Embed Size (px)

Citation preview

Korea Western Power Ratings Presentation

[June 2014]

Confidential Presentation

Table of Contents Agenda

1. Company Overview

2. Industry & Regulatory Update

3. Operation Overview

4. Financial Management

5. Financial Forecast

Company Overview

Korea Western Power (KOWEPO) has maintained a strong credit profile

Company Overview

Strong Credit Profile

Cancelled privatization plans for Gencos

Market-oriented public enterprise

Application of the cost-reflecting pricing

mechanism

Increasing Capacity Factor

Expanding Capacity Factor with 75.5% in

1Q2014

Long-term and medium-term raw material

contracts

Continuous cash flows from operations

- EBITDA: KRW196bn (1Q 2014)

Balanced and flexible debt portfolio : Well-

diversified maturity profile

Strong interest coverage (EBITDA / Net

Interest Expense: 5.80x)

Constantly growing power consumption

11.2% of the sales volume share for domestic

power market in 1Q2014

Strengthening competitiveness through

domestic & overseas investment

Solid Financial Profile

Industry Dynamics & Market

Position

Supportive Regulatory Environment

Cost-Effective Operations

4

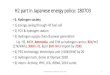

KOWEPO has established sophisticated power generating facilities in Korea

Company Overview

One of the Most Important Gencos in Korea

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Coal B.C. Oil LNG

Taean T/P

(4,000MW)

Pyeongtaek T/P

(1,400MW)

4,000MW

Seoincheon C/C

(1,800MW)

Pyeongtaek

C/C (480MW)

Gunsan

C/C (718.4MW)

3,509.3MW Coal

LNG BC Oil

1,400MW Taean

Pyeongtaek

Gunsan

Seoincheon

Seoul and Gyeonggi Metropolitan Area

Samrangjin

Others: Taean, Gunsan,

Samryangjin, Sejong

Solar, Taean Hydro,

Youngam Solar

(510.9 MW)

Metropolitan Area

Power Plant Region

Sejong City

Hydro

Solar

Generation Capacity by Type of Fuel Location of Plant Complex

___________________________ Note: T/P denotes “Thermal Power Plant”, C/C denotes “Combined Cycle.” Source: Company data as of 1Q 2014

As of March 2014, Coal, B.C. Oil, LNG and others account for 44.9%, 15.7% and 33.7% and 5.7% respectively in terms of generation

capacity in operation

Youngam

5

KOWEPO boasts significant market share both in capacity and sales volume

Company Overview

Strong Market Position

Market Share by Generation Capacity Market Share by Sales Volume

(MW)

Total Generation Capacity

86,975MW

(GWh)

Total Electricity Sales

125,593GWh ___________________________ Source: FSS, DART Filing as of 1Q 2014

KOWEPO, 14,014, 11.2%

KOSEP, 15,249, 12.1%

KOMIPO, 14,297, 11.4%

KOSPO, 16,117, 12.8%

EWP, 12,902, 10.3%

KHNP, 37,848, 30.1%

Others, 15,174, 12.1%

6

KOWEPO, 8,909, 10.2%

KOSEP, 8,227, 9.5%

KOMIPO, 8,934, 10.3%

KOSPO, 9,200, 10.6%

EWP, 9,343, 10.7%

KHNP, 26,039, 29.9%

Others, 16,323, 18.8%

Industry & Regulatory Update

Domestic power generation sector is expected to enjoy healthy demand growth and

government support

Industry & Regulatory Update

Strong Electricity Demand and Government Support

History of Power Consumption

___________________________ Source: “Electricity Supply and Demand Basic Plan #6”, MOTIE as of 2013.

Electricity Demand Forecast

Power consumption has continued to rise on the back of strong economic growth at an average rate of 5.6% per annum from 2000 to

2013

Power consumption is expected to grow at an average rate of 3.3% per annum from 2014 to 2027

The country imposed rolling blackouts as recently as September 2011, due to numerous maintenance issues which led to insufficient

peak load; this highlights the slim margin between electricity demand and supply

South Korea will have to develop more coal- and gas-fired generating capacity despite the strong expected growth in clean energy;

planned clean energy projects are insufficient to alleviate this shortage problem, and the government will have to increase capacity to

avoid an electricity shortfall

Commentary

240 258 278 294 312 332 349 369 385 394 434

455 467 485

0

100

200

300

400

500

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Twh

505 526

547 567

590 611

631 652

672 693

713 733

752 771

400

500

600

700

800

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

Twh CAGR 5.6% CAGR 3.3%

8

Electricity Pricing Mechanism Industry & Regulatory Update

Application of The Adjusted Coefficient of System Marginal Price (“SMP”)

