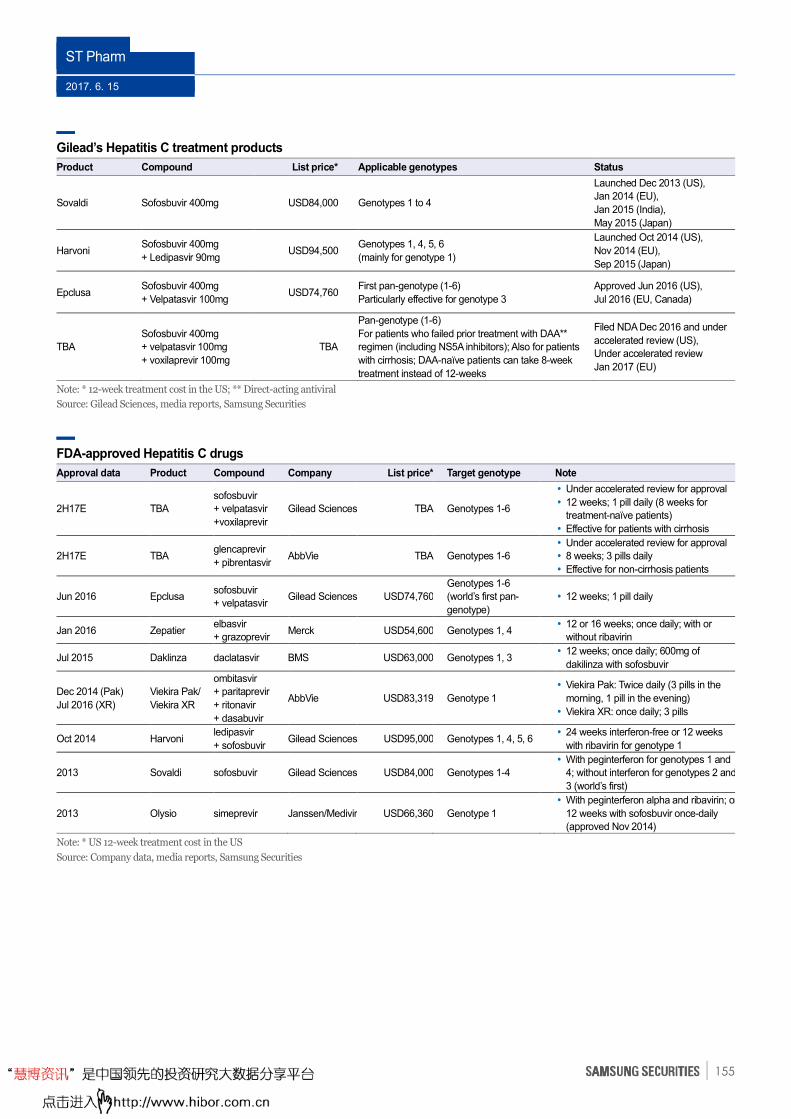

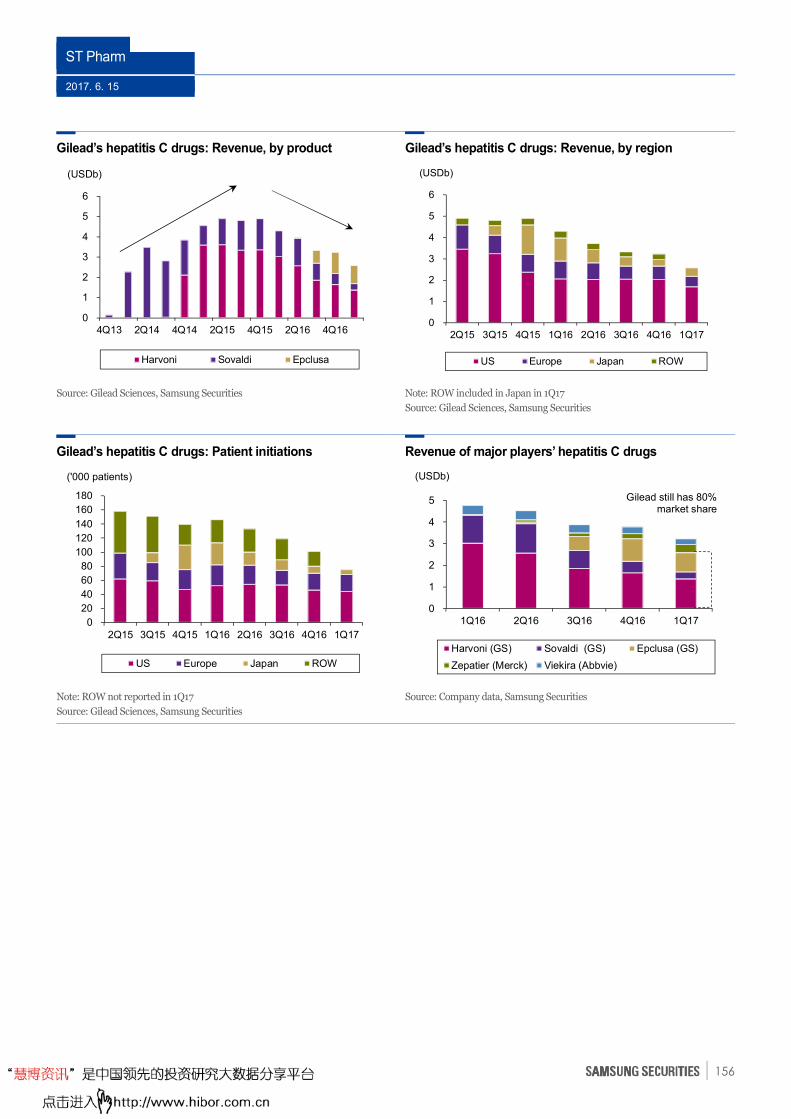

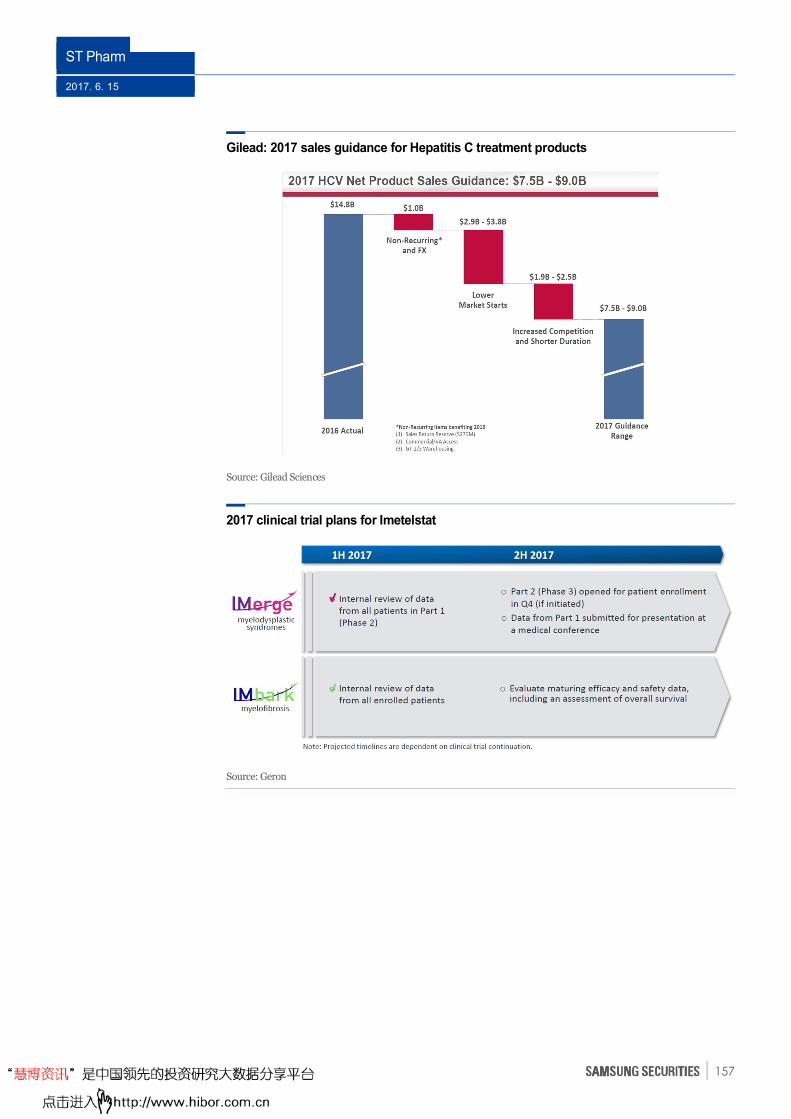

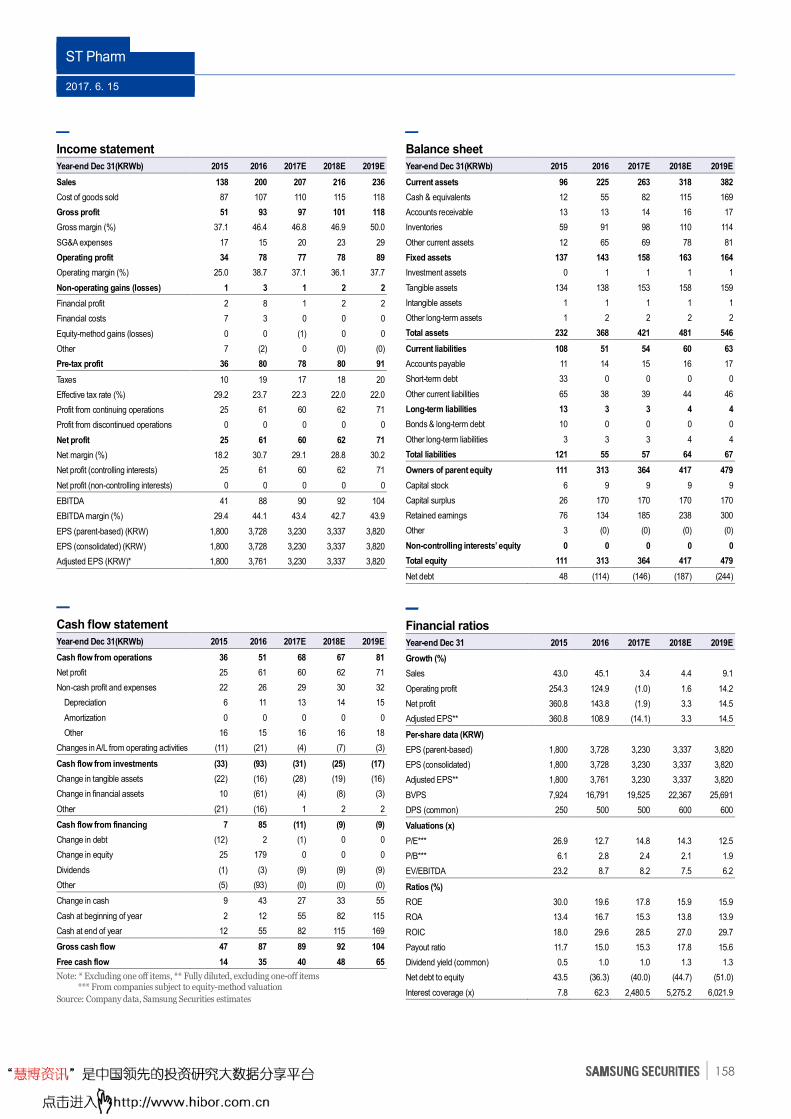

Embed Size (px)

