Embed Size (px)

Citation preview

SBA Fact Sheet 2012 – Lithuania

1

EN Enterprise and Industry

LITHUANIA SBA Fact Sheet 2012

1. SMEs in Lithuania — basic figures

EU27 EU27 EU27Number Share Share Number Share Share Billion € Share Share

Micro 91.838 87,6% 92,2% 182.729 23,6% 29,6% 1 12,1% 21,2%Small 10.742 10,2% 6,5% 208.510 26,9% 20,6% 2 21,9% 18,5%

Medium-sized 2.050 2,0% 1,1% 196.251 25,3% 17,2% 3 29,4% 18,4%SMEs 104.630 99,8% 99,8% 587.490 75,7% 67,4% 6 63,4% 58,1%Large 254 0,2% 0,2% 188.322 24,3% 32,6% 4 36,6% 41,9%Total 104.884 100,0% 100,0% 775.812 100,0% 100,0% 10 100,0% 100,0%

Estimates for 2011, based on 2005-2009 figures from the Structural Business Statistics Database (Eurostat). The estimates have been produced by Cambridge Econometrics.The data cover the 'business economy' which includes industry, construction, trade, and services (NACE Rev. 2 Sections B to J, L, M and N). The data does not cover the enterprises in agriculture, forestry, fishing or the largely non-market services such as education and health. The advantage of using Eurostat data is that the statistics from different countries have been harmonised and are comparable across countries. The disadvantage is that for some countries these data may be different from data published by national authorities.

Number of Enterprises Employment Value addedLithuania Lithuania Lithuania

As with its Baltic neighbours Latvia and Estonia, the Lithuanian SME sector shows a clear tendency towards a greater share of small and medium-sized enterprises and a correspondingly smaller percentage of micro ones. This characteristic helps to explain why the SME sector as a whole, while representing exactly the same percentage of all companies (99.8 %) as in the EU as a whole, nevertheless contributes more in terms of jobs and value-added: Lithuanian SMEs are larger than their EU peers. The sector they are most likely to be active in is trade, which accounts for a remarkable 47 % of Lithuanian SMEs, against an EU average of 30 %. However, these enterprises do not contribute in the

same manner to the creation of jobs and value-added, accounting for just 31 % and 27 % respectively, i.e. close to EU mean. It is therefore safe to assume that they are mostly active in small-scale trade. By contrast, SMEs in Lithuania specialising in services represent only 32 % of the total (EU average: 45 %), but nevertheless account for a similar share of value-added (41 % to 43 %), suggesting that they are much more productive than their trading peers. Lastly, the percentage of Lithuanian SMEs specialising in High-tech manufacturing or knowledge-intensive services is much lower than in the EU as a whole2. The available forecasts up to the end of 2011 suggest that the Lithuanian SME sector has been hit

In a nutshell: Lithuanian SME sector marked by fewer micro firms and small and medium-sized ones than the EU

average. SMEs hit by the crisis but less so than larger enterprises. Lithuania’s SBA profile largely in line with the EU average, but on a positive trend. Policy action in most SBA areas, in particular Responsive administration, Entrepreneurship and Second

chance About the SBA Fact Sheets1: The Small Business Act for Europe (SBA) is the EU’s flagship policy initiative to support small and medium-sized enterprises (SMEs). The aim of the annually updated Fact Sheets is to improve understanding of recent trends and national policies affecting SMEs. Since 2011, each EU Member State has appointed a high-ranking government official as its national SME envoy. SME envoys spearhead the implementation of the SBA agenda in their countries.

