Embed Size (px)

Citation preview

Livongo Health A Compelling Digital Health Growth Story, Initiate with an Outperform Rating

LVGO

Target price (12M, US$)

132.00

Outperform[V] Healthcare Technology & Distribution | Initiation

An Underpenetrated, Attractive TAM Driven by Growing Chronic Care Population.

We initiate coverage of Livongo, a digital health platform providing its members with

solutions for their chronic health conditions, with an Outperform rating and $132 TP.

LVGO operates in a highly underpenetrated and growing chronic care market. With a little

over $350 mln in annual rev (CS 2020 est), LVGO is barely scratching the surface in a

market which the company sizes at $46.7 bln (combined TAM for U.S. opportunities in

diabetes & hypertension). We believe this estimate is conservative for four reasons: 1)

LVGO uses chronic disease prevalence and population estimates using 2015 data, which

have moved exponentially higher today; 2) TAM does not incorporate its other solutions,

Prediabetes & Weight Management and Behavioral Health; 3) there are several other areas

of chronic care management that are largely underpenetrated where LVGO has yet to

enter; and 4) LVGO’s TAM estimates do not incorporate potential international expansion.

COVID Pulled Forward the Adoption of Remote Patient Monitoring, Opening New

Avenues of Growth. The COVID-19 pandemic has had a myriad of positive impacts on

LVGO, and others in digital health. With people with chronic conditions being most at-risk

during the pandemic, LVGO’s ability to monitor and maintain continuity of care for these

individuals and deliver a hard ROI for clients well position the company. LVGO recently

previewed its 2Q20 results above its prior expectations, setting the stage for another

upward guidance revision when reporting earnings in early August. Further, the pandemic

has accelerated LVGO’s opportunities in new markets, particularly Medicare fee-for-service,

which LVGO expects to become a growth contributor in 2021 vs. 2024-2025 pre-COVID.

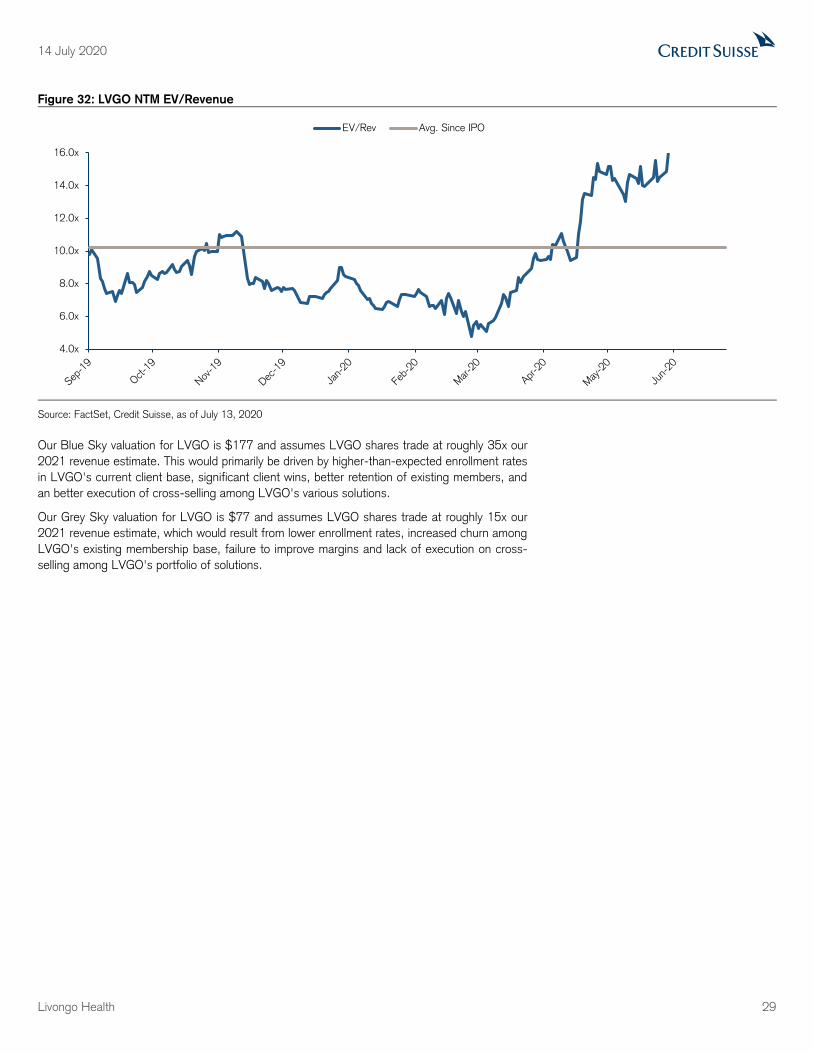

Valuation and TP. We expect LVGO shares to maintain the current one-year forward

EV/Sales multiple of ~26x 12 months from now. A 26x multiple on our 2021 rev est yields

a 12-month TP of $132, ~36% upside potential, and thus warrants an Outperform rating.

A 26x multiple, while high, is supported by the fact that comparable high growth

SaaS/HCIT companies expected to grow rev 27% Y/Y in 2021 (FactSet est) are trading

at 18.0x 2021 EV/Sales. Our 2021 rev growth estimate of 59% for LVGO is more than

double the 2021 avg rev growth rate for SaaS/HCIT companies, implying a

~1.5x premium multiple over the average is not a stretch. Risks to our rating and TP

include any major contract loss, slower enrollment rates, pricing pressure, sustaining

increase in unemployment, etc.

14 July 2020

Equity Research

Americas | United States

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS,

LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business

with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could

affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Price (13 Jul 20, US$) 97.38

52-week price range 107.56 - 15.92

Market cap (US$ m) 9,525.42

Enterprise value (US$ m) 9,446

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Jailendra Singh

212 325 8121

Jermaine Brown

212 325 8125

Adam Heussner

212 325 4727

Financial and valuation metrics

Year 12/19A 12/20E 12/21E 12/22E EPS (CS adj.) (US$) -0.39 -0.04 0.08 0.39 Prev. EPS (US$) - - - - Revenue (US$ m) 170.2 353.7 563.2 784.9 EBITDA (US$ m) -20.1 7.8 32.3 71.4 P/OCF (x) -63.4 n.m 344.2 157.4 EV/EBITDA (current) -463.4 1,202.1 288.9 130.6 Net debt (US$ m) -242 -80 -12 44 ROIC (%) -8.84 0.71 6.18 12.17

Number of shares (m) 97.82 IC (current, US$ m) 265.63 Net debt (Next Qtr., US$ m) -119.2 Dividend (current, US$) - Net debt/tot eq (Next Qtr.,%) -27.9

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 13-Jul-2020 the S&P 500 INDEX closed at 3155.22Daily

Jul25, 2019 - Jul13, 2020, 07/25/19 = US$38.1

Quarterly EPS Q1 Q2 Q3 Q4 2019A -0.48 -0.46 -0.05 0.02 2020E 0.03 0.03 -0.04 -0.07 2021E 0.02 0.01 0.02 0.03

14 July 2020

Livongo Health 2

Livongo Health (LVGO) Analyst: Jailendra Singh Price (13 Jul 2020): US$97.38 Target Price: 132.00 Rating: Outperform

Income Statement 12/19A 12/20E 12/21E 12/22E

Revenue (US$ m) 170.2 353.7 563.2 784.9

EBITDA (US$ m) (20) 8 32 71

Depr. & amort. (3) (5) (7) (9) EBIT (US$) (23) 2 25 63

Net interest exp 4 (7) (16) (16) PBT (US$) (20) (4) 9 47

Income taxes (0) 0 (0) (2) Profit after tax (20) (4) 9 44

Minorities - - - - Net profit (US$) (20) (4) 9 44

Reported net income (US$) (20) (4) 9 44

Other NPAT adjustments 0 0 0 0 Adjusted net income (20) (4) 9 44

Cash Flow 12/19A 12/20E 12/21E 12/22E

EBIT (23) 2 25 63 Net interest 4 (7) (16) (16) Change in working capital - - - - Cash flow from operations (20) 8 32 71

CAPEX (7) (14) (23) (31) Free cashflow to the firm (27) (7) 10 40

Acquisitions - - - - Divestments - - - - Cash flow from investments (7) (14) (23) (31)

Net share issue(/repurchase) - - - - Dividends paid 0 0 0 0 Changes in Net Cash/Debt 133 (162) (68) (55)

Balance Sheet (US$) 12/19A 12/20E 12/21E 12/22E

Assets Cash & cash equivalents 242 629 561 506 Account receivables 41 77 118 164 Other current assets 176 202 230 260 Total current assets 488 958 984 1,034

Total fixed assets 10 20 36 59 Investment securities - - - - Total assets 561 1,059 1,107 1,186

