Embed Size (px)

Citation preview

K. Ensor, STAT 4211

Spring 2004

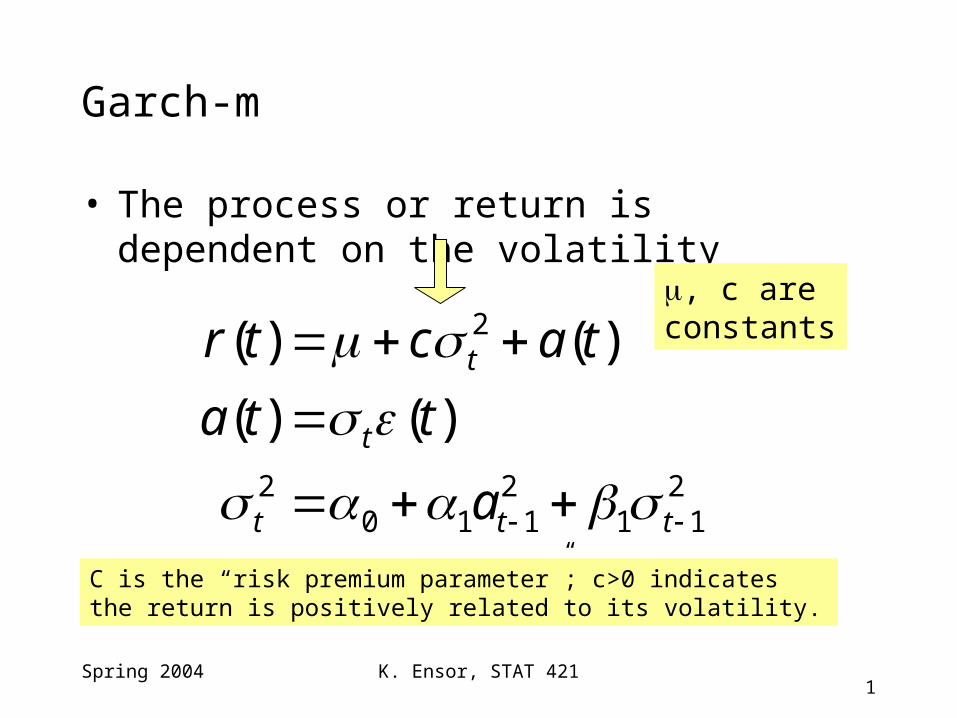

Garch-m

• The process or return is dependent on the volatility

211

2110

2

2

)()(

)()(

ttt

t

t

a

tta

tactr

, c are constants

C is the “risk premium parameter”; c>0 indicates the return is positively related to its volatility.

K. Ensor, STAT 4212

Spring 2004

Time

0 200 400 600 800

-0.2

0.2

Time

0 200 400 600 800

-0.2

0.2

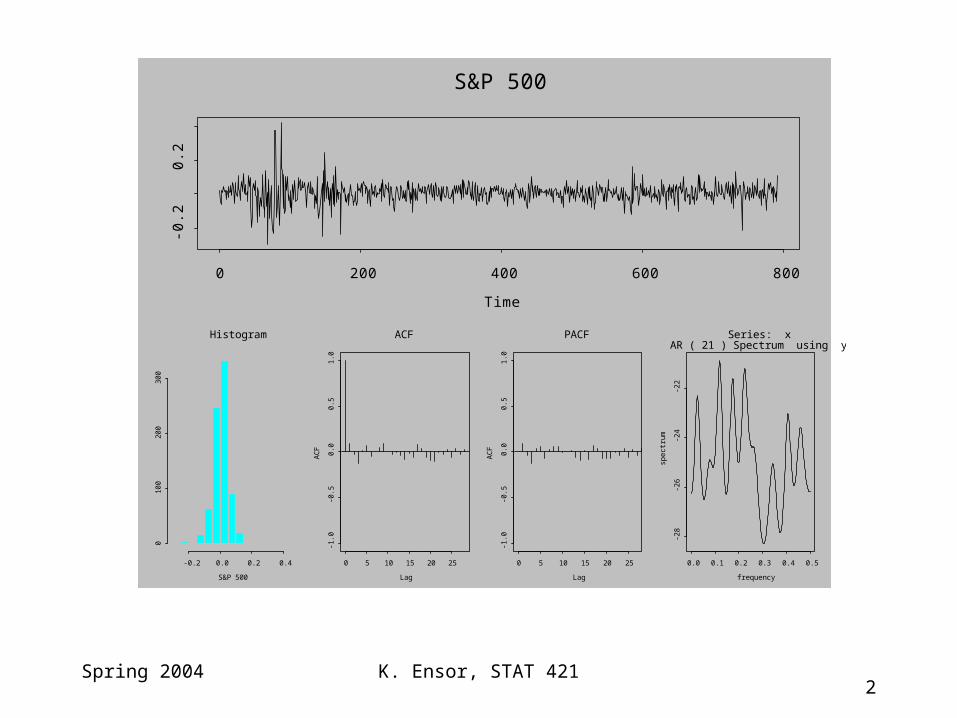

S&P 500

-0.2 0.0 0.2 0.4

01

00

20

03

00

Histogram

S&P 500 Lag

AC

F

0 5 10 15 20 25

-1.0

-0.5

0.0

0.5

1.0

ACF

Lag

AC

F

0 5 10 15 20 25

-1.0

-0.5

0.0

0.5

1.0

PACF

frequency

spe

ctru

m

0.0 0.1 0.2 0.3 0.4 0.5

-28

-26

-24

-22

Series: x AR ( 21 ) Spectrum using yule-walker

K. Ensor, STAT 4213

Spring 2004

Estimated Coefficients:

--------------------------------------------------------------

Value Std.Error t value Pr(>|t|)

C 0.00548675 0.00226173 2.426 7.747e-003

ARCH-IN-MEAN 1.08783589 0.81822755 1.330 9.203e-002

A 0.00008764 0.00002507 3.496 2.494e-004

ARCH(1) 0.12268468 0.02047268 5.993 1.571e-009

GARCH(1) 0.84939373 0.01957565 43.390 0.000e+000

--------------------------------------------------------------

Output from Splus m-garch fitgarch(x~1+var.in.mean,~garch(1,1))

Differs from Tsay’s fit slightly.