SBA Fact Sheet 2012 – Lithuania

2

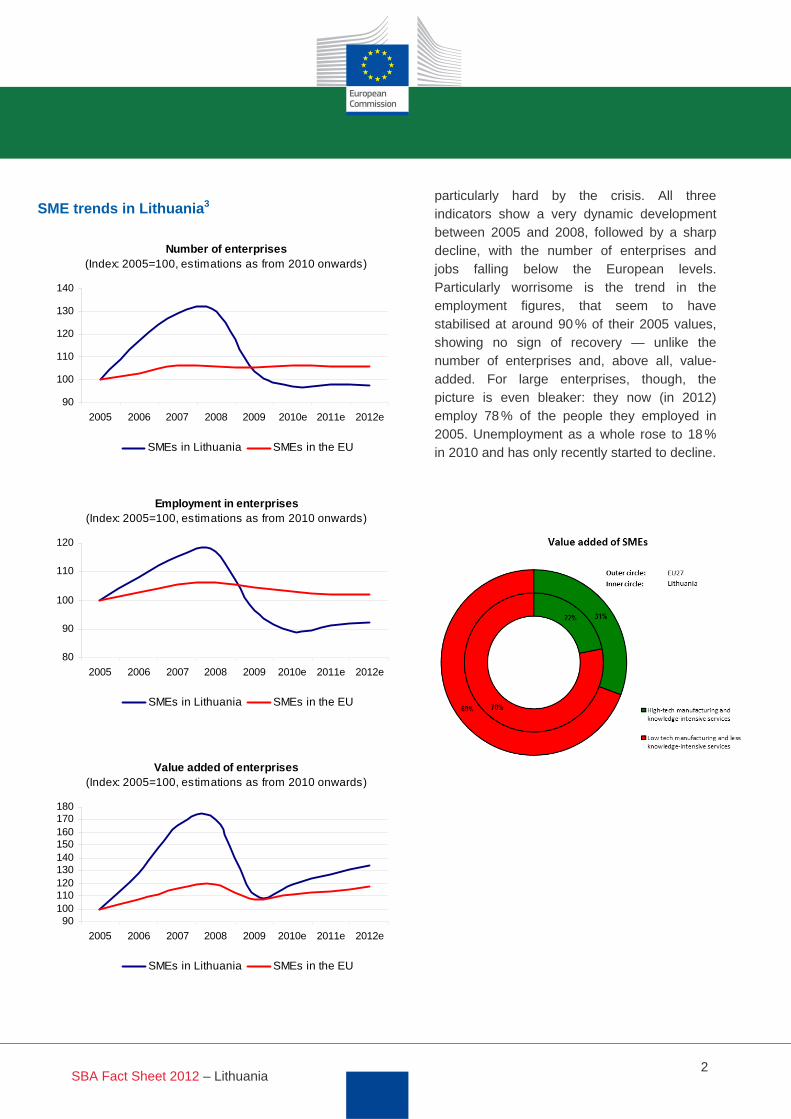

particularly hard by the crisis. All three indicators show a very dynamic development between 2005 and 2008, followed by a sharp decline, with the number of enterprises and jobs falling below the European levels. Particularly worrisome is the trend in the employment figures, that seem to have stabilised at around 90 % of their 2005 values, showing no sign of recovery — unlike the number of enterprises and, above all, value-added. For large enterprises, though, the picture is even bleaker: they now (in 2012) employ 78 % of the people they employed in 2005. Unemployment as a whole rose to 18 % in 2010 and has only recently started to decline.

SME trends in Lithuania3

Number of enterprises(Index: 2005=100, estimations as from 2010 onwards)

90

100

110

120

130

140

2005 2006 2007 2008 2009 2010e 2011e 2012e

SMEs in Lithuania SMEs in the EU

Employment in enterprises(Index: 2005=100, estimations as from 2010 onwards)

80

90

100

110

120

2005 2006 2007 2008 2009 2010e 2011e 2012e

SMEs in Lithuania SMEs in the EU

Value added of enterprises(Index: 2005=100, estimations as from 2010 onwards)

90100110120130140150160170180

2005 2006 2007 2008 2009 2010e 2011e 2012e

SMEs in Lithuania SMEs in the EU

SBA Fact Sheet 2012 – Lithuania

3

2. Lithuania’s SBA profile

The SBA profile for Lithuania as a whole is comfortably in line with the EU average. In two areas, Environment and Skills and innovation, it performs below average, and in two others — Access to finance and State aid and public procurement — above it. The remaining ones do not deviate significantly from the average. In terms of

development over time, the trend is quite positive, with significant progress in four areas (Skills and innovation, State aid and public procurement, Access to finance, the Single market and, less markedly, Responsive administration), while some ground has been lost in two (Entrepreneurship and Second chance). From a policy4 point of view, there has been significant action in particular in the areas of Responsive administration, Entrepreneurship and Second chance. The Ministry of Economy has prepared an entrepreneurship promotion programme for 2011-2020, including some guidelines from the SBA. Among the most relevant initiatives taken in 2011 are the launch of a new Internet portal, ‘Verslo turgus’ (‘Business market’), a resource for matching transferable businesses with potential new owners, a new database of entrepreneurs who are entering business for the second time, examples of second-time entrepreneurs’ success stories and, last but not least, new legislation introducing the rule of two dates for business commencement.

