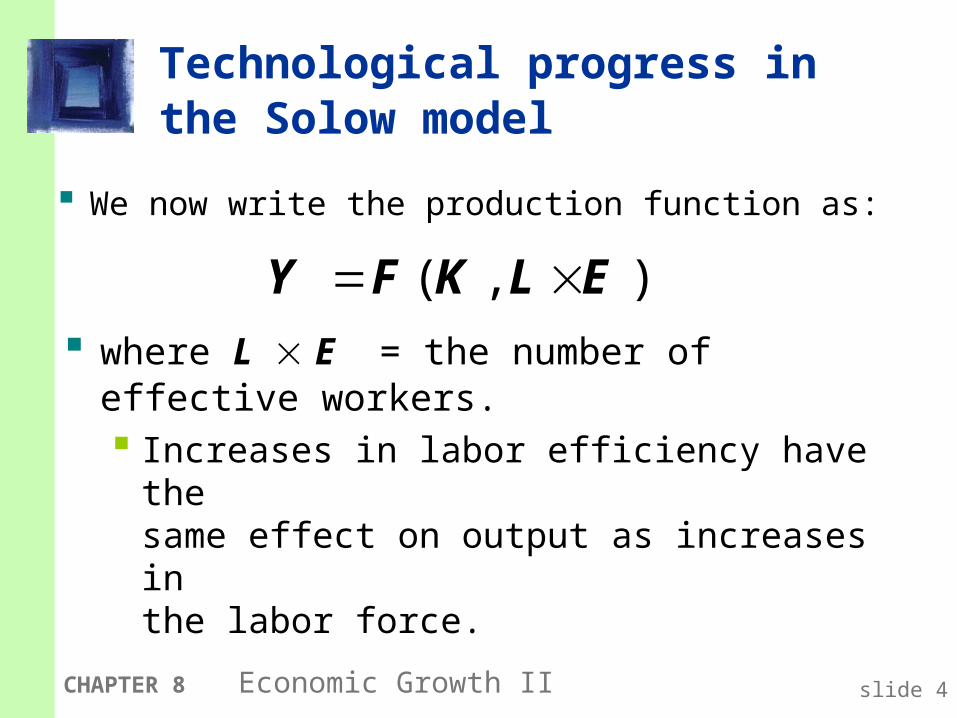

Technological progress in the Solow model

We now write the production function as:

where L E = the number of effective workers. Increases in labor efficiency have the

same effect on output as increases in the labor force.

( , )Y F K L E

CHAPTER 8 Economic Growth II slide 5

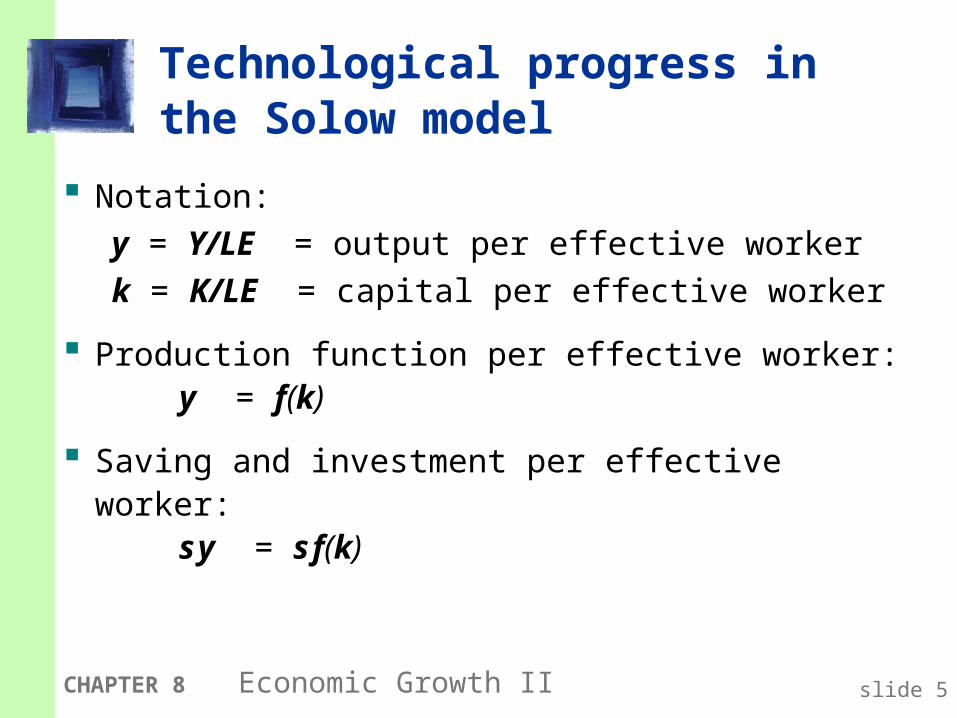

Technological progress in the Solow model

Notation:

y = Y/LE = output per effective worker

k = K/LE = capital per effective worker

Production function per effective worker:y = f(k)

Saving and investment per effective worker:s y = s f(k)

CHAPTER 8 Economic Growth II slide 6

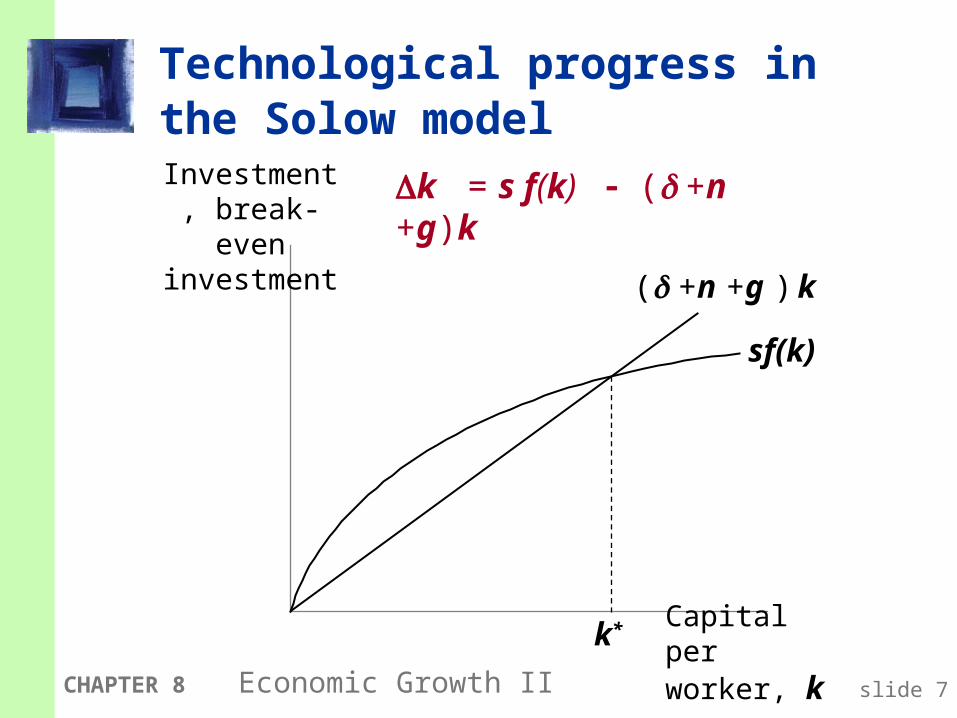

Technological progress in the Solow model

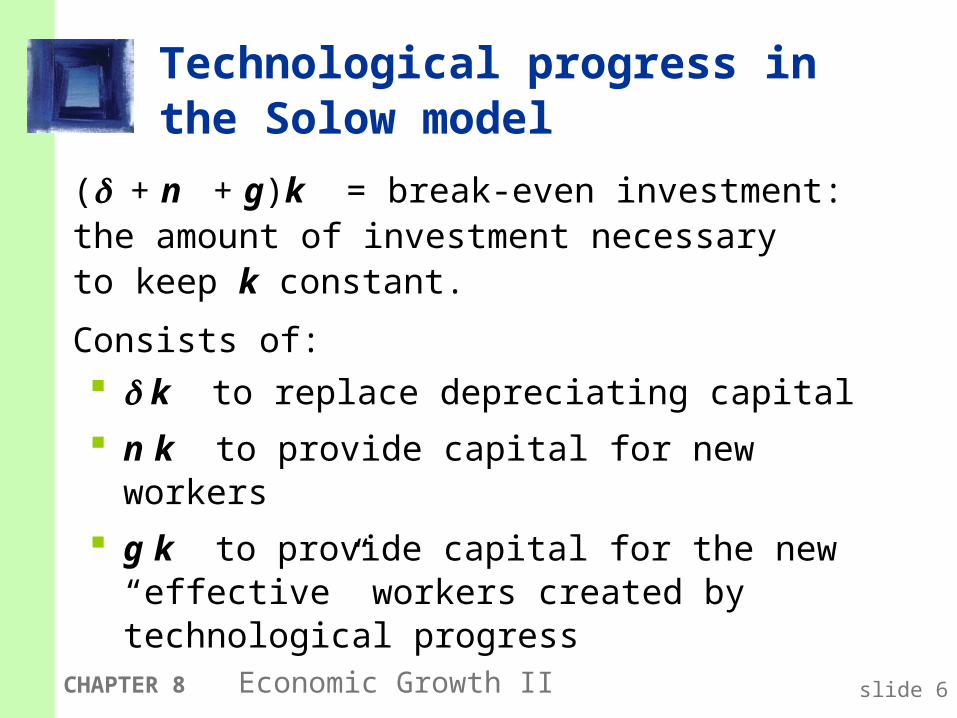

( + n + g)k = break-even investment: the amount of investment necessary to keep k constant.

Consists of: k to replace depreciating capital

n k to provide capital for new workers

g k to provide capital for the new “effective” workers created by technological progress

CHAPTER 8 Economic Growth II slide 7

Technological progress in the Solow model

Investment, break-even investment

Capital per worker, k

sf(k)

( +n +g ) k

k*

k = s f(k) ( +n +g)k

CHAPTER 8 Economic Growth II slide 8

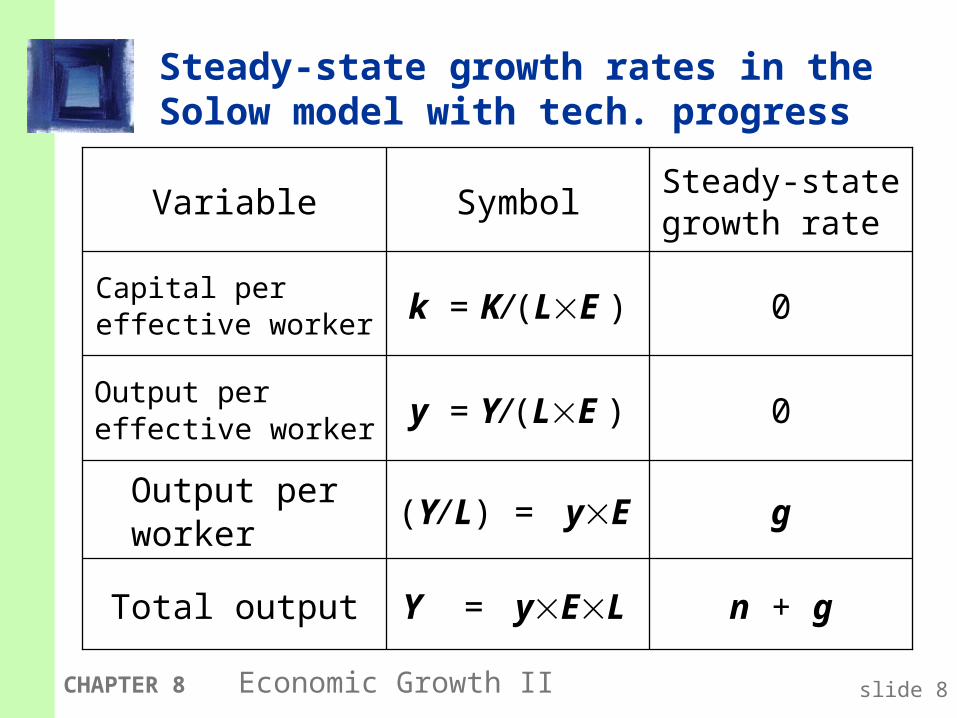

Steady-state growth rates in the Solow model with tech. progress

n + gY = yEL Total output

g(Y/ L) = yE Output per worker

0y = Y/(LE )Output per effective worker

0k = K/(LE )Capital per effective worker

Steady-state growth rate

SymbolVariable

CHAPTER 8 Economic Growth II slide 9

The Golden Rule

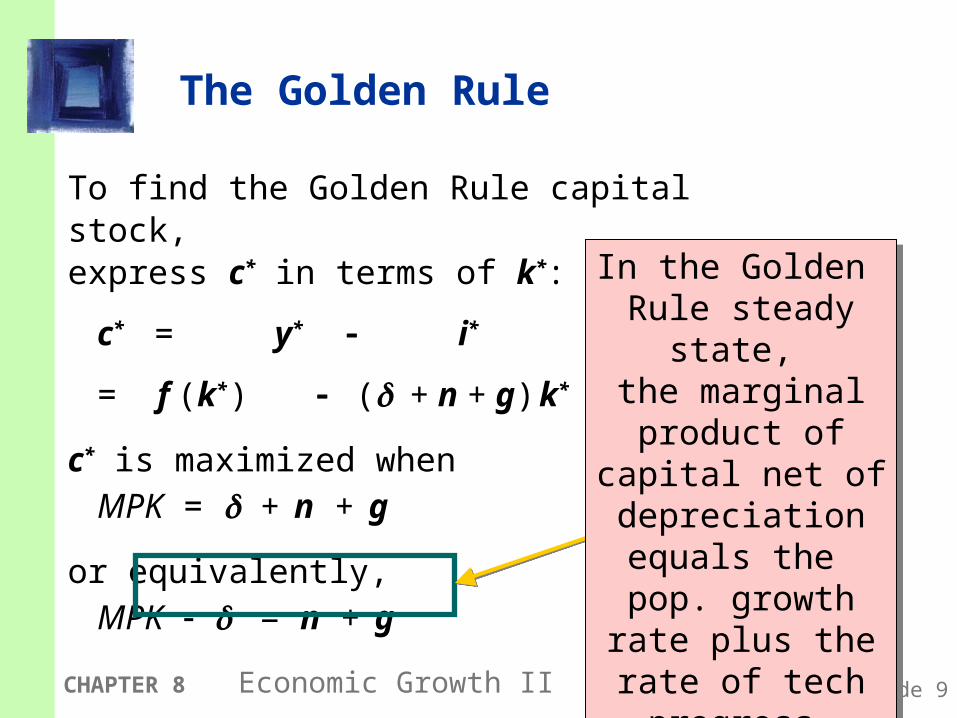

To find the Golden Rule capital stock, express c* in terms of k*:

