Embed Size (px)

Citation preview

FSRU: Risks and Opportunities

Karthik Sathyamoorthy President

Sudhanshu Haldar Manager

Galway Group 8 Temasek Blvd, #22–04,

Suntec Tower 3 Singapore 038988

www.galwaygroup.com

ABSTRACT

In the context of rising global energy demand and abundant shale gas reserves, governments

and developers across the world are considering natural gas as a viable fuel for augmenting their

energy portfolios. Increasingly, gas buyers are exploring floating regasification solutions for their

perceived speed of deployment, cost advantages, and redeployment flexibility.

FSRU solution comes in different configurations. For example, Brazil has two out of three FSRUs

converted from LNGC, whereas Uruguay is going forward with world’s biggest new-built FSRU.

However, the FSRU market is in early stages and there is an increasing need for understanding the

opportunities and risks associated with potential FSRU solutions.

This paper outlines and explores FSRU as a regasification solution, as compared to an onshore

terminal, and discusses some major risks and key drivers for FSRUs from a developer’s perspective.

These risks and opportunities have been discussed from investment, commercial and technology

aspects. This paper also points out some major considerations that a project developer should

weigh to gain a clear understanding of whether FSRU is the right solution for the project under

consideration.

Page 2 of 13

Introduction and Background

With increasing gas demand across the world, new and innovative LNG terminal solutions have

surfaced the industry. These innovations spread across both the technological and commercial

fronts. A unique combination of these innovations has resulted in the emergence of floating

regasification solutions as an alternate to the onshore regasification terminals.

Gulf Gateway Deepwater port, installed offshore Louisiana in March 2005, was the earliest

design of floating regasification solutions. This facility utilized a submerged turret-loading buoy that

allowed connection to multiple downstream pipelines. However, the shale boom was unforeseen at

the time of this development. As a result of this significant development in gas production in the

US, Gulf Gateway was decommissioned in 2012.

Gulf Gateway’s era may be over, but its proven technology opened the doors for a new age of

innovative floating regasification solutions. This technology has largely been derived from either

the offshore oil industry (e.g., mooring systems, unloading systems), the LNG shipping industry

(e.g., LNG containment systems), or land-based LNG regasification (e.g., vaporizers). Therefore,

the technology risks are well understood and can be managed effectively on a project-by-project

basis, leading to as increased acceptance of floating regasification solutions.

