Embed Size (px)

Citation preview

Jolanta Wysocka | CEO Mountain Pacific Group www.mountainpacificgroup.com

KL Gates Building Bridges III Innovations in Infrastructure Investment Platforms and the role of PPPs Washington, DC November 6, 2015

I-5 Bridge, Mt Vernon, WA, USA

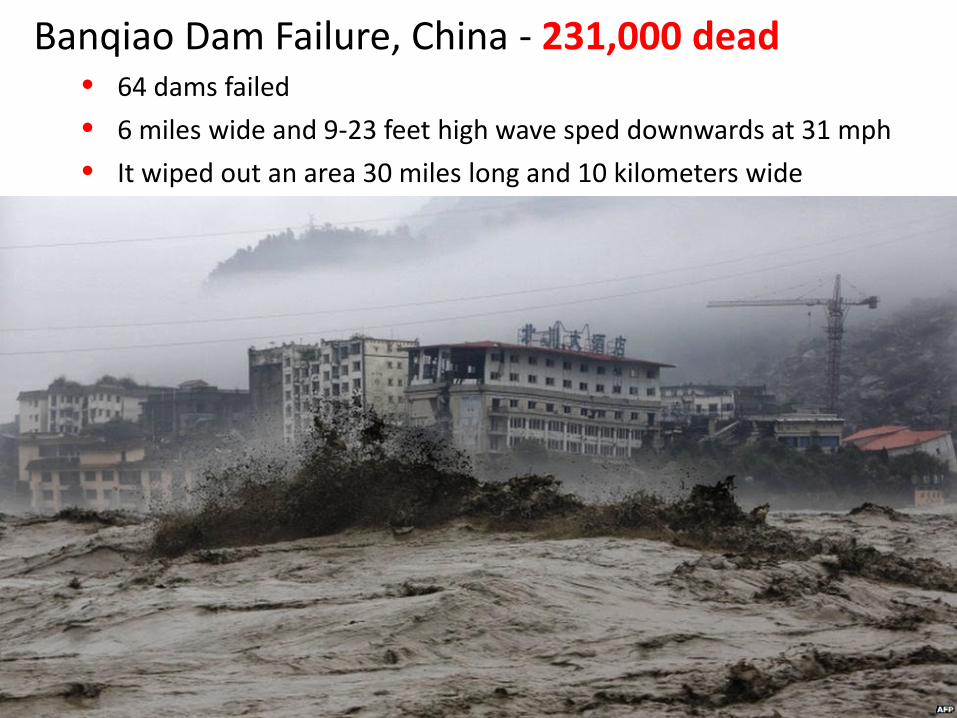

Banqiao Dam Failure, China - 231,000 dead • 64 dams failed • 6 miles wide and 9-23 feet high wave sped downwards at 31 mph • It wiped out an area 30 miles long and 10 kilometers wide

