Embed Size (px)

Citation preview

1

1H2008 Results1H2008 Results30 July 2008

2

Content

Financial Performance

Operations Review

Market Review and Outlook

Going Forward

2

3

Financial Performance

4

Financial Performance 1H08

(10.0)125.5113Net Profit

(4.6)166.6158.9Pre-tax Profit

15.3114.6132.1Operating Profit

13.3119.7135.6EBITDA

(29.9)654.6459Turnover

% Chg1H071H08$m

3

5

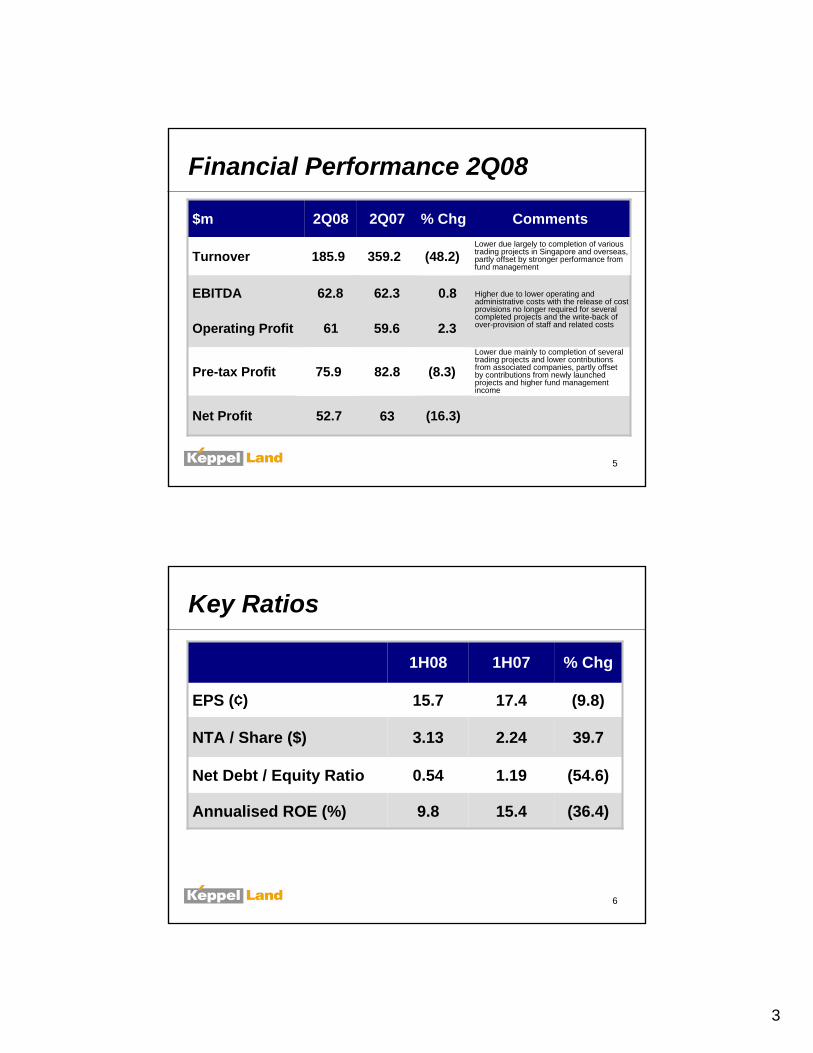

Financial Performance 2Q08

(16.3)

2.3

0.8

% Chg

6352.7Net Profit

Comments2Q072Q08$m

59.661Operating Profit

62.3EBITDA 62.8

359.2185.9Turnover

Lower due largely to completion of various trading projects and lower contributions from associated companies

Higher due to lower operating and administrative costs with the release of cost provisions no longer required for several completed projects and the write-back of over-provision of staff and related costs

(8.3)82.875.9Pre-tax Profit

(48.2)Lower due largely to completion of various trading projects in Singapore and overseas, partly offset by stronger performance from fund management

Lower due mainly to completion of several trading projects and lower contributions from associated companies, partly offset by contributions from newly launched projects and higher fund management income

6

Key Ratios

(36.4)15.49.8Annualised ROE (%)

(54.6)1.190.54Net Debt / Equity Ratio

39.72.243.13NTA / Share ($)

(9.8)17.415.7EPS (¢)

