Embed Size (px)

DESCRIPTION

KPIs for Enterprise

Citation preview

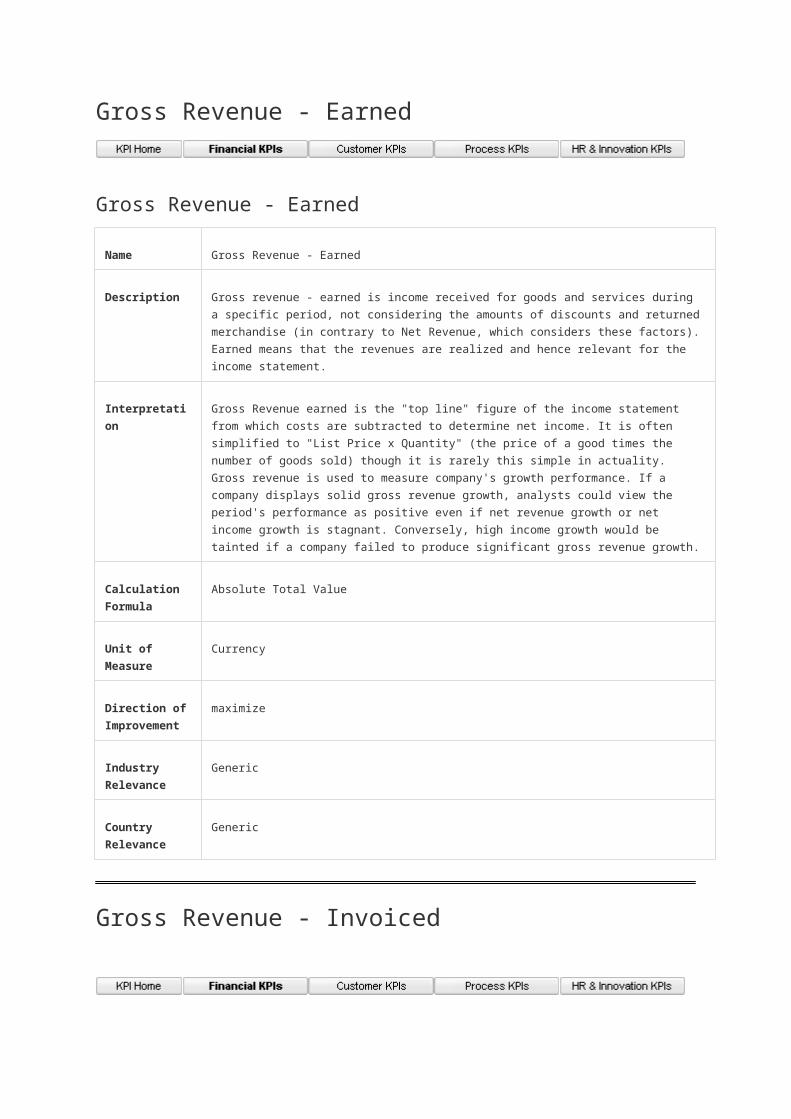

Gross Revenue - Earned

Gross Revenue - Earned

Name Gross Revenue - Earned

Description Gross revenue - earned is income received for goods and services during a specific period, not

considering the amounts of discounts and returned merchandise (in contrary to Net Revenue,

which considers these factors). Earned means that the revenues are realized and hence relevant

for the income statement.

Interpretation Gross Revenue earned is the "top line" figure of the income statement from which costs are

subtracted to determine net income. It is often simplified to "List Price x Quantity" (the price of a

good times the number of goods sold) though it is rarely this simple in actuality. Gross revenue is

used to measure company's growth performance. If a company displays solid gross revenue

growth, analysts could view the period's performance as positive even if net revenue growth or net

income growth is stagnant. Conversely, high income growth would be tainted if a company failed to

produce significant gross revenue growth.

Calculation

Formula

Absolute Total Value

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

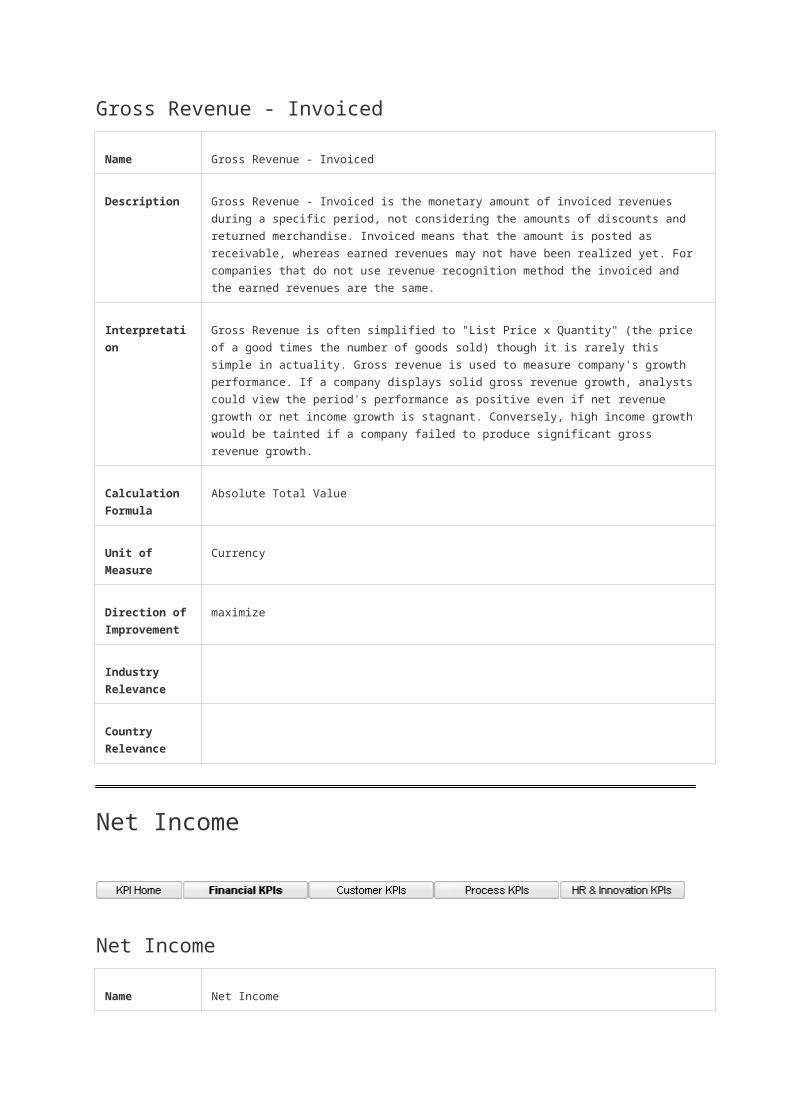

Gross Revenue - Invoiced

Gross Revenue - Invoiced

Name Gross Revenue - Invoiced

Description Gross Revenue - Invoiced is the monetary amount of invoiced revenues during a specific period,

not considering the amounts of discounts and returned merchandise. Invoiced means that the

amount is posted as receivable, whereas earned revenues may not have been realized yet. For

companies that do not use revenue recognition method the invoiced and the earned revenues are

the same.

Interpretation Gross Revenue is often simplified to "List Price x Quantity" (the price of a good times the number

of goods sold) though it is rarely this simple in actuality. Gross revenue is used to measure

company's growth performance. If a company displays solid gross revenue growth, analysts could

view the period's performance as positive even if net revenue growth or net income growth is

stagnant. Conversely, high income growth would be tainted if a company failed to produce

significant gross revenue growth.

Calculation

Formula

Absolute Total Value

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Net Income

Net Income

Name Net Income

Description Net income is a company's total earnings (or profit). Net income is calculated by subtracting costs,

expenses and taxes from the total revenue.