Lithuania’s SBA performance: status quo and development over 2007-20125

SBA Fact Sheet 2012 – Lithuania

4

I. Entrepreneurship

While Lithuania performs generally in line with the other EU countries in terms of Entrepreneurship, its score is quite low compared to the EU average when it comes to Lithuanians’ views about the role of schools in fostering an entrepreneurial attitude and (though less markedly so) their estimation of how feasible it is for them to become entrepreneurs. The self-employment rate, at 10 %, is likewise below the EU average (14 %). On the other hand, more Lithuanians than EU citizens in general planned in 2011 to start a business within the next three years, a fact that could be partly due to unemployment being exceptionally high. This latter explanation (unemployed people becoming entrepreneurs out of necessity) might also help to explain the apparent contradiction between the higher-than-average entrepreneurial intent and a lower-than-average figure measuring the feasibility of becoming self-employed. The remaining indicators fall within the

0.5 standard deviation band and can therefore be considered average. In 2011 there was significant policy action in the SBA area ‘Entrepreneurship’. First of all, there have been a range of ‘Enterprise Lithuania’ initiatives, aimed at encouraging entrepreneurship and self-employment among the population at large, with special reference to young people, women, and other target groups. Full information on starting a business and its further development is made available at these events, as are the ‘first-year business support baskets’. If individuals who have received business support baskets establish their companies within six months, they qualify for business services worth 6 000 Litas (€1 700). On 12 April 2011 the Ministry of Social Security and Labour announced the Action Plan for National Youth Policy Development Programme Implementation for 2011-2013. Youth Development Programme initiatives coordinate the activities in

SBA Fact Sheet 2012 – Lithuania

5

regional ‘Youth entrepreneurship centres’, which are geared to promoting youth entrepreneurship, and encouraging young people to become entrepreneurs and to learn to use their own and the local communities’ resources. The National Youth Policy Development Programme also features special programmes, such as the National Programme for the Training and Inducement of Youth Entrepreneurship for the period 2008-2012, the purpose being to create a consistent, effective

entrepreneurship education system targeted at young people. Lastly, on 13 July 2011 the Government ratified the decision implementing the ‘Development and introduction of methods for language teaching and entrepreneurship development, as well as innovative educational methods’, to encourage the creation of educational programmes focused on innovation and entrepreneurship skills development.

II. Second chance

In the ‘Second chance’ area Lithuania performs within the EU average. From an administrative point of view, the country deserves quite good marks: it takes less time (one and a half years instead of almost two) and costs less (7 % of the debtor’s estate instead of 10.64 %) to close a business than in the average EU Member State. However, Lithuanians are slightly less willing to agree that an

entrepreneur who is unsuccessful at the first time of asking deserves a second chance. Policy-wise, important amendments to the Enterprise Bankruptcy Law were introduced in 2011. They are aimed at simplifying the procedures, and are geared towards achieving the EU-wide SME policy goal of completing all legal procedures necessary for winding up a business, in the case of non-fraudulent bankruptcy, within a year.

III. Think small first

Since only one indicator is available in this area, it is not possible to draw any wide-reaching conclusions . However, it can be said that in Lithuania the burden

of government regulation does not appear to differ significantly from the EU average. On the policy front, the Lithuanian Government decided to introduce common starting dates for new

SBA Fact Sheet 2012 – Lithuania

6

legislation entering into force, thereby making it easier for businesses, especially smaller ones, to keep up to date. Consequently, on 13 July 2011, the ‘two date’ rule was adopted, to ensure that new or amended laws which regulate the activities of legal entities should come into force on either 1 May or 1 November. They should also be announced three months before they come into force. As from 1 September 2012 a new, simplified legal entity form called ‘small partnership’ is likely to be introduced. This is a limited-liability business entity

with no minimum capital requirement, and its members can only be individuals (natural persons). The idea is that its members should be able to distribute profits for a period shorter than the financial year. In order to reduce the regulatory burden, a compulsory quantitative evaluation of all new draft legislation in terms of administrative burdens on businesses was enforced from 1 March 2012 (the new methodology having been adopted in January 2012).