K. Ensor, STAT 4214

Spring 2004

-0.2

0.0

0.2

0.4

0 200 400 600 800

Conditional SD

0.05

0.10

0.15

0.20

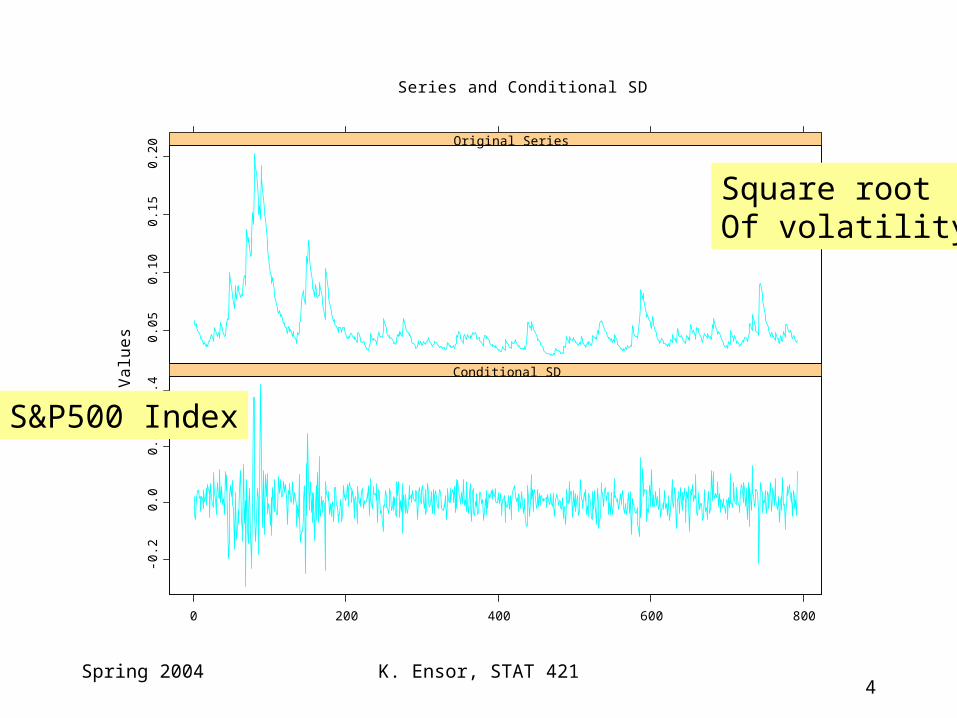

Original SeriesV

alu

es

Series and Conditional SD

S&P500 Index

Square rootOf volatility

K. Ensor, STAT 4215

Spring 2004

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25 30

ACF

Lags

ACF of Squared Observations

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25 30

ACF

Lags

ACF of Observations

-4

-2

0

2

0 200 400 600 800

residuals

Sta

nd

ard

ize

d R

esi

du

als

GARCH Standardized Residuals

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25 30

ACF

Lags

ACF of Std. Residuals

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25 30

ACF

Lags

ACF of Squared Std. Residuals

-4

-2

0

2

-3 -2 -1 0 1 2 3

QQ-Plot

147

173

742

Quantiles of gaussian distribution

Sta

nd

ard

ize

d R

esi

du

als

QQ-Plot of Standardized Residuals

Summary Graphs

K. Ensor, STAT 4216

Spring 2004

-10

-50

510

15

0 100 200 300 400 500

Conditional SD

24

68

Original Series

Va

lue

s

Series and Conditional SD

Hong Kong stock market index return (bottom graph) and estimated volatility.