Liabilities Total current liabilities 42 77 117 161

Total liabilities 53 640 687 739

Total liabilities and equity 561 1,059 1,107 1,186

Net debt (242) (80) (12) 44 Per share 12/19A 12/20E 12/21E 12/22E

No. of shares (wtd avg) 51 113 114 115 CS adj. EPS (0.39) (0.04) 0.08 0.39 Prev. EPS (US$) Dividend (US$) 0.00 0.00 0.00 0.00 Free cash flow per share (0.54) (0.06) 0.09 0.35

Earnings 12/19A 12/20E 12/21E 12/22E

Sales growth (%) 148.7 107.8 59.2 39.4 EBIT growth (%) 18.9 110.4 940.6 147.9 Net profit growth (%) 27.7 78.6 319.8 378.6 EPS growth (%) 76.5 90.3 317.3 373.2 EBITDA margin (%) (11.8) 2.2 5.7 9.1 EBIT margin (%) (13.8) 0.7 4.5 8.0 Pretax margin (%) (11.6) (1.2) 1.7 6.0 Net margin (%) (11.6) (1.2) 1.7 5.7 Valuation 12/19A 12/20E 12/21E 12/22E

EV/Sales (x) 54.55 26.71 16.89 12.19 P/E (x) (251.4) (2595.9) 1194.5 252.4 Price to book (x) 9.8 26.2 26.5 25.1 Asset turnover 0.3 0.3 0.5 0.7 Returns 12/19A 12/20E 12/21E 12/22E

ROE stated-return on (%) (9.4) (0.9) 2.2 10.3 ROIC (%) (8.8) 0.7 6.2 12.2 Gearing 12/19A 12/20E 12/21E 12/22E

Net debt/equity (%) (47.6) (19.1) (2.8) 9.7 Interest coverage ratio (X) 6.3 0.4 1.6 3.9 Quarterly EPS Q1 Q2 Q3 Q4 2019A -0.48 -0.46 -0.05 0.02 2020E 0.03 0.03 -0.04 -0.07 2021E 0.02 0.01 0.02 0.03

Company Background

Livongo operates a digital health platform focused on people with chronic

conditions. The company leverages data science and technology to create

a personalized experience for the member to encourage healthy behavior

and to ultimately save costs.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 177.00

Our Blue Sky valuation for LVGO is $177 and assumes LVGO shares

trade at roughly 35x our 2021 revenue estimate. This would primarily be

driven by higher-than-expected enrollment rates in LVGO's current client

base, significant client wins, better retention of existing members, and an

better execution of cross-selling among LVGO's various solutions.

Our Grey Sky Scenario (US$) 77.00

Our Grey Sky valuation for LVGO is $77 and assumes LVGO shares

trade at roughly 15x our 2021 revenue estimate, which would result from

lower enrollment rates, increased churn among LVGO's existing

membership base, failure to improve margins and lack of execution on

cross-selling among LVGO's portfolio of solutions.

Share price performance

On 13-Jul-2020 the S&P 500 INDEX closed at 3155.22

Daily Jul25, 2019 - Jul13, 2020, 07/25/19 = US$38.1

Source: Company data, Refinitiv, Credit Suisse estimates

14 July 2020

Livongo Health 3

Table of Contents

Key Charts 4

Executive Summary 5

Overarching Chronic Disease Trends .............................................................................. 5

Conservative Total Addressable Market ........................................................................... 5

A Sticky Platform with a Highly Attractive B2B2C go-to-market Strategy .......................... 5

AI+AI Data Engine Drives Real Hard ROI for LVGO’s Clients ............................................ 6

COVID-19 Pulled Forward the RPM Adoption ................................................................. 6

Valuation and Price Target ............................................................................................. 6

Investment Themes 7

Focused on the Largest Health Care Problems in the U.S. ............................................... 7

Attractive TAM With a Long Runway for Growth .............................................................. 9

Compelling Multi-channel B2B2C Go-to-Market Strategy ............................................... 11

Cross-Selling Opportunities .......................................................................................... 15

A Sticky Healthcare-as-a-Service (HaaS) Platform ........................................................ 16

COVID-19 Pulled Forward the RPM Adoption ............................................................... 17

New Payment Models Create Tailwind for LVGO ........................................................... 19

AI+AI Data Engine a Core Component of LVGO’s Competitive Strategy .......................... 21

Measurable Outcomes Bring Hard ROI for Clients.......................................................... 22

Recent Notable Clients Wins and Opportunities ............................................................. 23

Strong Financial Performance ...................................................................................... 24

Investment Risks 25

Exposure to High Unemployment Rate .......................................................................... 25

Channel Partners’ Influence on Revenue ....................................................................... 25

A New, But Rapidly Growing Market Brings Competition ................................................ 25

CGM Vendors & Device Manufacturers ......................................................................... 26

Health Insurers Offering Own Digital Care Programs ...................................................... 26

Price Performance and Valuation 27

Company Overview 30

Solution Overview ........................................................................................................ 30

Margin Expansion Opportunity Through CGMs ............................................................... 31

Business Model .......................................................................................................... 31

Financials 33

14 July 2020

Livongo Health 4

Key Charts

Figure 1: LVGO Revenue Growth Figure 2: LT Target Margins

Source: Company data, Credit Suisse estimates Source: Company data, Reflects average of LT targets, *Operating margin: +20%

Figure 3: Estimated Value of Agreements Figure 4: Diabetes Market Remains Largely Untapped by LVGO

Source: Company data Source: Company data, Credit Suisse, Based on 1Q20 Livongo Enrolled Diabetes

Members

$31 $68

$170

$354

$563

$785

$1,027

2017 2018 2019 2020E 2021E 2022E 2023E

$77.2

$11.3

$24.8

$62.3$56.1

$48.1

$74.2

$85.5

$76.7

$89.0

4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20

LVGO Diabetes Members: 1.04%

31.4 mln U.S. Adults With

Diabetes

14 July 2020

Livongo Health 5

Executive Summary

We are initiating coverage of Livongo (LVGO) with an Outperform rating and a $132

price target.

Overarching Chronic Disease Trends

Livongo (LVGO) stands to benefit from a healthcare industry that is becoming more connected

with the patient and the focus of employers and health plans to save costs. LVGO is focused on

improving the lives of people with chronic conditions through its consumer digital health platform

that provides over-the-air updatable devices, informed coaching, data science-enabled insights,

and facilitates access to medications across multiple chronic conditions. Currently, LVGO’s

solutions are available for those with diabetes, hypertension, pre-diabetes & weight

management, and behavioral health. LVGO sells its core Livongo for Diabetes solution on a

pure SaaS basis, which results in LVGO being able to cite a 90% visibility into future revenue.

As of 3/31/2020, LVGO had over 328k enrolled diabetes members on its platform, which

represents around 1% penetration when considering that there are over 31 mln insured people

in the U.S. living with diabetes. Further, according to the American Diabetes Association, 1.5

mln Americans are diagnosed with diabetes every year, representing an ongoing opportunity for

LVGO to capture new members. Chronic conditions go beyond just diabetes, however.

According to the CDC – going back to 2014 – 90% of the $3.5 trln in healthcare expenditures

were for people with chronic and mental health conditions. Though LVGO was built on helping

people with diabetes, the company has expanded its offerings to include weight management

and pre-diabetes, management of hypertension, and its most recent product launch (via

acquisition of myStrength) of behavioral health. With 70% of people with Type 2 diabetes

struggling with hypertension, and over 50% of those with Type 2 having a weight management

issue, LVGO is well-positioned to leverage its core Diabetes management platform to enable

those living with comorbidities to live better lives.

Conservative Total Addressable Market

LVGO sizes its total addressable market in the U.S. for the diabetes management solution at

$28.2 bln (based on 31.4 mln adults with diagnosed/undiagnosed diabetes and LVGO’s

annualized $75 Per Participant Per Month (PPPM) list price). For hypertension, LVGO

estimates an addressable market in the U.S. of $18.5 bln (based on 39.6 mln adults with

hypertension who do not also have diabetes, which is known to be about 74%, and LVGO’s

annualized $39 PPPM list price). Between diabetes and hypertension, LVGO operates in a

$46.7 bln TAM. We believe this estimate is conservative for four reasons: 1) LVGO uses

chronic disease prevalence and population estimates using 2015 data, which have moved

exponentially higher today; 2) TAM does not incorporate its other solutions, Prediabetes &

Weight Management & Behavioral Health; 3) There are several other areas of chronic care

management that are largely underpenetrated where LVGO has yet to enter; and 4) LVGO’s

TAM estimates do not incorporate potential international expansion.

A Sticky Platform with a Highly Attractive B2B2C go-

to-market Strategy

Livongo utilizes a B2B2C go-to-market strategy where it sells its platform to employers, health

plans/payors, health systems, labor unions, and government entities. LVGO currently has over

30% of Fortune 500 companies as clients. Unlike other benefit plan solutions where a company

might pay for its entire employee population to have access, employers and other LVGO clients

only pay for the subsets of their populations that are at-risk and who actually use the solution.

