Embed Size (px)

Citation preview

BurnVoir Corporate Finance Limited

BurnVoir Company Research 6 November 2016

Kalium Lakes Limited.

Kalium Lakes Ltd. (“Kalium Lakes” or “Company”) is an unlisted Australian public company seeking to raise up to $6 million via an Initial Public Offer (“IPO”) on the Australian Stock Exchange (“ASX”) in December 2016. The funds will be used to advance its 100% owned Beyondie Potash Project (“BPP”), located in the East Pilbara region of Western Australia.

Kurt Worden +61 2 8078 6455 [email protected]

John Ciganek +61 8 9215 0060 [email protected]

This Research has been prepared and issued by BurnVoir Corporate Finance Limited (“BurnVoir”) and remains the property of BurnVoir. No material contained in this Research may be reproduced or distributed without prior written approval of BurnVoir, except as allowed by the Copyright Act. This Research is current at the date of publishing. For updates or further information regarding this research, please contact BurnVoir. BurnVoir does or seeks to undertake business with companies covered in its research and therefore, Investors should consider this report as only a single factor in making their investment decisions. For explanations regarding other important disclosures, please refer to the disclosure section at the end of this document.

New potash entrant positioning for first mover advantage

Kalium Lakes Limited is seeking to advance its Beyondie

Potash Project to become Australia’s first Sulphate of Potash

(“SOP”) producer, with the opportunity to supply both domestic

and export markets. In our view, Kalium Lakes has the potential

to claim first mover advantage based on the project’s proximity

to infrastructure, its quality, and its development stage relative

to other hopeful brine players.

Seeking to raise A$3.0-6.0 million at IPO (A$0.20 per share)

Kalium Lakes is seeking to raise A$3.0 million through the issue of

15 million shares at A$0.20 per share, with the ability to accept a

further A$3 million from oversubscriptions. The funds will be applied

towards Resource definition drilling, additional pump testing, early

infrastructure, studies and engineering, and advancing regulatory

and other approvals.

Significant value upside

We have determined an indicative valuation of A$1.03 per share

(diluted, as at December 2017) for Kalium Lakes using a sum of parts

DCF model with maximum SOP production of 150ktpa and a long

term SOP price of US$500/t (real, September 2016), and 0.75

AUDUSD. On current pricing and currency (US$650/t SOP, 0.76

AUDUSD), our indicative valuation lifts to A$2.49 per share.

Further, Kalium Lakes’ key peers have market capitalisations of

A$50-80 million. Should the market accord with our assessment of

the Beyondie Potash Project and establish Kalium Lakes as a

credible peer, its equivalent share price would range from A$0.47 to

A$0.75 per share.

Large scale, high grade, advanced brine potash project

The Beyondie Potash Project covers ~2,400km2 in the East Pilbara

region of Western Australia. It has a 19.8Mt drainable SOP Resource

grading 13.6kg/m3 SOP, a low sodium: potassium ratio (9.4:1), and

over 5 million litres of brine have been extracted over an initial short

term pump test.

Compared to other Australian brine potash projects, it is one of the

closest to infrastructure, and one of the most advanced, having

completed a JORC 2012 and NI 43-101 technical report, and

secured necessary approvals to construct trial ponds and conduct

pilot scale pump testing.

Key Risks

Exploration success: Kalium Lakes’ ability to transition from

explorer to producer will be contingent on its ability to prove up the

Beyondie deposit further and convert its Resources to Reserves.

Technical / operational: it is yet to be determined that the aquifers

can deliver the target brine volumes reliably for a sustained period.

BurnVoir is currently acting as Corporate Finance Adviser and

Lead Manager for the IPO.

Use of Funds Amount

Existing cash reserves $0.6M

IPO Proceeds $3.0M

Total Funds Available $3.60M

Drilling and Pump Testing $1.25M

Infrastructure Costs $0.24M

Studies and Engineering $0.05M

Regulatory and Approvals $0.35M

Corporate and Working Capital $1.71M

Total Funds Allocated $3.60M

Capital Structure Post IPO No. Shares

Existing Shareholders 91.5M

IPO Shareholders 15.0M

Performance Options 20.0M

Management Options 7.5M

Total 134.0M

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 2

Investment Rationale

Kalium Lakes offers leverage to the ‘feed the world’ thematic

ASX-listed SOP explorer / developers have received strong market support, given their leverage to the

‘feed the world’ thematic, i.e. the ability to immediately deliver improved crop yields, given the increasing

pressure on agricultural resources to meet the demands of an expanding global population, which

continues to encroach upon arable land.

A realistic chance to become Australia’s first SOP producer

Closest deposit to infrastructure

One of the highest grade brine potash deposits in Australia

Opportunity to be the first to supply Australia’s SOP demand

There are a handful of brine potash explorers / developers listed on the ASX, most with projects in the

arid regions of Western Australia.

Kalium Lakes’ Beyondie Potash Project is very well located with respect to existing infrastructure, being

among the closest to sealed roads, gas pipeline infrastructure, and ports.

The Beyondie Potash Project is also one of the highest grade brine potash deposits in Australia, has

one of the lowest sodium: potassium ratios, and has one of the best reported geological /

hydrogeological architectures, based on the existence of a basal sand aquifer from which over five

million litres of brine has been successfully extracted during an initial short term pump test.

Finally, Kalium Lakes is well advanced compared to many of its peers regarding both the technical

aspects of the project (evidenced by the work undertaken by German specialists K-UTEC’s as described

in Snowden’s Independent Expert Report in the Prospectus) as well as key permitting and approvals,

having secured the necessary permits to construct trial ponds, conduct pilot scale pump testing, and

produce a bulk sample which can be processed through a pilot scale facility in Germany to provide

product for assessment by end users.

For these reasons, we consider Kalium Lakes a plausible chance to claim first mover advantage in

becoming Australia’s first domestic SOP producer.

Why is this important? Historically Australia has imported 300kt potash per annum, with internal demand

for SOP of approximately 70ktpa. In 2014-2015, this rose to 454kt. Currently, domestic end users are

paying A$975/t SOP FOT Kwinana. A Western Australian producer could price its product more

competitively, and capture market share, while still being able to deliver to the growing Asian market.

The opportunity to be re-rated on listing

Kalium would be worth A$0.47/sh to A$0.75/sh if the market considers Kalium Lakes as an equivalent peer of the key SOP players in Australia

On listing, Kalium Lakes will have a market capitalisation of A$21.3 million, assuming A$3 million is

raised at IPO. A number of its peers including Salt Lake Potash Limited, Reward Minerals Limited, and

Agrimin Limited, have market capitalisations of A$50-80 million.

Should the market share our view regarding the key attributes of the Beyondie Potash Project, there is

the potential for the valuation gap to narrow. If Kalium Lakes is valued at a similar level to the peers

listed above, its equivalent share price would be A$0.47 per share to A$0.75 per share.

Indicative DCF modelling supports a A$1.03 per share valuation

Indicative DCF supports a valuation of A$1.03/sh

We have modelled a 150ktpa operation, using capital and operating cost assumptions based on

estimates published by Kalium Lakes’ peers. Our indicative valuation for a fully funded project is

A$178.1 million, equivalent to A$1.03 per share (diluted), assuming a US$500/t SOP price and 0.75

AUDUSD. At the current pricing and currency (US$650/t, 0.76 AUDUSD), our valuation lifts to A$389.3

million, equivalent to A$2.49 per share (diluted).

SOP – a safer way to seek leverage to potash

Market fundamentals are positive for SOP

SOP represents about 10% of the global potassium fertiliser market (~6Mtpa), with the bulk being MOP,

(Muriate of Potash or potassium chloride), comprising 55Mtpa. SOP has an advantage over MOP in

that it does not contain chloride, which can be harmful to certain crops), and it contains sulphur, a

secondary nutrient. However, SOP trades at a premium to MOP, due to the scarcity of supply, and

which is underpinned by the high cost of production from secondary sources (e.g., Mannheim Process).

SOP demand is forecast to grow by 3.7% CAGR by 2020. Market share of SOP is expected to increase

from approximately 10% to 28% in 2028. Demand is anticipated to be driven by China, the world’s

largest consumer of potash (45%), Brazil, the world’s largest citrus producer (currently consuming only

32ktpa), and India, a large tobacco and tea grower (estimated to consume only 50ktpa currently).

On the supply side, there are few primary sources, the most obvious being moderate to large capex

development projects in Africa, in addition to brines, which are typically the lower cost producers.

Australia is one of the few regions globally where salt lakes have the requisite potassic brine chemistry.

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 3

Peer Analysis – building the case for a re-rate

There are a number of ASX-listed Western Australian brine potash explorer / developers against whom

Kalium Lakes can be compared. These include Agrimin Ltd (AMN AU), Goldphyre Resources Ltd (GPH

AU), Reward Minerals Ltd (RWD AU), Rum Jungle Resources Ltd (RUM ASX), and Salt Lake Potash

Ltd (SO4 AU).

When assessing Kalium Lakes’ Beyondie Potash Project against the projects of its ASX-listed peers,

we considered three key themes, to determine how the market is valuing these companies, and to form

a view of where the Company might be positioned upon listing on the ASX. These themes are:

Proximity to infrastructure: How remote is the asset from existing infrastructure and the

markets? This will affect the project economics and may prove to be a barrier to entry for some

brine SOP developers.

Asset quality: What is the brine grade? On what basis is the Mineral Resource defined, and in

particular, how much is drainable / extractable? Are the target aquifers in clays or sands? Have

flow rates been determined? What is the sodium: potassium ratio of the brine, i.e., how much

table salt needs to be produced and sent to waste for each tonne of SOP produced? These factors

will all impact the project economics.

Relative development stage: Has pump testing been undertaken? Are approvals in place to

construct trial ponds of sufficient size to allow continuous pump testing i.e., hectare-scale? Have

transport and logistics discussions been instigated, and to what level? Have scoping / technical

studies been undertaken? Are Native Title Agreements in place? These factors reduce the

execution risk and timing for production.

Collectively, these factors allow the better projects to be identified, provide a basis for assessing how

likely they are to be developed, and what their likelihood of claiming first mover advantage might be,

given Australia imports 100% of its SOP needs.

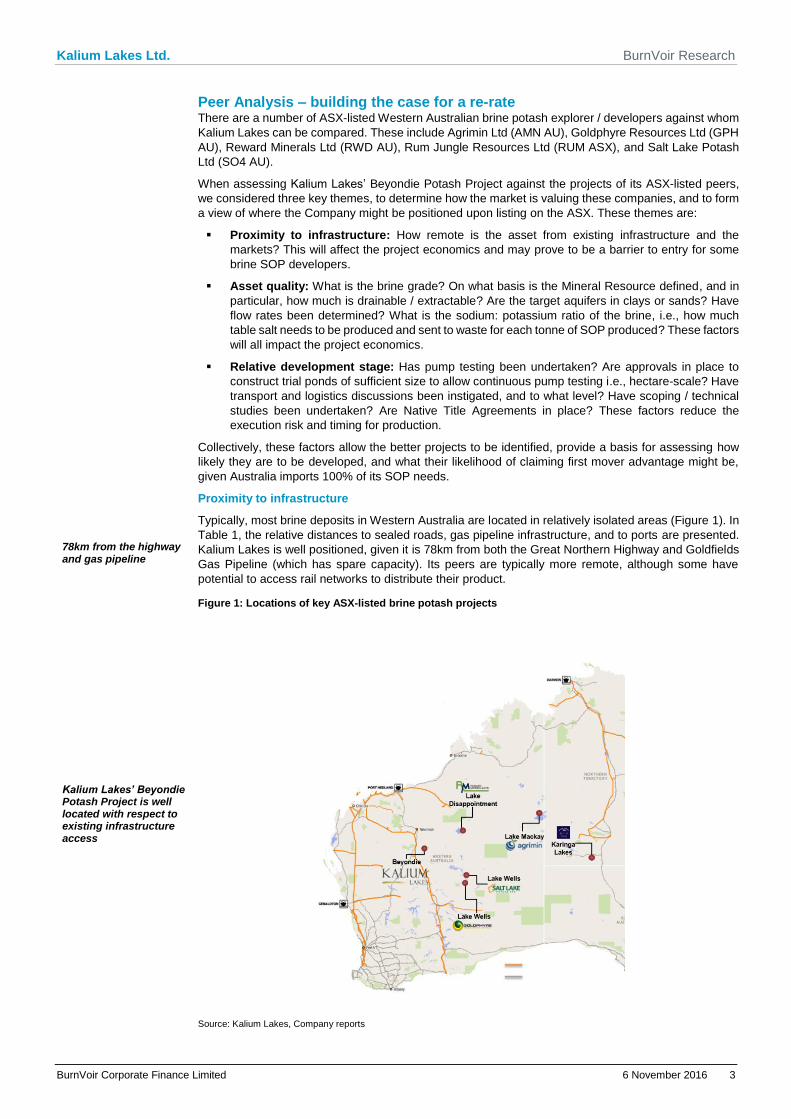

Proximity to infrastructure

78km from the highway and gas pipeline

Typically, most brine deposits in Western Australia are located in relatively isolated areas (Figure 1). In

Table 1, the relative distances to sealed roads, gas pipeline infrastructure, and to ports are presented.

