Embed Size (px)

Citation preview

CA. PRAMOD JAINFCA, FCS, FCMA, LL.B, MIMA, DISA

CA. PRAMOD JAINFCA, FCS, FCMA, LL.B, MIMA, DISA

LUNAWAT & CO.Chartered Accountants

LUNAWAT & CO.Chartered Accountants11th December 201411th December 2014

Overview with Schedule IIIOverview with Schedule IIIOverview with Schedule IIIOverview with Schedule IIIOverview with Schedule IIIOverview with Schedule IIIOverview with Schedule IIIOverview with Schedule III

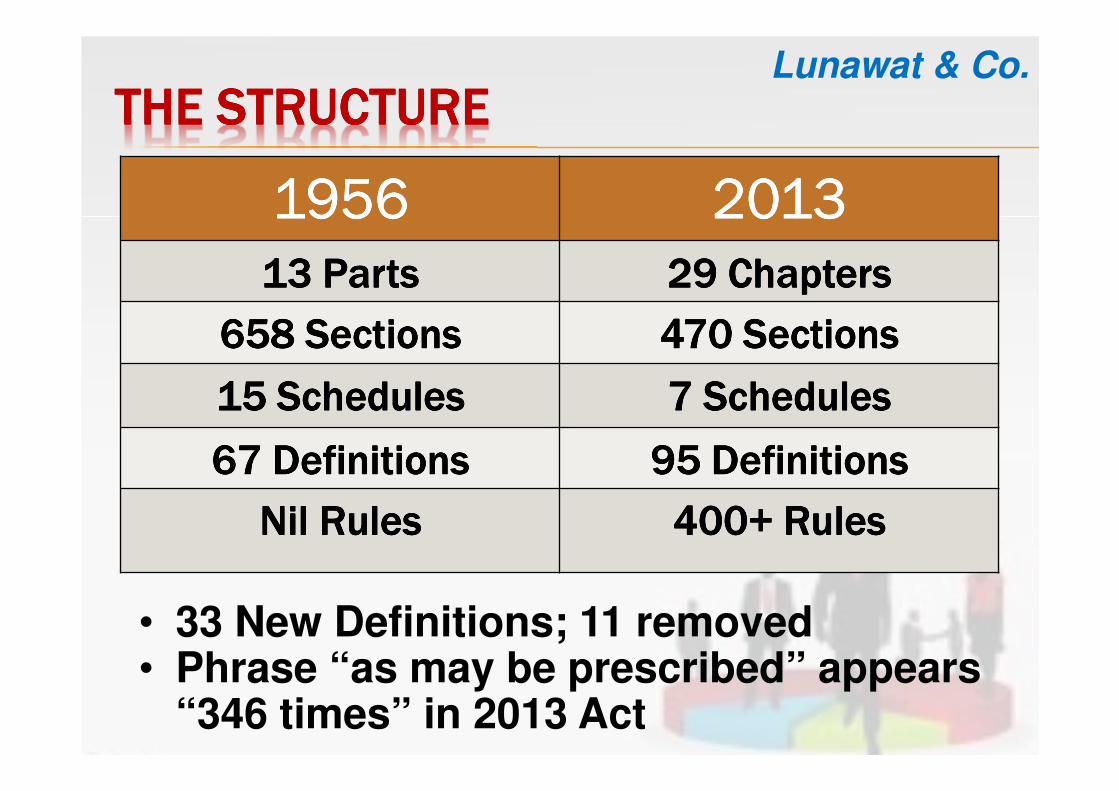

THE STRUCTURETHE STRUCTURETHE STRUCTURETHE STRUCTURE

1956195619561956 2013201320132013

13 Parts13 Parts13 Parts13 Parts 29 Chapters29 Chapters29 Chapters29 Chapters

658 Sections658 Sections658 Sections658 Sections 470 Sections470 Sections470 Sections470 Sections

15 Schedules15 Schedules15 Schedules15 Schedules 7 Schedules7 Schedules7 Schedules7 Schedules

67 Definitions67 Definitions67 Definitions67 Definitions 95 Definitions95 Definitions95 Definitions95 Definitions

Nil RulesNil RulesNil RulesNil Rules 400+ Rules400+ Rules400+ Rules400+ Rules

Lunawat & Co.

• 33 New Definitions; 11 removed• Phrase “as may be prescribed” appears

“346 times” in 2013 Act

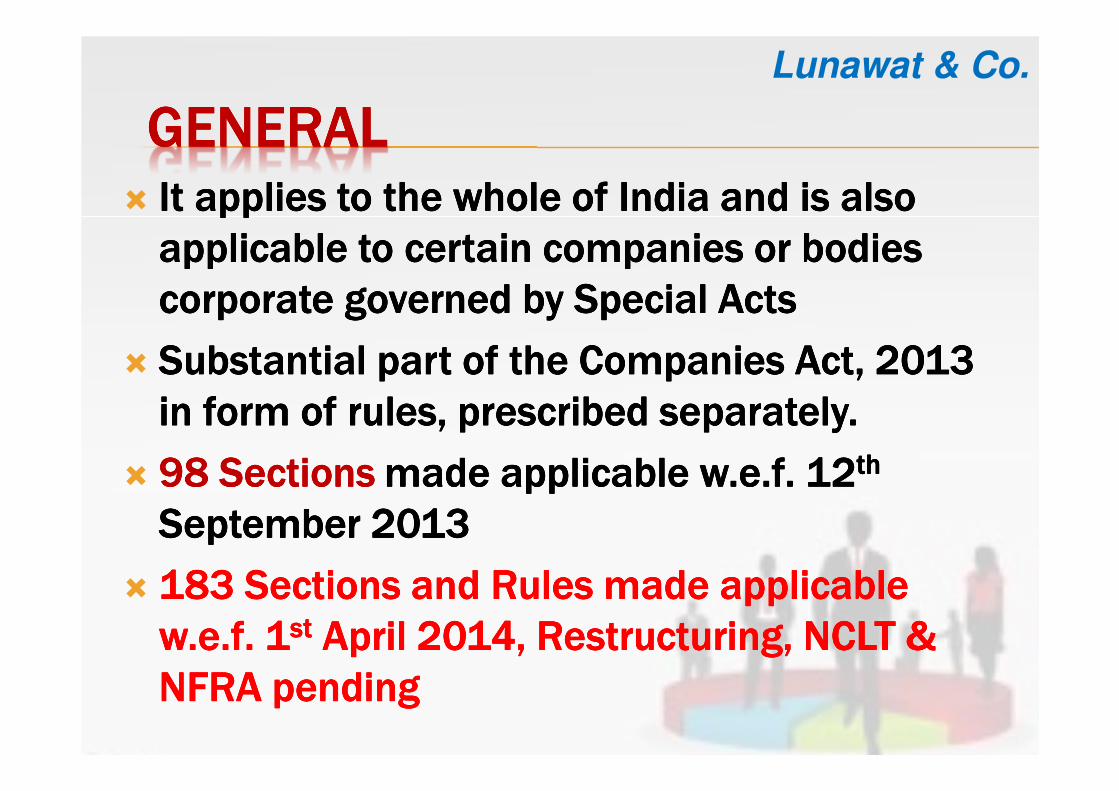

GENERALGENERALGENERALGENERAL� It applies to the whole of India and is also It applies to the whole of India and is also It applies to the whole of India and is also It applies to the whole of India and is also

applicable to certain companies or bodies applicable to certain companies or bodies applicable to certain companies or bodies applicable to certain companies or bodies

corporate governed by Special Actscorporate governed by Special Actscorporate governed by Special Actscorporate governed by Special Acts

� Substantial part of the Companies Act, 2013 Substantial part of the Companies Act, 2013 Substantial part of the Companies Act, 2013 Substantial part of the Companies Act, 2013

in form of rules, prescribed separately.in form of rules, prescribed separately.in form of rules, prescribed separately.in form of rules, prescribed separately.

� 98 Sections98 Sections98 Sections98 Sections made applicable made applicable made applicable made applicable w.e.fw.e.fw.e.fw.e.f. 12. 12. 12. 12thththth

September 2013September 2013September 2013September 2013

� 183 Sections and Rules made applicable 183 Sections and Rules made applicable 183 Sections and Rules made applicable 183 Sections and Rules made applicable

w.e.fw.e.fw.e.fw.e.f. 1. 1. 1. 1stststst April 2014, Restructuring, NCLT & April 2014, Restructuring, NCLT & April 2014, Restructuring, NCLT & April 2014, Restructuring, NCLT &

NFRA pendingNFRA pendingNFRA pendingNFRA pending

Lunawat & Co.

Lunawat & Co.

Public PrivateCompany

NEW PROVISIONSNEW PROVISIONSNEW PROVISIONSNEW PROVISIONS

� OPCOPCOPCOPC

� Small Co.Small Co.Small Co.Small Co.

� Dormant CoDormant CoDormant CoDormant Co

� NCLT & NCALTNCLT & NCALTNCLT & NCALTNCLT & NCALT

� CSRCSRCSRCSR

� NFRANFRANFRANFRA

� Registered Registered Registered Registered ValuersValuersValuersValuers

� FraudFraudFraudFraud

Lunawat & Co.

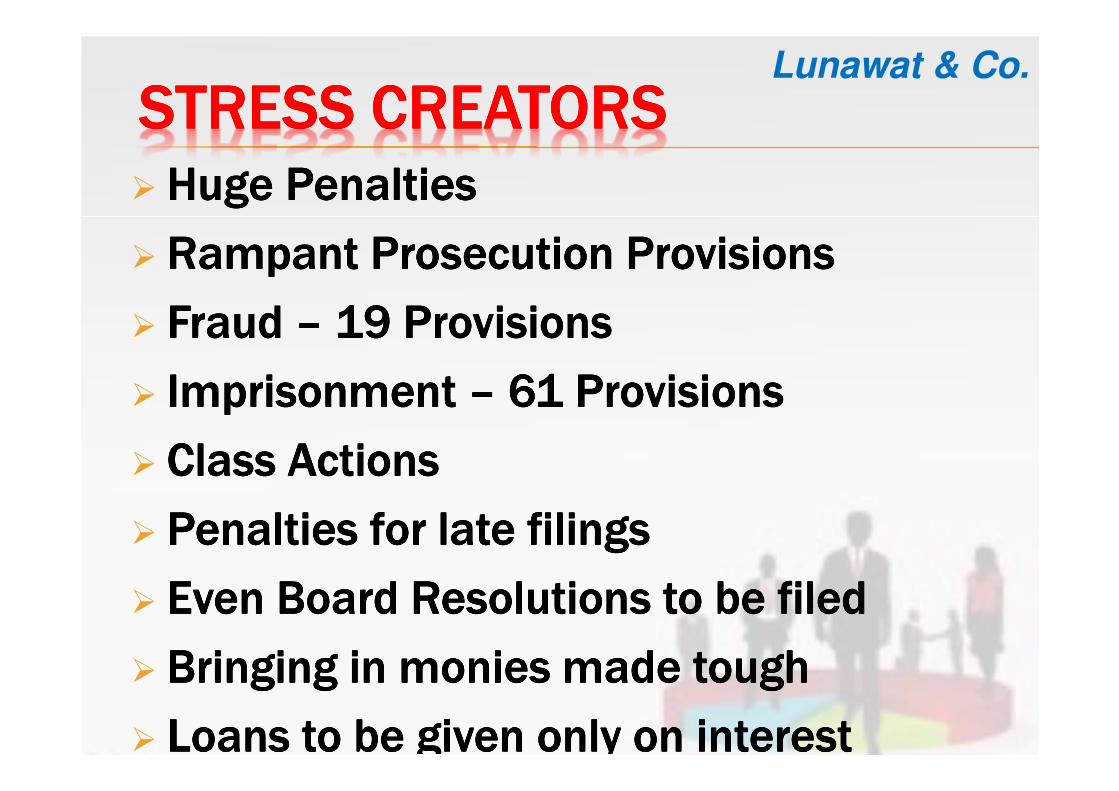

STRESS CREATORSSTRESS CREATORSSTRESS CREATORSSTRESS CREATORS� Huge Penalties Huge Penalties Huge Penalties Huge Penalties

� Rampant Prosecution ProvisionsRampant Prosecution ProvisionsRampant Prosecution ProvisionsRampant Prosecution Provisions

� Fraud Fraud Fraud Fraud –––– 19 Provisions19 Provisions19 Provisions19 Provisions

� Imprisonment Imprisonment Imprisonment Imprisonment –––– 61 Provisions61 Provisions61 Provisions61 Provisions

� Class ActionsClass ActionsClass ActionsClass Actions

� Penalties for late filingsPenalties for late filingsPenalties for late filingsPenalties for late filings

� Even Board Resolutions to be filedEven Board Resolutions to be filedEven Board Resolutions to be filedEven Board Resolutions to be filed

� Bringing in monies made toughBringing in monies made toughBringing in monies made toughBringing in monies made tough

� Loans to be given only on interestLoans to be given only on interestLoans to be given only on interestLoans to be given only on interest

Lunawat & Co.

STRESS CREATORSSTRESS CREATORSSTRESS CREATORSSTRESS CREATORS� Detailed Annual Returns Detailed Annual Returns Detailed Annual Returns Detailed Annual Returns

� Detailed Directors Reports Detailed Directors Reports Detailed Directors Reports Detailed Directors Reports

� SA compliance made mandatory for SA compliance made mandatory for SA compliance made mandatory for SA compliance made mandatory for

auditorsauditorsauditorsauditors

� Director duties Director duties Director duties Director duties –––– conflict of interestconflict of interestconflict of interestconflict of interest

� Hosting on Website made mandatory Hosting on Website made mandatory Hosting on Website made mandatory Hosting on Website made mandatory ––––

17 17 17 17 provisions including:provisions including:provisions including:provisions including:

� Closure of members RegisterClosure of members RegisterClosure of members RegisterClosure of members Register

� GM noticeGM noticeGM noticeGM notice

� Director ResignationDirector ResignationDirector ResignationDirector Resignation

Lunawat & Co.

OPPORTUNITIESOPPORTUNITIESOPPORTUNITIESOPPORTUNITIES

�Women DirectorsWomen DirectorsWomen DirectorsWomen Directors

� Independent DirectorsIndependent DirectorsIndependent DirectorsIndependent Directors

�Resident DirectorsResident DirectorsResident DirectorsResident Directors

�Registered Registered Registered Registered ValuersValuersValuersValuers

�OPCOPCOPCOPC & Dormant Cos& Dormant Cos& Dormant Cos& Dormant Cos

�NCLT & NCALTNCLT & NCALTNCLT & NCALTNCLT & NCALT

�Cash Flow StatementCash Flow StatementCash Flow StatementCash Flow Statement

�Consolidated Financial Consolidated Financial Consolidated Financial Consolidated Financial StatementsStatementsStatementsStatements

Lunawat & Co.

OPPORTUNITIESOPPORTUNITIESOPPORTUNITIESOPPORTUNITIES

� Internal Internal Internal Internal AuditAuditAuditAudit

�Fixed Asset Registers to ascertain Fixed Asset Registers to ascertain Fixed Asset Registers to ascertain Fixed Asset Registers to ascertain

actual life of each assetactual life of each assetactual life of each assetactual life of each asset

� Internal Financial Control SystemsInternal Financial Control SystemsInternal Financial Control SystemsInternal Financial Control Systems

�Secretarial Records and compliance Secretarial Records and compliance Secretarial Records and compliance Secretarial Records and compliance

auditsauditsauditsaudits

�Fast Track MergerFast Track MergerFast Track MergerFast Track Merger

�Conversion into LLPConversion into LLPConversion into LLPConversion into LLP

Lunawat & Co.

Lunawat & Co.

BOOKSBOOKSBOOKSBOOKS� Permits the maintenance of books of a/Permits the maintenance of books of a/Permits the maintenance of books of a/Permits the maintenance of books of a/cscscscs & & & &

other books & papers in electronic mode other books & papers in electronic mode other books & papers in electronic mode other books & papers in electronic mode

� Shall remain accessible in India Shall remain accessible in India Shall remain accessible in India Shall remain accessible in India

�RRRRetained etained etained etained completely in the format in which they were completely in the format in which they were completely in the format in which they were completely in the format in which they were

originally generated, sent or originally generated, sent or originally generated, sent or originally generated, sent or receivedreceivedreceivedreceived

� Back up to kept in server located in IndiaBack up to kept in server located in IndiaBack up to kept in server located in IndiaBack up to kept in server located in India

� To intimate to ROC along with FSTo intimate to ROC along with FSTo intimate to ROC along with FSTo intimate to ROC along with FS

�Name Name Name Name of the service provider; of the service provider; of the service provider; of the service provider;

� IP IP IP IP address of service provider; address of service provider; address of service provider; address of service provider;

�Location Location Location Location of the service provider (wherever applicable); of the service provider (wherever applicable); of the service provider (wherever applicable); of the service provider (wherever applicable);

�Where Where Where Where the books the books the books the books maintained maintained maintained maintained on cloud, such address as on cloud, such address as on cloud, such address as on cloud, such address as

provided by the service provider. provided by the service provider. provided by the service provider. provided by the service provider.

Lunawat & Co.

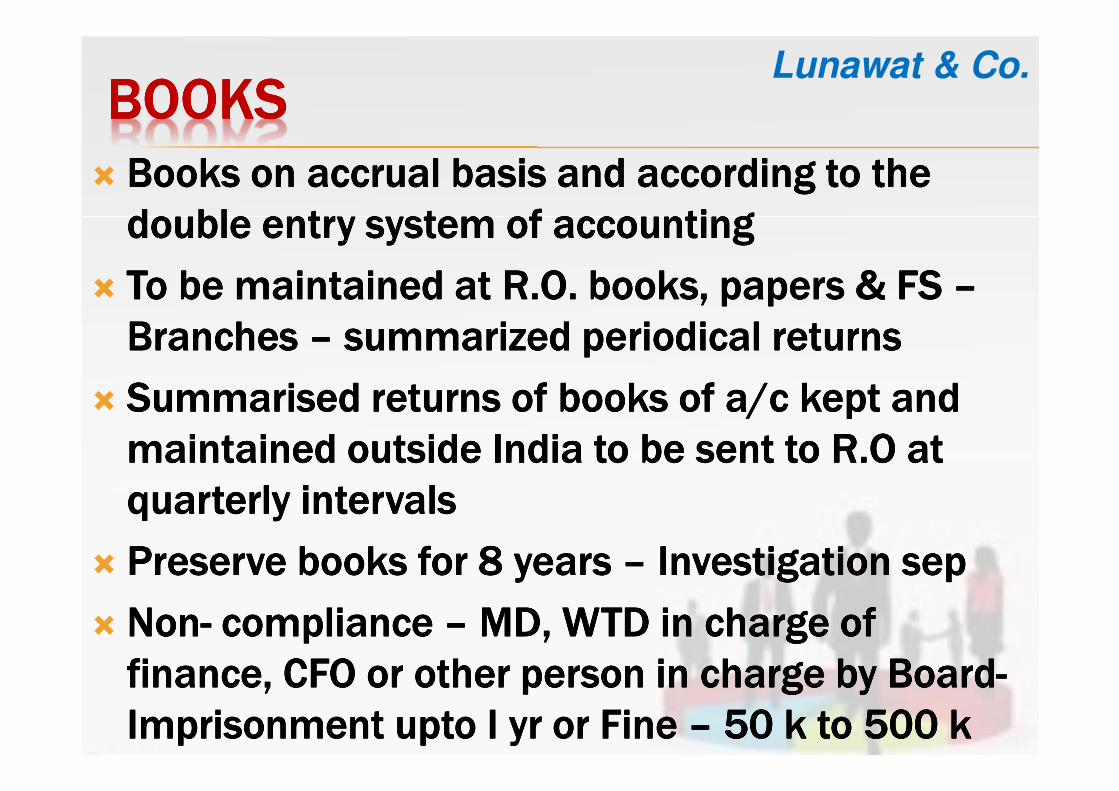

BOOKSBOOKSBOOKSBOOKS

� Books on accrual basis and according to the Books on accrual basis and according to the Books on accrual basis and according to the Books on accrual basis and according to the

double entry system of accountingdouble entry system of accountingdouble entry system of accountingdouble entry system of accounting

� To be maintained at R.O. books, papers & FS To be maintained at R.O. books, papers & FS To be maintained at R.O. books, papers & FS To be maintained at R.O. books, papers & FS ––––

Branches Branches Branches Branches –––– summarized periodical returnssummarized periodical returnssummarized periodical returnssummarized periodical returns

� SSSSummarised ummarised ummarised ummarised returns of returns of returns of returns of books books books books of of of of a/c kept a/c kept a/c kept a/c kept and and and and

maintained outside India maintained outside India maintained outside India maintained outside India to to to to be sent to be sent to be sent to be sent to R.O R.O R.O R.O at at at at

quarterly intervals quarterly intervals quarterly intervals quarterly intervals

� Preserve books for 8 years Preserve books for 8 years Preserve books for 8 years Preserve books for 8 years –––– Investigation Investigation Investigation Investigation sepsepsepsep

� NonNonNonNon---- compliance compliance compliance compliance –––– MD, WTD in charge of MD, WTD in charge of MD, WTD in charge of MD, WTD in charge of

finance, CFO or other person in charge by Boardfinance, CFO or other person in charge by Boardfinance, CFO or other person in charge by Boardfinance, CFO or other person in charge by Board----

Imprisonment Imprisonment Imprisonment Imprisonment uptouptouptoupto I I I I yryryryr or Fine or Fine or Fine or Fine –––– 50 k to 500 k50 k to 500 k50 k to 500 k50 k to 500 k

Lunawat & Co.

FINANCIAL STATEMENTSFINANCIAL STATEMENTSFINANCIAL STATEMENTSFINANCIAL STATEMENTS

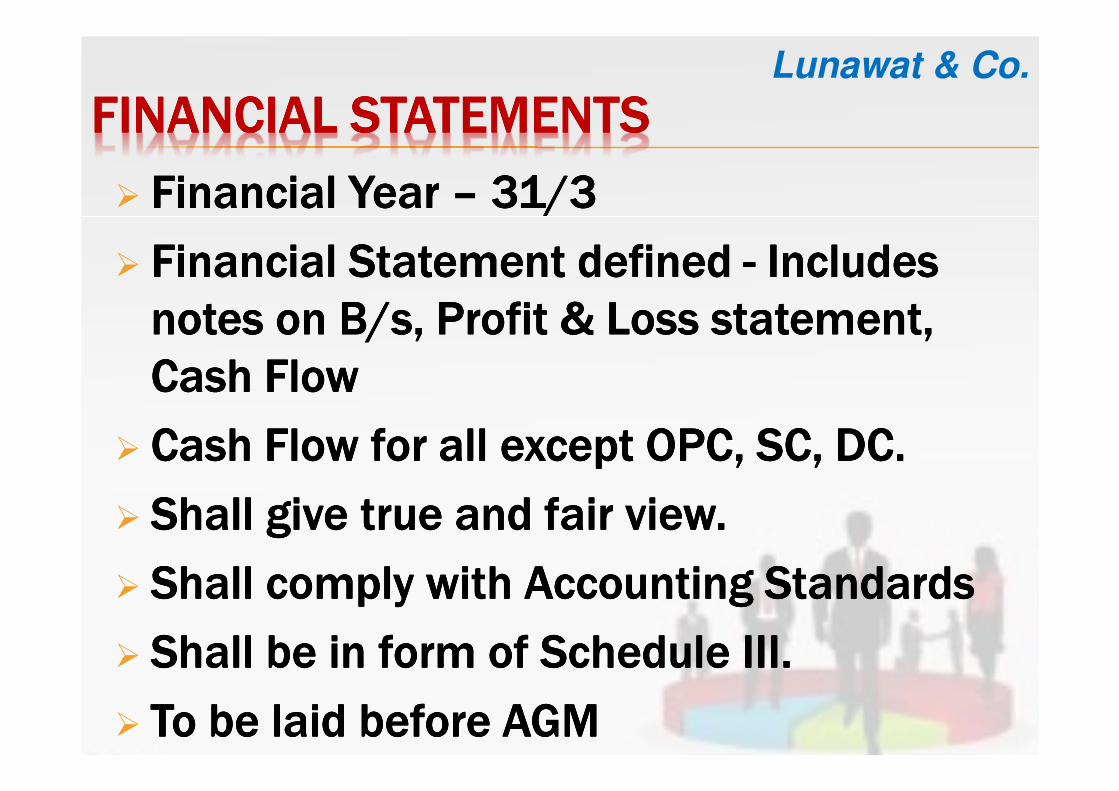

� Financial Year Financial Year Financial Year Financial Year –––– 31/331/331/331/3

� Financial Statement defined Financial Statement defined Financial Statement defined Financial Statement defined ---- Includes Includes Includes Includes

notes on B/s, Profit & Loss statement, notes on B/s, Profit & Loss statement, notes on B/s, Profit & Loss statement, notes on B/s, Profit & Loss statement,

Cash FlowCash FlowCash FlowCash Flow

� Cash Flow for all except OPC, SC, DC. Cash Flow for all except OPC, SC, DC. Cash Flow for all except OPC, SC, DC. Cash Flow for all except OPC, SC, DC.

