Embed Size (px)

Citation preview

Lecture Lecture 99

Impacts of financial Impacts of financial reporting decisions on reporting decisions on

individual financial individual financial statement users (module statement users (module

7)7)&&

Asset measurement Asset measurement (module 8)(module 8)

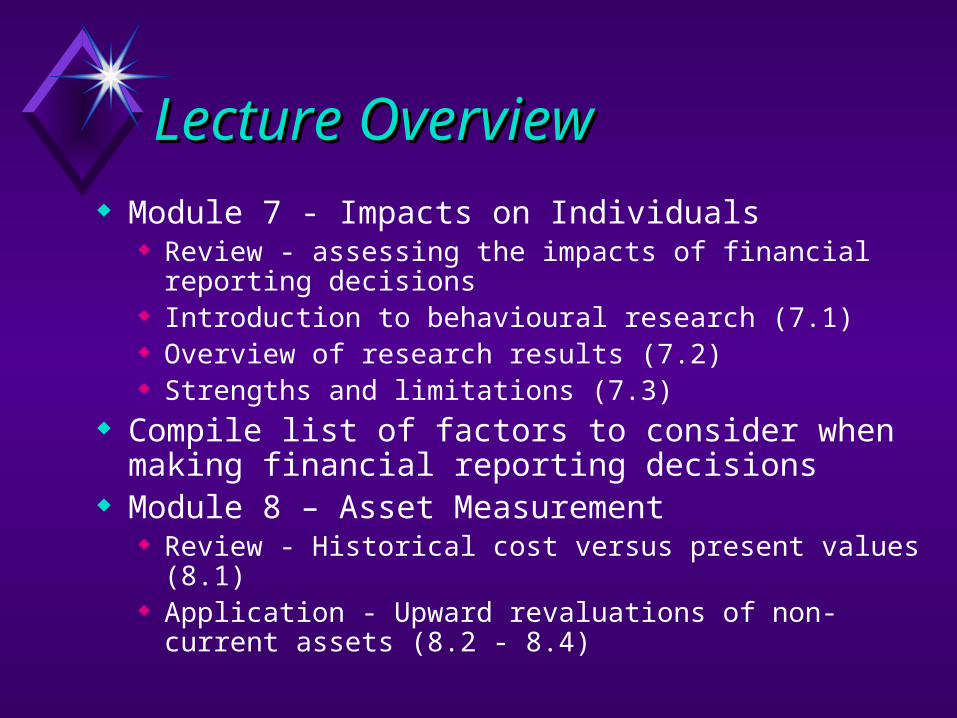

Lecture OverviewLecture Overview Module 7 - Impacts on Individuals

Review - assessing the impacts of financial reporting decisions

Introduction to behavioural research (7.1) Overview of research results (7.2) Strengths and limitations (7.3)

Compile list of factors to consider when making financial reporting decisions

Module 8 – Asset Measurement Review - Historical cost versus present values (8.1) Application - Upward revaluations of non-current

assets (8.2 - 8.4)

Module 7Module 7Impacts (of Impacts (of

financial reporting financial reporting decisions) on decisions) on

individual individual financial financial

statement usersstatement users

Impacts of Financial Impacts of Financial Reporting DecisionsReporting Decisions

You - Preparing Financial Statements & Making Financial ReportingDecisions

End user – MakingDecisions on the BasisOf Financial StatementInformation

Review - Assessing the Review - Assessing the Impacts of Financial Impacts of Financial Reporting DecisionsReporting Decisions

There are two ways to assess the impacts of financial reporting decisions: Determine what impact the release of

information had on share price? (capital markets research)

Determine the impact of the information on the decisions of individual information users (behavioural research)

Introduction to Introduction to Behavioural ResearchBehavioural Research

Examines the impact of accounting information on individuals

Decision making at the individual rather than the aggregate (share price) level

Focus of Focus of behavioural behavioural researchresearch

Investigates of the impact of alternative accounting and disclosure methods on decision making by INDIVIDUALS

For example, what is the impact of disclosure versus recognition alternative inventory valuation

methods capitalisation versus expense

Behavioural Research - Behavioural Research - Method is ExperimentalMethod is Experimental

Subjects (financial statement users) are divided into two or more groups

Individuals in each group are given financial statements prepared using different accounting/disclosure methods

Subjects are asked to make decisions based upon the information which they have been given

Comparison of Behavioural Comparison of Behavioural and Capital Markets and Capital Markets ResearchResearch Both examine the impact of financial reporting

decision on users of the info. Capital markets research assesses the aggregate

effect, while behavioural research assesses the effect on individuals

Capital markets research includes only investors, while behavioural research examines other types of financial statement users