Kalium Lakes is well positioned, given it is 78km from both the Great Northern Highway and Goldfields

Gas Pipeline (which has spare capacity). Its peers are typically more remote, although some have

potential to access rail networks to distribute their product.

Figure 1: Locations of key ASX-listed brine potash projects

Kalium Lakes’ Beyondie Potash Project is well located with respect to existing infrastructure access

Source: Kalium Lakes, Company reports

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 4

Table 1: Distance to Infrastructure of Australian Development Stage Potash Projects

Factor KLL AMN RWD SO4 RUM GPH

Distance to Sealed Road 78km 590km 360km 195km 1-25km 168km

Distance to Port 700 or 862km 2,300km 877 or 1,371km 1,105km 1,825km 4,078km

Distance to Gas Pipeline 78km 290km 175km 245km 150km 243km

Source: Kalium Lakes, Company reports

Asset Quality – Resource size

JORC 2012 and CIM – compliant Resource

In Table 2 below we compare several key attributes of each major deposit. Most companies have

Mineral Resources which would support long life operations.

Reward Minerals has the largest Mineral Resource at present, however it cannot be directly compared

with the other peers, given it is reported on a Total Brine Volume / in-situ basis rather than on a Drainable

Brine basis. We anticipate Reward Minerals’ resource will be closer to its peers (lower) after adjusting

for drainability, given its Mineral Resource comprises clay-based aquifers, with only the upper parts

likely amenable to extraction. Salt Lake Potash also reports on a Total Brine Volume basis.

The industry is moving towards reporting Drainable Brine standards, which includes a measure of the

recoverability of the contained brine. This is also consistent with the Canadian Institute of Mining

Metallurgy and Petroleum (“CIM”) reporting standards.

Asset Quality – Brine Grade

Reward Minerals and Kalium Lakes have the highest reported brine grades, at 13.7kg/m3 SOP and 13.6

g/m3 SOP respectively. These two deposits are part of the same drainage system. These grades are

significantly higher than the remainder of the peers, which typically have Mineral Resource grades

ranging from 8-9 kg/m3 SOP. Grade is important when determining capital costs to achieve a certain

production target: the lower the grade, the more trenches / bores that will be required to meet production,

and the larger the evaporation field and water to be evaporated.

Table 2: Comparison of deposit characteristics

Factor KLL AMN RWD SO4 RUM GPH

In-situ Resource 148.3 163.7 563.6 82.8 21.8 69.6

Drainable Resource 19.8 23.4 37.6 18.1 7.1 18.4

Potassium grade (kg/m3 SOP) 13.6 8.3 13.7 8.8 8.4-10.6 8.1

Sodium: potassium ratio 9.4:1 Not stated 15:1 22:1 Not stated 14:1

Type of Aquifer Sand Clay Clay Silt Sand Sand

Demonstrated Flow Rates litres / second) >5M l in 36hrs (Testing) 3.3 4.0 10.1 (Testing)

Source: Kalium Lakes, Company reports, BurnVoir estimates

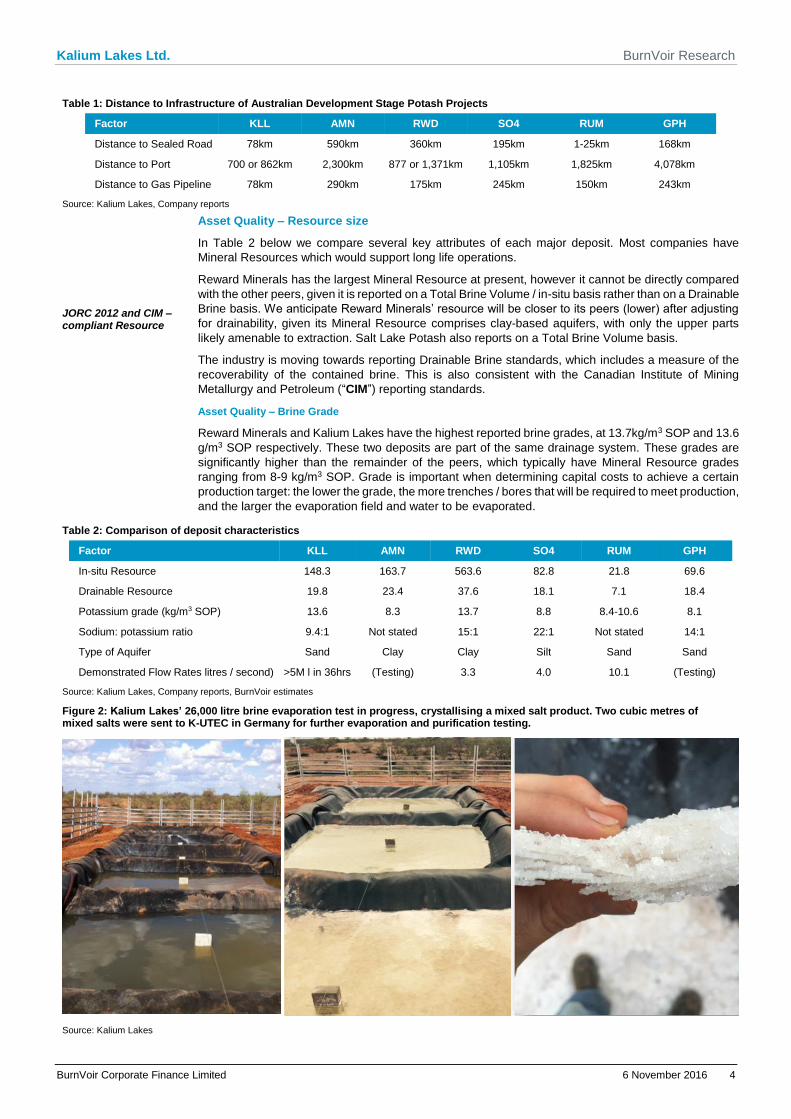

Figure 2: Kalium Lakes’ 26,000 litre brine evaporation test in progress, crystallising a mixed salt product. Two cubic metres of mixed salts were sent to K-UTEC in Germany for further evaporation and purification testing.

Source: Kalium Lakes

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 5

Asset Quality – sodium-potassium ratio

Low Na:K ratio

The sodium: potassium (Na:K) ratio is an important factor often not reported by the brine potash

developers. The higher the Na:K ratio, the more halite or common salt (NaCl) will be produced as

tailings. The Na:K ratio can therefore be considered as a proxy for the waste: ore ratio.

Kalium Lakes has a Na:K ratio of 10:1, whereas some of its peers have revealed ratios of up to 22:1

from assay data reported in ASX announcements.

Asset Quality – Clay vs sand aquifer

The Beyondie Potash Project has a basal sand aquifer

Deposits comprising brine-laden clay aquifers will have lower specific yields and therefore, lower brine

extraction characteristics than those comprising the more porous sands and gravels. Simply put, about

5% of total water can be recovered from clay versus 65% from sand. Therefore, clay-based deposits

are less likely to be viable or limited to the upper 5-10m of the lake surface, significantly reducing the

Resource size, and potential for Resource to Reserve conversion.

Extraction of brine from clay-dominated aquifers will be limited to trenching, and will require extensive

trenching networks (hundreds of kilometres) to be able to achieve significant production targets. This in

turn may have environmental implications, including barriers to permitting or rehabilitation costs.

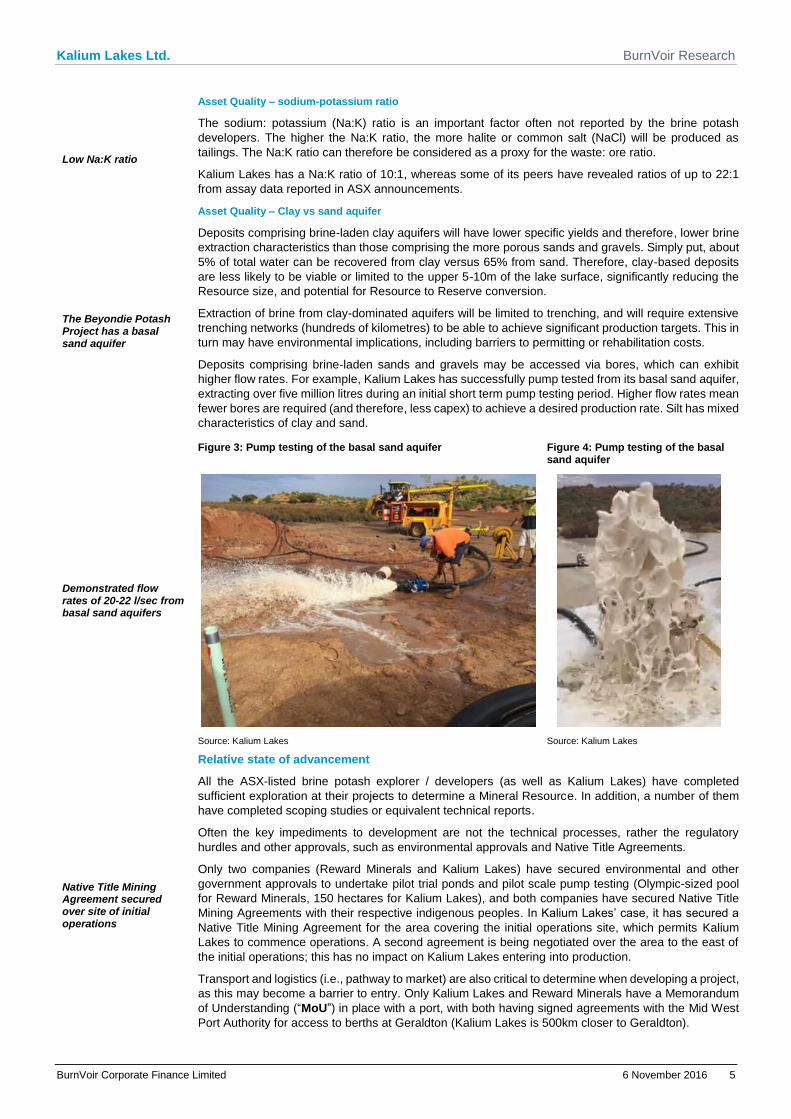

Deposits comprising brine-laden sands and gravels may be accessed via bores, which can exhibit

higher flow rates. For example, Kalium Lakes has successfully pump tested from its basal sand aquifer,

extracting over five million litres during an initial short term pump testing period. Higher flow rates mean

fewer bores are required (and therefore, less capex) to achieve a desired production rate. Silt has mixed

characteristics of clay and sand.

Figure 3: Pump testing of the basal sand aquifer Figure 4: Pump testing of the basal

sand aquifer

Demonstrated flow rates of 20-22 l/sec from basal sand aquifers

Source: Kalium Lakes Source: Kalium Lakes

Relative state of advancement

Native Title Mining Agreement secured over site of initial operations

All the ASX-listed brine potash explorer / developers (as well as Kalium Lakes) have completed

sufficient exploration at their projects to determine a Mineral Resource. In addition, a number of them

have completed scoping studies or equivalent technical reports.

Often the key impediments to development are not the technical processes, rather the regulatory

hurdles and other approvals, such as environmental approvals and Native Title Agreements.

Only two companies (Reward Minerals and Kalium Lakes) have secured environmental and other

government approvals to undertake pilot trial ponds and pilot scale pump testing (Olympic-sized pool

for Reward Minerals, 150 hectares for Kalium Lakes), and both companies have secured Native Title

Mining Agreements with their respective indigenous peoples. In Kalium Lakes’ case, it has secured a

Native Title Mining Agreement for the area covering the initial operations site, which permits Kalium

Lakes to commence operations. A second agreement is being negotiated over the area to the east of

the initial operations; this has no impact on Kalium Lakes entering into production.