K. Ensor, STAT 4217

Spring 2004

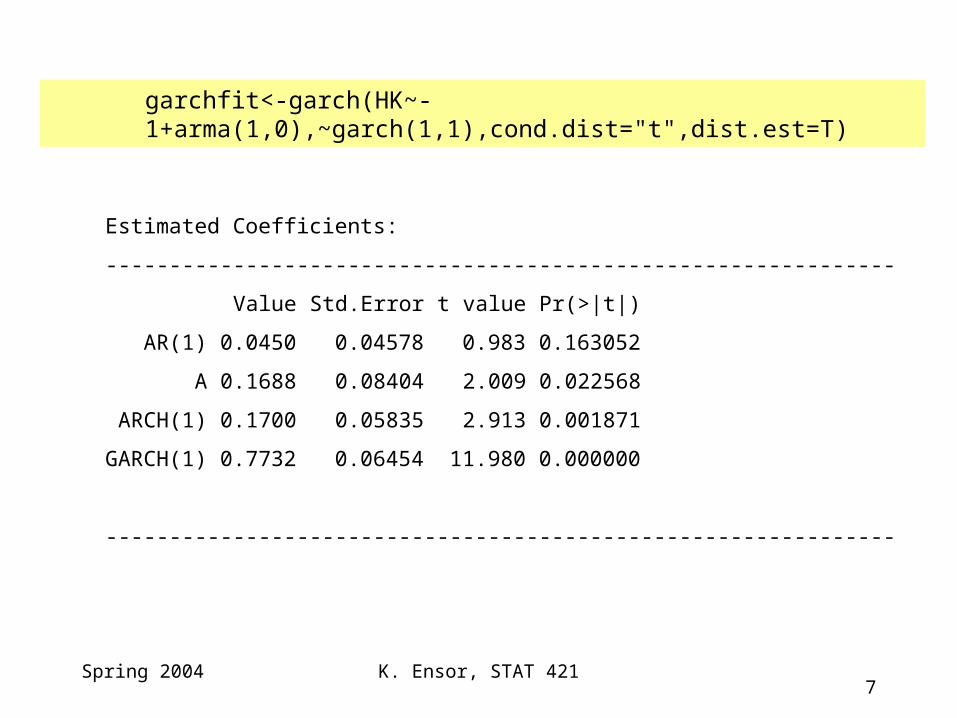

Estimated Coefficients:

--------------------------------------------------------------

Value Std.Error t value Pr(>|t|)

AR(1) 0.0450 0.04578 0.983 0.163052

A 0.1688 0.08404 2.009 0.022568

ARCH(1) 0.1700 0.05835 2.913 0.001871

GARCH(1) 0.7732 0.06454 11.980 0.000000

--------------------------------------------------------------

garchfit<-garch(HK~-1+arma(1,0),~garch(1,1),cond.dist="t",dist.est=T)

K. Ensor, STAT 4218

Spring 2004

-10

0

10

0 100 200 300 400 500

garchfit

Va

lue

s

Series with 2 Conditional SD Superimposed

HK - Garch fit +/- 2SD

K. Ensor, STAT 4219

Spring 2004

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Observations

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Squared Observations

-6

-4

-2

0

2

0 100 200 300 400 500

residuals

Sta

nd

ard

ize

d R

esi

du

als

GARCH Standardized Residuals

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Std. Residuals

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Squared Std. Residuals

-6

-4

-2

0

2

4

6

-5 0 5

QQ-Plot

32

1

Quantiles of t distribution

Sta

nd

ard

ize

d R

esi

du

als

QQ-Plot of Standardized Residuals

K. Ensor, STAT 42110

Spring 2004

--------------------------------------------------------------

Estimated Coefficients:

--------------------------------------------------------------

Value Std.Error t value Pr(>|t|)

AR(1) 0.1199 0.05709 2.100 1.811e-002

A 0.1424 0.04834 2.946 1.687e-003

ARCH(1) 0.1782 0.03693 4.827 9.287e-007

GARCH(1) 0.7592 0.04913 15.452 0.000e+000

--------------------------------------------------------------

garchfit<-garch(HK~-1+arma(1,0),~garch(1,1),cond.dist="gaussian",dist.est=T)

K. Ensor, STAT 42111

Spring 2004

-10

-50

510

15

0 100 200 300 400 500

Conditional SD

24

68

10

Original Series

Va

lue

s

Series and Conditional SD

K. Ensor, STAT 42112

Spring 2004

-20

-10

0

10

20

0 100 200 300 400 500

garchfit

Va

lue

s

Series with 2 Conditional SD Superimposed

K. Ensor, STAT 42113

Spring 2004

-6

-4

-2

0

2

0 100 200 300 400 500

residuals

Sta

nd

ard

ize

d R

esi

du

als

GARCH Standardized Residuals

-6

-4

-2

0

2

-3 -2 -1 0 1 2 3

QQ-Plot

471434

51

Quantiles of gaussian distribution

Sta

nd

ard

ize

d R

esi

du

als

QQ-Plot of Standardized Residuals

K. Ensor, STAT 42114

Spring 2004

-10

-50

510

15

0 100 200 300 400 500

Conditional SD

24

68

Original Series

Va

lue

s

Series and Conditional SD

Japanese stock market index and volatility based on Gaussian GARCH(1,1) model

K. Ensor, STAT 42115

Spring 2004

--------------------------------------------------------------

Estimated Coefficients:

--------------------------------------------------------------

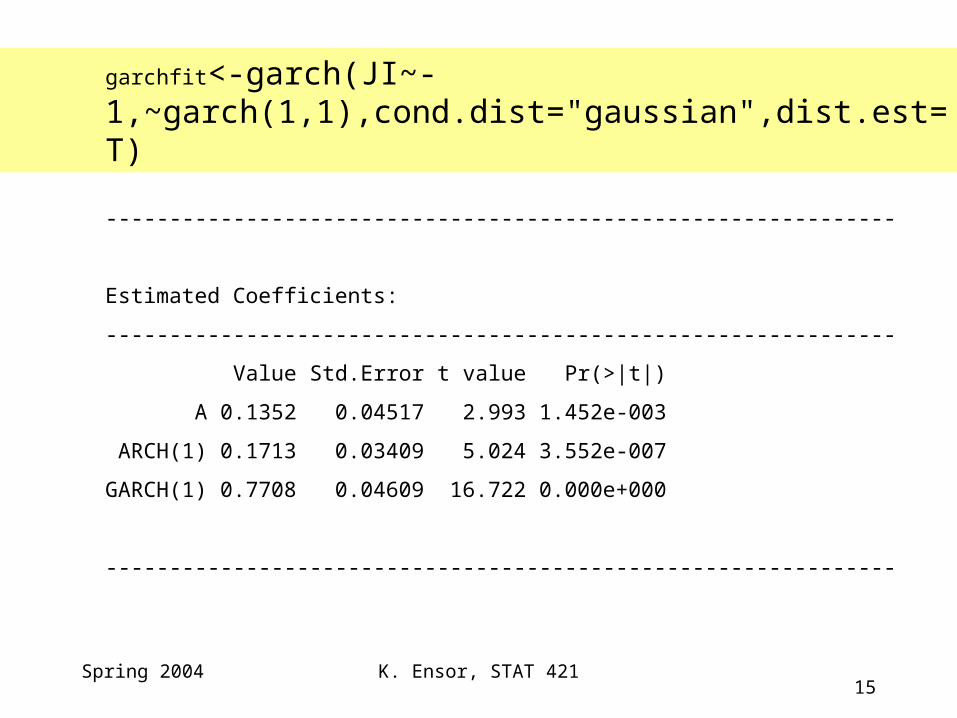

Value Std.Error t value Pr(>|t|)

A 0.1352 0.04517 2.993 1.452e-003

ARCH(1) 0.1713 0.03409 5.024 3.552e-007

GARCH(1) 0.7708 0.04609 16.722 0.000e+000

--------------------------------------------------------------

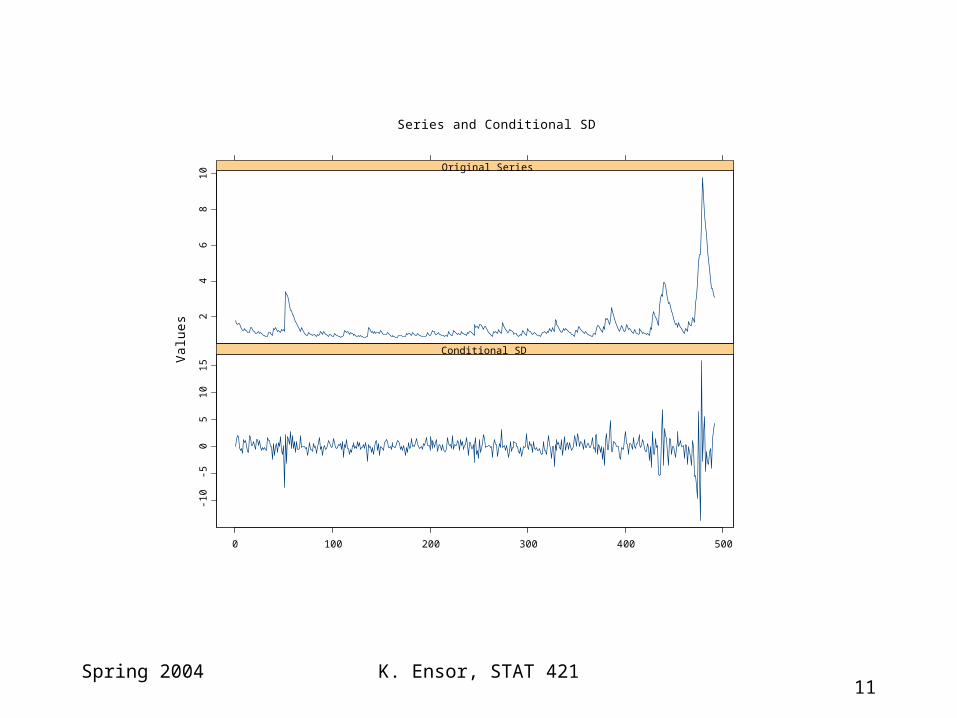

garchfit<-garch(JI~-1,~garch(1,1),cond.dist="gaussian",dist.est=T)

