Embed Size (px)

Citation preview

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 1/69

1

AN INDUSTRY INTERNSHIP REPORT

A STUDY ON FACTORS INFLUENCING MUTUAL FUNDS ADVISIORY IN BANKS AND

PERFORMANCE ANALYSIS OF EQUITY FUNDS WITH RESPECT TO SBI.

PROJECT UNDERTAKEN

AT

SBI MUTUAL FUND

BANJARA HILLS

SUBMITTED BY

KANCHAN TIWARI

ROLLNO:2B2-20

PGDM- BIFAAS

Corporate guide Faculty guide

Mr.C.Sundeep Mr.D.Sreekanth

(Senior relationship manager) (Assistant professor)

SIVA SIVANI INSTITUTE OF MANAGEMENT

KOMPALLY

(2011-2013)

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 2/69

2

DECLARATION

I hereby declare that the project work “on factors influencing mutual fund advisory in banks and

performance analysis of equity fund with respect to SBI” submitted to Siva Sivani Institute of

Management, is a record of an original work done by me under the guidance of Mr. D.Sreekanth,

Assistant professor Siva Sivani Institute of Management, Secunderabad and this project work is

submitted in the partial fulfillment of the requirement for the award of Post Graduate Diploma in

Management. The results embodied in this report have not been submitted to any other University or

Institute for the award of any degree or diploma.

Place:

Date:

Name of the student

Roll number

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 3/69

3

ACKNOWLEDGEMENTS

First and foremost, I sincerely thank to my industry guide MR. SUNDEEP CHIKALA, Senior

Relationship Manager- Andhra Pradesh for his guidance and encouragement in carrying out this

project work.

I would like to show my deep sense of gratitude to internal project guide, Mr.D.Sreekanth Assistant

Professor Siva Sivani Institute of Management for her constant encouragement and support

throughout this project, especially for the useful suggestions given during the course of the project

period. She inspired and motivated me tremendously whenever I had any hesitation.

Besides, I am also grateful to faculty members of Siva Sivani Institute of Management for their

assistance in data collection.

I take this opportunity to extend my deep appreciation to my family and friends, for all that they

meant to me during the crucial times of the completion of my project.

Apart from my efforts, the success of my project depends largely on the encouragement and

guidelines of many others. I take this opportunity to express my gratitude to all the people who have

been instrumental in the successful completion of this project.

Place:

Date:

Name of the student

Roll number

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 4/69

4

TABLE OF CONTENT

SERIAL NO TOPIC PAGE NO

1 DECELERATION 2

2 ACKNOWLEDGEMENT 3

3 PREFACE 6

4 EXECUTIVE SUMMARY 7

5 CHAPTER 1:

INTRODUCTION TO MUTUAL FUNDS

OBJECTIVES OF STUDY

SCOPE OF STUDY

STRUCTURE OF MUTUAL FUND

SIGNIFICANCE OF MUTUAL FUND

ROLE OF SEBI

ROLE OF AMFI

ROLE OF MUTUAL FUND

WHY MUTUAL FUND SCHEME

HOW MUTUAL FUND OPERATE

ADVANTAGES AND DISADVANTAGES OF

MUTUAL FUND

TYPES OF FUNDS AND ITS DESCRIPTION

LITERATURE REVIEW

9

10

11

12

14

14

15

16

16

17

19 and 20

21

24

6 CHAPTER 2:

INDUSTRY PROFILE

COMPANY PROFILE

25

26

31

7 CHAPTER 3: RESEARCH METHODOLOGY

INTRODUCTION TO SBI MUTUAL FUND

PRODUCT

ABOUT EQUITY SCHEMES

3536

36

38

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 5/69

5

PARAMETER WHICH HELP IN

EVALUATION OF MUTUAL FUND BY

BANK

FACTOR INFLUENCING MUTUAL FUND

SCHEME FROM BANK PERSPECTIVE

TOOLS AND METHODS FOR RISK

MEASUREMENT

LIMITATION OF STUDY

48

50

53

56

8 CHAPETER 4:

DATA ANALYSIS AND INTERPERTATION 58

9 CHAPTER 5:

FINDINGS

RECOMMENDATION AND SUGGESTIONS

CONCLUSION

BIBLIOGRAPHY

64

65

67

68

69

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 6/69

6

PREFACE

Savings form an important part of the economy of any nation. With the savings invested in various

options available to the people, the money acts as the driver for growth of the country. Indian

financial scene too presents a plethora of avenues to the investors. Though certainly not the best or

deepest of markets in the world, it has reasonable options for an ordinary man to invest in his

savings.

Mutual fund offer several benefits that are unmatched by other investment options. Post

liberalization, the industry has been growing at a rapid pace and has crossed rs. 100000 core sizes in

terms of its assets under management. However, due to the low key investor awareness, the inflow

under the industry is yet to overtake the inflows in banks. Rising inflation, falling interest rates and a

volatile equity market make a deadly cocktail for the investor for whom mutual fund offer a route

out of the impasse. The investments in mutual funds are not without risks because the same forces

such as regulatory frameworks, government policies, interest rate structures, performance of

companies etc. that rattle the equity and debt market, act on mutual funds too. But it is the skill of

the managing risks the investment managers seek to implement in order to strive and generate

superior returns than otherwise possible that makes them a better option than many others.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 7/69

7

EXECUTIVE SUMMARY

In a few years mutual fund has emerged as a tool for ensuring one‟s financial well- being. Mutual

funds have not only contributed to the Indian growth story but have also helped families tap into the

success of Indian industry. As information and awareness more and more people are enjoying the

benefits of investing in mutual funds. The main reason the number of retail mutual fund investors

remain small is that nine in ten people with income in India do not know that mutual fund exist. But

once people are aware of mutual fund investment opportunities, the number who decide to invest in

mutual funds increases to as many as one in five people. The trick for converting a person with no

knowledge of mutual funds to a new mutual fund customer is to understand which of the potential

investors are more likely to buy mutual fund and to use the right argument in the sales process that

customer will accept as important and relevant to their decision. This project gave me a great

learning experience and at the same time it gave me a enough scope to implement my analytical

ability and what evaluation methods done for suggesting mutual fund scheme. The analysis and

advice presented in this project is based on factor influencing mutual fund advisory in banks and

what major criteria they look for suggesting to their customer. They prefer any particular asset

management company, which type of product they prefer, which opinion(growth or dividend ) they

prefer and which investment strategy they follow(systematic investment plan or one time plan).

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 8/69

8

CHAPTER 1:

INTRODUCTION TO MUTUAL FUNDS

OBJECTIVES OF STUDY

SCOPE OF STUDY

STRUCTURE OF MUTUAL FUND

SIGNIFICANCE OF STUDY

ROLE OF SEBI

ROLE OF AMFI

ROLE OF MUTUAL FUND

WHY MUTUAL FUND SCHEME

HOW MUTUAL FUND OPERATE

ADVANTAGES AND DISADVANTAGES OF MUTUAL FUND

TYPES OF FUNDS AND ITS DESCRIPTION

LITERATURE REVIEW

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 9/69

9

INTRODUCTION TO MUTUAL FUNDS AND ITS VARIOUS ASPECTS

Mutual fund act like a vehicle to mobilize money from investors to invest in different market

and securities in line with the investment objective agreed upon between the mutual fund and

investor.

It is a trust that pools the savings of number of investors who share a common financial goal.

This pool of money is invested in accordance with a stated objective.

The money thus collected is the invested in capital market instrument such as shares,

debentures and other securities. The income earned through these investment and capital

appreciation realized are shared by its unit holders in proportion the number of units owned

by them.

Thus mutual fund is the most suitable investment for the common man as it offers anopportunity to invest in a diversified, professionally managed basket of securities at

relatively low cost.

A mutual fund is an investment tool that allow small investor access to well diversified

portfolio of equities, bonds and other securities. Each shareholder participates in the gain or

loss of fund. Units are issued and can be redeemed as needed. The fund‟s net asset value is

determined every day.

Investments in each security are spread across wide cross section of industries and sectors

that risk is reduced.

Diversification reduces the risk because all stocks may no move in the same direction and in

the same proportion at the same time.

Mutual fund issue units to the investors in accordance with quantum of money invested by

them investors of mutual fund are known as unit holders.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 10/69

10

OBJECTIVES OF STUDY

My project title “Factor‟s influencing mutual funds advisory in banks”. Its primary objective is to

emphasis a relation between mutual fund and bank.

However the detailed objectives are as follows:

To understand the factor influencing mutual funds advisory in SBI.

To assess performance of selected mutual funds.

To compare and evaluate the performance.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 11/69

11

SCOPE OF STUDY

The main purpose of doing this project was to know about mutual funds and its functioning. This

helps to know in details about mutual funds industry right from its inception stage, growth and

future prospects.

It also helps in understanding different schemes of mutual funds. Because my study depends on

prominent funds in India and their schemes like equity, income , balance as well as the return

associated with those schemes.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 12/69

12

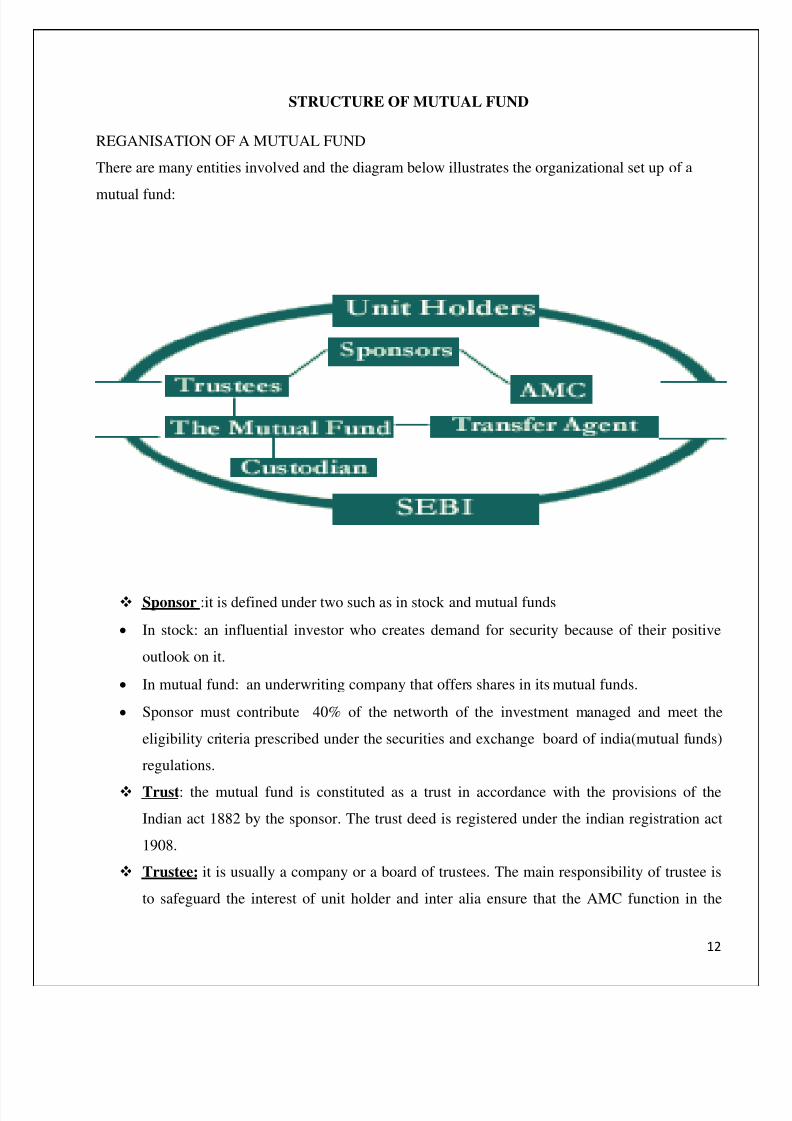

STRUCTURE OF MUTUAL FUND

REGANISATION OF A MUTUAL FUND

There are many entities involved and the diagram below illustrates the organizational set up of a

mutual fund:

Sponsor :it is defined under two such as in stock and mutual funds

In stock: an influential investor who creates demand for security because of their positive

outlook on it.