KOWEPO can pass through 100% of its fuel cost through the energy price

Electricity Generation Cost Evaluation Committee annually determines The Adjusted Coefficient

Adjusted Coefficient was readjusted with increase in December 2013 and effective from January 2014

Introduction of “The Adjusted Coefficient of SMP” will motivate Gencos to construct base load power plants and lead to fair

competition among Gencos. It will increase the efficiency of the power market by stimulating cost reduction

Price type Price Remarks

Capacity Payment

(CP) KRW 7.69/kwh

Standard price is KRW 7.69/kwh

CP can be adjusted in accordance with region, season and time

(’12: KRW 7.73/kwh ’13: KRW 7.80/kwh ‘14: KRW 7.69/kwh)

Energy Adjustment Price (Energy Price) [Max {(SMP-Fuel Cost), 0} x

The Adjusted Coefficient + Fuel Cost]

Adjusted Coefficient (effective from January 2014)

Nuclear (light-water reactor) : 0.3170 (←0.0450)

Nuclear (heavy-water reactor): 0.3298 (←0.0450)

Coal : 0.1565 (←0.0001)

B.C. Oil / Gas: 0.3281 (←0.0001)

Others/General : 0.2610 (←0.0001)

KOWEPO continues to enjoy 100% fuel cost pass through pricing mechanism

___________________________ Source: Company information, as of 1Q 2014.

Power Price Comparison

9

Current Implementation Stage of Vesting Contract (VC)

The Electric Utility Act involving the government-approved Vesting Contract(V.C.) was passed in April 2013. However, the detailed

implementation plan is still being worked out by a task force under the supervision of the Korea Power Exchange

The details of VC, such as contract amount, contract price and renewal interval, are still under discussion

Operation Overview

KOWEPO operates 57 generation units with a combined generation capacity of 8,909MW

Operation Overview

Power Plant Facilities in Operation

___________________________ Source: Company data as of 1Q 2014.

Type Fuel Type Number of Units Capacity (MW) Capacity Factor (%)

Taean

Thermal Bituminous 8 4,000 100.9

Solar - 2 0.67 12.4

Small Hydro - 1 2.20 21.8

Pyeongtaek Thermal BC Oil 4 1,400 28.9

Combined Cycle LNG 7 964 15.4

Seoincheon Combined Cycle LNG 16 1,800 81.1

Gunsan Combined Cycle LNG 3 718.40 93.3

Solar - 1 0.26 13.9

Samrangjin Solar - 2 3 13.8

Sejong City Solar - 5 4.93 12.2

Yongam Solar - 1 13.30 14.5

Gyeonggi Solar - 7 2.50 13.3

TOTAL 57 8,909 75.5

11

1,514 1,433

509

136

0

500

1000

1500

2000

Indonesia Australia North America Russia

Kiloton

Operation Overview

Cost Efficiency

Long-term supply contracts assure adequate supply of the raw materials

Hedging risks by adjusting proportion of long-term contracts with market

volatility

___________________________ Source: Company data as of 1Q 2014. 1. Represents fuel costs other than that required to generate electricity, such as fuel required to start up the generating units 2. Canada and US

Fuel Cost Composition

Fuel Cost

Major Suppliers of Coal

Total 3,592 kilotons

Coal LNG

KOWEPO has implemented a cost competitive strategy

(1)

Short Term 9%

Long Term 91%

0.0%

Long Term 100.0

%

50 50 54 55

148

204 223 215

129 143

159 176

0

50

100

150

200

250

2011 2012 2013 1Q2014

KRW / kWh

Coal Heavy Oil Combined(LNG)

12

Coal 27.5%

LNG 64.2%

B.C. Oil 8.4%

(2)

70

90

110

130

150

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

Operation Overview

Fuel Cost Forecast

___________________________ Source: Company information.

Coal

Favorable outlook for KOWEPO’s fuel cost

Coal price has come down recently due to slowdown in Chinese economy and robust

production level in major coal producing countries including Australia and Indonesia

Coal price may rebound slightly due to seasonal factors, but it is expected to move in a

limited range due to weakening fundamentals such as supply and demand

An Individual consumption tax for bituminous coal is included in the total amount of

purchases cost of electricity. Therefore, it does not have a direct impact on the

company’s revenue.