Interpretation Net income is sometimes called the bottom line because it is typically found on the last line of a

company's income statement. It is a useful snapshot of how profitable the company is over a

period of time. If a company's total expenses exceed its total revenues for a certain period, it can

be said to have a net loss. If revenues and expenses should turn out to be equal, the company will

have broken even. The change in net income reflects the trend of company's performance. In

general, when a company's net income is negative or is fairly low, this could suggest a myriad of

problems, ranging from inadequacies in customer or expenses management to unfavorable

accounting methods. Net income varies greatly from company to company and from industry to

industry. Generally, comparisons are most meaningful among companies within the same industry.

In addition to providing information on its own, net income is also frequently used to calculate other

figures in financial ratios in order to provide further information about a company's overall health,

for example, earnings per share, return on stockholder's equity. Note: As net income can be

changed considerably by various items such as changes in accounting principles, special items

and sales of discontinues operations, Earnings before interest and tax is more accuracy indicator

when analyzing business operating performance.

Calculation

Formula

Absolute Total Value from Income Statement

Unit of Measure Currency

Direction of

improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

Net Incoming Orders

Net Incoming Orders

Name Net Incoming Orders

Description Net Incoming Orders is the monetary amount of incoming sales and service orders during a

specific period, considering discounts and returned merchandise. It can be used for revenue

estimates and forecasting purposes.

Interpretation Net Incoming Orders is one of key indicators to monitor the sales activities occurring within

organization. As discounts and returned are included in net incoming orders, it is more precise

than gross incoming order in monitoring sales amount and comparing with net revenue invoiced

later. By analyzing the trend of net incoming orders, sales organization can optimize the sales

management resource, sales strategy, promotion campaign to achieve superior performance.

Stable growth of net incoming orders indicates that company has good sales perspective. It shows

that the product is gaining market share. If the net incoming order is steady over a period of time,

this generally means that the product has reached its maturity stage and demand is level.

Calculation

Formula

Net Incoming Orders = (Gross Incoming Orders) - (Sales Deductions) + (Merchandise Returned

from Credit) + (Allowances for Damaged or Missing Goods) + (Freight Out) + (Cash Discounts)

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

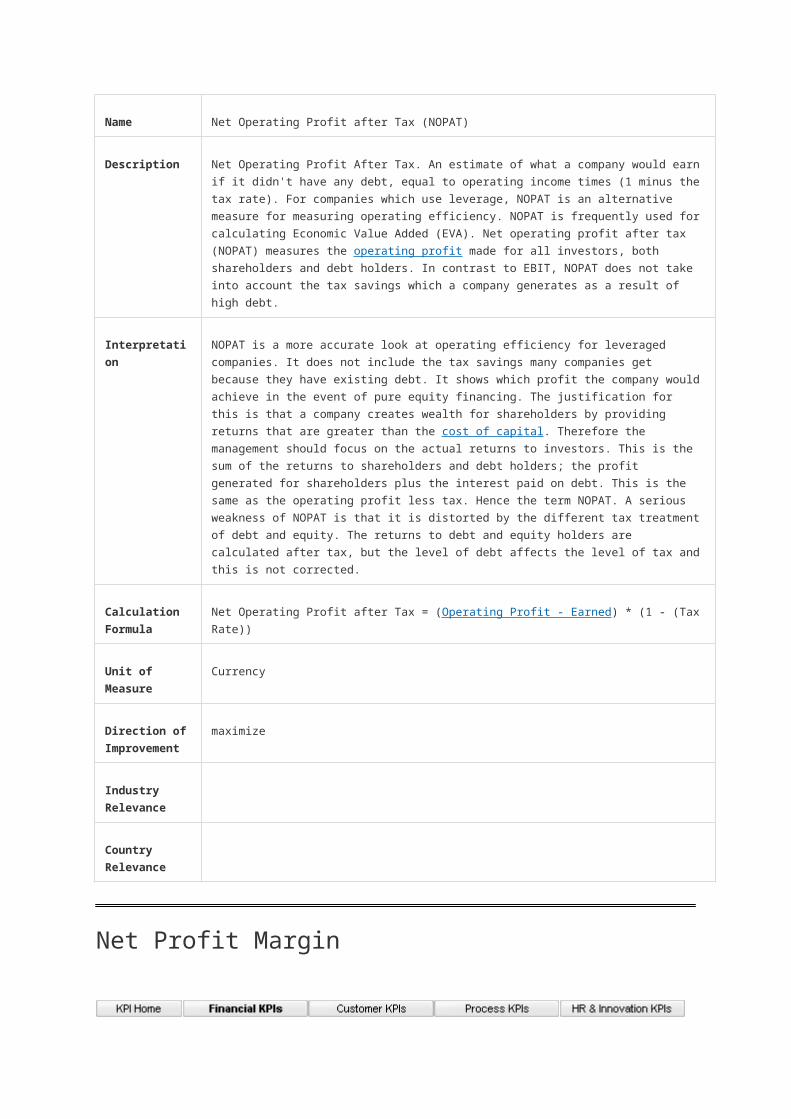

Net Operating Profit after Tax (NOPAT)

Net Operating Profit after Tax (NOPAT)

Name Net Operating Profit after Tax (NOPAT)

Description Net Operating Profit After Tax. An estimate of what a company would earn if it didn't have any

debt, equal to operating income times (1 minus the tax rate). For companies which use leverage,

NOPAT is an alternative measure for measuring operating efficiency. NOPAT is frequently used

for calculating Economic Value Added (EVA). Net operating profit after tax (NOPAT) measures the

operating profit made for all investors, both shareholders and debt holders. In contrast to EBIT,

NOPAT does not take into account the tax savings which a company generates as a result of high

debt.

Interpretation NOPAT is a more accurate look at operating efficiency for leveraged companies. It does not

include the tax savings many companies get because they have existing debt. It shows which

profit the company would achieve in the event of pure equity financing. The justification for this is

that a company creates wealth for shareholders by providing returns that are greater than the cost

of capital. Therefore the management should focus on the actual returns to investors. This is the

sum of the returns to shareholders and debt holders; the profit generated for shareholders plus the

interest paid on debt. This is the same as the operating profit less tax. Hence the term NOPAT. A

serious weakness of NOPAT is that it is distorted by the different tax treatment of debt and equity.

The returns to debt and equity holders are calculated after tax, but the level of debt affects the

level of tax and this is not corrected.

Calculation

Formula

Net Operating Profit after Tax = (Operating Profit - Earned) * (1 - (Tax Rate))