In mutual fund: an underwriting company that offers shares in its mutual funds.

Sponsor must contribute 40% of the networth of the investment managed and meet the

eligibility criteria prescribed under the securities and exchange board of india(mutual funds)

regulations.

Trust: the mutual fund is constituted as a trust in accordance with the provisions of the

Indian act 1882 by the sponsor. The trust deed is registered under the indian registration act

1908.

Trustee: it is usually a company or a board of trustees. The main responsibility of trustee is

to safeguard the interest of unit holder and inter alia ensure that the AMC function in the

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 13/69

13

interest of investor and in accordance with the securities and exchange board of India. At

least 2/3 of directors of the trustee are independent directors who are not associated with the

sponsor.

Asset management company: The Amc is appointed by trustee as the investment manager

of the mutual fund. The AMC is required to be approved by the securities and exchange

board of India to act asset management company of mutual fund. At least 50% of the

directors of the AMC are independent directors who are not associated with the sponsors in

any manner.

Transfer agent: The AMC is appointed by the Trust deed appoints the registrar process and

application form, redemption request and dispatches account statement to the unit holders.

The transfer agent also handles communication with investors and update investor records.

Custodian: The custodian has custody of the assets of funds and custodian needs to accept

and give delivery of securities for the purchase and transactions of the various schemes of the

fund.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 14/69

14

SIGNIFICANCE OF STUDY:

Mutual funds plays an vital role and it has wide importance.

ROLE OF SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI):

The following are the regulations put forth by SEBI to protect the investors‟ interest:

Every mutual fund must be recognized with SEBI and registration is granted only where

SEBI is satisfied with the background of the fund.

SEBI (Mutual funds) regulations, 1996 lays down the provisions for the appointment of the

trustees and their obligations. The regulations have also laid down the provisions for the

approval of the AMC and the custodian.

Every new scheme launched by a mutual fund needs to be filed with SEBI and SEBI reviews

the document in regard to the disclosures contained in such documents.

Regulations have been laid down regarding listing of funds, refund procedures, transfer

procedures, disclosures, guaranteeing returns etc.

SEBI has also laid down advertisement code to be followed by a mutual fund in making any

publicity regarding a scheme and its performance.

SEBI has prescribed norms/ restrictions for investment management with a view to

minimize/ reduce undue investment risks. SEBI has the authority to inspect the books of accounts, records and documents of a mutual

fund, its trustees, AMC and custodian where it deems it necessary. SEBI also has the

authority to initiate penal actions against an erring MF.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 15/69

15

ROLE OF ASSOCIATION OF MUTUAL FUND IN INDIA(AMFI)

The mutual fund industry has trade association called Association of mutual Funds in India

(AMFI) modeled on the lines of a self-regulating organization (SRO) with a view to

promoting and protecting the interest of mutual funds and their unit holders, increasing

public awareness of mutual funds, and serving the investor‟s interest by defining and

maintaining high ethical and professional standards in the mutual funds industry. AMFI plays

an important role in disciplining members and assist the regulatory authority in protecting

investor‟s interest.

One of the most effective industry bodies today is probably the Association of mutual funds

in India (AMFI). It has been a forum where mutual fund has been able to present their views,

debate and participate in creating their own regulatory framework. The association was

created originally as a body that would lobby with the regulator to on matters long before

regulations are framed, and it is often initiates many regulatory changes that prevent

malpractices that emerge from time to time.

AMFI works through a number of committees, some of which are standing committees to

address areas where there is a need for a constant vigil and improvements and other which

are adhoc committees constituted to address specific issues. These committees consist of

industry professionals from among the member mutual funds. AMFI has now decided to

become a self- regulatory organization since it has worked so effectively as an industry body.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 16/69

16

ROLE OF MUTUAL FUND:

The primary role of mutual fund is to assist investors in earning an income or building their

wealth, by participating in the opportunities available in various securities and markets.

It is possible for mutual funds to structure a scheme for any kind of investment objective.

In the mutual funds industry the fund and scheme are used inter changeably and various

categories of schemes are called funds

Money raised from investors, ultimately benefits governments, companies or other entities.

As a large investor, the mutual funds can keep a check on the operations of the investors

company and their corporate governance and ethical standards.

The projects that are facilitated through such financing, offer employment to people.

Mutual fund industry offers livelihood to a large number of employees of mutual funds,distributors, registrars and various other service providers.

Higher employment income and output in the economy boost the revenue collection of the

government through taxes and other means.

Mutual funds viewed as a key participant in the capital market of any economy.

WHY MUTUAL FUND SCHEMES?

Mutual fund scheme seek to mobilize money from all possible investors.

Various investors have different investment preferences.

In order to accommodate these preferences, mutual funds mobilize different pools of money.

Each such pool of money is called a mutual fund scheme.

Every scheme has a pre- announced investment objective.

HOW DO MUTUAL FUND SCHEMES OPERATE?

Mutual fund scheme announce their investment objective and seek investments form the

public

Depending on how the scheme is structured, it may be open to accept money from investors,

either during a limited period only or at any time.

The investment that an investor makes in a scheme is translated into a certain number of units

in the scheme. Thus, an investor in a scheme is issued units of the scheme.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 17/69

17

Under the law, every unit has a face value of rs 10.

The face value is relevant from an accounting perspective. The number of units multiplied

by its face value (RS 10 ) is the capital of the scheme- its unit capital

The schemes earn interest income or dividend income on the investments in holds

When it purchases and sells investments, it earns capital gains or incurs capital losses. These

are called realized capital gains or realized capital losses.

Investment owned by the scheme may be quoted in the market at higher than the cost paid

such gains in values on securities held is called valuations gains.

There can be valuation losses when securities are quoted in the market at a price below the

cost at which the scheme acquired them.

Running the scheme leads to its share of operating expenses.

Investments can be said to have been handled profitably, if the following profitability metric

is positive:

A. Interest income

B. Dividend income

C. Realized capital gains

D. Valuation gains

E. Realized capital losses

F. Valuation losses

G. Scheme expenses

When the investment activity is profitable, the true worth of unit goes up and when there are

losses the true worth of unit goes down. The true worth of unit of the scheme is otherwise

called Net Asset Value(NAV) of the scheme.

When a scheme is first made available for investment it is called a „New Fund Offer(NFO)‟.

During the NFO investors may have the chance of buying the units at their face value.

Post NFO when they buy into a scheme, they need to pay a price that is linked to its NAV.

Profits or losses as the case might be belonging to the investors. The investor does not

however bear a loss higher than the amount invested by him.

Various investors subscribing to investment objective might have different expectations on

how the profit is to be handled.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 18/69

18

Some may like it to be paid off regularly as dividends, others might like the money to grow

in the scheme.

Mutual fund address such differential expectations between investors within a scheme, by

offering various options such as:

a. Dividend payout option,

b. Dividend re- investment option and

c. Growth option

An investor buying into a scheme gets to select the preferred option also.

The relative size of mutual fund companies is assessed by their assests under

management(AUM).

When a scheme is first launched, asset under management would be the amount mobilized

from investors.

If the scheme has a positive profitability metric, its AUM goes up; a negative profitability

metric will pull it down.

If the scheme is open to receiving money from investors even post NFO then such

contributions from investors boost the AUM.

Conversely, if the scheme pays any money to the investors, either as dividend or as

consideration for buying back the units of investors, the AUM falls

The AUM thus captures the impact of the profitability metric and the flow of unit holder

money to or from the scheme.

ADVANTAGES OF MUTUAL FUNDS FOR INVESTORS:

Professional management- mutual funds offers investors the opportunity to earn an income or

build their wealth through professional management of their investible funds.

Portfolio diversification- units of scheme give investors exposure to a range of securities held

in the investment portfolio of the scheme. Thus, even a small investment of rs 5000 in amutual fund scheme can be giving investors a diversified investment portfolio.

Economies of scale- the pooling of large sums of money from so many investors makes it

possible for the mutual fund to engage professional managers to manage the investment.

Individual investor with small amounts to invest cannot, by themselves, to engage such

professional management.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 19/69

19

Liquidity – sometimes, investors in financial market are struck with a security for which they

can‟t find a buyer- worse at times they can‟t find the company the invested in such

investment become illiquid investments, which can end in a complete loss for investors.

Tax deferral- mutual funds are not liable to pay tax on the income they earn. If the same

income were to be earned by the investor directly, then tax may have to be paid in the same

financial year.

Tax benefits- specific schemes of mutual funds give investors that are liable to tax. This

reduces their taxable income and therefore the tax liability.

The dividend that the investor receives from the scheme, is tax-free.

Convenient options- the options offered under a scheme allow investors to structure their

investments in line with their liquidity preference and tax position.

Investment comfort- once an investment is made with a mutual fund, they make it convenient

for the investor to make further purchases with very little documentation. This simplifies

subsequent investment activity.

Regulatory comfort- the regulator, securities and exchange board of India (SEBI) has

mandated strict checks and balances in the structure of mutual funds and their activities.

DISADVANTAGES:

Costs: mutual funds don‟t exist solely to make your life easier – all funds are in it for a profit.

The mutual fund industry is masterful at burying costs over under layers of jargon. These costs

are so complicated that in this tutorial we have devoted an entire section to the subject.

Dilution: It‟s possible to have too much diversification. Because funds have small holdings in so

many different companies, high returns from a few investments often don‟t make much

difference on the overall return. Dilution is also the result of a successful fund getting too big.

When money pours into funds that have had strong success, the manager often has trouble

finding a good investment for all the new money.

Taxes: when making decisions about your money, fund managers don‟t consider your personal

tax situation. For example, when a fund manager sells a security, a capital-gain tax is triggered,

which affects how profitable the individual is from the sale. It might have been more

advantageous for the individual to defer the capital gains liability

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 20/69

20

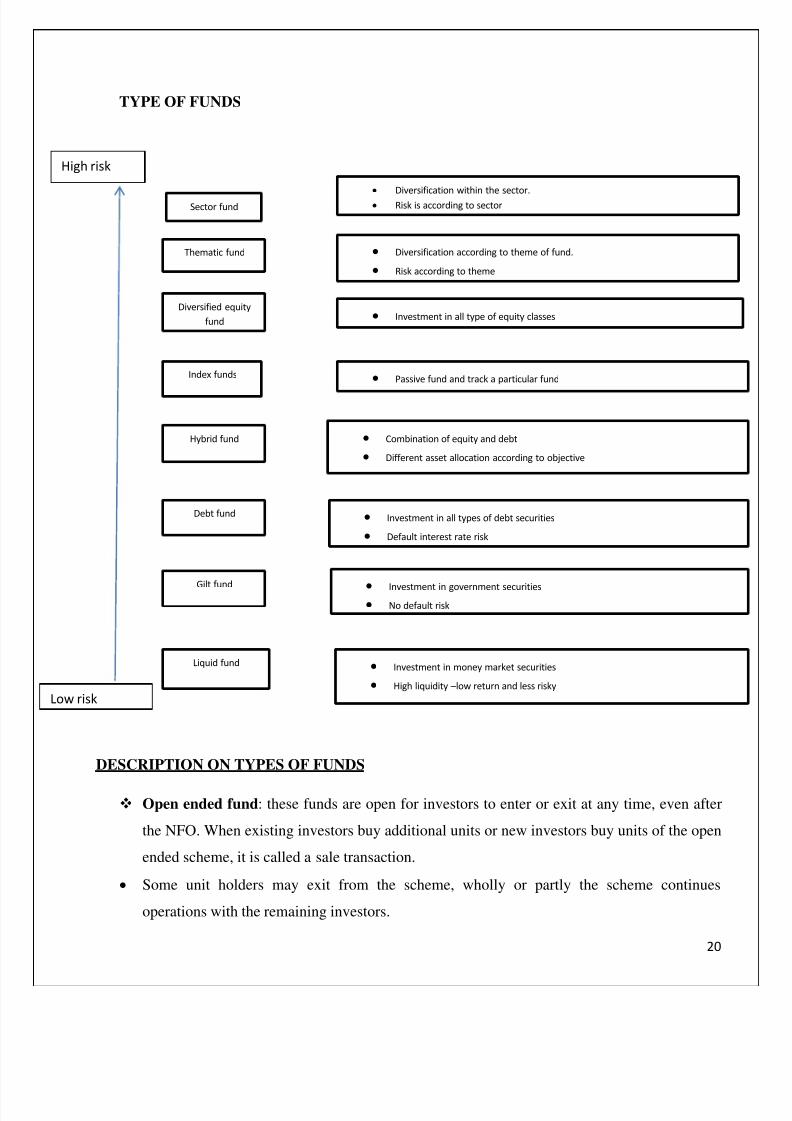

TYPE OF FUNDS

DESCRIPTION ON TYPES OF FUNDS

Open ended fund: these funds are open for investors to enter or exit at any time, even after

the NFO. When existing investors buy additional units or new investors buy units of the open

ended scheme, it is called a sale transaction.