LVGO operates a sticky platform, which is evident by a 2-3% average monthly member attrition

(driven primarily by members losing eligibility because of change in employer). Only a small portion

(~6%) of LVGO’s churn comes from clients deciding to terminate their contract with LVGO.

14 July 2020

Livongo Health 6

AI+AI Data Engine Drives Real Hard ROI for LVGO’s

Clients

The value in LVGO’s platform comes via its use of Applied Health Signals (e.g., blood pressure

checks, weight scale readings, blood glucose checks, etc.) to capture and then translate data

into actionable, personalized and timely signals to improve the lives of those with chronic

medical conditions, both medically and financially. The core of LVGO’s strategy is in its AI+AI

(which stands for Aggregate & Interpret, Apply & Iterate) Data Engine, where it takes over 500

mln data points and runs them against algorithms to help coach members on a clinical basis.

COVID-19 Pulled Forward the RPM Adoption

COVID-19 has resulted in a pull-forward of adoption of remote patient monitoring through

actions taken by various regulatory bodies. With people with chronic conditions most at risk

during the current pandemic, LVGO’s solutions have seen increased interest. Additionally,

LVGO is also seeing increased enrollment from clients already in LVGO’s portfolio via patients

looking to maintain some degree of care for their chronic condition and not being able/willing to

see a doctor in person, with a solution that is free of charge from their employer/health plan.

Further, as a result of CMS changing billable CPT codes specific to remote patient monitoring,

it has allowed LVGO to accelerate the penetration of the Medicare fee-for-service market.

LVGO is still in early stages in providing its RPM solutions to health systems, though the

company does have pilot programs in place in several health systems across the country.

Valuation and Price Target

Following LVGO’s IPO in July 2019, shares declined 34.2% in 2019, but have surged 289%

YTD in 2020 as COVID-19 has put a spotlight on companies in the digital healthcare market

and solutions with the ability to monitor patients remotely.

The primary valuation metric we use to value LVGO shares is EV/Sales primarily due to the

company’s growth profile and limited history of positive earnings. On an EV/Sales metric, LVGO

shares currently trade at approximately 25.9x our 2020 revenue estimate and 16.3x our 2021

revenue estimate. When compared with a mix of similar top-line growth profile software-as-a-

service (SaaS) and healthcare technology companies, LVGO trades at a discounted valuation

relative to the group average (16.3x our 2021 revenue estimate vs the group average of 18.0x),

despite a Y/Y revenue growth expectation of 59% in 2021, double the average revenue growth

expectation of 27% for the group.

We expect LVGO shares to maintain its current EV/Sales multiple of 26x one year from now. A

26x on our 2021 revenue estimate for LVGO yields a 12-month TP of $132. A $132 price

target would imply roughly 36% upside potential from the current levels, and thus an

Outperform rating. Risks to our rating and TP include any major contract loss, slower enrollment

rates, pricing pressure, sustaining increase in unemployment, etc.

14 July 2020

Livongo Health 7

Investment Themes

Focused on the Largest Health Care Problems in the

U.S.

According to the CDC, 6 in 10 adults in the U.S. have a chronic disease while 4 in 10 adults

are living with 2+ chronic diseases. Out of the $3.5 trillion spent on U.S. healthcare in 2017,

around 90% was attributable to people with chronic and mental health conditions.

More than 30 million people in the U.S. have diabetes, and 1 in 4 of them don’t know they have

it. More than 84 million U.S. adults have prediabetes, and 90% of them don’t know they have it.

Prediabetes is a serious health condition in which blood sugar levels are higher than normal, but

not high enough yet to be diagnosed as type 2 diabetes. A person with prediabetes is at high

risk of type 2 diabetes, heart disease, and stroke. Being overweight, being age 45 or older, and

being physically active less than 3 times a week are risk factors for prediabetes and type 2

diabetes. Based on a study conducted by the American Diabetes Association, the total cost of

diabetes in the U.S. was $327 billion in 2017, including $237 billion in direct medical costs and

$90 billion in reduced productivity. On average, people with diagnosed diabetes incur medical

expenditures of $16.7K per year, of which about $9.6K is attributed to diabetes. Also, people

with diagnosed diabetes have medical expenditures approximately 2.3x higher than what

expenditures would be in the absence of diabetes. Separately, according to the American

Diabetes Association, the cost of prediabetes was about $43 billion in 2017.

High blood pressure is one of the most prevalent health conditions facing Americans today with

roughly half of the U.S. population (108 million) living with a systolic blood pressure ≥ 130 mm

Hg or a diastolic blood pressure ≥ 80 mm Hg or are taking medication for hypertension. Only 1

in 4 adults with hypertension have their condition under control. In terms of cost in the U.S.,

around $131 billion is attributed to high blood pressure.

Approximately 40% of Americans are considered to be obese, which results in a higher risk of

developing other chronic conditions such as diabetes, heart disease, as well as cancer. The

estimated annual medical cost of obesity in the U.S. was $147 billion. The prevalence of

obesity in the U.S. has also been increasing over the past 20 years as the age-adjusted

prevalence in obesity increased from 30.5% in 1999-2000 to 42.4% in 2017-2018. In

addition, the prevalence of severe obesity has more than doubled over the same period, growing

from 4.7% to 9.2%.

Figure 5: Age-Adjusted Prevalence of Obesity & Severe Obesity in the U.S.

Source: NCHS, National Health and Nutrition Examination Survey, 1999–2018

30.5% 30.5%32.2%

34.3% 33.7%35.7% 34.9%

37.7%39.6%

42.4%

4.7% 5.1% 4.8% 5.9% 5.7% 6.3% 6.4% 7.7% 7.7% 9.2%

1999-2000 2001-2002 2003-2004 2005-2006 2007-2008 2009-2010 2011-2012 2013-2014 2015-2016 2017-2018

Obesity Severe Obesity

14 July 2020

Livongo Health 8

According to the National Institute of Mental Health, an estimated 46.6 million adults (18.9% of

all U.S. adults) in the U.S. had a mental illness in 2017. In addition, there was an estimated

11.2 million adults (4.5% of all U.S. adults) with a serious mental illness in 2017. However,

mental illness is not only prevalent, it is also costly. For instance, according to the National

Alliance on Mental Illness, mental illness costs the U.S. an estimated $300 billion per year. The

treatment of mental health cannot be thought of in isolation, however, as mental disease is

correlated with other chronic conditions, such as heart condition, diabetes, hypertension, etc.

Figure 6: Prevalence of Comorbid Health Conditions Among Nonelderly Adults with

Mental Illness, 2015

Source: Kaiser Family Foundation, Credit Suisse

Livongo operates a digital health platform geared toward helping its members with chronic

conditions live better, healthier lives while at the same time reducing the cost burden of

employers, health plans, and the entire healthcare system. LVGO is built around its core product,

Livongo for Diabetes, a solution that offers members a cellular-connected blood glucose meter,

unlimited blood glucose test strips, personalized Health Nudges that prompt members to take

action on their health, digital tools across mobile, web, and email, as well as coaching and

monitoring. While LVGO is still heavily concentrated in its marquee diabetes management

solution, the company has expanded its product offering to include Livongo for Prediabetes &

Weight Management, Livongo for Hypertension, and most recently through its acquisition of

myStrength in Feb 2019, myStrength for Behavioral Health. LVGO’s suite of solutions share a

common data structure and are all delivered through a common user interface, multi-channel

applications for management of conditions, and a cross-condition integrated coaching model.

Importantly, each of LVGO’s four solutions can be used alone or in tandem with one another.

LVGO generates around 90-95% of its revenue from monthly subscription fees, but the

company does recognize a small portion of revenue from the sale of connected devices, which

tend to be more apparent in revenue contribution in the 1H of the year as clients are launched

onto the platform and members begin to enroll. In addition, LVGO also has a small portion of at-

risk revenue based on performance metrics (e.g., clinical improvement in A1C scores, weight

loss improvement, Net Promoter Scores, etc.). If LVGO were to not hit a certain performance

metric, instead of generating incremental revenue, the company would be forced to provide a

credit to the client. However, LVGO is experiencing that clients are wanting to incorporate these

performance-based metrics into contracts much less relative to 3-4 years ago, which can be

explained by LVGO’s solutions proven capabilities and better brand recognition now. Clients

have ended up paying more when a performance-based metric is involved because of the

results LVGO is able to consistently deliver. LVGO is still open to incorporate a variable revenue

component into contracts if a client wants it.

