Embed Size (px)

Citation preview

Legal and Financial FrameworkLegal and Financial Framework

FP6FP6 Miriam Driessen ReillyMiriam Driessen Reilly

Legal Unit, DG INFSOLegal Unit, DG INFSO

Open Day - BrusselsOpen Day - Brussels

2 June 20052 June 2005

2

Overview – Legal AspectsOverview – Legal Aspects

Legal framework and general principles

Contract structure

Conclusion of the contract

Evolution of the consortium

Controls and sanctions

Consortium agreement

Intellectual property rights

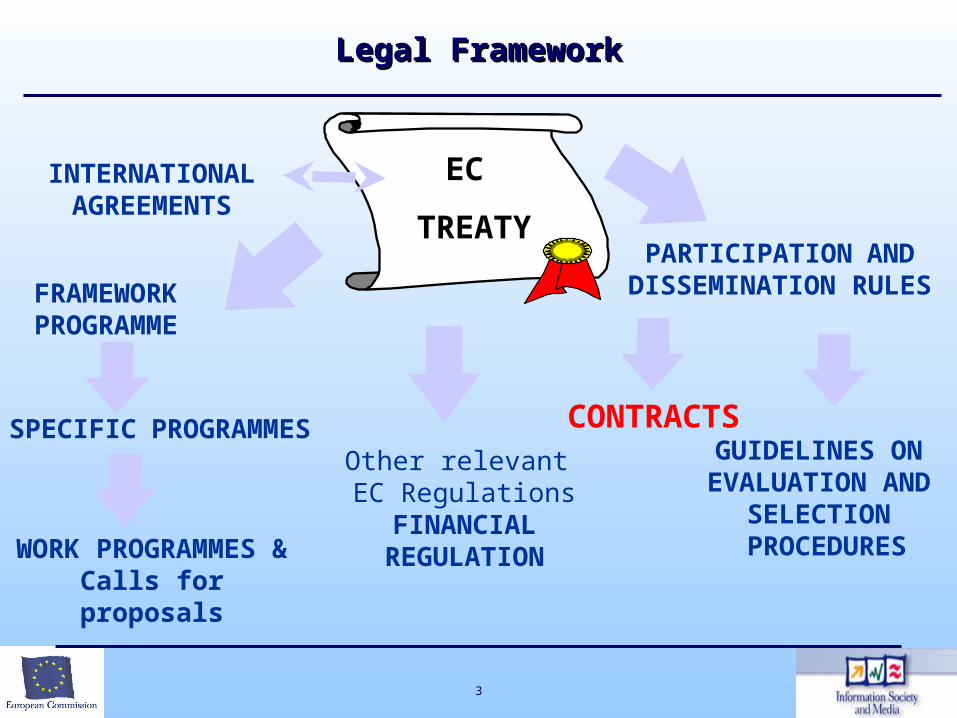

3

EC

TREATY

FRAMEWORK PROGRAMME

SPECIFIC PROGRAMMES

PARTICIPATION AND DISSEMINATION RULES

CONTRACTSOther relevant EC Regulations

FINANCIAL REGULATION

INTERNATIONAL AGREEMENTS

WORK PROGRAMMES &

Calls for proposals

GUIDELINES ON EVALUATION AND

SELECTION PROCEDURES

Legal FrameworkLegal Framework

4

Core contract (standard with specifics of project)(possibly including special clauses)

Annex I (technical tasks - the “project”)

Annex II General Conditions(applicable to every instrument)

Annex III Instrument specific provisions (specific to instrument)

Contract structureContract structure

5

Contract structureContract structure

Annex IV - Form A Consent of contractors identified in the core-contract

(article 1.2) to accede to the contract. To be signed by the contractor concerned and by the coordinator.

Annex V - Form B Accession of new legal entities to the contract. To be

signed by the new contractor concerned and by the co-ordinator

Annex VI - Form C Financial statement per activity. Specific to each

Instrument and/or type of action. To be filled periodically by each contractor

6

Annex II – General ConditionsAnnex II – General Conditions

Part A Implementation of the Project

Section 1 Implementation and deliverables

Section 2 Termination of the contract and responsibility

Part B Financial Provisions

Section 1 General financial provisions

Section 2 Controls, recoveries and sanctions

Part C Intellectual Property Rights

7

General Rule:

Participant = contractor

Every legal entity contributing to a project must have a

contractual link with the Community

Exceptional cases: subject to very restrictive rules

Third parties identified in Annex I

Subcontractors

ContractorsContractors

8

A contractor among other contractors

No additional rights

BUT

Additional obligations

Administrative tasks: single entry point for

communication, payments, reporting etc.