Some unit holders may exit from the scheme, wholly or partly the scheme continues

operations with the remaining investors.

Sector fund

Thematic fund

Diversified equity

fund

Index funds

Hybrid fund

Debt fund

Gilt fund

Liquid fund

Diversification within the sector.

Risk is according to sector

Diversification according to theme of fund.

Risk according to theme

Investment in all type of equity classes

Passive fund and track a particular fund

Combination of equity and debt

Different asset allocation according to objective

Investment in all types of debt securities

Default interest rate risk

Investment in government securities

No default risk

Investment in money market securities

High liquidity –low return and less risky

High risk

Low risk

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 21/69

21

The scheme does not have any kind of time frame in which it is to be closed.

The ongoing entry and exit of investors implies that the unit capital in an open ended fund

would keep changing on a regular basis.

Close ended fund: these funds are also called as fixed maturity fund. In this investors can

buy units of a close ended scheme from the fund only during its NFO.

The funds makes arrangement for the units to be traded, post NFO in a stock exchange. This

is done through a listing of the scheme in a stock exchange. Such listing is compulsory for

close ended scheme.

Post NFO investors who want to buy units will have to find a seller for those units in the

stock exchange.

Similarly investors who want to sell units will have to find a buyer for those units in the stock

exchange.

Post NFO sale and purchase of units happen to or from a counter- party in the stock

exchange and not to or from the mutual fund the unit of the scheme remains stable.

Interval funds: this fund has combine features of both open-ended and close ended

schemes.

Largely close ended but become open ended at pre-specified intervals.

For instance an interval scheme might become open-ended between January 1 to 15 and July

1 to 15 each year.

Benefit for investor is that, unlike in a purely close-ended scheme, they are not completely

dependent on the stock exchange to be able to buy or sell units of the interval fund.

Actively managed funds: these funds are funds where the fund manger has the flexibility to

choose the portfolio, within the broad parameters of the investment objective of the scheme.

This increases the role of the fund manager, the expenses for running the fund turn out to be

higher. Investors expect actively managed funds to perform better than the market.

Passive funds: these funds invested on the basis of a specified index, whose performance it

seeks to track. Thus, a passive fund tracking the BSE Sensex would buy only the shares that

are part of the composition of the BSE Sensex.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 22/69

22

Equity fund: a scheme might have an investment objective to invest largely in equity shares

and equity related investments like convertible debentures, such schemes are called equity

schemes.

Debt fund: schemes with an investment objective that limits them to investments in debt

securities like treasury bills, government securities, bonds and debentures are called debt

funds.

Hybrid funds: these funds have an investment charter that provides for reasonable level of

investment in both debt and equity.

Gilt funds: these funds invest only in treasury bills and government securities, which do not

have a credit risk(i.e. the risk that the issuer of the security defaults).

Floating rate funds: these funds invest largely in floating rate debt securities i.e. debt

securities where the interest rate is payable by the issuer changes in line with the market.

Liquid schemes or money market schemes: these schemes are variant of debt schemes that

invest only in debt securities where the money will be repaid within 91-days. These schemes

are widely recognized to be the lowest in risk among all kinds of mutual fund schemes.

Gold funds: these funds invest in gold and gold-related securities. They can be structured in

either of the following formats such as:

Gold exchange traded fund which is like an index fund that invests in gold. The NAV

of such funds moves in line with gold prices in the market. Gold sector funds i.e. the fund will invest in shares of companies engaged in gold

mining and processing.

Funds of funds: funds can be structured to invest in various other funds, whether in India or

abroad such funds are called „funds of funds‟. These „funds of funds‟ prespecify the mutual

funds whose schemes they will buy and the kind of scheme they will invest in. these scheme

have been designed to help investors get over the trouble choosing between multiple schemes

and their variants in the market.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 23/69

23

LITERATURE REVIEW

Literature on mutual fund performance is enormous. A few research studies that have influenced the

preparation drawing on results obtained in the field of portfolio analysis, economist jack l. tenor has

suggested a new predictor of mutual fund performance one that differs from virtually all those usedpreviously by incorporating the volatility of a fund‟s return. Michael . C. Jensen derived a risk-

adjusted measure of portfolio performance(Jensen‟ alpha) that estimates how much a manager‟s

forecasting ability contributes to fund‟s returns. As indicated by Stat man (2000) the e SDAR of

fund portfolio is the excess return of the portfolio over the return of the benchmark index where the

portfolio is leveraged to have the benchmark index‟s standard deviation. S. Narayan rao evaluated

performance of Indian mutual funds in a bear market through relative performance index. Risk

return analysis, trenyor‟s ratio, Sharpe‟s ratio. Sharpe‟s measure, Jensen measure and Fama‟s

measure. The result of performance measure suggest that most of mutual fund scheme in the sample

of 58 were able to satisfy investor‟s expectations by giving return over expected return based on both

premium for systematic risk and tool risk. The result suggests that the use of conditioning lagged

information variables improves the performance mutual fund scheme and reducing number of timing

coefficients. Measures of evaluating portfolio performance using lower partial moment. It helping in

the measures of evaluating portfolio performance based on lower partial moment .Goal performing

model is employed to determine proportion of selected mutual fund in the final portfolios. The study

found that socially responsible funds do not differ significantly from conventional funds in terms of

any of these attributes. The effect of diversification performance is not different between the groups.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 24/69

24

CHAPTER 2:

INDUSTRY PROFILE

COMPANY PROFILE

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 25/69

25

INDUSTRY -MUTUAL FUNDS PROFILE

If you've ever applied for your company's 401k, you've undoubtedly invested your earnings in a

mutual fund. Most companies give you a menu of mutual fund choices to pick from and a bunch of

books that describe what securities each fund invests in. As of December 2008, mutual funds were a

$9.6 trillion industry. Simply, mutual funds are professionally managed funds that collect money

from people to invest in a range of securities including stocks, bonds, money markets, and other

investments. If the fund is actively managed, then the fund manager makes trades on a regular basis.

But there are many mutual funds that are called index funds that mirror the performance of various

indexes like the Standard & Poor's 500 and do not need to make a lot of trades, and thus a fund

manager.

Mutual fund managers can work for one of the larger firms like Fidelity Investments, CapitalResearch, or Vanguard Group or work for one of the many smaller private funds. Managers arecharged with forecasting investor cash flows into and out of the fund, as well as future performance

of investments in the fund. Different mutual funds have different investment objectives, and the fundmanager must choose the appropriate securities for that objective. The one goal that is among allmanagers is to outperform certain benchmarks, like the Standard & Poor's 500 index, which tracks500 large U.S. companies. Sometimes travel is necessary for managers to talk with customers, meetcompanies to analyze their financial statements, visit factories, or whatever research the managersees appropriate to make a sound decision on the fund.

Mutual fund managers generally major in business, economics, accounting or math, but many havebackgrounds in computer science, engineering, physics or biology. Besides a MBA, many managershave an investment qualification such as Chartered Financial Analyst (CFA). Fresh MBAs are rarelyrecruited for manager positions, but can rise to the position by starting out as research analysts, who

research various securities and the institutions that have issued them, as well as making investmentrecommendations to the manager.

GENESIS OF MUTUAL FUND:

Mutual fund emerged in the UK and US as investment management institutions in the earlytwentieth century during the 1920‟s. The origin of the mutual fund may however be tracked to thedays of ancient geese where merchants banded together to take shares in commercial undertakings.Similar arrangements existed in Rome and Europe also where merchants in colonial America used totake shares in voyages which when completed would be liquidated and assets divided amongthemselves. The Scottish America investments trust was formed in 1873 to hold portfolio of

American rail road bonds and shares in trust were issued to the interested citizens of Dundee. Mostof these schemes were of closed type and the shares were sold and purchased at the market rates andthe law of demand and supply set the price.

The concept of mutual fund was experimented in the US from the 1920‟s and institutional businesswas becoming popular in the late 1940‟s. As the financial climate during the early 1980‟s enhanced

the competitiveness of certain investment the number and type of mutual funds.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 26/69

26

In the UK during 1920‟s the accepting houses emerged as a major force in the business of

investment management activities. Investment management has its genesis in the deployment of thelarge fortunes made by some of the Victorian merchant bankers. But the only in 1950 the acceptinghouses rapidly built up on their existing skill and knowledge to deal with increasing capital. Theinvestment trust was superseded by the Unit Trust as small savers means of access to professional

management.

HISTORY OF THE INDIAN MUTUAL FUND INDUSTRY:

The mutual fund industry in India started in 1963 with the formation of unit trust of India, at theinitiative of the government of India and reserve bank. The history of mutual funds in India can bebroadly divided into four distinct phases

First phase:1964-1987

Unit trust of India (UTI) was established on 1963 by an act of parliament. It was set up by the

reserve bank of India and functional under the regulatory and administrative control over the reservebank of India. In 1978 UTI was de-linked from the RBI and the Industrial Development Bank of India (IDBI) took over the regulatory and administrative control in place of RBI. The first schemelaunched by UTI was unit scheme 1964. At the end of 1988 UTI had rs 6,700 crores of assets undermanagement.

Second phase: 1987-1993 (entry of public sector funds):

1987 marked the entry of non-UTI, public sector mutual funds set up by public sector banks and lifeinsurance Corporation of India (LIC) and general Insurance Corporation of India (GIC). SBI mutualfund was the first non-UTI mutual fund established in June 1987 followed by canbank mutual fund

(DEC 87), Punjab national bank mutual fund (AUG 89), Indian bank mutual fund (NOV 89), bank of India(JUN 90 ), bank of Baroda mutual fund(OCT 92). LIC established its mutual fund in June1989 while GIC had set up its mutual fund in December 1990.

At the end of 1993, the mutual fund industry had assets under management of rs 47,004 crores.

Third phase: 1993-2003(entry of private sector funds)

With the entry of private sector funds in 993, a new era started in the Indian mutual fund industry,giving the Indian investors a wider choice of fund families. Also, 1993 was the year in which thefirst mutual fund regulations came into being, under which all mutual funds, expect UTI were to be

registered and governed. The erstwhile Kothari pioneer (now merged with franklin Templeton) wasthe first private sector mutual fund registered in July 1993.

The 1993 SEBI regulations were substituted by a more comprehensive and revised mutual fundregulations in 1996. The industry now functions under the SEBI regulations 1996.

The number of mutual fund houses went on increasing with many foreign mutual funds setting upfunds in India and also the industry has witnessed several mergers and acquisitions. As at the end of

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 27/69

27

January 2003, there were 33 mutual funds with mutual funds with total assets of rs 1,21,805 crores.The unit Trust of India with rs 44,541 crores of assets under management was way ahead of othermutual funds.