10% 10%

20%

15%

20%

Heart Condition Diabetes Hypertension Asthma Substance

Abuse/Addiction

14 July 2020

Livongo Health 9

Figure 7: Livongo Product Overview

Solution

Pricing

Model

Built vs

Bought

Launch/Acquisition

Date

Diabetes

~$75 PPPM Built Sep-14

Prediabetes & Weight

Management

~$35 PPPM Bought Apr-18

Hypertension

~$39 PPPM Built Aug-18

Behavioral Health by

myStrength

$LSDs PMPM

Bought Feb-19

Source: Company data, Credit Suisse, PPPM: Per-Participant-Per-Month, PMPM: Per-Member-Per-Month

Attractive TAM With a Long Runway for Growth

LVGO sizes its total addressable market in the U.S. for its diabetes management solution at

$28.2 bln (based on 31.4 mln adults with diagnosed/undiagnosed diabetes and LVGO’s

annualized $75 PPPM list price). For hypertension, LVGO estimates an addressable market in

the U.S. of $18.5 bln (based on 39.6 mln adults with hypertension who do not also have

diabetes, which is known to be about 74%, and LVGO’s annualized $39 PPPM list price).

Between diabetes and hypertension, LVGO operates in a $46.7 bln total addressable market.

Notably, due to limitations on the availability of data for both diabetes and hypertension, the total

addressable market of $46.7 bln cited by LVGO is based on chronic disease prevalence and

population estimates as of 2015. Therefore, it is likely the addressable market for these two

solutions has increased since then.

Further, LVGO’s cited TAM does not incorporate other solutions of pre-diabetes & weight

management or the myStrength Behavioral Health solution.

Figure 8: Breakdown of Diabetes & Hypertension Total Addressable Markets

Diabetes

Insured Lives LVGO List Price (PPPY) Addressable Market TAM

Employer Coverage 13.7 M $900 $12.3 B $28.2 B

Medicare/Medicaid 17.7 M $900 $15.9 B

Hypertension

Insured Lives LVGO List Price (PPPY) Addressable Market TAM

Employer Coverage 27.4 M $468 $12.8 B $18.5 B

Medicare/Medicaid 12.2 M $468 $5.7 B

Source: Company data, Credit Suisse estimates

LVGO has historically focused on the self-insured employer market where the company has had

success as employers look to save money on the most costly subsets of their employee

populations. However, LVGO also has an opportunity to go after other markets in need of cost-

savings and better outcomes. As more and more clients receive positive ROIs and better

outcomes, we see LVGO becoming more successful in winning business in the fully insured

employer/commercial health plan markets as well. Based on estimates of prevalence in insured

populations, we see a largely unaddressed market for LVGO to penetrate.

14 July 2020

Livongo Health 10

Figure 9: Underpenetrated Markets to Go After

Source: Company data, Kaiser, Credit Suisse

Given diabetes management is LVGO’s foundational pillar, we see the company as likely to roll

out additional solutions that are commonly correlated with those living with type 2 diabetes. For

example, for people living with type 2 diabetes, 73.6% have hypertension, 87.5% are

overweight/obese, 75.2% have hyperlipidemia, 36.5% have chronic kidney disease, and

32.2% have a cardiovascular disease. According to a Rand Corporation study on chronic

conditions, 27% of U.S. adults have hypertension while 21.6% are living with lipid disorders

(e.g., high cholesterol). Based on recent commentary by LVGO management, the company

plans on rolling out a solution for people with high cholesterol by the end of the year with other

areas on LVGO’s roadmap to further growth. Therefore, LVGO’s cited TAM is likely to expand

as the company enters new chronic care markets, in addition to the company’s TAM for

diabetes/hypertension as the population of persons living with the conditions increase.

Figure 10: Prevalence of Top Chronic Conditions (2014)

Source: Rand Corporation, Credit Suisse

International expansion provides LVGO further opportunity to expand its TAM, as chronic

conditions are not exclusive to the U.S. market. According to the International Diabetes

Federation, there were around 463 mln adults (age 20-79) globally living with diabetes, with

50% of people with diabetes being undiagnosed. However, by 2030, the number of people with

diabetes is expected to rise to 578 mln and by 2045 is expected to hit over 700 mln people.

With zero international exposure currently, international expansion for LVGO represents a large

runway for future growth given the expected increases in persons living with diabetes as well as

LVGO’s straightforward pricing model, which should allow the company to integrate with many

of the healthcare systems abroad. Management has noted that the company is likely to begin

expansion into international markets in countries where English is the language of medicine.

99 mln

64 mln 58 mln

36 mln24 mln

Prevalence: 8%

Prevalence: 9%Prevalence: 8%

Prevalence: 25%

Prevalence: 25%

Self-Insured

Employers

Medicaid Fully-Insured

Employers

Medicare FFS Medicare

Advantage

27.0%

21.6%

11.9%10.4% 9.7%

7.4% 7.4% 6.5% 6.3%4.8%

Hypertension Lipid disorders

(e.g., high

cholesterol)

Mood disorders

(e.g.,

depression,

bipolar disorder)

Diabetes

mellitus

Anxiety

disorders

Other upper

respiratory

disorders

Inflammatory

joint disorders

(other than

arthritis)

Osteoarthritis Asthma Coronary

atherosclerosis

and other heart

disease

14 July 2020

Livongo Health 11

Figure 11: Persons with Diabetes Globally

Source: International Diabetes Federation, Credit Suisse

Compelling Multi-channel B2B2C Go-to-Market Strategy

Livongo utilizes a B2B2C go-to-market strategy where it sells its platform to employers, health

plans/payors, health systems, labor unions, and government entities. Ultimately, LVGO looks to

sell its platform and services to anyone who has risk for the underlying population. LVGO

currently has over 30% of Fortune 500 companies as clients. Unlike other benefit plan solutions

where a company might pay for its entire employee population to have access, employers and

other LVGO clients only pay for the subsets of their populations that are at-risk and who actually

use the solution.

LVGO sells its solutions through its direct sales force in addition to relying on a limited number

of channel partners and resellers. These channel partners, which are made up of pharmacy

benefit managers (PBMs), health plans, and other resellers, speed up the process for LVGO in

gaining access to potential clients. In exchange for the increased speed and access the channel

partners provide, LVGO gives up a HSD% of top-line revenue in commission expenses. From

an accounting standpoint, in situations where LVGO utilizes a channel partner to obtain a client,

revenue would be recognized on a gross basis and the fee paid to the channel partner

recognized as commission expense in sales and marketing. The fee paid to channel partners

can be thought of as a revenue share arrangement as it is based on a percentage of revenue on

an ongoing basis.

For 2019, LVGO disclosed that sales generated through its top five channel partners (i.e.,

Express Scripts, CVS, Health Care Service Corporation, Anthem, and Highmark) represented

61.3% of revenue. The agreements with LVGO’s channel partners/resellers are on a non-

exclusive basis, and as such, they may refer business to competitors other than LVGO. LVGO

nonetheless maintains strong relationships with each of its channel partners due to the

evidence-based outcomes LVGO is able to deliver for its members. For example, LVGO is

Express Scripts’ only preferred provider for its digital health formulary, where Express Scripts

takes on risk, pointing to the financial ROI LVGO drives. Additionally, LVGO recently received

preferred status within Express Scripts’ new Health Connect 360 solution, which is the

industry’s first outcomes-based model that centers on engaging people in their care.

References to “clients” for LVGO include only contractually signed and paying clients. As such,

during the ~3 month ramp that it takes upon contract signing with a commercial client until

service launch, LVGO would not count that newly signed client in its membership base.

151194

246285

366 382415 425

463

578

700

2000 2003 2006 2009 2011 2013 2015 2017 2019 2030E2045E

14 July 2020

Livongo Health 12

LVGO refers to Estimated Value of Agreements (previously referred to as Total Contract Value,

or TCV) as contractually committed orders to be invoiced under agreements that were entered

into during the reporting period. For purposes of EVA, LVGO assumes an average member

enrollment rate in addition to making certain assumptions over the total number of recruitable

individuals at a client, commencement of the enrollment period, enrollment method, starting

enrollment rates, monthly increases to enrollment rates, contract length, and client size/industry.

Notably, until LVGO actually begins invoicing the client, amounts reflected in EVA do not show

up in deferred revenue, revenue, or anywhere else in the financial statements. Accordingly, EVA

should be thought of as the top of the funnel for where LVGO begins a path to revenue

generation.

LVGO currently experiences a 35% average enrollment rate in its diabetes management

solution with some of its best clients reaching a 50% enrollment rate for eligible populations. It

takes ~9 months to reach the average 35% enrollment run rate for a population due to the time

it takes for LVGO’s marketing and outreach initiatives to take effect. As a result, it takes ~12

months from contract signing to reach the full 35% average enrollment rate (e.g., 3 months

from contract signing until service launch and 9 months from service launch until run rate

enrollment). When LVGO is able to deploy an optimal outreach strategy, characterized by having

more availability to data, what is known about potential members, and how the company is

allowed to reach out to them, LVGO believes it can reach a 70% optimal enrollment rate.

Figure 12: EVA – Client – Members

Source: Company data

Figure 13: Estimated Value of Agreements (EVA)

Source: Company data

LVGO refers to clients as business entities having at least one active paid contract with the

company. Entities that utilize LVGO’s platform, but come through LVGO’s channel partners

(e.g., PBMs, resellers, etc.) are counted as individual clients. Prior to 1Q20, LVGO treated

multiple employers who contracted for LVGO’s services through a single health plan, as a single

client given the relatively small number of employers who were enrolling through health plans.

