Embed Size (px)

Citation preview

RTI International is a trade name of Research Triangle Institute www.rti.org

Long-Term Care in Hawaii: Issues and Options

Joshua M. Wiener, Ph.D. RTI International Washington, DC

www.rti.org 1/15/14

2

RTI International Project for LTCC: First Year

• Review of available published information • Survey of adult population on long-term care issues • Conduct stakeholder interviews: Government

officials, providers, consumers, researchers • Develop options for Commission decisionmaking

www.rti.org 1/15/14

3

Introduction

• Long-term care major component of health spending • Major component of state health and Medicaid

spending • Heavily publicly financed through Medicaid and

Medicare • Aging of the population = higher expenditures • How should long-term care be organized? • How should long-term care be financed?

www.rti.org 1/15/14

4

Goals of Long-Term Care Reform

• Treat long-term care as a normal life risk rather than unexpected event

• Protect against catastrophic out-of-pocket costs • Prevent dependence on welfare • Increase consumer choice by providing more options

for home and community-based services while providing needed institutional care

• Finance care in a way that is affordable for individuals and government

www.rti.org 1/15/14

5

SERVICE DELIVERY

www.rti.org 1/15/14

6

Nursing Home Residents per 1000 People Aged 75 and Older

0102030405060708090

100

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Year

Nursing Home Residents per 1000

75+

United States Hawaii

www.rti.org 1/15/14

7

Average Nursing Home ADL Index

0

2

4

6

8

10

2008

ADL Group Index

Score

United States Hawaii

www.rti.org 1/15/14

8

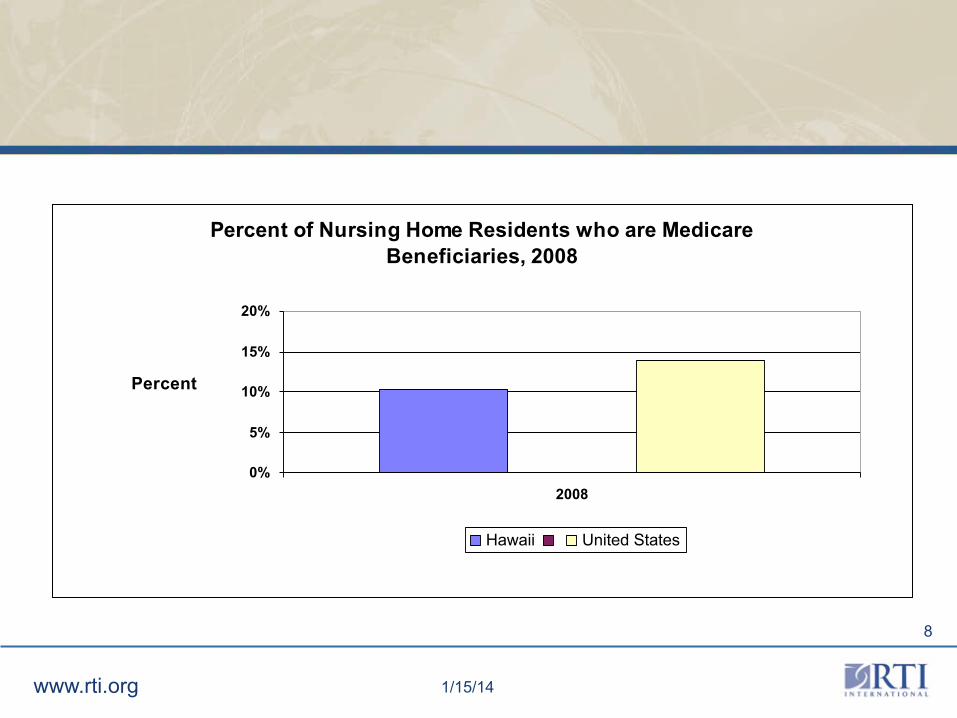

Percent of Nursing Home Residents who are Medicare Beneficiaries, 2008

0%

5%

10%

15%

20%

2008

Percent

Hawaii United States

www.rti.org 1/15/14

9

Assisted Living & Residential Care Beds per 1000 Persons 75+

0

10

20

30

40

50

60

2009

Population data is for 2008

Assisted Living and Residential Care Beds

per 1000 75+

Hawaii United States

www.rti.org 1/15/14

10

Delivery System Reform

• States implementing LTC reform have focused on delivery rather than financing

• Three main critiques: – Not enough home and community-based services;

too much emphasis on institutional care – Fragmented delivery system makes entry,

coordination, and transition difficult – Consumers do not have enough control over the

services they use

www.rti.org 1/15/14

11

Medicaid and State HCBS Expendituresper 1000 People 75+, 2007

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

2007

Expenditures

Hawaii United States

www.rti.org 1/15/14

12

Medicaid HCBS Expenditures per 1,000 People Aged 75 or Older

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Medicaid HCBS Expenditures per