Fourth phase: since February 2003

In February 2003, following the repeal of the unit trust of India Act 1963 UTI was bifurcated intotwo separate entities. One is the specified undertaking of the Unit Trust of India with assets undermanagement of rs 29,835 crores at the end of January 2003, representing broadly, the assets of us 64schemes, assured return and certain other schemes. The specified undertaking of Unit Trust of India,functioning under an administrator and under the rules framed by government of India and does notcome under the purview of the mutual fund regulations.

The second is the UTI mutual fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered withSEBI and functions under the Mutual Fund Regulations. With the bifurcation of the erstwhile UTIwhich had in march 2000 more than rs 76,000 crore of assets under management and with the setting

up of a UTI mutual fund, conforming to the SEBI mutual funds, the mutual fund industry hasentered its current phase of consolidation and growth. As at the end of October 31 2003, there were31 funds which manage assets of rs 126726 crores under 386 schemes.

UNIT TRUST OF INDIA (UTI)

UTI US-64 scheme has faced repeated problems owing to the administrative setting of entry/exitprices. In order to protect investors, Government interventions became necessary. Theseinterventions have accompanied by structural improvements also, most importantly, US-64 nowreports NAV on daily basis, and all new investors face a purely NAV-driven scheme, with noadministrative pricing. In the coming months, further efforts aimed at turning UTI into a normal

SEBI regulated mutual fund are expected.

FINANCIAL INTERVENTIONS INTO US-64 SCHEME

1. Special unit scheme 1999 (SU-99): on June 29, 1999, government of India did a buyback from UTI of psu shares at book value, which was higher than the then prevailing marketvalue. This effectively constituted a transfer of RS. 1,528 crore to the investors in US-64.

2. Limited repurchase facility (july, 2001): investors were given a window through which up to3000 units could be sold back to UTI, so that the investors exiting would not do so at theexpense of investors who did not exit. This programmed covered roughly 40 percent of theassets of US-64.

3. Extended repurchase facility (December, 2001): in December, 2001 the limit of 3000 unitswas raised to 5000 units. In addition, investors above 5000 units were given an assurance thatif they exited in May 2003, they would get the higher of NAV or Rs. 10. Once again,government would make up the gap between repurchase price and NAV experienced by UTI,if any.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 28/69

28

DIFFERENT MUTUAL FUNDS ARE AS FOLLOWS:

Reliance mutual fund, ICICI mutual fund, HDFC mutual fund, LIC mutual fund, kotak mutual fund.

Reliance mutual fund:

Reliance Mutual Fund, a part of the Reliance Group, is one of the fastest growing mutual funds inIndia. RMF offers investors a well-rounded portfolio of products to meet varying investorrequirements and has presence in 179 cities across the country. Reliance Mutual Fund constantlyendeavors to launch innovative products and customer service initiatives to increase value toinvestors. Reliance Capital Asset Management Limited („RCAM‟) is the asset manager of Reliance

Mutual Fund. RCAM a subsidiary of Reliance Capital Limited, which holds 92.93% of the paid-upcapital of RCAM, the balance paid up capital being held by minority shareholders.

Reliance Capital Ltd. is one of India‟s leading and fastest growing private sector financial services

companies, and ranks among the top 3 private sector financial services and banking companies, interms of net worth. Reliance Capital Ltd. has interests in asset management, life and generalinsurance, private equity and proprietary investments, stock broking and other financial services.

Sponsor : Reliance Capital Limited

Trustee : Reliance Capital Trustee Co. Limited

Investment Manager /

AMC : Reliance Capital Asset Management Limited

Statutory Details : The Sponsor, the Trustee and the Investment Manager are incorporatedunder the Companies Act 1956.

ICICI mutual fund:

ICICI Prudential Asset Management Company Ltd. (IPAMC/ the Company) is the joint venturebetween ICICI Bank, a well-known and trusted name in financial services in India and Prudential,one of UK‟s largest players in the financial services sectors. IPAMC was incorporated in the year

1993. The Company in a span of over 18 years since inception and just over 13 years of the JointVenture, has forged a position of preeminence in the Indian Mutual Fund industry as the third largestasset management company in the country, contributing significantly to the growth of the Indianmutual fund industry.

ICICI Bank offers a wide range of banking products and financial services to corporate and retailcustomers through a variety of delivery channels and through its specialized subsidiaries in the areasof investment banking, life and non-life insurance, venture capital and asset management.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 29/69

29

HDFC mutual fund:

HDFC Asset Management Company Ltd (AMC) was incorporated under the Companies Act, 1956,on December 10, 1999, and was approved to act as an Asset Management Company for the HDFCMutual Fund by SEBI vide its letter dated July 3, 2000.

The registered office of the AMC is situated at Ramon House, 3rd Floor, H.T. Parekh Marg, 169,Back bay Reclamation, Church gate, Mumbai - 400 020.

In terms of the Investment Management Agreement, the Trustee has appointed the HDFC AssetManagement Company Limited to manage the Mutual Fund. The paid up capital of the AMC is Rs.25.169 crore.

LIC mutual fund:

Life Insurance Corporation of India set up LIC Mutual Fund on 19th June 1989 and contributed Rs.2 Crores towards the corpus of the Fund. LIC Mutual Fund was constituted as a Trust in accordancewith the provisions of the Indian Trust Act, 1882. The settlor is not responsible for the managementof the Trust. The settlor is also not responsible or liable for any loss or shortfall resulting in any of the schemes of LIC Mutual Fund. The Trustees of the LIC Mutual Fund have exclusive ownership of Trust Fund and are vested with general power of superintendence, discretion and management of theaffairs of the Trust. LIC Mutual Fund Asset Management Company Ltd. was formed on 20th April1994 in compliance with the Securities and Exchange Board of India (Mutual Funds) Regulations,1993. The Company commenced business on 29th April 1994. The Trustees of LIC Mutual Fundhave appointed LIC Mutual Fund Asset Management Company Ltd. as the Investment Managers forLIC Mutual Fund. The Trustees are responsible for appointing a Custodian. The Trustees should also

ensure that the activities of the Trust and the Asset Management Company are in accordance withthe Trust Deed and the SEBI Mutual Fund Regulations as amended from time to time. The Trusteeshave also to report periodically to SEBI on the functioning of the Fund.

KOTAK mutual fund:

We are sponsored by Kotak Mahindra Bank Limited, one of India's fastest growing banks, with apedigree of over twenty years in the Indian Financial Markets. Kotak Mahindra Asset ManagementCo. Ltd., a wholly owned subsidiary of the bank, is our Investment Manager.

We made a humble beginning in the Mutual Fund space with the launch of our first scheme inDecember, 1998. Today we offer a complete bouquet of products and services suiting the diverseand varying needs and risk- return portfolios of investors.

We are committed to offering innovative investment solutions and world-class services andconveniences to facilitate wealth creation for our investors.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 30/69

30

COMPANY PROFILE

SBI MUTUAL FUND IDENTITY:

With 25 years of rich experience in fund management, we at SBI Funds Management Pvt. Ltd. bring

forward our expertise by consistently delivering value to our investors. We have a strong and proudlineage that traces back to the State Bank of India (SBI) - India's largest bank. We are a JointVenture between SBI and AMUNDI (France), one of the world's leading fund managementcompanies.

With our network of over 222 points of acceptance across India, we deliver value and nurture thetrust of our vast and varied family of investors.

Excellence has no substitute. And to ensure excellence right from the first stage of productdevelopment to the post-investment stage, we are ably guided by our philosophy of „growth throughinnovation‟ and our stable investment policies. This dedication is what helps our customers achieve

their financial objectives.

Our Vision

“To be the most preferred and the largest fund house for all asset classes, with a consistent track

record of excellent returns and best standards in customer service, product innovation, technologyand HR practices.”

Our Services

MUTUAL FUNDS

Investors are our priority. Our mission has been to establish Mutual Funds as a viable investmentoption to the masses in the country. Working towards it, we developed innovative, need-specificproducts and educated the investors about the added benefits of investing in capital markets viaMutual Funds.

Today, we have been actively managing our investor's assets not only through our investmentexpertise in domestic mutual funds, but also offshore funds and portfolio management advisoryservices for institutional investors.

This makes us one of the largest investment management firms in India, managing investment

mandates of over 5.4 million investors.

Portfolio Management and Advisory Services

SBI Funds Management has emerged as one of the largest player in India advising various financialinstitutions, pension funds, and local and international asset management companies.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 31/69

31

We have excelled by understanding our investor's requirements and terms of risk / returnexpectations, based on which we suggest customized asset portfolio recommendations. We alsoprovide an integrated end-to-end customized asset management solution for institutions in terms of advisory service, discretionary and non-discretionary portfolio management services.

OFFSHORE FUNDS

SBI Funds Management has been successfully managing and advising India's dedicated offshorefunds since 1988. SBI Funds Management was the 1st bank sponsored asset management companyfund to launch an offshore fund called 'SBI Resurgent India Opportunities Fund' with an objective toprovide our investors with opportunities for long-term growth in capital, through well-researchedinvestments in a diversified basket of stocks of Indian Companies.

FUND HOUSE EXPERTISE

INVESTMENT EXPERTISE

The best investment strategies put together by the best minds, our Fund Managers. With a sharp eyeto monitor, gauge and understand the changes in the market, our fund managers and analysts gear upto meet new challenging environments. Their ability to capture the growth potential of Indiansecurities and manage complex portfolios as well as the drive to deliver optimum results is theirforte. With superior securities selection, incisive research, intensive coverage including internalforecasts, active monitoring and regular tracking, our dedicated team ensures minimization of riskswhile protecting our investor's interest. Always.

INVESTMENT PHILOSOPHY

Growth through innovation.Our expert team of experienced and market savvy researchers prepare comprehensive analytical andinformative reports on diverse sectors and identify stocks that promise high performance in thefuture.

What is innovation?

Innovation is the process of turning ideas into concrete plans for progressive growth. We alwaysseek to provide our investors with opportunities for progressive growth through our innovativeproducts, superior stock selection and active portfolio management. Accordingly, we also enhanceand optimize asset allocation and stock selection based on internal and external research. Derivatives

are used to hedge and rebalance portfolios to keep the risk factors at reasonable levels,

The three main phrases, which act as a guiding force for the investment performance, are as follows:

Long-term capital appreciation for the investor: Our fund manager's view is not guided byany momentum play but by the objective of generating sustainable performance for theinvestor.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 32/69

32

Superior stock selection: Our team is encouraged to be ahead of the rest of the industry interms of identifying new ideas & opportunities.

Active fund management: While the performance of all the funds is benchmarked against aspecific index, we do not encourage our investment team to replicate the index compositionwith the fund portfolio.

Optimal Risk Management

Risk Management is an inherent part of any business. As one of the core focus areas, each of ourstrategies is subject to close scrutiny on a continuous basis. Regulatory agencies around the worldare placing increasing pressure on institutions to measure and manage risk better. At SBI FundsManagement, we follow enterprise wide approach to risk management with a dedicated, experiencedand professional risk management team covering significant functions of the organization. Risk Management focuses on:

Identifying actual and potential areas of risk

Assessing the adequacy of internal controls Proposing risk mitigating measures and Safeguarding investor interest through ongoing analysis and monitoring

Investment Objective

Setting benchmarks time and again. For our investors.

Our objective is to endeavor to outperform our benchmarks through well researched investments inIndian equities. This is achieved by implementing an active management style based on fundamentalanalysis, leading to the construction of a portfolio. It could be blended, large cap, mid cap, or

specific sector oriented - which aims at capturing the growth potential of Indian equities.

PRODUCTS:

Every investor is unique.

