Embed Size (px)

Citation preview

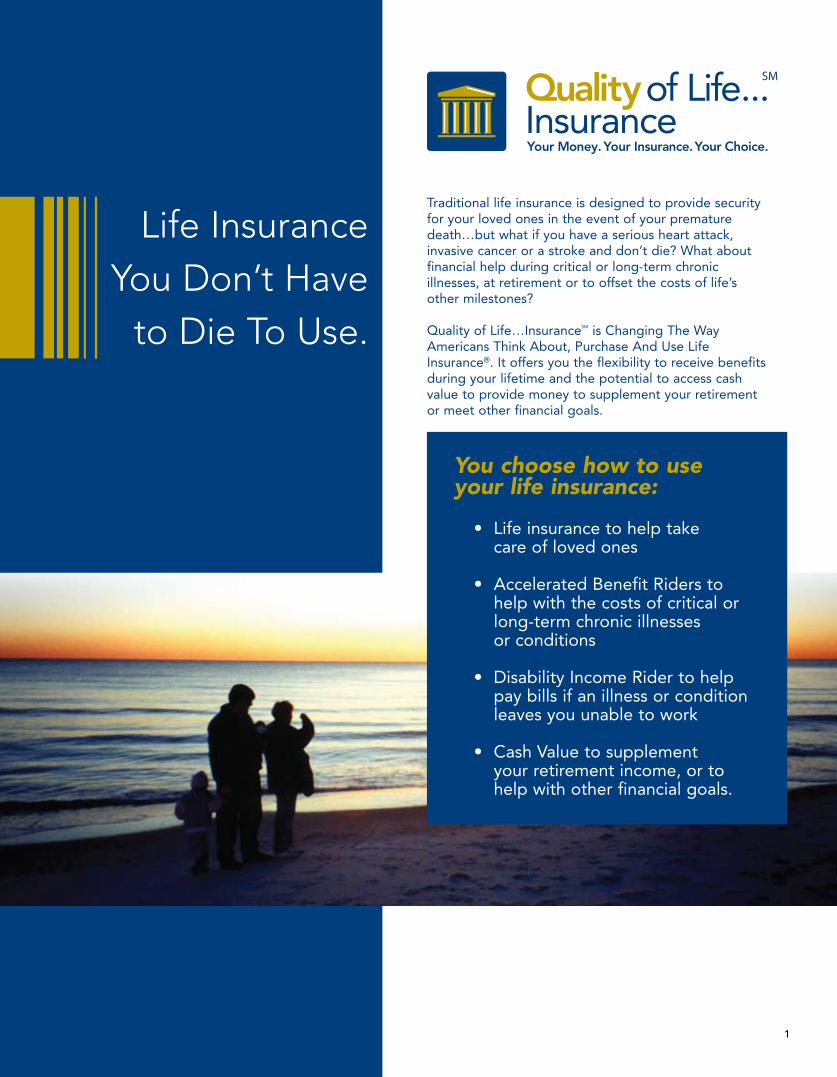

Life Insurance You Don’t Have

to Die To Use.

Traditional life insurance is designed to provide security for your loved ones in the event of your premature death…but what if you have a serious heart attack, invasive cancer or a stroke and don’t die? What about financial help during critical or long-term chronic illnesses, at retirement or to offset the costs of life’s other milestones?

Quality of Life…InsuranceSM is Changing The Way Americans Think About, Purchase And Use Life Insurance®. It offers you the flexibility to receive benefits during your lifetime and the potential to access cash value to provide money to supplement your retirement or meet other financial goals.

You choose how to use your life insurance:

• Lifeinsurancetohelptake care of loved ones

• AcceleratedBenefitRidersto help with the costs of critical or long-term chronic illnesses or conditions

• DisabilityIncomeRidertohelp pay bills if an illness or condition leaves you unable to work

• CashValuetosupplement your retirement income, or to help with other financial goals.

1

QualityofLife…InsuranceislifeinsurancewithNo-CostAcceleratedBenefitRiders.You and your agent will work together to decide which plan best fits your needs – allowing you to personalize a plan for the different stages in your life.

AGLAchoiceSM Performer – This plan is frequently chosen by responsible couples and parents, small business owners, and individual policyowners. Most often, customers who purchase an AGLAchoice Performer plan want access to their accumulated cash value in case of an emergency, or to use for a future major event (such as college funding or a dream vacation), and want to accomplish their goals on a defined budget.

AGLAchoiceSM Protector – This plan can be an excellent alternative to a traditional Term Insurance policy. Clients who purchase an AGLAchoice Protector plan are typically younger than the average life insurance buyer, and their goals often include protecting a mortgage and providing a dependable monthly income in the event of a disability. AGLAchoice Protector buyers are often young families just starting out in life who want to provide for their families, but are often on a tight budget. This product provides coverage at an affordable rate.

AGLAchoiceSM Accumulator – This plan offers clients the best potential to accumulate substantial cash value over time. AGLAchoice Accumulator buyers are typically couples and parents, small business owners or single policyowners who are more financially secure than the average life insurance buyer, and may want to use their life insurance cash value to supplement their retirement on a tax favored basis.

AGLA ConsumerChoice TermSM – With this plan, you choose the benefit period that fits your needs – either 10 years, 12 years, or any period from 15–35 years. AGLA ConsumerChoice Term covers a broader range of specific life events and offers a powerful new way to customize your life insurance plans to anticipate known future events. This policy is a good choice for families who need to cover temporary insurance needs, such as making sure a mortgage is protected, providing college tuition for their children or covering start-up costs from a small business. And if your circumstances change, this policy may be converted to permanent coverage.

TheNo-CostAcceleratedBenefitRidersthatmakeQualityofLife…Insurancesoinnovative are included on all of these plans. Your agent can help you decide which plan works best for you.

“Quality of Life...Insurance could be a huge benefit to my husband and I. We both do freelance work, so we don’t have a big company policy with a lot of benefits. Being able to customize a policy for each of us sounds great. It would give me peace of mind to be able to provide for my children, knowing that a lot of those concerns would be addressed and taken care of.” — Lucinda,

Focus Group Participant

What Exactly Is Quality of Life… Insurance?

2

Accelerated Benefit Riders:

“About 2.2 million Americans experienced medical bankruptcy in 2001. Among those illnesses that led to bankruptcy, out of pocket costs averaged $11,854 since the start of illness; 75% had insurance at the onset of illness.”1

Even with the best plans, the unexpected can happen – such as a critical illness or a long-term chronic illness or condition. The costs associated with treatment, as well as possible income lost if you are unable to work, can threaten your quality of life. Quality of Life...Insurance is designed to let you use your life insurance benefits when you need them most. This innovative life insurance policy can help pay the direct costs of treatment for qualifying illnesses or conditions – or any other indirect expenses.

