Embed Size (px)

Citation preview

Local Government Pension Scheme

24 March 2010

PENSION LIAISON OFFICERS’ GROUP (PLOG)

Local Government Pension Scheme

WELCOME / INTRODUCTIONS

• David Anthony – Head of Pensions

• Martin Summers – Pensions Manager

• Andy Cunningham – Employer Relationship Manager

Local Government Pension Scheme

AGENDA

1. Welcome/Attendance

2. Valuation data requirements (Andy Cunningham)

3. Valuation outlook and potential outcomes (David Anthony)

4. AVCs (Martin Summers)

5. FRS17 update (David Anthony)

6. Regulation changes and final pay protection (Martin Summers)

7. AOB

8. Dates/venue of forthcoming meetings

Local Government Pension Scheme

2. VALUATION DATA REQUIREMENTS- General data requirements

• Valuation will use data and accounting position as at 31st March 2010 to determine funding levels for all employers.

• Fund has until June to resolve all data issues up to 31st March.

• Out of date or incorrect records on our system have a direct effect on contribution rates (although the smaller the employer, the more significant one discrepancy will have)

Local Government Pension Scheme

2. VALUATION DATA REQUIREMENTS- End of year requirements

• End of year contributions spreadsheet sent out on 12/03/10 to be returned as soon as possible after 1st April 2010 (but no later than 19/05/10.

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

2010 Valuation

• Outlook

• Where are we now?

• Potential outcomes?

Local Government Pension Scheme

Outlook

• Not good! – Funding Levels or Contribution Rates• Political Pressure / Employer Affordability• Remember long term game for most• Longer term outlook:

– Economy

– Markets and returns

– Future benefit changes

– Further mortality improvements

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

CLG Consultations

• Consultations on valuations– Review of financing plans (short, medium and long term)– Local funding targets– Revised employee contributions

• Consultations on benefits and administration– Cost Sharing?

– Revised benefits?

