Embed Size (px)

Citation preview

Long- te rm ma cro a nd ma rket outlook

Eirik Wæ rness, SVP a nd Chief EconomistInstitute of Energy Economics, Tokyo, 27 September 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

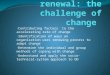

Recent signposts show diverging pa ths, in terms of:

• Growth• Efficiency• Coopera tion• Technology• Geopolitics

In which direction is the energy world moving?

Higher ca rbon prices

Energy dema nd

up over 2% in 20 17

Renewa ble costs

dropping

LNG ma rke t

growing

US-Chinatra de

tensions

Ira n nuclea r dea l a t risk?

Coa l dema nd

up

Booming EV sa les

Conflicts in ME

CO2emissions

upRecord

sola r a nd windca pa city

2 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

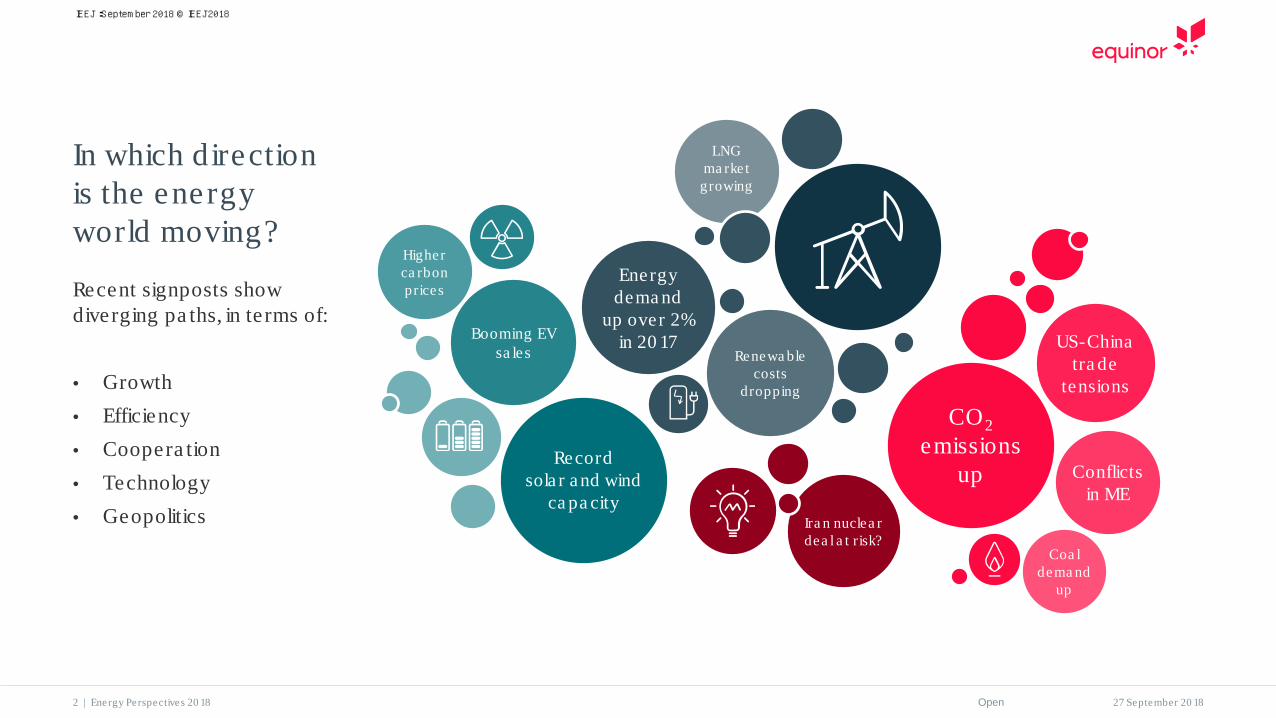

• Growth• Efficiency• Coopera tion• Technology• Geopolitics

Scena rios

In which direction is the energy world moving?

Recent signposts show diverging pa ths, in terms of:

Current trends a nd policy direction

Ma rket a nd Technology driven

NDCs

Geopolitica l vola tility

Boom a nd bust cycles

Destructive ma rket rule

La ck of coopera tion

Policy driven

Globa l coopera tion

Fa st tra nsition

2° ta rget

Riva lry

Reform

Renewa l

Higher ca rbon prices

Energy dema nd

up over 2% in 20 17

Renewa ble costs

dropping

LNG ma rke t

growing

US-Chinatra de

tensions

Ira n nuclea r dea l a t risk?

Coa l dema nd

up

Booming EV sa les

Conflicts in ME

CO2emissions

upRecord

sola r a nd windca pa city

3 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

• Globa l dema nd forenergy dependentgoods, services, a nda ctivities is growing

• The world is undergoinga n energy tra nsition

• La rge investmentsneeded in the energysystem

Wha t a re common be lie fs a bout the future?

4 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

20

40

60

80

100

1990

2000

2010

2020

2030

2040

2050

Re form Re ne wa l Riva lry

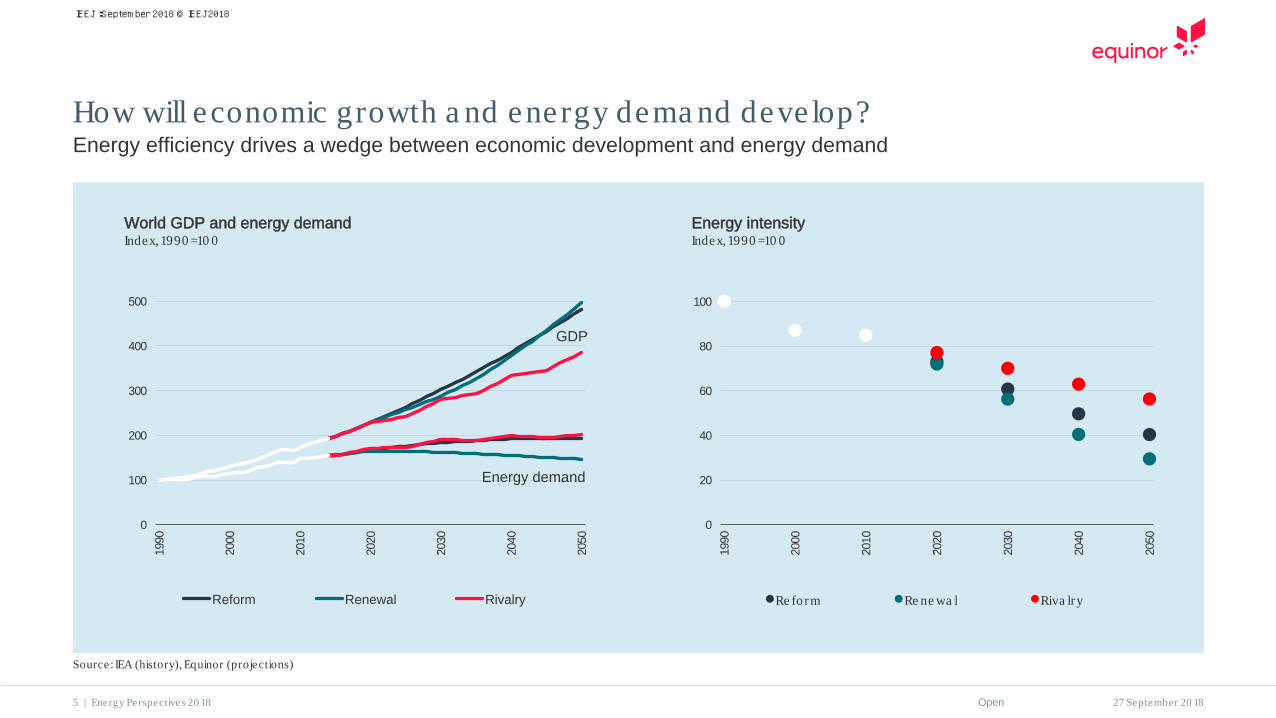

How will economic growth a nd energy dema nd deve lop?Energy efficiency drives a wedge between economic development and energy demand

0

100

200

300

400

500

1990

2000

2010

2020

2030

2040

2050

Reform Renewal Rivalry

Energy demand

GDP

World GDP and energy demandIndex, 1990 =10 0

Energy intensityIndex, 1990 =10 0

Source: IEA (history), Equinor (projections)

5 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

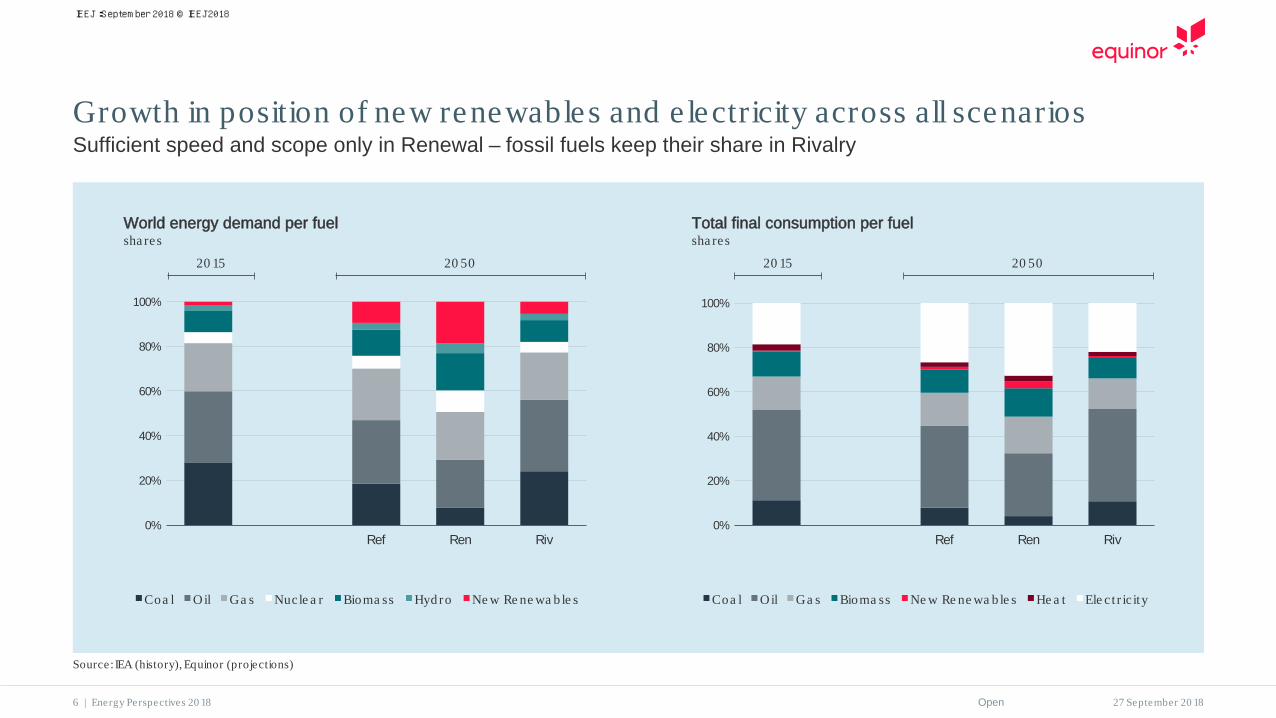

Growth in position of new renewa bles a nd e lectricity a cross a ll scena riosSufficient speed and scope only in Renewal – fossil fuels keep their share in Rivalry

