Embed Size (px)

Citation preview

Long Lived Assets

• Types

• Cost determination

• Balance sheet presentation

• Disposal

Types:

• Land

• Buildings and equipment (plant assets)

• Intangible assets

• Natural resources

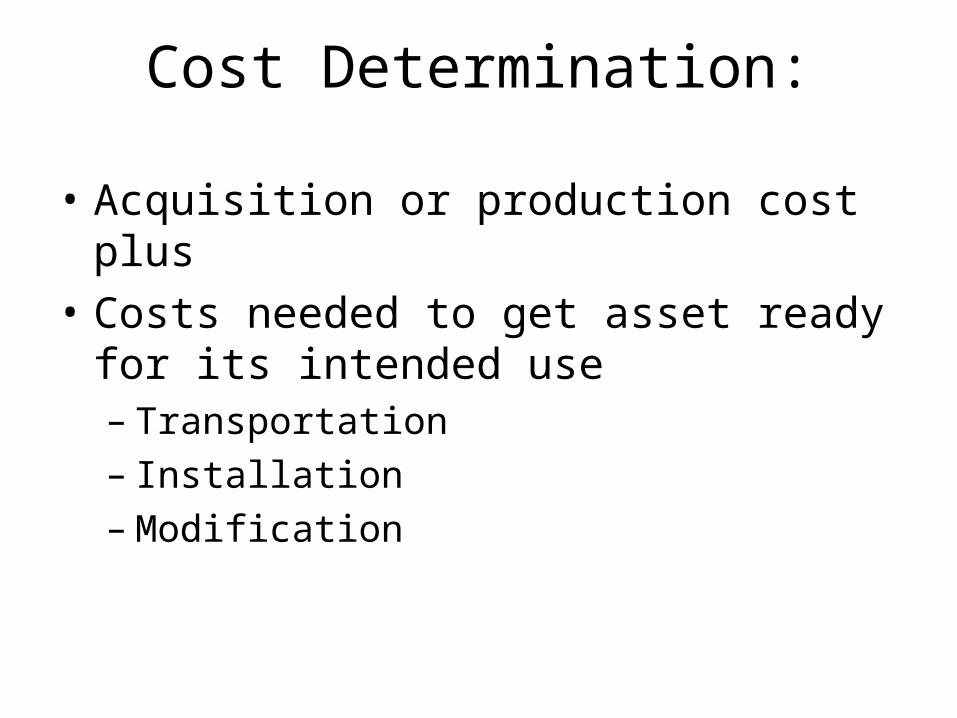

Cost Determination:

• Acquisition or production cost plus

• Costs needed to get asset ready for its intended use– Transportation– Installation– Modification

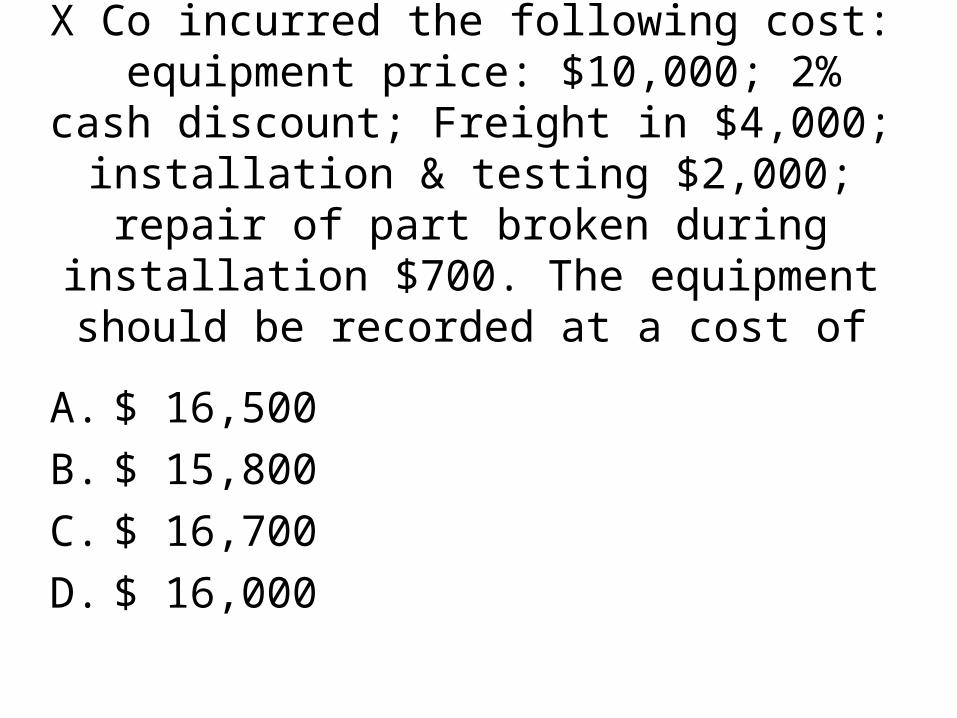

X Co incurred the following cost: equipment price: $10,000; 2% cash discount; Freight in $4,000; installation & testing $2,000; repair of part broken during installation $700. The equipment should be recorded at a cost of

