Embed Size (px)

DESCRIPTION

corp finance

Citation preview

Dr. Thomai Filippeli

Lecture 4

NPV and Stand-Alone Projects

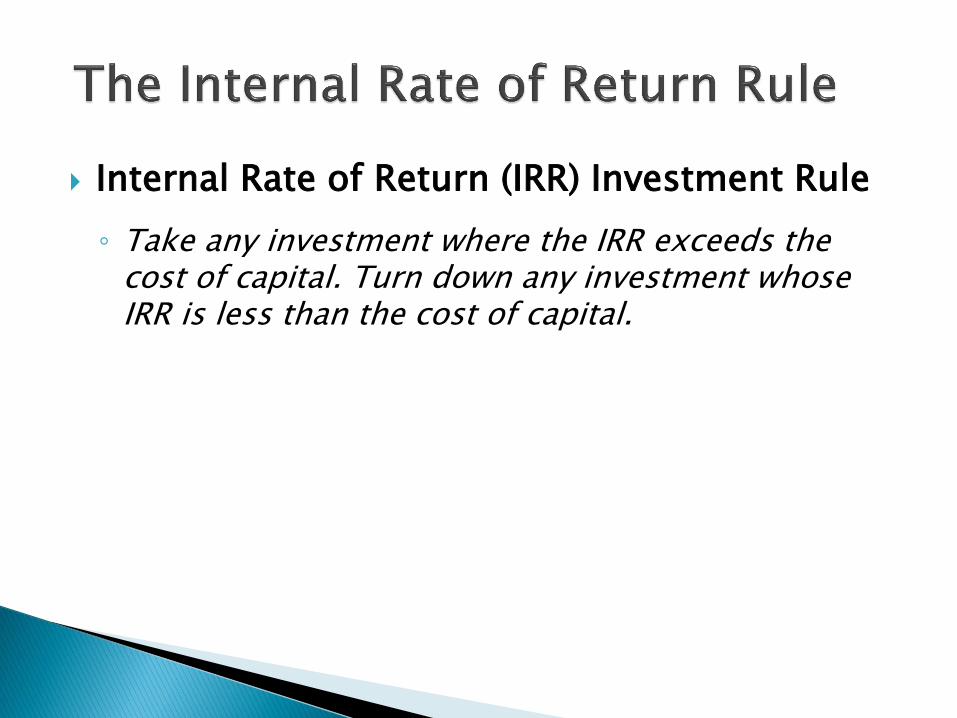

The Internal Rate of Return Rule

The Payback Rule

Choosing Between Projects

Project Selection with Resource Constraints

1. Define several commonly used techniques

Net Present Value (NPV)

Internal Rate of Return (IRR)

Payback Rule

Profitability Index

Incremental IRR

2. Describe decision rules for each technique

stand-alone projects

mutually exclusive projects.

3. Compare each technique and tell why NPV always gives the correct decision.

4. Discuss the reasons IRR can give a flawed decision.

5. Describe situations in which profitability index cannot be used to make a decision.

NPV of a project or investment:

NPV = PV (Benefits) – PV (Costs)

Or

NPV = PV (All project Cash flows)

Your computer manufacturing firm must purchase 10,000 keyboards from a supplier. One supplier demands a payment of $100,000 today plus $10 per keyboard, payable in one year. Another supplier will charge $21 per keyboard also payable in one year. The risk – free interest rate is 6%.

a) What is the difference in their offers in terms of dollars today? Which offer should your firm take?

b) Suppose your firm does not want to spend cash today. How can it take the first offer and not spend $100,000 of its own cash today?

You have been offered a unique investment opportunity. If you invest $10,000 today, you will receive $500 one year from now, $1,500 two years from now and $10,000 ten years from now.

a) What is the NPV of the opportunity if the interest rate is 6%? Should you take the opportunity?

b) What is the NPV of the opportunity if the interest rate is 2% per year? Should you take it now?

