Embed Size (px)

DESCRIPTION

A presentation from the Law Society event at Padstow Lifeboat Station on 4 May 2011.

Citation preview

www.winterrule.co.uk

BUDGET 2011 TAX UPDATE

IMPLICATIONS FOR SOLICITORS AND THEIR CLIENTS

4 May 2011

Budget 2011 Tax Update

Speakers:

John Endacott

Steve York

2

www.winterrule.co.uk

Developments at Winter Rule 3

www.winterrule.co.uk

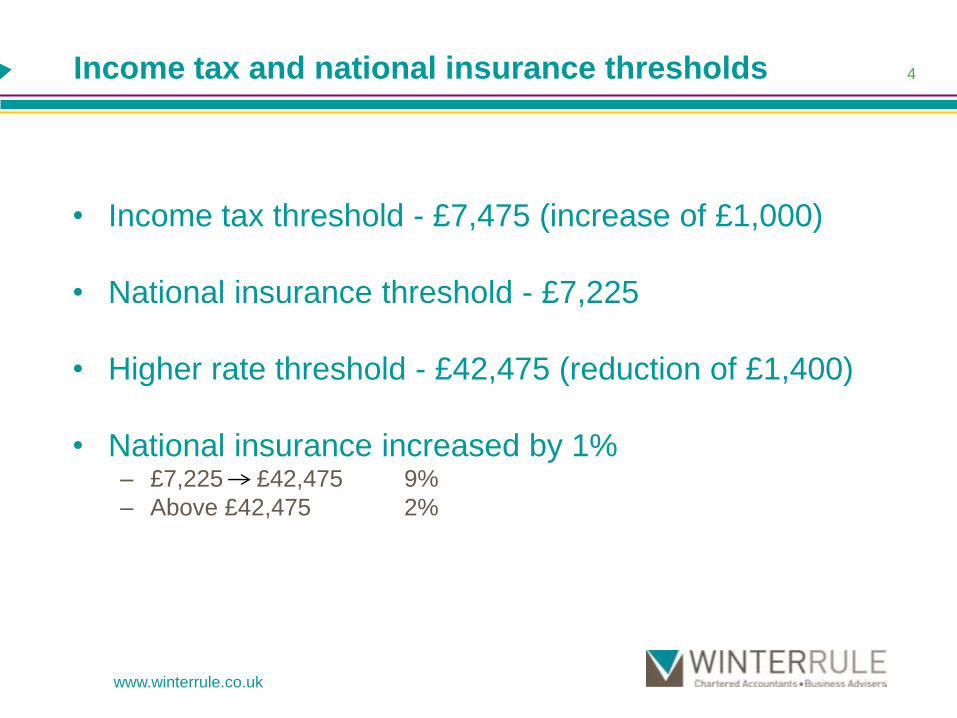

Income tax and national insurance thresholds

• Income tax threshold - £7,475 (increase of £1,000)

• National insurance threshold - £7,225

• Higher rate threshold - £42,475 (reduction of £1,400)

• National insurance increased by 1%– £7,225 £42,475 9%

– Above £42,475 2%

4

www.winterrule.co.uk

www.winterrule.co.uk

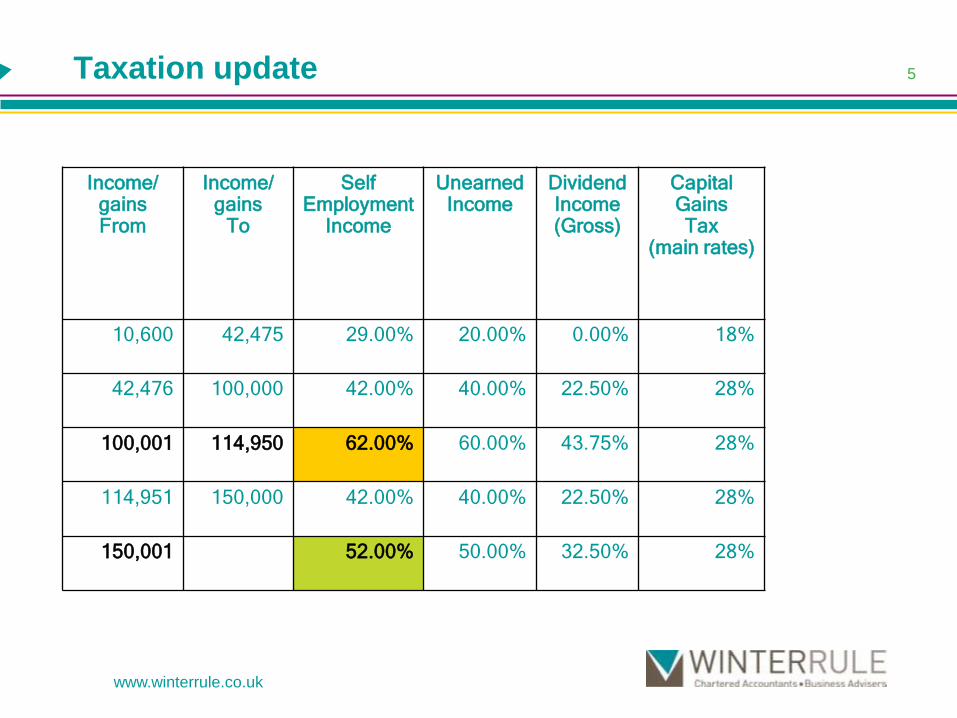

Taxation update

Income/gainsFrom

Income/gains

To

Self Employment

Income

Unearned Income

Dividend Income (Gross)

Capital Gains Tax

(main rates)