Co-ordinatorCo-ordinator

9

Conclusion of the contract Conclusion of the contract 1/21/2

The contract will be concluded between the Commission and all participants in an indirect action (the ‘Consortium’).

It will enter into force upon signature by the Commission and the contractor acting as ‘Co-ordinator’ of the project.

The other participants identified in the contract will accede to it in accordance with Article 2, assuming the rights and obligations of the contract with effect from the date on which it enters into force.

10

Evolution of the Consortium Evolution of the Consortium 1/31/3

The Consortium may be enlarged to include other legal entities, which shall accede to the contract by means of Accession Form B.

The Commission is deemed to have accepted this legal entity as a contractor to the Consortium if it does not object within six weeks of receipt of Form B (Tacit Approval).

Any acceding participant shall assume the rights and obligations of the contractors as established by the contract with effect from the date of its accession to the contract.

11

Evolution of the Consortium Evolution of the Consortium 2/32/3

Any contractor may request the termination of its participation in the contract.

The consortium may request the termination of any contractor.

Tacit approval of such termination after six weeks.

Contractors leaving the Consortium shall be bound by the provisions of the contract regarding the terms and conditions applicable to the termination of their participation.

12

Particular cases of NoE and IP Particular cases of NoE and IP 3/33/3

For some changes in the composition of the consortium, requirement of prior publication of a competitive call (see Annex III)

Specifications of the changes in the joint programme of activities for a NoE and in the implementation plan for IP

The competitive call shall be published by the consortium and advertised widely using specific information support (Internet sites of FP6, specialist press and brochures, national contact points)

Offers shall be evaluated by the consortium according to the evaluation and selection criteria of the indirect action (Article 10.4 and 10.5 of RFP), and with the assistance of independent experts appointed by the consortium

13

Controls and AuditsControls and Audits

Controls

Periodic activity reports (including plan for dissemination and use)

Periodic financial reports

Supplementary reports if foreseen (in Annex I or III)

Final reports covering the whole project duration

Audits

Scientific, technological and financial audits

Annual monitoring by Commission with external experts (particularly for IP and NoE)

Ethical or other reviews

Contractors right to refuse particular expert

14

SanctionsSanctions

Recovery of unjustified financial contribution

Liquidated damages for overstated expenditure

Administrative or financial sanctions foreseen in the Financial Regulation

False declarations

Exclusion from selection for 2-3 years, without prejudice to financial penalty of 2-10% of value of contract

Fraud, criminal activity, money laundering, bankruptcy, professional misconduct, tax offences, corruption

Exclusion from selection for 1-5 years

* Without prejudice to any civil remedies or criminal proceedings

15

Characteristics:

Private Contract between the contractors

Provides for internal operation and management of the consortium

Commission does not review it or approve it

However, provisions must not conflict with provisions of EC Contract

May be modified/amended after entry into force

Non-binding guidelines published by the Commission

The Consortium Agreement The Consortium Agreement 1/21/2

16

The Consortium Agreement The Consortium Agreement 2/22/2

Mandatory unless excluded by the call for proposals Internal Organisation

Designation of co-ordinator Management structure Technical implementation Organisation of work to be carried out (sub-projects) Allocation of funds paid to consortium Changes in consortium’s composition (modification)

Intellectual Property Rights ensure that agreements necessary for the implementation of the project have

been reached - Eg exclusion of background/sideground/Financial issues

initiate common strategy on dissemination/use/ protection + search for industrial partners

*See Suggested Consortium Agreement Checklist

http://europa.eu.int/comm/research/fp6/working-groups/model-contract/index-en.html

Settlement of Internal Disputes Applicable law Arbitration procedure Penalties

17

Intellectual Property Rights (IPR) Intellectual Property Rights (IPR) 1/21/2

General concepts:

Ownership

Grants - contractor carrying out work owns the results

Joint work between contractors – joint ownership

Agreement re allocation & terms of exercising it

public procurement - Commission owns results

transfer of ownership

prior notice to other participants + Commission (possible objection within 30 days)