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

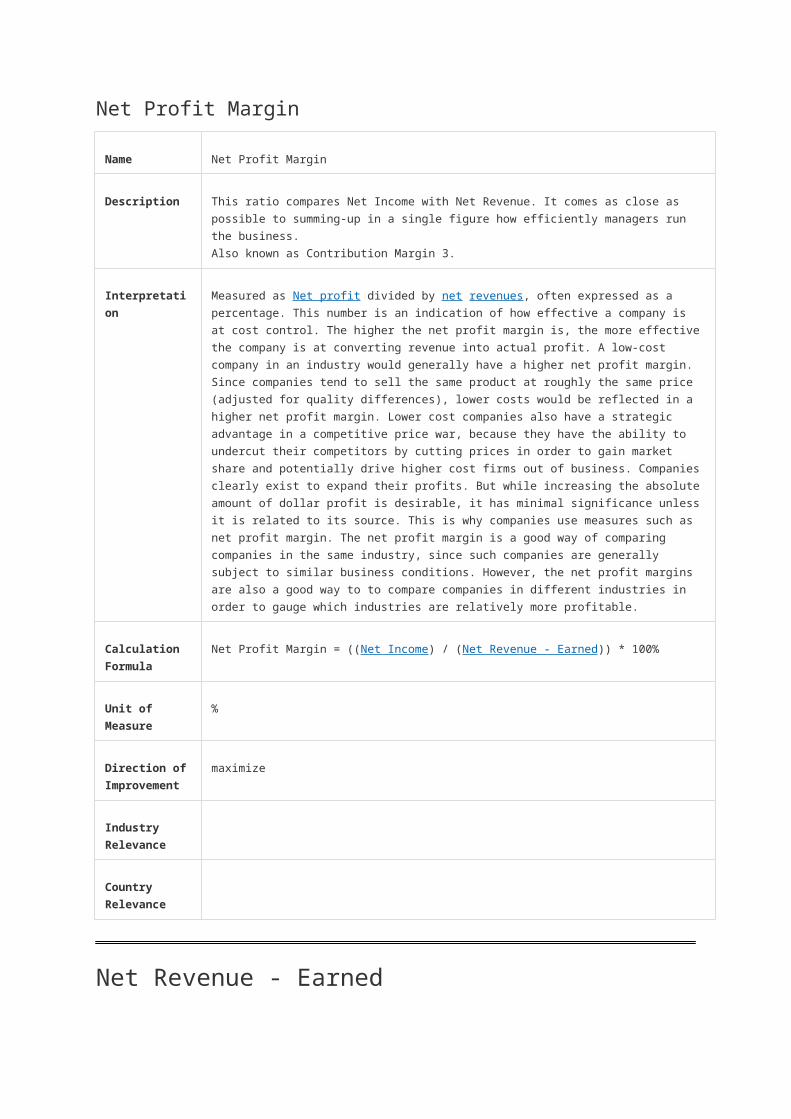

Net Profit Margin

Net Profit Margin

Name Net Profit Margin

Description This ratio compares Net Income with Net Revenue. It comes as close as possible to summing-up

in a single figure how efficiently managers run the business.

Also known as Contribution Margin 3.

Interpretation Measured as Net profit divided by net revenues, often expressed as a percentage. This number is

an indication of how effective a company is at cost control. The higher the net profit margin is, the

more effective the company is at converting revenue into actual profit. A low-cost company in an

industry would generally have a higher net profit margin. Since companies tend to sell the same

product at roughly the same price (adjusted for quality differences), lower costs would be reflected

in a higher net profit margin. Lower cost companies also have a strategic advantage in a

competitive price war, because they have the ability to undercut their competitors by cutting prices

in order to gain market share and potentially drive higher cost firms out of business. Companies

clearly exist to expand their profits. But while increasing the absolute amount of dollar profit is

desirable, it has minimal significance unless it is related to its source. This is why companies use

measures such as net profit margin. The net profit margin is a good way of comparing companies

in the same industry, since such companies are generally subject to similar business conditions.

However, the net profit margins are also a good way to to compare companies in different

industries in order to gauge which industries are relatively more profitable.

Calculation

Formula

Net Profit Margin = ((Net Income) / (Net Revenue - Earned)) * 100%

Unit of Measure %

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Net Revenue - Earned

Net Revenue - Earned

Name Net Revenue - Earned

Description Net Revenue - earned is a monetary amount of financial revenues during a specific period,

considering the amounts of discounts and returned merchandise (in contrary to Gross Revenue,

which does not consider these factors). Earned means that the revenues are realized and hence

relevant for the income statement.

Interpretation Net Revenue is a crucial part of any financial analysis. It represents the total finance revenue the

company collected for any goods provided and/or services performed after deducting sales return

and sales discount. Stable growth of net revenue indicates that company is in goods financial

standing. It shows that the product is gaining market share. If the company reports steady net

revenue over a period of time, this generally means that the product has reached its maturity stage

and demand is level.

Calculation

Formula

Net Revenue-Earned = (Gross Revenue - Earned) - ((Sales Deductions) + (Merchandise Returned

from Credit) + (Allowances for Damaged or Missing Goods) + (Freight Out) + (Cash Discounts))

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

Net Revenue - Invoiced

Net Revenue - Invoiced

Name Net Revenue - Invoiced

Description The monetary amount of invoiced revenues during a specific period, considering the amounts of

discounts and returned merchandise. Invoiced means that the amount is posted as receivable,

whereas earned revenues may not have been realized yet. For companies that do not use revenue

recognition method the invoiced and the earned revenues are the same.

Interpretation Net Revenue is a crucial part of any financial analysis. It represents the total finance revenue the

company collected for any goods provided and/or services performed after deducting sales return

and sales discount. Stable growth of net revenue indicates that company is in goods financial

standing. It shows that the product is gaining market share. If the company reports steady net

revenue over a period of time, this generally means that the product has reached its maturity stage

and demand is level.

Calculation

Formula

Net Revenue-Invoiced = (Gross Revenue - Invoiced) - ((Sales Deductions) + ( Merchandise

Returned from Credit) + (Allowances for Damaged or Missing Goods) + (Freight Out) + (Cash

Discounts))

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Net Revenue per Full Time Equivalent (FTE)

Net Revenue per Full Time Equivalent (FTE)

Name Net Revenue per Full Time Equivalent (FTE)

Description Net Revenue per Full Time Equivalent is calculated as a company's total net revenue --earned

divided by the number of its full time equivalent. It shows how much revenue each regular

employee generates. This ratio provides information on a company's efficiency within the peer

group.

Interpretation FTE or Full Time Equivalent is a unit of measure of an employee's or group's productivity. An FTE

of 1.0 means that the person, or group of people, is equivalent to a full-time worker. A person who

works half-time is counted as 0.5 FTE. FTE does not include contractual, temporary, or permanent

seasonal positions. An example of group with a full-time billing manager and a clerk who assists

him/her for about 10 hours/week has 1.25 FTE employees. (1 full-time + (40 hours/10 hours)) =

1.25 Net Revenue per Full Time Equivalent is basic measure of productivity. It is useful in

determining whether a corporation is being run efficiently. This ratio is very industry dependent.

Labor intensive businesses generally have low net revenue per FTE. When compared to the other

companies within same industry, it instantly gives a relative comparison of operational efficiency.

The higher the net revenue per FTE, the more efficient the operation, and therefore the more

sustainable and profitable. Another way to look at this is to look at the trend of specific companies.

If the revenue per FTE is stable over several years, it can be an indication that the business model

is still working well. Annual increase in revenue per FTE reveals the extent of productivity growth.

If the revenue per FTE is going down over time, it is an indication that the business is becoming

less efficient.

Calculation

Formula

Net Revenue per Full Time Equivalent = (Net Revenue - Earned) / (Full Time Equivalent)

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

Operating Profit - Earned

Operating Profit - Earned

Name Operating Profit - Earned

Description Operating Profit - Earned resulting from substracting operating expenses from Gross Profit-

Earned. It equals to the total operating result before interest, taxes and the financial result in the

Income Statement. * * * * Operating Profit excludes income and expenditure from unusual, non-

recurring or discontinued activities. In the US the ratio is also known as EBIT. Note: Operating

Profit is retrieved from the contribution margin analysis, while EBIT is from another data source,

income statement! Therefore this KPI is listed individually. > See "EBIT"

Interpretation Operating Profit is one of the most significant indicators of the company's profitability. It represents

the profit of a company before interest expenses and income taxes. Operating Profit is more focus

on the operating business itself, as it excludes income and expenditure from unusual activities,

and also interest income and expense, as well as taxes related to profitability are mostly the result

of factors. The figures are often used to gauge the financial performance of companies with high

levels of debt and interest expenses. From absolute number perspective, it shows how much profit

the company generates in order to be able to pay interest, taxes and dividends. The larger the

Operating Profit value, the more profitable the company is likely to be. The growth rate of

Operating Profit can be used to evaluate the company's growth. Sequential Operating Profit

increase is mostly due to higher sales and better operational performance. Operating Profit decline

could be mainly due to reduced revenue or increased manufacturing cost and operation costs.

