Embed Size (px)

Citation preview

Legislative and Regulatory HorizonBeyond the ACEA Voluntary Agreement

Dick ButtigiegDirector, Automotive Consulting

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 2

Presentation Outline

• Factors Driving Current Legislation Concerning CO2

• ACEA/Auto Industry Voluntary Agreement

• CO2 Related European Regulatory Landscape

• Impact Upon Auto Industry Voluntary Agreement

• Post Voluntary Agreement Era

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 3

Factors Driving Current

Legislation Concerning CO2

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 4

Factors Driving Current Legislation Concerning CO2

• Environmental factors– Climate change imperatives are driving EU/National Governments/Global

NGOs towards greater concern for the environment specifically the need to reduce/restrain carbon emissions

– Kyoto Protocol - April 2002 – European Council decision concerning addition of Kyoto Protocol to UN

Framework convention on climate Change – committing Community and Member states to reduce GHGs by 8% compared to 1990 levels between2008–12

– Feb 16 2005 – Kyoto Protocol finally entered into force in EU• Dependence on fossil fuels

– Have we reached the summit of our oil demand? Continuing debate in press and from scientists regarding peak of oil production, referred to as HubbertsPeak

– Sweden has put a stake in the ground, indicating its wish to be free from Oil Dependence by 2020

– The EU has stated it wishes to be free from oil dependence by 2030

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 5

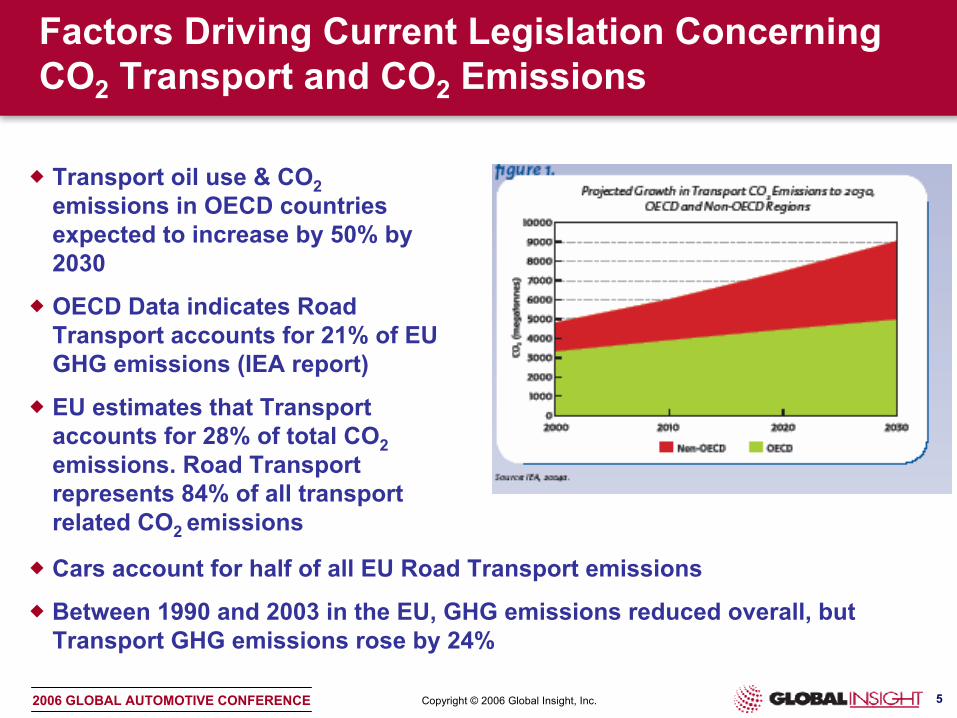

Factors Driving Current Legislation Concerning CO2 Transport and CO2 Emissions

Transport oil use & CO2 emissions in OECD countries expected to increase by 50% by 2030

OECD Data indicates Road Transport accounts for 21% of EU GHG emissions (IEA report)

EU estimates that Transport accounts for 28% of total CO2 emissions. Road Transport represents 84% of all transport related CO2 emissions

Cars account for half of all EU Road Transport emissions

Between 1990 and 2003 in the EU, GHG emissions reduced overall, but Transport GHG emissions rose by 24%

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 6

Factors Driving Current Legislation Concerning CO2

• “Polluter pays” policy– The consumer is penalised for driving vehicles with higher emissions

– although questionable if this has worked or is working!

• EU has evolved through Information e.g. Fuel Labelling and Fiscal Measures e.g. the draft proposal COM (2005) 261 Final which set out plans to introduce a CO2 element to Registration and Annual Circulation Tax, and targets for an increasing proportion of taxrevenue to be derived from CO2 based taxes

• Industry successfully presented a case for its ability to manageits own responsibilities – proposed voluntary agreements initially ACEA, then JAMA and KAMA