ChronicCare Income Accelerated Benefit RiderThe potential need for long term care and how to pay for it is a major concern for families today. In a 2008 study, the average annual cost for a private room in a nursing home was $76,460 - up 17% since 2004.2Bythetimeyouandyourfamilyneed care, chances are this cost will have increased even more.

People buy long term coverage for various reasons: • They don’t want to be a burden on their families. • They want access to quality care. • They want to protect their savings. • They want control over their own healthcare situation.

The ChronicCareIncomeRider3(CCIR)isanacceleratedbenefitriderthatisdesigned to be used as an economical alternative to traditional, cost-prohibitive long term care policies. It is available for an additional premium cost, and offers valuable benefits should you be diagnosed with a chronic illness or condition:

• You choose the amount of monthly benefit you want and how long that benefit would be payable to you. You can choose any benefit amount ranging from $1,000 to $8,400 per month (in $100 increments), with available payout periods of 24, 36, 48 or 60 months.

• Unlike many long term care policies, you choose how to spend your benefit – on nursing home care, home health care or anything else you decide. Your benefits are payable without regard to expense incurred or confinement.

Another attractive and affordable feature you should consider is the Extension of BenefitRider4, which could help provide protection in the event of an extended illness.AttheendoftheCCIRbenefitperiod,thisridercanpaythesamebenefitamount for an additional time period of your choice without further reducing your remaininglifeinsurancebenefit.ACostofLivingAdjustmentRidermayalsobeadded,whichincreasestheExtensionofBenefitRideramountovertime.

PLEASE noTE: The ChronicCareIncomeRiderisavailableonAGLAchoicePerformer,AGLAchoiceProtectorandAGLAchoice Accumulator in most states. It is not available on AGLA ConsumerChoice Term.

Preserving Your Quality of Life

“ Quality of Life...Insurance would be important for me and my family because you never know how your income situation is going to change if you or someone in your family became ill. You can never anticipate what could happen and when you would need protection. Quality of Life...Insurance is an all-encompassing product…and I think it’s a very flexible product.” — Pat,

Focus Group Participant

“One of my family members needed long term care, so I saw what devastation it caused financially. They were paying $2,000 or $3,000 a month for the care, which they really didn’t have, and eventually ended up losing their home. I feel like in their last days it really took a lot of dignity away from them, and I would never want to be in that situation.” — Brian,

Focus Group Participant 3

FooTnoTES

1. “Marketwatch:IllnessandInjuryasContributorstoBankruptcy.”HarvardLawSchool,2005.

2. Genworth Financial 2008 Cost of Care Study.

3. ThebaselifeinsuranceamountwouldbereducedbythetotalamountpaidoutundertheCCIR.PleasenotethatthetotalCCIRamountthatmaybeappliedforislimitedbythefaceamountoftheinsured’slifeinsurancecoverageavailable to accelerate, i.e., the total potential benefits that may be received cannot exceed the life insurance coverage.

4. ToqualifytoreceiveEOBriderbenefits,thepolicyownermustbecertifiedchronicallyillattheendoftheinitialbenefit period he or she elected under the ChronicCareIncomeRider.

no-CostAcceleratedBenefit Riders

Chronic Illness Accelerated Benefit Rider1

This rider allows the owner to accelerate some or all of the Insured Person’s base life insurance benefit in the event the insured is diagnosed with a chronic illness or condition.TheChronicIllnessAcceleratedBenefitRiderisincludedoneveryQuality of Life…Insurance policy.

Like the ChronicCareIncomeRider,itprovidesbenefitsintheeventofachronicillness. With this rider, however, the specific benefit amount or benefit period is not selected in advance. The amount of benefit received is determined by the company when a claim is filed, and is payable to the insured as a lump sum, not in monthly installments.

To qualify for benefits under the ChronicCareIncomeRiderortheno-cost ChronicIllnessAcceleratedBenefitRider,theinsuredmustbediagnosedwith a chronic illness.

A chronic illness is an illness or physical condition that was initially certified by a licensed healthcare practitioner within the past 12 months and affects the insured person so that he or she: • IsunabletoperformatleasttwoofthesixActivitiesofDailyLiving(ADLs); or • RequiressubstantialsupervisionbyanotherpersontoprotecttheInsured Person from threats to health and safety due to severe cognitive impairment.

ADLs:Bathing,Dressing,Toileting,Transferring,Continence,Eating

Critical Illness Accelerated Benefit Rider1

This rider allows the owner to accelerate some or all of the Insured Person’s base life insurance benefit in the event the insured is diagnosed with a critical illness orcondition.TheCriticalIllnessAcceleratedBenefitRiderisincludedonevery Quality of Life…Insurance policy.

A critical illness or condition is defined as one of the following:• HeartAttack• Major Organ Transplant• Stroke • Invasive Cancer• Blindness• EndStageRenalFailure• Paralysis • Amyotrophic Lateral Sclerosis (ALS – or Lou Gehrig’s disease)

Terminal Illness Accelerated Benefit Rider1

This rider allows the owner to accelerate some or all of the Insured Person’s base life insurance benefit in the event the insured is diagnosed with a terminal illness or condition.TheTerminalIllnessAcceleratedBenefitRiderisincludedoneveryQuality of Life…Insurance policy.

A terminal illness is defined as an illness or physical condition that is certified by a physician to be reasonably expected to result in the insured’s death within 24 months2 from the date of certification.

“ This policy gives my husband and me peace of mind because we know there’s going to be money there if we need it. We bought this policy because it’s not just for when we die, we can use it while we’re still alive.”

— Betty, Quality of Life...Insurance Policyowner

4

FooTnoTES

1. ThemaximumamountoflifeinsurancebenefitthatmaybeacceleratedissubjecttotheMaximumElectedDeathBenefit,whichisthelesserofthecurrentlifeinsurancebenefitoralifetimemaximumamountof$1,500,000.Benefiteligibilityissubjecttolimitationsand/orWaitingPeriod,EliminationPeriodandexclusionrequirements.Please read the rider carefully for a complete definition of benefits and the conditions applying to each rider.

2. 12monthsinPennsylvaniaandD.C.

Accelerate means to receive a portion of the base life insurance benefit early, while the Insured is still alive, in the event of a covered illness or condition. There are several factors to consider before deciding whether acceleration is right for you:

• Acceleration will reduce the Insured Person’s base life insurance benefit and policy values if any. This means there will be less benefit paid when the Insured dies.

• The actual payment received will be less than the portion of the base life insurance benefit accelerated. This means you will not get the full amount you accelerate because 1) it is paid prior to death, 2) it is subject to an actuarial discount, administrative charge and payment of any unpaid but due policy premiums.