A perpetuity is a stream of equal cash flows that occur at regular intervals and last forever.

Present Value of Perpetuity

PV (C in perpetuity) = C/r

An annuity is a stream of N equal cash flows paid at regular intervals (annuity ends after a some fixed number of payments)

Present Value of an Annuity

PV = C*(1/r) *(1 – 1/(1+r)

Perpetuities

◦ When a constant cash flow will occur at regular intervals forever it is called a perpetuity.

The value of a perpetuity is simply the cash flow divided by the interest rate.

Present Value of a Perpetuity

( in perpetuity) C

PV Cr

Annuities ◦ When a constant cash flow will occur at regular

intervals for a finite number of N periods, it is called an annuity.

Present Value of an Annuity

N

1nnN32 )r1(

C

)r1(

C...

)r1(

C

)r1(

C

)r1(

CPV

N N

PV(annuityof Cfor N periods)

P PV(Pin period N)

P 1P P 1

(1 r) (1 r)

What is the present value of $1000 paid at the end of each of the next 100 years if the interest rate is 7% per year?

You want to endow an annual MBA graduation party at the university you graduated. You want to be a memorable one so you budget $30,000 per year forever for the party. If the university earns 8% per year on its investments and if the first party is in one year’s time how much will you need to donate to endow the party?

In some situations you know the PV and the Cash Flows of an investment opportunity but you don’t know the interest rate that equates them.

Internal Rate of Return: Interest Rate that sets the net present value of cash flows equal to zero.

Example 5

Jessica has just graduated with her MBA. Rather than take the job she was offered at a prestigious investment bank she has decided to into business for herself. She believes that her business will require an initial investment of $1 million. After that it will generate a cash flow of $100,000 at the end of one year and this amount

Example 6

The firm that offered Jessica a job was so impressed with Jessica that it has decided to fund her business. In return for providing the initial capital of $1 million, Jessica has agreed to pay them $125,000 at the end of each year for the next 30 years. What is the internal rate of return on firm’s investment in Jessica’s company assuming she fulfils her commitment?

NPV and stand – alone Projects

Consider a take-it-or-leave-it investment decision involving a single, stand-alone project for Fredrick’s Feed and Farm (FFF).

◦ The project costs $250 million and is expected to generate cash flows of $35 million per year, starting at the end of the first year and lasting forever.

When making an investment decision take the alternative with the highest NPV. Choosing this alternative is equivalent to receiving its NPV in cash today.

The NPV of the project is calculated as (perpetual cash flow stream):

The NPV is dependent on the discount rate

For risk – free investment the cost of capital will be equal to the risk – free interest rate r.

35NPV 250

r

If FFF’s cost of capital is 10%, the NPV is $100 million and they should undertake the investment.

NPV is positive only for discount rates less than 14%

When r = 14%, NPV = 0

IRR: The discount rate that sets the NPV of the project’s cash flows equal to zero

IRR provides useful information regarding the sensitivity of project’s NPV to errors in estimate the cost of capital. The difference between the cost of capital and the IRR is the maximum estimation error in the cost of capital that can exist without the original decision.

Sometimes alternative investment rules may give the same answer as the NPV rule, but at other times they may disagree.

◦ When the rules conflict, the NPV decision rule should be followed.

Internal Rate of Return (IRR) Investment Rule

◦ Take any investment where the IRR exceeds the cost of capital. Turn down any investment whose IRR is less than the cost of capital.

The IRR Investment Rule will give the same answer as the NPV rule in many, but not all, situations.

In general, the IRR rule works for a stand-alone project if all of the project’s negative cash flows precede its positive cash flows.

◦ In Figure 1, whenever the cost of capital is below the IRR of 14%, the project has a positive NPV and you should undertake the investment.

In other cases, the IRR rule may disagree with the NPV rule and thus be incorrect.