A. $ 16,500

B. $ 15,800

C. $ 16,700

D. $ 16,000

Cost of Self Constructed Assets

• Material

• Labor

• Overhead

• Interest incurred during construction (FAS 34)

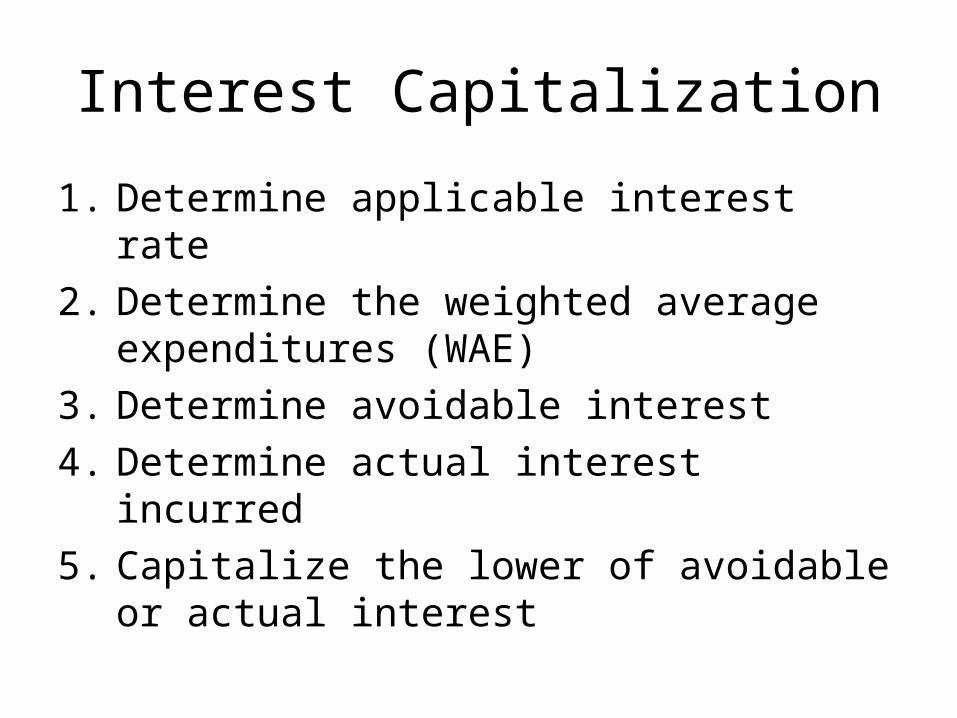

Interest Capitalization

1. Determine applicable interest rate

2. Determine the weighted average expenditures (WAE)

3. Determine avoidable interest

4. Determine actual interest incurred

5. Capitalize the lower of avoidable or actual interest

Exercise 10-10

1. Situation 1- Determine the amount of interest to be capitalized

2. Situation 3 Determine the amount of interest to be capitalized

Lump Sum purchases

Allocate the price paid in relation to the Fair Market Value of each asset.

1. E 10-13 – the land should be recorded at what cost?

2. E 10-13 – the building should be recorded at what cost?

Asset acquired for non interest bearing note – MUST be

discounted!

• E 10 – 14 Determine the cost at which the equipment should be recorded

Balance Sheet Presentation:

• Land, Goodwill at historical cost (unless written down for impairment)

• All other assets: Book value (BV):

• Cost – accumulated depreciation (or amortization or depletion)