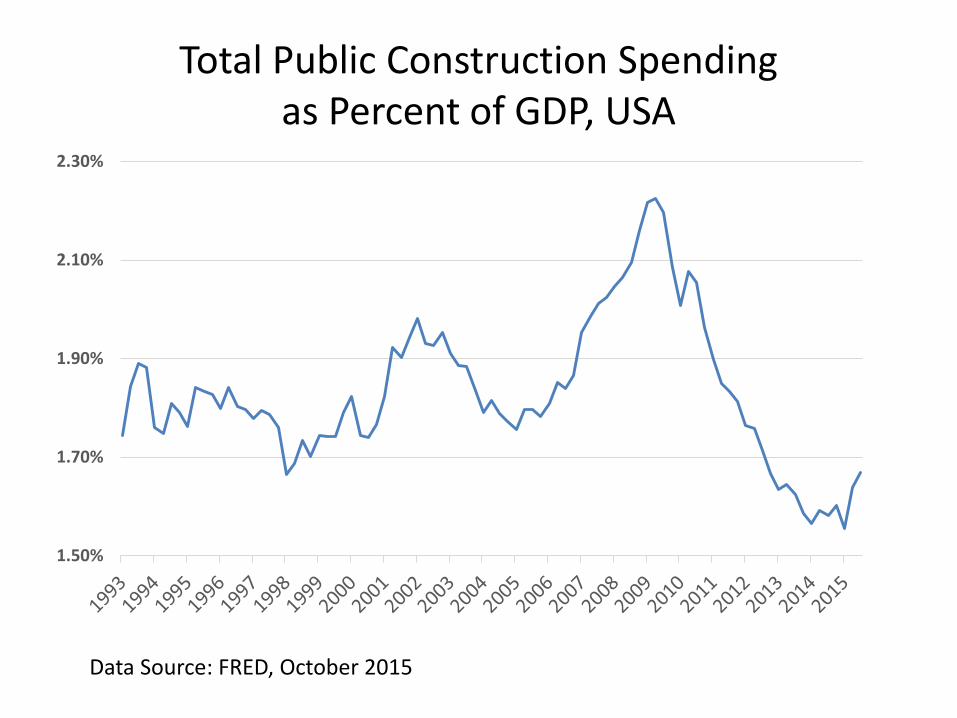

Data Source: FRED, October 2015

Total Public Construction Spending as Percent of GDP, USA

1.50%

1.70%

1.90%

2.10%

2.30%

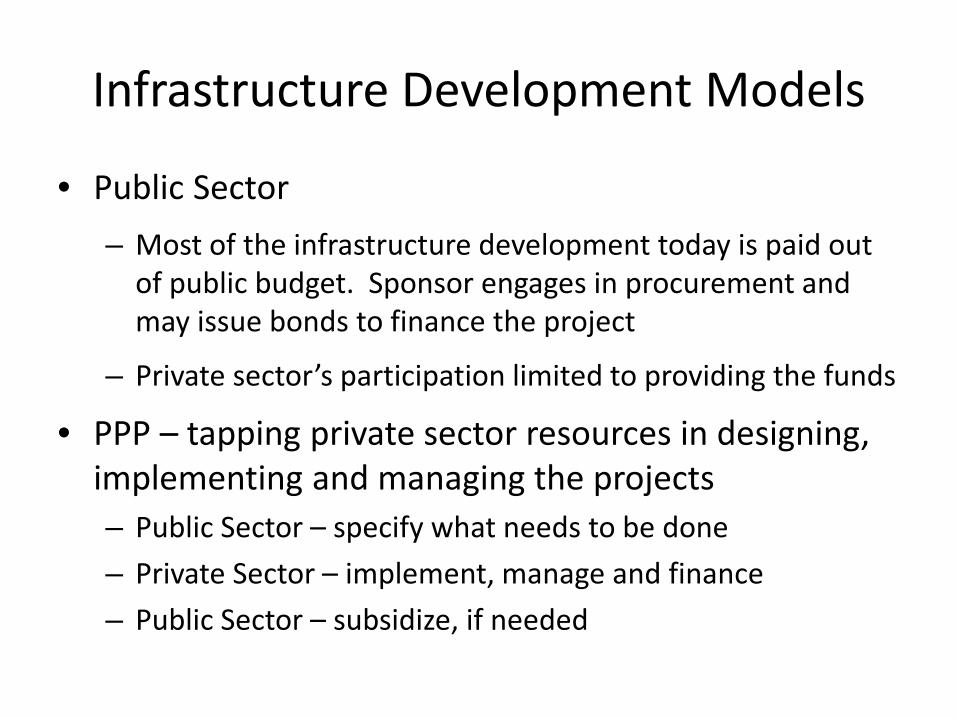

Infrastructure Development Models

• Public Sector – Most of the infrastructure development today is paid out

of public budget. Sponsor engages in procurement and may issue bonds to finance the project

– Private sector’s participation limited to providing the funds

• PPP – tapping private sector resources in designing, implementing and managing the projects – Public Sector – specify what needs to be done – Private Sector – implement, manage and finance – Public Sector – subsidize, if needed