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 7

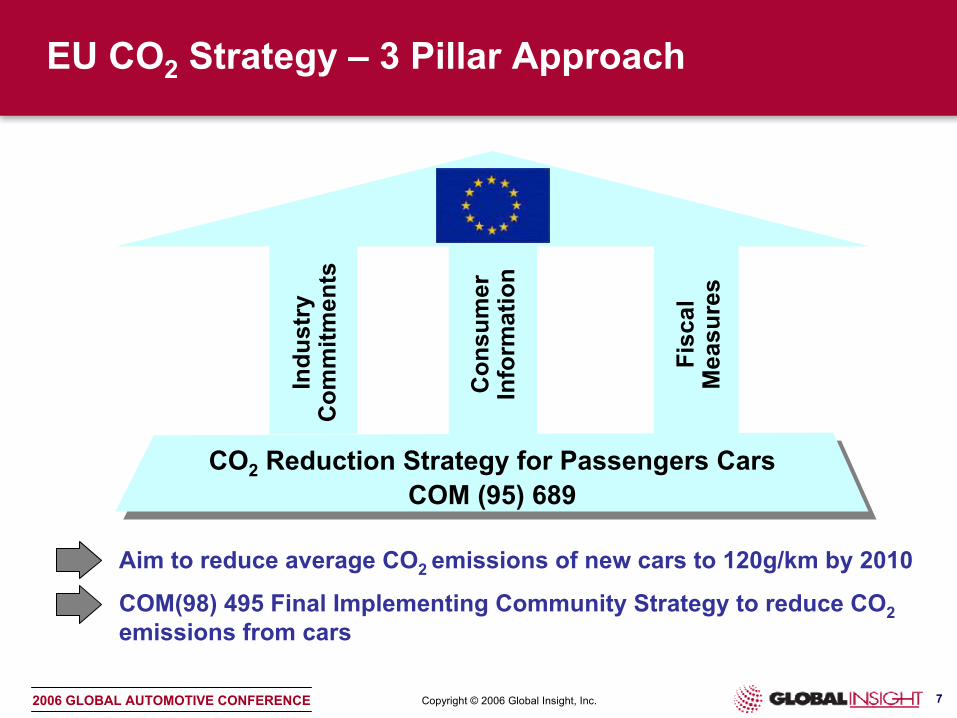

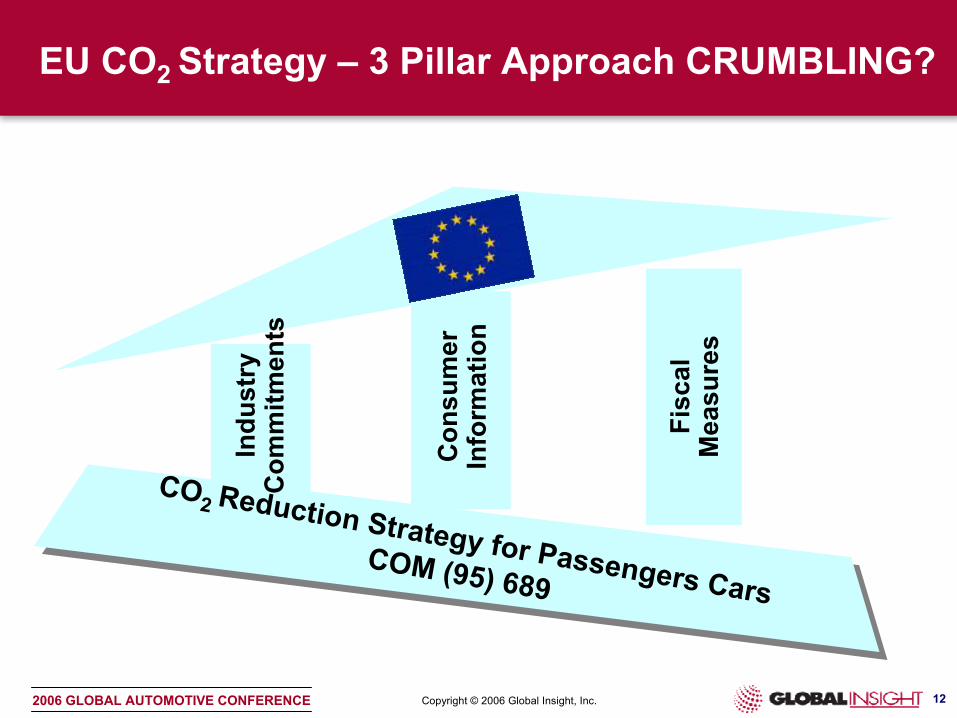

EU CO2 Strategy – 3 Pillar Approach

Aim to reduce average CO2 emissions of new cars to 120g/km by 2010

COM(98) 495 Final Implementing Community Strategy to reduce CO2emissions from cars