% Chg1H071H08

4

7

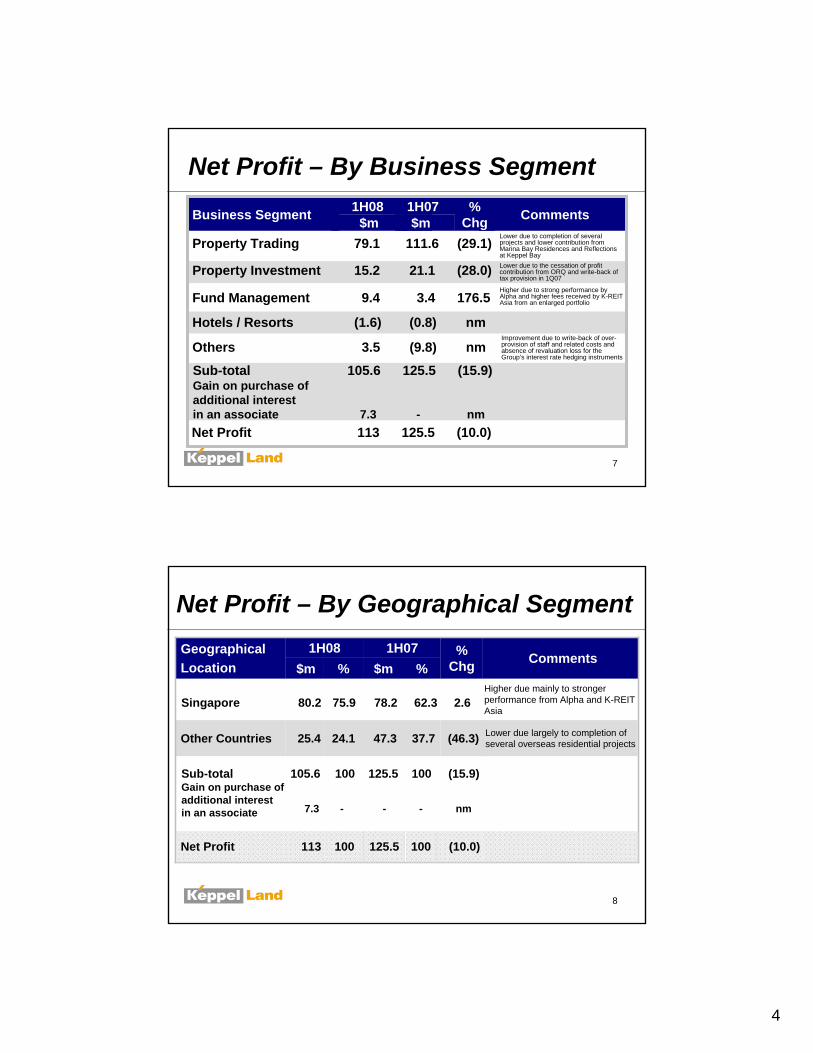

Net Profit – By Business Segment

Net Profit 113 125.5 (10.0)

Comments% Chg

1H071H08$m $mBusiness Segment

Property Investment 15.2 21.1 (28.0)

Property Trading 79.1 111.6 (29.1)

Others 3.5 (9.8) nm

Hotels / Resorts (1.6) (0.8) nm

Fund Management 9.4 3.4 176.5

Lower due to completion of several projects and lower contribution from Marina Bay Residences and Reflections at Keppel BayLower due to the cessation of profit contribution from ORQ and write-back of tax provision in 1Q07

Higher due to strong performance by Alpha and higher fees received by K-REIT Asia from an enlarged portfolio

Improvement due to write-back of over-provision of staff and related costs and absence of revaluation loss for the Group’s interest rate hedging instruments

Sub-total 105.6 125.5 (15.9)Gain on purchase of additional interest in an associate 7.3 - nm

8

Net Profit – By Geographical Segment

Comments% Chg

1H071H08$m %

80.2 75.9Higher due mainly to stronger performance from Alpha and K-REIT Asia

2.662.378.2Singapore

25.4 24.1 Lower due largely to completion of several overseas residential projects(46.3)37.747.3Other Countries

%$mGeographicalLocation

Sub-total 105.6 100 125.5 100 (15.9)Gain on purchase of additional interest in an associate

100 (10.0)100125.5Net Profit 113

7.3 - - - nm

5

9

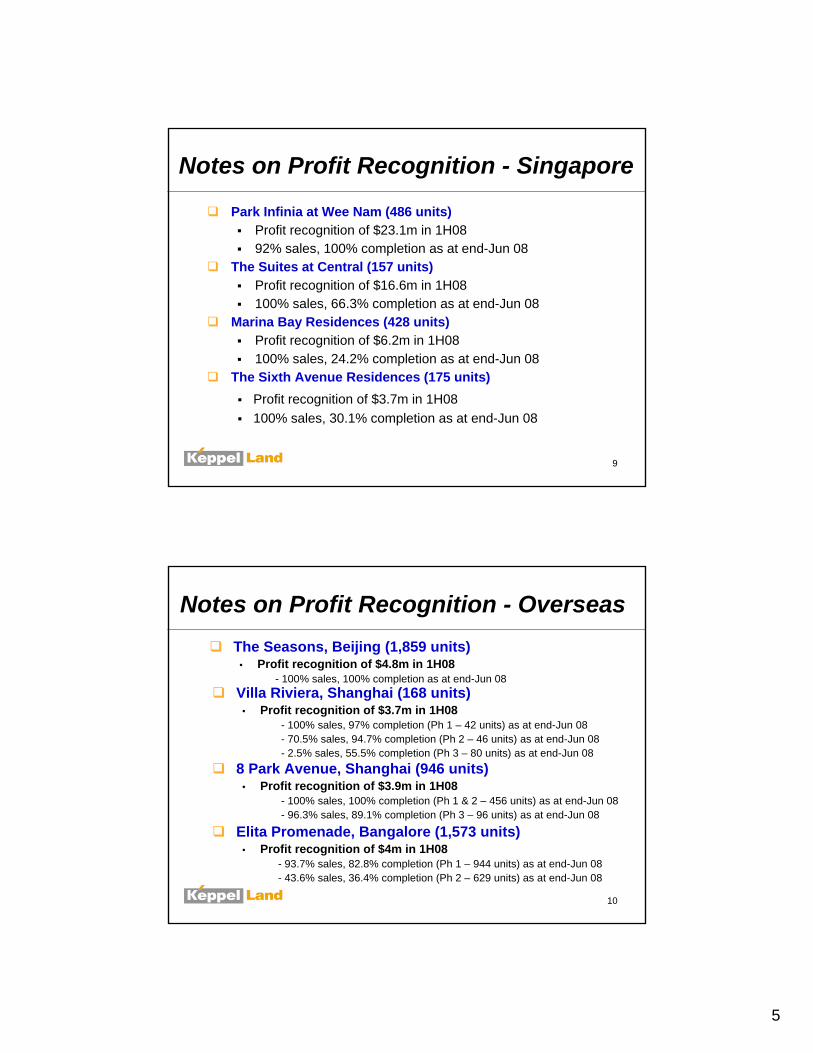

Notes on Profit Recognition - Singapore

Park Infinia at Wee Nam (486 units) Profit recognition of $23.1m in 1H0892% sales, 100% completion as at end-Jun 08

The Suites at Central (157 units) Profit recognition of $16.6m in 1H08100% sales, 66.3% completion as at end-Jun 08

Marina Bay Residences (428 units)Profit recognition of $6.2m in 1H08100% sales, 24.2% completion as at end-Jun 08