However, because of the increase in the number of employers enrolling through health plans

EVA

• Skews toward 2H as benefit plans are established

• Takes <6 months on Avg from initial outreach to signed contract

Client

• Represents signed & paying clients

• Additions skew toward 1H

• ~3 months on Avg from contract signing to enrollment initiation

Members

• Represents active employees/members & dependents on the LVGO platform

• Additions skew toward 1H

• ~9 months to full enrollment

$77.2

$11.3

$24.8

$62.3$56.1

$48.1

$74.2$85.5

$76.7

$89.0

4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20

14 July 2020

Livongo Health 13

instead of through other channels, LVGO now treats each entity that enrolls in the platform as a

separate client. Notably, along with this change, LVGO now treats health plans similar to how it

treats its channel partners, where they are counted as a client only if they also have an active

paid contract to use one of LVGO’s solutions.

Figure 14: Client Growth

Source: Company data

LVGO’s initial and primary solution is focused on the management of diabetes, one of the

fastest-growing chronic conditions in the world. LVGO defines Enrolled Diabetes Members as

all individuals that are enrolled in the Livongo for Diabetes solution at the end of the period.

Notably, the number of enrollees excludes: 1) employees or dependents of a client that have

ceased using the solution; 2) employees who no longer have an employment relationship with

an active client, and their dependents, and 3) employees/dependents who have not been active

on or used the solution for a period of time (specific in each client agreement), which is typically

between 4 and 6 months. Further, the number of Enrolled Diabetes Members does not include

employees/members of LVGO’s other three solutions (e.g., hypertension, prediabetes & weight

management, and behavioral health), which do not have the scale as that of the core diabetes

management solution, but serve as an important runway for growth going forward.

LVGO tends to sign more clients in the 2H of the year, which will show up in the company’s

Estimated Value of Agreements (EVA) metric, as companies decide which benefits to add

ahead of open enrollment season. Being that it takes ~2-3 months from contract signing until

service launch for commercial clients, additions to the number of reported clients and enrolled

diabetes members tend to skew toward the 1H of the year as prior period signings begin to

launch. However, LVGO is still able to sell all year long as its services are not necessarily tied to

the benefits season. For health plans in particular, it takes around 6-9 months after signing for

the enrollment period to begin, with a majority of enrollment periods for health plan clients

beginning in either January or July.

Without factoring any additional growth in enrolled diabetes members – taking LVGO’s 328K

members at the end of 1Q20 – and assuming an enrollment rate of 45% across LVGO’s entire

book, it would equate to an incremental ~$85 mln in annual revenue based on LVGO’s $75

PPPM list price for its diabetes solution. Given that LVGO is unlikely to operate at a 70%

targeted optimal enrollment rate across its whole book of business, as a result of differences in

outreach to varying client types, we see a 45% enrollment rate after 9 months since client

launch being an attainable target in the medium term. As LVGO becomes more sophisticated

with its enrollment and marketing strategy using its AI+AI engine, collecting further data around

populations and determining the optimal outreach approach, we see believe LVGO having a

large opportunity to drive top-line growth organically. Further, LVGO recently entered into an

agreement with one of its channel partners that allows the company to access all available

emails from their joint clients, providing another pathway to improve member outreach and drive

enrollment rates.

5 30100

218

413

872

1,252

2014 2015 2016 2017 2018 2019 1Q20

14 July 2020

Livongo Health 14

Figure 15: LVGO for Diabetes Enrollment Rates

Source: Company data, Credit Suisse estimate: 45% enrollment after ~9 months of client launch

(attainable within 3-5 years)

From 2014 to 1Q20, enrolled diabetes members have grown at a 185% CAGR while blood

glucose checks among LVGO’s diabetes members have grown at a 315% CAGR. We believe

this highlights the ability by LVGO to better engage with members through health nudges and

coaching the longer people are on the platform and through the enhancement of LVGO’s AI+AI

engine.

Figure 16: Enrolled Diabetes Members & Blood Glucose Checks

Source: Company data, Credit Suisse estimates

Once LVGO inks the deal with a client, the company begins working with the client to identify

the full population who may be eligible to enroll in the solution. LVGO utilizes a personalized and

targeted marketing strategy to notify potential members of their eligibility to enroll in the solution

and encourage them to sign up, which include email, direct mail, and company communications.

As a result of LVGO’s go-to market strategy, the company ends up selling its solution twice: 1)

to the employer, health plan, etc., and 2) to the employee/member encouraging them to enroll

in LVGO’s platform. And since LVGO only gets paid in its core diabetes management solution

for the subset of the at-risk populations it enrolls, the company is keenly focused on optimizing

enrollment.

27%

34% 35%

45%

2017 2018 2019 Estimate

0.6k 6k20k

54.0k

113.9k

222.7k

328.5k

1 mln 3 mln

12 mln

31 mln

73 mln

87 mln

0k

50k

100k

150k

200k

250k

300k

2014 2015 2016 2017 2018 2019 1Q20

0 mln

10 mln

20 mln

30 mln

40 mln

50 mln

60 mln

70 mln

80 mln

90 mln

Enrolled Diabetes Members Blood Glucose Checks

CAGR: 185% CAGR: 315%

14 July 2020

Livongo Health 15

LVGO not only uses its AI+AI Data Engine to create a more personalized experience for people

with chronic conditions, but also uses data science and technology to drive member enrollment.

As LVGO is primarily compensated based on the number of participants in its solution (i.e.,

PPPM), a successful marketing and enrollment strategy is paramount even beyond the contract

signing with the client. Leveraging the AI+AI engine, LVGO is able to test and iterate

messaging and other communications in various channels to drive better results.

Cross-Selling Opportunities

Livongo has continued to increase penetration of existing clients as well as attract new clients

outside of its core diabetes management platform, highlighted by 18% of LVGO’s clients having

purchased more than one solution from Livongo as of 1Q20, compared to just 4% of clients as

of 4Q18. Further, 20% of LVGO’s 3Q19 EVA of $85.53 mln (or ~$17 mln) and 35% of the

4Q19 EVA of $76.67 mln (or ~$27 mln) was for solutions other than the diabetes platform,

highlighting an increasing ability to cross-sell among solutions.

Figure 17: Percentage of LVGO Clients Purchasing Multiple Solutions

Source: Company data, Credit Suisse

By building out a portfolio of solutions aimed at covering the whole person and their care, LVGO

is able to offer an end-to-end client experience from implementation through reporting and

billing. And since all LVGO solutions are powered by the underlying AI+AI data engine, each

interface with a member is able to further feed the algorithm contributing to a valuable flywheel

effect able to provide members with better guidance over time for their health.

Figure 18: Supporting the Whole Person

Source: Company data

4%

14%

18%

4Q18 4Q19 1Q20

14 July 2020

Livongo Health 16

Using LVGO’s 1Q20 enrolled diabetes membership base and applying estimates of

comorbidities among people with diabetes, we see an annual revenue opportunity for LVGO’s

hypertension, prediabetes & weight management, and behavioral health solutions of around

$280 mln. However, LVGO is unlikely to penetrate additional solutions into its existing diabetes

membership base at the exact percentage of people living with multiple solutions. LVGO has

begun offering bundled packages of multiple solutions at reduced rates to clients in order to

take care of the “whole person,” which comes at a discounted rate and would therefore alter the

revenue opportunity for clients stacking multiple solutions for their populations.

Figure 19: Cross-Selling Revenue Opportunity

1Q20 Enrollment

LVGO for Diabetes 328.5K

Condition

% of People that

have diabetes AND

Annual

Fee

Relevant

Population

Annual Rev

Opportunity Note

Hypertension 70% $468 230K $108 mln

Overweight/Obese 85% $600 279K $168 mln 30% of overweight people have diabetes, and 85% of

diabetics are overweight

Mental Health/Depression 42% $36 136K $5 mln In any 18-month period, 33% to 50% of people with diabetes have diabetes distress.

Source: Company data, CDC, Harvard

A Sticky Healthcare-as-a-Service (HaaS) Platform

LVGO operates a sticky platform, which is evident by the 2-3% average monthly member

attrition. By way of background, LVGO calculates its monthly member churn by looking at the

members who were on the platform at the beginning of each month, subtracting the number of

those members still on the solution at the end of the month, and dividing that number by the

starting member number for such month. Then, to get the average monthly member churn

(which LVGO reports to be ~2-3%), the average of all twelve months of churn is taken.

The vast majority of LVGO’s 2-3% average monthly churn comes from members losing

eligibility, which would occur when a member leaves their current employer, followed by around

20% of churn occurring due to lapsed use of the service, where a member is no longer deemed

to be active on the platform, which depends on each client agreement, but is typically between

4 and 6 months of non-activity. Lastly, a small portion (~6%) of LVGO’s churn comes from

clients deciding to terminate their contracts with LVGO.