CO2 Reduction Strategy for Passengers CarsCOM (95) 689

Indu

stry

Com

mitm

ents

Con

sum

erIn

form

atio

n

Fisc

al

Mea

sure

s

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 8

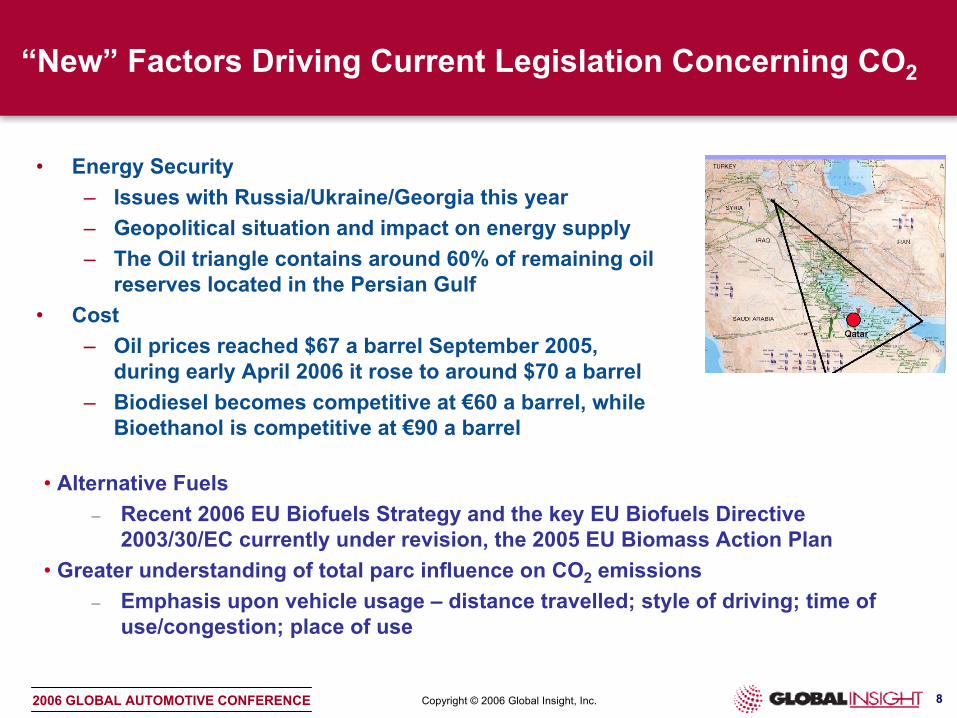

“New” Factors Driving Current Legislation Concerning CO2

• Energy Security– Issues with Russia/Ukraine/Georgia this year – Geopolitical situation and impact on energy supply – The Oil triangle contains around 60% of remaining oil

reserves located in the Persian Gulf• Cost

– Oil prices reached $67 a barrel September 2005, during early April 2006 it rose to around $70 a barrel

– Biodiesel becomes competitive at €60 a barrel, while Bioethanol is competitive at €90 a barrel

• Alternative Fuels– Recent 2006 EU Biofuels Strategy and the key EU Biofuels Directive

2003/30/EC currently under revision, the 2005 EU Biomass Action Plan• Greater understanding of total parc influence on CO2 emissions

– Emphasis upon vehicle usage – distance travelled; style of driving; time of use/congestion; place of use

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 9

ACEA/Auto Industry

Voluntary Agreement

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 10

The ACEA/Auto Industry Voluntary Agreement

• The Auto Industry Voluntary Agreement was one of the 3 pillars to reduce CO2 emissions

• The EU set out its targets in its 1995 Communication on Community strategy to reduce CO2 emissions in passenger cars. The EU’s strategy was aiming for an average new car emission of 120g/km by 2010. It failed to convince ACEA to adopt this target

• ACEA agreed in 1998 to set a 2008 target of 140g/km – this is a new car fleet average for ACEA members. JAMA/KAMA agreed to the same target but with a 2009 deadline. The agreements included a review of the potential for additional improvements with a view to moving the new car fleet average further towards 120g/km by 2012

• This review, based on 2003 data, was published in 2005

An environmental agreement with the European automobile industryoutlines the future Voluntary agreement with ACEA to target reduction of CO2 emissions to 140g/km by 2008 and a joint monitoring procedure

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 11

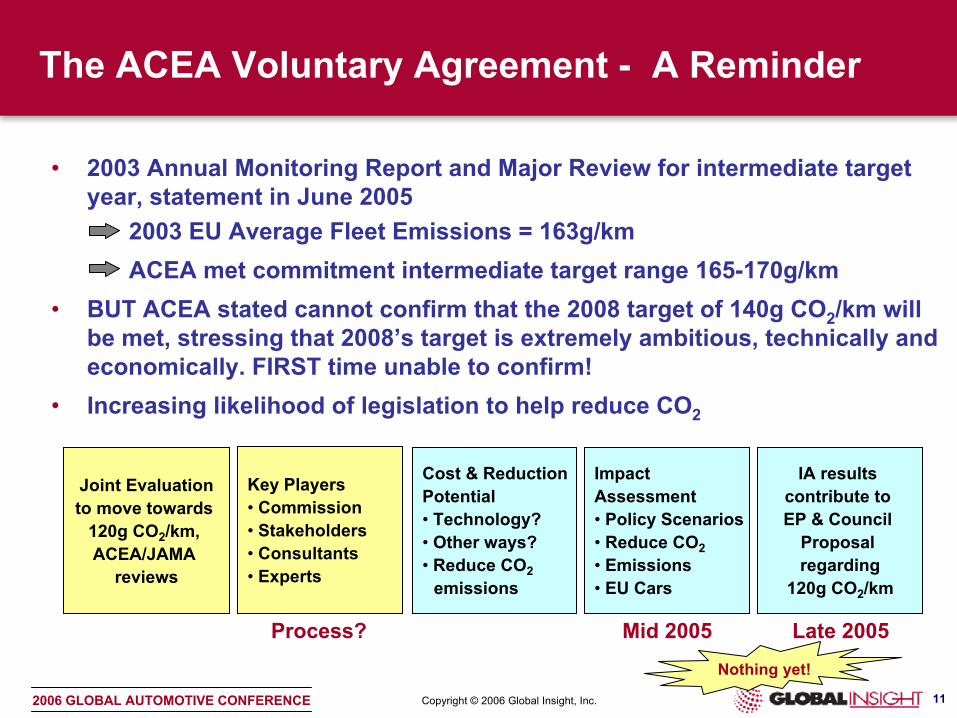

Nothing yet!

The ACEA Voluntary Agreement - A Reminder

• 2003 Annual Monitoring Report and Major Review for intermediate target year, statement in June 2005

2003 EU Average Fleet Emissions = 163g/km ACEA met commitment intermediate target range 165-170g/km

• BUT ACEA stated cannot confirm that the 2008 target of 140g CO2/km will be met, stressing that 2008’s target is extremely ambitious, technically and economically. FIRST time unable to confirm!

• Increasing likelihood of legislation to help reduce CO2

Joint Evaluationto move towards

120g CO2/km, ACEA/JAMA

reviews

Key Players• Commission • Stakeholders • Consultants • Experts

Cost & Reduction Potential • Technology? • Other ways? • Reduce CO2

emissions

Impact Assessment • Policy Scenarios • Reduce CO2• Emissions • EU Cars

IA results contribute to EP & Council

Proposal regarding

120g CO2/km

Process? Mid 2005 Late 2005

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 12

EU CO2 Strategy – 3 Pillar Approach CRUMBLING?