c* = y* i*

= f (k* ) ( + n + g) k*

c* is maximized when MPK = + n + g

or equivalently, MPK = n + g

In the Golden Rule steady state,

the marginal product of capital

net of depreciation equals the

pop. growth rate plus the rate of tech progress.

In the Golden Rule steady state,

the marginal product of capital

net of depreciation equals the

pop. growth rate plus the rate of tech progress.

CHAPTER 8 Economic Growth II slide 10

Growth empirics: Balanced growth

Solow model’s steady state exhibits balanced growth - many variables grow at the same rate.

Solow model predicts Y/L and K/L grow at the same rate (g), so K/Y should be constant.

This is true in the real world.

Solow model predicts real wage grows at same rate as Y/L, while real rental price is constant.

This is also true in the real world.

CHAPTER 8 Economic Growth II slide 11

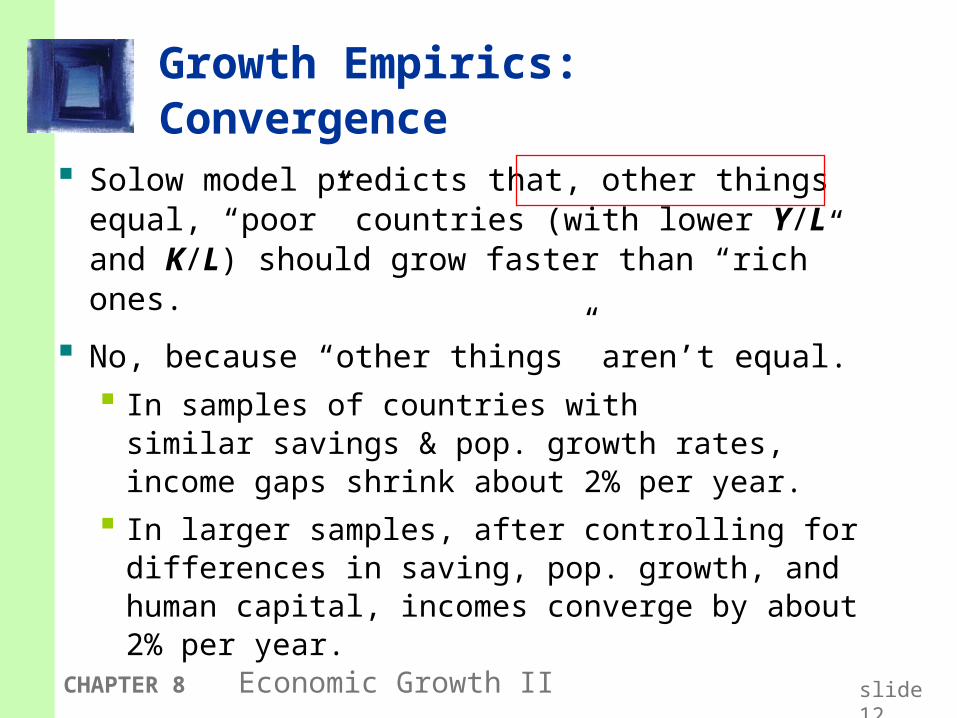

Growth empirics: Convergence

Solow model predicts that, other things equal, “poor” countries (with lower Y/L and K/L) should grow faster than “rich” ones.

If true, then the income gap between rich & poor countries would shrink over time, causing living standards to “converge.”

In real world, many poor countries do NOT grow faster than rich ones. Does this mean the Solow model fails?

CHAPTER 8 Economic Growth II slide 12

Growth Empirics: Convergence

Solow model predicts that, other things equal, “poor” countries (with lower Y/L and K/L) should grow faster than “rich” ones.

No, because “other things” aren’t equal.

In samples of countries with similar savings & pop. growth rates, income gaps shrink about 2% per year.

In larger samples, after controlling for differences in saving, pop. growth, and human capital, incomes converge by about 2% per year.

CHAPTER 8 Economic Growth II slide 13

Growth empirics: Convergence

What the Solow model really predicts is conditional convergence - countries converge to their own steady states, which are determined by saving, population growth, and education.

This prediction comes true in the real world.

CHAPTER 8 Economic Growth II slide 14

Growth empirics: Factor accumulation vs. production efficiency

Differences in income per capita among countries can be due to differences in

1. capital – physical or human – per worker

2. the efficiency of production (the height of the production function)

Studies: both factors are important. the two factors are correlated: countries with

higher physical or human capital per worker also tend to have higher production efficiency.

CHAPTER 8 Economic Growth II slide 15

Growth empirics: Factor accumulation vs. production efficiency

Possible explanations for the correlation between capital per worker and production efficiency:

Production efficiency encourages capital accumulation.

Capital accumulation has externalities that raise efficiency.

A third, unknown variable causes capital accumulation and efficiency to be higher in some countries than others.

CHAPTER 8 Economic Growth II slide 16

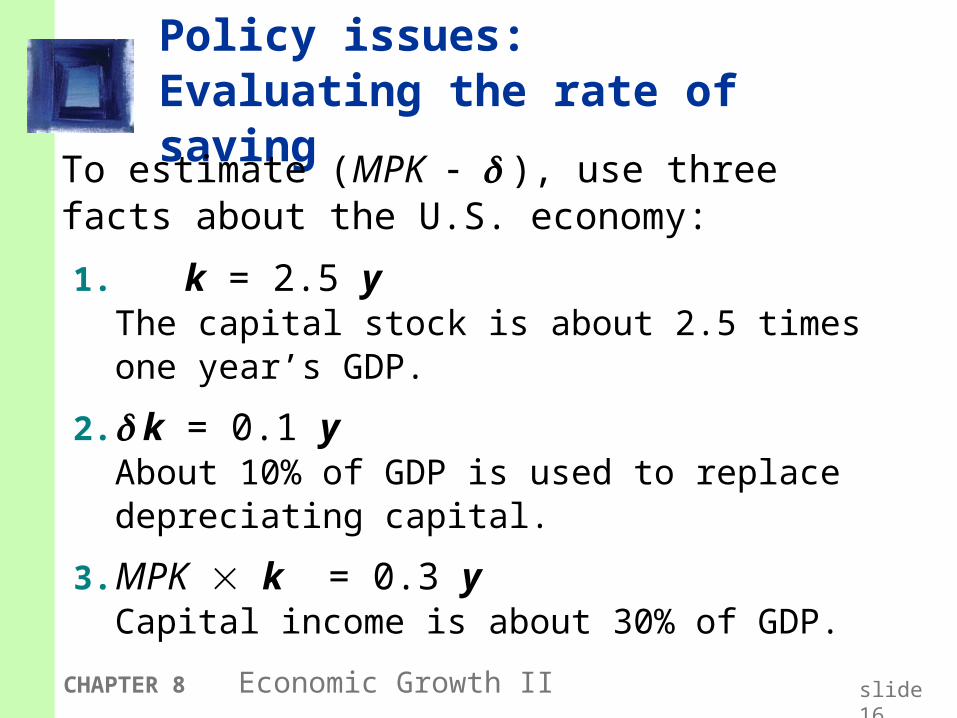

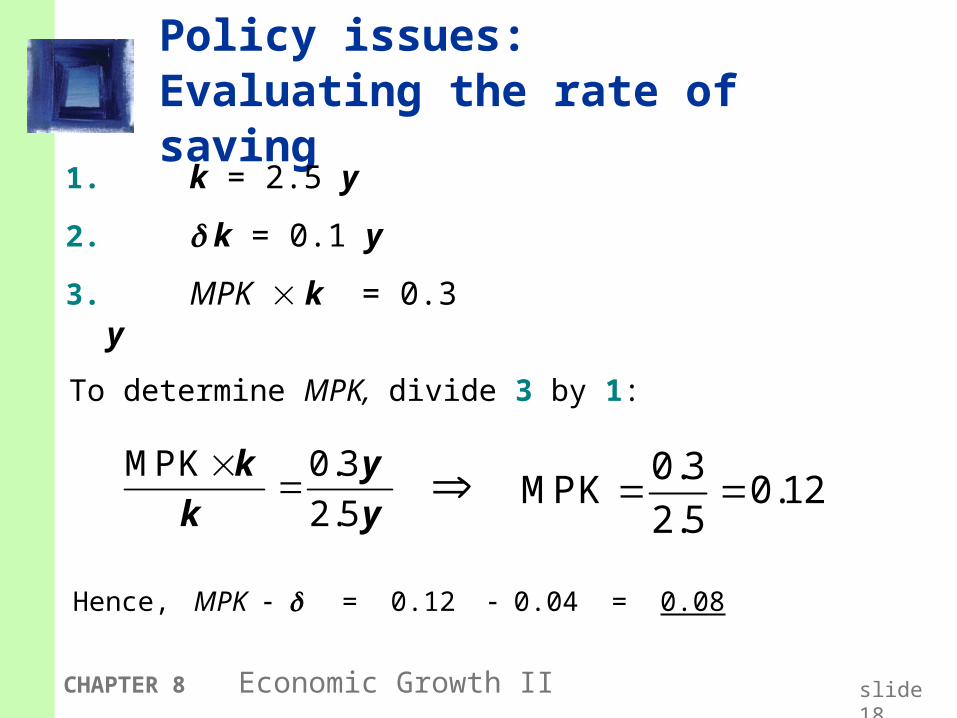

Policy issues: Evaluating the rate of saving

To estimate (MPK ), use three facts about the U.S. economy:

1. k = 2.5 yThe capital stock is about 2.5 times one year’s GDP.

2. k = 0.1 yAbout 10% of GDP is used to replace depreciating capital.