� Shall give true and fair view.Shall give true and fair view.Shall give true and fair view.Shall give true and fair view.

� Shall comply with Accounting StandardsShall comply with Accounting StandardsShall comply with Accounting StandardsShall comply with Accounting Standards

� Shall be in form of Schedule III.Shall be in form of Schedule III.Shall be in form of Schedule III.Shall be in form of Schedule III.

� To be laid before AGMTo be laid before AGMTo be laid before AGMTo be laid before AGM

Lunawat & Co.

FINANCIAL STATEMENTSFINANCIAL STATEMENTSFINANCIAL STATEMENTSFINANCIAL STATEMENTS

� Has to be AS compliant:Has to be AS compliant:Has to be AS compliant:Has to be AS compliant:

� FS to disclose deviation from ASFS to disclose deviation from ASFS to disclose deviation from ASFS to disclose deviation from AS

�Reason for deviationReason for deviationReason for deviationReason for deviation

� Financial effect arising of deviation Financial effect arising of deviation Financial effect arising of deviation Financial effect arising of deviation

� NonNonNonNon---- compliancecompliancecompliancecompliance

�MD, MD, MD, MD,

�WTD WTD WTD WTD inchargeinchargeinchargeincharge of financeof financeof financeof finance

� CFOCFOCFOCFO

� Any other person charged by Board Any other person charged by Board Any other person charged by Board Any other person charged by Board

� If no one If no one If no one If no one –––– all directors all directors all directors all directors

� Imprisonment Imprisonment Imprisonment Imprisonment uptouptouptoupto I I I I yryryryr or F or F or F or F –––– 50 k to 500 k or both50 k to 500 k or both50 k to 500 k or both50 k to 500 k or both

Lunawat & Co.

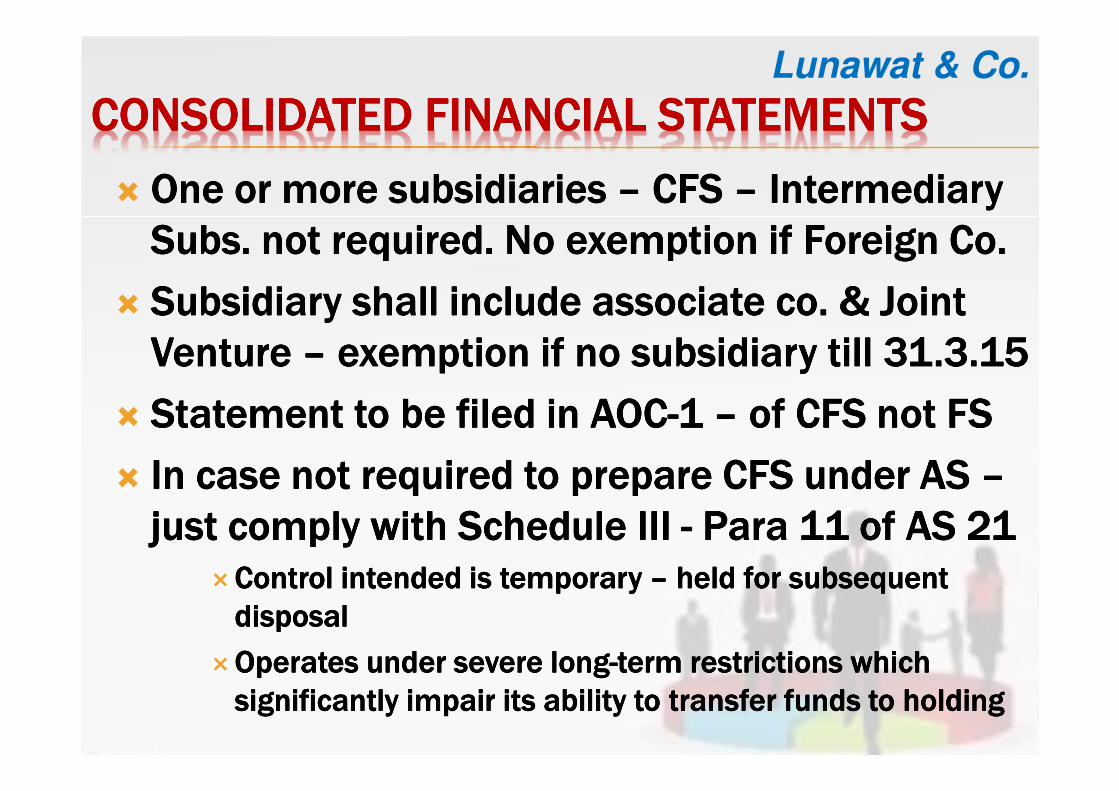

CONSOLIDATED FINANCIAL STATEMENTSCONSOLIDATED FINANCIAL STATEMENTSCONSOLIDATED FINANCIAL STATEMENTSCONSOLIDATED FINANCIAL STATEMENTS

� One or more subsidiaries One or more subsidiaries One or more subsidiaries One or more subsidiaries –––– CFS CFS CFS CFS –––– Intermediary Intermediary Intermediary Intermediary

Subs. not required. No exemption if Foreign Co.Subs. not required. No exemption if Foreign Co.Subs. not required. No exemption if Foreign Co.Subs. not required. No exemption if Foreign Co.

� Subsidiary shall include associate co. & Joint Subsidiary shall include associate co. & Joint Subsidiary shall include associate co. & Joint Subsidiary shall include associate co. & Joint

Venture Venture Venture Venture –––– exemption if no subsidiary till 31.3.15exemption if no subsidiary till 31.3.15exemption if no subsidiary till 31.3.15exemption if no subsidiary till 31.3.15

� Statement to be filed in AOCStatement to be filed in AOCStatement to be filed in AOCStatement to be filed in AOC----1 1 1 1 –––– of CFS not FSof CFS not FSof CFS not FSof CFS not FS

� In case not required to prepare CFS under AS In case not required to prepare CFS under AS In case not required to prepare CFS under AS In case not required to prepare CFS under AS ––––

just comply with Schedule III just comply with Schedule III just comply with Schedule III just comply with Schedule III ---- Para 11 of AS 21Para 11 of AS 21Para 11 of AS 21Para 11 of AS 21�Control intended is temporary Control intended is temporary Control intended is temporary Control intended is temporary –––– held for subsequent held for subsequent held for subsequent held for subsequent

disposaldisposaldisposaldisposal

�Operates under severe longOperates under severe longOperates under severe longOperates under severe long----term restrictions which term restrictions which term restrictions which term restrictions which

significantly impair its ability to transfer funds to holdingsignificantly impair its ability to transfer funds to holdingsignificantly impair its ability to transfer funds to holdingsignificantly impair its ability to transfer funds to holding

Lunawat & Co.

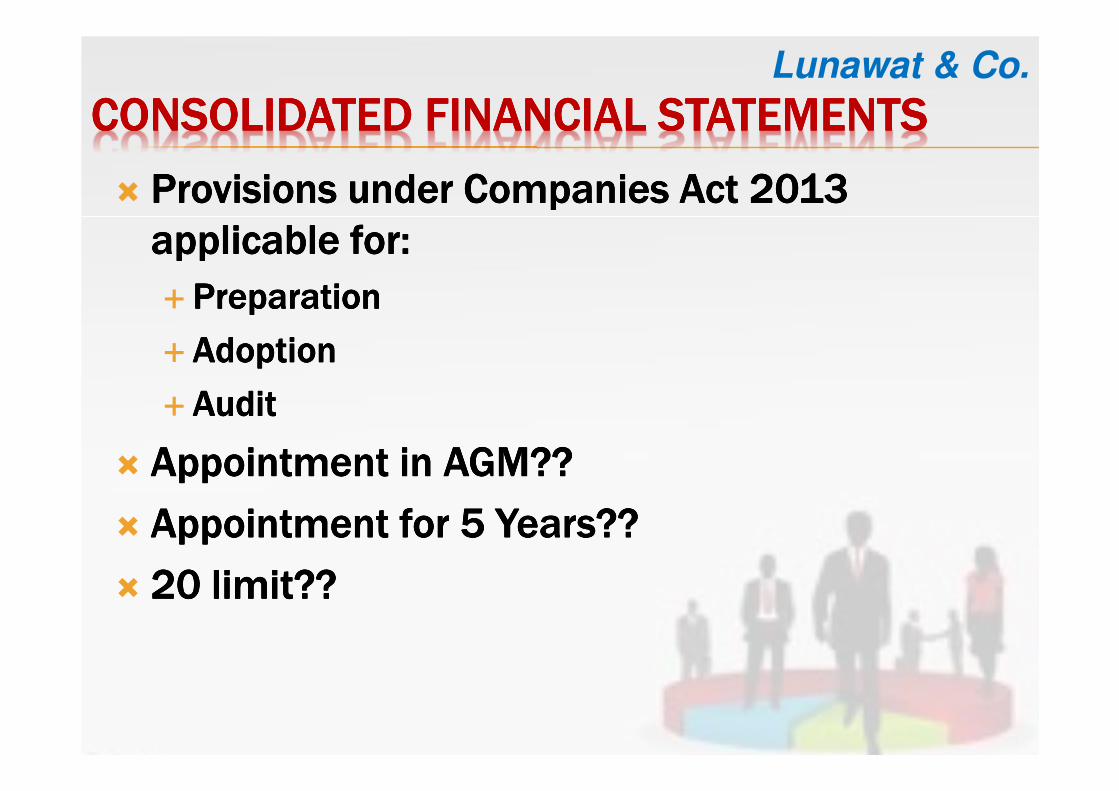

CONSOLIDATED FINANCIAL STATEMENTSCONSOLIDATED FINANCIAL STATEMENTSCONSOLIDATED FINANCIAL STATEMENTSCONSOLIDATED FINANCIAL STATEMENTS

� Provisions under Companies Act 2013 Provisions under Companies Act 2013 Provisions under Companies Act 2013 Provisions under Companies Act 2013

applicable for:applicable for:applicable for:applicable for:

� PreparationPreparationPreparationPreparation

� AdoptionAdoptionAdoptionAdoption

� AuditAuditAuditAudit

� Appointment in AGM??Appointment in AGM??Appointment in AGM??Appointment in AGM??

� Appointment for 5 Years??Appointment for 5 Years??Appointment for 5 Years??Appointment for 5 Years??

� 20 limit??20 limit??20 limit??20 limit??

Lunawat & Co.

Lunawat & Co.

USEFUL LIVESUSEFUL LIVESUSEFUL LIVESUSEFUL LIVES1.1.1.1. BuildingsBuildingsBuildingsBuildings

2.2.2.2. Bridges, Culverts, Bridges, Culverts, Bridges, Culverts, Bridges, Culverts, bundersbundersbundersbunders, etc., etc., etc., etc.

3.3.3.3. RoadsRoadsRoadsRoads

4.4.4.4. Plant & MachineryPlant & MachineryPlant & MachineryPlant & Machinery

5.5.5.5. Furniture & FixtureFurniture & FixtureFurniture & FixtureFurniture & Fixture

6.6.6.6. Motor VehiclesMotor VehiclesMotor VehiclesMotor Vehicles

7.7.7.7. ShipsShipsShipsShips

8.8.8.8. Aircrafts & HelicoptersAircrafts & HelicoptersAircrafts & HelicoptersAircrafts & Helicopters

9.9.9.9. Railway sidings, Locomotives, Rolling Stocks, Railway sidings, Locomotives, Rolling Stocks, Railway sidings, Locomotives, Rolling Stocks, Railway sidings, Locomotives, Rolling Stocks,

Tramways…Tramways…Tramways…Tramways…

Lunawat & Co.

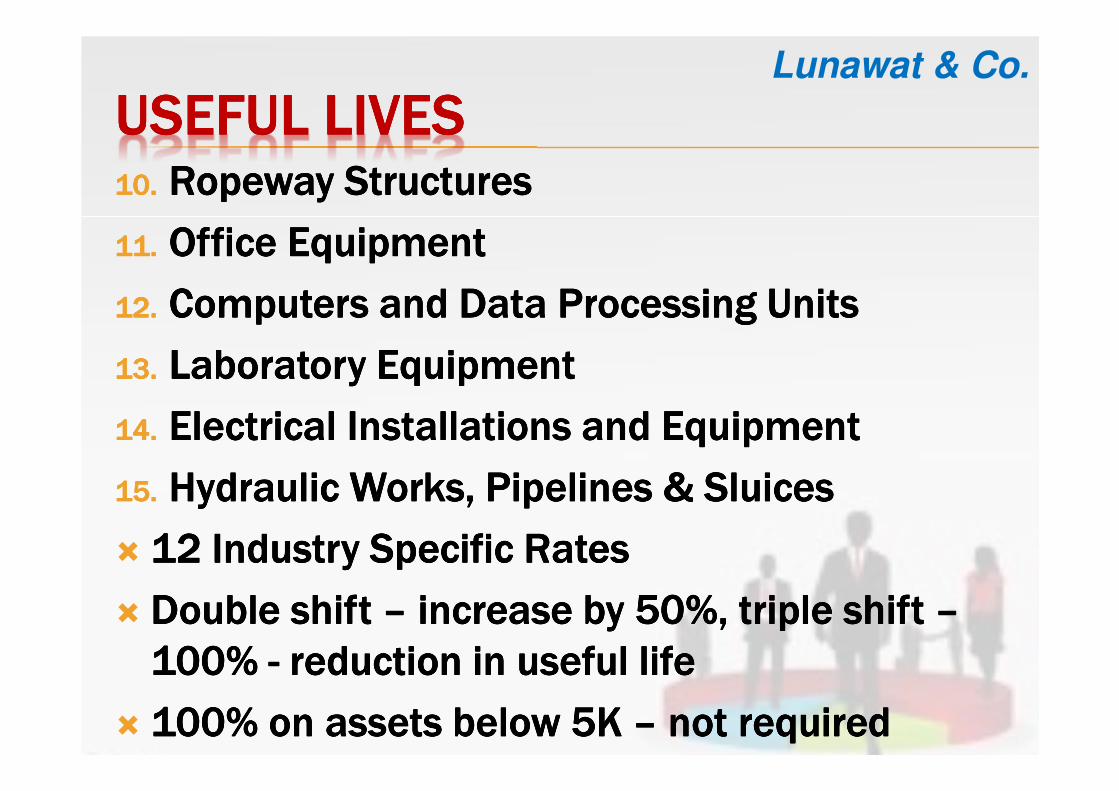

USEFUL LIVESUSEFUL LIVESUSEFUL LIVESUSEFUL LIVES10.10.10.10. Ropeway StructuresRopeway StructuresRopeway StructuresRopeway Structures

11.11.11.11. Office EquipmentOffice EquipmentOffice EquipmentOffice Equipment

12.12.12.12. Computers and Data Processing UnitsComputers and Data Processing UnitsComputers and Data Processing UnitsComputers and Data Processing Units

13.13.13.13. Laboratory EquipmentLaboratory EquipmentLaboratory EquipmentLaboratory Equipment

14.14.14.14. Electrical Installations and EquipmentElectrical Installations and EquipmentElectrical Installations and EquipmentElectrical Installations and Equipment

15.15.15.15. Hydraulic Works, Pipelines & SluicesHydraulic Works, Pipelines & SluicesHydraulic Works, Pipelines & SluicesHydraulic Works, Pipelines & Sluices

� 12 Industry Specific Rates12 Industry Specific Rates12 Industry Specific Rates12 Industry Specific Rates

� Double Double Double Double shift shift shift shift –––– increase by 50%, triple shift increase by 50%, triple shift increase by 50%, triple shift increase by 50%, triple shift ––––

100100100100% % % % ---- reduction in useful lifereduction in useful lifereduction in useful lifereduction in useful life

� 100% on assets below 5K 100% on assets below 5K 100% on assets below 5K 100% on assets below 5K –––– not not not not requiredrequiredrequiredrequired

Lunawat & Co.

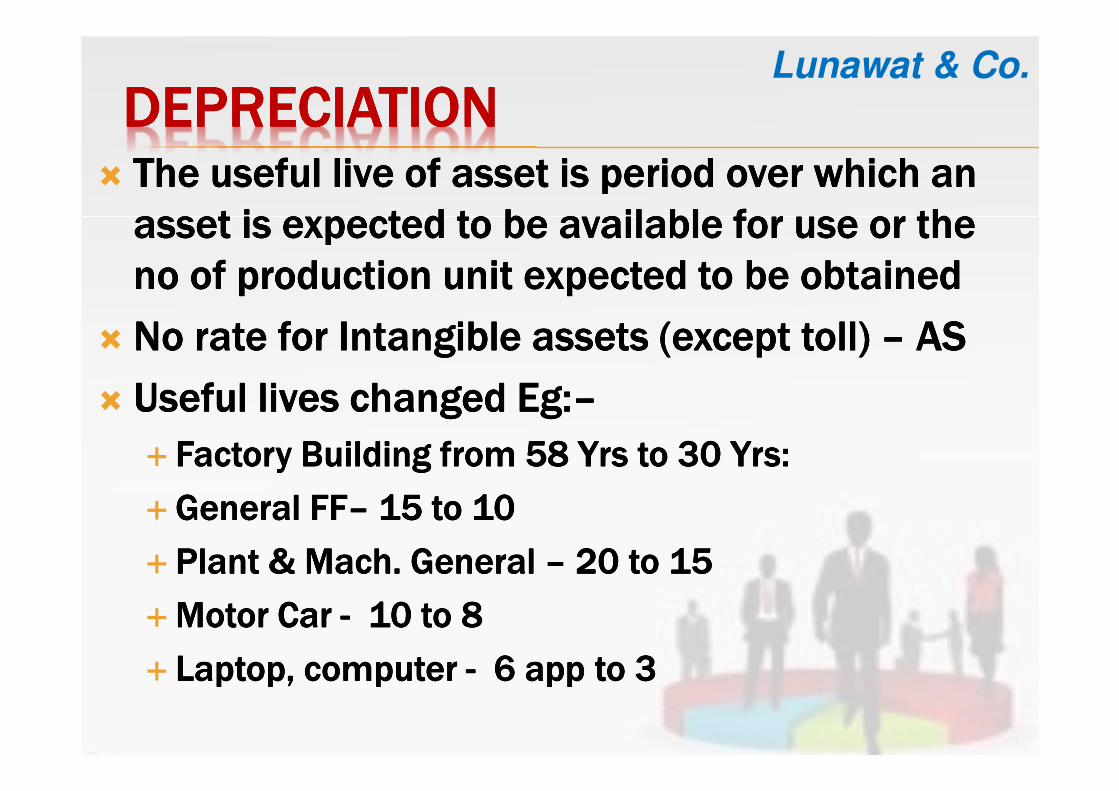

DEPRECIATIONDEPRECIATIONDEPRECIATIONDEPRECIATION� The useful live of asset is period over which an The useful live of asset is period over which an The useful live of asset is period over which an The useful live of asset is period over which an

asset is expected to be available for use or the asset is expected to be available for use or the asset is expected to be available for use or the asset is expected to be available for use or the

no of production unit expected to be obtainedno of production unit expected to be obtainedno of production unit expected to be obtainedno of production unit expected to be obtained

� No rate for Intangible assets (except toll) No rate for Intangible assets (except toll) No rate for Intangible assets (except toll) No rate for Intangible assets (except toll) –––– AS AS AS AS

� Useful lives changed Useful lives changed Useful lives changed Useful lives changed EgEgEgEg::::––––

� Factory Building from 58 Factory Building from 58 Factory Building from 58 Factory Building from 58 YrsYrsYrsYrs to 30 to 30 to 30 to 30 YrsYrsYrsYrs: : : :

�General FFGeneral FFGeneral FFGeneral FF–––– 15 to 1015 to 1015 to 1015 to 10

� Plant & Mach. General Plant & Mach. General Plant & Mach. General Plant & Mach. General –––– 20 to 1520 to 1520 to 1520 to 15

�Motor Car Motor Car Motor Car Motor Car ---- 10 to 810 to 810 to 810 to 8

� Laptop, computer Laptop, computer Laptop, computer Laptop, computer ---- 6 app to 3 6 app to 3 6 app to 3 6 app to 3

Lunawat & Co.

