Embed Size (px)

Citation preview

EN

André Bardow, Damien Green December – 2017

Low-Carbon Process Industries

Through Energy Efficiency and

Carbon Dioxide Utilisation

A study in support of a DG Research & Innovation Projects for Policy (P4P) report

Low-Carbon Process Industries Through Energy Efficiency and Carbon Dioxide Utilisation

European Commission

Directorate-General for Research and Innovation

Directorate Directorate D — Industrial Technologies

Unit [Directorate D.2. — Advanced Manufacturing Systems and Biotechnologies

Contact Nicolas Segebarth

Carmine Marzano

E-mail [email protected]

European Commission

B-1049 Brussels

Manuscript completed in December 2017.

This document has been prepared for the European Commission in support of a ‘Projects for Policy’ report. Projects for Policy

(P4P) is a European Commission initiative that aims to use research and innovation project results to shape policymaking

through evidence-based policy recommendations. The Research and Innovation Projects for Policy (P4P) report series

(https://ec.europa.eu/info/research-and-innovation-0/p4p_en) collects these recommendations to reach out to partners and

stakeholders, and contribute to an effective policymaking process.

This document reflects the views only of the authors, and the Commission cannot be held responsible for any use which may be made of the information contained therein.

More information on the European Union is available on the internet (http://europa.eu).

Luxembourg: Publications Office of the European Union, 2018

PDF ISBN 978-92-79-77788-2 doi:10.2777/175882 KI-04-18-022-EN-N

© European Union, 2018.

Reuse is authorised provided the source is acknowledged. The reuse policy of European Commission documents is regulated by

Decision 2011/833/EU (OJ L 330, 14.12.2011, p. 39).

For any use or reproduction of photos or other material that is not under the EU copyright, permission must be sought directly

from the copyright holders.

Cover page image: © Lonely # 46246900, ag visuell #16440826, Sean Gladwell #6018533, LwRedStorm #3348265, 2011;

kras99 #43746830, 2012. Source: Fotolia.com.

EUROPEAN COMMISSION

Low-Carbon Process Industries

Through Energy Efficiency and

Carbon Dioxide Utilisation

A study in support of a DG Research & Innovation

Projects for Policy (P4P) report

André Bardow, Damien Green

Directorate-General for Research and Innovation

2018 Key Enabling Technologies EN

Table of Contents

INTRODUCTION .................................................................................................. 3

1. POLICY CHALLENGES ...................................................................................... 4

1.1 Keeping global warming wall below 2˚C ......................................................................... 4

1.2 Transforming the emissions intensity of process industries ............................................... 5

1.3 Promoting industrial energy efficiency ............................................................................ 7

1.4 Unlocking the potential of carbon dioxide utilisation ......................................................... 9

2. PORTFOLIO OF EU-FUNDED R&I PROJECTS .................................................. 12

2.1 Programmes contributing to energy efficiency and CCU .................................................. 12

2.2 Portfolio of beneficiaries ............................................................................................. 16

3. IMPACT OF R&I FUNDING ON EU POLICY GOALS .......................................... 18

3.1 Supporting the transfer of policy-relevant innovations to market ..................................... 18

3.2 Supporting GHG abatement goals ................................................................................ 20

3.3 Supporting industrial efficiency goals ........................................................................... 21

3.4 Supporting goals to develop CO2 utilisation technologies ................................................ 23

4. POLICY RECOMMENDATIONS ........................................................................ 25

4.1 Remove barriers to energy efficiency investment ........................................................... 26

4.2 Optimise scale-up of challenge-relevant technologies with smart R&I ............................... 30

4.3 Take an evidence-based approach to integrating CCU into the policy framework ................ 32

4.4 Develop a supportive framework to promote industrial symbiosis .................................... 34

Appendix 1 – Project Identification ......................................................................... 39

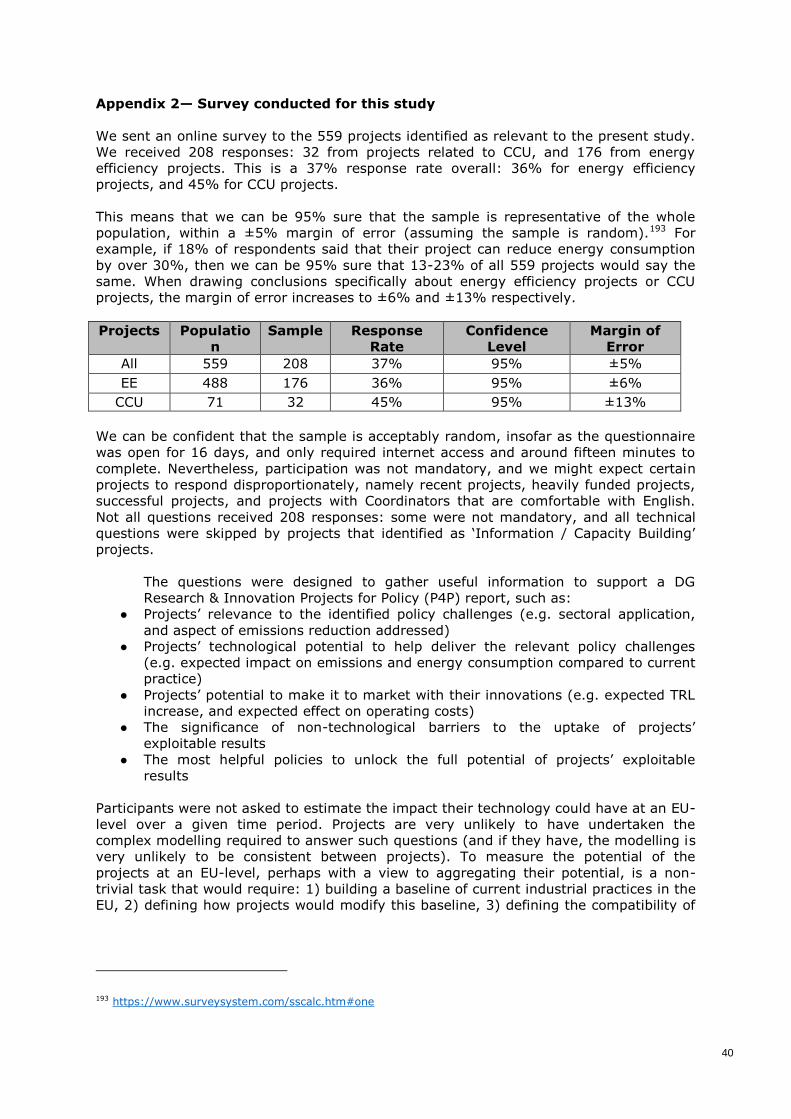

Appendix 2 – Survey conducted for this study .......................................................... 40

Appendix 3 – Data on TRL, Energy Saving, GHG Saving and Operation Costs ............... 42

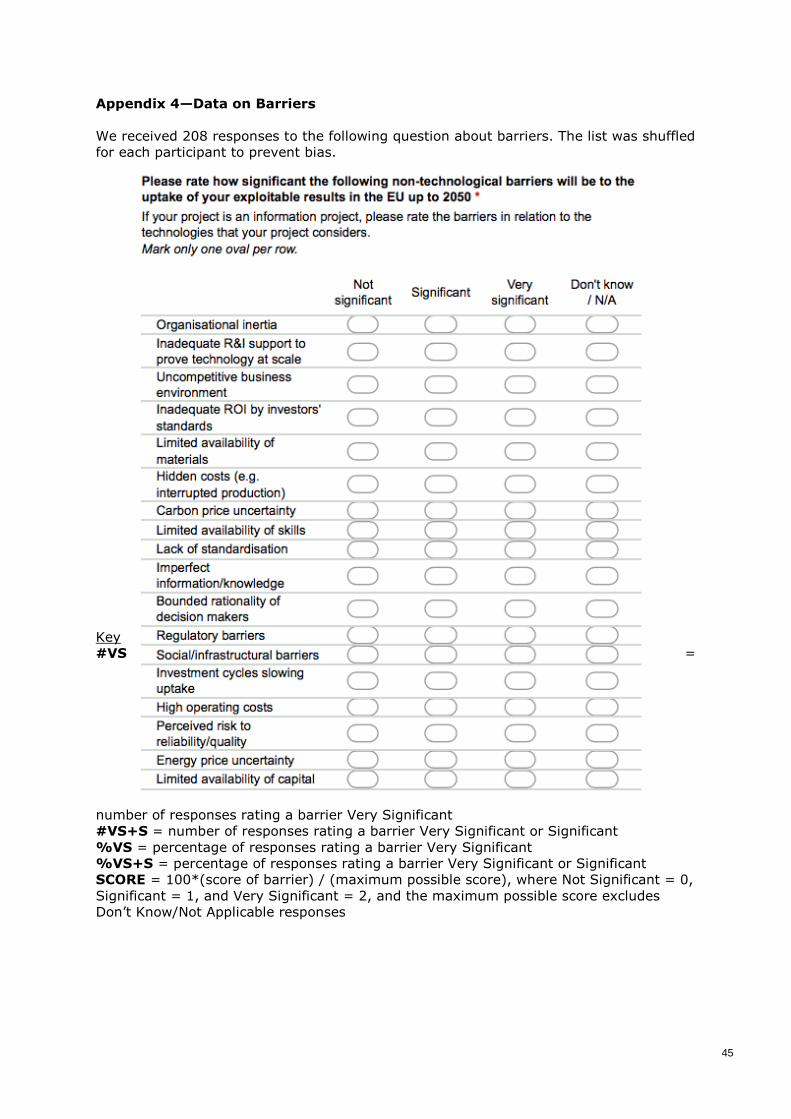

Appendix 4 – Data on Barriers ............................................................................... 45

Appendix 5 – Data on Policy Recommendations ........................................................ 51

3

INTRODUCTION

EU policymakers have set ambitious goals to tackle climate change, promote resource

efficiency, strengthen energy security, and enhance economic competitiveness. The

Research and Innovation (R&I) community, meanwhile, is developing the solutions

needed to meet these societal challenges. In this respect, R&I programmes at the

European level, such as the SPIRE PPP (funded with €900 million from 2014-20), as well

as initiatives at national and regional level, have been established to support delivery of

these targets. Projects for Policy (P4P) reports seek to facilitate a conversation between

policymakers and the R&I community, about how to better deliver shared goals. The

present study has been conducted to support a DG Research & Innovation Projects for

Policy report.

This particular study considers the challenge of establishing low-carbon process

industries, which is a key aspect of the wider societal challenges mentioned above.

Indeed, industry accounts for a quarter of EU emissions and energy consumption,

contributing 15% to GDP directly, and acting as the foundation for many value chains.

Establishing low-carbon process industries will call for a wide range of technologies, such

as CCS, electrification, and renewable hydrogen, but the present report focuses on

energy efficiency and carbon dioxide utilisation in particular. The intention is to cover a

long-standing field, and a more recent topic, providing policymakers with specific

insights in these areas, while generating insights of general relevance to other low-

carbon technologies at different stages of maturity. The joint discussion of energy

efficiency and carbon dioxide utilisation is also intended to broaden and guide the

current discussion around carbon dioxide utilisation, which today is often debated in the

context of carbon dioxide storage only, while many carbon dioxide utilisation pathways

in fact do not provide carbon storage, but aim at low-carbon processes by improving

energy and resource efficiency.

Section 1 of the report sets out four main policy challenges that relate to establishing

low-carbon process industries. These were identified by reviewing the policy

environment, and analysing industrial emissions and energy data. Section 2 outlines the

R&I projects that the EU has funded since 2007 that are relevant to the policy challenges

identified in Section 1. These were identified by reviewing project data from Framework

Programme 7 (FP7), Horizon 2020, Intelligent Energy Europe (IEE), and the Research

Fund for Coal and Steel (RFCS). Section 3 discusses the value of these projects in

relation to the goals identified in Section 1. This discussion is based on the projects’ self-

assessment (in response to an online survey), as well as analysis of specific projects,

drawing upon relevant literature where appropriate. Finally, Section 4 makes four policy

recommendations (each with two suggested accompanying measures). These are based

on information from the projects concerning barriers and policy interventions, which was

supplemented with insights and evidence from relevant recent literature, and comments

from stakeholders and policymakers at a workshop.

For the purposes of this report, industry has been defined broadly to include refining and

all major manufacturing sectors (see Appendix 1 for further details). While this report is

properly concerned with carbon dioxide utilisation, the acronym ‘CCU’ (which stands for

Carbon Capture and Utilisation) will be used throughout for convenience, because it is a

more established term than CDU, and CO2 capture is an important part of the CCU value

chain.

4

1. POLICY CHALLENGES

Four main policy challenges that relate to promoting low-carbon process industries

through energy efficiency and CCU have been identified. The challenges have been

selected and analysed by reviewing the policy environment and industrial emissions and

energy data.

1.1 Keeping global warming well below 2°C

The EU has played a leading role in international efforts to reduce greenhouse gas (GHG)

emissions since the inception of the United Nations Framework Convention on Climate

Change in 1992.1 During the first Kyoto Protocol commitment period (2008-12), the EU-

15 pledged to keep average annual emissions at least 8% below 1990 levels, and

overachieved its target by almost four percentage points.2 3 Now, in the second Kyoto

commitment period (2013-20), the EU-28 has promised to emit 20% less by 2020

(compared to 1990 levels), and is well on track.4 5

But the real challenge lies ahead. The United Nations forecasts that the global population

will increase by 30% by 2050, and 47% by the end of the century.6 At the same time,

the Paris Agreement—negotiated in 2015 and now in force—requires nations to keep

global warming ‘well below’ 2°C, and strive to limit it to 1.5°C (compared to pre-

industrial levels).7 In its first Nationally Determined Contribution (NDC), the EU has

pledged to emit 40% less by 2030 (compared to 1990 levels), which will require a step

change in climate action in the next decade.8 And, to be consistent with the wider Paris

objective, the EU will have to go much further, dramatically cutting emissions by the

middle of the century.