10,600 42,475 29.00% 20.00% 0.00% 18%

42,476 100,000 42.00% 40.00% 22.50% 28%

100,001 114,950 62.00% 60.00% 43.75% 28%

114,951 150,000 42.00% 40.00% 22.50% 28%

150,001 52.00% 50.00% 32.50% 28%

5

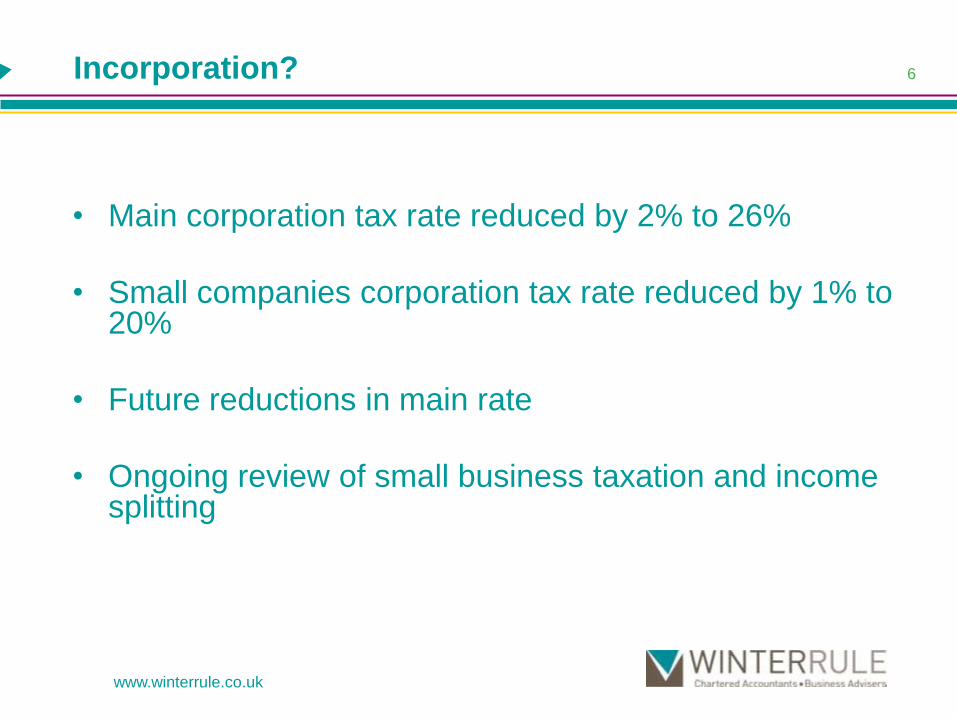

Incorporation?