CO2 Reduction Strategy for Passengers CarsCOM (95) 689

Indu

stry

Com

mitm

ents

Con

sum

erIn

form

atio

n

Fisc

al

Mea

sure

s

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 13

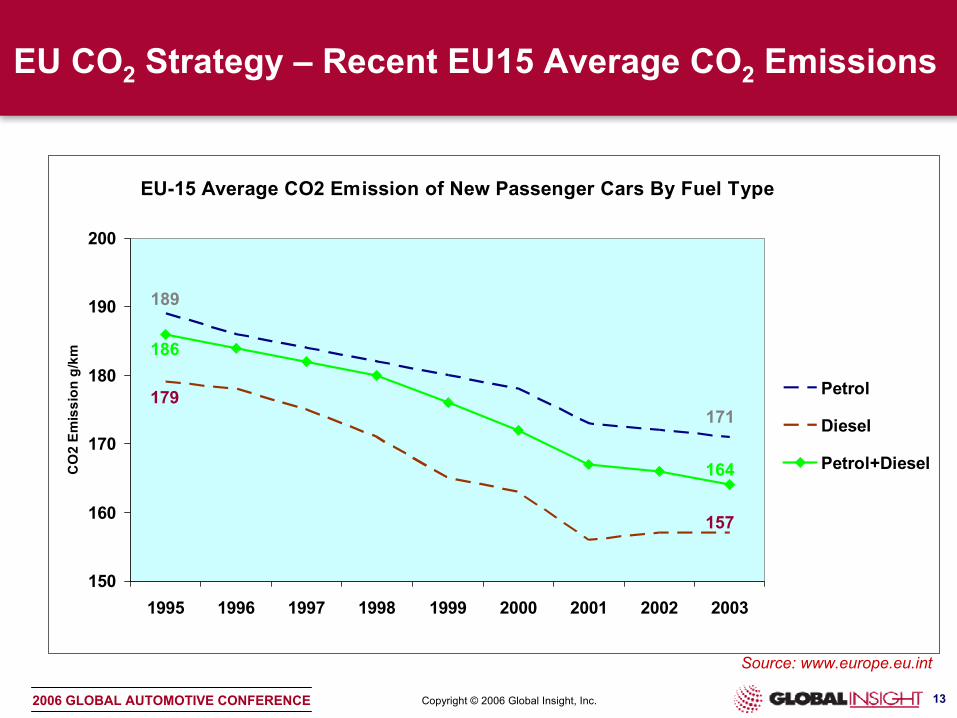

EU CO2 Strategy – Recent EU15 Average CO2 Emissions

EU-15 Average CO2 Emission of New Passenger Cars By Fuel Type

150

160

170

180

190

200

1995 1996 1997 1998 1999 2000 2001 2002 2003

CO

2 Em

issi

on g

/km

Petrol

Diesel

Petrol+Diesel

157

164

171179

186

189

Source: www.europe.eu.int

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 14

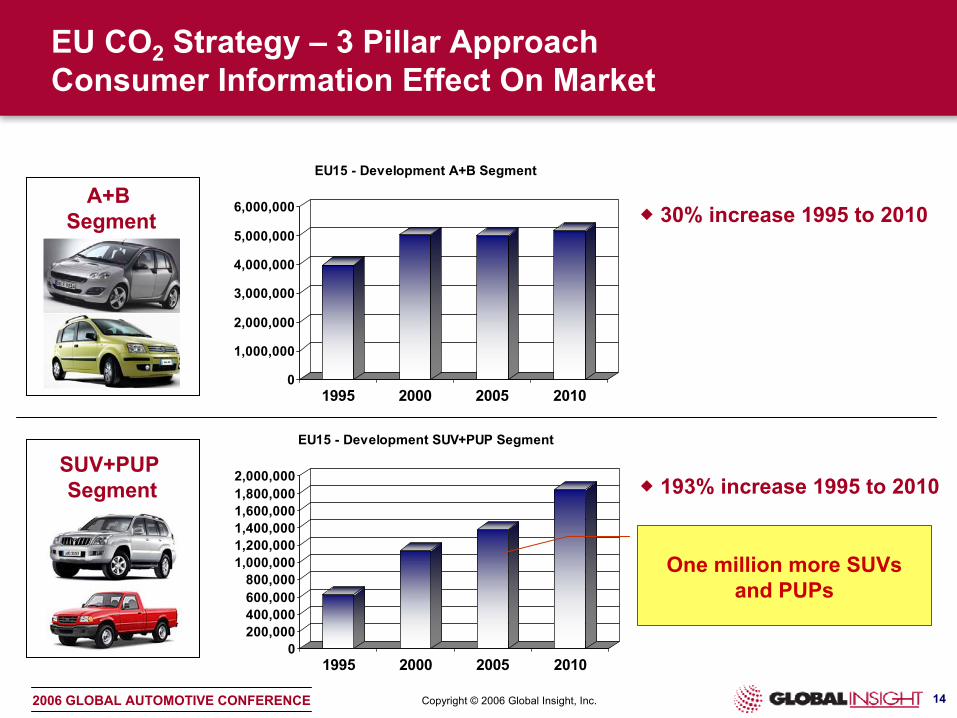

EU CO2 Strategy – 3 Pillar ApproachConsumer Information Effect On Market

A+B Segment

SUV+PUP Segment

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

1995 2000 2005 2010

EU15 - Development A+B Segment

0200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,0001,800,0002,000,000

1995 2000 2005 2010

EU15 - Development SUV+PUP Segment

30% increase 1995 to 2010

193% increase 1995 to 2010

One million more SUVs and PUPs

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 15

EU CO2 Strategy – 3 Pillar ApproachFiscal Measures

• The Commission issued a draft proposal for a Directive regardingPassenger Car Taxes in July 2005. This is still pending a European Parliament decision (July 2006 for a part-session reading by the European Parliament?). Unlikely we will see anything new on this proposal till either just before the summerbreak or the autumn