0%

20%

40%

60%

80%

100%

Ref Ren Riv

Coa l Oil Ga s Nucle a r Bioma ss Hyd ro Ne w Re ne wa b le s

20 15 20 50

World energy demand per fuelsha res

20 15 20 50

Total final consumption per fuelsha res

0%

20%

40%

60%

80%

100%

Ref Ren Riv

Coa l Oil Ga s Bioma ss Ne w Re ne wa b le s He a t Ele c t r ic ity

Source: IEA (history), Equinor (projections)

6 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

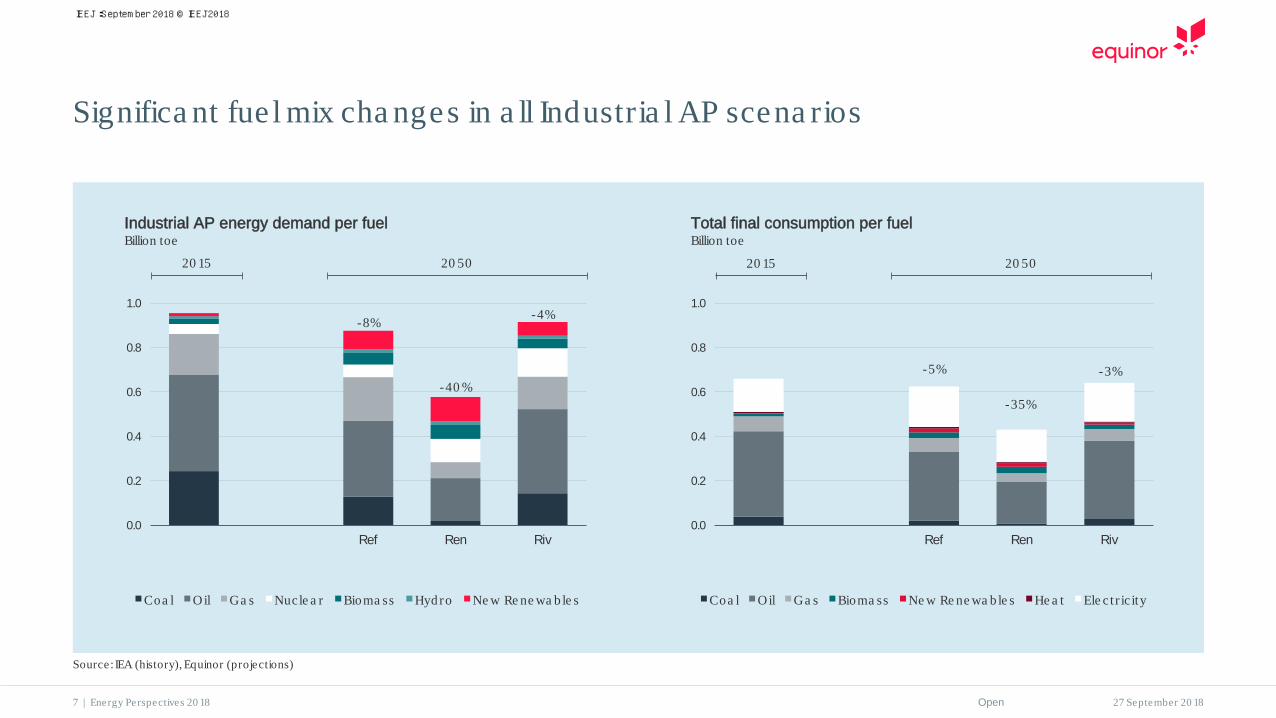

Significa nt fue l mix cha nges in a ll Industria l AP scena rios

Source: IEA (history), Equinor (projections)

7 | Energy Perspectives 20 18

-8%

-40 %

-4%

0.0

0.2

0.4

0.6

0.8

1.0

Ref Ren Riv

Coa l Oil Ga s Nucle a r Bioma ss Hyd ro Ne w Re ne wa b le s

20 15 20 50

Industrial AP energy demand per fuelBillion toe

-5%

-35%

-3%

0.0

0.2

0.4

0.6

0.8

1.0

Ref Ren Riv

Coa l Oil Ga s Bioma ss Ne w Re ne wa b le s He a t Ele c t r ic ity

20 15 20 50

Total final consumption per fuelBillion toe

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 188 | Energy Perspectives 20 18

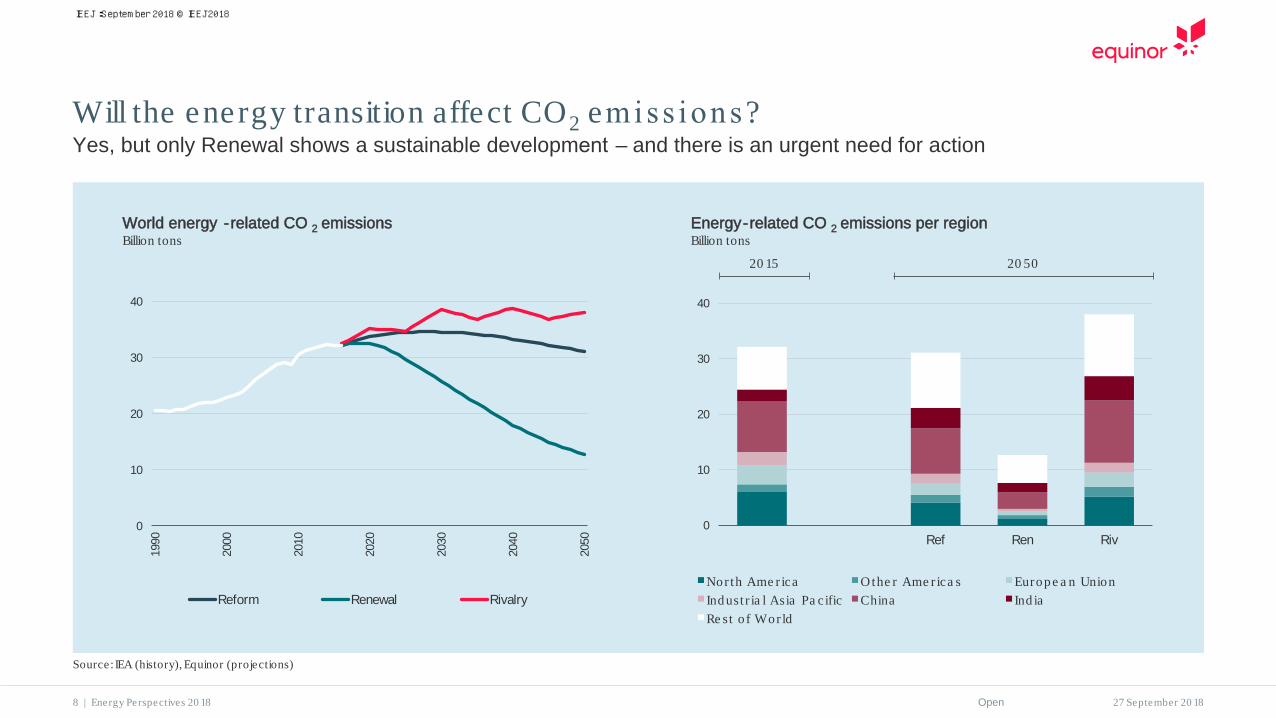

Will the energy tra nsition a ffect CO2 emiss ions?Yes, but only Renewal shows a sustainable development – and there is an urgent need for action

0

10

20

30

40

1990

2000

2010

2020

2030

2040

2050

Reform Renewal Rivalry

World energy -related CO 2 emissionsBillion tons

Source: IEA (history), Equinor (projections)

0

10

20

30

40

Ref Ren Riv

Nor th Ame r ica Othe r Ame r ica s Europ e a n UnionInd ust r ia l Asia Pa c ific China Ind iaRe st o f Wor ld

20 15 20 50

Energy-related CO 2 emissions per regionBillion tons

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

10

20

30

40

50

Ref Ren Riv

Industrial Residential Commercial

Transport Other

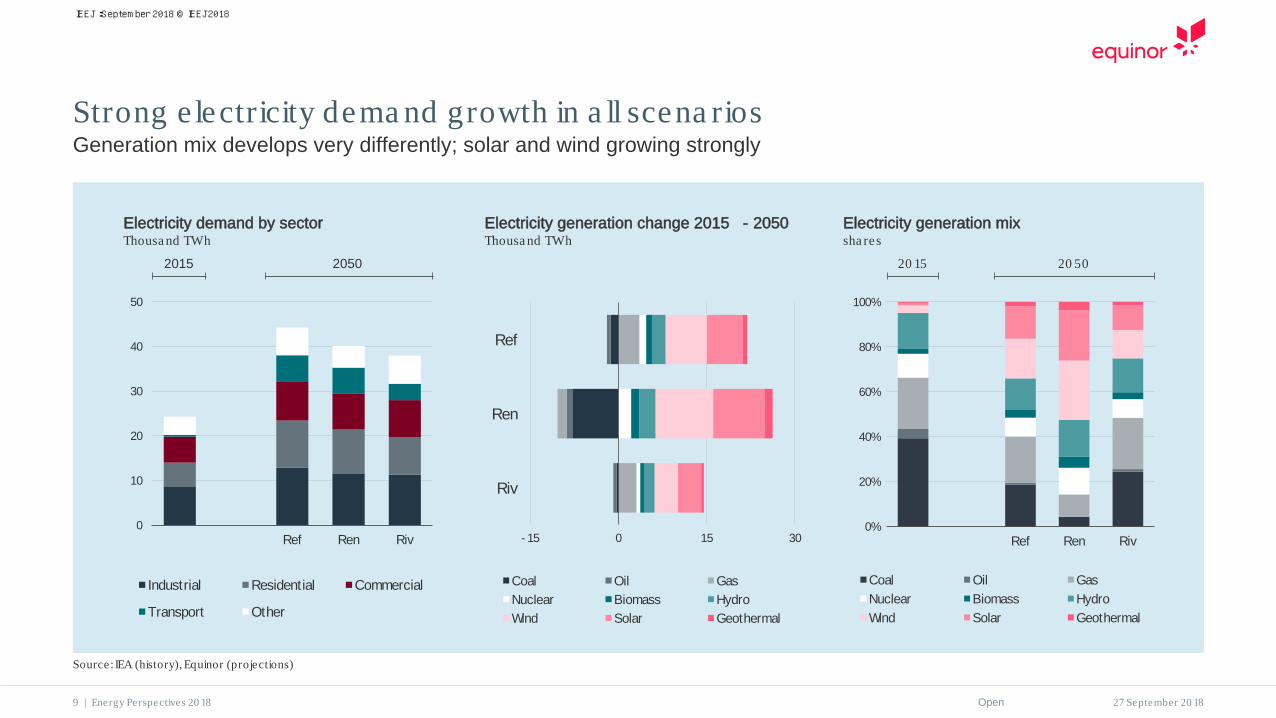

Strong e lectricity dema nd growth in a ll scena riosGeneration mix develops very differently; solar and wind growing strongly