• TheamountofanAcceleratedBenefitRiderbenefitthatmaybeofferedisdetermined by the company after a claim is submitted and when accepted, is payable to the owner in a lump sum. The amount of an offered benefit will, in significant part, be dependent upon any change in mortality of the Insured Person in question between the time the applicable life insurance policy with AcceleratedBenefitRiderswasunderwrittenandthetimeanyparticularAcceleratedBenefitRiderclaimisfiledandconsidered.Changesinhealthandother factors will have varying effects on the mortality of different Insured Persons. Circumstances will vary among individual Insured Persons.

• For an accelerated benefit to be payable, the policy must be in force on the date any accelerated benefit is paid (and not just on the date of any qualifying illness or condition). You should consider your options carefully before ever letting your coverage end for any reason, including the non-payment of premium, especially while a claim for any accelerated benefit is pending.

• If you are eligible, you will be offered the opportunity, when you receive your benefit election form, to purchase coverage to replace the amount accelerated. However,thecostsofthatcoveragemaybesignificantlyhigher.

noTE: Ridernames,benefitsanddefinitionsmayvaryinsomestatesand/ornotbeavailableinallstates.

5

John is a 40-year-old male who purchases a $250,000 AGLAchoice Accumulator policy. John doesn’t use tobacco, and qualifies for standard underwriting. He also purchases the ChronicCare Income Rider and elects a benefit of $3,000 per month for 36 months, and adds the Extension of Benefit Rider for an additional 36 months of extended coverage.

Here are some hypothetical examples of how John might use his Quality of Life...Insurance policy during his lifetime:

Ten years after purchasing the policy, John is 50 when he suffers a serious heart attack.

John is now 60 and recovered from his heartattack.However,he now develops a chronic illness that leaves him unable to perform 2 of the 6ADLs.

John is 66 when he is diagnosed with terminal cancer.

Hediesatage67.

Upon his retirement at age 65, John decides to go on an extended vacation.

John passes away unexpectedly, shortly after returning from his trip.

$250,000

$200,000

$92,000

$250,000

$250,000 lessloan balance

PLEASE noTE: ThelifeinsuranceofferedwithAcceleratedBenefitRidersisnotstand-alonelongtermcareinsurance,disabilityincomeinsurance or other insurance designed to cover specific costs associatedwithanillnessorcondition.Receivingbenefitsundertherider will reduce the amounts available for future acceleration under itandanyotherAcceleratedBenefitRiderattachedtothepolicy.Itwill also reduce the base life insurance benefit and the funds available to supplement retirement or other needs. The benefits paid under the rider may be less than what is needed to cover all of the costs associatedwithanillnessorcondition.Benefitamountsreceivedunderthe ChronicCareIncomeRiderandExtensionofBenefitRiderarechosen in advance by the owner and are payable without regard to actual expenses incurred or confinement. Even though accumulated cash value may be available to supplement retirement, it should not be relied upon as a significant source of retirement income. Your AGLA agent can provide you with details.

The values in this chart were calculated using current, non-guaranteed interest and cost of insurance rates, monthly administration fees and premium expense charge percentages as of January 2009. Therefore, they may be changed at any time for any reason. Your results may be more or less favorable.

* Assumes payment of premiums necessary to keep policy in force. Premium assumed for sample policy is $240.21 monthly.

**BenefitsundertheAGLAChronicCareIncomeRideraresubjecttolimitations and exclusions, as stated in the rider.

EachpaymentofaMonthlyBenefitAmountundertheAGLAChronicCareIncomeRiderwillreducetheinsured’sbaselifeinsurancebenefit and policy values. This means there will be less benefit paid when the insured dies. Your policy contract will have more information regarding how payment of benefits under the rider can impact your policy values. Please read it carefully.

BenefitsundertheAGLAChronicCareIncomeRiderareintendedtobeexcludedfromfederalgrossincomeundersections7702Band101(g)oftheInternalRevenueCode.Thatnotwithstanding,thebenefitspaidunder the rider may still be deemed as taxable. If so, you may incur a tax obligation. Neither the company nor its agents are authorized to offer you tax advice. You should consult your accountant, attorney or other qualified tax consultant to assess the impact of any benefit paid under the rider.

Event Base life insurance amount in force

Life Event 1: No-cost Critical Illness Accelerated BenefitRider

Life Event 2: ChronicCare IncomeRider

John dies at age 67

What if John hadstayed healthy?

Example

Life Event 3: No-cost Terminal Illness Accelerated BenefitRider

6

John considers all his options and decides to accelerate $50,000 of his $250,000 policy for financial assistance during his recovery.

John decides to use his ChronicCareIncomeRiderbenefits,and files a claim to begin receiving $3,000 a month for 36 months – which is the benefit amount and benefit period John chose when he purchased his policy.**

John doesn’t want his family to be burdened with medical bills after he passes away, so he decides to file a claim under his Terminal IllnessAcceleratedBenefitRidertoaccelerate another $50,000 of his remaining life insurance coverage.

Since no accelerated benefits have been elected, and there are no outstanding loans, John decides to access his accumulated cash value.

John’s family files a claim for the remainder of his life insurance benefit.

When John files his claim, AGLA determines his benefit based on the severity of his illness and how much it affects his life expectancy. Hisclaimoffermayrangefromaminimumof $3,228 to a maximum of $39,079.*

For example, if John’s heart attack was mild and he is expected to fully recover, he may be offered a lesser amount. If his heart attack was severe and has significantly shortened his life expectancy, he will be offered a larger amount.

After the 90-day elimination period, John receives $3,000 for 36 months, which helps him pay for home health care.

At the end of the three years, John is still chronicallyill,andhisExtensionofBenefitRiderpaymentsbegin.Hereceives$3,000amonth for an additional 36 months.

The company makes an offer to John to receive $44,100.

Johnreceives$50,000fromAGLA.Heandhis wife truly have the vacation of a lifetime and travel the globe for two months.

John’s beneficiaries (his wife, son and daughter) each receive their shares of $196,955, which is the amount of John’s life insurance coverage of $250,000 less the loan balance of$53,045.Hiswidowusesherportionto helpsupplementherretirementneeds.His son makes a down payment on a family vacation home. John’s daughter helps pay college expenses for John’s grandson.

John’s heart attack was serious, so the company offers him $22,759.*

John decides to accept the company’s offer, and accelerates $50,000 of his base life insurance benefit, which reduces his remaining coverage to $200,000.

John’s base policy is reduced only by the benefits he receives from the ChronicCare IncomeRider–notbythepaymentsfromhisExtensionofBenefitRider.Eventhoughhe has received a total of $216,000, his base life insurance is reduced by only $108,000($3,000x36months).Henowhas$92,000 life insurance remaining.

