Embed Size (px)

Citation preview

MODULE: C341 M441 | PRODUCT: 4547

Legal Aspects of International Finance

Legal Aspects of International Finance

Module Introduction and Overview

Contents

1 Introduction to the Module 2

2 The Module Author 2

3 Study Resources 2

4 Module Overview 3

5 Learning Outcomes 6

Legal Aspects of International Finance

2 University of London

1 Introduction to the Module Welcome to this module on the legal aspects of international finance. The first unit will introduce you to some of the topics you will study. This introduction will provide and outline some important information on Assessment and the on the Study process.

The teaching of this module is based on English law and makes reference to the law of other jurisdictions where this is relevant. You will be shown how contractual principles are applied to commercial fundraising transactions and how to differentiate between legal principles and the market practices that shape these transactions.

We hope that you will find the module instructive, useful and occasionally challenging.

2 The Module Author Dr Dalvinder Singh is currently a Professor in the School of Law, University of Warwick. His area of research is in bank and financial regulation from both a policy and practical perspective in both the UK system and the US system, including European and international dimensions. Professor Singh is also a member of the Research and Guidance Committee of the International Asso-ciation of Deposit Insurers, Basel Switzerland, and Managing Editor of the Journal of Banking Regulation, and Financial Regulation International.

3 Study Resources This study guide is your main learning resource for the module as it directs your study through eight study units. Each unit has recommended reading either from the key text or from supplementary module readings.

Key text

Alastair Hudson (2013) The Law of Finance. 2nd Edition. London, Sweet & Maxwell.

This is a comprehensive and useful textbook covering this field. The text-book coverage has been complemented and supplemented by articles and extracts from other texts in the module readings.

Module readings

The module readings include a range of academic journal articles, extracts from supplementary textbooks and other reports or material.

Please feel free to raise queries with your tutor and with your fellow students, if there are issues that are not clear to you. Do this as soon as you find a problem, because waiting will hold you up as you work through the module.

Specimen Examination

Centre for Financial and Management Studies 3

4 Module Overview The module is structured around eight units, which should be studied on a weekly basis. It is expected that studying each unit, including the recom-mended readings and activities, will take between 15 and 20 hours. However, these timings may vary according to your familiarity with the subject matter and your own study experience. You will receive feedback through comments on your assignments and there is a specimen examina-tion paper to help you prepare for the final examination.

Unit 1 The Law of International Finance

1.1 Introduction 1.2 The International Financial Market 1.3 Introduction to International Finance 1.4 Legal Aspects of International Finance 1.5 Introduction to International Capital Markets 1.6 Dealing with Risk in International Finance 1.7 Conclusion

Unit 2 International Loan Finance

2.1 Introduction 2.2 International Term Loan Agreements 2.3 Syndicated Loans 2.4 Structure of Typical Syndicated Loan 2.5 Secondary Market 2.6 Conclusion

Unit 3 Corporate and Sovereign Bonds

3.1 Introduction 3.2 Forms and Legal Characteristics of International Bonds 3.3 Issuing an International Bond – the Parties and Documentation 3.4 Issuing, Marketing and Distributing the Bonds 3.5 Basic Legal Terms and Conditions 3.6 Tax Considerations 3.7 Contractual Aspects of Sovereign Bond Offerings 3.8 A Brief Note on State Insolvency 3.9 Differences between Corporate and Sovereign Bonds 3.10 Conclusion

Unit 4 Project Finance

4.1 Introduction 4.2 What is Project Finance? 4.3 Special Features of Project Finance 4.4 Security in Project Finance 4.5 Some Particular Types of Contract 4.6 PPPs and PFIs 4.7 Conclusion

Legal Aspects of International Finance

4 University of London

Unit 5 Financial Derivatives and Securitisation

5.1 Introduction to Financial Derivatives 5.2 Basic Aspects of International Derivatives Markets 5.3 Managing Legal Risk in International Derivative Transactions 5.4 Capacity and Authority to Enter into Financial Derivative Contracts 5.5 Termination and Close-Out Netting 5.6 The Structure and Main Provisions of the 2002 ISDA Master Agreement 5.7 Central Counterparties 5.8 Trade Repositories 5.9 Securitisation 5.10 Conclusion

Unit 6 Alternative Investment Funds

6.1 Alternative Investments 6.2 Private Equity 6.3 Equity-Debt-Leverage Finance 6.4 Hedge Funds 6.5 Risks 6.6 Comparing Hedge Funds and Private Equity Funds 6.7 Conclusion

Unit 7 Payment and Securities Settlement Systems

7.1 Introduction and Overview of Payment Systems 7.2 Risks and Legal Issues in Payment Systems 7.3 Types of Payment System 7.4 Securities Settlement Systems 7.5 Risks and Legal Issues in Securities Settlement Systems 7.6 Implications of Using Intermediaries 7.7 Financial Collateral 7.8 Conclusion

Unit 8 Conflict of Laws, Jurisdiction and Enforcement

8.1 Introduction to the Conflict of Financial Laws 8.2 The Choice of Governing Law by the Parties 8.3 Choice of Jurisdiction 8.4 Legal Opinions 8.5 Conclusion – Conflict of Laws and International Financial Markets

This is a module on the legal aspects of raising different forms of interna-tional finance and how international finance disputes are settled.

Unit 1 provides a primer on the size of the global financial markets and some international legal principles governing the flow of capital across borders. It looks at the role of primary and secondary markets and the importance of financial depth of markets. In it, we will set out in simple terms the different features of debt and equity finance and some of the key risks in international finance. The module is designed to introduce you to the different forms of international finance and then some of the

Specimen Examination

Centre for Financial and Management Studies 5

underlying issues, such as payment and settlement systems in Unit 7 and conflicts of law and jurisdiction in Unit 8.

The issues in Units 7 and 8 bring together all the components of the module. The forms of finance and their structures are explored in Units 2, 3, 4, 5 and 6. Unit 2 looks at basic forms of loan finance. Bilateral and syndicated loans are a common means for governments and corporate borrowers to raise large sums in the financial market. The unit starts by looking at the key contractual features of a bilateral loan and a syndicated loan. A crucial component of the syndicated loan market that will be explored in detail is the secondary market.

Moving on from the basics of loan finance, we look at the other principal form of debt finance namely Bonds. The main purpose of Unit 3 is to exam-ine the main legal aspects and terms of international corporate and sovereign bonds. Specific emphasis is placed on the key contractual provi-sions and their purpose. It finally explores the distinguishing features of corporate and sovereign bonds. The forms of finance explored in Units 2 and 3 provide the underlying basis of project finance.

Project finance is a tremendously complex and multi faceted form of infra-structure finance. However, Unit 4 provides an overview of the key features and parties involved in negotiating project finance. The unit will outline and discuss the main documents, transactions and parties involved in the financ-ing of international projects. Moving on from the traditional forms of finance, we then explore the role of derivatives and securitisation as forms of finance. Financial derivatives and securitisation can together be referred to as refinancing techniques since they facilitate the repackaging of assets and allow risk management.

In examining the different forms of debt finance, the module introduces some aspects of equity finance by exploring the role of Private Equity and Hedge Funds, as alternative. As noted above, Unit 7 will look at payment systems and securities settlement systems. In practice, these are closely bound up with payment systems, since one ‘leg’ of the settlement of securi-ties transaction will generally involve a payment being made. The unit will go on to look at the main issues raised by the use of intermediaries to hold securities, since this practice is now very much bound up with the way in which securities settlement systems operate.