Figure 20: Components of Member Churn (based on 2018 data)

Source: Company data, Credit Suisse

Though 2-3% of existing membership churning out each month may be alarming at first, the

most significant reason for member churn comes as a result of the underlying turnover of

employees at LVGO’s clients. In addition, LVGO has averaged a 95% client retention rate over

the past two years (94.2% in 2018 and 95.9% in 2019), which is a more important metric to

74%

20%

6%

Members Losing Eligibility Lapsed Use by Members Client Contract Terminations

14 July 2020

Livongo Health 17

track because even if there is employee turnover at the client, as long as LVGO maintains the

contract with that client, they are able to target new employees who may be eligible to enroll in

a LVGO solution.

Another important variable in thinking about LVGO’s overall retention and performance at the

client level is the company’s dollar-based net expansion rate, which takes the monthly service

revenue at the end of the period for a set of clients (where LVGO generated monthly service

revenue 2 years prior to the calculation date) and divided by the monthly service revenue one

year prior to the calculation date for the same set of clients. The monthly service revenue is

calculated as the monthly fee for the LVGO for Diabetes and LVGO for Hypertension solutions,

multiplied by the number of active members who were on or used the solution. For 2019, the

dollar-based net expansion rate was 111.5% and for 2018 it was 113.8%. As a result, LVGO

has shown the ability to add members at clients at a rate that surpasses any attrition due to

underlying employee turnover or change in benefits.

Similar to other SaaS model companies, LVGO operates at a negative contribution margin in

year one of solution rollout after taking into account cost of devices and other direct costs

before turning to profitability in the second year of service. Note, however, that LVGO has

witnessed significant growth since 2016, and as such, we believe that the actual contribution

margins may be better than as depicted below given the company’s improved enrollment efforts

and continued scalability of its AI+AI engine.

Figure 21: LVGO Contribution Margin Overview (2016 Cohort)

Source: Company data, Credit Suisse

COVID-19 Pulled Forward the RPM Adoption

Similar to the impact COVID-19 has had on the telehealth industry, so too has the pandemic

resulted in a pull-forward of adoption of remote patient monitoring through actions taken by

various regulatory bodies. For example, the Federal Drug Administration (FDA) granted an

emergency period waiver to allow any inpatient facility in the United States to use LVGO’s

cellular-enabled diabetes meter, allowing people with COVID-19 to monitor their blood glucose

levels within the hospital inpatient setting. As personal protective equipment (PPE) has been in

high demand and supply has been a key issue in fighting the pandemic, the ability for a patient

to use LVGO’s hardware and have the data automatically transmitted to the cloud allows

healthcare providers to continually monitor patients with diabetes all while saving PPE for other

purposes. Outside of this emergency period offering, LVGO does not sell into the inpatient

setting, and has no plans to. However, LVGO has shown the flexibility of its solutions to meet

member/client needs whatever they might be.

$3.7

$12.8 $15.7

($7.15) ($5.40) ($6.20)

-92%

58%61%

-95%

-75%

-55%

-35%

-15%

5%

25%

45%

65%

($10)

($5)

$0

$5

$10

$15

$20

2016 2017 2018

Revenue Variable Costs Contribution Margin %

14 July 2020

Livongo Health 18

The sharp decline in patient visit volumes across the United States, and internationally, has

resulted in patients not receiving the proper treatment and diagnosis that would have otherwise

occurred without COVID-19. In addition, people with chronic conditions are most notably at risk

during the current pandemic as hospitalizations have been six times higher and deaths twelve

times higher for COVID-19 patients with reported underlying conditions, particularly patients

with diabetes, cardiovascular disease, and chronic lung disease. Accordingly, we expect

LVGO’s solutions to see increased interest from potential clients in the near term as entities

look to better understand the populations they are at risk for. Additionally, we see opportunity

for LVGO to report increased enrollment near term from clients already in LVGO’s portfolio via

patients looking to maintain some degree of care for their chronic condition and not being

able/willing to see a doctor in person, with a solution that is free of charge from their

employer/health plan.

Figure 22: Reported Underlying Conditions Among Persons

with Confirmed COVID-19 (Jan 22 – May 30, 2020)

Figure 23: CDC Data Highlight Vulnerability of Patients with

Underlying Health Conditions

Source: CDC, Credit Suisse Source: CDC, Credit Suisse

LVGO was relatively well-positioned heading into COVID-19 from an operational perspective

given that over one-third of LVGO employees, including health coaches and certified diabetes

educators had already been working remotely. In addition, LVGO had previously been

diversifying its supply chain by multi-sourcing production locations for the company’s connected

hardware devices.

The overall impact of COVID-19, however, is still uncertain in terms of its effect on LVGO’s

underlying member base and associated employee turnover. Based on LVGO’s prospectus filing

in 2019, some of the company’s top clients in terms of revenue in 2018 include some

prominent companies from the travel and entertainment industries, including Delta Air Lines and

Hyatt Hotels. However, management has noted that many of their employer clients, including

Amazon, have actually increased hiring. Further, some of the heavily impacted industries have

asked LVGO to accelerate their programs as a means to provide cost savings in a time

companies need it most.

Additionally, many employers have continued benefits for furloughed employees as well as some

employers structuring benefit payments for laid off employees to continue for a period of time,

which has allowed LVGO to retain those members. Further, some members after being laid off

would continue to receive their health benefits through continuation of coverage under COBRA.

Although a very small percentage of LVGO’s client base, LVGO also sells in a direct-to-

consumer (DTC) model for members that may have lost their benefit package to buy direct from

LVGO. The company has been offering this at a discounted rate in light of the current

environment to ensure members are able to continue to receive LVGO’s services.

32%

30%

17%

8%

5%

5%

1%

Any cardiovascular disease

Diabetes

Any chronic lung disease

Renal disease

Immunocompromised

Neurologic disability

Liver disease

45.4%

19.5%

7.6%1.6%

Reported Hospitalizations

(Including ICU)

Died

Patients with Underlying Condition

Patients with NO Underlying Condition

14 July 2020

Livongo Health 19

New Payment Models Create Tailwind for LVGO

As a result of Medicare not considering remote patient monitoring as a telehealth service, the

regulations for telehealth surrounding originating site and provision of services to patients limited

to rural areas do not apply to remote patient monitoring. Though these regulations have been

waived as part of the government’s response to COVID-19, the waivers are in effect for as long

as the public health emergency persists. As such, it will take lobbying and advocacy by

telehealth stakeholders to maintain these relaxations going forward – something vendors/parties

in the remote patient monitoring space do not have to spend time focusing on.

As a result of CMS changing billable CPT codes specific to remote patient monitoring, it has

allowed LVGO to accelerate penetration of the Medicare fee-for-service market. Within the

Medicare fee-for-service market, provider organizations are able to use LVGO as a tool to

manage their patient populations, and pay LVGO via its traditional subscription fee model.

However, since the provider is now able to be reimbursed under RPM CPT, the provider

organization essentially ends up paying LVGO’s subscription fee out of the money the provider

is being reimbursed with through CMS. This model is different than LVGO’s traditional client

which holds the underlying risk for the patient population (e.g., self-insured employers, health

plans, Medicare Advantage plans, etc.). As such, the underlying value proposition by LVGO is

different based on the two different models. For the self-insured employers, MA plans, etc., the

value from using LVGO comes through the ability to lower costs through better management of

chronic conditions through LVGO’s platforms. From a health system and provider perspective,

the incentive to use LVGO’s platform comes through the ability to earn a spread through billing

Medicare FFS using RPM billable CPT codes offset by the subscription fee paid to LVGO. With

the RPM CPT codes now more easily billable, LVGO has indicated that the Medicare FFS

market has become quickly available in a manner of months, versus the years it might have

taken to reach otherwise.

LVGO is still in early stages in providing its RPM solutions to health systems, though the

company does have pilot programs in place in several health systems across the country. LVGO

currently works with a number of health systems providing the LVGO solutions to employees of

the health system. However, the next step for the model would be for health systems to broadly

stand up RPM programs to monitor their patient populations, which would provide the health

system with an incremental source of revenue. In terms of payment for LVGO, management

noted that the company is still figuring out how such partnerships would work, but is assessing

whether LVGO would take a percentage of revenue or be paid under its standard subscription

model. With the changes to the remote patient monitoring reimbursable codes, it is still in the

early innings for how the structure would work as well as health systems still figuring out how

they will stand up the programs on a widespread basis and how they will be staffed.

Notably, LVGO’s preliminary 2Q20 revenue of $86-$87 mln did not come as a result of any

significant pickup in the Medicare FFS program, nor does the company expect there to be much

of a meaningful contributor for the rest of 2020. However, as a result of relaxed regulations

around Medicare reimbursement, LVGO expects the program to start generating noticeable

revenue in 2021, which previously had been thought of more as a 2024-2025 type of

opportunity.