The Sixth Avenue Residences (175 units)Profit recognition of $3.7m in 1H08100% sales, 30.1% completion as at end-Jun 08

10

Notes on Profit Recognition - Overseas

Villa Riviera, Shanghai (168 units)• Profit recognition of $3.7m in 1H08

- 100% sales, 97% completion (Ph 1 – 42 units) as at end-Jun 08- 70.5% sales, 94.7% completion (Ph 2 – 46 units) as at end-Jun 08- 2.5% sales, 55.5% completion (Ph 3 – 80 units) as at end-Jun 08

8 Park Avenue, Shanghai (946 units) • Profit recognition of $3.9m in 1H08

- 100% sales, 100% completion (Ph 1 & 2 – 456 units) as at end-Jun 08- 96.3% sales, 89.1% completion (Ph 3 – 96 units) as at end-Jun 08

Elita Promenade, Bangalore (1,573 units) • Profit recognition of $4m in 1H08

- 93.7% sales, 82.8% completion (Ph 1 – 944 units) as at end-Jun 08- 43.6% sales, 36.4% completion (Ph 2 – 629 units) as at end-Jun 08

The Seasons, Beijing (1,859 units)• Profit recognition of $4.8m in 1H08

- 100% sales, 100% completion as at end-Jun 08

6

11

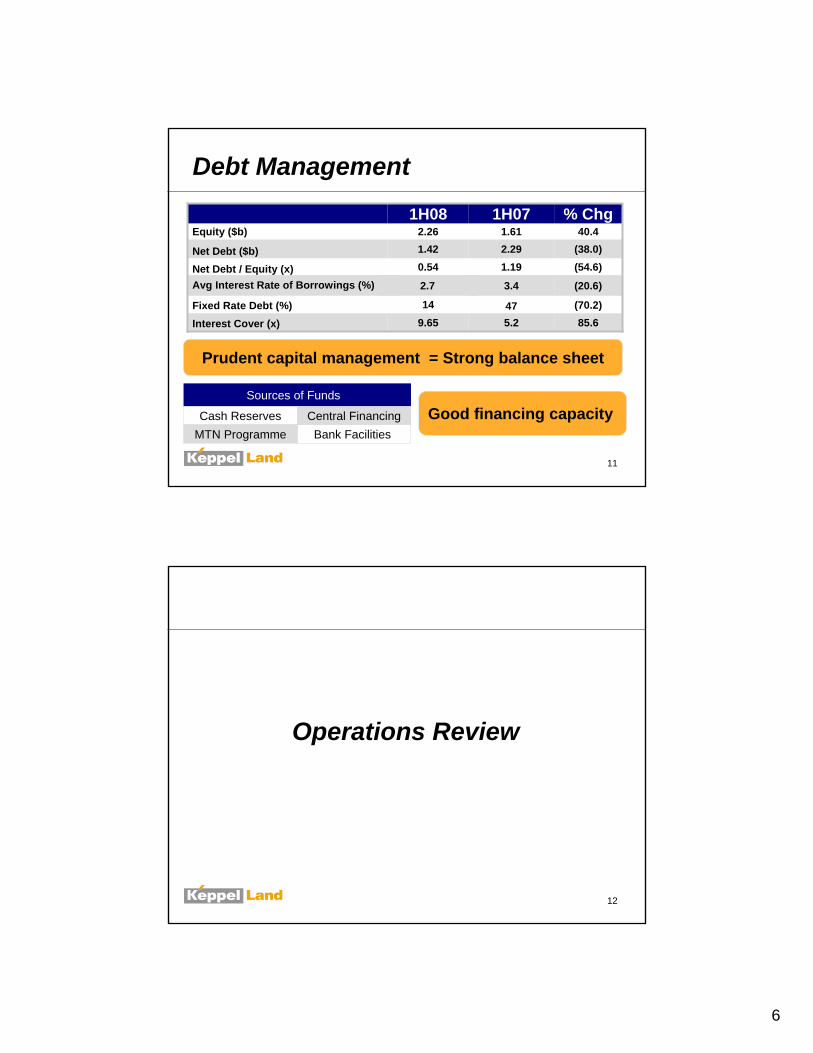

Debt Management

Prudent capital management = Strong balance sheet

85.65.29.65Interest Cover (x)

(20.6)3.42.7Avg Interest Rate of Borrowings (%)(54.6)1.190.54Net Debt / Equity (x)

(38.0)2.291.42Net Debt ($b)

40.41.612.26Equity ($b)% Chg1H071H08

(70.2)4714Fixed Rate Debt (%)