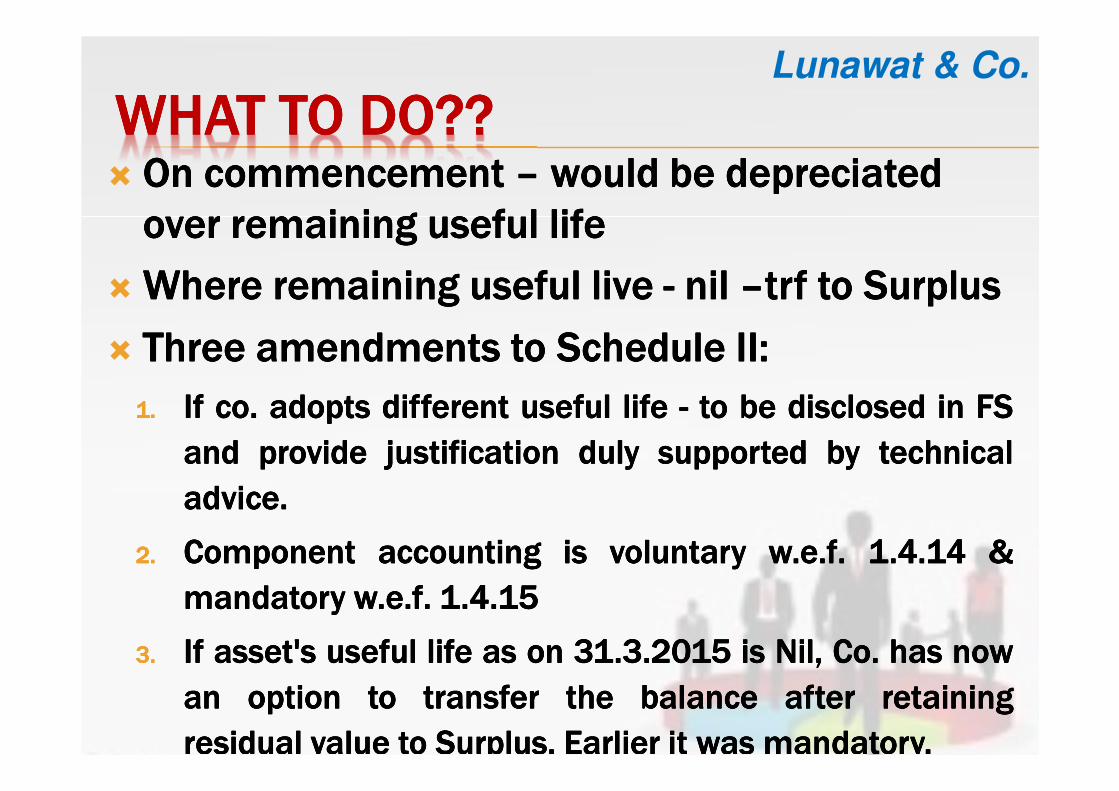

WHAT TO DO??WHAT TO DO??WHAT TO DO??WHAT TO DO??� On commencement On commencement On commencement On commencement –––– would be depreciated would be depreciated would be depreciated would be depreciated

over remaining useful lifeover remaining useful lifeover remaining useful lifeover remaining useful life

� Where remaining useful live Where remaining useful live Where remaining useful live Where remaining useful live ---- nil nil nil nil ––––trftrftrftrf to Surplus to Surplus to Surplus to Surplus

� ThreeThreeThreeThree amendmentsamendmentsamendmentsamendments totototo ScheduleScheduleScheduleSchedule IIIIIIII::::

1.1.1.1. IfIfIfIf cocococo.... adoptsadoptsadoptsadopts differentdifferentdifferentdifferent usefulusefulusefuluseful lifelifelifelife ---- totototo bebebebe discloseddiscloseddiscloseddisclosed inininin FSFSFSFS

andandandand provideprovideprovideprovide justificationjustificationjustificationjustification dulydulydulyduly supportedsupportedsupportedsupported bybybyby technicaltechnicaltechnicaltechnical

adviceadviceadviceadvice....

2.2.2.2. ComponentComponentComponentComponent accountingaccountingaccountingaccounting isisisis voluntaryvoluntaryvoluntaryvoluntary wwww....eeee....ffff.... 1111....4444....14141414 &&&&

mandatorymandatorymandatorymandatory wwww....eeee....ffff.... 1111....4444....15151515

3.3.3.3. IfIfIfIf asset'sasset'sasset'sasset's usefulusefulusefuluseful lifelifelifelife asasasas onononon 31313131....3333....2015201520152015 isisisis Nil,Nil,Nil,Nil, CoCoCoCo.... hashashashas nownownownow

anananan optionoptionoptionoption totototo transfertransfertransfertransfer thethethethe balancebalancebalancebalance afterafterafterafter retainingretainingretainingretaining

residualresidualresidualresidual valuevaluevaluevalue totototo SurplusSurplusSurplusSurplus.... EarlierEarlierEarlierEarlier itititit waswaswaswas mandatorymandatorymandatorymandatory....

Lunawat & Co.

SCHEDULE IIISCHEDULE IIISCHEDULE IIISCHEDULE IIILunawat & Co.

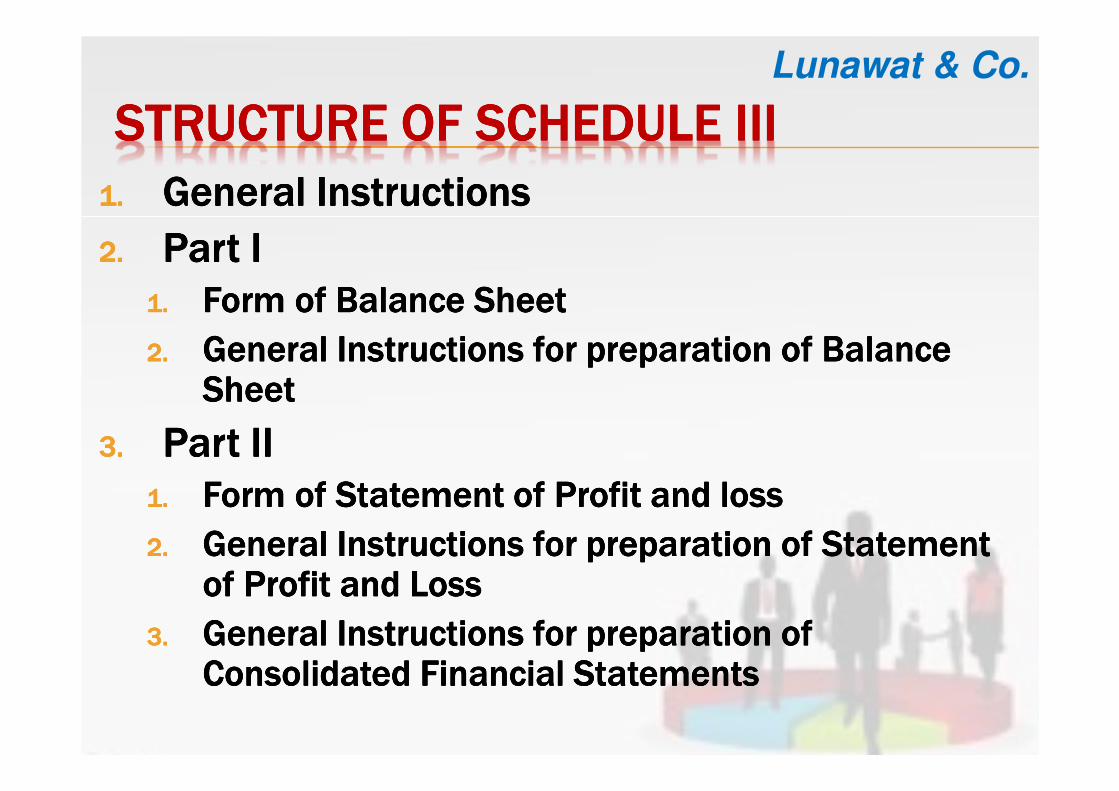

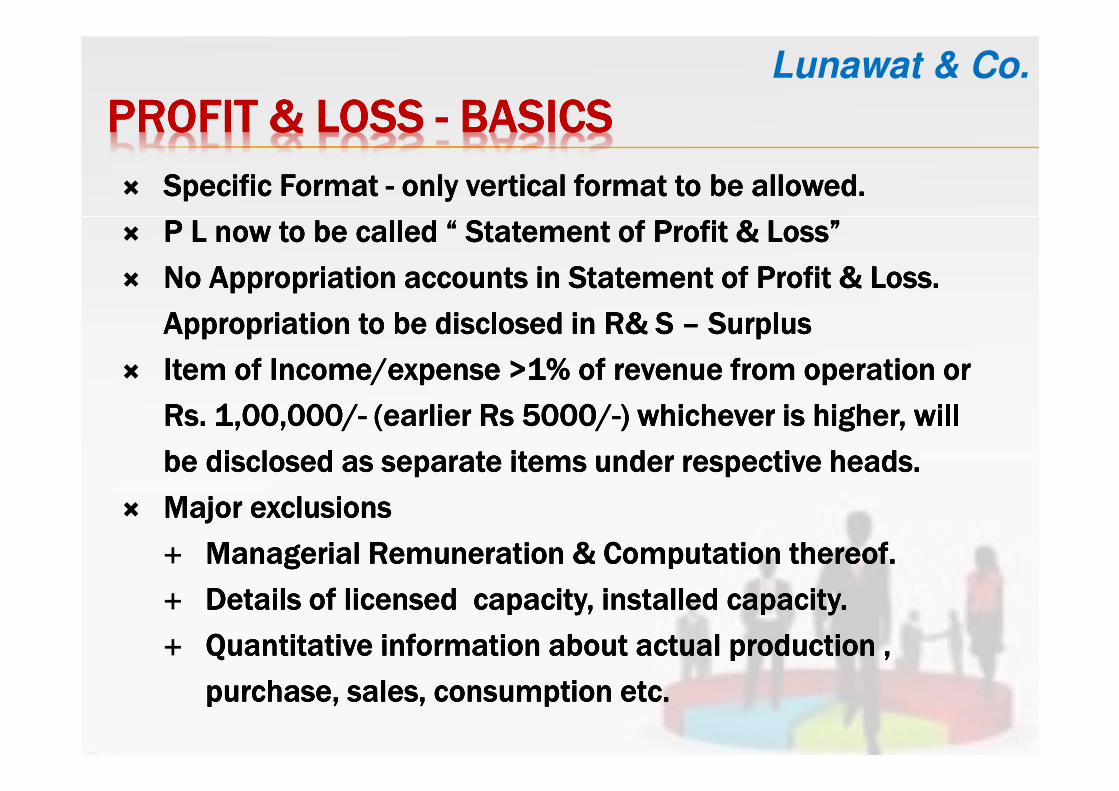

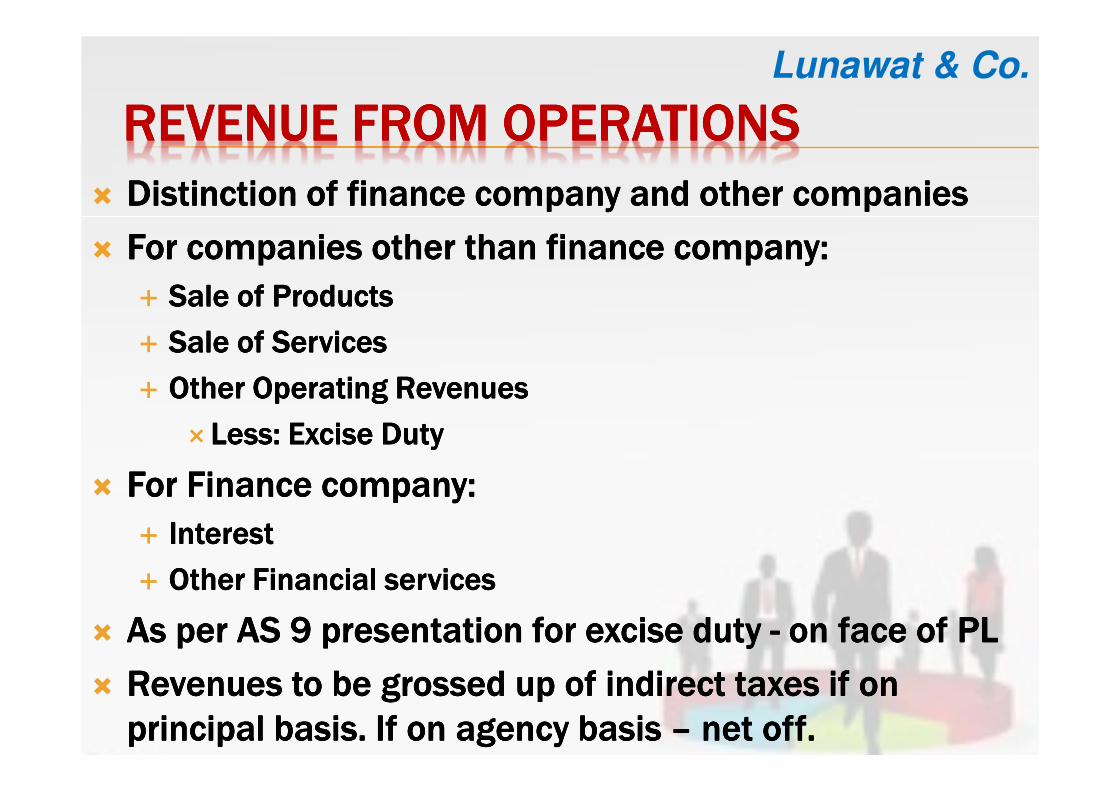

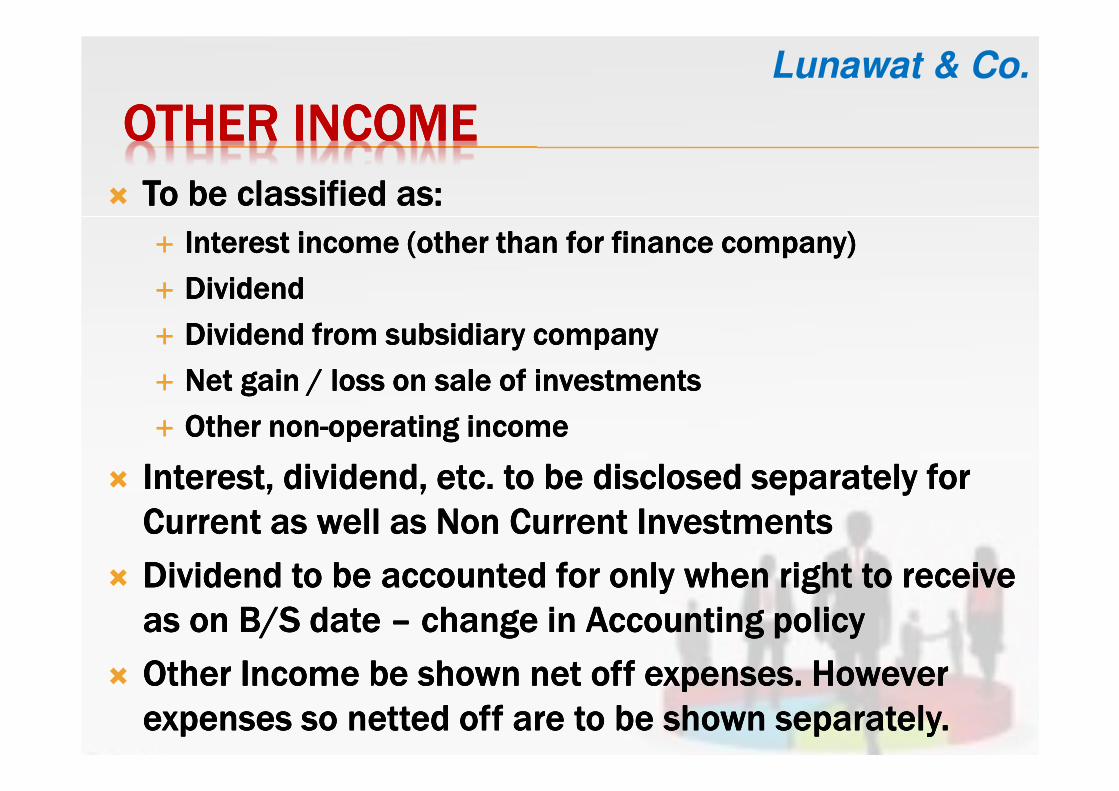

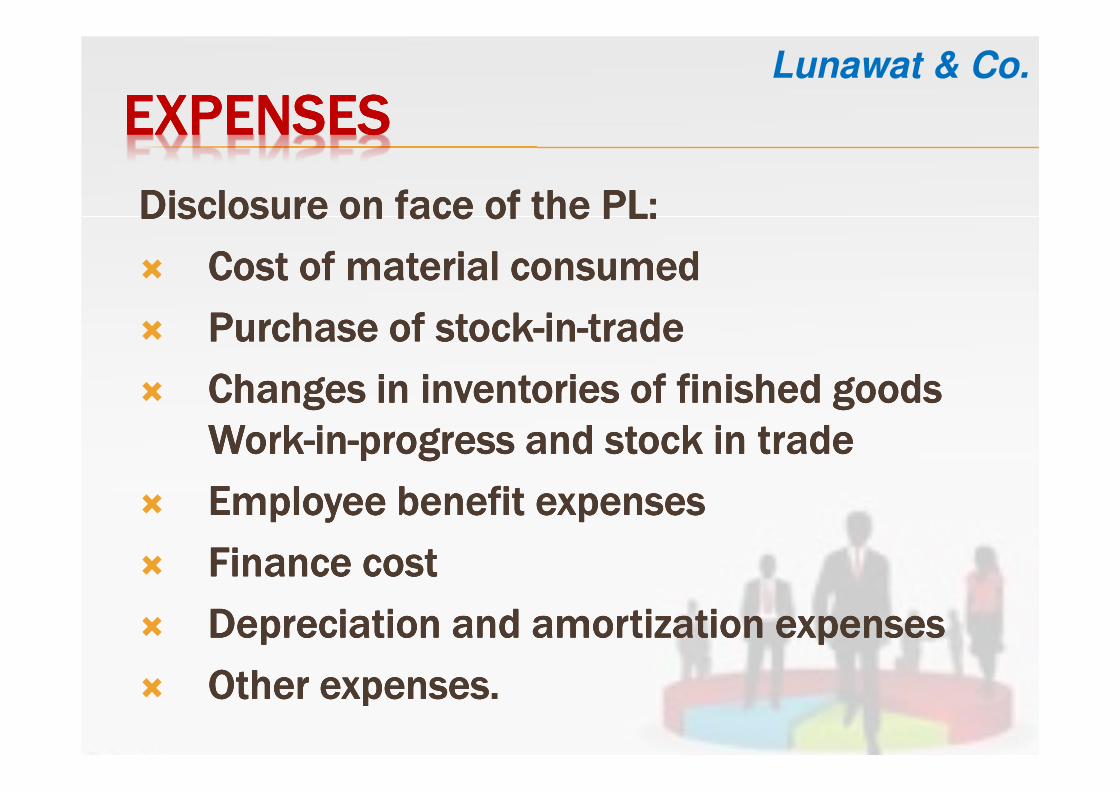

STRUCTURE OF SCHEDULE IIISTRUCTURE OF SCHEDULE IIISTRUCTURE OF SCHEDULE IIISTRUCTURE OF SCHEDULE III

1.1.1.1. General InstructionsGeneral InstructionsGeneral InstructionsGeneral Instructions

2.2.2.2. Part IPart IPart IPart I

1.1.1.1. Form of Balance SheetForm of Balance SheetForm of Balance SheetForm of Balance Sheet

2.2.2.2. General Instructions for preparation of Balance General Instructions for preparation of Balance General Instructions for preparation of Balance General Instructions for preparation of Balance SheetSheetSheetSheet

3.3.3.3. Part IIPart IIPart IIPart II

1.1.1.1. Form of Statement of Profit and lossForm of Statement of Profit and lossForm of Statement of Profit and lossForm of Statement of Profit and loss

2.2.2.2. General Instructions for preparation of Statement General Instructions for preparation of Statement General Instructions for preparation of Statement General Instructions for preparation of Statement of Profit and Lossof Profit and Lossof Profit and Lossof Profit and Loss

3.3.3.3. General Instructions for preparation of General Instructions for preparation of General Instructions for preparation of General Instructions for preparation of Consolidated Financial StatementsConsolidated Financial StatementsConsolidated Financial StatementsConsolidated Financial Statements

Lunawat & Co.

GENERAL INSTRUCTIONSGENERAL INSTRUCTIONSGENERAL INSTRUCTIONSGENERAL INSTRUCTIONS

� Disclosure requirements of AS shall Disclosure requirements of AS shall Disclosure requirements of AS shall Disclosure requirements of AS shall prevailprevailprevailprevail over over over over

Schedule III. Companies Act disclosures also required.Schedule III. Companies Act disclosures also required.Schedule III. Companies Act disclosures also required.Schedule III. Companies Act disclosures also required.

� Disclosures are in addition to and not in substitution Disclosures are in addition to and not in substitution Disclosures are in addition to and not in substitution Disclosures are in addition to and not in substitution

of the disclosure requirements of AS.of the disclosure requirements of AS.of the disclosure requirements of AS.of the disclosure requirements of AS.

� Each item on face of B/S & Statement of P & L is to Each item on face of B/S & Statement of P & L is to Each item on face of B/S & Statement of P & L is to Each item on face of B/S & Statement of P & L is to

be cross referenced to related information in notes to be cross referenced to related information in notes to be cross referenced to related information in notes to be cross referenced to related information in notes to

a/ca/ca/ca/c

� Notes to accounts to contain information in addition Notes to accounts to contain information in addition Notes to accounts to contain information in addition Notes to accounts to contain information in addition

to that presented in the financial statement including to that presented in the financial statement including to that presented in the financial statement including to that presented in the financial statement including

narrative descriptionsnarrative descriptionsnarrative descriptionsnarrative descriptions

� Corresponding amounts for immediately preceding Corresponding amounts for immediately preceding Corresponding amounts for immediately preceding Corresponding amounts for immediately preceding

reporting period to be given, except for first year of reporting period to be given, except for first year of reporting period to be given, except for first year of reporting period to be given, except for first year of

incorporation.incorporation.incorporation.incorporation.

Lunawat & Co.

GENERAL INSTRUCTIONSGENERAL INSTRUCTIONSGENERAL INSTRUCTIONSGENERAL INSTRUCTIONS

� Balance to be maintained between providing Balance to be maintained between providing Balance to be maintained between providing Balance to be maintained between providing

excessive details that may not assist users and not excessive details that may not assist users and not excessive details that may not assist users and not excessive details that may not assist users and not

providing important information.providing important information.providing important information.providing important information.

� Terms used shall be as per ASTerms used shall be as per ASTerms used shall be as per ASTerms used shall be as per AS

� Rounding off based on turnover.Rounding off based on turnover.Rounding off based on turnover.Rounding off based on turnover.

� Less than Less than Less than Less than RsRsRsRs. 100 Crores . 100 Crores . 100 Crores . 100 Crores ---- To the nearest hundreds, To the nearest hundreds, To the nearest hundreds, To the nearest hundreds,

thousands, lacs or millions or decimal thereofthousands, lacs or millions or decimal thereofthousands, lacs or millions or decimal thereofthousands, lacs or millions or decimal thereof

� RsRsRsRs. 100 Crores or more . 100 Crores or more . 100 Crores or more . 100 Crores or more ---- To the nearest lacs or millions or To the nearest lacs or millions or To the nearest lacs or millions or To the nearest lacs or millions or

crores or decimal thereofcrores or decimal thereofcrores or decimal thereofcrores or decimal thereof

Lunawat & Co.

BASICS BASICS BASICS BASICS –––– CURRENT VS. NONCURRENT VS. NONCURRENT VS. NONCURRENT VS. NON----CURRENTCURRENTCURRENTCURRENT

� Current / NonCurrent / NonCurrent / NonCurrent / Non---- Current.Current.Current.Current.

� Current Asset Current Asset Current Asset Current Asset ---- satisfies any of following criteria; it is:satisfies any of following criteria; it is:satisfies any of following criteria; it is:satisfies any of following criteria; it is:

� In the company’s normal operating cycle it is; In the company’s normal operating cycle it is; In the company’s normal operating cycle it is; In the company’s normal operating cycle it is;

� Intended for sale; orIntended for sale; orIntended for sale; orIntended for sale; or

� Intended to be consumed; orIntended to be consumed; orIntended to be consumed; orIntended to be consumed; or

�Expected to be realized.Expected to be realized.Expected to be realized.Expected to be realized.

� Held primarily for the purpose of being traded; orHeld primarily for the purpose of being traded; orHeld primarily for the purpose of being traded; orHeld primarily for the purpose of being traded; or

� Expected to be realized within 12 months after the Expected to be realized within 12 months after the Expected to be realized within 12 months after the Expected to be realized within 12 months after the

reporting date; orreporting date; orreporting date; orreporting date; or

� Cash or cash equivalent unless it is restricted from being Cash or cash equivalent unless it is restricted from being Cash or cash equivalent unless it is restricted from being Cash or cash equivalent unless it is restricted from being

exchanged or used to settle a liability for at least 12 exchanged or used to settle a liability for at least 12 exchanged or used to settle a liability for at least 12 exchanged or used to settle a liability for at least 12

months after reporting date.months after reporting date.months after reporting date.months after reporting date.