Obligation to pass on obligations AR/dis/use to assignee

Personnel Agreements

Protection

where there is commercial application and subject to legitimate interests, it is a requirement to protect (include in PUDK)

where there is no protection, Commission may protect

18

Intellectual Property Rights (IPR) Intellectual Property Rights (IPR) 2/22/2

General concepts:

Publication allowed if not detrimental to protection

prior notice to Commission + other contractors (possible objection within 30 days)

Use/dissemination obligation to use and disseminate knowledge

St protection/use w/in 2 yrs of end of project

Commission may disseminate itself if needed

Access Rights – PEKH & Knowledge Granted to other contractors upon written request

On a need to use basis

May exclude specific PEKH by written agreement prior to EC contract signature

No automatic entitlement to grant sublicences

19

FP6 System of Access RightsFP6 System of Access Rights

Access rights topre-existing know-how

Access rights toknowledge

If a contractor needs them for carrying out its own work under the project

For carrying out the project

Royalty-free unless otherwise agreed

before signing the contract

Royalty-free

If a contractor needs them for using its own knowledgeFor use

(exploitation + further research)

Non-discriminatory conditions to be agreed

Royalty-free unless otherwise agreed

before signing the contract

Possibility for participants to agree on exclusion of specific pre-existing know-how before signature of the contract (or

before entry of a new participant)

20

Overview – Financial AspectsOverview – Financial Aspects

Introduction to financial modalities

New concepts introduced in FP6

21

IntroductionIntroduction

Grant to budget and grant for integration

Eligibility of costs /ineligibility of costs

Principle of cost reimbursement

Cost reporting models

Maximum reimbursement per Activity

22

IntroductionIntroductionGrant to budget – grant for integrationGrant to budget – grant for integration

Grant to budget – IP and other instruments calculated as a percentage of the budget established by

the participants to carry out the work the expense needed to implement the work shall be

certified by an external auditor or, in the case of public bodies or competent public officer

Grant for integration – NoE calculated taking into account the degree of integration,

the number of researchers that all participants intend to integrate, the characteristics of the field of research concerned and the joint programme activities

paid on the basis of results, … and on condition its expenses, which are to be certified….. are greater then the grant itself.

23

IntroductionIntroductionPrinciples of cost reimbursementPrinciples of cost reimbursement

CONCEPT OF ELIGIBLE COSTS

Actual, economic and necessary

Subject to the usual accounting principles of the contractor

Incurred during the project … except … drawing up the final reports … which may be incurred during the period of up to 45 days after the end of the project

Recorded in the accounts …

In case of contributions made by third parties … be recorded in the accounts of the third party

24

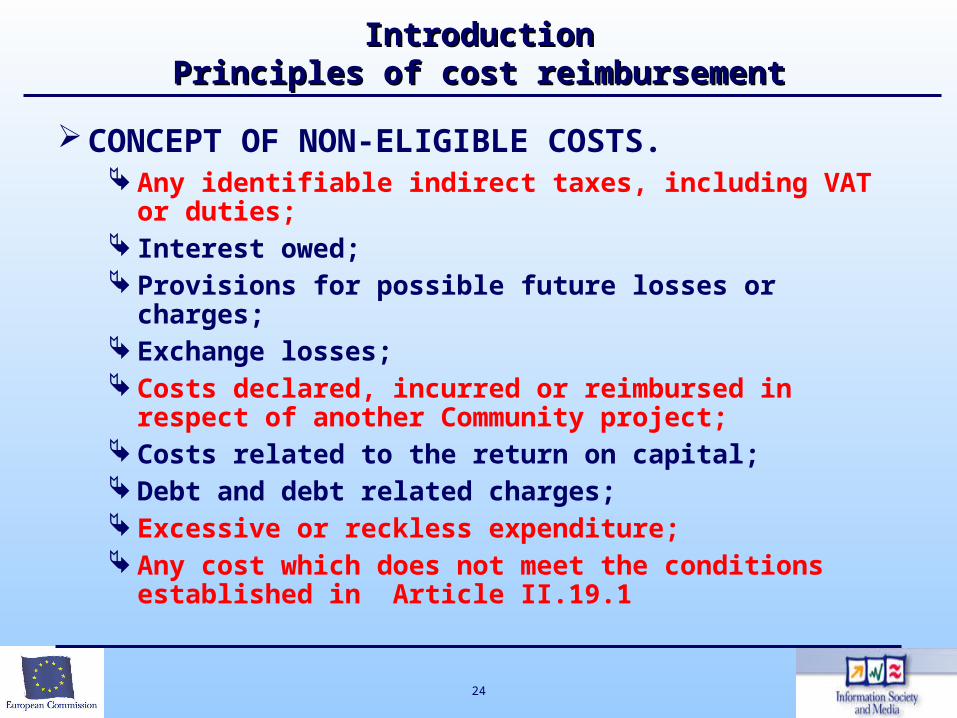

IntroductionIntroductionPrinciples of cost reimbursementPrinciples of cost reimbursement