2015 2050

Electricity demand by sectorThousa nd TWh

Electricity generation change 2015 - 2050 Thousa nd TWh

- 15 0 15 30

Riv

Ren

Ref

Coal Oil GasNuclear Biomass HydroWind Solar Geothermal

0%

20%

40%

60%

80%

100%

Ref Ren Riv

Coal Oil GasNuclear Biomass HydroWind Solar Geothermal

Electricity generation mixsha res

20 15 20 50

Source: IEA (history), Equinor (projections)

9 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0.0

0.5

1.0

1.5

2.0

2.5

Ref Ren Riv

Industrial Residential Commercial

Transport Other

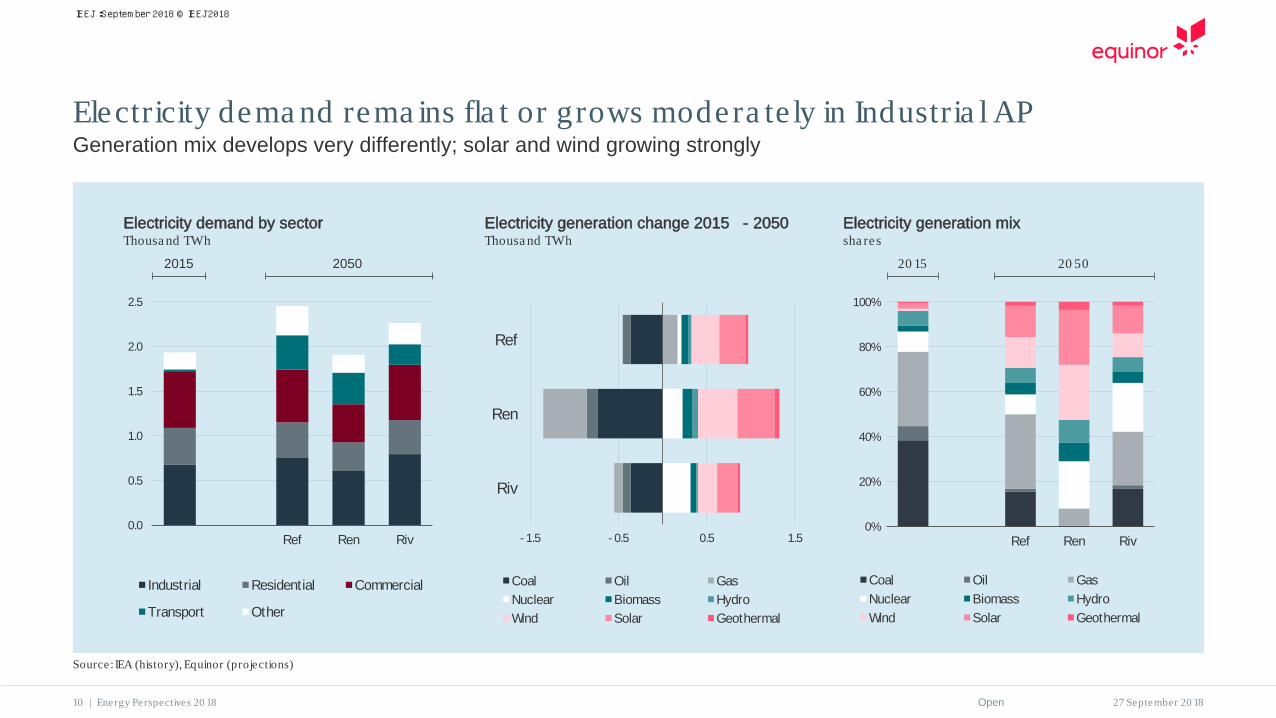

Electricity dema nd rema ins fla t or grows modera te ly in Industria l APGeneration mix develops very differently; solar and wind growing strongly

2015 2050

Electricity demand by sectorThousa nd TWh

Electricity generation change 2015 - 2050 Thousa nd TWh

0%

20%

40%

60%

80%

100%

Ref Ren Riv

Coal Oil GasNuclear Biomass HydroWind Solar Geothermal

Electricity generation mixsha res

20 15 20 50

Source: IEA (history), Equinor (projections)

10 | Energy Perspectives 20 18

- 1.5 - 0.5 0.5 1.5

Riv

Ren

Ref

Coal Oil GasNuclear Biomass HydroWind Solar Geothermal

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

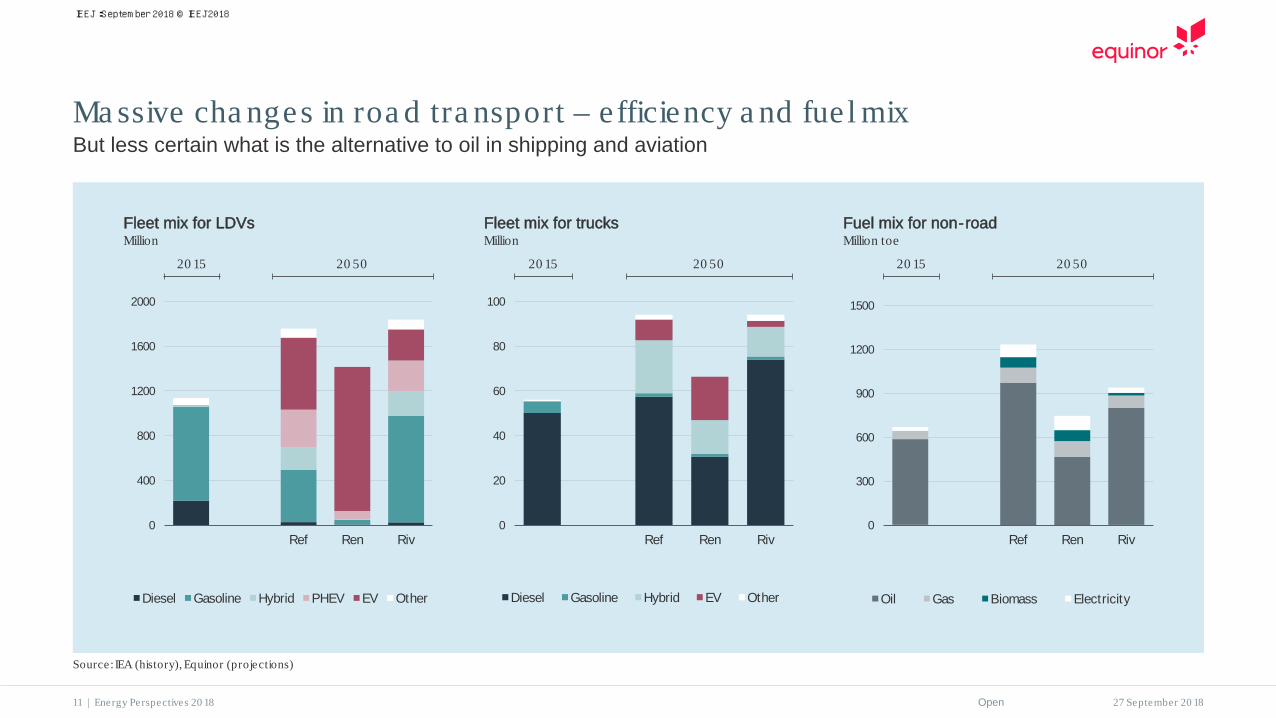

Ma ssive cha nges in roa d tra nsport – efficiency a nd fue l mixBut less certain what is the alternative to oil in shipping and aviation

Fleet mix for LDVsMillion

Fuel mix for non-roadMillion toe

Fleet mix for trucksMillion

0

400

800

1200

1600

2000

Ref Ren Riv

Diesel Gasoline Hybrid PHEV EV Other

0

20

40

60

80

100

Ref Ren Riv

Diesel Gasoline Hybrid EV Other

0

300

600

900

1200

1500

Ref Ren Riv

Oil Gas Biomass Electricity

20 15 20 50 20 15 20 50 20 15 20 50

Source: IEA (history), Equinor (projections)

11 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

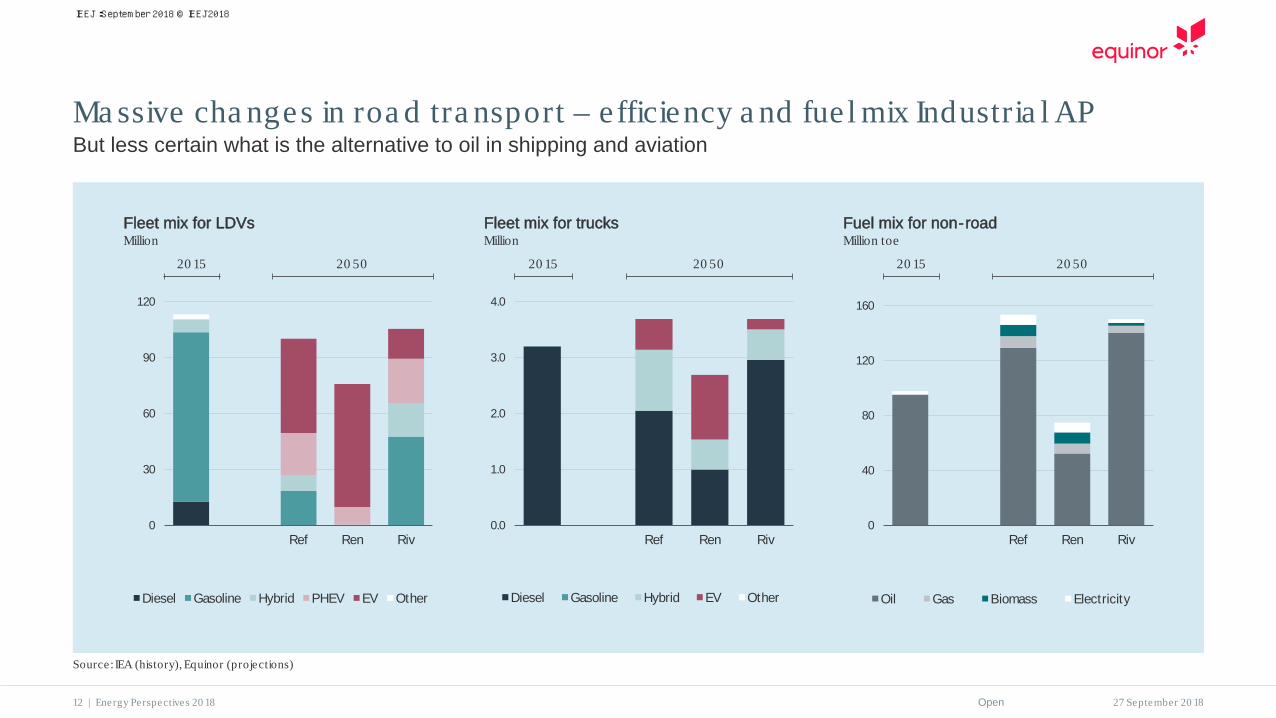

Ma ssive cha nges in roa d tra nsport – efficiency a nd fue l mix Industria l APBut less certain what is the alternative to oil in shipping and aviation