Transport and logistics (i.e., pathway to market) are also critical to determine when developing a project,

as this may become a barrier to entry. Only Kalium Lakes and Reward Minerals have a Memorandum

of Understanding (“MoU”) in place with a port, with both having signed agreements with the Mid West

Port Authority for access to berths at Geraldton (Kalium Lakes is 500km closer to Geraldton).

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 6

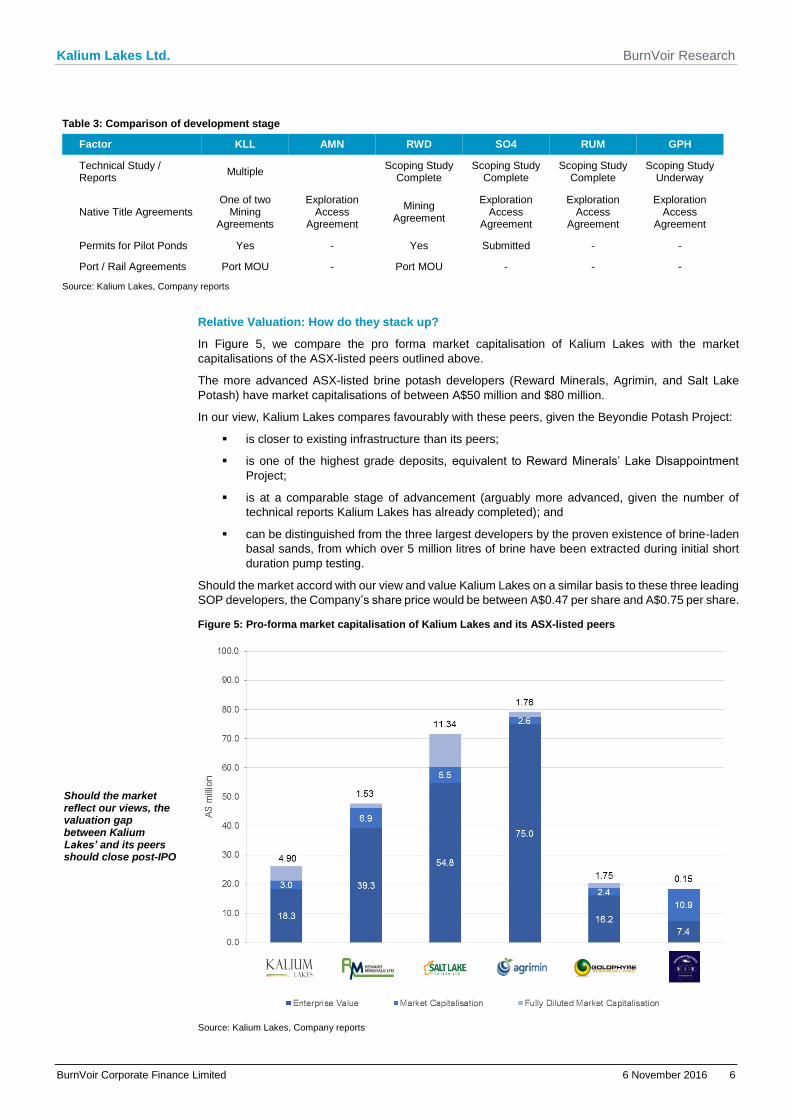

Table 3: Comparison of development stage

Factor KLL AMN RWD SO4 RUM GPH

Technical Study / Reports

Multiple Scoping Study

Complete Scoping Study

Complete Scoping Study

Complete Scoping Study

Underway

Native Title Agreements One of two

Mining Agreements

Exploration Access

Agreement

Mining Agreement

Exploration Access

Agreement

Exploration Access

Agreement

Exploration Access

Agreement

Permits for Pilot Ponds Yes - Yes Submitted - -

Port / Rail Agreements Port MOU - Port MOU - - -

Source: Kalium Lakes, Company reports

Relative Valuation: How do they stack up?

In Figure 5, we compare the pro forma market capitalisation of Kalium Lakes with the market

capitalisations of the ASX-listed peers outlined above.

The more advanced ASX-listed brine potash developers (Reward Minerals, Agrimin, and Salt Lake

Potash) have market capitalisations of between A$50 million and $80 million.

In our view, Kalium Lakes compares favourably with these peers, given the Beyondie Potash Project:

is closer to existing infrastructure than its peers;

is one of the highest grade deposits, equivalent to Reward Minerals’ Lake Disappointment

Project;

is at a comparable stage of advancement (arguably more advanced, given the number of

technical reports Kalium Lakes has already completed); and

can be distinguished from the three largest developers by the proven existence of brine-laden

basal sands, from which over 5 million litres of brine have been extracted during initial short

duration pump testing.

Should the market accord with our view and value Kalium Lakes on a similar basis to these three leading

SOP developers, the Company’s share price would be between A$0.47 per share and A$0.75 per share.

Figure 5: Pro-forma market capitalisation of Kalium Lakes and its ASX-listed peers

Should the market reflect our views, the valuation gap between Kalium Lakes’ and its peers should close post-IPO

Source: Kalium Lakes, Company reports

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 7

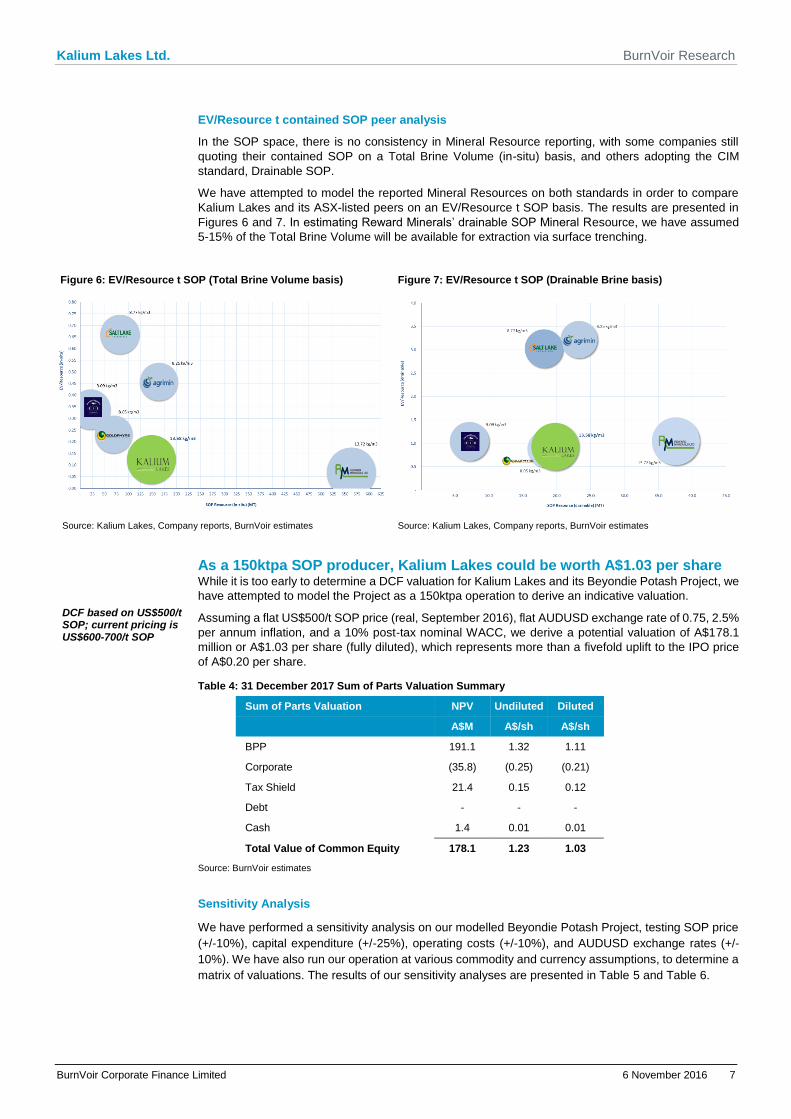

EV/Resource t contained SOP peer analysis

In the SOP space, there is no consistency in Mineral Resource reporting, with some companies still

quoting their contained SOP on a Total Brine Volume (in-situ) basis, and others adopting the CIM

standard, Drainable SOP.

We have attempted to model the reported Mineral Resources on both standards in order to compare

Kalium Lakes and its ASX-listed peers on an EV/Resource t SOP basis. The results are presented in

Figures 6 and 7. In estimating Reward Minerals’ drainable SOP Mineral Resource, we have assumed

5-15% of the Total Brine Volume will be available for extraction via surface trenching.

Figure 6: EV/Resource t SOP (Total Brine Volume basis) Figure 7: EV/Resource t SOP (Drainable Brine basis)

Source: Kalium Lakes, Company reports, BurnVoir estimates Source: Kalium Lakes, Company reports, BurnVoir estimates

As a 150ktpa SOP producer, Kalium Lakes could be worth A$1.03 per share

DCF based on US$500/t SOP; current pricing is US$600-700/t SOP

While it is too early to determine a DCF valuation for Kalium Lakes and its Beyondie Potash Project, we

have attempted to model the Project as a 150ktpa operation to derive an indicative valuation.

Assuming a flat US$500/t SOP price (real, September 2016), flat AUDUSD exchange rate of 0.75, 2.5%

per annum inflation, and a 10% post-tax nominal WACC, we derive a potential valuation of A$178.1

million or A$1.03 per share (fully diluted), which represents more than a fivefold uplift to the IPO price

of A$0.20 per share.

Table 4: 31 December 2017 Sum of Parts Valuation Summary

Sum of Parts Valuation NPV Undiluted Diluted

A$M A$/sh A$/sh

BPP 191.1 1.32 1.11

Corporate (35.8) (0.25) (0.21)

Tax Shield 21.4 0.15 0.12

Debt - - -

Cash 1.4 0.01 0.01

Total Value of Common Equity 178.1 1.23 1.03

Source: BurnVoir estimates

Sensitivity Analysis

We have performed a sensitivity analysis on our modelled Beyondie Potash Project, testing SOP price

(+/-10%), capital expenditure (+/-25%), operating costs (+/-10%), and AUDUSD exchange rates (+/-

10%). We have also run our operation at various commodity and currency assumptions, to determine a

matrix of valuations. The results of our sensitivity analyses are presented in Table 5 and Table 6.

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 8

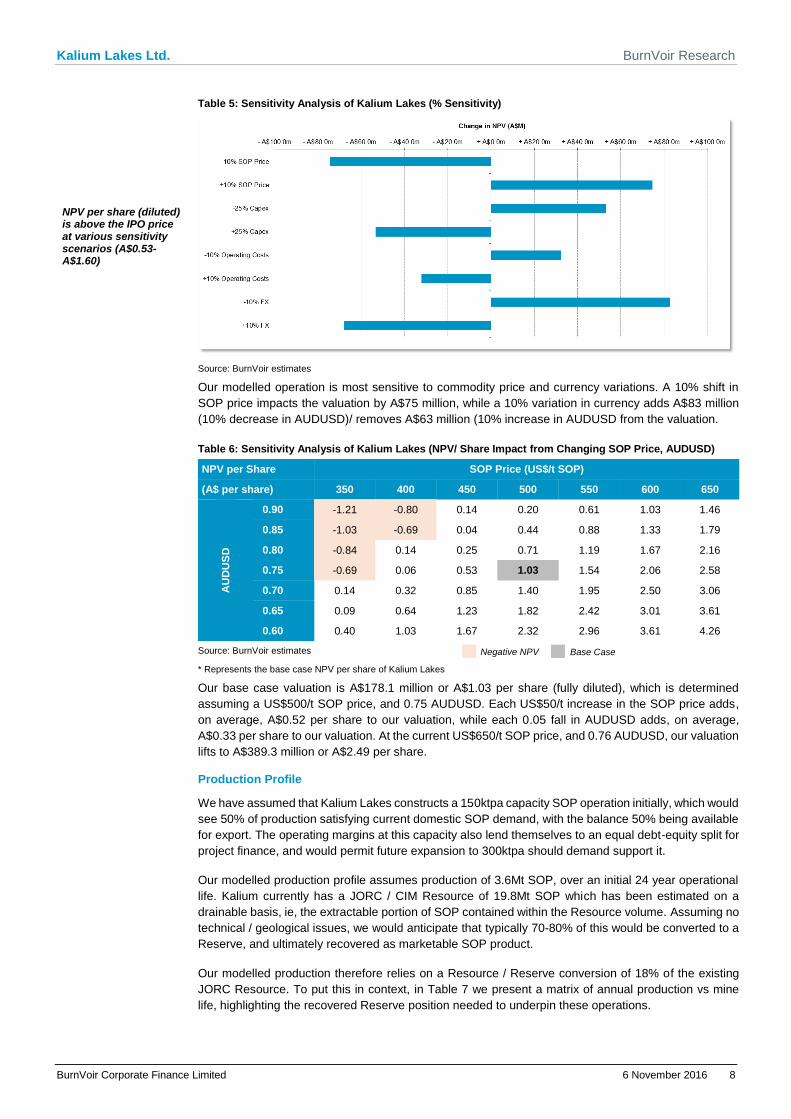

Table 5: Sensitivity Analysis of Kalium Lakes (% Sensitivity)

NPV per share (diluted) is above the IPO price at various sensitivity scenarios (A$0.53-A$1.60)

Source: BurnVoir estimates

Our modelled operation is most sensitive to commodity price and currency variations. A 10% shift in

SOP price impacts the valuation by A$75 million, while a 10% variation in currency adds A$83 million

(10% decrease in AUDUSD)/ removes A$63 million (10% increase in AUDUSD from the valuation.