• Serves to highlight the slowness of introduction of fiscal measures

• The proposal sets targets for CO2 related tax in registration tax (RT) and annual circulation tax (ACT). It also recommends the gradual abolition of RT and a move towards ACT

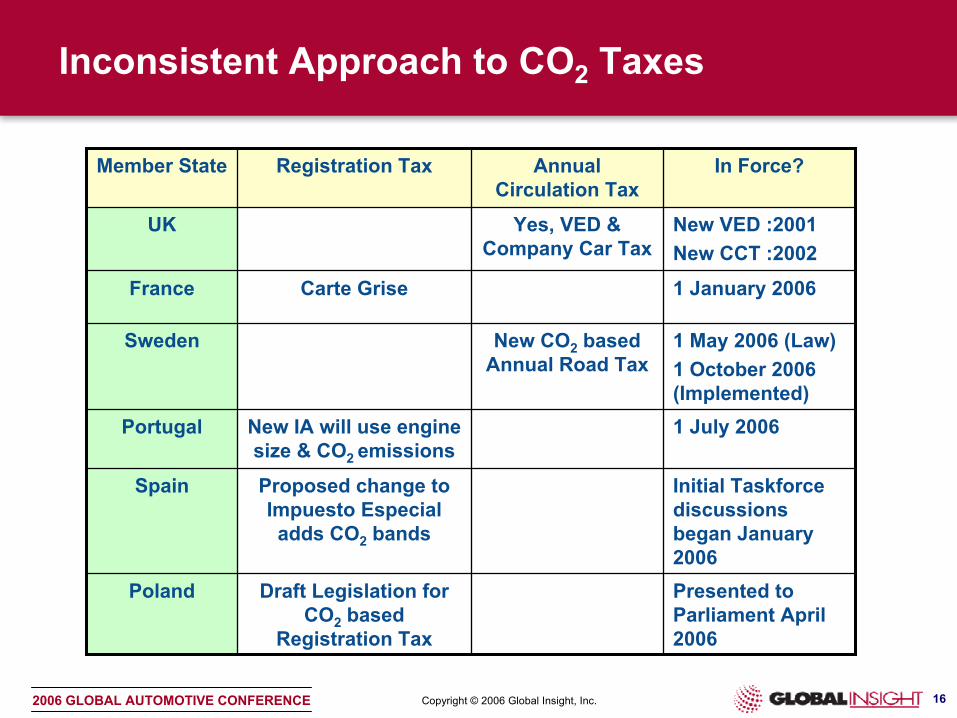

• Progress to date in this area by Member States has been inconsistent…

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 16

Inconsistent Approach to CO2 Taxes

Presented to Parliament April 2006

Draft Legislation for CO2 based

Registration Tax

Poland

Initial Taskforce discussions began January 2006

Proposed change to Impuesto Especial adds CO2 bands

Spain

1 July 2006New IA will use engine size & CO2 emissions

Portugal

1 May 2006 (Law)1 October 2006 (Implemented)

New CO2 based Annual Road Tax

Sweden

1 January 2006Carte GriseFrance

New VED :2001New CCT :2002

Yes, VED & Company Car Tax

UK

In Force?Annual Circulation Tax

Registration TaxMember State

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 17

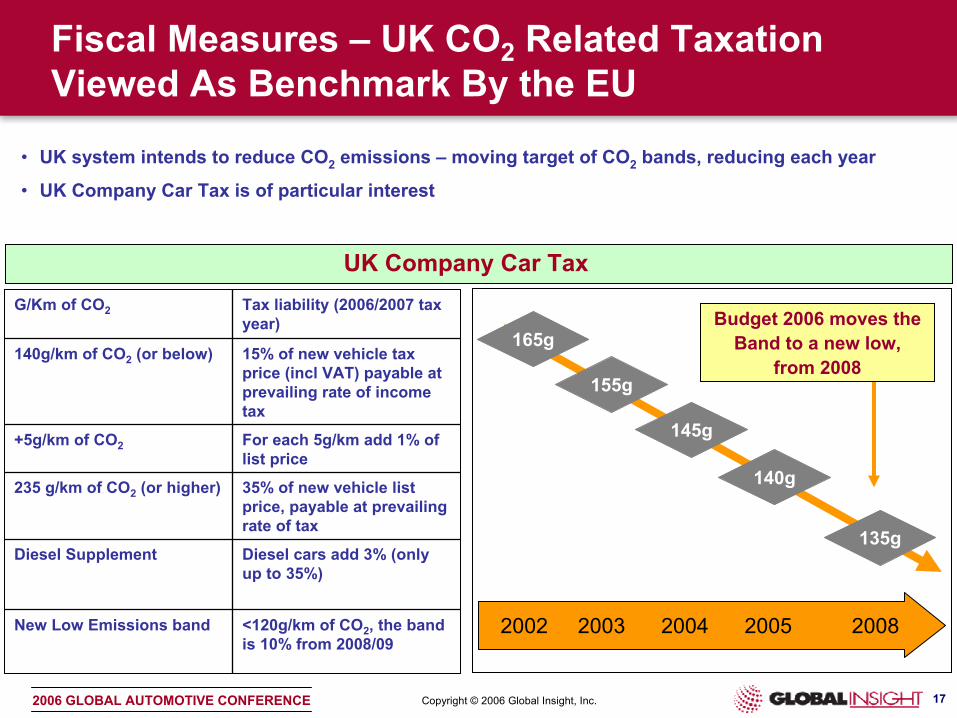

Fiscal Measures – UK CO2 Related Taxation Viewed As Benchmark By the EU

Diesel cars add 3% (only up to 35%)