Member State Environment Ministers first endorsed a 2°C limit in 1996, and in 2011 the

European Council agreed that it would require an 80–95% cut in emissions by 2050

(compared to 1990 levels), in keeping with the findings of the Intergovernmental Panel

on Climate Change’s Fourth Assessment Report.9 10 11 The European Commission

accordingly issued a Roadmap in 2011, setting out how this level of abatement could be

achieved, and proposing a 60% milestone target for 2040.12

The Commission will review its mid-century strategy in light of the 1.5°C aspiration in

the Paris Agreement, and the latest evidence from UNEP provided at COP23, which

suggests that there exists a significant ‘emissions gap’ between current NDCs and the

overall goal of the Agreement, and calls for urgent action during the Facilitative Dialogue

period (2018) ahead of the submission of updated NDCs in 2020.13 14 The European

Parliament, meanwhile, passed a Resolution in October ahead of COP23, calling for a

zero-emissions strategy for 2050 by 2018.15

1 http://unfccc.int/essential_background/convention/items/6036.php 2 http://unfccc.int/kyoto_protocol/items/3145.php 3 https://www.eea.europa.eu/data-and-maps/indicators/greenhouse-gas-emission-trends-5/assessment 4 https://treaties.un.org/doc/Publication/CN/2012/CN.718.2012-Eng.pdf 5 http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=t2020_30&plugin=1 6 https://www.un.org/development/desa/en/news/population/world-population-prospects-2017.html 7 https://unfccc.int/files/essential_background/convention/application/pdf/english_paris_agreement.pdf 8 http://www4.unfccc.int/submissions/INDC/Published%20Documents/Latvia/1/LV-03-06-EU%20INDC.pdf 9 http://europa.eu/rapid/press-release_PRES-96-188_en.htm?locale=en 10 http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/119175.pdf 11 http://www.ipcc.ch/pdf/assessment-report/ar4/syr/ar4_syr_full_report.pdf 12 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52011DC0112 13 https://cop23.unfccc.int/ 14 https://www.unenvironment.org/resources/emissions-gap-report 15 http://www.europarl.europa.eu/sides/getDoc.do?type=TA&language=EN&reference=P8-TA-2017-0380

5

1.2 Transforming the emissions intensity of process industries

Reducing industrial emissions is a crucial aspect of the EU’s wider goal of moving to a

low-carbon society, because direct industrial emissions account for a quarter of EU

emissions, and indirect industrial emissions associated with energy-use about a further

tenth.16 17 Bearing in mind that the EU’s industrial strategy seeks to promote

manufacturing growth—aiming for manufacturing to account for 20% of GDP by 2020—a

radical transformation is required in the emissions intensity of process industries.18

The Commission has proposed reducing direct industrial emissions by at least 80% by

2050 (compared to 1990 levels) in its 2011 Roadmap.19 Based on 2015 emissions figures

from the EEA GHG Inventory, industry has already made very significant progress,

especially in certain sectors.20 The chemicals industry and non-ferrous metal producers,

for instance, have reduced direct emissions by over 60% since 1990, primarily through

energy efficiency improvements and abating non-CO2 GHG emissions associated with

certain processes.21 22

Sector

Emissions Reduction (CO2e)

2015 compared to 1990

% Reduction Absolute Reduction

(Million tonnes)

Industry as a whole 37 680

Chemicals 61 197

Iron/Steel 38 104

Minerals 31 87

Non-Ferrous Metals 67 32

Table 1: Industrial direct emissions reduction (EEA 2015 GHG Inventory) ‘Industry as a whole’ (which includes refining and other sectors not listed in the table) comprises inventory categories 1A1b, 1A1c, 1A2, 1B, 2, and 5D; ‘Chemicals’ comprises categories 1A2c and 2B; ‘Iron/Steel’ comprises categories 1A2a and 2C1; ‘Minerals’ comprises categories 1A2f and 2A; and Non-Ferrous Metals comprises categories 1A2b, 2C3, 2C4, 2C5, 2C6, and 2C7.

Nevertheless, industry as a whole is not yet halfway towards an 80% reduction in direct

emissions, and reducing emissions will become progressively more challenging over the

next few decades, as non-CO2 GHG abatement opportunities are exhausted, and energy

16 Based on 2015 emissions in categories 1A1b, 1A2, 1B, CRF Sector 2, and 5D of the EEA’s GHG inventory, compared to the EU’s total emissions (not including LULUCF): http://www.eea.europa.eu/data-and-maps/data/data-viewers/greenhouse-gases-viewer 17 Based on a 2012 report from the EEA on indirect emissions: https://www.eea.europa.eu/highlights/households-and-industry-responsible-for 18 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2017:479:FIN 19 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52011DC0112 20 The GHG inventory was used rather than verified emissions data from ETS installations because it covers a

wider range of GHGs as well as emissions from smaller industrial sites that do not participate in the ETS, and it allowed for consistent comparison with a 1990 baseline, which is how the 2050 target is defined (whereas the ETS only started in 2005). 21 https://www.eea.europa.eu/publications/european-union-greenhouse-gas-inventory-2017 22 Analysis from the EEA has found that the economic downturn following the 2008 financial crisis has also contributed significantly to industrial emissions reductions in more recent years: https://www.eea.europa.eu/publications/why-are-greenhouse-gases-decreasing

EU GHG TARGETS

20% reduction in emissions by 2020 (compared to 1990)

40% reduction in emissions by 2030 (compared to 1990)

80-95% reduction in emissions by 2050 (compared to 1990)

‘Emissions’ = CO2, CH4, N2O, PFCs, SF6, and NF3 measured in CO2e

6

efficiency improvements become increasingly incremental. In addition, there are wider

challenges to reduce indirect emissions associated with the upstream production of

materials and energy used by industry, as well as the downstream waste management

of products made from carbon feedstocks, such as those produced by the chemicals

industry.23 24

To achieve this radical transformation, the EU will have to use policy levers and very

significant public funding to help industry bring breakthrough technologies to market. In

this respect, the EU currently funds innovation under Horizon 2020, the Research Fund

for Coal and Steel, and NER300, and Member States have a range of research and

innovation programmes.25 26 27 The European Commission is also currently considering

an initiative to promote technological breakthroughs capable of producing zero-emissions

steel from 2030 (the Big Ticket Initiative), following a recommendation in the Pascal

Lamy report on priorities for Framework Programme 9.28 29 Ensuring that industry has

access to cheap low-carbon electricity, will also be vital if breakthrough technologies

involving electrification are to be viable.

While the 2011 Roadmap contains the EU’s only industry-specific emissions goal,

industrial sectors also participate in the EU Emissions Trading System (ETS), which

progressively limits CO2, N2O and PFC emissions from industrial processes, electricity

generation, and aviation.30 The ETS is currently calibrated to issue a number of

allowances in 2020 that corresponds to an emissions level that is 21% below 2005

levels.31 A provisional agreement has been reached that the ETS will issue a number of

allowances in 2030 that is 43% below 2005 levels.32 This gives an indication of the EU’s

shorter-term goals for reducing industrial emissions.33

23 The EU has a range of policy mechanisms and initiatives relating to tier 2 and 3 industrial emissions, such as the Renewable Energy Directive (which promotes renewable electricity), and the forthcoming Plastics Strategy (which will consider how to reduce the climate impact of plastics). 24 The Ellen MacArthur Foundation, for instance, suggests that plastics could account for 20% of global oil consumption by 2050, which would take up 15% of the global carbon budget: https://www.ellenmacarthurfoundation.org/assets/downloads/EllenMacArthurFoundation_TheNewPlasticsEconomy_15-3-16.pdf 25 https://ec.europa.eu/programmes/horizon2020/ 26 http://ec.europa.eu/research/industrial_technologies/rfcs_en.html 27 https://ec.europa.eu/clima/policies/lowcarbon/ner300_en 28 https://publications.europa.eu/en/publication-detail/-/publication/f5a82742-2a44-11e7-ab65-01aa75ed71a1 29 https://ec.europa.eu/research/evaluations/pdf/archive/other_reports_studies_and_documents/hlg_2017_report.pdf#view=fit&pagemode=none 30 See Annex 1: eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:02003L0087-20140430 31 https://ec.europa.eu/clima/policies/ets_en 32 http://www2.consilium.europa.eu/en/press/press-releases/2017/11/22/reform-of-the-eu-emissions-trading-system-council-endorses-deal-with-european-parliament/# 33 The ETS target is only indicative for industry because the cap also covers other sectors’ emissions, and the number of allowances available for compliance in a given year can exceed the number issued that year, due to the market surplus.

EU INDUSTRY GHG REDUCTION TRAJECTORY 21% reduction in direction emissions by 2020 (compared to 2005)

CO2, N20, and PFC emissions measured in CO2e. Shared with the power sector and affected by the ETS market surplus

43% reduction in direct emissions by 2030 (compared to 2005) CO2, N20, and PFC emissions measured in CO2e.

Shared with the power sector and affected by the ETS market surplus

>80% reduction in direct emissions by 2050 (compared to 1990)

CO2, CH4, N2O, PFCs, SF6, and NF3 measured in CO2e

7

1.3 Promoting industrial energy efficiency

The EU recognises that improving energy efficiency is one of the best ways of reducing

emissions: efficiency is often the cheapest form of abatement, and has the additional

benefits of enhancing competitiveness and bolstering energy security.34 For this reason,

promoting energy efficiency is one of five fundamental goals in the EU’s Energy Union

strategy, and the EU has regularly endorsed the principle of putting ‘efficiency first’ in its

policymaking.35 36

The EU has an overarching target—which is currently on track—to consume 20% less

energy in 2020 compared to projections (PRIMES 2007), and is in the process of

finalising a new efficiency target for 2030.37 38 39 Reducing industrial energy consumption

is a crucial part of this wider efficiency drive, because industry accounts for a quarter of

EU final energy consumption.40 Industries have greatly improved their energy efficiency

over the last few decades, but models suggest that there is the technical potential to

reduce industrial energy consumption by over 20% by 2050 compared to business-as-

usual consumption projections.41 42 43

Sector

Technical Possible Energy Saving by 2050

(Compared to BAU projections for 2050)

Million tonnes of oil

equivalent %

Iron/Steel 18.9 26

Chemicals/Pharmaceutical

s 17.8 22

Refining 8.3 23

Minerals 6.3 18

Food/Drink 5.7 24

Pulp/Paper 5.5 17

Engineering/Machinery 4.8 25

Non-Ferrous Metals 1.6 21 Table 2: Industrial energy saving potential (ICF, 2015), not endorsed by industry

To unlock this technical potential, the EU will have to promote research and innovation

(R&I), and remove barriers to the uptake of efficiency solutions. The EU has set five

specific goals in this respect, working with industry and the R&I community under its

Strategic Energy Technology (SET) Plan Action 6 on Energy Efficiency in Industry.44 45

The first two goals are specific to the steel and chemicals industries (which have been

identified as high-impact areas), while the remaining three are designed to promote

efficiency across all sectors.

34 It should be noted that deep reductions in emissions may require technologies that increase energy consumption (e.g. CCS); but even in these cases, efficiency is a virtue. 35 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2015:80:FIN 36 http://europa.eu/rapid/press-release_IP-15-5358_en.htm 37 http://www.consilium.europa.eu/ueDocs/cms_Data/docs/pressData/en/ec/93135.pdf 38 https://ec.europa.eu/commission/sites/beta-political/files/report-energy-efficiency-progress_en.pdf 39 https://ec.europa.eu/energy/sites/ener/files/documents/trends_to_2030_update_2007.pdf 40 https://www.eea.europa.eu/data-and-maps/indicators/final-energy-consumption-by-sector-9/assessment-1 41 https://www.eea.europa.eu/data-and-maps/indicators/energy-efficiency-and-energy-consumption-6/assessment 42 https://ec.europa.eu/energy/sites/ener/files/documents/151201%20DG%20ENER%20Industrial%20EE%20study%20-%20final%20report_clean_stc.pdf 43 This estimate has not been endorsed by industry. 44 https://setis.ec.europa.eu/system/files/integrated_set-plan/declaration_action6_ee_industry_0_0.pdf 45 The EU has recently adopted an Implementation Plan with stakeholders to deliver these goals, which is due to be published shortly.

8

The Energy Efficiency Directive (EED), Industrial Emissions Directive (IED), and

Ecodesign Directive (ED) support the delivery of the EU’s industrial efficiency goals. The

EED allows Member States to count industrial efficiency policies towards energy saving

obligations, and requires large industrial sites to conduct energy audits every four

years.46 The IED sets efficiency standards by requiring Member States to issue permits

for industrial activities according to Best Available Technique reference documents

(BREFs).47 48 And the ED sets standards for energy-related products sold in the EEA,

including industrial equipment such as electric motors, pumps, and fans.49 50

46 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:32012L0027 47 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32010L0075 48 http://eippcb.jrc.ec.europa.eu/reference/ 49 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32009L0125 50 https://ec.europa.eu/energy/sites/ener/files/documents/list_of_ecodesign_measures.pdf

SET Plan Industrial Efficiency Targets (Action 6)

By 2030, ≥1/3 of technical energy savings should offer pay back in three years (steel and chemicals)

By 2030, ≥1/3 of key emerging technologies should be demonstrated at TRL 8 (steel and chemicals)

By 2025, cost-effective heat/cold recovery solutions should be demonstrated at TRL 8

By 2025, industrial components that are ≥15% more efficient should be demonstrated at TRL 8

By 2025, solutions that enable industries to reduce energy consumption by ≥20%, while reducing

emissions proportionately, should be developed and demonstrated

9

1.4 Unlocking the potential of carbon dioxide utilisation

CCU has been acknowledged as an important research priority under the Energy Union,

together with Carbon Capture and Storage (CCS).51 The EU is calling for a forward-

looking approach to CCS and CCU for the power and industrial sectors, which will be

critical to reaching the 2050 climate objectives in a cost-effective way.52 Stepping up

research and innovation activities on the commercial viability of CCU is priority Action 9

of the SET Plan.53 Since COP21, the European Union has been an active member in

Mission Innovation, which aims to double Clean Energy R&D Investment by 2020

compared to 2013-2015 levels. In Mission Innovation, the EU is part of the Clean Energy

R&D Focus Area on CCU and CCS.54

However, it is important to distinguish CCU from CCS: while CCS mitigates climate

change solely through storage, and some CCU technologies also offer permanent CO2

storage in a product (e.g. mineralisation), most CCU technologies aim to reduce CO2

emissions by either increasing resource and energy efficiency compared to current

products (e.g. CO2-based polyols), or by integrating renewable energy into the value

chain (e.g. CO2-based fuels). Most CCU technologies thus try to use less fossil

resources.55 Thereby, fossil carbon would be left in the ground and these CCU

technologies would avoid CO2 emissions compared to current fossil-based practise.