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

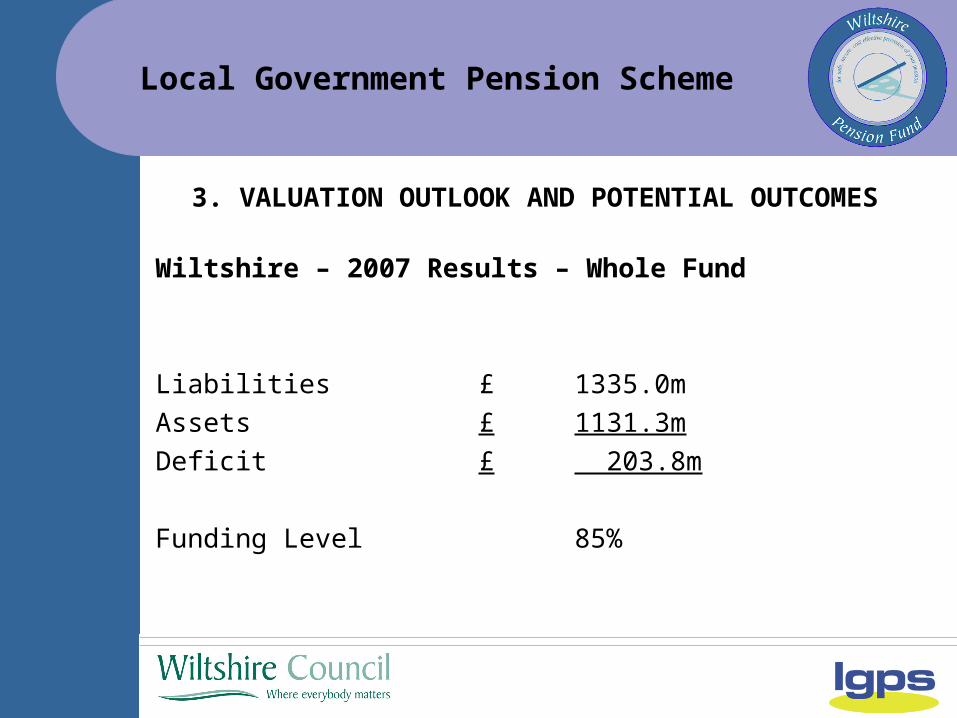

Wiltshire – 2007 Results – Whole Fund

Liabilities £ 1335.0m

Assets £ 1131.3m

Deficit £ 203.8m

Funding Level 85%

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

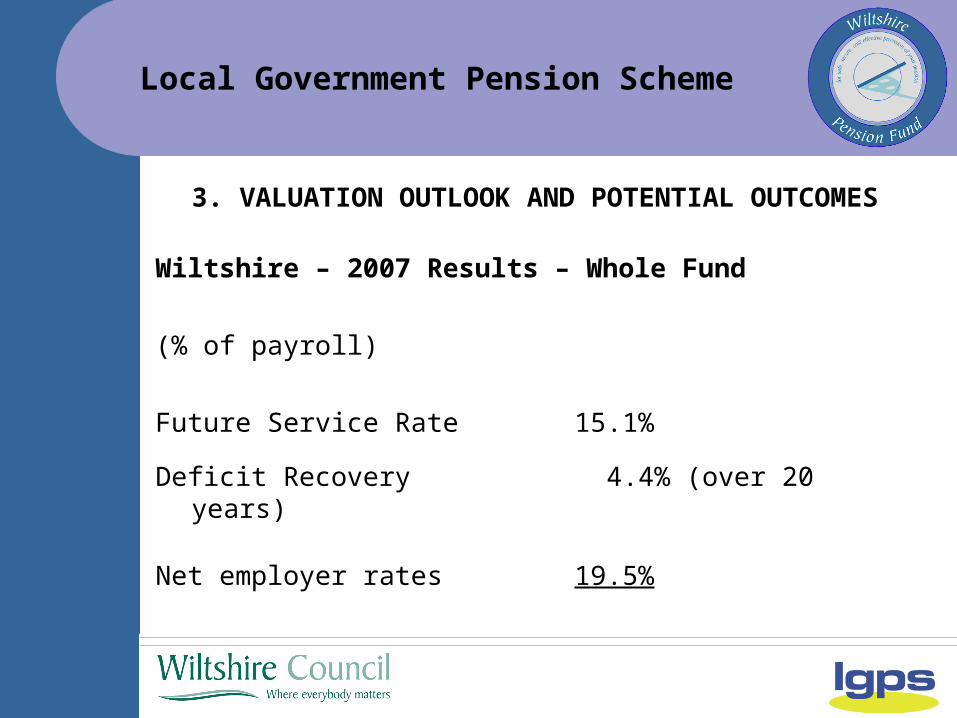

Wiltshire – 2007 Results – Whole Fund

(% of payroll)

Future Service Rate 15.1%

Deficit Recovery 4.4% (over 20 years)

Net employer rates 19.5%

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

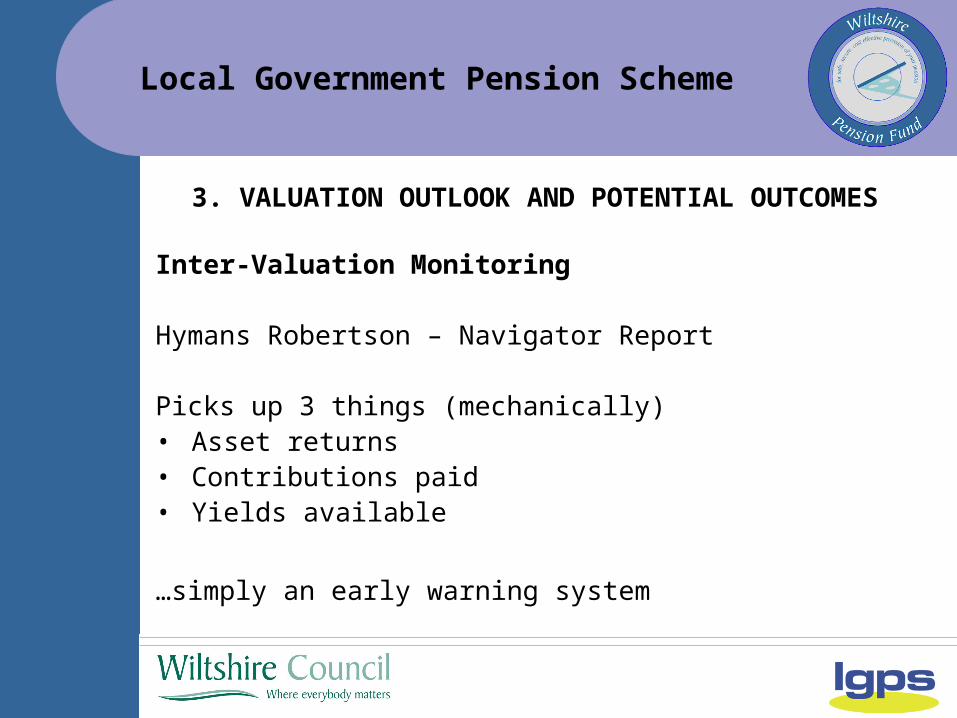

Inter-Valuation Monitoring

Hymans Robertson – Navigator Report

Picks up 3 things (mechanically)• Asset returns• Contributions paid• Yields available

…simply an early warning system

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

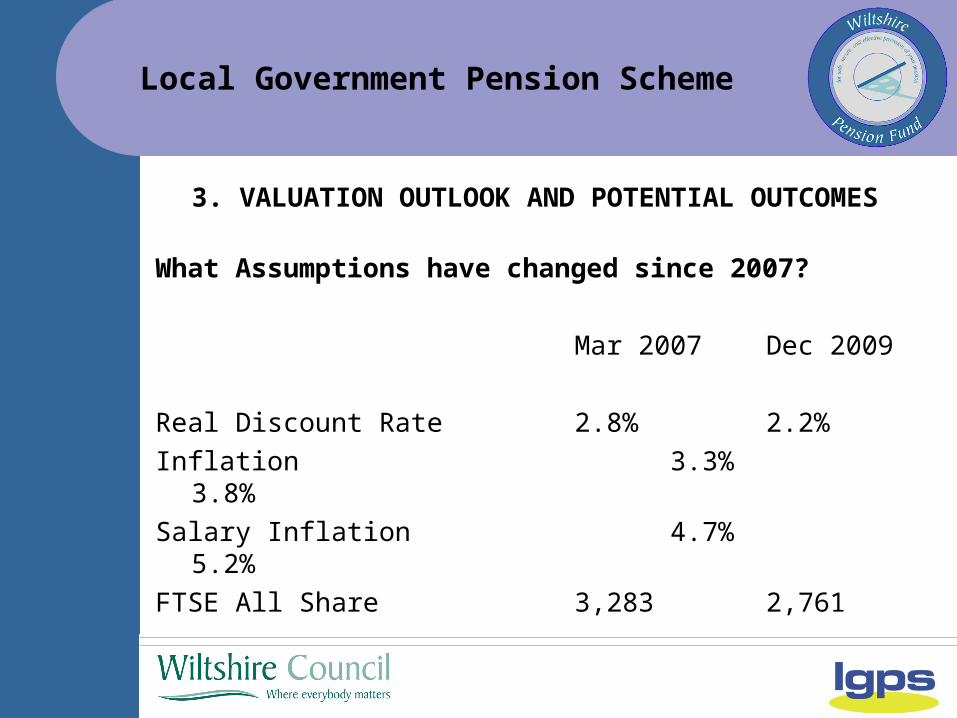

What Assumptions have changed since 2007?

