Embed Size (px)

Citation preview

Ag Credit ACA • www.agcredit.net • December 2010

Tribute to Maxwell NiemeyerThe Importance of a Balance Sheet

Year-End Loan Payment and Tax Pointers

Leaderis published quarterly for stockholders, directors and friends of Ag Credit, Agricultural Credit Association.

PresidentNeil Jordan

Board Of DirectorsHal Dalton, ChairmanJerry Layman, Vice ChairmanPaul AleyGary BaldosserCharles BostdorffDeborah Johlin-BachHarold Lunde, Ph.D.Keith RobertsScott SchroederMike Stump

EditorConstance Ruth

PublisherAgFirst Farm Credit Bank

Publishing DirectorDonna Camacho

DesignersAthina EargleDarren HillAmanda SimpsonTravis Taylor

PrinterSpectra True Colour

CirculationKathi DeFlorio

Address changes, questions, comments or requests for copies of our financial reports should be directed to Ag Credit, ACA by writing 610 W. Lytle Street, Fostoria, Ohio 44830 or calling 800-837-3678. Our quarterly financial report can also be obtained on our Web site: www.agcredit.net.

AdvertisementsIf you are interested in advertising in the Leader magazine, which goes to more than 7,000 households in 18 Ohio counties, please call the Norwalk office for more information at1-800-686-0756.

Cover PhotoThe cover photo was taken by Connie Ruth of Bacon Woods sledding hill in Lorain County, Ohio.

’Tis the season to appreciate friends and family.

www.agcredit.net

Merry Christmas and Happy New Year from your friends

at Ag Credit and Country Mortgages. Contact us for all your

agricultural and residential loan needs.

419-435-7758 ext. 1033 or 10371-800-837-3678

Contents

Page 8

Page 16

Page 15

Message from the PresidentMaking a Smart Choice 4

Recent Land Sales 5

The Lighter SideIdeal Schools Require Family Involvement 6

A Rural Perspective— Raking Hay 7

FeatureTribute to Maxwell Niemeyer 8

Community NewsBuilding Dreams with Your Cooperative 9

Building and Protecting the Farm 10

The Importance of a Balance Sheet 11

Association NewsAround AgCredit 12

Buy Locally Grown 15

Appreciation Days 16

Industry NewsYear-End Loan Payment and Tax Pointers 18

Cranium: The Sixth “C” of Credit 20

Why is an Appraisal Important? 21

FinancialsThird Quarter Financial Report 22

LifestyleAgates from Agatha 23

Internet Security 24

December 2010, Ag Credit ACA | 3

Neil Jordan Making a Smart Choice

Message from the President

\\Imdprfil03\data_mkt$\Athina WIP\LEADERS\---In Progress---\AgCredit-Winter10\AgCredit-December Leader info\Files from FTP\Pictures\Art#1-2009 current charts.xlsx

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

PERMANENT CAPITAL RATIO AS OF SEPTEMBER, 2010

Permanent Capital RatioAs of September 2010

How Do You Select a Lender?Recently, several of our cooperative’s team members and I had the opportunity to attend a large real estate auction. You know the kind. This one had multiple parcels totaling over 1,000 acres. The acres were initially bid off individually, then bidders could bid on the entire offering or any combination of the parcels thereafter. It sure did get interesting!

After the auction, one of the bidders from an area quite a distance from our lending territory, approached our team about potentially starting a lending relationship with us. He and his family had heard good things about our cooperative and wanted to know more. Jennifer Stirm, an account officer from our Bucyrus Office, explained who Ag Credit is, our cooperative’s structure, member ownership, how our excess capital from annual profits is distributed to our members, and how we continually try to maximize our cooperative’s value to our membership’s operations.

After our ownership and structural explanations, Jennifer explained the potential of 5, 10, 15, to 20-year fixed-rate terms designed to minimize future threats of inflation and rising interest rates. She also explained how our competitive long-term fixed rates are enhanced even more by our past 5-year average of patronage refunds. She described profit sharing—how we distribute over 25 percent of the interest our members paid, comes back to them in cash and allocated reserve equity.

After Jennifer’s excellent explanation they chose to do business with Ag Credit.

Going Deeper into the DecisionJennifer had only 15 minutes to “hit the highlights” of our cooperative principles, operating procedures, profit sharing, and other ways of adding value to our membership. Later, on the drive home, I thought about her thorough and graceful explanation about the advantages of our cooperative and it prompted me to think about all the factors we should consider when selecting a lender. For me, these considerations include a wide range of factors surrounding the company and the employees of the company:

• Do the company’s team members have strong ethical standards? Can I trust them?

• Do they follow any specific corporate and personal core values?• Do they have a mission statement that relates to helping

their customers?• Is their business structure sound? Is the company

financially strong?• Do they have a historical trend of profitability and

financial strength?• Are they viable for the long-term? Will they be here for me and

my family for years to come?• Do they have a passion for agriculture and for farm families,

like mine?

These considerations have become more important to me over the years—since the Enron and WorldCom scandals. Will this company I am about to choose do the right thing for me and my family through thick and thin? As the spokesman for our board, our management and our team members, I can pledge absolutely, we will.

Company Core ValuesMany years ago, our directors and team members developed our cooperative’s core values. We will

• Treat our customers and prospects as we would like to be treated.• Conduct ourselves professionally with unyielding integrity.• Meet new challenges objectively with a positive mental attitude.• Focus on building, nurturing, and maintaining genuine

relationships with our stockholders.• Exceed our customers’ expectations, produce what we promise.

These core values hold each of us to high standards and expectations in our interactions with prospects, members, vendors, interested parties and with each other. They have stood the test of time.

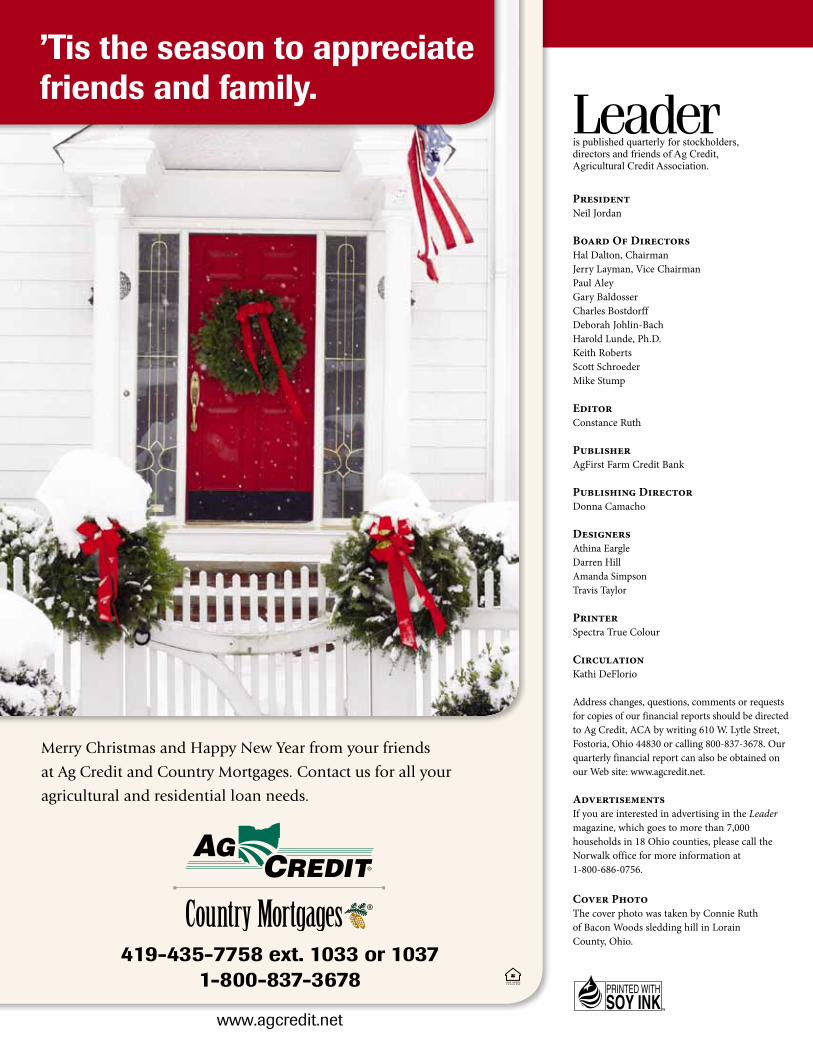

Financial Stability and TrendsOur cooperative has exhibited sterling long-term trends in profitability, capital strength, volume growth, market share, and distribution of profits to our membership. Our cooperative structure provides an excellent tool to minimize state and federal taxes eliminating double taxation, thus creating value for our membership. We provide the lowest net cost of funds possible. Generally, a lender with a strong capital base reflects a long-term trend of favorable annual net-incomes and growth.

By the end of our 2010 third quarter, our permanent capital ratio exceeded 19 percent. In spite of four years of double-digit loan volume growth, this level of capital is considered very favorable in any lender’s circles.