Table 6: Sensitivity Analysis of Kalium Lakes (NPV/ Share Impact from Changing SOP Price, AUDUSD)

NPV per Share SOP Price (US$/t SOP)

(A$ per share) 350 400 450 500 550 600 650

AU

DU

SD

0.90 -1.21 -0.80 0.14 0.20 0.61 1.03 1.46

0.85 -1.03 -0.69 0.04 0.44 0.88 1.33 1.79

0.80 -0.84 0.14 0.25 0.71 1.19 1.67 2.16

0.75 -0.69 0.06 0.53 1.03 1.54 2.06 2.58

0.70 0.14 0.32 0.85 1.40 1.95 2.50 3.06

0.65 0.09 0.64 1.23 1.82 2.42 3.01 3.61

0.60 0.40 1.03 1.67 2.32 2.96 3.61 4.26

Source: BurnVoir estimates

* Represents the base case NPV per share of Kalium Lakes

Our base case valuation is A$178.1 million or A$1.03 per share (fully diluted), which is determined

assuming a US$500/t SOP price, and 0.75 AUDUSD. Each US$50/t increase in the SOP price adds,

on average, A$0.52 per share to our valuation, while each 0.05 fall in AUDUSD adds, on average,

A$0.33 per share to our valuation. At the current US$650/t SOP price, and 0.76 AUDUSD, our valuation

lifts to A$389.3 million or A$2.49 per share.

Production Profile

We have assumed that Kalium Lakes constructs a 150ktpa capacity SOP operation initially, which would

see 50% of production satisfying current domestic SOP demand, with the balance 50% being available

for export. The operating margins at this capacity also lend themselves to an equal debt-equity split for

project finance, and would permit future expansion to 300ktpa should demand support it.

Our modelled production profile assumes production of 3.6Mt SOP, over an initial 24 year operational

life. Kalium currently has a JORC / CIM Resource of 19.8Mt SOP which has been estimated on a

drainable basis, ie, the extractable portion of SOP contained within the Resource volume. Assuming no

technical / geological issues, we would anticipate that typically 70-80% of this would be converted to a

Reserve, and ultimately recovered as marketable SOP product.

Our modelled production therefore relies on a Resource / Reserve conversion of 18% of the existing

JORC Resource. To put this in context, in Table 7 we present a matrix of annual production vs mine

life, highlighting the recovered Reserve position needed to underpin these operations.

Negative NPV Base Case

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 9

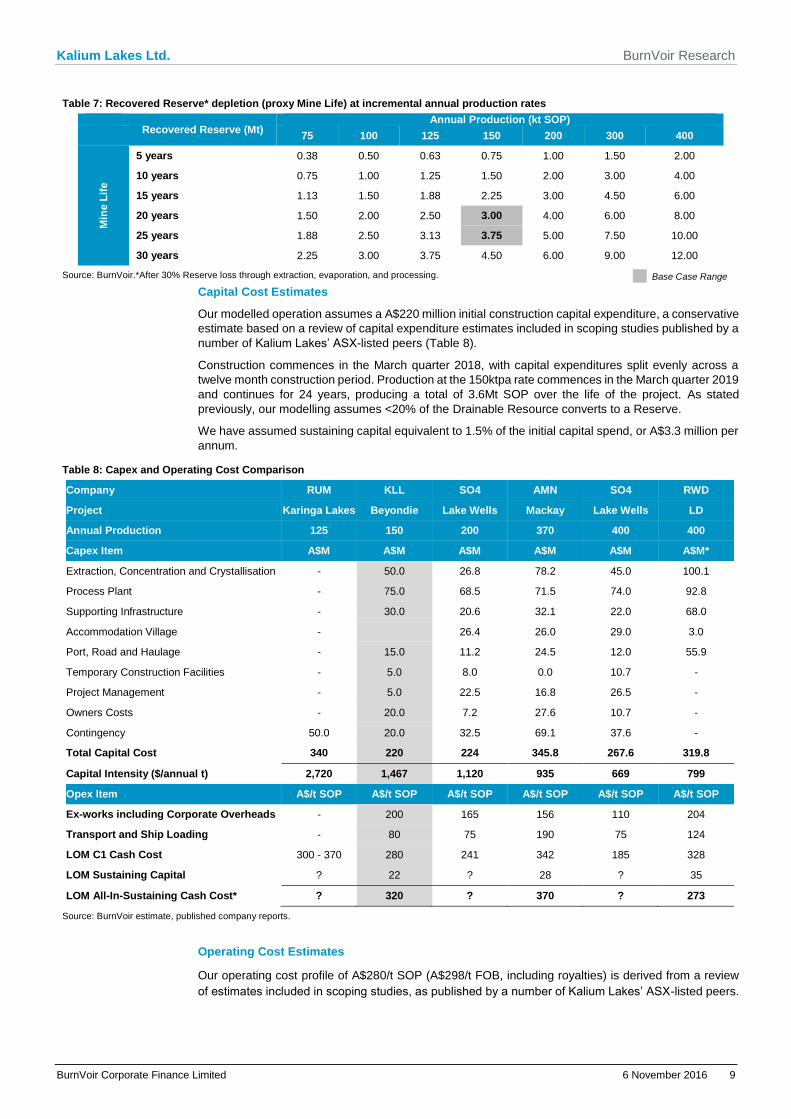

Table 7: Recovered Reserve* depletion (proxy Mine Life) at incremental annual production rates

Recovered Reserve (Mt)

Annual Production (kt SOP) 75 100 125 150 200 300 400

Min

e L

ife

5 years 0.38 0.50 0.63 0.75 1.00 1.50 2.00

10 years 0.75 1.00 1.25 1.50 2.00 3.00 4.00

15 years 1.13 1.50 1.88 2.25 3.00 4.50 6.00

20 years 1.50 2.00 2.50 3.00 4.00 6.00 8.00

25 years 1.88 2.50 3.13 3.75 5.00 7.50 10.00

30 years 2.25 3.00 3.75 4.50 6.00 9.00 12.00

Source: BurnVoir.*After 30% Reserve loss through extraction, evaporation, and processing.

Capital Cost Estimates

Our modelled operation assumes a A$220 million initial construction capital expenditure, a conservative

estimate based on a review of capital expenditure estimates included in scoping studies published by a

number of Kalium Lakes’ ASX-listed peers (Table 8).

Construction commences in the March quarter 2018, with capital expenditures split evenly across a

twelve month construction period. Production at the 150ktpa rate commences in the March quarter 2019

and continues for 24 years, producing a total of 3.6Mt SOP over the life of the project. As stated

previously, our modelling assumes <20% of the Drainable Resource converts to a Reserve.

We have assumed sustaining capital equivalent to 1.5% of the initial capital spend, or A$3.3 million per

annum.

Table 8: Capex and Operating Cost Comparison

Company RUM KLL SO4 AMN SO4 RWD

Project Karinga Lakes Beyondie Lake Wells Mackay Lake Wells LD

Annual Production 125 150 200 370 400 400

Capex Item A$M A$M A$M A$M A$M A$M*

Extraction, Concentration and Crystallisation - 50.0 26.8 78.2 45.0 100.1

Process Plant - 75.0 68.5 71.5 74.0 92.8

Supporting Infrastructure - 30.0 20.6 32.1 22.0 68.0

Accommodation Village - 26.4 26.0 29.0 3.0

Port, Road and Haulage - 15.0 11.2 24.5 12.0 55.9

Temporary Construction Facilities - 5.0 8.0 0.0 10.7 -

Project Management - 5.0 22.5 16.8 26.5 -

Owners Costs - 20.0 7.2 27.6 10.7 -

Contingency 50.0 20.0 32.5 69.1 37.6 -

Total Capital Cost 340 220 224 345.8 267.6 319.8

Capital Intensity ($/annual t) 2,720 1,467 1,120 935 669 799

Opex Item A$/t SOP A$/t SOP A$/t SOP A$/t SOP A$/t SOP A$/t SOP

Ex-works including Corporate Overheads - 200 165 156 110 204

Transport and Ship Loading - 80 75 190 75 124

LOM C1 Cash Cost 300 - 370 280 241 342 185 328

LOM Sustaining Capital ? 22 ? 28 ? 35

LOM All-In-Sustaining Cash Cost* ? 320 ? 370 ? 273

Source: BurnVoir estimate, published company reports.

Operating Cost Estimates

Our operating cost profile of A$280/t SOP (A$298/t FOB, including royalties) is derived from a review

of estimates included in scoping studies, as published by a number of Kalium Lakes’ ASX-listed peers.

Base Case Range

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 10

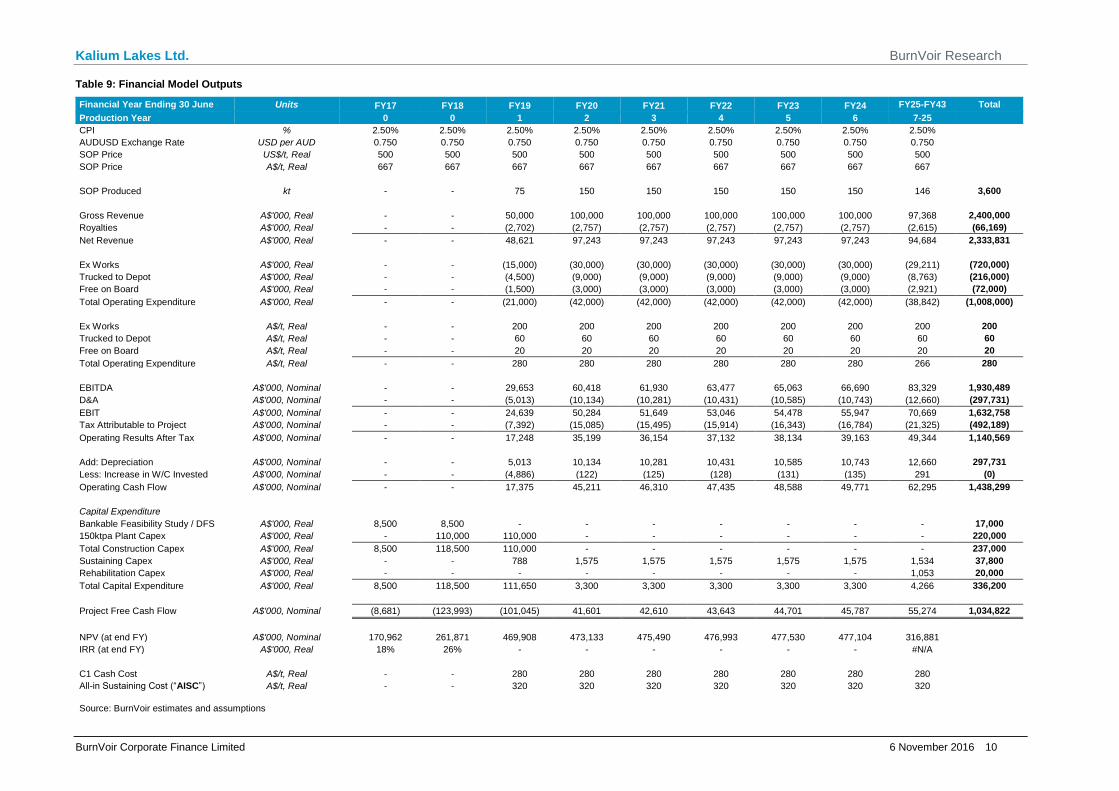

Table 9: Financial Model Outputs

Financial Year Ending 30 June Units FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25-FY43 Total