Citation preview

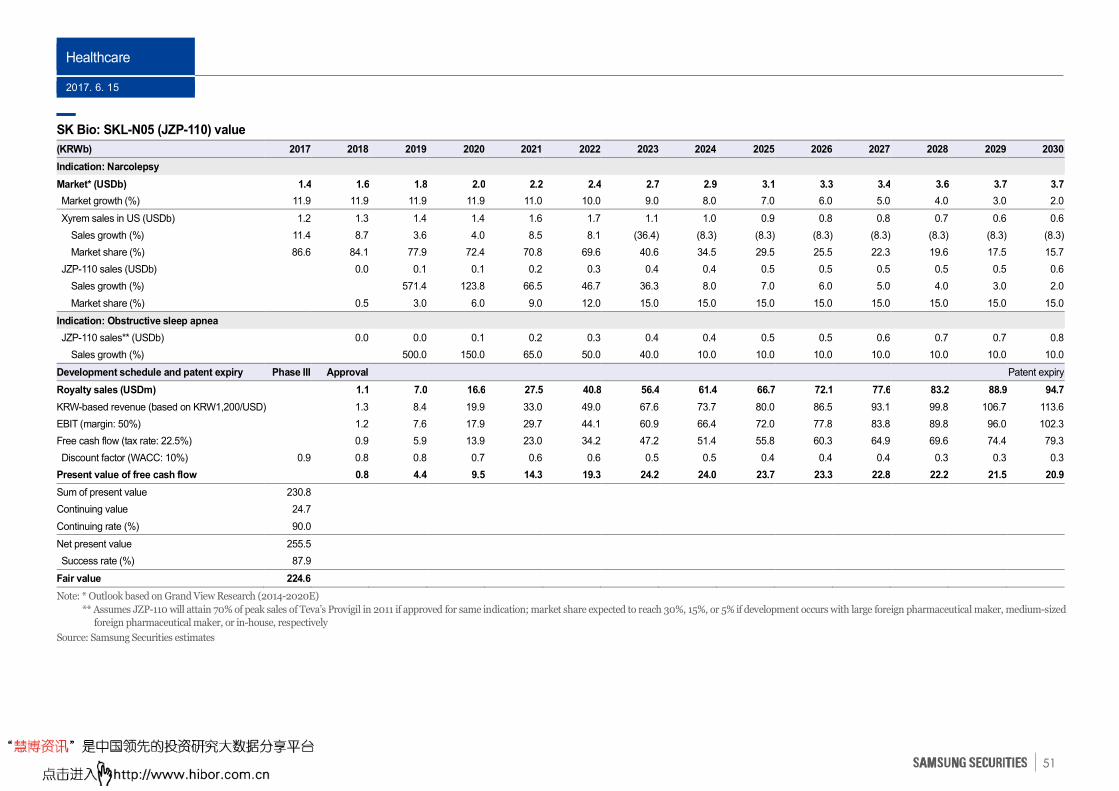

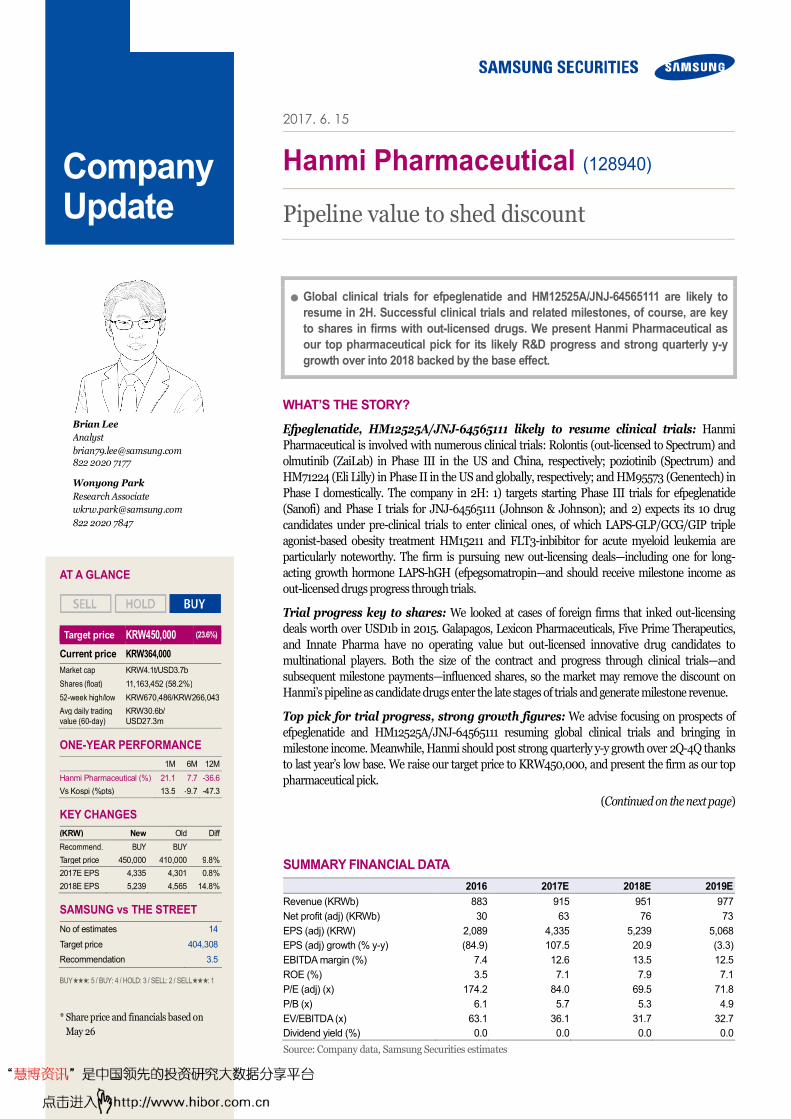

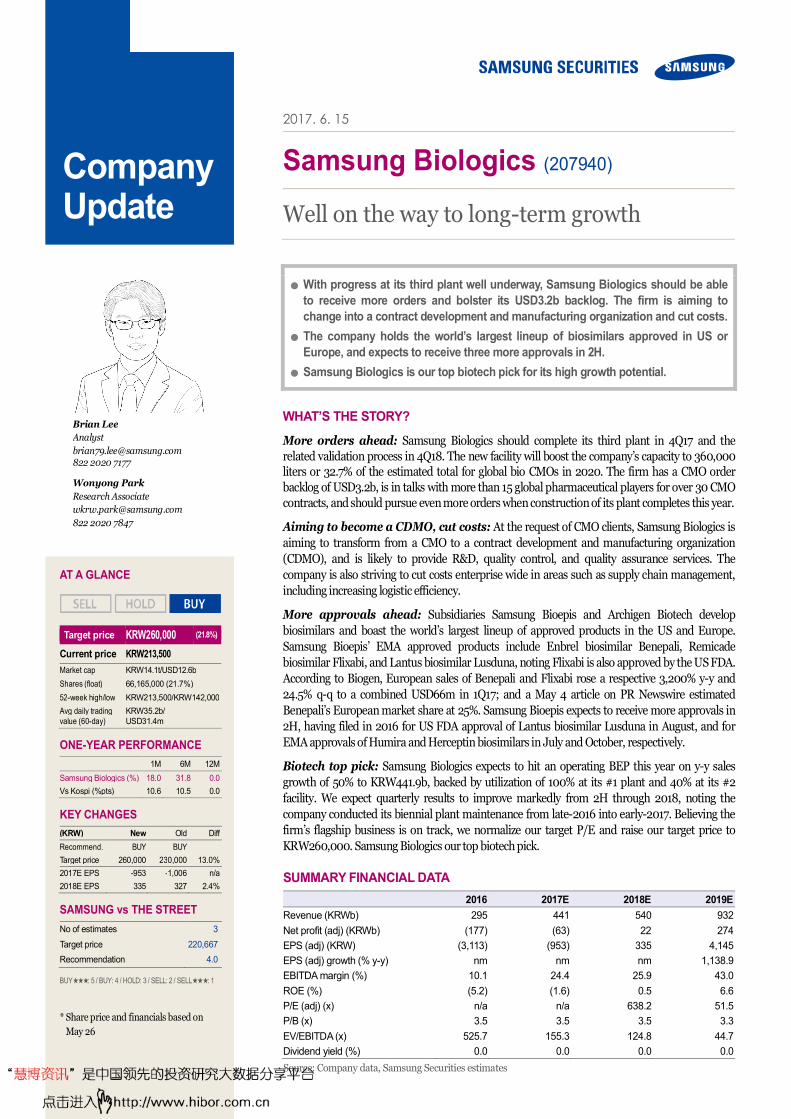

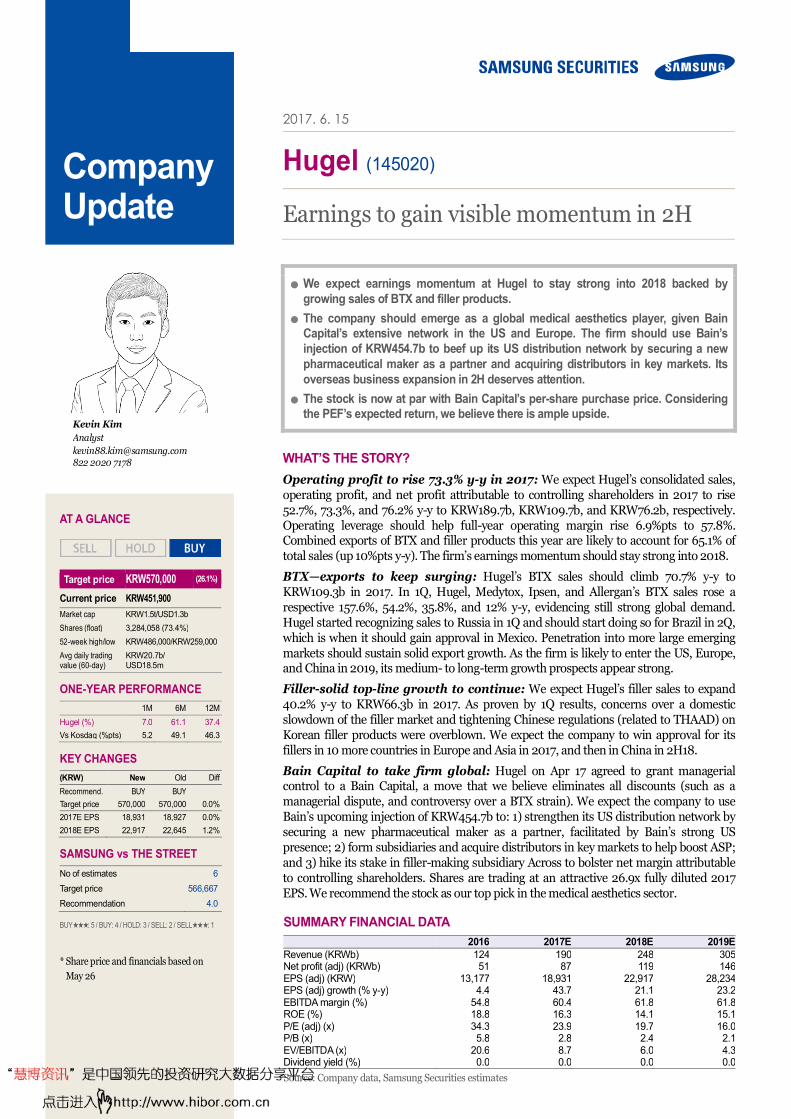

2017. 6. 15

Pharmaceuticals(OVERWEIGHT)

Earnings growth, R&D results in the spotlight in 2H

● Global, Korean pharma markets to grow 6.3% and 4.4% pa, respectively. Multiple

blockbusters to come off patent over 2016-2020, benefiting Korean biosimilar firms.

● Sea change from 2012 as Korean healthcare integrates with global ecosystem.

Next five years, virtuous circle: stronger brands/track records →→→→ financial gains. ● Eye government policy, regulatory direction; visibility to improve in 2H. Be

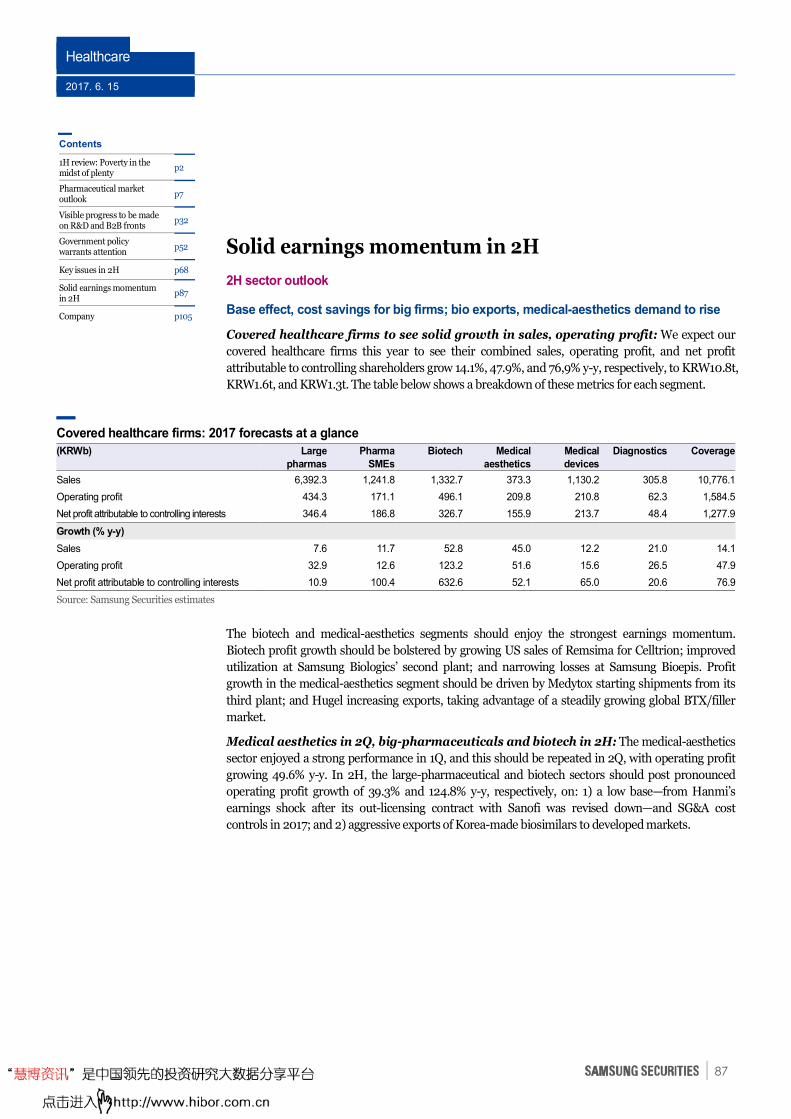

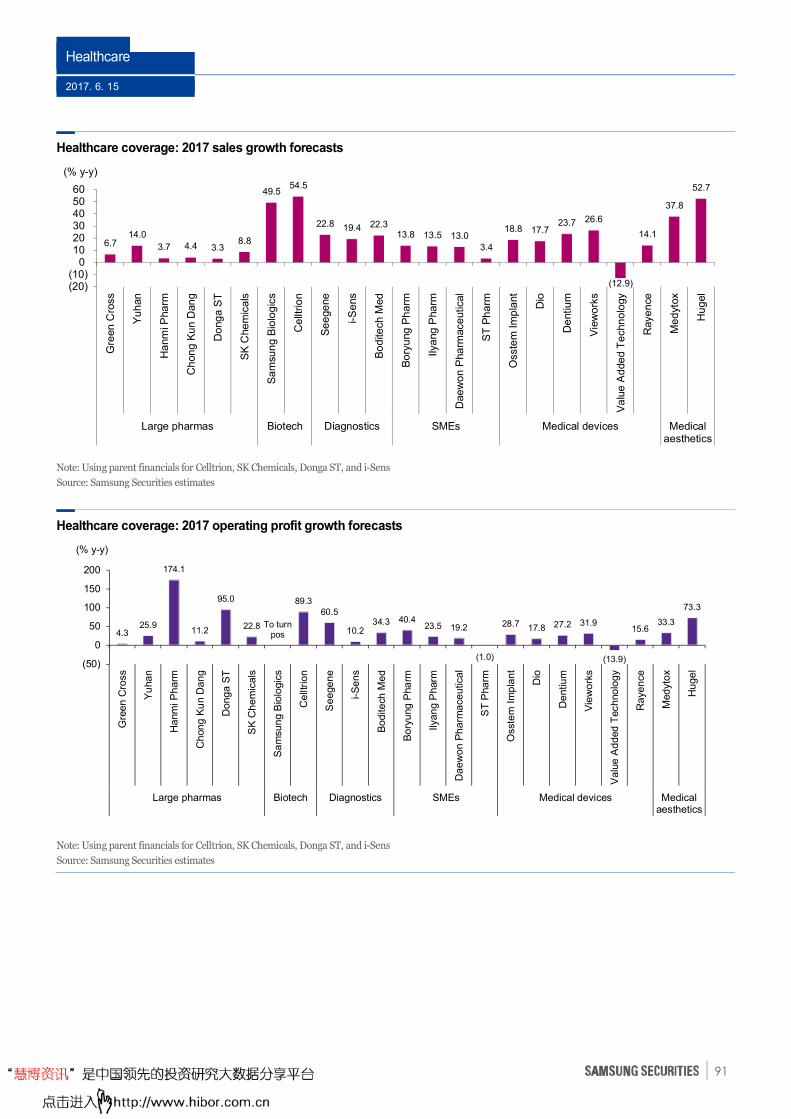

selective: buy firms with R&D successes, B2B track record, or improving earnings. ● Covered stocks: combined sales, operating profit to grow 14.1%, 47.9% y-y in 2017.

Medical aesthetics to stand out in 2Q; large pharmaceutical, biotech stocks in 2H. ● Top picks: Hanmi Pharm, Samsung Biologics, Hugel, Dentium, ST Pharm, Huons.

WHAT’S THE STORY?

Solid growth ahead for global, Korean pharmaceutical markets: The global pharmaceutical market is projected to grow at a 2016-2022 CAGR of 6.3% to reach USD1.12t, while its Korean counterpart should expand at 2017-2021 CAGR of 4.4% to KRW18.6t. Meanwhile, a second patent cliff is ahead: blockbuster drugs (including several biologics) worth USD249b will lose patent protection over 2016-2020. In short, things are looking good for the Korean companies that lead the global biosimilar market.

Sea change for Korean healthcare: Over 2012-2017, Korean healthcare firms made massive progress on R&D, B2B operations, and exports. Some signed large out-licensing deals with global pharmaceutical firms. Korea-made biosimilars dominate the global market, while Korea-made botulinum toxins and fillers are gaining global market share. We expect Korea to produce the world’s top biologics contract manufacturing organization and one of the world’s top-ten chemical-drug contract manufacturing services. Successes over the past five years owe much to the accumulation of technology, effective business strategies, investments by chaebol, and supportive government policies. Over the next five years, Korean healthcare firms should enter a virtuous cycle wherein stronger brand equities and track records lead to greater financial gains.

Monitor policy, regulatory direction: Korea’s healthcare industry should benefit if the government keeps election pledges to nurture the pharmaceutical, biotechnology, and medical device industries; halts the introduction of for-profit medical corporations; and raises subsidies for implants, hearing aids, and Alzheimer’s treatments. But prescription-drug makers will suffer if a total drug cost limit is enforced. Focus on firms specialized in OTC drugs, supplements, biotech, diagnostics, medical aesthetics, and medical devices.