4 | December 2010, Ag Credit ACA

Recent Land Sales

The following information was provided by:

Wayne Wilson—Wilson Auction and Realty825 North Main StreetBryan, OH 43506www.WilsonAuctionLtd.com

Location 1Acres: 123Location: Preble County, OHDate of Sale: 10-01-10Selling Price: $390,000

Location 2Acres: 53 Location: Preble County, OHDate of Sale: 10-01-10Selling price: $132,000

Schrader Real Estate and Auction Co.P.O. Box 508 950 North Liberty DriveColumbia City, IN 46725www.schraderauction.com

Location 1Acres: 102Location: Allen County, Spencer TownshipDate of Sale: 10-11-10Selling Price: $505,000Unimproved

Location 2Acres: 261 Location: Butler CountyDate of Sale: 10-07-10Selling Price: $910,000Improved Tract 8 contains a 2-story farmhouse and farm storage building.

Location 3Acres: 192Location: Pickaway County, OHDate of Sale: 09-23-10Selling Price: $850,000Improved1) 3-bedroom, 1 bath, 2,157

square feet, 2-story country home with 3 grain bins and outbuildings

2) 3-bedroom, 1 bath, 1,458 square feet, cape cod home with 20’x25’ detached garage

Location 4Acres: 408+Location: Henry County, Harrison TownshipDate of Sale: 10-18-10 Selling Price: $2,985,000ImprovedTract #2 has an older barn

Ned F. Gregg Realty, Inc.P.O. Box 364Sycamore, OH 44882www.nedsold.com

Location 1Acres: 1,010Location: Crawford CountyDate of Sale: 10-21-10Selling Price: $5,919,000Unimproved

Attention Auctioneers: Would you like to be featured in a future column? It’s easy. Visit our website www.agcredit.net and click on the Auctioneer’s link to find the Recent Land Sale form online. Fax the completed forms to 419-663-4120. n

Adding Value to MembersOur past two years are proving to be marquee years in further adding value to our membership! As the interest rate environment moved down to lower levels, our team has successfully reduced the interest rates charged on your fixed-rate loans. Over 7,800 note modifications have been processed since April 2009, with a projected membership approximate annual saving of over $5 million for the next five years!

Our cooperative will also experience an interest cost savings of approximately $3.5 million annually for the next five years as well! When contacting you to reprice your loan at a lower interest rate, we were also able to establish a lower direct note rate from AgFirst Farm Credit Bank. This was accomplished by exercising the callable debt obligations we have built into our bank and association operating procedures. This feature has performed very favorably in this exceptionally low interest-rate environment.

So, why should new applicants choose Ag Credit as a lender? For the same reasons you and I did:

• Clear, concise, ethical core values, and people we could trust;• A strong company bolstered by favorable net income trends

bringing capital stability;• Member focused, competitive products solving our risk

management needs; and,• A cooperative structure to truly add value to my operation.

And, as you and I can attest, they will be glad they chose our cooperative! n

The information being provided in this column is only a sample of recent land sales around Ohio. Since there are many factors taken into consideration when a buyer and seller establish a price, these sales may or may not reflect the current market value in any particular area and should not be used in lieu of a formal appraisal by a state certified real estate appraiser to establish a value for a particular tract of land.

December 2010, Ag Credit ACA | 5

President’s message continued

Section Heading

Ideal SchoolS RequIRe FamIly Involvement

The Lighter Side

Pat Leimbach

Pat Leimbach is a farm widow who still farms with her son Orrin at End o’ Way Farm near Vermilion, Ohio. Her late husband, Paul, and her father-in-law, Henry, were both directors of the Production Credit Association at Ashland, Ohio during the 1960s. Pat wrote A Country Wife column for the Elyria, Ohio, Chronicle Telegram for many years, as well as for farm magazines nationwide. She has shared her lively wit with audiences in 48 states and five Canadian provinces. Among those audiences have been dozens of Farm Credit groups.

She is also the author of three books, A Thread of Blue Denim, All My Meadows, and Harvest of Bittersweet.

The quality of our school teachers has lately risen to prominence in the unending struggle to improve American schools. I recently unearthed an article clipped from an issue of Harpers Magazine long ago devoted to the “ideal school.”

The lead article is a discussion among four of America’s “leading educators” who are challenged by Harper’s editor, Lewis Lapham, to describe their ideal school.

One doesn’t read far in the discussion without recognizing why presidents, legislators, and bureaucrats don’t have a prayer where resolving these problems are concerned.

Although the experts were of one mind on the need for reform and the conviction that standardized tests are not the answer, on almost every other issue they were at odds.

The success of the schools they described and in which they had been involved—charter schools, private schools, for-profit schools—hinged upon the ideal teacher, whom they described at length:

• Ideal teachers know how to keep their students engaged in the question at hand.

• They can reach students of very different learning styles.

• “They’ve got to be real people!”• They must know their subjects cold, so well

that they have real confidence.• They must be passionate about their subjects.• They must be dynamic.

Well ... sure!All we need is a million teachers answering

that description and the problems would be resolved.

Where do we get them?I wanted to be a teacher from the day I entered

first grade. I had well-seasoned teachers who inspired me, I finished high in my class and went on to a good university. I got “As” in my major subjects. I completed my practice teaching with the premier critic teacher in my field in the city of

Cleveland. I took all those teaching courses the state requires and passed the qualifying exam.

Still, when I walked into my first classroom, I didn’t exhibit any of those “ideal” teacher qualities. Standing there before those unsophisticated country sophomores my knees were shaking.

Didn’t I know my subject cold?Well, one of them, maybe. (I was hired to teach

five different subjects.) And I was very lucky to have ideal students. They were patient while I was learning to be real, to gain confidence, to discover different approaches for pupils on different levels.

If they hadn’t been, their parents would have handed me their heads. As a parent in one of our neighboring schools once said about his obstreperous son, “I sent him up there and you better learn him!”

That first classroom was a swampy place beneath the stage. The janitor lay planks on the floor between rows of seats so we wouldn’t get wet feet after a rain. Those kids could have been poster children for the disadvantaged, but nobody ever told them. They learned French and English in spite of me and the swamp.

If I could have stayed at it steadily a few years, I might have become a good teacher. I might even have become dynamic. Who knows?

Instead, I became pregnant and resigned to raise our sons. (I returned to substitute for 23 years but that is a different bag.)

America has school problems that neither teachers, nor money, nor buildings, nor standardized tests will fix. We need to engage families in the total process of education and restore some discipline to the classrooms.

It may be true that some few teachers are born dynamic, self-confident, brilliant, passionate masters of their subjects, but the vast majority only achieve these ideals with time and experience in a relatively un-hostile environment. n

6 | December 2010, Ag Credit ACA

I’ve been driving a tractor since I was nine years old. The first specific task I was allowed to do was raking hay. My grandfather had a small Ford tractor where the pedals were within reach,

especially if I slid off the seat and used my weight to disengage the clutch and press on the brake. The first tractor driving job I could aspire to was raking hay. This was the least complicated, most straightforward task on the farm.

The old, steel-wheel, side-delivery rake had originally been pulled by a team of horses but now, with a shortened hitch, did the job just as well behind mechanical horsepower. All a person had to do to begin was drop a pin through the hitch of the rake and the drawbar of the tractor, lower the rake with a simple lever so the tines could sweep the hay off the ground and then engage the ground-driven gearbox to make the rake spin. Simple enough. It was easy to understand why it was the starter job for eager nine-year-olds. Once the novelty wore off, it even became monotonous. This may be hard to believe, but one time the rhythmic clatter of the old rake, the slow pace and purr of the tractor was so mesmerizing I didn’t realize the draw pin had popped out and I was no longer pulling the rake until I drove up behind it on the next time around the field.

I’ve been raking hay for a lot of years since then and with a number of different rakes. Regardless of any innovations or design improvements, the hay rake still remained the least complex implement on the farm and the task of raking hay was still the job for breaking in new generations of tractor drivers.

Enter the Gyrorake. No longer can the hay rake be classified as simple and uncomplicated and no longer can raking hay be a job to entrust to nine-year-olds. In fact, there is good reason

to question if sixty-something tractor drivers, regardless of previous experience, might be up to the challenge. Let me explain:

My daughter, Elaine, and son-in-law, Robert, now manage the haying enterprise on our farm. They decided to upgrade to a more versatile, higher tech rake to move the hay more gently and leave it in a fluffier windrow for better drying. Good idea. This implement does not, however, resemble in any way the hay rakes of my youth. Instead of a relatively compact, lightweight implement that can be tucked away in a corner of the barn, the Gyrorake is over thirty feet long, weighs over two tons and requires two remote hydraulic connections and an electrical hookup for controls. It has two horizontal spinning rotors with twelve arms per rotor and eight tines per arm. It folds out or in, swings left or right, lifts up or pushes down, can do one windrow or two and not only appears gangly and awkward, it is gangly and awkward. In addition to looking as if it was designed on an Etch-a-Sketch, perhaps the most telling indication this was not my father’s hay rake was the need for a 60-page operator’s manual. I have to admit, it does a beautiful job in the hands of an experienced operator. Gaining the experience is the trick.