• Main corporation tax rate reduced by 2% to 26%

• Small companies corporation tax rate reduced by 1% to 20%

• Future reductions in main rate

• Ongoing review of small business taxation and income splitting

6

www.winterrule.co.uk

www.winterrule.co.uk

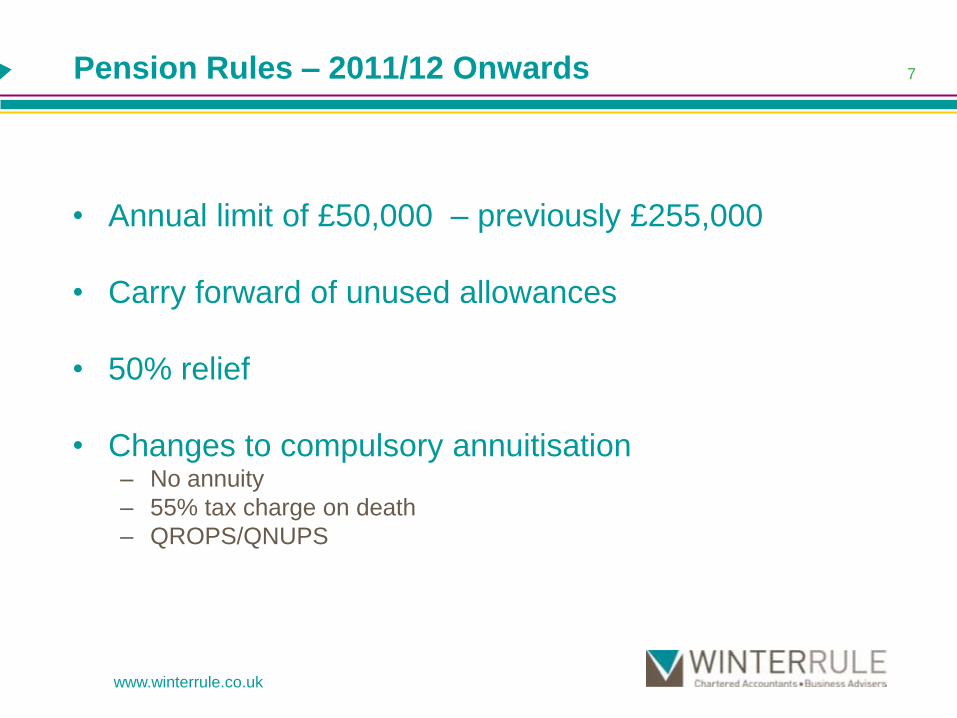

7Pension Rules – 2011/12 Onwards

• Annual limit of £50,000 – previously £255,000

• Carry forward of unused allowances

• 50% relief

• Changes to compulsory annuitisation– No annuity

– 55% tax charge on death

– QROPS/QNUPS

www.winterrule.co.uk

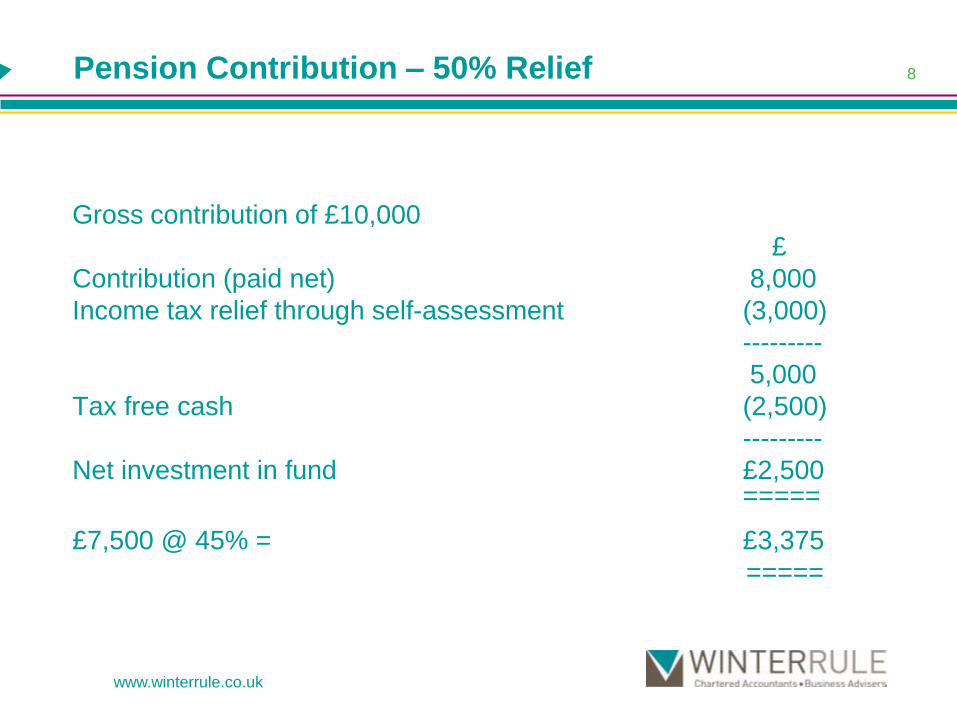

8Pension Contribution – 50% Relief

Gross contribution of £10,000

£

Contribution (paid net) 8,000

Income tax relief through self-assessment (3,000)

---------

5,000

Tax free cash (2,500)

---------

Net investment in fund £2,500=====

£7,500 @ 45% = £3,375

=====

www.winterrule.co.uk

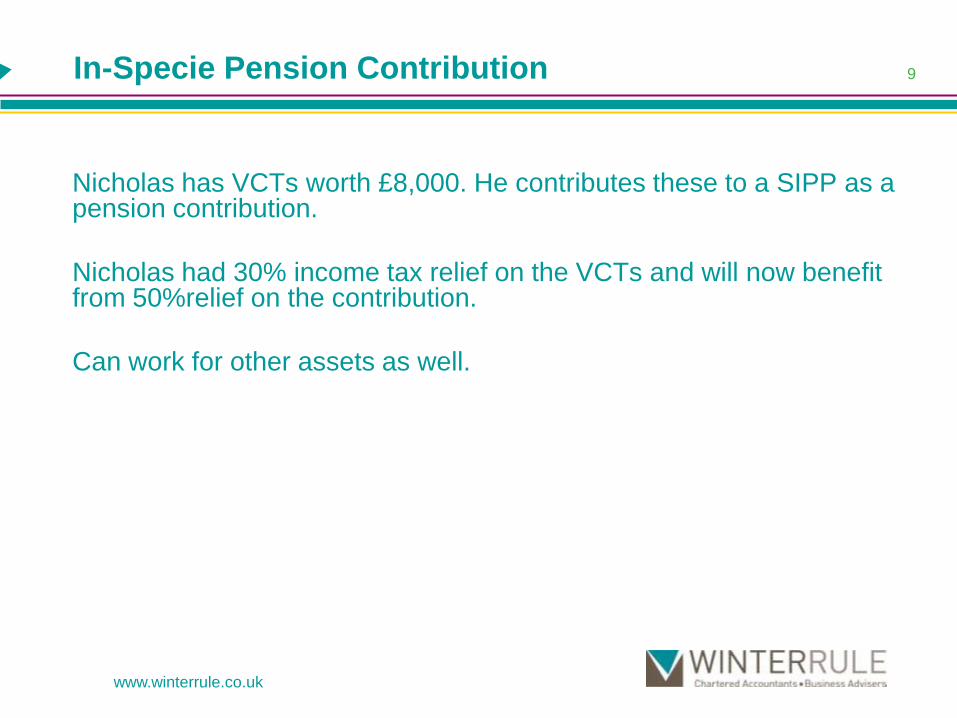

In-Specie Pension Contribution

Nicholas has VCTs worth £8,000. He contributes these to a SIPP as a pension contribution.

Nicholas had 30% income tax relief on the VCTs and will now benefit from 50%relief on the contribution.

Can work for other assets as well.