Production Year 0 0 1 2 3 4 5 6 7-25

CPI % 2.50% 2.50% 2.50% 2.50% 2.50% 2.50% 2.50% 2.50% 2.50%

AUDUSD Exchange Rate USD per AUD 0.750 0.750 0.750 0.750 0.750 0.750 0.750 0.750 0.750

SOP Price US$/t, Real 500 500 500 500 500 500 500 500 500

SOP Price A$/t, Real 667 667 667 667 667 667 667 667 667

SOP Produced kt - - 75 150 150 150 150 150 146 3,600

Gross Revenue A$'000, Real - - 50,000 100,000 100,000 100,000 100,000 100,000 97,368 2,400,000

Royalties A$'000, Real - - (2,702) (2,757) (2,757) (2,757) (2,757) (2,757) (2,615) (66,169)

Net Revenue A$'000, Real - - 48,621 97,243 97,243 97,243 97,243 97,243 94,684 2,333,831

Ex Works A$'000, Real - - (15,000) (30,000) (30,000) (30,000) (30,000) (30,000) (29,211) (720,000)

Trucked to Depot A$'000, Real - - (4,500) (9,000) (9,000) (9,000) (9,000) (9,000) (8,763) (216,000)

Free on Board A$'000, Real - - (1,500) (3,000) (3,000) (3,000) (3,000) (3,000) (2,921) (72,000)

Total Operating Expenditure A$'000, Real - - (21,000) (42,000) (42,000) (42,000) (42,000) (42,000) (38,842) (1,008,000)

Ex Works A$/t, Real - - 200 200 200 200 200 200 200 200

Trucked to Depot A$/t, Real - - 60 60 60 60 60 60 60 60

Free on Board A$/t, Real - - 20 20 20 20 20 20 20 20

Total Operating Expenditure A$/t, Real - - 280 280 280 280 280 280 266 280

EBITDA A$'000, Nominal - - 29,653 60,418 61,930 63,477 65,063 66,690 83,329 1,930,489

D&A A$'000, Nominal - - (5,013) (10,134) (10,281) (10,431) (10,585) (10,743) (12,660) (297,731)

EBIT A$'000, Nominal - - 24,639 50,284 51,649 53,046 54,478 55,947 70,669 1,632,758

Tax Attributable to Project A$'000, Nominal - - (7,392) (15,085) (15,495) (15,914) (16,343) (16,784) (21,325) (492,189)

Operating Results After Tax A$'000, Nominal - - 17,248 35,199 36,154 37,132 38,134 39,163 49,344 1,140,569

Add: Depreciation A$'000, Nominal - - 5,013 10,134 10,281 10,431 10,585 10,743 12,660 297,731

Less: Increase in W/C Invested A$'000, Nominal - - (4,886) (122) (125) (128) (131) (135) 291 (0)

Operating Cash Flow A$'000, Nominal - - 17,375 45,211 46,310 47,435 48,588 49,771 62,295 1,438,299

Capital Expenditure

Bankable Feasibility Study / DFS A$'000, Real 8,500 8,500 - - - - - - - 17,000

150ktpa Plant Capex A$'000, Real - 110,000 110,000 - - - - - - 220,000

Total Construction Capex A$'000, Real 8,500 118,500 110,000 - - - - - - 237,000

Sustaining Capex A$'000, Real - - 788 1,575 1,575 1,575 1,575 1,575 1,534 37,800

Rehabilitation Capex A$'000, Real - - - - - - - - 1,053 20,000

Total Capital Expenditure A$'000, Real 8,500 118,500 111,650 3,300 3,300 3,300 3,300 3,300 4,266 336,200

Project Free Cash Flow A$'000, Nominal (8,681) (123,993) (101,045) 41,601 42,610 43,643 44,701 45,787 55,274 1,034,822

NPV (at end FY) A$'000, Nominal 170,962 261,871 469,908 473,133 475,490 476,993 477,530 477,104 316,881

IRR (at end FY) A$'000, Real 18% 26% - - - - - - #N/A

C1 Cash Cost A$/t, Real - - 280 280 280 280 280 280 280

All-in Sustaining Cost (“AISC”) A$/t, Real - - 320 320 320 320 320 320 320

Source: BurnVoir estimates and assumptions

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 11

Royalties

The Beyondie Potash Project will be subject to Government royalties, Native Title Royalties, and a

Founders’ Royalty.

There does not appear to be a provision for potash products in the Mining Regulations 1981. We

assume salt is the closest product to use as a basis, given SOP is derived as a salt from evaporation

and purification. Salt royalties are covered under State Agreements and the Mining Regulations 1981.

A recent WA Government review (2015) recommended that all salt production be treated under the

Mining Regulations 1981, and subject to a specific royalty based on Amount A (currently A$0.73/t). We

have assumed this royalty rate in our model.

The Native Title royalty under the Gingirana Mining Agreement has been set at 0.75% and we have

assumed any subsequent Mining Agreements will be of the same royalty amount.

There is also a 1.9% royalty on gross revenues from potash production, payable to the three founding

shareholders of Kalium Lakes Potash Pty Ltd. These individuals are Brett Hazelden, Rudolph van

Niekerk, and Brent Smoothy. Each of the royalties have been factored into our modelled revenue.

Financing

We have assumed the cost to completion of the Definitive Feasibility Study (“DFS”) will $20 million

(including corporate overheads), which will be funded by the proceeds of the $5 million IPO (assuming

$2 million is raised from oversubscriptions), and a further A$15 million equity raise in June quarter 2017,

at an assumed issue price of A$0.52 per share (representing a 60% discount to the NPV at the

preceding quarter and is within the valuation range of A$0.47 to A$0.75 per share if Kalium Lakes is

valued at a similar level to its SOP peers in Australia).

Based on our pricing assumptions which approximate a bank’s price path, the Beyondie Potash Project

can support A$120 million debt while maintaining typical project financing debt covenants.

The balance of the A$120 million capital expenditure (allowing for capitalised interest during

construction and corporate overheads) will need to be equity funded, which will likely involve offtake

agreements including pre-payments, and conventional equity.

The modelling assumes an A$120 million conventional equity raising in the March quarter 2018, at

A$0.92 per share (representing a 25% discount to the NPV at the preceding quarter) and no pre-

payments are included. The A$120 million debt facility is drawn down in the June quarter 2018, once

the equity raising has completed. Our debt facility has a seven year tenor, with a sculpted repayment

profile, and all in interest rate of 8.1%.

Initial Public Offer

Kalium Lakes is seeking to raise A$3.0 million via an Initial Public Offering on the ASX, with the ability

to accept a further A$3 million from oversubscriptions. The IPO is priced at A$0.20 per share, resulting

in a pre-market valuation of A$18.3 million. Post-IPO, Kalium Lakes will have a market capitalisation of

A$21.3-A$24.3 million, scaling with any additional funding raised. Proceeds will be applied toward

Resource definition drilling, prolonged pump testing, studies and engineering, and advancing regulatory

requirements and approvals.

Table 10: Use of Funds

Use of Funds (including existing $0.6m existing cash) Amount

$3M Raise $6M Raise

Drilling and Pump Testing $1.25M $2.27M

Infrastructure Costs $0.24M $0.64M

Studies and Engineering $0.05M $1.05M

Regulatory and Approvals $0.35M $0.58M

Corporate and Working Capital $1.71M $2.06M

Total $3.60M $6.60M

Source: Kalium Lakes

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 12

Table 11: Key Dates

Event Date

Lodgement of IPO Prospectus Friday, 4th November

Opening Date of Offer Friday 14th November

Closing Date of Offer Monday 12th December

Expected Issue and Allotment of IPO Shares Thursday 15th December

Expected Holding Statement Despatch Date Friday 16th December

Expected Official Quotation of Shares on ASX Monday 19th December

Source: Kalium Lakes

Capital Structure

Shares

There are presently 91.5 Million shares on issue in Kalium Lakes. A further 15 million shares will be

issued under the IPO, lifting the total number of shares on issue to 106.5 million.

Performance Options

There are 20.0 million Performance Rights on issue to the company founders (Brett Hazelden, Rudolph

van Niekerk, and Brent Smoothy), which vest if key milestones for the Beyondie Potash Project are

achieved within five years These milestones are:

Completion of the DFS (5 million);

Securing project finance (5 million); and

Achieving commercial production of SOP (10 million).

Management Options

There are 7.5 Management Options on issue, which have a three year term, and an exercise price of

$0.25 per share. These are held by the Chairman Mal Randall (4.0 million), Non-Executive Director

Brendan O’Hara (2.0 million), with 0.50 million each issued to Company Secretary Gareth Widger, and

Brad Cribb and Cary Rossetti, both members of Kalium Lakes’ management team.

Table 12: Current Company shareholding and pro-forma shareholdings post $3 million IPO

Shareholder* Current Shareholdings# Post $3M IPO

#M % #M %

Brent Smoothy 53.6 58.5 53.6 50.3

Brett Hazelden 13.6 14.9 13.6 12.8

Rudolph van Niekerk 3.3 3.6 3.3 3.1

Other Existing Investors 21.0 23.0 21.0 19.7

IPO Investors - - 15.0 14.1

Total (Undiluted) 91.5 100.0 106.5 100.0

Source: Kalium Lakes

*Includes entities associated with the shareholder. Includes Performance Rights and Management Options.

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 13

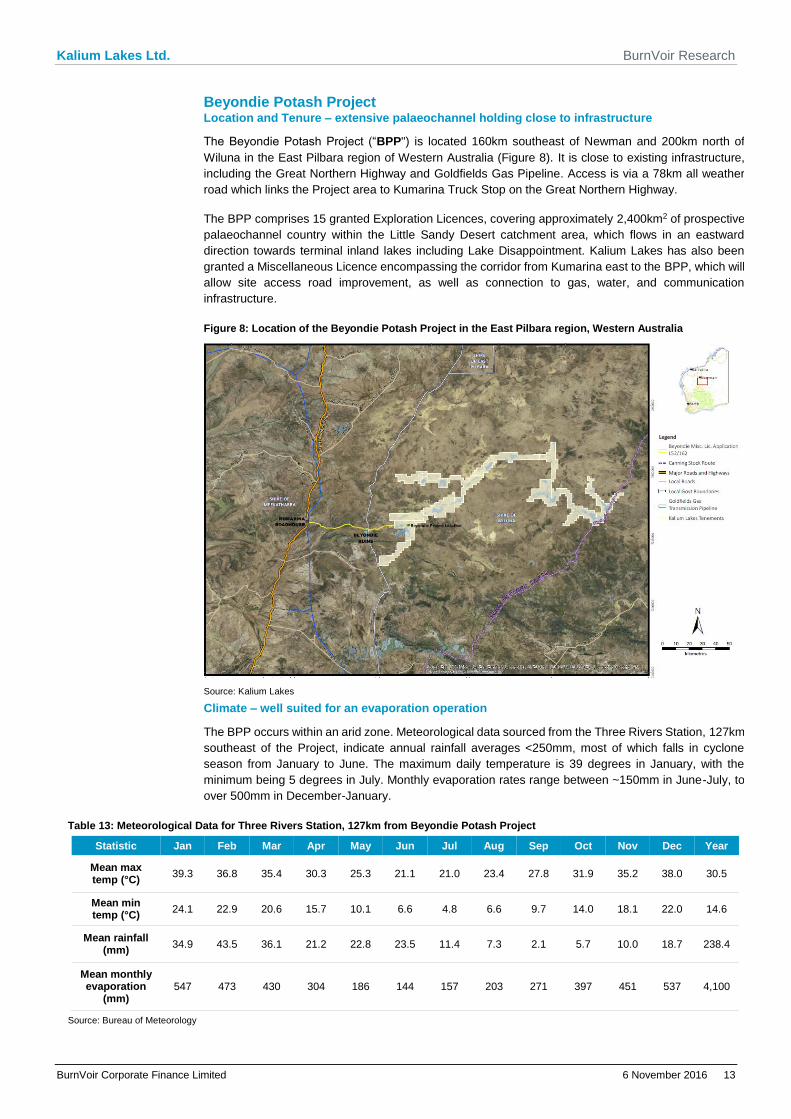

Beyondie Potash Project Location and Tenure – extensive palaeochannel holding close to infrastructure

The Beyondie Potash Project (“BPP") is located 160km southeast of Newman and 200km north of

Wiluna in the East Pilbara region of Western Australia (Figure 8). It is close to existing infrastructure,

including the Great Northern Highway and Goldfields Gas Pipeline. Access is via a 78km all weather

road which links the Project area to Kumarina Truck Stop on the Great Northern Highway.