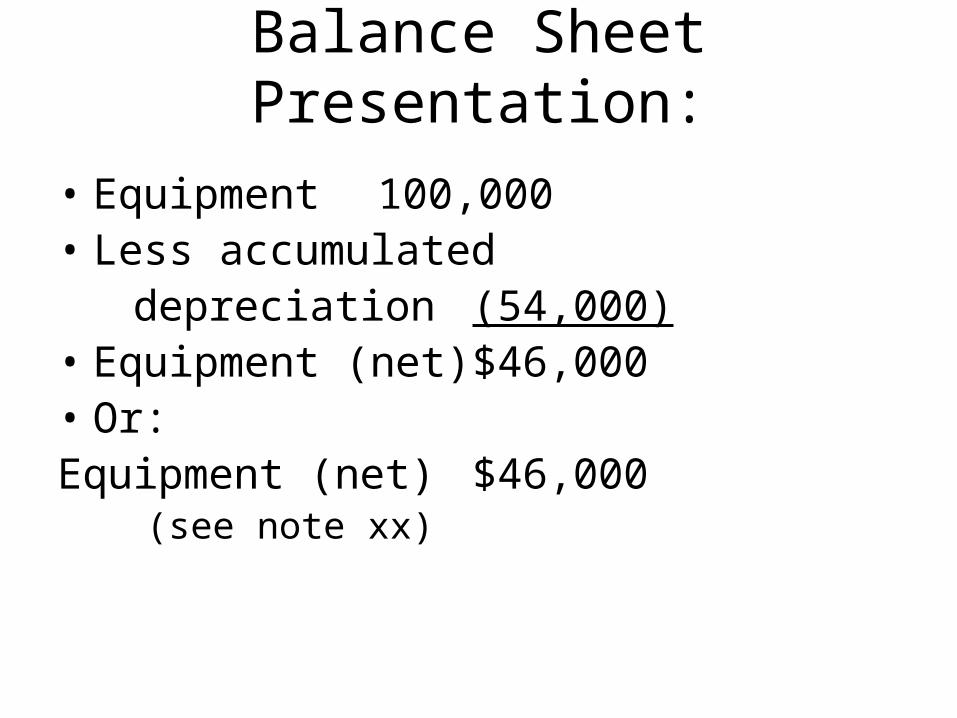

Balance Sheet Presentation:

• Equipment 100,000• Less accumulated depreciation (54,000)• Equipment (net) $46,000• Or:Equipment (net) $46,000 (see note xx)

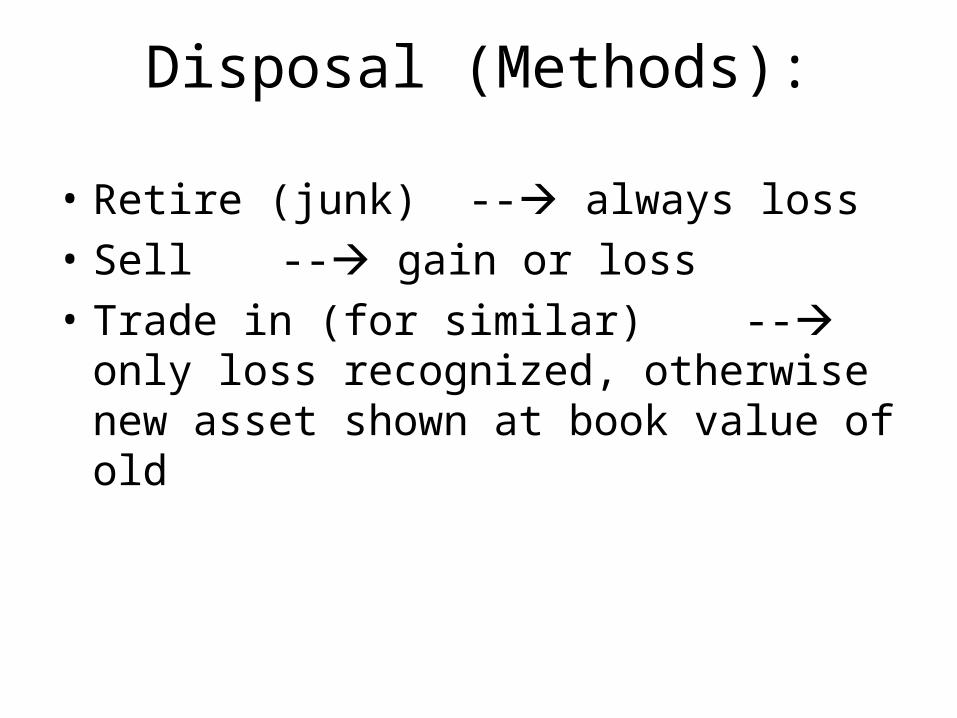

Disposal (Methods):

• Retire (junk) -- always loss

• Sell -- gain or loss

• Trade in (for similar) -- only loss recognized, otherwise new asset shown at book value of old