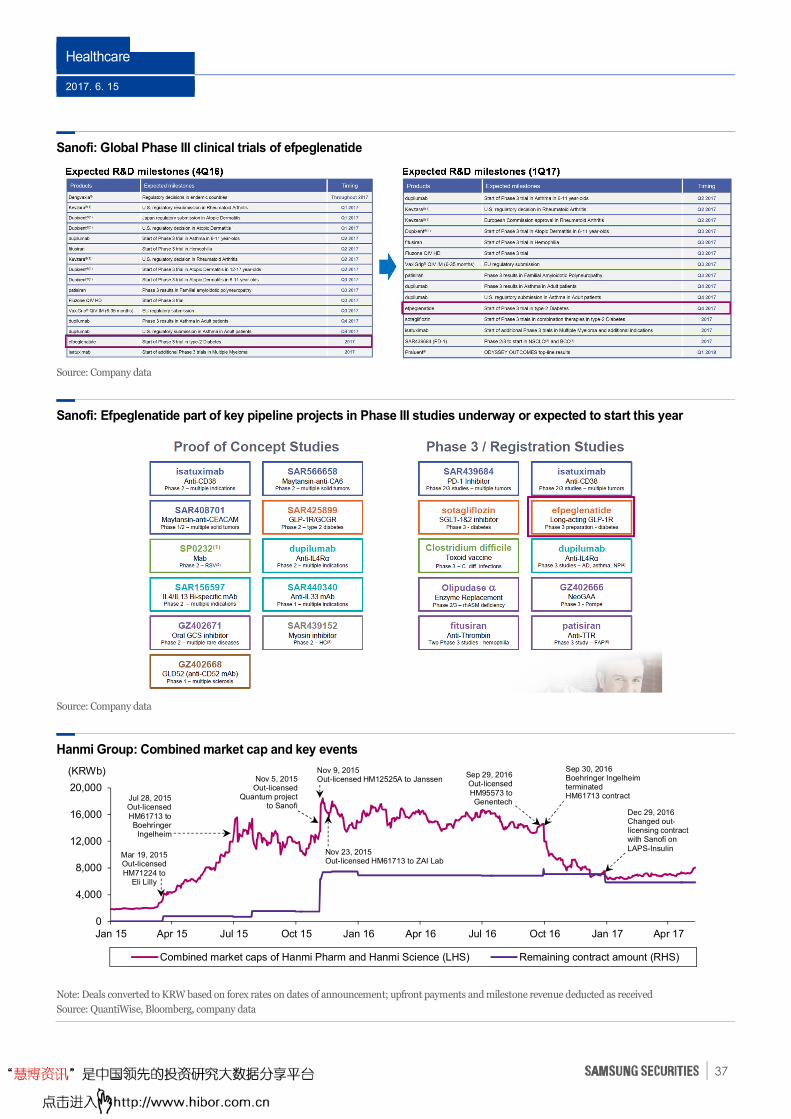

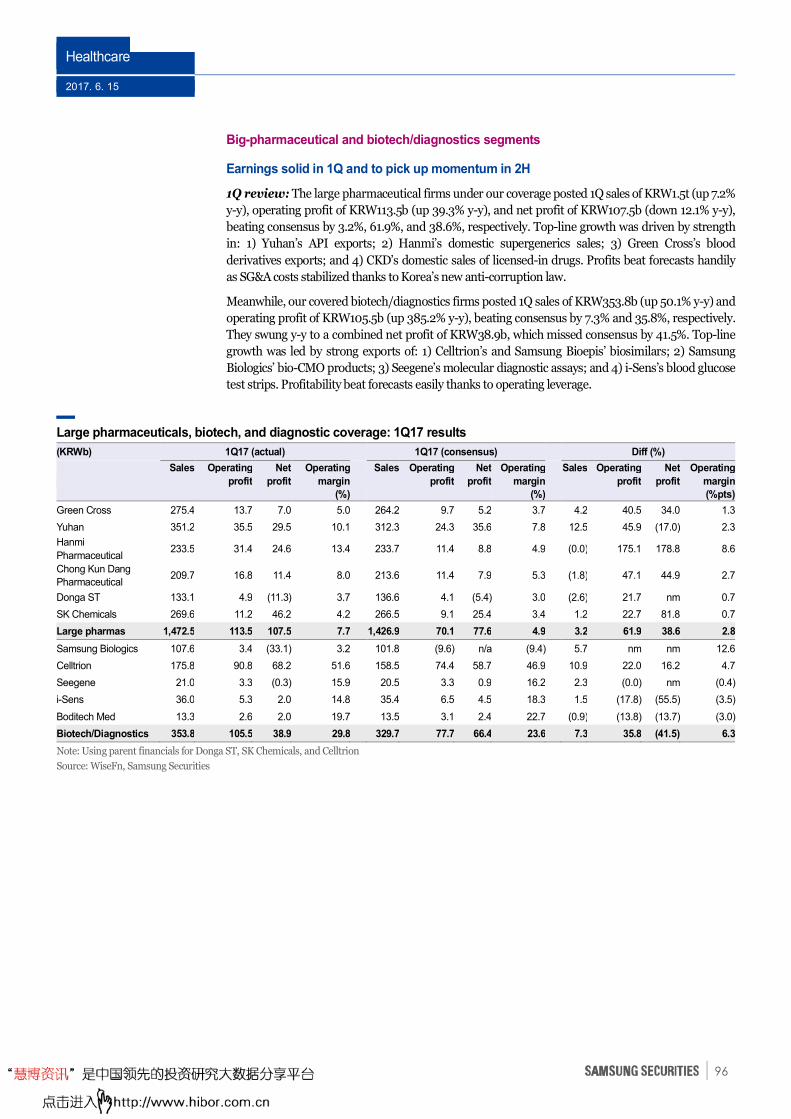

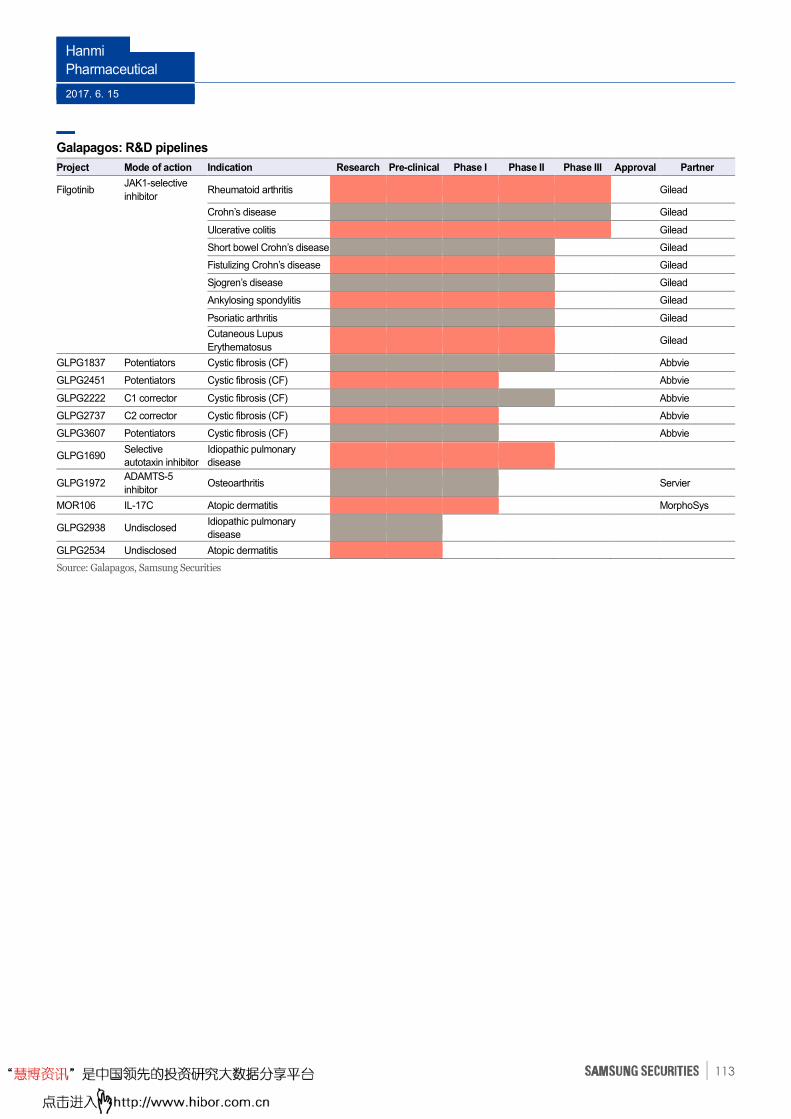

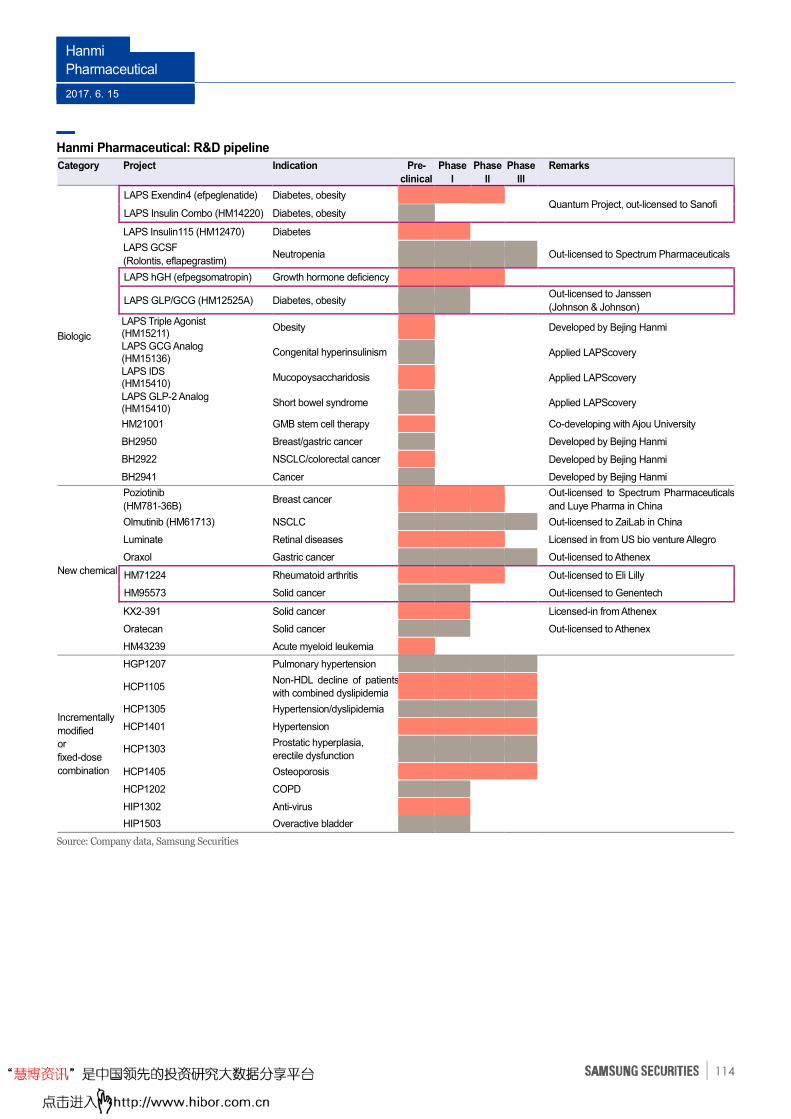

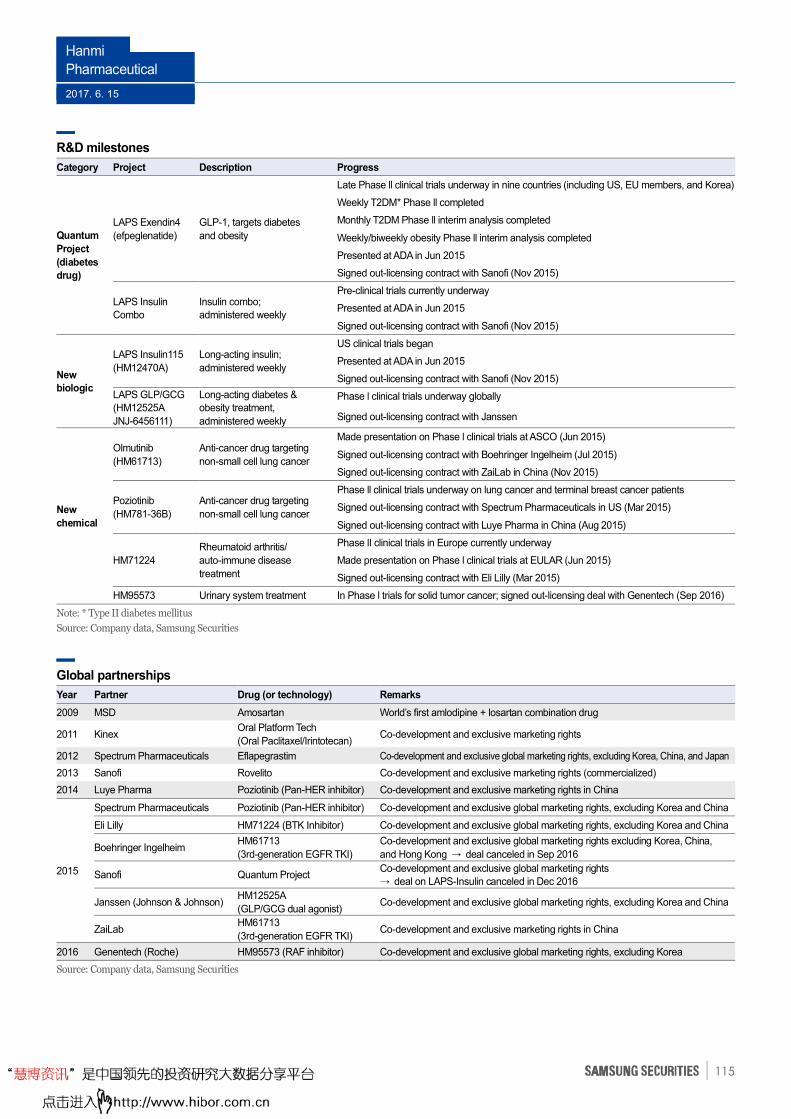

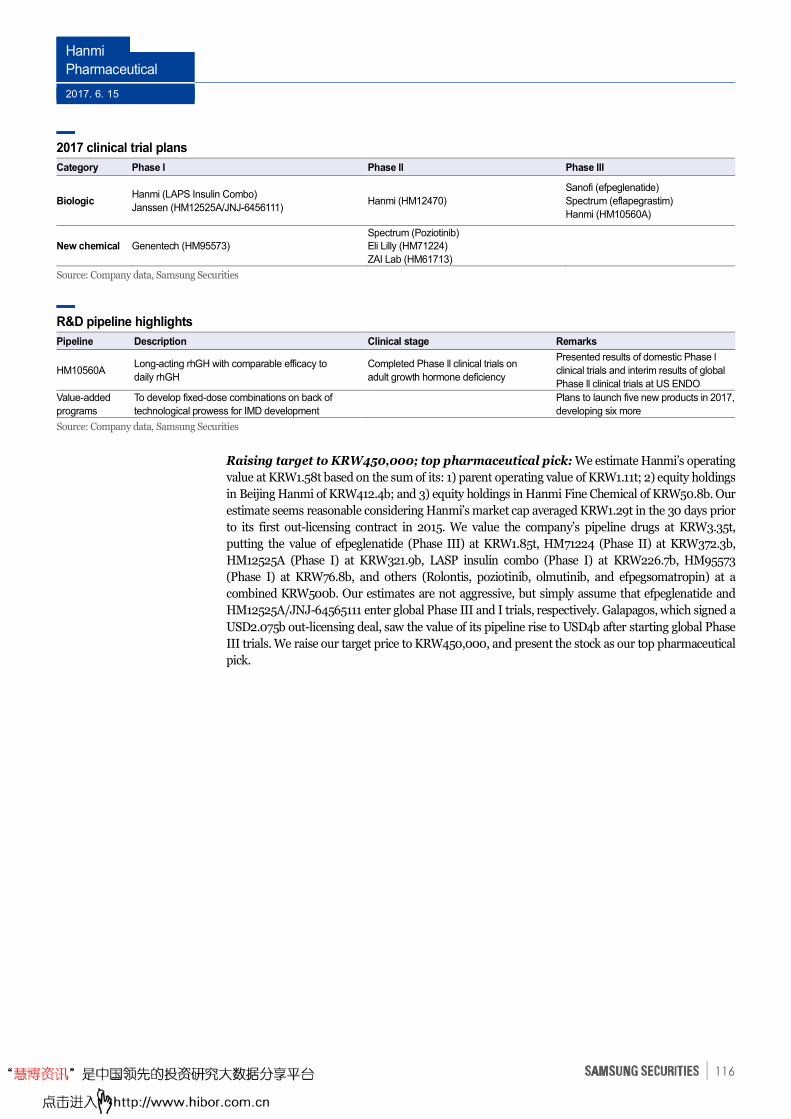

To make visible progress on R&D, B2B fronts: In 2H, Hanmi Pharmaceutical should begin global Phase III clinical trials for Efpeglenatide and resume global Phase I trials for HM12525A/JNJ-64565111; Green Cross should win US approval for IVIG; Samsung Biologics should win US and European approval for three biosimilars; Medytox-Allegan should begin global Phase III trials for Innotox; Kolon Life Science should win domestic approval for Invossa; Genexine and Qurient should make progress on their B2B operations; and Seegene should begin supplying ODM products to Beckman Coulter.