Sources of Funds

Cash ReservesBank Facilities

Central FinancingMTN Programme

Good financing capacity

12

Operations Review

7

13

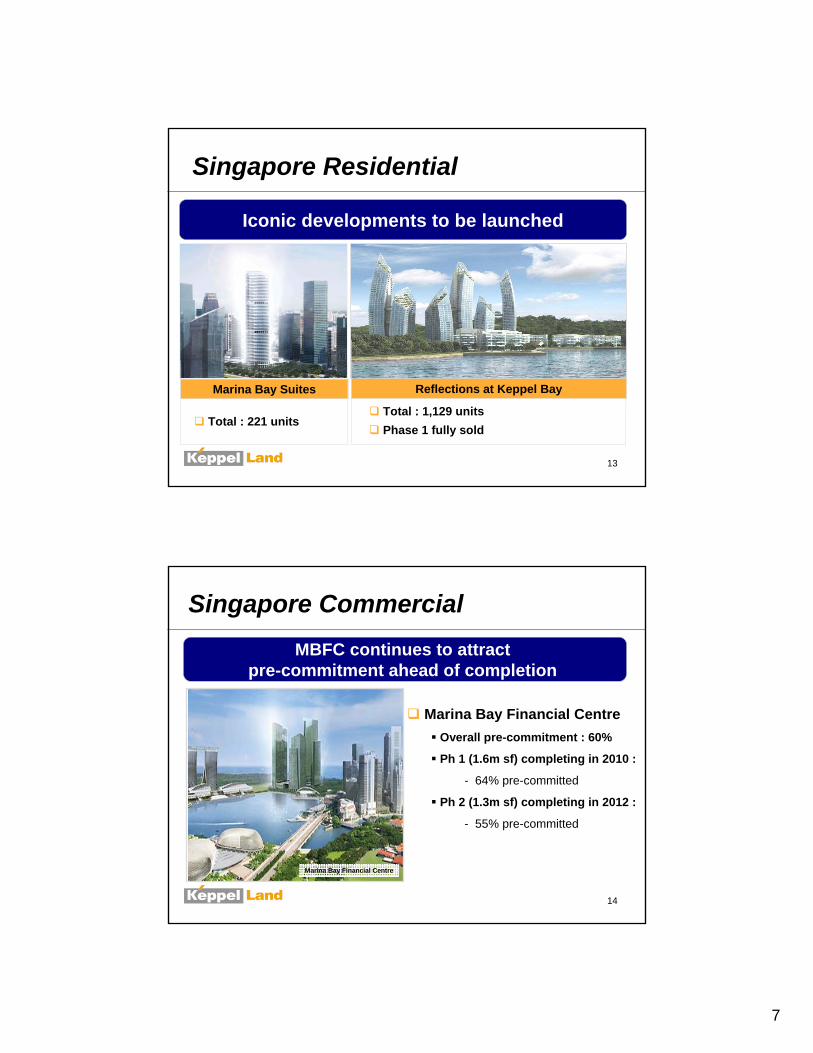

Singapore Residential

Iconic developments to be launched

Total : 1,129 unitsPhase 1 fully sold

Reflections at Keppel Bay Marina Bay Suites

Total : 221 units

14

Singapore Commercial MBFC continues to attract

pre-commitment ahead of completion

Marina Bay Financial Centre

Marina Bay Financial CentreOverall pre-commitment : 60%

Ph 1 (1.6m sf) completing in 2010 :

- 64% pre-committed

Ph 2 (1.3m sf) completing in 2012 :

- 55% pre-committed

8

15

Singapore Commercial – K-REIT

Annualised DPU :11.1 cents* for 1H08

Aggregate leverage down to 27.7%

Post-rights issue:

647.2m units, up from 250.2m units

KLL’s stake : 43.6%

Committed occupancy : 100% as at

end-Jun 08One Raffles Quay

K-REIT Asia continues to outperform

* Based on weighted average no. of units in issue

16

Overseas Residential

Sold : 93% of 350launched units

Residential sales supported by good underlying demand

Sold : 76% of 111 launched units

Elita Garden VistaKolkata, India

Villa RivieraShanghai, China

The EstellaHCMC, Vietnam

Sold : 283 units

9

17

Overseas Residential

Steady sales for residential township developments

Sold : 91% of 191 launched units

Central Park CityWuxi, China

Jakarta Garden CityJakarta, Indonesia

Sold: 96% of 728 launched units

18

Overseas Residential Acquired adjoining 10-ha land in Shenyang

for integrated township development

Township in Shenyang

Combined land area : 34-ha

Total GFA : 677,000 sm

Total units : 5,600 homes

Phase 1 sales launch : 2009

Foray into first marina lifestyle residential Foray into first marina lifestyle residential development in Zhongshandevelopment in Zhongshan

Waterfront development, Zhongshan

KLL’s stake in JV: 80%Total land area : 82-ha (acquired 20-ha)

Total GFA : 408,000 smTotal Units :

No. of Berths : 550

- 305 villas - 1,350 condos- 1,200 serviced apartments

10

19

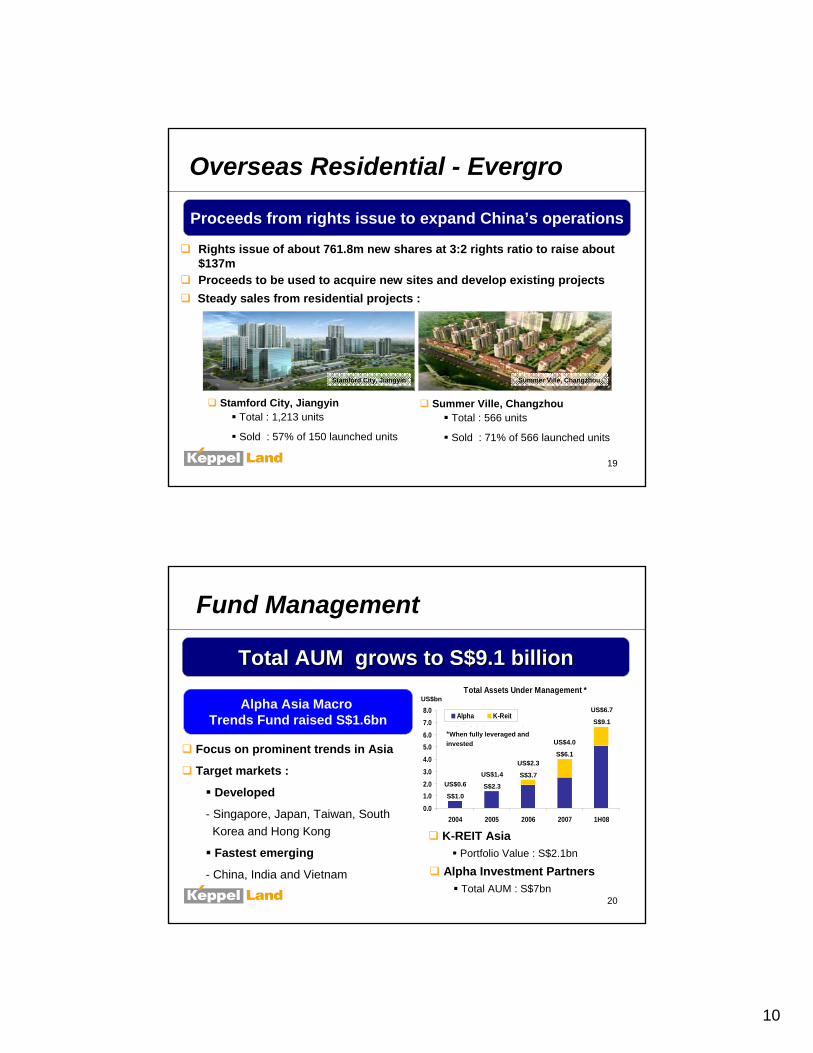

Overseas Residential - Evergro

Proceeds from rights issue to expand China’s operations

Rights issue of about 761.8m new shares at 3:2 rights ratio to raise about $137mProceeds to be used to acquire new sites and develop existing projects

