Embed Size (px)

Citation preview

Lincoln Institute of Land Policy Economic Perspectives on State and Local Taxes

January 23, 2015 Dr. Phyllis Resnick

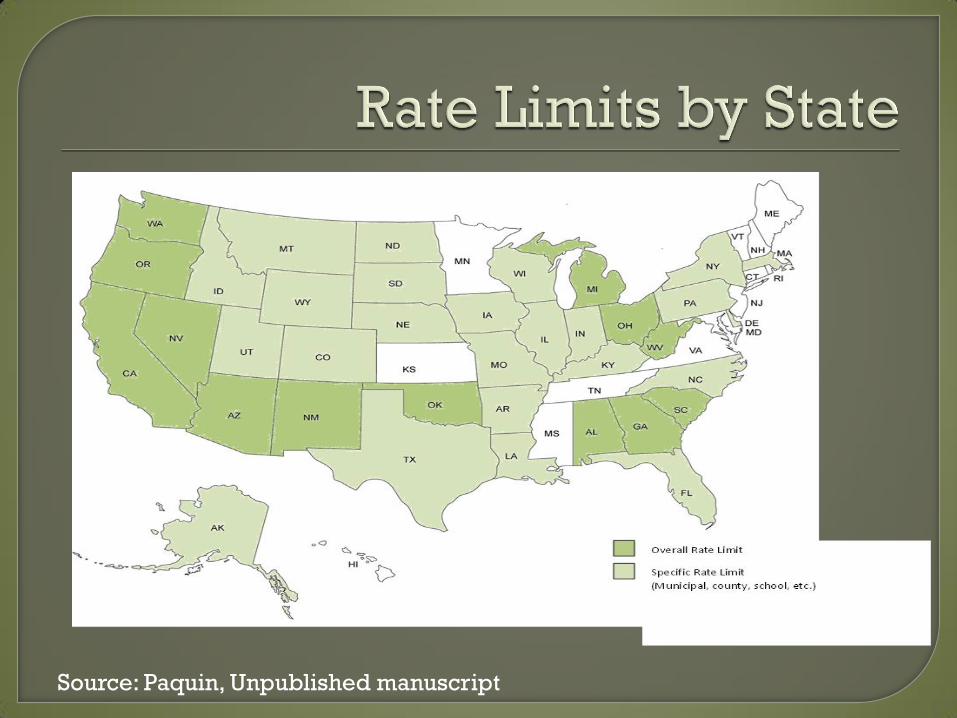

