Embed Size (px)

Citation preview

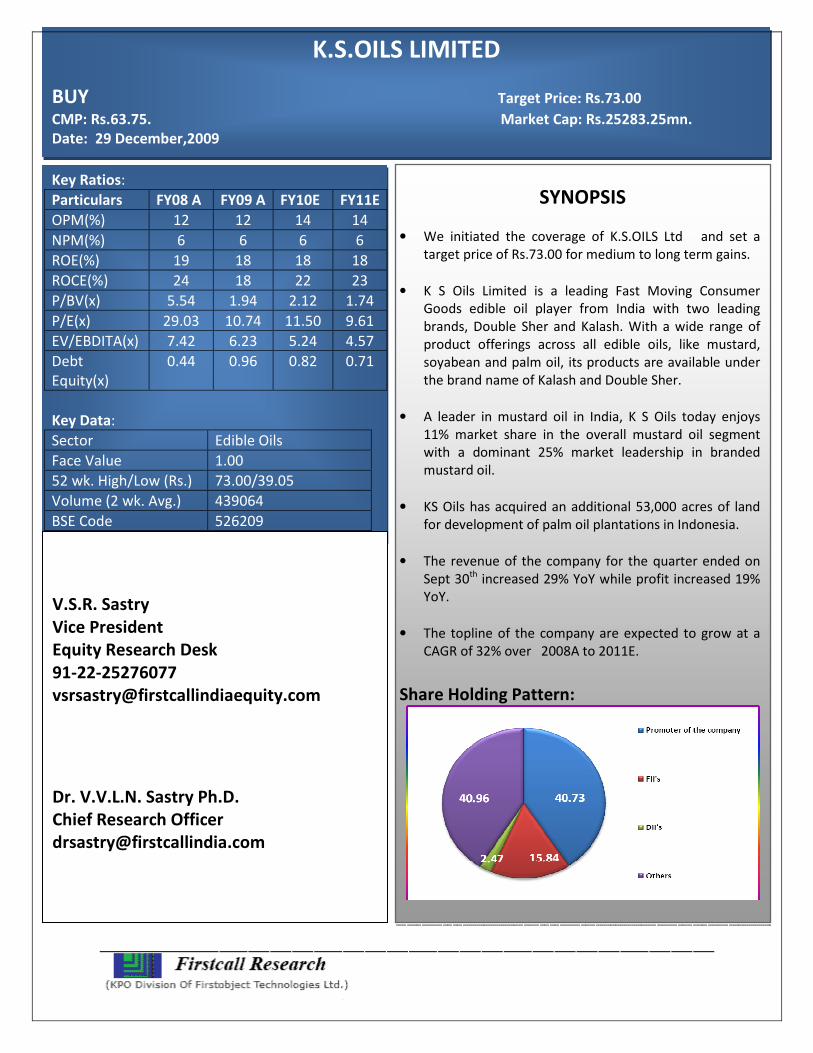

K.S.OILS LIMITED

BUY Target Price: Rs.73.00

CMP: Rs.63.75. Market Cap: Rs.25283.25mn.

Date: 29 December,2009

Key Ratios:

Particulars FY08 A FY09 A FY10E FY11E

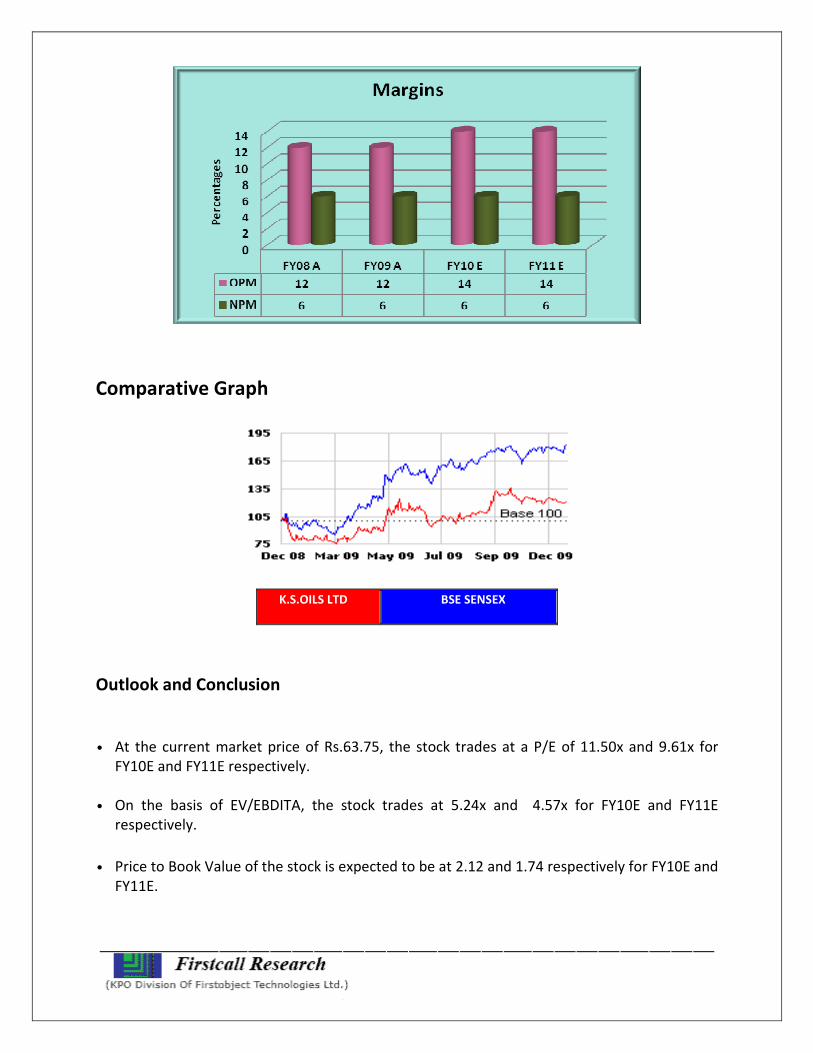

OPM(%) 12 12 14 14

NPM(%) 6 6 6 6

ROE(%) 19 18 18 18

ROCE(%) 24 18 22 23

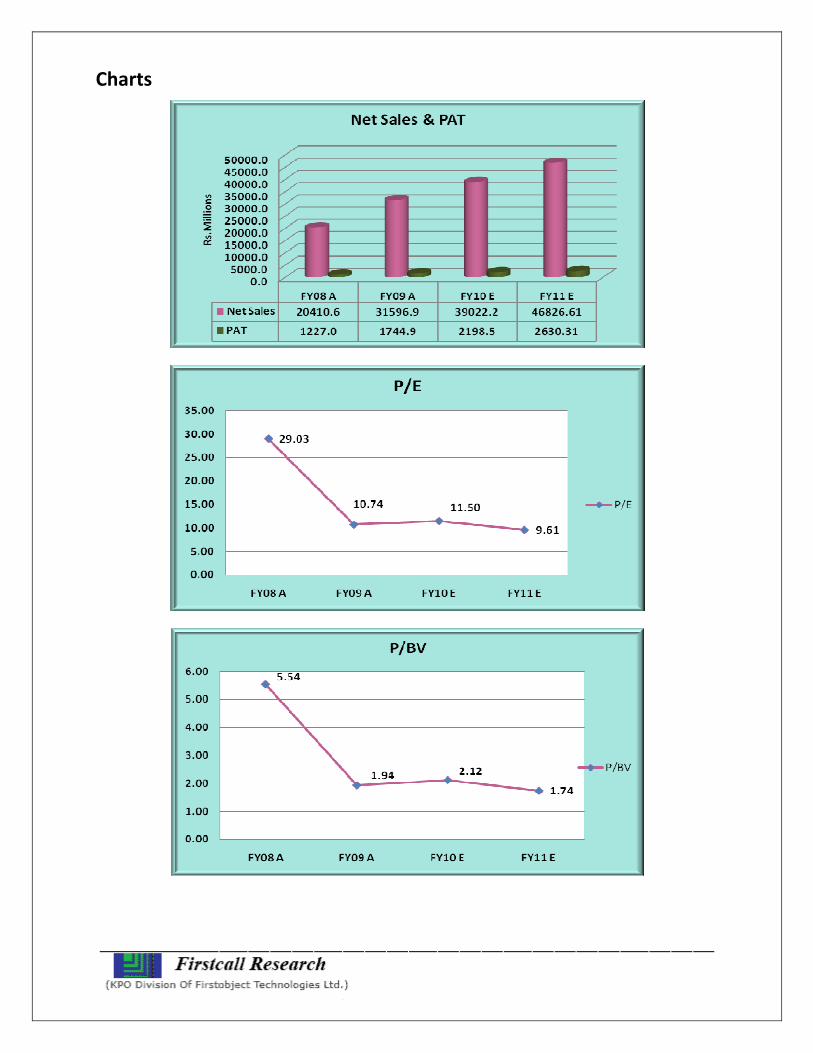

P/BV(x) 5.54 1.94 2.12 1.74

P/E(x) 29.03 10.74 11.50 9.61

EV/EBDITA(x) 7.42 6.23 5.24 4.57

Debt

Equity(x)

0.44 0.96 0.82 0.71

Key Data:

Sector Edible Oils

Face Value 1.00

52 wk. High/Low (Rs.) 73.00/39.05

Volume (2 wk. Avg.) 439064

BSE Code 526209

SYNOPSIS

• We initiated the coverage of K.S.OILS Ltd and set a

target price of Rs.73.00 for medium to long term gains.

• K S Oils Limited is a leading Fast Moving Consumer

Goods edible oil player from India with two leading

brands, Double Sher and Kalash. With a wide range of

product offerings across all edible oils, like mustard,

soyabean and palm oil, its products are available under

the brand name of Kalash and Double Sher.

• A leader in mustard oil in India, K S Oils today enjoys

11% market share in the overall mustard oil segment

with a dominant 25% market leadership in branded

mustard oil.

• KS Oils has acquired an additional 53,000 acres of land

for development of palm oil plantations in Indonesia.

• The revenue of the company for the quarter ended on

Sept 30th increased 29% YoY while profit increased 19%

YoY.

• The topline of the company are expected to grow at a

CAGR of 32% over 2008A to 2011E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

Table of Content

Investment Highlights ................................................................................................................................... 3

Peer Group Comparison ................................................................................................................................ 3

Financials ....................................................................................................................................................... 8

Charts .......................................................................................................................................................... 11

Outlook and Conclusion .............................................................................................................................. 12

Industry Overview ....................................................................................................................................... 13