3. MPK k = 0.3 yCapital income is about 30% of GDP.

CHAPTER 8 Economic Growth II slide 17

Policy issues: Evaluating the rate of saving

1. k = 2.5 y

2. k = 0.1 y

3. MPK k = 0.3 y

0.1

2.5

k yk y

0.1

0.042.5

To determine , divide 2 by 1:

CHAPTER 8 Economic Growth II slide 18

Policy issues: Evaluating the rate of saving

MPK 0.3

2.5

k yk y

0.3

MPK 0.122.5

To determine MPK, divide 3 by 1:

Hence, MPK = 0.12 0.04 = 0.08

1. k = 2.5 y

2. k = 0.1 y

3. MPK k = 0.3 y

CHAPTER 8 Economic Growth II slide 19

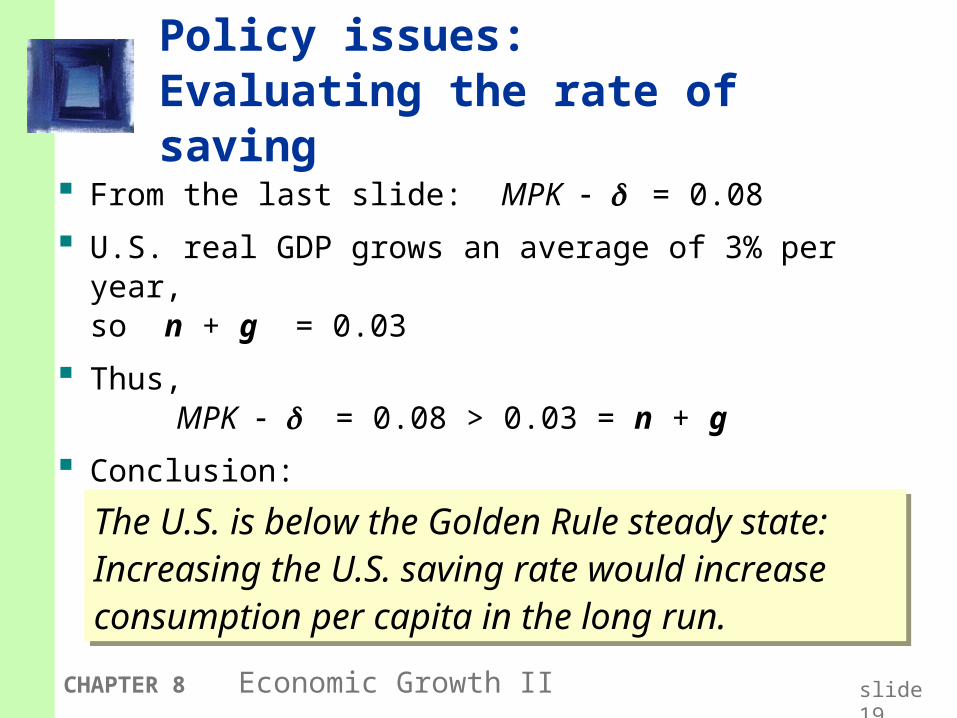

Policy issues: Evaluating the rate of saving

From the last slide: MPK = 0.08

U.S. real GDP grows an average of 3% per year, so n + g = 0.03

Thus, MPK = 0.08 > 0.03 = n + g

Conclusion:

The U.S. is below the Golden Rule steady state: Increasing the U.S. saving rate would increase consumption per capita in the long run.

The U.S. is below the Golden Rule steady state: Increasing the U.S. saving rate would increase consumption per capita in the long run.

CHAPTER 8 Economic Growth II slide 20

Policy issues: How to increase the saving rate

Reduce the government budget deficit(or increase the budget surplus).

Increase incentives for private saving: reduce capital gains tax, corporate income tax,

estate tax as they discourage saving. replace federal income tax with a consumption

tax. expand tax incentives for IRAs (individual

retirement accounts) and other retirement savings accounts.

CHAPTER 8 Economic Growth II slide 21

Policy issues: Allocating the economy’s investment

In the Solow model, there’s one type of capital.

In the real world, there are many types,which we can divide into three categories: private capital stock public infrastructure human capital: the knowledge and skills that

workers acquire through education.

How should we allocate investment among these types?

CHAPTER 8 Economic Growth II slide 22

Policy issues: Allocating the economy’s investment

Two viewpoints:

1. Equalize tax treatment of all types of capital in all industries, then let the market allocate investment to the type with the highest marginal product.

2. Industrial policy: Govt should actively encourage investment in capital of certain types or in certain industries, because they may have positive externalities that private investors don’t consider.

CHAPTER 8 Economic Growth II slide 23

Policy issues: Establishing the right institutions

Creating the right institutions is important for ensuring that resources are allocated to their best use. Examples:

Legal institutions, to protect property rights.

Capital markets, to help financial capital flow to the best investment projects.

A corruption-free government, to promote competition, enforce contracts, etc.

CHAPTER 8 Economic Growth II slide 24

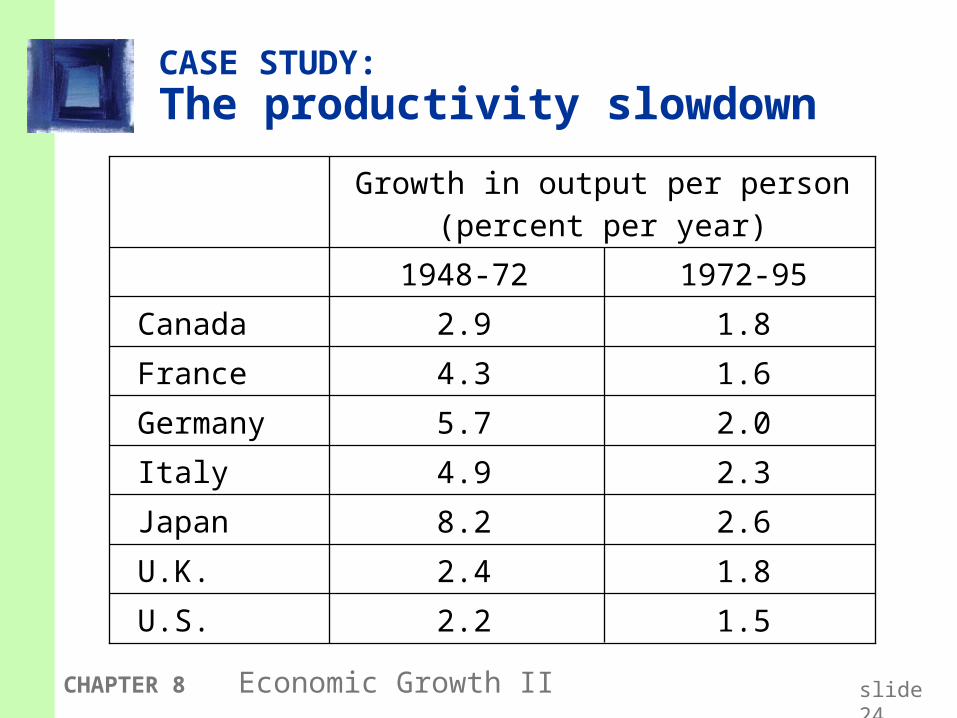

CASE STUDY: The productivity slowdown

1.5

1.8

2.6

2.3

2.0

1.6

1.8

2.2

2.4

8.2

4.9

5.7

4.3

2.9

1972-951948-72

U.S.

U.K.

Japan

Italy

Germany

France

Canada

Growth in output per person(percent per year)

CHAPTER 8 Economic Growth II slide 25

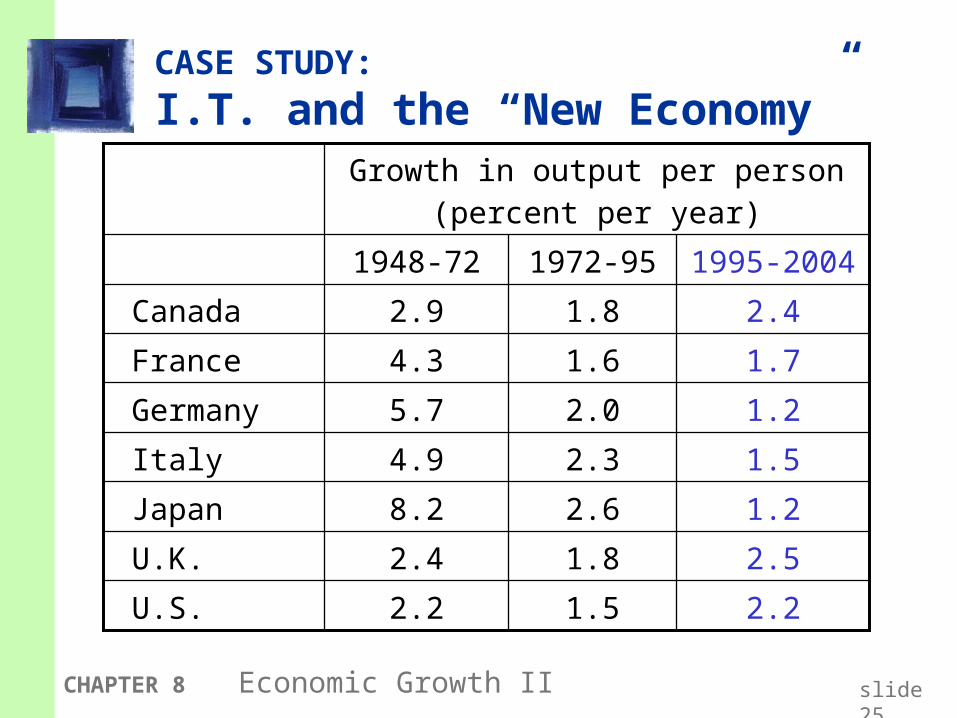

CASE STUDY:

I.T. and the “New Economy”

2.2

2.5

1.2

1.5

1.2

1.7

2.4

1.5

1.8

2.6

2.3

2.0

1.6

1.8

2.2

2.4

8.2

4.9

5.7

4.3

2.9

1995-20041972-951948-72

U.S.

U.K.

Japan

Italy

Germany

France

Canada

Growth in output per person(percent per year)

CHAPTER 8 Economic Growth II slide 26

CASE STUDY:

I.T. and the “New Economy”Apparently, the computer revolution did not affect aggregate productivity until the mid-1990s.

Two reasons:

1. Computer industry’s share of GDP much bigger in late 1990s than earlier.

2. Takes time for firms to determine how to utilize new technology most effectively.

The big, open question: How long will I.T. remain an engine of growth?

CHAPTER 8 Economic Growth II slide 27

Endogenous growth theory

Solow model: sustained growth in living standards is due to

tech progress. the rate of tech progress is exogenous.

Endogenous growth theory: a set of models in which the growth rate of

productivity and living standards is endogenous.

CHAPTER 8 Economic Growth II slide 28

A basic model

Production function: Y = A Kwhere A is the amount of output for each unit of capital (A is exogenous & constant)

Key difference between this model & Solow: MPK is constant here, diminishes in Solow

Investment: s Y

Depreciation: K

Equation of motion for total capital: K = s Y K

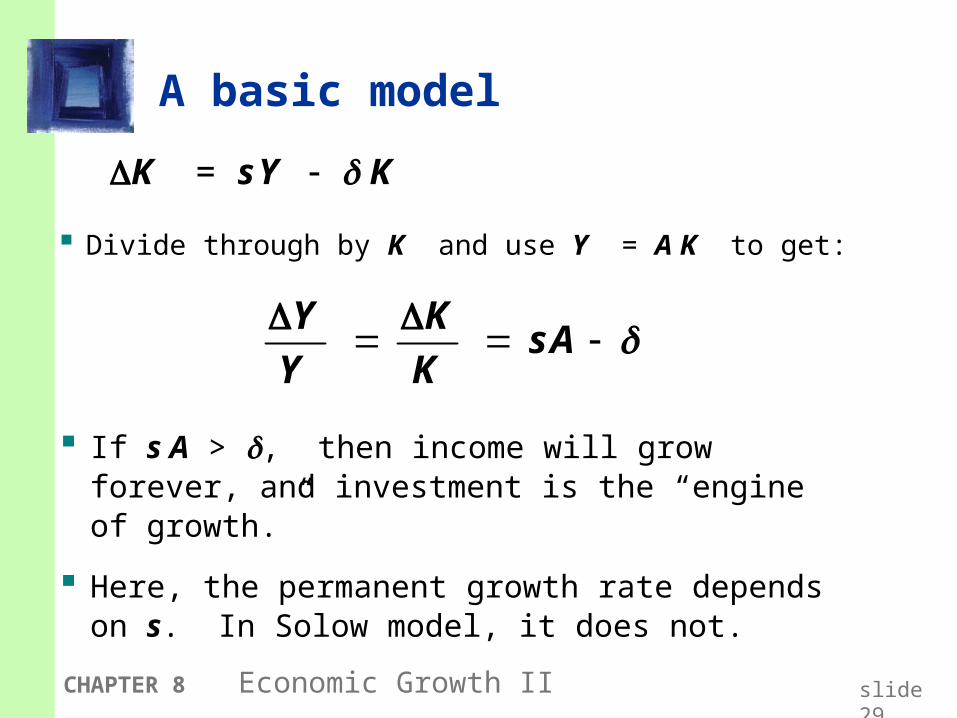

CHAPTER 8 Economic Growth II slide 29

A basic model

K = s Y K

Y KsA

Y K

If s A > , then income will grow forever, and investment is the “engine of growth.”

Here, the permanent growth rate depends on s. In Solow model, it does not.

Divide through by K and use Y = A K to get:

CHAPTER 8 Economic Growth II slide 30

Does capital have diminishing returns or not?

Depends on definition of “capital.”

If “capital” is narrowly defined (only plant & equipment), then yes.

Advocates of endogenous growth theory argue that knowledge is a type of capital.

If so, then constant returns to capital is more plausible, and this model may be a good description of economic growth.