Elaine and Robert learned to use it and the Gyrorake worked as well as advertised and everything was fine until the day they were in a pinch for help and asked me if I could rake a field of hay for them. I got a crash course on operating basics the evening before from my son-in-law. He made it sound simple enough and assured me I’d have little problem figuring it out. I had my doubts but thought certainly, with my vast reservoir of experience, I’d be fine.

Of course, instead of a day with bright sunshine and a good breeze, the next day was still and humid. Time was of the essence once the dew was off to get the hay raked if there would be any chance of baling hay that afternoon. Once in the field and trying to hurry, my confidence from the previous evening

soon evaporated. Robert’s comments about the idiosyncrasies of this tractor’s hydraulic system and his note saying I might need to make a slight adjustment to level the rotors and compensate for drawbar height proved to be more significant than I thought at the time.

After fumbling through the process of using the hydraulics and selector switch to position the two rotors and other essential components, I tackled the “slight adjustment” Robert said would be necessary. I couldn’t understand why every time I thought I had the rotors leveled correctly, the next time I looked they were again out of position and I’d have to make an additional adjustment to the linkage mechanism. Then I remembered Robert’s caution about the tendency of this tractor’s hydraulics to creep out of position every few minutes. I had to undo all of the previous adjustments, try to remember my original point and start over. I found there was very little difference between a setting that swept the field clean and settings that either left the hay untouched or attempted to uproot every alfalfa plant in the field.

My first couple passes around the field were real adventures. Not only was I learning the tendencies of an unstable hydraulic system, I had to learn where to drive in relation to the hay swaths and how to set the rake to gather it all in without tangling with fence posts or leaving large patches of hay unraked. Those first couple times around the field had to be repeated until I got it more nearly right. All told, the first hour in the field was not very productive.

I have since become more proficient with the Gyrorake and can, with increasing levels of confidence, tackle most challenges this new-fangled monster presents. It is clear, though, it will be a very long time before raking hay becomes monotonous or mesmerizing and it certainly will not be the first tractor driving job for my grandchildren. Such is progress, I guess. n

December 2010, Ag Credit ACA | 7

A Rural Perspective

Raking HayBy James McConnell

James McConnell is a member of Ag Credit who farms 2,500 acres in southern Lorain County with his two brothers.

Ideal SchoolS RequIRe FamIly Involvement

Jim McConnell

By Eric Miller

Tribute to Maxwell Niemeyer Morrow County

The 5th Annual Harvest Celebration and Hog Roast at MadMax Farms on September 25 was a great success. The fall celebration was organized by Ag Credit members, Eric and Stephanie Niemeyer, with the help of their daughter, Madison. Beautiful fall weather, family fun, and plenty of pumpkins attracted many visitors to their farm. There were a variety of activities to entertain people of all ages; hay-rides, corn-hole games, pumpkin painting, face painting, and even a juggler.

MadMax Farms was established in 2005 as a tribute to Maxwell Niemeyer, the late son of Eric and Stephanie. Max was born in September 1999 and was diagnosed with

Lissencephaly, a rare neurological disorder, shortly after birth. Max lived for five years. The Niemeyer family is very grateful for the generosity of the community and the care he received at Columbus Children’s Hospital. To help show their gratitude, 100 percent of the contributions accepted by the farm are given to children’s charities.

Along with raising pumpkins, Eric and Stephanie operate a 335-acre cash grain farm growing corn and soybeans. Since starting from scratch in 2005, the Niemeyers have accumulated a full line of equipment and continue to expand this part of their farm operation.

Ag Credit team members were happy to attend the Annual Harvest Celebration and look forward to working with the Niemeyer family in the future. If you would like more information on MadMax Farms and the Annual Harvest Celebration please visit www.madmaxfarms.com. n

Feature

Tribute to “our little buddy”

Sign welcomes all to the celebration The band tunes up

Great day for a hayride

8 | December 2010, Ag Credit ACA

December 2010, Ag Credit ACA | 9

Eric Barker owns two acres of land in Graytown, Ohio. He came to Ag Credit to pursue his plan to build the perfect home. After walking through a home his mother had recently built, Eric knew the layout would be great for his own home. Eric broke ground in late July and plans to be in his new home by the holidays.

The Behnfeldt family (Chad, Sara, Ben, and Grace) from McClure, Ohio, needed a larger home. Now, with the new addition, their 1,500-square-foot home will soon be 3,000 square feet. This is something their family had been looking forward to for a long time. Beyond the pond and pine trees, the Behnfeldts are now watching their dream become a reality. The Behnfeldts broke ground in July and are looking forward to their added space.

By Matt Gray, Home Loan Originator

Building Dreams with Your Cooperative

Nothing creates more excitement, involves so many choices and is quite as gratifying as building a new home! We are proud of the home loan programs we offer. Unlike many banks and financial institutions, we still consider construction loan requests. Our goal is to help our members come to a sound financial loan decision and help them reach their goals. This is what makes our home loan department special. No two construction loans are alike and we are willing to work with many unique circumstances.

The Benfer Family (Scott, Jessica, Logan, Evan, and Addison) resides in Monroeville, Ohio. When they came to Ag Credit they had just sold their home and were ready to start their new lives in a home built just for their growing family. Nestled on a five-acre partially wooded lot down a winding drive sits a one-and-a-half story home with a walkout basement. The Benfers broke ground in late May and were ready to move in to their new home in mid-October.

There is something very appealing about building a new home. The scent of new lumber, the dusty smell of drywall, and the clean fragrance of new carpet are exciting! It is also fun to watch as dreams are fulfilled and a shell of a building transforms into a beautiful home. Are you thinking about building or know of someone who is? Come in and see us. We look forward to hearing about your construction projects and would love to discuss your ideas, plans and dreams! n

Community News

Community News

Building and Protecting the Farm Risk Management Capstone On August 13 and 14, more than 150 people participated in the Risk Management Week-End Capstone. The two-day event, held at the Hilton Garden Inn in Perrysburg, Ohio, gave the series participants another chance to network, explore tools to manage risk in their operations, and meet with industry leaders. Breakout sessions held Saturday morning covered each of the five areas of risk in agriculture. Participants had the opportunity

to hear Dr. David Kohl address the future of agriculture. This capstone was the final program for the Building & Protecting Your Farm, Risk Management series. Funding for the series was made possible by a grant through the North Central Risk Management Education Center. This January through August series was coordinated by Van Wert, Account Officer, Kendra Heffelfinger. n

10 | December 2010, Ag Credit ACA

October 2010, Ag Credit ACA | 11

The Importance of Balance Sheets By Brian Ricker

As the new year approaches I always find myself thinking about my new goals for the coming year. For me the new year is a way to make a fresh start. I think about what old habits I should break and what new activity or project I should take on.

One activity I started 13 years ago, shortly after I started working for Ag Credit, was preparing a year-end balance sheet. Of course the idea of preparing a balance sheet came about because I was a new account officer and was asking our Ag Credit borrowers to complete balance sheets of their own. It only seemed right for me to practice what I preached!

My year-end balance sheet does not take a lot of time to complete and has historically been done during half-time of a New Year’s Day bowl game. I have always dated the balance sheet January 1 and all balances are figured as of that date. By completing it on the same day each year I can easily compare my financial progress or lack of progress. I write down all my assets on the left side of the paper in order of very liquid assets, such as savings and checking accounts to intermediate assets, such as retirement accounts and vehicles. The final asset category is long- term assets, such as real estate which, in my

situation, is my home (I still have dreams of owning a farm someday).

On the right side of the paper I state my financial liabilities. I start with any accounts payable bills outstanding and I continue with loan balances on my vehicle and home. After completing each side of the balance sheet I subtract my total liabilities from the assets to come up with my net worth. Over the years I have taken this net worth figure and made some adjustments to take out the large changes due to appreciation or a loss on my 401K for the year. This typically only takes me around twenty minutes to prepare and this simple approach gives me peace of mind because it shows I am making financial progress.

Looking back on my 13 years of personal balance sheets is a trend of some ups and also some downs. The financially down years, in my case, were the result of poor stock market performance (lower 401K and IRA balances) purchasing a home (extra expense with home ownership), birth of children (medical expenses), and events like helping to pay for my wedding and honeymoon. Most events were memorable and joyous, however, each event had an impact on my financial picture.

Your balance sheet may take more time and effort than mine. I encourage you to

complete your year-end balance sheet and share it with your Ag Credit account officer. Doing so could speed up the decision-making process on your next loan request. Accurate year-end balance sheets completed annually allow you and your account officer an opportunity to view your financial trends. This will be extremely beneficial when making important financial decisions now and in the future. The lack of accurate and quality financials could negatively impact a future loan request. As you grow your operation Ag Credit wants to be there for you.

One excellent Web site to help you better understand balance sheets and overall financial statements is a site from the Center for Farm Financial Management through the University of Minnesota at http://ifsam.cffm.umn.edu/. The site has videos to explain balance sheets and all facets of farm financial management.