Diesel Supplement

<120g/km of CO2, the band is 10% from 2008/09

New Low Emissions band

35% of new vehicle list price, payable at prevailing rate of tax

235 g/km of CO2 (or higher)

For each 5g/km add 1% of list price

+5g/km of CO2

15% of new vehicle tax price (incl VAT) payable at prevailing rate of income tax

140g/km of CO2 (or below)

Tax liability (2006/2007 tax year)

G/Km of CO2

2002 2003 2004 2005 2008

• UK system intends to reduce CO2 emissions – moving target of CO2 bands, reducing each year

• UK Company Car Tax is of particular interest

Budget 2006 moves theBand to a new low,

from 2008165g

155g

145g

140g

135g

UK Company Car Tax

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 18

EU CO2 Strategy – 3 Pillar ApproachIndustry Commitments

• Industry has made great strides in CO2 improvement through technology enhancements such as the common rail fuel injection, direct injection and advanced transmissions

• Industry has also respected other EU legislation, such as Safety (crashworthiness; pedestrian safety, rear vision etc) with consequent impact upon weight of vehicle and, in turn, a negative impact upon CO2 target achievement

• But because the consumer is buying bigger cars the industry struggles to meet 2008 goals

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 19

CO2 Related European

Regulatory Landscape

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 20

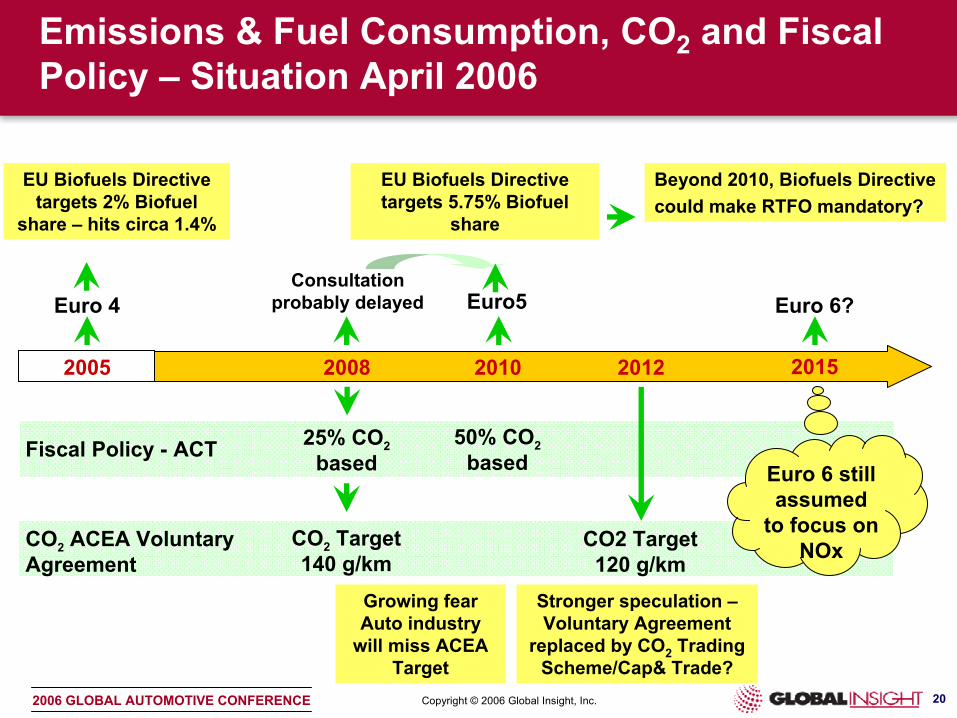

Emissions & Fuel Consumption, CO2 and Fiscal Policy – Situation April 2006

Euro 4

2005

Euro5

2008 2010 2012 2015

Fiscal Policy - ACT 25% CO2based

50% CO2based

CO2 Target 140 g/km

CO2 Target 120 g/km

CO2 ACEA Voluntary Agreement

Euro 6?

EU Biofuels Directive targets 2% Biofuel

share – hits circa 1.4%

Consultationprobably delayed

Growing fear Auto industry

will miss ACEA Target

Euro 6 still assumed

to focus on NOx

EU Biofuels Directive targets 5.75% Biofuel

share

Beyond 2010, Biofuels Directive could make RTFO mandatory??

Stronger speculation –Voluntary Agreement

replaced by CO2 Trading Scheme/Cap& Trade?

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 21

Recent Trends in CO2 Based Tax Systems

• Existence of bands which can be altered, intensified, ratcheted up. UK led the way with Company Car Tax extended to VED (Circulation Tax)

– Portugal, Sweden and Spain are all looking at introducing CO2 bands in some form• Variety of components which allow system to be ‘flexed’. CO2 emissions, type of fuel,

addition of Alternative Fuels too– Sweden uses fuel type and CO2 g/km– Portugal – although complicated – uses Cylinder Capacity and CO2 g/km– Over time focus can be moved e.g. in Portugal, derive larger % of tax from the CO2

element• Therefore able to manipulate certain parts of the market, eg Sweden’s new CO2 tax.