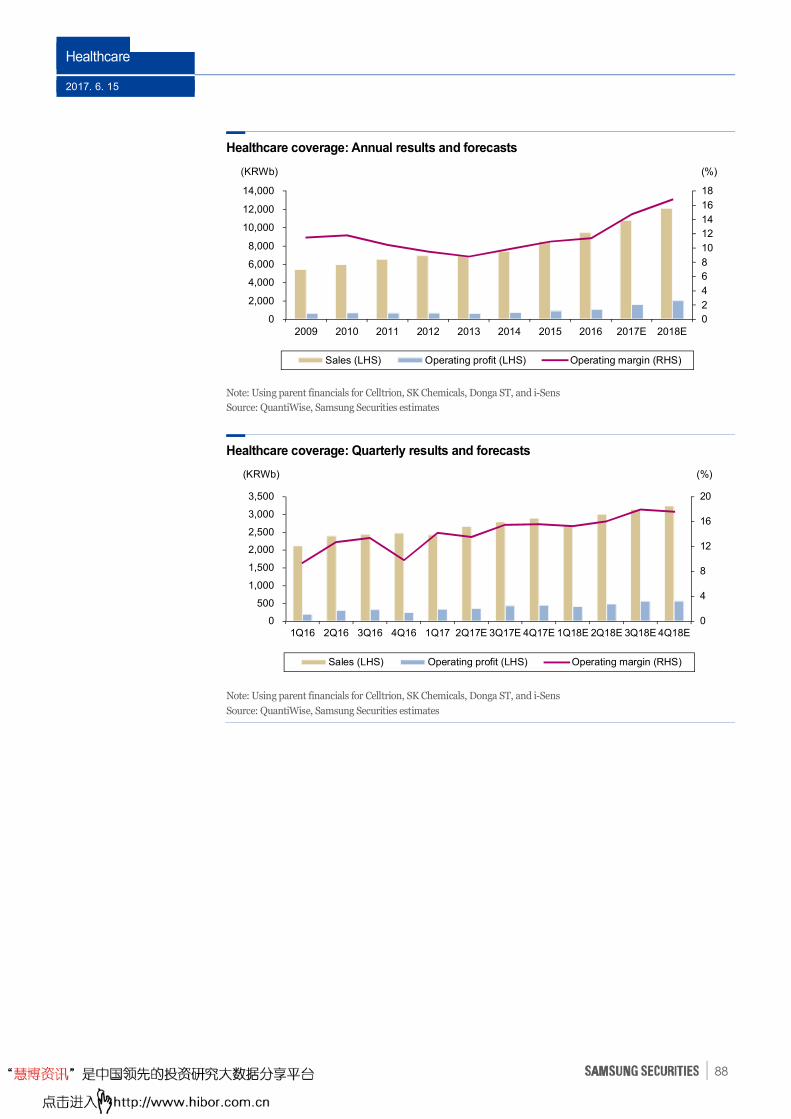

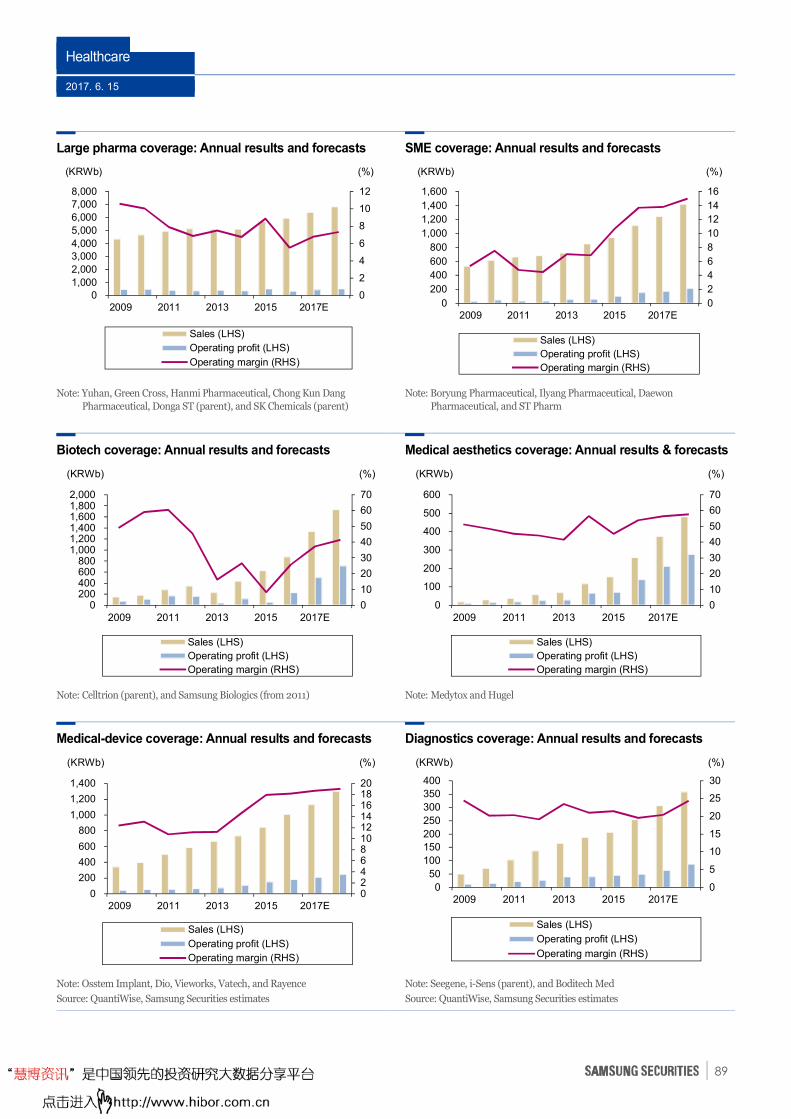

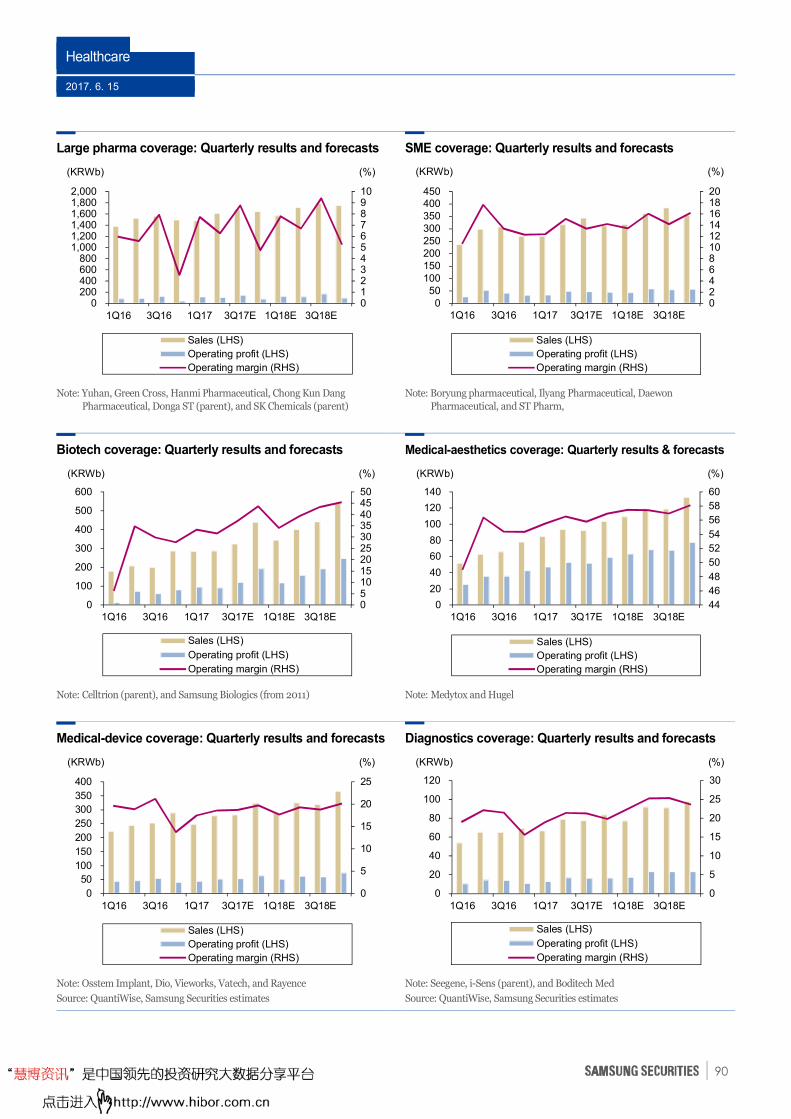

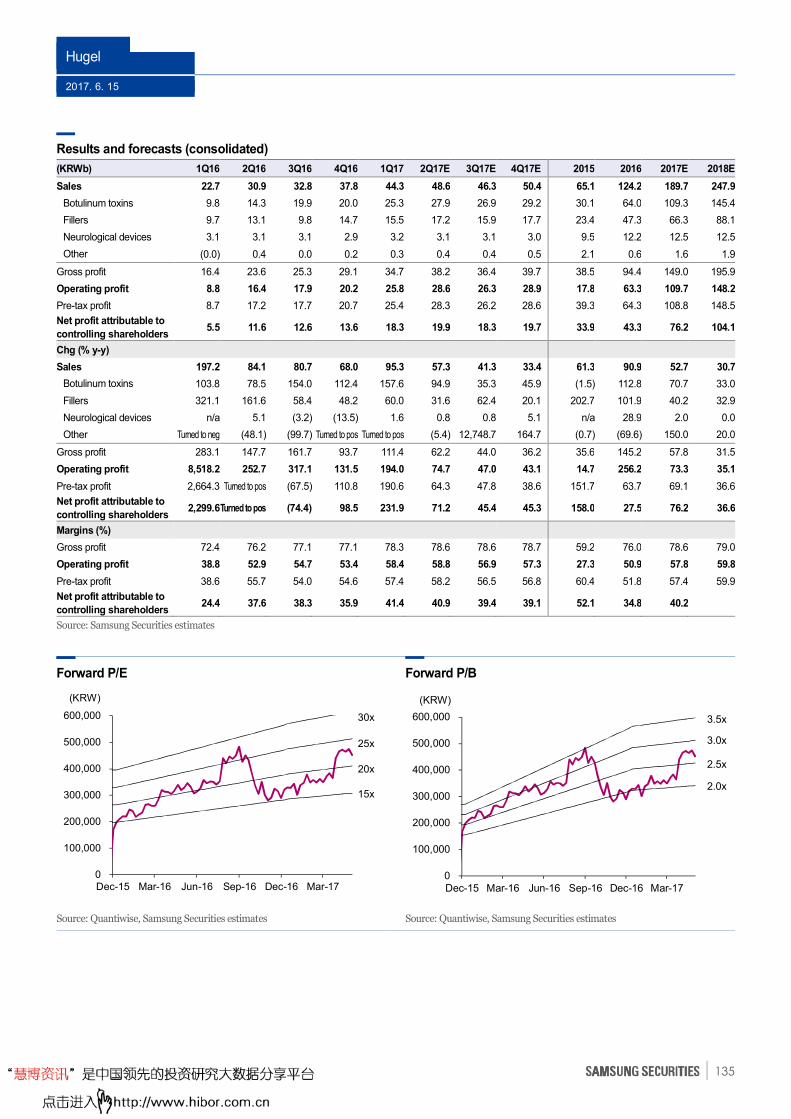

Operating profit growth: We have operating profits at our covered large pharmaceutical firms, medium-sized pharmaceutical firms, biotech, medical-diagnostics, medical-aesthetics, and medical-device firms growing 32.9%, 12.6%, 123.2%, 26.5%, 51.6%, and 15.6% y-y, respectively, in 2017. Medical aesthetics profits should stand out in 2Q on rising demand. In 2H, large pharmaceutical firms should shine on base effect and SG&A cost-cutting; biotech firms should shine on export growth. We foresee outstanding earnings growth over 2Q-4Q for Hanmi Pharm, Donga ST, Celltrion, Seegene, and Hugel.

Team Analysts

Brian Lee Team Head (Pharm/Biotech) [email protected] 822 2020 7177

SunYoung Yoon (Pharm/Biotech) [email protected] 822 2020 7840

Kevin Kim (Medical Devices/Medical Aesthetics) [email protected] 822 2020 7178

Research Associate

Wonyong Park [email protected] 822 2020 7847

Sector Update

AT A GLANCE

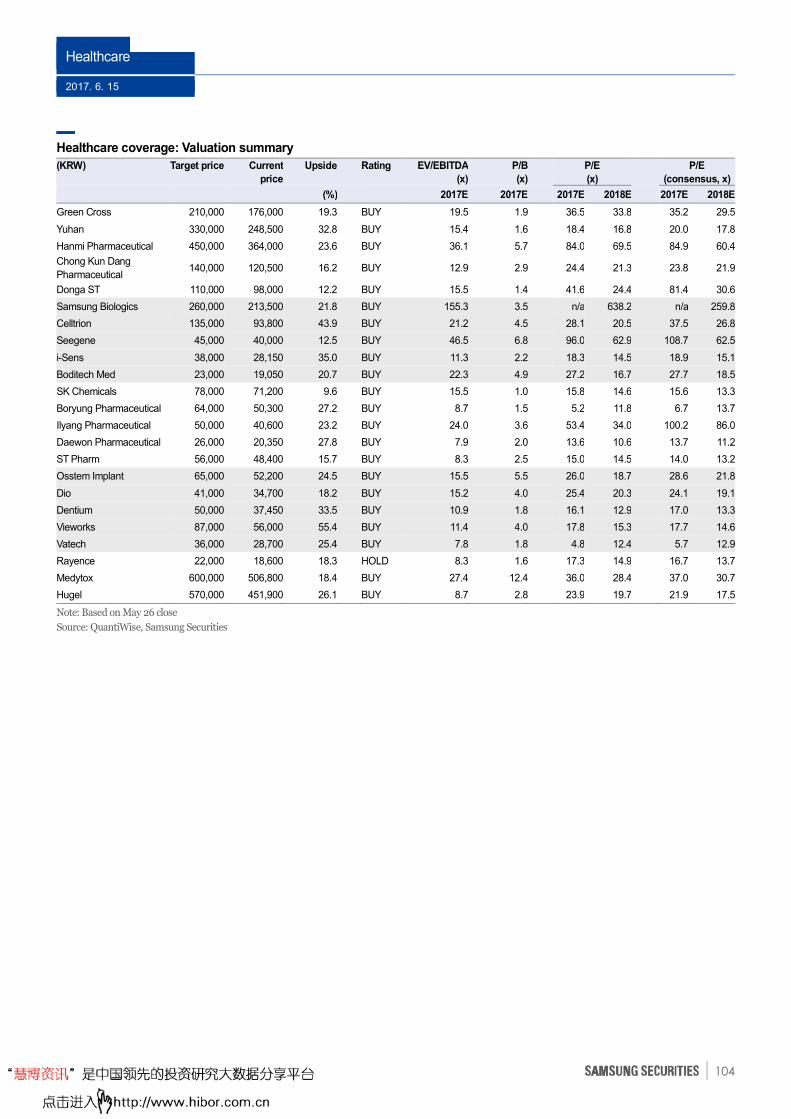

Hanmi Pharmaceutical (128940 KS, KRW364,000)

Target price: KRW450,000 (23.6%)

Samsung Biologics (207940 KS,

KRW213,500)

Target price: KRW260,000 (21.8%)

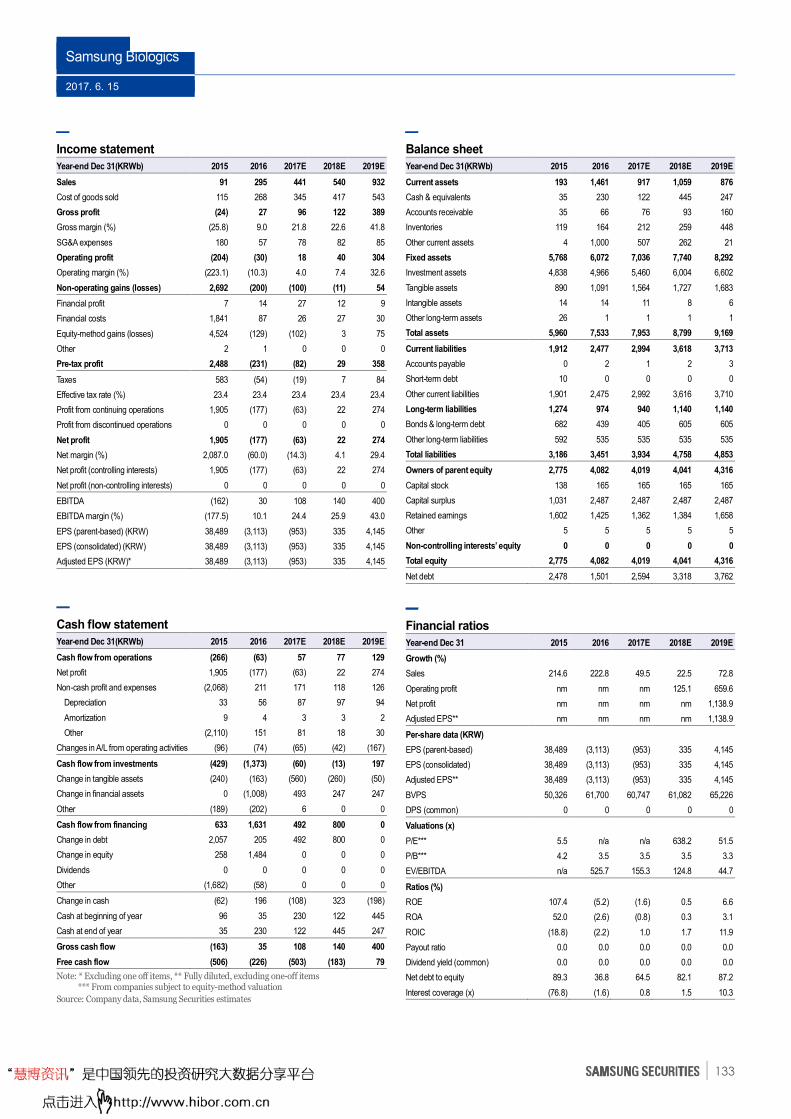

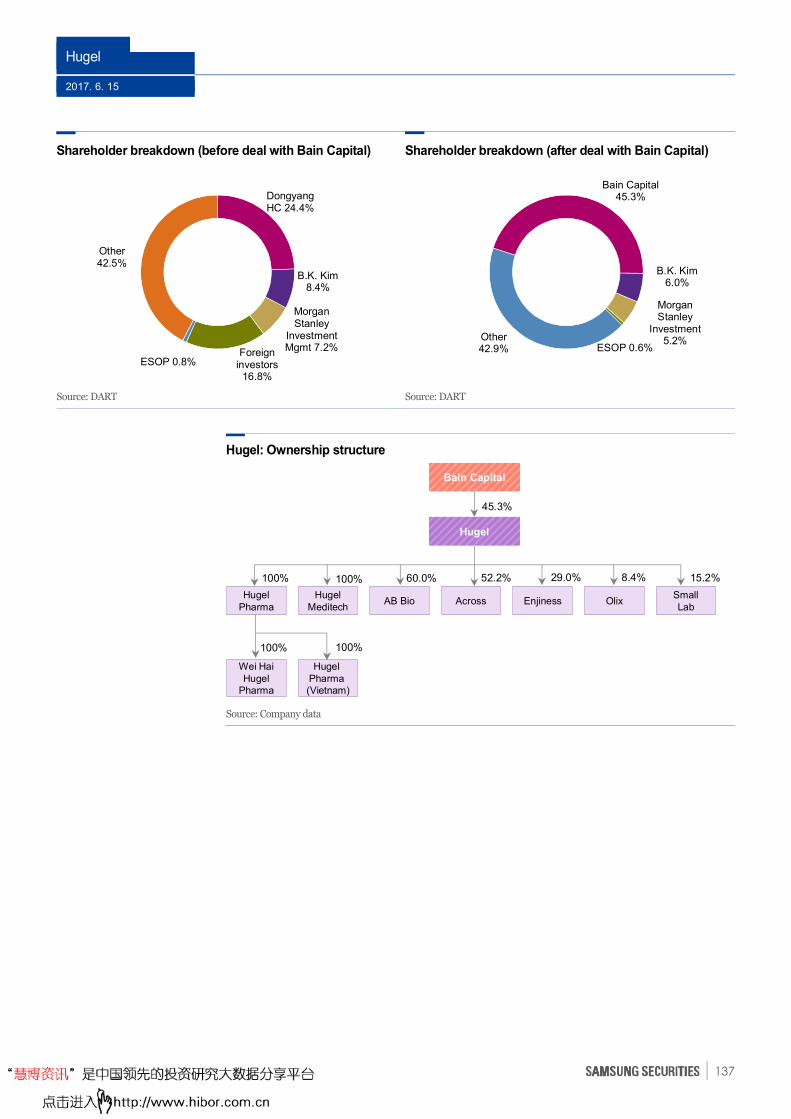

Hugel (145020 KS, KRW451,900)