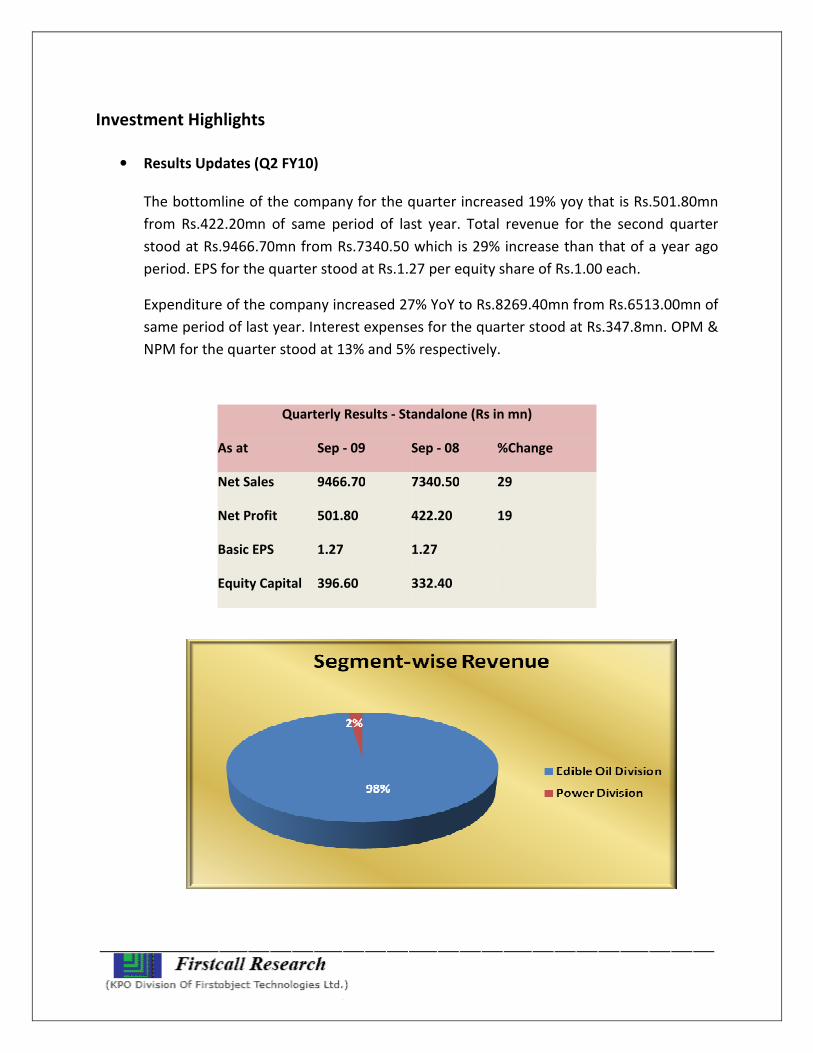

Investment Highlights

• Results Updates (Q2 FY10)

The bottomline of the company for the quarter increased 19% yoy that is Rs.501.80mn

from Rs.422.20mn of same period of last year. Total revenue for the second quarter

stood at Rs.9466.70mn from Rs.7340.50 which is 29% increase than that of a year ago

period. EPS for the quarter stood at Rs.1.27 per equity share of Rs.1.00 each.

Expenditure of the company increased 27% YoY to Rs.8269.40mn from Rs.6513.00mn of

same period of last year. Interest expenses for the quarter stood at Rs.347.8mn. OPM &

NPM for the quarter stood at 13% and 5% respectively.

Quarterly Results - Standalone (Rs in mn)

As at Sep - 09 Sep - 08 %Change

Net Sales 9466.70 7340.50 29

Net Profit 501.80 422.20 19

Basic EPS 1.27 1.27

Equity Capital 396.60 332.40

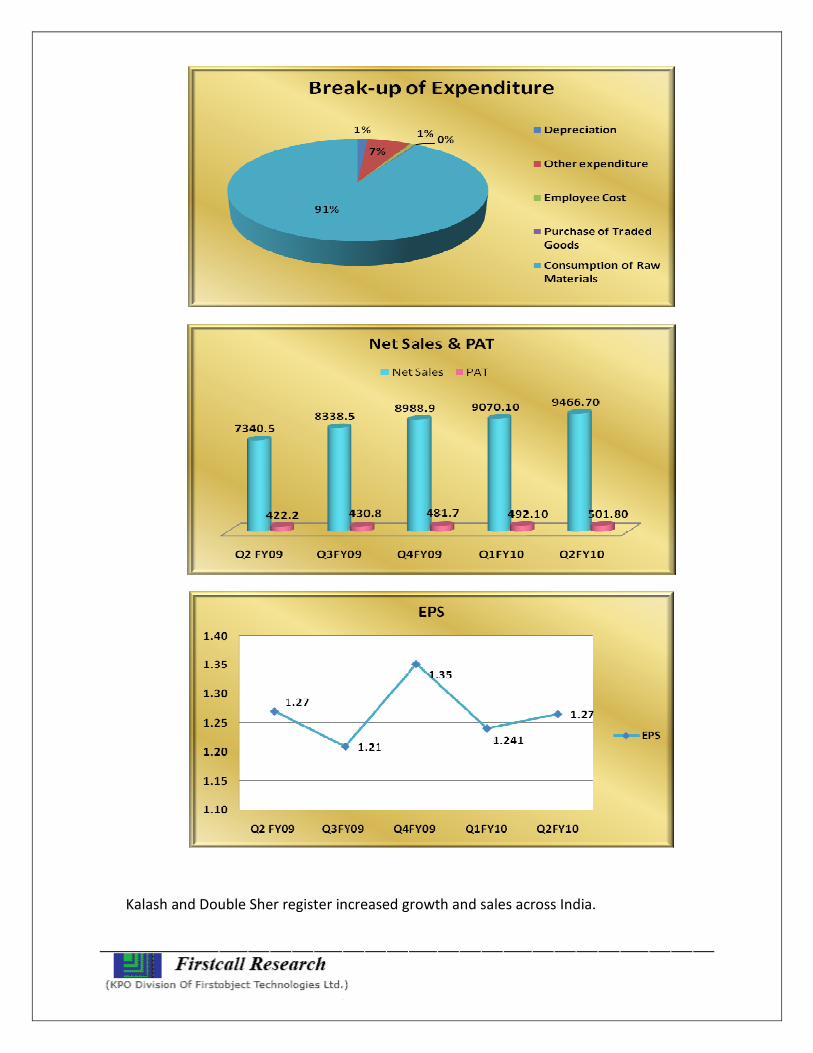

Kalash and Double Sher register increased growth and sales across India.