If John accepts the company’s offer, his life insurance will be reduced to $42,000. When John passes away at age 67, his family will receive the remainder of his death benefit – $92,000 if he did not accept the company’s offer, or $42,000 if he did.

$50,000 is withdrawn from the policy as a preferred loan, where the interest charged for the loan is the same as the interest credited.Hislifeinsurancecoverageis now $250,000 less the loan balance at time of death.

John, his wife, his children and grandchildren all benefit from John’s policy, which is terminated after the payments are made to the beneficiaries.

Action Result Effect on Policy

How Does It Work?

7

How Long Could You Financially Survive an Extended Disability?

Consider the Facts:

• 51.2 million people in American have some level of disability. They represent 18 percent of the population.1

• Men have a 43 percent chance of becoming seriously disabled during their working years, while women have a 54 percent chance.2

• A disabling injury occurs every 1.5 seconds.3

• The average disability claim lasts almost 13 months, and mortgage foreclosures due to disability occur 16 times as often as they do for death. Yet, more than 40 percent of full-time workers do not have coverage in the event of a short or long term disability to protect against a loss of income.4

Despite all this, isn’t it amazing that most Americans have little or no disability coverage?

1. U.SCensusBureau,FactsforFeatures,July26,20062. “WhyDisability”booklet,publishedbyNationalUnderwriter3. National Safety Council: www.nsc.org as of April 20044. Financial Planning Association, Medical Issues, www.fpanet.org as of February 2007

“ If you didn’t have good short term disability insurance through your employer, your bills would continue to grow while you were getting better. With this plan, you don’t have that financial strain hanging over you.”

–– April Quality of Life…Insurance Policyowner

DisabilityIncome Rider

8

What AreYour options?

Add the Disability Income Rider to Your Policy

Pays you a portion of your income if you become disabled.

Plan options Benefits would begin after • 2YearBenefitperiod-90Days • 5YearBenefitperiod-180Days

Plan Details: • Issue ages 18-55 • Minimum monthly benefit - $500 • Maximum monthly benefit* is the lesser of the following amounts: - $5,000 for the 2-year option, $3,500 for the 5-year option - $20 per $1,000 of life insurance purchased, rounded to the nearest $10, or - Percentage of Gross Monthly Income (see agent for details)

Deplete Your SavingsAssuming 10 percent of income is saved each year, it will take 10 years to save one year’s worth of income. Doyouhaveenoughinsavings to last during an extended disability?

Ask others for AssistanceIt is unlikely that a creditor would lend money to a disabled income earner. If you were able to secure a loan, a lengthy disability could make it difficult to pay that loan back.

Sell Your AssetsAssuming a market exists, forced liquidation of assets can reduce their value. A single disabling event could consume the assets you’ve worked a lifetime to accumulate.

Rely on Spouse’s IncomeMost lifestyles today are built on dual incomes. Would your spouse’s income be enough to compensate for the loss of yours?

Collect Social Security Disability PaymentsSixty-nine percent of all initial disability benefit claims were denied from 1994 to 2003.

(Annual Statistical Report on Social Security Disability Insurance Program, 2004)

* The maximum amount of disability income available may be reduced by existing personal,employer-providedand/orstatedisabilityincomecoverages.

9

Cash Value –How do I make the most of it?

Competitive Current Crediting Rates Plus Guaranteed Crediting Rates for LifeUniversal Life insurance products have an accumulation value on which interest is credited. Interest crediting rates vary depending on which life insurance plan you choose.

You have the option to use this accumulated value to supplement your retirement income, help pay educational expenses, start a small business, or pay off your homemortgageearly.How,andwhether,youuseyourmoneyisuptoyou.

Paid-Up InsuranceYour protection needs change over time. You may decide you no longer wish to pay premiums, but want to keep an amount of permanent coverage. After the first policy year, you can use your cash value to purchase a fully paid-up life policy.

“ Quality of Life...Insurance builds cash value, which I like. Now that I’m a father, I know that I can use that money for college for my son. Or, I can use it for any emergencies that may come up.

Yet my policy also provides me with a death benefit and Accelerated Benefit Riders if anything happens to me before I can build my cash value, so my family can maintain their standard of living.”

— Kelly, Quality of Life…Insurance Policyowner

10

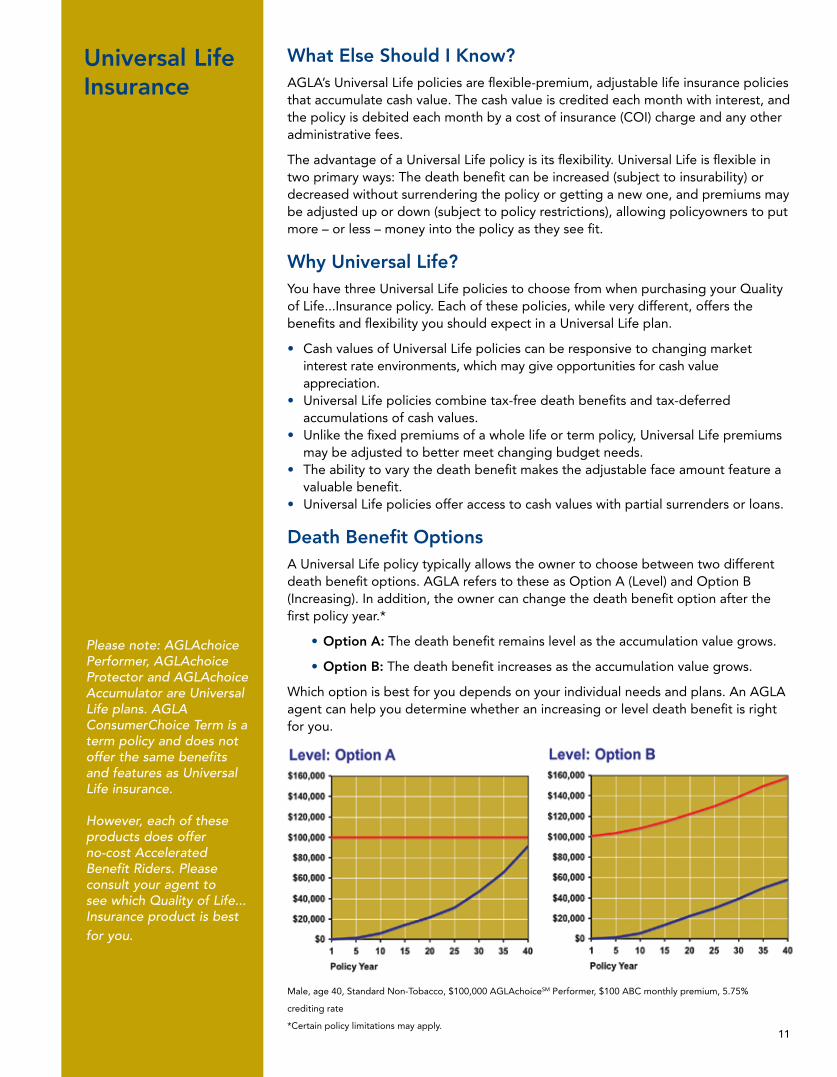

Universal LifeInsurance

What Else Should I Know?AGLA’s Universal Life policies are flexible-premium, adjustable life insurance policies that accumulate cash value. The cash value is credited each month with interest, and the policy is debited each month by a cost of insurance (COI) charge and any other administrative fees.