9

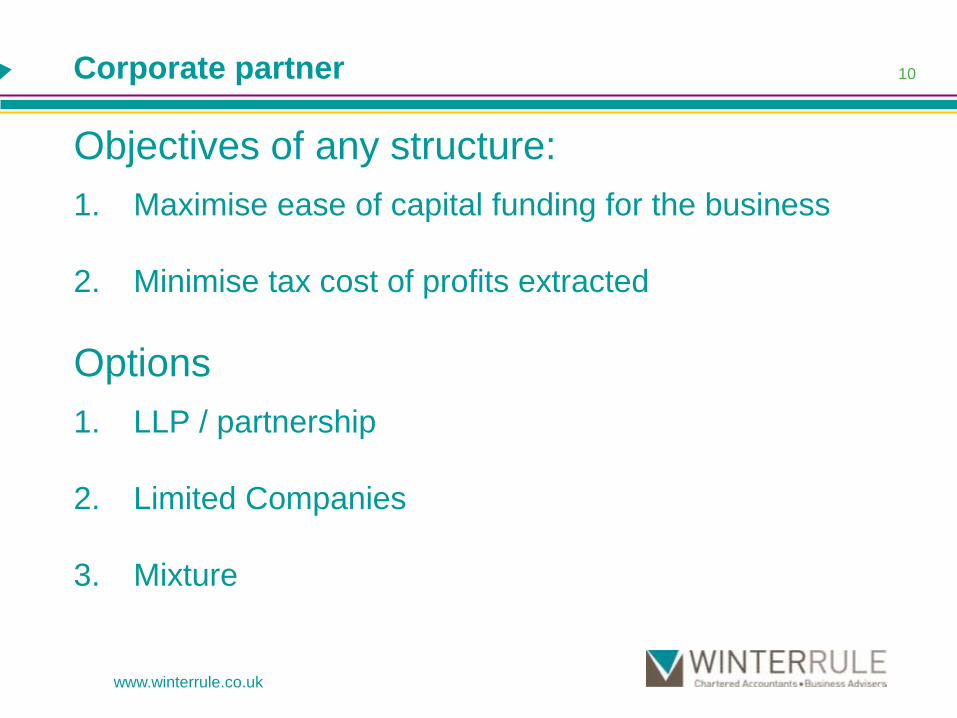

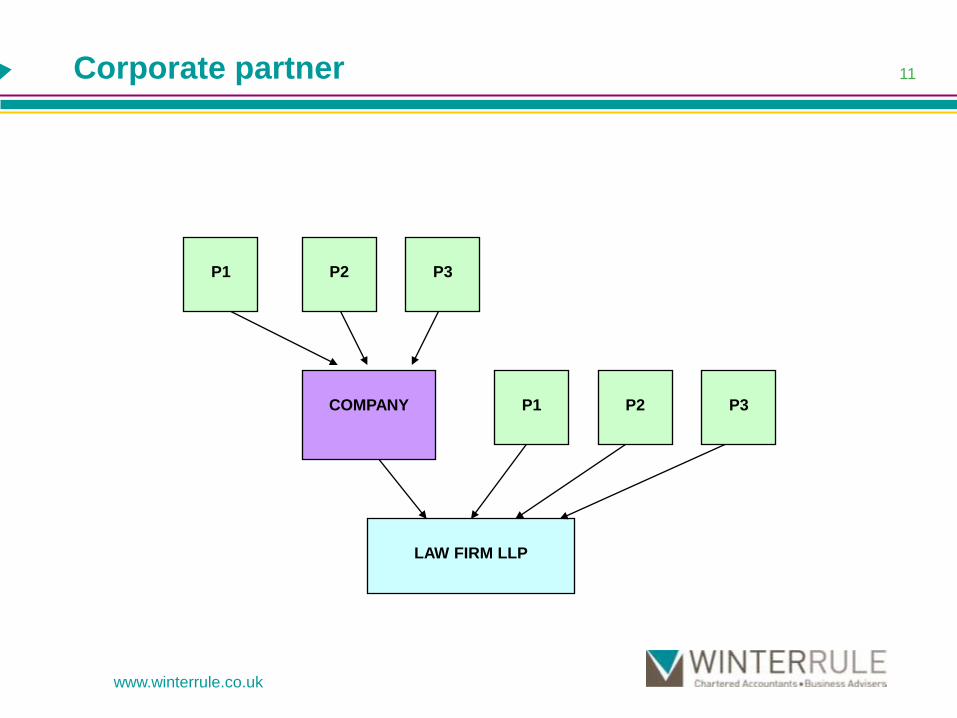

Corporate partner

Objectives of any structure:

1. Maximise ease of capital funding for the business

2. Minimise tax cost of profits extracted

Options

1. LLP / partnership

2. Limited Companies

3. Mixture

10

www.winterrule.co.uk

www.winterrule.co.uk

Corporate partner

LAW FIRM LLP

P3P2P1COMPANY

P3P1 P2

11

www.winterrule.co.uk

Corporate partner

Why?

• Provide capital to trading LLP post 20% / 26% tax rather than post 52% income tax.

• Refinance existing partner capital in the business to provide more cash (for investment or extraction)

• Potentially create longer term conversion of income to capital for tax purposes.

• Family involvement post October 2011

12

www.winterrule.co.uk

Other Points of Interest

• Tax free mileage allowance (up to 10,000 miles) increased to 45p per mile

• SDLT rate on residential properties over £1m – 5%

• Review of taxation of “very high value property”

• VAT registration threshold - £73,000

13

Budget 2011 Tax Update

Steve YorkTAX MANAGER

TAX PLANNING USING GIFT AID

14

www.winterrule.co.uk

Lifetime Charitable GivingGift Aid“If you can’t feed a hundred people, then feed just one” –Mother Teresa

15

Budget 2011 Changes

Millennium Gift Aid –Scrapped (for 989 years!)

“Donate tax refunds” box on tax return – Scrapped

16

www.winterrule.co.uk

Budget 2011 Changes

Tainted Charity Donations – no tax relief if arrangements in place

Charities no longer need signed gift aid declarations – First £5,000

Increased relief where donor receives a benefit from the donee charity

17

www.winterrule.co.uk

Tax Relief

• Basic rate tax relief at source

• Billy gives the RNLI £80. The RNLI is able to reclaim a further £20 from HM Revenue & Customs (HMRC). The RNLI ends up with £80+£20=£100