(FOB US$/ton) $143.13

(’11.1

$86.64

(’10.8

$73.08

(’14.3)

(6,080 kcal/kg net calorific value)

Recent Price Trend

Commentary

13

LNG

LNG price is expected to decline due to the increased utilization of

shale gas in the future

As KOWEPO purchases LNG from KOGAS based on the cost-based

pool(CBP) system which is determined by the oil price and FX rate,

the effect of LNG price movement on KOWEPO’s operation is

expected to be minimal

Recent Price Trend

Commentary

400

500

600

700

800

900

1,000

1,100

1,200

1,300

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

(KRW '000) 1,208

('12.6)

717

('10.11)

Strategy to defend its strong market position and superb operating performance through

both domestic and overseas plant constructions and projects

Operation Overview

New Business – Domestic & Overseas

Power Plant Type Capacity Construction Period Remarks

New Plant

Taean #9, #10 Thermal 2,100MW Oct. 2012

~Dec. 2016

Largest unit capacity in Korea

Lowest fuel cost

Taean IGCC Integrated Gasification

Combined Cycle (“IGCC”) 380MW

Nov. 2011

~Nov. 2015 Clean energy source securing by utilizing Bituminous and meeting RPS standard

Pyung-taek 2nd Combined Cycle 946.5MW July. 2012

~Oct. 2014

Emergency power plant to prepare exponential increase in demand in summer of 2013

(GT construction completed in July 2013)

Constructing high efficiency eco-friendly LNG plant for maximizing the rate of return

Equity Investment

Garolim Tidal 520MW Nov 2014

~Feb. 2021

Consortium with POSCO E&C, Daewoo E&C, Lotte E&C

KOWEPO to be in charge of construction management, operation and maintenance

World’s largest tidal plant

Dongdu-cheon Combined Cycle 1,880MW Jun. 2012

~Dec. 2014

Consortium with Samsung E&C, Hyundai Development Company

KOWEPO to be in charge of construction management

___________________________ Source: Company data s of 1Q 2014.

14

Domestic

Overseas

Power Plant Type Capacity Remarks

Equity Investment

Maharashtra, India C/C 388MW Consortium with PPIL (construction started in January 2012 / expected to complete in October 2014)

Build, Own, Operates and maintenance

Xe-Namnoi, Laos Hydro 410MW

Consortium with SK E&C, Ratchaburi (Thailand), LHSE (Laos)

KOWEPO to be in charge of operation and maintenance

Financing completed in November 2013 and started construction

Financial Management

Capital Expenditure Plan

1,770.9

1,180.0

508.6

179.4

299.9

236.9

228.7

234.9

70.6

40.1

13.0

14.0

2,141.4

428.4

750.3

1,457.0

0

500

1,000

1,500

2,000

2,500

3,000

2014 2015 2016 2017

KRW billions

Expansion Maintenance Others

Capital Expenditure Schedule

___________________________ Source: Company information, as of 1Q 2014

15

Operation Overview

Insurance Coverage

KOWEPO is fully insured on its facilities under operation or construction and shipment/transportation of

fuels and raw materials in the event of any unexpected accident and subsequent losses

___________________________ Source: Company data as of 1Q 2014.

Asset Comprehensive Insurance

Details

Insurance Type Asset Comprehensive Insurance

Insurer

Insured Period 2013.04.01 ~ 2014.05.31

Insured Amount KRW11,440 bn

Insured Target Generation Facilities

Insurance on Cargo

Details

Insurance Type Fuel and Equipment Facilities Comprehensive

Insurance on Cargo

Insurer

Insured Period 2014.02.01 ~ 2015.01.31

Insured Amount KRW2,013 bn

Insured Target Fuel and Equipments

Erection All Risks (EAR) Insurance

Details

Insurance Type EAR Insurance on Pyungtaek 2nd EAR Insurance on Taean IGCC EAR Insurance on Taean #9, #10

Insurer

Insured Period 2012.09.28 ~ 2014.12.31 2013.01.01 ~ 2015.11.30 2013.05.01 ~ 2016.12.31

Insured Amount KRW580 bn KRW841 bn KRW1,635 bn

Insured Target Operational and Final Acceptance Test

Generation Facilities

Operational and Final Acceptance Test

Generation Facilities

Operational and Final Acceptance Test

Generation Facilities

16

Financial Management

5,840

7,154 7,293

3,222 3,141 3,161

2,618

4,1324,013

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2012 2013 1Q 2014

(KRW bn)