The advantage of a Universal Life policy is its flexibility. Universal Life is flexible in two primary ways: The death benefit can be increased (subject to insurability) or decreased without surrendering the policy or getting a new one, and premiums may be adjusted up or down (subject to policy restrictions), allowing policyowners to put more – or less – money into the policy as they see fit.

Why Universal Life?You have three Universal Life policies to choose from when purchasing your Quality of Life...Insurance policy. Each of these policies, while very different, offers the benefits and flexibility you should expect in a Universal Life plan.

• Cash values of Universal Life policies can be responsive to changing market interest rate environments, which may give opportunities for cash value appreciation.• Universal Life policies combine tax-free death benefits and tax-deferred accumulations of cash values.• Unlike the fixed premiums of a whole life or term policy, Universal Life premiums may be adjusted to better meet changing budget needs.• The ability to vary the death benefit makes the adjustable face amount feature a valuable benefit.• Universal Life policies offer access to cash values with partial surrenders or loans.

Death Benefit optionsA Universal Life policy typically allows the owner to choose between two different deathbenefitoptions.AGLAreferstotheseasOptionA(Level)andOptionB(Increasing). In addition, the owner can change the death benefit option after the first policy year.*

• option A: The death benefit remains level as the accumulation value grows.

• option B: The death benefit increases as the accumulation value grows.

Which option is best for you depends on your individual needs and plans. An AGLA agent can help you determine whether an increasing or level death benefit is right for you.

Universal LifeInsurance

Male, age 40, Standard Non-Tobacco, $100,000 AGLAchoiceSMPerformer,$100ABCmonthlypremium,5.75%

crediting rate

*Certain policy limitations may apply.11

Please note: AGLAchoice Performer, AGLAchoice Protector and AGLAchoice Accumulator are Universal Life plans. AGLA ConsumerChoice Term is a term policy and does not offer the same benefits and features as Universal Life insurance.

However, each of these products does offer no-cost Accelerated Benefit Riders. Please consult your agent to see which Quality of Life...Insurance product is best for you.

Quality of Life…InsuranceSM is Changing The Way Americans Think About, Purchase And Use Life Insurance®.Howlongwillyouwaitbeforeyoutakethis vital step to protect your family’s future?

Take some time to speak with your representative today, while you’re probably in good health and can qualify for this important coverage.

12

The quotes within this brochure are from focus group participants and our customers. Their comments are their own. No actors were used. Although each received compensation for time and travel, their involvement is priceless to us.

AGLAchoiceSM Performer

AGLAchoice Performer is recommended most frequently for responsible couples and parents, businessowners, and individual policy owners. Most often, customers who purchase these plans want access totheir accumulated cash value in case of an emergency, or to use for a future big event (such as collegefunding or a dream vacation), and want to accomplish their goals on a defined budget.

AGLAchoice Performer has a 5% guaranteed minimum interest crediting rate for the first seven policyyears and a feature that protects your excess monies paid from early surrender charges. In addition, youcan tailor your policy to match your specific needs. This includes flexible payments, a flexible death benefitand the ability to add or delete coverage and riders in the future1. These policies remain in force aslong as enough cash value is maintained to cover policy expenses and mortality charges.

Competitive Current Crediting Rates Plus A 5%Guaranteed Rate for the First Seven YearsUniversal life insurance products have an accumulation value on which interest is credited. WhileAGLAchoice Performer may offer higher than guaranteed current interest crediting rates, we guarantee aminimum interest crediting rate of 5 percent for the first seven years, and 2.25 percent thereafter. Youcan use this interest rate to build cash for supplemental retirement income, help pay educationalexpenses, or pay off your home mortgage early. How or whether you use such value is up to you.

Protected MoneyDuring the first five years of your policy, monies paid above benchmark premium as described in the policyare available to you without surrender charges. Whether it is cash value transferred from an older lifeinsurance policy or money from a maturing bank CD, anything you pay above the monthly benchmarkpremium will be protected from surrender charges and available for you to use as you see fit.1

Possible uses for Protected Money may include:• Financial emergency fund • Vacations• College funds • Large purchases• Business opportunities

There is a $25 administration charge for withdrawing Protected Money. Also, using Protected Moneymay reduce the policy death benefit and specified amount. Your decision on whether or not to takeadvantage of Protected Money depends on your specific financial needs and situation. It is important totalk to an AGLA agent about which options might be right for you.

Paid-Up InsuranceYour protection needs change over time. You may decide you no longer wish to pay premiums, but wantto keep an amount of permanent coverage. After the first policy year, you can use your cash value topurchase a fully paid-up life policy. 2

Other Benefits and Riders3

Our no-cost Chronic, Critical and Terminal Illness Accelerated Benefit Riders are included with our Quality ofLife…Insurance policies. You may also decide to purchase additional protection for you and your familywith the AGLA ChronicCare Income Rider or Disability Income Rider.

You can choose to apply for any of the following additional riders to build on the financial support providedby AGLAchoice Performer:

Disability Income RiderThe Disability Income Rider is designed to provide monthly income in the event of a qualifyingdisability. Disability Income may be purchased for two or five years of monthly income. Refer to theQuality of Life…Insurance consumer brochure4 for more information on this important coverage.

AGLA ChronicCare Income RiderThe AGLA ChronicCare Income Rider allows you to lock in a guaranteed monthly cash flow in theevent of a qualifying Chronic Illness. Refer to the Quality of Life…Insurance consumer brochure4 for moreinformation.

Waiver of Monthly Deduction RiderIssues Ages: 0-55, Termination Age: 65This rider waives the monthly guarantee premium if the primary insured becomes totally disabledduring the monthly guarantee premium period. If the primary insured becomes totally disabled afterthis period, this rider waives the monthly deductions and other administrative charges.

Accidental Death Benefit RiderIssue Ages: 0-65, Termination Age: 70This rider provides an additional death benefit if the insured’s death results from an accident.

Additional Insurance Option RiderIssue Ages: 0-35, Termination Age: 40This rider provides the owner the ability to increase the insured’s life insurance coverage amountwithout evidence of insurability on specified option dates.