If year-end balance sheet preparation is an old habit, I encourage you to keep it up. If not, why not start a valuable new habit in 2011 and learn more about farm financial management? n

Association News

In Hardin CountyLast year Ridgemont FFA won the title of Best Chapter in Ohio proving students from little schools can work hard and accomplish a lot. This year they set a goal of being The Best Chapter in the Nation. On October 21, they accomplished their goal when they were picked as the number one chapter out of 7,500 chapters in the nation! At the National FFA Convention the students were judged on their three top projects: Safe Teen Driving, Bullying and Abuse, and Farm Safety. After the convention, supporters lined the streets to welcome students home and a rally was held at the school on November 1, to honor the students and thank the community for their support. FFA Advisor, Stephanie Jollif, and her husband, Tom, are members of Ag Credit. Congratulations!

In Van Wert CountyAg Credit, Van Wert Company Farm Bureau, Edwards Jones Investments and three other buyers purchased Tanner Matthews’ dairy steer at the Jr. Fair Livestock Sale this year. The steer was processed at Ebel’s Butcher Shop in Grover Hill and the meat was donated to three Van Wert- area food pantries. Pictured are Tracey Keber, Edward Jones Investments; David Kemler, President Van Wert Co. Farm Bureau; Aaron Stoller, Ag Credit; and Tanner Matthews.

12 | December 2010, Ag Credit ACA

Calendar

December 24 Offices closed for Christmas

December 31 Offices open

January 3 Offices closed for New Years

January 17 Offices closed for Martin Luther King Jr. birthday

February 21 Closed for President’s Day

October 2010, Ag Credit ACA | 13

In Crawford County Nathan Brausy (Soil and Water) and Darrell Swinehart (Ag Credit) present Ron Schroeder with the Cooperator of the Year award sign donated by Ag Credit.

Joe Erb, representing Ag Credit, hands out FFA handbooks for the 2010–11 school year. Helping young people is a small part of what we do, but a very important part.

In Huron CountyNorwalk Ag Credit member, Dale Smith, of Willard, Ohio, was selected as a winner in the America’s Farmers Grow Communities program which gives farmers a chance to win $2,500 for their favorite charity. Dale chose “God’s Little Critters” to get the prize.

In Morrow CountyAg Credit sponsored the “Master Showman” awards for the 2010 Morrow County Fair. The “Master Showman” award recognizes the top showman after the final showmanship class for each of several different species including hogs, feeder cattle, market beef, sheep, rabbits, goats, poultry, and dairy.

Ag Credit presented the “Master Showman” winners with director’s chairs embroidered with the title of each individual’s award. Winners were: Hogs, Tyler Beck; Feeders, Ellie Logan; Beef, Kyndall Williams; Sheep, Allison Welty; Rabbits, Nick Hayes; Goats, Tyler Beck; Poultry, Valerie Tolle; and Dairy, Kayla Mason.

Eric Miller presents award to Ellie Logan, Master Showman for Feeders Joe Erb presents director’s chair award to Allison Welty for Master Sheep Showman

December 2010, Ag Credit ACA | 13

Association News

14 | October 2010, Ag Credit ACA

Coming up: Van Wert County—January 28AgOutlook Meeting—Van Wert. Call 419-238-6838 for details.

Hancock, Wood, and Seneca Counties Farm Electrical Safety Day is a free event for all farming members of Hancock-Wood Electric Cooperative, Prism Propane and Farm Bureau Members of Hancock, Seneca and Wood Counties. The event will be held on January 26, 2011, at the Hancock-Wood Co-op, 1399 Business Park Drive South, N. Baltimore, OH 45872. The free breakfast begins at 7:30–8:00 a.m. with programs following at 8, 9, and 10. Come visit our Ag Credit booth. Call Tiffany Hussey 419-257-5012 for more details.

Wood and Erie Counties Farm Finance for Women Seminar—sponsored by The Ohio State University Extension will be held in Wood County on February 9, 16, 23 and March 2. Call Doris Herringshaw at 419-345-9050 for details.

The series will be held in Erie County on February 17 and 24 and March 3 and 10. For more information, call Julia Nolan Woodruff at 419-627-7631.

Annie’s Project—Education for Farm Women This program was introduced in Ohio in January of 2007. Currently over 7,000 women have completed the project in 22 states. Annie’s Project will be held throughout the state during the winter of 2011. For a program in your county, contact Julie Nolan Woodruff: 419-627-7631.

Mark your calendars—January 25–26The Ohio Farm Management Conference will be held at University Plaza Hotel in Columbus, OH. This event is sponsored by The Ohio State Extension. For more information, call 419-627-7631. n

Winter Ag Conference—February 2, 2011Sponsored by Ag Credit and Silveus Insurance GroupCamden Falls, 2458 S. State Rt. 231, Tiffin, Ohio 44883 from 9 a.m.–3 p.m. For more information contact, Randy Owen at 1-800-531-9909

Check us out on Facebook, Twitter and our Web site

In Erie CountyHugh Storer (Norwalk) and Stacey Dvorak (Wellington) represented Ag Credit and acted as hosts for the Erie County Farm Tour on Sunday, October 10 at the Willoway Nurseries Huron greenhouse location. Other stops included Orchard Hill Orchards of Berlin Heights (Bill Gammie and family) and Heritage Farms (John Hartman and family). 150 people went on the tour and gained knowledge about agriculture in Erie County.

In Putnam CountyLooks like everyone had a great time at the Kiddie Tractor-Pull, sponsored by Ag Credit, at the Fall Festival in Continental on September 24.

14 | December 2010, Ag Credit ACA

Pandora, Ohio

419-384-7373John Schulte

Schulte’S logging

Buyer of standing timberLow impact logging

“Harvesting Quality Trees with Care”

http://www.facebook.com/agcredit

http://twitter.com/agcredit

www.agcredit.net

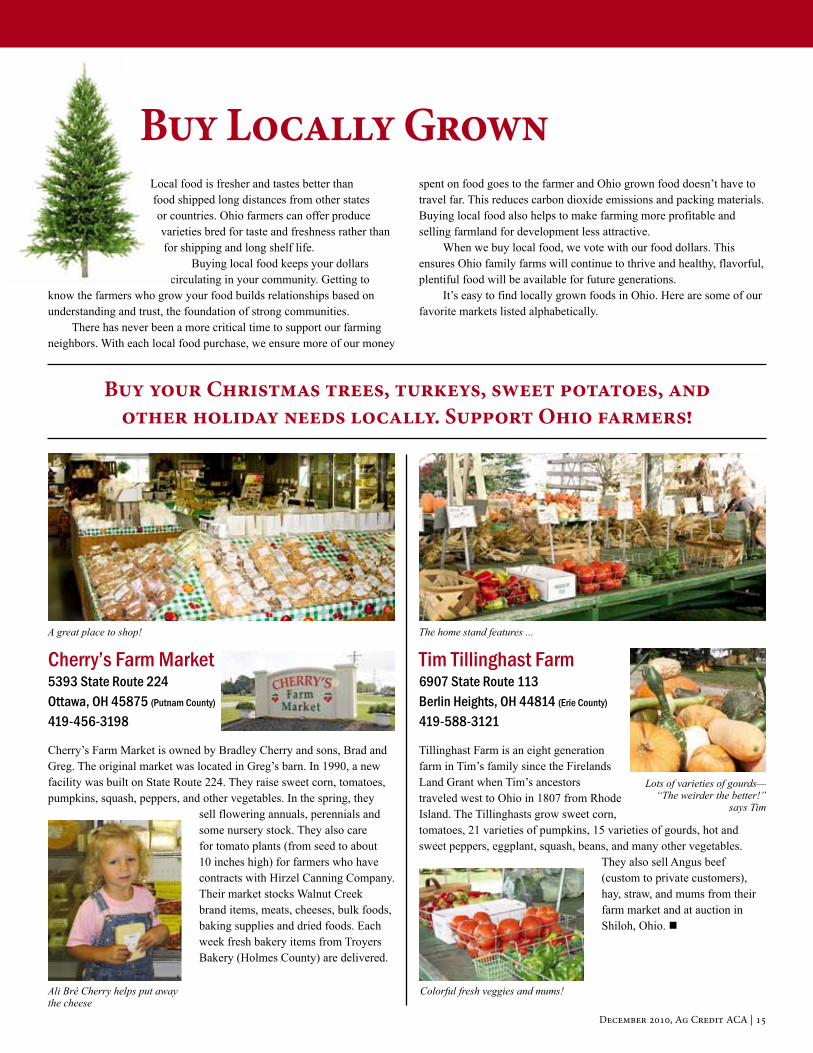

Local food is fresher and tastes better than food shipped long distances from other states or countries. Ohio farmers can offer produce varieties bred for taste and freshness rather than for shipping and long shelf life.

Buying local food keeps your dollars circulating in your community. Getting to

know the farmers who grow your food builds relationships based on understanding and trust, the foundation of strong communities.