Every legal issue under a financial contract must be determined in accord-ance with a system of law and litigated in a court located somewhere regardless of whether it involves parties in different countries or within a single location. Those are the key issues explored in Unit 8. In this final unit of the module, you will study the choice of governing law and the choice of jurisdiction by the parties concerned.

Legal Aspects of International Finance

6 University of London

5 Learning Outcomes When you have completed your study of this module, you will be able to:

• outline the difference forms of international finance available in global capital markets and the role of the primary and secondary market

• evaluate the key issues associated with the different forms of debt finance and alternative investment funds

• determine the role of the various parties involved in the different forms of international finance

• evaluate the importance of derivatives and securitisation as a form of international finance and risk management technique

• analyse the key contractual provisions and documentation associated with the different forms of debt finance and alternative investment finance

• explain the role of payment and settlement systems in international finance

• critically assess the importance of the choice of law and jurisdiction clause in international financial transactions.

Assessment Your performance on each module is assessed through two written assignments and one examination. The assignments are written after Unit 4 and Unit 8 of the module session. Please see the VLE for submission deadlines. The examination is taken at a local examination centre in September/October.

Preparing for assignments and exams

The examinations you will sit are designed to evaluate your knowledge and skills in the subjects you have studied; they are not designed to trick you. If you have studied the module thoroughly, you will pass the exam.

Understanding assessment questions

Examination and assignment questions are set to test your knowledge and skills. Sometimes a question will contain more than one part, each part testing a different aspect of your skills and knowledge. You need to spot the key words to know what is being asked of you. Here we categorise the types of things that are asked for in assignments and exams, and the words used. All the examples are from the Centre for Financial and Management Studies examination papers and assignment questions.

Definitions

Some questions mainly require you to show that you have learned some concepts by setting out their precise meanings. Such questions are likely to be preliminary and will be supplemented by more analytical questions. Generally, ‘Pass marks’ are awarded if the answer only contains definitions. These questions will contain words such as:

describe contrast define write notes on examine outline distinguish between what is meant by compare list.

Reasoning

Other questions are designed to test your reasoning, by asking you to explain cause and effect. Convincing explanations generally carry more marks than basic definitions. These questions will include words such as:

interpret explain what conditions influence what are the consequences of what are the implications of.

Judgement

Others ask you to make a judgement, perhaps of a policy or a course of action. They will include words like:

evaluate critically examine

assess do you agree that to what extent does.

Calculation

Sometimes you are asked to make a calculation using a specified technique; these questions begin:

use indifference curve analysis to using any economic model you know calculate the standard deviation test whether.

It is most likely that questions that ask you to make a calculation will also ask for an application or interpretation of the result.

Advice

Other questions ask you to provide advice in a particular situation. This applies to law questions and to policy papers where advice is asked in relation to a policy problem. Your advice should be based on relevant law, applicable principles, and evidence of what actions are likely to be effective. The questions may begin:

advise provide advice on explain how you would advise.

Critique

In many cases the question will include the word ‘critically’. This means that you are expected to look at the question from at least two points of view, offering a critique of each view and your judgement. You are expected to be critical of what you have read.

The questions may begin:

critically analyse critically consider critically assess critically discuss the argument that.

Examine by argument

Questions that begin with ‘discuss’ are similar; they ask you to examine by argument, to debate and give reasons for and against a variety of options. For example:

discuss the advantages and disadvantages of discuss this statement discuss the view that discuss the arguments and debates concerning.

The grading scheme: assignments

The assignment questions contain fairly detailed guidance about what is required. All assignments are marked using marking guidelines. When you receive your grade, it is accompanied by comments on your paper, including advice about how you might improve, and any clarifications about matters you may not have

understood. These comments are designed to help you master the subject and to improve your skills as you progress through your programme.

Postgraduate assignment marking criteria

The marking scheme for your programme draws upon these minimum core criteria, which are applicable to the assessment of all assignments:

• understanding of the subject • utilisation of proper academic or other style (eg citation of references, or use

of proper legal style for court reports) • relevance of material selected and arguments proposed • planning and organisation • logical coherence • critical evaluation • comprehensiveness of research • evidence of synthesis • innovation/creativity/originality.

The language used must be of a sufficient standard to permit assessment of these aspects.

The guidelines below reflect the standards of work expected at postgraduate level. All assessed work is marked by your tutor or a member of academic staff, and a sample is then moderated by another member of academic staff. Any assignment may be made available to the external examiner(s).

80+ (Distinction). A mark of 80+ will fulfil the following criteria:

• very significant ability to plan, organise and execute independently a research project or coursework assignment

• very significant ability to evaluate literature and theory critically and make informed judgements

• very high levels of creativity, originality and independence of thought • very significant ability to critically evaluate existing methodologies and

suggest new approaches to current research or professional practice • very significant ability to analyse data critically • outstanding levels of accuracy, technical competence, organisation and

expression.

70–79 (Distinction). A mark in the range 70–79 will fulfil the following criteria:

• significant ability to plan, organise and execute independently a research project or coursework assignment

• clear evidence of wide and relevant reading, referencing and an engagement with the conceptual issues

• capacity to develop a sophisticated and intelligent argument • rigorous use and a sophisticated understanding of relevant source

materials, balancing appropriately between factual detail and key theoretical issues. Materials are evaluated directly, and their assumptions and arguments challenged and/or appraised

• correct referencing • significant ability to analyse data critically • original thinking and a willingness to take risks.

60–69 (Merit). A mark in the 60–69 range will fulfil the following criteria:

• ability to plan, organise and execute independently a research project or coursework assignment

• strong evidence of critical insight and thinking • a detailed understanding of the major factual and/or theoretical issues and

direct engagement with the relevant literature on the topic • clear evidence of planning and appropriate choice of sources and

methodology with correct referencing • ability to analyse data critically • capacity to develop a focused and clear argument and articulate clearly and

convincingly a sustained train of logical thought.

50–59 (Pass). A mark in the range 50–59 will fulfil the following criteria:

• ability to plan, organise and execute a research project or coursework assignment

• a reasonable understanding of the major factual and/or theoretical issues involved

• evidence of some knowledge of the literature with correct referencing • ability to analyse data • examples of a clear train of thought or argument • the text is introduced and concludes appropriately.

40–49 (Fail). A Fail will be awarded in cases in which there is:

• limited ability to plan, organise and execute a research project or coursework assignment

• some awareness and understanding of the literature and of factual or theoretical issues, but with little development

• limited ability to analyse data • incomplete referencing • limited ability to present a clear and coherent argument.

20–39 (Fail). A Fail will be awarded in cases in which there is:

• very limited ability to plan, organise and execute a research project or coursework assignment

• failure to develop a coherent argument that relates to the research project or assignment

• no engagement with the relevant literature or demonstrable knowledge of the key issues

• incomplete referencing • clear conceptual or factual errors or misunderstandings • only fragmentary evidence of critical thought or data analysis.

0–19 (Fail). A Fail will be awarded in cases in which there is:

• no demonstrable ability to plan, organise and execute a research project or coursework assignment

• little or no knowledge or understanding related to the research project or assignment

• little or no knowledge of the relevant literature • major errors in referencing • no evidence of critical thought or data analysis • incoherent argument.

The grading scheme: examinations

The written examinations are ‘unseen’ (you will only see the paper in the exam centre) and written by hand over a three-hour period. We advise that you practise writing exams in these conditions as part of your examination preparation, as it is not something you would normally do.