K. Ensor, STAT 42116

Spring 2004

-20

-10

0

10

20

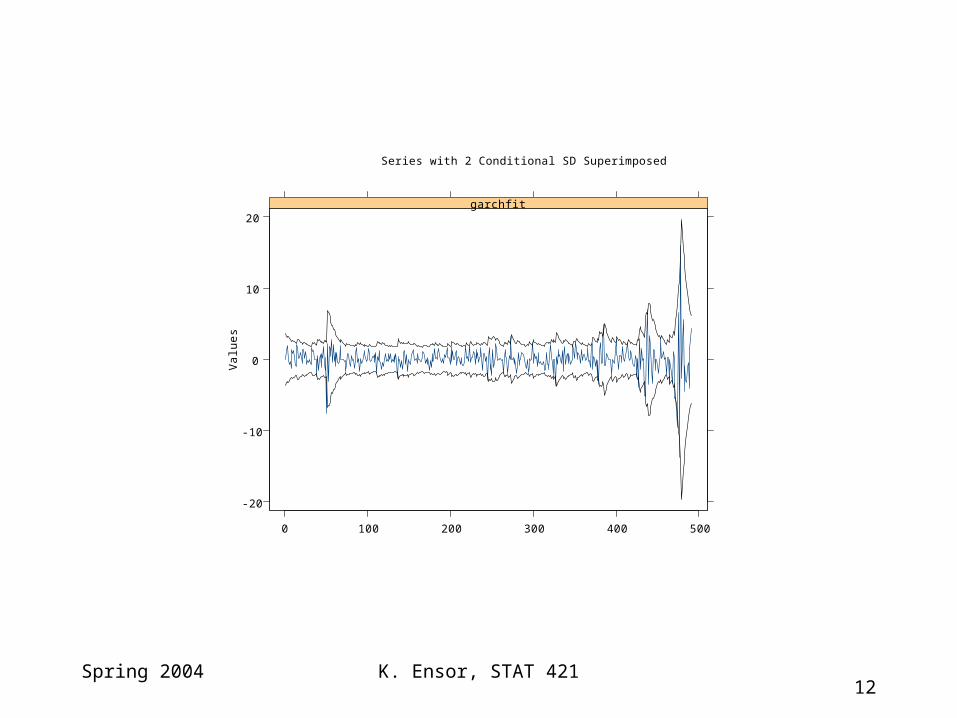

0 100 200 300 400 500

garchfitV

alu

es

Series with 2 Conditional SD Superimposed

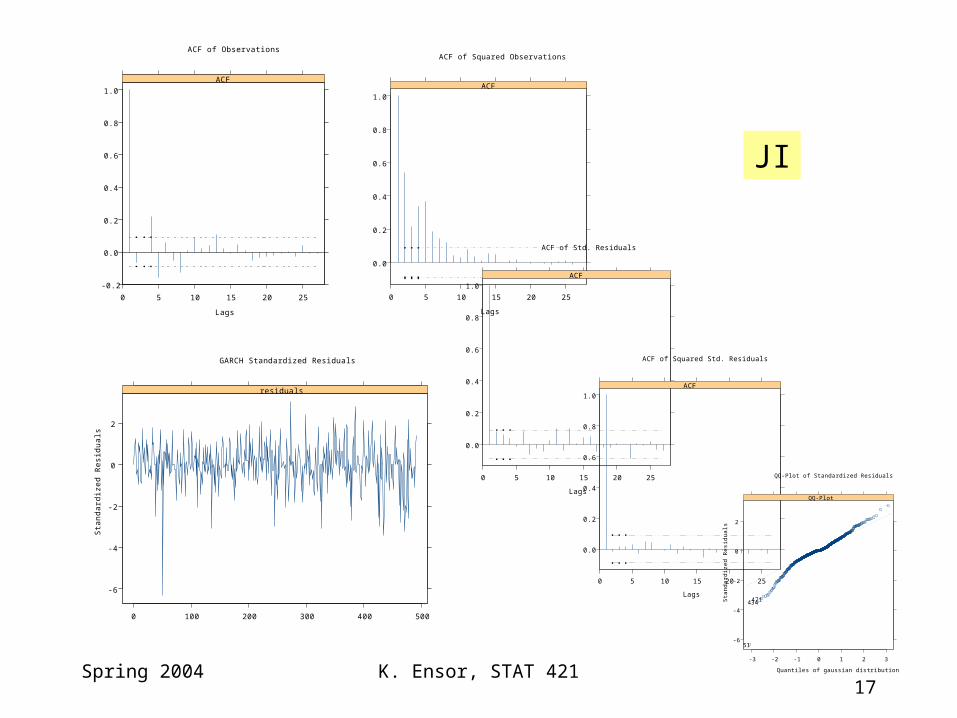

JI

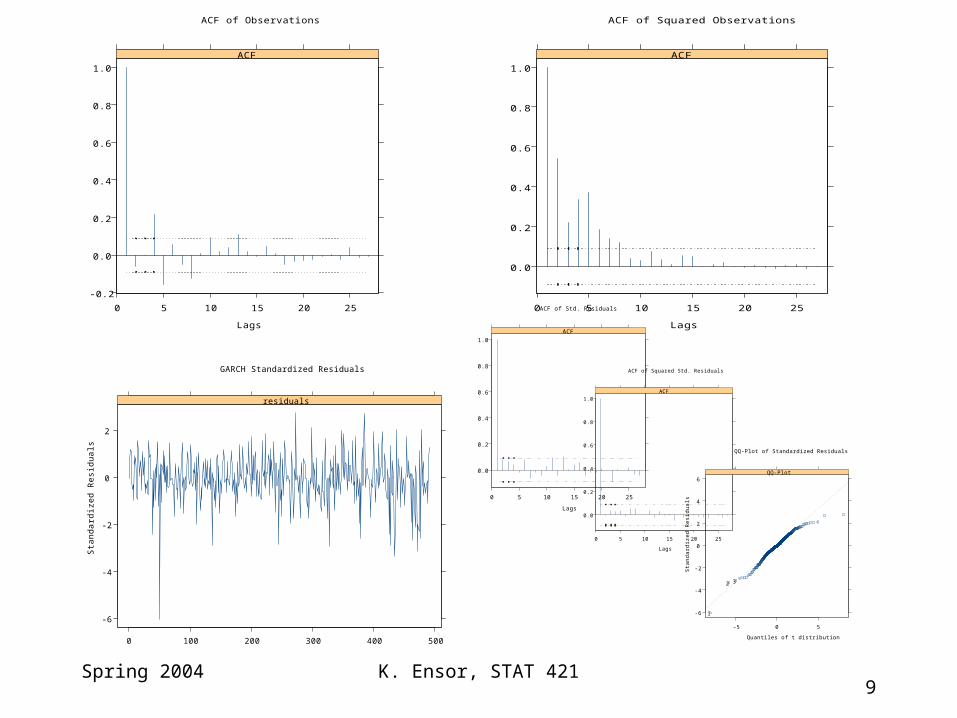

K. Ensor, STAT 42117

Spring 2004

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Observations

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Squared Observations

-6

-4

-2

0

2

0 100 200 300 400 500

residuals

Sta

nd

ard

ize

d R

esi

du

als

GARCH Standardized Residuals