Property tax limits • Rate limits

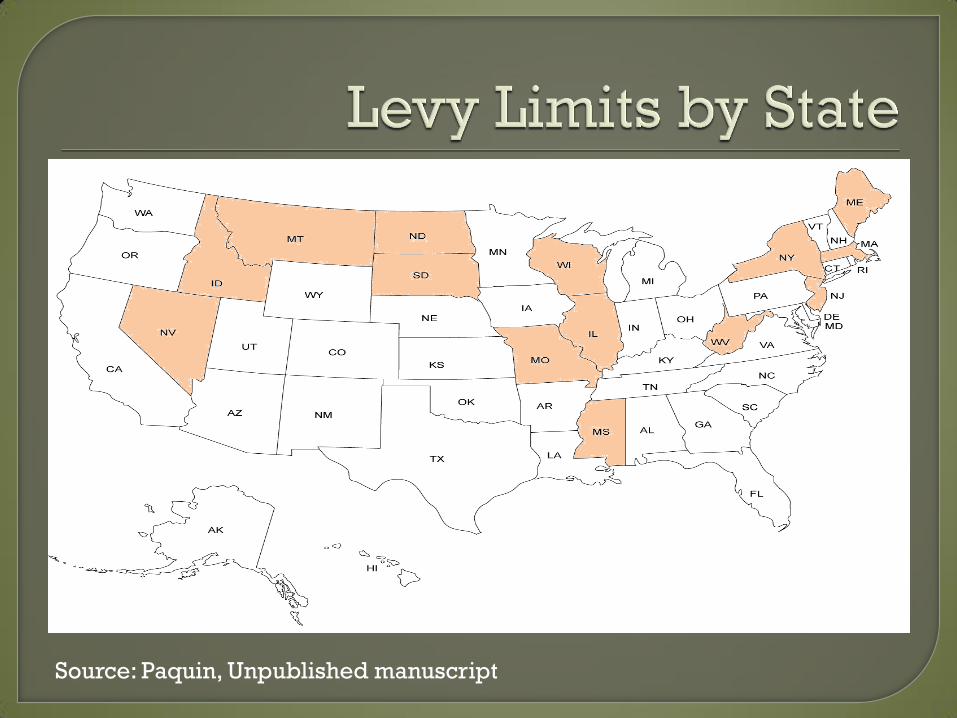

• Levy limits

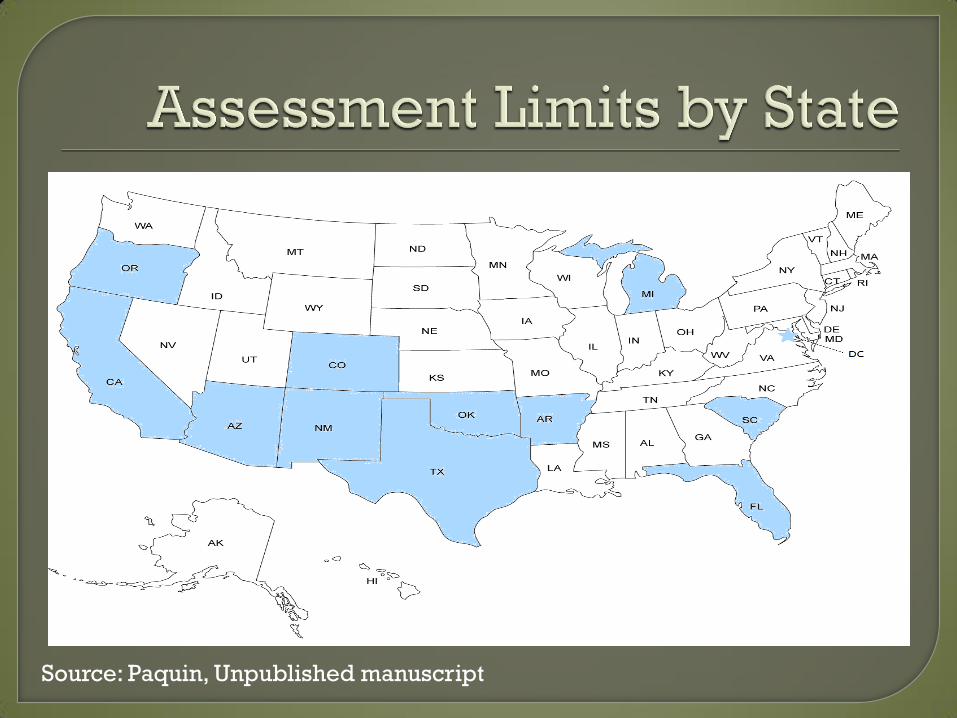

• Assessment limits

Fiscal cap tax and expenditure limitations

Supermajority requirements