Fleet mix for LDVsMillion

Fuel mix for non-roadMillion toe

Fleet mix for trucksMillion

0

30

60

90

120

Ref Ren Riv

Diesel Gasoline Hybrid PHEV EV Other

0.0

1.0

2.0

3.0

4.0

Ref Ren Riv

Diesel Gasoline Hybrid EV Other

0

40

80

120

160

Ref Ren Riv

Oil Gas Biomass Electricity

20 15 20 50 20 15 20 50 20 15 20 50

Source: IEA (history), Equinor (projections)

12 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

300

600

900

1200

1500

Ref Ren Riv

Coal Oil Gas

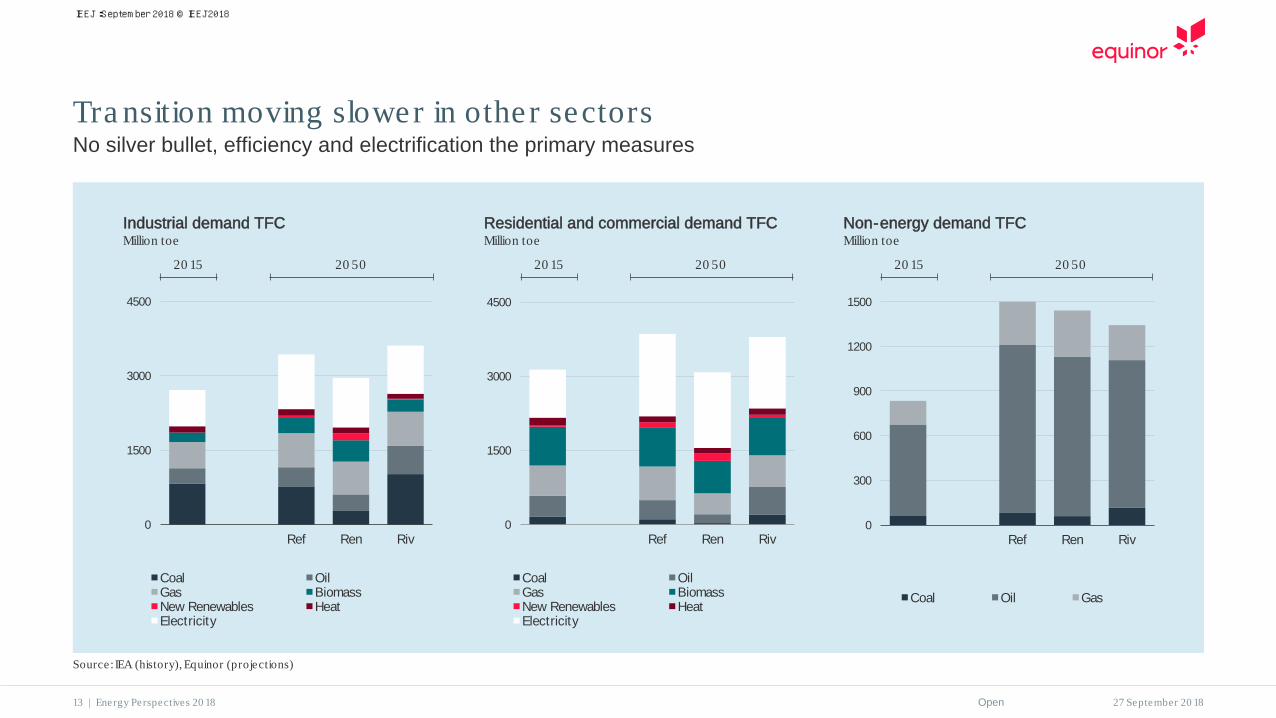

Tra nsition moving slower in other sectorsNo silver bullet, efficiency and electrification the primary measures

0

1500

3000

4500

Ref Ren Riv

Coal OilGas BiomassNew Renewables HeatElectricity

0

1500

3000

4500

Ref Ren Riv

Coal OilGas BiomassNew Renewables HeatElectricity

Industrial demand TFCMillion toe

Non-energy demand TFCMillion toe

Residential and commercial demand TFCMillion toe

20 15 20 50 20 15 20 5020 15 20 50

Source: IEA (history), Equinor (projections)

13 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

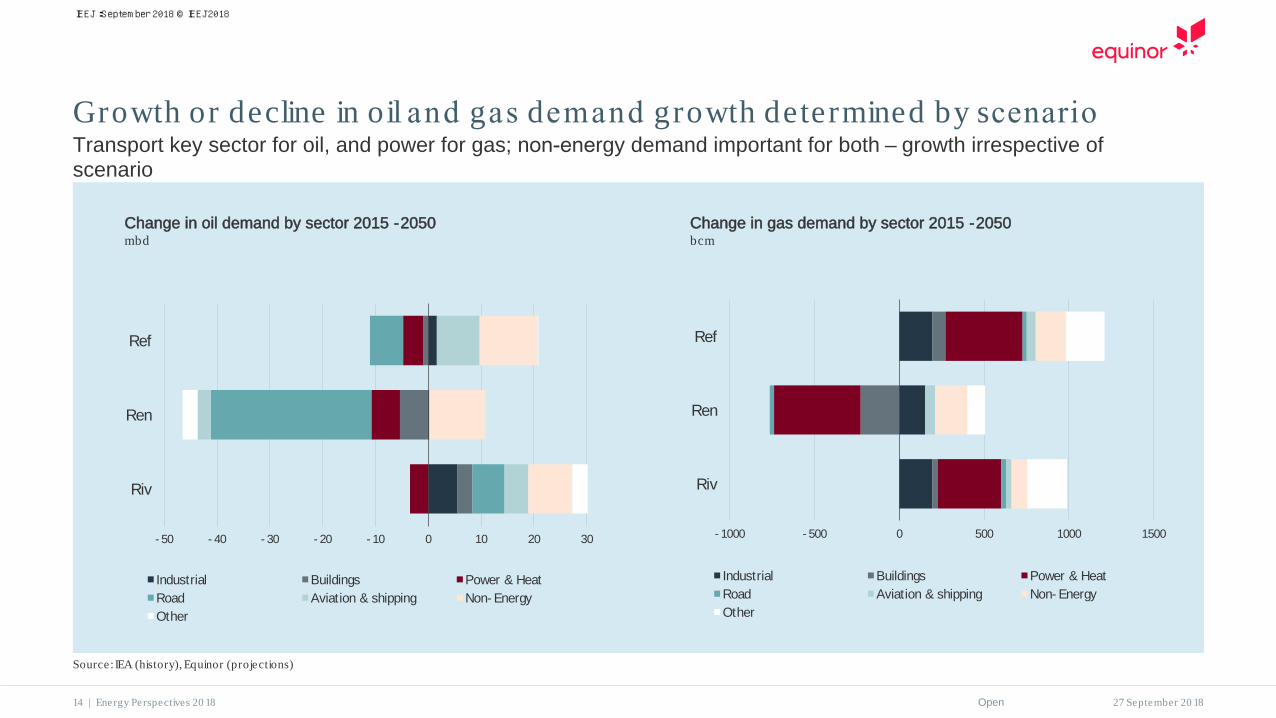

Growth or decline in oil and gas demand growth determined by scenarioTransport key sector for oil, and power for gas; non-energy demand important for both – growth irrespective of scenario

Change in oil demand by sector 2015 -2050mbd

Change in gas demand by sector 2015 -2050bcm

- 50 - 40 - 30 - 20 - 10 0 10 20 30

Riv

Ren

Ref

Industrial Buildings Power & HeatRoad Aviation & shipping Non- EnergyOther

- 1000 - 500 0 500 1000 1500

Riv

Ren

Ref

Industrial Buildings Power & HeatRoad Aviation & shipping Non- EnergyOther

Source: IEA (history), Equinor (projections)

14 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

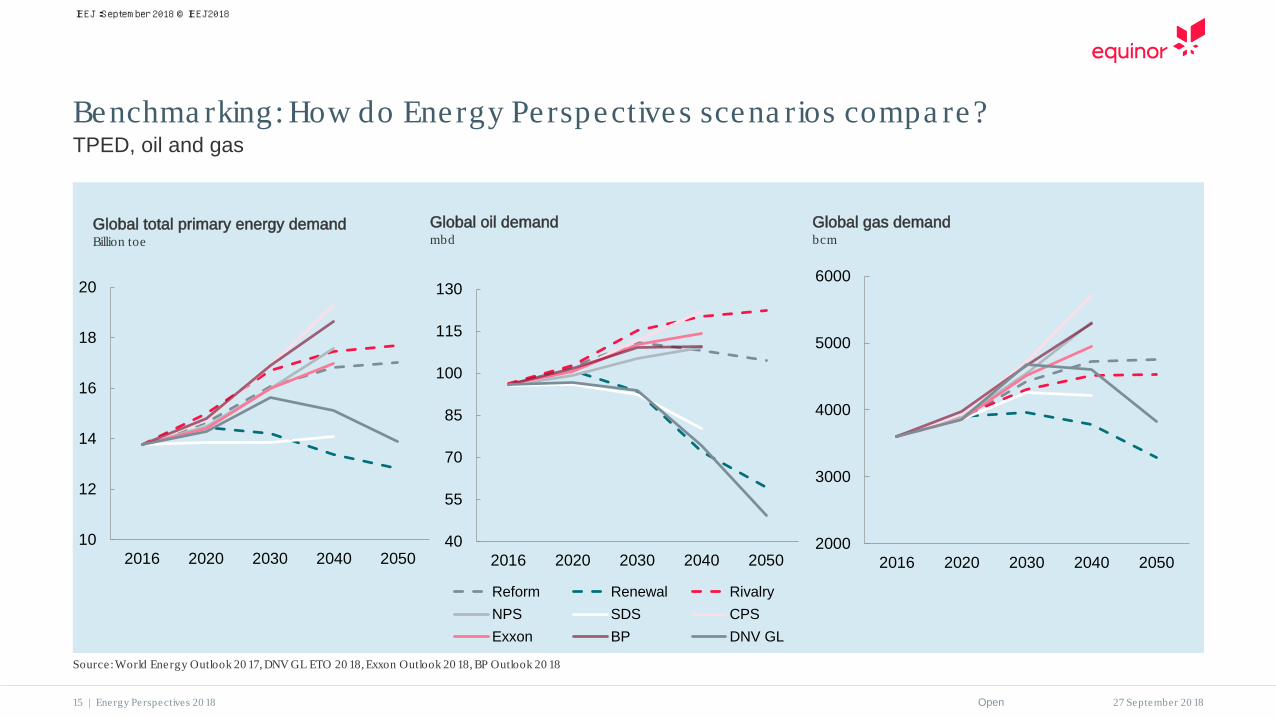

Benchma rking: How do Energy Perspectives scena rios compa re?TPED, oil and gas

Global total primary energy demandBillion toe

15 | Energy Perspectives 20 18

Global oil demandmbd

Global gas demandbcm

Source: World Energy Outlook 20 17, DNV GL ETO 20 18, Exxon Outlook 20 18, BP Outlook 20 18