The company added 2 C&F agents, 97 distributors, launched its products in over 100 new

towns during the quarter; taking the total number to over 1,133 distributors in 1,200 cities

covering 375 districts all over India, reaching out to over 1,70,000 retailers.

• KS Oils acquires additional palm plantation land in Indonesia

KS Oils has acquired an additional 53,000 acres of land for development of palm oil

plantations in Indonesia. This land has been purchased through its Singapore-based wholly-

owned subsidiary, K S Natural Resources.

The acquisition will be funded through internal accruals and debt at subsidiary level.

Further, the company is expected to spend about Rs 380 crore on this project over the next

three years time.

• KS Oil bags various honours

KS Oils has bagged various honours such as 'Highest processor of rapeseed oilcake for oil

for year 2008-09' and '2nd Highest exporter of rapeseed extraction (De-oilcake) for oil for

year 2008-09” at Solvent Extractors Association of India's award

Further, it has also received the award 'Kalash" -- as the fastest growing Edible Oil Brand in

India for oil for year 2008-09' at Globoil India Award.

• KS Oils raises $12.34mn via GDR issue

KS Oils has raised little over $12.34 million worth of fresh funds via global depository

receipts (GDR). The board of the company has approved allotment of 1,24,09,520 equity

shares of Rs 1 each underlying the GDRs issue and raised fund of $12,347,472.40. The

funds raised are expected to be utilized to do capacity expansion at Haldia refinery and on

palm plantations in Indonesia.

Company Profile

K S Oils is a leading integrated edible oil company and is the trusted name behind renowned

brands like Kalash, Double Sher, K S Gold, among others. The company’s consumer brands and

products in mustard oil, soybean oil and palm oil are a household name with Indian consumers

who use these oils regularly as a healthy cooking medium. A leader in mustard oil in India, K S

Oils today enjoys 11% market share in the overall mustard oil segment with a dominant 25%

market leadership in branded mustard oil.

K S Oils is an Indian company with international footprint and global ambitions; a leader in the

edible oil market in India, it has generated a turnover of over Rs. 2000 crores during the

financial year 2007-08. The company has in the recent past successfully undertaken the growth

strategy of capacity expansion, green field projects and acquisitions, thus creating an

unchallenged competitive advantage.

K S Oils is a strong family of near to 3000 employees spread over its 5 manufacturing plants,

marketing offices and plantations in India, Malaysia, Indonesia and Singapore. With the

company registering explosive growth, opportunity for fresh and experienced talent is immense

with Indian and overseas opportunities.

As one of India’s leading companies in the edible oil sector, K S Oils has deep understanding of

agri-commodity and farmer community issues. Today, K S Oils is part of the Indian growth story

– using the country’s inherent strength in agricultural resources and best managerial talent to

serve millions of consumers in India and abroad. Creating an Indian MNC with international

footprint of knowledge, leadership and value for its stakeholders across the globe!

Subsidiaries

• K S Natural Resources Pte. Ltd.

K S Natural Resources Pte. Ltd. (KSNR) Singapore is one of Asia's fastest growing agri-

focused conglomerates, with diverse interests in agri-commodity trading, export and

import of edible oils, oil palm plantation cultivations. It has interests in value added areas

like oil mills, logistics, port facilities and ocean carriers. The Singapore headquartered

company, KSNR, is a 100% subsidiary of K S Oils Limited, India's leading edible oil FMCG

player.

Company Products

Over the past two decades, K S Oils has built, nurtured and continually improved upon its

various brands of edible oils. As a leading FMCG player in India and a leader in the mustard oil

segment, K S brands dominate the market especially in East and North East India.

Brands

Mustard Oil

o Kalash

o Double Sher

Refined Oil

o K S Soya

o K S Gold

Vanaspati

o K S Gold Plus

Manufacturing Process

K S Oils has all its manufacturing plants located in the rich mustard growing belt of Madhya

Pradesh and Rajasthan in India. The mother plant is situated in Morena and is one of the best

state-of-the-art integrated manufacturing facilities in the country. This unit situated in the

midst of the Mustard growing region of Madhya Pradesh is a state-of-the-art plant that houses

all facilities under one roof. Equipped with Kohllus and expellers to crush the oil seeds,

refineries to refine the crude oil, solvent extractor, vanaspati plant and storage tanks; what

makes it an integrated plant is its packaging department.