Based on Operating Profit, Operating Profit Margin which is the ratio of Operating Profit to sales

can be calculated and used to compare Operating Profit profitability in different time periods for a

same company, or compare in different companies. Also See EBIT.

Calculation

Formula

Operating Profit-Earned = Total Value Resulting from Substracting Operating Expenses from

Gross Profit - Earned

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Operating Profit - Invoiced

Operating Profit - Invoiced

Name Operating Profit - Invoiced

Description Operating Profit - Invoiced resulting from substracting operating expenses from Gross Profit-

Invoiced. * * Operating Profit excludes income and expenditure from unusual, non-recurring or

discontinued activities. In the US the ratio is also known as EBIT. Note: Operating Profit is

retrieved from the contribution margin analysis, while EBIT is from another data source, income

statement! Therefore this KPI is listed individually. > See "EBIT" Invoiced means that Operating

Profit is only relevant to goods and services invoiced.

Interpretation Operating Profit is one of the most significant indicators of the company's profitability. It represents

the profit of a company before interest expenses and income taxes. Operating Profit is more focus

on the operating business itself, as it excludes income and expenditure from unusual activities,

and also interest income and expense, as well as taxes related to profitability are mostly the result

of factors. The figures are often used to gauge the financial performance of companies with high

levels of debt and interest expenses. From absolute number perspective, it shows how much profit

the company generates in order to be able to pay interest, taxes and dividends. The larger the

Operating Profit value, the more profitable the company is likely to be. The growth rate of

Operating Profit can be used to evaluate the company's growth. Sequential Operating Profit

increase is mostly due to higher sales and better operational performance. Operating Profit decline

could be mainly due to reduced revenue or increased manufacturing cost and operation costs.

Based on Operating Profit, Operating Profit Margin which is the ratio of Operating Profit to sales

can be calculated and used to compare Operating Profit profitability in different time periods for a

same company, or compare in different companies. Also See EBIT.

Calculation

Formula

Operating Profit-Invoiced = Total Value Resulting from Substracting Operating Expenses from

Gross Profit - Invoiced

Unit of Measure Currency

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Operating Profit - Ordered

Operating Profit - Ordered

Name Operating Profit - Ordered

Description Operating Profit - Ordered resulting from substracting operating expenses from Gross Profit-

Ordered. The Operating Profit ordered is used to determine the Operating Profit Margin ordered.

The ordered values are useful to calculate Income Statement forecasts.

Interpretation Operating Profit is one of the most significant indicators of the company's profitability. It represents

the profit of a company before interest expenses and income taxes. Operating Profit is more focus

on the operating business itself, as it excludes income and expenditure from unusual activities,

and also interest income and expense, as well as taxes related to profitability are mostly the result

of factors. The figures are often used to gauge the financial performance of companies with high

levels of debt and interest expenses. From absolute number perspective, it shows how much profit

the company generates in order to be able to pay interest, taxes and dividends. The larger the

Operating Profit value, the more profitable the company is likely to be. The growth rate of

Operating Profit can be used to evaluate the company's growth. Sequential Operating Profit

increase is mostly due to higher sales and better operational performance. Operating Profit decline

could be mainly due to reduced revenue or increased manufacturing cost and operation costs.

Based on Operating Profit, Operating Profit Margin which is the ratio of Operating Profit to sales

can be calculated and used to compare Operating Profit profitability in different time periods for a

same company, or compare in different companies. Also See EBIT.

Calculation

Formula

Operating Profit-Ordered = Total Value Resulting from Substracting Operating Expenses from

Gross Profit - Ordered

Unit of Measure Currency

Direction of

Improvement

maximize minimize range

Industry

Relevance

Country

Relevance

Operating Profit Margin - Earned

Operating Profit Margin - Earned

Name Operating Profit Margin - Earned

Description Relation of the Operating Profit Margin to Net Revenue: Shows how efficiently a company's

management has been in generating income from the operation of the business. Considers earned

values.

Also known as Contribution Margin 2.

Interpretation This indicator gives information on a company's profits ability based on earned values. Increase in

Operating Profit Marin is mainly due to growth of net revenue, good cost control and strong

productivity, Decrease in Operating Profit Margin largely results from reduction in revenue and

higher operating costs. Operating Profit Margin is most useful when compared against other

companies in the same industry. The higher Operating Profit Margin reflects the more efficient cost

management or the more profitable business. If no positive Operating Profit Margin can be

generated over a longer period, then the company should rethink the business model. Note: This

margin can be used as relative indicator for international, cross-industry comparisons. Operating

Profit Margin margin, however, varies greatly between industries, as factors both net revenue and

Operating Profit directly impact on the Operating Profit Margin. E.g. retailers have quite a small

Operating Profit Margin as they rely on small margins accompanied with high sales volume. Other

industries would have small sales volume but expect to offset that with higher Operating Profit

Margin.

Calculation

Formula

Operating Profit Margin-Earned= ((Operating Profit-Earned) / ((Net Revenue-Earned)) * 100%

Unit of Measure %

Direction of

improvement

maximize

Industry

Relevance

Country

Relevance

Operating Profit Margin - Invoiced

Operating Profit Margin - Invoiced

Name Operating Profit Margin - Invoiced

Description Relation of the Operating Profit Margin to Net Revenue: Shows how efficiently a company's

management has been in generating income from the operation of the business. Only Considers

invoiced values.

Interpretation This indicator gives information on a company's profits ability based on invoiced values. Increase

in Operating Profit Marin is mainly due to growth of net revenue, good cost control and strong

productivity, Decrease in Operating Profit Margin largely results from reduction in revenue and

higher operating costs. Operating Profit Margin is most useful when compared against other

companies in the same industry. The higher Operating Profit Margin reflects the more efficient cost

management or the more profitable business. If no positive Operating Profit Margin can be

generated over a longer period, then the company should rethink the business model. Note: This

margin can be used as relative indicator for international, cross-industry comparisons. Operating

Profit Margin margin, however, varies greatly between industries, as factors both net revenue and

Operating Profit directly impact on the Operating Profit Margin. E.g. retailers have quite a small

Operating Profit Margin as they rely on small margins accompanied with high sales volume. Other

industries would have small sales volume but expect to offset that with higher Operating Profit

Margin.

Calculation

Formula

Operating Profit Margin-Invoiced = ((Operating Profit-Invoiced) / (Net Revenue-Invoiced)) * 100%

Unit of Measure %

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Operating Profit Margin - Ordered

Operating Profit Margin - Ordered

Name Operating Profit Margin - Ordered

Description Relation of the Operating Profit Margin to Net Revenue: Shows how efficiently a company's

management has been in generating income from the operation of the business. Only Considers

ordered values.

Interpretation This indicator gives information on a company's profits ability based on ordered values. Increase in

Operating Profit Marin is mainly due to growth of net revenue, good cost control and strong

productivity, Decrease in Operating Profit Margin largely results from reduction in revenue and

higher operating costs. Operating Profit Margin is most useful when compared against other

companies in the same industry. The higher Operating Profit Margin reflects the more efficient cost

management or the more profitable business. If no positive Operating Profit Margin can be

generated over a longer period, then the company should rethink the business model. Note: This

margin can be used as relative indicator for international, cross-industry comparisons. Operating

Profit Margin margin, however, varies greatly between industries, as factors both net revenue and

Operating Profit directly impact on the Operating Profit Margin. E.g. retailers have quite a small

Operating Profit Margin as they rely on small margins accompanied with high sales volume. Other

industries would have small sales volume but expect to offset that with higher Operating Profit

Margin.