You are not allowed to take in books or notes to the exam room. This means that you need to revise thoroughly in preparation for each exam. This is especially important if you have completed the module in the early part of the year, or in a previous year.

Details of the general definitions of what is expected in order to obtain a particular grade are shown below. These guidelines take account of the fact that examination conditions are less conducive to polished work than the conditions in which you write your assignments. Note that as the criteria for each grade rise, they accumulate the elements of the grade below. Assignments awarded better marks will therefore have become comprehensive in both their depth of core skills and advanced skills.

Postgraduate unseen written examinations marking criteria

80+ (Distinction). A mark of 80+ will fulfil the following criteria:

• very significant ability to evaluate literature and theory critically and make informed judgements

• very high levels of creativity, originality and independence of thought • outstanding levels of accuracy, technical competence, organisation and

expression • outstanding ability of synthesis under exam pressure.

70–79 (Distinction). A mark in the 70–79 range will fulfil the following criteria:

• clear evidence of wide and relevant reading and an engagement with the conceptual issues

• development of a sophisticated and intelligent argument • rigorous use and a sophisticated understanding of relevant source

materials, balancing appropriately between factual detail and key theoretical issues

• direct evaluation of materials, and challenging and/or appraisal of their assumptions and arguments

• original thinking and a willingness to take risks • significant ability of synthesis under exam pressure.

60–69 (Merit). A mark in the 60–69 range will fulfil the following criteria:

• strong evidence of critical insight and critical thinking • a detailed understanding of the major factual and/or theoretical issues and

direct engagement with the relevant literature on the topic • development of a focused and clear argument, with clear and convincing

articulation of a sustained train of logical thought • clear evidence of planning and appropriate choice of sources and

methodology, and ability of synthesis under exam pressure.

50–59 (Pass). A mark in the 50–59 range will fulfil the following criteria:

• a reasonable understanding of the major factual and/or theoretical issues involved

• evidence of planning and selection from appropriate sources • some demonstrable knowledge of the literature • the text shows, in places, examples of a clear train of thought or argument • the text is introduced and concludes appropriately.

40–49 (Fail). A Fail will be awarded in cases in which:

• there is some awareness and understanding of the factual or theoretical issues, but with little development

• misunderstandings are evident • there is some evidence of planning, although irrelevant/unrelated material

or arguments are included.

20–39 (Fail). A Fail will be awarded in cases which:

• fail to answer the question or to develop an argument that relates to the question set

• do not engage with the relevant literature or demonstrate a knowledge of the key issues

• contain clear conceptual or factual errors or misunderstandings.

0–19 (Fail). A Fail will be awarded in cases which:

• show no knowledge or understanding related to the question set • show no evidence of critical thought or analysis • contain short answers and incoherent argument.

[2015–16: Learning & Teaching Quality Committee]

DO NOT REMOVE THE QUESTION PAPER FROM THE EXAMINATION HALL

UNIVERSITY OF LONDON

CENTRE FOR FINANCIAL AND MANAGEMENT STUDIES

MSc Examination Postgraduate Diploma Examination for External Students

91DFM C241 91DFM C341

FINANCE AND FINANCIAL LAW

Legal Aspects of International Finance

Specimen Examination This is a specimen examination paper designed to show you the type of examination you will have at the end of the year for Legal Aspects of International Finance. The number ofquestions and the structure of the examination will be the same as on this one, but the wording and the requirements of each question will be different. Best wishes for success on your final examination.

You have THREE hours to complete the examination.

You must answer THREE questions. Answer at least ONE question from Section A. The remaining two questions may be chosen from either Section A or Section B.

PLEASE TURN OVER

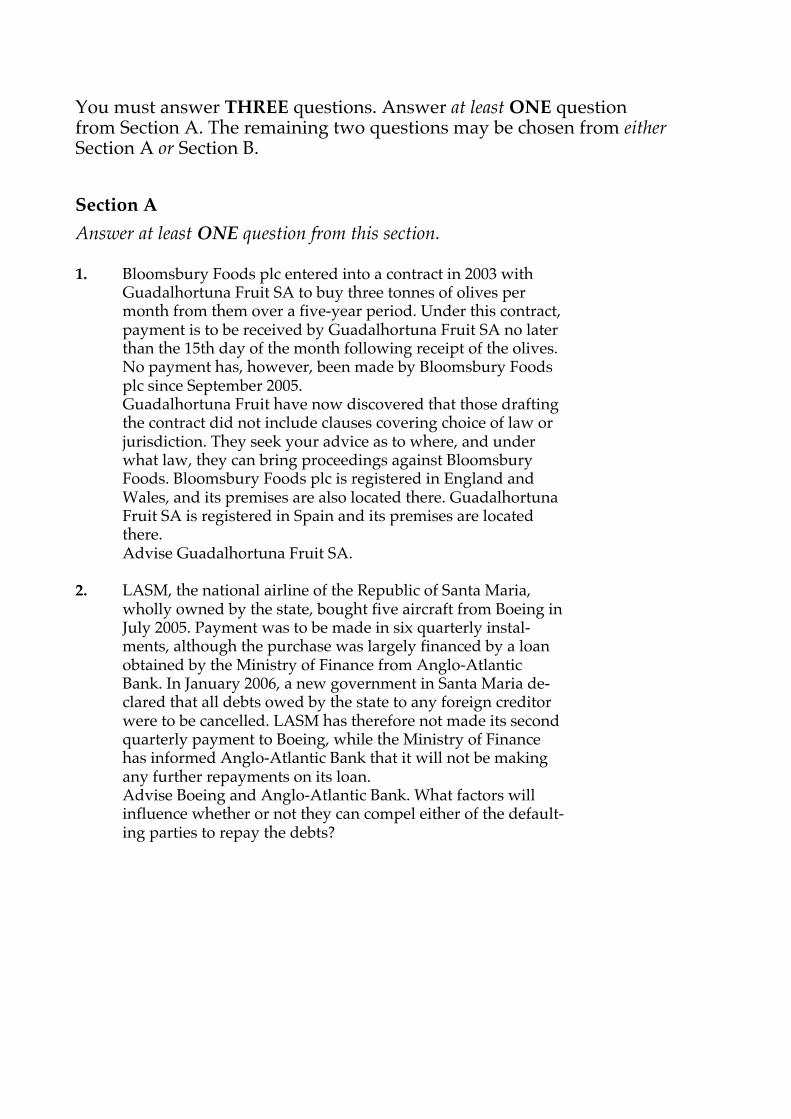

You must answer THREE questions. Answer at least ONE question from Section A. The remaining two questions may be chosen from either Section A or Section B.

Section A Answer at least ONE question from this section.

1. Bloomsbury Foods plc entered into a contract in 2003 withGuadalhortuna Fruit SA to buy three tonnes of olives permonth from them over a five-year period. Under this contract,payment is to be received by Guadalhortuna Fruit SA no laterthan the 15th day of the month following receipt of the olives.No payment has, however, been made by Bloomsbury Foodsplc since September 2005.Guadalhortuna Fruit have now discovered that those draftingthe contract did not include clauses covering choice of law orjurisdiction. They seek your advice as to where, and underwhat law, they can bring proceedings against BloomsburyFoods. Bloomsbury Foods plc is registered in England andWales, and its premises are also located there. GuadalhortunaFruit SA is registered in Spain and its premises are locatedthere.Advise Guadalhortuna Fruit SA.