Lunawat & Co.

BASICS BASICS BASICS BASICS –––– OPERATING CYCLEOPERATING CYCLEOPERATING CYCLEOPERATING CYCLE

� Operating cycle is the time between the acquisition of Operating cycle is the time between the acquisition of Operating cycle is the time between the acquisition of Operating cycle is the time between the acquisition of

assets for processing and their realization in Cash or assets for processing and their realization in Cash or assets for processing and their realization in Cash or assets for processing and their realization in Cash or

cash equivalent. cash equivalent. cash equivalent. cash equivalent.

� In other words Operating cycle is a period beginning In other words Operating cycle is a period beginning In other words Operating cycle is a period beginning In other words Operating cycle is a period beginning

from acquisition of raw material and ending on from acquisition of raw material and ending on from acquisition of raw material and ending on from acquisition of raw material and ending on

realization. realization. realization. realization.

� Hence, an operating cycle would be =Hence, an operating cycle would be =Hence, an operating cycle would be =Hence, an operating cycle would be =

Average holding period of Raw MaterialAverage holding period of Raw MaterialAverage holding period of Raw MaterialAverage holding period of Raw Material

++++ Average Production Period Average Production Period Average Production Period Average Production Period

+ + + + Average Holding period of Finished GoodsAverage Holding period of Finished GoodsAverage Holding period of Finished GoodsAverage Holding period of Finished Goods

+ + + + Average Collection PeriodAverage Collection PeriodAverage Collection PeriodAverage Collection Period

Lunawat & Co.

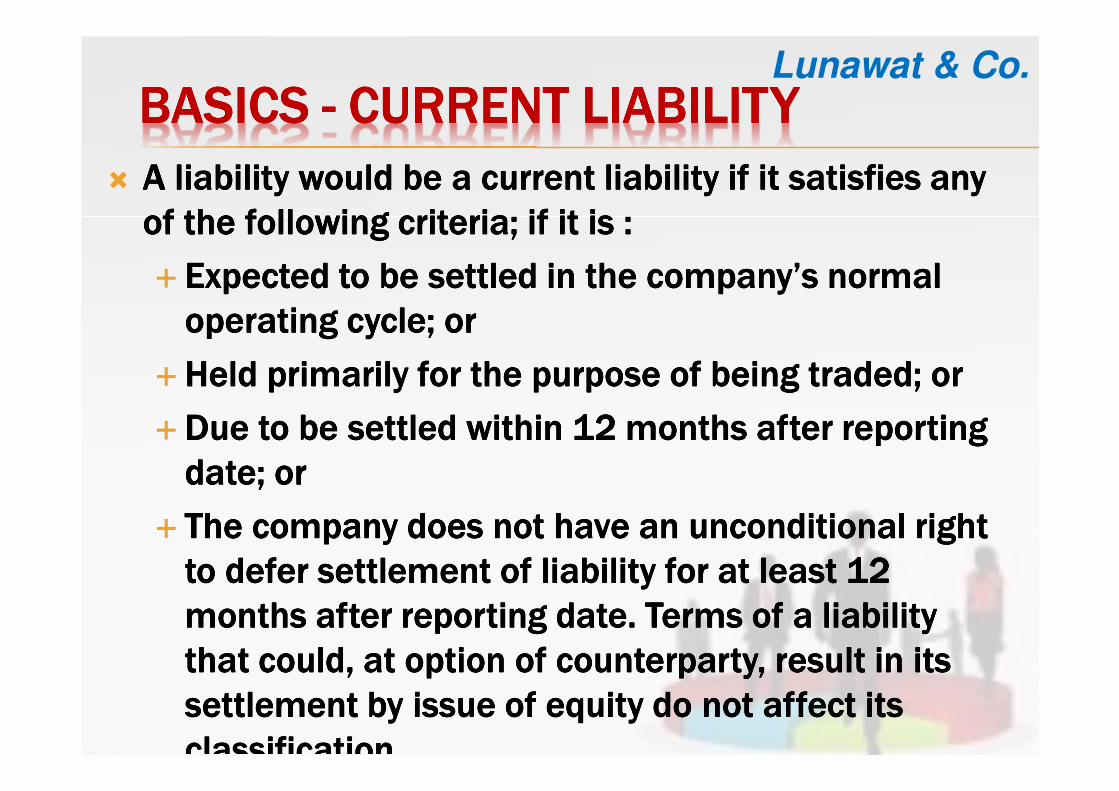

BASICS BASICS BASICS BASICS ---- CURRENT LIABILITYCURRENT LIABILITYCURRENT LIABILITYCURRENT LIABILITY

� A liability would be a current liability if it satisfies any A liability would be a current liability if it satisfies any A liability would be a current liability if it satisfies any A liability would be a current liability if it satisfies any

of the following criteria; if it is :of the following criteria; if it is :of the following criteria; if it is :of the following criteria; if it is :

� Expected to be settled in the company’s normal Expected to be settled in the company’s normal Expected to be settled in the company’s normal Expected to be settled in the company’s normal

operating cycle; oroperating cycle; oroperating cycle; oroperating cycle; or

�Held primarily for the purpose of being traded; orHeld primarily for the purpose of being traded; orHeld primarily for the purpose of being traded; orHeld primarily for the purpose of being traded; or

�Due to be settled within 12 months after reporting Due to be settled within 12 months after reporting Due to be settled within 12 months after reporting Due to be settled within 12 months after reporting

date; ordate; ordate; ordate; or

� The company does not have an unconditional right The company does not have an unconditional right The company does not have an unconditional right The company does not have an unconditional right

to defer settlement of liability for at least 12 to defer settlement of liability for at least 12 to defer settlement of liability for at least 12 to defer settlement of liability for at least 12

months after reporting date. Terms of a liability months after reporting date. Terms of a liability months after reporting date. Terms of a liability months after reporting date. Terms of a liability

that could, at option of counterparty, result in its that could, at option of counterparty, result in its that could, at option of counterparty, result in its that could, at option of counterparty, result in its

settlement by issue of equity do not affect its settlement by issue of equity do not affect its settlement by issue of equity do not affect its settlement by issue of equity do not affect its

classification.classification.classification.classification.

Lunawat & Co.

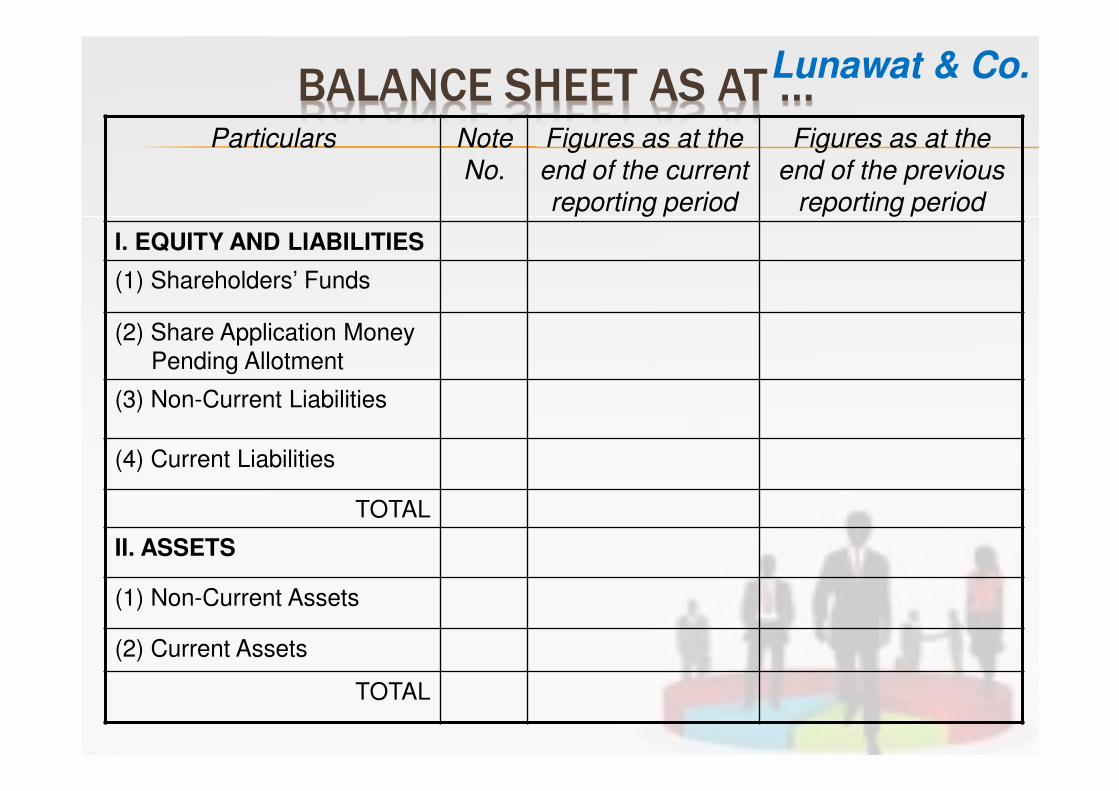

ORGANIZING THE BALANCE SHEETORGANIZING THE BALANCE SHEETORGANIZING THE BALANCE SHEETORGANIZING THE BALANCE SHEET

� Preparing Balance Sheet and Profit and Loss Preparing Balance Sheet and Profit and Loss Preparing Balance Sheet and Profit and Loss Preparing Balance Sheet and Profit and Loss

Account in “Horizontal Format” has been done Account in “Horizontal Format” has been done Account in “Horizontal Format” has been done Account in “Horizontal Format” has been done

away.away.away.away.

� Now only the “Vertical Format” is allowed.Now only the “Vertical Format” is allowed.Now only the “Vertical Format” is allowed.Now only the “Vertical Format” is allowed.

� No need to prepare schedules to form part of the No need to prepare schedules to form part of the No need to prepare schedules to form part of the No need to prepare schedules to form part of the

financial statements. Only notes are to be given.financial statements. Only notes are to be given.financial statements. Only notes are to be given.financial statements. Only notes are to be given.

� In place of “Schedule Numbers”, we shall have to In place of “Schedule Numbers”, we shall have to In place of “Schedule Numbers”, we shall have to In place of “Schedule Numbers”, we shall have to

give “Note Numbers”.give “Note Numbers”.give “Note Numbers”.give “Note Numbers”.

� Old terms of “Sources of Funds” and “Application of Old terms of “Sources of Funds” and “Application of Old terms of “Sources of Funds” and “Application of Old terms of “Sources of Funds” and “Application of

Funds” are replaced by “Equity & Liabilities” and Funds” are replaced by “Equity & Liabilities” and Funds” are replaced by “Equity & Liabilities” and Funds” are replaced by “Equity & Liabilities” and

“Assets”, respectively“Assets”, respectively“Assets”, respectively“Assets”, respectively

Lunawat & Co.

BALANCE SHEET AS AT …Particulars Note

No.

Figures as at the

end of the current

reporting period

Figures as at the

end of the previous

reporting period

I. EQUITY AND LIABILITIES

(1) Shareholders’ Funds

(2) Share Application Money

Pending Allotment

(3) Non-Current Liabilities

(4) Current Liabilities

TOTAL

II. ASSETS

(1) Non-Current Assets

(2) Current Assets

TOTAL

Lunawat & Co.

FORM OF BALANCE SHEET (PART 1)Particulars Note

No.

Figures as at the

end of the CRP

Figures as at the

end of the PRP

I. EQUITY AND LIABILITIES

(1) Shareholders’ Funds

(a) Share capital

(b) Reserve and Surplus

(c) Money received against share warrants

1

2

(2) Share application money pending allotment

3

(3) Non-current Liabilities

(a) Long term borrowings

(b) Deferred tax liabilities (net)

(c) Other long term liabilities

(d) Long term provisions

4

5

6

7

(4) Current Liabilities

(a) Short term borrowings

(b) Trade payables

(c) Other current liabilities

(d) Short term provisions

8

9

10

TOTAL

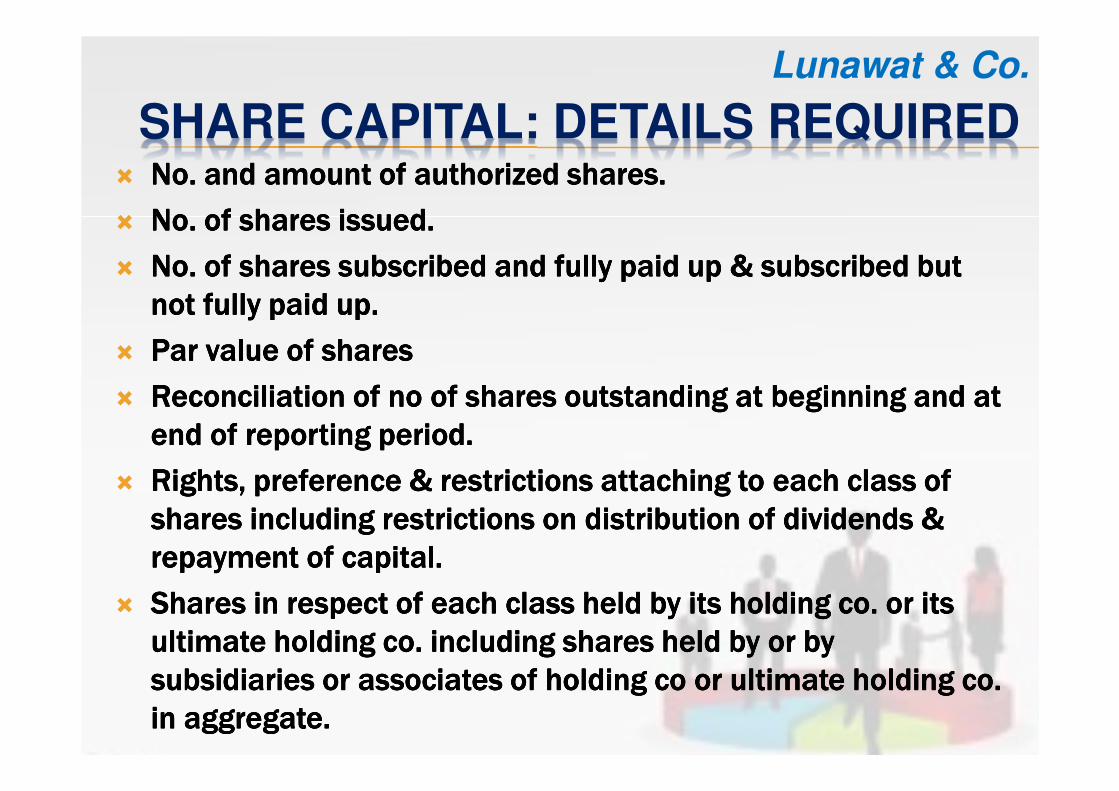

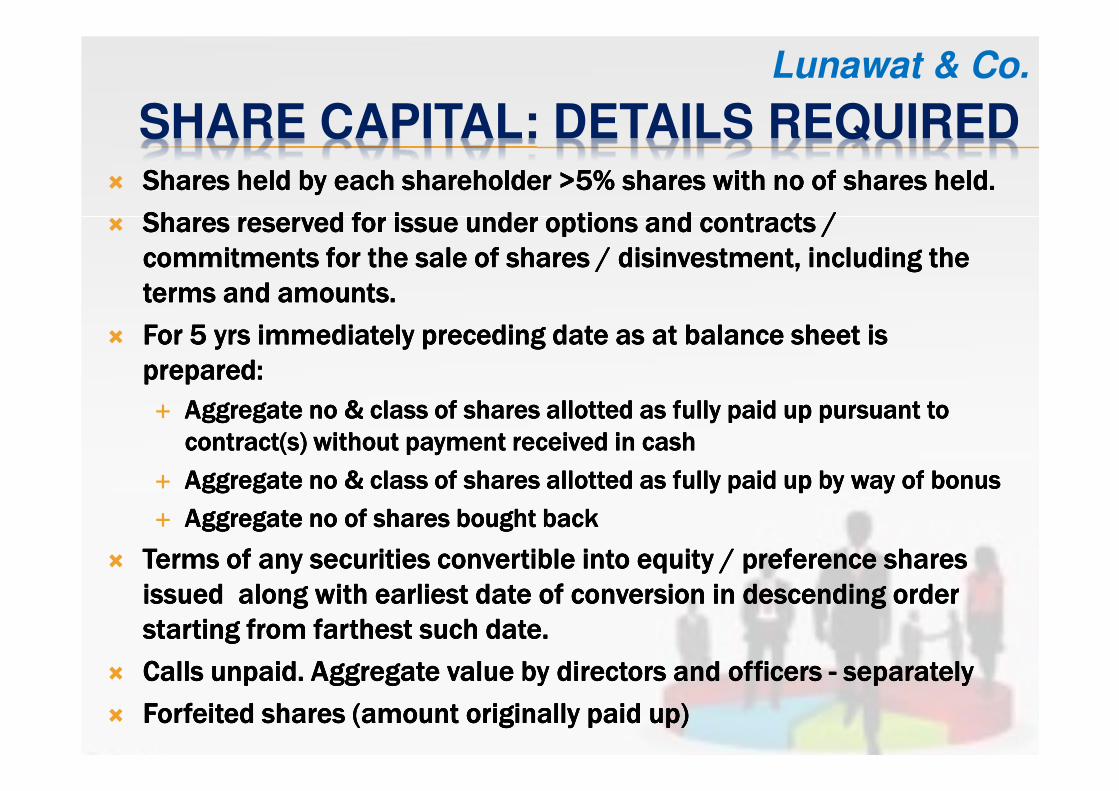

SHARE CAPITAL: DETAILS REQUIRED� No. and amount of authorized shares.No. and amount of authorized shares.No. and amount of authorized shares.No. and amount of authorized shares.

� No. of shares issued. No. of shares issued. No. of shares issued. No. of shares issued.

� No. of shares subscribed and fully paid up & subscribed but No. of shares subscribed and fully paid up & subscribed but No. of shares subscribed and fully paid up & subscribed but No. of shares subscribed and fully paid up & subscribed but

not fully paid up.not fully paid up.not fully paid up.not fully paid up.

� Par value of sharesPar value of sharesPar value of sharesPar value of shares

� Reconciliation of no of shares outstanding at beginning and at Reconciliation of no of shares outstanding at beginning and at Reconciliation of no of shares outstanding at beginning and at Reconciliation of no of shares outstanding at beginning and at

end of reporting period.end of reporting period.end of reporting period.end of reporting period.

� Rights, preference & restrictions attaching to each class of Rights, preference & restrictions attaching to each class of Rights, preference & restrictions attaching to each class of Rights, preference & restrictions attaching to each class of

shares including restrictions on distribution of dividends & shares including restrictions on distribution of dividends & shares including restrictions on distribution of dividends & shares including restrictions on distribution of dividends &

repayment of capital.repayment of capital.repayment of capital.repayment of capital.

� Shares in respect of each class held by its holding co. or its Shares in respect of each class held by its holding co. or its Shares in respect of each class held by its holding co. or its Shares in respect of each class held by its holding co. or its

ultimate holding co. including shares held by or by ultimate holding co. including shares held by or by ultimate holding co. including shares held by or by ultimate holding co. including shares held by or by

subsidiaries or associates of holding co or ultimate holding co. subsidiaries or associates of holding co or ultimate holding co. subsidiaries or associates of holding co or ultimate holding co. subsidiaries or associates of holding co or ultimate holding co.

in aggregate.in aggregate.in aggregate.in aggregate.

Lunawat & Co.

SHARE CAPITAL: DETAILS REQUIRED� Shares held by each shareholder >5% shares with no of shares held.Shares held by each shareholder >5% shares with no of shares held.Shares held by each shareholder >5% shares with no of shares held.Shares held by each shareholder >5% shares with no of shares held.

� Shares reserved for issue under options and contracts / Shares reserved for issue under options and contracts / Shares reserved for issue under options and contracts / Shares reserved for issue under options and contracts /

commitments for the sale of shares / disinvestment, including the commitments for the sale of shares / disinvestment, including the commitments for the sale of shares / disinvestment, including the commitments for the sale of shares / disinvestment, including the

terms and amounts.terms and amounts.terms and amounts.terms and amounts.

� For 5 yrs immediately preceding date as at balance sheet is For 5 yrs immediately preceding date as at balance sheet is For 5 yrs immediately preceding date as at balance sheet is For 5 yrs immediately preceding date as at balance sheet is

prepared:prepared:prepared:prepared:

� Aggregate no & class of shares allotted as fully paid up pursuant to Aggregate no & class of shares allotted as fully paid up pursuant to Aggregate no & class of shares allotted as fully paid up pursuant to Aggregate no & class of shares allotted as fully paid up pursuant to

contract(s) without payment received in cashcontract(s) without payment received in cashcontract(s) without payment received in cashcontract(s) without payment received in cash

� Aggregate no & class of shares allotted as fully paid up by way of bonus Aggregate no & class of shares allotted as fully paid up by way of bonus Aggregate no & class of shares allotted as fully paid up by way of bonus Aggregate no & class of shares allotted as fully paid up by way of bonus

� Aggregate no of shares bought backAggregate no of shares bought backAggregate no of shares bought backAggregate no of shares bought back

� Terms of any securities convertible into equity / preference shares Terms of any securities convertible into equity / preference shares Terms of any securities convertible into equity / preference shares Terms of any securities convertible into equity / preference shares

issued along with earliest date of conversion in descending order issued along with earliest date of conversion in descending order issued along with earliest date of conversion in descending order issued along with earliest date of conversion in descending order

starting from farthest such date.starting from farthest such date.starting from farthest such date.starting from farthest such date.

� Calls unpaid. Aggregate value by directors and officers Calls unpaid. Aggregate value by directors and officers Calls unpaid. Aggregate value by directors and officers Calls unpaid. Aggregate value by directors and officers ---- separatelyseparatelyseparatelyseparately

� Forfeited shares (amount originally paid up)Forfeited shares (amount originally paid up)Forfeited shares (amount originally paid up)Forfeited shares (amount originally paid up)

Lunawat & Co.

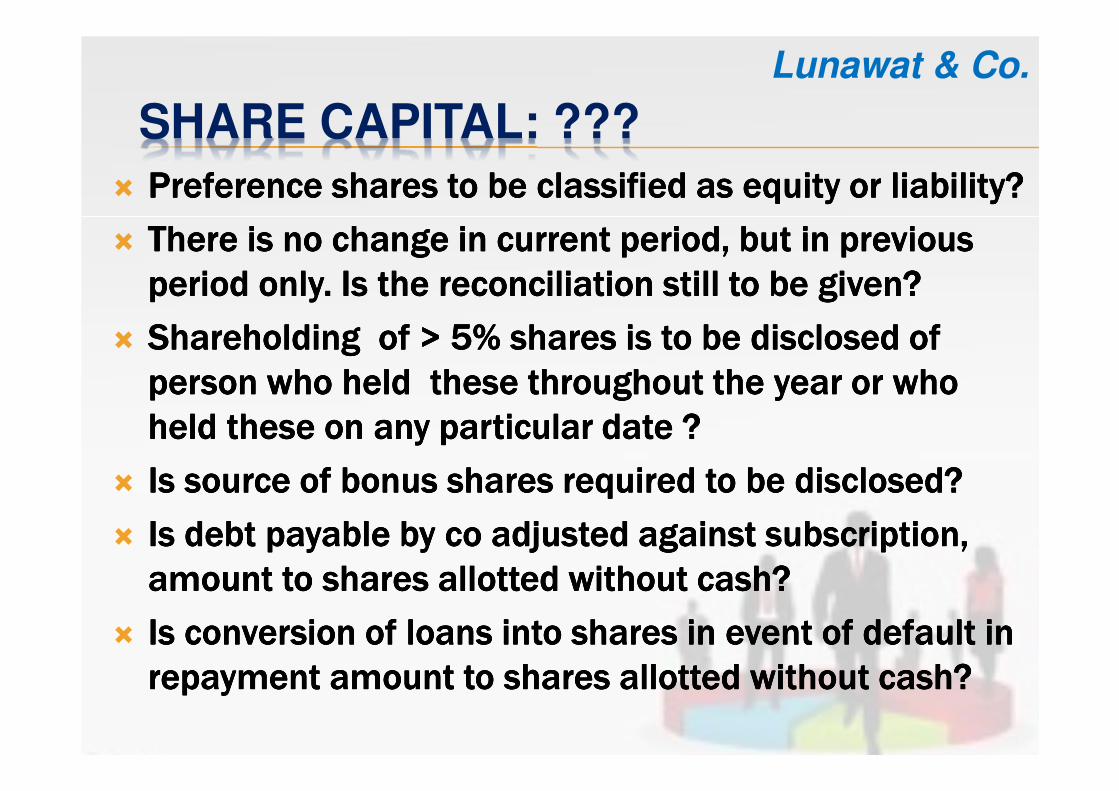

SHARE CAPITAL: ???