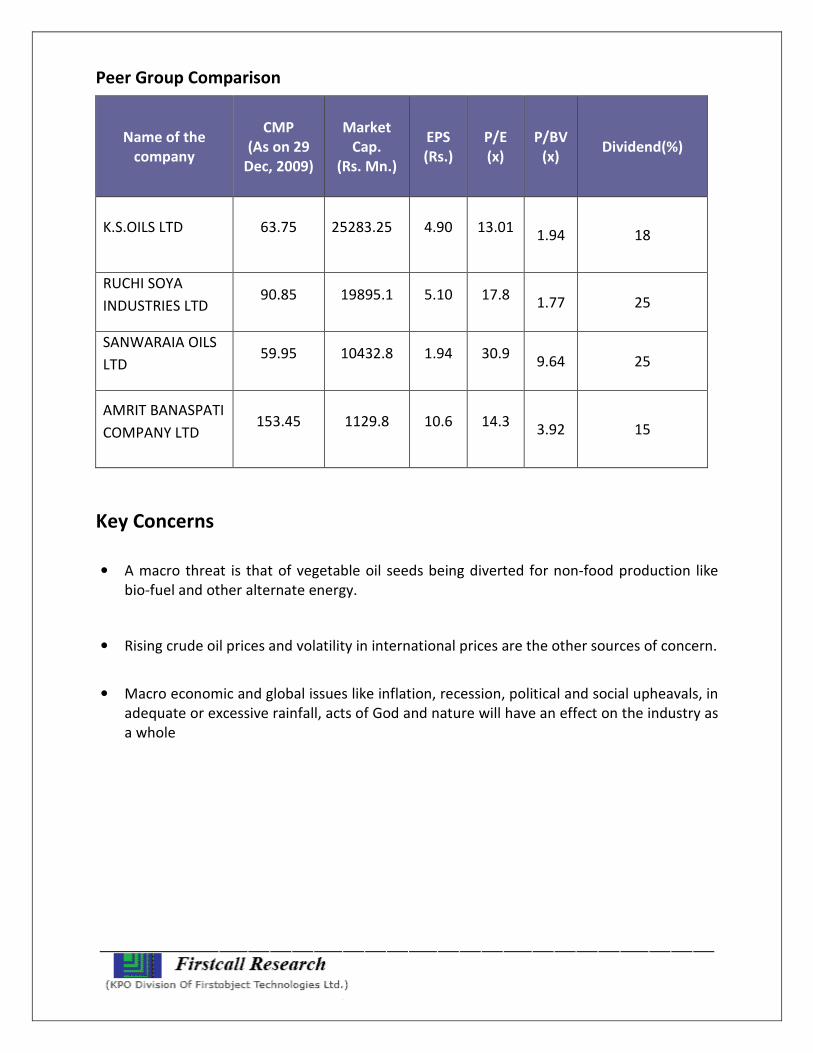

Peer Group Comparison

Name of the

company

CMP

(As on 29

Dec, 2009)

Market

Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E

(x)

P/BV

(x) Dividend(%)

K.S.OILS LTD 63.75 25283.25 4.90 13.01 1.94 18

RUCHI SOYA

INDUSTRIES LTD 90.85 19895.1 5.10 17.8

1.77 25

SANWARAIA OILS

LTD 59.95 10432.8 1.94 30.9

9.64 25

AMRIT BANASPATI

COMPANY LTD 153.45 1129.8 10.6 14.3

3.92 15

Key Concerns

• A macro threat is that of vegetable oil seeds being diverted for non-food production like

bio-fuel and other alternate energy.

• Rising crude oil prices and volatility in international prices are the other sources of concern.

• Macro economic and global issues like inflation, recession, political and social upheavals, in

adequate or excessive rainfall, acts of God and nature will have an effect on the industry as