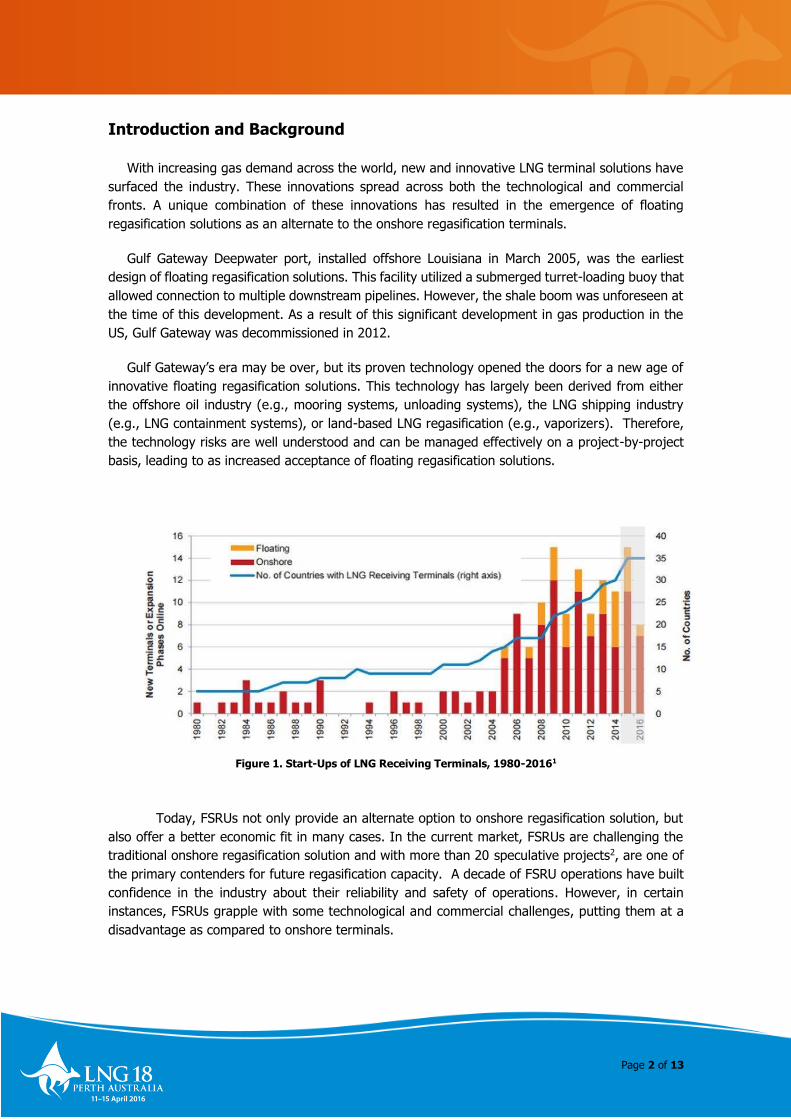

Figure 1. Start-Ups of LNG Receiving Terminals, 1980-20161

Today, FSRUs not only provide an alternate option to onshore regasification solution, but

also offer a better economic fit in many cases. In the current market, FSRUs are challenging the

traditional onshore regasification solution and with more than 20 speculative projects2, are one of

the primary contenders for future regasification capacity. A decade of FSRU operations have built

confidence in the industry about their reliability and safety of operations. However, in certain

instances, FSRUs grapple with some technological and commercial challenges, putting them at a

disadvantage as compared to onshore terminals.

Page 3 of 13

How are FSRUs different from an Onshore Facility?

An FSRU is a ship or barge that is built (or retrofitted from an LNG carrier) to be able to perform

regasification operations onboard. The vessel requires little or no site preparation (except

associated facilities) and is equipped with an onboard LNG storage facility. In some instances, it

can also connect to the existing offshore gas pipeline grid. This is unlike an onshore development,

which requires on-land site preparation and development, constructing cryogenic storage tanks,

integrating LNG regasification units and developing a berthing facility for LNG carriers.

An FSRU can be built either by retrofitting an existing LNG ship (“Retrofit”) or a by building an

entirely new LNG ship fitted onboard regasification equipment (“Newbuild”). A retrofitted FSRU is

one that is adapted from an LNG carrier. Retrofitting includes making modifications and adding a

regasification unit onboard. Many factors come into the equation when determining which type of

LNG carrier would make the best FSRU – availability and costs being the leading factors.

The two most prominent drivers that have made the FSRU option attractive to the developers

are (i) shorter project development timeline as compared to an onshore terminal with a similar gas

send-out rate, and; (ii) lower upfront project development capital costs as compared to a similar

sized onshore terminal. FSRUs have proven to be a better alternative for locations where either

space for development or additional infrastructure is a constraint. FSRUs can also be employed for

the use of offshore gas grids, which are no longer in use. Shorter permitting timelines are also

often pronounced as one of the benefits, however, this can vary case by case basis.

Current FSRU market and outlook

The floating LNG terminal market is a relatively new one. However, FSRUs have been gaining

a market share, especially among the new and proposed regasification terminals. The share of

FSRU as an import terminal option among the LNG importing countries is increasing swiftly and

FSRUs continue to gain popularity, especially in countries that are looking to enter the LNG import

market with lower capital investment and within a short timeframe. Since the inception of the

floating LNG solutions in 2005, more than 20 FSRUs have been constructed and deployed.

Over the last decade, the highest activity in the FSRU segment has been observed in Middle-

east and South America. Recently European and Asian economies have started deploying FSRUs to

meet their natural gas needs. By end of 2014, Brazil’s Bahia/TRBA, Indonesia’s Lampung, and

Lithuania’s Klaipeda LNG began their operations. In 2015, three additional FSRUs came online,

including one in Pakistan chartered from Excelerate Energy, one in Egypt chartered from Hoegh

LNG and one in Jordan chartered from Golar LNG1.