These differences between CCU and CCS have to be recognised to link CCU appropriately

into the policy framework. Member States already employ different approaches to CCU,

e.g. as raw materials or industrial symbiosis technology.56 To shed light on the broader

climate mitigation potential of CCU technologies, the Commission has called upon the

Scientific Advice Mechanism High Level Group, which will study the potential of CCU for

emissions reduction, industrial innovation, and competitiveness of energy-intensive

industries.57

CCU projects have already been granted under Framework Programmes 6 and 7, and

CO2-use-specific calls have been part of the Horizon 2020 programme. In parallel, the

EU Commission started a comprehensive stakeholder dialogue in 2015, with its scoping

workshop ‘Transforming CO2 into value for a rejuvenated European economy’.58 Based

on these actions, potential contributions of CCU technologies to several key EU policy

goals have been identified, such as the transition towards a more circular economy, GHG

mitigation, energy security, and transport emissions reduction, while avoiding any

potential conflict with the food sector. However, since many CCU technologies are rather

novel, further research and development is required to establish competitive

technologies, and to clarify if, how, and which CCU technologies can actually realise

these potential contributions. Beneficial CCU technologies should be integrated into the

existing policy framework according to the mechanism by which they provide benefits.

The transition towards a more circular economy is a key priority for the European

Commission. By turning waste into a resource, the Circular Economy Action Plan aims to

reduce primary resource use and its associated environmental impacts including GHG

emissions, and increase resource security, while boosting the competitiveness of the

European economy.59 Current measures include eco-design, waste prevention, and the

re-use and recycling of products, but the Circular Economy Action Plan also mentions the

51 http://eur-lex.europa.eu/legal-content/en/TXT/?uri=COM%3A2015%3A80%3AFIN 52 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52015DC0080 53 https://ec.europa.eu/energy/sites/ener/files/documents/1_EN_ACT_part1_v8_0.pdf 54 http://mission-innovation.net/participating-countries/european-union/ 55

The present report discusses only CCU and its potential role in low-carbon industries. The focus on CCU does not imply any statement with respect to CCS and its relative importance in climate change mitigation. 56 E.g. https://www.thyssenkrupp.com/en/carbon2chem/ 57 https://ec.europa.eu/research/sam/index.cfm?pg=ccu

58 https://publications.europa.eu/en/publication-detail/-/publication/a89ae7bf-1bef-407a-9a02-4c76a5b55b49 59 http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1453384154337&uri=CELEX:52015DC0614

10

re-use of CO2 effluent gases as an innovative production process to be promoted

through R&I funding and Cohesion Policy funds

In a carbon cycle, CO2 captured (i) during the end-of-life treatment of a CCU product,

(ii) via biomass, or (iii) via direct air capture, could be a renewable carbon source and

substitute for conventional (often fossil) raw materials.60 This substitution not only

increases resource security, but can also reduce the emission intensity of value chains.61

In addition, CO2-use technologies, such as mineralisation and enhanced oil recovery,

could store carbon as long as geological storage; thus, eventually even enabling carbon-

negative pathways. However, there is no established monitoring and verification

methodology to ascertain the permanence of storage through mineralisation. In this

context, a first court ruling has recognised that the CO2 used in a precipitated calcium

carbonate product is chemically bound in that stable product, and that the following

provision from the Monitoring and Reporting Regulation 601/2012 is invalid: ‘Where CO2

is used in the plant or transferred to another plant for the production of PCC

(precipitated calcium carbonate), that amount of CO2 shall be considered emitted by the

installation producing the CO2’. Incentives for permanent carbon storage through CO2

use are missing under the current ETS.

CO2 utilisation can also support the integration of renewable energy into the European

energy mix, which is a key priority of the Energy Union and SET Plan. Quantitative

targets and measures have been defined by the Renewable Energy Directive.62 CCU

could help integrate renewables into the energy mix by utilising electricity from

fluctuating renewable sources. In CCU value chains, electricity is commonly used for the

production of hydrogen via electrolysis, which is an important co-reactant for many CO2-

based products, including fuels and bulk chemicals such as methanol and carbon

monoxide. Pathways to hydrogen with low CO2 emissions are therefore a key

prerequisite for many CCU technologies. The flexible use of renewable electricity in CCU

processes could enhance grid stability, and CO2-based fuels could provide both energy

storage and energy transportation. A common methodology to account for grid flexibility

options offered by CCU and power-to-hydrogen in general, however, is currently missing

in the policy framework. Due to the early stage of development, the potential role of

CCU in this context is only emerging.

Current literature suggests that CO2-based fuels require very low-carbon energy to be

less carbon-intensive than fossil fuels.63 According to Life Cycle Assessment (LCA)

literature, the expected EU grid mix in 2050 might still be too carbon-intensive. At the

same time, it has been shown that the current grid mix in several countries is already

sufficient to allow for CO2-based chemicals and fuels with reduced GHG emissions

today.64 65 Valorisation of residual streams with low calorific value by CCU could also

provide promising pathways.66 Properly locating potential production sites for CO2-based

fuels and chemicals therefore seems important. As long as a limited energy input is

used, this planning has to take into account the efficiency in the utilisation of low-carbon

energy for GHG mitigation, which can be high, e.g. if CO2-based production leads to

more energy and resource efficient production. 67 But it can often be lower for CO2 use

than for many competing technologies.68

60 The RED currently specifies renewable carbon only if it comes from sustainable biomass: http://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX%3A32009L0028 61 https://doi.org/10.1039/c4gc00513a 62 http://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:32009L0028 63 http://dx.doi.org/10.1021/es500191g 64 http://dx.doi.org/10.1021/acs.chemrev.7b00435 65 http://pubs.acs.org/doi/10.1021/acs.chemrev.7b00435 66 https://www.thyssenkrupp.com/de/carbon2chem/ 67 https://doi.org/10.1016/j.jcou.2017.10.001 68 http://dx.doi.org/10.1039/C4EE03051F

11

Fuels from CO2 and renewable energy could help integrate renewable energy into the

transport sector. The Renewable Energy Directive (RED) requires that at least 10% of

the transport fuels in all EU countries come from renewable sources by 2020.69 The

proposal for a revised Renewable Energy Directive (REDII) for the period 2021-2030

includes so-called ‘waste-based fossil fuels’ which could be produced from CO2

processing gases or exhaust gases.70 The Fuel Quality Directive (FQD) requires that the

GHG intensity of transport fuels is reduced by 6% in 2020 from a 2010 baseline.71 In

2015, CO2-based renewable fuels have been further incentivised by a new Directive on

Indirect Land Use Change (ILUC) amending the RED and the FQD.72 This Directive sets

an indicative 0.5% target for so-called advanced biofuels (including CO2-based fuels) as

a reference for national targets, and encourages the use of renewable electricity in

transport by counting it 2.5 times (rail) or 5 times (road) towards the 2020 target of

10% renewable energy use in transport. The Commission is empowered to adopt a

delegated act by the end of 2017, specifying the GHG intensity of novel fuels, including

fuels from CCU. Available LCA calculations undertaken by the Joint Research Centre

(JRC) for this purpose, and in the scientific literature, show that CO2-based fuels have

intrinsically a lower efficiency from renewable energy to mobility than more direct

pathways and that the GHG intensity of these fuels is therefore highly dependent on the

GHG intensity of the electricity used to produce them.73 74

If successful, the large-scale application of CCU technologies could potentially contribute

to lowering the costs of CO2 supply through the implementation and development of a

CO2 supply infrastructure and required technologies. The COSME project on Phase 2 of

the Regional Hot Spot Analysis, and the European Sustainable Chemicals Support

Service (ESCSS) studies infrastructure which is expected to require regionalised and

industrial cross-sectoral collaboration for CCU.75 Infrastructures for CCU and CCS will not

be identical in all details, but the CCU infrastructure would certainly include both CO2

capture facilities and a distribution system. These elements would also be part of an

infrastructure for geological storage of carbon dioxide, which is part of the Energy Union

Strategy for cost-efficient achievement of the 2050 GHG targets. CCU could thus

contribute to reducing the cost of CCS.

These potential contributions of CCU to EU policy areas can be enabled through the

development of innovative technologies to ensure future competitive advantages and

technological leadership in the field of CO2 utilisation in European industry.

69 http://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX%3A32009L0028 70 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52016PC0767R%2801%29 71 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32009L0030 72 http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32015L1513 73 INFORMAL EXPERT GROUP ON TRANSPOSITION AND HARMONISED IMPLEMENTATION OF COUNCIL DIRECTIVE (EU) 2015/652 AND FUEL QUALITY DIRECTIVE 98/70/EC ARTICLE 7A 74 http://dx.doi.org/10.1021/acs.chemrev.7b00435 75 http://ted.europa.eu/TED/notice/udl?uri=TED:NOTICE:22992-2017:TEXT:EN:HTML

12

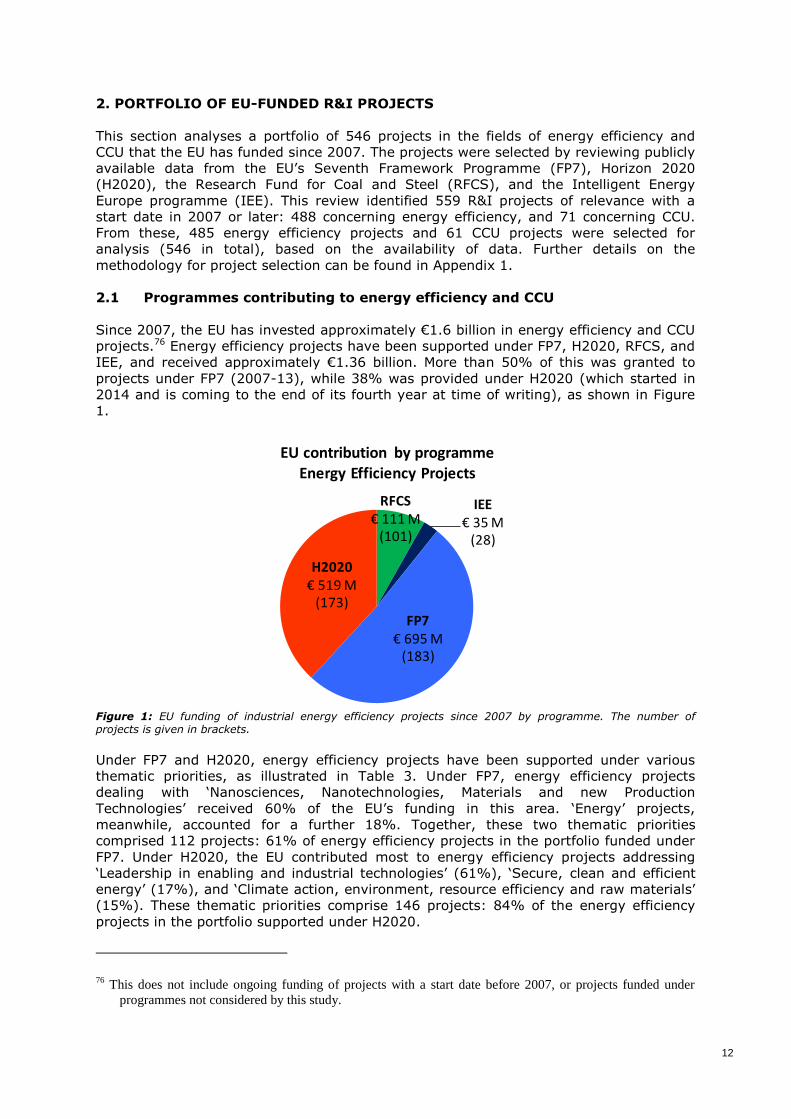

2. PORTFOLIO OF EU-FUNDED R&I PROJECTS

This section analyses a portfolio of 546 projects in the fields of energy efficiency and

CCU that the EU has funded since 2007. The projects were selected by reviewing publicly

available data from the EU’s Seventh Framework Programme (FP7), Horizon 2020

(H2020), the Research Fund for Coal and Steel (RFCS), and the Intelligent Energy

Europe programme (IEE). This review identified 559 R&I projects of relevance with a

start date in 2007 or later: 488 concerning energy efficiency, and 71 concerning CCU.

From these, 485 energy efficiency projects and 61 CCU projects were selected for

analysis (546 in total), based on the availability of data. Further details on the

methodology for project selection can be found in Appendix 1.

2.1 Programmes contributing to energy efficiency and CCU

Since 2007, the EU has invested approximately €1.6 billion in energy efficiency and CCU

projects.76 Energy efficiency projects have been supported under FP7, H2020, RFCS, and

IEE, and received approximately €1.36 billion. More than 50% of this was granted to

projects under FP7 (2007-13), while 38% was provided under H2020 (which started in

2014 and is coming to the end of its fourth year at time of writing), as shown in Figure

1.

Figure 1: EU funding of industrial energy efficiency projects since 2007 by programme. The number of projects is given in brackets.