Additional Insured RiderIssue Ages: 0-85This rider provides life insurance coverage on the primary insured’s spouse. The minimum coverageamount is $15,000. The maximum amount of coverage is up to the primary insured’s coverageamount. This coverage also includes the no-cost Accelerated Benefit Riders.

Children’s Term Life Insurance RiderChild’s Issue Ages: 7 days - 17 yearsThis rider provides term life insurance on children born to or adopted by the primary insured andincludes dependent stepchildren living in the insured’s home. The primary insured must be less than60 years old for issue and coverage expires at primary insured’s 65th birthday. Coverage amount isavailable from $5,000 up to $25,000.

Maturity Extension Rider:This rider allows the policyowner to extend coverage past the original maturity date of age 121, untilthe death of the insured. The death benefit during the extension period will be equal to the deathbenefit in effect on the day prior to the maturity date. Your death benefit may increase if youraccumulation value increases, but it is guaranteed to never be less than the accumulation value.

Thisbrochure is tobeusedonly in conjunctionwithForm8532QOL. It is not tobeusedasa stand-alonepiece.1May be subject to certain policy limitations. Special rules apply to conversion credits. See your policy for details if applicable.2For an equal to or lesser amount of Base Life Insurance.3Not all benefits and riders are available in all states. Rider names may vary by state.4AGLA Quality of Life…Insurance consumer brochure, 8532 QOL.

Benefits&

Riders

American General Life and Accident Insurance CompanyA subsidiary of American International Group, Inc.

AmericanGeneral Center •Nashville, Tennessee 37250-0001The underwriting risks, financial and contractual obligations and support functions associated with products issued by American General Lifeand Accident Insurance Company (AGLA) are its responsibility. American International Group, Inc. does not underwrite any insurance policy

referenced herein. AGLA does not solicit business in the states of New York and Wyoming.Policies may be subject to tax consequences when continued beyond the maturity date. The policy may not qualify as life insurance

under Internal Revenue Code after age 100. Policy owners should consult a qualified tax advisor before electing this option.The insurance company may contest the policy from the date of policy issue, a reinstatement or an increase in coverage, during a period provided by applicable law and

described in the policy, for the misstatement or misrepresentation of material fact on the application for such policy, reinstatement, or increase.If an Insured Person dies by suicide within the suicide period provided by applicable law and described in the policy, the death benefit will be limited as provided by the policy.

© 2008American International Group, Inc.All rights reserved.

AGLA8532-2 REV1008

Policy issued by: American General Life and Accident Insurance Company

For Policy Forms AGLA 08174 and Riders AGLA 04GHIR, AGLA 04CRIR, AGLA04TIR, AGLA 07CHP, AGLA 04001, AGLA 05AHA REV0308, AGLA 05AHB, AGLA05AHC, AGLA 05AHG, AGLA 05AD2, AGLA EMD-DB and state variations.

AGLAchoiceSMAccumulator

AGLAchoice Accumulator is designed for individuals who desire life insurance protection with a realpotential to accumulate cash value over time. If needed, cash accumulations may also be used for big budgetitems, such as college funding or a dream vacation; or to fund a future business opportunity.

This product also appeals to responsible couples, parents, business owners, and individual policy ownerswho may wish to access cash accumulation during their retirement years.

AGLAchoice Accumulator also allows you to tailor your policy to match your specific needs. It allows forflexible payments, provides a flexible death benefit and the ability to add or delete coverage and riders inthe future1. The policy remains in-force as long as it maintains enough cash value to cover policy expensesand mortality charges.

Competitive Current Crediting Rates Plus A3% Guaranteed Rate for the Life of the PolicyUniversal life insurance products have an accumulation value on which interest is credited. WhileAGLAchoice Accumulator may offer higher than guaranteed current interest crediting rates, we guarantee aminimum interest crediting rate of 3 percent for the life of the policy. You can use this interest rate to buildcash for supplemental retirement income, help pay educational expenses, or pay off your home mortgageearly. How or whether you use such value is up to you.

Paid-Up InsuranceYour protection needs change over time. You may decide you no longer wish to pay premiums, but wantto keep an amount of permanent coverage. After the first policy year, you can use your cash value to purchase afully paid-up life policy. 2

Other Benefits and Riders3

Our no-cost Chronic, Critical and Terminal Illness Accelerated Benefit Riders are included with ourQuality of Life…InsuranceSM policies.

You can choose to apply for any of the following additional riders to build on the financial support providedby AGLAchoice Accumulator:

Disability Income RiderThe Disability Income Rider is designed to provide monthly income in the event of a qualifying disability.Disability Income may be purchased for two or five years of monthly income. Refer to the Quality ofLife…Insurance consumer brochure4 for more information on this important coverage.

AGLA ChronicCare Income RiderSM

The AGLA ChronicCare Income Rider allows you to lock in a guaranteed monthly cash flow in the event of aqualifying Chronic Illness. Refer to the Quality of Life…Insurance consumer brochure4 for moreinformation.

No-Lapse GuaranteeIssue Ages: 0-85The Monthly Guarantee Premium to Age 121 Rider provides guaranteed lifetime coverage, regardlessof the policy’s cash values, as long as the cumulative monthly guarantee premium requirement asstated in the policy is met.

Waiver of Specified Premium (WSPR)Issue Ages: 15 – 55Termination Age: 60This rider pays a benefit into the policy each month during the total disability of the primary insuredfollowing a 180 day elimination period. The monthly benefit is determined on the date the rider isissued as the lesser of the 1/12 of the annualized Planned Periodic Premium (PPP) at issue, but notless than $10.00, the Monthly Benchmark Premium for the policy or $2,000.

The rider uses an“own occupation”definition of disability during the first two years of the benefit period.For the remaining portion of the benefit period, an “any-occupation” definition of disability is used.The benefit under this rider does not guarantee that the policy will remain in force.

Accidental Death Benefit RiderIssue Ages: 20-65Termination Age: 70This rider provides an additional death benefit if the primary insured’s death results from an accident.

Children’s Term Life Insurance RiderChild’s Issue Ages: 7 days – 17 yearsThis rider provides term life insurance on children born to or adopted by the primary insured andincludes dependent stepchildren living in the primary insured’s home. The primary insured must beless than 60 years old for issue and coverage expires at primary insured’s 65th birthday. Coverageamount is available from $5,000 up to $25,000.

Additional Insurance Option RiderIssue Ages: 0-35Termination Age: 40This rider provides the owner the ability to increase the primary insured’s life insurance coverageamount under the policy without evidence of insurability on specified option dates.

Additional Insured RiderIssue Ages: 0-85This rider provides life insurance coverage on the primary insured’s spouse. The minimum coverageamount is $25,000. The maximum amount of coverage is up to the primary insured’s coverageamount. This coverage also includes the no-cost Accelerated Benefit Riders.