10

12

14

16

18

20

2016 2020 2030 2040 205040

55

70

85

100

115

130

2016 2020 2030 2040 2050

Reform Renewal RivalryNPS SDS CPSExxon BP DNV GL

2000

3000

4000

5000

6000

2016 2020 2030 2040 2050

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

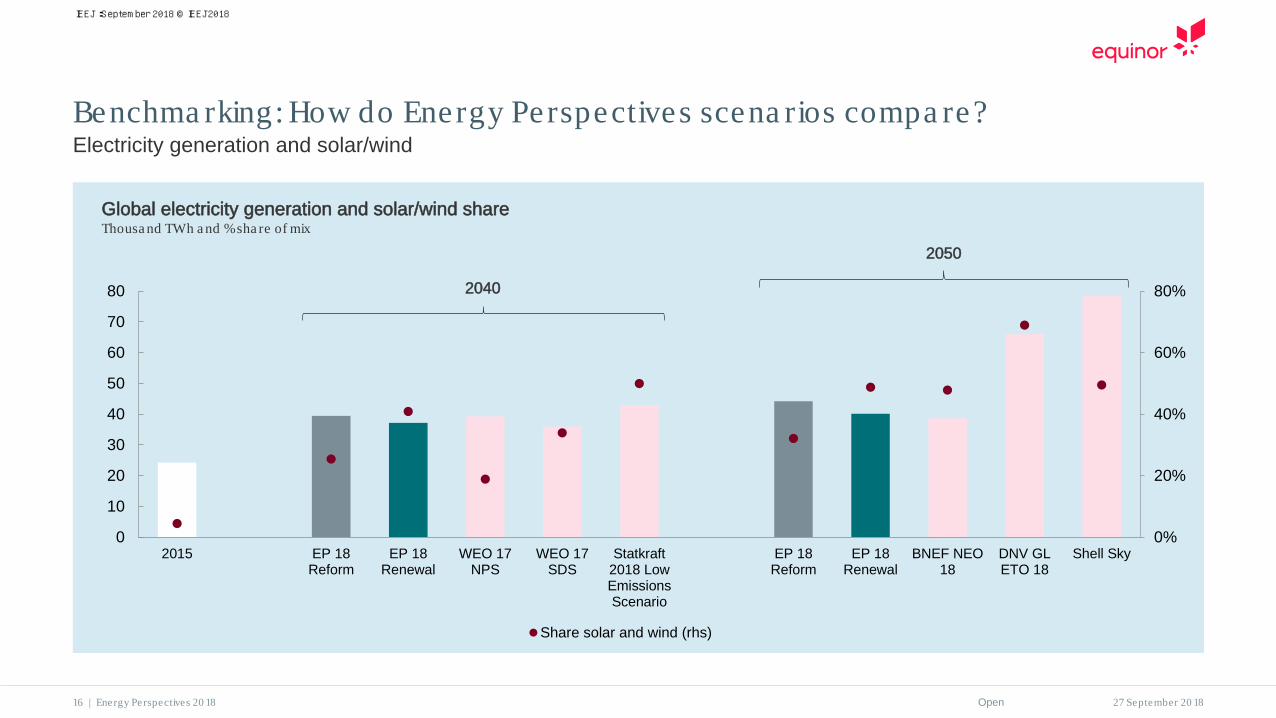

Benchma rking: How do Energy Perspectives scena rios compa re?Electricity generation and solar/wind

Global electricity generation and solar/wind shareThousa nd TWh a nd % sha re of mix

16 | Energy Perspectives 20 18

2040

2050

0%

20%

40%

60%

80%

0

10

20

30

40

50

60

70

80

2015 EP 18Reform

EP 18Renewal

WEO 17NPS

WEO 17SDS

Statkraft2018 LowEmissionsScenario

EP 18Reform

EP 18Renewal

BNEF NEO18

DNV GLETO 18

Shell Sky

Share solar and wind (rhs)

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

200

400

600

800

1000

USA Opec

Rivalry add- onReform add- onRenewal add- onPotential legacy supply

Dema nd ra nge

Decline ra nge

Lega cy supply0

25

50

75

100

125

2015

2020

2030

2040

2050

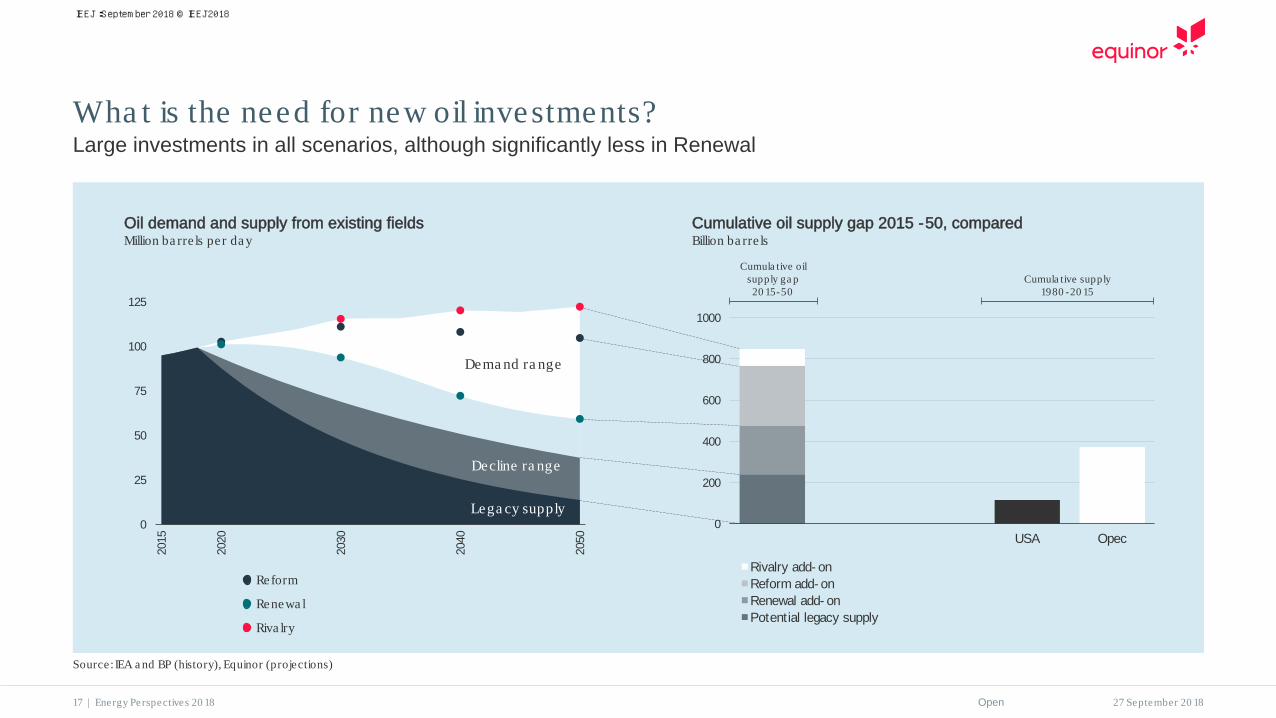

Wha t is the need for new oil investments?Large investments in all scenarios, although significantly less in Renewal

Oil demand and supply from existing fieldsMillion ba rre ls per da y

Cumulative oil supply gap 2015 -50, compared Billion ba rre ls

Cumula tive oilsupply ga p20 15-50

Cumula tive supply1980 -20 15

Source: IEA a nd BP (history), Equinor (projections)

17 | Energy Perspectives 20 18

Reform

Renewa l

Riva lry

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

Dema nd ra nge

Decline ra nge

Lega cy supply0

1000

2000

3000

4000

5000

2015

2020

2030

2040

2050

0

20

40

60

80

100

USA Russia Middle East

Reform add- onRivalry add- onRenewal add- onPotential legacy supply

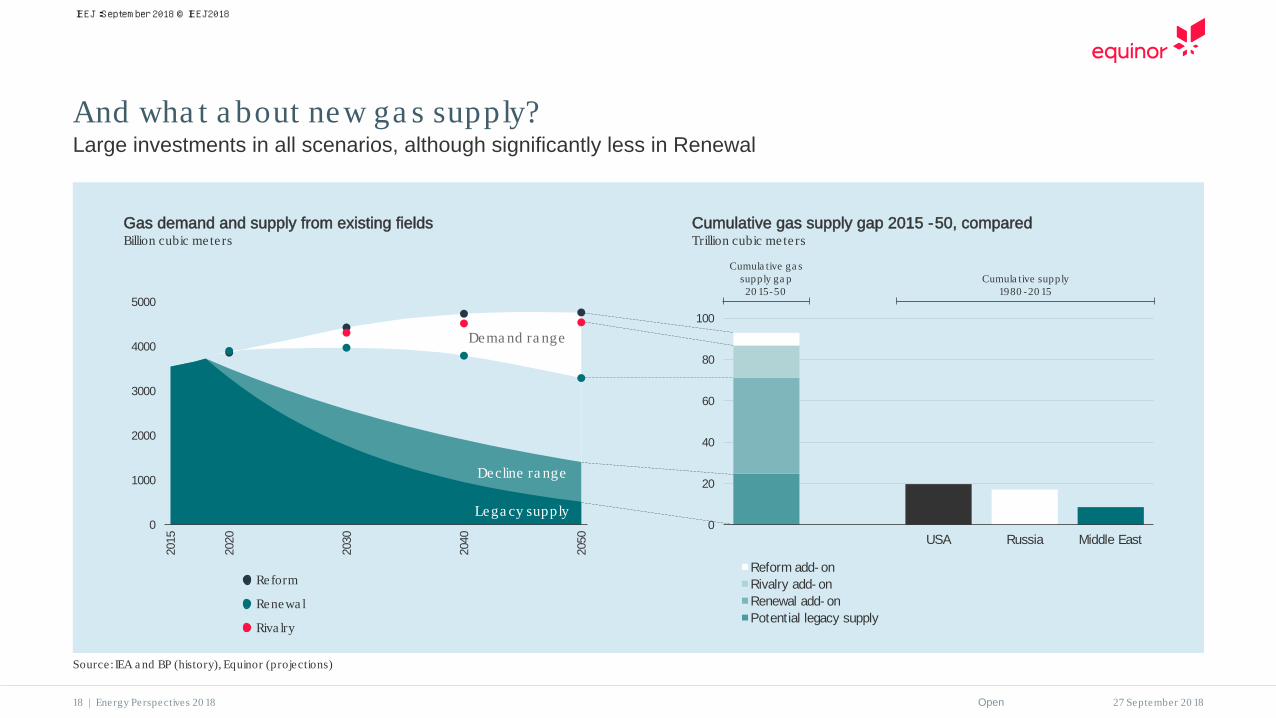

And wha t a bout new ga s supply?Large investments in all scenarios, although significantly less in Renewal