CHAPTER 8 Economic Growth II slide 31

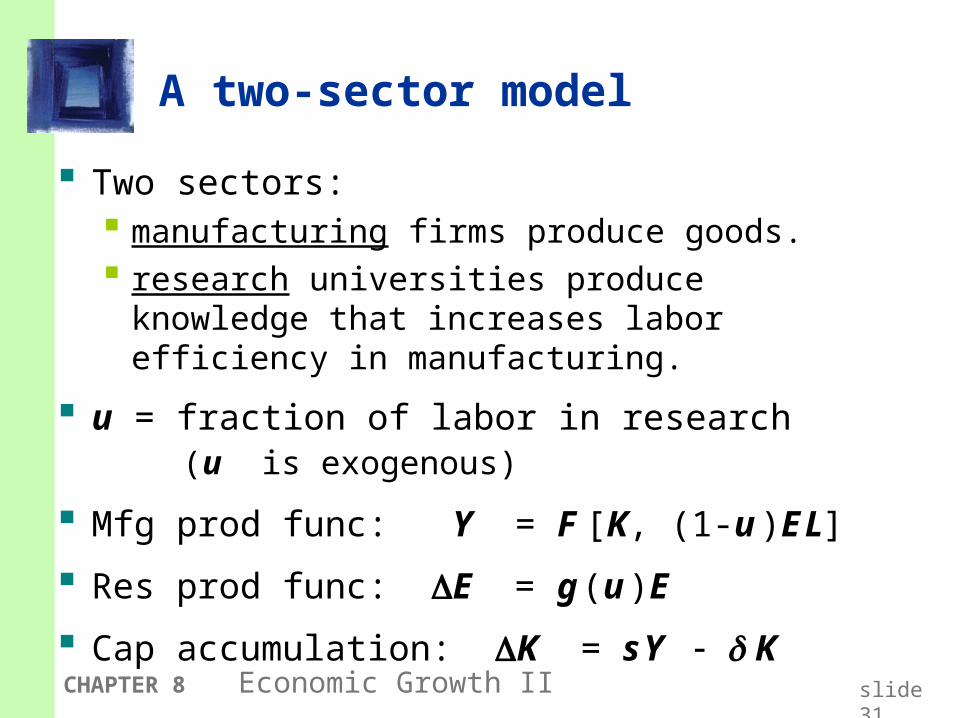

A two-sector model

Two sectors: manufacturing firms produce goods. research universities produce knowledge that

increases labor efficiency in manufacturing.

u = fraction of labor in research (u is exogenous)

Mfg prod func: Y = F [K, (1-u )E L]

Res prod func: E = g (u )E

Cap accumulation: K = s Y K

CHAPTER 8 Economic Growth II slide 32

A two-sector model

In the steady state, mfg output per worker and the standard of living grow at rate E/E = g (u ).

Key variables:s: affects the level of income, but not its

growth rate (same as in Solow model)u: affects level and growth rate of income

Question: Would an increase in u be unambiguously good for the economy?

CHAPTER 8 Economic Growth II slide 33

Facts about R&D

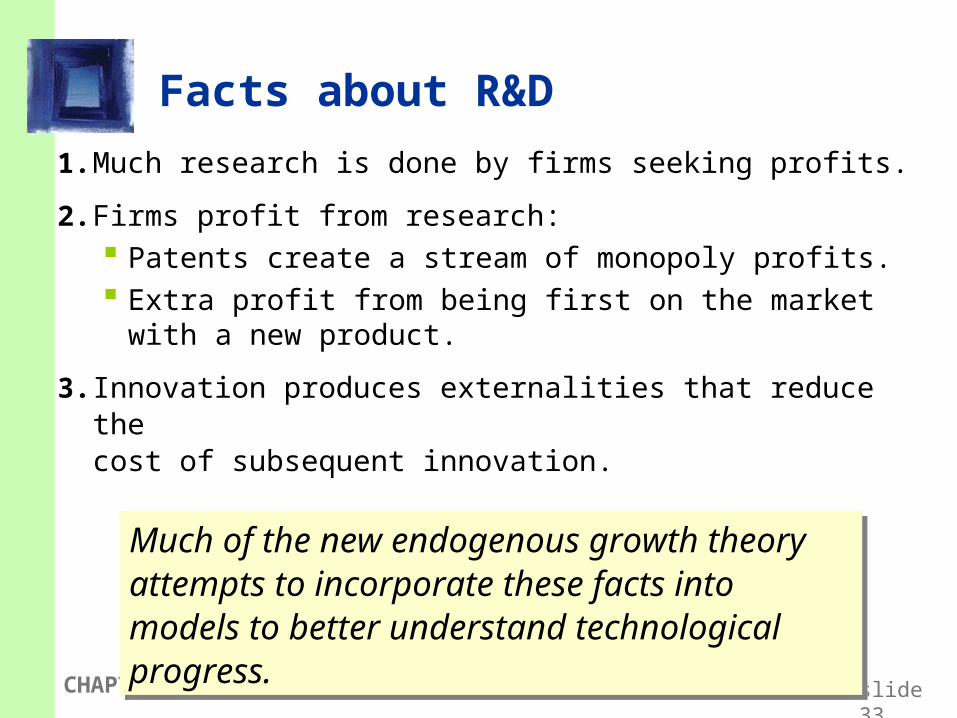

1. Much research is done by firms seeking profits.

2. Firms profit from research: Patents create a stream of monopoly profits. Extra profit from being first on the market with a

new product.

3. Innovation produces externalities that reduce the cost of subsequent innovation.

Much of the new endogenous growth theory attempts to incorporate these facts into models to better understand technological progress.

Much of the new endogenous growth theory attempts to incorporate these facts into models to better understand technological progress.

Chapter SummaryChapter Summary

1. Key results from Solow model with tech progress steady state growth rate of income per person

depends solely on the exogenous rate of tech progress

the U.S. has much less capital than the Golden Rule steady state

2. Ways to increase the saving rate increase public saving (reduce budget deficit) tax incentives for private saving

CHAPTER 8 Economic Growth II slide 34

Chapter SummaryChapter Summary

3. Productivity slowdown & “new economy” Early 1970s: productivity growth fell in the U.S.

and other countries. Mid 1990s: productivity growth increased,

probably because of advances in I.T.

4. Empirical studies Solow model explains balanced growth,

conditional convergence Cross-country variation in living standards is

due to differences in cap. accumulation and in production efficiency

CHAPTER 8 Economic Growth II slide 35

Chapter SummaryChapter Summary

5. Endogenous growth theory: Models that examine the determinants of the rate of

tech. progress, which Solow takes as given. explain decisions that determine the creation of

knowledge through R&D.

CHAPTER 8 Economic Growth II slide 36

MMACROECONOMICSACROECONOMICS

C H A P T E R

Introduction to Economic Fluctuations

9

CHAPTER 8 Economic Growth II slide 38

In this chapter, you will learn…

facts about the business cycle

how the short run differs from the long run

an introduction to aggregate demand

an introduction to aggregate supply in the short run and long run

how the model of aggregate demand and aggregate supply can be used to analyze the short-run and long-run effects of “shocks.”

CHAPTER 8 Economic Growth II slide 39

Facts about the business cycle

GDP growth averages 3–3.5 percent per year over the long run with large fluctuations in the short run.

Consumption and investment fluctuate with GDP, but consumption tends to be less volatile and investment more volatile than GDP.

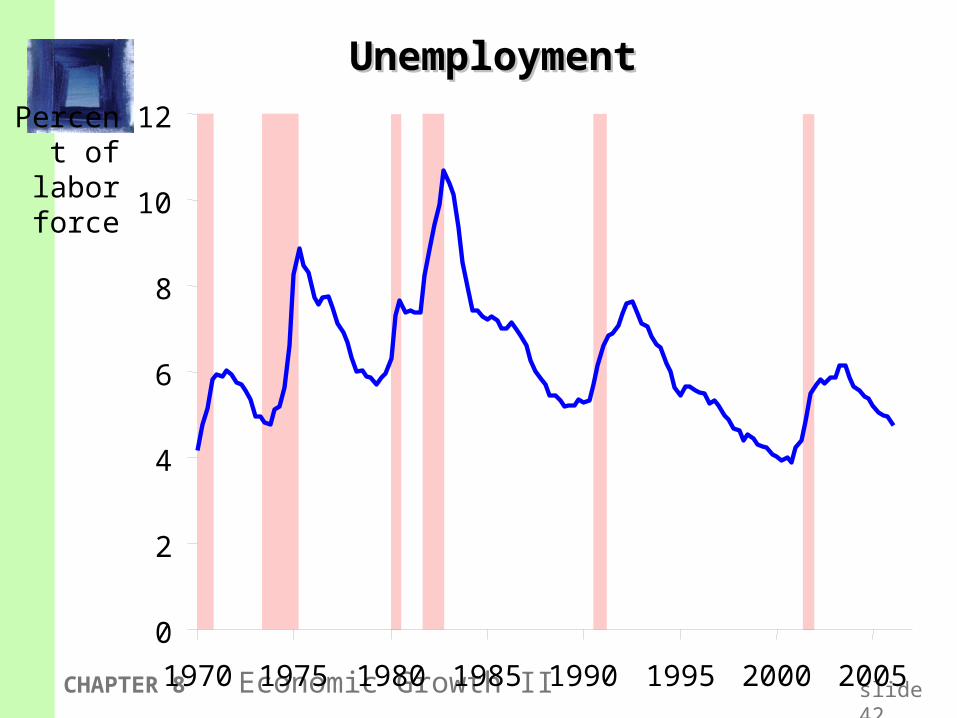

Unemployment rises during recessions and falls during expansions.

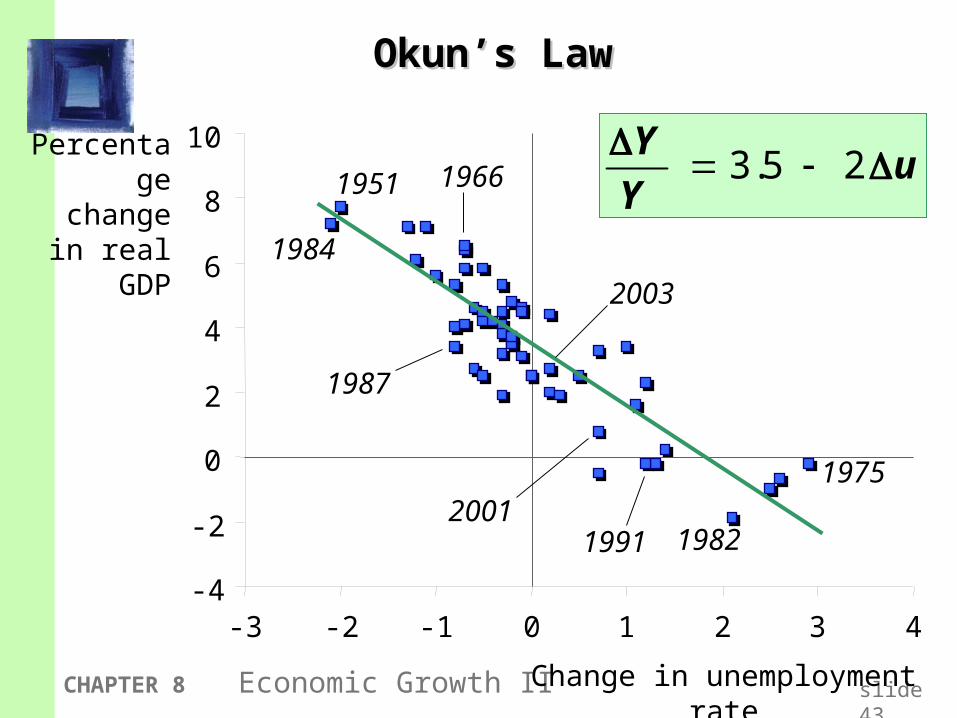

Okun’s Law: the negative relationship between GDP and unemployment.