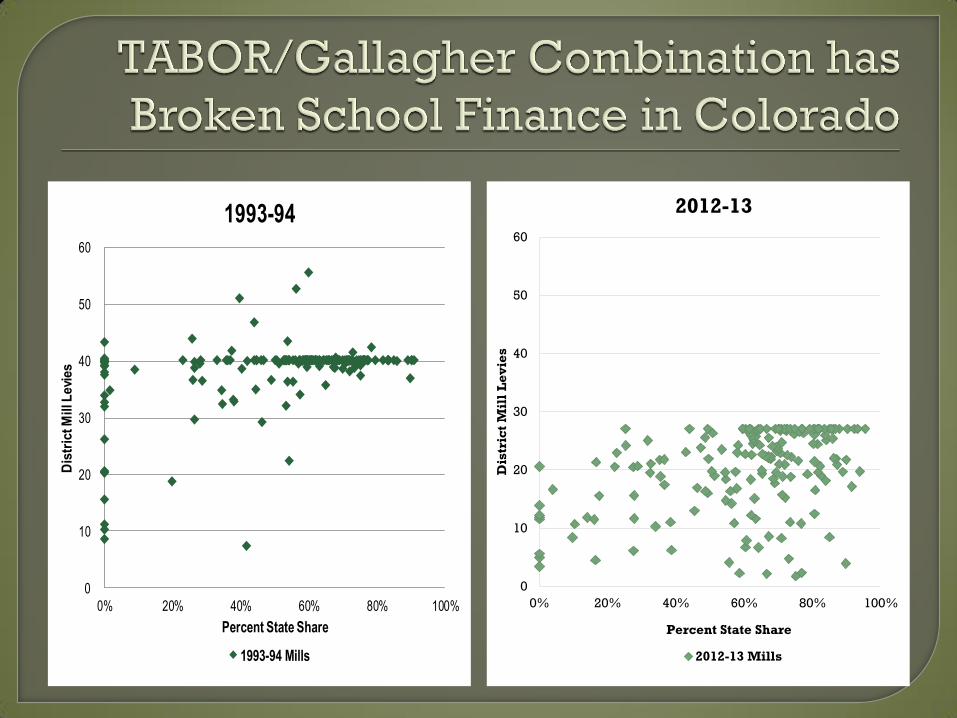

50 States…50 systems of limits

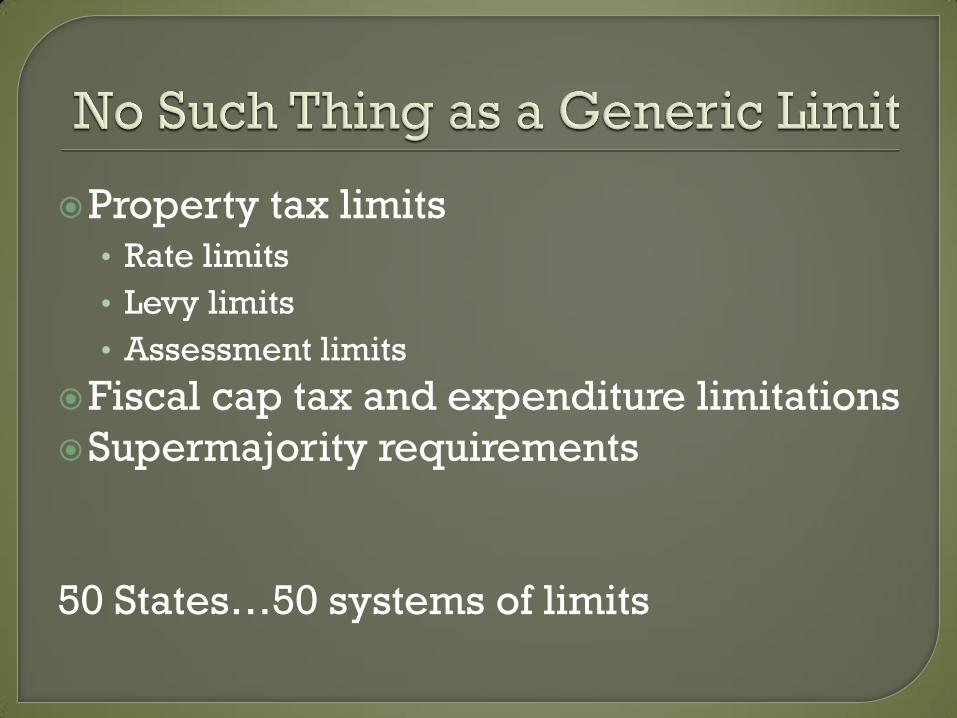

Source: Initiative and Referendum Institute, USC. http://www.iandrinstitute.org/statewide_i&r.htm