At SBI Mutual Fund we know that every investor has unique financial goals and requires a differentset of products. Which is why, we have a wide range of schemes that fulfill every kind of investors‟

requirements. Each scheme is managed by devising a different strategy which is reflective of theinvestors profile and carries with it different risks and rewards.

There are six basic asset classes, which we manage, and variations of these six asset classes formvarious products:

Equity Schemes: The primary objective of the equity asset class is to provide capital growth / appreciation.

Hybrid Schemes: These schemes invest in a mixture of debt and equity securities in differentproportions.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 33/69

33

Debt / Income Schemes: The schemes in this asset class generally invest in fixed incomesecurities.

Fixed Maturity Plans: These are closed ended debt schemes with a fixed maturity date . Liquid Schemes The strategy for liquid funds include investments in short investment. Exchange Traded Funds ETFs are nothing but a basket of securities that are traded on the

stock exchange.

COMPETITOR OF SBI MUTUAL FUND:

1. ICICI mutual fund2. Reliance mutual fund3. UTI mutual fund4. Birla Sun Life mutual fund5. Kotak mutual fund6. HDFC mutual fund7. Sundaram mutual fund

8.

LIC mutual fund9. Principal10. Franklin Templeton

AWARDS AND ACHIEVEMENT OF SBI MUTUAL FUND:

LIPER AWARD- THE LIPPER INDIA FUND AWARDS 2008

ICRA MUTUAL FUND AWARD 2008

OUTLOOK MONEY- NDTV PROFIT AWARDS

CNBC- AWAAZ CONSUMER AWARD 2007

LIPPER AWARD - THE LIPPER INDIA FUND AWARDS 2007

ICRA MUTUAL FUND AWARD 2007 CNBC TV18- CRISIL MUTUAL FUND OF THE YEAR AWARD 2007

CNBC AWAAZ CONSUMER AWARDS 2006

LIPPER AWARD- THE LIPPER INDIA FUND AWARDS 2006

CNBC TV18- CRISIL MUTUAL FUND OF THE YEAR AWARD 2006

ICRA MUTUAL FUND AWARD 2005

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 34/69

34

CHAPTER 3:

RESEARCH METHODOLOGY

INTRODUCTION TO SBI MUTUAL FUND PRODCUT

ABOUT EQUITY SCHEMES

PARAMETER WHICH HELP IN EVALUATION OF MUTUAL FUND BY BANK

FACTOR INFLUENCING MUTUAL FUND SCHEME FROM BANK PERSPECTIVE

TOOLS AND METHODS FOR RISK MEASUREMENT

LIMITATION OF STUDY

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 35/69

35

METHODOLOGY INVOLVED

This report is based on secondary data, however secondary data collection was given more

importance since it is overhearing factor. One of the most important users of research methodology

is that it helps in identifying the problem, collecting, analyzing the required information data andproviding an alternate solution to the problem. It also helps in collecting the vital information that is

required by the top management to assist them for the better decision making both day to day

decision and critical ones.

DATA SOURCES

Research is totally based on Secondary data can be used only for the reference. Research has been

done by secondary data collection . The secondary data has been collected through various mutual

fund company‟s websites

INTRODUCTION ABOUT SBI MUTUAL FUND PRODUCTS

Equity schemes

Debt/ income schemes

Liquid schemes

Hybrid schemes

Fixed maturity plans

Exchanges traded schemes

Fund of fund scheme

EQUITY SCHEMES

The primary objective of the equity asset class is to provide capital growth / appreciation byinvesting in the equity and equity related instruments of companies over medium to long term.

Equity/ Growth Funds

SBI Magnum Multicap Fund

SBI Magnum Equity Fund SBI Magnum Multiplier Plus 1993 SBI Blue Chip Fund SBI Magnum Global Fund SBI One India Fund SBI Magnum Midcap Fund

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 36/69

36

Sectoral Funds

SBI Magnum Sector Funds Umbrella - Emerging Businesses Fund SBI Magnum Sector Funds Umbrella - Contra Fund SBI Magnum Sector Funds Umbrella - FMCG Fund

SBI Magnum Sector Funds Umbrella - IT Fund SBI Magnum Sector Funds Umbrella - Pharma Fund

Thematic Funds

SBI Magnum COMMA Fund SBI Infrastructure Fund - Series I SBI PSU Fund

ELSS Funds

SBI Tax Advantage Fund - Series I SBI Tax Advantage Fund - Series II SBI Magnum Tax gain Scheme 1993

Index Funds

SBI Magnum Index Fund

Market Neutral Strategy

SBI Arbitrage Opportunities Fund

Debt / Income Schemes

The schemes in this asset class generally invest in fixed income securities such as bonds, corporatedebentures, government securities (gilts), money market instruments, etc. and provide regular andsteady income to investors.

SBI Magnum Children's Benefit Plan SBI Magnum Income Plus Fund - Saving Plan SBI Magnum Income Fund Floating Rate Plan - Savings Plus Bond Plan

SBI Magnum Income Fund Floating Rate Plan - Long Term SBI Magnum Income Fund

SBI Dynamic Bond Fund SBI Magnum Gilt Fund - Short Term Plan SBI Magnum Gilt Fund - Long Term Plan SBI Short Horizon Debt Fund - Short Term Fund SBI Short Horizon Debt Fund - Ultra Short Term Fund

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 37/69

37

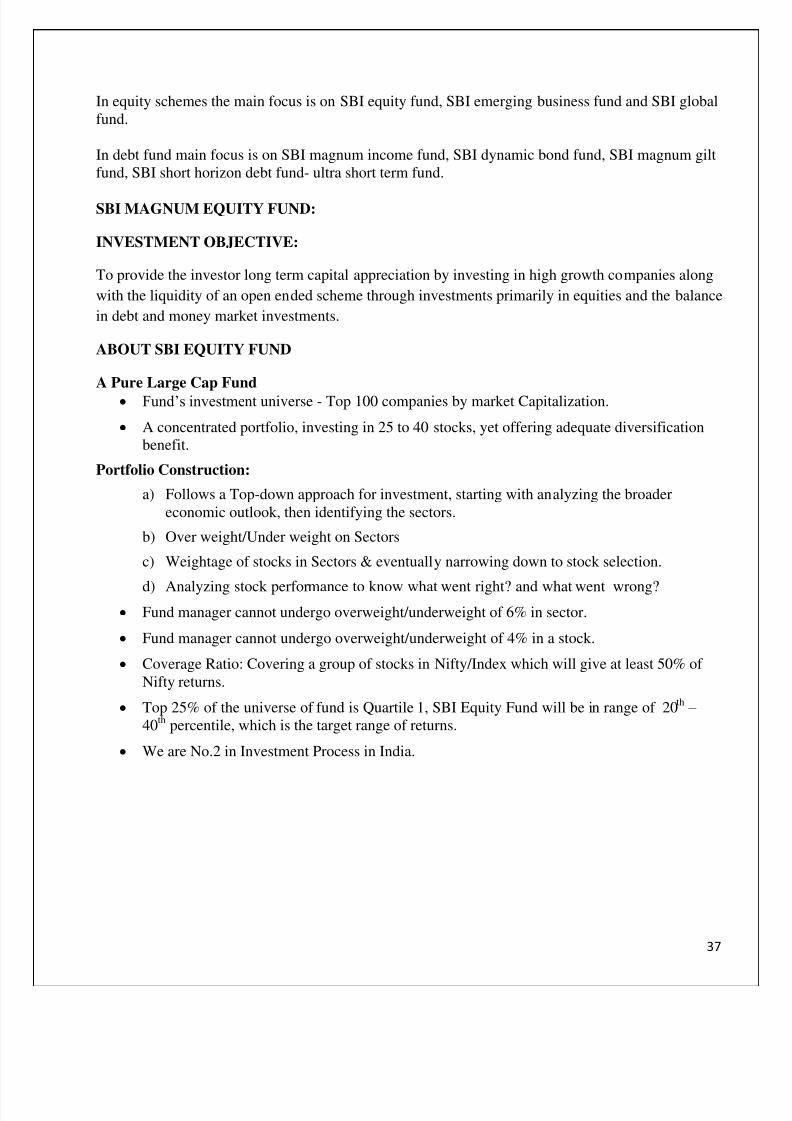

In equity schemes the main focus is on SBI equity fund, SBI emerging business fund and SBI globalfund.

In debt fund main focus is on SBI magnum income fund, SBI dynamic bond fund, SBI magnum giltfund, SBI short horizon debt fund- ultra short term fund.

SBI MAGNUM EQUITY FUND:

INVESTMENT OBJECTIVE:

To provide the investor long term capital appreciation by investing in high growth companies along

with the liquidity of an open ended scheme through investments primarily in equities and the balance

in debt and money market investments.

ABOUT SBI EQUITY FUND

A Pure Large Cap Fund

Fund‟s investment universe - Top 100 companies by market Capitalization.

A concentrated portfolio, investing in 25 to 40 stocks, yet offering adequate diversificationbenefit.

Portfolio Construction:

a) Follows a Top-down approach for investment, starting with analyzing the broadereconomic outlook, then identifying the sectors.

b) Over weight/Under weight on Sectors

c) Weightage of stocks in Sectors & eventually narrowing down to stock selection.

d) Analyzing stock performance to know what went right? and what went wrong? Fund manager cannot undergo overweight/underweight of 6% in sector.

Fund manager cannot undergo overweight/underweight of 4% in a stock.

Coverage Ratio: Covering a group of stocks in Nifty/Index which will give at least 50% of Nifty returns.

Top 25% of the universe of fund is Quartile 1, SBI Equity Fund will be in range of 20th – 40th percentile, which is the target range of returns.

We are No.2 in Investment Process in India.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 38/69

38

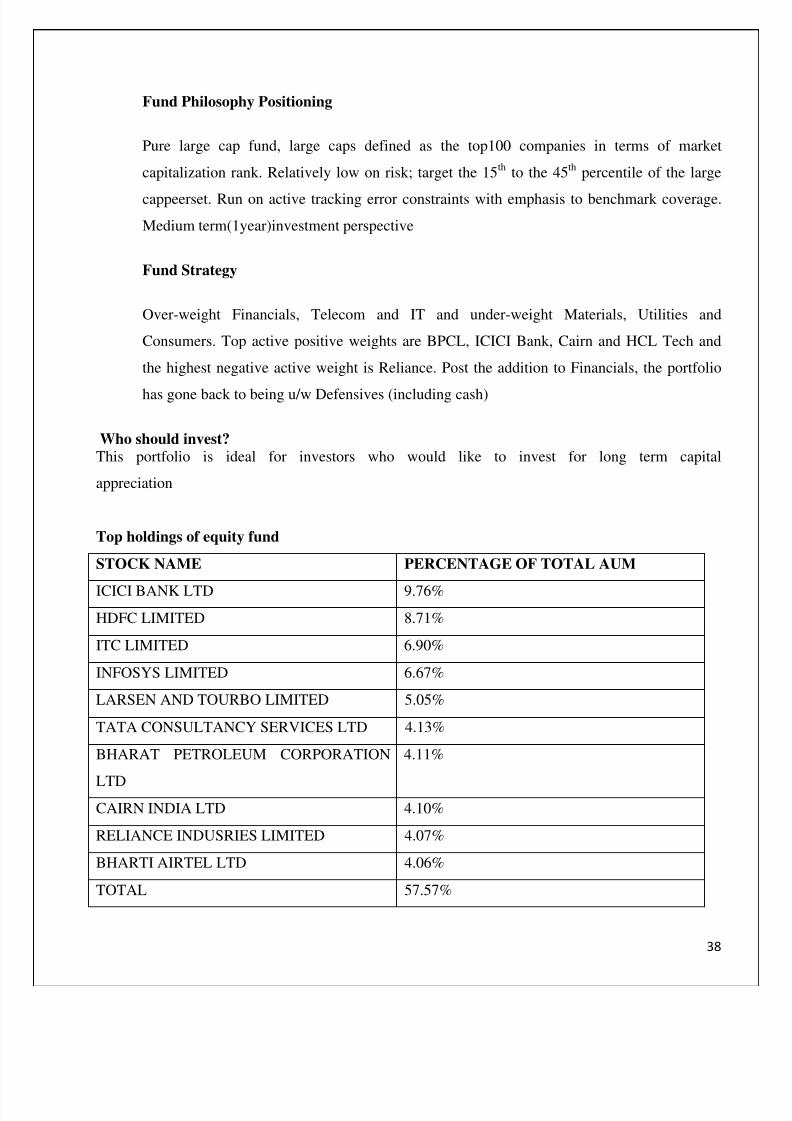

Fund Philosophy Positioning

Pure large cap fund, large caps defined as the top100 companies in terms of market

capitalization rank. Relatively low on risk; target the 15 th to the 45th percentile of the large

cappeerset. Run on active tracking error constraints with emphasis to benchmark coverage.