2. LASM, the national airline of the Republic of Santa Maria,wholly owned by the state, bought five aircraft from Boeing inJuly 2005. Payment was to be made in six quarterly instal-ments, although the purchase was largely financed by a loanobtained by the Ministry of Finance from Anglo-AtlanticBank. In January 2006, a new government in Santa Maria de-clared that all debts owed by the state to any foreign creditorwere to be cancelled. LASM has therefore not made its secondquarterly payment to Boeing, while the Ministry of Financehas informed Anglo-Atlantic Bank that it will not be makingany further repayments on its loan.Advise Boeing and Anglo-Atlantic Bank. What factors willinfluence whether or not they can compel either of the default-ing parties to repay the debts?

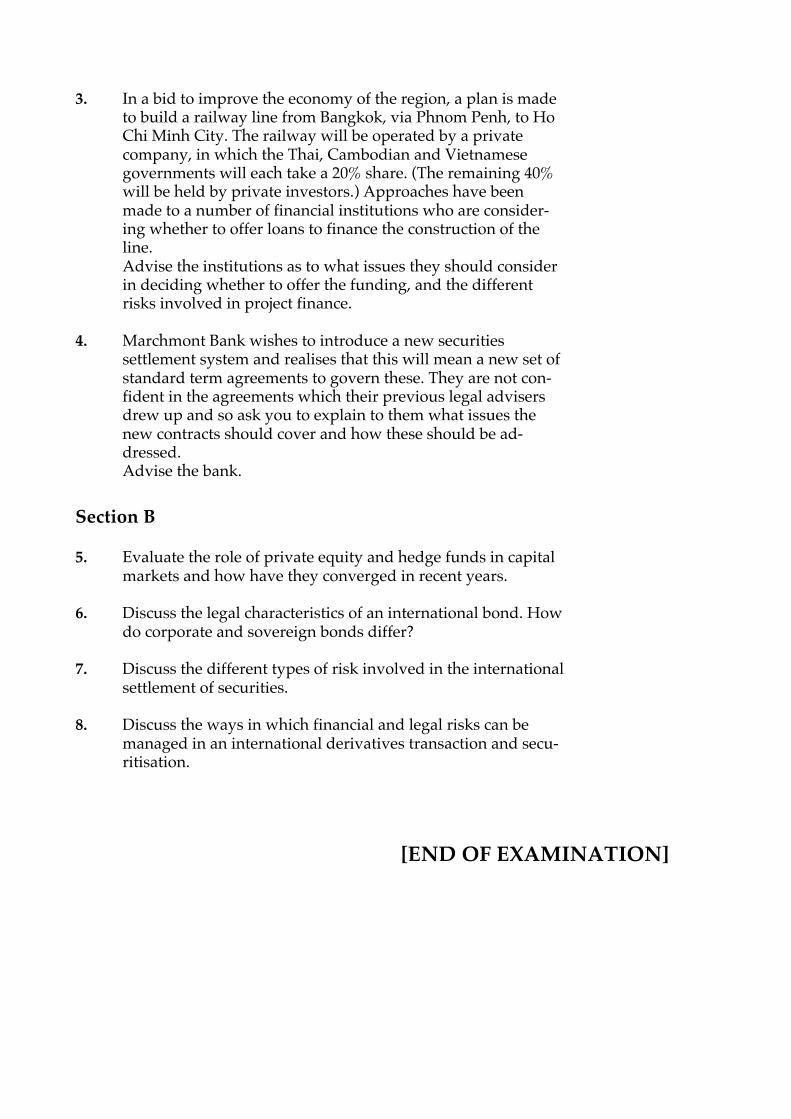

3. In a bid to improve the economy of the region, a plan is madeto build a railway line from Bangkok, via Phnom Penh, to HoChi Minh City. The railway will be operated by a privatecompany, in which the Thai, Cambodian and Vietnamesegovernments will each take a 20% share. (The remaining 40%will be held by private investors.) Approaches have beenmade to a number of financial institutions who are consider-ing whether to offer loans to finance the construction of theline.Advise the institutions as to what issues they should considerin deciding whether to offer the funding, and the differentrisks involved in project finance.

4. Marchmont Bank wishes to introduce a new securitiessettlement system and realises that this will mean a new set ofstandard term agreements to govern these. They are not con-fident in the agreements which their previous legal advisersdrew up and so ask you to explain to them what issues thenew contracts should cover and how these should be ad-dressed.Advise the bank.

Section B

5. Evaluate the role of private equity and hedge funds in capitalmarkets and how have they converged in recent years.

6. Discuss the legal characteristics of an international bond. Howdo corporate and sovereign bonds differ?

7. Discuss the different types of risk involved in the internationalsettlement of securities.

8. Discuss the ways in which financial and legal risks can bemanaged in an international derivatives transaction and secu-ritisation.

[END OF EXAMINATION]

Legal Aspects of International Finance

Unit 1 The Law of International Finance

Contents

Unit Overview 2

1.1 Introduction 3

1.2 The International Financial Market 6

1.3 Introduction to International Finance 7

1.4 Legal Aspects of International Finance 9

1.5 Introduction to International Capital Markets 12

1.6 Dealing with Risk in International Finance 14

1.7 Conclusion 16

References 16

Legal Aspects of International Finance

2 University of London

Unit Overview Welcome to this module on the legal aspects of international finance. Unit 1 offers a primer on the global financial market, the various financial assets and types of financial flows across borders. In doing so, it examines the concept of legal risk and the need for international legal principles, and contracts governing the flow of capital across borders. We will also look at various types of financial flows. In studying this first unit, you will learn about different types of international financial assets and cross-border capital flows, and you should be prepared for studying the following units, where all these issues are examined in detail.

Learning outcomes

When you have completed your study of this unit and its readings, you will be able to:

• identify the various types of financial assets and cross-border financial flows

• distinguish between domestic and international financial transactions and identify the main characteristics of international financial contracts

• identify the various categories of legal and political risk relating to international financial transactions and explain how lenders and borrowers manage those risks.

Reading for Unit 1

Gerd Häusler (2002) ‘The globalization of finance’. Finance & Development, 39 (1).

Hal Scott (2000) ‘Internationalization of primary public securities markets’. Law and Contemporary Problems, 63 (3), 71–104.

Lee Buchheit (2007) ‘Law, ethics and international finance’. Law and Contemporary Problems, 70 (3), 1–6.

Ingo Walter (1982) ‘Country risk and international bank lending’. University of Illinois Law Review, 1, 71–88.

James Woepking (1999) ‘International capital markets and their importance’. Transnational Law and Contemporary Problems, 9, 233–246.

Richard Debs (1987) ‘Globalization of financial markets: “What is happening and why”’. International Business Lawyer, 15, 198–202.

Michael Gruson (1996) ‘Management of legal risks in international agreements’. Willamette Bulletin of International Law and Policy, 4, 27–41.

Alastair Hudson (2013) Chapter 1 ‘The components of the law of finance’. In: The Law of Finance. 2nd Edition. London, Sweet & Maxwell. pp. 5–38.

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 3

1.1 Introduction This module naturally complements another of the Finance and Financial law core modules, Financial Law, which you may already have taken. (Those of you who have not, rest assured that no prior knowledge of that module is assumed.) The Financial Law module discusses the various ways in which the financial needs of commercial undertakings and private individuals alike are met by legal structures created by the jurisdiction in which they operate. English law is used as a model, but the principles may be applied to any legal jurisdiction, save that the intervention of the state may be greater in some jurisdictions than others. The principles learned in the Financial Law module mainly apply where the financial transactions concerned operate within one jurisdiction.