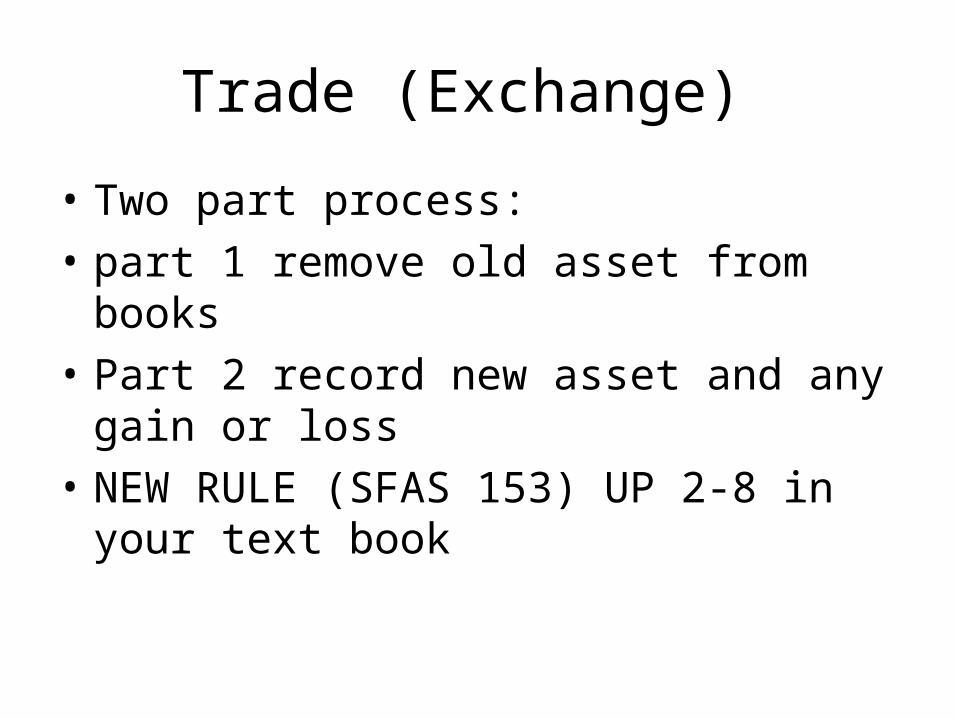

Trade (Exchange)

• Two part process:

• part 1 remove old asset from books

• Part 2 record new asset and any gain or loss

• NEW RULE (SFAS 153) UP 2-8 in your text book

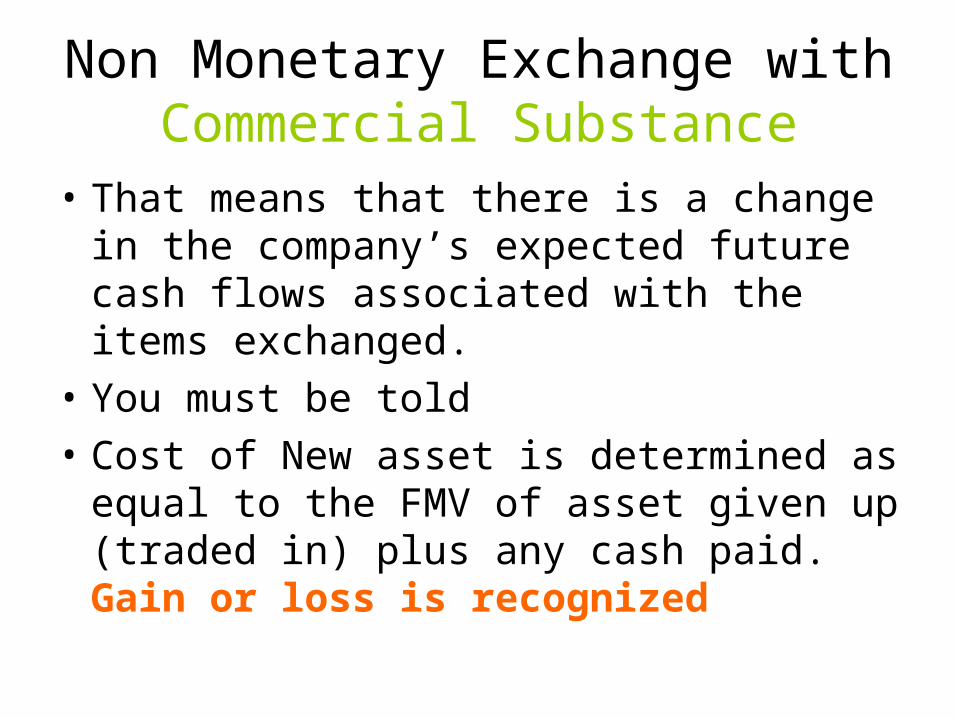

Non Monetary Exchange with Commercial Substance

• That means that there is a change in the company’s expected future cash flows associated with the items exchanged.