Maturity Extension Rider:This rider allows the policyowner to extend coverage past the original maturity date of age 121, untilthe death of the insured. The death benefit during the extension period will be equal to the deathbenefit in effect on the day prior to the maturity date. Your death benefit may increase if youraccumulation value increases, but it is guaranteed to never be less than the accumulation value.

Thisbrochure is tobeusedonly in conjunctionwithForm8532QOL. It is not tobeusedasa stand-alonepiece.1May be subject to certain policy limitations.2For an equal to or lesser amount of Base Life Insurance.3Not all benefits and riders are available in all states. Rider names may vary by state.4AGLA Quality of Life…Insurance consumer brochure, 8532 QOL.

American General Life and Accident Insurance CompanyA subsidiary of American International Group, Inc.

AmericanGeneral Center •Nashville, Tennessee 37250-0001The underwriting risks, financial and contractual obligations and support functions associated with products issued by American General Life and

Accident Insurance Company (AGLA) are its responsibility. American International Group, Inc. does not underwrite any insurance policyreferenced herein. AGLA does not solicit business in the states of New York and Wyoming.

Policies may be subject to tax consequences when continued beyond the maturity date. The policy may not qualify as life insuranceunder Internal Revenue Code after age 100. Policy owners should consult a qualified tax advisor before electing this option.

The insurance company may contest the policy from the date of policy issue, a reinstatement or an increase in coverage, during a period provided by applicable law anddescribed in the policy, for the misstatement or misrepresentation of material fact on the application for such policy, reinstatement, or increase.

If an Insured Person dies by suicide within the suicide period provided by applicable law and described in the policy, the death benefit will be limited as provided by the policy.© 2008American International Group, Inc.All rights reserved.

AGLA8532-3 REV1008

Policy issued by: American General Life and Accident Insurance Company

For Policy Forms AGLA 05AHO and Riders AGLA 04CHIR, AGLA 04CRIR, AGLA04TIR, AGLA 07CHP, AGLA 05AHA REV0308, AGLA 05AHC, AGLA 05AHB, AGLA05AHG, AGLA 05AHP, AGLA 05AD2, AGLA 08MGP, AGLA EMD-DB and statevariations

AGLAchoiceSMProtector

AGLAchoice Protector is an excellent alternative to a traditional Term Life Insurance policy. It featuresaffordable rates that are typical with most Term policies, but it includes the added protection of the no-costAccelerated Benefit Riders.

Clients who purchase an AGLAchoice Protector plan are typically younger than the average life insurancebuyer, and their goals often include protecting a mortgage and providing a dependable monthly incomein the event of a disability.

AGLAchoice Protector buyers are often young families just starting out in life who want to provide lifeinsurance protection for their families, but who are often facing difficult financial choices. AGLAchoiceProtector provides important coverage at a rate that won’t break the family budget.

AGLAchoice Protector also allows you to tailor your policy to match your specific needs. It allows forflexible payments, provides a flexible death benefit and the ability to add or delete coverage and riders inthe future1. The policy remains in-force as long as it maintains enough cash value to cover policy expensesand mortality charges.

Competitive Current Crediting Rates Plus A3% Guaranteed Rate for the Life of the PolicyUniversal life insurance products have an accumulation value on which interest is credited.While AGLAchoice Protectormay offer higher than guaranteed current interest crediting rates, weguarantee a minimum interest crediting rate of 3 percent for the life of the policy. You can use this interestrate to build cash for supplemental retirement income, help pay educational expenses, or pay off yourhome mortgage early. How or whether you use such value is up to you.

Paid-Up InsuranceYour protection needs change over time. You may decide you no longer wish to pay premiums, but wantto keep an amount of permanent coverage. After the first policy year, you can use your cash value to purchasea fully paid-up life policy.2

Other Benefits and Riders3

Our no-cost Chronic, Critical and Terminal Illness Accelerated Benefit Riders are included with our Quality ofLife…Insurance policies. You may also decide to purchase additional protection for you and your familywith the AGLA ChronicCare Income Rider or Disability Income Rider.

You can choose to apply for any of the following additional riders to build on the financial support providedby AGLAchoice Protector .

Disability Income RiderThe Disability Income Rider is designed to provide monthly income in the event of a qualifyingdisability. Disability Income may be purchased for two or five years of monthly income. Refer to theQuality of Life…Insurance consumer brochure4 for more information on this important coverage.

AGLA ChronicCare Income RiderThe AGLA ChronicCare Income Rider allows you to lock in a guaranteed monthly cash flow in theevent of a qualifying Chronic Illness. Refer to the Quality of Life…Insurance consumer brochure4 formore information.

Waiver of Specified Premium (WSPR)Issue Ages: 15 – 55Termination Age: 60This rider pays a benefit into the policy each month during the total disability of the primary insuredfollowing a 180 day elimination period. The monthly benefit is determined on the date the rider isissued as the lesser of the 1/12 of the annualized Planned Periodic Premium (PPP) at issue, but notless than $10.00, the Monthly Benchmark Premium for the policy or $2,000.

The rider uses an “own occupation” definition of disability during the first two years of the benefitperiod. For the remaining portion of the benefit period, an “any-occupation” definition of disability isused.

The benefit under this rider does not guarantee that the policy will remain in force.

Accidental Death Benefit RiderIssue Ages: 20-65Termination Age: 70This rider provides an additional death benefit if the insured’s death results from an accident.

Children’s Term Life Insurance RiderIssue Ages: 7 days – 17 yearsThis rider provides term life insurance on children born to or adopted by the primary insured andincludes dependent stepchildren living in the insured’s home. The primary insured must be less than60 years old for issue and coverage expires at primary insured’s 65th birthday. Coverage amount isavailable from $5,000 up to $25,000.

Additional Insurance Option RiderIssue Ages: 0-35Termination Age: 40This rider provides the owner the ability to increase the primary insured’s life insurance coverageamount under the policy without evidence of insurability on specified option dates.

Additional Insured RiderIssue Ages: 0-85This rider provides life insurance coverage on the primary insured’s spouse. The minimum coverageamount is $25,000. The maximum amount of coverage is up to the primary insured’s coverageamount. This coverage also contains Accelerated Benefit Riders.

Maturity Extension Rider:This rider allows the policyowner to extend coverage past the original maturity date of age 121, untilthe death of the insured. The death benefit during the extension period will be equal to the deathbenefit in effect on the day prior to the maturity date. Your death benefit may increase if youraccumulation value increases, but it is guaranteed to never be less than the accumulation value.

Thisbrochure is tobeusedonly in conjunctionwithForm8532QOL. It is not tobeusedasa stand-alonepiece.1May be subject to certain policy limitations.2For an equal to or lesser amount of Base Life Insurance.3Not all benefits and riders are available in all states. Rider names may vary by state.4AGLA Quality of Life…Insurance consumer brochure, 8532 QOL.