� Preference shares to be classified as equity or liability?Preference shares to be classified as equity or liability?Preference shares to be classified as equity or liability?Preference shares to be classified as equity or liability?

� There is no change in current period, but in previous There is no change in current period, but in previous There is no change in current period, but in previous There is no change in current period, but in previous

period only. Is the reconciliation still to be given?period only. Is the reconciliation still to be given?period only. Is the reconciliation still to be given?period only. Is the reconciliation still to be given?

� Shareholding of > 5% shares is to be disclosed of Shareholding of > 5% shares is to be disclosed of Shareholding of > 5% shares is to be disclosed of Shareholding of > 5% shares is to be disclosed of

person who held these throughout the year or who person who held these throughout the year or who person who held these throughout the year or who person who held these throughout the year or who

held these on any particular date ?held these on any particular date ?held these on any particular date ?held these on any particular date ?

� Is source of bonus shares required to be disclosed?Is source of bonus shares required to be disclosed?Is source of bonus shares required to be disclosed?Is source of bonus shares required to be disclosed?

� Is debt payable by co adjusted against subscription, Is debt payable by co adjusted against subscription, Is debt payable by co adjusted against subscription, Is debt payable by co adjusted against subscription,

amount to shares allotted without cash?amount to shares allotted without cash?amount to shares allotted without cash?amount to shares allotted without cash?

� Is conversion of loans into shares in event of default in Is conversion of loans into shares in event of default in Is conversion of loans into shares in event of default in Is conversion of loans into shares in event of default in

repayment amount to shares allotted without cash?repayment amount to shares allotted without cash?repayment amount to shares allotted without cash?repayment amount to shares allotted without cash?

Lunawat & Co.

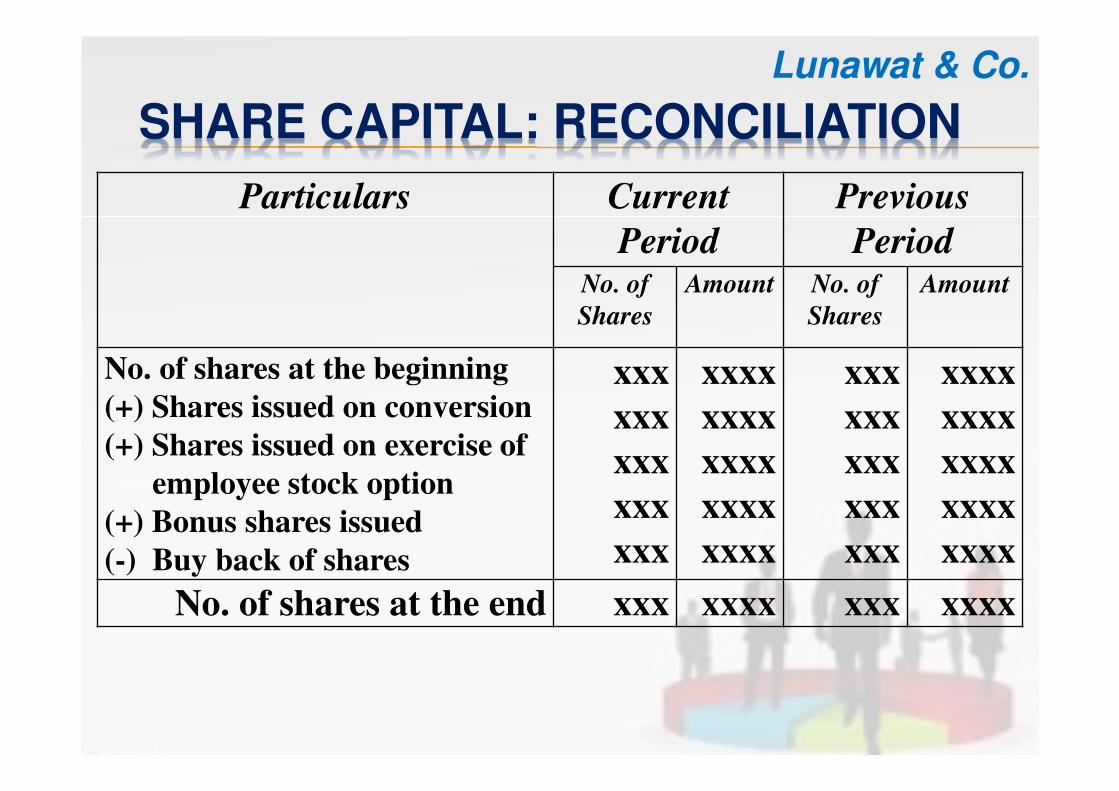

SHARE CAPITAL: RECONCILIATION

Particulars Current

Period

Previous

PeriodNo. of

Shares

Amount No. of

Shares

Amount

No. of shares at the beginning

(+) Shares issued on conversion

(+) Shares issued on exercise of

employee stock option

(+) Bonus shares issued

(-) Buy back of shares

xxx

xxx

xxx

xxx

xxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxx

xxx

xxx

xxx

xxx

xxxx

xxxx

xxxx

xxxx

xxxx

No. of shares at the end xxx xxxx xxx xxxx

Lunawat & Co.

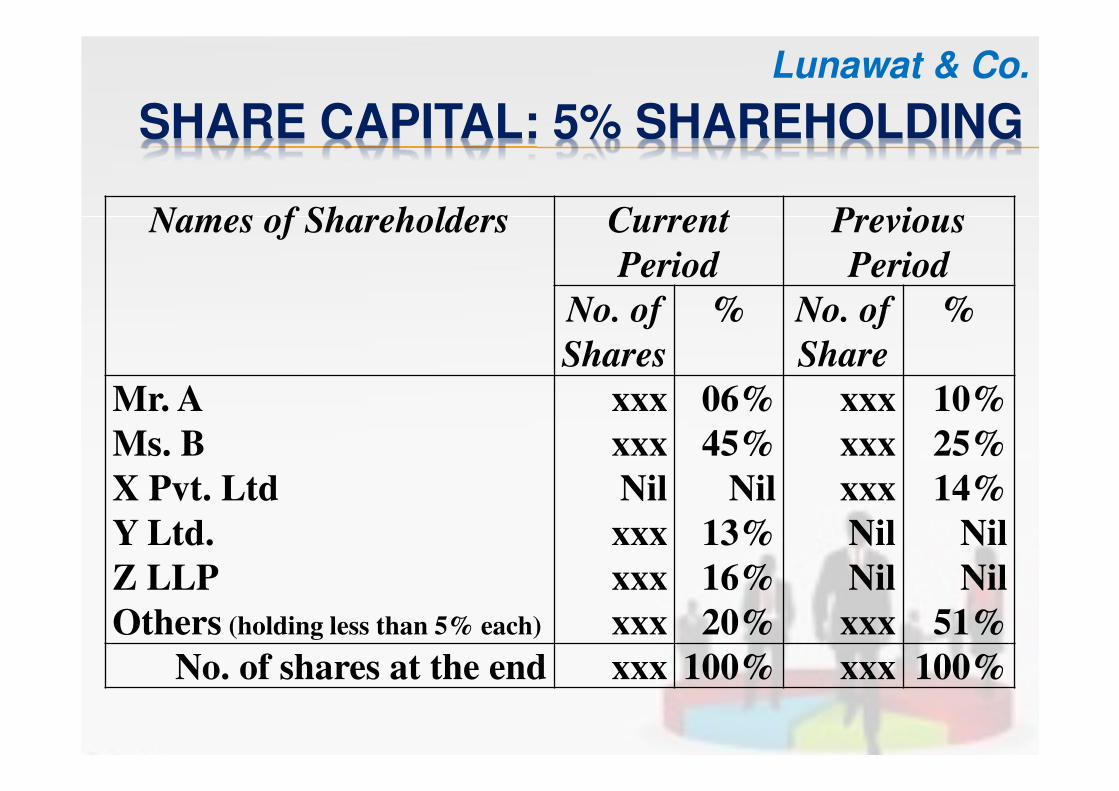

SHARE CAPITAL: 5% SHAREHOLDING

Names of Shareholders Current

Period

Previous

Period

No. of

Shares

% No. of

Share

%

Mr. A

Ms. B

X Pvt. Ltd

Y Ltd.

Z LLP

Others (holding less than 5% each)

xxx

xxx

Nil

xxx

xxx

xxx

06%

45%

Nil

13%

16%

20%

xxx

xxx

xxx

Nil

Nil

xxx

10%

25%

14%

Nil

Nil

51%

No. of shares at the end xxx 100% xxx 100%

Lunawat & Co.

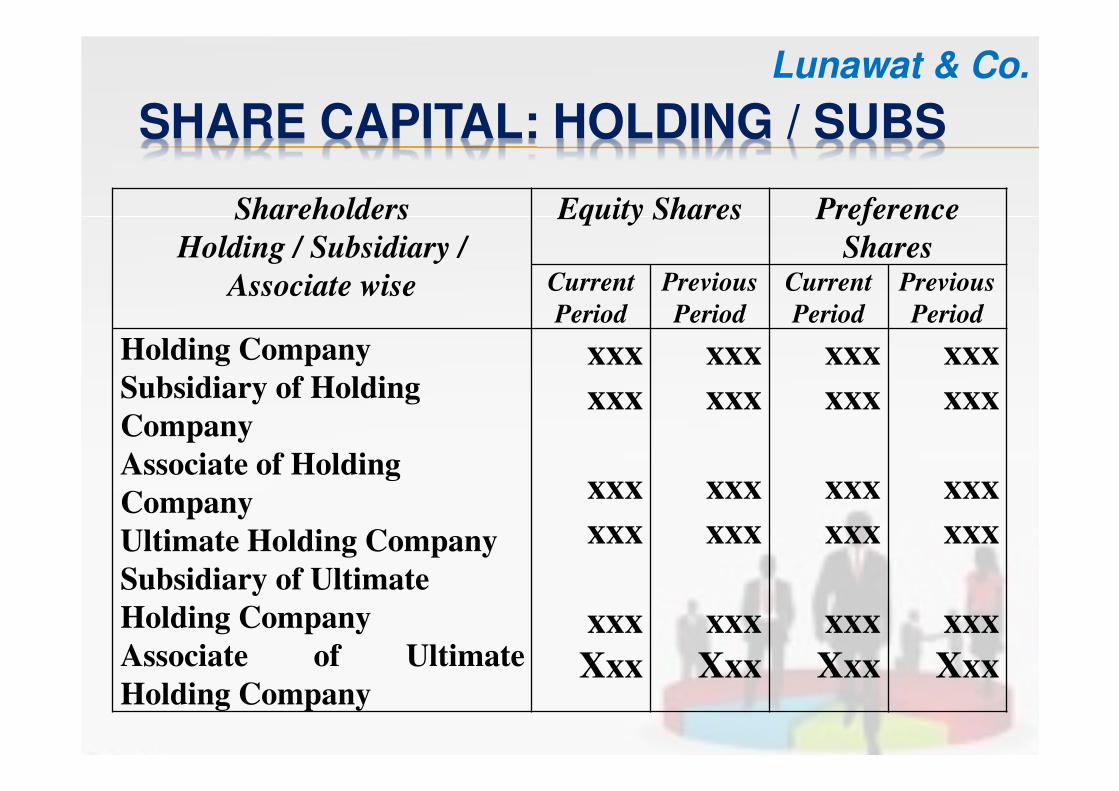

SHARE CAPITAL: HOLDING / SUBS

Shareholders

Holding / Subsidiary /

Associate wise

Equity Shares Preference

SharesCurrent

Period

Previous

Period

Current

Period

Previous

Period

Holding Company

Subsidiary of Holding

Company

Associate of Holding

Company

Ultimate Holding Company

Subsidiary of Ultimate

Holding Company

Associate of Ultimate

Holding Company

xxx

xxx

xxx

xxx

xxx

Xxx

xxx

xxx

xxx

xxx

xxx

Xxx

xxx

xxx

xxx

xxx

xxx

Xxx

xxx

xxx

xxx

xxx

xxx

Xxx

Lunawat & Co.

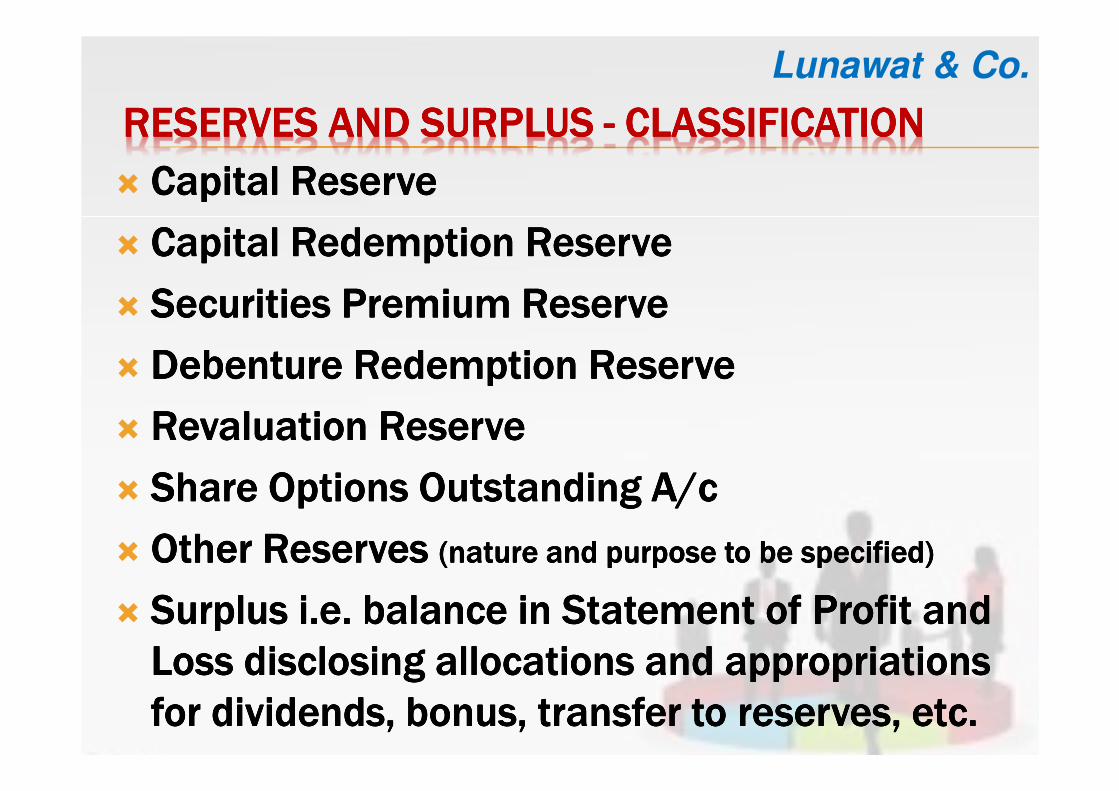

RESERVES AND SURPLUS RESERVES AND SURPLUS RESERVES AND SURPLUS RESERVES AND SURPLUS ---- CLASSIFICATIONCLASSIFICATIONCLASSIFICATIONCLASSIFICATION

� Capital ReserveCapital ReserveCapital ReserveCapital Reserve

� Capital Redemption ReserveCapital Redemption ReserveCapital Redemption ReserveCapital Redemption Reserve

� Securities Premium ReserveSecurities Premium ReserveSecurities Premium ReserveSecurities Premium Reserve

� Debenture Redemption ReserveDebenture Redemption ReserveDebenture Redemption ReserveDebenture Redemption Reserve

� Revaluation ReserveRevaluation ReserveRevaluation ReserveRevaluation Reserve

� Share Options Outstanding A/cShare Options Outstanding A/cShare Options Outstanding A/cShare Options Outstanding A/c

� Other Reserves Other Reserves Other Reserves Other Reserves (nature and purpose to be specified)(nature and purpose to be specified)(nature and purpose to be specified)(nature and purpose to be specified)

� Surplus i.e. balance in Statement of Profit and Surplus i.e. balance in Statement of Profit and Surplus i.e. balance in Statement of Profit and Surplus i.e. balance in Statement of Profit and

Loss disclosing allocations and appropriations Loss disclosing allocations and appropriations Loss disclosing allocations and appropriations Loss disclosing allocations and appropriations

for dividends, bonus, transfer to reserves, etc.for dividends, bonus, transfer to reserves, etc.for dividends, bonus, transfer to reserves, etc.for dividends, bonus, transfer to reserves, etc.

Lunawat & Co.

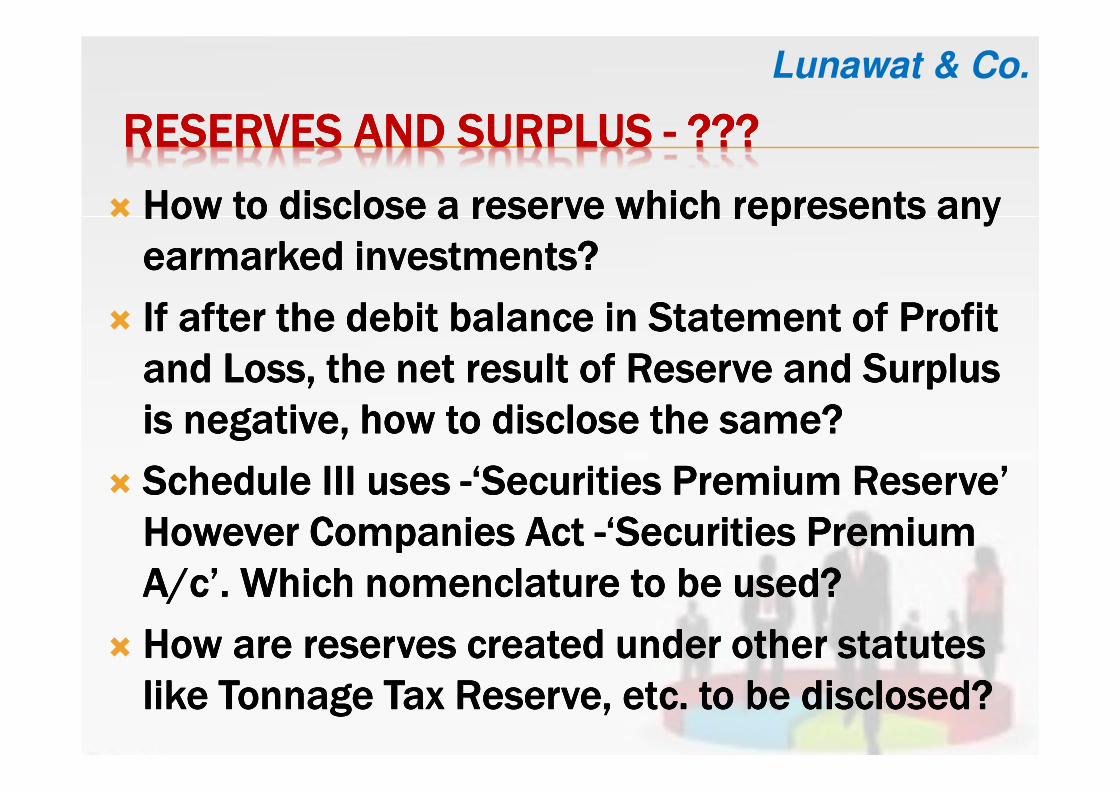

RESERVES AND SURPLUS RESERVES AND SURPLUS RESERVES AND SURPLUS RESERVES AND SURPLUS ---- ????????????

� How to disclose a reserve which represents any How to disclose a reserve which represents any How to disclose a reserve which represents any How to disclose a reserve which represents any

earmarked investments?earmarked investments?earmarked investments?earmarked investments?

� If after the debit balance in Statement of Profit If after the debit balance in Statement of Profit If after the debit balance in Statement of Profit If after the debit balance in Statement of Profit

and Loss, the net result of Reserve and Surplus and Loss, the net result of Reserve and Surplus and Loss, the net result of Reserve and Surplus and Loss, the net result of Reserve and Surplus

is negative, how to disclose the same?is negative, how to disclose the same?is negative, how to disclose the same?is negative, how to disclose the same?

� Schedule III uses Schedule III uses Schedule III uses Schedule III uses ----‘Securities Premium Reserve’ ‘Securities Premium Reserve’ ‘Securities Premium Reserve’ ‘Securities Premium Reserve’

However Companies Act However Companies Act However Companies Act However Companies Act ----‘Securities Premium ‘Securities Premium ‘Securities Premium ‘Securities Premium

A/c’. Which nomenclature to be used?A/c’. Which nomenclature to be used?A/c’. Which nomenclature to be used?A/c’. Which nomenclature to be used?

� How are reserves created under other statutes How are reserves created under other statutes How are reserves created under other statutes How are reserves created under other statutes

like Tonnage Tax Reserve, etc. to be disclosed?like Tonnage Tax Reserve, etc. to be disclosed?like Tonnage Tax Reserve, etc. to be disclosed?like Tonnage Tax Reserve, etc. to be disclosed?

Lunawat & Co.