CHAPTER 8 Economic Growth II slide 40

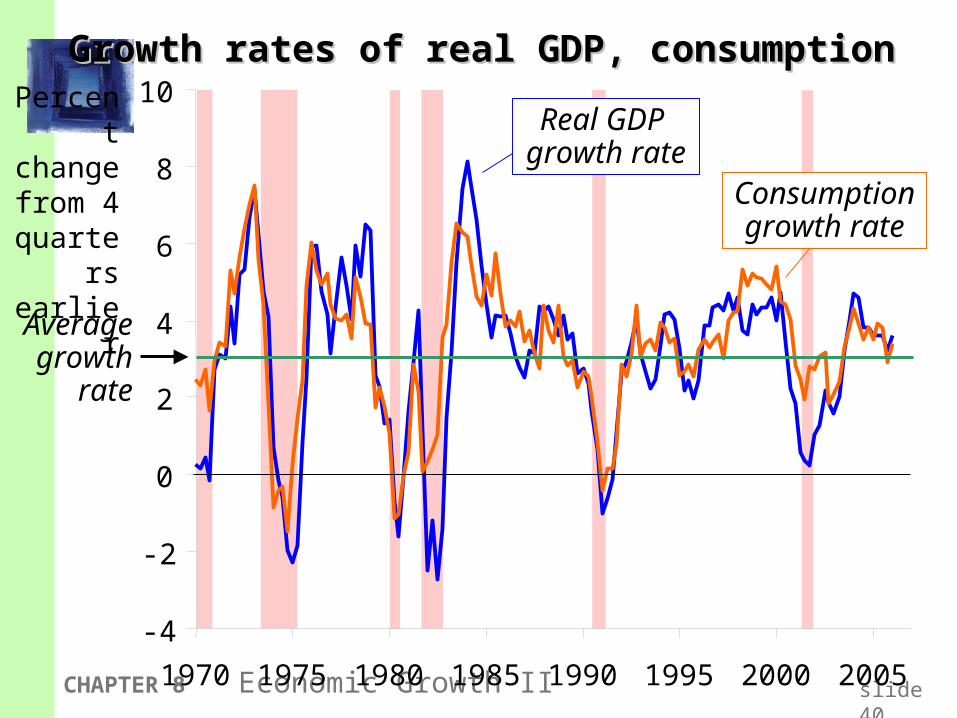

Growth rates of real GDP, consumptionGrowth rates of real GDP, consumption

-4

-2

0

2

4

6

8

10

1970 1975 1980 1985 1990 1995 2000 2005

Real GDP growth rate

Average growth

rate

Consumption growth rate

Percent change from 4

quarters earlier

CHAPTER 8 Economic Growth II slide 41

Growth rates of real GDP, consumption, investmentGrowth rates of real GDP, consumption, investment

-30

-20

-10

0

10

20

30

40

1970 1975 1980 1985 1990 1995 2000 2005

Percent change from 4

quarters earlier

Investment growth rate

Real GDP growth rate

Consumption growth rate

CHAPTER 8 Economic Growth II slide 42

UnemploymentUnemployment

0

2

4

6

8

10

12

1970 1975 1980 1985 1990 1995 2000 2005

Percent of labor

force

CHAPTER 8 Economic Growth II slide 43

Okun’s LawOkun’s Law

Percentage change in real GDP

Change in unemployment rate

-4

-2

0

2

4

6

8

10

-3 -2 -1 0 1 2 3 4

1975

198219912001

1984

1951 1966

2003

1987

3.5 2

Y

uY

CHAPTER 8 Economic Growth II slide 44

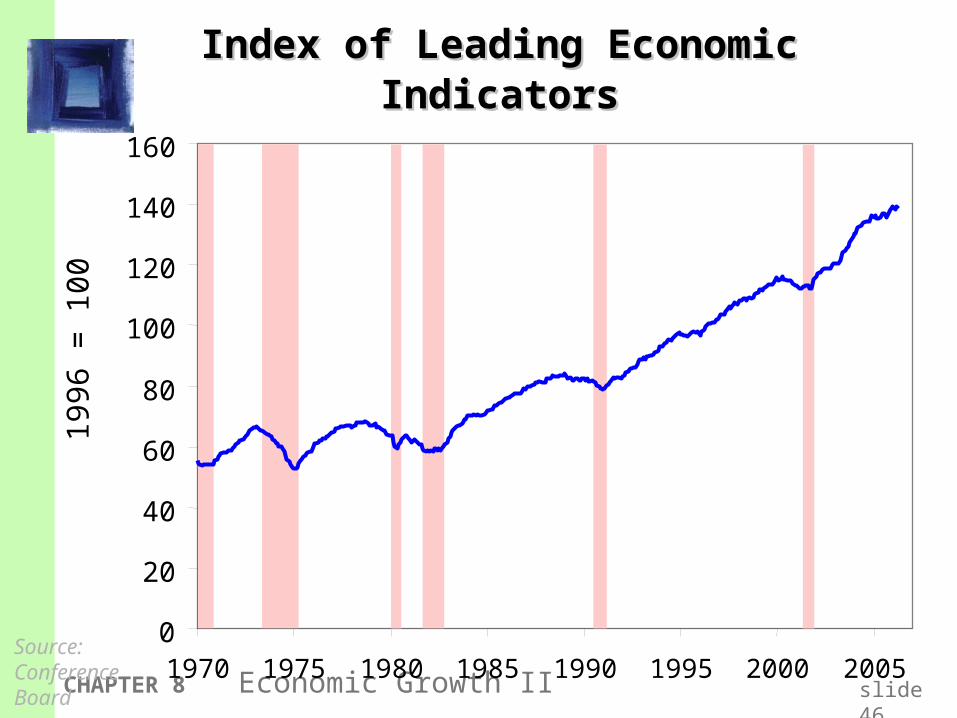

Index of Leading Economic Indicators

Published monthly by the Conference Board.

Aims to forecast changes in economic activity 6-9 months into the future.

Used in planning by businesses and govt, despite not being a perfect predictor.

CHAPTER 8 Economic Growth II slide 45

Components of the LEI index

Average workweek in manufacturing

Initial weekly claims for unemployment insurance

New orders for consumer goods and materials

New orders, nondefense capital goods

Vendor performance

New building permits issued

Index of stock prices

M2

Yield spread (10-year minus 3-month) on Treasuries

Index of consumer expectations

CHAPTER 8 Economic Growth II slide 46

Index of Leading Economic IndicatorsIndex of Leading Economic Indicators

0

20

40

60

80

100

120

140

160

1970 1975 1980 1985 1990 1995 2000 2005

19

96

= 1

00

Source: Conference Board

CHAPTER 8 Economic Growth II slide 47

Time horizons in macroeconomics

Long run: Prices are flexible, respond to changes in supply or demand.

Short run:Many prices are “sticky” at some predetermined level.

The economy behaves much differently when prices are sticky.

CHAPTER 8 Economic Growth II slide 48

Recap of classical macro theory (Chaps. 3-8)

Output is determined by the supply side: supplies of capital, labor technology.

Changes in demand for goods & services (C, I, G ) only affect prices, not quantities.

Assumes complete price flexibility.

Applies to the long run.

CHAPTER 8 Economic Growth II slide 49

When prices are sticky…

…output and employment also depend on demand, which is affected by fiscal policy (G and T ) monetary policy (M ) other factors, like exogenous changes in

C or I.

CHAPTER 8 Economic Growth II slide 50

The Quantity Equation as Aggregate Demand

From Chapter 4, recall the quantity equation

M V = P Y

For given values of M and V, this equation implies an inverse relationship between P and Y :

CHAPTER 8 Economic Growth II slide 51

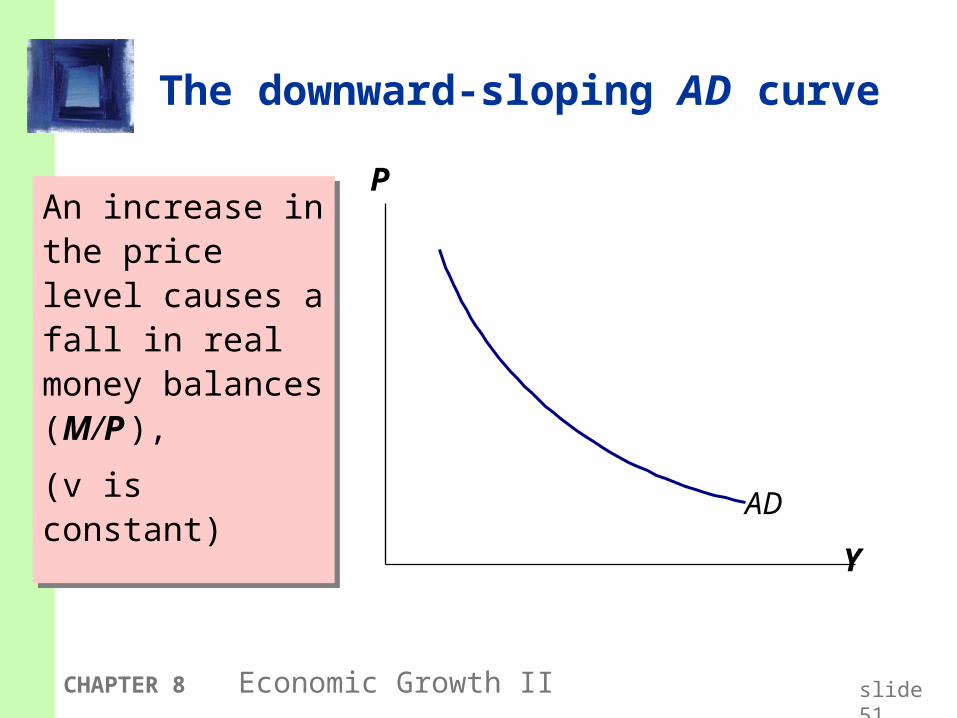

The downward-sloping AD curve

An increase in the price level causes a fall in real money balances (M/P ),

(v is constant)

An increase in the price level causes a fall in real money balances (M/P ),

(v is constant)

Y

P

AD

CHAPTER 8 Economic Growth II slide 52

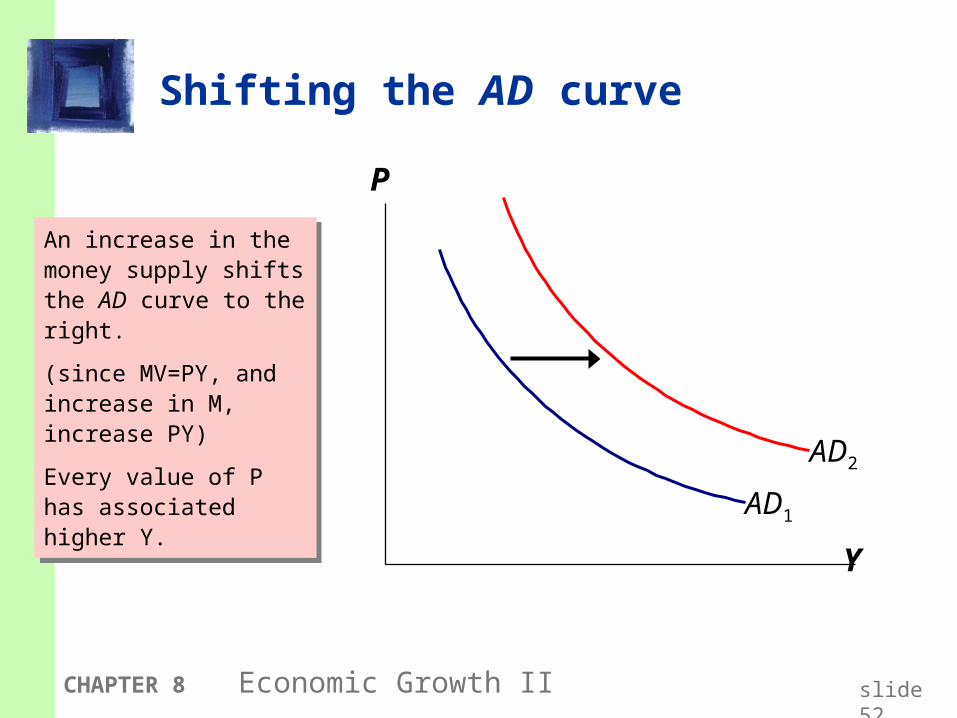

Shifting the AD curve

An increase in the money supply shifts the AD curve to the right.

(since MV=PY, and increase in M, increase PY)

Every value of P has associated higher Y.

An increase in the money supply shifts the AD curve to the right.

(since MV=PY, and increase in M, increase PY)

Every value of P has associated higher Y.

Y

P

AD1

AD2

CHAPTER 8 Economic Growth II slide 53

Aggregate supply in the long run

Recall from Chapter 3: In the long run, output is determined by factor supplies and technology

, ( )Y F K L

is the full-employment or natural level of output, the level of output at which the economy’s resources are fully employed.

Y

“Full employment” means that unemployment equals its natural rate (not zero).

CHAPTER 8 Economic Growth II slide 54

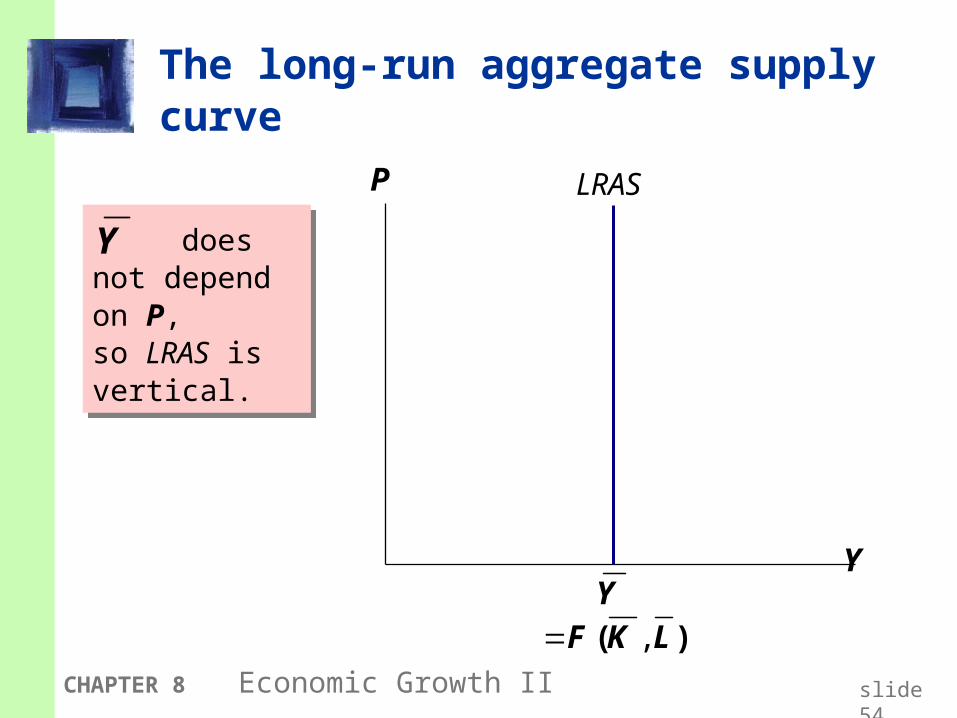

The long-run aggregate supply curve

Y

P LRAS

does not depend on P, so LRAS is vertical.

does not depend on P, so LRAS is vertical.