18

www.winterrule.co.uk

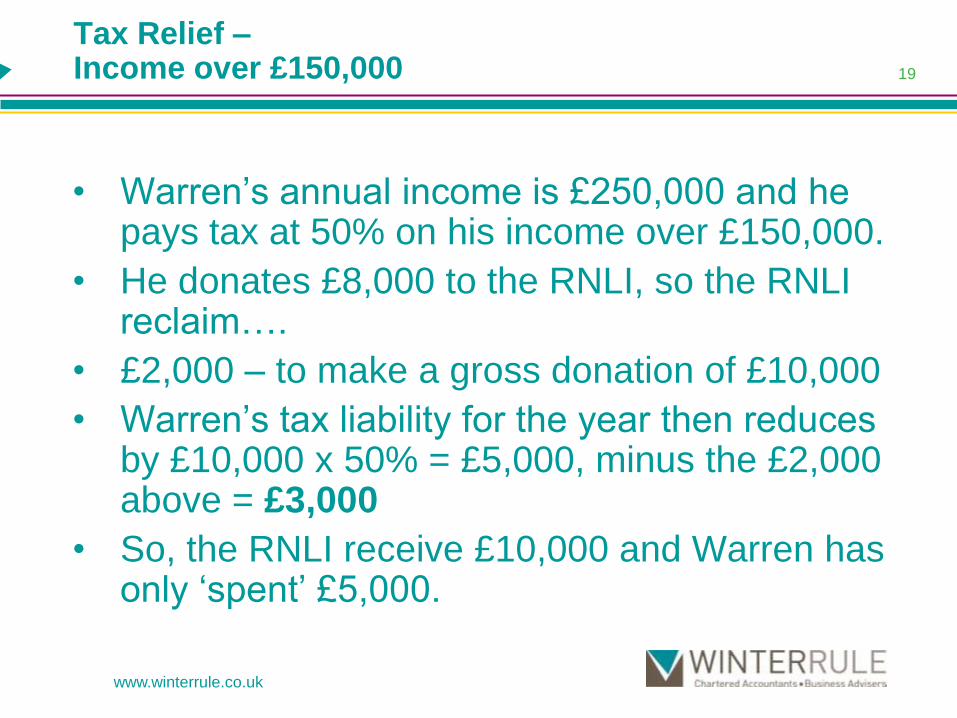

Tax Relief –Income over £150,000

• Warren‟s annual income is £250,000 and he pays tax at 50% on his income over £150,000.

• He donates £8,000 to the RNLI, so the RNLI reclaim….

• £2,000 – to make a gross donation of £10,000

• Warren‟s tax liability for the year then reduces by £10,000 x 50% = £5,000, minus the £2,000 above = £3,000

• So, the RNLI receive £10,000 and Warren has only „spent‟ £5,000.

19

www.winterrule.co.uk

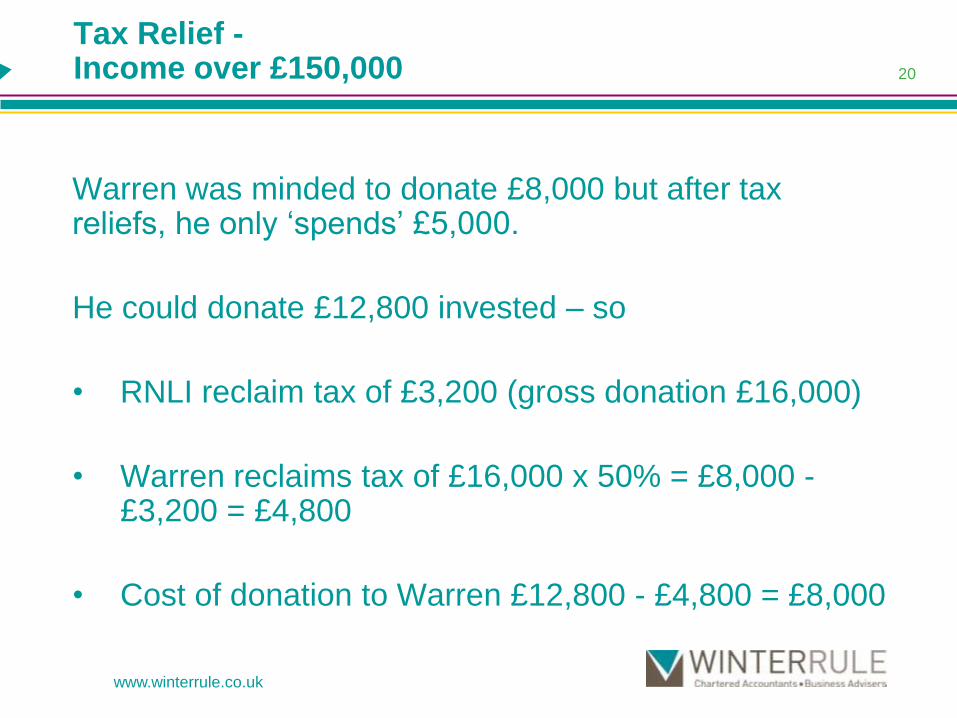

Tax Relief -Income over £150,000

Warren was minded to donate £8,000 but after tax reliefs, he only „spends‟ £5,000.

He could donate £12,800 invested – so

• RNLI reclaim tax of £3,200 (gross donation £16,000)