◦ Situations where the IRR rule and NPV rule may be in conflict:

Delayed Investments

Nonexistent IRR

Multiple IRRs

Delayed Investments

◦ Assume you have just retired as the CEO of a successful company. A major publisher has offered you a book deal. The publisher will pay you $1 million upfront if you agree to write a book about your experiences. You estimate that it will take three years to write the book. The time you spend writing will cause you to give up speaking engagements amounting to $500,000 per year. You estimate your opportunity cost to be 10%.

Delayed Investments ◦ Should you accept the deal?

Calculate the IRR.

◦ The IRR is greater than the cost of capital. Thus, the IRR rule indicates you should accept the deal.

When the benefits of an investment occur before the costs, the NPV is an increasing function of the discount rate.

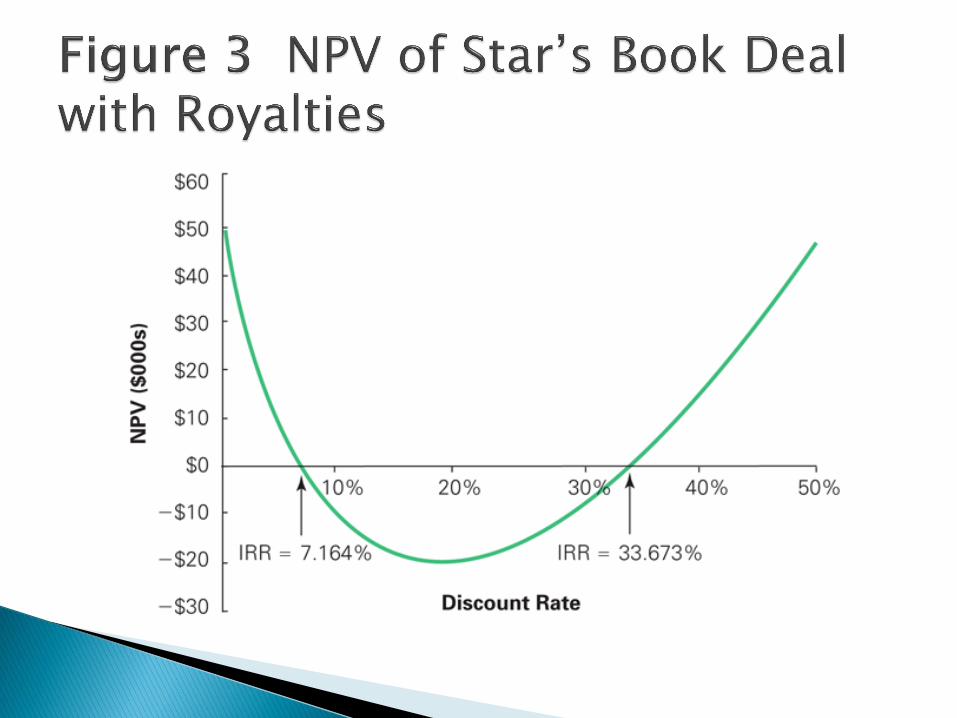

Multiple IRRs

◦ Suppose Star informs the publisher that it needs to sweeten the deal before he will accept it. The publisher offers $550,000 advance and $1,000,000 in four years when the book is published.

◦ Should he accept or reject the new offer?

Multiple IRRs ◦ The cash flows would now look like:

◦ The NPV is calculated as:

2 3 4

500,000 500,000 500,000 1,000,000 550,000 - - -

1 (1 ) (1 ) (1 )NPV

r r r r

Multiple IRRs

◦ By setting the NPV equal to zero and solving for r, we find the IRR. In this case, there are two IRRs: 7.164% and 33.673%. Because there is more than one IRR, the IRR rule cannot be applied.

Multiple IRRs

◦ Between 7.164% and 33.673%, the book deal has a negative NPV. Since your opportunity cost of capital is 10%, you should reject the deal.

Nonexistent IRR

◦ Finally, Star is able to get the publisher to increase his advance to $750,000, in addition to the $1 million when the book is published in four years. With these cash flows, no IRR exists; there is no discount rate that makes NPV equal to zero.