Stamford City, JiangyinTotal : 1,213 units

Sold : 57% of 150 launched units

Stamford City, Jiangyin Summer Ville, Changzhou

Steady sales from residential projects :

Summer Ville, ChangzhouTotal : 566 units

Sold : 71% of 566 launched units

20

Fund Management

Total AUM grows to S$9.1 billionTotal AUM grows to S$9.1 billion

Alpha Asia Macro Trends Fund raised S$1.6bn

US$bn

* When fully leveraged and invested

Total Assets Under Management *

0.01.02.03.04.05.06.07.08.0

2004 2005 2006 2007 1H08

Alpha K-ReitUS$6.7

S$9.1

US$4.0

S$6.1US$2.3

S$3.7US$1.4

S$2.3US$0.6

S$1.0

*When fully leveraged and investedFocus on prominent trends in Asia

Target markets :

Developed

- Singapore, Japan, Taiwan, South Korea and Hong Kong

Fastest emerging

- China, India and Vietnam

K-REIT AsiaPortfolio Value : S$2.1bn

Alpha Investment PartnersTotal AUM : S$7bn

11

21

Recent Awards

BT Corporate Transparency Index (12 May 2008)Ranked 3rd out of 703 companies

ACCA Singapore Environmental and Social Reporting Awards 2008Finalist for 3rd year

Finance Asia Best Managed Companies Poll 2008Best Managed Company (5th)Best Corporate Governance (4th)Best Investor Relations (8th)

22

FIABCI Prix d’ Excellence Awards 2008Winner in the Office category : One Raffles Quay

Recent Awards

World Travel Awards 2008Indonesia’s Leading Resort : Hotel Sedona Manado Myanmar’s Leading Hotel :

- Sedona Hotel Yangon - Sedona Hotel Mandalay

The Guide Awards 2008Best Performance Luxury Apartments:

- Sedona Suites Hanoi - Sedona Suites HCMC

12

23

Green Awards

BCA Green Mark Awards (2008) – Platinum

Ocean Financial Centre : First office building in

Singapore to achieve Platinum Award

BCA Green Mark Awards (2008) – Gold

MBFC Phase 1 (Commercial)