Calculation

Formula

Operating Profit Margin - Ordered =

(Operating Profit - Ordered / Net Revenue - Ordered) * 100%

Unit of Measure %

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Tools

o Business KPIs1. Business KPIs2. Process

Perfect (Purchase) Order

Skip to end of metadata Page restrictions apply Added by Christine Meyer, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Name Perfect (Purchase) Order

Description

Calculates the percentage of perfect purchase orders among all purchase orders.

The following criteria apply to a perfect order:

right quantitiy

damage free

arrives on-time

arrives at the right location

is filled completly on the first call

is entered correctly

is communicated via a customer-specific medium (e.g. EDI, fax, phone, internet etc)

has no invoicing or collection errors.

Interpretation

This KPI measures the ability of a vendor to deliver to the customers' wishes.

Perfect Order Characteristics:

has the right amount of products; is damage free; arrives on-time; arrives at the right location; is

filled completly on the first call; in entered correctly; is communicated via a customer-specific

medium (e.g. EDI, fax, phone, internet etc); has no invoicing or collection errors.

Calculation

Formula Perfect Order Calculation:

Order Fill-Rate * Order Shipping Accuracy * Damage free order percentage *On-Time Order

Percentage * claim free Order Percentage * Order Entry Accuracy * Order Comm Accuracy *

Order Doc Accuracy

Example Perfect Order Calculation:

has the right amount of products; 97%

is damage free; 98%

arrives on-time; 93%

arrives at the right location; 96%

is filled completly on the first call; 72%

in entered correctly; 94%

is communicated via a custoemr-specific medium (e.g. EDI, fax, phone, internet etc); 89%

has no invoicing or collection errors; 93%

===============================

48%

Unit of Measure %

Direction of

Improvement

Maximize

Industry

Relevance

ALL industries that want to measure their vendor compliance,

e.g. Consumer Product (CP) Industry, Process Industry.

Country

Relevance

Global

Tools

o Business KPIs1. Business KPIs2. Process

Inventory Days of Supply - Work in Process

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Nov 02, 2011 (view change) show comment

Go to start of metadata

Inventory Days of Supply - Work in Process

Name Inventory Days of Supply - Work in Process

Description Total gross value of inventory at standard cost before reserves for excess and obsolescence. Only

includes inventory on company books, future liabilities should not be included. Five point annual

average of the sum of all gross inventories of direct and indirect materials, where direct material

includes:

raw materials

WIP

plant FG, field FG, field samples

and indirect material consists of:

tangible fixed assets

low value assets

consumable goods

NOTE:

For indirect materials IDS-TOTAL only applies as long as they are in stock only, once they are in

use they are not "inventory" anymore. They turn into either "consumption" (? from a cost

perspective this is likely to be assigned to SGA) or into "tangible fixed assets" (? from a cost

perspective this is likely to cause the need for depreciation with the enterprise asset management

function typically within financials dept.)

This definition is in close alignment with SCOR 7.0.

Total gross value of inventory at standard cost before reserves for excess and obsolescence.

Only includes inventory on company books, future liabilities should not be included. Five point

annual average of the sum of all gross inventories (raw materials & WIP, plant FG, field FG, field

samples, other) ÷ (COGS ÷ 365).

Interpretation The Inventory-Days-of-Supply allows to estimate for how long a stock level of a certain material will

be sufficient to match upcoming requirements - basic assumption is a steady demand function.

Calculation

Formula

IDS-wip [BPX:days] = SUMn (IDS_goodn-classified-as-WIP) [BPX:days]

where the term of the SUM is derived from:

IDS_ goodn-classified-as-WIP [BPX:days]

= Stock-Value_ goodn [BPX:$]/Stock-Consumption_goodn [BPX:$/day]

and with the sub-terms defined as:

Stock-Value_ goodn [BPX:$] = Qty-per-Stock-Segment [BPX:UoM]

x Price [BPX:$/UoM]

Stock-Consumption_goodn [BPX:$/day] = Qty-per-Stock-Segment [BPX:UoM/day]

x Price [BPX:$/UoM]

NOTE1:

The assignment of material classes to certain stock elements maybe customer specific and needs

to be configurable. Details can be derived from Figure 2 and Figure 3.

NOTE2:

It is assumed that the product master contains:

a flag that indicates, what kind of material class a product belongs to (e.g. raw material, semi-

finished product, finished good etc.)

a suitable price that contains actual data per period, since the stock consumption always requires

a period to be specified, the lowest level of granularity will typically be a day (the calculation will

always relate to the past, so the fixed data may be assumed, no more shifts will happen.)

Unit of Measure days

Direction of

Improvement

Meet target value

Industry ALL industries that incorporate physical goods.

Relevance

Country

Relevance

GLOBAL

Tools

o Business KPIs1. Business KPIs2. Process

Inventory Days of Supply - Raw Material

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Nov 02, 2011 (view change) show comment

Go to start of metadata

Inventory Days of Supply - Raw Material

Name Raw Material

Description Total gross value of inventory at standard cost before reserves for excess and obsolescence. Only

includes inventory on company books, future liabilities should not be included. Five point annual

average of the sum of all gross inventories of direct and indirect materials, where direct material

includes:

raw materials

WIP

plant FG, field FG, field samples

and indirect material consists of:

tangible fixed assets

low value assets

consumable goods

NOTE:

For indirect materials IDS-TOTAL only applies as long as they are in stock only, once they are in

use they are not "inventory" anymore. They turn into either "consumption" (? from a cost

perspective this is likely to be assigned to SGA) or into "tangible fixed assets" (? from a cost

perspective this is likely to cause the need for depreciation with the enterprise asset management

function typically within financials dept.)

This definition is in close alignment with SCOR 7.0.[BPX: ]

Interpretation The Inventory-Days-of-Supply allows to estimate for how long a stock level of a certain material will

be sufficient to match upcoming requirements - basic assumption is a steady demand function.

Calculation

Formula

IDS-raw [BPX:days] = SUMn (IDS_goodn-classified-as-RAW) [BPX:days]

where the term of the SUM is derived from:

IDS_ goodn-classified-as-RAW [BPX:days]

= Stock-Value_ goodn [BPX:$] / Stock-Consumption_goodn [BPX:$/day]

and with the sub-terms defined as:

Stock-Value_ goodn [BPX:$] = Qty-per-Stock-Segment [BPX:UoM]

x Price [BPX:$/UoM]

Stock-Consumption_goodn [BPX:$/day] = Qty-per-Stock-Segment [BPX:UoM/day]

x Price [BPX:$/UoM]

NOTE1:

The assignment of material classes to certain stock elements maybe customer s\pecific and needs

to be configurable. Details can be derived from Figure 2 and Figure 3.

NOTE2:

It is assumed that the product master contains:

a flag that indicates, what kind of material class a product belongs to (e.g. raw material, semi-

finished product, finished good etc.)

a suitable price that contains actual data per period, since the stock consumption always requires

a period to be specified, the lowest level of granularity will typically be a day (the calculation will

always relate to the past, so the fixed data may be assumed, no more shifts will happen.)

Unit of Measure days

Direction of

Improvement

meet target value

Industry

Relevance

ALL industries that incorporate physical goods.

Country

Relevance

GLOBAL

bpx_business_kpis bpx_process_kpis

Tools

o Business KPIs

1. Business KPIs2. Process

Number of Contracts

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Number of Contracts

Name Number of Contracts

Description This KPI is defined as the number of maintained purchasing contracts in the system. Only valid

and released contracts are counted.