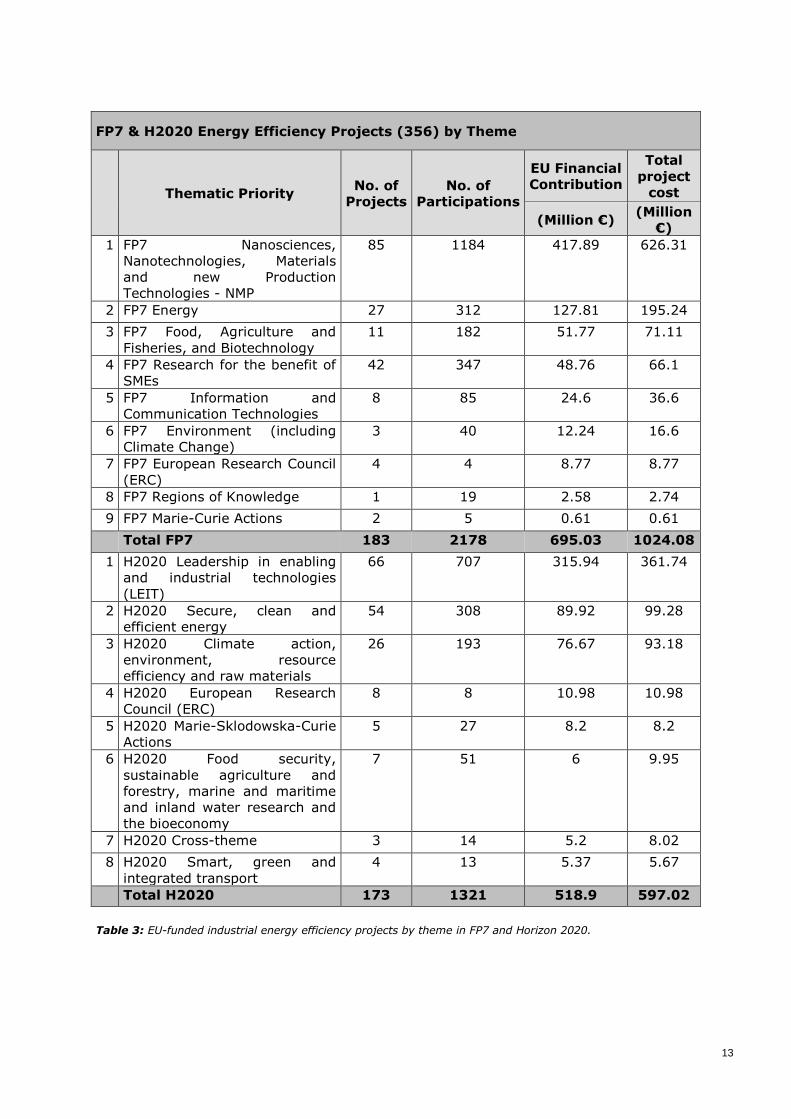

Under FP7 and H2020, energy efficiency projects have been supported under various

thematic priorities, as illustrated in Table 3. Under FP7, energy efficiency projects

dealing with ‘Nanosciences, Nanotechnologies, Materials and new Production

Technologies’ received 60% of the EU’s funding in this area. ‘Energy’ projects,

meanwhile, accounted for a further 18%. Together, these two thematic priorities

comprised 112 projects: 61% of energy efficiency projects in the portfolio funded under

FP7. Under H2020, the EU contributed most to energy efficiency projects addressing

‘Leadership in enabling and industrial technologies’ (61%), ‘Secure, clean and efficient

energy’ (17%), and ‘Climate action, environment, resource efficiency and raw materials’

(15%). These thematic priorities comprise 146 projects: 84% of the energy efficiency

projects in the portfolio supported under H2020.

76 This does not include ongoing funding of projects with a start date before 2007, or projects funded under

programmes not considered by this study.

RFCS€ 111 M

(101)

IEE€ 35 M

(28)

FP7€ 695 M

(183)

H2020€ 519 M

(173)

EU contribution by programme Energy Efficiency Projects

13

FP7 & H2020 Energy Efficiency Projects (356) by Theme

Thematic Priority No. of

Projects

No. of

Participations

EU Financial

Contribution

Total

project

cost

(Million €) (Million

€)

1 FP7 Nanosciences,

Nanotechnologies, Materials

and new Production

Technologies - NMP

85 1184 417.89 626.31

2 FP7 Energy 27 312 127.81 195.24

3 FP7 Food, Agriculture and

Fisheries, and Biotechnology

11 182 51.77 71.11

4 FP7 Research for the benefit of

SMEs

42 347 48.76 66.1

5 FP7 Information and

Communication Technologies

8 85 24.6 36.6

6 FP7 Environment (including

Climate Change)

3 40 12.24 16.6

7 FP7 European Research Council

(ERC)

4 4 8.77 8.77

8 FP7 Regions of Knowledge 1 19 2.58 2.74

9 FP7 Marie-Curie Actions 2 5 0.61 0.61

Total FP7 183 2178 695.03 1024.08

1 H2020 Leadership in enabling

and industrial technologies

(LEIT)

66 707 315.94 361.74

2 H2020 Secure, clean and

efficient energy

54 308 89.92 99.28

3 H2020 Climate action,

environment, resource

efficiency and raw materials

26 193 76.67 93.18

4 H2020 European Research

Council (ERC)

8 8 10.98 10.98

5 H2020 Marie-Sklodowska-Curie

Actions

5 27 8.2 8.2

6 H2020 Food security,

sustainable agriculture and

forestry, marine and maritime

and inland water research and

the bioeconomy

7 51 6 9.95

7 H2020 Cross-theme 3 14 5.2 8.02

8 H2020 Smart, green and

integrated transport

4 13 5.37 5.67

Total H2020 173 1321 518.9 597.02

Table 3: EU-funded industrial energy efficiency projects by theme in FP7 and Horizon 2020.

14

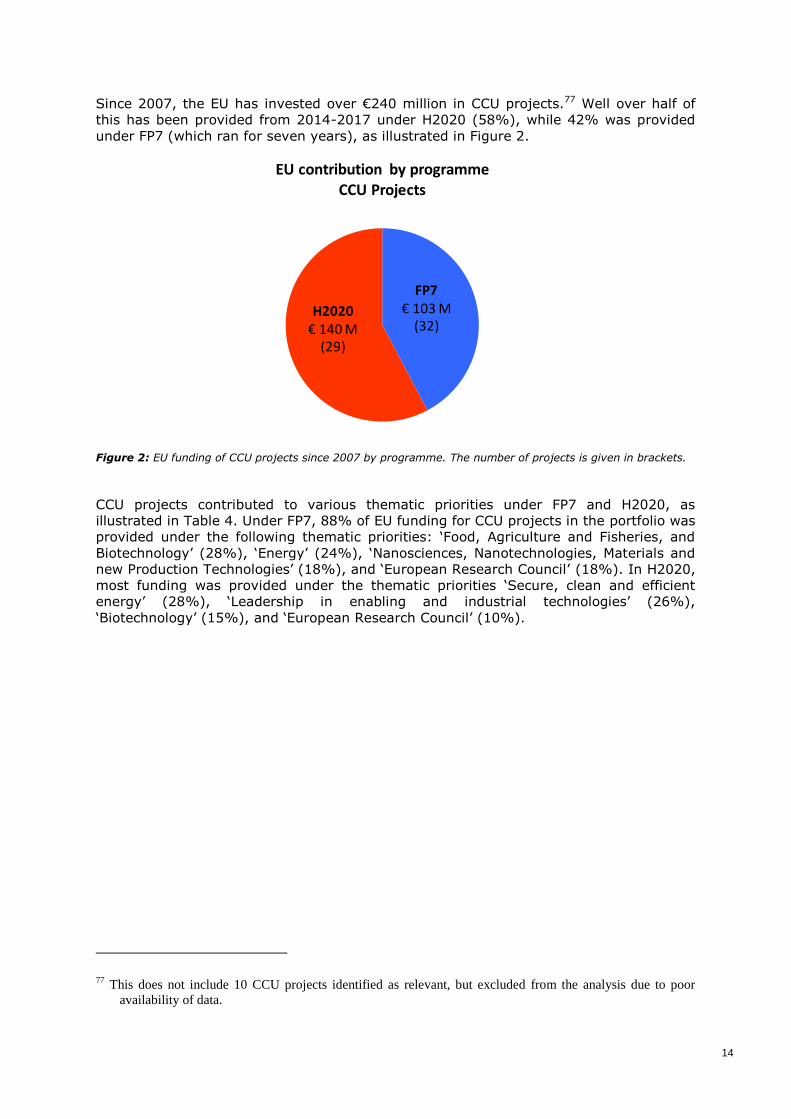

Since 2007, the EU has invested over €240 million in CCU projects.77 Well over half of

this has been provided from 2014-2017 under H2020 (58%), while 42% was provided

under FP7 (which ran for seven years), as illustrated in Figure 2.

Figure 2: EU funding of CCU projects since 2007 by programme. The number of projects is given in brackets.

CCU projects contributed to various thematic priorities under FP7 and H2020, as

illustrated in Table 4. Under FP7, 88% of EU funding for CCU projects in the portfolio was

provided under the following thematic priorities: ‘Food, Agriculture and Fisheries, and

Biotechnology’ (28%), ‘Energy’ (24%), ‘Nanosciences, Nanotechnologies, Materials and

new Production Technologies’ (18%), and ‘European Research Council’ (18%). In H2020,

most funding was provided under the thematic priorities ‘Secure, clean and efficient

energy’ (28%), ‘Leadership in enabling and industrial technologies’ (26%),

‘Biotechnology’ (15%), and ‘European Research Council’ (10%).

77 This does not include 10 CCU projects identified as relevant, but excluded from the analysis due to poor

availability of data.

FP7€ 103 M

(32)H2020

€ 140 M (29)

EU contribution by programme CCU Projects

15

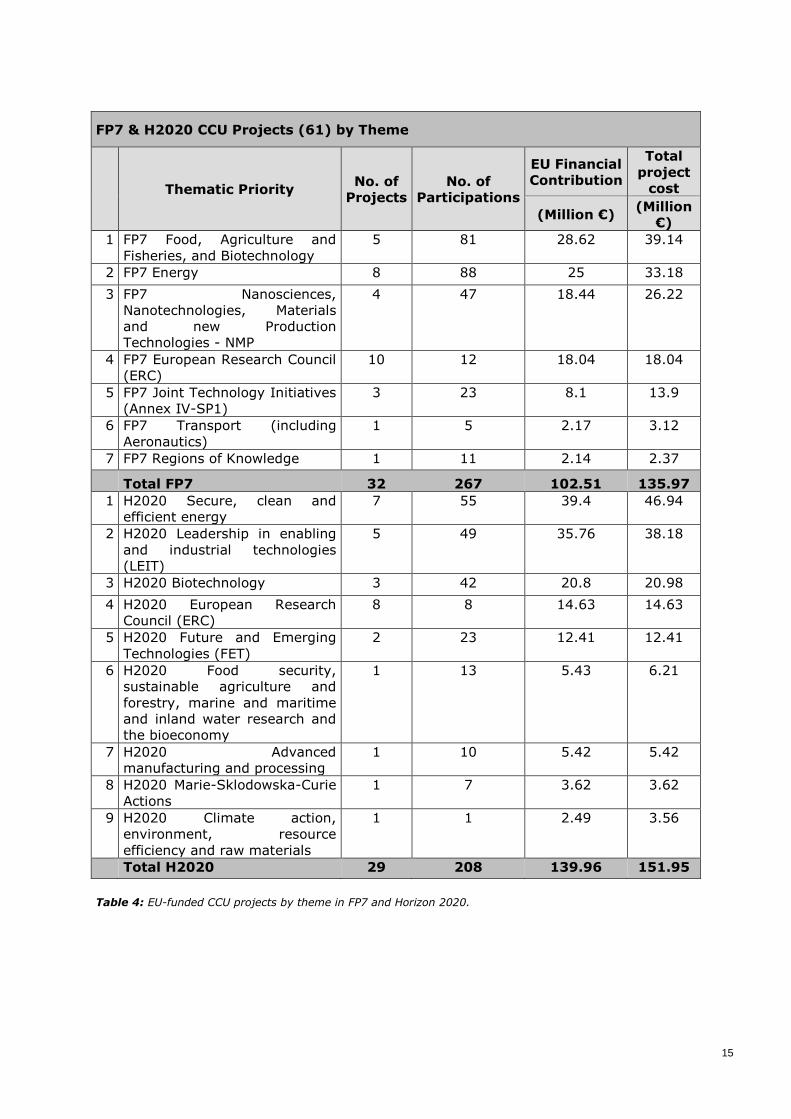

FP7 & H2020 CCU Projects (61) by Theme

Thematic Priority No. of

Projects

No. of

Participations

EU Financial

Contribution

Total

project

cost

(Million €) (Million

€)

1 FP7 Food, Agriculture and

Fisheries, and Biotechnology

5 81 28.62 39.14

2 FP7 Energy 8 88 25 33.18

3 FP7 Nanosciences,

Nanotechnologies, Materials

and new Production

Technologies - NMP

4 47 18.44 26.22

4 FP7 European Research Council

(ERC)

10 12 18.04 18.04

5 FP7 Joint Technology Initiatives

(Annex IV-SP1)

3 23 8.1 13.9

6 FP7 Transport (including

Aeronautics)

1 5 2.17 3.12

7 FP7 Regions of Knowledge 1 11 2.14 2.37

Total FP7 32 267 102.51 135.97

1 H2020 Secure, clean and

efficient energy

7 55 39.4 46.94

2 H2020 Leadership in enabling

and industrial technologies

(LEIT)

5 49 35.76 38.18

3 H2020 Biotechnology 3 42 20.8 20.98

4 H2020 European Research

Council (ERC)

8 8 14.63 14.63

5 H2020 Future and Emerging

Technologies (FET)

2 23 12.41 12.41

6 H2020 Food security,

sustainable agriculture and

forestry, marine and maritime

and inland water research and

the bioeconomy

1 13 5.43 6.21

7 H2020 Advanced

manufacturing and processing

1 10 5.42 5.42

8 H2020 Marie-Sklodowska-Curie

Actions

1 7 3.62 3.62

9 H2020 Climate action,

environment, resource

efficiency and raw materials

1 1 2.49 3.56

Total H2020 29 208 139.96 151.95

Table 4: EU-funded CCU projects by theme in FP7 and Horizon 2020.