No IRR exists because the NPV is positive for all values of the discount rate. Thus the IRR rule cannot be used.

IRR Versus the IRR Rule

◦ While the IRR rule has shortcomings for making investment decisions, the IRR itself remains useful. IRR measures the average return of the investment and the sensitivity of the NPV to any estimation error in the cost of capital.

The payback period is amount of time it takes to recover or pay back the initial investment. If the payback period is less than a pre-specified length of time, you accept the project. Otherwise, you reject the project.

◦ The payback rule is used by many companies because of its simplicity.

Assume Fredrick’s requires all projects to have a payback period of five years or less. Would the firm undertake the fertilizer project under this rule?

Problem

◦ Projects A, B, and C each have an expected life of 5 years.

◦ Given the initial cost and annual cash flow information below, what is the payback period for each project?

A B C

Cost $80 $120 $150

Cash Flow $25 $30 $35

Solution

◦ Project A

$80 ÷ $25 = 3.2 years

◦ Project B

$120 ÷ $30 = 4.0 years

◦ Project C

$150 ÷ $35 = 4.29 years

Pitfalls:

◦ Ignores the project’s cost of capital and time value of money.

◦ Ignores cash flows after the payback period.

◦ Relies on an ad hoc decision criterion.

Mutually Exclusive Projects

◦ When you must choose only one project among several possible projects, the choice is mutually exclusive.

◦ NPV Rule

Select the project with the highest NPV.

◦ IRR Rule

Selecting the project with the highest IRR may lead to mistakes.

If a project’s size is doubled, its NPV will double. This is not the case with IRR. Thus, the IRR rule cannot be used to compare projects of different scales.

When projects differ in their scale of investment, the timing of their cash flows or their riskiness, then their IRRs can’t be meaningful compared.

Bookstore Coffee Shop

Initial Investment $300,000 $400,000

Cash FlowYear 1 $63,000 $80,000

Annual Growth Rate 3% 3%

Cost of Capital 8% 8%

IRR 24% 23%

NPV $960,000 $1,200,000

◦ Consider two of the projects from Example 7.3

Another problem with the IRR is that it can be affected by changing the timing of the cash flows, even when the scale is the same.

◦ IRR is a return, but the dollar value of earning a given return depends on how long the return is earned.

Consider again the coffee shop and the music store investment in Example 7.3. Both have the same initial scale and the same horizon. The coffee shop has a lower IRR, but a higher NPV because of its higher growth rate.

An IRR that is attractive for a safe project need not be attractive for a riskier project.

Consider the investment in the electronics store from Example 7.3. The IRR is higher than those of the other investment opportunities, yet the NPV is the lowest.

The higher cost of capital means a higher IRR is necessary to make the project attractive.