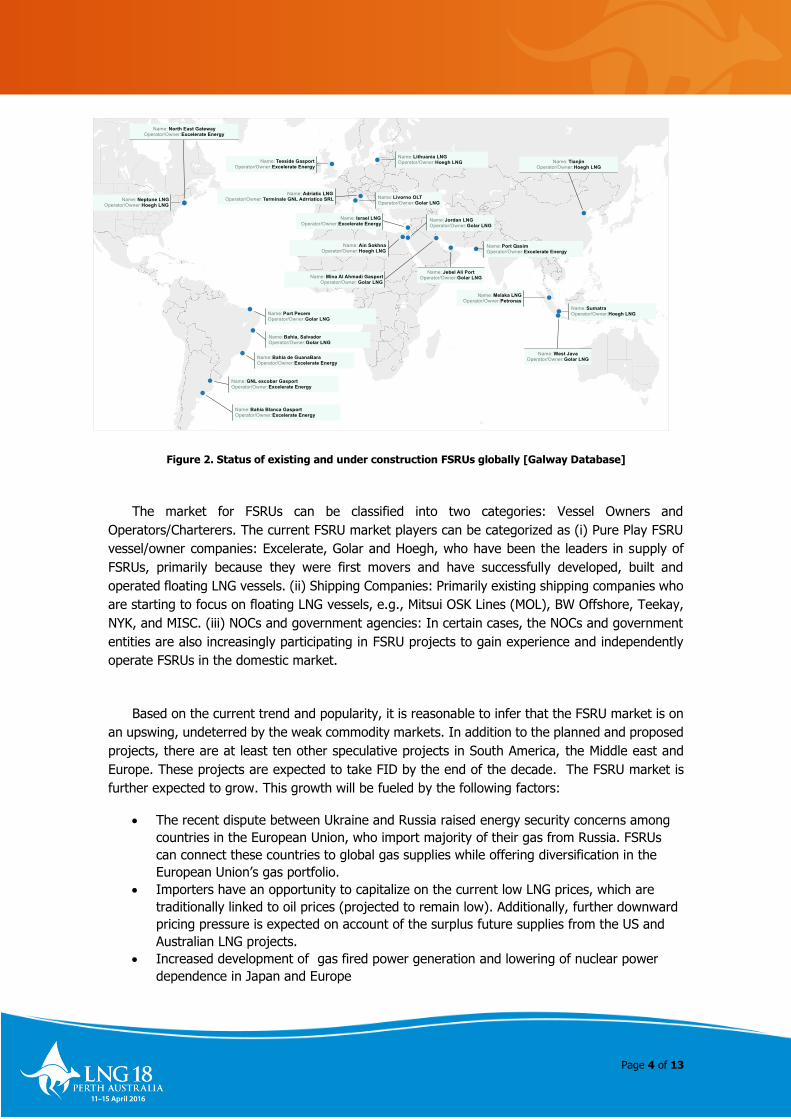

The following chart (Figure 2) maps the existing terminals across the globe.

Page 4 of 13

Figure 2. Status of existing and under construction FSRUs globally [Galway Database]

The market for FSRUs can be classified into two categories: Vessel Owners and

Operators/Charterers. The current FSRU market players can be categorized as (i) Pure Play FSRU

vessel/owner companies: Excelerate, Golar and Hoegh, who have been the leaders in supply of

FSRUs, primarily because they were first movers and have successfully developed, built and

operated floating LNG vessels. (ii) Shipping Companies: Primarily existing shipping companies who

are starting to focus on floating LNG vessels, e.g., Mitsui OSK Lines (MOL), BW Offshore, Teekay,

NYK, and MISC. (iii) NOCs and government agencies: In certain cases, the NOCs and government

entities are also increasingly participating in FSRU projects to gain experience and independently

operate FSRUs in the domestic market.

Based on the current trend and popularity, it is reasonable to infer that the FSRU market is on

an upswing, undeterred by the weak commodity markets. In addition to the planned and proposed

projects, there are at least ten other speculative projects in South America, the Middle east and

Europe. These projects are expected to take FID by the end of the decade. The FSRU market is

further expected to grow. This growth will be fueled by the following factors:

The recent dispute between Ukraine and Russia raised energy security concerns among

countries in the European Union, who import majority of their gas from Russia. FSRUs

can connect these countries to global gas supplies while offering diversification in the

European Union’s gas portfolio.

Importers have an opportunity to capitalize on the current low LNG prices, which are

traditionally linked to oil prices (projected to remain low). Additionally, further downward

pricing pressure is expected on account of the surplus future supplies from the US and

Australian LNG projects.