Mar 2007 Dec 2009

Real Discount Rate 2.8% 2.2%

Inflation 3.3% 3.8%

Salary Inflation 4.7% 5.2%

FTSE All Share 3,283 2,761

Local Government Pension Scheme

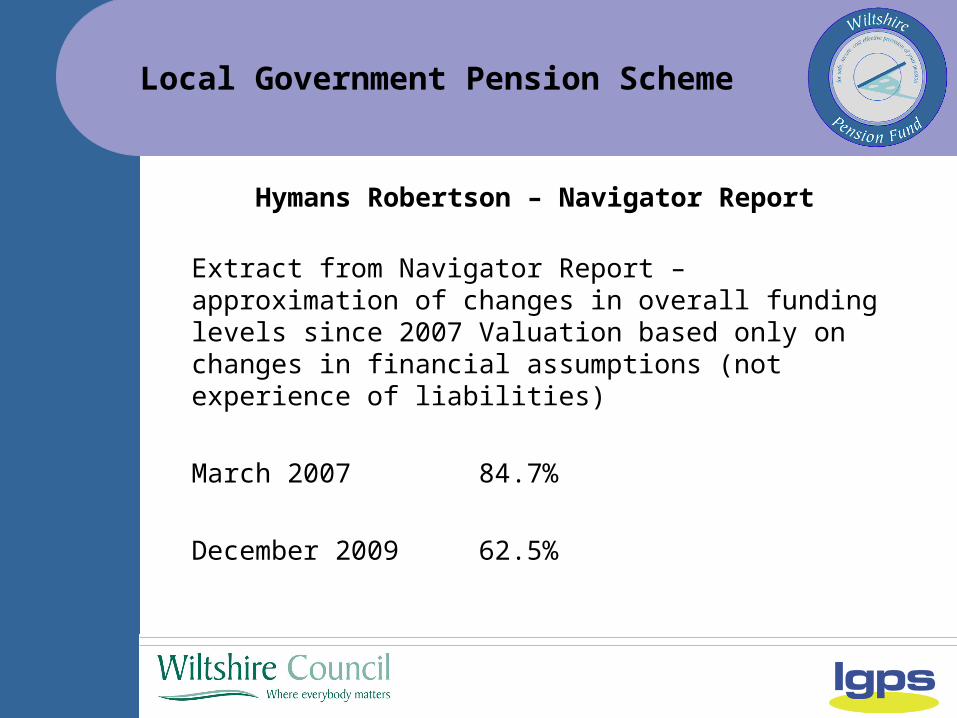

Hymans Robertson – Navigator Report

Extract from Navigator Report – approximation of changes in overall funding levels since 2007 Valuation based only on changes in financial assumptions (not experience of liabilities)

March 2007 84.7%

December 200962.5%

Local Government Pension Scheme

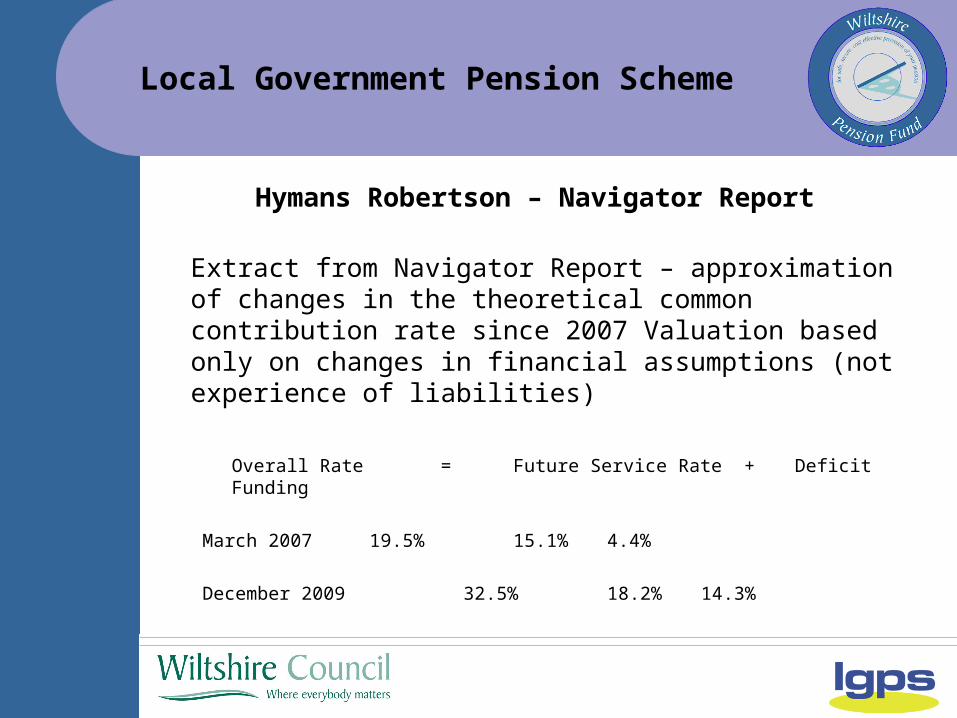

Hymans Robertson – Navigator Report

Extract from Navigator Report – approximation of changes in the theoretical common contribution rate since 2007 Valuation based only on changes in financial assumptions (not experience of liabilities)