There has never been a more critical time to support our farming neighbors. With each local food purchase, we ensure more of our money

spent on food goes to the farmer and Ohio grown food doesn’t have to travel far. This reduces carbon dioxide emissions and packing materials. Buying local food also helps to make farming more profitable and selling farmland for development less attractive.

When we buy local food, we vote with our food dollars. This ensures Ohio family farms will continue to thrive and healthy, flavorful, plentiful food will be available for future generations.

It’s easy to find locally grown foods in Ohio. Here are some of our favorite markets listed alphabetically.

Buy your Christmas trees, turkeys, sweet potatoes, and other holiday needs locally. Support Ohio farmers!

Buy Locally Grown

Cherry’s Farm Market5393 State Route 224Ottawa, OH 45875 (Putnam County)

419-456-3198

Cherry’s Farm Market is owned by Bradley Cherry and sons, Brad and Greg. The original market was located in Greg’s barn. In 1990, a new facility was built on State Route 224. They raise sweet corn, tomatoes, pumpkins, squash, peppers, and other vegetables. In the spring, they

sell flowering annuals, perennials and some nursery stock. They also care for tomato plants (from seed to about 10 inches high) for farmers who have contracts with Hirzel Canning Company. Their market stocks Walnut Creek brand items, meats, cheeses, bulk foods, baking supplies and dried foods. Each week fresh bakery items from Troyers Bakery (Holmes County) are delivered.

Tim Tillinghast Farm6907 State Route 113Berlin Heights, OH 44814 (Erie County)

419-588-3121

Tillinghast Farm is an eight generation farm in Tim’s family since the Firelands Land Grant when Tim’s ancestors traveled west to Ohio in 1807 from Rhode Island. The Tillinghasts grow sweet corn, tomatoes, 21 varieties of pumpkins, 15 varieties of gourds, hot and sweet peppers, eggplant, squash, beans, and many other vegetables.

They also sell Angus beef (custom to private customers), hay, straw, and mums from their farm market and at auction in Shiloh, Ohio. n

A great place to shop!

Ali Bré Cherry helps put away the cheese

The home stand features ...

Colorful fresh veggies and mums!

Lots of varieties of gourds—“The weirder the better!”

says Tim

December 2010, Ag Credit ACA | 15

Section HeadingAssociation News

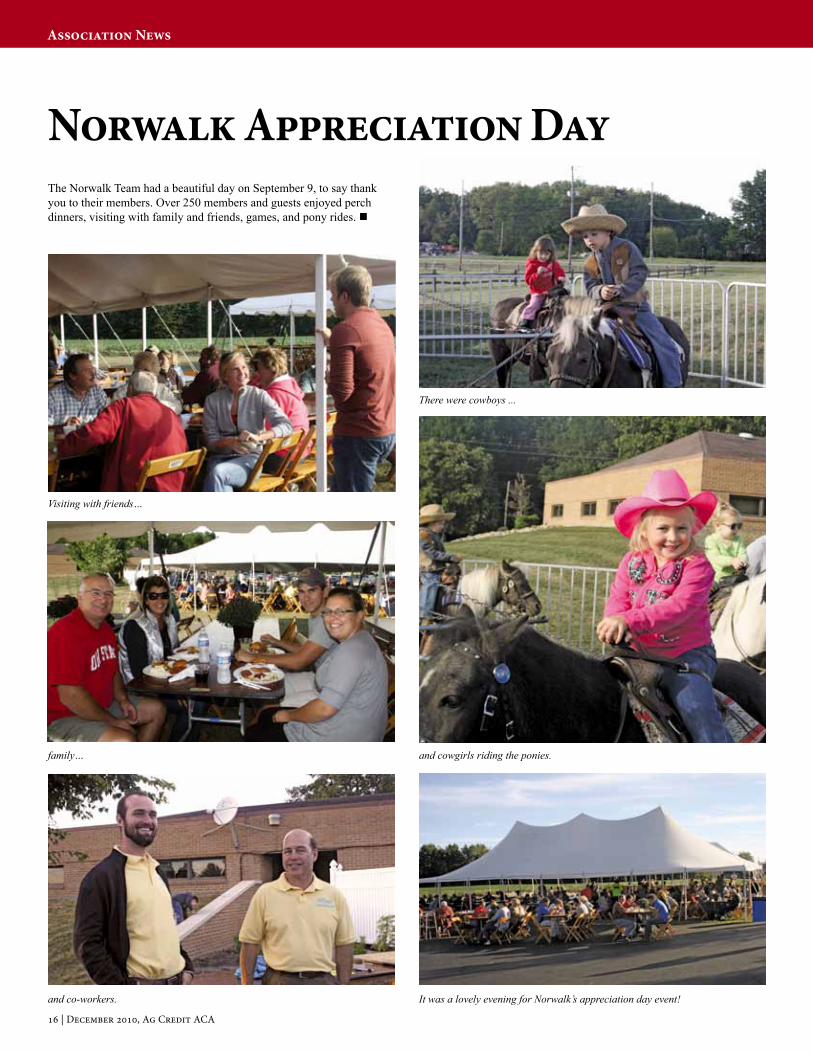

The Norwalk Team had a beautiful day on September 9, to say thank you to their members. Over 250 members and guests enjoyed perch dinners, visiting with family and friends, games, and pony rides. n

Norwalk Appreciation Day

It was a lovely evening for Norwalk’s appreciation day event!

family…

Visiting with friends…

and co-workers.

There were cowboys ...

and cowgirls riding the ponies.

16 | December 2010, Ag Credit ACA

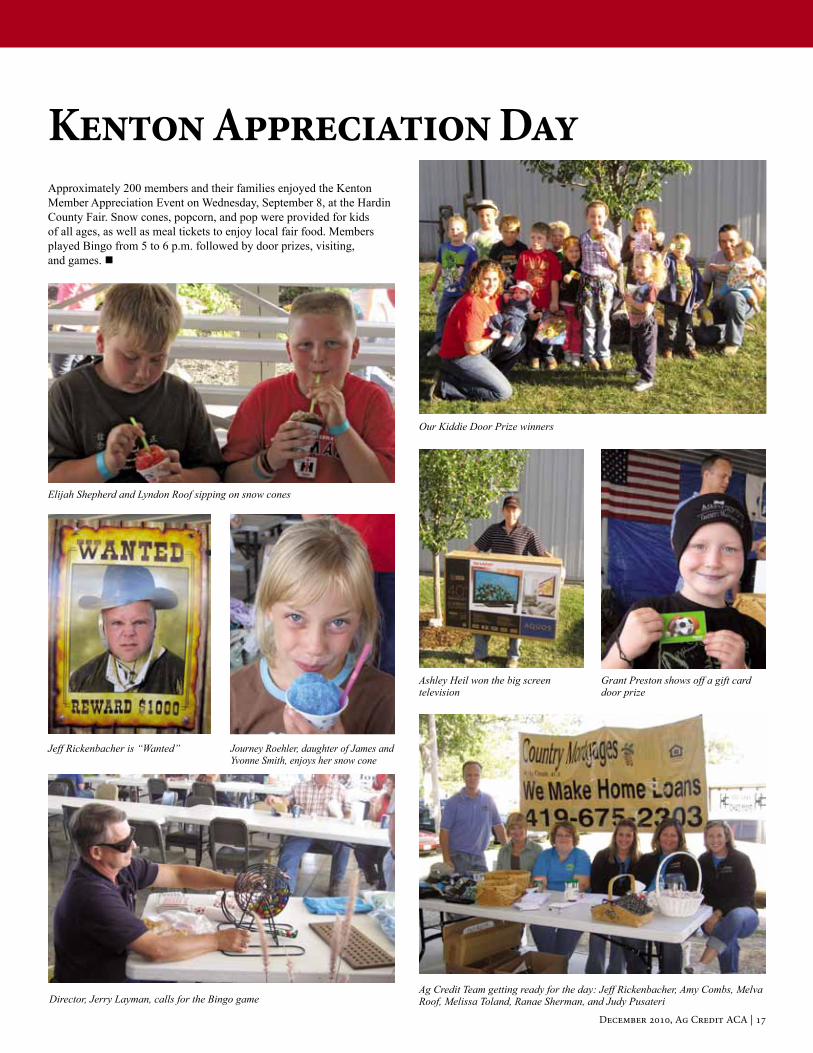

Approximately 200 members and their families enjoyed the Kenton Member Appreciation Event on Wednesday, September 8, at the Hardin County Fair. Snow cones, popcorn, and pop were provided for kids of all ages, as well as meal tickets to enjoy local fair food. Members played Bingo from 5 to 6 p.m. followed by door prizes, visiting, and games. n

Kenton Appreciation Day

Ag Credit Team getting ready for the day: Jeff Rickenbacher, Amy Combs, Melva Roof, Melissa Toland, Ranae Sherman, and Judy Pusateri

Ashley Heil won the big screen television

Grant Preston shows off a gift card door prize

Our Kiddie Door Prize winners

Director, Jerry Layman, calls for the Bingo game

Jeff Rickenbacher is “Wanted” Journey Roehler, daughter of James and Yvonne Smith, enjoys her snow cone

Elijah Shepherd and Lyndon Roof sipping on snow cones

December 2010, Ag Credit ACA | 17

18 | October 2010, Ag Credit ACA18 | October 2010, Ag Credit ACA

Industry News

18 | December 2010, Ag Credit ACA

Year-End Loan Payment and Tax PointersBy Dan Ebert and Greg Siebenaller

As the holiday season approaches we are reminded year-end is just around the corner. With each year-end comes the task of finishing up your business plan for the current year and readying a plan for the new one. The following are a few items to keep in mind to assist you in planning for the end of the year, making principal or interest payments before the end of the year and preparing for the upcoming income tax season.