Total Assets Total Shareholders' Equity Total Liability

Financial Management

Capital Structure

___________________________ Source: Company data as of 1Q 2014. Note: K-IFRS accounting standards.

Capital Structure

Assets

KRW7,293 bn

Non-Current Assets / Total

Assets Ratio : 82.2%

Liability KRW4,132 bn

Shareholders

Equity

KRW3,161 bn

Wholly owned by KEPCO

Revenue KRW1,521 bn

EBITDA KRW196 bn

Net Income: KRW51 bn

Overview – 1Q 2014

18

3.1x 2.0x

6.1x

2.9x 4.3x

7.2x

15.6x

21.1x

0.0x

4.0x

8.0x

12.0x

16.0x

20.0x

24.0x

2012 2013 1Q 2013 1Q 2014

EBIT / Gross Interest Expense Debt / EBITDA

Financial Management

Financial Performance

Revenue

Interest Coverage

EBITDA

Leverage

___________________________ Source: Company filing as of 1Q 2014. Note: 1. Debt consists of the sum of debentures (net of discount) and long-term borrowings (including current position) and short-term borrowing 2. Equity equals total shareholder’s equity 3. EBITDA is defined as earnings before interest expense, income taxes and depreciation and amortization

5,967 5,761

1,487 1,521

0

2,000

4,000

6,000

8,000

2012 2013 1Q 2013 1Q 2014

(KRW billions)

603 565

177 196

0

200

400

600

800

2012 2013 1Q 2013 1Q 2014

(KRW billions)

55.7%

99.4%

60.0%

99.3%

30.7%

43.6% 32.2%

43.1%

0%

20%

40%

60%

80%

100%

2012 2013 1Q 2013 1Q 2014

Debt / Equity Debt / Capital

19

(X) (%)

5.8

12.6

8.7

6.1

9.1

0

4

8

12

16

KOWEPO KOSEP KOMIPO KOSPO EWP

Financial Management

Financial Performance (Cont’d)

EBITDA(1) / Revenue Debt(2) / Equity(3) EBITDA(1) / Net Interest Expense

___________________________ Source: FSS, Dart Filings as of 1Q 2014 Note: 1. EBITDA is defined as earnings before interest expense, income taxes and depreciation and amortization 2. Debt consists of the sum of debentures (net of discount) and long-term borrowings (including current position) and short-term borrowing 3. Equity equals total shareholder’s equity

20

12.9

30.3

12.3

8.8

17.3

0

4

8

12

16

20

24

28

32

KOWEPO KOSEP KOMIPO KOSPO EWP

99.3

93.5

86.8

99.8

91.1

80.0

90.0

100.0

110.0

KOWEPO KOSEP KOMIPO KOSPO EWP

(%) (X) (%)

Industry & Regulatory Update

KOWEPO’s Measures on 4-Year Deleveraging Plan

___________________________ Source: Company information.as of 1Q 2014 Note: Debt Ratio = Total Liabilities / Total Shareholder’s Equity

21

In accordance with the Government’s deleveraging plan on quasi-sovereign corporations,

KOWEPO has established its debt reduction policy to reduce its debt ratio from 170% to

155% by 2017 through project adjustment, asset sales and a tight expense control policy Guideline

Reduce over KRW1.5 tn of debt by 2017 (305% of KRW5 tn which is the increased debt amount from 2012 to 2017)

Self-Effort

KOWEPO’s target self-effort ratio of 155% in 2017 will enable the company to exceed the guideline by KRW5.5bn by the end of 2017

KOWEPO’s Plans to Downscale Debt

81%

128%

160%

174% 171% 170%

153%166%

160%

138%149% 148%

155%

2012 2013 2014 2015 2016 2017

Outlook Self-effort Guideline

Type 2014 2015 2016 2017

Debt Amount

Outlook 5,555.6 6,587.0 7,076.1 7,750.4

Guideline 4,674.3 5,396.3 5,738.6 6,210.7

Self-efforts 5,167.3 6,016.8 6,185.0 6,205.2

Financial Management

Financial Management Policy

Overview of KOWEPO’s Financial Management Policy

Dividend Policy

Risk Management

To manage interest rate risks, KOWEPO borrows most of its debt under fixed rate

As of 1Q 2014, 99.9% of KOWEPO’s debt was fixed rate

Company holds quarterly committee meetings to manage its FX risk strategies

Basic strategy to hedge long-term risks through currency swap and limit short-term risk to below 50%