Target price: KRW570,000 (26.1%)

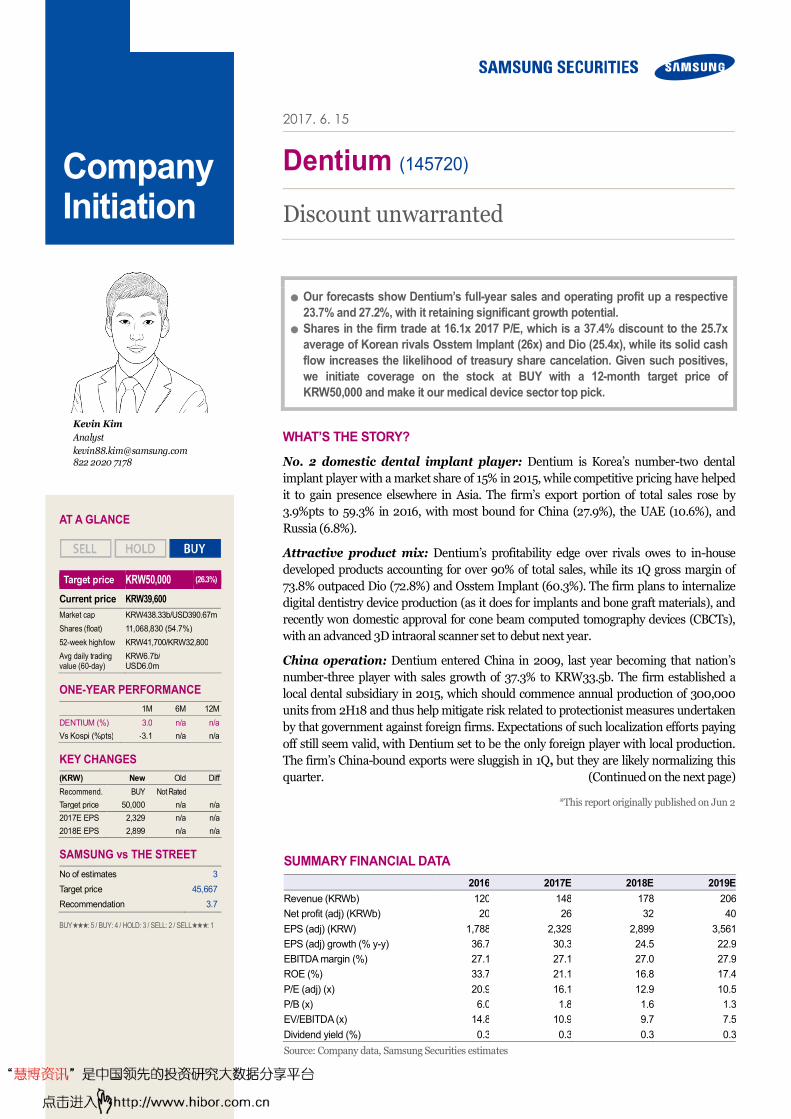

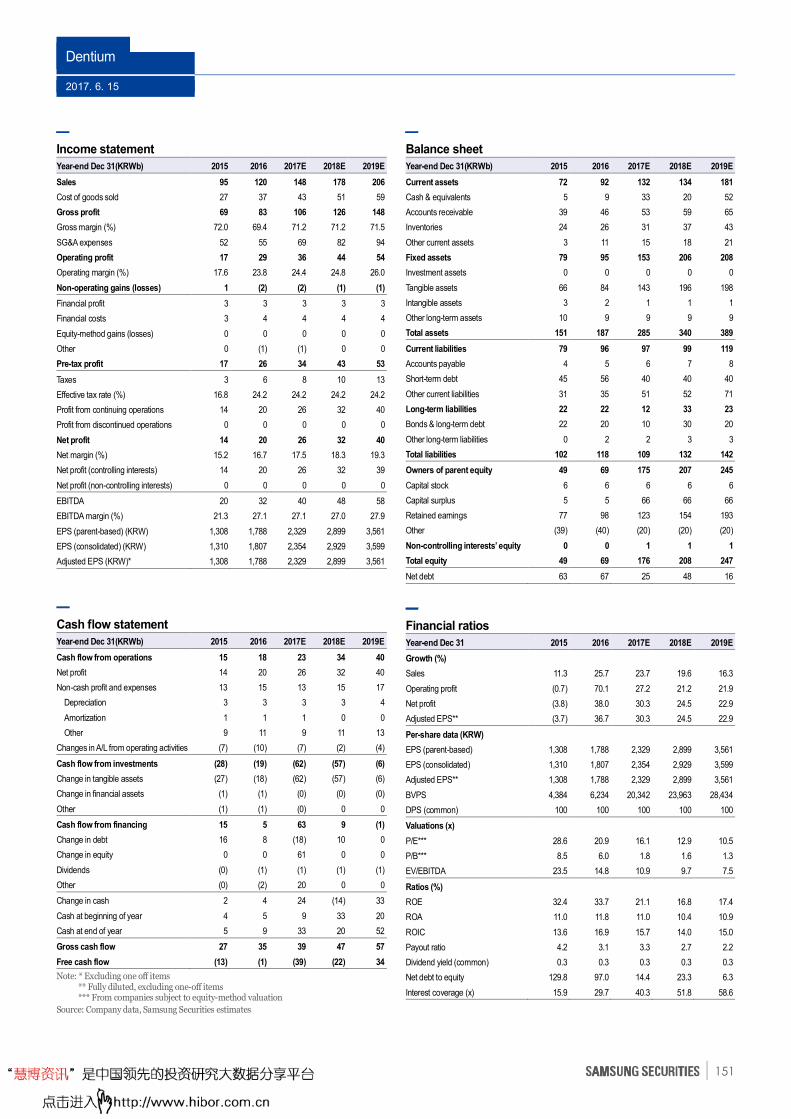

Dentium (145720 KS, KRW37,450)

Target price: KRW50,000 (33.5%)

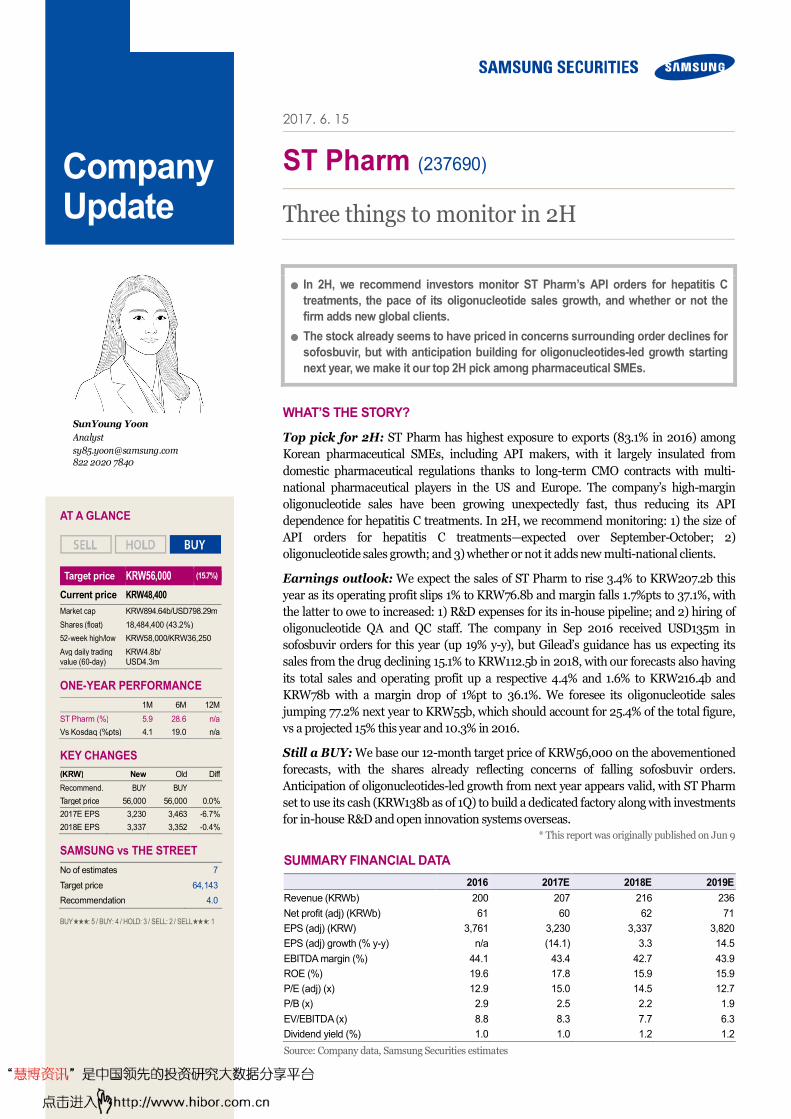

ST Pharm (237690 KS, KRW48,400)

Target price: KRW56,000 (15.7%)

Huons (243070 KS, KRW58,800)

Target price: n/a

* Share price and financials based on May 26

Healthcare

2017. 6. 15

2

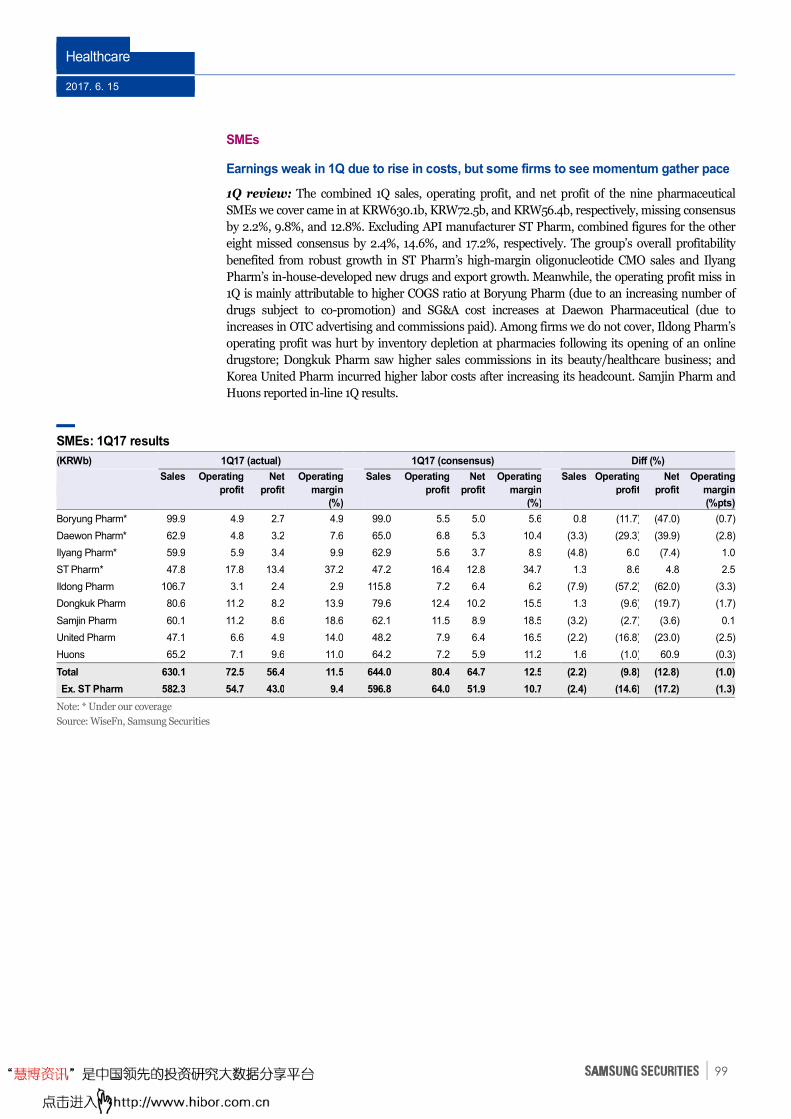

1H review: Poverty in the midst of plenty

Healthcare indices largely in line with market in 1H; stock performances diverge

Kospi Medical Supplies Index performing in line in 1H: The Kospi Medical Supplies Index

peaked at 11,297 on Jun 10, 2016, bottomed at 6,988 on Dec 2, 2016, and bounced back to stand at

8,888 on May 26, 2017. The index is up 17.1% ytd, in line with the Kospi’s ytd gains of 16.2%. The

index excluding Samsung Biologics was valued as high as 40.1x P/E (Jul 22, 2016) and as low as

18.5x (Nov 18, 2016). It was valued at 26.2x on May 26, 2017.

Kosdaq Pharmaceutical Index underperforming in 1H: The Kosdaq Pharmaceutical Index

peaked at 7,552 on Feb 5, 2016, bottomed at 5,662 on Mar 24, 2017, and crept back up to stand at

6,209 on May 26, 2017. The index is down 1.3% ytd, underperforming the Kosdaq, which has gained

2.3%. The index’s P/E valuation peaked at 39.4x (Jan 29, 2015) and hit bottom at 24.6x (Mar 24,

2017). It was valued at 26.3x on May 26, 2017.