Gas demand and supply from existing fields Billion cubic meters

Cumulative gas supply gap 2015 -50, compared Trillion cubic meters

Cumula tive ga s supply ga p 20 15-50

Cumula tive supply1980 -20 15

Source: IEA a nd BP (history), Equinor (projections)

18 | Energy Perspectives 20 18

Reform

Renewa l

Riva lry

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

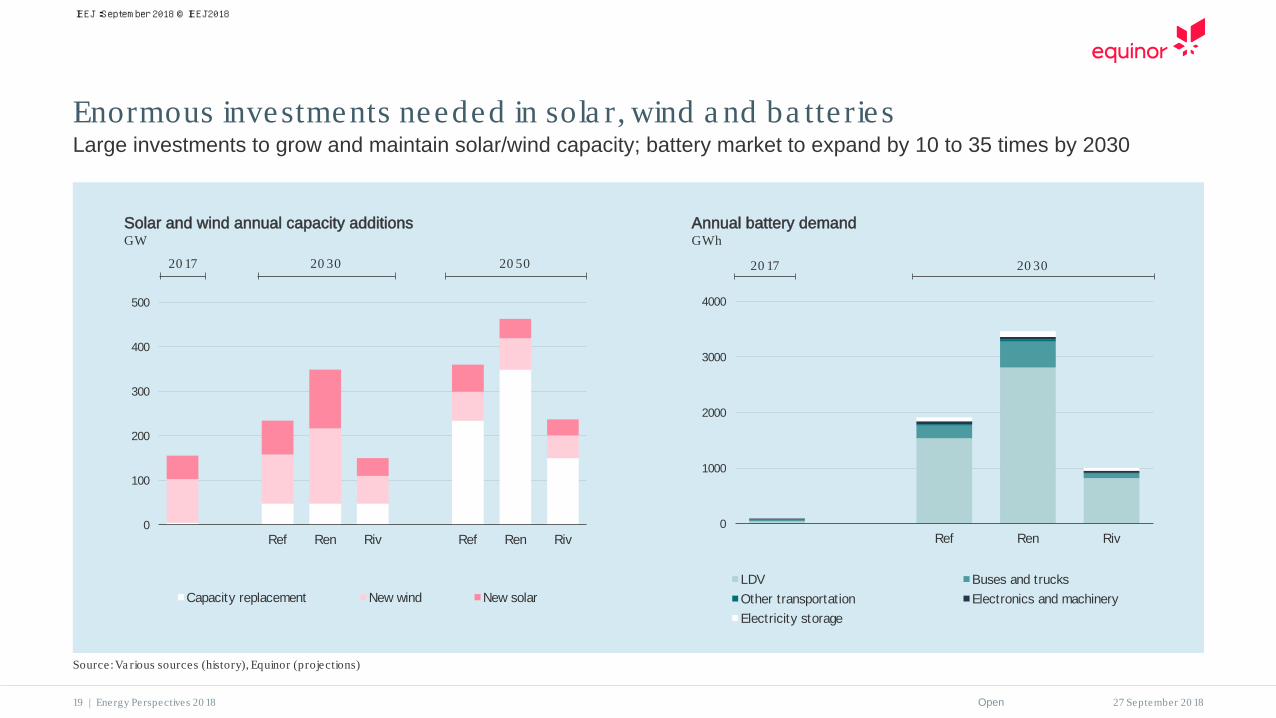

Enormous investments needed in sola r, wind a nd ba tte riesLarge investments to grow and maintain solar/wind capacity; battery market to expand by 10 to 35 times by 2030

Solar and wind annual capacity additionsGW

Annual battery demandGWh

0

100

200

300

400

500

Ref Ren Riv Ref Ren Riv

Capacity replacement New wind New solar

20 17 20 30 20 50

0

1000

2000

3000

4000

Ref Ren Riv

LDV Buses and trucksOther transportation Electronics and machineryElectricity storage

20 17 20 30

Source: Va rious sources (history), Equinor (projections)

19 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

© Equinor ASAThis presentation, including the contents and arrangement of the contents of each individual page or the collection of the pages, is owned by Equinor. Copyright to a ll ma teria l including, but not limited to, written ma teria l, photogra phs, dra wings, ima ges, ta bles a nd da ta rema ins the property of Equinor. All rights reserved. Any other use , reproduction, tra nsla tion, a da ption, a rra ngement, a lte ra tion, distribution or stora ge of this presenta tion, in whole or in pa rt, without the prior written permission of Equinor is prohibited. The informa tion conta ined in this presenta tion ma y not be a ccura te , up to da te or a pplica ble to the circumsta nces of a ny pa rticula r ca se , despite our e fforts. Equinor ca nnot a ccept a ny lia bility for a ny ina ccura cies or omissions.

Eirik Wæ rnessSenior vice president a nd Chief economist

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

30

60

90

120

Ref Ren Riv

Coal Oil Gas

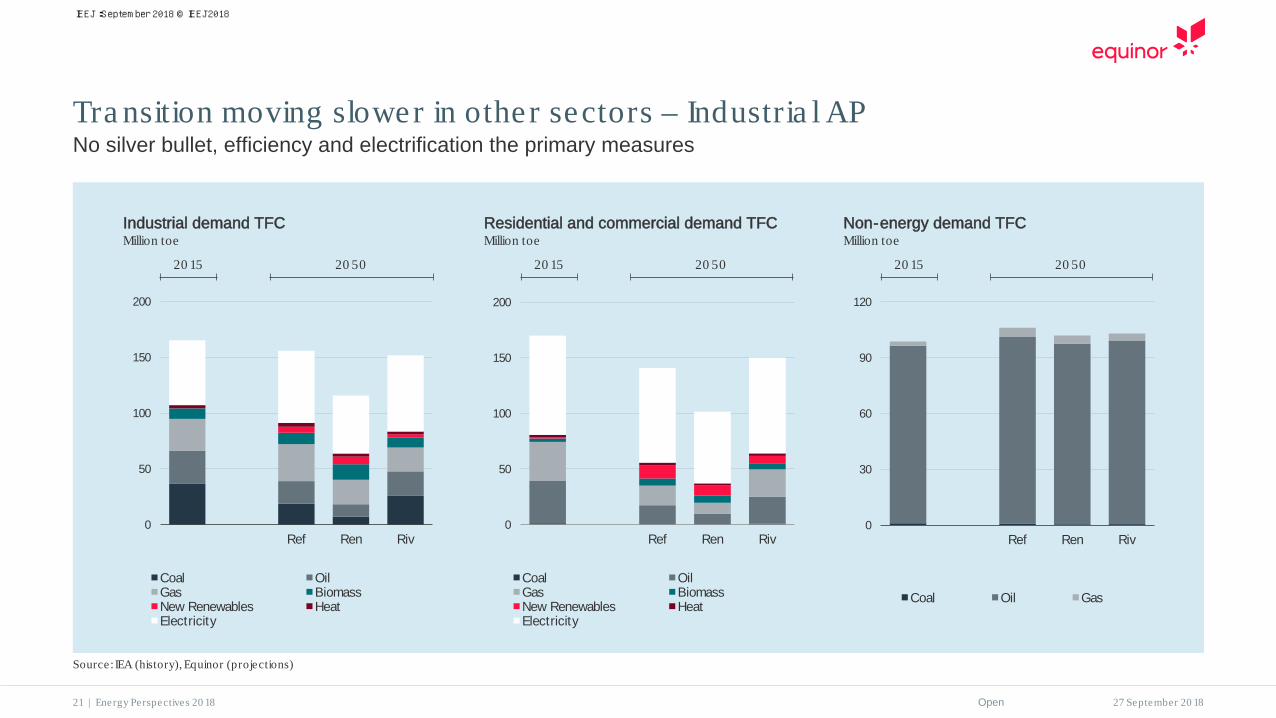

Tra nsition moving slower in other sectors – Industria l APNo silver bullet, efficiency and electrification the primary measures

0

50

100

150

200

Ref Ren Riv

Coal OilGas BiomassNew Renewables HeatElectricity

0

50

100

150

200

Ref Ren Riv

Coal OilGas BiomassNew Renewables HeatElectricity

Industrial demand TFCMillion toe

Non-energy demand TFCMillion toe

Residential and commercial demand TFCMillion toe

20 15 20 50 20 15 20 5020 15 20 50

Source: IEA (history), Equinor (projections)