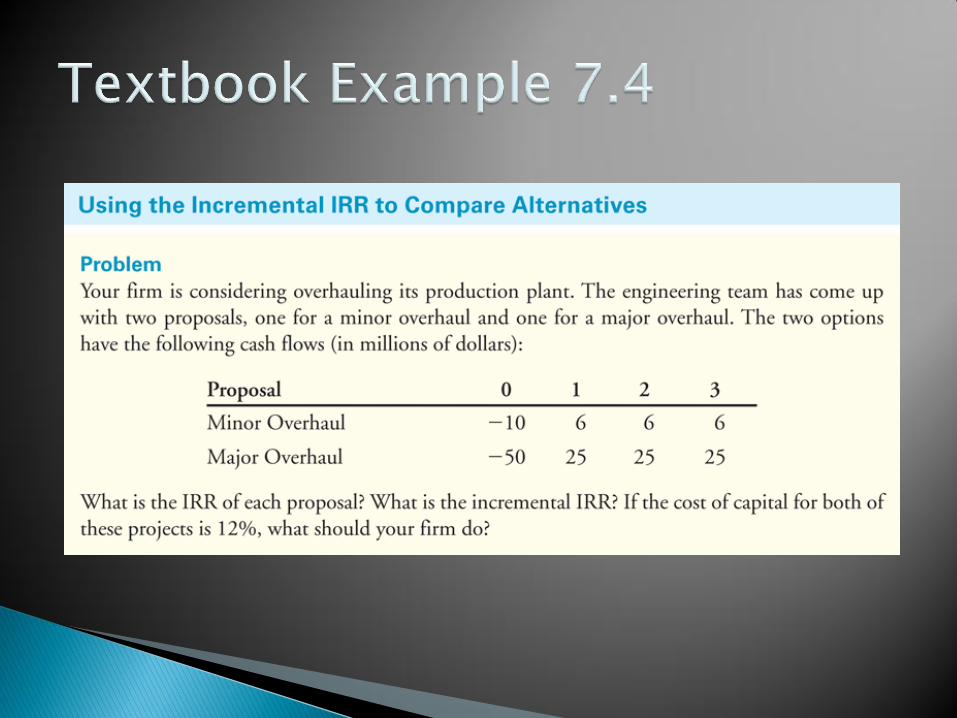

Incremental IRR Investment Rule ◦ Apply the IRR rule to the difference between the

cash flows of the two mutually exclusive alternatives (the increment to the cash flows of one investment over the other).

◦ Generally, if the incremental internal rate of return is higher than the minimum acceptable rate of return (cost of capital), the more expensive investment is considered the better one.

Shortcomings of the Incremental IRR Rule

◦ The incremental IRR may not exist.

◦ Multiple incremental IRRs could exist.

◦ The fact that the IRR exceeds the cost of capital for both projects does not imply that either project has a positive NPV.

◦ When individual projects have different costs of capital, it is not obvious which cost of capital the incremental IRR should be compared to.

Evaluation of Projects with Different Resource Constraints ◦ Consider three possible projects with a $100 million

budget constraint

Table 7.1 Possible Projects for a $100 Million Budget

The profitability index can be used to identify the optimal combination of projects to undertake. It measures the value created in terms of NPV per unit of resource consumed.

◦ From Table 7.1, we can see it is better to take projects II & III together and forego project I.

Value Created NPVProfitability Index

Resource Consumed Resource Consumed

Problem ◦ Suppose your firm has the following five positive NPV projects

to choose from. However, there is not enough manufacturing space in your plant to select all of the projects. Use profitability index to choose among the projects, given that you only have 100,000 square feet of unused space.

Project NPV Square feet needed

Project 1 100,000 40,000

Project 2 88,000 30,000

Project 3 80,000 38,000

Project 4 50,000 24,000

Project 5 12,000 1,000

Total 330,000 133,000

Solution ◦ Compute the PI for each project.

Project NPV Square feet

needed

Profitability Index

(NPV/Sq. Ft)

Project 1 100,000 40,000 2.5

Project 2 88,000 30,000 2.93

Project 3 80,000 38,000 2.10

Project 4 50,000 24,000 2.08

Project 5 12,000 1,000

12.0

Total 330,000 133,000

Solution ◦ Rank order them by PI and see how many projects

you can have before you run out of space.

Project NPV Square

feet

needed

Profitability

Index

(NPV/Sq. Ft)

Cumulative total

space used

Project 5 12,000 1,000 2.5 1,000

Project 2 88,000 30,000 2.93 31,000

Project 1 100,000 40,000 2.5 71,000

Project 3 80,000 38,000 2.11

Project 4 50,000 24,000 2.08

In some situations the profitability Index does not give an accurate answer.

◦ Suppose in Example 7.4 that NetIt has an additional small project with a NPV of only $120,000 that requires 3 engineers. The profitability index in this case is 0.1 2/ 3 = 0.04, so this project would appear at the bottom of the ranking. However, 3 of the 190 employees are not being used after the first four projects are selected. As a result, it would make sense to take on this project even though it would be ranked last.

With multiple resource constraints, the profitability index can break down completely.