Reflections at Keppel Bay

24

Market Review and Outlook

13

25

Singapore Residential Market

Market affected by US subprime problems

High-end price consolidatingMid-tier / mass market stableLow transaction volume

Good fundamentals and economic growth

Market direction substantially influenced by how soon the

US mortgage crisis can be stabilised

Fundamentals support market

26

Singapore Office Market

Balanced demand and supply expected

Source: *CBRE

Moderate rental growth in 1H08

Average 2m sf new supply per

annum over next few years23% pre-committed

2.62m sf 2.60m sf2.42m sf

0.87m sf

Mill

ion

sf 1.53m sf

Annual average demand: 1.62m sf*

Future Supply of Office Space

0.40

1.021.20

2.54

1.72

0.06

0.39 0.39

0.06

0.41

0.12

1.03 0.70

0.09

0.2

0.40.6

0.8

1.0

1.2

1.4

1.6

1.8

2.02.2

2.42.6

2.8

2008 2009 2010 2011 2012

0.39More balanced demand and

supply in the next few years

Rentals and capital values

expected to have steady

growth

14

27

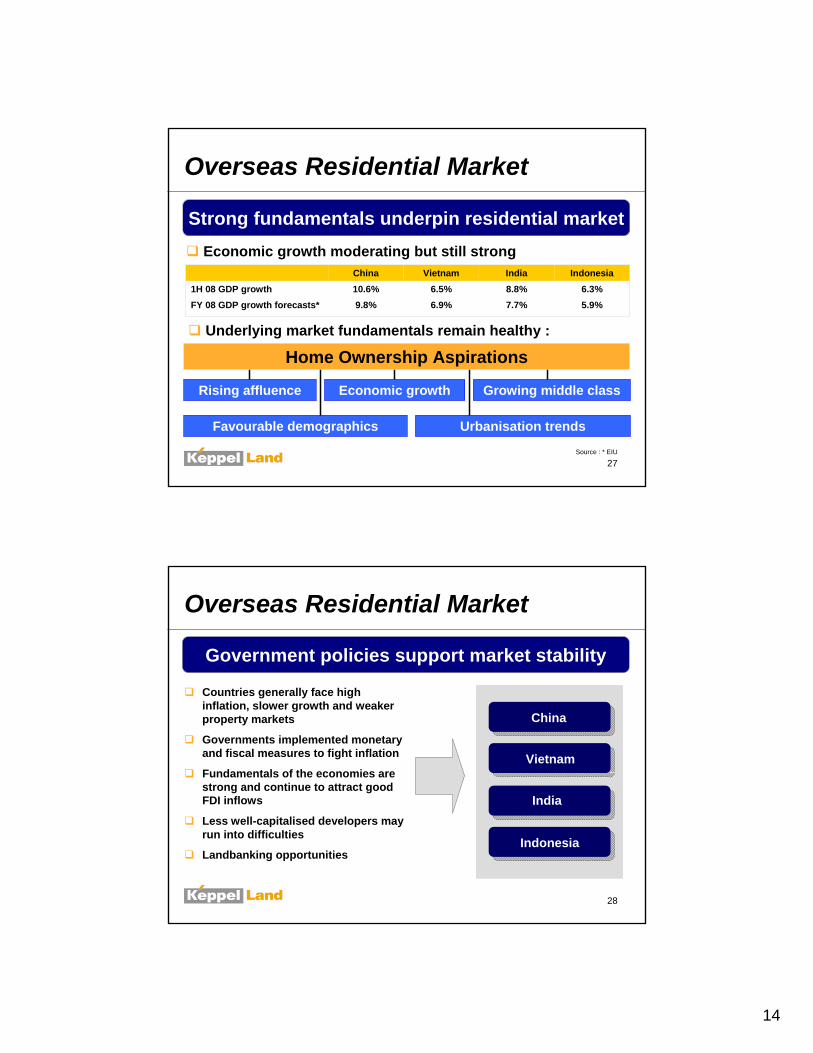

Overseas Residential Market

Strong fundamentals underpin residential market

Underlying market fundamentals remain healthy :

Rising affluence Economic growth Growing middle class

Favourable demographics Urbanisation trends

Home Ownership Aspirations

5.9%7.7%6.9%9.8%FY 08 GDP growth forecasts*6.3%8.8%6.5%10.6%1H 08 GDP growth

IndonesiaIndiaVietnamChina

Economic growth moderating but still strong

Source : * EIU

28

Overseas Residential Market

Government policies support market stability

Countries generally face high inflation, slower growth and weaker property markets

Governments implemented monetary and fiscal measures to fight inflation

Fundamentals of the economies are strong and continue to attract goodFDI inflows

Less well-capitalised developers may run into difficulties

Landbanking opportunities

China

Vietnam

Indonesia

India

15

29

Going Forward

30

Growth Strategy

Closely monitor market conditions to : Look out for new opportunities for acquisitions in Singapore and overseas

Time project launches

Grow township division and pursue lifestyle development projects

Explore new markets such as Middle East and Russia

Presence of 6 township developments in China, Vietnam and Indonesia

Waterfront residential cum marina development in Zhongshan

16

31

Singapore Residential

Monitor market conditions for possible launches in 2H08Monitor market conditions for possible launches in 2H08

Units to LaunchExpected Launch Date Projects

221Marina Bay Suites (33.3% stake)

400Reflections at Keppel Bay (30% stake) *

2H08

2H08Park Infinia at Wee Nam * 2H08 52

33The Tresor *15The Promont 2H08

Total 77756

2H082H08Madison Residences

The Tresor Madison Residences Park Infinia at Wee Nam The Promont

* Planned balance units

32

Singapore Commercial

Draw on robust demand for office spaceDraw on robust demand for office space

KLL's Office Occupancy Rates

81.1%

89.6% 91.3%94.8% 95.0%

70%75%

80%85%90%

95%100%

2004 2005 2006 2007 1H08

Improve pre-commitment

level at MBFC

Resilient portfolio with

potential for positive rent

reversions

17

33

Overseas Residential

TOTAL 1,865 3,705 4,859

Villa Riviera, Shanghai* 84 - -The Botanica, Chengdu* 653 1,000 1,000

Project Launch Schedule - China 2008 2009 20108 Park Avenue, Shanghai * - - 130

The Arcadia, Tianjin* 100 31 -Central Park City , Wuxi – Ph 1*, 2^,3^ 759 801 829Stamford City, Jiangyin* 269 265 594Shenyang Township^ - 1,000 1,322Residential Devt, Nanhui, Shanghai^ - 608 699 Integrated Marina Lifestyle Devt, Zhongshan^ - - 285

* Balance Units ^ New Launches

Stamford City, Jiangyin The Arcadia, Tianjin Villa Riviera, Shanghai

34

Overseas Residential

* Balance Units ^ New Launches

Project Launch Schedule 2008 2009 2010Vietnam

Saigon Sports City (Ph 1), HCMC ^ - - 300The Estella, HCMC * 367 443 300Waterfront condo, Binh Thanh District, HCMC ^ - - 350Waterfront condo, District 7, HCMC ^ - 480 680Waterfront township (Ph 1), Dong Nai Province ^ - - 300Prime condo, District 2, HCMC ^ - 200 410Villa devt., District 9, HCMC ^ - - 90Prime condo, District 9, HCMC ^ - - 300Luxury villa devt., District 9, HCMC ^ - 72 29

ThailandVilla Arcadia at Srinakarin, Bangkok * 41 50 50Villa Arcadia at Watcharapol, Bangkok * 40 40 40

IndiaElita Promenade, Bangalore * 350 - -Elita Horizon, Bangalore ^ 370 401 201Elita Garden Vista, Kolkata * 634 227 90

IndonesiaJakarta Garden City, Jakarta * 448 618 639

Middle EastSeafront condo devt., Jeddah, Saudi Arabia ^ 180 300 300

PhilippinesPalmdale Heights (Ph 2), Pasig City ^ 316 474 474SM-KL residential devt., Manila ^ - 430 -

TOTAL 2,746 3,735 4,553

18

35

Thank You

36

Additional Slides

19

37

(36.4)15.49.8Annualised ROE (%)

(54.6)1.190.54Net Debt / Equity Ratio (x)

39.72.243.13NTA / Share ($)

(9.8)17.415.7EPS (¢)

(36.1)37.724.1Overseas Earnings (% of PATMI)(10.0)125.5113.0*PATMI ($m)

(9.0)166.6151.6Pre-tax Profit ($m)

15.3114.6132.1Operating Profit ($m)

(29.9)654.6459.0Turnover ($m)

% Chg1H20071H2008

1H08 Financial Highlights

* Includes a gain of 7.3m arising from excess subscription of K-REIT Asia’s rights issue

38

Attributable AttributableLand Area GFA

(%) (sf) (sf)