Overall Rate = Future Service Rate + Deficit Funding

March 2007 19.5% 15.1% 4.4%

December 2009 32.5% 18.2% 14.3%

Local Government Pension Scheme

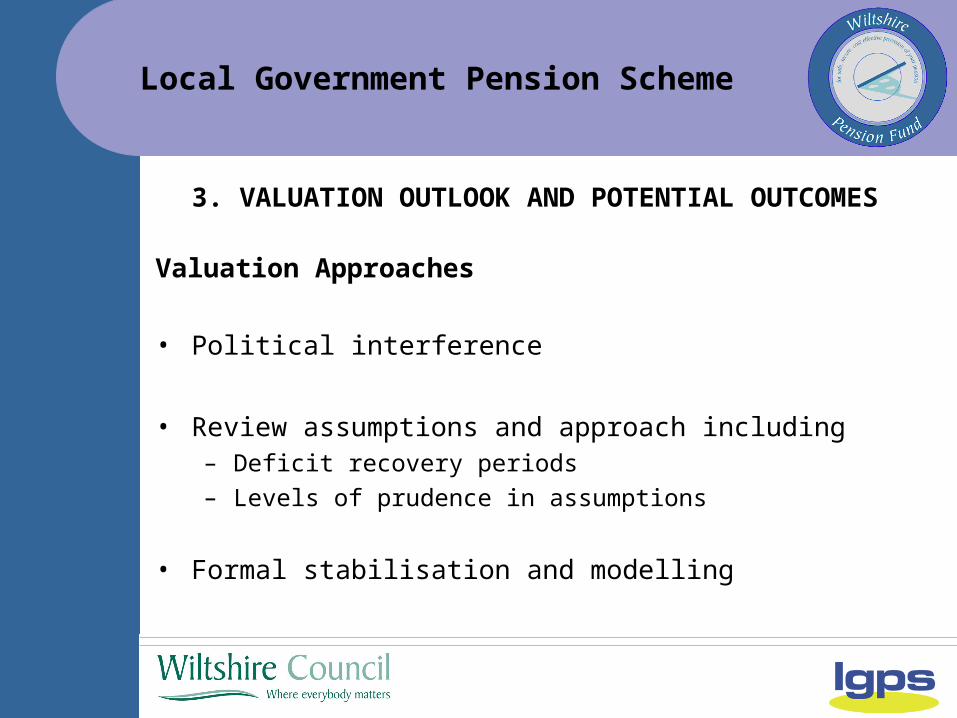

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

Valuation Approaches

• Political interference

• Review assumptions and approach including– Deficit recovery periods

– Levels of prudence in assumptions

• Formal stabilisation and modelling

Local Government Pension Scheme

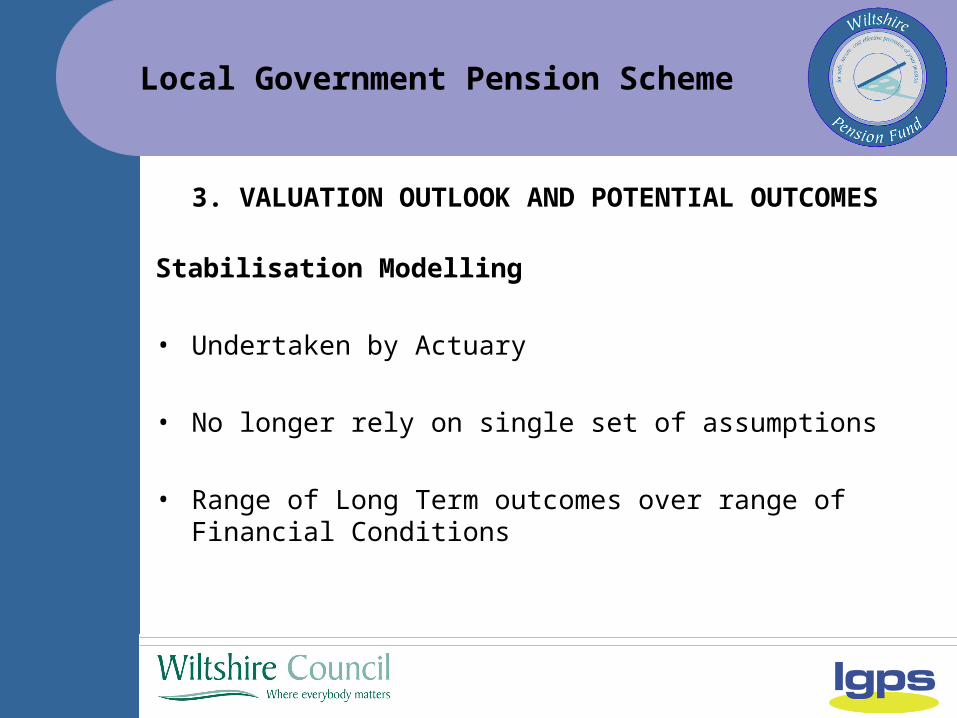

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

Stabilisation Modelling

• Undertaken by Actuary

• No longer rely on single set of assumptions

• Range of Long Term outcomes over range of Financial Conditions

Local Government Pension Scheme

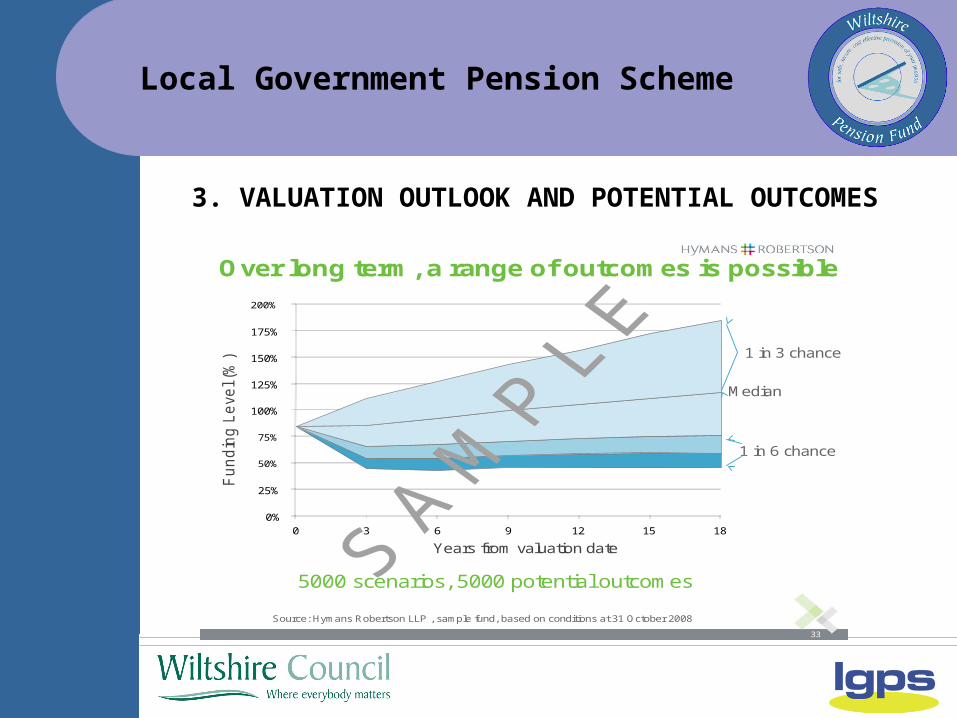

33