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Std. Residuals

0.0

0.2

0.4

0.6

0.8

1.0

0 5 10 15 20 25

ACF

Lags

ACF of Squared Std. Residuals

-6

-4

-2

0

2

-3 -2 -1 0 1 2 3

QQ-Plot

471434

51

Quantiles of gaussian distribution

Sta

nd

ard

ize

d R

esi

du

als

QQ-Plot of Standardized Residuals

JI

K. Ensor, STAT 42118

Spring 2004

-10

-50

510

15

0 100 200 300 400 500

Series 1

-4-2

02

46

8

Series 2V

alu

es

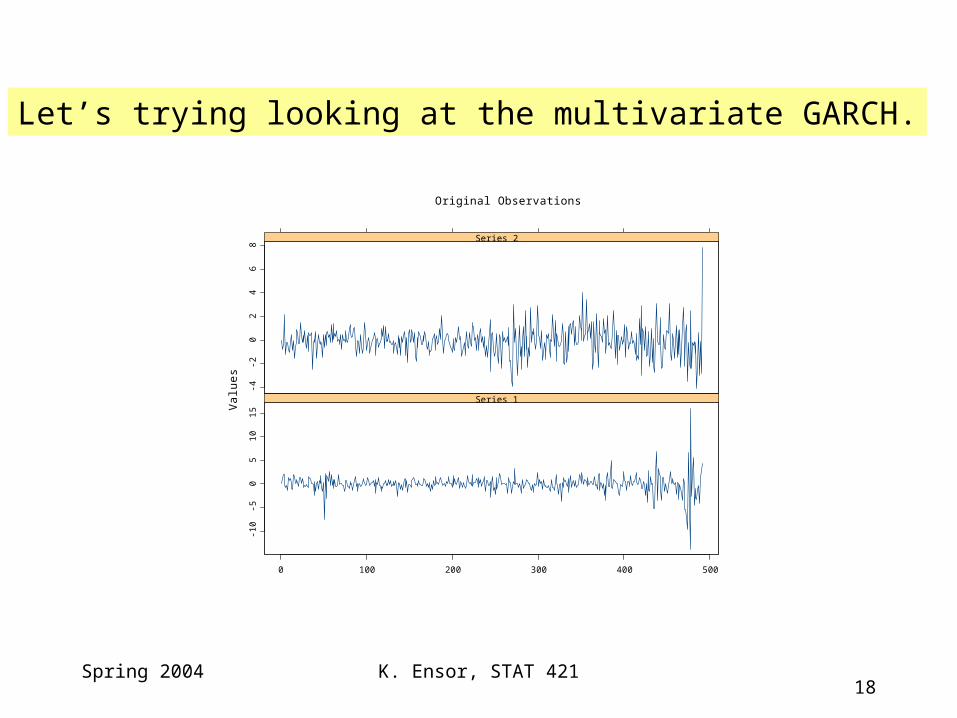

Original Observations

Let’s trying looking at the multivariate GARCH.