Increased development of gas fired power generation and lowering of nuclear power

dependence in Japan and Europe

Page 5 of 13

Bridging solution for countries transitioning from being natural gas exporters to importers

and countries that need temporary intermediate energy solutions while development of

large onshore terminals is underway

Bridging solution until cleaner and renewable fuels can be scalable and commercialized

Small scale opportunities for FSRUs in areas with scattered demand e.g. Indonesia

On the back of the current situation and the expected developments in this space, it is

reasonable to assume that FSRUs have the potential to develop into a highly preferred regasification

option in the future. However, there are numerous complexities – technological, commercial and

operational – which can undermine the prospects of FSRU project development. These potential

challenges need to be overcome for the industry’s full potential to be achieved.

FSRUS: Opportunities and Risks - A developer’s dilemma

Although, natural gas is increasingly expected to play a pivotal role in the energy mix for a

large number of countries, the availability of the natural gas resources are not shared equally. A

growing number of countries are turning to LNG imports to meet their growing gas demand. This

presents the developers with an opportunity to come up with an economically sound and a safe

natural gas import strategy. There are multiple decisions to be made when strategizing a

regasification project. The primary decision is on the type of import terminal to be developed –

onshore or offshore.

Further, there are hybrid solutions such as a Floating Storage Unit (FSU) with regasification

units located onshore that can be considered. Such a solution might be required depending on site

considerations and may be more appropriate if:

There are exclusion zone limitations with siting of LNG storage tanks onshore e.g.,

adherence to thermal radiation and vapor dispersion regulations;

An LNG import facility is being fast-tracked and operations have to start before

completion of the onshore storage tanks.

A developer must clearly understand various pros and cons of onshore and offshore solutions

before embarking on a development plan. The following section offers some insights on these risks

and opportunities associated with offshore regasification solutions when compared with onshore

solutions.

Key Drivers in favor of an FSRU

FSRUs are becoming increasingly popular among the new LNG regasification project developers

because of following perceived benefits

A. Lower upfront development cost as compared to an onshore regasification

facility

One of the primary drivers in favor of the FSRU option is the low upfront capital investment

requirement. A typical FSRU can cost in the range of US $250 million to US $350 million (additional

US $200 to US $400 million for associated facilities) as compared to a similar sized (gas send-out)

onshore facility, which can cost in the range of US $1.0 billion to US $1.5 billion. FSRU capital costs

are typically lower onshore regasification terminals because of following reasons:

Page 6 of 13

FSRUs do not require expensive site development and the construction of stand-alone

LNG storage tanks (each tank can costs in excess of US $150 million)

FSRUs are built in a shipyard, so there can be a better control over costs as compared to

an onshore terminal

FSRUs and associated facilities have a lower footprint as compared to onshore terminals,

thus reducing land procurement costs

Depending on the project developer’s needs, a further reduction in upfront cost can also be

attained by retrofitting an existing LNG carrier, or leasing an existing FSRU vessel. The latter option,

however, will result in loss of ship deck customization and can turn expensive if employed on a

long term basis.

B. Faster project development timeline as compared to an onshore facility

The development timeline of an FSRU based project can vary between 12 to 36 months. If an

FSRU is already available, the delivery time is even shorter. However, if an existing vessel is

converted, it could be take anywhere in the range of 12 to 18 months. In the case of a newbuild

FSRU, the construction and delivery time could be up to 3 years. This is considerably shorter as

compared to an onshore development, which requires 48 to 56 months for development. Reasons

for faster delivery time of an FSRU solutions include:

FSRUs are built in shipyards that have years of experience in ship design and have a

better understanding of construction bottlenecks and resources at hand

In most cases FSRU projects enjoy the advantage of shorter permitting timelines on

account of fewer participants and affected entities involved. However, it is important to

note that such permitting timelines can be site specific

Speculation based inventory management by leading FSRU developers, long lasting

relationship with the shipyards and, in certain cases, standardized design.

Project delivery in such a relatively shorter time frame makes FSRU a very lucrative option for

developers who are running against the clock to meet acute supply shortages.

An onshore terminal project development is usually exposed to various potential bottlenecks

including site preparation, temporary material handling, labor shortages, equipment transportation,

and schedule mismatch among the various participants. These factors can significantly delay the

construction timeline and result in unexpected cost overruns.