The BPP comprises 15 granted Exploration Licences, covering approximately 2,400km2 of prospective

palaeochannel country within the Little Sandy Desert catchment area, which flows in an eastward

direction towards terminal inland lakes including Lake Disappointment. Kalium Lakes has also been

granted a Miscellaneous Licence encompassing the corridor from Kumarina east to the BPP, which will

allow site access road improvement, as well as connection to gas, water, and communication

infrastructure.

Figure 8: Location of the Beyondie Potash Project in the East Pilbara region, Western Australia

Source: Kalium Lakes

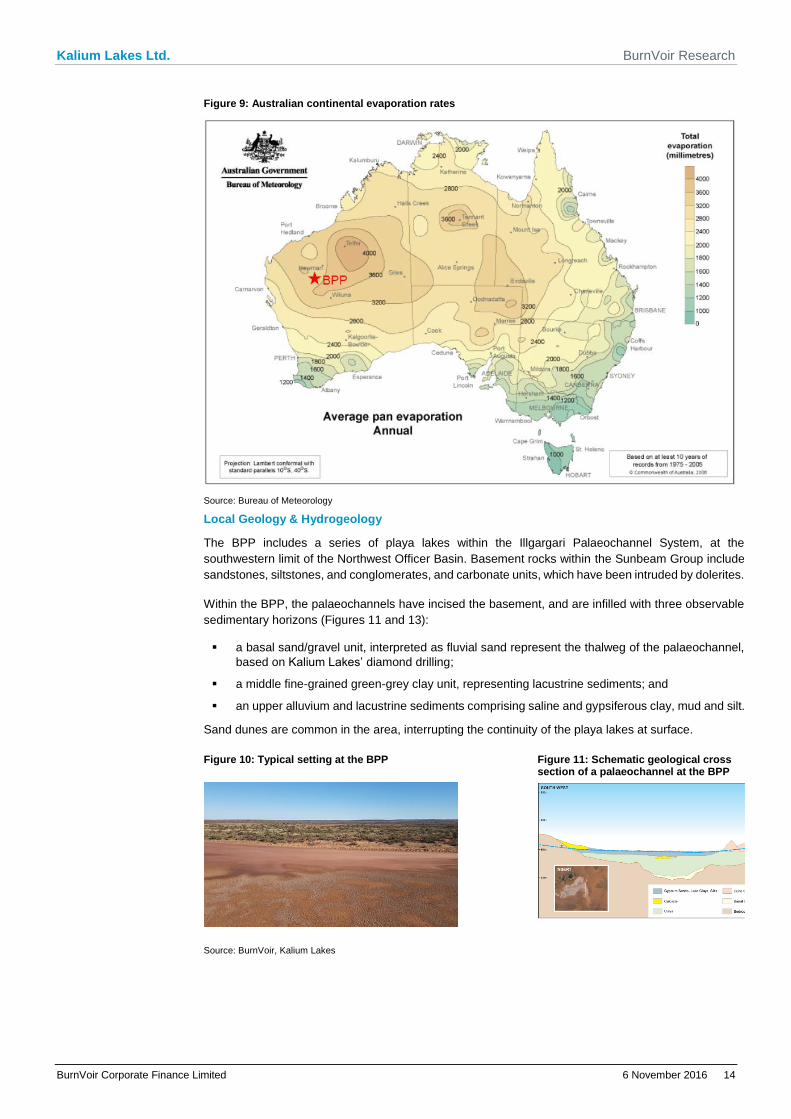

Climate – well suited for an evaporation operation

The BPP occurs within an arid zone. Meteorological data sourced from the Three Rivers Station, 127km

southeast of the Project, indicate annual rainfall averages <250mm, most of which falls in cyclone

season from January to June. The maximum daily temperature is 39 degrees in January, with the

minimum being 5 degrees in July. Monthly evaporation rates range between ~150mm in June-July, to

over 500mm in December-January.

Table 13: Meteorological Data for Three Rivers Station, 127km from Beyondie Potash Project

Statistic Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

Mean max temp (°C)

39.3 36.8 35.4 30.3 25.3 21.1 21.0 23.4 27.8 31.9 35.2 38.0 30.5

Mean min temp (°C)

24.1 22.9 20.6 15.7 10.1 6.6 4.8 6.6 9.7 14.0 18.1 22.0 14.6

Mean rainfall (mm)

34.9 43.5 36.1 21.2 22.8 23.5 11.4 7.3 2.1 5.7 10.0 18.7 238.4

Mean monthly evaporation

(mm) 547 473 430 304 186 144 157 203 271 397 451 537 4,100

Source: Bureau of Meteorology

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 14

Figure 9: Australian continental evaporation rates

Source: Bureau of Meteorology

Local Geology & Hydrogeology

The BPP includes a series of playa lakes within the Illgargari Palaeochannel System, at the

southwestern limit of the Northwest Officer Basin. Basement rocks within the Sunbeam Group include

sandstones, siltstones, and conglomerates, and carbonate units, which have been intruded by dolerites.

Within the BPP, the palaeochannels have incised the basement, and are infilled with three observable

sedimentary horizons (Figures 11 and 13):

a basal sand/gravel unit, interpreted as fluvial sand represent the thalweg of the palaeochannel,

based on Kalium Lakes’ diamond drilling;

a middle fine-grained green-grey clay unit, representing lacustrine sediments; and

an upper alluvium and lacustrine sediments comprising saline and gypsiferous clay, mud and silt.

Sand dunes are common in the area, interrupting the continuity of the playa lakes at surface.

Figure 10: Typical setting at the BPP Figure 11: Schematic geological cross

section of a palaeochannel at the BPP

Source: BurnVoir, Kalium Lakes

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 15

Figure 12: Surface inflow of brine at the BPP Figure 13: BPP drill core: basal sands

(in blue), clay, alluvium

Source: BurnVoir

Mineral Resource and Exploration Target

The BPP is a brine deposit, largely hosted within the palaeochannel sediments. Consistent with the

palaeochannel geology outlined above, there are three key aquifers which have been included in the

Mineral Resource estimate: the basal sand aquifer, the middle clay aquifer, and the upper alluvium

aquifer (refer Figure 11). The brine has been recorded within these sedimentary horizons in the lake,

and also in the sediments adjacent to the lakes.

Kalium Lakes’ Mineral Resource estimate of 19.8Mt drainable SOP grading 13.6kg/m3 SOP has been

reported in compliance with the CIM guidelines for brine deposits, in addition to being JORC 2012

compliant. Details of the Mineral Resource are included in the Technical Report, which was compiled

by K-UTEC Salt Technologies of Germany, and provided in May 2016.

Table 14: JORC 2012 / NI 43-101 Compliant Drainable Brine Resource, April 2016

Geological Layer K Grade Total Brine

Volume Drainable Brine

Volume Drainable Brine

SOP

mg/L M m3 M m3 Mt K2SO4

Indicated Resource

Alluvium 7,145 52 19 0.30

Clays 7,145 349 21 0.33

Basal Sands 7,145 27 19 0.30

Total 7,145 428 59 0.93

Inferred Resource

Alluvium 6,051 1,935 700 9.45

Clays 6,051 8,270 496 6.70

Basal Sands 6,051 286 200 2.70

Total 6,051 10,491 1,396 18.85

Source: Technical Report

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 16

Table 15: Exploration Target

Geological Layer K Grade Total Brine

Volume Drainable Brine

Volume Drainable Brine

SOP

mg/L M m3 M m3 Mt K2SO4

Minimum Exploration Target

Alluvium 1,100 2,186 546 1.34

Clays 1,100 19,512 434 1.06

Basal Sands 1,100 806 461 1.13

Total 1,100 22,504 1,441 3.53

Maximum Exploration Target

Alluvium 4,515 2,733 1,093 11.01

Clays 4,515 23,848 1,734 17.46

Basal Sands 4,515 1,036 691 6.96

Total 4,515 27,617 3,518 35.43

Source: Technical Report

Figure 14: Plan of the BPP Resource.

Source: Kalium Lakes

Extraction and Processing

It is envisaged that brine production will primarily be via extraction bores targeting brines within the

basal sands aquifer, augmented by brine pumped from trenches in the surficial alluvium aquifer. The

Company has already successfully extracted over 5 million litres of brine from the basal aquifers during

initial short duration pump tests.

The brine will be pumped into sequential evaporation ponds. In the initial two ponds, gypsum

(CaSO4.2H2O), halite (NaCl), and astrakanite (NaMg(SO).4H2O) will precipitate, with the residual brine

pumped to the next ponds, where it crystallises as a Kainite (KMgSO4Cl.3H2O) Type Mixed Salt

(“KTMSalt”) comprising leonitic, schoenitic and carnallitic mixed salts. These mixed salts are harvested,

and stored for further processing by the SOP plant. The residual bittern may be further processed to

Epsomite (MgSO4.7H2O), a potential byproduct

The remaining solution is then evaporated and mixed with a calcium chloride (CaCl2) solution, producing

gypsum and a magnesium chloride brine, to which quicklime (CaO) is added before evaporation to

produce bischofite (MgCl.6H2O).

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 17

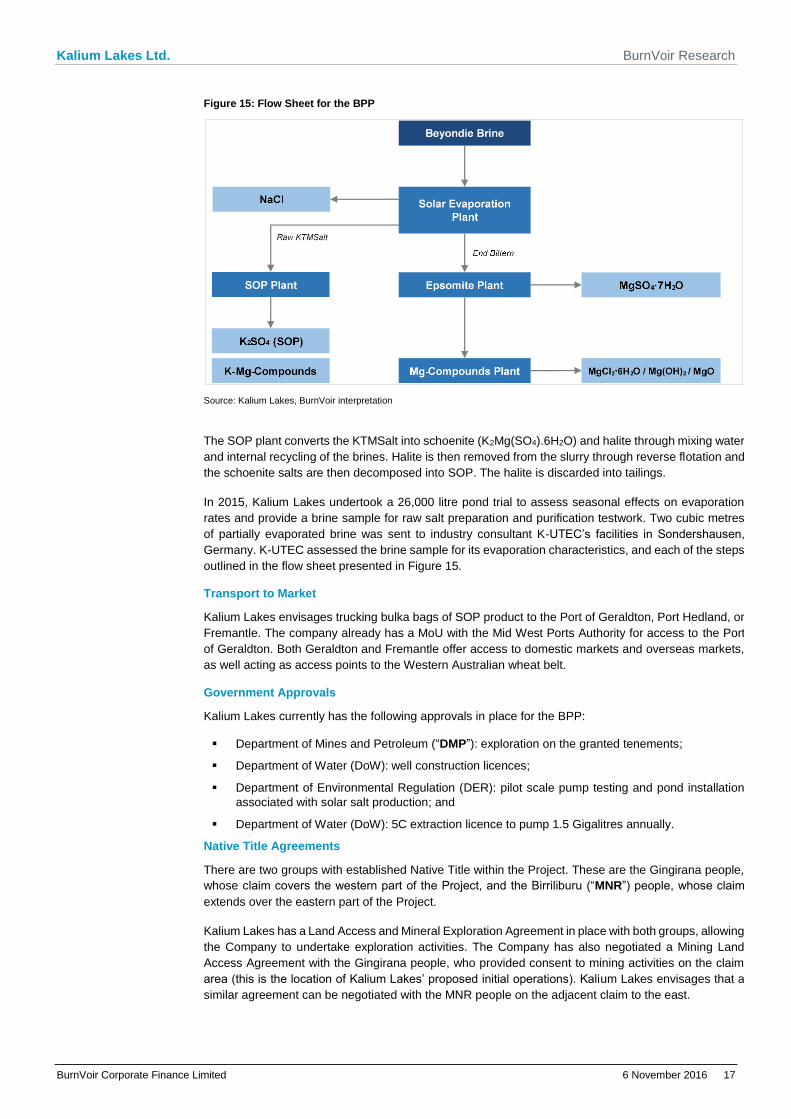

Figure 15: Flow Sheet for the BPP

Source: Kalium Lakes, BurnVoir interpretation

The SOP plant converts the KTMSalt into schoenite (K2Mg(SO4).6H2O) and halite through mixing water

and internal recycling of the brines. Halite is then removed from the slurry through reverse flotation and

the schoenite salts are then decomposed into SOP. The halite is discarded into tailings.