IV. Responsive administration

The overall score of Lithuania in this area is within the EU mean, though the individual indicators are often quite far from the mean, in both directions. Lithuania easily beats the EU average in terms of the time and cost elements in transferring a property: three days instead of 36, and 0.8 % of its value instead of 4.69 %. On the other hand, it lags behind in terms of the availability of online public services, the time needed to start a business6, and the minimum capital required to do so (action has now been taken on this latter point, but its effects are not yet reflected in the data). The remaining indicators, measuring the cost of starting a business

and the administrative burden of taxation, are close to the EU average. Taking all indicators into account, Lithuania’s performance is somewhat mixed and does not give a clear picture. In 2011 Lithuania was particularly active, policy-wise, in the area of Responsive administration. The Business Environment Improvement Action Plan for 2011 was introduced to reduce the time needed to set up a business and to accelerate the start of SMEs’ commercial operations by reducing and simplifying the procedures for obtaining licences and permits. For instance, the list of activities for which the acquisition of business licenses is required was

SBA Fact Sheet 2012 – Lithuania

7

reduced, and a number of procedures related to starting a business were removed, such as getting the documents of incorporation of a private limited-liability company approved by a notary (if the company is registered and incorporated online) or the transmission of information about the company’s activity to the Labour Inspectorate. The Business Environment Improvement Action Plan for 2011 also features measures designed to speed up the issue of construction permits, simplify the payment of taxes, and make it easier to export and import. As part of the Legal Entities Registration eService project (JAREP, i.e. Juridinių asmenų registravimo

elektroninė paslauga) new e-services were introduced. The project is run by the State Enterprise Centre of Registers through its Register of Legal Entities. It created new electronic services for business licensing and the registration of individual business activity; online registration and incorporation services were expanded to cover all private limited-liability companies. Furthermore, it is now possible for individual enterprises, private limited-liability companies, associations and public institutions to amend their documents of incorporation electronically.

V. State aid and public procurement

Lithuania is a top-scorer with regard to the SBA area State aid and public procurement. Lithuanian SMEs are awarded half of all public contracts by value, beating the EU average of 35 %. State aid is twice as likely to be targeted at Lithuanian SMEs than in the EU as a whole (8 % as against 4 %), and e-procurement is readily available to them. Regarding the use of EU funds, regional funds are allocated to entrepreneurship and SMEs at a percentage similar to the average EU country, but Lithuania once again beats the average in the way agricultural funds are channelled to business creation and development. Lastly, Lithuanian public authorities pay as promptly as in the rest of the EU.

On the policy front in 2011, EU Directive 2009/81/EC was transposed into the Lithuanian Law on Public Procurement in the Fields of Defence and Security. So SMEs will be able to benefit from more favourable conditions when they compete in defence and security procurement markets. As regards mainstream public procurement, the recently adopted amendments to the Lithuanian Law on Public procurement have led to the Director of the Public Procurement Office adopting an ordinance regulating in which cases suppliers may provide a declaration of compliance with the minimum qualification requirements in place of the documents proving their qualification. This measure should reduce administrative burden and simplify the

SBA Fact Sheet 2012 – Lithuania

8

conditions for SMEs’ participation in public procurement. Finally, Lithuania has set the target for up to 5 % of total public procurement to be

innovative by 2013, in a bid to get public authorities to purchase R&D and innovation-related products and services.

VI. Access to finance

In this SBA area Lithuania scores slightly above the EU average and can also boast, as we saw previously, a positive trend (e.g. the relative difference between larger and smaller loans fell to 12 % from 20 % between 2010 and 2011, and only 9 % of respondents indicated that banks had become less willing to provide loans, down from 30 % in 2010). Only one indicator, measuring the strength of legal rights, comes in at below the EU average, while four are above the average. In particular, Lithuanian SMEs enjoy good access to public financial support; In 2011 compared to 2010, fewer entrepreneurs reported deterioration in the banks the willingness to grant loans. The difference between the interest charged on smaller loans and larger ones is smaller than in the average EU country (12 % as against

19 %); and Lithuania possesses a good credit information system. The remaining indicators can be considered within the EU-wide average score. Policy-wise, 2011 has seen the continuation of previously established measures rather than the introduction of new ones. Nevertheless, some specific action has been taken which will have an impact on access to finance and investment. One example is the amendment to the Law on Profit Tax, whereby the income threshold under which firms are allowed to pay a 5 % profit tax rate has been increased from 500 000 to 1 million Litas (EUR 289 620). This measure will encourage greater investment by increasing net revenues.