a whole

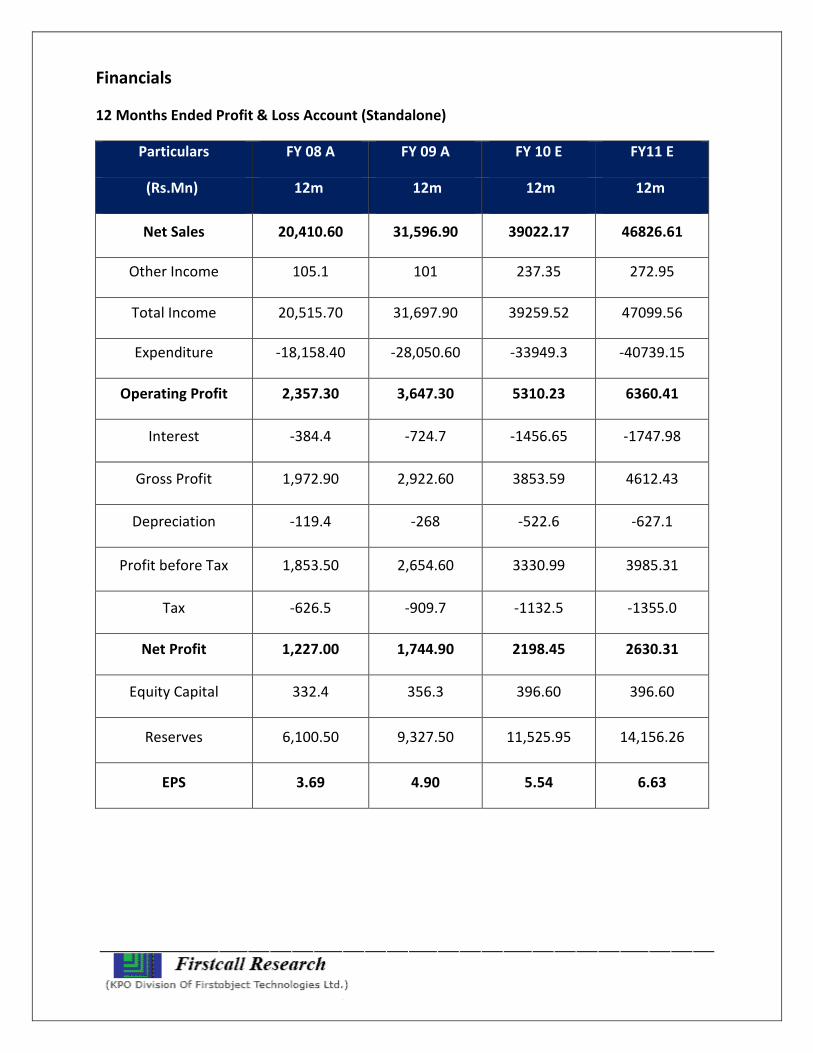

Financials

12 Months Ended Profit & Loss Account (Standalone)

Particulars FY 08 A FY 09 A FY 10 E FY11 E

(Rs.Mn) 12m 12m 12m 12m

Net Sales 20,410.60 31,596.90 39022.17 46826.61

Other Income 105.1 101 237.35 272.95

Total Income 20,515.70 31,697.90 39259.52 47099.56

Expenditure -18,158.40 -28,050.60 -33949.3 -40739.15

Operating Profit 2,357.30 3,647.30 5310.23 6360.41

Interest -384.4 -724.7 -1456.65 -1747.98

Gross Profit 1,972.90 2,922.60 3853.59 4612.43

Depreciation -119.4 -268 -522.6 -627.1

Profit before Tax 1,853.50 2,654.60 3330.99 3985.31

Tax -626.5 -909.7 -1132.5 -1355.0

Net Profit 1,227.00 1,744.90 2198.45 2630.31

Equity Capital 332.4 356.3 396.60 396.60

Reserves 6,100.50 9,327.50 11,525.95 14,156.26

EPS 3.69 4.90 5.54 6.63

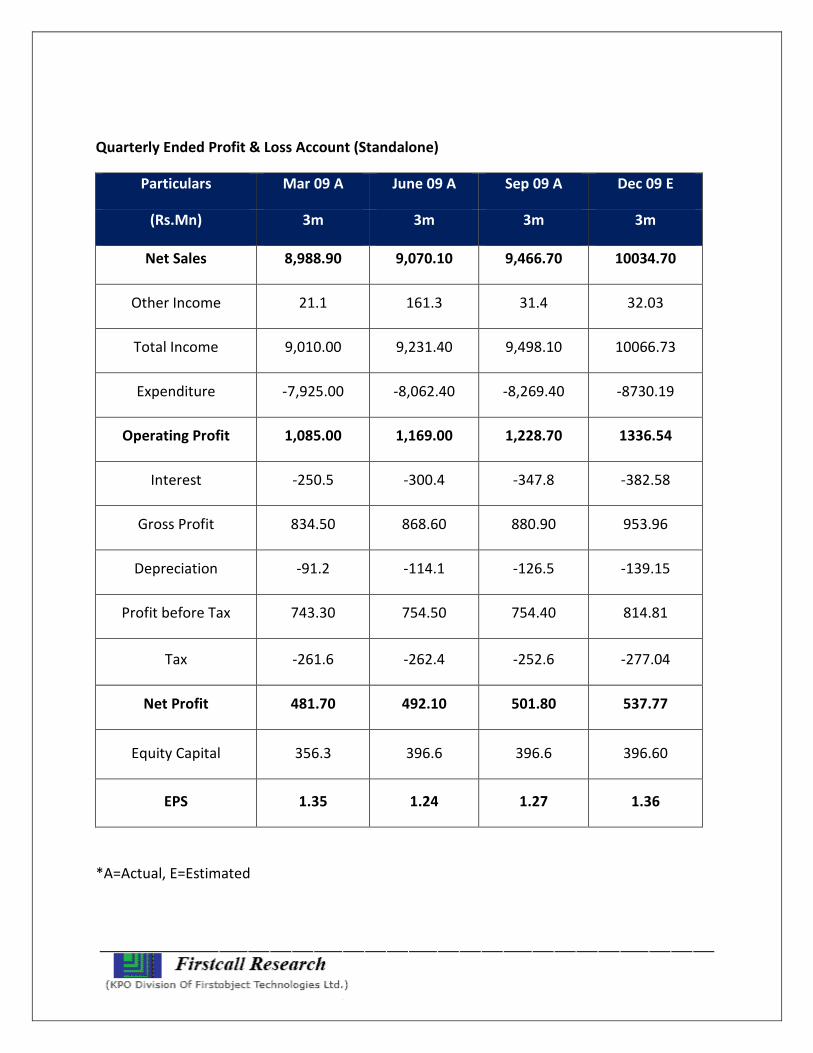

Quarterly Ended Profit & Loss Account (Standalone)

Particulars Mar 09 A June 09 A Sep 09 A Dec 09 E

(Rs.Mn) 3m 3m 3m 3m

Net Sales 8,988.90 9,070.10 9,466.70 10034.70

Other Income 21.1 161.3 31.4 32.03

Total Income 9,010.00 9,231.40 9,498.10 10066.73

Expenditure -7,925.00 -8,062.40 -8,269.40 -8730.19

Operating Profit 1,085.00 1,169.00 1,228.70 1336.54

Interest -250.5 -300.4 -347.8 -382.58

Gross Profit 834.50 868.60 880.90 953.96

Depreciation -91.2 -114.1 -126.5 -139.15

Profit before Tax 743.30 754.50 754.40 814.81

Tax -261.6 -262.4 -252.6 -277.04

Net Profit 481.70 492.10 501.80 537.77

Equity Capital 356.3 396.6 396.6 396.60

EPS 1.35 1.24 1.27 1.36

*A=Actual, E=Estimated

Charts

Comparative Graph

Outlook and Conclusion

• At the current market price of Rs.63.75, the stock trades at a P/E of 11.50x and 9.61x for

FY10E and FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 5.24x and 4.57x for FY10E and FY11E

respectively.