1,000 People Aged 75+

United-States Hawaii

www.rti.org 1/15/14

13

Percentage of Medicaid LTC Expenditures for HCBS 2008

0%

10%

20%

30%

40%

2008

Percentage

Hawaii United States

www.rti.org 1/15/14

14

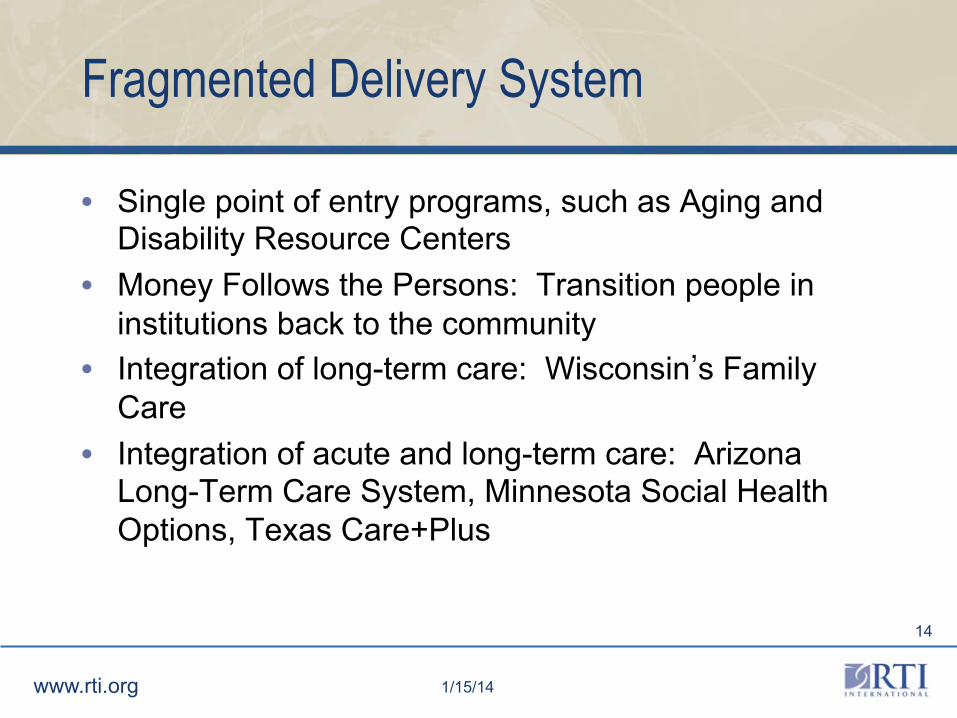

Fragmented Delivery System

• Single point of entry programs, such as Aging and Disability Resource Centers

• Money Follows the Persons: Transition people in institutions back to the community

• Integration of long-term care: Wisconsin’s Family Care

• Integration of acute and long-term care: Arizona Long-Term Care System, Minnesota Social Health Options, Texas Care+Plus

www.rti.org 1/15/14

15

Average Medicare Spending per Enrollee Age 65 and Older, by Functional Limitations, 2005

SOURCE: Komisar, Tumlinson, Feder & Burke. Long-‐Term Care in Health Care Reform: Policy OpGons to Improve Both. The SCAN FoundaGon. 2009.

Note: ADLs = acGviGes of daily living. Amounts shown are spending for Medicare Parts A and B only, for enrollees in fee-‐for-‐service Medicare who are not residing in nursing homes or other insGtuGons.