14 July 2020

Livongo Health 20

Figure 24: LVGO Economic Model with Medicare Fee-for-Service

Source: Company data

When working with Medicare Advantage (MA) plans, LVGO operates in a similar manner to how

it provides its services with self-insured or fully-insured employers, whereby the MA plan will pay

LVGO its traditional PPPM fee and the MA plan will benefit from cost savings associated with

providing better, more proactive care to MA members and keep individuals out of the

emergency room or other costly sites of care. In addition, LVGO is also in a place to help MA

plans improve their HEDIS scores, which becomes an important factor that affects the

reimbursement rate a plan receives from CMS. By providing more proactive, and preventative,

care to MA populations by using LVGO’s solutions, MA plans are able to improve their member

satisfaction while at the same time improving their own financial position.

Figure 25: LVGO Economic Model with Medicare Advantage Plans

Source: Company data

Because of changes to Medicare regulations, LVGO was approved in early 2019 as an enrolled

provider for Medicare Advantage members. As a result, a lot of what LVGO’s certified diabetes

educators do for members is potentially billable. LVGO has been figuring out what activities their

coaches are already doing in their day-to-day can be potentially billed for and reimbursed by

CMS. Since the fee for LVGO’s coaching and other services would likely be included in the

PPPM fee paid by a health system, LVGO’s opportunity to be reimbursed by CMS for the

coaching and diabetes education it provides would most likely come through a DTC model.

Patient

PPPM

Fee

ReimbursementProvider

LVGO Platform

Access/Devices

LVGO Platform

Access/Devices

MA/LVGO

Member

MA Plan

PPPM Fee

LVGO Platform Access/Devices

Cost

Savings

Capitated Payments

14 July 2020

Livongo Health 21

Figure 26: LVGO Economic Model Using Direct-to-Consumer (DTC) Approach

Source: Company data, Credit Suisse

AI+AI Data Engine a Core Component of LVGO’s

Competitive Strategy

LVGO’s digital health platform is powered by its proprietary data engine, which the company

refers to as its AI+AI: Aggregate, Interpret, Apply, and Iterate. Through a constant feedback

loop, LVGO Aggregates data from multiple sources, Interprets that data to identify what it is a

member actually needs, Apply the insights learned from previous iterations of the AI+AI loop

about the specific member’s chronic conditions as well as similar members, and Iterate the

process tailoring the member’s experience based on their behavior and feedback. We see

LVGO’s AI+AI engine as a core component of the company’s competitive strategy. Across the

entire healthcare and consumer landscape, there is an ample amount of data to understand the

underlying trends in someone’s health and then be able to recommend and coach that person

on how to better manage their health. The key, however, is the ability to extract and understand

the data, which is why LVGO employs more data scientists than people coding their solutions.

By aggregating dozens of data sets outside of LVGO’s own proprietary data, the company is

able to create a well-rounded picture of what the key drivers are of a member’s behavior

change and do so on a member-by-member level, much like an Amazon or Netflix experience,

which is tailored specifically to an individual’s preference level. In fact, LVGO takes over 500

million data points and runs them against their algorithms to translate data into actionable,

personalized signals that improve member outcomes and financial savings. The more members

using LVGO’s various solutions, the more data are collected and the more robust and

personalized the platform is able to become for members. Members have shown appreciation

for the LVGO platform as well, as LVGO claims a +64 average net promoter score (NPS) as of

December 31, 2019.

When a member in the diabetes management solution tracks their blood glucose, they receive a

highly personalized message about what to do at that moment, which LVGO refers to as a

Health Nudge. As a result of the vast amount of data LVGO collects about each member, it is

able to engage with the member using Health Nudges that may include diet advice, medication

information, or suggestions for increases in physical activity in the relevant context. For example,

when a member measures their blood sugar in the morning and it comes back at a high level,

LVGO will ask if they had breakfast, what they ate, etc. Based on the member’s answers,

LVGO is able put their blood sugar reading in context and provide nutritional advice (e.g.,

replace the doughnut with a healthier, yet still tasteful breakfast that is better for blood sugar

levels).

Additionally, when a member takes a blood sugar measurement before they had breakfast,

LVGO is able to collect an important data point since what happens to someone’s blood sugar

while sleeping is an indication of how well their medication and dosage are working. How a

member responds to a specific Health Nudge allows LVGO to further adapt its AI+AI engine to

provide better insights in the future. 40% of LVGO’s members take action upon receiving a

Health Nudge, resulting in LVGO being able to constantly refine their algorithms.

PatientPPPM Fee

Reimbursement

LVGO Platform Access/Devices

14 July 2020

Livongo Health 22

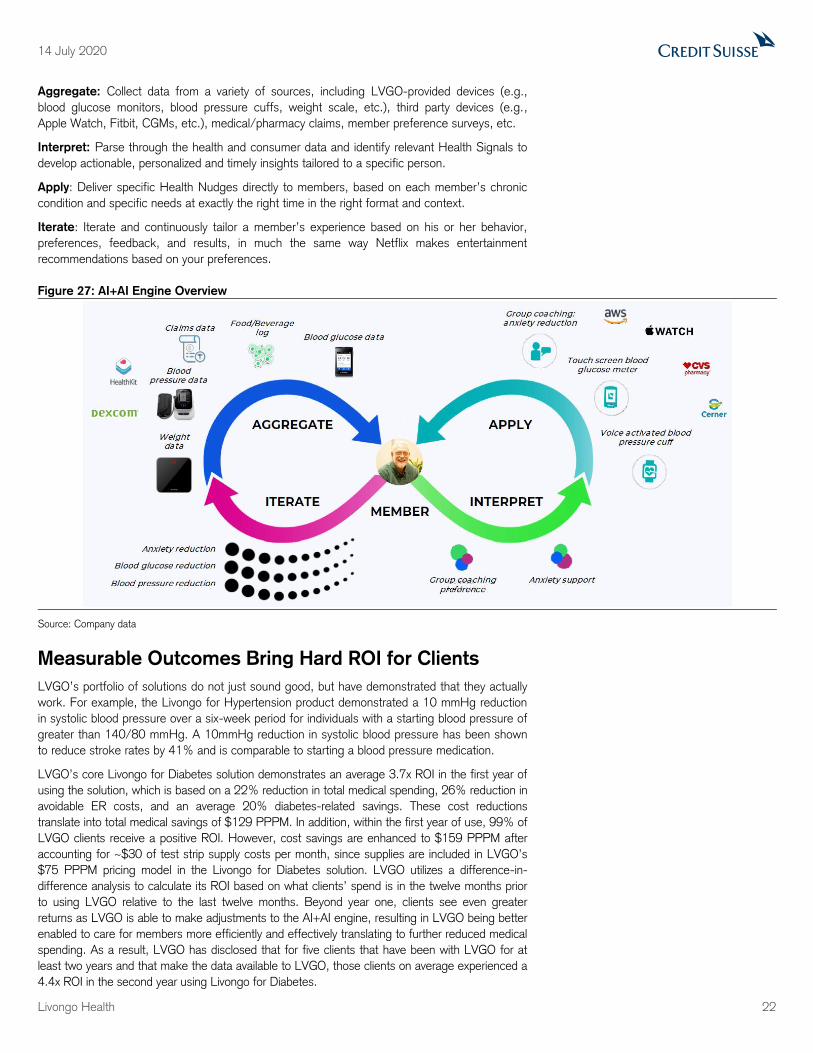

Aggregate: Collect data from a variety of sources, including LVGO-provided devices (e.g.,

blood glucose monitors, blood pressure cuffs, weight scale, etc.), third party devices (e.g.,

Apple Watch, Fitbit, CGMs, etc.), medical/pharmacy claims, member preference surveys, etc.

Interpret: Parse through the health and consumer data and identify relevant Health Signals to

develop actionable, personalized and timely insights tailored to a specific person.

Apply: Deliver specific Health Nudges directly to members, based on each member’s chronic

condition and specific needs at exactly the right time in the right format and context.

Iterate: Iterate and continuously tailor a member’s experience based on his or her behavior,

preferences, feedback, and results, in much the same way Netflix makes entertainment

recommendations based on your preferences.

Figure 27: AI+AI Engine Overview

Source: Company data

Measurable Outcomes Bring Hard ROI for Clients

LVGO’s portfolio of solutions do not just sound good, but have demonstrated that they actually

work. For example, the Livongo for Hypertension product demonstrated a 10 mmHg reduction

in systolic blood pressure over a six-week period for individuals with a starting blood pressure of

greater than 140/80 mmHg. A 10mmHg reduction in systolic blood pressure has been shown

to reduce stroke rates by 41% and is comparable to starting a blood pressure medication.