K. Ensor, STAT 42119

Spring 2004

Series 1: Hong Kong Stock IndexSeries 2: Japanese Stock Index

Series 1 A

CF

0 5 10 15 20 25

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Series 1 and Series 2

0 5 10 15 20 25

-0.1

0.0

0.1

0.2

0.3

Series 2 and Series 1

Lag

AC

F

-25 -20 -15 -10 -5 0

-0.1

0.0

0.1

0.2

0.3

Series 2

Lag0 5 10 15 20 25

0.0

0.2

0.4

0.6

0.8

1.0

ACF of Observations

K. Ensor, STAT 42120

Spring 2004

Series 1 A

CF

0 5 10 15 20

0.0

0.2

0.4

0.6

0.8

1.0

Series 1 and Series 2

0 5 10 15 20

-0.0

50

.00

.05

0.1

00

.15

Series 2 and Series 1

Lag

AC

F

-20 -15 -10 -5 0

0.0

0.2

0.4

0.6

Series 2

Lag0 5 10 15 20

0.0

0.2

0.4

0.6

0.8

1.0

Multivariate Series : X

Series 1: Hong Kong Stock Index SquaredSeries 2: Japanese Stock Index Squared

K. Ensor, STAT 42121

Spring 2004

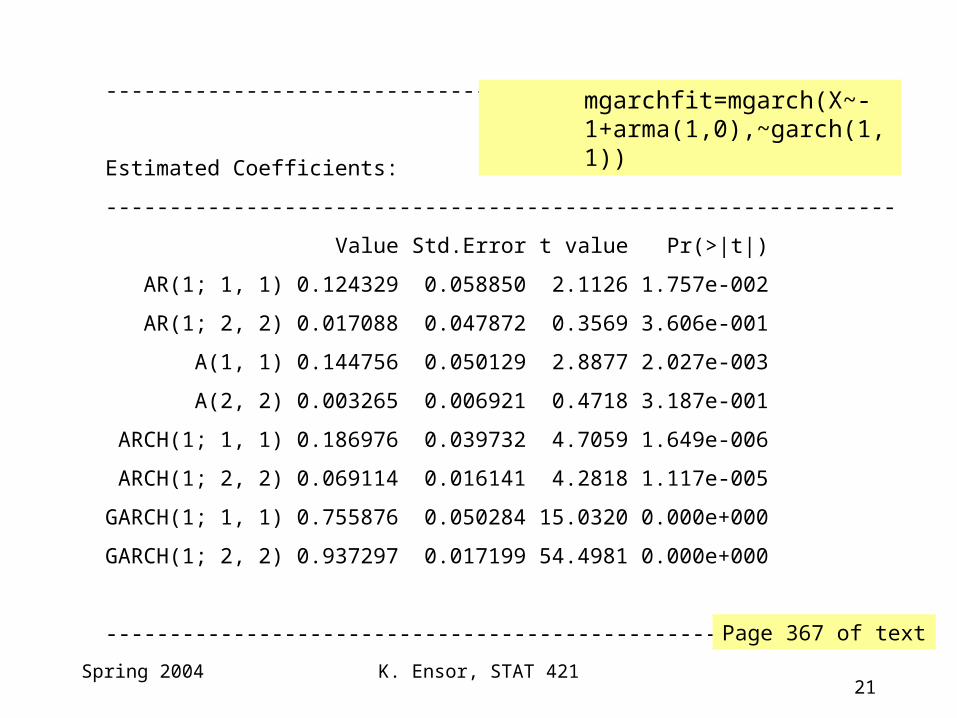

--------------------------------------------------------------

Estimated Coefficients:

--------------------------------------------------------------

Value Std.Error t value Pr(>|t|)

AR(1; 1, 1) 0.124329 0.058850 2.1126 1.757e-002

AR(1; 2, 2) 0.017088 0.047872 0.3569 3.606e-001

A(1, 1) 0.144756 0.050129 2.8877 2.027e-003

A(2, 2) 0.003265 0.006921 0.4718 3.187e-001

ARCH(1; 1, 1) 0.186976 0.039732 4.7059 1.649e-006

ARCH(1; 2, 2) 0.069114 0.016141 4.2818 1.117e-005

GARCH(1; 1, 1) 0.755876 0.050284 15.0320 0.000e+000

GARCH(1; 2, 2) 0.937297 0.017199 54.4981 0.000e+000

--------------------------------------------------------------

mgarchfit=mgarch(X~-1+arma(1,0),~garch(1,1))