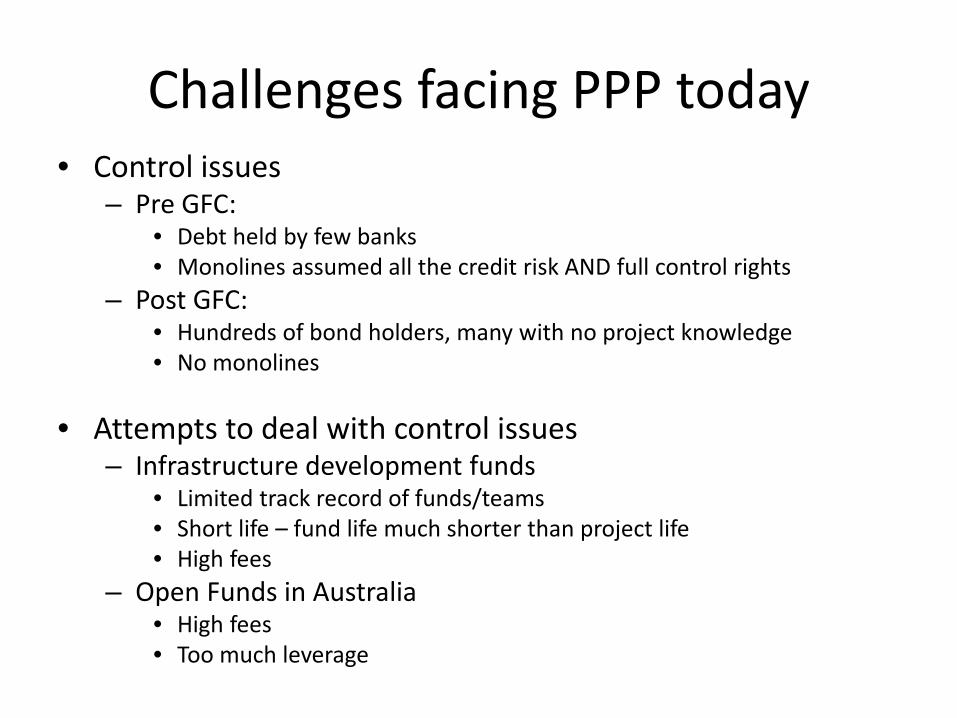

Challenges facing PPP today • Control issues

– Pre GFC: • Debt held by few banks • Monolines assumed all the credit risk AND full control rights

– Post GFC: • Hundreds of bond holders, many with no project knowledge • No monolines

• Attempts to deal with control issues

– Infrastructure development funds • Limited track record of funds/teams • Short life – fund life much shorter than project life • High fees

– Open Funds in Australia • High fees • Too much leverage

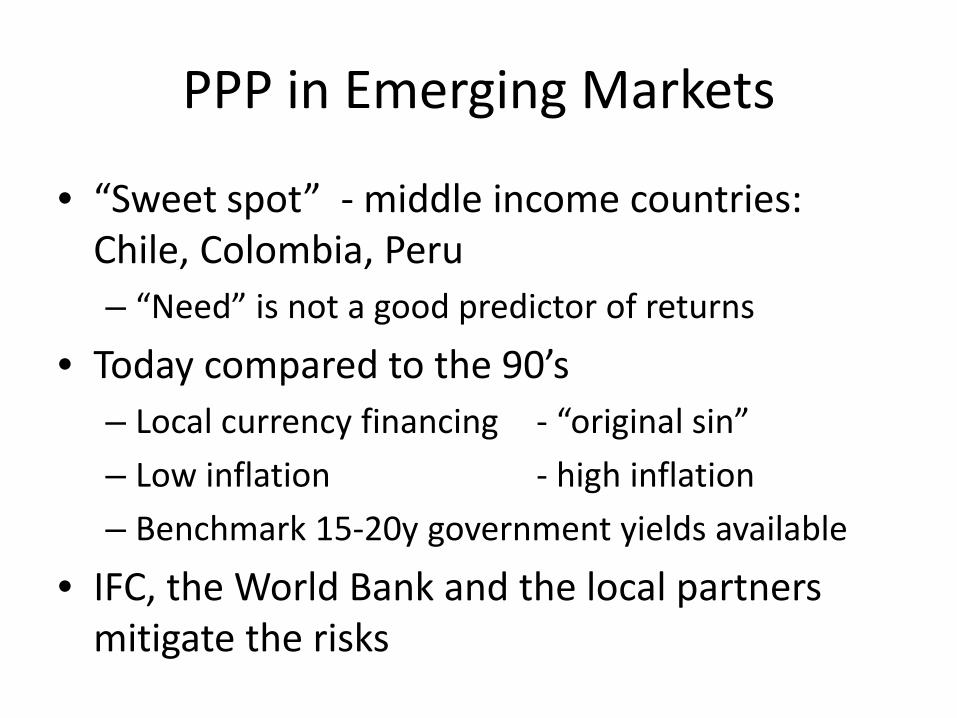

PPP in Emerging Markets

• “Sweet spot” - middle income countries: Chile, Colombia, Peru – “Need” is not a good predictor of returns

• Today compared to the 90’s – Local currency financing - “original sin” – Low inflation - high inflation – Benchmark 15-20y government yields available