Capital markets research assesses WHETHER the information is used, while behavioural research can asses HOW the information is used

Research ResultsResearch Results

Our focus is on the impact of our financial reporting decisions on the users of annual reports

Only a small amount of this type of research

Research results relate to: use of particular items of information the form of information disclosure

(presentation)

Research evidence - the Research evidence - the

use of information items use of information items In making predictions of financial returns,

analysts found to acquire EARNINGS and SALES information more often than other types (Pankoff and Virgil 1970; Mear and Firth 1987)

Some studies questioned the provision of current cost information, subjects relied more on historical cost information (Heintz 1973; McIntyre 1973)

Research evidence - the Research evidence - the presentation of presentation of informationinformation

Different PRESENTATION FORMATS found to influence users’ decisions including bar charts, line graphs, pie charts

and tables Studies examining decision making by

loan officers based on whether information is incorporated within the financial statements or included as footnotes FOUND PRESENTATION MADE NO DIFFERENCE (Wilkins and Zimmer 1983)

Limitations of Limitations of behavioural behavioural researchresearch

Research examining similar issues have generated conflicting results difficult to determine causes of

inconsistencies Settings of studies often different to

real-world settings implications for generalisability

Very difficult to replicate information available in the workplace

Students often used as surrogates Small number of subjects often used

Why is behavioural Why is behavioural research useful?research useful?

Gives us an idea what impact our financial reporting decisions will have on the users of our information

Useful for regulators to know about these results when deciding on new or changed accounting standards

Can be undertaken by researchers prior to new regulations being developed

Factors to consider when making financial reporting

decisions

Complete the attached handout to make a list of factors to consider when

making unregulated financial reporting decisions

Module 8Module 8Asset MeasurementAsset Measurement

Review - The Fundamental Review - The Fundamental Problem of Financial Problem of Financial Accounting TheoryAccounting Theory

Provision of relevantProvision of relevantinfo. to aid investorinfo. to aid investorDecision makingDecision making

Provision of reliableProvision of reliableinfo. to controlinfo. to controlmanagement behaviourmanagement behaviour

Review - Historical Cost Review - Historical Cost versus Present Valueversus Present Value

Relevance vs reliability - impossible to achieve both simultaneously

To use a present value model you need to know: future cash flows (probability of occurrence) discount rate

PV model involves estimation and compromise these estimates make the information subject

to error and therefore (unacceptably?) unreliable

Issue - Upward Issue - Upward revaluation of non-revaluation of non-current assetscurrent assets

Application of concepts covered in prior modules Information asymmetry - managers have

more information about the current value of some assets than outsiders

Regulation - what aspects of revaluation decisions are regulated and unregulated?

Determinants of revaluation decision Impacts on financial statement users

Regulations Regulations (AASB 1010 & AASB (AASB 1010 & AASB 1041)1041)

AASB 1010 deals with downward revaluations while AASB 1041 deals with upward revaluations

The decision to recognise an upward revaluation is VOLUNTARY

DISCLOSURES of current valuations of land and buildings required every 3 years

AASB 1041 specifies the accounting treatments to be followed, and disclosures to be made, in relation to recognised revaluations

Latest changes to Latest changes to revaluation standardsrevaluation standards

AASB 1041 revisions apply to reporting periods ending on or after 30/9/01

allows choice of either cost or fair value basis of measurement for each class of non-current assets

if fair value is chosen, revaluations must be kept up to date

frequency of revaluations depends on materiality of value changes

Discretion remaining - Discretion remaining - Unregulated financial Unregulated financial reporting decisionsreporting decisions

Whether to recognise a revaluation for each asset class (becomes choice between cost and fair value basis under new rules)

Amount of revaluation increment (discretion relating to estimation)

Frequency of revaluation (less discretion under new rules)

Type of valuer (independent or directors)

Financial statement Financial statement impacts of recognising a impacts of recognising a revaluationrevaluation increased assets increased equity decreased future profits if

assets are depreciable

Predictions and Research Predictions and Research Evidence about Asset Evidence about Asset RevaluationsRevaluations

Complete the attached handouts to make lists of :- economic determinants of the revaluation decision- impacts of recognising a revaluation

For TutorialsFor Tutorials Required reading

module 7 Text chapter 11, just sections identified

in study book module 8

Selected Reading 8.1 plus study book

Self assessment questions Questions 1 - 6 from module 7 Questions 1 - 6 from module 8