American General Life and Accident Insurance CompanyA subsidiary of American International Group, Inc.

AmericanGeneral Center •Nashville, Tennessee 37250-0001The underwriting risks, financial and contractual obligations and support functions associated with products issued by American General Life and

Accident Insurance Company (AGLA) are its responsibility. American International Group, Inc. does not underwrite any insurance policyreferenced herein. AGLA does not solicit business in the states of New York and Wyoming.

Policies may be subject to tax consequences when continued beyond the maturity date. The policy may not qualify as life insuranceunder Internal Revenue Code after age 100. Policy owners should consult a qualified tax advisor before electing this option.

The insurance company may contest the policy from the date of policy issue, a reinstatement or an increase in coverage, during a period provided by applicable law anddescribed in the policy, for the misstatement or misrepresentation of material fact on the application for such policy, reinstatement, or increase.

If an Insured Person dies by suicide within the suicide period provided by applicable law and described in the policy, the death benefit will be limited as provided by the policy.

© 2008American International Group, Inc.All rights reserved.

AGLA8532-4 REV1008

Policy issued by: American General Life and Accident Insurance Company

For Policy Forms AGLA 08ALO and Riders AGLA 04CHIR, AGLA 04CRIR, AGLA04TIR, AGLA 07CHP, AGLA 05AHA REV0308, AGLA 05AHC, AGLA 05AHB, AGLA05AHG, AGLA 05AHP, AGLA 05AD2, AGLA EMD-DB and state variations

AGLA ConsumerChoice TermSM

Historically, term life insurance has been a good solution for millions of American families who need lifeinsurance coverage at affordable rates.

Traditional term insurance provides affordable, guaranteed death benefit coverage for a specific periodof time. People buy term insurance when they have temporary insurance needs. Some examples includemaking sure their mortgage would be protected, providing college tuition for their children, or coveringstart-up costs from a small business.

Term insurance can provide for these needs for families on a tight budget. But if your circumstancesshould change, the conversion feature allows you to exchange your term policy for a permanent lifepolicy without providing evidence of insurability.

Why should I choose AGLA ConsumerChoice Term?You Choose Your Benefit Period

Life doesn’t always fit into neat five-year term periods (which is typical for most term products). WithAGLA ConsumerChoice Term, you choose how long you want coverage.

For example, if there are 24 years remaining on your mortgage, it may not make sense for your family topurchase a 30-year term plan. Insurance companies typically offer a basic solution for everyone in a 10,15, 20, or 30 year plan. But in reality, everyone has different needs for insurance coverage. And by selectingonly the term coverage you need, you avoid paying unnecessary costs associated with a longer duration.

AGLA ConsumerChoice Term may be purchased for level premium periods* of:• 10 Years• 12 Years• Any period from 15-35 Years

You Can Convert Your Policy to Permanent CoverageCircumstances change. Your AGLA ConsumerChoice Term policy may be a good decision for you now, butif your life changes in the future, you may decide that permanent coverage is best for you. Purchasingpermanent coverage can allow you to protect your family and loved ones for your entire lifetime, notmerely for a specified term period.

Each AGLA ConsumerChoice Term policy includes an Accelerated Benefit Rider special conversion expirydate, which allows you to convert your term policy to a permanent policy with ABRs, without providingevidence of insurability. This provision begins on the issue date of the contract and expires on the 24th

policy month.

A conversion to a permanent plan of insurance without Accelerated Benefit Riders is allowed withoutevidence of insurability during the policy's conversion period. The conversion period is 80% of the levelpremium period not beyond the Insured's age 75. Ask your agent for details.

*Based on age and tobacco usage.

Other Benefits and RidersOur no-cost Chronic, Critical and Terminal Illness Accelerated Benefit Riders are included with mostQuality of Life…Insurance policies. You can choose to apply for any of the following additional ridersto build on the financial support provided by AGLA ConsumerChoice Term:

Disability Income RiderThe Disability Income Rider is designed to pay you a portion of your income if you becomedisabled and are unable to work. It is available in either a 2-year or a 5-year plan.

Plan benefits would begin after:2-Year Benefit period: 90 days5-Year Benefit period: 180 days

Plan Details:Issue ages: 20-55Minimum monthly benefit: $500Maximum monthly benefit is the lesser of the following amounts:

- $5,000 for the 2-year option, $3,500 for the 5-year option- $20 per $1,000 of life insurance purchased, rounded to the nearest $10, or- Percentage of Gross Monthly Income (ask agent for details)

Please note, the maximum amount of disability income available may be reduced by existingpersonal, employer-provided and/or state disability income coverages.

Premium WaiverIssue ages: 20-55Termination age: 65

This rider provides coverage for the waiver of premiums after the Insured becomes totallydisabled for 6 months.

Children’s Term Life Insurance RiderIssue ages for base Insured: 20-50; children: 7 days-17 yearsExpires at child’s age 25, Insured’s age 65Issue amounts: $5,000–$12,500

This rider provides a level amount of term insurance on each Insured Child with level premiumspayable for the same period in which the coverage is provided. It may be converted to apermanent plan at any time and may be converted for up to 5 times coverage if conversion ismade effective at child's age 25.

RIDER NAMES, BENEFITS AND AVAILABILITY MAY VARY BY STATE.

This brochure is to be used only in conjunction with Form AGLA8532 QOL.It is not to be used as a stand-alone piece.

American General Life and Accident Insurance CompanyA subsidiary of American International Group, Inc.

AmericanGeneral Center •Nashville, Tennessee 37250-0001The underwriting risks, financial and contractual obligations and support functions associated with products issued by American General Lifeand Accident Insurance Company (AGLA) are its responsibility. American International Group, Inc. does not underwrite any insurance policy

referenced herein. AGLA does not solicit business in the states of New York and Wyoming.Policies may be subject to tax consequences when continued beyond the maturity date. The policy may not qualify as life insurance

under Internal Revenue Code after age 100. Policy owners should consult a qualified tax advisor before electing this option.The insurance company may contest the policy from the date of policy issue, a reinstatement or an increase in coverage, during a period provided by applicable law and

described in the policy, for the misstatement or misrepresentation of material fact on the application for such policy, reinstatement, or increase.If an Insured Person dies by suicide within the suicide period provided by applicable law and described in the policy, the death benefit will be limited as provided by the policy.

© 2008American International Group, Inc.All rights reserved.

AGLA8532-5 REV1008

Policy issued by: American General Life and Accident Insurance Company

For Policy Forms AGLA 08TRM and Riders AGLA 04CRIR, AGLA 04CHIR, AGLA04TIR, AGLA05AD2, AGLA05AHP, AGLA05AHC, AGLA20140-1, PW-A-NL and statevariations.