Element for different type of fuel– SEK 15 per gram of CO2 for Petrol– Multiplier of 3.5 for Diesel– SEK 10 per gram of CO2 for alternative fuels

• Also seeing Registration Tax and Annual Circulation Taxes supplemented with other systems which penalise heavy polluters and reward low CO2 emitters

– Congestion Charging – in London, Hybrids go free, with lobbying to discount E85 vehicles

– Free parking – in some Swedish cities, environmentally friendly cars and electric vehicles take advantage of free parking permits.

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 22

Likely New Regulatory Landscape

• Stronger “classic” legislation, introduction sooner and harder hitting

• Fuel quality– Remove the quantitative limits on ethanol– Amend the limits regarding vapour pressure– Blending of 10% biodiesel by 2010 with option to increase this to 25% by 2020

• Other – Common Agricultural Policy and Trade Reforms

• Biofuels directive

• Move from final user (polluter) pays to manufacturer and/or distributor pays - see Renewable Transport Fuel Obligations; but what will be the mechanism?

Whatever new legislation is introduced it will need to adhere to the principle of“proportionality” which justifies Community action only where it is ‘necessary’ or‘required’ in order to reach a certain end and that actions are “quantifiable”“measurable” and “repeatable”

To achieve EU CO2 emission targets requires the “Third Pillar” to be strong

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 23

Biofuels Directive – Revision in 2006

• The EU Biofuels Directive 2003/30– Sets reference values for market share of biofuels for

2005 and 2010 – aka RTFO – Renewable Transport Fuel Obligations

• The 2003 Biofuels Directive required a report in 2006 regarding the implementation of the directive and a possible revision

• The Revision will define what steps need to be taken to ensure the EU25 meets the 2010 biofuels target

• The 2006 Report will also look at:– Using biofuels obligations more widely– Setting national targets for the market share of biofuels– Establishing a system of certificates so that only

biofuels cultivated according to minimum sustainability targets can count towards biofuels targets

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 24

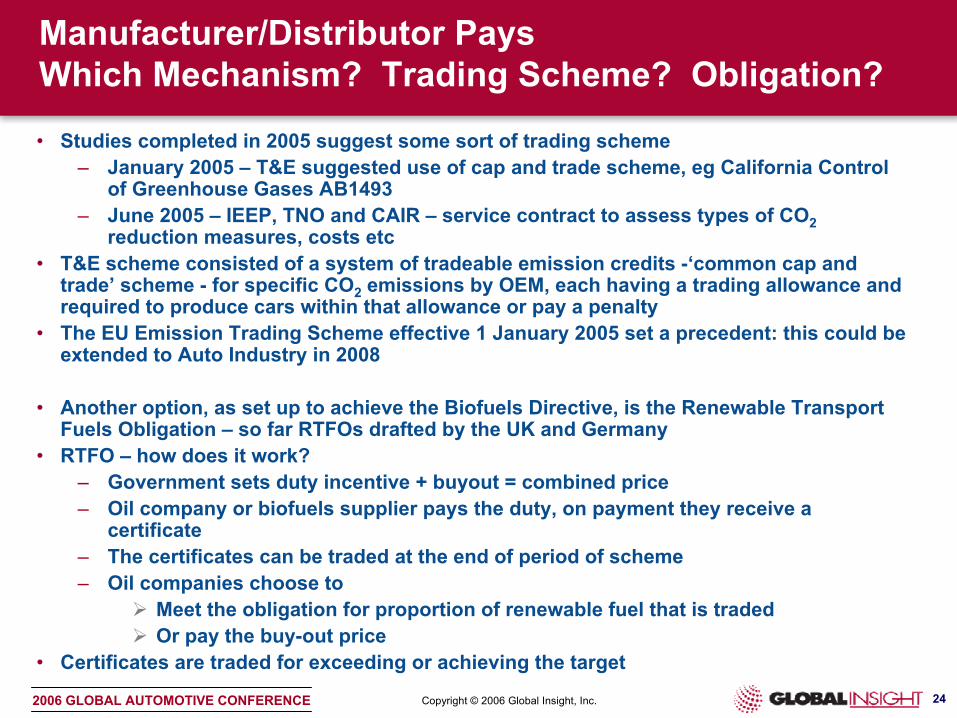

Manufacturer/Distributor Pays Which Mechanism? Trading Scheme? Obligation?

• Studies completed in 2005 suggest some sort of trading scheme– January 2005 – T&E suggested use of cap and trade scheme, eg California Control

of Greenhouse Gases AB1493 – June 2005 – IEEP, TNO and CAIR – service contract to assess types of CO2

reduction measures, costs etc• T&E scheme consisted of a system of tradeable emission credits -‘common cap and

trade’ scheme - for specific CO2 emissions by OEM, each having a trading allowance and required to produce cars within that allowance or pay a penalty

• The EU Emission Trading Scheme effective 1 January 2005 set a precedent: this could be extended to Auto Industry in 2008

• Another option, as set up to achieve the Biofuels Directive, is the Renewable Transport Fuels Obligation – so far RTFOs drafted by the UK and Germany

• RTFO – how does it work?– Government sets duty incentive + buyout = combined price– Oil company or biofuels supplier pays the duty, on payment they receive a

certificate – The certificates can be traded at the end of period of scheme – Oil companies choose to

Meet the obligation for proportion of renewable fuel that is traded Or pay the buy-out price