21 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

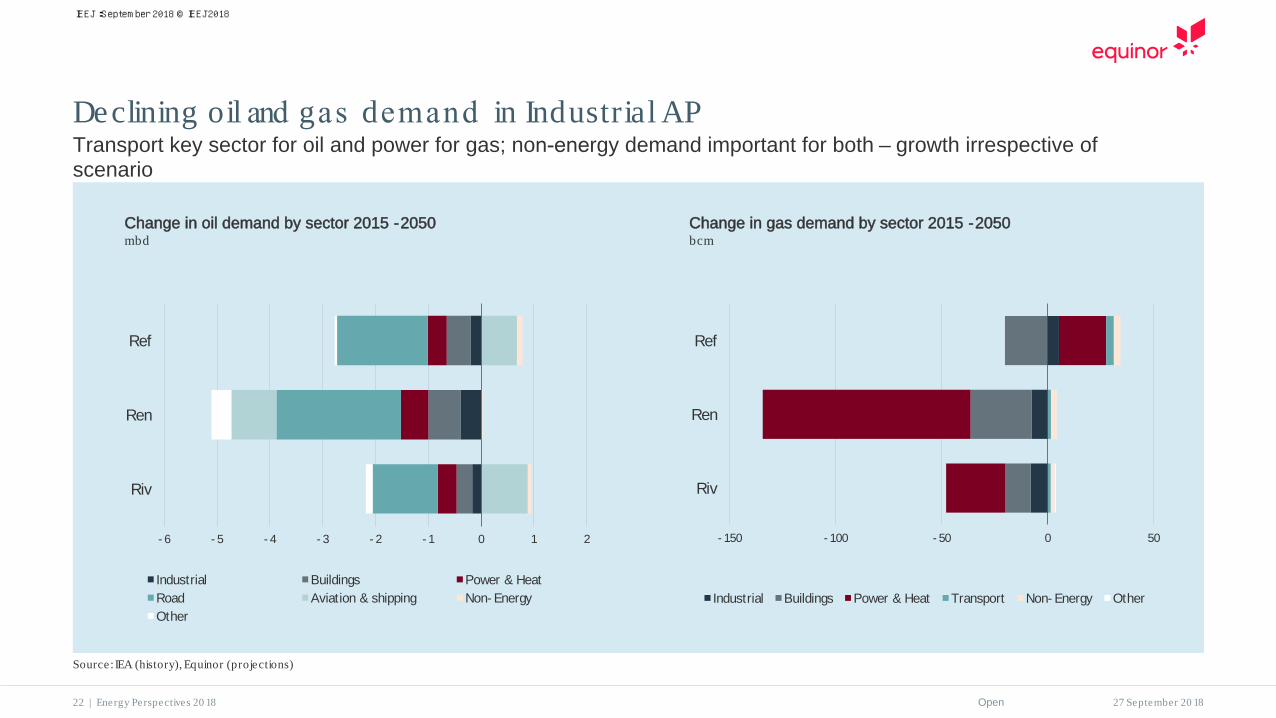

Declining oil and gas demand in Industria l APTransport key sector for oil and power for gas; non-energy demand important for both – growth irrespective of scenario

Change in oil demand by sector 2015 -2050mbd

- 6 - 5 - 4 - 3 - 2 - 1 0 1 2

Riv

Ren

Ref

Industrial Buildings Power & HeatRoad Aviation & shipping Non- EnergyOther

- 150 - 100 - 50 0 50

Riv

Ren

Ref

Industrial Buildings Power & Heat Transport Non- Energy Other

Source: IEA (history), Equinor (projections)

22 | Energy Perspectives 20 18

Change in gas demand by sector 2015 -2050bcm

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

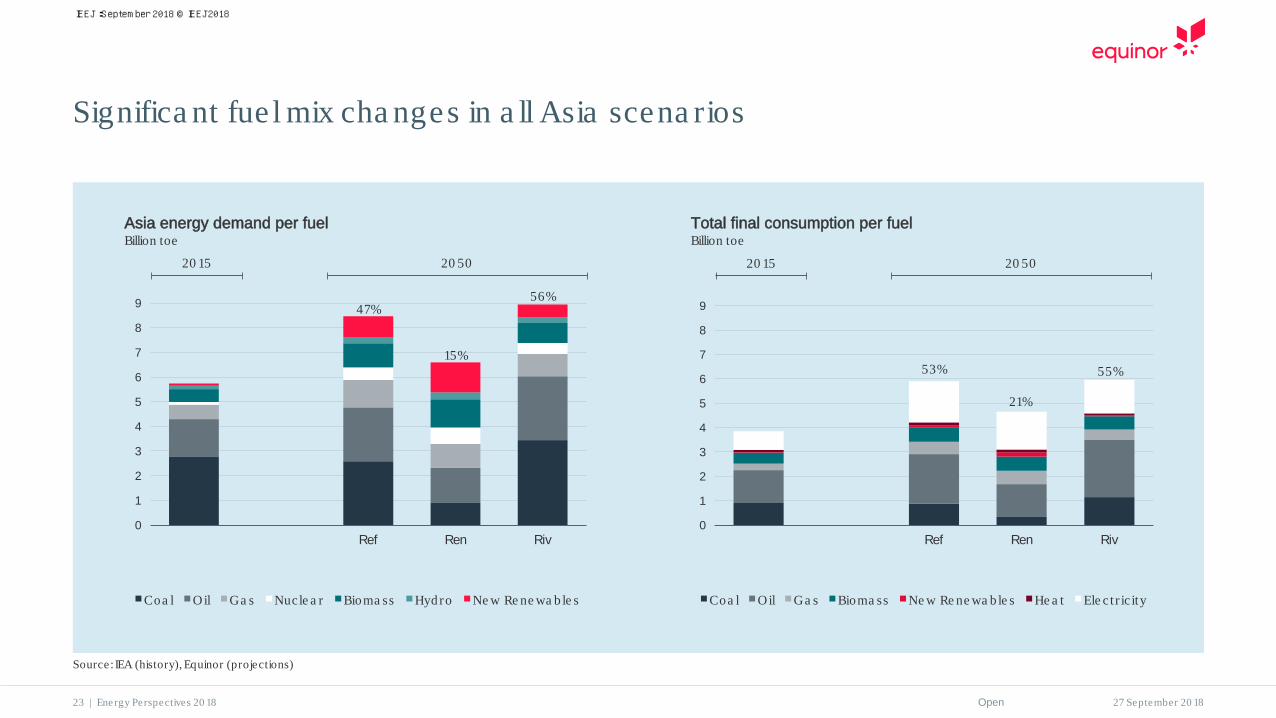

Significa nt fue l mix cha nges in a ll Asia scena rios

Source: IEA (history), Equinor (projections)

23 | Energy Perspectives 20 18

47%

15%

56%

0

1

2

3

4

5

6

7

8

9

Ref Ren Riv

Coa l Oil Ga s Nucle a r Bioma ss Hyd ro Ne w Re ne wa b le s

20 15 20 50

Asia energy demand per fuelBillion toe

53%

21%

55%

0

1

2

3

4

5

6

7

8

9

Ref Ren Riv

Coa l Oil Ga s Bioma ss Ne w Re ne wa b le s He a t Ele c t r ic ity

20 15 20 50

Total final consumption per fuelBillion toe

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

5

10

15

20

25

Ref Ren Riv

Industrial Residential Commercial

Transport Other

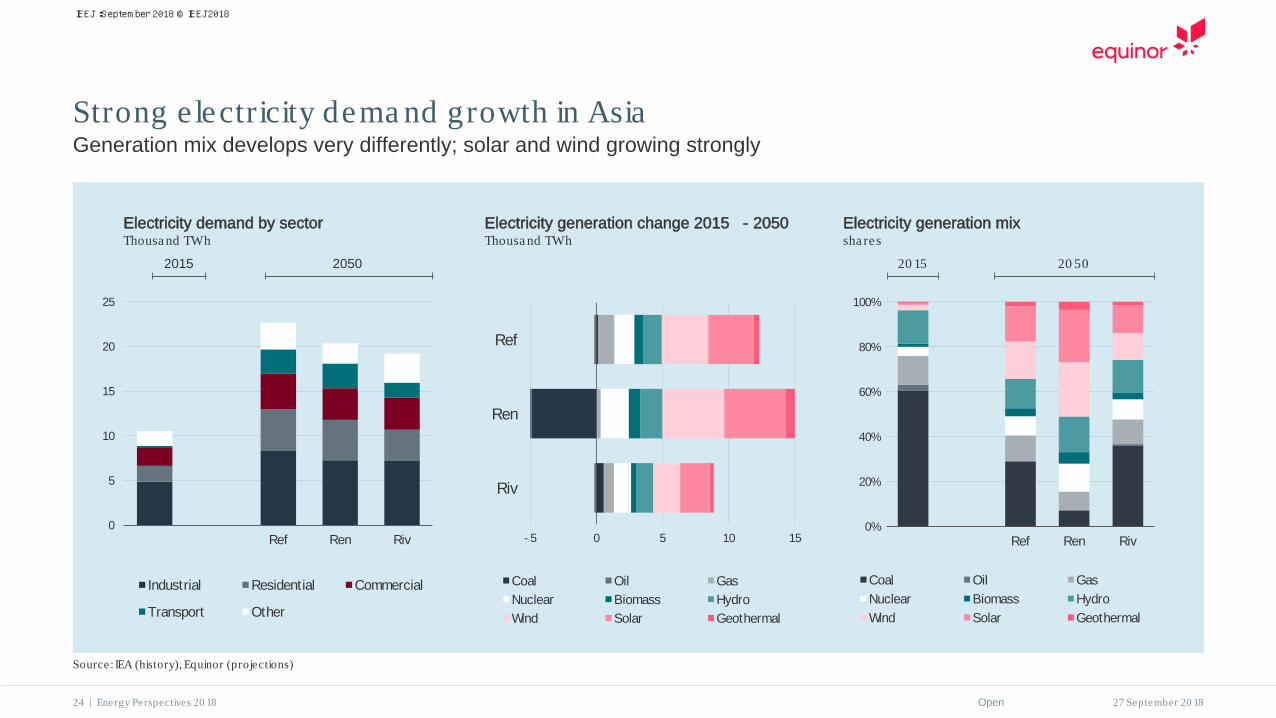

Strong e lectricity dema nd growth in AsiaGeneration mix develops very differently; solar and wind growing strongly

2015 2050

Electricity demand by sectorThousa nd TWh

Electricity generation change 2015 - 2050 Thousa nd TWh

0%

20%

40%

60%

80%

100%

Ref Ren Riv

Coal Oil GasNuclear Biomass HydroWind Solar Geothermal

Electricity generation mixsha res

20 15 20 50

Source: IEA (history), Equinor (projections)