CONCEPT OF NON-ELIGIBLE COSTS. Any identifiable indirect taxes, including VAT or

duties; Interest owed; Provisions for possible future losses or charges; Exchange losses; Costs declared, incurred or reimbursed in respect

of another Community project; Costs related to the return on capital; Debt and debt related charges; Excessive or reckless expenditure; Any cost which does not meet the conditions

established in Article II.19.1

25

IntroductionIntroductionPrinciples of costs reimbursementPrinciples of costs reimbursement

Reimbursement of eligible costs claimed by contractors

In accordance with the cost reporting models used by each contractor

Maximum reimbursement rates of eligible costs per type of activity

Approval of requested periodic reports

Subject – if required in the contract - to the submission of an audit certificate

Taking into account the receipts of the project

Limits of public funding established by international regulations and in particular by the Community framework for State aid for research and development for certain activities

26

IntroductionIntroductionCost reporting modelsCost reporting models

FC: actual direct and indirect costs all instruments, however in case of Co-ordination

Actions and Specific Support Actions flat rate for indirect costs (20% of direct costs minus subcontracting) reimbursed

FCF (variant of FC): actual direct costs + flat rate for indirect costs (20% of direct costs minus subcontracting)

all instruments

AC: actual additional non-recurring direct costs + flat rate for indirect costs (20% of direct costs minus subcontracting)

all instruments

27

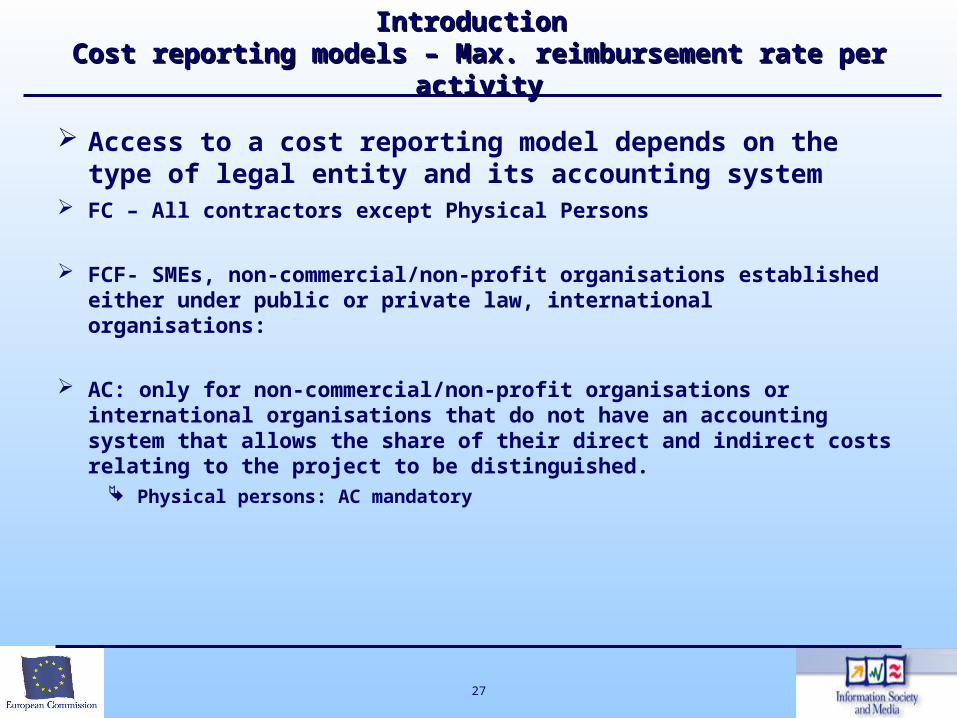

Introduction Introduction Cost reporting models – Max. reimbursement rate per activityCost reporting models – Max. reimbursement rate per activity

Access to a cost reporting model depends on the type of legal entity and its accounting system

FC – All contractors except Physical Persons

FCF- SMEs, non-commercial/non-profit organisations established either under public or private law, international organisations:

AC: only for non-commercial/non-profit organisations or international organisations that do not have an accounting system that allows the share of their direct and indirect costs relating to the project to be distinguished.