16

EU

fundin

g i

n m

illi

on €

E

U f

undin

g i

n m

illi

on €

2.2 Portfolio of beneficiaries

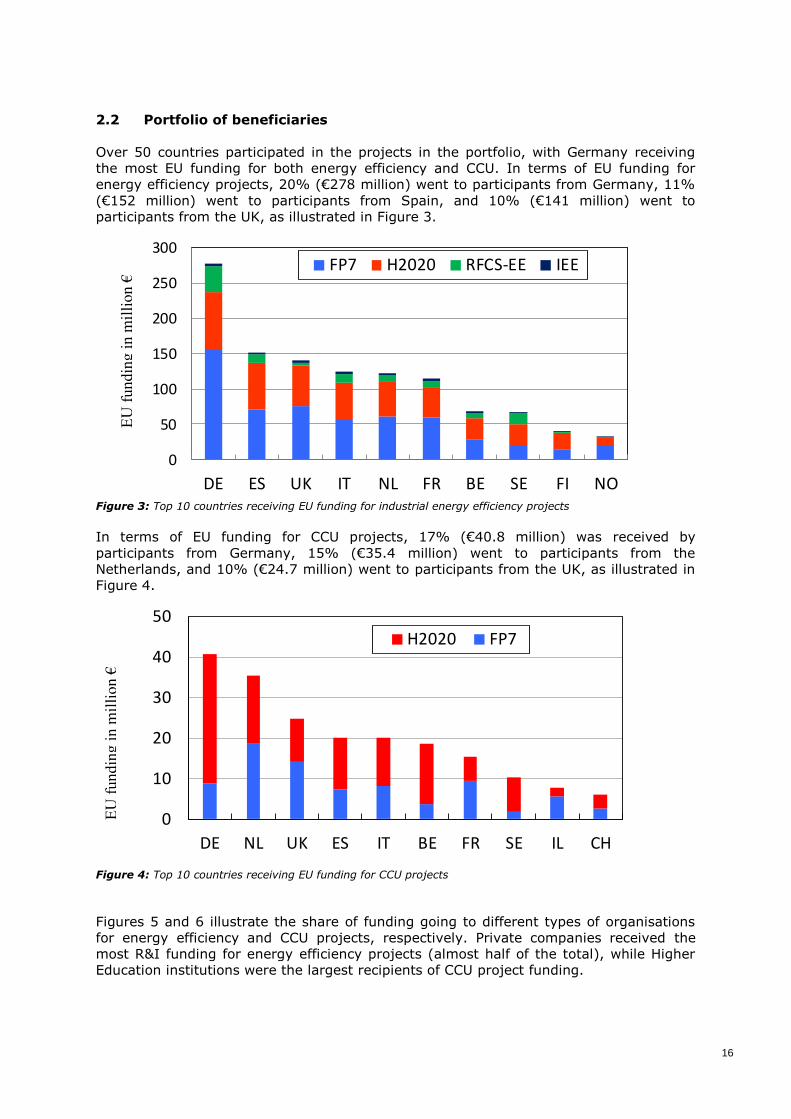

Over 50 countries participated in the projects in the portfolio, with Germany receiving

the most EU funding for both energy efficiency and CCU. In terms of EU funding for

energy efficiency projects, 20% (€278 million) went to participants from Germany, 11%

(€152 million) went to participants from Spain, and 10% (€141 million) went to

participants from the UK, as illustrated in Figure 3.

Figure 3: Top 10 countries receiving EU funding for industrial energy efficiency projects

In terms of EU funding for CCU projects, 17% (€40.8 million) was received by

participants from Germany, 15% (€35.4 million) went to participants from the

Netherlands, and 10% (€24.7 million) went to participants from the UK, as illustrated in

Figure 4.

Figure 4: Top 10 countries receiving EU funding for CCU projects

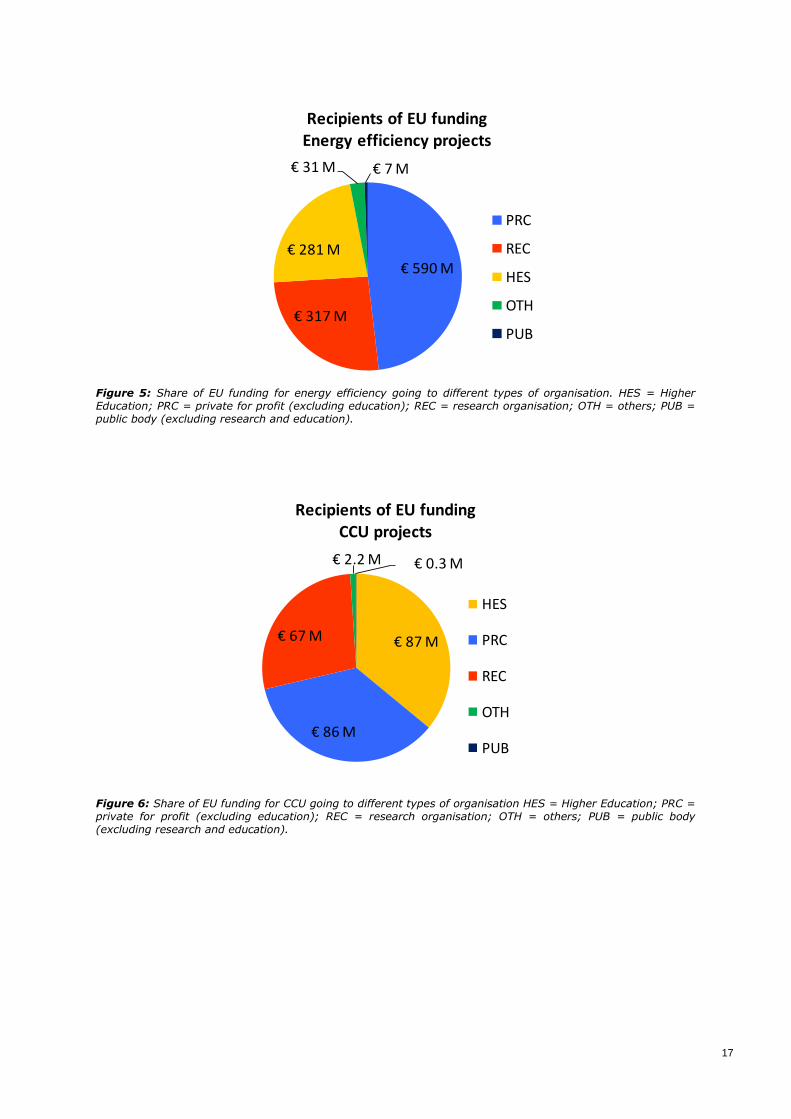

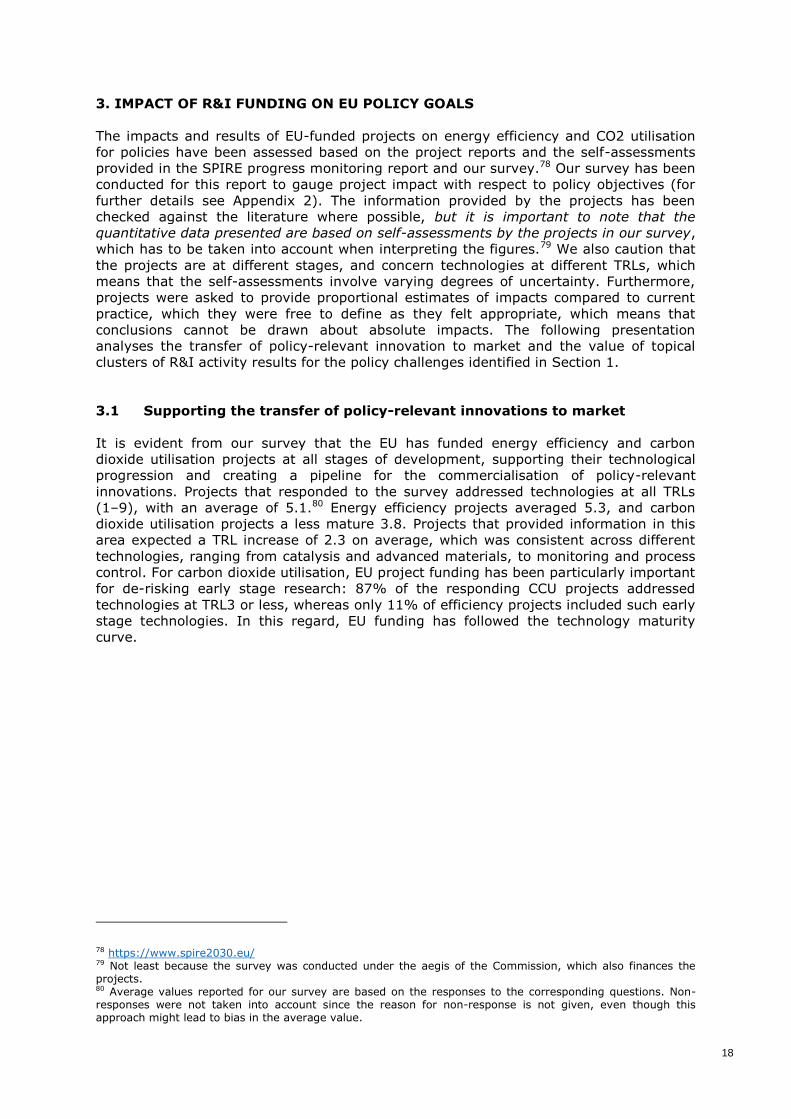

Figures 5 and 6 illustrate the share of funding going to different types of organisations

for energy efficiency and CCU projects, respectively. Private companies received the

most R&I funding for energy efficiency projects (almost half of the total), while Higher

Education institutions were the largest recipients of CCU project funding.

0

50

100

150

200

250

300

DE ES UK IT NL FR BE SE FI NO

FP7 H2020 RFCS-EE IEE

0

10

20

30

40

50

DE NL UK ES IT BE FR SE IL CH

H2020 FP7

17

Figure 5: Share of EU funding for energy efficiency going to different types of organisation. HES = Higher Education; PRC = private for profit (excluding education); REC = research organisation; OTH = others; PUB = public body (excluding research and education).

Figure 6: Share of EU funding for CCU going to different types of organisation HES = Higher Education; PRC = private for profit (excluding education); REC = research organisation; OTH = others; PUB = public body (excluding research and education).

€ 590 M

€ 317 M

€ 281 M

€ 31 M € 7 M

Recipients of EU fundingEnergy efficiency projects

PRC

REC

HES

OTH

PUB

€ 87 M

€ 86 M

€ 67 M

€ 2.2 M € 0.3 M

Recipients of EU fundingCCU projects

HES

PRC

REC

OTH

PUB

18

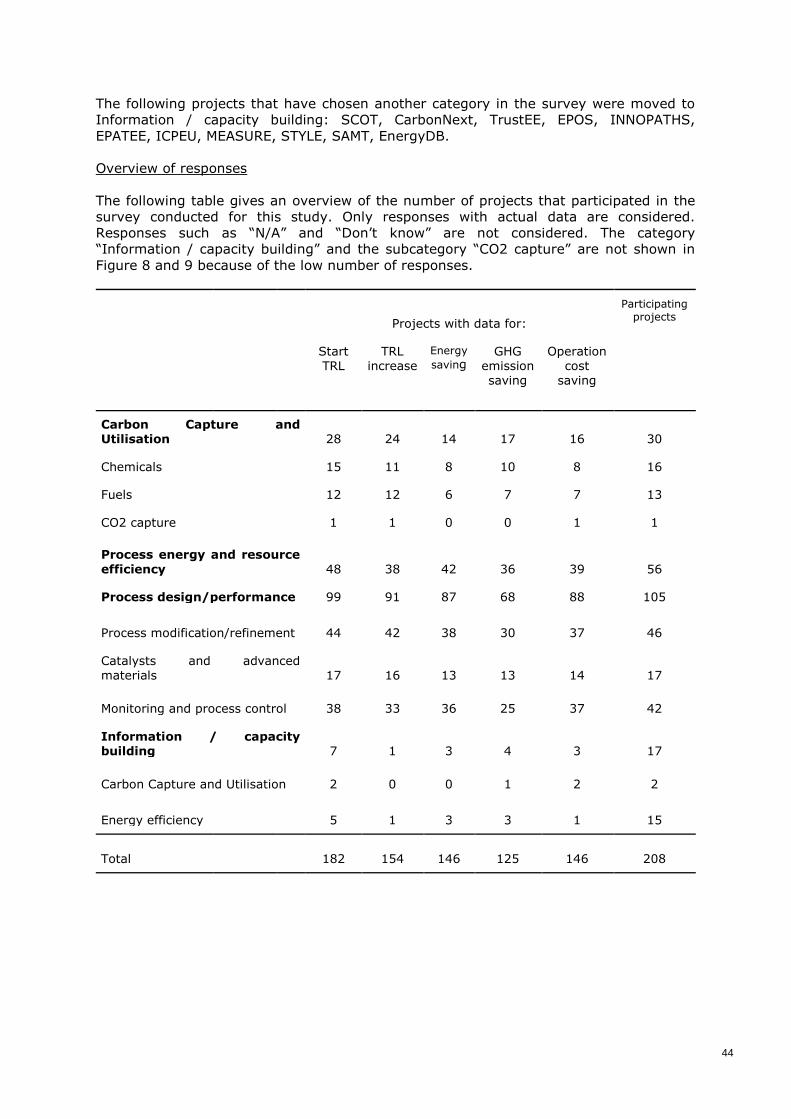

3. IMPACT OF R&I FUNDING ON EU POLICY GOALS

The impacts and results of EU-funded projects on energy efficiency and CO2 utilisation

for policies have been assessed based on the project reports and the self-assessments

provided in the SPIRE progress monitoring report and our survey.78 Our survey has been

conducted for this report to gauge project impact with respect to policy objectives (for

further details see Appendix 2). The information provided by the projects has been

checked against the literature where possible, but it is important to note that the

quantitative data presented are based on self-assessments by the projects in our survey,

which has to be taken into account when interpreting the figures.79 We also caution that

the projects are at different stages, and concern technologies at different TRLs, which

means that the self-assessments involve varying degrees of uncertainty. Furthermore,

projects were asked to provide proportional estimates of impacts compared to current

practice, which they were free to define as they felt appropriate, which means that

conclusions cannot be drawn about absolute impacts. The following presentation

analyses the transfer of policy-relevant innovation to market and the value of topical

clusters of R&I activity results for the policy challenges identified in Section 1.