24 | Energy Perspectives 20 18

- 5 0 5 10 15

Riv

Ren

Ref

Coal Oil GasNuclear Biomass HydroWind Solar Geothermal

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

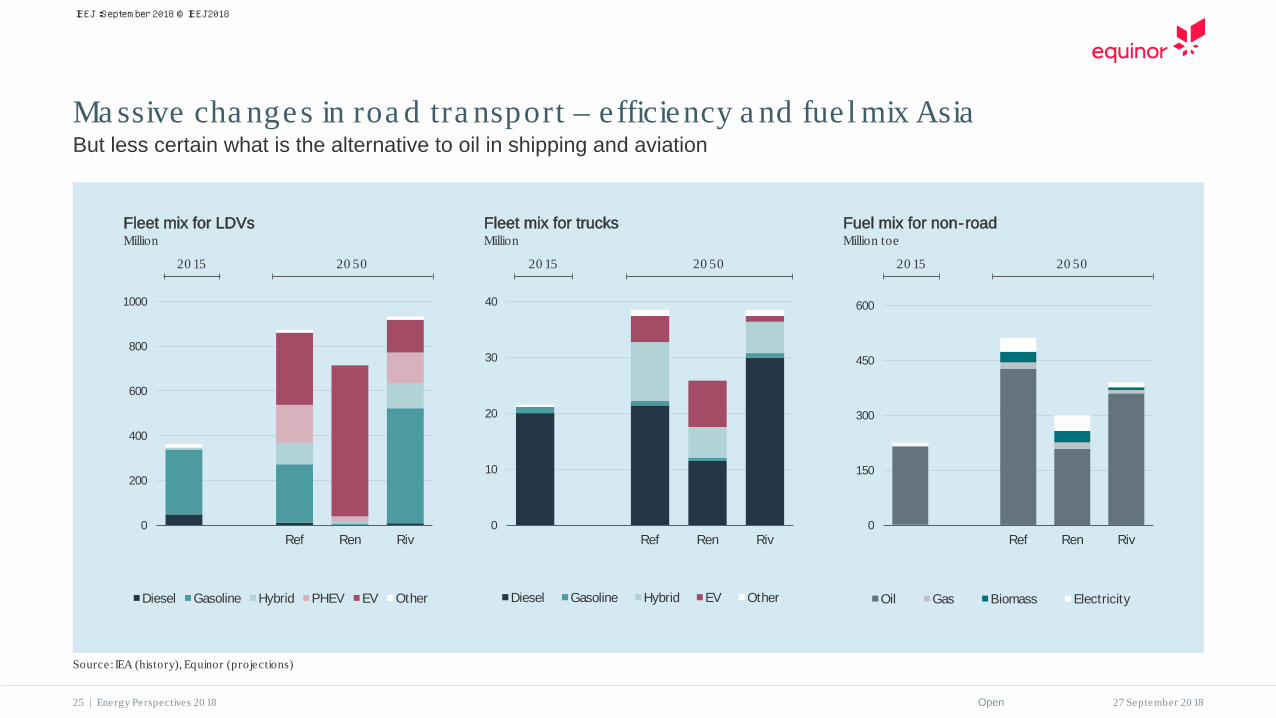

Ma ssive cha nges in roa d tra nsport – efficiency a nd fue l mix AsiaBut less certain what is the alternative to oil in shipping and aviation

Fleet mix for LDVsMillion

Fuel mix for non-roadMillion toe

Fleet mix for trucksMillion

0

200

400

600

800

1000

Ref Ren Riv

Diesel Gasoline Hybrid PHEV EV Other

0

10

20

30

40

Ref Ren Riv

Diesel Gasoline Hybrid EV Other

0

150

300

450

600

Ref Ren Riv

Oil Gas Biomass Electricity

20 15 20 50 20 15 20 50 20 15 20 50

Source: IEA (history), Equinor (projections)

25 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

0

200

400

600

800

Ref Ren Riv

Coal Oil Gas

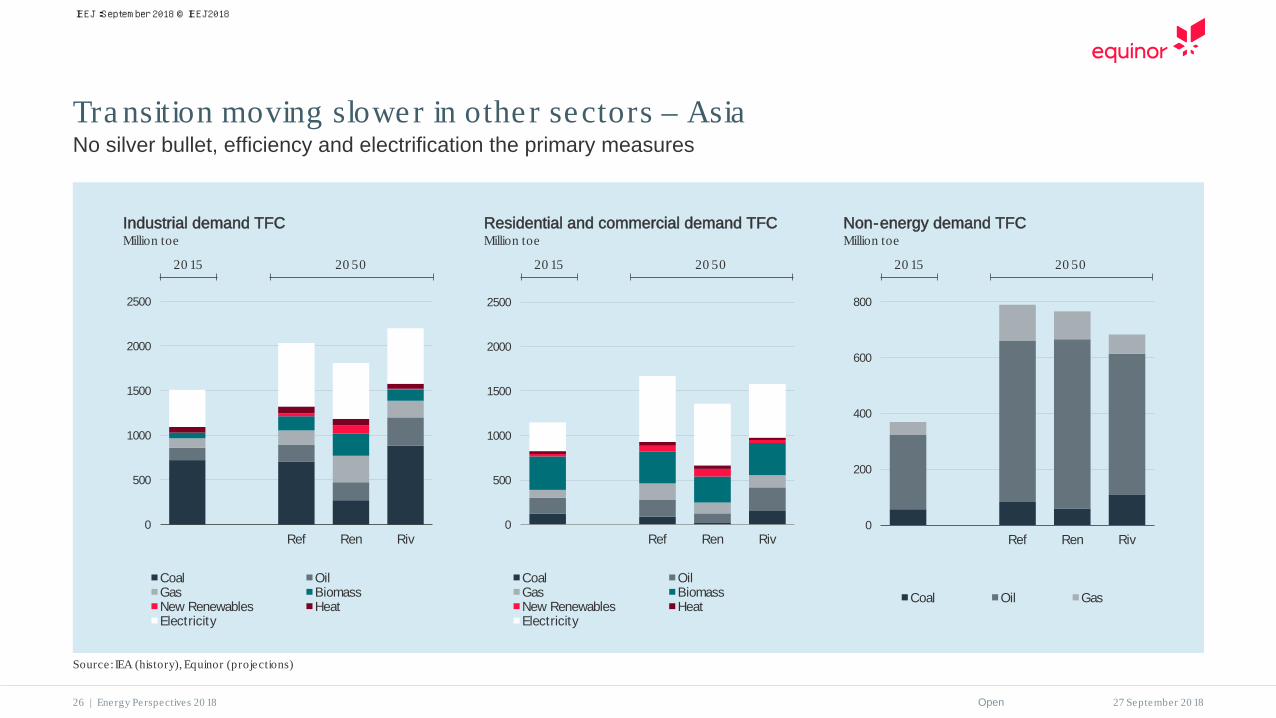

Tra nsition moving slower in other sectors – AsiaNo silver bullet, efficiency and electrification the primary measures

0

500

1000

1500

2000

2500

Ref Ren Riv

Coal OilGas BiomassNew Renewables HeatElectricity

0

500

1000

1500

2000

2500

Ref Ren Riv

Coal OilGas BiomassNew Renewables HeatElectricity

Industrial demand TFCMillion toe

Non-energy demand TFCMillion toe

Residential and commercial demand TFCMillion toe

20 15 20 50 20 15 20 5020 15 20 50

Source: IEA (history), Equinor (projections)

26 | Energy Perspectives 20 18

IEEJ:September 2018 © IEEJ2018

Open 27 September 20 18

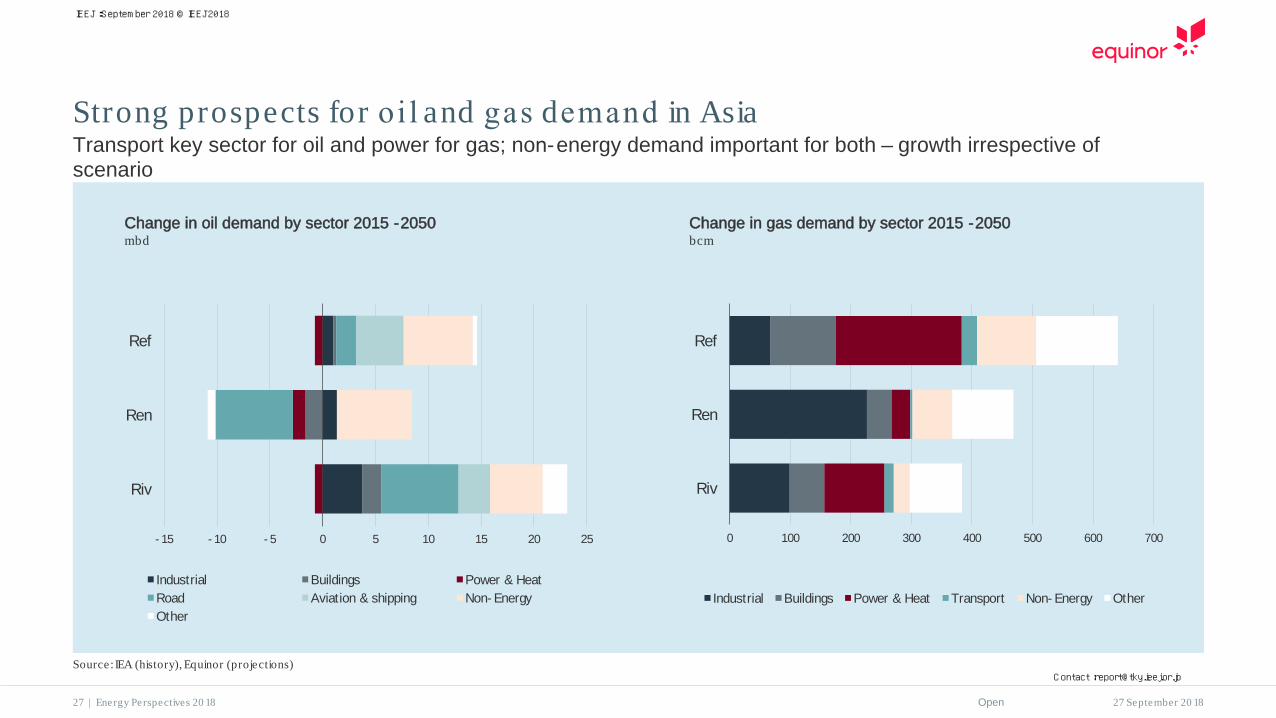

Strong prospects for oil and gas demand in AsiaTransport key sector for oil and power for gas; non-energy demand important for both – growth irrespective of scenario

Change in oil demand by sector 2015 -2050mbd

- 15 - 10 - 5 0 5 10 15 20 25

Riv

Ren

Ref

Industrial Buildings Power & HeatRoad Aviation & shipping Non- EnergyOther

0 100 200 300 400 500 600 700

Riv

Ren

Ref

Industrial Buildings Power & Heat Transport Non- Energy Other

Source: IEA (history), Equinor (projections)

27 | Energy Perspectives 20 18

Change in gas demand by sector 2015 -2050bcm

IEEJ:September 2018 © IEEJ2018

Contact :[email protected]

![Min.era] urces of t'he Plain »and East Cact s Plain Wild rness … · 2011-12-08 · 6. Aeromagnetic anomaly map of Cactus Plain and East Cactus Plain Wilderness Study Areas, La](https://img.pdfslide.us/doc/110x75/5f1175291bc649787879dfc3/minera-urces-of-the-plain-and-east-cact-s-plain-wild-rness-2011-12-08-6.jpg)