In 2015, Kalium Lakes undertook a 26,000 litre pond trial to assess seasonal effects on evaporation

rates and provide a brine sample for raw salt preparation and purification testwork. Two cubic metres

of partially evaporated brine was sent to industry consultant K-UTEC’s facilities in Sondershausen,

Germany. K-UTEC assessed the brine sample for its evaporation characteristics, and each of the steps

outlined in the flow sheet presented in Figure 15.

Transport to Market

Kalium Lakes envisages trucking bulka bags of SOP product to the Port of Geraldton, Port Hedland, or

Fremantle. The company already has a MoU with the Mid West Ports Authority for access to the Port

of Geraldton. Both Geraldton and Fremantle offer access to domestic markets and overseas markets,

as well acting as access points to the Western Australian wheat belt.

Government Approvals

Kalium Lakes currently has the following approvals in place for the BPP:

Department of Mines and Petroleum (“DMP”): exploration on the granted tenements;

Department of Water (DoW): well construction licences;

Department of Environmental Regulation (DER): pilot scale pump testing and pond installation

associated with solar salt production; and

Department of Water (DoW): 5C extraction licence to pump 1.5 Gigalitres annually.

Native Title Agreements

There are two groups with established Native Title within the Project. These are the Gingirana people,

whose claim covers the western part of the Project, and the Birriliburu (“MNR”) people, whose claim

extends over the eastern part of the Project.

Kalium Lakes has a Land Access and Mineral Exploration Agreement in place with both groups, allowing

the Company to undertake exploration activities. The Company has also negotiated a Mining Land

Access Agreement with the Gingirana people, who provided consent to mining activities on the claim

area (this is the location of Kalium Lakes’ proposed initial operations). Kalium Lakes envisages that a

similar agreement can be negotiated with the MNR people on the adjacent claim to the east.

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 18

Potash Themes

Growing population requires increased agricultural yields

The global population continues to grow, with increasing urbanisation leading to a reduction in arable

land. These two factors combine to reduce the arable land per capita (refer Figure 16). A further

complication is the increase in dietary intake (and quality) of urban inhabitants versus their rural

counterparts. To address this issue, arable land must increase or higher crop intensity / crop yields are

required to meet the food requirements of the growing population.

The Food and Agriculture Organisation (“FAO”) of the United Nations considers that fertilisers will be

the dominant factor to increase crop yields, which is reflected in the increase in fertiliser demand as

presented in Figure 17.

Figure 16: Global Population and Arable Land Per Capita

An increasing population with decreasing arable land to feed it

Figure 17: Global Fertiliser Consumption

Fertiliser demand responds as a means to address the issue

Source: FAO, United Nations, Potash Corp Source: FAO, United Nations, Potash Corp

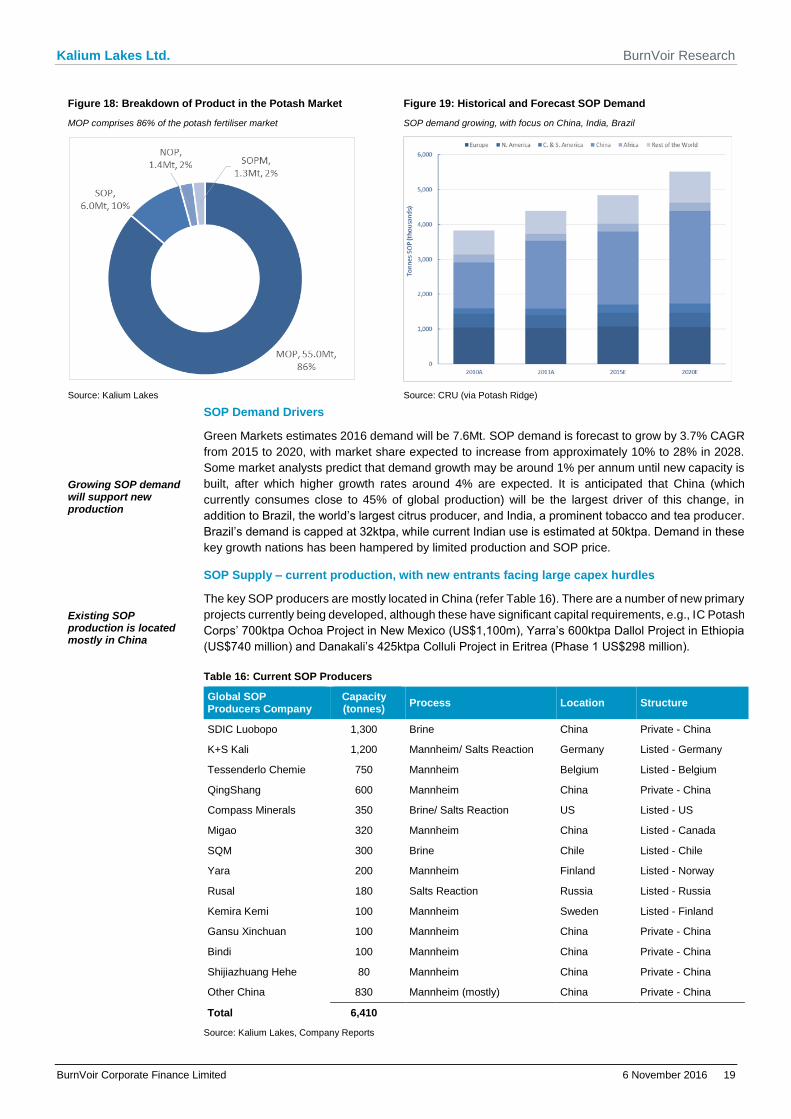

Know your potash

The global potash market totals 60-70Mt annually. Within this market there are four key potash products;

Muriate of Potash (“MOP”), Sulphate of Potash (“SOP”), Sulphate of Potash Magnesia (“SOPM”) and

Nitrate of Potash (“NOP”) (refer Figure 18).

MOP (50% potassium, 46% chloride) is the most common form of potash, and the cheapest. The

chloride content can be beneficial where soil salinity is not an issue, otherwise its use may it cause

toxicity if soil or water irrigation chloride levels are elevated. Current pricing is US$200-220/t (FOB

Vancouver).

SOP (41% potassium and 18% sulphur) is required for crops that are chloride sensitive, or where soil

or water irrigation contains elevated chloride levels, or where sulphur is deficient. SOP can be used to

replaced MOP, and enhances yield and quality, extends shelf life of produce, and improves taste. It is

mainly used for leafy plants and high value crops, such as tobacco, tea, fruit, and vegetables, nuts,

horticultural plants. Current pricing is US$600-700/t (USA ex store Florida).

SOPM (18% potassium, 11% magnesium, and 22% sulphur) is primarily used for high value crops.

NOP (38% potassium and 13% nitrogen) is also referred to as saltpetre and is applied to crops that are

highly sensitive to chloride. Given it is highly soluble, it is frequently used in foliar sprays and fertigation

systems. NOP is currently priced at US$825/t (FOB China).

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 19

Figure 18: Breakdown of Product in the Potash Market

MOP comprises 86% of the potash fertiliser market

Figure 19: Historical and Forecast SOP Demand

SOP demand growing, with focus on China, India, Brazil

Source: Kalium Lakes Source: CRU (via Potash Ridge)

SOP Demand Drivers

Growing SOP demand will support new production

Green Markets estimates 2016 demand will be 7.6Mt. SOP demand is forecast to grow by 3.7% CAGR

from 2015 to 2020, with market share expected to increase from approximately 10% to 28% in 2028.

Some market analysts predict that demand growth may be around 1% per annum until new capacity is

built, after which higher growth rates around 4% are expected. It is anticipated that China (which

currently consumes close to 45% of global production) will be the largest driver of this change, in

addition to Brazil, the world’s largest citrus producer, and India, a prominent tobacco and tea producer.

Brazil’s demand is capped at 32ktpa, while current Indian use is estimated at 50ktpa. Demand in these

key growth nations has been hampered by limited production and SOP price.

SOP Supply – current production, with new entrants facing large capex hurdles

Existing SOP production is located mostly in China

The key SOP producers are mostly located in China (refer Table 16). There are a number of new primary

projects currently being developed, although these have significant capital requirements, e.g., IC Potash

Corps’ 700ktpa Ochoa Project in New Mexico (US$1,100m), Yarra’s 600ktpa Dallol Project in Ethiopia

(US$740 million) and Danakali’s 425ktpa Colluli Project in Eritrea (Phase 1 US$298 million).

Table 16: Current SOP Producers

Global SOP Producers Company

Capacity (tonnes)

Process Location Structure

SDIC Luobopo 1,300 Brine China Private - China

K+S Kali 1,200 Mannheim/ Salts Reaction Germany Listed - Germany

Tessenderlo Chemie 750 Mannheim Belgium Listed - Belgium

QingShang 600 Mannheim China Private - China

Compass Minerals 350 Brine/ Salts Reaction US Listed - US

Migao 320 Mannheim China Listed - Canada

SQM 300 Brine Chile Listed - Chile

Yara 200 Mannheim Finland Listed - Norway

Rusal 180 Salts Reaction Russia Listed - Russia

Kemira Kemi 100 Mannheim Sweden Listed - Finland

Gansu Xinchuan 100 Mannheim China Private - China

Bindi 100 Mannheim China Private - China

Shijiazhuang Hehe 80 Mannheim China Private - China

Other China 830 Mannheim (mostly) China Private - China

Total 6,410

Source: Kalium Lakes, Company Reports

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 20

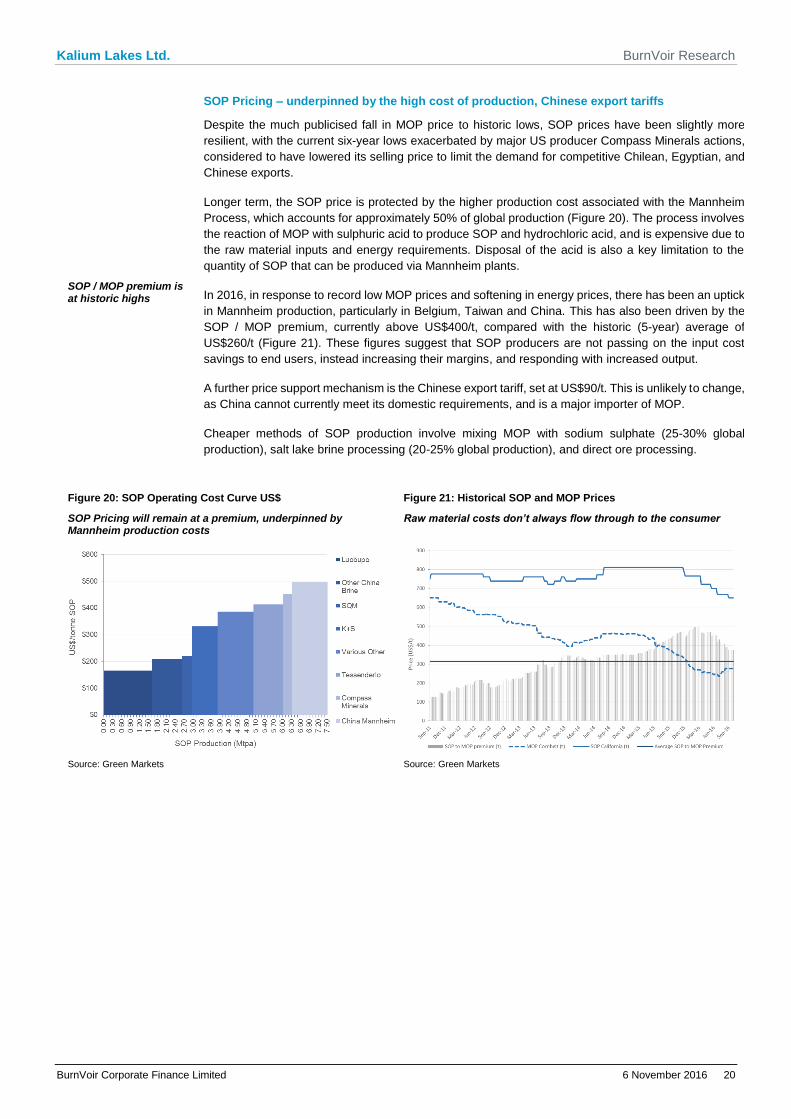

SOP Pricing – underpinned by the high cost of production, Chinese export tariffs

SOP / MOP premium is at historic highs

Despite the much publicised fall in MOP price to historic lows, SOP prices have been slightly more

resilient, with the current six-year lows exacerbated by major US producer Compass Minerals actions,

considered to have lowered its selling price to limit the demand for competitive Chilean, Egyptian, and

Chinese exports.