LOAN PAYMENTSuThe branches will close 2010 business at

3:00 p.m. on Friday, December 31, 2010.

oPayments received after this time will be credited effective January 4, 2011.

oWe encourage you to make your loan payments prior to December 31, 2010, to help ensure the proper crediting of the payment to your account for 2010,

oPlease take into account mail time if you mail the payment to your local branch. We give you credit based on when we receive the payment and not the date of the check or when the payment is post marked.

uCan I prepay my loan interest and get credit for 2010?

oYes. You can prepay all or a portion of your accrued interest before the end of the year.

oMake your intentions to pay accrued interest clear to the branch team.

o If you mail the payment, clearly mark your intent to pay interest and allow adequate mailing time to ensure it will be processed before the end of the year.

oIf you go to your local Ag Credit office to make the payment, make sure you tell the Customer Service Representative (CSR) you want your payment applied to interest for 2010.

oThe total interest paid on all of your loans for 2010 will appear on the IRS Form 1098 Mortgage Interest Statement you receive from Ag Credit in January 2011.

uCan I prepay my January 2011 real estate mortgage loan payment in 2010 and get interest credit for 2010?

oYes. The entire payment must be made and received by the Association before 3:00 p.m. on Friday, December 31 to ensure you receive credit for the payment in 2010.

oYou cannot use funds held interest credit to pay a portion of the payment and get credit in 2010.

oIt is very important for you to clearly indicate to the branch team whether you want to receive credit for your payment in 2010 or 2011.

oIf the full amount of the loan payment is received on or before December 31, 2010, the loan payment will be recorded in 2010 rather than in January, 2011.

IRS INFORMATIONAL RETURNSuAll informational returns are reported

under the taxpayer identification number (social security number or business tax number) for the person or entity listed as the primary borrower for the borrowing entity.

uStatements are available on Account Access in mid-January 2011. Paper forms, along with your Member Summary Statement, will be mailed out in late January.

1098 – Mortgage Interest Statements – This form is issued to each member who paid interest to Ag Credit in 2010. Any interest refinanced by another loan is not reported. Only interest paid by you is reported on this statement.

1099-INT – Interest Income – If you had funds in escrow (funds held) for future payments or the Reserve Account during the year, the interest earned on this money is reported on this IRS form.

1099-DIV – Dividends and Distributions – This form shows any dividends earned during 2010 on any Class A Preferred stock you have with Ag Credit.

1099 PATR – Taxable Distributions Received from Cooperatives – This form shows the

December 2010, Ag Credit ACA | 19

amount of taxable patronage you received, either by check or notice, during the 2010 tax year. Keep in mind that any patronage refund and revolvement of allocated equities is at the discretion of the board of directors. The taxable patronage for 2010 includes the following

u2009 Cash Patronage distributed in April 2010.

u2004 Nonqualified Allocated Surplus distributed in September 2010.

Nonqualified allocated equity is taxable in the year it is distributed to you in cash.

uPlease note the 2005 Qualified Allocated Surplus payment distributed in September 2010 is not taxable. You paid taxes on this amount with your 2005 tax return.

Once you receive your tax statements through Account Access or by mail, please review them carefully for accuracy. If you find an error, please notify your local branch team right away. If we are notified in time, we are

able to make corrections and have new notices issued through the normal, automated process

MEMBER SUMMARY STATEMENTSStatements will be produced and mailed to each borrowing entity at the end of January 2011. The statement will be available online via Account Access in mid-January 2011. This is an informational statement. It is not sent to the IRS.

Your member summary statement will show beginning and ending loan balances, interest paid, fees or late charges paid, stock and allocated equity balances.

ACCOUNTACCESSAccountAccess is Ag Credit’s program that provides you with 24/7 on-line, internet access to your Ag Credit loans. AccountAccess provides you with the following benefits:

uQuicker access to your 2010 IRS informational tax forms and member summary statement.

uThe ability to request draws on your line of credit and make loan payments, day or night, from your home or business at your convenience.

If you’re not signed up for AccountAccess or have forgotten your password, contact your local branch team for assistance.

As you say “Goodbye” to the old year and “Hello” to the new one, remember to jot down your inventories and other information necessary to complete a balance sheet in preparation for the completion of the financial analysis of your business. If you need assistance with this process contact your Ag Credit account officer.

Finally, the Operation’s team members at the administrative office in Fostoria would like to “Thank You” for choosing to do business with Ag Credit. We wish you a blessed holiday season and joyous New Year. n

December 2010, Ag Credit ACA | 19

Industry News

Many agricultural producers who have sought loans have overheard loan officers discuss that you will be evaluated on the “Five C’s of Credit.” These include capacity of repayment, character of the borrower, conditions of the credit, collateral to back the loan, and capital or net worth. Another dimension of creditworthiness is emerging as agriculture becomes more interconnected with other segments of the domestic and global economy. Whether you are a lifestyle agricultural producer, traditional farmer or rancher, or operate a large complex business, the sixth C, cranium, will become more important not only for the sustainability of your business but for a balanced lifestyle.

First, an important component of the Sixth C is synergy management in business arrangements. This is one’s ability to find, develop, and coordinate business partners or associates who accentuate strengths and compliment or offset weaknesses. This usually requires an owner, manager, and management team with a clear cut vision, goals, and actions with fine-tuned evaluation metrics that evolve as economic game conditions change. The synergy in business arrangements and partners must be not only structured and formalized, but also flexible and fluid to proactively capitalize on changing internal and external business conditions.

A strong component of the Sixth C is whether a manager, owner, or business has taken an adverse event “punch” and bounced back. Many times the good years are the ones that create business problems, referred to as the “curse of prosperity.” Many successful sustainable businesses will redefine and focus in periods of adversity, which makes the business model even stronger in the future.

The cranium factor requires a borrower, producer, or manager to be able to handle an unexpected “black swan” or tail risk, which is much more prevalent in a global economic environment that can change overnight than the environment of the past. For example, wheat prices changed $2.51 per bushel in 27 days this past summer. The degree of financial leverage, shock absorbers in the form of liquidity and cash, the backup of equity, and the sensitivity test to profits

and cash flow must be in place to counter an unusual event or “black swan.” This can apply to the business’ and family’s financial picture. Are systems, strategies, and standard operating procedures in place for the various components of the business including production, risk management, marketing, operations, and exit strategies? Are these plans communicated and executed effectively through the proper channels?

Along with adversity management comes the other end of the spectrum, the aforementioned “curse of prosperity.” During profitable economic cycles, a windfall “slug” of cash can be large, often amounting to high six and seven figures. Has the individual had experience managing these profits well? Does the profit plan include disciplined growth, added efficiency, more effective results, and an improved bottom line? Is necessary working capital and, yes, cash, preserved to capitalize on business opportunities or handle a “black swan” event? Are profits channeled into excess family living expense or exuberant consumption, sometimes called “killer toys” or side show business ventures that are outside the expertise and scope of management? Disciplined profit mangers with stellar liquidity and cash flow management abilities will be a key to wealth accumulation and sustainability in the future.

Regardless of whether you are involved with a small lifestyle operation or the most complex agribusiness, managers who have a high “cranium factor” will increasingly have a written business plan that is executed, monitored, and evolved as business conditions change. A written business plan can be a road map to keep the team players on the correct route in the business journey. Research has found that having a written business plan has led to businesses earning four times more profits than those that “shoot from the hip.” A written business plan is not an option but a requirement in a domestic and global economic environment with surprises around every corner.

Drilling deeper, the cranium factor is all about being proactive in a changing economic and business environment. The astute manager of the Sixth C will consider all perspectives,

including those that both confirm and challenge beliefs and business and personal paradigms. Successful businesses include lenders and managers working side-by-side who are above average in many areas of business management without glaring weaknesses. They are strategic thinkers with reasonable emotional intelligence, which helps them work with people and seek to improve the individuals with which they come in contact.

Finally, the Sixth C is all about balance of the business, family, and lifestyle. Time management with defined priorities in each component is necessary in a high tech, 24-7 environment. A plan for both business and self-improvement is important to maintain the competitive edge as an agricultural knowledge worker, which is a vital part of the Sixth C of credit as you manage your business and lifestyle. n

David Kohl received his M.S. and Ph.D. degrees in Agricultural Economics from Cornell University. For 25 years, Kohl was Professor of Agricultural Finance and Small Business

Management and Entrepreneurship in the Department of Agricultural and Applied Economics at Virginia Tech, Blacksburg, Virginia. He was on special leave with the Royal Bank of Canada working on advanced initiatives for two years, and also assisted in the launch of the successful entrepreneurship program at Cornell University. Kohl is Professor Emeritus in the AAEC Department at Virginia Tech.