Over long term, a range of outcomes is possible

Source: Hymans Robertson LLP , sample fund, based on conditions at 31 October 2008

0%

25%

50%

75%

100%

125%

150%

175%

200%

0 3 6 9 12 15 18

Fu

nd

ing

Le

ve

l (%

)

Years from valuation date

5000 scenarios, 5000 potential outcomes

Median

1 in 3 chance

1 in 6 chance

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

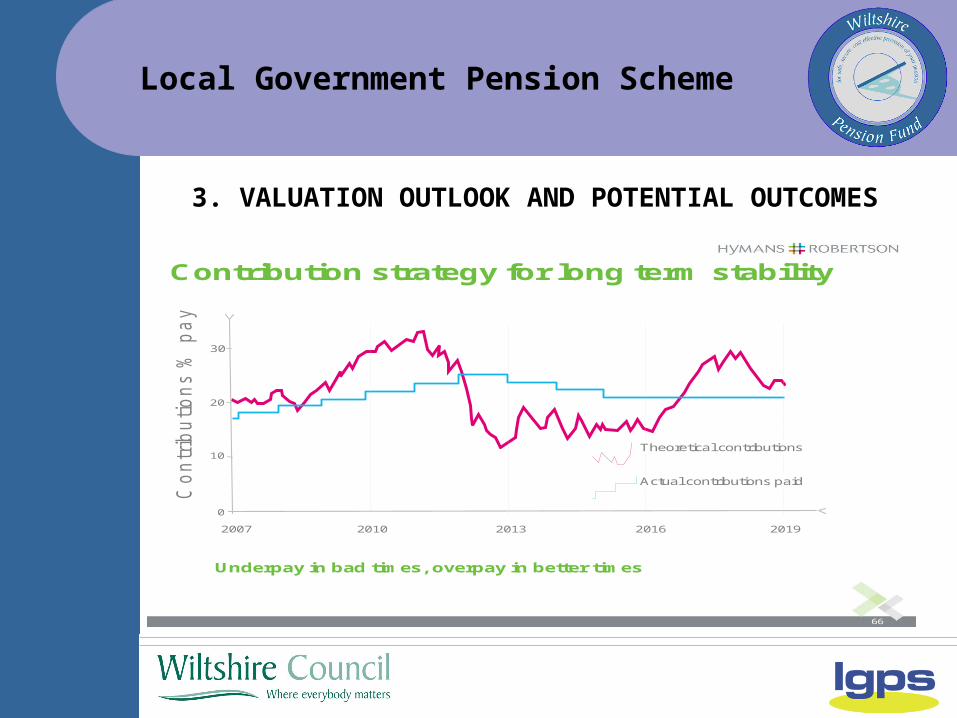

66

Contribution strategy for long term stability

Co

ntr

ibu

tio

ns %

pa

y

2007

30

20

10

0

2010 2013 2016 2019

Theoretical contributions

Actual contributions paid

Underpay in bad times, overpay in better times

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

Stabilisation Policy

• WPF needs to be comfortable 100% Funding Level achieved over Long Term (24 years)