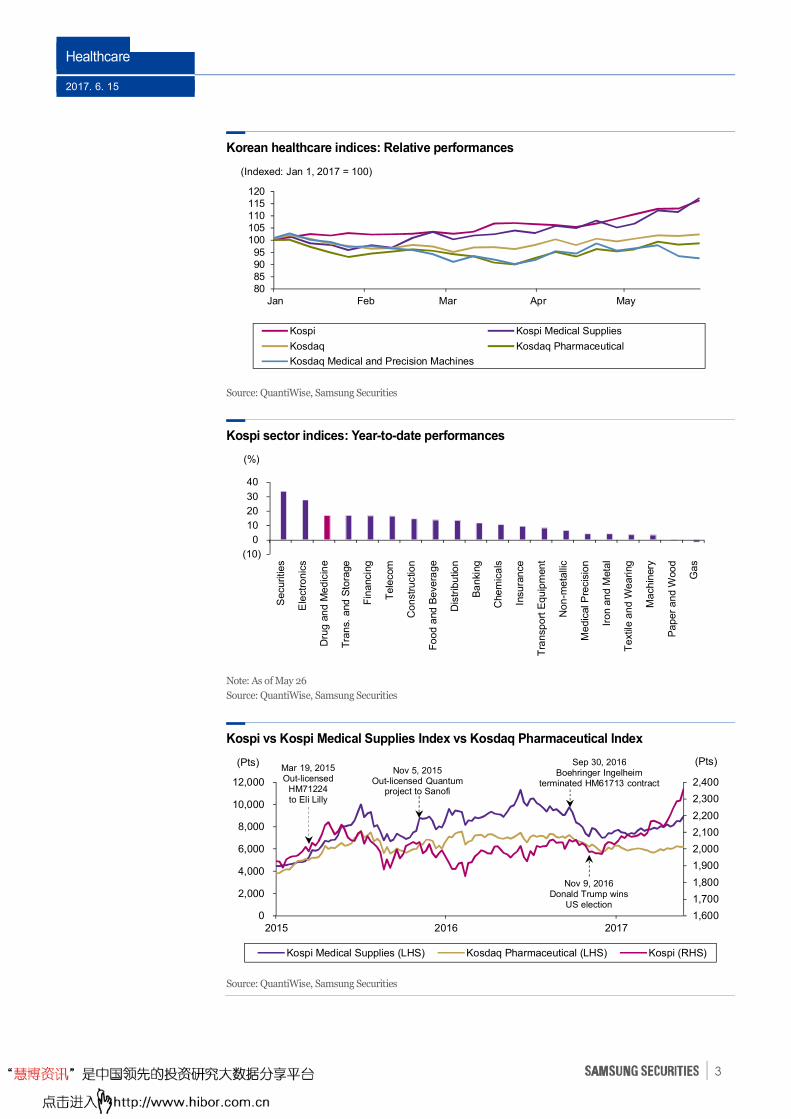

Sector sentiment weakening: Investors have been in thrall to the IT sector in 1H on prospects of

record earnings amid a semiconductor supply shortage and smartphone launches. Cyclical sectors

have also appealed to those who anticipate US infrastructure investments and inflation under

President Trump. In contrast, the belief that the US has begun a period of rate hikes has reduced the

investment appeal of high-multiple sectors. Sentiment towards the healthcare sector weakened after

Hanmi Pharmaceutical in 2016 announced that some out-licensing contracts it signed in 2015 have

been revised or canceled. The sector has remained lackluster in 1H due to a lack of standout R&D

successes and earnings momentum. Still, steep share-price corrections in late 2016 made valuations

less demanding, leading shares to bottom out in 1Q.

Oversold stocks and those with earnings momentum bounce back in 1H: The Kospi

Medical Supplies Index performed in line with the Kospi, but stocks with earnings momentum

posted the steepest share-price gains. Among our covered healthcare stocks, Samsung Biologics is up

41.4% ytd, Medytox 42.1%, Hugel 40.7%, Hanmi Pharmaceutical 27.4%, and Yuhan 24.6%. Also,

stocks that had plunged more than 50% from their previous peaks have rebounded almost 20% from

their lows as bargain hunters snapped them up. Healthcare stocks that have rebounded strongly

include Huons Global (45.4%), Hanmi Pharmaceutical (36.8%), Hanmi Science (32.3%), and Jeil

Pharmaceutical (30.3%).

Contents

1H review: Poverty in the midst of plenty

p2

Pharmaceutical market outlook

p7

Visible progress to be made on R&D and B2B fronts

p32

Government policy warrants attention

p52

Key issues in 2H p68

Solid earnings momentum in 2H

p87

Company p105

Healthcare

2017. 6. 15

3

Korean healthcare indices: Relative performances

Source: QuantiWise, Samsung Securities

Kospi sector indices: Year-to-date performances

Note: As of May 26

Source: QuantiWise, Samsung Securities

Kospi vs Kospi Medical Supplies Index vs Kosdaq Pharmaceutical Index

Source: QuantiWise, Samsung Securities

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

0

2,000

4,000

6,000

8,000

10,000

12,000

2015 2016 2017

Kospi Medical Supplies (LHS) Kosdaq Pharmaceutical (LHS) Kospi (RHS)

(Pts) (Pts)Nov 5, 2015

Out-licensed Quantumproject to Sanofi

Sep 30, 2016Boehringer Ingelheim

terminated HM61713 contract

Nov 9, 2016Donald Trump wins

US election

Mar 19, 2015Out-licensed

HM71224to Eli Lilly

80859095

100105110115120

Jan Feb Mar Apr May

Kospi Kospi Medical Supplies

Kosdaq Kosdaq Pharmaceutical

Kosdaq Medical and Precision Machines

(Indexed: Jan 1, 2017 = 100)

(10)

0

10

20

30

40

Se

cu

ritie

s

Ele

ctr

on

ics

Dru

g a

nd

Me

dic

ine

Tra

ns.

and

Sto

rage

Fin

ancin

g

Te

lecom

Co

nstr

uctio

n

Fo

od

and

Be

ve

rag

e

Dis

trib

utio

n

Ba

nki

ng

Che

mic

als

Insu

ran

ce

Tra

nsp

ort

Eq

uip

men

t

No

n-m

eta

llic

Me

dic

al P

recis

ion

Iro

n a

nd

Meta

l

Te

xtil

e a

nd

We

ari

ng

Ma

ch

inery

Pa

pe

r a

nd

Woo

d

Ga

s

(%)

Healthcare

2017. 6. 15

4

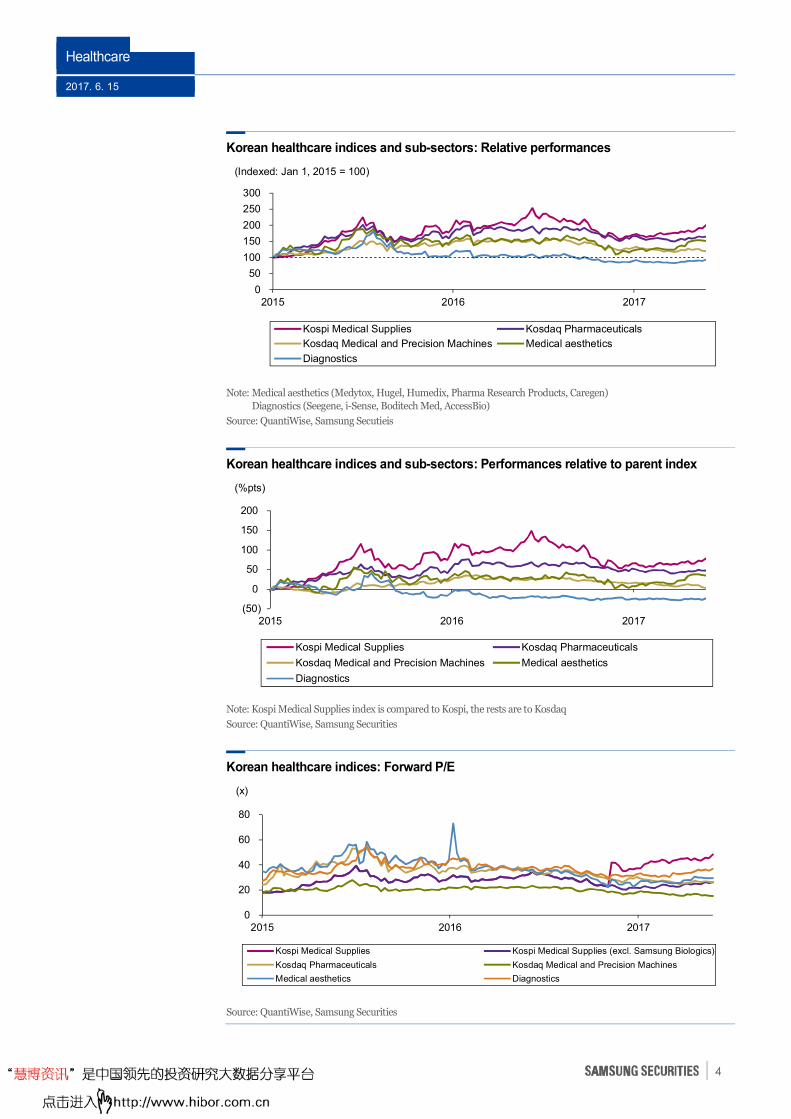

Korean healthcare indices and sub-sectors: Relative performances

Note: Medical aesthetics (Medytox, Hugel, Humedix, Pharma Research Products, Caregen)

Diagnostics (Seegene, i-Sense, Boditech Med, AccessBio)

Source: QuantiWise, Samsung Secutieis

Korean healthcare indices and sub-sectors: Performances relative to parent index

Note: Kospi Medical Supplies index is compared to Kospi, the rests are to Kosdaq

Source: QuantiWise, Samsung Securities

Korean healthcare indices: Forward P/E

Source: QuantiWise, Samsung Securities

0

20

40

60

80

2015 2016 2017

Kospi Medical Supplies Kospi Medical Supplies (excl. Samsung Biologics)

Kosdaq Pharmaceuticals Kosdaq Medical and Precision Machines

Medical aesthetics Diagnostics

(x)

0

50

100

150

200

250

300

2015 2016 2017

Kospi Medical Supplies Kosdaq Pharmaceuticals

Kosdaq Medical and Precision Machines Medical aesthetics

Diagnostics

(Indexed: Jan 1, 2015 = 100)

(50)

0

50

100

150

200

2015 2016 2017

Kospi Medical Supplies Kosdaq Pharmaceuticals

Kosdaq Medical and Precision Machines Medical aesthetics

Diagnostics

(%pts)

Healthcare

2017. 6. 15

5

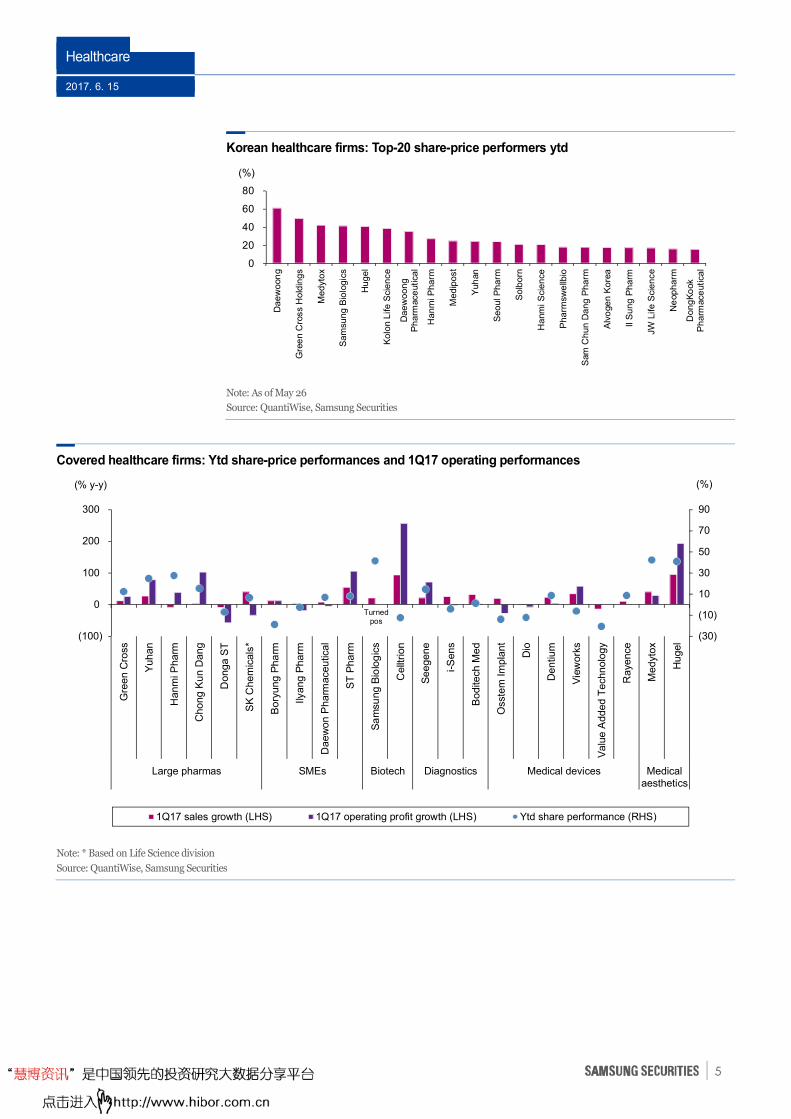

Korean healthcare firms: Top-20 share-price performers ytd

Note: As of May 26

Source: QuantiWise, Samsung Securities

Covered healthcare firms: Ytd share-price performances and 1Q17 operating performances

Note: * Based on Life Science division

Source: QuantiWise, Samsung Securities

0

20

40

60

80

Da

ew

oon

g

Gre

en C

ross

Ho

ldin

gs

Me

dyt

ox

Sa

msu

ng

Bio

log

ics

Hu

ge

l

Ko

lon L

ife

Sci

en

ce

Da

ew

oo

ng

Ph

arm

ace

utica

l

Ha

nm

i Ph

arm

Me

dip

ost

Yuh

an

Se

ou

l Ph

arm

So

lbo

rn

Ha

nm

i S

cie

nce

Ph

arm

swe

llbio

Sam

Ch

un

Da

ng

Ph

arm

Alv

oge

n K

ore

a

Il S

un

g P

ha

rm

JW L

ife

Sci

en

ce

Ne

op

ha

rm

Do

ng

Ko

ok

Ph

arm

ace

utica

l

(%)

(30)

(10)

10

30

50

70

90

(100)

0

100

200

300

Gre

en C

ross

Yuhan

Hanm

i Pharm

Chong K

un D

ang

Donga S

T

SK

Chem

icals

*

Bory

ung P

ha

rm

Ilyang P

harm

Daew

on P

harm

ace

utic

al

ST

Pharm

Sa

msu

ng B

iolo

gic

s

Cellt

rion

Seegene

i-S

ens

Bodite

ch M

ed

Oss

tem

Im

pla

nt

Dio

Dentiu

m

Vie

work

s

Valu

e A

dded T

ech

nolo

gy

Raye

nce

Medyt

ox

Hugel

Large pharmas SMEs Biotech Diagnostics Medical devices Medicalaesthetics

1Q17 sales growth (LHS) 1Q17 operating profit growth (LHS) Ytd share performance (RHS)

(% y-y) (%)

Turnedpos

Healthcare

2017. 6. 15

6

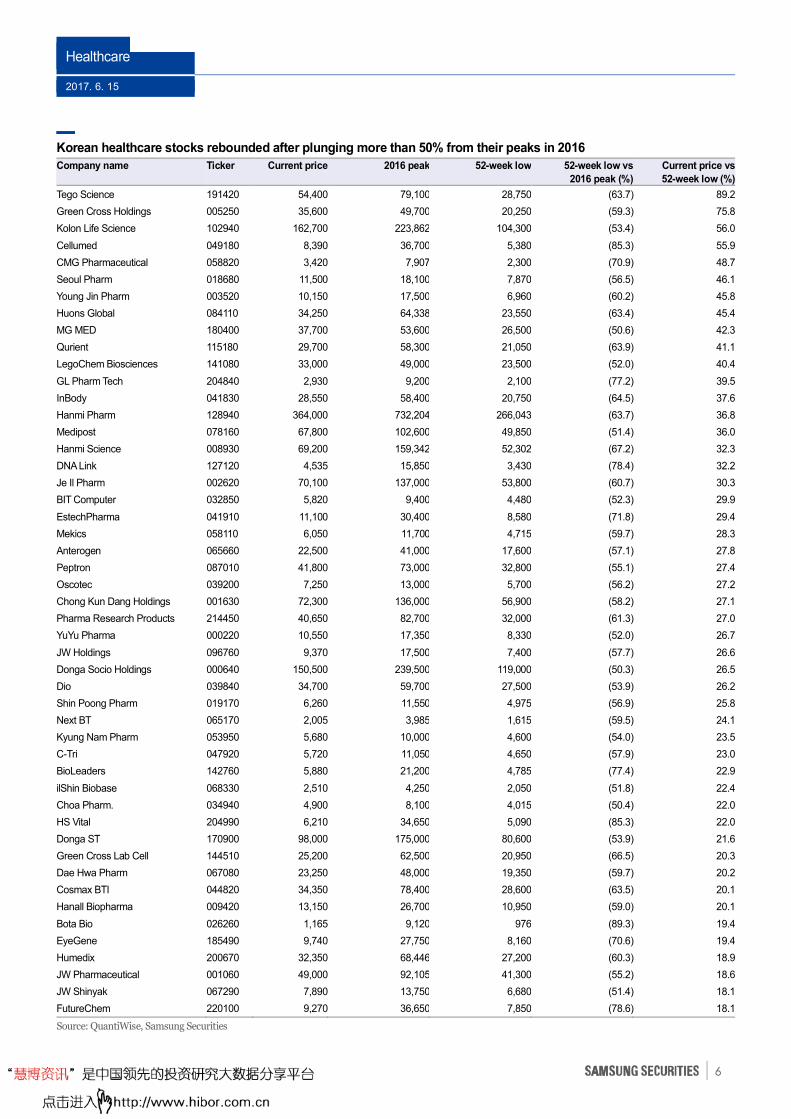

Korean healthcare stocks rebounded after plunging more than 50% from their peaks in 2016

Company name

Ticker

Current price 2016 peak 52-week low 52-week low vs

2016 peak (%)