Kohl has traveled over 7 million miles throughout his professional career! He has conducted more than 5,000 workshops and seminars for agricultural groups such as bankers, Farm Credit, FSA, and regulators, as well as producer and agribusiness groups. He has published four books and over 1,000 articles on financial and business-related topics in journals, extension, and other popular publications. Kohl regularly writes for Ag Lender and Corn and Soybean Digest.

Cranium: The Sixth “C” of CreditBy: Dr. David M. Kohl

20 | December 2010, Ag Credit ACA

Establish a PriceWhen you buy a property, an appraisal can save you from paying more than market value. When you sell property, an appraisal can help you determine your asking price.

Tax PurposesWhen you give land to your children or to charity, you’ll need to document the value for tax purposes.

Business PlanningWhen incorporating or forming a partnership, it is important to know the value of your farm business.

Estate PlanningDuring a time of loss, or as part of a transition plan, an appraiser can provide an impartial determination of market value of real estate and assets.

Why is an Appraisal Important?

Meet our team

William (Bill) Eirich, ARA Senior AppraiserOttawa Branch419-523-6677 x1107Cell: [email protected]

Lisa Wickersham AppraiserMarion Branch740-387-2270 x1604Cell: [email protected]

Kurk ZieglerAppraiserNorwalk Branch419-663-4020 x2107Cell: [email protected]

Contact Ag Credit today for more details about our fee appraisal service.

www.agcredit.net

Agricultural Appraisal ExpertiseWe have the most experienced farm appraisers in Northern Ohio.

Our Three-Part Appraisal ProcessAg Credit determines market value by using three methods:

• sales comparison• cost approach• income approach

The results of all three methods will be incorporated into your final appraisal for the most accurate result.

More Than Real EstateAg Credit’s certified specialists are qualified to prepare appraisals for dairies, hog confinement operations, grain farms, and other specialty operations.

AffordabilityAt your request, Ag Credit will provide you with a fee estimate. Our competitive rates are based on the time required to inspect the property, research court records, analyze the data, and prepare the report.

Why Choose Ag Credit?

December 2010, Ag Credit ACA | 21

22 | December 2010, Ag Credit ACA

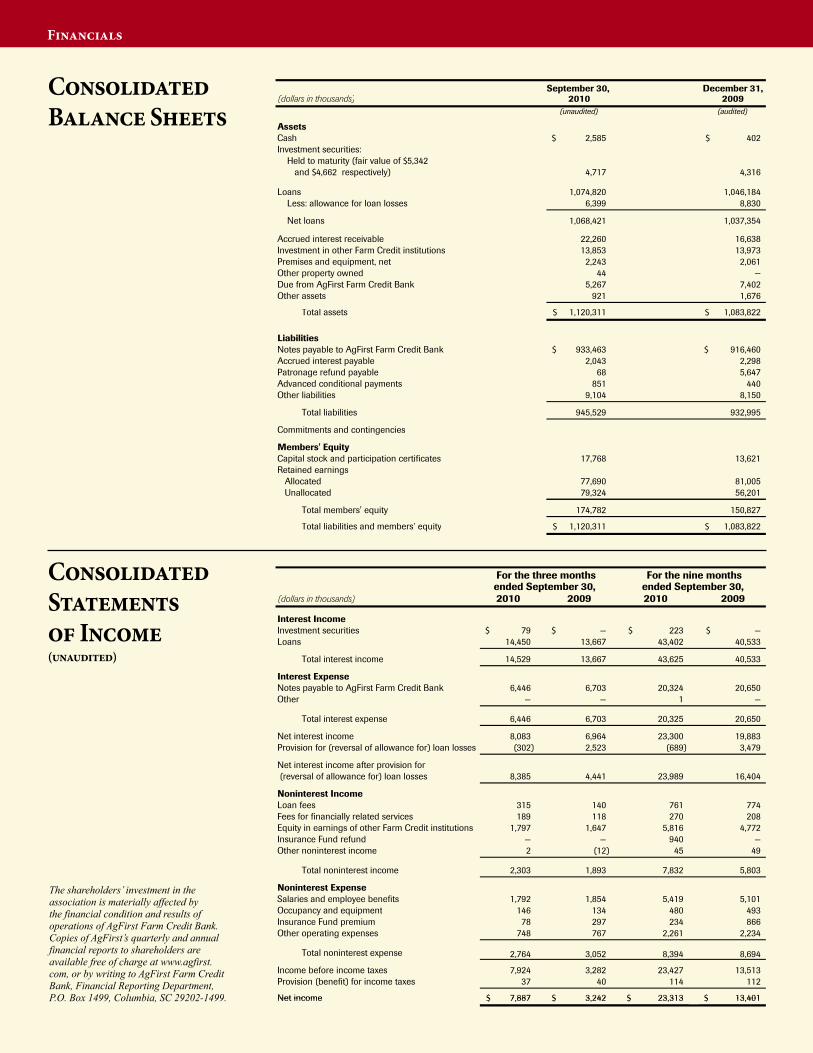

The shareholders’ investment in the association is materially affected by the financial condition and results of operations of AgFirst Farm Credit Bank. Copies of AgFirst’s quarterly and annual financial reports to shareholders are available free of charge at www.agfirst.com, or by writing to AgFirst Farm Credit Bank, Financial Reporting Department, P.O. Box 1499, Columbia, SC 29202-1499.

September 30, December 31,(dollars in thousands) 2010 2009

(unaudited) (audited)

AssetsCash 2,585$ 402$ Investment securities: Held to maturity (fair value of $5,342 and $4,662 respectively) 4,717 4,316

Loans 1,074,820 1,046,184 Less: allowance for loan losses 6,399 8,830

Net loans 1,068,421 1,037,354

Accrued interest receivable 22,260 16,638 Investment in other Farm Credit institutions 13,853 13,973 Premises and equipment, net 2,243 2,061 Other property owned 44 — Due from AgFirst Farm Credit Bank 5,267 7,402 Other assets 921 1,676

Total assets 1,120,311$ 1,083,822$

LiabilitiesNotes payable to AgFirst Farm Credit Bank 933,463$ 916,460$ Accrued interest payable 2,043 2,298 Patronage refund payable 68 5,647 Advanced conditional payments 851 440 Other liabilities 9,104 8,150

Total liabilities 945,529 932,995

Commitments and contingencies

Members' EquityCapital stock and participation certificates 17,768 13,621 Retained earnings Allocated 77,690 81,005 Unallocated 79,324 56,201

Ag Credit Agricultural Credit Association

Consolidated Balance Sheets

Total members' equity 174,782 150,827

Total liabilities and members' equity 1,120,311$ 1,083,822$

(dollars in thousands) 2010 2009 2010 2009

Interest IncomeInvestment securities 79$ —$ 223$ —$ Loans 14,450 13,667 43,402 40,533

Total interest income 14,529 13,667 43,625 40,533

Interest ExpenseNotes payable to AgFirst Farm Credit Bank 6,446 6,703 20,324 20,650 Other — — 1 —

Total interest expense 6,446 6,703 20,325 20,650

Net interest income 8,083 6,964 23,300 19,883 Provision for (reversal of allowance for) loan losses (302) 2,523 (689) 3,479

Net interest income after provision for (reversal of allowance for) loan losses 8,385 4,441 23,989 16,404

Noninterest IncomeLoan fees 315 140 761 774 Fees for financially related services 189 118 270 208 Equity in earnings of other Farm Credit institutions 1,797 1,647 5,816 4,772 Insurance Fund refund — — 940 — Other noninterest income 2 (12) 45 49

Total noninterest income 2,303 1,893 7,832 5,803

Noninterest ExpenseSalaries and employee benefits 1,792 1,854 5,419 5,101 Occupancy and equipment 146 134 480 493 Insurance Fund premium 78 297 234 866 Other operating expenses 748 767 2,261 2,234

Total noninterest expense 2,764 3,052 8,394 8,694

Income before income taxes 7,924 3,282 23,427 13,513 Provision (benefit) for income taxes 37 40 114 112

Net income 7 887$ 3 242$ 23 313$ 13 401$

ended September 30,

Consolidated Statements of Income (unaudited)

For the three months ended September 30,

For the nine months

Net income 7,887$ 3,242$ 23,313$ 13,401$

September 30, December 31,(dollars in thousands) 2010 2009

(unaudited) (audited)

AssetsCash 2,585$ 402$ Investment securities: Held to maturity (fair value of $5,342 and $4,662 respectively) 4,717 4,316

Loans 1,074,820 1,046,184 Less: allowance for loan losses 6,399 8,830

Net loans 1,068,421 1,037,354

Accrued interest receivable 22,260 16,638 Investment in other Farm Credit institutions 13,853 13,973 Premises and equipment, net 2,243 2,061 Other property owned 44 — Due from AgFirst Farm Credit Bank 5,267 7,402 Other assets 921 1,676