However, more and more, commerce and finance has become international in nature to exploit new markets and raise finance at competitive rates. As international commerce and finance has grown, so the law has adapted to keep pace with it. However, as you will appreciate after completing this module, significant reliance is still placed on private mechanisms to settle disputes. This is the focus of Legal Aspects of International Finance.

The financial sector consists of many types of activities, institutions and markets. The notions of international finance and international financial market encompass the totality of those activities and markets, while capital markets are essentially made up of equity, debt and derivatives finance and markets. This module will focus primarily on debt finance, derivatives finance, private equity and hedge funds as ‘new forms of finance’, and then on payment and settlements and conflicts of law issues. It will focus on the primary markets for raising finance and then also look at the secondary markets where necessary for the purposes of refinancing and managing portfolio risks. When we consider the sophistication and depth of capital markets, focus is on the existence of both a primary and secondary market.

As you know, financial markets facilitate the transfer of financial assets – ie the transfer of funds from those who have surplus funds to invest (‘savers’ or ‘investors’) to those whose spending exceeds, or is going to exceed, their income and therefore need additional funds to invest in tangible assets or finance their current operations, or even consume (‘borrowers’). Companies borrowing money in the international syndicated loan markets, individuals borrowing to finance the acquisition of residential property in another jurisdiction or governments borrowing to finance their public spending are all ‘borrowers’ and rely on borrowed funds from domestic and international financial markets. Other forms of finance arise from techniques that are generally referred to as refinancing techniques through the secondary markets in the form of loan transfers and financial derivatives.

This flow of funds from ‘savers’ or ‘investors’ to ‘borrowers’ is made possi-ble by the activities of financial intermediaries and financial markets such as securities brokers, commercial banks, investment banks etc. Regarding the

Legal Aspects of International Finance

4 University of London

mode of financial flows, funds flow from ‘savers’ to ‘borrowers’ either directly or via the operations of a financial intermediary.

In the first case, ‘borrowers’ receive funds directly from ‘savers’. In return, ‘savers’ acquire debt, equity or mixed-type claims in the form of primary securities. Financial intermediaries facilitate this process, assisting in the design, marketing and completion of the transaction. These financial in-struments are marketable in secondary markets.

In intermediated flows, financial intermediaries engage in the business of receiving funds from ‘savers’ and lending funds to ‘borrowers’. The flow of funds from intermediaries to ‘borrowers’ occurs either in the form of direct financial accommodation or by means of purchasing from borrowers’ primary debt, equity or mixed-type securities.

The ultimate objective and benchmark of international finance is the undis-turbed flow of funds from ‘savers’ to ‘borrowers’ regardless of national borders. When a South African cement company desires to raise €400 million in the European markets to fund the acquisition of plant or equip-ment, the company may borrow the funds from an international bank syndicate or it may issue debt securities (‘notes’ or ‘bonds’) in the interna-tional bond markets. Regardless of the legal form of the borrowing (whether a bank loan or a securities offering), the objective of the international financ-ing is the availability and movement of €400 million to the South African company in question. International finance is all about moving money across borders. Legal aspects of international finance cover the legal risks and protections available to those participating in those markets.

If a cross-border financial flow (ie the movement of capital from one jurisdic-tion to another) is the essence and sole objective of international finance, we should examine its legal treatment in some detail.

The OECD Code of Liberalisation of Capital Movements, under which OECD countries have accepted legally binding obligations to liberalise capital movements, sets out a comprehensive typology of cross-border financial flows. In accordance with the OECD typology, one may identify the following types of transfers:

a) operations in securities or collective investment securities (CIS) on capital markets, in particular (i) the private placement, public sale or introduction of equity or debt securities or CIS on a foreign organised or OTC capital market; for example, a UK-based software company issues shares to investors in the United States and introduces its shares for listing and trading into the New York Stock Exchange and (ii) purchases or sales of equity or debt securities or CIS abroad by residents; for example, a private equity fund established and operating in the United Kingdom invests in equities and bonds listed on Euronext Paris

b) the deposit of funds by non-residents with resident financial institutions and vice-versa; for example, E.ON AG, a German energy

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 5

company with huge cash reserves makes a deposit of €5 billion with a bank in the London market

c) credits and loans granted by non-residents to residents and vice-versa; for example, a consortium of London-based commercial banks, led by The Royal Bank of Scotland Group, arrange for a syndicated loan of €45 billion to be provided to the government of Indonesia

d) the purchase or sale of domestic currency with or for foreign currency by residents abroad or by non-residents in the domestic market

e) sureties, guarantees and financial back-up facilities by non-residents to residents or vice-versa; for example, E.ON AG provides a full and unconditional guarantee for the bonds issued by E.ON International Finance B.V. the wholly-owned subsidiary of E.ON AG. While the issuer of the bonds is a Dutch entity, the guarantor is a German entity and the guarantee is therefore provided on a cross-border basis.

Each of the international financial transactions listed above has its domestic counterpart. A loan of a UK bank to the government of Indonesia is not conceptually different from a loan given by a UK bank to a company in Surrey, England. They are both loans, in that they involve the provision of credit and the supply of funds in return of a promise by the borrower to repay the loan and also pay some interest. They are both documented in a loan agreement signed between the lender and the borrower. The two loan agreements have a lot of similarities, including a long list of provisions governing the payment of the loan, the payment of interest, event of default, how the lenders may request early repayment of the loan etc.

You should appreciate, however, that there is a limit to the similarities of the two loans. The reality is that a domestic loan by a UK bank to a UK borrow-er is, from a legal and financial perspective, also very different from a cross-border loan by a syndicate of banks to an Indonesian person. The fact that the loan involves parties in two different countries, involving two, or per-haps more, different legal systems raises a range of issues that purely domestic transactions do not have to resolve. The international aspects of legal issues relating to cross-border financial transactions such as loans or bond offerings will be the subject matter of this module.

Reading 1.1

As your first reading, please study Gerd Häusler’s 2002 paper on the globalisation of finance.

The author observes that during the final two decades of the 20th century, financial markets around the world became increasingly interconnected. He argues that financial globalisation had brought considerable benefits to national economies and to investors and savers, but it also changed the structure of markets, creating new risks and challeng-es for markets participants and policymakers.

Make sure your notes cover the main points raised.

Häusler (2002) ‘The globalization of finance’. Reproduced in the Module Reader from Finance & Development

Legal Aspects of International Finance

6 University of London

1.2 The International Financial Market According to the McKinsey Global Institute’s (2013)) annual analysis of long-term trends that are reshaping global capital markets, the total value of the world’s financial assets has declined in recent years due to the impact of the Global Financial Crisis (GFC). The financial bubble in the form of equity valuations and private debt finance has burst, therefore setting the global financial system back several decades, both in developed and emerging markets. The 2013 McKinsey report highlights that the depth and size of the markets for international finance remain staggeringly high but the impact of the GFC has had a significant impact on the size and volume of global financial assets. According to the 2013 report, the totality of ’equity market capitalization, corporate and government bonds and loans – grew from around $12 trillion in 1980 to $206 trillion in 2007’ (p. 2). Over-the-Counter (OTC) derivatives, an area of finance that caught considerable policy atten-tion, remain an important source of refinancing with notional $693 trillion concentrated in a dozen or so countries still outstanding by mid-2013. The legal aspects of derivatives are looked at in Unit 5. However, the impact of the GFC has meant that the world’s financial assets have only grown to $225 trillion since 2007, which represents a slowdown of 43 per cent due to a fall in average growth per annum, from a previous 7.9 per cent to 1.9 per cent. The report further highlights that the GFC has also had a significant impact on the growth and size of international finance. According to the report:

cross border capital flows rose from $0.5 trillion in 1980 to a peak of $11.8 trillion in 2007. But they collapsed during the crisis, and as of 2012, they remain more than 60 percent below their former peak

Source: McKinsey Global Institute (2013) p. 3.