• You must be told

• Cost of New asset is determined as equal to the FMV of asset given up (traded in) plus any cash paid. Gain or loss is recognized

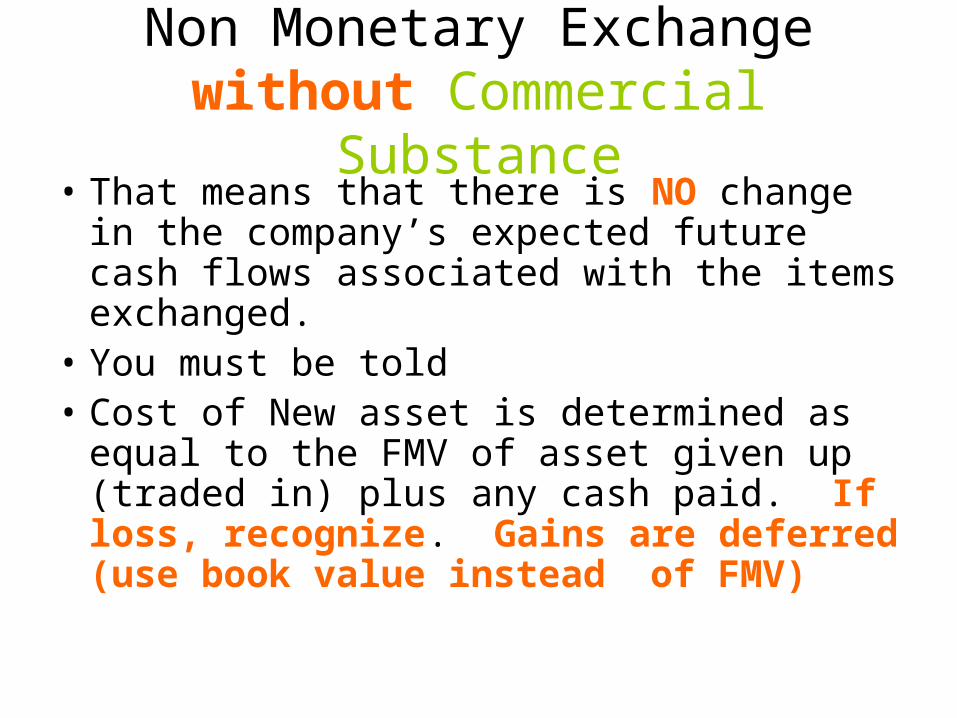

Non Monetary Exchange without Commercial Substance

• That means that there is NO change in the company’s expected future cash flows associated with the items exchanged.

• You must be told• Cost of New asset is determined as equal

to the FMV of asset given up (traded in) plus any cash paid. If loss, recognize. Gains are deferred (use book value instead of FMV)