• Warren reclaims tax of £16,000 x 50% = £8,000 -£3,200 = £4,800

• Cost of donation to Warren £12,800 - £4,800 = £8,000

20

www.winterrule.co.uk

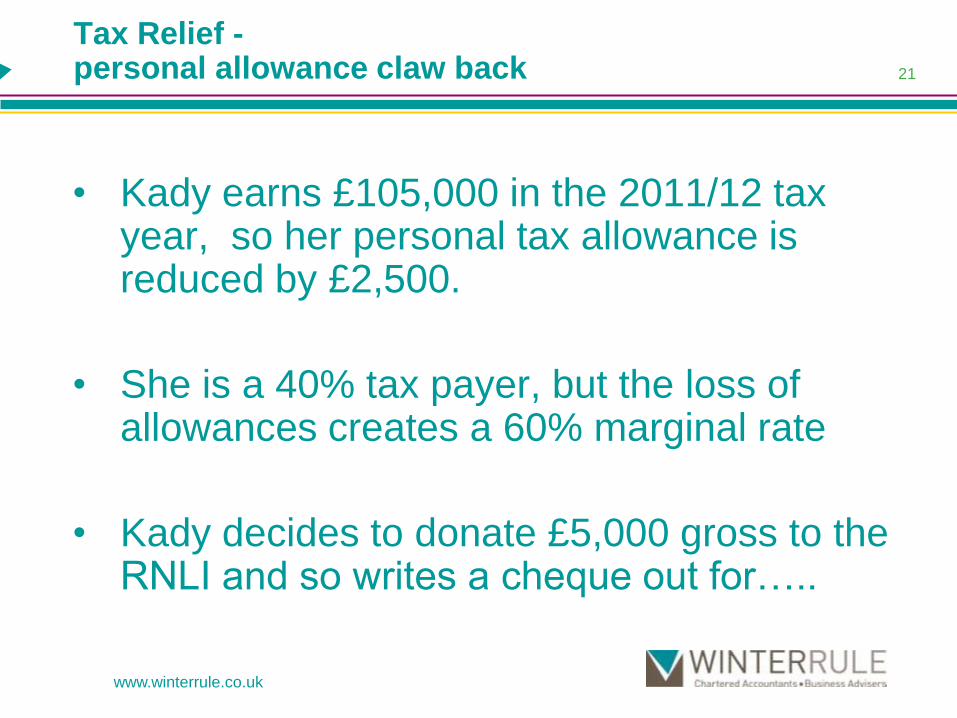

Tax Relief -personal allowance claw back

• Kady earns £105,000 in the 2011/12 tax year, so her personal tax allowance is reduced by £2,500.

• She is a 40% tax payer, but the loss of allowances creates a 60% marginal rate

• Kady decides to donate £5,000 gross to the RNLI and so writes a cheque out for…..

www.winterrule.co.uk

21

Tax Relief -personal allowance claw back (cont)

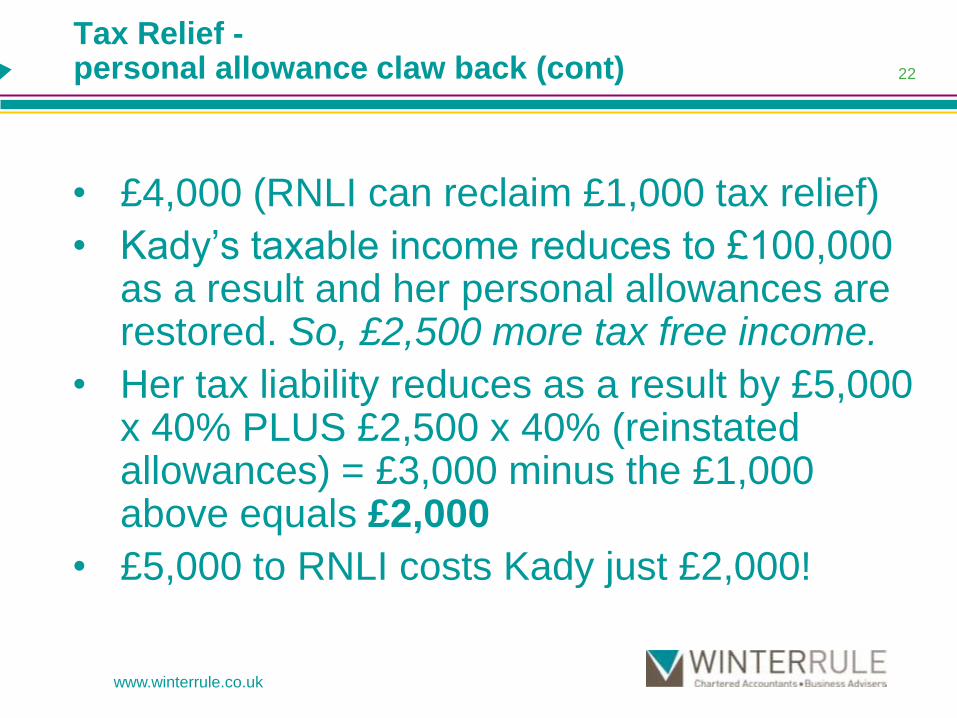

• £4,000 (RNLI can reclaim £1,000 tax relief)

• Kady‟s taxable income reduces to £100,000 as a result and her personal allowances are restored. So, £2,500 more tax free income.

• Her tax liability reduces as a result by £5,000 x 40% PLUS £2,500 x 40% (reinstated allowances) = £3,000 minus the £1,000 above equals £2,000

• £5,000 to RNLI costs Kady just £2,000!