Interpretation Often the purchasing department wants to control the maximum of purchasing spend. Negotiating

prices and conditions with the supplier and maintaining them in purchasing contracts is the best

way to reach this objective, because then these prices and conditions are available as sources of

supply and can be used for operational purchasing.

Calculation

Formula

Number of Contracts = Number of Valid and Released Contracts Maintained in the System

Unit of Measure number

Direction of

Improvement

maximize

Industry

Relevance

generic

Country

Relevance

generic

1. Business KPIs2. Business KPIs3. Process

Ratio of Purchase Order Items with Product IDS

Skip to end of metadata

Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Ratio of Purchase Order Items with Product IDS

Name Ratio of Purchase Order Items with Product IDs

Description This KPI is defined as the ratio between the number of purchase order items with reference to a

product ID to the total number of purchase order items. Only sent purchase orders are taken into

account.

Interpretation With this number the buyers get to know if there are many purchase order items with no reference

to a product ID. Very often these purchase orders will have then a free text entry. If the ratio is

low, it is a hint to maintain product master in purchasing, if the purchasing activities shall be

controllable and effective.

Calculation

Formula

Ratio of Purchase Order Items with Product IDs =

((Number of sent purchase order items with a reference to a product ID) / (Total number of sent

purchase order items)) * 100%

Unit of Measure %

Direction of

Improvement

maximize

Industry

Relevance

generic

Country

Relevance

generic

1. Business KPIs2. Business KPIs3. Process

Price Trend

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Price Trend

Name Price Trend

Description The Price Trend compares the price of two different time intervals. The time interval can be year

or month. The Price Trend is calculated per product, but can be aggregated on product category,

supplier, country of supplier or on any organizational level.

Interpretation This KPI displays price changes on different levels and can be used to counter steer certain price

development in the market.

Calculation

Formula

Price Trend = (((Average Purchase Order Price of Current Period) - (Average Purchase Order

Price of a Previous Period)) / (Average Purchase Order Price of Previous Period)) * 100%

Unit of Measure %

Direction of

Improvement

minimize

Industry

Relevance

Generic

Country

Relevance

Generic

1. Business KPIs2. Business KPIs3. Process

Supplier Evaluation Score

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Supplier Evaluation Score

Name Supplier Evaluation Score

Description The Supplier Evaluation Score is the aggregated result of the manual and automatic

evaluation for a supplier. It is an outcome of the supplier evaluation.

Interpretation This KPI gives an overview how the suppliers perform.

Calculation Formula The calculation of the score is maintained by the user by defining relevant main criteria,

criteria and weighting factors between them.

Unit of Measure %

Direction of

Improvement

maximize

Industry Relevance Generic

Country Relevance Generic

Tools

o Business KPIs1. Business KPIs2. Process

Supplier-On Time Delivery Performance

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Supplier-On Time Delivery Performance

Name Supplier-On Time Delivery Performance

Description The KPI Supplier-On Time Delivery Performance is the comparison of the required delivery date

in the purchase order to the actual goods receipt entry date per supplier. For the calculation of

the Supplier-On Time Delivery Performance the delivery tolerances are respected.

Interpretation This KPI gives an overview how many deliveries were in time and how many arrived not in time.

This KPI is an important KPI to derive the supplier's performance.

Calculation 1. Is the actual delivery date in the goods receipt equal to the required delivery date in the purchase

Formulaorder/purchase order acknowledgement or in the defined tolerance for the delivery, the document

gets evaluated with a one.

2. Is the actual delivery date in the goods receipt not equal to the required delivery date in the

purchase order/purchase order acknowledgement and not in the defined tolerance for the

delivery, the document gets evaluated with a zero.

Supplier-On Time Delivery Performance = ((Number of purchase order items evaluated with one)

/ (Total number of purchase order items per supplier)) * 100%

Unit of Measure %

Direction of

Improvement

maximize

Industry

Relevance

generic

Country

Relevance

generic

Tools

o Business KPIs1. Business KPIs2. Process

First Call Resolution Rate

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

First Call Resolution Rate

Name First Call Resolution Rate

Description Shows the percentage of Service Order Items with only one related Service Confirmation Item.

Interpretation It is essential to track the effectiveness of the Field Organization. If it is taking more than one call

to complete a customer issue, it means that a process is broken somewhere (either in the

logistics process, or in the training/knowledge of the Field force).

Calculation

Formula

First Call Resolution Rate = (Number of Service Order Items with only one Related Service

Confirmation Item) / (Total Number of Service Order Items)

Unit of Measure %

Direction of

Improvement

Usually Maximize

Industry

Relevance

Country

Relevance

start of metadata

Sales Quantity - Earned

Name Sales Quantity - Earned

Description Sales Quantity - Earned is quantity of goods sold in a specified period. Earned means that the

sales quantity is matched with realized revenue in same period.

Interpretation By showing overall changes in sales quantity, sales, product, marketing and finance managers can

see at-a glance which region sales organization, product and customer group, etc. require

attention. The analyses of sales quantity answer common business questions as below, - Which

products have the greatest sales quantity and the least sales quantity? - What other products are

selling at the same time to the top sales customer? - Which products have declining sales

momentum? - How have sales quantities of product X changed period over period? - What is the

annual sales trend of each product? - How do promotion activities effort in sales quantities? In

general speaking, increase in sales quantity results in sales revenue if sales price and market

requirement remain fairly constant over a period. In reality, however, actual results may be

constrained by various factors, such as promotion campaign, competitors' sales strategy, change

of economics environment etc.

Calculation

Formula

Quantity

Unit of Measure UoM defined in MDM

Direction of

Improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

Tools

o Business KPIs1. Business KPIs2. Process

Sales Quantity - Invoiced

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Sales Quantity - Invoiced

Name Sales Quantity - Invoiced

Description Sales Quantity - Invoiced is quantity of goods sold in a specified period. Invoiced means that the

sales quantity is matched with invoiced revenue in same period.

Interpretation By showing overall changes in sales quantity, sales, product, marketing and finance managers can

see at-a glance which region sales organization, product and customer group, etc. require

attention. The analyses of sales quantity answer common business questions as below, - Which

products have the greatest sales quantity and the least sales quantity? - What other products are

selling at the same time to the top sales customer? - Which products have declining sales

momentum? - How have sales quantities of product X changed period over period? - What is the

annual sales trend of each product? - How do promotion activities effort in sales quantities? In

general speaking, increase in sales quantity results in sales revenue if sales price and market

requirement remain fairly constant over a period. In reality, however, actual results may be

constrained by various factors, such as promotion campaign, competitors' sales strategy, change

of economics environment etc.

Calculation

Formula

Quantity

Unit of Measure UoM defined in MDM

Direction of

Improvement

maximize

Industry

Relevance

Country

Relevance

Tools

o Business KPIs1. Business KPIs2. Process

Sales Quantity - Ordered

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Sales Quantity - Ordered

Name Sales Quantity - Ordered

Description Sales Quantity - Ordered is the sales quantity reflected in the incoming orders.

Interpretation By showing overall changes in sales quantity, sales, product, marketing and finance managers can

see at-a glance which region sales organization, product and customer group, etc. require

attention. The analyses of sales quantity answer common business questions as below, - Which

products have the greatest sales quantity and the least sales quantity? - What other products are

selling at the same time to the top sales customer? - Which products have declining sales

momentum? - How have sales quantities of product X changed period over period? - What is the

annual sales trend of each product? - How do promotion activities effort in sales quantities? In

general speaking, increase in sales quantity results in sales revenue if sales price and market

requirement remain fairly constant over a period. In reality, however, actual results may be

constrained by various factors, such as promotion campaign, competitors' sales strategy, change

of economics environment etc.