• Avoid ‘knee-jerk’ increases in Contribution Rates• Stable contributions over time (e.g. max +1% / -1% p.a.)• Set Contribution rates for next 6 years • Review every 3 years validity of assumptions

Local Government Pension Scheme

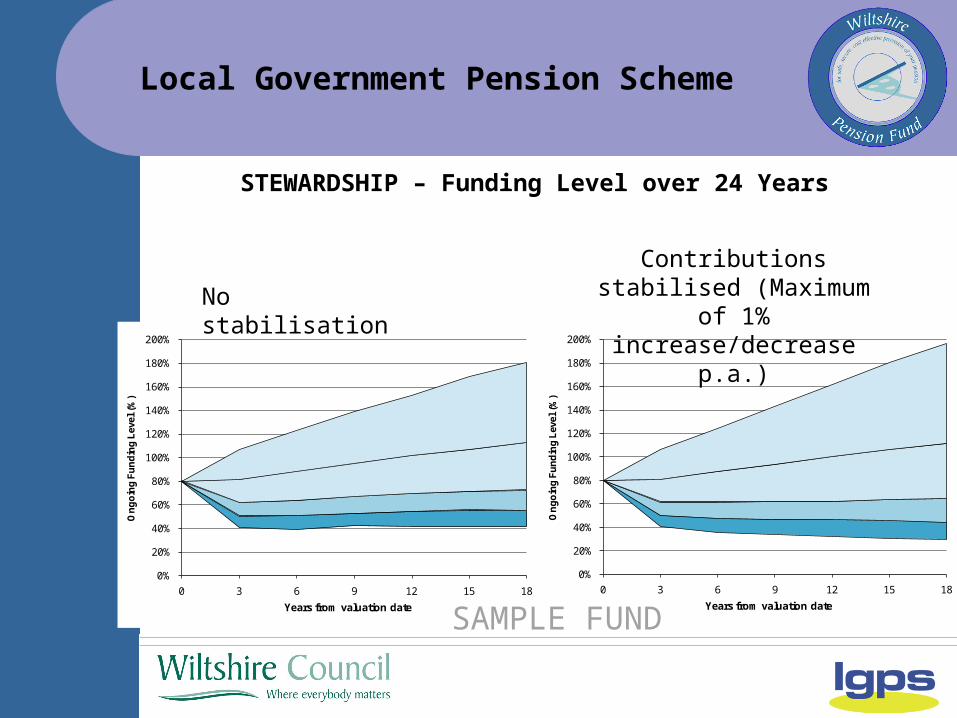

STEWARDSHIP – Funding Level over 24 Years

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0 3 6 9 12 15 18

On

go

ing

Fu

nd

ing

Lev

el (

%)

Years from valuation date

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0 3 6 9 12 15 18

On

go

ing

Fu

nd

ing

Lev

el (

%)

Years from valuation date

No stabilisation

Contributions stabilised (Maximum of 1%

increase/decrease p.a.)

SAMPLE FUND

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

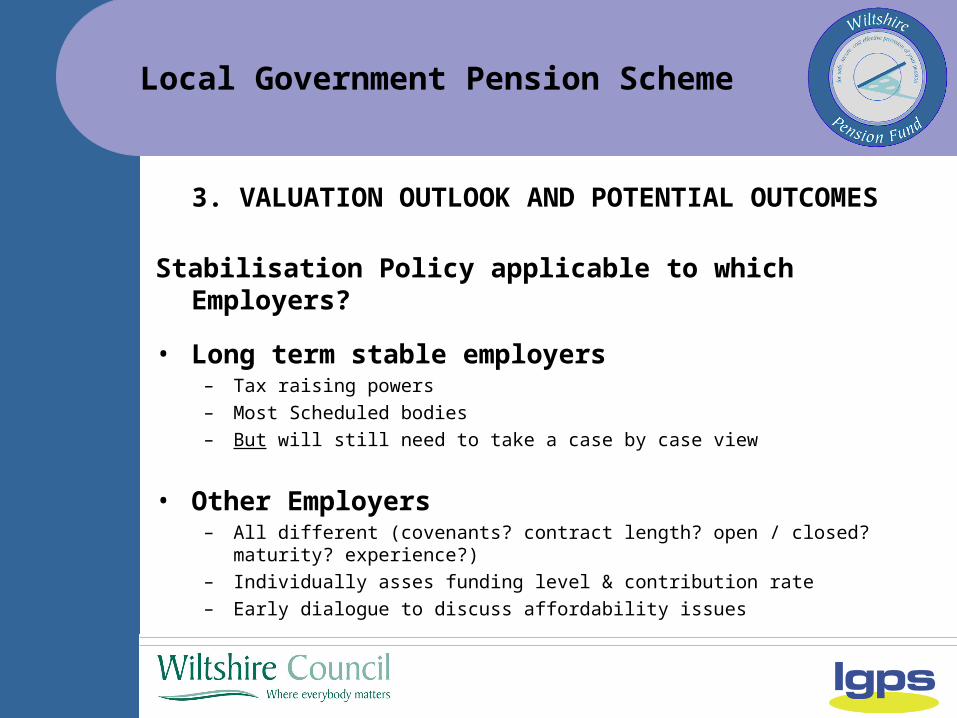

Stabilisation Policy applicable to which Employers?