LVGO’s core Livongo for Diabetes solution demonstrates an average 3.7x ROI in the first year of

using the solution, which is based on a 22% reduction in total medical spending, 26% reduction in

avoidable ER costs, and an average 20% diabetes-related savings. These cost reductions

translate into total medical savings of $129 PPPM. In addition, within the first year of use, 99% of

LVGO clients receive a positive ROI. However, cost savings are enhanced to $159 PPPM after

accounting for ~$30 of test strip supply costs per month, since supplies are included in LVGO’s

$75 PPPM pricing model in the Livongo for Diabetes solution. LVGO utilizes a difference-in-

difference analysis to calculate its ROI based on what clients’ spend is in the twelve months prior

to using LVGO relative to the last twelve months. Beyond year one, clients see even greater

returns as LVGO is able to make adjustments to the AI+AI engine, resulting in LVGO being better

enabled to care for members more efficiently and effectively translating to further reduced medical

spending. As a result, LVGO has disclosed that for five clients that have been with LVGO for at

least two years and that make the data available to LVGO, those clients on average experienced a

4.4x ROI in the second year using Livongo for Diabetes.

14 July 2020

Livongo Health 23

In LVGO’s Pre-Diabetes and Weight Management solution, LVGO has been able to show

weight loss in the first year of use. Further, as of December 2018, the average decrease in

weight for members who had been using the solution for 12 months was 7.32%.

As for LVGO’s Behavioral Health solution by myStrength, after tracking members’ Depression

Anxiety Stress Scale (DASS) since May 2011, and as of September 2019, 55% of LVGO’s

members showed clinical improvement.

Clients see the value in LVGO’s approach, as the company has several clients that reduce or

entirely waive the co-pay for diabetes and hypertension medications, but only if the employee

joins Livongo and engages with the platform. As a result of employers encouraging this behavior,

LVGO not only improves enrollment rates, and therefore revenue, but also helps its clients save

money across their populations.

In fact, Sony recently conducted a study geared toward assessing consumer adoption and

interest in remote health technology aimed at helping people manage chronic conditions. The

study found that almost 50% of survey respondents would visit their doctor’s office less often if

they had the means to share health data digitally. Separately, 54% of respondents indicated

they could avoid three or more annual visits to the doctor with just 10% of respondents saying

they would still need all of the visits they typically have.

Recent Notable Clients Wins and Opportunities

Livongo has recently announced some notable client wins outside of the company’s core

diabetes management solution. For example, in April 2020, Kaiser Permanente announced it

made Livongo’s myStrength mental health solution available to members in most regions with a

contract length of 5 years. Kaiser is one of the largest not-for-profit health plans in the U.S.,

serving ~12.4 mln members.

Livongo has also had recent success winning business in the government payer space, having

landed a large contract with the Government Employee Health Association (GEHA) in May

2020 as well as a contract with the Federal Employees Health Benefits Program (FEHBP) back

in October 2019. The contract with GEHA is one of LVGO’s largest yet, with GEHA

representing 2 million lives. Further, the contract with GEHA allows LVGO to provide diabetes,

hypertension, and prediabetes solutions as a benefit to eligible members.

LVGO’s largest contract win came in October 2019 through the Federal Employees Health

Benefits Program (FEHBP) under one health plan covering 5.3 mln federal employees, retirees,

and their families out of ~8 mln people who receive their benefits through the FEHBP. Notably,

LVGO is expecting FEHBP to contribute 25k enrolled diabetes members in 2020 and 25k

more in 2021 with a revenue contribution of $20-25 mln in 2020 and $30-35 mln in 2021.

LVGO also picked up an important win in March 2020 when the Health Transformation Alliance

(HTA) and Welltok selected LVGO as the first health and wellbeing partner for the consumer

engagement platform available to the over 50 HTA member/owners. By way of background,

Welltok operates as an enterprise SaaS company delivering a healthcare consumer activation

platform. Welltok pre-integrates digital health platforms, like LVGO for example, and then offers

its own aggregated platform of resources to health plans, health systems, and had been

recently selected to operate the HTA’s marketplace (see our HCDT&I note featuring Welltok).

Notably, the HTA’s marketplace of health and well-being programs will offer LVGO’s Diabetes,

Hypertension, Prediabetes & Weight Management programs to the more than 7 million lives

covered by the cooperative’s 50+ self-insured employer member/owners. The underlying

member/owners of the HTA will allow LVGO to gain access to more of largest Fortune 500

employers in the country.

Most recently, it was announced that Priority Health, the second largest health plan in Michigan,

would be offering LVGO’s myStrength behavioral health solution at no cost for all members who

sign up. In addition, BlueCross BlueShield of Western New York is offering the myStrength app

to its nearly one million members to support members’ overall wellness during the pandemic.

14 July 2020

Livongo Health 24

Strong Financial Performance

LVGO has shown consistent, strong revenue growth most notably from its foundational Livongo

for Diabetes solution, as the company has grown its client base and improved enrollment rates

among its members. Notably, a significant majority of this revenue growth has come from

LVGO’s penetration in the self-insured employer market. Even with the strong growth already

experienced, we see a long runway ahead for LVGO to capture more share in the self-insured

market given that LVGO’s 328.5K enrolled diabetes members represent just ~1% of the total

+30 mln people living with diabetes in the U.S. Further, management has pointed to the

company gaining traction in the fully insured health plan market, as LVGO has been able to

demonstrate clinical improvements in its existing base, which further solidifies the company’s

value proposition. In addition, we see a significant, largely untouched growth opportunity for

LVGO in the Medicare (MA and FFS) and Medicaid markets.

In terms of EBITDA, since LVGO entered the public markets the company has indicated an

expectation to turn adjusted EBITDA positive and remain there on a sustained basis beginning

in 2021. However, LVGO has been continuing to show improvement in EBITDA margins as the

company has continued to gain operating leverage through its AI+AI engine in recruitment of

members, better retention, and in the use of digital coaching. In addition, LVGO has seen

improvements from the higher incremental margins associated from members who stay on the

LVGO platform for longer. As a result of improved operating leverage, LVGO posted positive

adjusted EBITDA of $3.8 mln in 1Q20. Notably, 4Q19 although showing positive EBITDA of

$1.6 mln, the quarter included a $1.9 mln one-time beneficial adjustment for the deferral of

costs in the hypertension solution’s blood pressure cuffs and the weight scales in the

prediabetes & weight management solution, which LVGO will defer and amortize going forward.

4Q19 also benefited from a one-time adjustment of $1.2 mln for a portion of sales

commissions deferred/amortized moving forward. Taking into account these one-time

adjustments, we see 1Q20 as LVGO’s first quarter of true positive adjusted EBITDA. Based on

LVGO’s preliminary reported revenue for 2Q20 of $86-$87 mln (vs. previous guidance of $73-

$75 mln) we expect LVGO to report positive adjusted EBITDA for 2Q20. For reference, going

into 1Q20, LVGO was guiding to revenue of $60-$62 mln and adjusted EBITDA of ($4.5)-

($5.5) mln, where the company also preannounced revenues of $65.5-$66.5 mln. When the

company actually reported 1Q20 results, LVGO came in at $68.8 mln in revenue and a positive

$3.8 mln in EBITDA.

Figure 28: LVGO Annual Revenue Figure 29: LVGO Annual Adj. EBITDA

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

$31 $68 $170

$354

$563

$785

$1,027

2017 2018 2019 2020E 2021E 2022E 2023E

($14.1)($27.7)

($20.1)

$7.8

$32.3

$71.4

$128.2

2017 2018 2019 2020E 2021E 2022E 2023E

14 July 2020

Livongo Health 25

Investment Risks

Exposure to High Unemployment Rate

LVGO derives a high concentration of revenue to clients that are self-insured employers. Thus,

the significant rise in unemployment as a result of COVID-19 brings inherent risk. In addition,

any prolonged economic recession poses risk to the future of LVGO’s revenue outlook if layoffs

were to be disproportionately concentrated to where LVGO derives its members.

Channel Partners’ Influence on Revenue

LVGO has a significant amount of revenue influenced by its channel partners, who collect an

administrative/marketing commission for their services. Sales through LVGO’s top five channel

partners (Express Scripts, CVS Pharmacy, Health Care Service Corporation, Anthem, and

Highmark) represented 61.3% of LVGO’s revenue in 2019. Further, LVGO contracts with its

channel partners and resellers on a non-exclusive basis. As a result, such channel partners are

able to refer business to LVGO’s competitors or develop their own solutions.

In exchange for the speed and access to new client populations LVGO’s channel partners

provide, LVGO gives up a high-single-digit percentage of top-line revenue. As a result of the

upfront cost LVGO incurs as part of bringing in a client through its partner channel rather than

through its own direct sales force, the time to breakeven on a cash basis is further delayed.

LVGO and CVS have worked together since 2017 through CVS Health’s Transform Diabetes

Care (TDC) program, which aims to help CVS’ PBM clients improve health outcomes for their

members and therefore lower costs by using solutions like LVGO. Recently, CVS rolled out a

next generation Transform Diabetes Care program, in which LVGO has opted not to participate.