3.1 Supporting the transfer of policy-relevant innovations to market

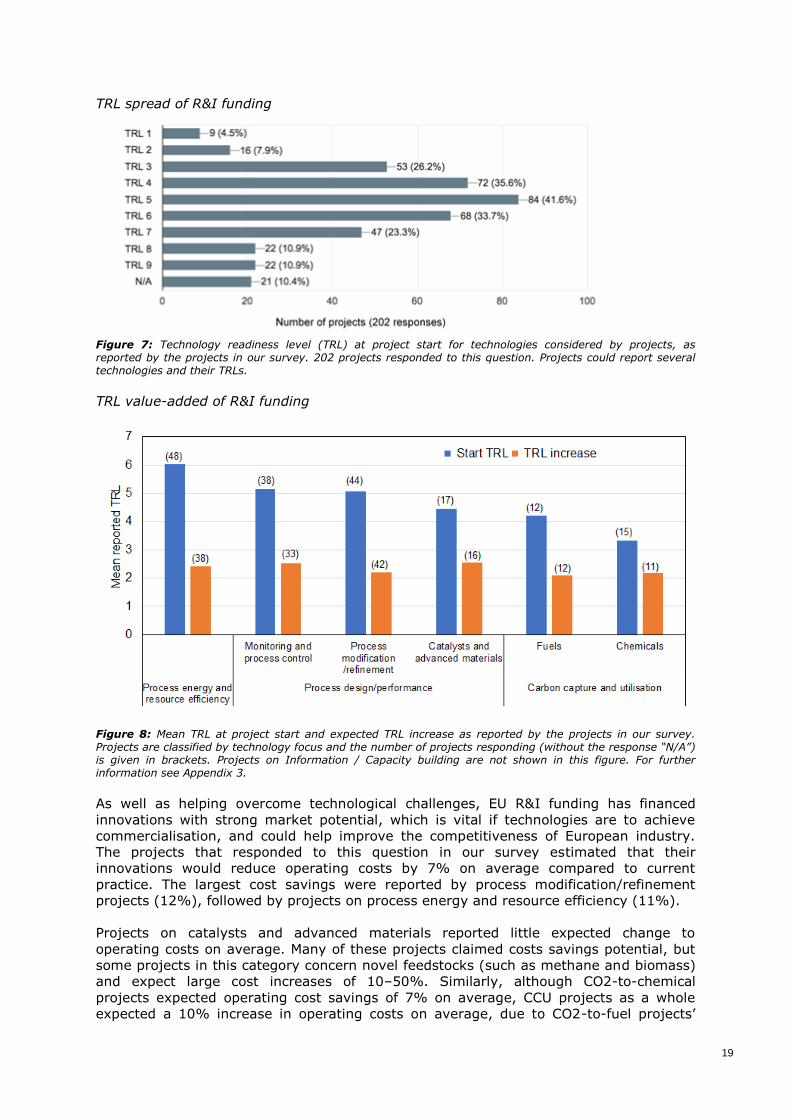

It is evident from our survey that the EU has funded energy efficiency and carbon

dioxide utilisation projects at all stages of development, supporting their technological

progression and creating a pipeline for the commercialisation of policy-relevant

innovations. Projects that responded to the survey addressed technologies at all TRLs

(1–9), with an average of 5.1.80 Energy efficiency projects averaged 5.3, and carbon

dioxide utilisation projects a less mature 3.8. Projects that provided information in this

area expected a TRL increase of 2.3 on average, which was consistent across different

technologies, ranging from catalysis and advanced materials, to monitoring and process

control. For carbon dioxide utilisation, EU project funding has been particularly important

for de-risking early stage research: 87% of the responding CCU projects addressed

technologies at TRL3 or less, whereas only 11% of efficiency projects included such early

stage technologies. In this regard, EU funding has followed the technology maturity

curve.

78 https://www.spire2030.eu/ 79 Not least because the survey was conducted under the aegis of the Commission, which also finances the projects. 80 Average values reported for our survey are based on the responses to the corresponding questions. Non-responses were not taken into account since the reason for non-response is not given, even though this approach might lead to bias in the average value.

19

TRL spread of R&I funding

Figure 7: Technology readiness level (TRL) at project start for technologies considered by projects, as reported by the projects in our survey. 202 projects responded to this question. Projects could report several technologies and their TRLs.

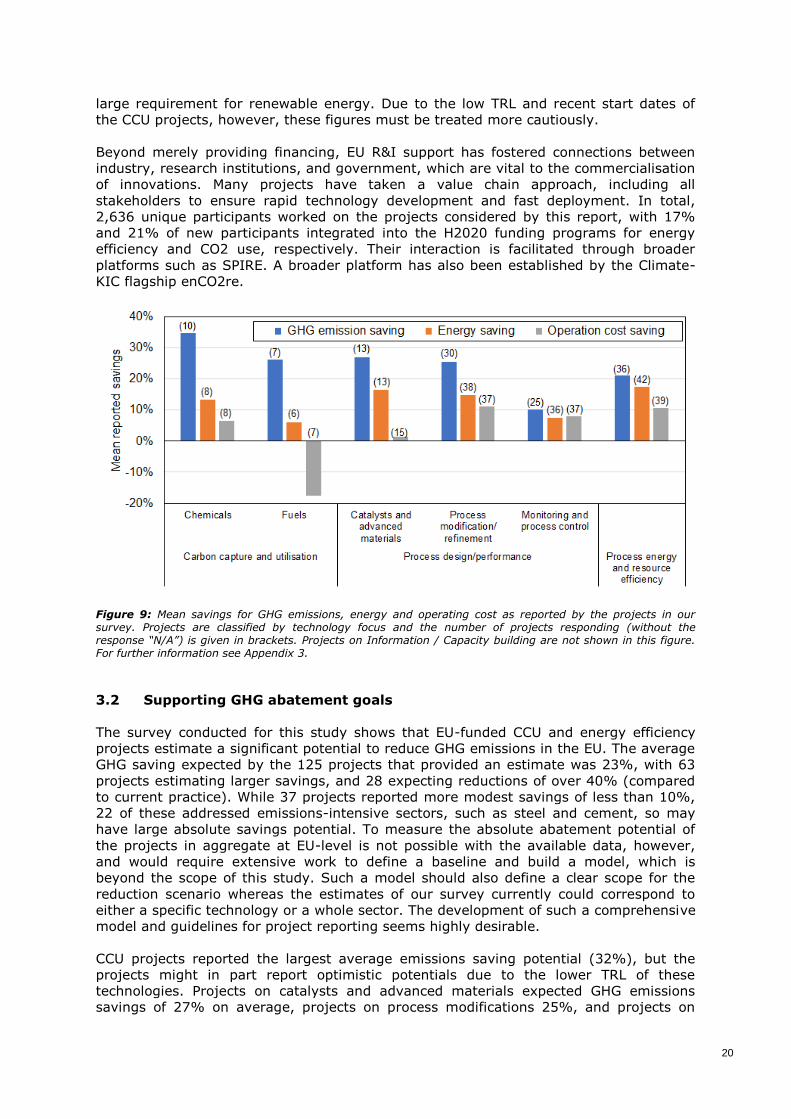

TRL value-added of R&I funding

Figure 8: Mean TRL at project start and expected TRL increase as reported by the projects in our survey. Projects are classified by technology focus and the number of projects responding (without the response “N/A”) is given in brackets. Projects on Information / Capacity building are not shown in this figure. For further information see Appendix 3.

As well as helping overcome technological challenges, EU R&I funding has financed

innovations with strong market potential, which is vital if technologies are to achieve

commercialisation, and could help improve the competitiveness of European industry.

The projects that responded to this question in our survey estimated that their

innovations would reduce operating costs by 7% on average compared to current

practice. The largest cost savings were reported by process modification/refinement

projects (12%), followed by projects on process energy and resource efficiency (11%).

Projects on catalysts and advanced materials reported little expected change to

operating costs on average. Many of these projects claimed costs savings potential, but

some projects in this category concern novel feedstocks (such as methane and biomass)

and expect large cost increases of 10–50%. Similarly, although CO2-to-chemical

projects expected operating cost savings of 7% on average, CCU projects as a whole

expected a 10% increase in operating costs on average, due to CO2-to-fuel projects’

20

large requirement for renewable energy. Due to the low TRL and recent start dates of

the CCU projects, however, these figures must be treated more cautiously.

Beyond merely providing financing, EU R&I support has fostered connections between

industry, research institutions, and government, which are vital to the commercialisation

of innovations. Many projects have taken a value chain approach, including all

stakeholders to ensure rapid technology development and fast deployment. In total,

2,636 unique participants worked on the projects considered by this report, with 17%

and 21% of new participants integrated into the H2020 funding programs for energy

efficiency and CO2 use, respectively. Their interaction is facilitated through broader

platforms such as SPIRE. A broader platform has also been established by the Climate-

KIC flagship enCO2re.

Figure 9: Mean savings for GHG emissions, energy and operating cost as reported by the projects in our survey. Projects are classified by technology focus and the number of projects responding (without the response “N/A”) is given in brackets. Projects on Information / Capacity building are not shown in this figure. For further information see Appendix 3.

3.2 Supporting GHG abatement goals

The survey conducted for this study shows that EU-funded CCU and energy efficiency

projects estimate a significant potential to reduce GHG emissions in the EU. The average

GHG saving expected by the 125 projects that provided an estimate was 23%, with 63

projects estimating larger savings, and 28 expecting reductions of over 40% (compared

to current practice). While 37 projects reported more modest savings of less than 10%,

22 of these addressed emissions-intensive sectors, such as steel and cement, so may

have large absolute savings potential. To measure the absolute abatement potential of

the projects in aggregate at EU-level is not possible with the available data, however,

and would require extensive work to define a baseline and build a model, which is

beyond the scope of this study. Such a model should also define a clear scope for the

reduction scenario whereas the estimates of our survey currently could correspond to

either a specific technology or a whole sector. The development of such a comprehensive

model and guidelines for project reporting seems highly desirable.

CCU projects reported the largest average emissions saving potential (32%), but the

projects might in part report optimistic potentials due to the lower TRL of these

technologies. Projects on catalysts and advanced materials expected GHG emissions

savings of 27% on average, projects on process modifications 25%, and projects on

21

energy and resource efficiency 21%. Lower average GHG savings are reported by

projects concerning monitoring and process control (10%), but these predominantly

addressed large-scale processes where absolute savings could be more significant (e.g.

24 out of the 42 projects addressed the sectors iron/steel and cement).

While the average GHG saving reported by the projects is lower than the Commission’s

2011 Roadmap target to reduce industrial emissions by at least 80% by 2050, we should

bear in mind that this target is set based on a 1990 baseline, while the projects were

responding compared to current practice, which is already almost halfway towards the

target. Furthermore, energy efficiency is usually a result of several technological steps

and in this regard, the projects provide significant steps. In addition, several projects

have been funded that could deliver very significant savings.

Of the six technology-oriented projects reporting the largest GHG emission savings

(>80% compared to the relevant current practices in the EU), four projects addressed

production, recycling and replacement of critical and rare materials (CritCat,

REMAGHIC), and production of chemicals and fuels based on renewable energy (SUN-to-

LIQUID, CO2EXIDE). Projects addressing electro-winning routes to steel (IERO,

SIDERWIN) also reported potential to reduce emissions by 71-80% compared to current

practices. All of these projects are, however, at an early stage or low TRL. Further

technologies related to integrating renewable energy into the fuel, chemical, and steel

sectors were prominent among the projects stating larger GHG emissions savings. These

stated breakthroughs, however, critically rely on the availability of electricity with a low

or very low carbon footprint as an enabling technology.

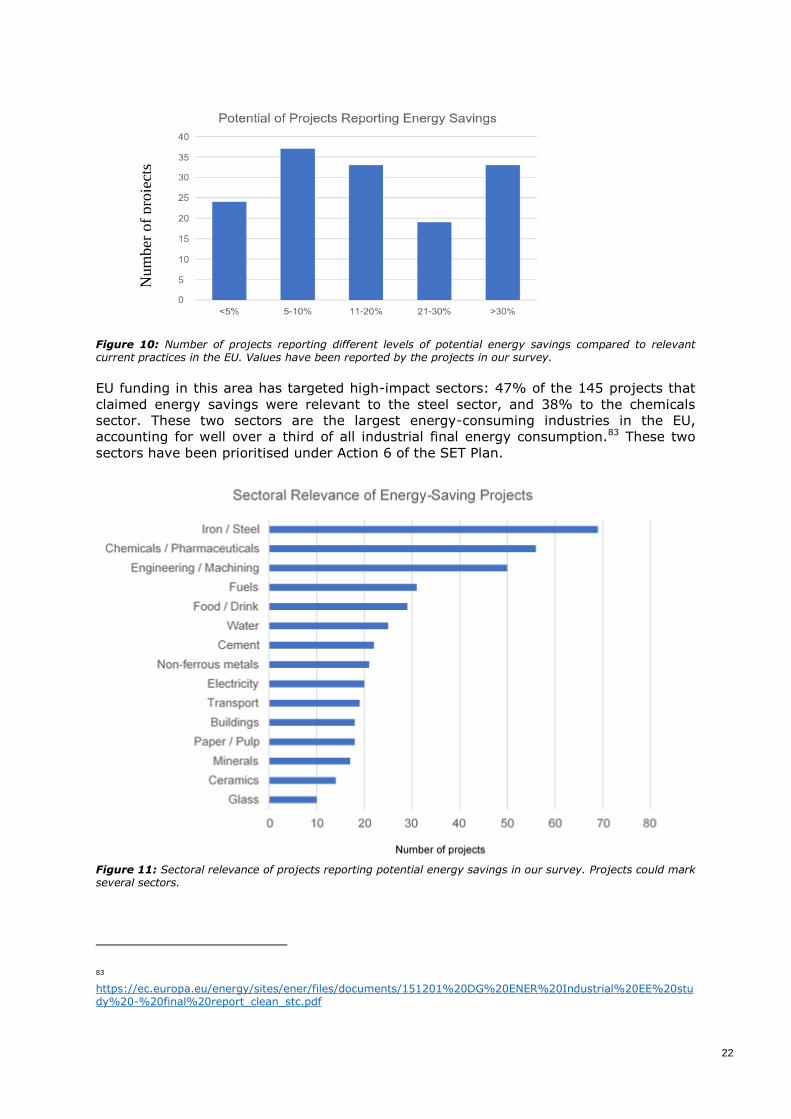

3.3 Supporting industrial efficiency goals

It is evident from our survey that EU-funded R&I projects estimate a significant potential

to help deliver industrial energy efficiency goals. Over 70% of respondents (146 projects

in total) were able to estimate their energy saving potential.81 Of these, 59% expected

energy savings of over 10% compared to current practice, 36% expected savings over

20%, and 23% expected savings over 30%. More than half of these projects addressed

technologies with a TRL of 8, which supports the demonstration targets of Action 6 of the

SET Plan. Energy and resource efficiency projects reported the largest energy savings

with 17% on average, followed by projects concerning process design/performance with

12% energy savings on average. Projects concerned with large-scale energy-intensive

industries, such as steel and cement, reported lower relative emissions savings on

average, but these could still lead to large absolute savings.82 Interestingly, 14 projects

on carbon dioxide utilisation responded regarding energy efficiency and estimated

energy savings of 10% on average.