• Long term stable employers– Tax raising powers

– Most Scheduled bodies

– But will still need to take a case by case view

• Other Employers– All different (covenants? contract length? open / closed? maturity? experience?)

– Individually asses funding level & contribution rate

– Early dialogue to discuss affordability issues

Local Government Pension Scheme

3. VALUATION OUTLOOK AND POTENTIAL OUTCOMES

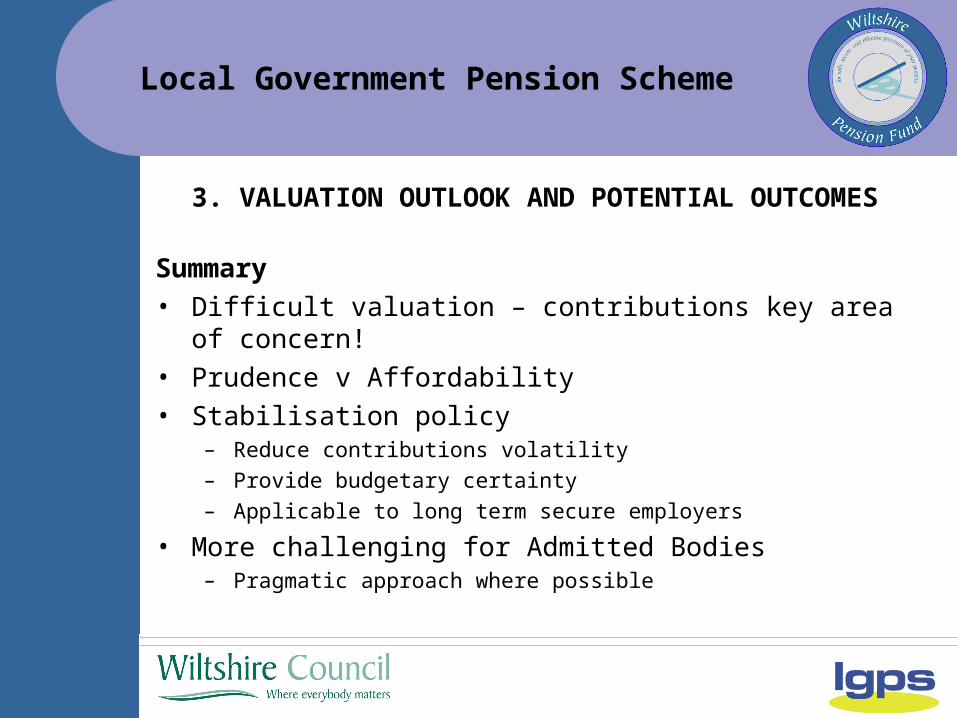

Summary• Difficult valuation – contributions key area of concern!• Prudence v Affordability• Stabilisation policy

– Reduce contributions volatility– Provide budgetary certainty – Applicable to long term secure employers

• More challenging for Admitted Bodies– Pragmatic approach where possible

Local Government Pension Scheme

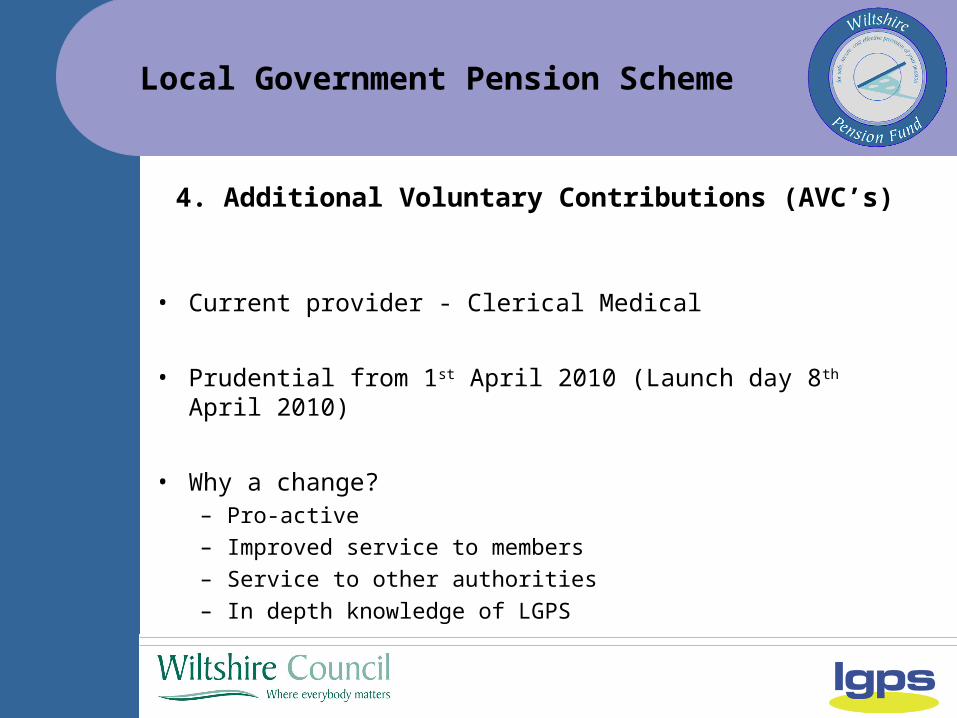

• Current provider - Clerical Medical

• Prudential from 1st April 2010 (Launch day 8th April 2010)