Physical persons: AC mandatory

28

IntroductionIntroductionCost reporting models- Max. reimbursement rate per activityCost reporting models- Max. reimbursement rate per activity

General rule: a legal entity applies the same cost reporting model in ALL contracts established under FP6 except may move from AC to FCF/FC or from FCF to FC (“one way ticket”) – a contractor however cannot change midway in a project

Note: special clause 22 “Different cost reporting models within the same legal entity” – in case legal entity uses AC and one of its departments uses FC

29

IntroductionIntroductionCost reporting models - reminderCost reporting models - reminder

Direct costs for contractors using the Additional Cost model

direct costs of personnel shall be limited to the actual costs of the personnel assigned to the project where the contractor has concluded with the personnel

a temporary contract for working on Community RTD projects

a temporary contract for completing a doctorate

a contract which depends, in full or in part, upon external funding additional to the normal recurring funding of the contractor. In that case, the costs charged to this contract must exclude any costs borne by the normal recurring funding

30

IntroductionIntroductionMaximum reimbursement rates of eligible costs Maximum reimbursement rates of eligible costs

per instrument, activity and cost modelper instrument, activity and cost modelMaximum

reimbursement rates of eligible costs

Research and technological

development or innovation activities

Demonstration activities Training activitiesManagement of the

consortium activitiesOther specific activities

(*)

Network of excellence100%

(up to 7% of the contribution)(AC : eligible direct costs)

100%

Integrated projectFC/FCF : 50%

AC : 100%FC/FCF : 35%

AC : 100%100%

100%(up to 7% of the contribution)

(AC : eligible direct costs)

Specific targeted research or innovation project

FC/FCF : 50%AC : 100%

FC/FCF : 35%AC : 100%

100%(up to 7% of the contribution)

(AC : eligible direct costs)

Specific research project for SMEs

FC/FCF : 50%AC : 100%

100%(for collective research only)

100%(up to 7% of the contribution)

(AC : eligible direct costs)

Integrated infrastructures initiative

FC/FCF : 50%AC : 100%

FC/FCF : 35%AC : 100%

100%(up to 7% of the contribution)

(AC : eligible direct costs)100%

Coordination action 100%(FC indirect costs : f lat rate(**))

100%(up to 7% of the contribution)

(AC : eligible direct costs)(FC indirect costs : f lat rate(**))

100%(FC indirect costs : f lat rate(**))

Specific support action

100%(up to 7% of the contribution)

(AC : eligible direct costs)(FC indirect costs : f lat rate(**))

100%(FC indirect costs : f lat rate(**))

(*): Other specif ic activities means: - for Netw ork of Excellence : Joint Programme of Activities, except management of the consortium activities.- for Integrated infrastructures initiative: any "specif ic activity" covered by Annex I, including transnational access to infrastructures- for Coordination Action: Coordination activities, except management of the consortium activities- for Specif ic support action: any "specif ic activity" covered by Annex I, including transnational access to infrastructures

(**): Flat rate for FC indirect costs : 20% of all their eligible direct costs minus the eligible direct costs of sub-contracts.

31

New concepts introduced in FP6New concepts introduced in FP6

Collective Financial Responsibility

Third party costs

Receipts

Subcontracting

32

New ConceptsNew ConceptsCollective Financial Responsibility Collective Financial Responsibility

Definition Art. II.18.1/2 – Termination of one contractor = rest

of consortium responsible for reimbursement on pro-rata basis.

“Should the contract be terminated or the participation of a contractor be terminated in accordance with Art. II.16, and any contractor does not honour the reimbursement of the amount due by that contractor, the consortium will reimburse the amount due to the Commission.The amount due to the Commission may not exceed the value of the contribution due to the consortium in accordance with Art. 5.”

Allocated pro-rata in relation to share of finance

Max reimbursement may not exceed amount entitled to

33

In some cases the rule of financial collective responsibility is not applicable – see Art. II.18.3 & 4:

a) The contractor is: a public body an international organisation a contractor whose participation is guaranteed by a Member or

Associated State

These type of contractors shall be solely responsible for their budget.