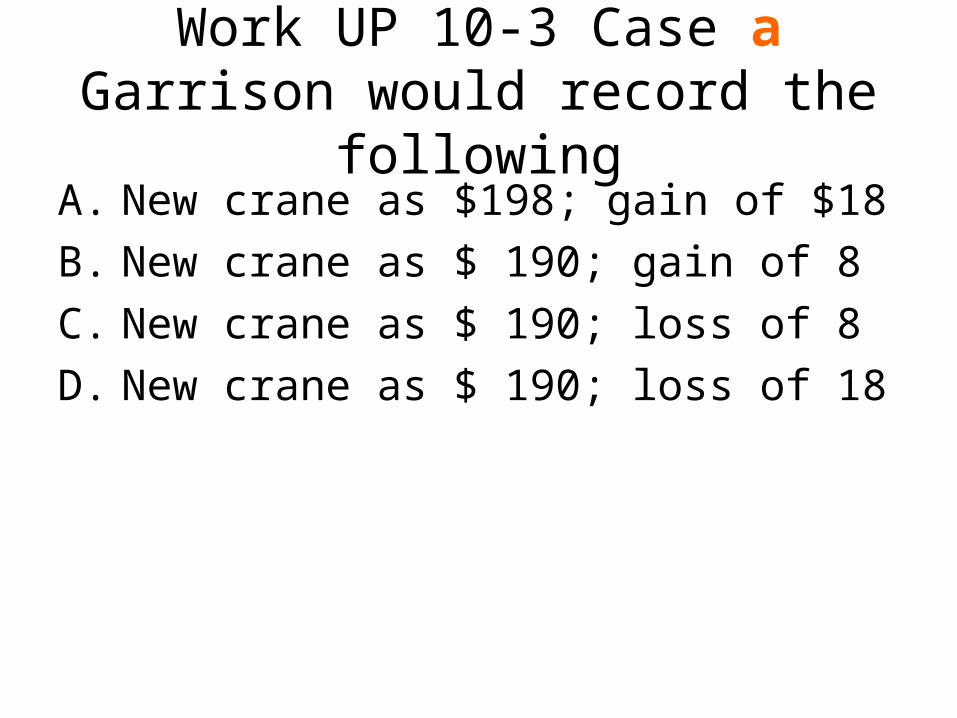

Work UP 10-3 Case a Garrison would record the following

A. New crane as $198; gain of $18

B. New crane as $ 190; gain of 8

C. New crane as $ 190; loss of 8

D. New crane as $ 190; loss of 18

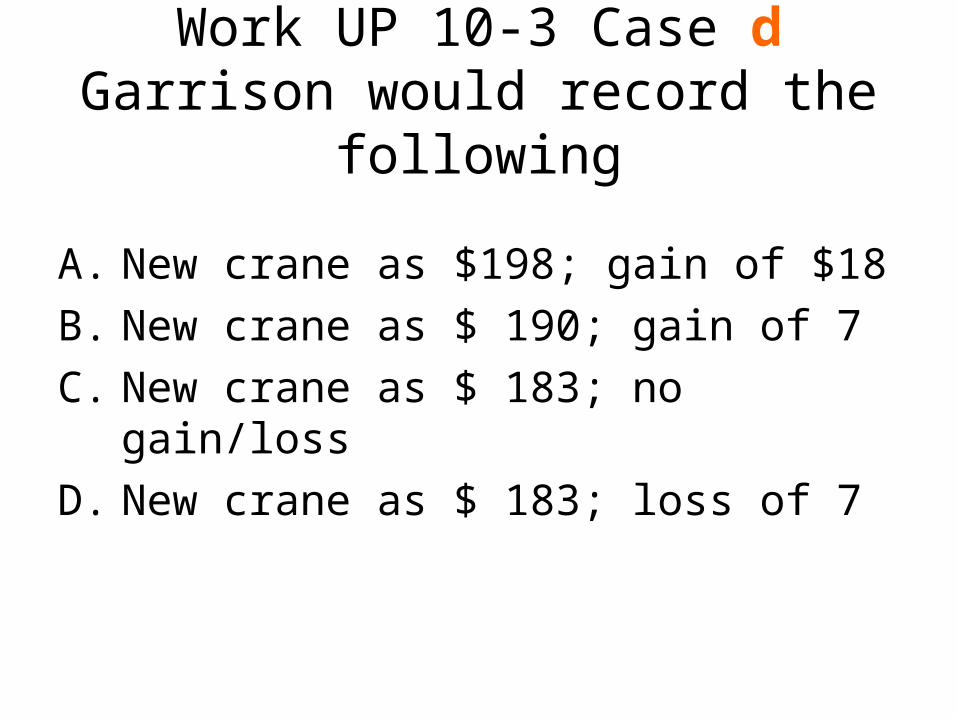

Work UP 10-3 Case d Garrison would record the following

A. New crane as $198; gain of $18