SBA Fact Sheet 2012 – Lithuania

9

VII. Single market

Lithuania’s performance in the SBA area Single market is very close to the EU standard. This applies to both sets of indicators: the one gauging the level of Lithuanian SMES engaged in intra-EU trade, and the one measuring the country’s ability to transpose EU legislation. Regarding the latter point, policy measures were taken in 2011 to make it easier for SMEs to comply with. More especially, guidelines about the principle of mutual recognition were

prepared, with the aim of ensuring its correct application. The guidelines are based on the experience of Denmark and the United Kingdom, and were explained to enterprises by representatives from the Ministry of Economy and ‘Enterprise Lithuania’ at specially organised workshops.

VIII. Skills and innovation

SBA Fact Sheet 2012 – Lithuania

10

Despite a positive trend over recent years, as highlighted in the SBA profile, Lithuania still lags behind in this area. Its score is particularly low when it comes to the ability of its SMEs to introduce innovations: only 22 % have introduced product or process innovations, and 21 % marketing or organisational ones, against an EU average of 34 % and 30 % respectively. Lithuania SMEs also appear to be less likely to be innovative in-house, to participate in EU-funded research, to bring innovation to the market, and (albeit less markedly so) to collaborate with other innovative SMEs. On the other hand, the country’s performance in terms

of workforce training provision and participation is only slightly below the mean. Lithuania now performs within the mean range with regard to the share of SMEs purchasing online, and above it (21 % vs. 13 %) for selling online. On the policy front, the Ministry of Economy is running the project ‘Business ABC’ in 2012 in order to develop SMEs’ skills. Its main objective is to ensure the availability of free consulting, training and information services to entrepreneurs in each county of Lithuania. More than 3000 hours of free counselling, training and events organisation services are set to be delivered.

IX. Environment

Environment is an area where, relative to its EU peers, Lithuania receives its lowest marks. Its score is dragged down in particular by the fact that only 79 % of SMEs have embraced resource-efficiency measures (compared with 93 % in the EU as a whole), and only 3 % (only a third of the EU average) have benefitted from public support in order to do so. Public support measures for the production of green products are also less common than in the average EU Member State, and Lithuanian SMEs are less likely, though not dramatically so, to

specialise in this particular market than their EU counterparts. Only for innovations with environmental benefits does Lithuania earn marks in line with the EU average. On the policy front, while there was action in the environment field in 2011 (with a special focus on renewable forms of energy), all the measures taken in this area fall within general national environmental policy, with no specific focus on SMEs and their particular needs.

SBA Fact Sheet 2012 – Lithuania

11

X. Internationalisation

Lithuania lies comfortably within the average in the area of internationalisation. This holds true for most of the indicators too, except for the share of SMEs exporting outside the EU, where it beats the EU mean of 3 % with a share of 5 %. On the other side, the number of documents needed for exporting is higher than the EU average. On the policy front, no wide-ranging measures or reforms were undertaken in 2011 or the first quarter of 2012. However, much has been done to encourage international cooperation between business, government and science. International business forums, symposiums and other meetings were organised, such as the World Lithuanian

Economic Forum in July. In addition Lithuania, represented by the Ministry of Economy, is active alongside nine Baltic Sea Region countries in running the programme for the development of innovation, clusters and SME networks in the Baltic Sea Region — the BSR Stars programme. To support and strengthen international collaboration between existing SMEs /SME networks and to facilitate new ones, the international workshop ‘BSR Stars SME networking day on smart/wooden houses’ was organised in April. The overall goal of these events was to encourage international cooperation, business ties and network-building.

SBA Fact Sheet 2012 – Lithuania

12

3. Good practice

To show what the government is doing to promote SMEs, we include an example of good practice.

On 14 September 2011 nine state authorities responsible for the supervision of business activities in Lithuania signed a Declaration on the First Business Year, undertaking to avoid punishing business entities during the first year of their economic activity in Lithuania, and to consult with them instead. During this time, i.e. at least 12 months from the moment of starting a business in Lithuania or from the start of a particular activity supervised by a particular institution, the parties to the Declaration have agreed to refrain from imposing sanctions (e.g. fines, activity restrictions) and to determine how much time the business entity should be given to deal with the infringements. Only in exceptional cases will the Institutions which signed the Declaration start proceedings against the business entities covered by the Declaration during their first year of activity, using such measures as the last resort, and only when necessary to prevent damage to the public, the interests of other persons or the environment. The authorities believe that this initiative will help to increase national competitiveness, improve the business environment, promote job creation and retention, reduce the administrative burden on businesses, and optimise the performance of inspectors and their supervisory functions. The following institutions have signed the Declaration: State Tax Inspectorate under the Ministry of Finance, State Labour Inspectorate, State Food and Veterinary Authority, Environmental Protection Agency, State Non-Food Products Inspectorate under the Ministry of Economy, State Territorial Planning and Construction Inspectorate under the Ministry of Environment, Fire and Rescue Department under the Ministry of Interior, State Road Transport Inspectorate under the Ministry of Transport and Communications, the State Public Health Service Authority under the Ministry of Health.