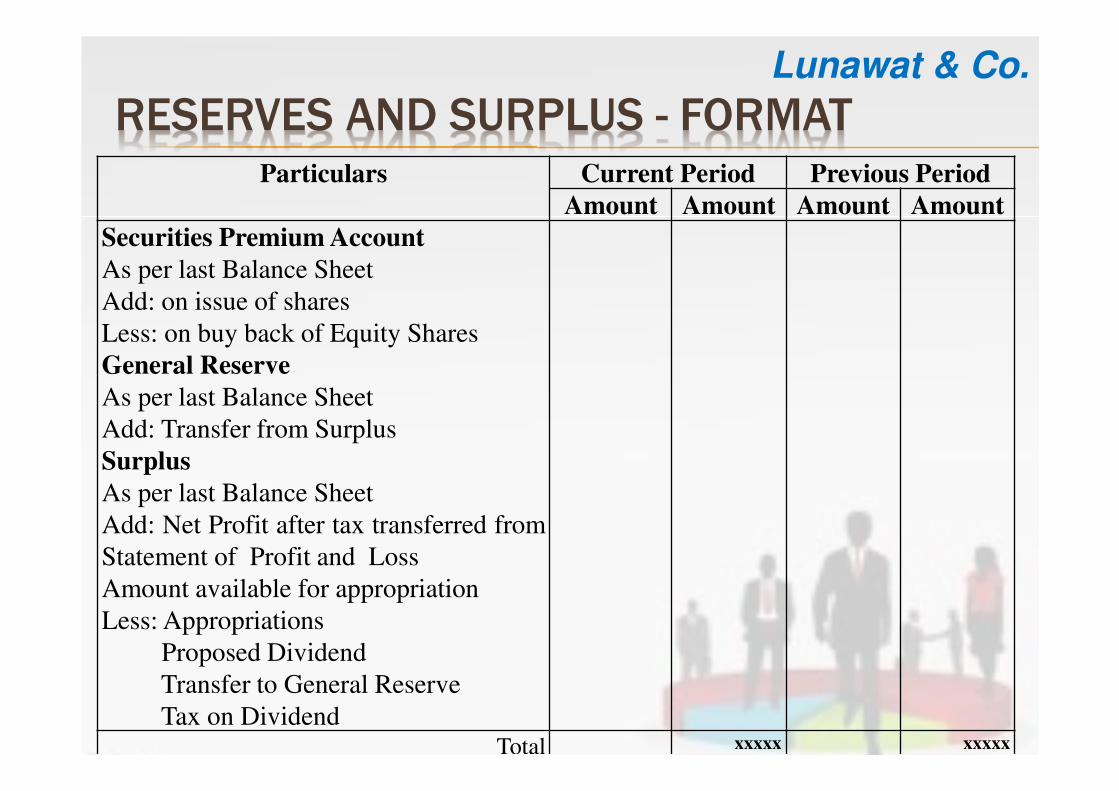

RESERVES AND SURPLUS - FORMATParticulars Current Period Previous Period

Amount Amount Amount Amount

Securities Premium Account

As per last Balance Sheet

Add: on issue of shares

Less: on buy back of Equity Shares

General Reserve

As per last Balance Sheet

Add: Transfer from Surplus

Surplus

As per last Balance Sheet

Add: Net Profit after tax transferred from

Statement of Profit and Loss

Amount available for appropriation

Less: Appropriations

Proposed Dividend

Transfer to General Reserve

Tax on DividendTotal xxxxx xxxxx

Lunawat & Co.

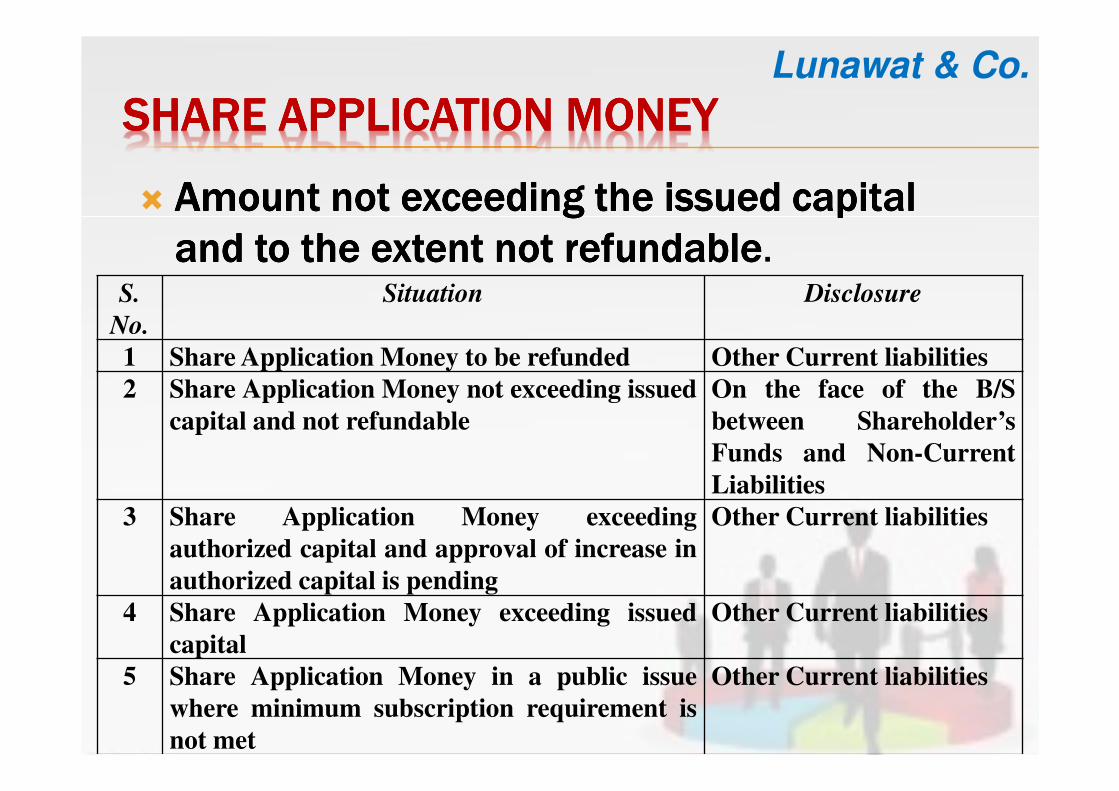

SHARE APPLICATION MONEYSHARE APPLICATION MONEYSHARE APPLICATION MONEYSHARE APPLICATION MONEY

� Amount not exceeding the issued capital Amount not exceeding the issued capital Amount not exceeding the issued capital Amount not exceeding the issued capital

and to the extent not refundableand to the extent not refundableand to the extent not refundableand to the extent not refundable.S.

No.

Situation Disclosure

1 Share Application Money to be refunded Other Current liabilities

2 Share Application Money not exceeding issued

capital and not refundable

On the face of the B/S

between Shareholder’s

Funds and Non-Current

Liabilities

3 Share Application Money exceeding

authorized capital and approval of increase in

authorized capital is pending

Other Current liabilities

4 Share Application Money exceeding issued

capital

Other Current liabilities

5 Share Application Money in a public issue

where minimum subscription requirement is

not met

Other Current liabilities

Lunawat & Co.

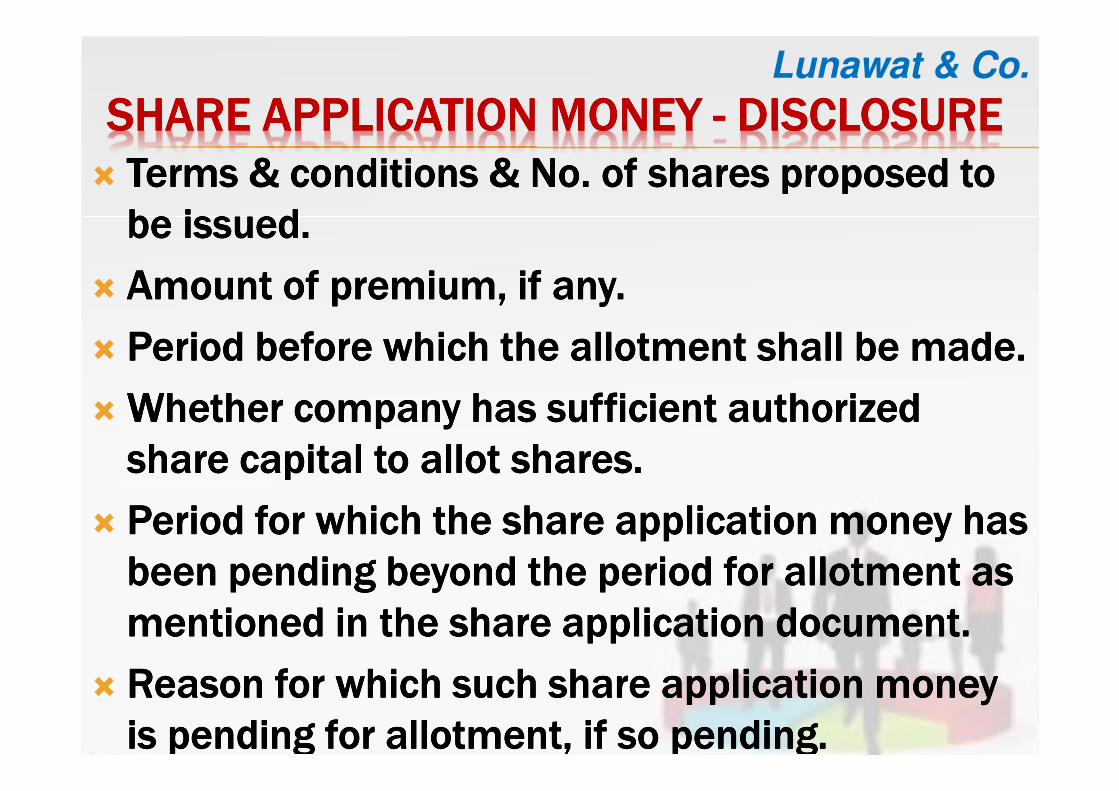

SHARE APPLICATION MONEY SHARE APPLICATION MONEY SHARE APPLICATION MONEY SHARE APPLICATION MONEY ---- DISCLOSUREDISCLOSUREDISCLOSUREDISCLOSURE

� Terms & conditions & No. of shares proposed to Terms & conditions & No. of shares proposed to Terms & conditions & No. of shares proposed to Terms & conditions & No. of shares proposed to

be issued.be issued.be issued.be issued.

� Amount of premium, if any.Amount of premium, if any.Amount of premium, if any.Amount of premium, if any.

� Period before which the allotment shall be made.Period before which the allotment shall be made.Period before which the allotment shall be made.Period before which the allotment shall be made.

� Whether company has sufficient authorized Whether company has sufficient authorized Whether company has sufficient authorized Whether company has sufficient authorized

share capital to allot shares.share capital to allot shares.share capital to allot shares.share capital to allot shares.

� Period for which the share application money has Period for which the share application money has Period for which the share application money has Period for which the share application money has

been pending beyond the period for allotment as been pending beyond the period for allotment as been pending beyond the period for allotment as been pending beyond the period for allotment as

mentioned in the share application document.mentioned in the share application document.mentioned in the share application document.mentioned in the share application document.

� Reason for which such share application money Reason for which such share application money Reason for which such share application money Reason for which such share application money

is pending for allotment, if so pending.is pending for allotment, if so pending.is pending for allotment, if so pending.is pending for allotment, if so pending.

Lunawat & Co.

LIABILITIESLIABILITIESLIABILITIESLIABILITIES

(3) Non(3) Non(3) Non(3) Non----current liabilitiescurrent liabilitiescurrent liabilitiescurrent liabilities

� (a) Long term borrowings(a) Long term borrowings(a) Long term borrowings(a) Long term borrowings

� (b) Deferred tax liabilities (net)(b) Deferred tax liabilities (net)(b) Deferred tax liabilities (net)(b) Deferred tax liabilities (net)

� (c) Other long term liabilities(c) Other long term liabilities(c) Other long term liabilities(c) Other long term liabilities

� (d) Long term provisions(d) Long term provisions(d) Long term provisions(d) Long term provisions

(4) Current liabilities(4) Current liabilities(4) Current liabilities(4) Current liabilities

� (a) Short term borrowings(a) Short term borrowings(a) Short term borrowings(a) Short term borrowings

� (b) Trade payables(b) Trade payables(b) Trade payables(b) Trade payables

� (c) Other current liabilities(c) Other current liabilities(c) Other current liabilities(c) Other current liabilities

� (d) Short term provisions(d) Short term provisions(d) Short term provisions(d) Short term provisions

Lunawat & Co.

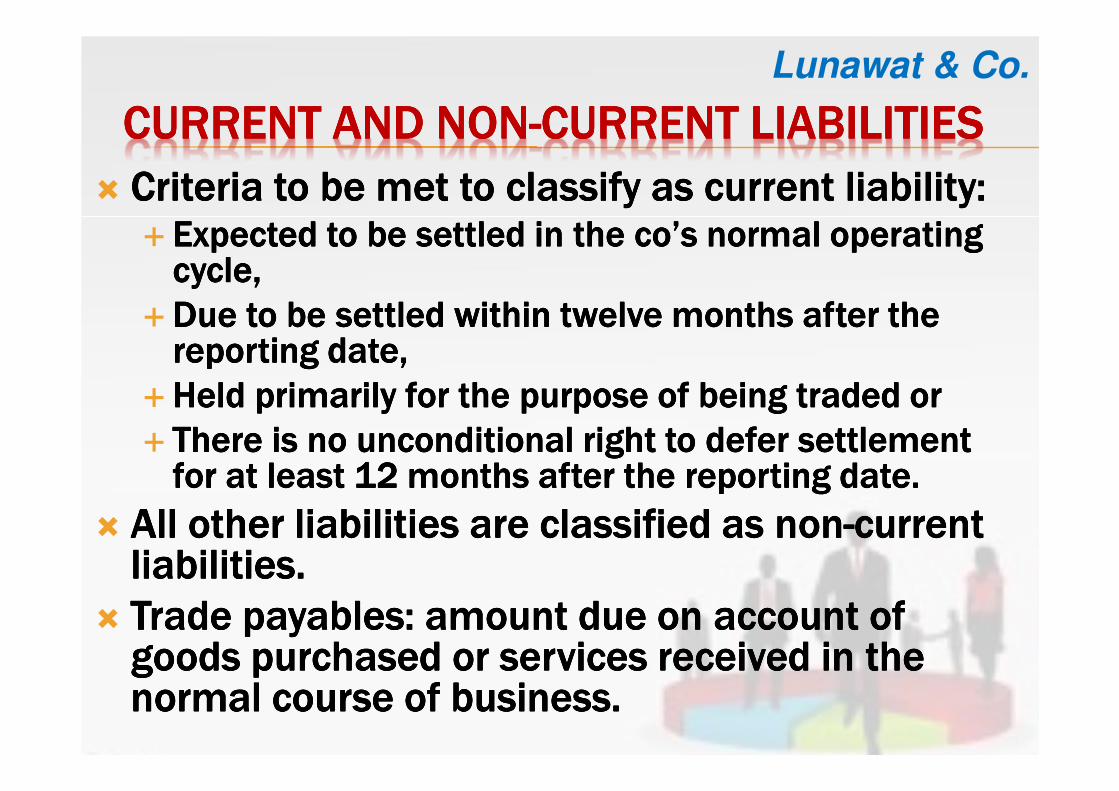

CURRENT AND NONCURRENT AND NONCURRENT AND NONCURRENT AND NON----CURRENT LIABILITIESCURRENT LIABILITIESCURRENT LIABILITIESCURRENT LIABILITIES

� Criteria to be met to classify as current liability:Criteria to be met to classify as current liability:Criteria to be met to classify as current liability:Criteria to be met to classify as current liability:� Expected to be settled in the Expected to be settled in the Expected to be settled in the Expected to be settled in the co’sco’sco’sco’s normal operating normal operating normal operating normal operating cycle,cycle,cycle,cycle,

�Due to be settled within twelve months after the Due to be settled within twelve months after the Due to be settled within twelve months after the Due to be settled within twelve months after the reporting date,reporting date,reporting date,reporting date,

�Held primarily for the purpose of being traded orHeld primarily for the purpose of being traded orHeld primarily for the purpose of being traded orHeld primarily for the purpose of being traded or

� There is no unconditional right to defer settlement There is no unconditional right to defer settlement There is no unconditional right to defer settlement There is no unconditional right to defer settlement for at least 12 months after the reporting date.for at least 12 months after the reporting date.for at least 12 months after the reporting date.for at least 12 months after the reporting date.

� All other liabilities are classified as nonAll other liabilities are classified as nonAll other liabilities are classified as nonAll other liabilities are classified as non----current current current current liabilities.liabilities.liabilities.liabilities.

� Trade payables: amount due on account of Trade payables: amount due on account of Trade payables: amount due on account of Trade payables: amount due on account of goods purchased or services received in the goods purchased or services received in the goods purchased or services received in the goods purchased or services received in the normal course of business.normal course of business.normal course of business.normal course of business.

Lunawat & Co.

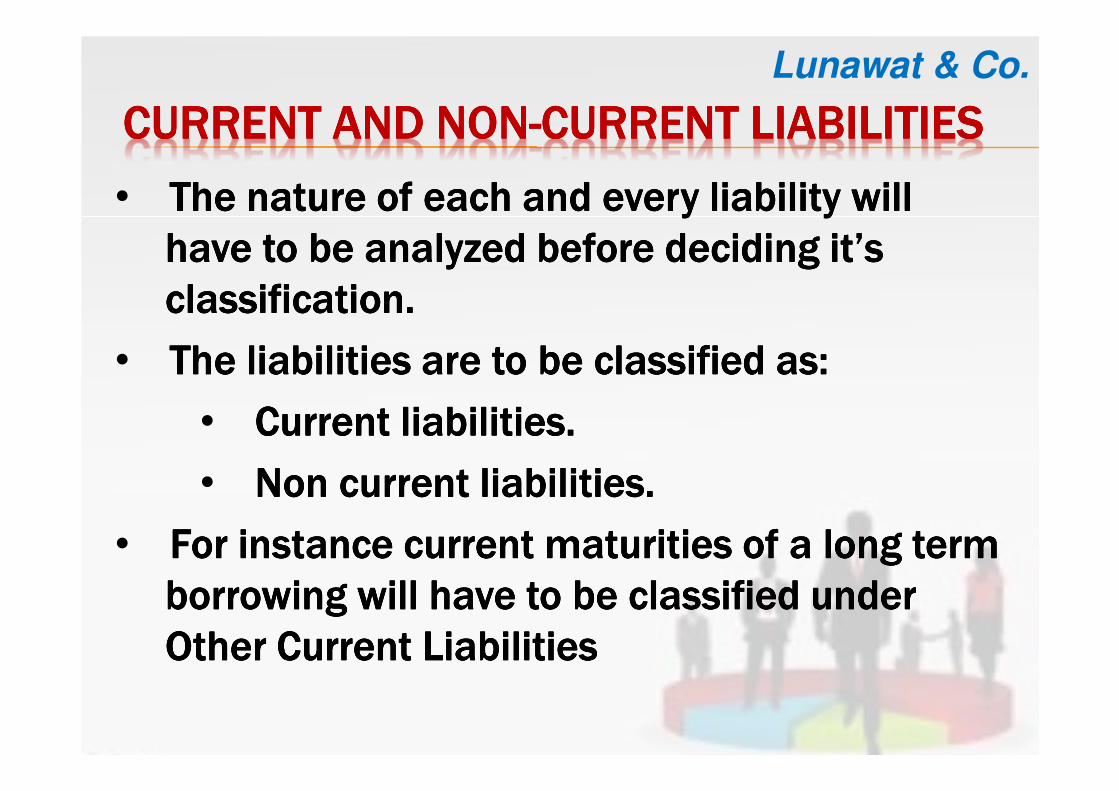

CURRENT AND NONCURRENT AND NONCURRENT AND NONCURRENT AND NON----CURRENT LIABILITIESCURRENT LIABILITIESCURRENT LIABILITIESCURRENT LIABILITIES

• The nature of each and every liability will The nature of each and every liability will The nature of each and every liability will The nature of each and every liability will

have to be analyzed before deciding it’s have to be analyzed before deciding it’s have to be analyzed before deciding it’s have to be analyzed before deciding it’s

classification.classification.classification.classification.

• The liabilities are to be classified as:The liabilities are to be classified as:The liabilities are to be classified as:The liabilities are to be classified as:

• Current liabilities.Current liabilities.Current liabilities.Current liabilities.

• Non current Non current Non current Non current liabilitiesliabilitiesliabilitiesliabilities. . . .

• For instance current maturities of a long term For instance current maturities of a long term For instance current maturities of a long term For instance current maturities of a long term

borrowing will have to be classified under borrowing will have to be classified under borrowing will have to be classified under borrowing will have to be classified under

Other Current LiabilitiesOther Current LiabilitiesOther Current LiabilitiesOther Current Liabilities

Lunawat & Co.

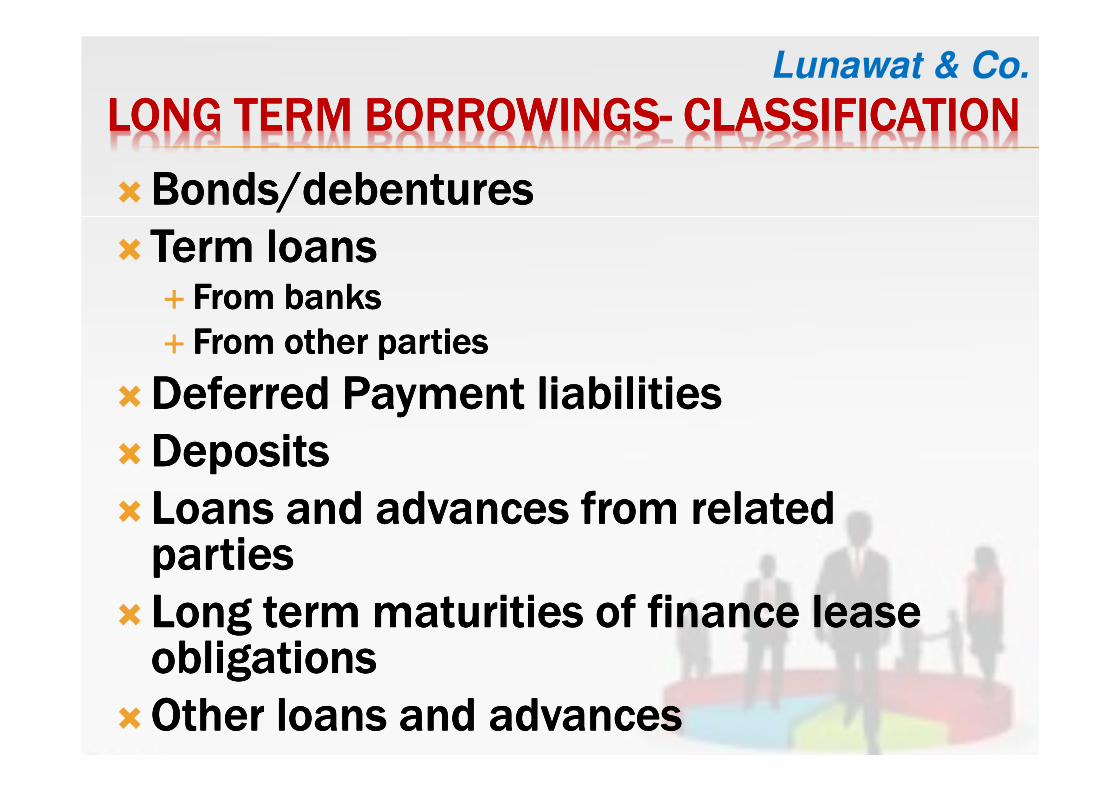

LONG TERM BORROWINGSLONG TERM BORROWINGSLONG TERM BORROWINGSLONG TERM BORROWINGS---- CLASSIFICATIONCLASSIFICATIONCLASSIFICATIONCLASSIFICATION

�Bonds/debenturesBonds/debenturesBonds/debenturesBonds/debentures

�Term loansTerm loansTerm loansTerm loans� From banksFrom banksFrom banksFrom banks

� From other partiesFrom other partiesFrom other partiesFrom other parties

�Deferred Payment liabilitiesDeferred Payment liabilitiesDeferred Payment liabilitiesDeferred Payment liabilities

�DepositsDepositsDepositsDeposits

�Loans and advances from related Loans and advances from related Loans and advances from related Loans and advances from related partiespartiespartiesparties

�Long term maturities of finance lease Long term maturities of finance lease Long term maturities of finance lease Long term maturities of finance lease obligationsobligationsobligationsobligations

�Other loans and advancesOther loans and advancesOther loans and advancesOther loans and advances

Lunawat & Co.