Percent of enrollees: 86% 14% 7%

www.rti.org 1/15/14

16

Consumer-Directed Home Care

• Most home care provided by agencies, which hire, train, schedule, monitor, and fire employees

• Consumer-directed home care give those responsibilities to consumers or their agents

• Promoted by Centers for Medicare & Medicaid Services, a growing number of states are using this approach

• Studies find quality the same or better as agency-directed services

www.rti.org 1/15/14

17

FINANCING

www.rti.org 1/15/14

18

Long-Term Care is Expensive

Type of Care Hawaii United States

Year in nursing home care (private room)

$131,400 $79,935

Year in assisted living facility

$54,900 $37,572

Home health aide (per hour)

$23 $21

www.rti.org 1/15/14

19

Nursing Facility Resident Payer Sources, 2009

Source of Payment

Hawaii United States

Medicare 11 14

Medicaid

70 64

Other Payer 19 22

Total 100 100

www.rti.org 1/15/14

20

Medicaid LTC Expenditures per 1,000 People Aged 75 or Older

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

2008

Medicaid LTC Expenditures

per 1,000 People Aged 75+

United-States Hawaii

www.rti.org 1/15/14

21

Public and Private Expenditures on LTC for Older People as Percentage of GDP, 2000

Source: OECD, 2005.

21

www.rti.org 1/15/14

22 22

Projected Public Long-Term Care Expenditures (All Ages) in Selected Countries, as a Percentage of GDP, 2005 and 2050

Source: OECD, 2006.

0

0.5

1

1.5

2

2.5

3

3.5

Germany Japan United Kingdom United States

2005

2050 (Low)

2050 (High)

www.rti.org 1/15/14

23

Means Testing vs. Universal Financing

• Unlike health care, many countries means test (e.g., United Kingdom, New Zealand)

• Countries with universal coverage (Austria, Germany, Japan, Netherlands, Sweden, Luxembourg)

• Private insurance not a major source of financing • Public and private insurance sometimes blurred (e.g.,

Germany)

www.rti.org 1/15/14

24

Private Sector Initiatives: Private Long-Term Care Insurance PROS • Consistent with current health insurance system for

most people (but not older people) • Reflects general principle of personal responsibility • Allows for competition CONS • Market has not taken off and proposals to jump start

market unlikely to work on broad basis • Products are too expensive for most people • People who have medical problems cannot enroll

www.rti.org 1/15/14

25

Private Long-Term Care Insurance

• “The Dream” • Affordability:

– Good quality policy: $2,300 at age 60 – 10-20 percent can afford

• Thinks Medicare covers it • Denial of risk • Medical underwriting

www.rti.org 1/15/14

26

Options to Encourage Private Long-Term Care Insurance

• Tax incentives • Partnership for LTC • Employer-sponsored LTC insurance

www.rti.org 1/15/14

27

Tax Incentives for Private Long-Term Care Insurance

• Income tax deductions or credits • HIPAA and 36 states and DC offer tax incentives • Incentives are small, not substantially reducing price • Sentinel effect? • Only about 40% of federal taxpayers itemize and

many older people pay no federal taxes • Recent study by Stevenson find little effect • Efficiency vs. equity

www.rti.org 1/15/14

28

Public-Private Partnerships

• Allows higher level of protected assets under Medicaid to people who buy state-approved policy

• Lowering amount of insurance needed • Connecticut, Indiana, California, and New York • Market penetration very low—less than 3 percent of

older people • Premiums still high • Asset protection not draw people • Not want to be on Medicaid • Deficit Reduction Act of 2005: 30 States

www.rti.org 1/15/14

29

Promoting Employer-Sponsored LTC Insurance

• Lower premiums due to younger ages and economies of scale—Federal plan: $950 for a 40 year old

• Idea to have federal and state employees to prime the pump—not worked

• Very small market, but growing, approximately 1,000,000 policies in place

• Federal tax incentives comparable to health insurance

• Employee pay all • Low market demand—6-7% take-up

www.rti.org 1/15/14

30

Public Sector Options: Expand State Programs for Home Care

• Most states have small state-funded programs for long-term care

• Often associated with U.S. Administration on Aging-funded programs

• Easy to control expenditures through appropriation process, rather than open-ended entitlement