• Certificates are traded for exceeding or achieving the target

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 25

Impact Upon Auto Industry

Voluntary Agreement

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 26

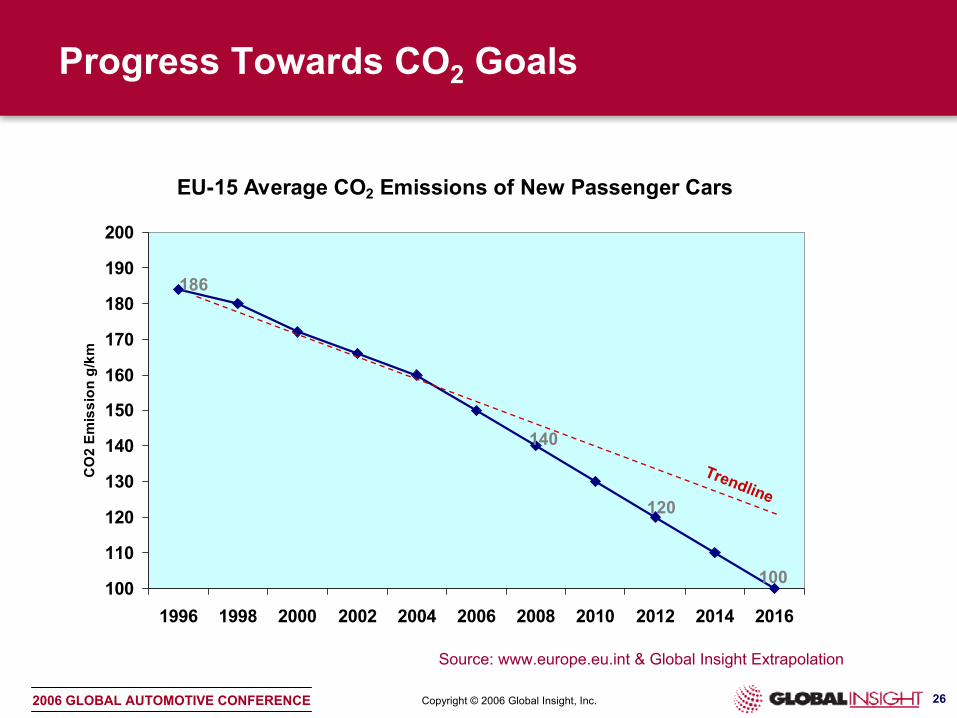

Progress Towards CO2 Goals

EU-15 Average CO2 Emissions of New Passenger Cars

100

110

120

130

140

150

160

170

180

190

200

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

CO

2 Em

issi

on g

/km

100

186

120

140

Trendline

Source: www.europe.eu.int & Global Insight Extrapolation

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 27

Impact Upon Auto Industry Voluntary Agreement

• There is no direct impact, no penalty, for failure to achieve voluntary agreement targets……..

• BUT the European Commission has made it clear that failing to meet the 140g/km CO2 target will lead to legislation

• And auto industry will feel pressure from other sources, e.g. investors interested to know the financial impact of having to meet the targets; continued pressure from the “green lobby”; continued pressure from alternative transport lobby groups

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 28

Impact Upon Auto Industry Voluntary Agreement

• Voluntary to mandatory

• Further, more demanding targets…. 100g/km by 2016 is the lobby groups favourite; or, more likely, 120g/km by 2012

• Measurement by OEM rather than by sectors of the industry – help identify good/bad performers/citizens

• Emissions trading scheme either g/km or €/ton easier to apply to individual OEMs

• Strengthening of already announced fiscal policy through changes in Registration Taxes, Circulation Taxes and, more generally, fiscal tools such as Fuel Tax, Company Car Tax

• Integrated approach (auto industry proposal)

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 29

Impact Upon Auto Industry Voluntary Agreement

• ACEA Proposal – An integrated approach– Consumer/Fuel Industry/Auto Industry/Transport

Managers– Auto industry technology improvements– Alternative fuels– Knock-on effect of new legislation (pedestrian safety

etc.)– Total CO2 emissions management (tons/year) instead of

tail pipe emissions (g/km)

• In itself insufficient so a voluntary agreement based on an integrated approach (only) will not be accepted

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 30

Post Voluntary Agreement Era

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 31

What Might the Post Voluntary Agreement Era Look Like?

• Information

– New car labelling

– Fuel quality labelling

• OEM responsibility for its vehicle sales weighted new fleet

• CO2 credits trading scheme

• Stronger application of fiscal policies (registration/circulation/company car/fuel tax – applied sooner, harder across EU 25

• An acceptance of an integrated approach (vehicle technology, fuel and fuel supply, infrastructure, consumer) without dilutionof the newly imposed EU mandatory requirements

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 32

What Might the Post Voluntary Agreement Era Look Like?

• Information/whole life criteria– Used vehicle labelling– Cost per kms per annum (10,000; 20,000; 30,000)– Total parc (not just new cars) – Aftermarket; Synthetic oils; Low rolling resistance tyres; Regular servicing

• OEM responsibility for its vehicle parc weighted fleet• CO2 credits trading scheme

– OEMS considered as one/two responsibility units (manufacturing and/or car use)

– Credit for EC wide renewable fuel content; CO2 from this source is benign• Congestion charging/road pricing• Fuel duties • Well to wheels measurement• CO2 tons per year

Has EU set the wrong performance standard (g/km)?

Copyright © 2006 Global Insight, Inc.2006 GLOBAL AUTOMOTIVE CONFERENCE 33

Conclusion

Pressure is on EU from many NGOs and GOs for more demandingaction to combat CO2 emissions If (when?) voluntary agreement targets are missed, or deemed to be missed, likely result will be:-

– Dissemination of information to continue – consumer encouraged to change his requirements and PULL low CO2vehicles into the market

– Legislation (with teeth), some sort of emissions trading, penalties for “failing” OEMs (and others) to PUSH low CO2 vehicles into the market

Won’t happen just through technology; need to involve user,alternative fuels will help as will a step change in transportmethods…….. the battle is far from won!