Source: Paquin, Unpublished manuscript

Source: Paquin, Unpublished manuscript

Source: Paquin, Unpublished manuscript

…yet universal lessons

Limits Result in

“Unintended”

Consequences

0

10

20

30

40

50

60

0% 20% 40% 60% 80% 100%

Dis

tric

t M

ill L

evi

es

Percent State Share

1993-94

1993-94 Mills

0

10

20

30

40

50

60

0% 20% 40% 60% 80% 100%

Dis

tric

t M

ill

Le

vie

s

Percent State Share

2012-13

2012-13 Mills

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1994-95 2013-14

General Fund Share of K-12 Total Program Funding

Limits May Even Result

in the Opposite of

What Was Intended

TABOR will likely require

that Colorado refund ALL

recreational marijuana taxes

in FY 15…but only for FY 15

Limits Beget

Workarounds

The College Opportunity Fund provides

a stipend to eligible undergraduate

students. Eligible undergraduate students

must apply, be admitted and enroll at a

participating Colorado institution. Both

new and continuing students are eligible

for the stipend.

The College Opportunity Fund provides

state-tax dollars to colleges and

universities on behalf of eligible

undergraduate students.

The Fund was created by an Act of the

Colorado State Legislature in May 2004

to heighten awareness that state tax

dollars are used to offset the costs of

undergraduate education.

Limits Beget Other

Limits/Mandates

And, Multiple

Limits/Mandates

Almost Always

Conflict

Limits Beget Elections (and in the process

undermine representative government)

Tax/Revenue increases

Retain excess revenue (“deBrucing”)

Create indebtedness

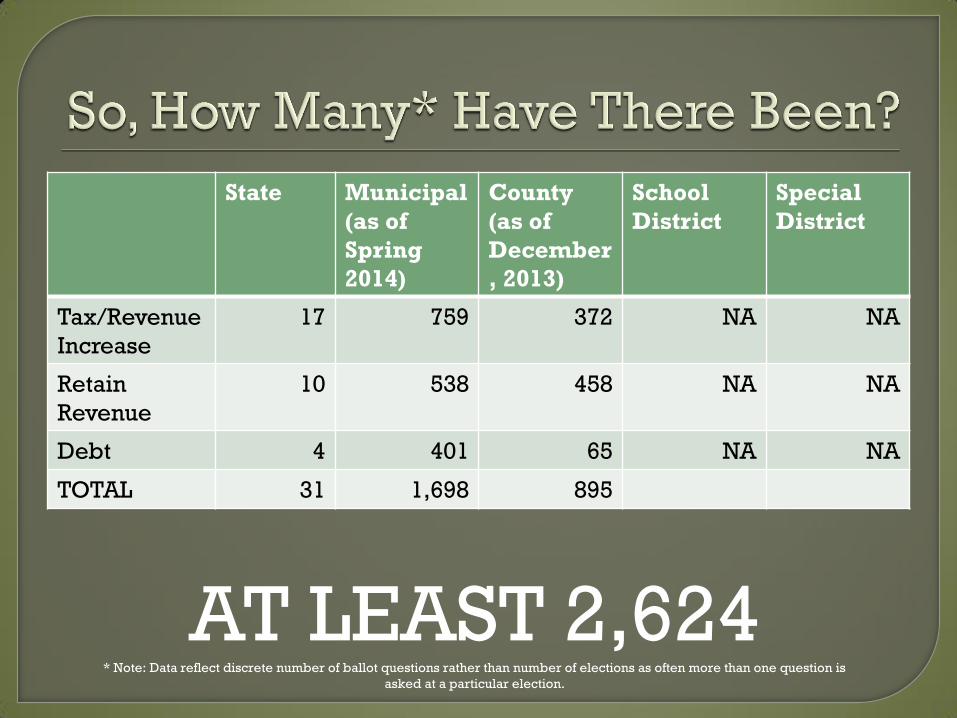

State Municipal

(as of

Spring

2014)