81 Our survey did not ask respondents to specify the type of energy saved (primary, final, fossil, etc), which should be borne in mind when interpreting the results. 82 Most respondents to the survey did not provide absolute saving estimates, however, and the scale of savings cannot be accurately inferred from sector alone, which should be borne in mind when interpreting the results.

22

Energy saving compared to relevant current

practices in the EU

Num

ber

of

pro

ject

s

Figure 10: Number of projects reporting different levels of potential energy savings compared to relevant current practices in the EU. Values have been reported by the projects in our survey.

EU funding in this area has targeted high-impact sectors: 47% of the 145 projects that

claimed energy savings were relevant to the steel sector, and 38% to the chemicals

sector. These two sectors are the largest energy-consuming industries in the EU,

accounting for well over a third of all industrial final energy consumption.83 These two

sectors have been prioritised under Action 6 of the SET Plan.

Figure 11: Sectoral relevance of projects reporting potential energy savings in our survey. Projects could mark several sectors.

83 https://ec.europa.eu/energy/sites/ener/files/documents/151201%20DG%20ENER%20Industrial%20EE%20study%20-%20final%20report_clean_stc.pdf

23

EU R&I funding has effectively supported high-impact sector-specific technologies

recognised by the SET Plan as offering the most technical potential. These include

breakthrough routes to iron and steel, such as bath smelting, blast furnace top-gas

recycling, and electro-winning (e.g. HIsarna B and C, LoCO2FE, ULCOS TGRBF, IERO,

SIDERWIN),84 as well as key technologies for the chemicals sectors, such as cracking

furnace optimisation, catalytic/membrane reactors, process intensification, and heat

exchange optimisation (e.g. IMPROOF, INTENT, ROMEO, MEMERE, TUNEMEM, ADREM,

DEMCAMER, TOPCHEM, F3 FACTORY, SYNFLOW, CLEANEX, THERMONANO).

As well as facilitating sector-specific improvements in industrial energy efficiency, EU

funding has effectively supported key cross-sectoral technologies, such as integrated

control systems, real-time monitoring, and combustion optimisation options, as well as

capacity building projects that promote efficiency networks, energy auditing, Energy

Management Systems, training, and benchmarking (e.g. COCOP, DISIRE, MORE, CoPro,

FUDIPO, CONSENS, TASIO, COMBI, VADEMECOM, VULKANO, SAMT, STYLE, MEASURE,

EuPlastVoltage, STEEEP, EUREMplus, PINE, TrustEE). Industrial symbiosis projects, were

less well represented in the portfolio, but some offered great promise for facilitating

significant cross-sectoral efficiency improvements in the EU (e.g. EPOS, SHAREBOX). A

number of projects have been funded that specifically address the issue of barriers to

energy efficiency and effective policymaking, which may be of interest to policymakers

and have informed Section 4 of this report (e.g. ODYSSEE-MURE, CA EED).

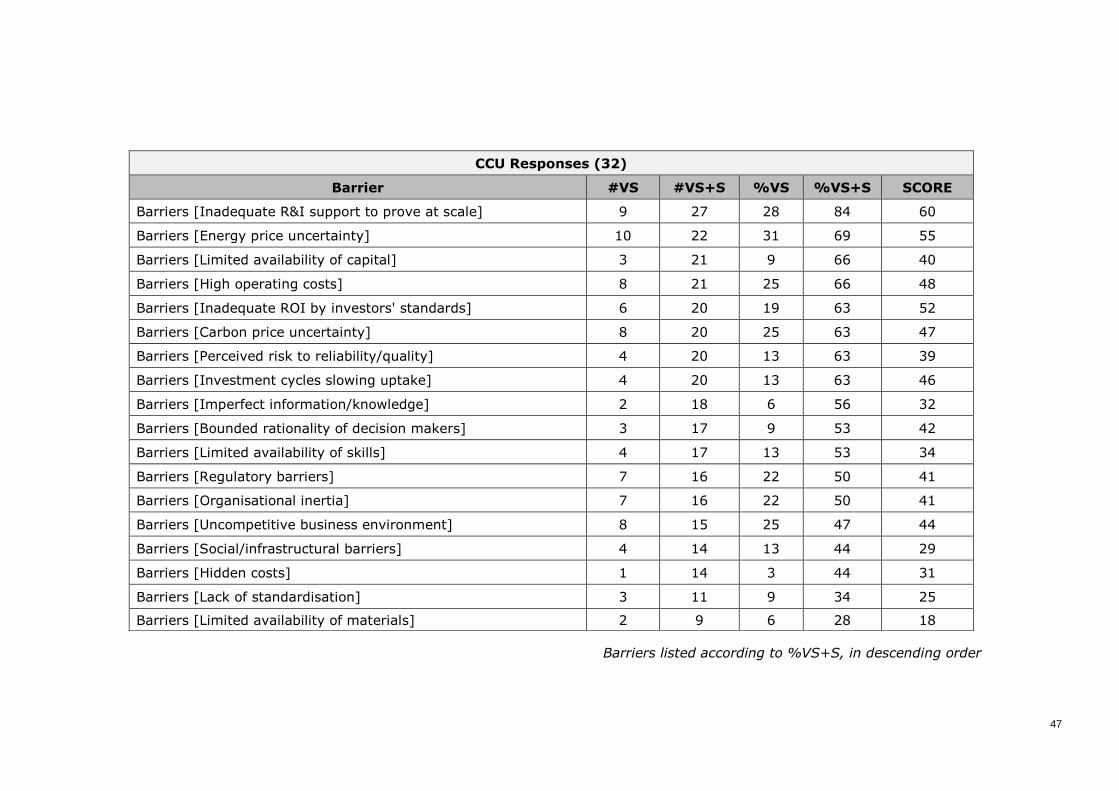

3.4 Supporting goals to develop CO2 utilisation technologies

CCU projects reported the largest GHG savings potential among the responses to the

survey conducted for this study (see Figure 9), which indicates that the projects see a

large potential for their technologies to help deliver EU climate goals. The mechanism for

GHG reduction is different for different CCU technologies (see Section 1). This is

reflected in the findings of our survey where e.g. projects on CO2-for-fuels differ with

respect to cost impacts from CO2-for-chemicals (see above). The CO2-based products

investigated in the EU-funded projects include chemicals (e.g. syngas, ethane, propane,

oxygenates and alkenes, polymers, and carboxylic acid) and fuels (e.g. methanol and

kerosene). The chemicals mainly address bulk chemicals, which could sometimes even

be used as fuels. Thereby, the largest potential markets in the chemical industry are

addressed, but these type of CCU products also usually require large amounts of low

carbon electricity to reduce GHG emissions compared to their fossil-based

counterparts.85 Notably, the projects in the portfolio on CO2 use aim at GHG reductions

via replacing fossil-based feedstocks, improving energy and resource efficiency, and

integrating renewable energy, but not via carbon storage. Thus, the current scientific

debate about the impact of temporary storage by CCU is not relevant to the findings of

this report and to these technologies.

EU R&I investment has been highly valuable to the field of CO2 utilisation in providing

funding to early stage research with a low TRL. Hereby, CO2 utilisation projects have

identified and further developed a broad range of process concepts to sustainably

introduce CO2 into the chemical value chain. In line with the early stage of the field, all

catalytic concepts have been addressed ranging from chemo-catalysis (e.g. CyclicCO2R,

MefCO2) to electro-catalytic (e.g. CEOPS), photo-catalysis (e.g., ECO2CO2) and bio-

catalysis, which had an emphasis on algae-based conversion of CO2 (e.g. GIAVAP,

AquaFuels). Algae-based biorefineries are a topic of further intensive research, e.g. as

part of the Bio-Based Industry – Joint Undertaking (BBI-JU).86 Some projects focused

specifically on catalysis aspects (e.g. AfterTheGoldrush, EURECAT, FunCBonds, novcat)

84 Although there were no DRI or hydrogen steelmaking projects in the portfolio. 85 http://publications.jrc.ec.europa.eu/repository/handle/JRC99380 86 https://www.bbi-europe.eu/

24

or CO2 capture (e.g. NoCO2, CaOling, IOLICAP, CAPSOL, RECaL, ASC2), while other

projects consider the entire value chain from feedstock supply to the final product (e.g.

DirectFuel, MIRACLES, BioWalk4Biofuels). Key breakthroughs towards the development

of carbon dioxide technologies have also been achieved in various projects with

demonstration of novel technologies in continuous production (e.g. CyclicCO2R,

ECO2CO2) and along the full value chain (e.g. SOLAR-JET).

EU funding not only supported the technological development of the field, but also the

development of an understanding of the potential of CCU for policy challenges. In this

regard, information-oriented projects like SCOT as well as reports and studies on

CCU (e.g. by JRC, Carbon Count/Ecofys’ 2013 study for DG Climate Action) have been

very valuable to provide techno-economic and environmental assessments, and to

propose action plans for policy.87 88 For carbon dioxide utilisation, Climate-KIC

established the flagship enCO2re to fund research with a focus on valorisation and has

also had a strong impact on start-up development, while also serving as a technology

platform and supporting knowledge dissemination.89 The SCOT project has developed a

Joint Action Plan for Smart CO2 Transformation in Europe90. Through this better

understanding, the critical needs of certain CCU technologies, e.g. for clean electricity,

have been identified as well as further promising options for CO2 utilisations beyond the

fuel and bulk chemical market. The EU-funding portfolio has therefore been expanded to

integrate projects offering high GHG savings while also reducing operation cost, albeit in

smaller markets than fuels (e.g. Carbon4PUR). CO2 conversion and valorisation by

mineralisation has already been recognised as highly promising since it could offer both

valuable products, e.g. for the building sector, and carbon storage.91 Still, CO2

valorisation by mineralisation is still largely unexplored.

The EU-funded projects have also provided significant support for policy implementation

by identifying current barriers for the large-scale implementation of CO2 utilisation. The

major barriers for CO2 utilisation projects are the low price of fossil feedstocks (DEMA,

ECO2CO2), the often higher operating costs, and the low price of the substitute fossil-

based products. The projects draw attention to their need for an explicit definition of the

role of captured and avoided CO2 by utilisation in the current phase of the EU ETS

scheme and for agreed rules for life-cycle assessment (LCA) specific to CCU

technologies. These insights have been picked up in the current revision of the Fuel

Quality Directive, which will include CO2-based fuels and where the greenhouse gas

intensity of novel transport fuels will be calculated through a common LCA methodology.

A workshop series has also been started on the definition of LCA for CCU.92

87 http://publications.jrc.ec.europa.eu/repository/handle/JRC99380 88 https://www.ecofys.com/en/project/assessing-co2-reuse-technologies/ 89 http://enco2re.climate-kic.org/ 90 www.scotproject.org/images/SCOT%20JAP.pdf 91 http://publications.jrc.ec.europa.eu/repository/bitstream/JRC86324/co2%20re-use%20workshop%20report__isbn__online__eur__pages.pdf 92 https://ec.europa.eu/energy/en/content/workshop-life-cycle-analysis-carbon-capture-utilisation-6-june-2017

25

4. POLICY RECOMMENDATIONS

Having outlined the potential of the projects in the study portfolio, this section seeks to

identify non-technological barriers to realising this potential, and recommend policy

approaches that could alleviate these barriers to help deliver the policy challenges

identified in Section 1.

Four broad policy recommendations are set out below with accompanying measures.

These have been derived directly from the projects in the portfolio. Firstly, through the

survey conducted for this study, which asked Project Coordinators what they thought

would be the most significant barriers and beneficial policies for their projects’

innovations up to 2050.93 And secondly through analysing specific learnings from

relevant projects in the portfolio. This was then complemented with a review of the

recent white and grey literature, and consultation with stakeholders at a workshop, to

turn the information from the projects into more concrete and evidenced

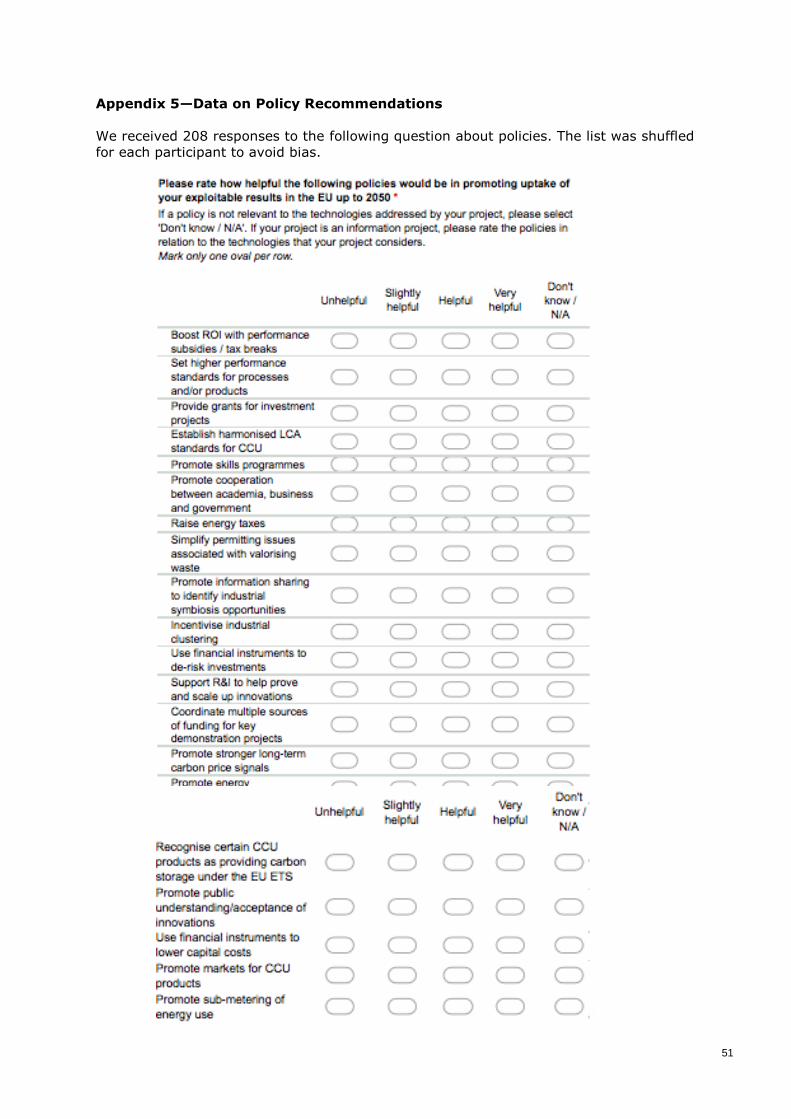

recommendations for policymakers’ consideration. (For further information on the survey

please see Appendices 2–5.)