B. New crane as $ 190; gain of 7

C. New crane as $ 183; no gain/loss

D. New crane as $ 183; loss of 7

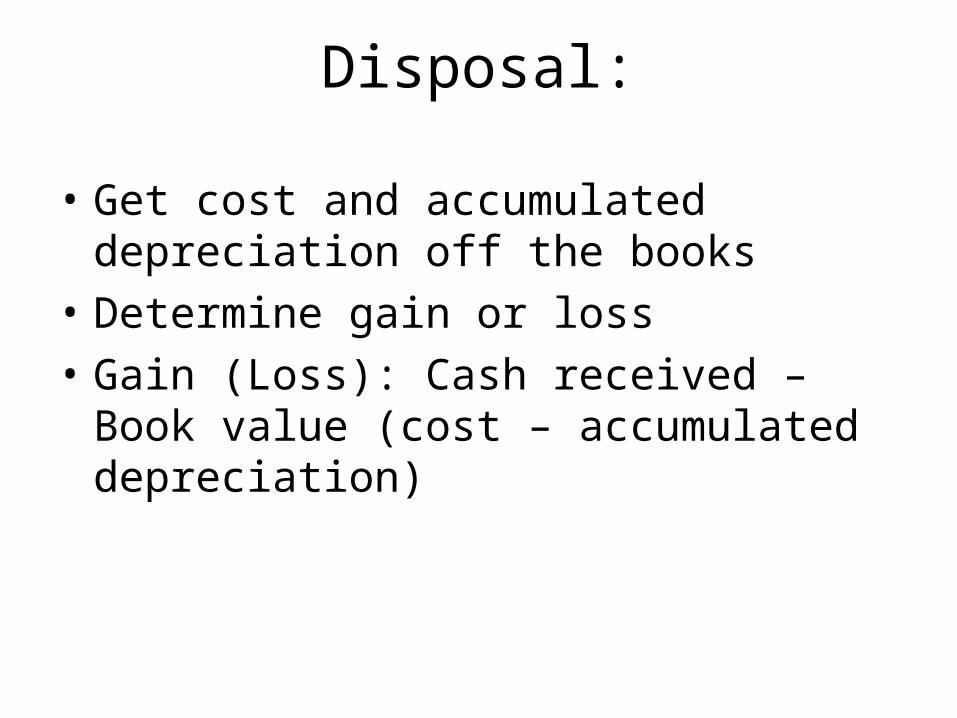

Disposal:

• Get cost and accumulated depreciation off the books

• Determine gain or loss

• Gain (Loss): Cash received – Book value (cost – accumulated depreciation)

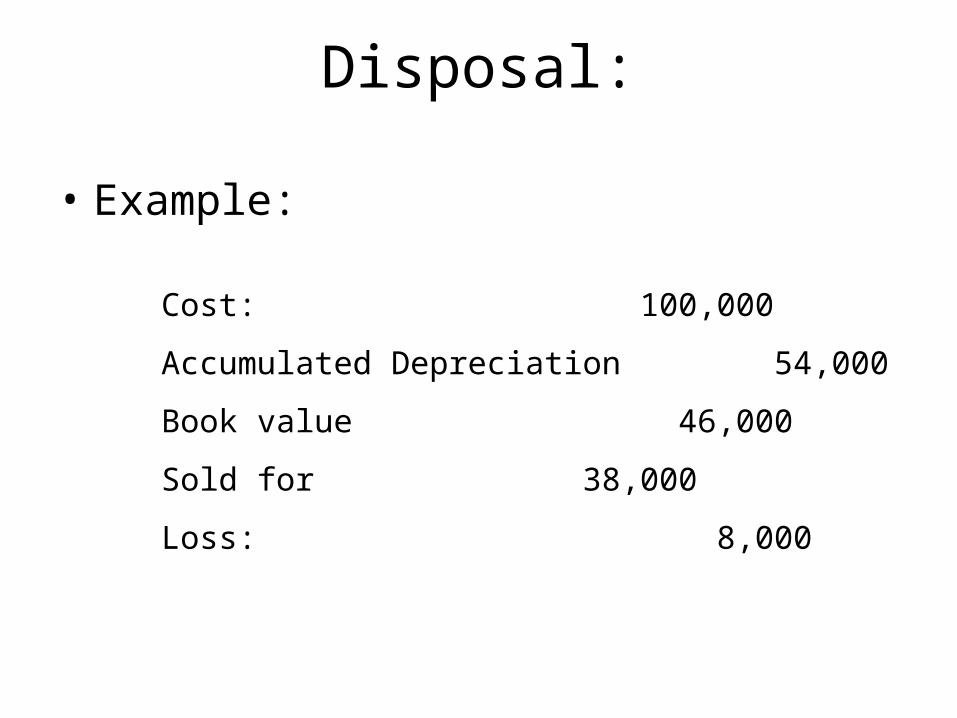

Disposal:

• Example:

Cost: 100,000

Accumulated Depreciation 54,000

Book value 46,000

Sold for 38,000

Loss: 8,000

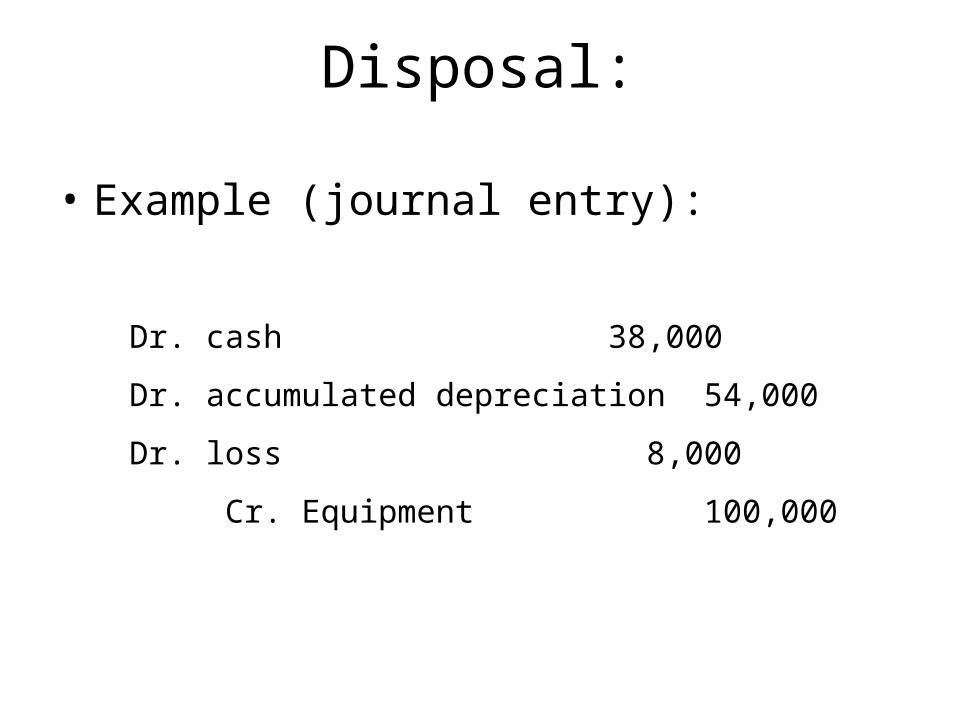

Disposal:

• Example (journal entry):

Dr. cash 38,000

Dr. accumulated depreciation54,000

Dr. loss 8,000

Cr. Equipment 100,000

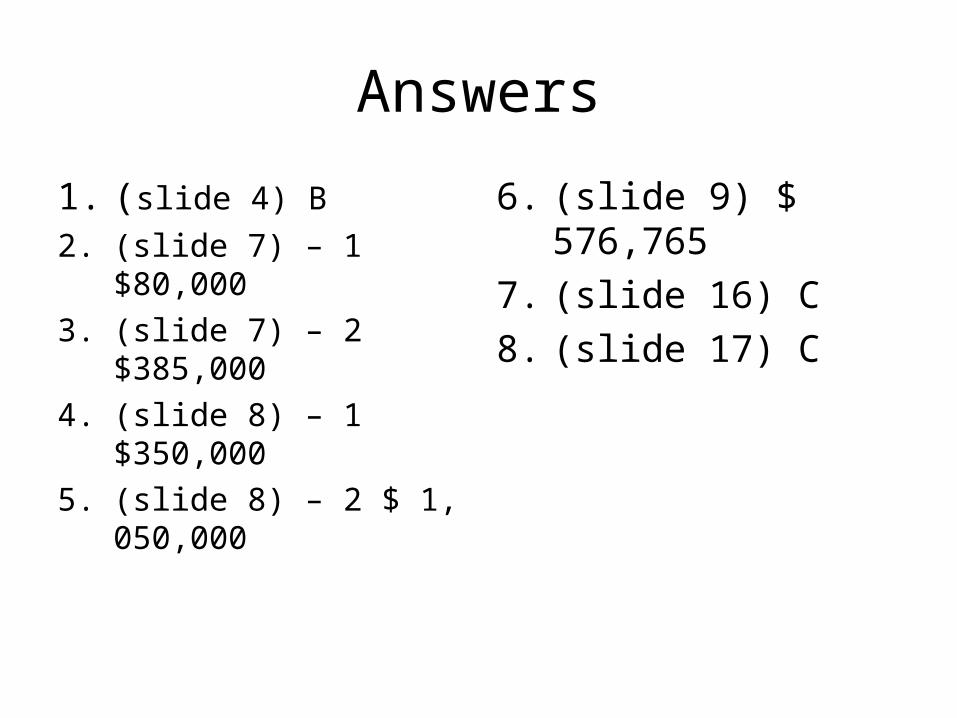

Answers

1. (slide 4) B

2. (slide 7) – 1 $80,000

3. (slide 7) – 2 $385,000

4. (slide 8) – 1 $350,000

5. (slide 8) – 2 $ 1, 050,000

6. (slide 9) $ 576,765

7. (slide 16) C

8. (slide 17) C