www.winterrule.co.uk

22

Interaction with dividend income

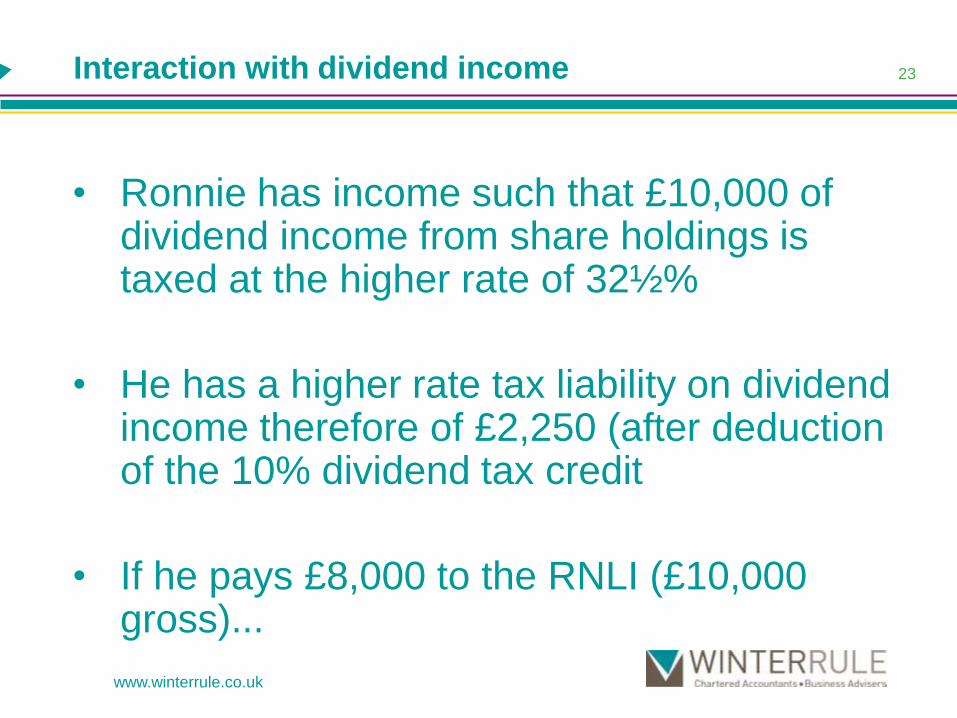

• Ronnie has income such that £10,000 of dividend income from share holdings is taxed at the higher rate of 32½%

• He has a higher rate tax liability on dividend income therefore of £2,250 (after deduction of the 10% dividend tax credit

• If he pays £8,000 to the RNLI (£10,000 gross)...

www.winterrule.co.uk

23

Ronnie continued

• His tax liability will be £2,250 less.

• So, he would have gifted £10,000 to the RNLI for a cost to him of £8,000 - £2,250 = £5,750

www.winterrule.co.uk

24

Tax Relief

• Gift aid relief can be useful for tax planning

• Extra tax relief may be available

• Careful timing of gifts can reduce tax liabilities – which tax year to donate in?

• Consider who should be making donations –eg husband or wife (who would receive the most relief?

• Charities could „sell‟ the availability of higher tax relief and possibly increase donations

www.winterrule.co.uk

25

Carry Back

• Gift aid relief is now just about the only tax relief that can be carried back to the previous tax year.

• Must be claimed on the earlier year tax return

• Donation must be before the tax return is filed and before the normal tax return deadline (31 January)

“Next to being shot at and missed, nothing is quite as satisfying as an income tax refund” – FJ Raymond

www.winterrule.co.uk

26

Word of Warning

• To be eligible for gift aid, the donor must pay at least as must in tax as is being reclaimed by the donee charity

• May get an unexpected tax bill for the extra if they do not.

• If in doubt, best not to claim gift aid

www.winterrule.co.uk

27

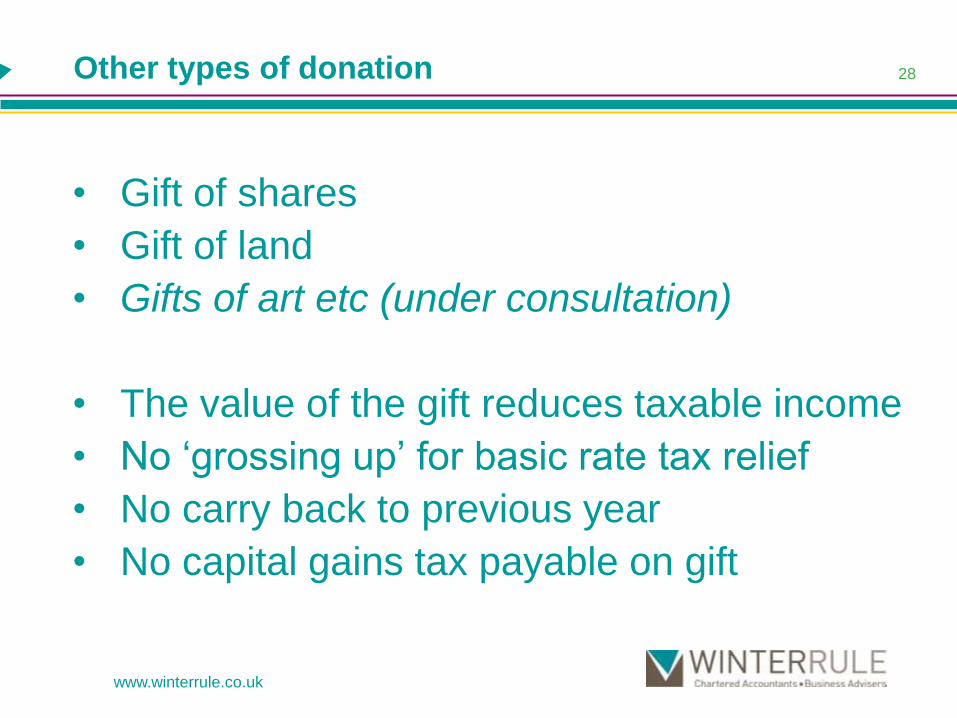

Other types of donation

• Gift of shares

• Gift of land

• Gifts of art etc (under consultation)