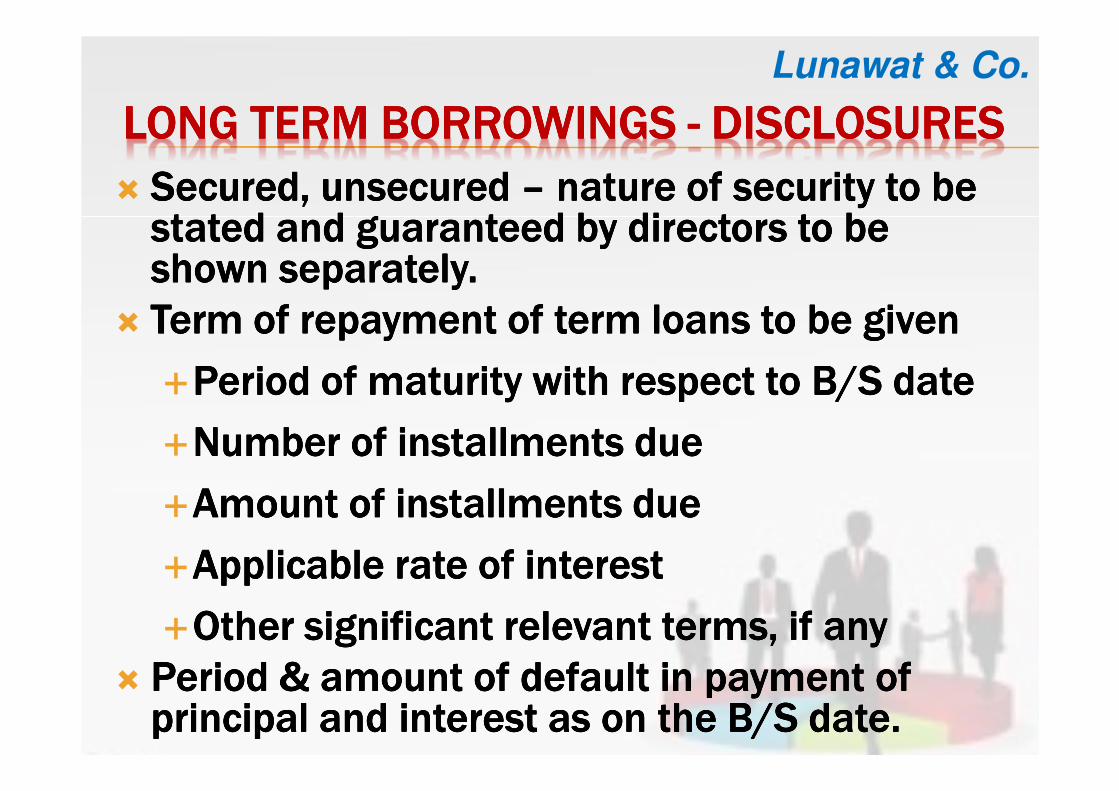

LONG TERM BORROWINGS LONG TERM BORROWINGS LONG TERM BORROWINGS LONG TERM BORROWINGS ---- DISCLOSURESDISCLOSURESDISCLOSURESDISCLOSURES

� Secured, unsecured Secured, unsecured Secured, unsecured Secured, unsecured –––– nature of security to be nature of security to be nature of security to be nature of security to be stated and guaranteed by directors to be stated and guaranteed by directors to be stated and guaranteed by directors to be stated and guaranteed by directors to be shown separately.shown separately.shown separately.shown separately.

� Term of repayment of term loans to be givenTerm of repayment of term loans to be givenTerm of repayment of term loans to be givenTerm of repayment of term loans to be given

�Period of maturity with respect to B/S datePeriod of maturity with respect to B/S datePeriod of maturity with respect to B/S datePeriod of maturity with respect to B/S date

�Number of installments dueNumber of installments dueNumber of installments dueNumber of installments due

�Amount of installments dueAmount of installments dueAmount of installments dueAmount of installments due

�Applicable rate of interestApplicable rate of interestApplicable rate of interestApplicable rate of interest

�Other significant relevant terms, if anyOther significant relevant terms, if anyOther significant relevant terms, if anyOther significant relevant terms, if any

� Period & amount of default in payment of Period & amount of default in payment of Period & amount of default in payment of Period & amount of default in payment of principal and interest as on the B/S date.principal and interest as on the B/S date.principal and interest as on the B/S date.principal and interest as on the B/S date.

Lunawat & Co.

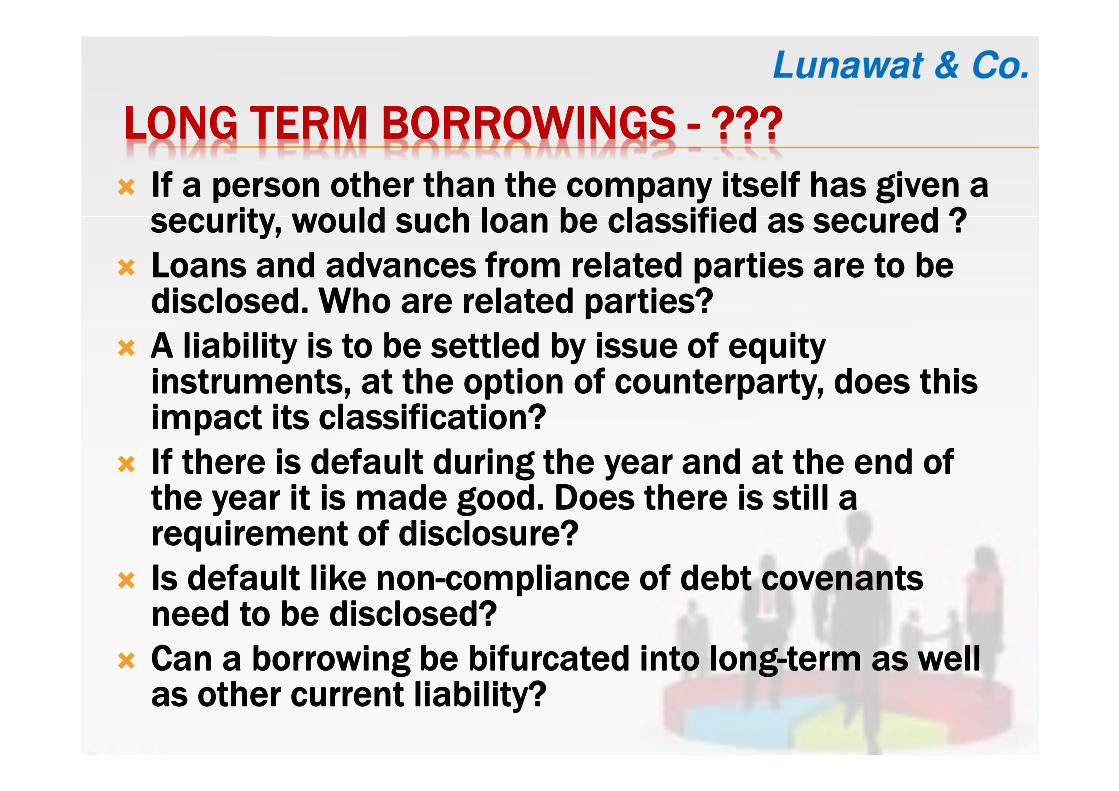

LONG TERM BORROWINGS LONG TERM BORROWINGS LONG TERM BORROWINGS LONG TERM BORROWINGS ---- ????????????

� If a person other than the company itself has given a If a person other than the company itself has given a If a person other than the company itself has given a If a person other than the company itself has given a security, would such loan be classified as secured ?security, would such loan be classified as secured ?security, would such loan be classified as secured ?security, would such loan be classified as secured ?

� Loans and advances from related parties are to be Loans and advances from related parties are to be Loans and advances from related parties are to be Loans and advances from related parties are to be disclosed. Who are related parties?disclosed. Who are related parties?disclosed. Who are related parties?disclosed. Who are related parties?

� A liability is to be settled by issue of equity A liability is to be settled by issue of equity A liability is to be settled by issue of equity A liability is to be settled by issue of equity instruments, at the option of counterparty, does this instruments, at the option of counterparty, does this instruments, at the option of counterparty, does this instruments, at the option of counterparty, does this impact its classification?impact its classification?impact its classification?impact its classification?

� If there is default during the year and at the end of If there is default during the year and at the end of If there is default during the year and at the end of If there is default during the year and at the end of the year it is made good. Does there is still a the year it is made good. Does there is still a the year it is made good. Does there is still a the year it is made good. Does there is still a requirement of disclosure?requirement of disclosure?requirement of disclosure?requirement of disclosure?

� Is default like nonIs default like nonIs default like nonIs default like non----compliance of debt covenants compliance of debt covenants compliance of debt covenants compliance of debt covenants need to be disclosed?need to be disclosed?need to be disclosed?need to be disclosed?

� Can a borrowing be bifurcated into longCan a borrowing be bifurcated into longCan a borrowing be bifurcated into longCan a borrowing be bifurcated into long----term as well term as well term as well term as well as other current liability?as other current liability?as other current liability?as other current liability?

Lunawat & Co.

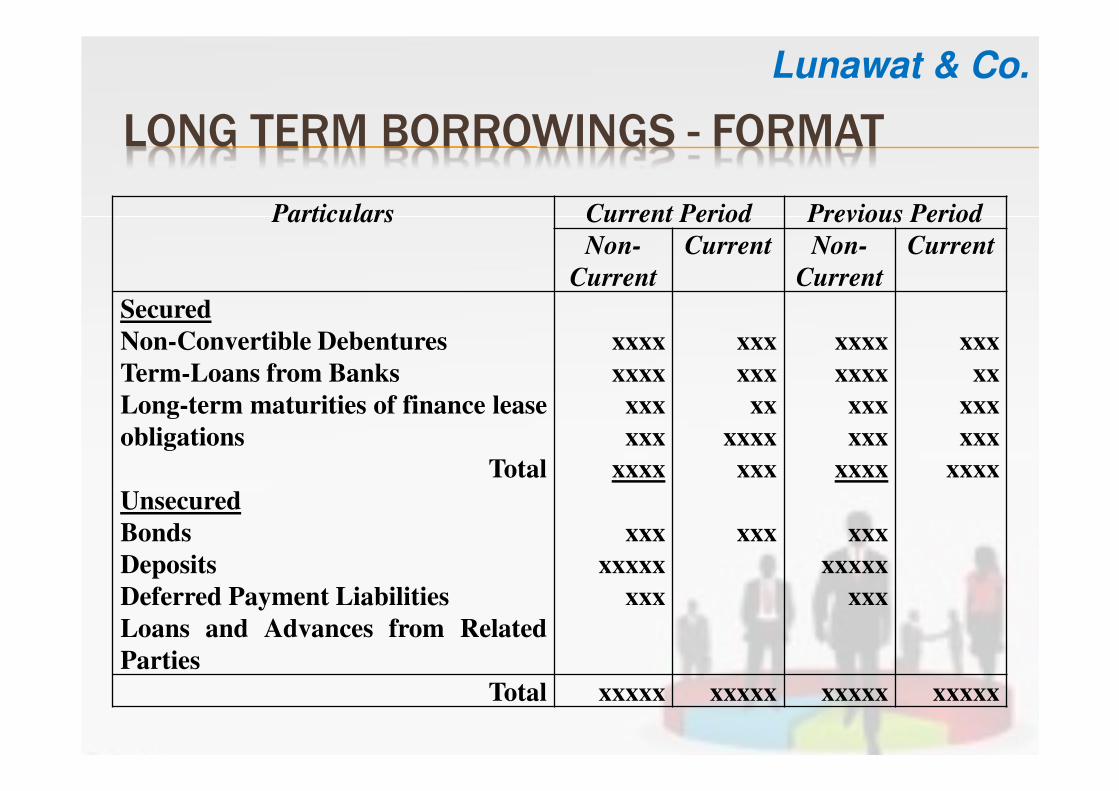

LONG TERM BORROWINGS - FORMAT

Particulars Current Period Previous Period

Non-

Current

Current Non-

Current

Current

Secured

Non-Convertible Debentures

Term-Loans from Banks

Long-term maturities of finance lease

obligations

Total

Unsecured

Bonds

Deposits

Deferred Payment Liabilities

Loans and Advances from Related

Parties

xxxx

xxxx

xxx

xxx

xxxx

xxx

xxxxx

xxx

xxx

xxx

xx

xxxx

xxx

xxx

xxxx

xxxx

xxx

xxx

xxxx

xxx

xxxxx

xxx

xxx

xx

xxx

xxx

xxxx

Total xxxxx xxxxx xxxxx xxxxx

Lunawat & Co.

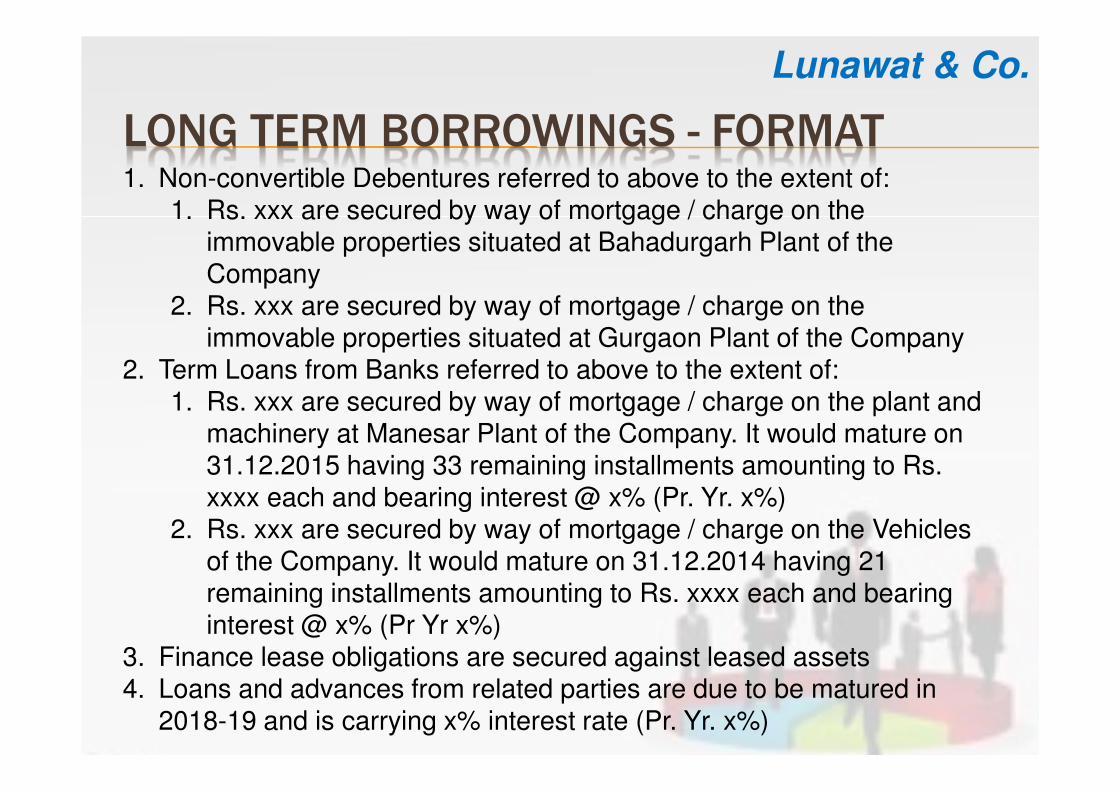

LONG TERM BORROWINGS - FORMAT1. Non-convertible Debentures referred to above to the extent of:

1. Rs. xxx are secured by way of mortgage / charge on the immovable properties situated at Bahadurgarh Plant of the Company

2. Rs. xxx are secured by way of mortgage / charge on the immovable properties situated at Gurgaon Plant of the Company

2. Term Loans from Banks referred to above to the extent of:1. Rs. xxx are secured by way of mortgage / charge on the plant and

machinery at Manesar Plant of the Company. It would mature on 31.12.2015 having 33 remaining installments amounting to Rs. xxxx each and bearing interest @ x% (Pr. Yr. x%)

2. Rs. xxx are secured by way of mortgage / charge on the Vehicles of the Company. It would mature on 31.12.2014 having 21 remaining installments amounting to Rs. xxxx each and bearing interest @ x% (Pr Yr x%)

3. Finance lease obligations are secured against leased assets4. Loans and advances from related parties are due to be matured in

2018-19 and is carrying x% interest rate (Pr. Yr. x%)

Lunawat & Co.

LONG TERM BORROWINGS - FORMAT

Rate of

Interest

Maturity Profile

2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

X% xx xx xx xx - -

X% - - - xx xx -

X% - - - - - xx

5. Maturity profile and rate of interest of non5. Maturity profile and rate of interest of non5. Maturity profile and rate of interest of non5. Maturity profile and rate of interest of non----convertible debentures are as under:convertible debentures are as under:convertible debentures are as under:convertible debentures are as under:

6. Maturity profile and rate of interest of bonds are as under:6. Maturity profile and rate of interest of bonds are as under:6. Maturity profile and rate of interest of bonds are as under:6. Maturity profile and rate of interest of bonds are as under:Rate of

Interest

Maturity Profile

2015-16 2018-19 2022-23 2031-32 2052-53 2053-54

X% xx xx xx xx - -

X% - - - xx xx -

X% - - - - xx xx

7. Maturity profile and rate of interest of deposits are as under:7. Maturity profile and rate of interest of deposits are as under:7. Maturity profile and rate of interest of deposits are as under:7. Maturity profile and rate of interest of deposits are as under:

Rate of

Interest

Maturity Profile

2012-13 2013-14 2014-15 2015-16 2016-17

X% xx xx xx - -

X% xx xx xx xx xx

X% xx xx xx xx -

Lunawat & Co.

DEFERRED TAX LIABILITYDEFERRED TAX LIABILITYDEFERRED TAX LIABILITYDEFERRED TAX LIABILITY

� To be disclosed as nonTo be disclosed as nonTo be disclosed as nonTo be disclosed as non---- current liability in current liability in current liability in current liability in

Schedule IIISchedule IIISchedule IIISchedule III

� Para 30 of ASPara 30 of ASPara 30 of ASPara 30 of AS---- 22222222---- presentationpresentationpresentationpresentation---- after the after the after the after the

head ‘unsecured loan’ ?head ‘unsecured loan’ ?head ‘unsecured loan’ ?head ‘unsecured loan’ ?

� It is being amended by revision to AS 22It is being amended by revision to AS 22It is being amended by revision to AS 22It is being amended by revision to AS 22

� Para 31 of ASPara 31 of ASPara 31 of ASPara 31 of AS---- 22 22 22 22 –––– breakup of major breakup of major breakup of major breakup of major

components of the respective balances to be components of the respective balances to be components of the respective balances to be components of the respective balances to be

disclosed.disclosed.disclosed.disclosed.

Lunawat & Co.

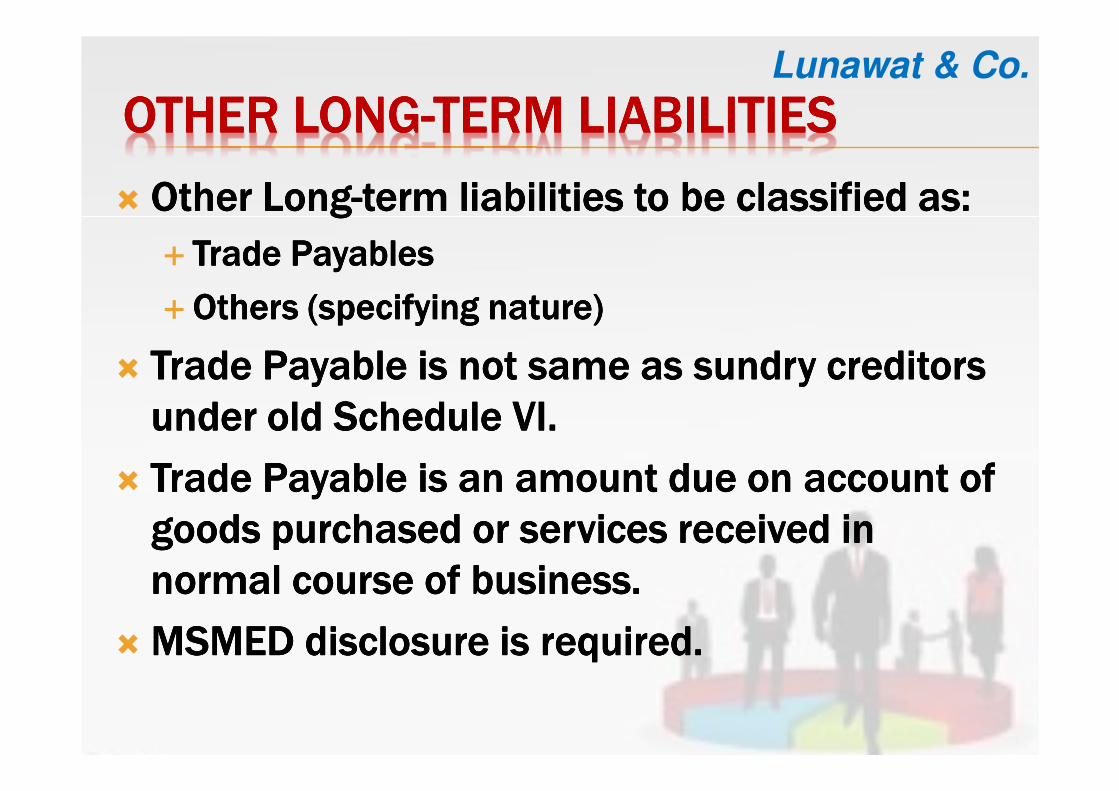

OTHER LONGOTHER LONGOTHER LONGOTHER LONG----TERM LIABILITIESTERM LIABILITIESTERM LIABILITIESTERM LIABILITIES

� Other LongOther LongOther LongOther Long----term liabilities to be classified as:term liabilities to be classified as:term liabilities to be classified as:term liabilities to be classified as:

� Trade PayablesTrade PayablesTrade PayablesTrade Payables

�Others (specifying nature)Others (specifying nature)Others (specifying nature)Others (specifying nature)

� Trade Payable is not same as sundry creditors Trade Payable is not same as sundry creditors Trade Payable is not same as sundry creditors Trade Payable is not same as sundry creditors

under old Schedule VI.under old Schedule VI.under old Schedule VI.under old Schedule VI.

� Trade Payable is an amount due on account of Trade Payable is an amount due on account of Trade Payable is an amount due on account of Trade Payable is an amount due on account of

goods purchased or services received in goods purchased or services received in goods purchased or services received in goods purchased or services received in

normal course of business. normal course of business. normal course of business. normal course of business.

� MSMED disclosure is required.MSMED disclosure is required.MSMED disclosure is required.MSMED disclosure is required.

Lunawat & Co.