County

(as of

December

, 2013)

School

District

Special

District

Tax/Revenue

Increase

17 759

372 NA NA

Retain

Revenue

10 538 458 NA NA

Debt 4 401 65 NA NA

TOTAL 31 1,698 895

AT LEAST 2,624 * Note: Data reflect discrete number of ballot questions rather than number of elections as often more than one question is

asked at a particular election.

Limits Cast a State’s

Fiscal System in

“Soft Concrete”

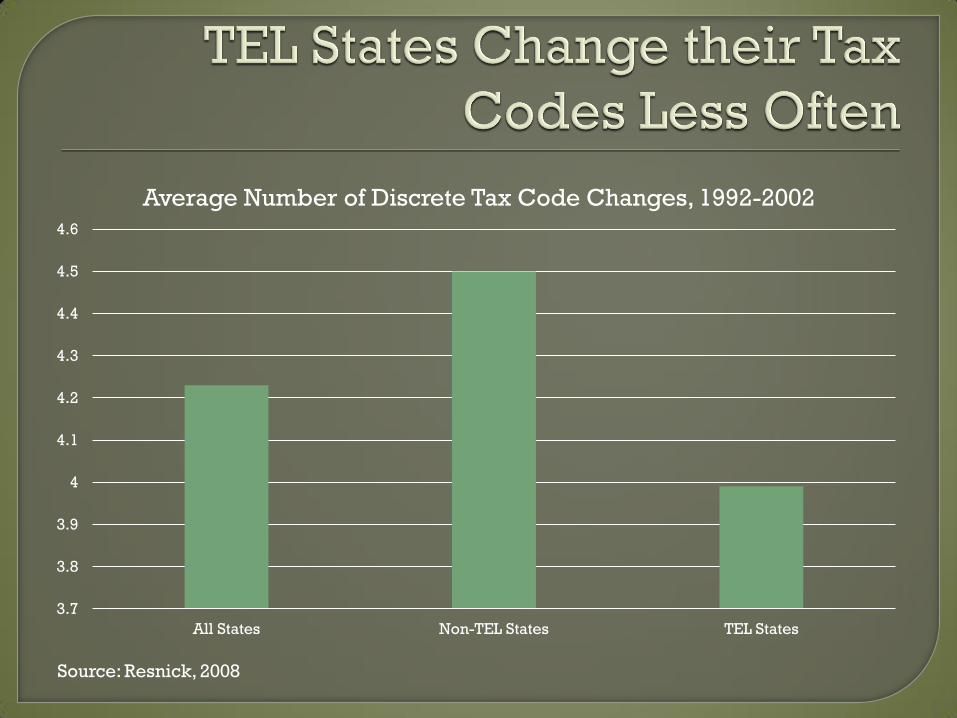

3.7

3.8

3.9

4

4.1

4.2

4.3

4.4

4.5

4.6

All States Non-TEL States TEL States

Average Number of Discrete Tax Code Changes, 1992-2002

Source: Resnick, 2008

Limits Hamper Flexibility (and lead

to a culture of learned hopelessness)