The Tresor * Duchess Rd 100% 999-yr 80,504 112,689 62Reflections at Keppel Bay * Keppel Bay 30% 99-yr 269,930 624,521 1,129Marina Bay Suites Marina Bay 33.3% 99-yr 19,015 156,462 221The Promont Cairnhill Circle 100% Freehold 11,183 31,310 15Madison Residences Bukit Timah Rd 100% Freehold 49,168 110,810 56Keppel Bay Plot 3 Keppel Bay 30% 99-yr 125,366 152,999 307Keppel Bay Plot 4 Keppel Bay 11.7% 99-yr 36,114 40,300 234Keppel Bay Plot 6 Keppel Bay 30% 99-yr 141,429 67,813 94Total 732,709 1,296,904 2,118

Project Location Tenure Total Units

KLL's Stake

* Includes units and area sold

Singapore Residential Landbank

20

39

Project Location Stake Land Area Total GFA Remaining Area Remaining Units (%) (sm) (sm) For Sale (sm) For Sale

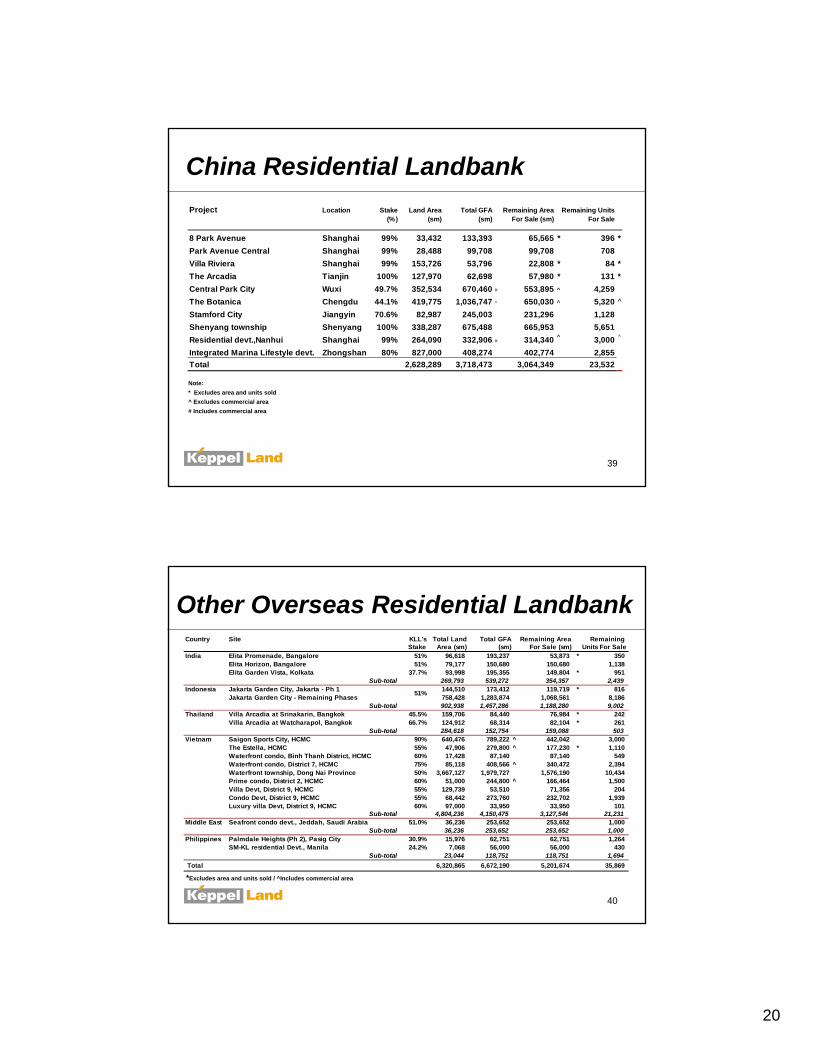

8 Park Avenue Shanghai 99% 33,432 133,393 65,565 * 396 *Park Avenue Central Shanghai 99% 28,488 99,708 99,708 708Villa Riviera Shanghai 99% 153,726 53,796 22,808 * 84 *The Arcadia Tianjin 100% 127,970 62,698 57,980 * 131 *Central Park City Wuxi 49.7% 352,534 670,460 # 553,895 ^ 4,259The Botanica Chengdu 44.1% 419,775 1,036,747 ^ 650,030 ^ 5,320 ^Stamford City Jiangyin 70.6% 82,987 245,003 231,296 1,128Shenyang township Shenyang 100% 338,287 675,488 665,953 5,651Residential devt.,Nanhui Shanghai 99% 264,090 332,906 # 314,340 ^ 3,000 ^

Integrated Marina Lifestyle devt. Zhongshan 80% 827,000 408,274 402,774 2,855Total 2,628,289 3,718,473 3,064,349 23,532

Note: * Excludes area and units sold^ Excludes commercial area# Includes commercial area

China Residential Landbank

40

Country Site KLL's Total Land Total GFA Remaining Area Remaining Stake Area (sm) (sm) For Sale (sm) Units For Sale

India Elita Promenade, Bangalore 51% 96,618 193,237 53,873 * 350Elita Horizon, Bangalore 51% 79,177 150,680 150,680 1,138Elita Garden Vista, Kolkata 37.7% 93,998 195,355 149,804 * 951

Sub-total 269,793 539,272 354,357 2,439Indonesia Jakarta Garden City, Jakarta - Ph 1 144,510 173,412 119,719 * 816

Jakarta Garden City - Remaining Phases 758,428 1,283,874 1,068,561 8,186Sub-total 902,938 1,457,286 1,188,280 9,002

Thailand Villa Arcadia at Srinakarin, Bangkok 45.5% 159,706 84,440 76,984 * 242Villa Arcadia at Watcharapol, Bangkok 66.7% 124,912 68,314 82,104 * 261