Total assets 1,120,311$ 1,083,822$

LiabilitiesNotes payable to AgFirst Farm Credit Bank 933,463$ 916,460$ Accrued interest payable 2,043 2,298 Patronage refund payable 68 5,647 Advanced conditional payments 851 440 Other liabilities 9,104 8,150

Total liabilities 945,529 932,995

Commitments and contingencies

Members' EquityCapital stock and participation certificates 17,768 13,621 Retained earnings Allocated 77,690 81,005 Unallocated 79,324 56,201

Ag Credit Agricultural Credit Association

Consolidated Balance Sheets

Total members' equity 174,782 150,827

Total liabilities and members' equity 1,120,311$ 1,083,822$

(dollars in thousands) 2010 2009 2010 2009

Interest IncomeInvestment securities 79$ —$ 223$ —$ Loans 14,450 13,667 43,402 40,533

Total interest income 14,529 13,667 43,625 40,533

Interest ExpenseNotes payable to AgFirst Farm Credit Bank 6,446 6,703 20,324 20,650 Other — — 1 —

Total interest expense 6,446 6,703 20,325 20,650

Net interest income 8,083 6,964 23,300 19,883 Provision for (reversal of allowance for) loan losses (302) 2,523 (689) 3,479

Net interest income after provision for (reversal of allowance for) loan losses 8,385 4,441 23,989 16,404

Noninterest IncomeLoan fees 315 140 761 774 Fees for financially related services 189 118 270 208 Equity in earnings of other Farm Credit institutions 1,797 1,647 5,816 4,772 Insurance Fund refund — — 940 — Other noninterest income 2 (12) 45 49

Total noninterest income 2,303 1,893 7,832 5,803

Noninterest ExpenseSalaries and employee benefits 1,792 1,854 5,419 5,101 Occupancy and equipment 146 134 480 493 Insurance Fund premium 78 297 234 866 Other operating expenses 748 767 2,261 2,234

Total noninterest expense 2,764 3,052 8,394 8,694

Income before income taxes 7,924 3,282 23,427 13,513 Provision (benefit) for income taxes 37 40 114 112

Net income 7 887$ 3 242$ 23 313$ 13 401$

ended September 30,

Consolidated Statements of Income (unaudited)

For the three months ended September 30,

For the nine months

Net income 7,887$ 3,242$ 23,313$ 13,401$

Financials

ConsolidatedBalance Sheets

Consolidated Statements of Income(unaudited)

By Connie Ruth, aka Agatha CreditNote: Agatha Credit is the nickname my late husband, Dan, bestowed upon me when I first started working at Ag Credit. He enjoyed the enthusiasm I had for my new job.

I am sitting at my computer having my first coffee of the day on a Saturday morning. It is cold outside and I hear the wind in the trees but I feel cozy because I have my little gas heater glowing beside me here in the dining room. It is one of those perfect little moments in time. Daydreaming, I glance up at the bookshelf and right at eye-level I see a book called, “The Great Short Works of Stephen Crane.” I jump to my feet and yell, “There you are!” My dog, Daisy, who has been sleeping at my feet, is so startled she jumps up and barks.

The Back StoryTwo weeks ago, my daughter, Jen,

called from college asking me to please send her a book she left at home after taking English Composition her freshman year. She also needed a pink notebook containing her collection of conjugated Spanish verbs from high school for her college class. She tells me, “Remember, Mom? We left this stuff in the upstairs hall after we painted my room.” I take a deep breath. Yes, I remember. Last summer we painted her room and a pile of books and notebooks never got put back in her now-pristine space.

A tinge of guilt comes over me as I also remember my recent cleaning binge. After months of walking around the pile of clutter, I finally decided to take matters into my own hands. I pitched the left-over Trapper-Keepers and notebooks from years gone by. There is a slight chance I might have stashed something in the already-overflowing bookcase but I recall thinking, “Why would anyone want these old papers?” (I didn’t know Ms. Myers had told her high school Spanish students, as they spent weeks conjugating verbs, “College

students will someday offer to pay you for all these lists!”) I should have given Jen the opportunity to decide what to keep and what to throw away. But in my defense, hadn’t the stuff been sitting there for months?

I hung up the phone and searched the hall and bookcase pretty sure I wasn’t going to find Stephen Crane stories or conjugated verbs. Then I ransacked the entire upstairs. After looking in every bookcase and under every bed and in every closet I finally decided the pink notebook had probably been tossed in the trash and the book must have been given to Theresa for the latest garage sale.

Before calling Jen and admitting defeat I did what every fast-thinking mother would do. I found the exact 1968 edition paperback Stephen Crane book on E-bay for the bargain buy-it-now price of $2 and overnight shipped it to her for an additional $23.

Instead of feeling bad about spending $25 I actually felt better—crazy, but spending the money eased my conscience somehow. Jen was bummed about the lost notebook but agreed she should have returned the things she wanted to keep back to her room after the painting project.

Now, as I find the missing book, I lament, “Why can’t I have an organized house, office and car?” I have been trying to toss out clutter instead of letting it get out of hand but I have several obstacles to leading an organized life.

Obstacle #1: I am a nester, gatherer, collector, and saver.

Obstacle #2: There are certain times I love to clean and organize but my life priorities tend to be social. Cleaning and organizing tend to be solitary tasks.

Obstacle #3: I am sentimental about most everything (except piles of old notebooks, school books, catalogs and magazines.)

Obstacle/Excuse #4: Life is really busy for all of us.

Everyone likes to be organized. It’s wonderful to gaze at a fresh kitchen shelf where all the Tupperware and matching lids are neatly stacked. I even invested in a divider for my sock drawer so each pair of socks has its own little home. The same goes for my office. I have cute cardboard bins for all my papers with piles of papers next to and in front of as well as inside the bins. I want to keep my office neat but things just pile up. As my stacks of paper grow, I envy my young co-workers who don’t feel the need to print out copies of all their emails for future reference and who do not need to make copious notes on Post-It pads because they can remember long lists of instructions without writing anything down. Working in an organized office is heavenly. I just wish I could make it last longer.

All of us are busy—especially during the holidays. But, even during the holidays many people manage to lead organized lives.

I decide not to beat myself up any further. Jen is over losing the notebook. The other book is replaced. We were both at fault. It’s over and done! I need to get on with my day so I toss the Stephen Crane book in a bag marked—Garage Sale. Even though I am not naturally organized I will just keep on trying.

It’s almost noon! I’ve wasted enough time thinking about my lack of organization. I need to do something productive. I will get out the Christmas decorations and make some new bows for the Christmas garlands. Now, where did I put the spool of red ribbon I got half-price after Christmas last year? I know it’s around here somewhere…

Enjoy the holidays with the ones you love best. Merry Christmas! n

Agatha

Lifestyle

Finding Things

October 2010, Ag Credit ACA | 23

610 W. Lytle StreetFostoria, OH 44830

Address Service Requested.

PRSRT STD US POSTAGE

PAIDCOLUMBIA SCPERMIT 1160

Internet SecurityBy Allan Campbell

One Internet site with a wealth of information on safely using the Internet is the National Cyber Security Alliance’s StaySafeOnline.org site. Here are a few do’s and don’ts you might find helpful when using the Internet for your household and farm operations.

Be alert when on the Internet. Being an alert and aware Internet user is your first line of defense. Don’t click on suspicious links or open files you weren’t expecting. Stay away from any site that looks less than completely professional. You wouldn’t walk in an unsafe area in the “real” world so don’t do it on the Internet. Beware of sites offering free software or file-sharing since you don’t know what you may really be downloading from these sites.

Keep your money safe. It is a good practice to review and reconcile banking and credit card statements monthly especially if you make purchases on the

Internet. Consider asking your bank for a separate credit card with a low credit limit and use this card exclusively for all online accounts and shopping.

Keep your system safe. Install operating system and other software updates when available. Don’t ignore the automatic prompts usually located in the lower right corner of your screen. Data thieves take advantage of the fact many computers are not kept up-to-date with the latest security patches.

Keep your data safe. Be sure you have a good backup. StaySafeOnline.org describes various effective ways to backup your data. Solutions include Internet backup solutions, external USB hard drives and network-attached storage. One will work for you. If you haven’t experienced a system crash it is only a matter of time. Your files (accounting data or family pictures) are important to you so it is important to back them up.

Keep your kids safe. StaySafeOnline.org recommends setting up home computers in open areas so parents can easily watch what their kids are doing online. Sit down with your children and discuss the risks they face online. Consider installing software to limit access to risky or unacceptable sites and monitor chat conversations, Web sites visited and other online activity.

Keep your accounts safe. Use strong passwords. Change your passwords regularly and use a different password for each account. Avoid easily guessed passwords. Try to use a password containing as many characters as the site permits. A phrase will be easier to remember than a long grouping of random letters.

The Internet brings an incredible amount of added convenience to all our lives but we need to remember to be aware and be safe. n