A primary cause of the decline has been that financial institutions have undergone a process of deleveraging since the GFC both in developed and emerging market economies. However, the stagnation in the advanced economies has been countered by a sizeable increase in investment in emerging market economies. According to the report, the level of foreign capital directed towards emerging economies in 2013, amounted to $1.5 trillion.

Another indicator of growth in international financial flows is the global value of all foreign direct investments, which now accounts for approxi-mately 40 per cent of global capital flows. Notwithstanding this, McKinsey estimate that foreign direct investment fell by 15 per cent in 2012. However, what is notable is the level of individual country investment in certain regions – China provided to Latin America and Africa a larger amount of finance than the Latin American Development Bank and World Bank, respectively. This trend is not unusual with a significant proportion of foreign investment in emerging market economies now originating from other emerging market economies. It is estimated that the proportion of global growth emanating from emerging market economies will be around

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 7

70 per cent by 2025 in light of the slowdown in advanced economies, accord-ing to the 2013 McKinsey report.

The reliance on international capital markets remains essential for two primary reasons:

1. the need for competitive sources of finance and 2. to bridge the limited options in one’s home jurisdiction as to the forms

of finance.

In the emerging market economies, the depth of the financial markets varies considerably and so the options firms have available to raise finance, other than traditional bank finance, are limited due to the shallowness of their capital markets, in comparison with developed economies. Therefore, the demand for international sources of finance is likely to remain strong.

1.3 Introduction to International Finance Borrowers, primarily corporations, raise cash in two principal ways – by issuing equity or by issuing debt. The equity consists largely of common stock, but companies may also issue preferred stock. Internationally, the raising of cash takes primarily the form of international debt issuance (in the form of international debt securities offerings or international loans) or international equity issuance (in the form of international share offerings to investors, often combined with a foreign stock exchange listing). We will briefly examine international equity offerings, and we will then move on to international debt issuance.

1.3.1 International equity finance

A share (also referred to as ‘equity share’) of stock represents a share of ownership in a corporation. Stock typically takes the form of shares of common stock (or voting shares). As a unit of ownership, common stock typically carries voting rights that can be exercised in corporate decisions. Preferred stock differs from common stock in that it typically does not carry voting rights but is legally entitled to receive a certain level of dividend payments before any dividends can be issued to other shareholders. Con-vertible preferred stock is preferred stock that includes an option for the holder to convert the preferred shares into a fixed number of common shares, usually any time after a predetermined date.

Although there is a great deal of commonality between the stocks of differ-ent companies, each new equity issue can have legal clauses attached to it that make it dynamically different from the more general cases. Some shares of common stock may be issued without the typical voting rights being included, for instance, or some shares may have special rights unique to them and be issued only to certain parties. Note that not all equity shares are the same.

Legal Aspects of International Finance

8 University of London

In addition to voting rights, holders of shares of common stock have the right to share in distributions of the company’s income, the right to purchase new shares issued by the company, and the right to a company’s assets during a liquidation of the company (unless the company is insolvent).

As part of international finance, international equity finance involves the issuance and sale of shares of common stock to non-residents. For example, a Greek corporation with shares listed on the Athens Stock Exchange de-cides to raise equity finance abroad and conducts marketing activities in view of selling some of its shares to institutional investors such as insurance companies and pension funds in the United States. As a result of its market-ing activities, the Greek company manages to sell approximately 10 per cent of its common stock to investors in the United States who, as a result of their investment, have now become the company’s shareholders. Stock exchanges where equity securities are listed have greatly facilitated the purchase of equity securities by non-resident investors in international equity financings.

A stock exchange is an organisation that provides a marketplace for either physical or virtual trading of shares, bonds and warrants and other financial products where investors (represented by stock brokers) may buy and sell shares of a wide range of companies. A company will usually list its shares by satisfying and maintaining the listing requirements of a particular stock exchange.

Many large companies choose to list on several major exchanges within and outside their home country in order to broaden their investor base. Regard- less of the location of the shareholder, the legal rights and duties of share-holder are governed by the law of the country of incorporation of the company and its articles of association. Nevertheless, foreign shareholders encounter several legal risks and issues including those of tax of foreign equity investments, transfer restrictions, issues with voting rights etc.

1.3.2 International debt finance

When companies borrow money, they promise to make regular interest payments and to repay the principal amount of the borrowed funds. In the realm of international finance, international debt issuance comes with a bewildering choice of legal forms of debt – such as international bank loans, commercial paper, senior unsecured bonds and debentures, subordinated and unsecured notes and debentures and other types of debt instruments. In its very basic form, all of those debt instruments, from the most uncompli-cated bank loan to the most complex and esoteric international bond facility, are similar – they all reflect a basic agreement on behalf of the lender to advance the borrowed funds and a promise on behalf of the borrower to return the funds lent.

The additional variation in the terms and complexity of those instruments is derived from the responses given by the borrower and its advisors to a number of pertinent questions:

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 9

1. Should the borrower borrow short-term or long-term? If the company simply needs to finance a temporary increase in inventories ahead of the Christmas season, then it may make sense to take out a short-term bank loan. But suppose that the cash is needed to pay for expansion of an oil refinery. In that case, it would be more appropriate to issue a long-term 20-year bond in the international bond markets.

2. Should the debt be fixed or floating rate? 3. Should the company borrow domestic currency or an international currency?

Many companies often borrow in international currency. It makes sense to have debt in foreign currency if the borrower needs to spend foreign currency. For example, a Greek airline without US operations needs to borrow a certain amount of US dollars to finance the purchase of aircraft fuel, which is almost always bought and sold in US dollars.

4. What other legal promises should the borrower make to the lenders? Is the debt senior or junior (subordinated) to other debt? The junior (subordinated) debt holders are paid only after all senior creditors are satisfied.

These are some of the many issues that define the details of the specific debt instrument. The international loan and bond markets have developed very sophisticated ways to deal with each one of those issues.

Reading 1.2

Please study carefully Hal Scott’s 2000 paper, ‘Internationalization of primary public securities markets’, which is a good introduction to the various conflicting laws and regulations that impede international financial activities and the legal solutions that have been devised to address those risks.

Scott examines the trends leading to the internationalisation and globalisation of international securities markets and concludes that it would be desirable for borrowers in the form of debt or equity securities to be able to issue securities to investors worldwide and access global markets using one set of distribution procedures and disclosure documents, and one set of liability standards and enforcement remedies.

Make sure your notes cover the various reasons he advances as to why this state of affairs is currently not possible.

1.4 Legal Aspects of International Finance It should be appreciated that international financial transactions are not subject to some sort of ‘international financial law’. The United Nations does not legislate international financial law and the same is true for all other international organisations! In reality, international financial transactions are governed by a system of national law: a loan given by an English bank to a Japanese corporation will be governed by English law, Japanese law or some other system of law.

Scott (2000) ‘Internationalization of primary public securities markets’. Reproduced in the Module Reader from Law and Contemporary Problems.