About the SBA Fact Sheets The Small Business Act (SBA) Fact Sheets are produced by DG ENTR as part of the SME Performance Review (SPR), which is its main vehicle providing an economic analysis of SME issues. They combine the latest available statistical and policy information for the 27 EU Member States and another ten non-member countries, They also feed in to the EU’s Competitiveness and Innovation Framework Programme (CIP). The Fact Sheets — produced annually — help to marshal the available information to facilitate SME policy assessments and monitor SBA implementation. They document the status quo and progress. They are not an assessment of Member States’ policies but should be regarded as an additional source of information to underpin evidence-based policy making. For example, the Fact Sheets cite only those policy measures deemed relevant by local SME policy experts. They do not, and cannot, reflect all measures taken by the government over the reference period. More policy information can be found on a database accessible from the SPR website. Please also see the end notes overleaf. For more information SME Performance Review: http://ec.europa.eu/enterprise/policies/sme/facts-figures-analysis/performance-review/index_en.htm Small Business Act: http://ec.europa.eu/enterprise/policies/sme/small-business-act/index_en.htm The European Small Business Portal: http://ec.europa.eu/small-business/index_en.htm [email protected]

SBA Fact Sheet 2012 – Lithuania

13

1 The SBA Fact Sheets 2012 benefited substantially from input by the European Commission’s Joint Research Centre (JRC) in Ispra, Italy. The JRC made major improvements to the methodological approach, statistical work on the dataset and the visual presentation of the data. 2 The indicators measuring the number of high-technology SMEs in the manufacturing industries and knowledge-intensive SMEs in the service sectors and their contribution to employment and value-added were calculated by reference to the Eurostat definition of ‘High-technology’ and ‘knowledge-based services’ aggregations based on NACE Rev. 2. For more information please see: http://epp.eurostat.ec.europa.eu/cache/ITY_SDDS/Annexes/htec_esms_an3.pdf 3 The three graphs below describe the trend over time for the variables. They consist of index values for the years since 2005, with the base year 2005 set at a value of 100. As from 2010, the graphs show estimates of the development over time, based on 2005-2009 figures from the Structural Business Statistics Database (Eurostat). The estimates were produced by Cambridge Econometrics. The data cover the ‘business economy’, which includes industry, construction, trade, and services (NACE Rev. 2 Sections B to J, L, M, N). The data do not cover enterprises in agriculture, forestry, fishing or largely non-market services, such as education and health. A detailed methodology can be consulted at: http://ec.europa.eu/enterprise/policies/sme/facts-figures-analysis/performance-review/index_en.htm. 4 The policy measures presented in this SBA Fact Sheet may be only a selection of the measures taken by the Government in 2011 and the first three months of 2012. The selection was made by the national SME policy expert contracted by Ecorys (DG ENTR´s lead contractor for the 2012 Fact Sheets). The experts were asked to select only those measures that, in their view, were the most important, i.e. were expected to have the highest impact in the specific SBA area. The complete range of measures that the experts compiled in producing this year’s Fact Sheets will be published alongside the Fact Sheets in the form of a policy database on the DG ENTR website. 5 The quadrant chart combines two sets of information. Firstly it shows the status quo performance based on data for the latest available years. This information is plotted along the X-axis measured in standard deviations of the simple, non-weighted arithmetical average for EU-27. The vertical corridor marked by the dotted lines defines the EU average. Secondly, it reveals progress over time, i.e. the average annual growth rates for the period 2007-2012. The growth rates are those of the individual indicators which make up the SBA area averages. Hence, the location of a particular SBA area average in any of the four quadrants indicates not only where the country is located in this SBA area relative to the rest of the EU at a given point in time, but also the extent of progress made in the period 2007-2012. 6 The start-up indicators are based on World Bank data. For methodological details, please consult the Doing Business 2012 report at http://www.doingbusiness.org/. It should be noted that these findings differ from corresponding figures obtained directly from Member States. Under a self-reporting exercise it evidently took four days and a cost of 130-289 euro to start a business in Lithuania in 2011. For more details please see: http://ec.europa.eu/enterprise/policies/sme/business-environment/start-up-procedures/index_en.htm.