Y

( ) ,Y

F K L

CHAPTER 8 Economic Growth II slide 55

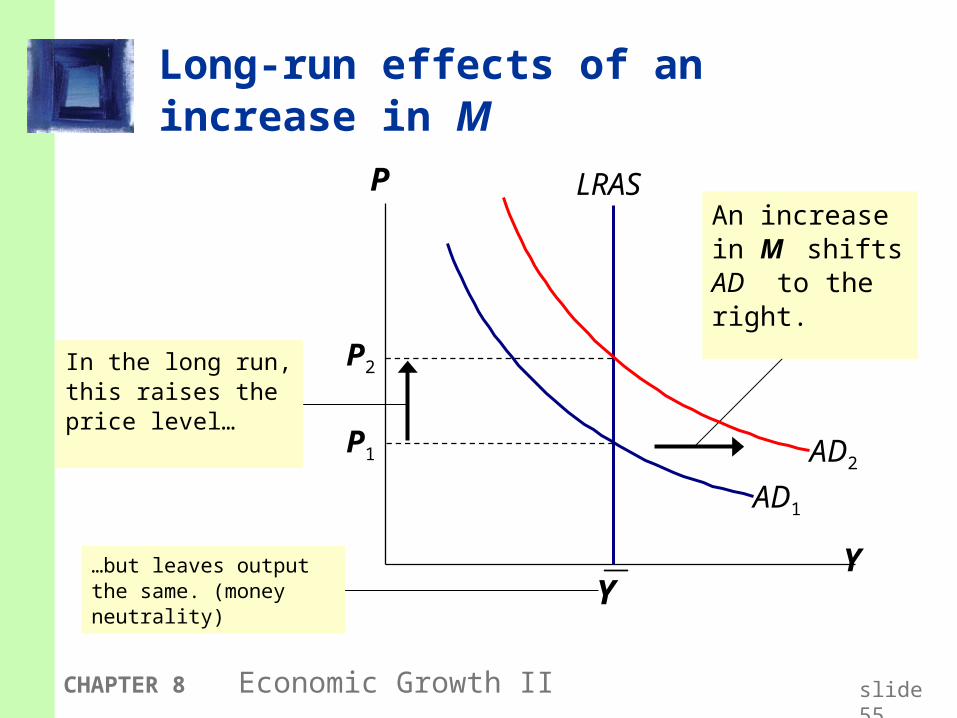

Long-run effects of an increase in M

Y

P

AD1

LRAS

Y

An increase in M shifts AD to the right.

P1

P2In the long run, this raises the price level…

…but leaves output the same. (money neutrality)

AD2

CHAPTER 8 Economic Growth II slide 56

Aggregate supply in the short run

Many prices are sticky in the short run.

For now (and through Chap. 12), we assume all prices are stuck at a predetermined level in

the short run. firms are willing to sell as much at that price

level as their customers are willing to buy.

Therefore, the short-run aggregate supply (SRAS) curve is horizontal:

CHAPTER 8 Economic Growth II slide 57

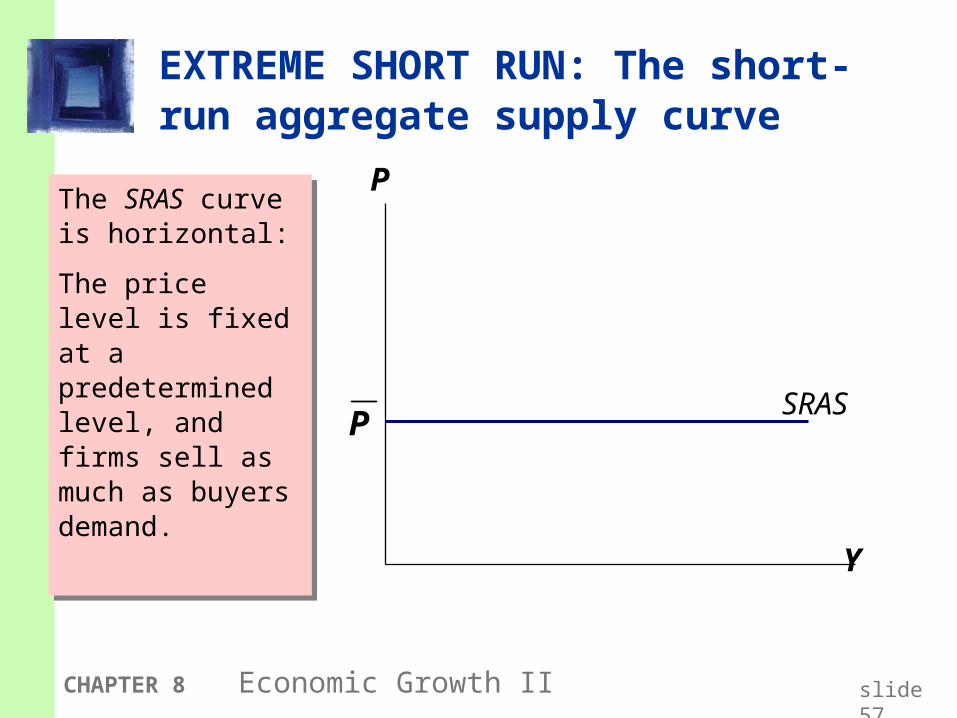

EXTREME SHORT RUN: The short-run aggregate supply curve

Y

P

PSRAS

The SRAS curve is horizontal:

The price level is fixed at a predetermined level, and firms sell as much as buyers demand.

The SRAS curve is horizontal:

The price level is fixed at a predetermined level, and firms sell as much as buyers demand.

CHAPTER 8 Economic Growth II slide 58

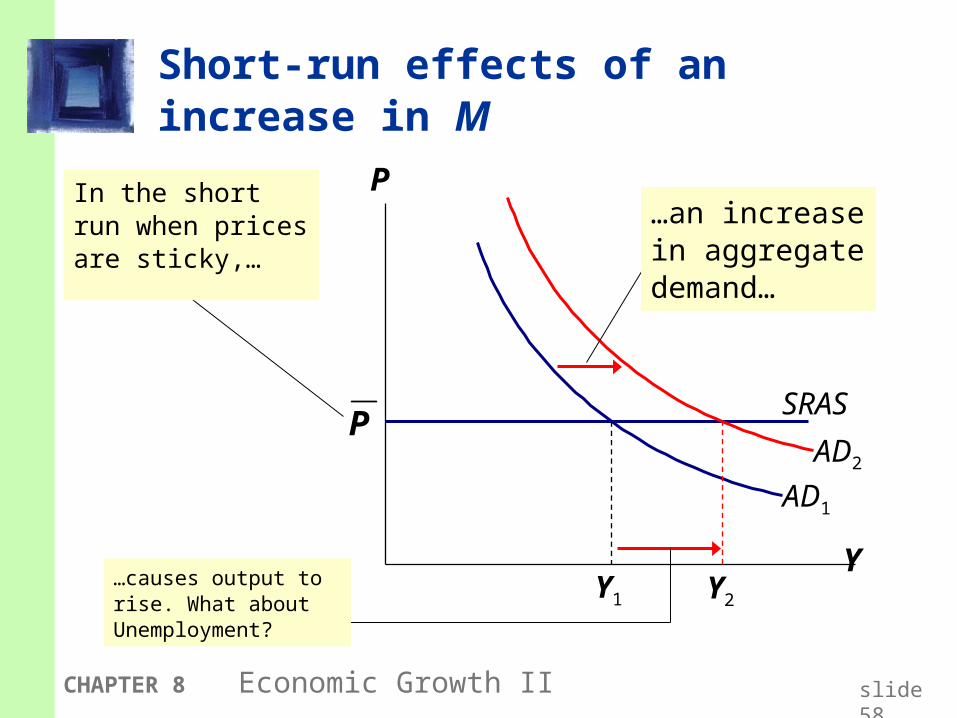

Short-run effects of an increase in M

Y

P

AD1

In the short run when prices are sticky,…

…causes output to rise. What about Unemployment?

PSRAS

Y2Y1

AD2

…an increase in aggregate demand…

CHAPTER 8 Economic Growth II slide 59

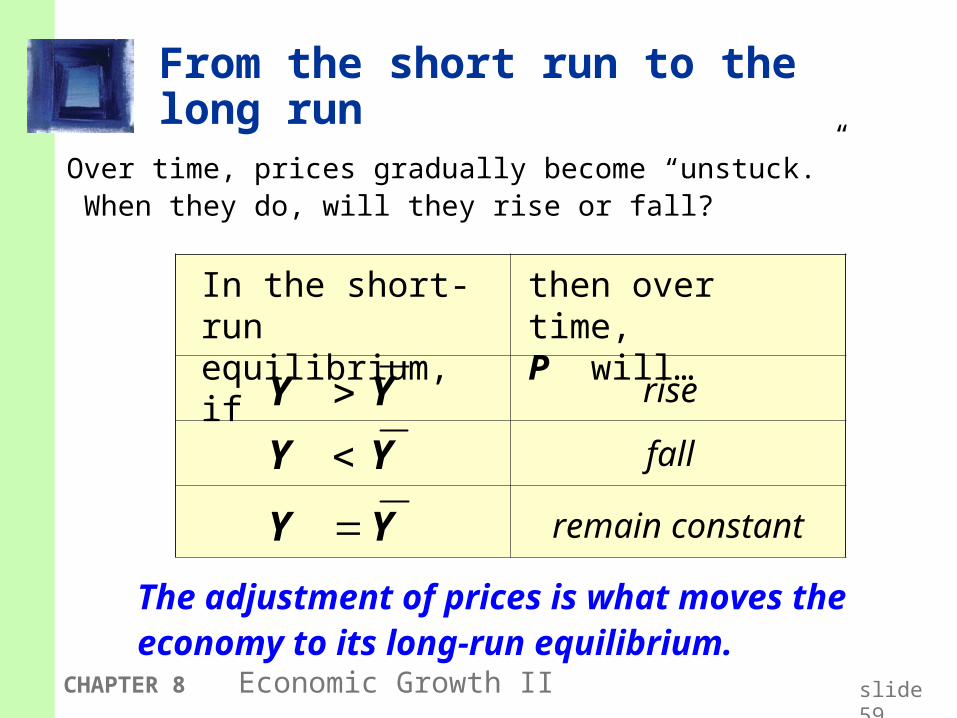

From the short run to the long run

Over time, prices gradually become “unstuck.” When they do, will they rise or fall?

Y Y

Y Y

Y Y

rise

fall

remain constant

In the short-run equilibrium, if

then over time, P will…

The adjustment of prices is what moves the economy to its long-run equilibrium.

CHAPTER 8 Economic Growth II slide 60

The SR & LR effects of M > 0

Y

P

AD1

LRAS

Y

PSRAS

P2

Y2

A = initial equilibrium

AB

CB = new short-

run eq’m after Fed increases M

C = long-run equilibrium

AD2

CHAPTER 8 Economic Growth II slide 61

How shocking!!!

shocks: exogenous changes in agg. supply or demand

Shocks temporarily push the economy away from full employment.

Example: exogenous decrease in velocity

If the money supply is held constant, a decrease in V means people will be using their money in fewer transactions, causing a decrease in demand for goods and services.

CHAPTER 8 Economic Growth II slide 62

PSRAS

LRAS

AD2

The effects of a negative demand shock

Y

P

AD1

Y

P2

Y2

AD shifts left, depressing output and employment in the short run.

AD shifts left, depressing output and employment in the short run.

AB

C

Over time, prices fall and the economy moves down its demand curve toward full-employment.

Over time, prices fall and the economy moves down its demand curve toward full-employment.

CHAPTER 8 Economic Growth II slide 63

Supply shocks

A supply shock alters production costs, affects the prices that firms charge. (also called price shocks)

Examples of adverse supply shocks: Bad weather reduces crop yields, pushing up

food prices. Workers unionize, negotiate wage increases. New environmental regulations require firms to

reduce emissions. Firms charge higher prices to help cover the costs of compliance.

Favorable supply shocks lower costs and prices.

CHAPTER 8 Economic Growth II slide 64

CASE STUDY: The 1970s oil shocks

Early 1970s: OPEC coordinates a reduction in the supply of oil.

Oil prices rose11% in 1973 68% in 1974 16% in 1975

Such sharp oil price increases are supply shocks because they significantly impact production costs and prices.