• IFC, the World Bank and the local partners mitigate the risks

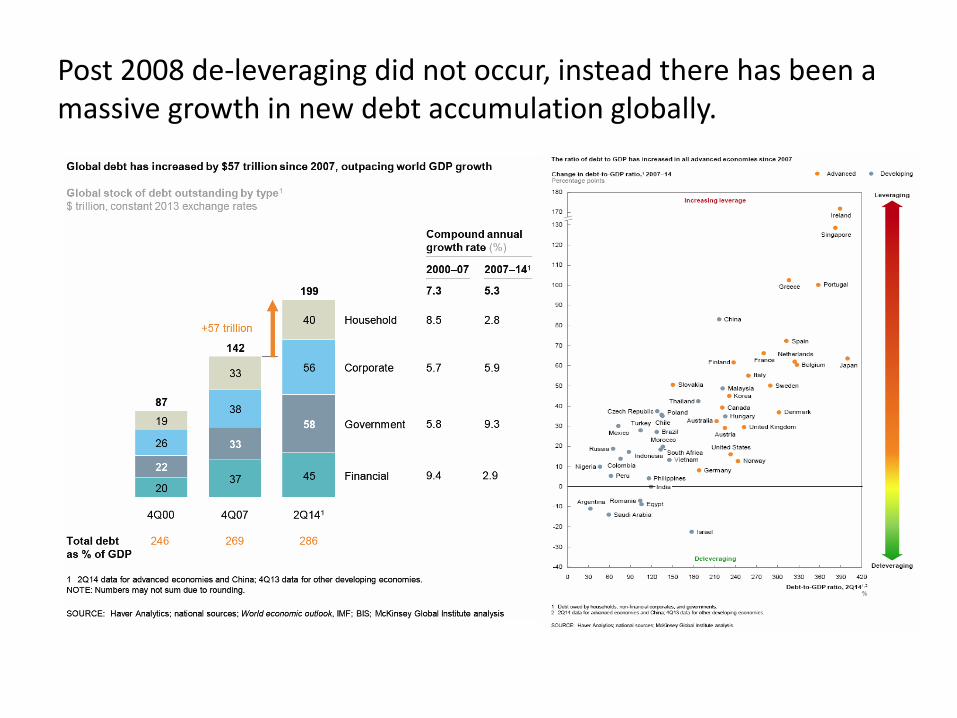

Post 2008 de-leveraging did not occur, instead there has been a massive growth in new debt accumulation globally.

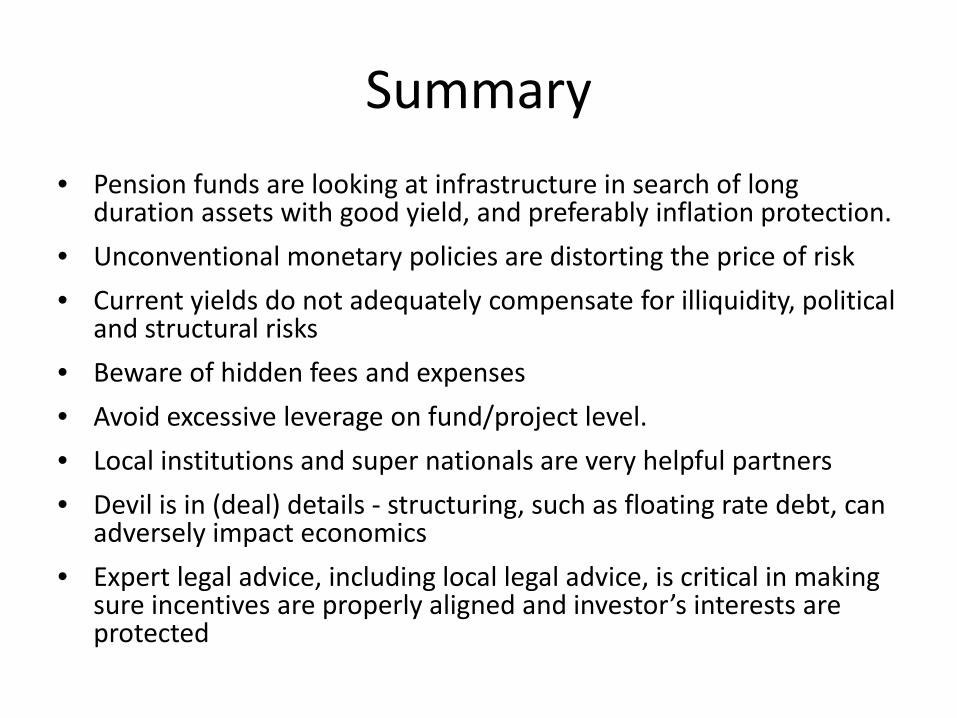

Summary • Pension funds are looking at infrastructure in search of long

duration assets with good yield, and preferably inflation protection. • Unconventional monetary policies are distorting the price of risk • Current yields do not adequately compensate for illiquidity, political

and structural risks • Beware of hidden fees and expenses • Avoid excessive leverage on fund/project level. • Local institutions and super nationals are very helpful partners • Devil is in (deal) details - structuring, such as floating rate debt, can

adversely impact economics • Expert legal advice, including local legal advice, is critical in making

sure incentives are properly aligned and investor’s interests are protected