Page 367 of text

K. Ensor, STAT 42122

Spring 2004

-10

-50

510

15

0 100 200 300 400 500

Series 1

-4-2

02

46

8

Series 2

Re

sid

ua

ls

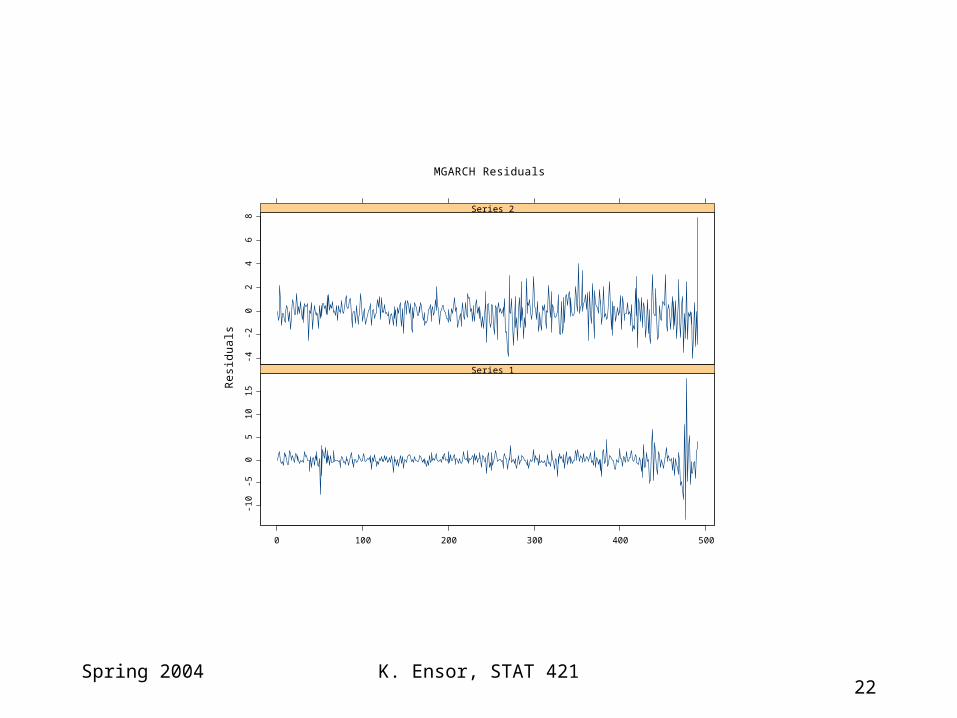

MGARCH Residuals

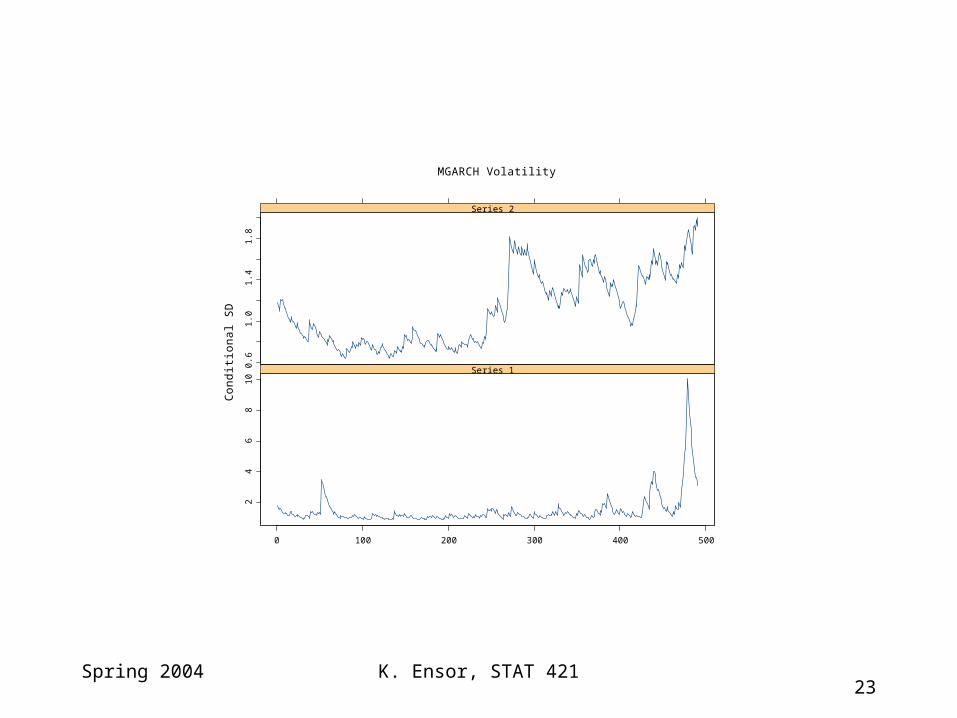

K. Ensor, STAT 42123

Spring 2004

24

68

10

0 100 200 300 400 500

Series 10.6

1.0

1.4

1.8

Series 2

Co

nd

itio

na

l SD

MGARCH Volatility

K. Ensor, STAT 42124

Spring 2004

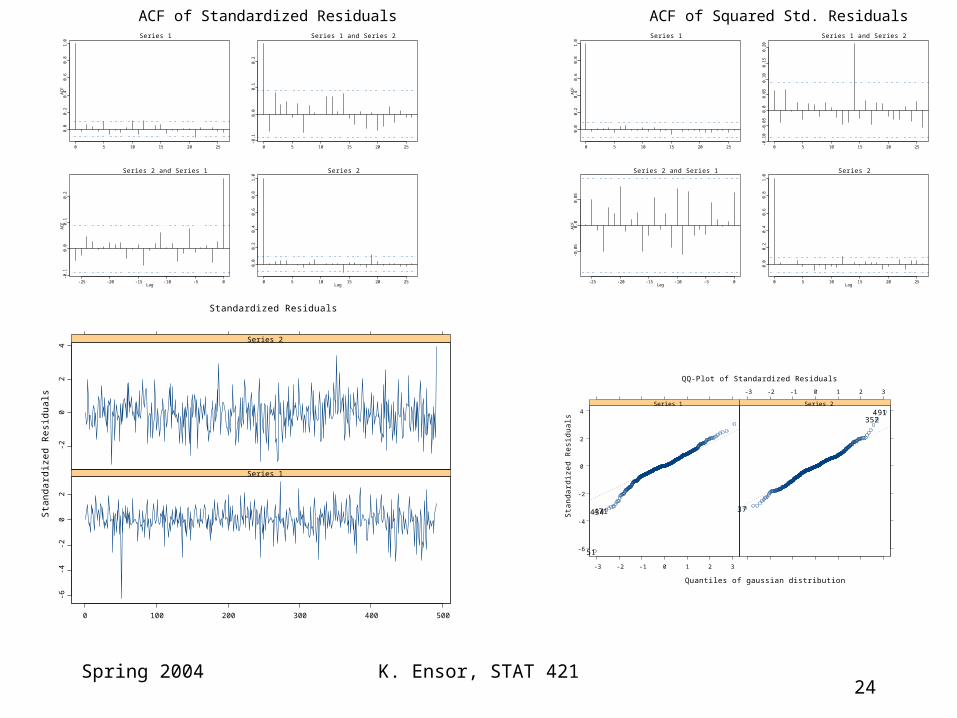

-6-4

-20

2

0 100 200 300 400 500

Series 1

-20

24

Series 2

Sta

nd

ard

ize

d R

esi

du

als

Standardized Residuals

Series 1

AC

F

0 5 10 15 20 25

0.0

0.2

0.4

0.6

0.8

1.0

Series 1 and Series 2

0 5 10 15 20 25

-0.1

0.0

0.1

0.2

Series 2 and Series 1

Lag

AC

F

-25 -20 -15 -10 -5 0

-0.1

0.0

0.1

0.2

Series 2

Lag0 5 10 15 20 25

0.0

0.2

0.4

0.6

0.8

1.0

ACF of Standardized Residuals Series 1

AC

F

0 5 10 15 20 25

0.0

0.2

0.4

0.6

0.8

1.0

Series 1 and Series 2

0 5 10 15 20 25

-0.1

0-0

.05

0.0

0.0

50

.10

0.1

50

.20

Series 2 and Series 1

Lag

AC

F

-25 -20 -15 -10 -5 0

-0.0

50

.00

.05

Series 2

Lag0 5 10 15 20 25

0.0

0.2

0.4

0.6

0.8

1.0

ACF of Squared Std. Residuals

-6

-4

-2

0

2

4

-3 -2 -1 0 1 2 3

Series 1

471434

51

-3 -2 -1 0 1 2 3

Series 2

37

352491

Quantiles of gaussian distribution

Sta

nd

ard

ize

d R

esi

du

als

QQ-Plot of Standardized Residuals