Legal Aspects of International Finance

10 University of London

What, then, is the meaning of legal aspects of international finance? If every international financial contract is subject to a domestic system of law, what is the ‘international’ element of the legal aspects of international financial transactions?

In summary, it is the identification of legal risks pertaining to cross-border transnational contracts, the identification of which law applies and which court decides a dispute, issues relating to currencies and foreign exchange, international taxation and international regulatory standards applicable to international financial operations. Let us examine some examples.

A, a bank in England, agrees to provide a multi-currency term loan facility to B, a textile company in Japan, over a period of twenty years. Suppose there is a problem and one of the parties wishes to sue for breach of contract. Will English law or Japanese law apply? Will the case be heard in the courts of England or of Japan?

Normally, the parties may choose and therefore, when preparing the agree-ment, the lawyers advising the parties should ensure that these matters are decided and then specified in the contract. They should also be aware that the answers to the two questions are not necessarily the same: ‘choice of law’ simply refers to which country’s law will apply, while ‘jurisdiction’ tells us which country’s courts will decide the case. It is quite possible for a contract to provide that the governing law is that of England and Wales, but that the Japanese courts will have jurisdiction over any dispute.

Note that the term ‘jurisdiction’ is used in two distinct ways. Firstly, it means a territory with a given legal system. This will often be a country, but it may be a part of a country with a separate legal system: examples include the parts of the United Kingdom (England and Wales, Scotland, Northern Ireland), the states of the USA and the provinces of Canada or indeed territories with special status, such as Hong Kong. Secondly, however, the term is used to mean competence or power to judge a particular dispute, as with the ‘jurisdiction clause’ mentioned above. For example, ‘the courts of South Africa have jurisdiction’ means that the courts of South Africa are empowered to rule on the matter in question.

It is important to note that where a state is concerned which comprises a number of different legal jurisdictions, such as the United States, Canada or Switzerland, the choice of law and jurisdiction clauses will need to specify the precise territory, not just the country – such as the State of New York or the Canton of Zürich.

Although, in some cases, choice of law and jurisdiction can be agreed fairly easily, it is not always so. National pride or political issues may be at stake: a party in one jurisdiction may not see why the agreement should be gov-erned by the law of the other party rather than their own. This can be a particularly sensitive issue where one of the parties is based in a developing country while the other is in, for example, Western Europe or North Ameri-ca. The lawyers negotiating the contract may need to be as skilled in diplomacy as in any other area.

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 11

One solution to such a disagreement can be to choose the law of a ‘neutral’ third jurisdiction. There is no requirement for either the governing law or the court with jurisdiction to be that where one of the parties is located – in the example given above, it would be quite possible for the parties to choose that the governing law will be that of Switzerland while the courts of Singa-pore will have jurisdiction. As an alternative to the latter, the contract will often, while specifying the governing law, state that any dispute is to be resolved by arbitration. In place of the usual jurisdiction clause, an interna-tionally recognised arbitration centre will then be nominated, such as London or Paris.

The choice of law is not merely a matter of convenience and clarity: certain causes of action recognised in one legal system may simply not exist in another. For example, the ‘requirement of consideration’, an important principle of English contract law, does not exist in Scots law. Similarly, the purpose of the contract may be illegal in certain jurisdictions but not others: examples include gambling and the sale of alcohol. If the purpose of the contract is viewed by one jurisdiction’s law as illegal, that law is likely not to enforce any rights or obligations arising under it.

This whole area, termed ‘conflicts of laws’, is covered in detail in Unit 8. The following examples show further ways in which international complexities relating to finance need legal clarification.

Major loans for a large-scale corporate project may be too large for one financial institution on its own to provide. Examples are a major tunnel such as the Channel Tunnel linking the United Kingdom and France, the building of a new airport, possibly even the setting up of a new airline. Several financial institutions may therefore come together to provide between them the amount of funds required. In some cases, it may be possible for all the institutions to be found within one jurisdiction but, frequently, they will be drawn from a number of major financial centres, such as London, New York and Singapore. The law relating to such loans needs to be flexible in order to deal with this.

As you have seen, it is now common for shares of international companies to be traded on more than one exchange in more than one jurisdiction – for example, on both the London and the New York Stock Exchanges. In addi-tion, however, companies in smaller or developing commercial centres may wish their shares also to be listed on a more established market in order to access a wider range of investors: shares in the growing mainland Chinese corporate sector are increasingly listed not only in Shanghai or Shenzhen, but also on the Hong Kong Stock Exchange and, more recently, in London, with their different rules and legal systems. The same is also true of debt securities: these, too, may be traded internationally. A legal framework is required so that securities can easily be traded globally with a minimum of barriers from different legal systems.

What distinguishes international finance from domestic finance are primari-ly two key elements:

Legal Aspects of International Finance

12 University of London

• the jurisdictions in which the borrower and lender are located • the currency in which the credit is offered.

Domestic markets serve borrowers located in the same jurisdiction as the lender. The currency of the loan will typically be that of the jurisdiction in question, although in some cases an alternative currency may be agreed on as being more stable. International markets are precisely that – markets that offer credit both to borrowers located in the same jurisdiction as the lender and to those in other jurisdictions. They are generally found in the large financial centres, such as the United States, the UK, Germany, Hong Kong and Japan.

Offshore markets can be slightly different. A number of these offer credit and investment services to borrowers located in other jurisdictions, but only to these: they do not also offer these services to local borrowers. This is often because they are located in jurisdictions that are geographically small and therefore do not have a large, diverse economy from which such borrowers might emerge. Indeed, frequently, international finance is the main econom-ic sector of these jurisdictions. Examples include a number of the Caribbean island jurisdictions (eg the Cayman Islands or British Virgin Islands), and also small European jurisdictions such as Jersey, Monaco, Luxembourg or Gibraltar. This is a growing sector: a number of newer financial centres have developed offshore credit markets. Examples include Lebanon and some of the Gulf States.

Nonetheless, it is important to recognise that, although the term ’offshore financial centre’ is often used to refer to jurisdictions that offer services exclusively (or at least primarily) to foreign borrowers or investors, its actual meaning is simply a centre that offers financial services to non-residents – whether or not it also does so to local residents. New York and London are key offshore financial centres.

Reading 1.3 and 1.4

Please read carefully the article by Buchheit (2007), ‘Law, ethics and international finance’, for an excellent introduction into the distinguishing characteristics of the law governing international financial transactions, compared with the law governing purely domestic financial transactions.

Also, please read and study carefully Walter’s (1082) article, ‘Country risk and interna-tional bank lending’, for an excellent introduction into the concepts of country and political risk that are so particularly important in the legal framework governing interna-tional financial transactions.

Be sure to cover their main points in your notes.

1.5 Introduction to International Capital Markets International securities markets are all about raising money and the match-ing of those who want capital (borrowers) with those who have it (lenders).

Buchheit (2007) ‘Law, ethics and international finance’. Reproduced in the Module Reader from Law and Contemporary Problems.

Walter (1982) ‘Country risk and international bank lending’. Reproduced in the Module Reader from University of Illinois Law Review.

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 13

When the money is lent, it may simply be a deposit with the bank. Most of the time, however, the obligation to repay the debt will take the form of a document, issued by the borrower, who promises to repay the debt. We call the document containing the promise to repay the debt security.