Dividend Policy

KOWEPO’s basic stance on dividend payout is to achieve a balance between meeting the shareholder’s expectations and maximizing corporate

value

While the Company strives to provide stable dividends at a reasonable level, KOWEPO also considers the sustainability of financial soundness and

liquidity, as well as retaining sufficient financial resources for continued investments of its facilities

In FY2013, KOWEPO’s payout ratio was 30%

2010 2011 2012 2013

Net income 246.3 44.8 118.3 106.8

Dividend 73.9 31.4 59.2 32.0

Total equity 176.0 158.9 158.9 158.9

Dividend yield 42.0% 19.8% 37.3% 20.1%

Payout ratio 30% 70% 50% 30%

(KRW bn)

___________________________ Source: Company data.

22

Financial Management

Details on Credit Line Facilities – 1Q 2014

Bank Amount Remarks

NACF KRW100 bn Committed Line

KEB KRW100 bn Committed Line

Bank Overdraft Facilities

Bank Amount Remarks

KEB KRW84 bn

Shinhan KRW100 bn

Bill Acceptance Facilities

Bank Amount Remarks

KEB USD18 mn

RBS USD130 mn

BNP Paribas USD60 mn

SC First Bank USD50 mn

Shinhan USD30 mn

HSBC USD100 mn

Mizuho Corporate Bank USD100 mn

Deutsche Bank USD100 mn

Bank of Communications USD100 mn Committed Line

Bank of Nova Scotia USD50 mn

KDB USD80 mn

Short-term FCY Credit Facilities

___________________________ Source: Company data as of 1Q 2014.

23

80.3100.4

404.2

570.4

897.2

237.1

881.2

0

100

200

300

400

500

600

700

800

900

1,000

2014 2015 2016 2017 2018 2019 2020~

Financial Management

Debt Profile

Debt Maturity Profile Local vs. Foreign Currency

Fixed vs. Floating Rate Debt

___________________________ Source: Bloomberg data as of 1Q 2014 Note: 1. Debt consists of the sum of debentures (excluding amortization of discount) and long-term borrowings (including current position) 2. Foreign currency debt portion is based on the net amount swapped into KRW.

Foreign

(KRW 1,487.3bn)

46.9%

Local

(KRW 1,683.4bn)

53.1%

Floating

(KRW 3.4bn) 0.1%

Fixed

(KRW 3,167.3bn)

99.9%

24

(1) (1), (2)

(1)

Financial Management

Financial Statements – Income Statement

___________________________ Source: Company information. Note: Consolidated K-IFRS accounting standard.

25

Income Statement

(Unit : KRW bn) 2010 2011 2012 2013 1Q2013 1Q2014

Sales 4,572 5,208 5,967 5761 1,487 1,521

Cost of Sales 4,277 5,030 5,717 5,576 1,383 1,428

Gross Profit 295 178 251 185 104 93

SG&A 39 55 60 65 15 10

Operating Profit 256 123 190 120 90 83

Other Operating Income 4.4 5.0 3.6 3.1 0.8 1.1

Other Operating Expense 0.9 10.3 1.1 1.4 0.5 0.1

Other Income 15 2 2.6 10.4 (3) 4

Financial Income 47 13 75 35 29 23

Financial Expense 81 64 114 94 44 43

Share in Loss of Joint Ventures and Associates (2.5) (1.5) (4.9) 1.4 0.7 (0.6)