C. Inherent flexibility offered by FSRU solution

Traditionally, there has been a lack of infrastructure to meet the needs of scattered energy

demand centers in archipelago countries like Indonesia or vast countries like Brazil and Argentina

with long coastlines. In such cases, distribution of natural gas (post LNG regasification) received at

an onshore facility through cross-country pipelines becomes cumbersome, expensive and

infeasible. In such cases, an FSRU presents the most optimal solution providing flexibility in location

(can be located as close to the demand centre as possible) and regasification capacity at a lower

cost of delivered gas. Some of the mentionable flexibility options provided by this solution are as

follows:

Page 7 of 13

Unlike a fixed onshore facility, an FSRU can be relocated and deployed according to the

need of downstream market. A good example of this can be seen in Brazil where a Golar

FSRU located in Guanabara Bay was relocated to Bahia, Salvador. The Guanabara Bay

FSRU was replaced by an Excelerate FSRU3.

In case of a seasonal gas demand profile, an FSRU can be used to supply gas during

periods when there is gas demand and during the remainder of the year it can be used

as an LNG carrier. This model has been adopted by the Kuwait National Petroleum

Company (KNPC), where the vessel is deployed as an FSRU for nine months and is free

to pursue other spot LNG opportunities for three months4.

An FSRU can act as a base-load solution for smaller demand centers or peak-shaving

solution for larger center.

FSRUs can be moved away to safety in case of a tsunami or similar natural or man-made

disasters.

D. Economic Options and Financial Incentives of an FSRU

During the early years, offshore regasification solutions were conventional, long-term and rigid,

which was likely a lender’s requirement for the unestablished market. However, over the years,

this rigidity in FSRU chartering has diminished significantly to less than five years of contract. Such

short-term chartering option facilitates the use of FSRU as a bridging solution during the

development of a land based regasification solution at the location. Such development strategies

have been seen in Chile (FSU), Egypt and Kuwait.

From an investor perspective, FSRUs have been drawing attention because of a faster return

on capital invested and a better residual value. The former depends on the utilization rate of the

FSRU (a higher utilization will result in a faster capital recovery) and the value of latter lies in the

option of re-deployment of the vessel as an LNG carrier.

Key challenges for an FSRU

As we discussed in the previous section, the opportunities that FSRUs bring to the table are

numerous and multifold. However, there are some challenges that the FSRU industry is currently

grappling with and these are discussed in the following section.

A. Metocean conditions threaten the availability of an FSRU

Meteorological and oceanic condition pose some serious challenges for the FSRU industry.

Depending on the severity of ocean conditions, LNG unloading could become one of the most

difficult tasks in FSRU operations. For side by side cargo unloading, a calm to mild sea state is

paramount, in absence of which an LNG carrier may have to wait for the ocean to return to normal

conditions before commencing safe operations. It is the same case when the FSRU is loaded with

LNG. Metocean factors can affect the send-out operations of an FSRU by disrupting the mooring

and regasified LNG connections. These factors can severely hurt the reliability and availability of an

FSRU.

An onshore plant, on the other hand, uses hard arms for unloading LNG and further onshore

operations usually escape the risk of uncertain open ocean behavior. LNG stored in onshore tanks

remains safe from the uncertain ocean and the regasification unit can meet the downstream gas

demand with more certainty and reliability.

Page 8 of 13

B. Technological challenges may limit the availability of an FSRU

In the process of ship-to-ship transfer (STS), an LNG carrier moors along-side the FSRU and

discharges LNG into the FSRU using flexible cryogenic hoses. This is still an evolving technology

and the long-term reliability of flexible cryogenic hoses in a marine environment is unproven and

is being evaluated for long life.

STS operations require benign conditions to ensure high regasification and berthing/unloading

availability.

Additionally, many of the deep-water unloading concepts such as Submerged Single/Double

Moored Buoy and Above Water Single Point Mooring – which can operate in deep water – still

remain theoretical because of the supplier’s and operator’s discomfort with implementing such a

system in deep water.

On the other hand, with years of successful operations all over the world, onshore regasification

terminals have significantly overcome most of the technological challenges. Also, industry practices

are well defined and -accepted by LNG suppliers and standards are well established and risks are

known and tested. These advantages may tend to make the onshore terminal option as the most

preferred one amongst suppliers.