Limits Provide an

Accountability Shield

for Elected Officials

Hawaii

New Hampshire Tennessee Vermont

No major state

provision

limiting property

taxation

Phyllis Resnick

Lead Economist, Colorado Futures Center

Colorado State University

303.579.8992

http://coloradofutures.colostate.edu/

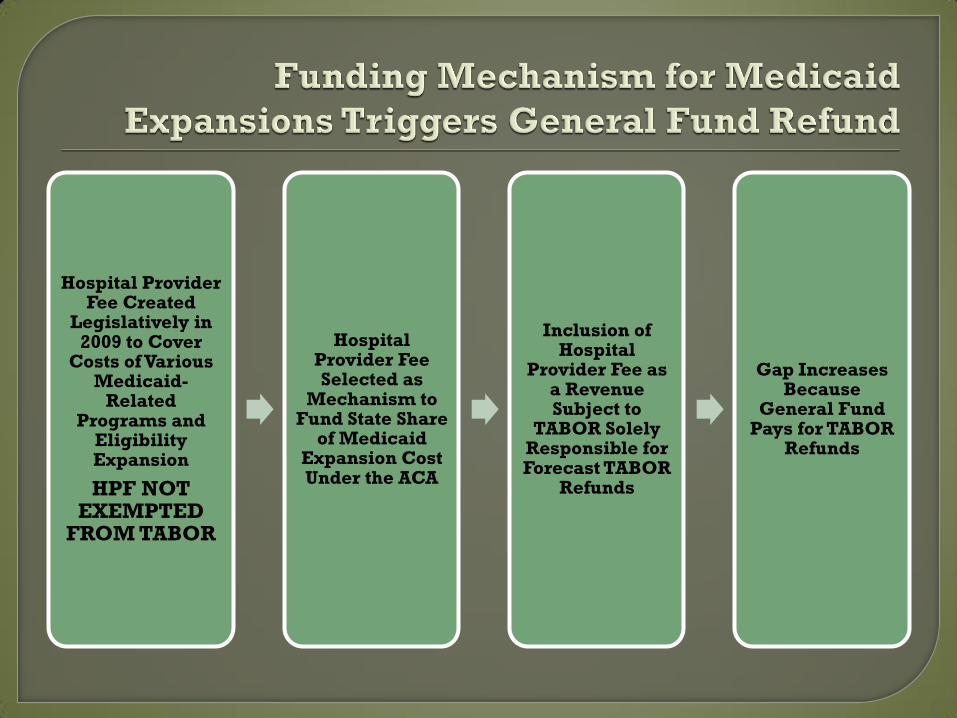

Hospital Provider Fee Created

Legislatively in 2009 to Cover

Costs of Various Medicaid-

Related Programs and

Eligibility Expansion

HPF NOT EXEMPTED

FROM TABOR

Hospital Provider Fee Selected as

Mechanism to Fund State Share

of Medicaid Expansion Cost Under the ACA

Inclusion of Hospital

Provider Fee as a Revenue Subject to