• Requires additional state funds

www.rti.org 1/15/14

31

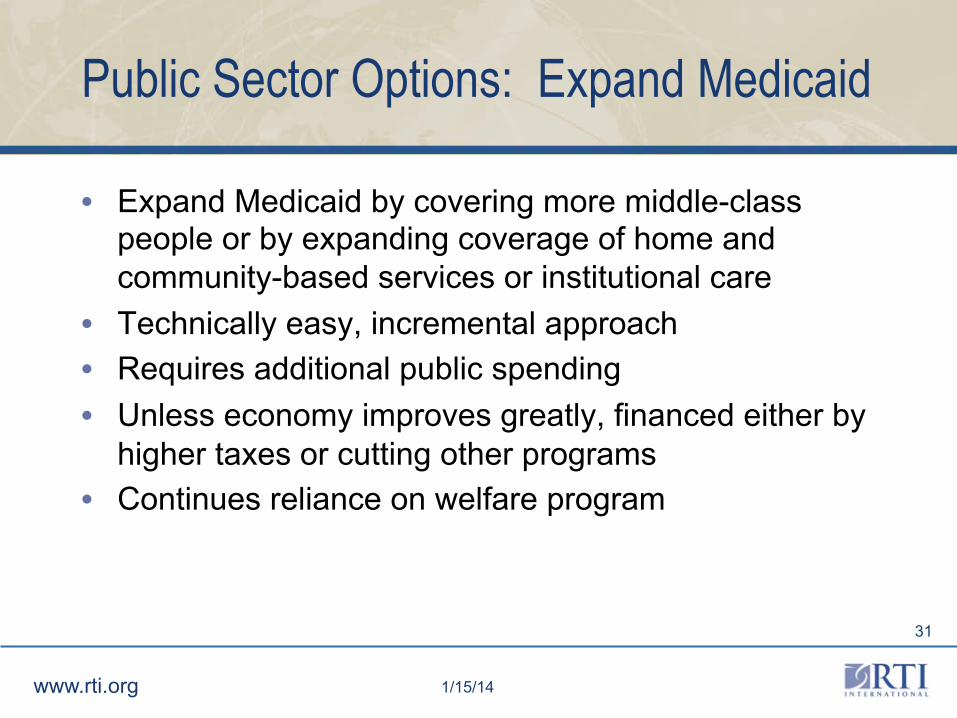

Public Sector Options: Expand Medicaid

• Expand Medicaid by covering more middle-class people or by expanding coverage of home and community-based services or institutional care

• Technically easy, incremental approach • Requires additional public spending • Unless economy improves greatly, financed either by

higher taxes or cutting other programs • Continues reliance on welfare program

www.rti.org 1/15/14

32

Public Insurance for LTC PROS • Medicare already provides funding for limited nursing

home and home health care • Creates a level playing field with medical care • If mandatory, only approach that will achieve

universal coverage • If mandatory, spreads the risk broadly over entire

society • Insurance premiums provide new benefits, which may

be more attractive than tax increases • Reduces two-tiered system between private pay and

Medicaid

www.rti.org 1/15/14

33

Public Insurance (cont.)

CONS • Some oppose increase in role of government and

expenditures • Some oppose mandatory participation • Voluntary program subject to adverse selection • More than very modest benefits require premium

subsidies to moderate and low-income people • Provides coverage to some people who can afford to

pay for their own care

www.rti.org 1/15/14

34

Community Living Assistance Services and Supports (CLASS) Act

• Voluntary government long-term care insurance program, originally developed by Senator Kennedy

• Part of health reform bills passed by Senate and House and endorsed by President Obama

• No medical underwriting • Cash benefit of an average of $50 per day • Lifetime benefit

www.rti.org 1/15/14

35

CLASS Act (cont.)

• Self-financed by insured, estimated premium over $100 per month

• No premium subsidy for middle or low-income people • “Saves” $72 - $102 billion over 10 years

www.rti.org 1/15/14

36

CLASS Act (cont.)

• Major issue of adverse selection – Automatic enrollment unless opt out – 5 year vesting before eligible for benefits – Initial enrollment limited to the working population

• Minimalist definition of “working” • Excludes retired elderly who do not work • Excludes current population with disabilities

who do not work

www.rti.org 1/15/14

37

Conclusions

• Hawaii has fewer services and spends less on long-term care than country as whole

• Long-term care expenditures sure to grow, but are relatively small percentage of total health spending

• Long-term care financing is primarily public or quasi-public sector in almost all developed countries

• Unsubsidized private LTC insurance unlikely to play a major financing role

www.rti.org 1/15/14

38

Conclusions (cont.)

• How should the long-term care system be structured? • How should we finance the large increase in

spending that is coming? • Who is responsible for long-term care?

www.rti.org 1/15/14

39

Contact Information

Joshua M. Wiener, Ph.D. Distinguished Fellow and Program Director Aging, Disability and Long-Term Care RTI International 701 13th Street, NW Suite 750 Washington, DC 20005 (202) 728-2094 [email protected]