Medium term(1year)investment perspective

Fund Strategy

Over-weight Financials, Telecom and IT and under-weight Materials, Utilities and

Consumers. Top active positive weights are BPCL, ICICI Bank, Cairn and HCL Tech and

the highest negative active weight is Reliance. Post the addition to Financials, the portfolio

has gone back to being u/w Defensives (including cash)

Who should invest?

This portfolio is ideal for investors who would like to invest for long term capital

appreciation

Top holdings of equity fund

STOCK NAME PERCENTAGE OF TOTAL AUM

ICICI BANK LTD 9.76%

HDFC LIMITED 8.71%

ITC LIMITED 6.90%

INFOSYS LIMITED 6.67%

LARSEN AND TOURBO LIMITED 5.05%

TATA CONSULTANCY SERVICES LTD 4.13%

BHARAT PETROLEUM CORPORATION

LTD

4.11%

CAIRN INDIA LTD 4.10%

RELIANCE INDUSRIES LIMITED 4.07%

BHARTI AIRTEL LTD 4.06%

TOTAL 57.57%

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 39/69

39

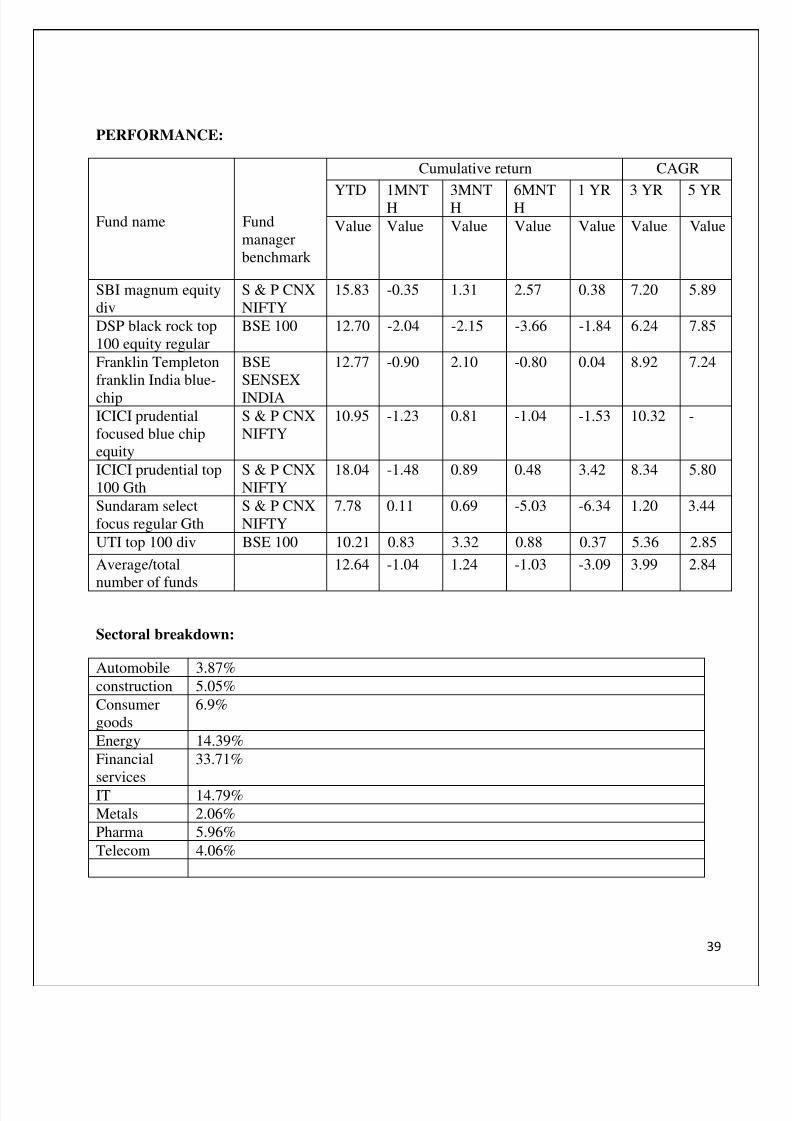

PERFORMANCE:

Fund name Fundmanagerbenchmark

Cumulative return CAGR

YTD 1MNTH 3MNTH 6MNTH 1 YR 3 YR 5 YR

Value Value Value Value Value Value Value

SBI magnum equitydiv

S & P CNXNIFTY

15.83 -0.35 1.31 2.57 0.38 7.20 5.89

DSP black rock top100 equity regular

BSE 100 12.70 -2.04 -2.15 -3.66 -1.84 6.24 7.85

Franklin Templetonfranklin India blue-

chip

BSESENSEX

INDIA

12.77 -0.90 2.10 -0.80 0.04 8.92 7.24

ICICI prudentialfocused blue chipequity

S & P CNXNIFTY

10.95 -1.23 0.81 -1.04 -1.53 10.32 -

ICICI prudential top100 Gth

S & P CNXNIFTY

18.04 -1.48 0.89 0.48 3.42 8.34 5.80

Sundaram selectfocus regular Gth

S & P CNXNIFTY

7.78 0.11 0.69 -5.03 -6.34 1.20 3.44

UTI top 100 div BSE 100 10.21 0.83 3.32 0.88 0.37 5.36 2.85

Average/total

number of funds

12.64 -1.04 1.24 -1.03 -3.09 3.99 2.84

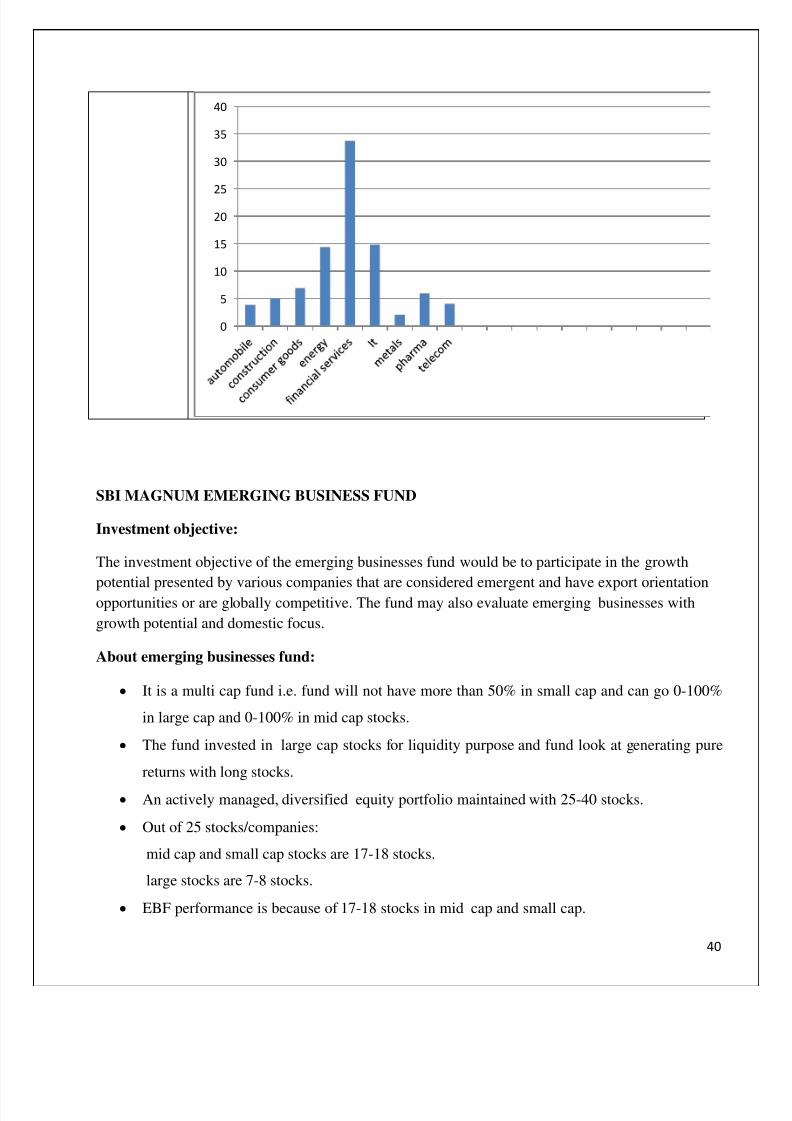

Sectoral breakdown:

Automobile 3.87%

construction 5.05%

Consumergoods

6.9%

Energy 14.39%

Financialservices

33.71%

IT 14.79%

Metals 2.06%

Pharma 5.96%

Telecom 4.06%

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 40/69

40

SBI MAGNUM EMERGING BUSINESS FUND

Investment objective:

The investment objective of the emerging businesses fund would be to participate in the growth

potential presented by various companies that are considered emergent and have export orientationopportunities or are globally competitive. The fund may also evaluate emerging businesses with

growth potential and domestic focus.

About emerging businesses fund:

It is a multi cap fund i.e. fund will not have more than 50% in small cap and can go 0-100%

in large cap and 0-100% in mid cap stocks.

The fund invested in large cap stocks for liquidity purpose and fund look at generating pure

returns with long stocks.

An actively managed, diversified equity portfolio maintained with 25-40 stocks.

Out of 25 stocks/companies:

mid cap and small cap stocks are 17-18 stocks.

large stocks are 7-8 stocks.

EBF performance is because of 17-18 stocks in mid cap and small cap.

0

5

10

15

20

25

30

35

40

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 41/69

41

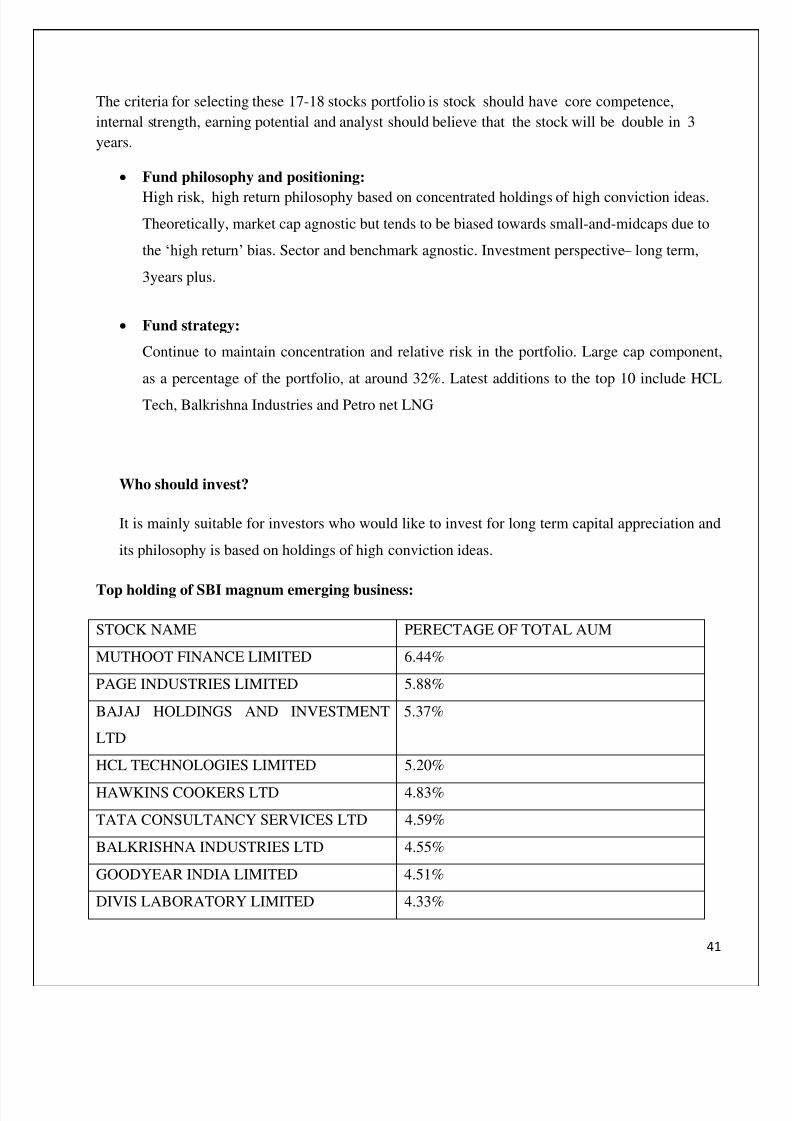

The criteria for selecting these 17-18 stocks portfolio is stock should have core competence,

internal strength, earning potential and analyst should believe that the stock will be double in 3

years.