C. Challenges attributed to limited deck and storage space

Another challenge faced by FSRUs is the limited deck and storage space. Unlike an onshore

facility, where future expansions can be a part of the original plan, an offshore solution suffers

from the lack of available footprint. The cheaper and relatively flexible open rack vaporizers (ORV)

used in a majority of onshore terminals may not be appropriate for an FSRU because of space

constraints. Also, Expansion of storage capacity is not straight forward once the FSRU has been

put in place.

The space constraints in an FSRU result in a much stricter firewater regulation as compared to

onshore facilities. Some other constraints which increase the design complexity of an FSRU pertain

to the storage of LNG and onboard fuel, sloshing of LNG stored in the FSRU, high pressure

regasification equipment installed onboard, mooring arrangement and transfer of LNG.

An onshore regasification facility, as compared to FSRUs, enjoys sufficient footprint – in most of

the cases – and can have flexible regasification options, warehouses, fuel storage tanks and

firewater operations. The terminal can also pre-plan expansion options and construct the necessary

expansion interface in advance to speed up such future plans. Such expansions can result in major

economies of scale for the onshore regasification plant, a feature that is unavailable in FSRUs.

Page 9 of 13

D. Challenges related to operation and maintenance

The typical cost of operation (variable cost) of an FSRU is higher than that of an onshore

terminal. The costs include the labor, crew costs, consumables, fuel and spare inventory. As

compared to an onshore terminal, the crew in an FSRU terminal is more specialized and requires

both LNG and ship operations experience. Such personnel are usually in high demand, leading to

a further escalation in operational costs. There also are additional costs associated with storage of

fuel, inventory management and disposal of processed waste – which pushes the operating costs

higher.

From the maintenance perspective, unlike in an onshore terminal, the spare parts in an offshore

terminal could be highly FSRU specific. Consequently, in case of an equipment fault in an FSRU,

the operations can suffer severe delays or send-out interruptions because the customized spare

parts may have a longer lead time.

These costs, if supplemented with limited availability of the FSRU on account of uncertain

metocean conditions, can result in higher per unit cost of operations and tends to eliminate the

advantage of low initial capital costs. For an onshore regasification plant, the processes are rather

standardized, thus resulting in significantly lower operational costs. Additionally, operational risks

are well understood and the reliability of equipment is well known.

An objective approach to assess the viability of a regasification solution

As compared to an onshore terminal, FSRU’s enjoy an inherent set of advantages. However,

the potential challenges of operating an FSRU cannot be ignored altogether. This makes it

imperative to lay-down a methodology to assess the optimum solution which aligns with the

developer’s objective while ensuring that the solution meets the current industry standards.

The decision of suitability of a development (onshore vs offshore) opportunity rests on the

fulfilment of the questions related to stakeholders’ risk appetite and return expectations, the

projects’ ability to meet the development and demand objectives, the required timeline to deliver

the development and capital requirement for the development. These considerations are explained

as below.

What is the type of demand under question?

For a project developer, it is important to understand the type of market and the demand

profile a project is expected to service. Demand of a market can have a mixture of following three

characters:

Short-term demand vs. Long term demand: Short-term demand to bridge until an

alternate solution is reached; long-term demand to develop a permanent solution.

Baseload demand vs. Peak-shaving demand: Baseload demand to meet a large

consistent gap; a peak-shaving demand to meeting acute changes in demand profile.

Yearlong demand vs. Seasonal demand: the profile of demand can be seasonal to

meet the requirements in a few high demand seasons; continuous demand profile to

meet demand in all seasons.

Page 10 of 13

Strength of an onshore terminal lies in meeting constant downstream demand and providing

continuous reliable operations, which makes it the most suitable candidate for a baseload facility.

The onshore facility also have possibility of large storage space and possibility of expansion, and

therefore, can the meet daily fluctuation of demand easily. However, an onshore facility might not

be an appropriate solution if the demand profile is not continuous or a facility requirement is short-

term or demand is scattered in the region where transporting natural gas through available

infrastructure is not feasible. Partial utilization of these onshore terminals will yield the investment

uneconomical and un-optimized.

An FSRU successfully bridges the drawbacks of an onshore facility in this regard. The inherent

flexibility of an FSRU – can be used as a regasification vessel or an LNG carrier – successfully meets

the utilization requirement if demand is seasonal. Alternatively, an FSRU can encompass the

capacity range from baseload to small scale requirement. The chartering option of an FSRU makes

the solution lucrative in case of a bridging solution. Historically there have been a few examples

where FSRUs are chartered for a short-term (under 5 years), like in Kuwait, till the permanent

regasification solutions can be developed. These advantages, however, shall be weighted properly

against the possible risks – including send-out rates and availability – that an FSRU solution can

face as discussed in the previous sections.