Calculation

Formula

Quantity

Unit of Measure UoM defined in MDM

Direction of

Improvement

maximize

Industry

Relevance

Generic

Country

Relevance

Generic

Tools

o Business KPIs1. Business KPIs2. Process

Discounts as % of Gross Revenue - Earned

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Discounts as % of Gross Revenue - Earned

Name Discounts as % of Gross Revenue - Earned

Description This indicator shows the ratio of total discounts to total Gross Revenue-Earned for a given period.

Interpretation Generally, the offering of discounts to customers is a form of price competition. Higher discounts

may result in increase in demand, especially for those customers who are price sensitive.

Discounts, on the other hand, sometimes are very damaging to profits because discounts affect

net income directly. It is possible to have good sales volume and productivity and still lose money.

By analyzing discounts as % of gross revenue, sales, product, marketing managers can promote

more effectively and discount more judiciously. Discounts as % of Gross Revenue reveals the

extent of discounting based on gross revenue and displays trends and responses to special

promotions. Increase in Discounts as % of Gross Revenue results in net revenue decreases,

provided list prices remain and discounts can not be offset by additional sales.

Calculation

Formula

Discounts as % of Gross Revenue-Earned = ((Discounts) / (Gross Revenue - Earned)) * 100%

Unit of Measure %

Direction of

Improvement

range

Industry

Relevance

Generic

Country

Relevance

Generic

Tools

o Business KPIs1. Business KPIs2. Process

Inventory Days of Supply - Direct Materials (IDS-DIR)

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Nov 02, 2011 (view change) show comment

Go to start of metadata

Inventory Days of Supply - Direct Materials (IDS-DIR)

Name Inventory Days of Supply - Direct Materials (IDS-DIR)

Description Total gross value of inventory at standard cost before reserves for excess and obsolescence. Only

includes inventory on company books, future liabilities should not be included. Five point annual

average of the sum of all gross inventories of direct and indirect materials, where direct material

includes: - raw materials - WIP - plant FG, field FG, field samples and indirect material consists of: *

tangible fixed assets * low value assets * consumable goods NOTE:

For indirect materials IDS-TOTAL only applies as long as they are in stock only, once they are in

use they are not "inventory" anymore. They turn into either "consumption" (from a cost perspective

this is likely to be assigned to SGA) or into "tangible fixed assets" (from a cost perspective this is

likely to cause the need for depreciation with the enterprise asset management function typically

within financials dept.) This definition is in close alignment with SCOR 7.0 (see URL of the Supply-

Chain Council www.supply-chain.org).

Interpretation The Inventory-Days-of-Supply allows to estimate for how long a stock level of a certain material will

be sufficient to match upcoming requirements - basic assumption is a steady demand function.

Calculation

Formula

Inventory Days of Supply-Total = (Inventory Days of Supply - Raw Material) + (Inventory Days of

Supply - Work in Process) + (Inventory Days of Supply - Finished Goods)

where the individual terms represent:

IDS-raw equals the valued sum of all goods assigned to "Raw Material".

IDS-wip equals the valued sum of all goods assigned to "Work-in-Process".

IDS-fgd equals the valued sum of all goods assigned to "Finished Goods".

Unit of

Measure

days

Direction Minimize

Industry

relevance

ALL industries that incorporate physical goods.

*Country * GLOBAL

[# ftnref1|BPX:1] Total gross value of inventory at standard cost before reserves for excess and obsolescence.

Only includes inventory on company books, future liabilities should not be included. Five point annual average of the

sum of all gross inventories (raw materials and WIP, plant FG, field FG, field samples, other) ÷ (COGS ÷ 365).

Tools

o Business KPIs1. Business KPIs2. Process

Opportunity Success Rate

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Opportunity Success Rate

Name Opportunity Success Rate

Description Number of Won Opportunities as % of the total closed Opportunities

Interpretation Providing information about won and lost opportunities the KPI helps the user to assess the sales

performance. This is much more valuable if you are able to compare it over a period whereby you

can find the trends in your sales performance. If calculated with respect to sales people, you can

set a benchmark for the entire team and any deviance needs to be studied.

Calculation

Formula

Opportunity Success Rate = (((Number of Opportunities-Status Won) / ((Number of Opportunities-

Status Won) + (Lost))) * 100%

Unit of Measure %

Direction of

Improvement

Usually: Maximize

Industry

Relevance

Opportunity Management only in industries with long pre-sales cycles.

Country

Relevance

Tools

o Business KPIs1. Business KPIs2. Process

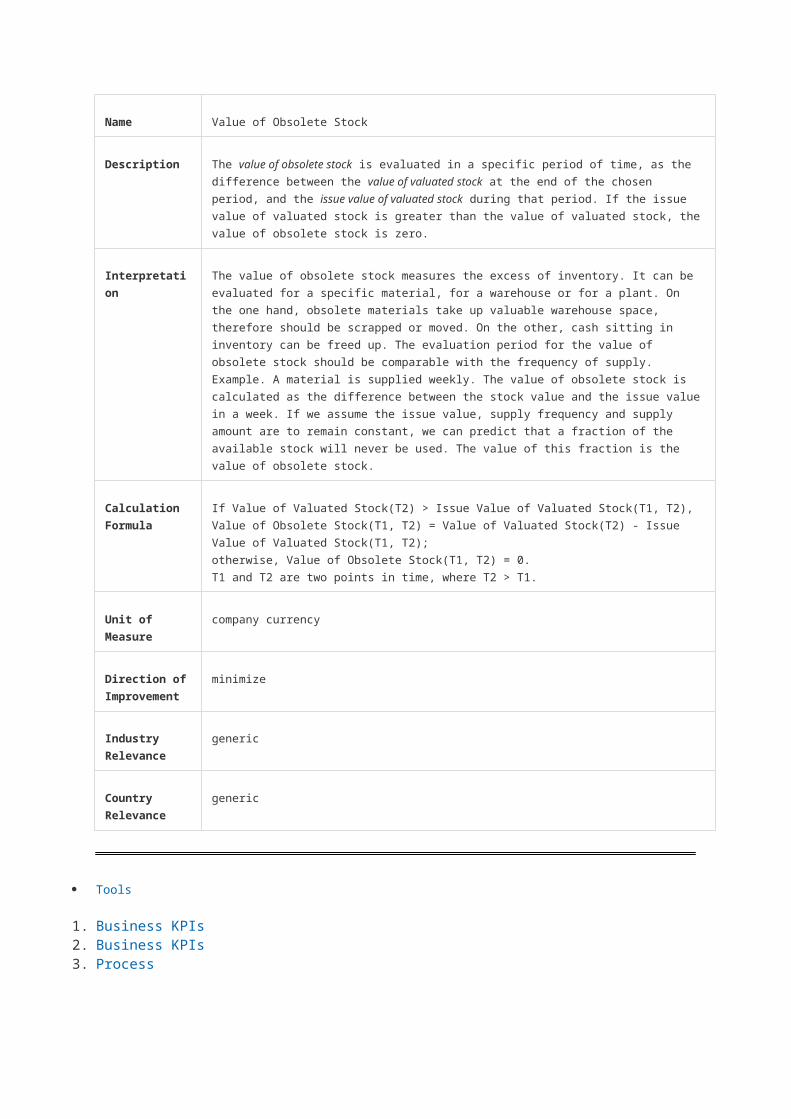

Value of Obsolete Stock

Skip to end of metadata Page restrictions apply Added by Davide Cavallari, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Value of Obsolete Stock

Name Value of Obsolete Stock

Description The value of obsolete stock is evaluated in a specific period of time, as the difference between the

value of valuated stock at the end of the chosen period, and the issue value of valuated stock

during that period. If the issue value of valuated stock is greater than the value of valuated stock,

the value of obsolete stock is zero.