CHAPTER 8 Economic Growth II slide 65

1P SRAS1

Y

P

AD

LRAS

YY2

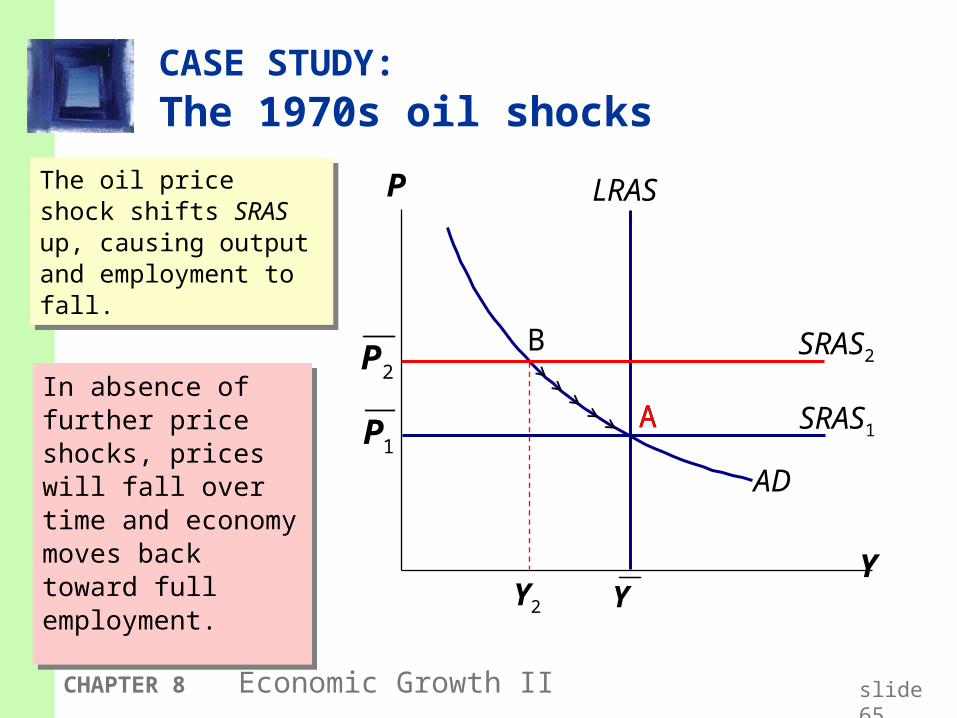

CASE STUDY: The 1970s oil shocks

The oil price shock shifts SRAS up, causing output and employment to fall.

The oil price shock shifts SRAS up, causing output and employment to fall.

A

B

In absence of further price shocks, prices will fall over time and economy moves back toward full employment.

In absence of further price shocks, prices will fall over time and economy moves back toward full employment.

2P SRAS2

A

CHAPTER 8 Economic Growth II slide 66

Stabilization policy

def: policy actions aimed at reducing the severity of short-run economic fluctuations.

Example: Using monetary policy to combat the effects of adverse supply shocks:

CHAPTER 8 Economic Growth II slide 67

Stabilizing output with monetary policy

1P SRAS1

Y

P

AD1

B

A

Y2

LRAS

Y

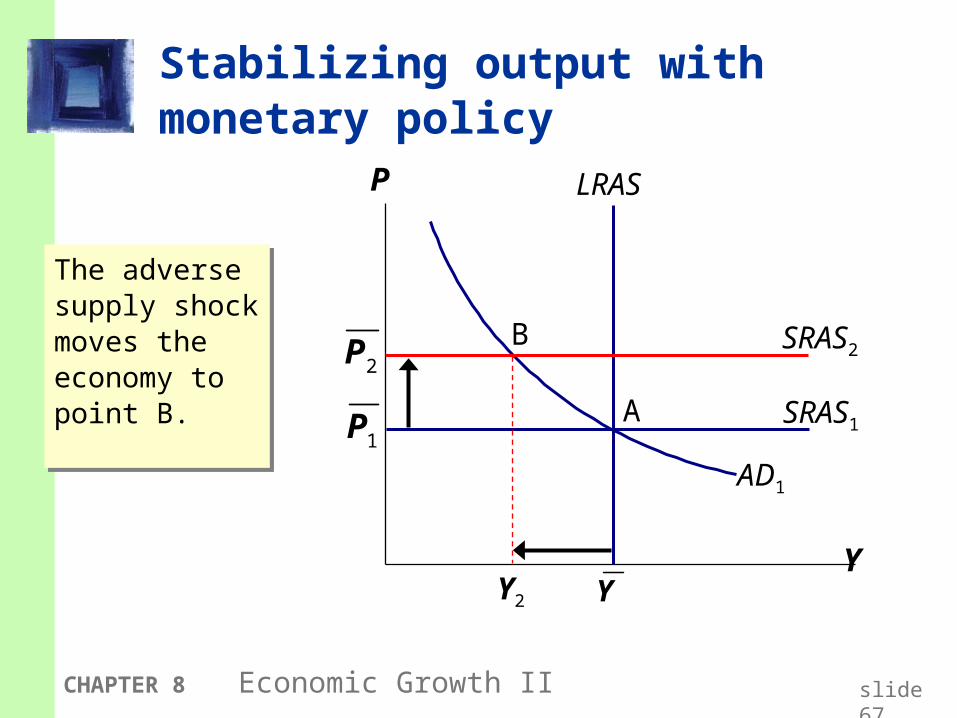

The adverse supply shock moves the economy to point B.

The adverse supply shock moves the economy to point B.

2P SRAS2

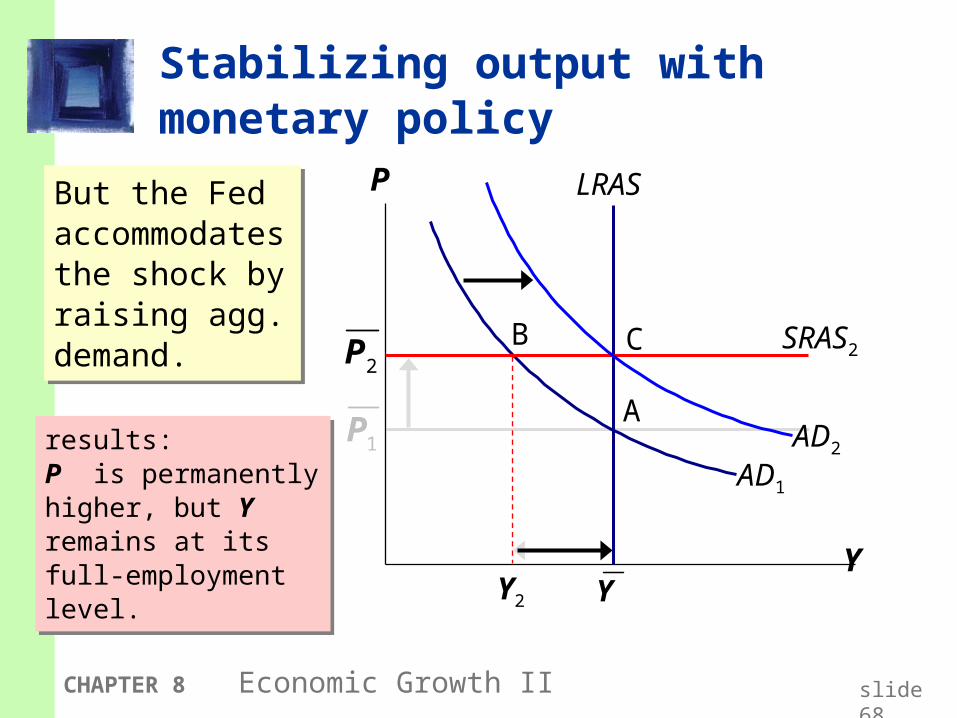

CHAPTER 8 Economic Growth II slide 68

Stabilizing output with monetary policy

1P

Y

P

AD1

B

A

C

Y2

LRAS

Y

But the Fed accommodates the shock by raising agg. demand.

But the Fed accommodates the shock by raising agg. demand.

results: P is permanently higher, but Y remains at its full-employment level.

results: P is permanently higher, but Y remains at its full-employment level.

2P SRAS2

AD2

CHAPTER 8 Economic Growth II slide 69

Chapter SummaryChapter Summary

1. Long run: prices are flexible, output and employment are always at their natural rates, and the classical theory applies.

Short run: prices are sticky, shocks can push output and employment away from their natural rates.

2. Aggregate demand and supply: a framework to analyze economic fluctuations

CHAPTER 9 Introduction to Economic Fluctuations slide 69

CHAPTER 8 Economic Growth II slide 70

Chapter SummaryChapter Summary

3. The aggregate demand curve slopes downward.

4. The long-run aggregate supply curve is vertical, because output depends on technology and factor supplies, but not prices.

5. The short-run aggregate supply curve is horizontal, because prices are sticky at predetermined levels.

CHAPTER 9 Introduction to Economic Fluctuations slide 70

CHAPTER 8 Economic Growth II slide 71

Chapter SummaryChapter Summary

6. Shocks to aggregate demand and supply cause fluctuations in GDP and employment in the short run.

7. The Fed can attempt to stabilize the economy with monetary policy.

CHAPTER 9 Introduction to Economic Fluctuations slide 71

MMACROECONOMICSACROECONOMICS

C H A P T E R

Aggregate Demand I:Building the IS -LM Model

10

CHAPTER 8 Economic Growth II slide 73

In this chapter, you will learn…

the IS curve, and its relation to the Keynesian cross the loanable funds model

the LM curve, and its relation to the theory of liquidity preference

how the IS-LM model determines income and the interest rate in the short run when P is fixed

CHAPTER 8 Economic Growth II slide 74

Context

Chapter 9 introduced the model of aggregate demand and aggregate supply.

Long run prices flexible output determined by factors of production &

technology unemployment equals its natural rate

Short run prices fixed output determined by aggregate demand unemployment negatively related to output

CHAPTER 8 Economic Growth II slide 75

Context

This chapter develops the IS-LM model, the basis of the aggregate demand curve.

We focus on the short run and assume the price level is fixed (so, SRAS curve is horizontal).

This chapter (and chapter 11) focus on the closed-economy case. Chapter 12 presents the open-economy case.

CHAPTER 8 Economic Growth II slide 76

The Keynesian Cross

A simple closed economy model in which income is determined by expenditure. (due to J.M. Keynes)

Notation:

I = planned investment

E = C + I + G = planned expenditure

Y = real GDP = actual expenditure

Difference between actual & planned expenditure = unplanned inventory investment

CHAPTER 8 Economic Growth II slide 77

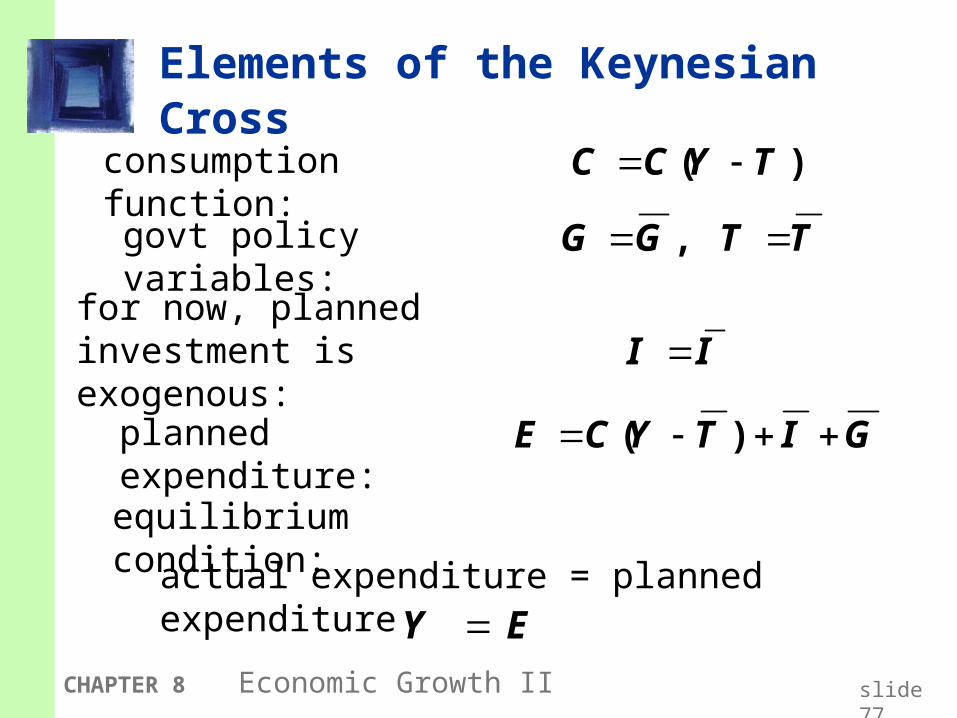

Elements of the Keynesian Cross

( )C C Y T

I I

,G G T T

( )E C Y T I G

Y E

consumption function:

for now, plannedinvestment is exogenous:

planned expenditure:

equilibrium condition:

govt policy variables:

actual expenditure = planned expenditure

CHAPTER 8 Economic Growth II slide 78

Graphing planned expenditure

income, output, Y

E

planned

expenditure

E =C +I +G

MPC1

CHAPTER 8 Economic Growth II slide 79

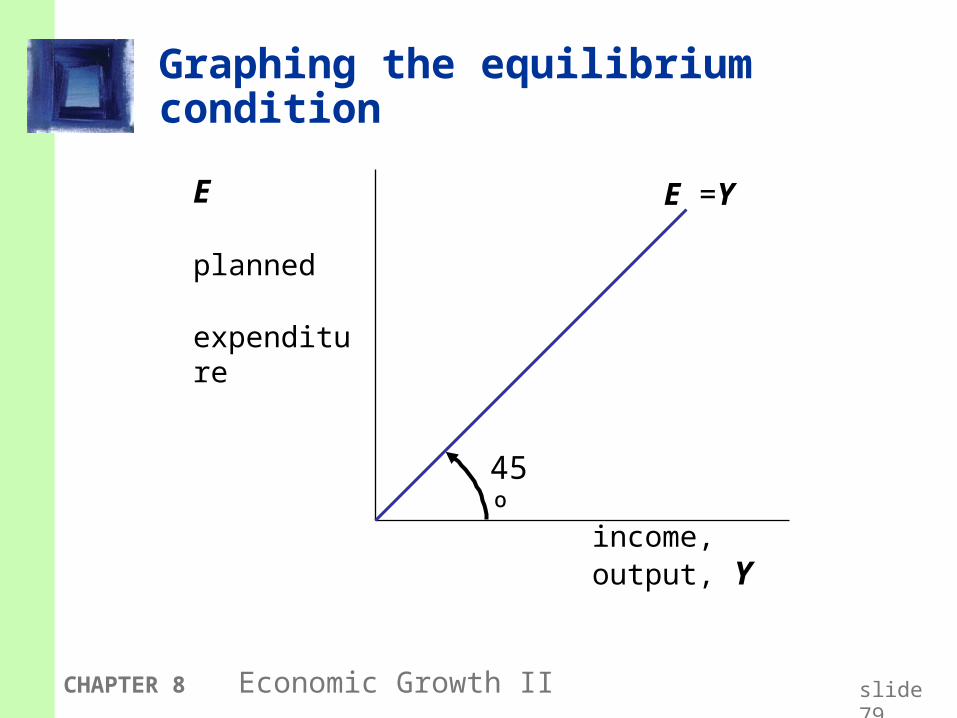

Graphing the equilibrium condition

income, output, Y

E

planned

expenditure

E =Y

45º

CHAPTER 8 Economic Growth II slide 80

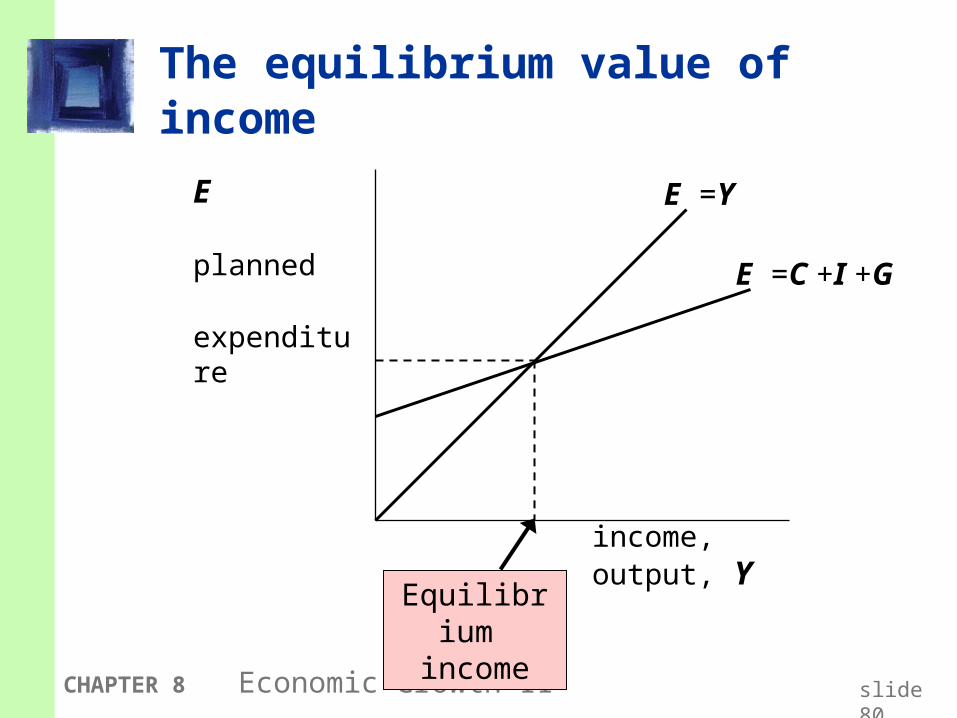

The equilibrium value of income

income, output, Y

E

planned

expenditure

E =Y

E =C +I +G

Equilibrium income

CHAPTER 8 Economic Growth II slide 81

An increase in government purchases

Y

E

E =Y

E =C +I +G1

E1 = Y1

E =C +I +G2

E2 = Y2Y

At Y1,

there is now an unplanned drop in inventory…

…so firms increase output, and income rises toward a new equilibrium.

G

CHAPTER 8 Economic Growth II slide 82

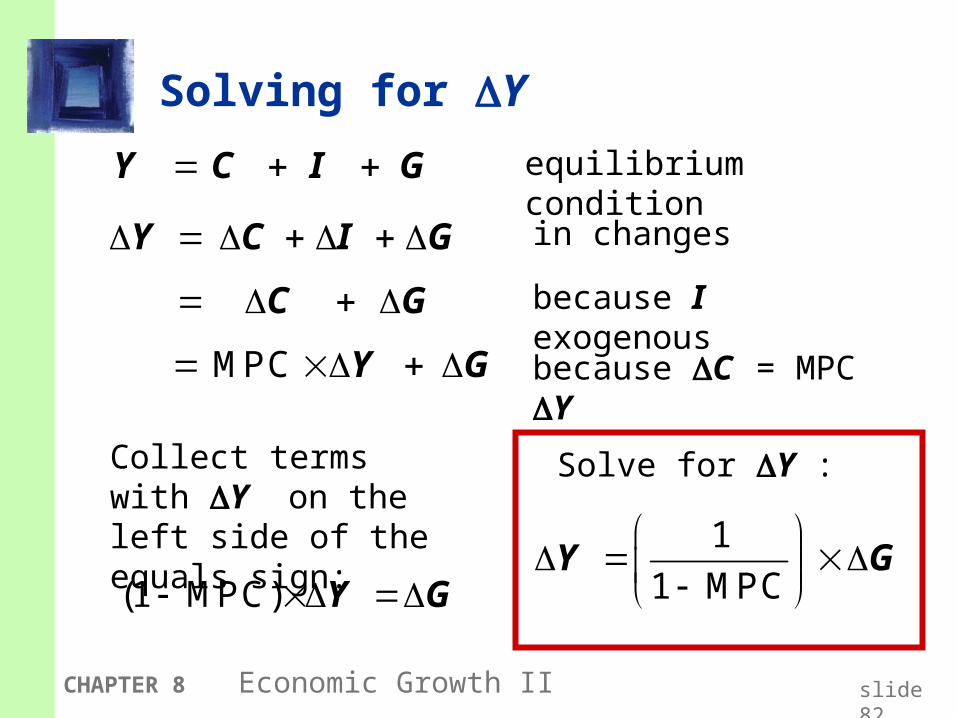

Solving for Y

Y C I G

Y C I G

MPC Y G

C G

(1 MPC) Y G

1

1 MPC

Y G

equilibrium condition

in changes

because I exogenous

because C = MPC

Y

Collect terms with Y on the left side of the equals sign:

Solve for Y :

CHAPTER 8 Economic Growth II slide 83

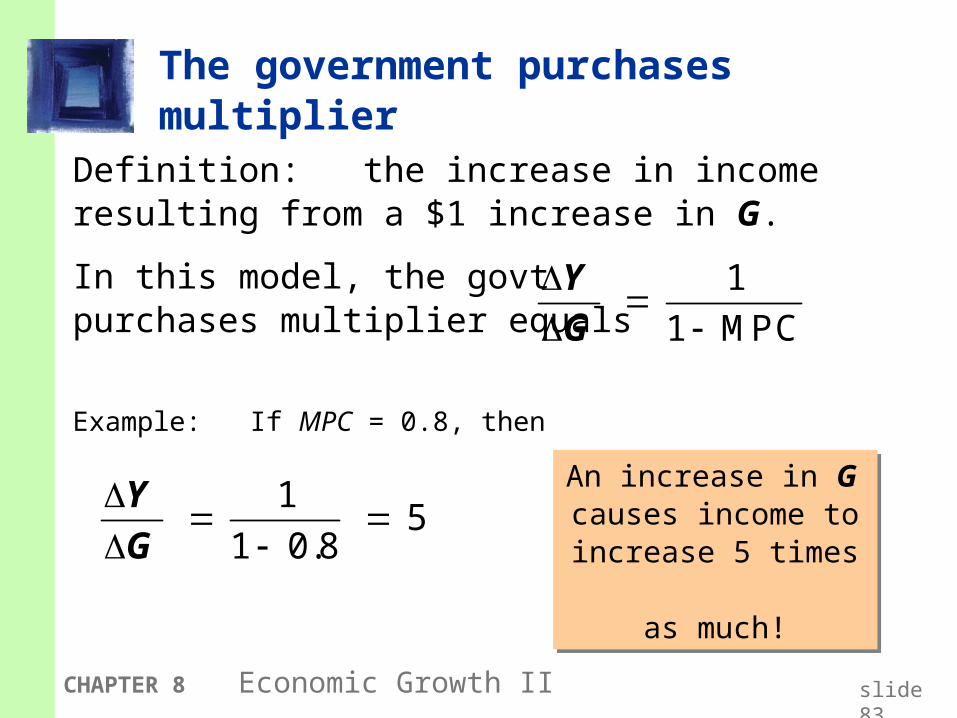

The government purchases multiplier

Example: If MPC = 0.8, then

Definition: the increase in income resulting from a $1 increase in G.

In this model, the govt purchases multiplier equals

1

1 MPC

YG

15

1 0.8

YG

An increase in G causes income to increase 5 times

as much!

An increase in G causes income to increase 5 times

as much!

CHAPTER 8 Economic Growth II slide 84

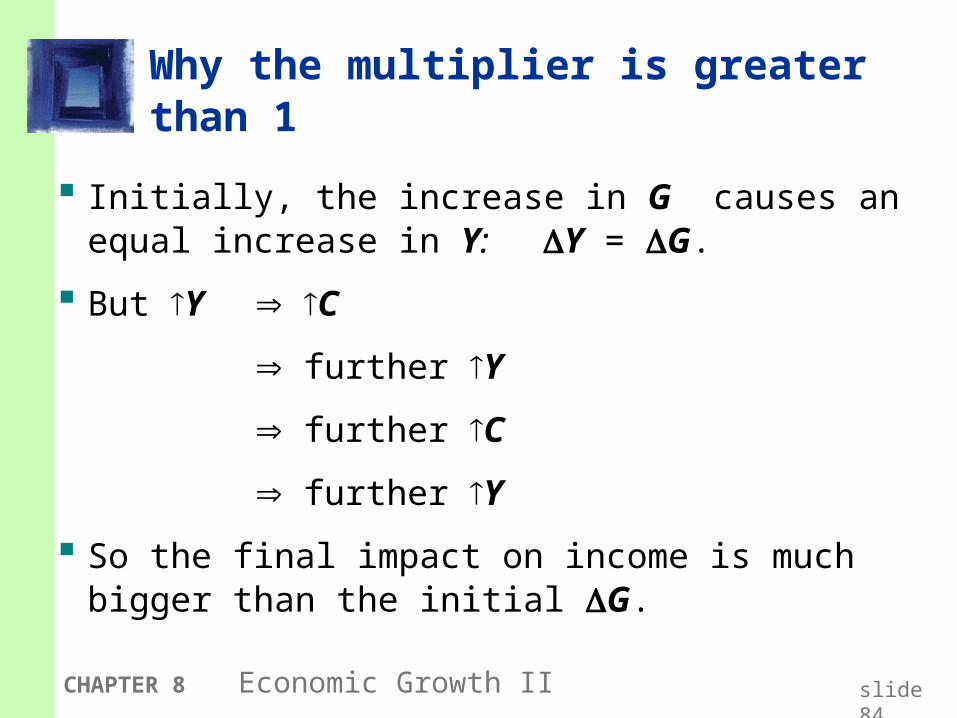

Why the multiplier is greater than 1

Initially, the increase in G causes an equal increase in Y: Y = G.

But Y C

further Y

further C

further Y

So the final impact on income is much bigger than the initial G.