Sub-total 284,618 152,754 159,088 503Vietnam Saigon Sports City, HCMC 90% 640,476 789,222 ^ 442,042 3,000

The Estella, HCMC 55% 47,906 279,800 ^ 177,230 * 1,110Waterfront condo, Binh Thanh District, HCMC 60% 17,428 87,140 87,140 549Waterfront condo, District 7, HCMC 75% 85,118 408,566 ^ 340,472 2,394Waterfront township, Dong Nai Province 50% 3,667,127 1,979,727 1,576,190 10,434Prime condo, District 2, HCMC 60% 51,000 244,800 ^ 166,464 1,500Villa Devt, District 9, HCMC 55% 129,739 53,510 71,356 204Condo Devt, District 9, HCMC 55% 68,442 273,760 232,702 1,939Luxury villa Devt, District 9, HCMC 60% 97,000 33,950 33,950 101

Sub-total 4,804,236 4,150,475 3,127,546 21,231Middle East Seafront condo devt., Jeddah, Saudi Arabia 51.0% 36,236 253,652 253,652 1,000

Sub-total 36,236 253,652 253,652 1,000Philippines Palmdale Heights (Ph 2), Pasig City 30.9% 15,976 62,751 62,751 1,264

SM-KL residential Devt., Manila 24.2% 7,068 56,000 56,000 430Sub-total 23,044 118,751 118,751 1,694

Total 6,320,865 6,672,190 5,201,674 35,869

51%

*Excludes area and units sold / ^Includes commercial area

Other Overseas Residential Landbank

21

41

* Office tower to be demolished upon completion of Ocean Financial Centre

KLL's TotalStake NLA (sf)

Completed Ocean Towers* 75.7% 229,481Equity Plaza 64.6% 249,165Keppel Bay Tower 11.7% 387,676HarbourFront Tower One 11.7% 370,551HarbourFront Tower Two 11.7% 154,688Subtotal 1,391,561

Under Development Marina Bay Financial Centre (Phase 1) 33.3% 1,620,000Marina Bay Financial Centre (Phase 2) 33.3% 1,300,000Ocean Financial Centre 75.7% 850,000Subtotal 3,770,000

Total 5,161,561

Building

Singapore Commercial Landbank

42

Singapore Residential

New Downtown Line (DTL)Values of properties nearby expected to rise*12 MRT stations for Bukit Timahby 2015

Developments to benefit from new DTL

Source: DTL map from LTA / *JLL

Duchess

Projects Location Station

The Tresor Duchess Rd

Bukit Timah RdMadison Residences

KLL’s developments to benefit from DTL

Park Infinia Wee Nam Rd NewtonInterchange

Botanic Gardens /Stevens

22

43

Singapore Office Market

Healthy take-up at MBFC shows strength of leasing market

Tenant NLA (sf)Phase 1 1,026509Standard Chartered 513,045Natixis 65,165Wellington Inv Mgt 21,786Amex 49,934Barclays 99,998Pictet 24,757Icap 32,399Others 219,425Phase 2 - DBS 690,448

Total pre-commitment 1,716,957 60%

64%

55%

44

Singapore Office Market

Rentals and occupancy continue to rise

Average Grade A rental and occupancy : $18.80 psf and 99.4% (2Q08)*Grade A rents rose moderately at 9.6% in 1H08 Singapore prime office rents cheaper than Hong Kong and Japan

Source: *CBRE

A v e r a g e Pr ime R e n ta ls ( $ p s f p m ) A v e ra g e G r a d e A Re n ta ls ( $ p s f p m ) C o re CB D O c c u p a n c y

30 Sep 31 Dec2006

31 Mar 30 Jun 30 Sep 31 Dec2007

31 Mar 30 Jun 2008

6.90 7.81 8.6010.80

12.6015.00 16.00 16.10 17.00 17.50

15.50

7.608.73

10.6012.40

14.9017.15

18.65 18.80 19.00 20.00 19.00

97.6% 97.1%95.5% 97.6%97.1%97.3%96.8%96.4%

$4

$6

$8

$10

$12

$14

$16

$18

$20

30-Sep-06 31-Dec-06 31-Mar-07 30-Jun-07 30-Sep-07 31-Dec-07 31-Mar-08 30-Jun-08 2008E 2009E 2010E0%10%20%

30%40%50%60%70%80%90%100%

Average Prime Rentals ($psf pm) Average Grade A Rentals ($psf pm) Core CBD Occupancy

Forecast Rents: Prime & Grade A

23

45

Singapore Office Market

Singapore’s transformation into a business hub supports office demand

Greater presence of financial institutions and legal and accounting firms

Wealth management continues to grow

Source : Nomura Singapore

Growth of Singapore’s Asset Management Industry1998 2002 2006 2009E

Assets under management (S$bn) 151.0 344.0 891.0 1,389

Industry share of GDP (%) 1.0 2.0 3.8 4.5

AUM / GDP (%) 109.2 217.7 410.6 489.0

Source : Nomura Singapore

46

This release may contain statements which are subject to risks and uncertainties that could cause actual results to differ materially from such statements. You are

cautioned not to place undue reliance on such statements, which are based on the current views of Management on future developments and events.

![User Manual Aplikasi VClaim v. 1.4 - 61.8.75.22661.8.75.226/itblog/attachments/article/1359/User_Manual_Aplikasi_V... · Jaminan [Penambahan fitur Monitoring SEP Kasus KLL] 9. Referensi](https://img.pdfslide.us/doc/110x75/5c812a2b09d3f265358c0594/user-manual-aplikasi-vclaim-v-14-6187522661875226itblogattachmentsarticle1359usermanualaplikasiv.jpg)

![[ njH ] [ gVd ] [ kLl ] [ TINk ] [ 'hxpI ] [ nau ] [ tJC ]](https://img.pdfslide.us/doc/110x75/56649e3f5503460f94b30286/-njh-gvd-kll-tink-hxpi-nau-tjc-.jpg)