1.5.1 Primary and secondary markets

When a security is issued for the first time, it is offered on what is known as the ‘primary market’. The primary market involves the sale of securities by an issuer to investors in order for the issuer to borrow (‘raise’) the money it requires. If the investor holds the security until the security matures and the debt is duly repaid by the issuer, the transaction is confined to the primary market. This is rare. Investors want the ability to re-sell a security before it matures, allowing them to recoup the capital value of the investment earlier than the maturity date.

The resale of already issued securities takes place in the ‘secondary capital market’, in which investors and traders can buy and sell securities already in issue. The most familiar types of secondary markets are organised stock exchanges, where capital changes hands daily in the form of marketable securities. For example, an investor wishing to save for retirement may purchase a 30-year government bond which pays annual interest of 4 per cent. After 10 years, the investor decides that this investment was not such a good idea and he would be better off placing the money in a bank savings account. What does he do? He simply sells the security in the secondary securities market.

The existence of secondary capital markets where securities are sold and bought is very important for the success of primary securities markets where securities are for the first time distributed from the borrower to the lender (original investor). Investors are more willing to purchase new securities from borrowers because they know that a secondary market exists where their securities could be resold in a very short period of time.

1.5.2 Domestic and international markets

A ‘domestic market’ is the capital market in a currency located in the coun-try of the currency. Borrowing US dollars in the United States, sterling in the United Kingdom and euros in France are all examples of using domestic capital markets. The largest domestic capital market is the United States for securities denominated in US dollars.

The subject matter of this module, however, is the examination of ‘interna-tional securities markets’. It should be noted from the outset that the term ‘Euromarkets’ does not imply any connection with the single European currency, or indeed with any European capital market, and is now broadly referred to as simply international capital markets. It is simply technical jargon used in international capital markets to refer to securities and curren-cies that are held and traded outside the country of the currency. Thus, Eurodollar deposits are deposits in US dollars held by banks outside the

Legal Aspects of International Finance

14 University of London

United States, while Euroyen deposits are deposits held in Japanese yen by banks outside Japan. These all essentially form the basis of international capital markets.

1.5.3 Debt and equity securities

There are two main types of securities traded in international capital mar-kets, debt and equity securities. The best-known securities are perhaps equity securities such as ordinary shares in listed companies, which are traded on the stock market. Investors in equity securities are not entitled to a fixed return on their investment. Unlike debt instruments such as bonds, equity investors have a right to receive dividends out of future profits of the company and significant voting rights as legal owners of the company. Equity investors rank behind all other creditors of the company, which means that in the event of insolvency they will not receive any funds before all other creditors are fully repaid. In practice, this means that they will not receive any funds at all: if the company were able to repay all its creditors in full, it would not be insolvent.

Reading 1.5 and 1.6

Please now study carefully the paper by James Woepking (1999), ‘International capital markets and their importance’, for a summary of the main characteristics and typologies of the international capital markets.

You should also read the seminal article by the President of Morgan Stanley, Richard Debs (1987), which is a brief review of the history of the globalisation of financial markets and the main drivers of such globalisation.

As usual, your notes on the readings should be useful for your revision of the unit, and enable you to answer the question:

Were Debs’ predictions right?

1.6 Dealing with Risk in International Finance Risk is the possibility that something unpleasant, undesirable or detrimental might happen and in finance, including international finance, it is normally accompanied by a specification of the source each time in question. Of course, the notion of risk is not peculiar to finance. It is effectively associated with the very essence of life and dominates in all entrepreneurial undertak-ings. Consequently, risk cannot be eliminated completely; it can only be managed and controlled. This process entails proper identification and monitoring as well as a prompt response to the key components of any type of risk – namely, the probability of occurrence and the associated derivative impact in such a case.

The most typical risk associated with international finance is credit risk, which can be defined as the possibility of the failure of the debtor to perform its contractual obligations in accordance with the relevant credit agreement. In addition, international lending operations can be subject to country,

Woepking (1999) ‘International capital markets and their importance’. Reproduced in the Module Reader from Transnational Law and Contemporary Problem.

Debs (1987) ‘Globalization of financial markets: What is happening and why’. Reproduced in the Module Reader from International Business Lawyer.

Unit 1 The Law of International Finance

Centre for Financial and Management Studies 15

political or sovereign risks, which refer to the possibility of the debtor’s default due to the social, economic and political environments of his home jurisdic-tion.

Furthermore, market risk is associated with the trading activities of investors in securities and other financial instruments and refers to the possibility of losses arising from adverse movements in market prices. One specific element of market risk is foreign exchange or currency risk, which refers to the possibilities of losses attributed to fluctuations and volatility of foreign exchange rates. Moreover, interest rate risks refer to the exposure of the institution’s financial condition to adverse movements in interest rates. Liquidity risk arises from the inability of a lender or borrower to accommo-date decreases in liabilities or to fund increases in assets. For financial institutions, the concept of operational risk refers to the risk of direct or indirect loss resulting from inadequate or failed internal processes, people and systems or from external events. Such failures can lead to financial distress through error, fraud, or failure to perform in a timely manner or cause the interests of the financial institution to be compromised in some other way – for example, by its dealers, lending officers or other staff ex-ceeding their authority or conducting business in an unethical or risky manner. This is termed personnel risk.

Other aspects of operational risk include major failure of information technology systems or events such as major fires or other disasters. Finally, lenders in international financial transactions are subject to various types of legal risk, including the possibility that assets will turn out to be worth less or liabilities will turn out to be greater than expected because of inadequate or incorrect legal advice or documentation.

It is fair to say that the legal documentation governing international finan-cial transactions – that is, the international lending agreement (for loans) or the international bond indenture (for the issuance and offering of bonds) has one primary objective: the management or elimination of legal, credit, currency, interest rate, market and political risk surrounding the decision of the lender to lend the funds to a borrower across borders.

Reading 1.7 and 1.8

Please first study the seminal article by Michael Gruson (1996), ‘Management of Legal Risks in International Agreements’, in which he discusses common legal devices used by drafters of international financing agreements to manage certain, but not all, legal risks.

Make sure your notes cover the major points.

Now study Hudson (2013)’s Chapter, 1 pp. 5–38. In this chapter, Hudson sets out the key principles of the law of finance and the law of international finance.

When you have finished reading, please answer the following questions.

Outline each of the seven categories of finance. What types of risk exist in finance?

Gruson (1996) ‘Management of Legal Risks in International Agreements’. Reproduced in the Module Reader from the Willamette Bulletin of International Law and Policy.

Hudson (2013) Chapter 1 ‘The components of the law of finance’ from The Law of Finance.

Legal Aspects of International Finance

16 University of London

1.7 Conclusion This unit has covered in brief several topics important in international finance, and it has served as an introduction to the rest of the module, which considers those topics in detail. You should now be able to complete the learning suggestions set out on the introductory page; if not, you should return to the relevant section and be sure you do understand the concepts before going on to study Unit 2.

Here are the questions implied in the unit’s learning outcomes:

• What are the various types of financial assets and cross-border financial flows?

• What are the main characteristics of international financial transactions compared with purely domestic transactions?

• What is the function of the choice of law and jurisdiction clauses in international financial agreements?

• What are the various categories of risk relating to international financial transactions?

References McKinsey Global Institute (2013) Financial Globalization: Retreat or Reset? Global Capital Markets 2013. Lund S, Daruvala T, Dobbs R, Härle P, Kwek J-H and Falcón R. (Eds.) Available from: https://www.mckinsey.com/featured-insights/employment-and-growth/financial-globalization [Accessed 22 November 2018]