The recommendations have been designed to be barrier-responsive, and focus on high-

impact interventions, while remaining consistent with existing EU policies, and respecting

instrument-neutrality.

93 Survey participants were asked to provide their long-term view on barriers and policies up to 2050, so as to

capture issues relevant to the market uptake stage as well as the R&I stage. This is a speculative exercise (especially for projects with a lower TRL) and we should bear in mind that Coordinators are (typically) not decision-makers within companies, nor policy experts. Nevertheless, it is assumed that they are an informed audience that is relatively well placed to provide a view on barriers and policies in relation to their own innovations, which may be of interest to policymakers.

26

4.1 Remove barriers to energy efficiency investment

There is significant technical potential to improve industrial efficiency, as the discussion

in section 3 and the literature suggests. To unlock this potential and attract investment,

the EU will have to create stable long-term economic conditions, and a hospitable

regulatory environment, as well as alleviate a range of economic and non-economic

barriers, which the following two actions seek to address.

The EU should promote cutting-edge auditing and energy management within

active energy efficiency communities. An extensive literature suggests that many

economic energy efficiency opportunities are not pursued, due to a range of behavioural

and knowledge barriers, such as imperfect information, insufficient skills, organisational

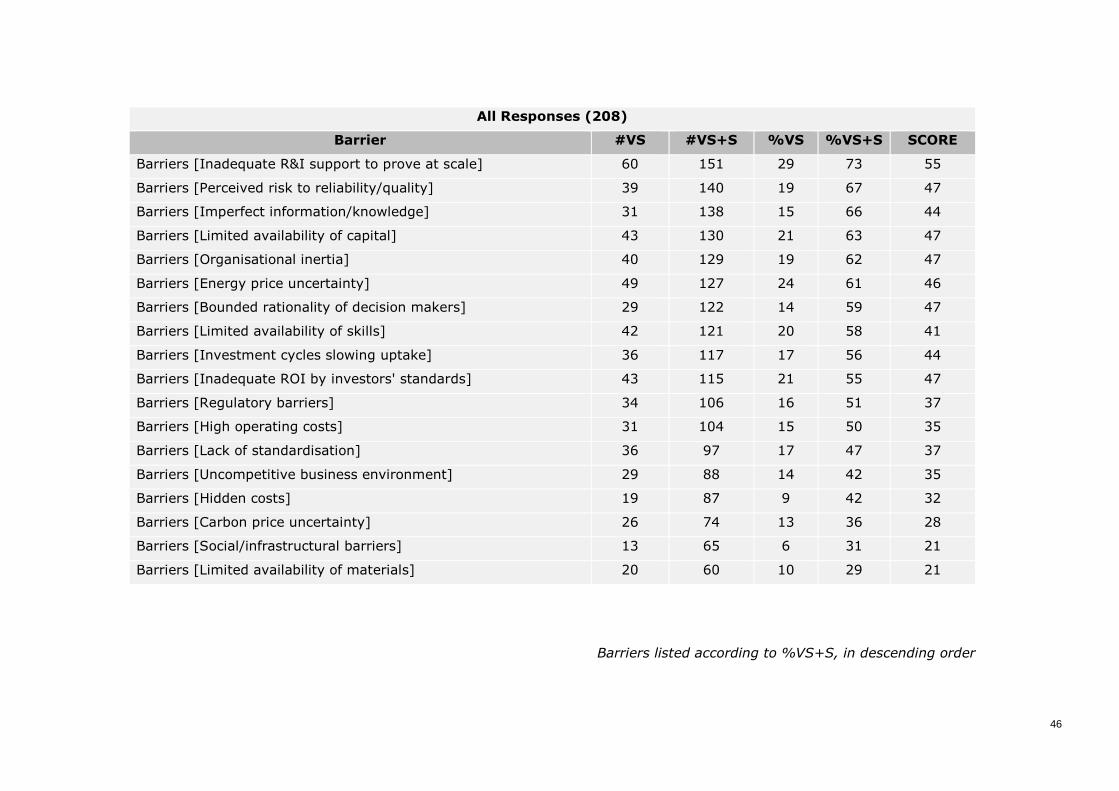

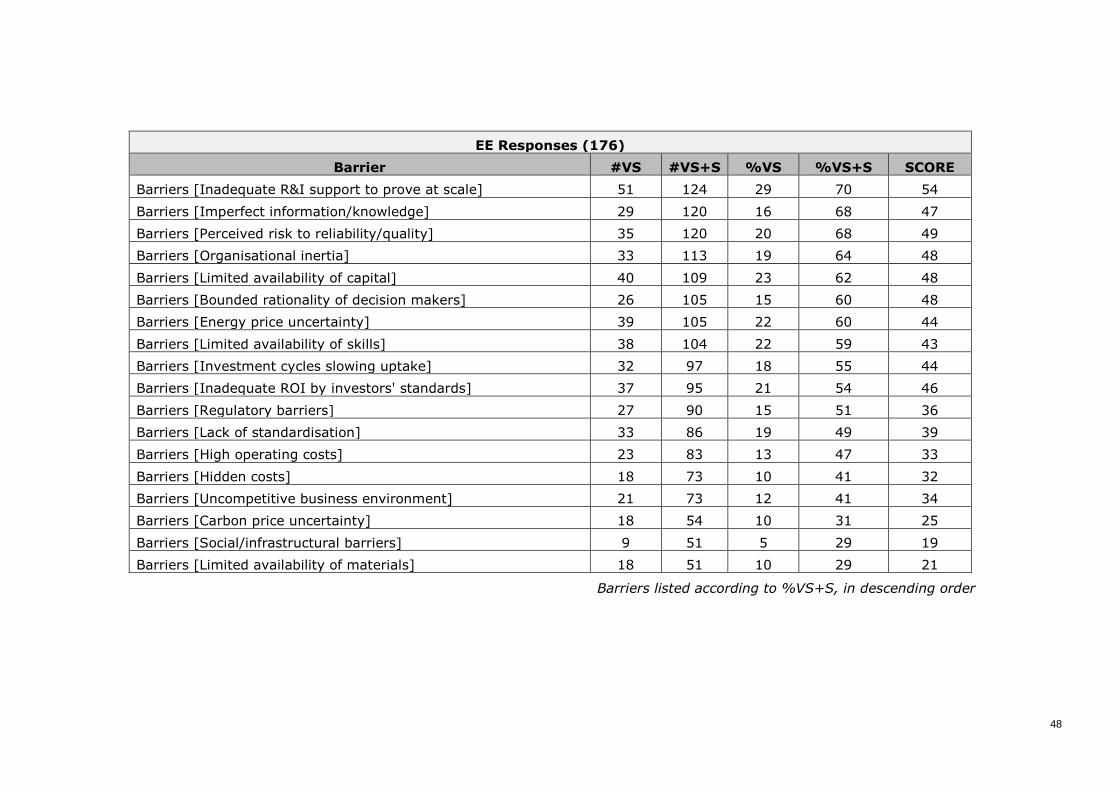

inertia, and bounded rationality. 94 95 This is corroborated by our survey, which found

that on average, 63% of energy efficiency respondents rated these barriers Very

Significant or Significant to the uptake of their innovations: more than any other type of

barrier. To tackle this problem, the EU must work with Member States to promote active

energy efficiency communities that practise cutting-edge auditing and energy

management, and use their results to mobilise energy efficiency investments.

The ODYSSEE-MURE project has identified audit promotion as one of the most effective

policy interventions, and there is significant scope for the EU to do more in this area. 96

Under the EED, large enterprises are required to conduct energy audits every four years,

and Member States must implement policies to promote energy auditing among SMEs.97

The CA EED project has found in a preliminary assessment, however, that Member

States have implemented these requirements with varying degrees of success, and

auditing among industrial SMEs still faces significant barriers, which is corroborated by

the wider literature. 98 99 100 The effectiveness of energy audits also critically depends on

the method used, and the auditor’s awareness of energy saving opportunities, which are

numerous and constantly evolving.

The EU should continue to fund projects in this area, which have proven their value in

the past. For instance, PInE (funded under IEE) unlocked €8.4m of investment in three

years through an SME auditing programme, leading to 6,056 toe/year primary energy

savings, and 12,505 tCO2/year of GHG emissions reduction.101 The EU should also

promote best practice in high-quality auditing among Member States, developing central

resources for this purpose. To this end, as well as developing tools and templates, the

EU should build and maintain a central library of energy saving opportunities, based on

Member State audit data, and the latest exploitable results from EU and Member State

R&I.102 This would improve auditors’ awareness of opportunities, and ensure audits take

account of the latest technological developments. Complementary incentives could then

be provided for companies prepared to implement new technologies in the database,

either at EU or Member State level, supporting market uptake of innovation.

To roll out cutting-edge auditing, the EU will have to build skills capacity. Indeed, the CA

EED project has identified that Member States are concerned about a shortage of energy

94 http://sro.sussex.ac.uk/53957/1/WP102011_Barriers_to_Industrial_Energy_Efficiency_-_A_Literature_Review.pdf 95 http://proceedings.eceee.org/papers/proceedings2012/5-172-12_Cagno.pdf?returnurl... 96 http://www.measures-odyssee-mure.eu/successful-detail-measures.asp 97 http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1399375464230&uri=CELEX:32012L0027 98 http://www.ca-eed.eu/private-area/outcomes/executive-summary-report 99 https://www.iea.org/publications/freepublications/publication/SME_2015.pdf 100 https://ec.europa.eu/energy/sites/ener/files/documents/EED-Art8-Energy%20audits%20recommendations-Task%205-report%20FINAL.pdf 101 http://www.pineaudit.eu/eng/resources.aspx 102 https://ec.europa.eu/energy/sites/ener/files/documents/EED-Art8-Energy%20audits%20recommendations-Task%205-report%20FINAL.pdf

27

auditors, and the quality of auditors. This is also recognised in the literature, and

corroborated by our survey, which found that almost 60% of energy efficiency

respondents said that inadequate skills were a Very Significant or Significant barrier to

the uptake of their innovations. 103 104 The EU should continue to fund capacity building

projects, e.g. the EUREM programme, which now offers training in 19 European

countries, and has trained over 4,500 energy managers.105 In addition, the EU should

encourage harmonisation of qualification requirements across Member States (so as not

to constrain auditors’ activity within international companies), and explore the possibility

of working with Member States on capacity building under the new Blueprint for Sectoral

Cooperation on Skills. 106 107

While periodic audits are very valuable, the EU must also promote the implementation of

Energy Management Systems (EnMSs) that ensure companies consider energy

consumption in their day-to-day decision making.108 Indeed, 56% of energy efficiency

respondents to our survey said that promoting EnMSs would be Very Helpful or Helpful

to supporting uptake of their innovations, and the value of EnMS is widely acknowledged

in the literature.109 110 The EED exempts large enterprises from the requirement to

conduct energy audits every four years if they have implemented an EnMS, but there is

no requirement to have an EnMS, and implementation varies significantly between

Member States.111 112 Furthermore, SMEs are particularly unlikely to have an Energy

Management System due to their more limited resources. For SMEs, minimising the

administrative burden of energy audits and EnMS seems therefore particularly

important. The EU should continue to fund projects that promote EnMSs (e.g. EXBESS),

and support dissemination of best practice in terms of Member State policies. It is

evident, for instance, that fiscal reliefs for implementing EnMS have proven very

effective in Germany, which has over 2,000 ISO 50001 certifications (more than any

other country in the world).113 The CA EED project has also drawn attention to the value

of simplified web-based EnMSs for SMEs, and SMEs’ particular need for financial and

technical support to implement energy management practices.114

Truly effective auditing and energy management does not happen in isolation, but in

energy efficiency communities. Companies must communicate and compare practices to

identify potential, share expertise among interested actors in energy efficiency markets

(including financial actors), and motivate each other to implement opportunities. A

number of Member States have adopted initiatives in this regard, but there is significant

103 http://www.esd-ca.eu/outcomes/executive-summary-report 104 https://ec.europa.eu/energy/sites/ener/files/documents/151201%20DG%20ENER%20Industrial%20EE%20study%20-%20final%20report_clean_stc.pdf 105 eurem-plus.eu/download/attachments/511082775/Final%20Report_Web.pdf 106 http://www.ca-eed.eu/private-area/outcomes/executive-summary-report 107 http://ec.europa.eu/social/main.jsp?catId=738&langId=en&pubId=7969 108 https://www.oecd.org/sti/ind/DSTI-SU-SC(2014)14-FINAL-ENG.pdf 109 https://ec.europa.eu/energy/sites/ener/files/documents/151201%20DG%20ENER%20Industrial%20EE%20study%20-%20final%20report_clean_stc.pdf 110 https://ec.europa.eu/energy/sites/ener/files/documents/EED-Art8-Energy%20audits%20recommendations-Task%205-report%20FINAL.pdf 111 http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1399375464230&uri=CELEX:32012L0027 112 http://publications.jrc.ec.europa.eu/repository/bitstream/JRC95432/survey%20of%20energy%20audits%20and%20energy%20management%20systems%20in%20the%20member%20states_pub.pdf 113 http://publications.jrc.ec.europa.eu/repository/bitstream/JRC95432/survey%20of%20energy%20audits%20and%20energy%20management%20systems%20in%20the%20member%20states_pub.pdf

114 http://www.esd-ca.eu/outcomes/executive-summary-report

28