Interpretation The value of obsolete stock measures the excess of inventory. It can be evaluated for a specific

material, for a warehouse or for a plant. On the one hand, obsolete materials take up valuable

warehouse space, therefore should be scrapped or moved. On the other, cash sitting in inventory

can be freed up. The evaluation period for the value of obsolete stock should be comparable with

the frequency of supply.

Example. A material is supplied weekly. The value of obsolete stock is calculated as the difference

between the stock value and the issue value in a week. If we assume the issue value, supply

frequency and supply amount are to remain constant, we can predict that a fraction of the

available stock will never be used. The value of this fraction is the value of obsolete stock.

Calculation

Formula

If Value of Valuated Stock(T2) > Issue Value of Valuated Stock(T1, T2), Value of Obsolete

Stock(T1, T2) = Value of Valuated Stock(T2) - Issue Value of Valuated Stock(T1, T2);

otherwise, Value of Obsolete Stock(T1, T2) = 0.

T1 and T2 are two points in time, where T2 > T1.

Unit of Measure company currency

Direction of

Improvement

minimize

Industry

Relevance

generic

Country

Relevance

generic

Tools

o Business KPIs1. Business KPIs2. Process

Vendors Fill Rate or Supplier performance

Skip to end of metadata Page restrictions apply Added by MURALIDHARA H.N, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Name Vendors Fill Rate or Supplier performance

Description In Retail Industry, vendor evaluation will not play major role. Therefore, we have to create Fill

rate based on ordered verses received Quantity.

Interpretation This KPI gives a hint how often the merchandising / purchasing department can fulfill users

requirements. The value of this KPI is dependent on the purchasing DC's performance

and/or from the quantity of reliability of `company's suppliers.

Calculation

Formula Vendor Fill Rate = (Supplied Quantity / Ordered Quantity) x 100%

This development can be handled through ABAP / BW with following Logic:* Article Number

is available at the Table EKPO as a field MATNR

Ordered = How much Purchase qty ordered for that Vendor, available at the EKPO table as

field MENGE, Current Month (Current month is Purchasing Document Date as a field in the

EKKO BEDAT)

Supplied = Against that Ordered qty how much Purchase qty been supplied by Vendor,

available at the MSEG table as field MENGE Current Month

Formula = Supplied/ Ordered*100

Unit of Measure %

Direction of

Improvement

maximize

Industry

Relevance

Generic but more specific Retail

Country

Relevance

Generic but very common in India

Tools

o Business KPIs1. Business KPIs2. Process

Average Lead Time of Service Requests

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Average Lead Time of Service Requests

Name Average Lead Time of Service Requests

Description Lead time is calculated as the time between creation of a Service Request and the setting of the

request status to Closed. It is displayed in hours. Division by Number of Service Requests gives

the Average Lead Time of Service Requests.

Interpretation Shows the average time required to complete Service Requests within the user's service

organization. It gives an indication of the efficiency of the internal processes, and is an important

factor that can influence customer satisfaction.

Calculation

Formula

Average Lead Time of Service Requests = (Lead Time of Service Requests) / (Number of

Service Requests)

Lead Time of Service Requests =

Time between Creation of a Service Request and the Setting of the Request Status to Closed-in

Hours

Unit of Measure Hours

Direction of

Improvement

Usually Minimize

Industry

Relevance

Country

Relevance

Tools

o Business KPIs1. Business KPIs2. Process

Quote Success Rate

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Quote Success Rate

Name Quote Success Rate

Description Order value of the quote items that have actually been converted to sales order items compared

to their original quote value.

Interpretation The Quote Success Rate can be used to analyze the quote value that is actually sold to the

customer. This in turn helps the user to monitor which products or services are popular and to

spot areas where action is required.

Calculation

Formula

Quote Success Rate = (Referred Value) / (Net Value of Accepted Quote Items)

Unit of Measure %

Direction of

Improvement

Usually: Maximize

Industry

Relevance

Country

Rekevance

Tools

o Business KPIs1. Business KPIs2. Process

Average Call Closure Time

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Oct 31, 2011 (view change) show comment

Go to start of metadata

Average Call Closure Time

Name Average Call Closure Time

Description Call Closure Time time is calculated as the time between creation of a Service Order and the

setting of the order status to Completed. It is displayed in hours. Division by the Number of

Service Orders gives the Average Call Closure Time.

Interpretation The Average Call Closure Time gives an indication of the efficiency of the internal processes,

and is an important factor that can influence customer satisfaction.

Calculation

Formula

Average Call Closure Time = (Call Closure Time) / (Number of Service Orders)

Call Closure Time =

Time between Creation of a Service Order and the Setting of the Order Status to Completed-in

Hours

Unit of Measure Hours

Direction of

Improvement

Usually Minimize

Industry

Relevance

Country

Relevance

1. Business KPIs2. Business KPIs3. Process

Inventory Days of Supply - Finished Goods

Skip to end of metadata Page restrictions apply Added by Florian Stapf, last edited by Alon Mizrahi on Nov 02, 2011 (view change) show comment

Go to start of metadata

Inventory Days of Supply - Finished Goods

Name Inventory Days of Supply - Finished Goods

Description Total gross value of inventory at standard cost before reserves for excess and obsolescence. Only

includes inventory on company books, future liabilities should not be included. Five point annual

average of the sum of all gross inventories of direct and indirect materials, where direct material

includes:

raw materials

WIP

plant FG, field FG, field samples

and indirect material consists of:

tangible fixed assets

low value assets

consumable goods

NOTE:

For indirect materials IDS-TOTAL only applies as long as they are in stock only, once they are in

use they are not "inventory" anymore. They turn into either "consumption" (? from a cost

perspective this is likely to be assigned to SGA) or into "tangible fixed assets" (? from a cost

perspective this is likely to cause the need for depreciation with the enterprise asset management

function typically within financials dept.)

This definition is in close alignment with SCOR 7.0.

Total gross value of inventory at standard cost before reserves for excess and obsolescence.

Only includes inventory on company books, future liabilities should not be included. Five point

annual average of the sum of all gross inventories (raw materials & WIP, plant FG, field FG, field

samples, other) ÷ (COGS ÷ 365).

Interpretation The Inventory-Days-of-Supply allows to estimate for how long a stock level of a certain material will

be sufficient to match upcoming requirements - basic assumption is a steady demand function.

Calculation

Formula

IDS-fgd [BPX:days] = SUMn (IDS_goodn-classified-as-FGD) / n [BPX:days]

where n is the no. of materials summed up and the term of the SUM is derived from:

IDS_ goodn-classified-as-FGD [BPX:days]

= Stock-Value_ goodn [BPX:$] / Stock-Consumption_goodn [BPX:$/day]

and with the sub-terms defined as:

Stock-Value_ goodn [BPX:$] = Qty-per-Stock-Segment [BPX:UoM]

x Price [BPX:$/UoM]

Stock-Consumption_goodn [BPX:$/day] = Qty-per-Stock-Segment [BPX:UoM/day]

x Price [BPX:$/UoM]

NOTE1:

The assignment of material classes to certain stock elements maybe customer specific and needs

to be configurable. Details can be derived from Figure 2 and Figure 3.

NOTE2:

It is assumed that the product master contains:

a flag that indicates, what kind of material class a product belongs to (e.g. raw material, semi-

finished product, finished good etc.)

a suitable price that contains actual data per period, since the stock consumption always requires

a period to be specified, the lowest level of granularity will typically be a day (the calculation will

always relate to the past, so the fixed data may be assumed, no more shifts will happen.)

Unit of Measure days

Direction of

Improvement

Meet target value

Industry

Relevance

ALL industries that incorporate physical goods.

Country

Relevance

GLOBAL