Fund philosophy and positioning:

High risk, high return philosophy based on concentrated holdings of high conviction ideas.

Theoretically, market cap agnostic but tends to be biased towards small-and-midcaps due to

the „high return‟ bias. Sector and benchmark agnostic. Investment perspective – long term,

3years plus.

Fund strategy:

Continue to maintain concentration and relative risk in the portfolio. Large cap component,

as a percentage of the portfolio, at around 32%. Latest additions to the top 10 include HCL

Tech, Balkrishna Industries and Petro net LNG

Who should invest?

It is mainly suitable for investors who would like to invest for long term capital appreciation and

its philosophy is based on holdings of high conviction ideas.

Top holding of SBI magnum emerging business:

STOCK NAME PERECTAGE OF TOTAL AUM

MUTHOOT FINANCE LIMITED 6.44%

PAGE INDUSTRIES LIMITED 5.88%

BAJAJ HOLDINGS AND INVESTMENT

LTD

5.37%

HCL TECHNOLOGIES LIMITED 5.20%

HAWKINS COOKERS LTD 4.83%

TATA CONSULTANCY SERVICES LTD 4.59%

BALKRISHNA INDUSTRIES LTD 4.55%

GOODYEAR INDIA LIMITED 4.51%

DIVIS LABORATORY LIMITED 4.33%

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 42/69

42

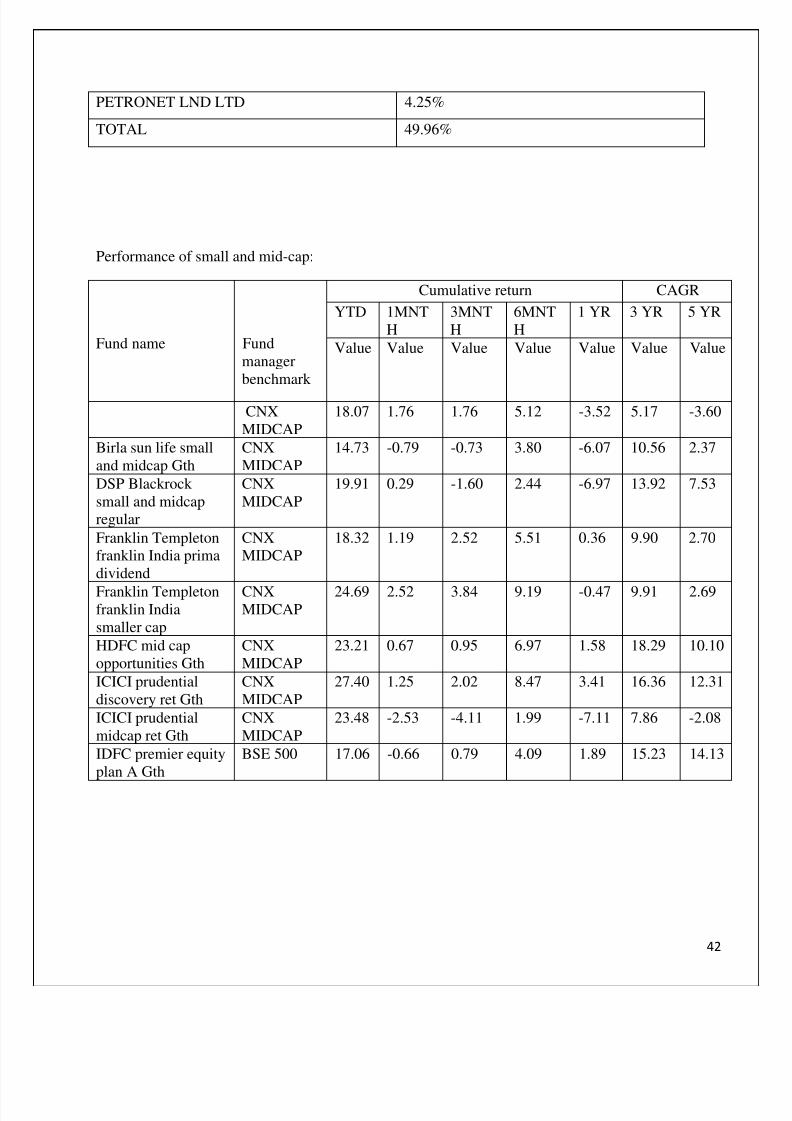

PETRONET LND LTD 4.25%

TOTAL 49.96%

Performance of small and mid-cap:

Fund name Fundmanagerbenchmark

Cumulative return CAGR

YTD 1MNTH

3MNTH

6MNTH

1 YR 3 YR 5 YR

Value Value Value Value Value Value Value

CNXMIDCAP

18.07 1.76 1.76 5.12 -3.52 5.17 -3.60

Birla sun life smalland midcap Gth

CNXMIDCAP

14.73 -0.79 -0.73 3.80 -6.07 10.56 2.37

DSP Blackrock small and midcapregular

CNXMIDCAP

19.91 0.29 -1.60 2.44 -6.97 13.92 7.53

Franklin Templetonfranklin India primadividend

CNXMIDCAP

18.32 1.19 2.52 5.51 0.36 9.90 2.70

Franklin Templetonfranklin Indiasmaller cap

CNXMIDCAP

24.69 2.52 3.84 9.19 -0.47 9.91 2.69

HDFC mid capopportunities Gth

CNXMIDCAP

23.21 0.67 0.95 6.97 1.58 18.29 10.10

ICICI prudentialdiscovery ret Gth

CNXMIDCAP

27.40 1.25 2.02 8.47 3.41 16.36 12.31

ICICI prudentialmidcap ret Gth

CNXMIDCAP

23.48 -2.53 -4.11 1.99 -7.11 7.86 -2.08

IDFC premier equityplan A Gth

BSE 500 17.06 -0.66 0.79 4.09 1.89 15.23 14.13

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 43/69

43

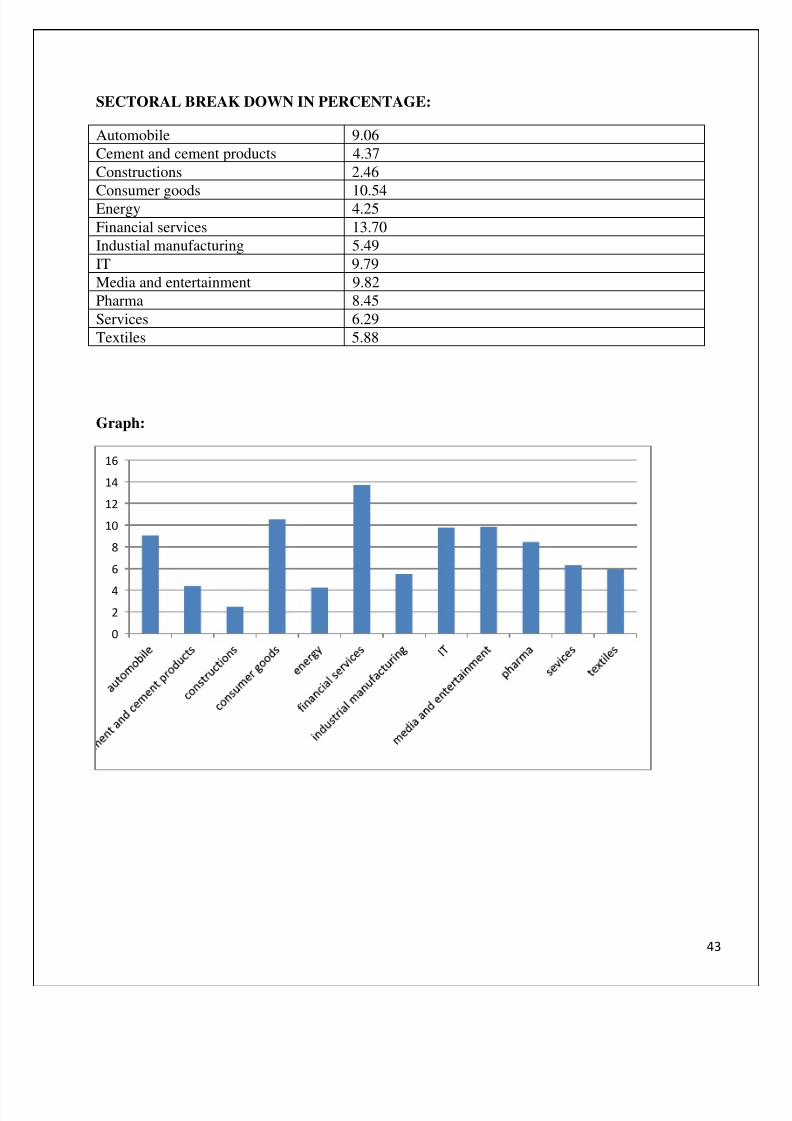

SECTORAL BREAK DOWN IN PERCENTAGE:

Automobile 9.06

Cement and cement products 4.37

Constructions 2.46

Consumer goods 10.54Energy 4.25

Financial services 13.70

Industial manufacturing 5.49

IT 9.79

Media and entertainment 9.82

Pharma 8.45

Services 6.29

Textiles 5.88

Graph:

0

2

4

6

8

10

12

14

16

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 44/69

44

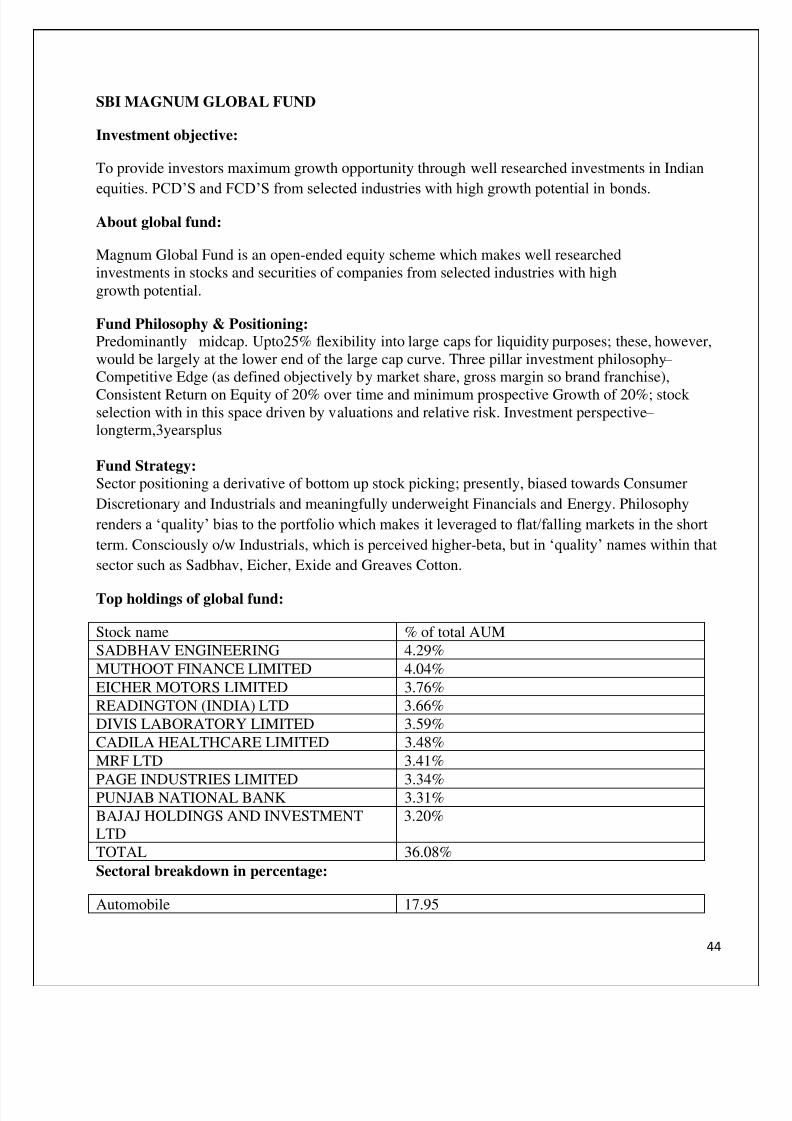

SBI MAGNUM GLOBAL FUND

Investment objective:

To provide investors maximum growth opportunity through well researched investments in Indian

equities. PCD‟S and FCD‟S from selected industries with high growth potential in bonds.

About global fund:

Magnum Global Fund is an open-ended equity scheme which makes well researchedinvestments in stocks and securities of companies from selected industries with highgrowth potential.

Fund Philosophy & Positioning: Predominantly midcap. Upto25% flexibility into large caps for liquidity purposes; these, however,would be largely at the lower end of the large cap curve. Three pillar investment philosophy –

Competitive Edge (as defined objectively by market share, gross margin so brand franchise),

Consistent Return on Equity of 20% over time and minimum prospective Growth of 20%; stock selection with in this space driven by valuations and relative risk. Investment perspective –

longterm,3yearsplus

Fund Strategy: Sector positioning a derivative of bottom up stock picking; presently, biased towards Consumer

Discretionary and Industrials and meaningfully underweight Financials and Energy. Philosophy

renders a „quality‟ bias to the portfolio which makes it leveraged to flat/falling markets in the short

term. Consciously o/w Industrials, which is perceived higher- beta, but in „quality‟ names within that

sector such as Sadbhav, Eicher, Exide and Greaves Cotton.

Top holdings of global fund:

Stock name % of total AUM

SADBHAV ENGINEERING 4.29%

MUTHOOT FINANCE LIMITED 4.04%

EICHER MOTORS LIMITED 3.76%

READINGTON (INDIA) LTD 3.66%

DIVIS LABORATORY LIMITED 3.59%

CADILA HEALTHCARE LIMITED 3.48%

MRF LTD 3.41%

PAGE INDUSTRIES LIMITED 3.34%PUNJAB NATIONAL BANK 3.31%

BAJAJ HOLDINGS AND INVESTMENTLTD

3.20%

TOTAL 36.08%

Sectoral breakdown in percentage:

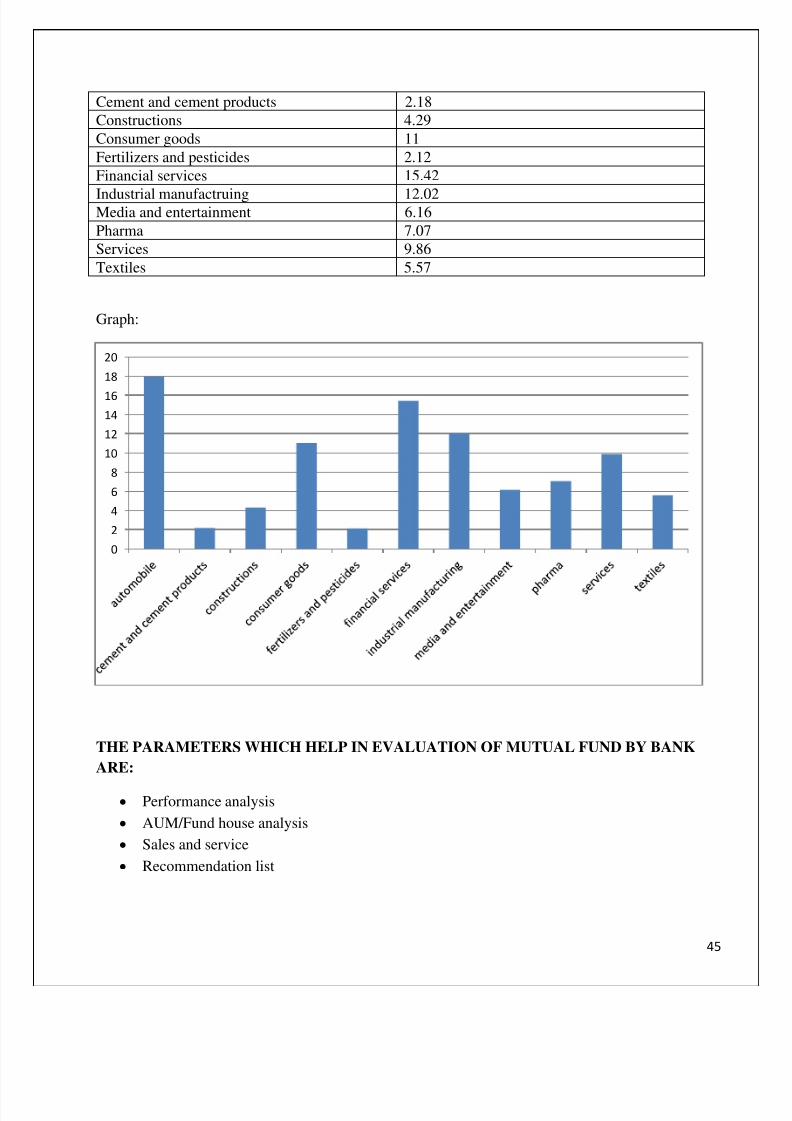

Automobile 17.95

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 45/69

45

Cement and cement products 2.18

Constructions 4.29

Consumer goods 11

Fertilizers and pesticides 2.12

Financial services 15.42

Industrial manufactruing 12.02Media and entertainment 6.16

Pharma 7.07

Services 9.86

Textiles 5.57

Graph:

THE PARAMETERS WHICH HELP IN EVALUATION OF MUTUAL FUND BY BANK

ARE:

Performance analysis

AUM/Fund house analysis

Sales and service

Recommendation list

0

2

4

6

8

10

12

14

16

18

20

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 46/69

46

Performance analysis of mutual fund in India:

Capital market plays a vital role to stabilize the economic growth, strength industrial performance

and provide various investment avenues to the investors to help the various industries and to ensure

portfolio return. Among various financial products, mutual fund ensures the minimum risks and

maximum return to the investors, its having own policies, term condition that are different fromother products, so the market volatilization will not make more effect in return.

AUM/Fund house analysis:

Asset Management Company: a firm that invest the pooled funds of retail investors in securities in

line with state disinvestment objective.

It is constituted as a company under the Indian companies act.

Minimum net worth of rs 10 corers of AMC

Minimum contribution sponsor40% of share capital of AMC

At least 50% of directors of AMC to be independent

AMC accountable to the trustees

AMC charges asset management fees subject to celling prescribed by SEBI

Asset management agreement between AMC and Trustee

Obligations of AMC:

Limit of 5% of aggregate purchase and sales securities under its entire scheme per broker per

quarter.

All security transaction with a sponsor and his associates to be disclosed.

Sales and service:

Investors can purchase and sell mutual funds units through various types of intermediaries-

individual agent, distribution companies, national/regional brokers, banks, post office etc. As well

as from the asset management companies including the unit trust of India.

To different type of investor, the mutual fund industry comprising of AMC‟s and intermediaries at

present offers the following two levels of service such as value added service and basic services.

Valued added service and basic services:

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 47/69

47

This includes product information and advice on financial planning and investment strategies. The

advice encompasses analyzing an investor financial goals depending upon the segment of investor

and then using information to recommend an asset allocation specific investment that are with

investor needs.

Recommendation list:

It is a list which is prepared by bank by evaluating performance and this performance is evaluated by

the head of fund house. These let you build a well balanced portfolio that will help you reach your

most important financial goals. It mainly focuses on criteria that have real predictive value, low

expenses, a strong record for putting share holder interest first, a consistent investment strategy and

experienced managers.

Recommend list of mutual funds and exchange traded fund help you better than most. More than

60% of our actively managed funds ranked in the top half of their categories and 83% beet their

peers.

Factor influencing mutual fund scheme from banker perspective:

Product quality:

Funds/ schemes performance

Funds/ schemes reputation or brand name

Funds/ schemes expense ratio

Funds/ schemes portfolio of investment

Funds/schemes withdrawal facility

Funds/ schemes product with tax benefits

Funds/ schemes entry and exit load

Fund sponsor qualities:

Reputation of fund house sponsoring firm

Sponsors offer a wide range of schemes with different investment objective

Sponsor has a recognized brand name

Investor services

Things which bank see while suggesting mutual fund scheme to customer

Firstly bank will not consider NAV as deciding factor while investing in mutual fund. NAV

keep changing due to performance of the fund and that depends on market and fund manager

performance.

Secondly, difference in performance of dividend or growth plan.

Thirdly, what are charges in mutual funds.

Finally, mutual fund or direct equity – who is winner.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 48/69

48

Factors to be considered before investment in mutual fund from customer perspective:

Market risk

Inflation risk

Credit risk

Interest rate risk

Exchange risk

Investment risk

Market risk:

At times the prices or yields of all the securities in a particular market rise or fall due to broad

outside influences. When this happens, the stock prices of both an outstanding highly profitable

company and a fledgling corporation may be affected. This changes in price is due to market risk.

Inflation risk:

Sometimes referred to as “loss of purchasing power.” Whenever inflation sprints forward faster than

the earnings on your investment, you run the risk that you‟ll actually be able to buy less, not more,

inflation risk also occurs when prices rise faster than your returns.

Credit risk:

In short, how stable is the company or entity to which you lend your money when you invest. How

certain are you that it will be able to pay the interest you are promised, or repay your principal when

the investment matures

Interest risk:

Changing interest rates affect both equities and bonds in many ways. Investors are reminded that

“predicting” which way rates will go is rarely successful. A diversified portfolio can help in

offsetting these changes.

Exchange risk:

A number of companies generate revenues in foreign currencies and may have investments or

expenses also denominated in foreign currencies. Changes in exchange rates may, therefore have apositive or negative impact on companies which in turn would have an effect on the investment of

the fund.

Changes in government policies:

Changes in government policy especially in regard to the tax benefits may impact the business

prospects of the companies leading to an impact on the investments made by the fund.

7/29/2019 Kanchan Final Iip

http://slidepdf.com/reader/full/kanchan-final-iip 49/69

49

What are the steps involved in selection of an equity fund?

Classify equity funds into broad categories that signify their return and risk characterstics.

Equity funds can be grouped into diversified funds, index funds, sectoral funds, and

specialized funds.

Classify funds further on the basis of fund manager style. Investors may want to choosebetween value and growth styles, depending on their risk and return prefrences.

Evaluate the performance of the scheme. This is done both within the peer group, and in

comparison with the benchmark.