Current price vs

52-week low (%)

Tego Science 191420 54,400 79,100 28,750 (63.7) 89.2

Green Cross Holdings 005250 35,600 49,700 20,250 (59.3) 75.8

Kolon Life Science 102940 162,700 223,862 104,300 (53.4) 56.0

Cellumed 049180 8,390 36,700 5,380 (85.3) 55.9

CMG Pharmaceutical 058820 3,420 7,907 2,300 (70.9) 48.7

Seoul Pharm 018680 11,500 18,100 7,870 (56.5) 46.1

Young Jin Pharm 003520 10,150 17,500 6,960 (60.2) 45.8

Huons Global 084110 34,250 64,338 23,550 (63.4) 45.4

MG MED 180400 37,700 53,600 26,500 (50.6) 42.3

Qurient 115180 29,700 58,300 21,050 (63.9) 41.1

LegoChem Biosciences 141080 33,000 49,000 23,500 (52.0) 40.4

GL Pharm Tech 204840 2,930 9,200 2,100 (77.2) 39.5

InBody 041830 28,550 58,400 20,750 (64.5) 37.6

Hanmi Pharm 128940 364,000 732,204 266,043 (63.7) 36.8

Medipost 078160 67,800 102,600 49,850 (51.4) 36.0

Hanmi Science 008930 69,200 159,342 52,302 (67.2) 32.3

DNA Link 127120 4,535 15,850 3,430 (78.4) 32.2

Je Il Pharm 002620 70,100 137,000 53,800 (60.7) 30.3

BIT Computer 032850 5,820 9,400 4,480 (52.3) 29.9

EstechPharma 041910 11,100 30,400 8,580 (71.8) 29.4

Mekics 058110 6,050 11,700 4,715 (59.7) 28.3

Anterogen 065660 22,500 41,000 17,600 (57.1) 27.8

Peptron 087010 41,800 73,000 32,800 (55.1) 27.4

Oscotec 039200 7,250 13,000 5,700 (56.2) 27.2

Chong Kun Dang Holdings 001630 72,300 136,000 56,900 (58.2) 27.1

Pharma Research Products 214450 40,650 82,700 32,000 (61.3) 27.0

YuYu Pharma 000220 10,550 17,350 8,330 (52.0) 26.7

JW Holdings 096760 9,370 17,500 7,400 (57.7) 26.6

Donga Socio Holdings 000640 150,500 239,500 119,000 (50.3) 26.5

Dio 039840 34,700 59,700 27,500 (53.9) 26.2

Shin Poong Pharm 019170 6,260 11,550 4,975 (56.9) 25.8

Next BT 065170 2,005 3,985 1,615 (59.5) 24.1

Kyung Nam Pharm 053950 5,680 10,000 4,600 (54.0) 23.5

C-Tri 047920 5,720 11,050 4,650 (57.9) 23.0

BioLeaders 142760 5,880 21,200 4,785 (77.4) 22.9

ilShin Biobase 068330 2,510 4,250 2,050 (51.8) 22.4

Choa Pharm. 034940 4,900 8,100 4,015 (50.4) 22.0

HS Vital 204990 6,210 34,650 5,090 (85.3) 22.0

Donga ST 170900 98,000 175,000 80,600 (53.9) 21.6

Green Cross Lab Cell 144510 25,200 62,500 20,950 (66.5) 20.3

Dae Hwa Pharm 067080 23,250 48,000 19,350 (59.7) 20.2

Cosmax BTI 044820 34,350 78,400 28,600 (63.5) 20.1

Hanall Biopharma 009420 13,150 26,700 10,950 (59.0) 20.1

Bota Bio 026260 1,165 9,120 976 (89.3) 19.4

EyeGene 185490 9,740 27,750 8,160 (70.6) 19.4

Humedix 200670 32,350 68,446 27,200 (60.3) 18.9

JW Pharmaceutical 001060 49,000 92,105 41,300 (55.2) 18.6

JW Shinyak 067290 7,890 13,750 6,680 (51.4) 18.1

FutureChem 220100 9,270 36,650 7,850 (78.6) 18.1

Source: QuantiWise, Samsung Securities

Healthcare

2017. 6. 15

7

Pharmaceutical market outlook

Breakthrough-therapy approvals brighten outlook for global market

Worldwide pharmaceutical sales outlook: EvaluatePharma has the global pharmaceutical

industry growing at a 2016-2022 CAGR of 6.3% to reach USD1.12t, with a new wave of innovative

therapies approved by regulators over the last three years serving as the core engine. The market

research firm expects the orphan drug market to almost double over the same period, expanding at

an 11.5% CAGR to peak at USD217b in 2022, while generic sales should grow at a 6.2% CAGR to

USD115b. R&D programs should increasingly be oriented towards narrower patient populations

characterized by larger unmet need, limited market competition, and favorable environment to gain

approvals. Yet, tightening of insurance-benefit rules and drug-pricing policies by the US

administration and large pharmacy benefit managers (PBMs) warrant attention.

Worldwide biologics sales outlook: The world’s chemical and biologic drug markets should

continue to grow at CAGRs of 5.1% and 9.1%, respectively, through 2022 to reach USD827b and

KRW337b. Biotech product penetration increased from 16.9% in 2008 to 24.6% in 2016, and it

should hit 29% in 2022, when 50% of the value of the top-100 products comes from biologics (vs 30%

in 2008 and 47% in 2016).

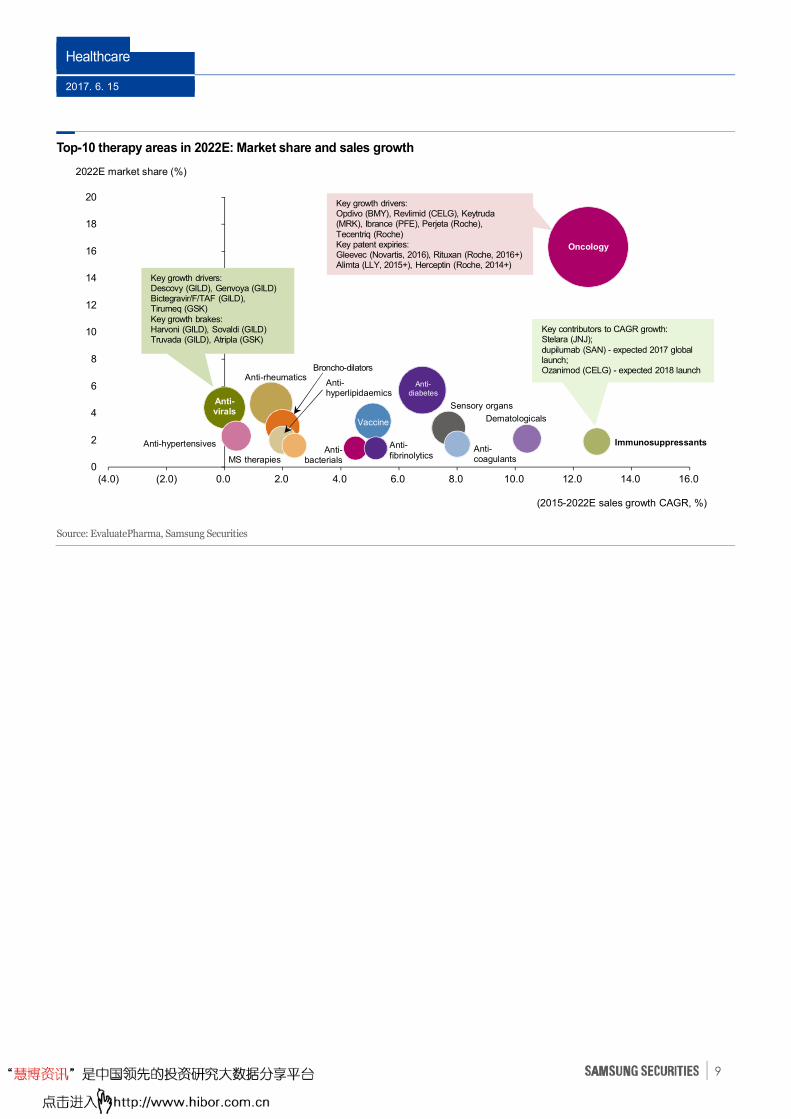

Oncology should remain the fastest-growing therapy area, expanding at a 2016-2022 CAGR of 12.5%

to reach USD190b in annual sales and represent 16.3% of the global pharmaceuticals market (vs 10.7%

in 2015). Top player Roche should see its oncology sales grow 3.3% pa to USD32.2b over the same

period, though its market share is likely to slide to 17% (vs 30.9% in 2015) due to the release of

biosimilars (of Avastin, Herceptin, and Rituxan) after key patents expire. Anti-diabetes is forecast to

be the second biggest therapy area, with sales of USD66.1b in 2022 (6.8% CAGR), accounting for 5.7%

of the pharmaceuticals market (vs 5.4% in 2015). Sales of number-one anti-diabetes drug Lantus

should shrink at a 2016-2022 CAGR of 11.8% to USD3b in 2022 on the advent of biosimilars after

patent expiration. Accordingly, Sanofi’s anti-diabetes sales should slide 1.1% pa to USD7.7b in 2022,

while its market share should tumble from 20% to 11.7%. Meanwhile, anti-rheumatics should remain

a low-growth market, expanding just 1.6% pa to USD54.5b in 2022 due to price erosion caused by

the entry of biosimilars. We expect sales of the blockbusters Humira, Enbrel, and Remicade to

decline 0.7%, 3.2%, and 10.9% pa, respectively, to USD13.6b, USD7.2b, and KRW3.6b in 2022.

Contents

1H review: Poverty in the midst of plenty

p2

Pharmaceutical market outlook

p7

Visible progress to be made on R&D and B2B fronts

p32

Government policy warrants attention

p52

Key issues in 2H p68

Solid earnings momentum in 2H

p87

Company p105

Healthcare

2017. 6. 15

8

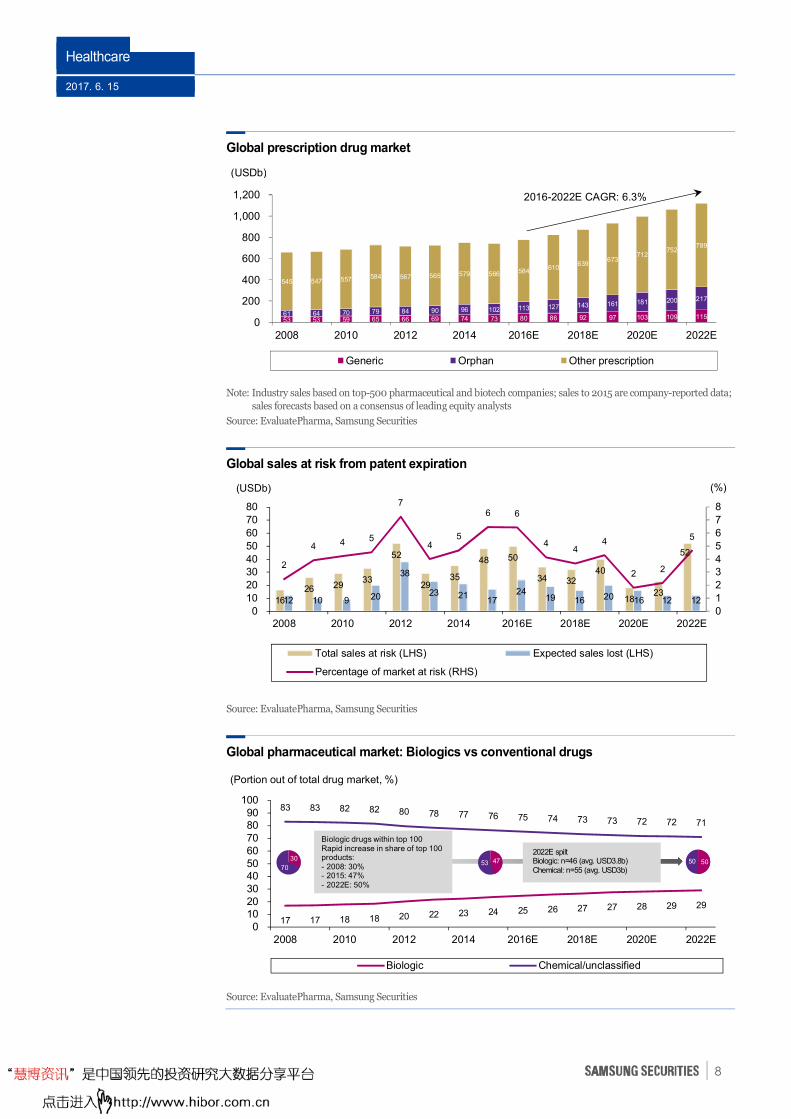

Global prescription drug market

Note: Industry sales based on top-500 pharmaceutical and biotech companies; sales to 2015 are company-reported data;

sales forecasts based on a consensus of leading equity analysts

Source: EvaluatePharma, Samsung Securities

Global sales at risk from patent expiration

Source: EvaluatePharma, Samsung Securities

Global pharmaceutical market: Biologics vs conventional drugs

Source: EvaluatePharma, Samsung Securities

53 53 59 65 66 69 74 73 80 86 92 97 103 109 115 61 64 70 79 84 90 96 102 113 127 143 161 181 200 217

545 547 557 584 567 565 579 566 584 610

639 673

712 752

789

0

200

400

600

800

1,000

1,200

2008 2010 2012 2014 2016E 2018E 2020E 2022E

Generic Orphan Other prescription

(USDb)

2016-2022E CAGR: 6.3%

17 17 18 18 20 22 23 24 25 26 27 27 28 29 29

83 83 82 82 80 78 77 76 75 74 73 73 72 72 71

0102030405060708090

100

2008 2010 2012 2014 2016E 2018E 2020E 2022E

Biologic Chemical/unclassified

(Portion out of total drug market, %)

Biologic drugs within top 100Rapid increase in share of top 100 products:- 2008: 30%- 2015: 47%- 2022E: 50%

2022E spiltBiologic: n=46 (avg. USD3.8b)Chemical: n=55 (avg. USD3b)

30

7053 47 50 50

16

26 29 33

52

29 35

48 50

34 32 40

18 23

52

12 10 9 20

38

23 21 17

24 19 16 20 16 12 12

2

4 4 5

7

4 5

6 6

4 4

4

2 2

5

0

1

2

34

5

6

7

8

0

10

20

3040

50

60

70

80

2008 2010 2012 2014 2016E 2018E 2020E 2022E

Total sales at risk (LHS) Expected sales lost (LHS)

Percentage of market at risk (RHS)

(USDb) (%)

Healthcare

2017. 6. 15

9

Top-10 therapy areas in 2022E: Market share and sales growth

Source: EvaluatePharma, Samsung Securities

0

2

4

6

8

10

12

14

16

18

20

(4.0) (2.0) 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0

2022E market share (%)

(2015-2022E sales growth CAGR, %)

Oncology

Anti-diabetes

Immunosuppressants

Dematologicals

Anti-virals

Anti-rheumatics

Anti-hypertensives

Vaccine

Sensory organs

MS therapiesAnti-coagulants

Broncho-dilators

Anti-fibrinolytics

Anti-bacterials

Key growth drivers:Descovy (GILD), Genvoya (GILD)Bictegravir/F/TAF (GILD), Tirumeq (GSK)Key growth brakes:Harvoni (GILD), Sovaldi (GILD)Truvada (GILD), Atripla (GSK)

Key growth drivers:Opdivo (BMY), Revlimid (CELG), Keytruda (MRK), Ibrance (PFE), Perjeta (Roche), Tecentriq (Roche)Key patent expiries:Gleevec (Novartis, 2016), Rituxan (Roche, 2016+)Alimta (LLY, 2015+), Herceptin (Roche, 2014+)

Key contributors to CAGR growth:Stelara (JNJ); dupilumab (SAN) - expected 2017 global launch; Ozanimod (CELG) - expected 2018 launch