Longer term, the SOP price is protected by the higher production cost associated with the Mannheim

Process, which accounts for approximately 50% of global production (Figure 20). The process involves

the reaction of MOP with sulphuric acid to produce SOP and hydrochloric acid, and is expensive due to

the raw material inputs and energy requirements. Disposal of the acid is also a key limitation to the

quantity of SOP that can be produced via Mannheim plants.

In 2016, in response to record low MOP prices and softening in energy prices, there has been an uptick

in Mannheim production, particularly in Belgium, Taiwan and China. This has also been driven by the

SOP / MOP premium, currently above US$400/t, compared with the historic (5-year) average of

US$260/t (Figure 21). These figures suggest that SOP producers are not passing on the input cost

savings to end users, instead increasing their margins, and responding with increased output.

A further price support mechanism is the Chinese export tariff, set at US$90/t. This is unlikely to change,

as China cannot currently meet its domestic requirements, and is a major importer of MOP.

Cheaper methods of SOP production involve mixing MOP with sodium sulphate (25-30% global

production), salt lake brine processing (20-25% global production), and direct ore processing.

Figure 20: SOP Operating Cost Curve US$

SOP Pricing will remain at a premium, underpinned by Mannheim production costs

Figure 21: Historical SOP and MOP Prices

Raw material costs don’t always flow through to the consumer

Source: Green Markets Source: Green Markets

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 21

Investment Risks

Commodity Price: Given its primary business focus, Kalium Lakes will be affected by market sentiment

towards the SOP price.

Currency: The SOP price is US dollar denominated. Therefore, the Company’s future earnings are

exposed to AUDUSD currency movements.

Project Development Risk: Kalium Lakes’ ability to transition from explorer to producer will be

contingent on its ability to prove up the BPP further and convert its Mineral Resources to Ore Reserves

as well as mitigate the risk of construction cost blowouts or construction delays.

Native Title Risk: Kalium Lakes has secured one of the two Native Title Mining Agreements required

for the Beyondie Potash Project. The remaining agreement is currently at the negotiation stage. While

this is not required for the initial planned operation, it will be required if Kalium Lakes wants to extract

brine from the tenements further to the east of the Project.

Government Risk: Government policy changes may impact on the permitting / approvals process,

which could impact Kalium Lakes’ ability to deliver and operate the Project. There is also risk regarding

the DMP’s determination of the applicable royalty for potash; if it determines that potash does not attract

a specific royalty under Amount A per the Mining Regulations 1981, there is a risk of a higher royalty

being applied, leading to lower revenues from the Project.

Financing Risk: All operational and cash flow forecasts are made with the underlying assumption that

Kalium Lakes is able to raise the equity financing detailed in this research note, as well as additional

project financing before development of BPP.

Operating Risk: Once in production, Kalium Lakes will be subject to the usual operating risks that

producers face, which may include weather, processing issues, etc.

Key risks include hydrogeological risks, including such as the recovered brine grade being less than

expected, or highly variable, or not consistently achieving required extraction rates. This would reduce

brine recoverability, result in poor product quality and cause production/ ramp-up delays. Other key

technical risk include being able to extract the brine in way that does not compromise the aquifers. The

Company would also need to manage the brine chemistry through the SOP plant to deliver a product

that meets offtaker / market specifications.

Risks are inherently higher for single project companies due to a lack of diversification.

Delayed Market Entry Risk: Entering the market as quickly as possible is crucial to developing the

BPP. Demand for domestic SOP supply is limited, thus initiating production and locking down offtake

contracts before competing developers will be crucial. If Kalium Lakes is unable to enter production

quickly enough, there is a risk it could get locked out from offtakers, thereby threatening the viability of

the Project or exposing the Project to spot market price volatility.

Key Personnel: Kalium Lakes has assembled a team with extensive geological expertise in the area.

Exploration and production could be affected if these personnel depart.

Liquidity: Following the pre-IPO and IPO raisings, Kalium Lakes will continue to have a tightly held

register, with the top shareholder controlling more than 43% of the register. These shares will likely be

escrowed for a period of up to 24 months. There is no guarantee that there will be an ongoing liquid

market for Kalium Lakes’ shares, and if illiquidity arises, there is a risk that shareholders may not be

able to realise their investment in the Company.

Board of Directors Mal Randall B.Chem, FAICD – Non-Executive Chairman

Mr Randall is a chemical engineer with over 41 years’ experience in corporate management and

marketing in the resources sector, including more than 20 years with the Rio Tinto group of companies.

His experience extends over a broad range of commodities including iron ore, diamonds, base metals,

coal, uranium, mineral sands, and industrial minerals both in Australia and internationally.

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 22

Mr Randall has been an independent non-executive director of Thundelarra Resources Ltd since 2003

and is currently on the boards of MZI Resources Ltd (Chairman), Summit Resources Ltd, and Magnetite

Mines Ltd.

Mr Randall owns 0.45 million shares in the Company, equating to 0.5% of the shares outstanding, and

has 4.0 million Management Options, which have a three year exercise period, and a strike price of

$0.25 per share.

Brett Hazelden B.Sc, MBA, GAICD – Managing Director

Mr Hazelden is a metallurgist with over 19 years’ experience in project management, engineering design and operations within the Australasian resources industry, having previously studied, managed, and executed projects from small scale through to multibillion dollar complex projects.

His experience includes project management, feasibility study evaluation, engineering & design, estimating, financial evaluation, cost control, scheduling, contracts & procurement, business risk and strategic development. Brett has previously worked for iron ore companies including Ferraus Ltd and Iron Ore Holdings Ltd, gold producer Newcrest, engineering and construction firms such as Fluor Corporation, and for Rio Tinto as a metallurgist. Brett’s work experience extends across various iron, copper and gold projects located in South and Western Australia, and Indonesia.

Mr Hazelden owns 13.6 million shares in the Company, equating to 14.9% of the shares outstanding.

He also has 4.2 million Performance Options, which are zero exercise price options, and which vest on

achievement of key project milestones for the Beyondie Potash Project including completion of a DFS,

securing project financing, and commercial production.

As a founding shareholder of Kalium Lakes Potash Pty Ltd, Mr Hazelden is entitled to a royalty on

potash production. The Royalty Deed between Kalium Lakes Potash Pty and a unit trust, of which the

founding shareholders including Mr Hazelden are beneficiaries, grants a royalty of 1.9% of gross

revenue from potash produced to the unit trust. The other beneficiaries are Rudolph van Niekerk and

Brent Smoothy.

Rudolph van Niekerk B.Eng, GAICD – Non-Executive Director

Mr van Niekerk is a mechanical engineer with more than 12 years’ experience in project and business

management. He has held various roles in management of projects and operations, being responsible

for financial evaluation, risk review and management, project management, study management,

development of capital and operating cost estimates, budget development and cost control, design

management, planning, reporting, contract administration, quality control, expediting, construction,

commissioning, production ramp-up and project hand-over to operations. Mr van Niekerk has worked

extensively in iron ore projects located in the Plibara region for Ferraus Ltd and Iron Ore Holdings Ltd,

on a gold project for Newcrest in Indonesia as well as for AngloGold Ashanti and Dowding Reynard &

Associates on several gold and platinum projects located in South Africa.

Mr van Niekerk owns 3.3 million shares in the Company, equating to 3.62% of the shares outstanding.

He also has 1.2 million Performance Options, which are zero exercise price options, and which vest on

achievement of key project milestones for the Beyondie Potash Project including completion of a DFS,

securing project financing, and commercial production.

As a founding shareholder of Kalium Lakes Potash Pty Ltd, Mr van Niekerk is entitled to a royalty on

potash production. The Royalty Deed between Kalium Lakes Potash Pty and a unit trust, of which the

founding shareholders including Mr van Niekerk are beneficiaries, grants a royalty of 1.9% of gross

revenue from potash produced to the unit trust. The other beneficiaries are Brett Hazelden and Brent

Smoothy.

Brendan O’Hara B.Juris, LLB, SS Fin – Non-Executive Director

Mr O’Hara holds Bachelor of Jurisprudence (Hons) and Bachelor of Laws. He is a Senior Fellow of FINSIA and a former legal practitioner of the Supreme Court of WA and a member of the Business Law Section of the Law Council of Australia. His previous roles include eight years as Executive Chairman of ASX-listed Summit Resources Limited, and State Executive Director of the ASX.

Mr O’Hara does not own any shares in the Company. However, he has 2.0 million Management Options,

which have a three year exercise period, and a strike price of $0.25 per share.

Kalium Lakes Ltd. BurnVoir Research

BurnVoir Corporate Finance Limited 6 November 2016 23

This Research has been prepared and issued by BurnVoir Corporate Finance Limited (“BurnVoir”) and remains the property of BurnVoir. No material contained in

this Research may be reproduced or distributed, except as allowed by the Copyright Act, without the prior written approval of BurnVoir.

This report has been prepared and issued (in Australia) by BurnVoir Corporate Finance Limited (ABN 84 097 814 134 / AFS Licence No. 247 387) (“BurnVoir”) and is subject to

the disclosures and restrictions set out below.

Analyst Certification

The research analyst(s) identified on the cover of this report individually certify that in respect of each security or issuer that the research analyst covers that this report accurately reflects his or her personal views about any and all of the subject issuer(s) or securities.

Disclosure

BurnVoir has been appointed Corporate Finance Advisor and Joint Lead Manager to the Initial Public Offering as announced in the Prospectus published by the company on 30 August 2016.

Contact with Kalium Lakes Ltd. has been made during the preparation of this report for assistance with verification of facts.

BurnVoir and its associates (as defined in Chapter 1 of the Corporations Act 2001), officers, directors, employees and agents, from time to time, may own or have positions in securities of the company(ies) covered in this report and may trade in the securities mentioned either as principal or agent or may be materially interested in such securities.

BurnVoir does and seeks to do business with companies covered in its research reports. As a result, investors should consider this report as only a single factor in making their investment decision.

Disclaimer & Warning

This report may contain general advice or recommendations which, while believed to be accurate at the time of publication, are not appropriate for all persons or accounts. This report does not purport to contain all the information that a prospective investor may require. Before making an investment or trading decision, the recipient must consider Market developments subsequent to the date of this document, and whether the advice is appropriate in light of his or her financial circumstances or seek further advice on its appropriateness or should form his/her own independent view given the person’s investment objectives, financial situation and particular needs regarding any securities or Financial Products mentioned herein. Information in this document has been obtained from sources believed to be true but neither BurnVoir nor its associates make any recommendation or warranty concerning the Financial Products or the accuracy, or reliability or completeness of the information or the performance of the companies referred to in this document. Past performance is not indicative of future performance. This document is not an offer, invitation, solicitation or recommendation with respect to the subscription for, purchase or sale of any Financial Product, and neither this document or anything in it shall form the basis of any contract or commitment. Although every attempt has been made to verify the accuracy of the information contained in the document, liability for any errors or omissions (except any statutory liability which cannot be excluded) is specifically excluded by BurnVoir, its associates, officers, directors, employees and agents. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Country specific disclosures

US Investors: This material is intended for use by “major U.S. institutional investors” (as defined in Rule 15(a)-6 of the U.S. Securities Exchange Act of 1934, (SEA 1934)). The

information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, its accuracy is not guaranteed. Additional and supporting information is available upon request. This is not an offer or solicitation of an offer to buy or sell any security or to make any investment. Any opinion or estimate constitutes the preparer's best judgement as of the date of preparation and is subject to change without notice. BurnVoir and their associates or affiliates, and their respective officers, directors and employees may buy or sell securities mentioned herein as agent or principal for their own account.

United Kingdom: This report is issued and distributed by BurnVoir only to persons falling within Articles 19 (5), 38, 47 and 49, of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, (all such persons together being referred to as “relevant persons”). Directors, officers and employees of such entities are also included provided their responsibilities regarding those entitles involve engaging in investment activity. Persons who do not have professional experience relating to investments should not rely on this document.

Canada: The investments or investment services referred to in this document are available in Canada only to “Designated Institutions”, as defined by the Securities Act (Ontario).

Other International Investors: International investors outside the US, UK or Canada are encouraged to contact their local regulatory authorities to determine whether any restrictions apply to their ability to purchase this investment.

Recipient Representations/Warranties: By accepting this report, the recipient represents and warrants that he or she is entitled to receive such report in accordance with the restrictions set out in this document and agrees to be bound by the limitations contained herein. Any failure to comply with these limitations may constitute a violation of law.