• Why a change?– Pro-active

– Improved service to members

– Service to other authorities

– In depth knowledge of LGPS

4. Additional Voluntary Contributions (AVC’s)

Local Government Pension Scheme

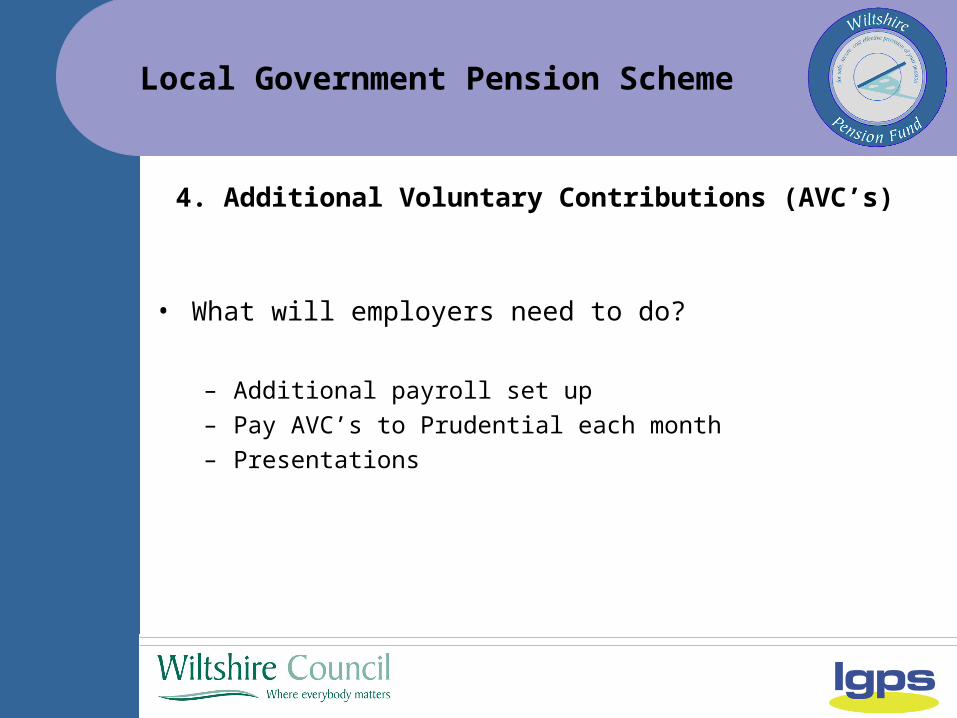

4. Additional Voluntary Contributions (AVC’s)

• What will employers need to do?

– Additional payroll set up

– Pay AVC’s to Prudential each month

– Presentations

Local Government Pension Scheme

• Current Clerical Medical contributors

– Continue with current arrangement

– Stop contributing (Leave funds with Clerical Medical)

– Stop contributing (Transfer)

– Letter from Pension Fund

4. Additional Voluntary Contributions (AVC’s)

Local Government Pension Scheme

5. FRS17 UPDATE

• Commission reports of behalf of Employers (24 p.a)– Prescribed format– Compare pension obligations of employers– Different from Valuation

• Standardised Reports– Economies of scale– Standardised Financial / non financial assumptions– Standard Discount Rates

• Quotes for additional work – FRS17 projections– Non-standard reports – New employers

Local Government Pension Scheme

• March 2010 Reports– Earlier delivery of reports (w/c 19th April)

– Based on 31 December 2009 data

– Notify WPF of any material changes post 31/12/09 (e.g. bulk transfers / redundancy programmes)

• Outlook

– Expect larger deficits this year!

– ‘Real’ discount rates 3.7% (2009) 1.7% (Nov 2009)

5. FRS17 UPDATE

Local Government Pension Scheme

• LGPS Miscellaneous (Regulations) 2009

• Pay Protection

• Additional Survivor Benefits Contributions (ASBC’s)

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

Local Government Pension Scheme

• Pay Protection

• Reduction in pay

– Single Status– Job Evaluation

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

Local Government Pension Scheme

• Pay Protection*

• Member can elect to use average 3 consecutive year’s pay to the 31st March in the last 13 years

• Member must make an election “no later than one month prior to the date that they cease membership of the scheme”

• *Currently the best year of the last 3 is provided to WPF

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

Local Government Pension Scheme

• Pay Protection - Challenges

• Getting notification from members before they leave/retire• Pensionable Salary information for member to make

decision• Employers access to payroll/pension information for 13

years

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

Local Government Pension Scheme

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

• Additional Survivor Benefit Contributions (ASBC’s)

• LGPS Regulations 2008

– Co-habiting partners

– Post 6th April 1988 service

Local Government Pension Scheme

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

• Additional Survivor Benefit Contributions (ASBC’s)

• 2009 Regulations

– Purchase service Pre 6th April 1988

– Election to pay ASBC’s before 31st March 2011

– Additional percentage of pay (GAD factors)

– Medical clearance from member

Local Government Pension Scheme

6. REGULATIONS CHANGES AND FINAL PAY PROTECTION

• What will employers need to do?

– Additional payroll set up

– Pay AVC’s to Wiltshire Pension Fund each month with normal contributions

– Notifications of members wishing to pay ASBC’s will be sent from Wiltshire Pension Fund

Local Government Pension Scheme

7. ANY OTHER BUSINESS

Any Questions?

Local Government Pension Scheme

8. DATES OF FORTHCOMING MEETINGS

Final Valuation Results Meeting:2:30pm, Thursday 30th September 2010 at County Hall, Trowbridge