• The value of the gift reduces taxable income

• No „grossing up‟ for basic rate tax relief

• No carry back to previous year

• No capital gains tax payable on gift

www.winterrule.co.uk

28

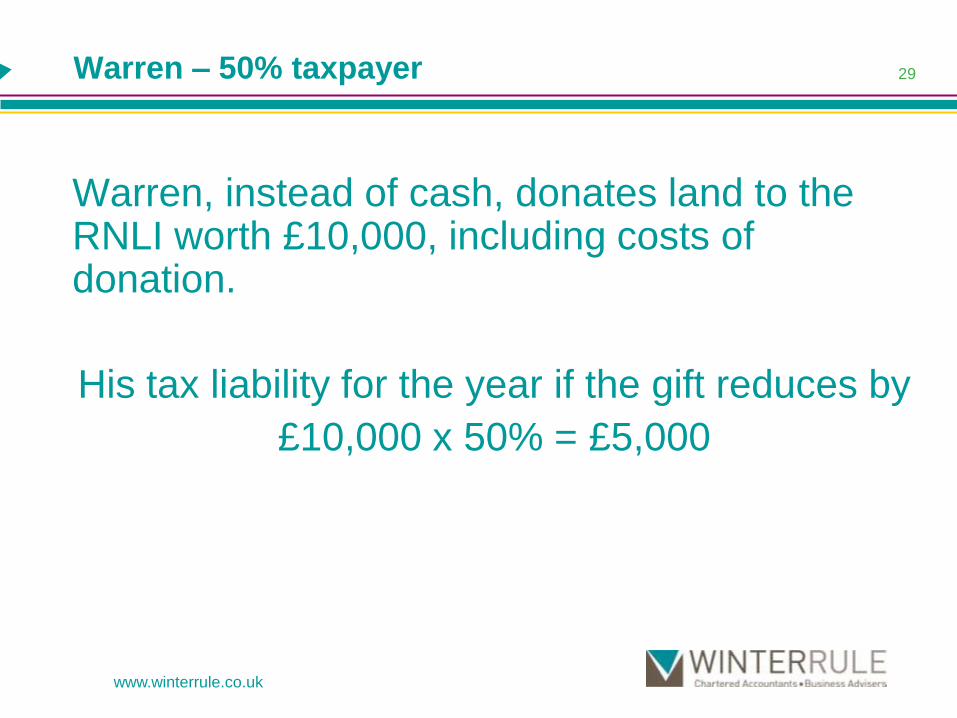

Warren – 50% taxpayer

Warren, instead of cash, donates land to the RNLI worth £10,000, including costs of donation.

His tax liability for the year if the gift reduces by

£10,000 x 50% = £5,000

www.winterrule.co.uk

29

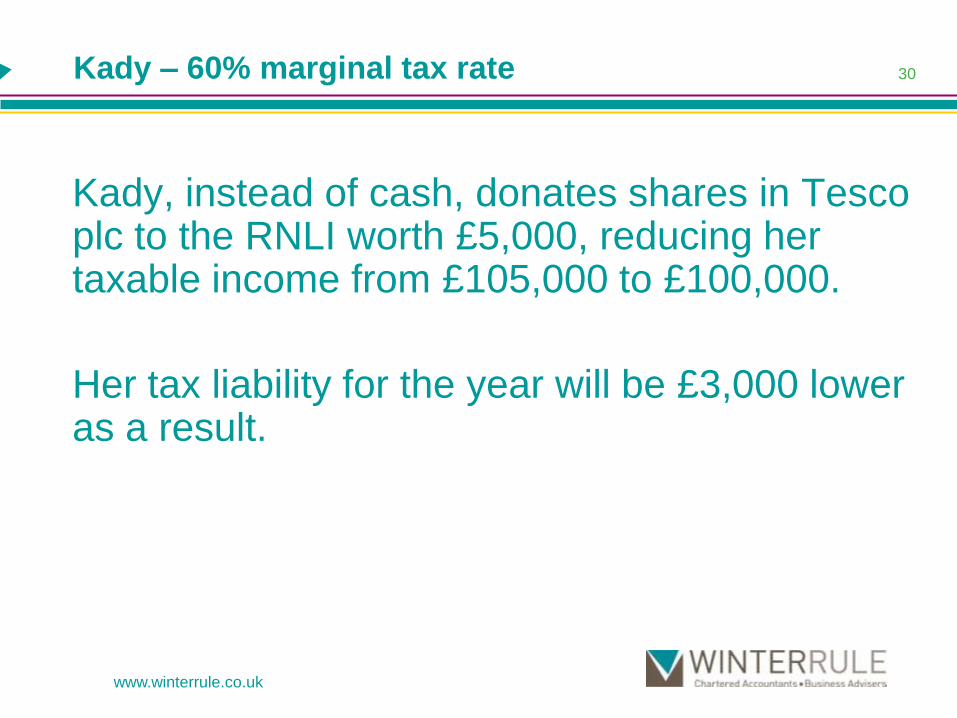

Kady – 60% marginal tax rate

Kady, instead of cash, donates shares in Tesco plc to the RNLI worth £5,000, reducing her taxable income from £105,000 to £100,000.

Her tax liability for the year will be £3,000 lower as a result.

www.winterrule.co.uk

30

Budget 2011 Tax Update

John EndacottTAX PARTNER

CHARITABLE GIVING AND THE DEATH ESTATE

31

Death Estate – Things to Watch for

• Specific legacies

• Gifts out of residue

• Interaction with:• Spouse exemption

• Business / agricultural property relief

• Watch domicile

www.winterrule.co.uk

The Charitable Exemption

• Exemptions for gifts to:• Charities

• Political parties

• National purposes

• Maintenance funds for historic buildings

33

www.winterrule.co.uk

Budget 2011 Announcement

• Charitable gifts > 10% of net estate

• 36% tax rate

• Deaths after 6 April 2012

• Consultation document – summer 2011

• Finance Bill 2012

34

www.winterrule.co.uk

Nil Rate Band

• Frozen until April 2015

• Then increasing at CPI

• Office for Tax Simplification (OTS) Report

35

www.winterrule.co.uk

Heritage Property

• Commonly paintings, sculptures, ceramics

• Conditional exemption for Estate Duty

• Public access

• Gifts in lieu

• New consultation on gifts of art work –summer 2011

36

www.winterrule.co.uk

Summary

• High tax rates here for the foreseeable future

• Business structuring planning can save tax

• Otherwise maximise pension contributions / gift aid payments

• Charitable giving likely to remain tax favoured for the foreseeable future

37

www.winterrule.co.uk

Budget 2011 Tax Update

LOWIN HOUSE

TREGOLLS ROAD

TRURO

CORNWALL

TR1 2NA

TELEPHONE: 01872 276477

EMAIL: [email protected]

38

www.winterrule.co.uk