• Price to Book Value of the stock is expected to be at 2.12 and 1.74 respectively for FY10E and

FY11E.

K.S.OILS LTD BSE SENSEX

• EPS of the company for the earnings of FY10E and FY11E are expected to be at Rs.5.54 and

Rs.6.63 respectively.

• The Net sales of the company are expected to grow at a CAGR of 32% over 2008 to 2011E.

• Kalash and Double Sher register increased growth and sales across India. The company

added 2 C&F agents, 97 distributors, launched its products in over 100 new towns during the

quarter; taking the total number to over 1,133 distributors in 1,200 cities covering 375

districts all over India, reaching out to over 1,70,000 retailers.

• KS Oils has acquired an additional 53,000 acres of land for development of palm oil

plantations in Indonesia. This land has been purchased through its Singapore-based wholly-

owned subsidiary, K S Natural Resources.

• We expect that the company will keep its growth story in the coming quarters also. We

recommend ‘BUY’ in this particular scrip with a target price of Rs.73.00. for Medium to Long

Term Gains.

Industry Overview

India is one of the largest producers of oilseeds in the world. The oilseeds area and output is

concentrated in Central and southern parts of India, mainly in Madhya Pradesh, Gujarat,

Rajasthan, Andhra Pradesh and Karnataka. The nine major oilseeds cultivated in India are

groundnut, mustard/rapeseed, sesame, safflower, linseed, niger seed, castorseed, soyabean

and sunflower. Coconut is the most important source of edible oil amongst plantation crops,

while in non-conventional oils, rice bran oil and cottonseed oil are the most important.

Groundnut, soyabean and mustard together contribute about 85 percent of the country’s soil

seeds production.

Oilseeds and edible oils are two of the most sensitive essential commodities. India is one of the

largest producers of oilseeds in the world and this sector occupies an important position in the

agricultural economy and accounting for the estimated production of 28.21 million tonnes of

nine cultivated oilseeds during the year 2007-08. India contributes about 6-7% of the world

oilseeds production. Export of oilmeals, oilseeds and minor oils has increased from 5.06

million Tones in the financial year 2005-06 to 7.3 million tons in the financial year 2006-07. In

terms of value, realization has gone up from Rs. 5514 crores to Rs.7997 crores. India accounted

for about 6.4% of world oilmeal export.

Types of Oils commonly in use in India

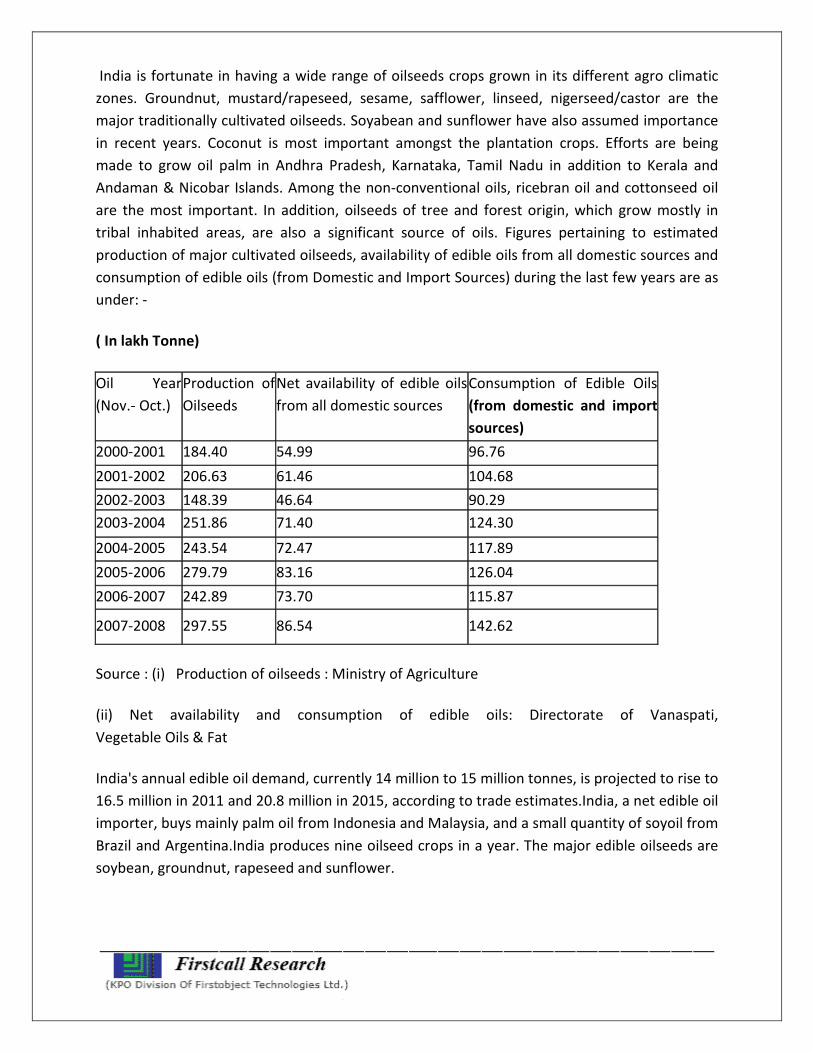

India is fortunate in having a wide range of oilseeds crops grown in its different agro climatic

zones. Groundnut, mustard/rapeseed, sesame, safflower, linseed, nigerseed/castor are the

major traditionally cultivated oilseeds. Soyabean and sunflower have also assumed importance

in recent years. Coconut is most important amongst the plantation crops. Efforts are being

made to grow oil palm in Andhra Pradesh, Karnataka, Tamil Nadu in addition to Kerala and

Andaman & Nicobar Islands. Among the non-conventional oils, ricebran oil and cottonseed oil

are the most important. In addition, oilseeds of tree and forest origin, which grow mostly in

tribal inhabited areas, are also a significant source of oils. Figures pertaining to estimated

production of major cultivated oilseeds, availability of edible oils from all domestic sources and

consumption of edible oils (from Domestic and Import Sources) during the last few years are as

under: -

( In lakh Tonne)

Oil Year

(Nov.- Oct.)