Other contractors are not responsible for these contractors.

b) The consortium is not responsible for: any amount owed by a defaulting contractor for any contractual

breach discovered after the end of the contract liquidated damages due by a defaulting contractor other financial penalties and other sanctions imposed on a

defaulting contractor

ExceptionsExceptionsCollective Financial ResponsibilityCollective Financial Responsibility

34

New conceptsNew conceptsThird party costsThird party costs

Resources made available by third parties on the basis of prior agreement are eligible as costs for the project

The tasks and their execution by such third parties are clearly identified in the Annex I

Costs will have to be recorded in the accounts of this third party - to be covered by audit certificates

Contractors shall ensure that third parties whose resources are made available to the project are informed on the use of their resources

35

New conceptsNew conceptsReceipts Receipts

Three kinds of receipts financial transfers or their equivalent to the contractor from

third parties, contributions in kind from third parties, income generated by the project

Financial transfers or contributions in kind considered as receipts of the project if the third party has

provided them specifically to be used in the project

If at the discretion of the contractor they are not to be considered as receipts.

Income generated by the project General rule: any income generated by the project itself,

including the sale of assets bought for the project, are considered as income to the project

Derogation: income generated by the use of the knowledge resulting from the project is not considered as a receipt

36

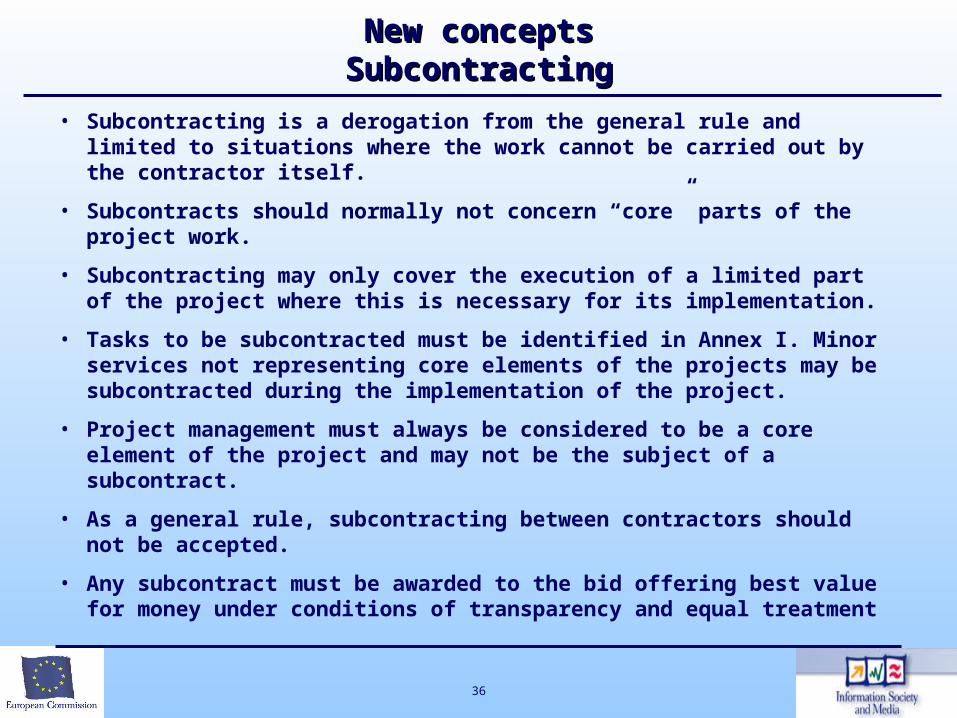

• Subcontracting is a derogation from the general rule and limited to situations where the work cannot be carried out by the contractor itself.

• Subcontracts should normally not concern “core” parts of the project work.

• Subcontracting may only cover the execution of a limited part of the project where this is necessary for its implementation.

• Tasks to be subcontracted must be identified in Annex I. Minor services not representing core elements of the projects may be subcontracted during the implementation of the project.

• Project management must always be considered to be a core element of the project and may not be the subject of a subcontract.

• As a general rule, subcontracting between contractors should not be accepted.

• Any subcontract must be awarded to the bid offering best value for money under conditions of transparency and equal treatment

New conceptsNew conceptsSubcontractingSubcontracting

37

End of PresentationEnd of Presentation

Thank you for your attention

The previous slides constitute an overview of the legal and financial provisions of the FP6 EC contracts. However, this should not be taken to constitute legal advice.