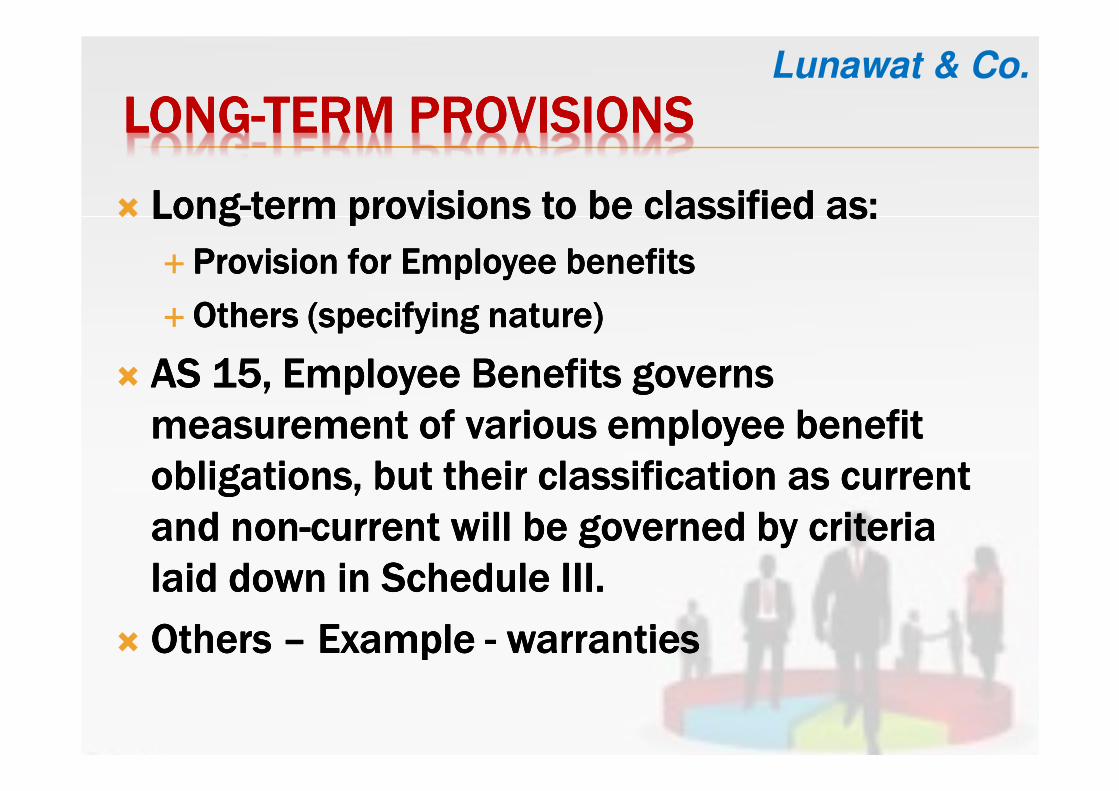

LONGLONGLONGLONG----TERM PROVISIONSTERM PROVISIONSTERM PROVISIONSTERM PROVISIONS

� LongLongLongLong----term provisions to be classified as:term provisions to be classified as:term provisions to be classified as:term provisions to be classified as:

� Provision for Employee benefitsProvision for Employee benefitsProvision for Employee benefitsProvision for Employee benefits

�Others (specifying nature)Others (specifying nature)Others (specifying nature)Others (specifying nature)

� AS 15, Employee Benefits governs AS 15, Employee Benefits governs AS 15, Employee Benefits governs AS 15, Employee Benefits governs

measurement of various employee benefit measurement of various employee benefit measurement of various employee benefit measurement of various employee benefit

obligations, but their classification as current obligations, but their classification as current obligations, but their classification as current obligations, but their classification as current

and nonand nonand nonand non----current will be governed by criteria current will be governed by criteria current will be governed by criteria current will be governed by criteria

laid down in Schedule III.laid down in Schedule III.laid down in Schedule III.laid down in Schedule III.

� Others Others Others Others –––– Example Example Example Example ---- warrantieswarrantieswarrantieswarranties

Lunawat & Co.

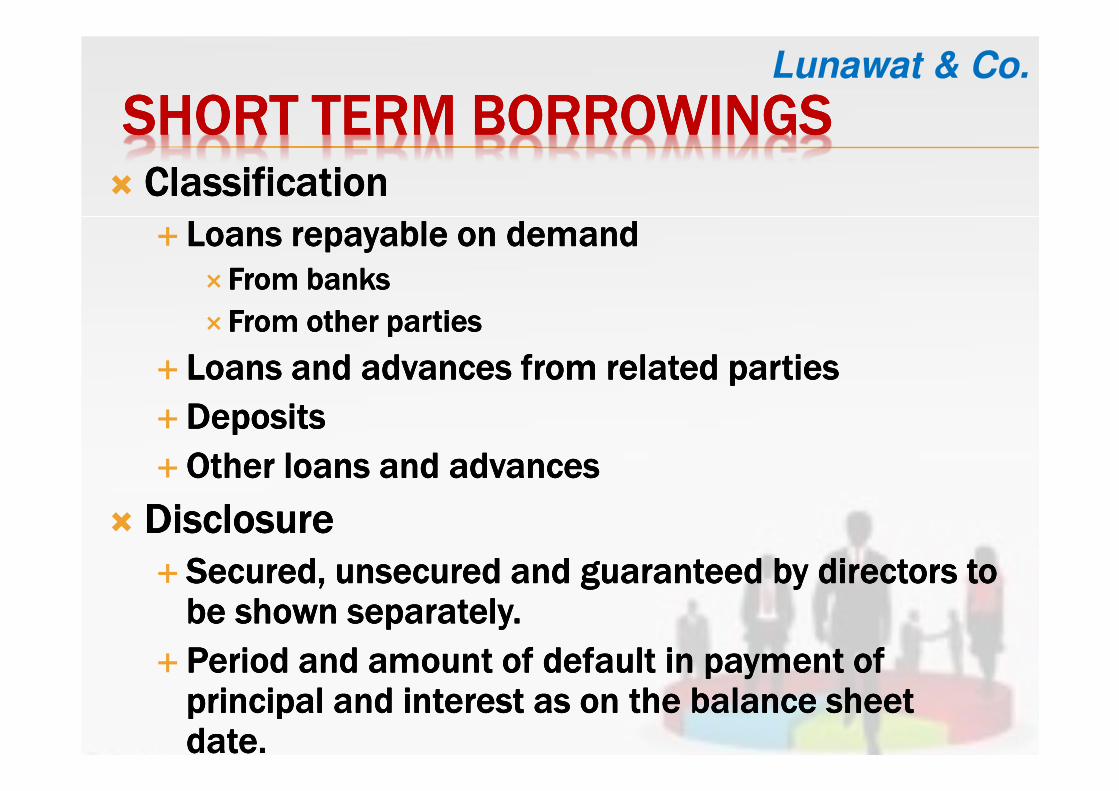

SHORT TERM BORROWINGSSHORT TERM BORROWINGSSHORT TERM BORROWINGSSHORT TERM BORROWINGS� ClassificationClassificationClassificationClassification

� Loans repayable on demandLoans repayable on demandLoans repayable on demandLoans repayable on demand

�From banksFrom banksFrom banksFrom banks

�From other partiesFrom other partiesFrom other partiesFrom other parties

� Loans and advances from related partiesLoans and advances from related partiesLoans and advances from related partiesLoans and advances from related parties

�DepositsDepositsDepositsDeposits

�Other loans and advancesOther loans and advancesOther loans and advancesOther loans and advances

� DisclosureDisclosureDisclosureDisclosure

� Secured, unsecured and guaranteed by directors to Secured, unsecured and guaranteed by directors to Secured, unsecured and guaranteed by directors to Secured, unsecured and guaranteed by directors to be shown separately.be shown separately.be shown separately.be shown separately.

� Period and amount of default in payment of Period and amount of default in payment of Period and amount of default in payment of Period and amount of default in payment of principal and interest as on the balance sheet principal and interest as on the balance sheet principal and interest as on the balance sheet principal and interest as on the balance sheet date.date.date.date.

Lunawat & Co.

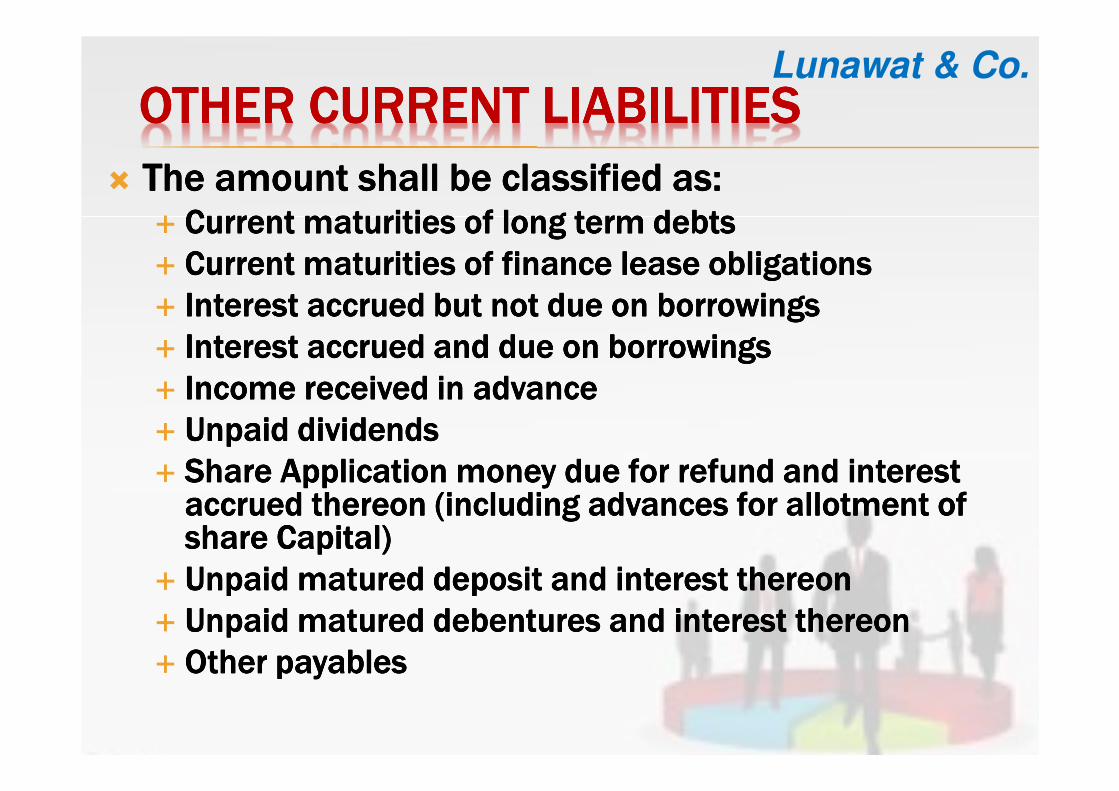

OTHER CURRENT LIABILITIESOTHER CURRENT LIABILITIESOTHER CURRENT LIABILITIESOTHER CURRENT LIABILITIES

� The amount shall be classified as:The amount shall be classified as:The amount shall be classified as:The amount shall be classified as:� Current maturities of long term debtsCurrent maturities of long term debtsCurrent maturities of long term debtsCurrent maturities of long term debts

� Current maturities of finance lease obligationsCurrent maturities of finance lease obligationsCurrent maturities of finance lease obligationsCurrent maturities of finance lease obligations

� Interest accrued but not due on borrowingsInterest accrued but not due on borrowingsInterest accrued but not due on borrowingsInterest accrued but not due on borrowings

� Interest accrued and due on borrowingsInterest accrued and due on borrowingsInterest accrued and due on borrowingsInterest accrued and due on borrowings

� Income received in advanceIncome received in advanceIncome received in advanceIncome received in advance

� Unpaid dividendsUnpaid dividendsUnpaid dividendsUnpaid dividends

� Share Application money due for refund and interest Share Application money due for refund and interest Share Application money due for refund and interest Share Application money due for refund and interest accrued thereon (including advances for allotment of accrued thereon (including advances for allotment of accrued thereon (including advances for allotment of accrued thereon (including advances for allotment of share Capital)share Capital)share Capital)share Capital)

� Unpaid matured deposit and interest thereonUnpaid matured deposit and interest thereonUnpaid matured deposit and interest thereonUnpaid matured deposit and interest thereon

� Unpaid matured debentures and interest thereonUnpaid matured debentures and interest thereonUnpaid matured debentures and interest thereonUnpaid matured debentures and interest thereon

� Other payablesOther payablesOther payablesOther payables

Lunawat & Co.

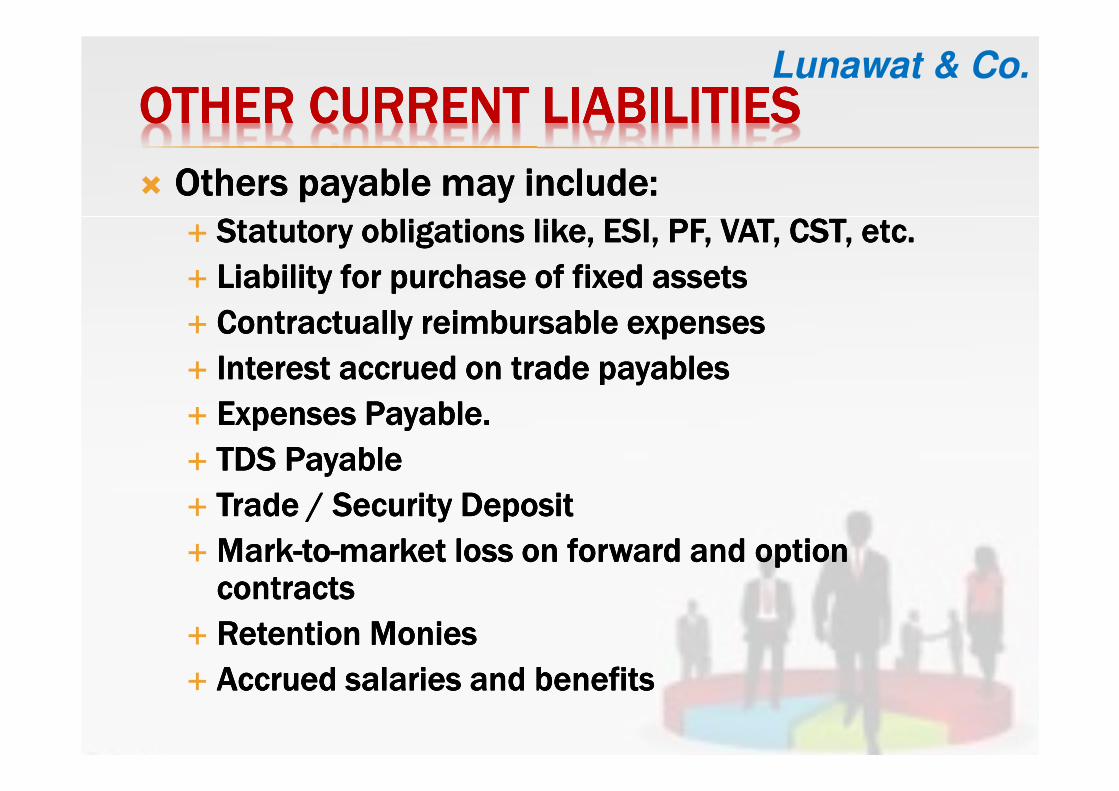

OTHER CURRENT LIABILITIES OTHER CURRENT LIABILITIES OTHER CURRENT LIABILITIES OTHER CURRENT LIABILITIES

� Others payable may include:Others payable may include:Others payable may include:Others payable may include:

� Statutory obligations like, ESI, PF, VAT, CST, etc.Statutory obligations like, ESI, PF, VAT, CST, etc.Statutory obligations like, ESI, PF, VAT, CST, etc.Statutory obligations like, ESI, PF, VAT, CST, etc.

� Liability for purchase of fixed assetsLiability for purchase of fixed assetsLiability for purchase of fixed assetsLiability for purchase of fixed assets

� Contractually reimbursable expensesContractually reimbursable expensesContractually reimbursable expensesContractually reimbursable expenses

� Interest accrued on trade payablesInterest accrued on trade payablesInterest accrued on trade payablesInterest accrued on trade payables

� Expenses Payable.Expenses Payable.Expenses Payable.Expenses Payable.

� TDS PayableTDS PayableTDS PayableTDS Payable

� Trade / Security DepositTrade / Security DepositTrade / Security DepositTrade / Security Deposit

� MarkMarkMarkMark----totototo----market loss on forward and option market loss on forward and option market loss on forward and option market loss on forward and option contractscontractscontractscontracts

� Retention MoniesRetention MoniesRetention MoniesRetention Monies

� Accrued salaries and benefitsAccrued salaries and benefitsAccrued salaries and benefitsAccrued salaries and benefits

Lunawat & Co.

FORM OF BALANCE SHEET (PART 2)Particulars Note

No.Figures as at the end of the CRP

Figures as at the end of the PRP

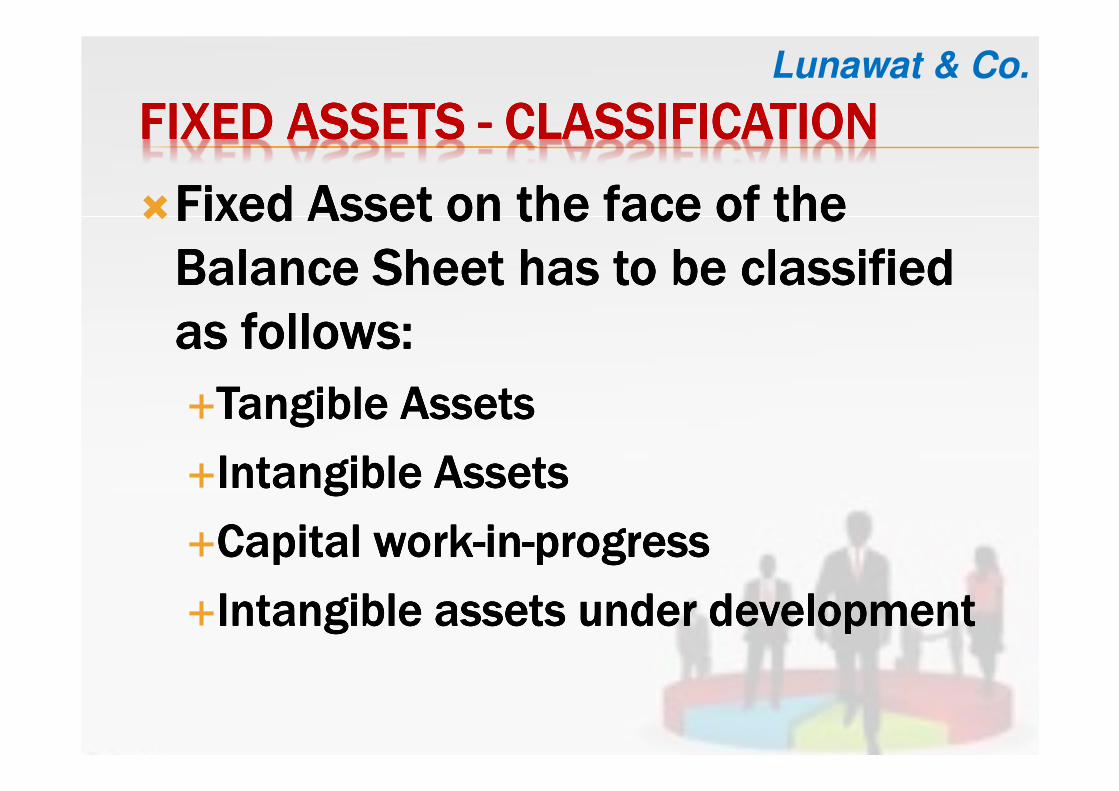

II. ASSETS

(1)Non-current assets

(a) Fixed assets

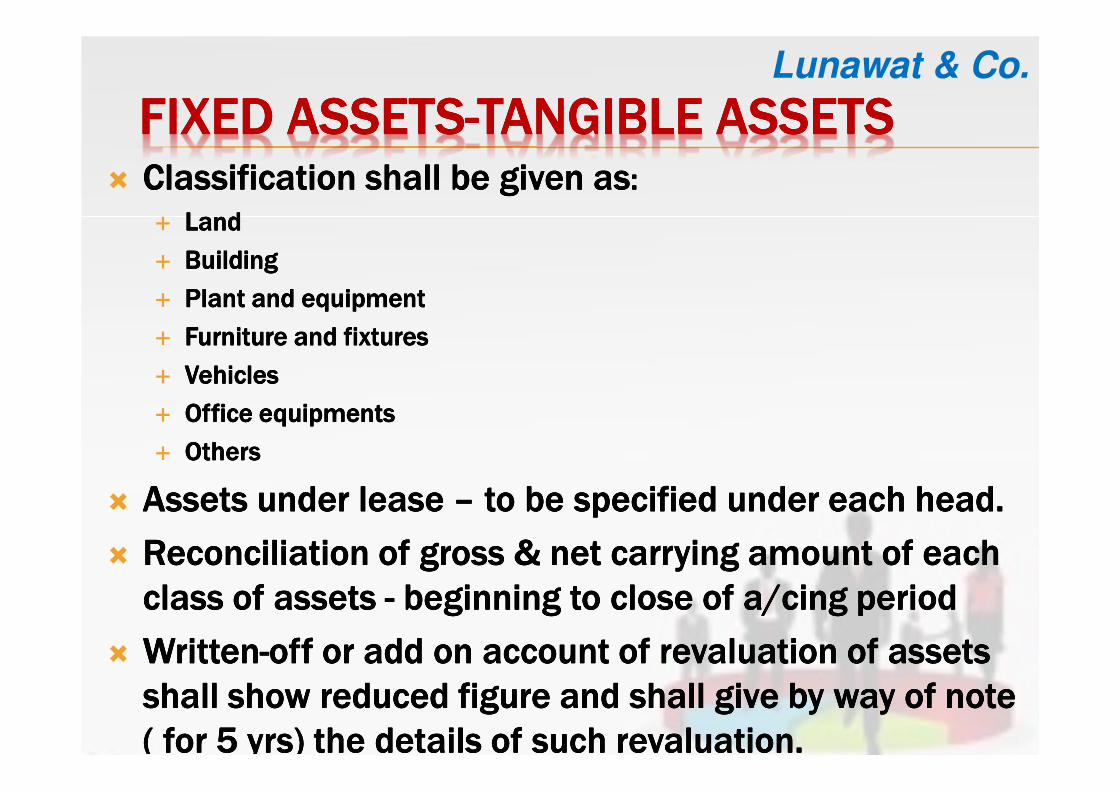

(i) Tangible assets

(ii) Intangible assets

(iii) Capital work-in-progress

(iv) Intangible assets under development

(b) Non- current investments

(c) Deferred tax assets (Net)

(d) Long term loans and advances

(e) Other non-current assets

11

12

13

14

15

(2) Current assets

(a) Current investments

(b) Inventories

(c) Trade receivables

(d) Cash and cash equivalents

(e) Short term loans and advances

(f) Other current assets

16

17

18

19

20

TOTAL

CURRENT AND NONCURRENT AND NONCURRENT AND NONCURRENT AND NON----CURRENT ASSETSCURRENT ASSETSCURRENT ASSETSCURRENT ASSETS

� Criteria to be met to classify as current asset:Criteria to be met to classify as current asset:Criteria to be met to classify as current asset:Criteria to be met to classify as current asset:

� Expected to be Expected to be Expected to be Expected to be realisedrealisedrealisedrealised in or intended for sale or in or intended for sale or in or intended for sale or in or intended for sale or consumption in normal operating cycle of the co.,consumption in normal operating cycle of the co.,consumption in normal operating cycle of the co.,consumption in normal operating cycle of the co.,

� Held primarily for the purpose of trading,Held primarily for the purpose of trading,Held primarily for the purpose of trading,Held primarily for the purpose of trading,

� Expected to be Expected to be Expected to be Expected to be realisedrealisedrealisedrealised within 12 months from the within 12 months from the within 12 months from the within 12 months from the closing date closing date closing date closing date orororor

� It is cash or cash equivalent.It is cash or cash equivalent.It is cash or cash equivalent.It is cash or cash equivalent.