TABOR Solely Responsible for Forecast TABOR

Refunds

Gap Increases Because

General Fund Pays for TABOR

Refunds

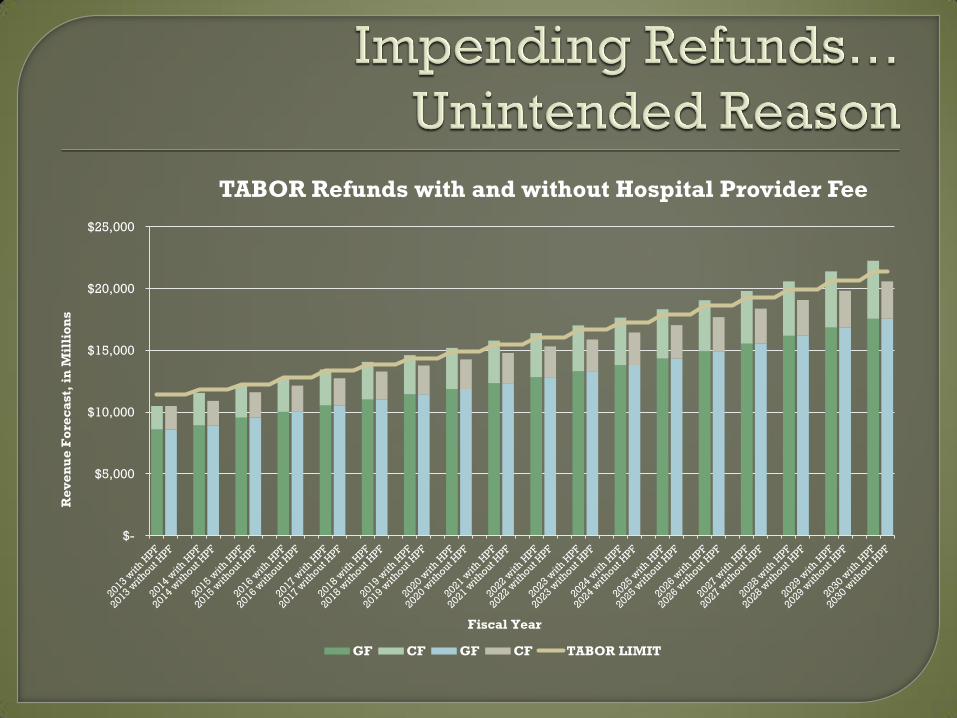

$-

$5,000

$10,000

$15,000

$20,000

$25,000

Re

ve

nu

e F

ore

ca

st,

in

Mil

lio

ns

Fiscal Year

TABOR Refunds with and without Hospital Provider Fee

GF CF GF CF TABOR LIMIT

Limits are Almost

Always Economically

Inappropriate

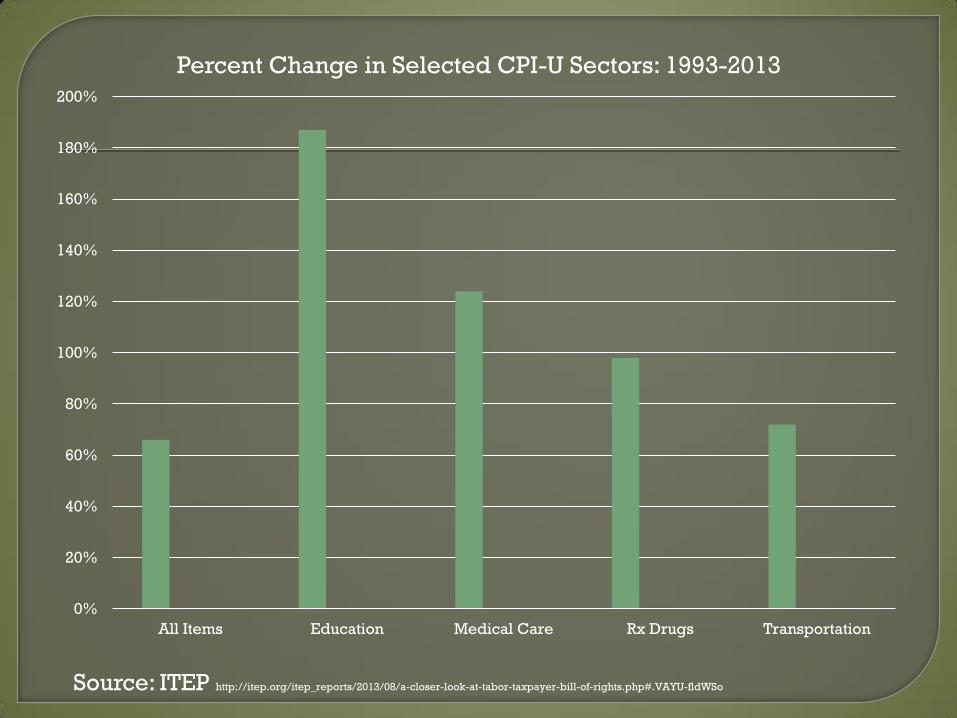

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

All Items Education Medical Care Rx Drugs Transportation

Percent Change in Selected CPI-U Sectors: 1993-2013

Source: ITEP http://itep.org/itep_reports/2013/08/a-closer-look-at-tabor-taxpayer-bill-of-rights.php#.VAYU-fldWSo