Income From Continuing Operations Before Income Tax 239 67 151 75 73 68

Income Tax Expense From Continuing Operations 55 25 46 (20) 16 18

Net Income From Continuing Operations 185 42 105 95 58 50

Net Income From Discontinued Operations 34 - - - - -

Net Income (Loss) 218 42 105 95 58 50

Financial Management

Financial Statements – Balance Sheet

___________________________ Source: Company information. Note: Consolidated K-IFRS accounting standard.

26

Balance Sheet

(Unit : KRW bn) 2010 2011 2012 2013 1Q2013 1Q2014

Assets

Current Assets 1,348 1,182 1,280 1,343 1,331 1,295

Non-Current Assets 4,040 4,105 4,560 5,811 4,667 5,998

Total Assets 5,388 5,287 5,840 7,154 5,998 7,293

Liabilities

Current Liabilities 995 938 797 684 900 894

Non-Current Liabilities 1,137 1,397 1,821 3,329 1,878 3,238

Total Liabilities 2,132 2,335 2,618 4,013 2,778 4,132

Stockholder’s Equity

Capital Stock 1,443 1,192 1,192 1,192 1,192 1,192

Capital Surplus 22 3 201 85 204 88

Retained Earning 1,791 1,757 1,829 1,864 1,825 1,881

Total Stockholders’ Equity 3,256 2,952 3,222 3,141 3,221 3,161

Total Liabilities and Stockholders’ Equity 5,388 5,287 5,840 7,154 5,999 7,293

Financial Management

Financial Statements – Cash Flow Statement

___________________________ Source: Company information. Note: Consolidated K-IFRS accounting standard.

27

Cash Flow Statement

(Unit : KRW bn) 2010 2011 2012 2013 1Q2013 1Q2014

Cash Flows From Operating Activities

Net Income 218 42 105 95 58 50

Non-cash Income & Expenses 546 478 498 487 138 171

Changes in Assets and Liabilities (52) (167) (50) (134) (139) 84

Other (88) (76) (39) 18 25 51

Net Cash Provided by Operating Activities 624 277 514 375 40 299

Cash Flows from Investing Activities

Purchase of Fixed Assets (506) (452) (791) (1,606) (189) (320)

Others, Net (12) 11 (60) 20 8 11

Net Cash Provided by Investing Activities (518) (441) (851) (1,586) (181) (309)

Cash Flows from Financing Activities

Cash Inflows 968 721 1,269 2,064 108 -

Cash Outflows (1,061) (422) (808) (753) (1) (2)

Net Cash Provided by Financing Activities (93) 299 461 1,311 107 (2)

Cash and Cash Equivalent at End of Period 153 285 409 503 374 491

Financial Forecast

Key Financial Indicator Forecast

Key Financial Indicator Outlook

(Unit : KRW bn) 2014 2015 2016 2017

Revenue 6,031 5,993 6,067 7,026

EBIT 255 392 550 558

Depreciation & Amortization 405 461 533 656

EBITDA 642 802 1,020 1,143

(Unit : %) 2014 2015 2016 2017

ROE 4.15% 6.16% 8.11% 6.53%

Return on Sales 2.32% 3.73% 5.17% 3.72%

Debt / Equity 153.1% 165.8% 159.8% 155.0%

EBITDA Margin Ratio 10.6% 13.4% 16.8% 16.3%

___________________________ Source: Company information. Note: EBIT = Net Profit + Interest Expense + Corporate Tax EBITDA = EBIT + Depreciation + Amortization Debt = Total liabilities EBITDA Margin Ratio = EBITDA / Revenue

29

Financial Forecast

Financial Statements Forecast

Balance Sheet

(Unit : KRW bn) 2014 2015 2016 2017

Assets 8,542 9,645 10,057 10,209

Liabilities 5,167 6,017 6,185 6,205

Equity 3,375 3,628 3,872 4,004

___________________________ Note: Forecast is based on 2014-2020 mid to long term financial projections (consolidated basis).

30

Financial Forecast

Income Statement

(Unit : KRW bn) 2014 2015 2016 2017

Revenue 6,031 5,994 6,067 7,026

SG&A 636 713 816 981

Depreciation & Amortization 405 461 533 656

Net Income 140 223 314 261

Disclaimer

This presentation material is prepared by Korea Western Power (the “Company”) solely for your information only. All or any part of this presentation material may not be

taken away, reproduced, redistributed, or retransmitted in any manner. You agree to be bound by the above condition by participating into this presentation. Any non-

compliance may be against the related laws and requirements.

This presentation material does not constitute an offer to purchase or sell the related securities or forms the basis of, or be relied upon in connection with any contract,

commitment or investment decision whatsoever.

This presentation material may contain forward-looking statements. These forward-looking statements are based on a number of assumptions about the future, some of

which are beyond the Company’s control. The Company does not undertake any obligation to update any forward-looking statements to reflect events that occur or

circumstances that arises after the date of this presentation. Potential investors should bear in mind that actual financial results may differ materially from the following

forward-looking statements.

The information contained in this presentation material is not verified by any independent third party. No warranty is made as to, and no reliance should be placed on,

the fairness, accuracy, completeness or correctness of the information contained herein. The information contained in this presentation material should be interpreted

under the prevailing circumstances. There is no update and nothing to be updated upon the presentation to reflect any significant change in the development. At no

time does the Company or the related directors, management, employees, agents or advisers accept any liability for the information contained in this presentation

material and accordingly accept any liability whatsoever for any loss howsoever arising from any use of this presentation material.

31