Production of

Oilseeds

Net availability of edible oils

from all domestic sources

Consumption of Edible Oils

(from domestic and import

sources)

2000-2001 184.40 54.99 96.76

2001-2002 206.63 61.46 104.68

2002-2003 148.39 46.64 90.29

2003-2004 251.86 71.40 124.30

2004-2005 243.54 72.47 117.89

2005-2006 279.79 83.16 126.04

2006-2007 242.89 73.70 115.87

2007-2008 297.55 86.54 142.62

Source : (i) Production of oilseeds : Ministry of Agriculture

(ii) Net availability and consumption of edible oils: Directorate of Vanaspati,

Vegetable Oils & Fat

India's annual edible oil demand, currently 14 million to 15 million tonnes, is projected to rise to

16.5 million in 2011 and 20.8 million in 2015, according to trade estimates.India, a net edible oil

importer, buys mainly palm oil from Indonesia and Malaysia, and a small quantity of soyoil from

Brazil and Argentina.India produces nine oilseed crops in a year. The major edible oilseeds are

soybean, groundnut, rapeseed and sunflower.

India grows the oilseed crops over two seasons.Soybean is the main summer sown crop, while

rapeseed, with the highest oil yield content, is the main winter season crop.In the 2008/09 crop

year, India produced 7.4 million tonnes of rapeseed and 9.9 million tonnes of soybean.

In the crop year to June 2009, total oilseed output has fallen 5.4 percent to 28.2 million

tonnes.India's vegetable oil imports, comprising edible oils, hydrogenated fats and non-edible

oils, hit an all-time high of 8.7 million tonnes in 2008/09, up 38 percent from the record imports

of 6.3 million tonnes in 2007-08.

Consumption Pattern of Edible Oils in India

India is a vast country and inhabitants of several of its regions have developed specific

preference for certain oils largely depending upon the oils available in the region. For example,

people in the South and West prefer groundnut oil while those in the East and North use

mustard/rapeseed oil. Likewise several pockets in the South have a preference for coconut and

sesame oil. Inhabitants of northern plain are basically hard fat consumers and therefore,

prefer Vanaspati, a term used to denote a partially hydrogenated edible oil mixture. Vanaspati

has an important role in our edible oil economy. Its production is about 1.2 million tonnes

annually. It has around 10% share of the edible oil market. It has the ability to absorb a

heterogeneous variety of oils, which do not generally find direct marketing opportunities

because of consumers’ preference for traditional oils such as groundnut oil, mustard oil,

sesame oil etc. For example, newer oils like soyabean, sunflower, ricebran and cottonseed and

oils from oilseeds of tree and forest origin had found their way to the edible pool largely

through vanaspati route. Of late, things have changed. Through technological means such as

refining, bleaching and de-odouraisation, all oils have been rendered practically colourless,

odourless and tasteless and, therefore, have become easily interchangeable in the kitchen.

Newer oils which were not known before have entered the kitchen, like those of cottonseed,

sunflower, palm oil or its liquid fraction (palmolein), soyabean and ricebran. These tend to

have a strong and distinctive taste preferred by most traditional customers. The share of raw

oil, refined oil and vanaspati in the total edible oil market is estimated at 35%, 55% and 10%

respectively.

Major Features of Edible Oil Economy

There are two major features, which have very significantly contributed to the development of

this sector. One was the setting up of the Technology Mission on Oilseeds in 1986. This gave a

thrust to Government's efforts for augmenting the production of oilseeds. This is evident by the

very impressive increase in the production of oilseeds from about 11.3 million tonnes in 1986-

87 to 24.8 million tonnes in 1998-99. There was some setback in 1999-2000 because of the un-

seasonal rain followed by inclement weather. The production of oilseeds declined to 20.7

million tonnes in 1999-2000. However, the oilseeds production went up to 27.98 million tones

in 2005-06 and was 24.29 million tonnes during 2006-07 oil year. As per the 3rd advance

estimate by Ministry of Agriculture dated 22.4.08 the production of nine major oilseeds is

estimated to be about 28.21 million tonnes during 2007-08. The other dominant feature which

has had significant impact on the present status of edible oilseeds/oil industry has been the

programme of liberalisation under which the Government's economic policy allowing greater

freedom to the open market and encourages healthy competition and self regulation rather

than protection and control. Controls and regulations have been relaxed resulting in a highly

competitive market dominated by both domestic and multinational players.

____________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but we do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking & Financial Services

B. Prathap IT

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods; Real & Infra

D.Asha Kiran Kumar Auto

E. Swethalatha Oil & Gas

A.Rajesh FMCG

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,TakeoverOffers, Offer for Sale and Buy

Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,Placement of Equity / Debt with

multilateral organizations, Short Term Funds Management Debt & Equity, Working Capital Limits, Equity &

DebtSyndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and cross-border), divestitures, spin-offs,

valuation of business, corporate restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising of capital through FCCBs, GDRs,

ADRs and listing of the same on International Stock Exchanges namely AIMs, Luxembourg, Singapore Stock

Exchanges and other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com