How fast the development has to be up and running?

An LNG project is an intricate web of agencies and participants connected with individual

timeline commitments. The supplier, the terminal developer, the aggregator, and the downstream

customer must understand the implications of project development timelines. The factors which

affect the timeline of a project are duration required to get permits, requirement of new and existing

infrastructure, and downstream gas commitments.

The project development timeline is one of the primary factors to narrow down the choice of

regasification development. A typical onshore project takes around three to five years from

permitting to starts operations, and delays in such construction timelines are rather frequent. The

reasons for such delays may include issues such as remote location, labor shortages, permitting

delays, and inspection and testing schedule mismatches.

The implications of such uncertainty in construction timelines might not be acceptable to many

participants as the bottlenecks may push the construction timelines of an onshore terminal further.

In such cases, where meeting the construction timeline at the earliest is a necessity, an onshore

regasification terminal might not be the best solution to meet the downstream demand.

On the other hand, an FSRU meets the criteria of fast and on-time implementation well. The

permitting and construction goes in parallel and it usually take a shorter timeframe for solution to

be ready (12 to 36 months). The key to faster delivery of an FSRU lies in clarity of operational

requirement. An FSRU construction happens in the shipyards in a controlled environment, and is

less likely to face a delay. However, a project developer must scrutinize the permitting timelines

and regulations well in advance to avoid roadblocks or change in design requirements.

Page 11 of 13

Whether the FSRU fits the investment strategy of the developer?

Projects in the LNG industry are capital intensive and, usually, form a part of long-term energy

strategy. Therefore, from a project developer perspective, it is important to understand the

developer’s risk appetite. The development must be scrutinized from the both country and project

risk perspective. Understanding of country risk will help the developer get comfortable with the

security of the investment, whereas the understanding of project risk will help the developer get a

feel for the investment as compared to the other projects.

An onshore regasification development, for example, is usually a part of a long-term

development strategy of a country. A high upfront investment is required in the case of such

development and the return is tied to the long-term viability and operations of the plant. The project

also faces a significant country risk because the assets developed will be immovable and, in case

of an unrest or change in demand pattern of the country, will get stranded with no residual value.

An offshore FSRU development, however, faces some relief from the above mentioned risks.

The upfront investment required, in most of the cases, is low and the vessel is mobile. This brings

the country risk down significantly as the asset will not get stranded. Another aspect of such

investment is low project risk as in case demand dries up, the vessel can be redeployed as an LNG

Carrier. However, the FSRU availability and technology risks are much higher for an FSRU as

compared to an onshore vessel.

The above mentioned risk gets morphed in a different dimension with type of project structure.

A build, own, operate and transfer (BOOT) structure for example will have different set of risk than

a build operate and transfer (BOT) structure. The perceived confidence in country’s credit will affect

the financing of these projects and eventually the expected return and investment security.

A comparative thorough assessment of the above mentioned risks between an onshore

development and an offshore development options is of utmost importance for a project developer

to ensure the security of the investment.

Conclusion

FSRUs are the new players, in the world dominated by onshore terminals, and they offer a

unique solution in the LNG regasification industry – low cost, faster delivery, location flexibility and

scale of operations – that fits the need of many countries. With the world moving towards the

cleaner hydrocarbon, FSRU presents an attractive set of opportunities which makes the option

lucrative, but the technological and commercial challenges are yet to completely overcome.

A project developer must follow a structured investigation to understand how these risks and

opportunities are applicable to the development in question, and ensure such developments are

proposed based on objective rationale and mutual benefit of all the stakeholders.

Page 12 of 13

References:

[1] International Gas Union (June 2015).

[2] Galway Regasification database and World LNG Factbook 2015.

[3] http://www.gastechnews.com/lng/petrobras-starts-up-brazils-third-fsru-import-facility/

[4] http://gcaptain.com/golar-lng-fsru-igloo-kuwait/ Kuwait Petroleum Signs Charter Contract for

Golar LNG’s Newbuild FSRU, ‘gCaptain’, 5 August 2013.

Page 13 of 13