Anti-hyperlipidaemics

Healthcare

2017. 6. 15

10

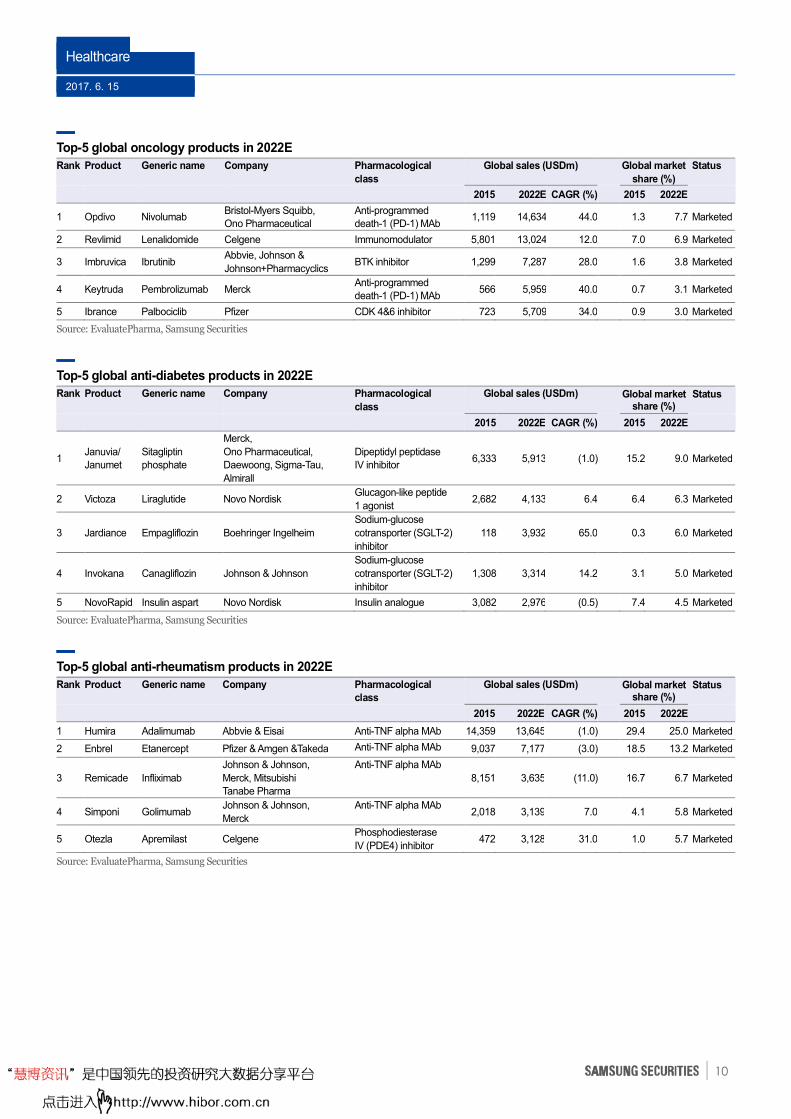

Top-5 global oncology products in 2022E

Rank

Product

Generic name

Company

Pharmacological

class

Global sales (USDm)

Global market

share (%)

Status

2015 2022E CAGR (%) 2015 2022E

1 Opdivo Nivolumab Bristol-Myers Squibb,

Ono Pharmaceutical

Anti-programmed

death-1 (PD-1) MAb 1,119 14,634 44.0 1.3 7.7 Marketed

2 Revlimid Lenalidomide Celgene Immunomodulator 5,801 13,024 12.0 7.0 6.9 Marketed

3 Imbruvica Ibrutinib Abbvie, Johnson &

Johnson+Pharmacyclics BTK inhibitor 1,299 7,287 28.0 1.6 3.8 Marketed

4 Keytruda Pembrolizumab Merck Anti-programmed

death-1 (PD-1) MAb 566 5,959 40.0 0.7 3.1 Marketed

5 Ibrance Palbociclib Pfizer CDK 4&6 inhibitor 723 5,709 34.0 0.9 3.0 Marketed

Source: EvaluatePharma, Samsung Securities

Top-5 global anti-diabetes products in 2022E

Rank

Product

Generic name

Company

Pharmacological

class

Global sales (USDm)

Global market share (%)

Status

2015 2022E CAGR (%) 2015 2022E

1 Januvia/

Janumet

Sitagliptin

phosphate

Merck,

Ono Pharmaceutical,

Daewoong, Sigma-Tau,

Almirall

Dipeptidyl peptidase

IV inhibitor 6,333 5,913 (1.0) 15.2 9.0 Marketed

2 Victoza Liraglutide Novo Nordisk Glucagon-like peptide

1 agonist 2,682 4,133 6.4 6.4 6.3 Marketed

3 Jardiance Empagliflozin Boehringer Ingelheim

Sodium-glucose

cotransporter (SGLT-2)

inhibitor

118 3,932 65.0 0.3 6.0 Marketed

4 Invokana Canagliflozin Johnson & Johnson

Sodium-glucose

cotransporter (SGLT-2)

inhibitor

1,308 3,314 14.2 3.1 5.0 Marketed

5 NovoRapid Insulin aspart Novo Nordisk Insulin analogue 3,082 2,976 (0.5) 7.4 4.5 Marketed

Source: EvaluatePharma, Samsung Securities

Top-5 global anti-rheumatism products in 2022E

Rank

Product

Generic name

Company

Pharmacological

class

Global sales (USDm)

Global market share (%)

Status

2015 2022E CAGR (%) 2015 2022E

1 Humira Adalimumab Abbvie & Eisai Anti-TNF alpha MAb 14,359 13,645 (1.0) 29.4 25.0 Marketed

2 Enbrel Etanercept Pfizer & Amgen &Takeda Anti-TNF alpha MAb 9,037 7,177 (3.0) 18.5 13.2 Marketed

3 Remicade Infliximab

Johnson & Johnson,

Merck, Mitsubishi

Tanabe Pharma

Anti-TNF alpha MAb

8,151 3,635 (11.0) 16.7 6.7 Marketed

4 Simponi Golimumab Johnson & Johnson,

Merck

Anti-TNF alpha MAb 2,018 3,139 7.0 4.1 5.8 Marketed

5 Otezla Apremilast Celgene Phosphodiesterase

IV (PDE4) inhibitor 472 3,128 31.0 1.0 5.7 Marketed

Source: EvaluatePharma, Samsung Securities

Healthcare

2017. 6. 15

11

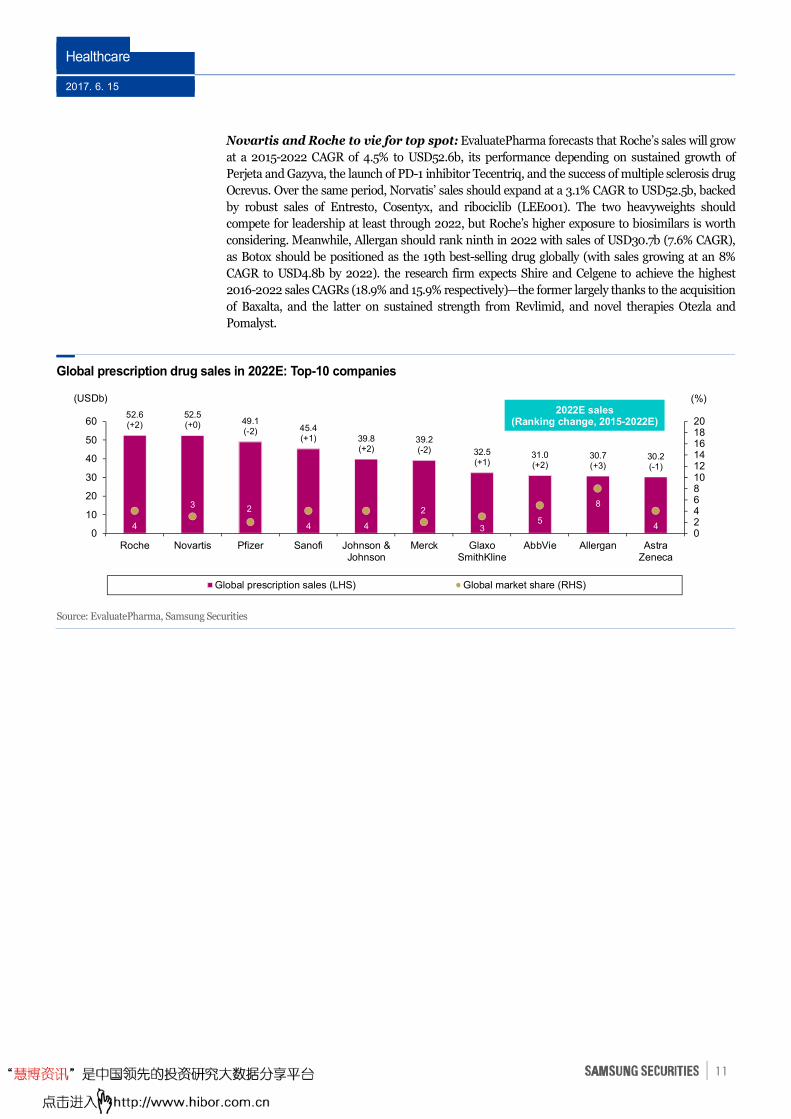

Novartis and Roche to vie for top spot: EvaluatePharma forecasts that Roche’s sales will grow

at a 2015-2022 CAGR of 4.5% to USD52.6b, its performance depending on sustained growth of

Perjeta and Gazyva, the launch of PD-1 inhibitor Tecentriq, and the success of multiple sclerosis drug

Ocrevus. Over the same period, Norvatis’ sales should expand at a 3.1% CAGR to USD52.5b, backed

by robust sales of Entresto, Cosentyx, and ribociclib (LEE001). The two heavyweights should

compete for leadership at least through 2022, but Roche’s higher exposure to biosimilars is worth

considering. Meanwhile, Allergan should rank ninth in 2022 with sales of USD30.7b (7.6% CAGR),

as Botox should be positioned as the 19th best-selling drug globally (with sales growing at an 8%

CAGR to USD4.8b by 2022). the research firm expects Shire and Celgene to achieve the highest

2016-2022 sales CAGRs (18.9% and 15.9% respectively)—the former largely thanks to the acquisition

of Baxalta, and the latter on sustained strength from Revlimid, and novel therapies Otezla and

Pomalyst.

Global prescription drug sales in 2022E: Top-10 companies

Source: EvaluatePharma, Samsung Securities

52.6(+2)

52.5(+0) 49.1

(-2) 45.4(+1) 39.8

(+2)39.2(-2) 32.5

(+1)31.0(+2)

30.7(+3)

30.2(-1)

4

3 2

4 4

2

35

8

402468101214161820

0

10

20

30

40

50

60

Roche Novartis Pfizer Sanofi Johnson &Johnson

Merck GlaxoSmithKline

AbbVie Allergan AstraZeneca

Global prescription sales (LHS) Global market share (RHS)

(USDb) (%)2022E sales

(Ranking change, 2015-2022E)

Healthcare

2017. 6. 15

12

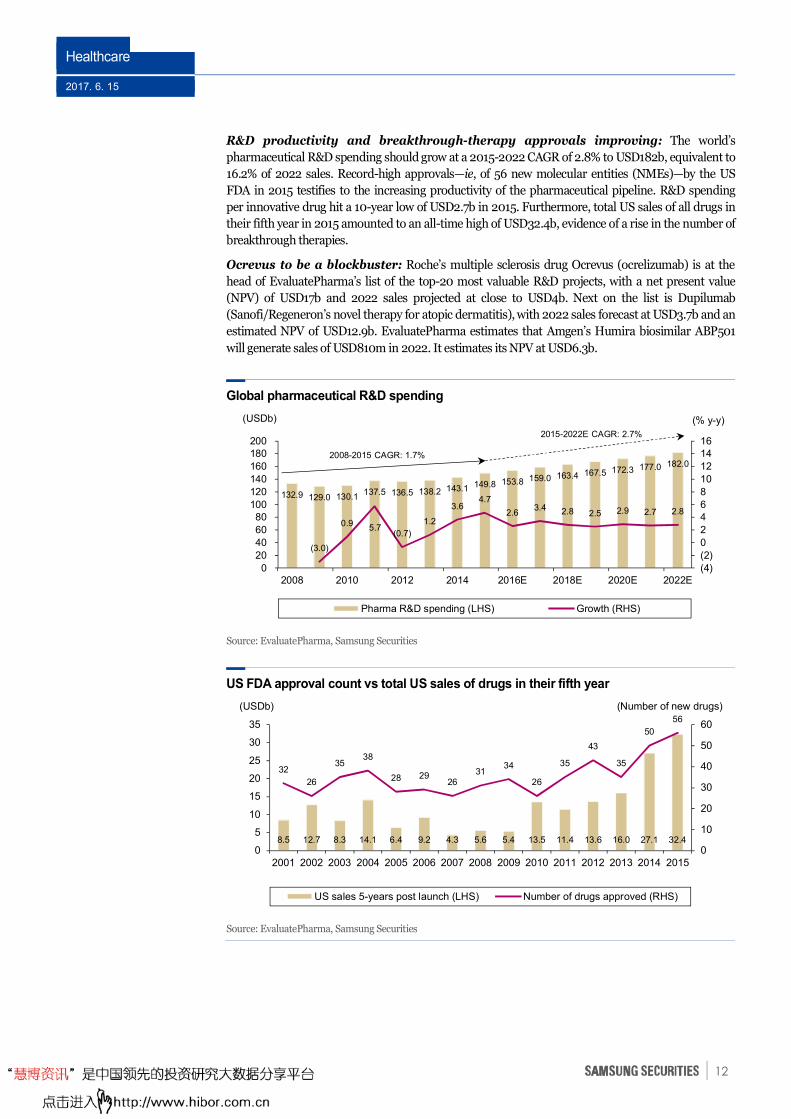

R&D productivity and breakthrough-therapy approvals improving: The world’s

pharmaceutical R&D spending should grow at a 2015-2022 CAGR of 2.8% to USD182b, equivalent to

16.2% of 2022 sales. Record-high approvals—ie, of 56 new molecular entities (NMEs)—by the US

FDA in 2015 testifies to the increasing productivity of the pharmaceutical pipeline. R&D spending

per innovative drug hit a 10-year low of USD2.7b in 2015. Furthermore, total US sales of all drugs in

their fifth year in 2015 amounted to an all-time high of USD32.4b, evidence of a rise in the number of

breakthrough therapies.

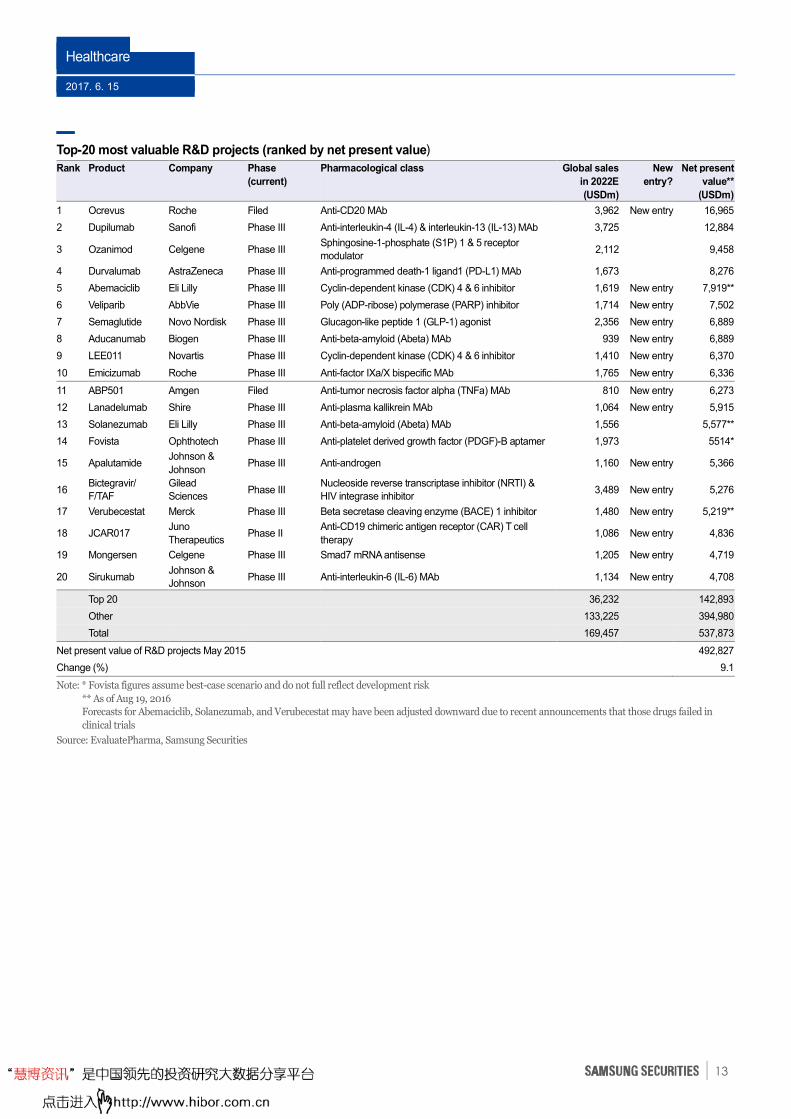

Ocrevus to be a blockbuster: Roche’s multiple sclerosis drug Ocrevus (ocrelizumab) is at the

head of EvaluatePharma’s list of the top-20 most valuable R&D projects, with a net present value

(NPV) of USD17b and 2022 sales projected at close to USD4b. Next on the list is Dupilumab

(Sanofi/Regeneron’s novel therapy for atopic dermatitis), with 2022 sales forecast at USD3.7b and an

estimated NPV of USD12.9b. EvaluatePharma estimates that Amgen’s Humira biosimilar ABP501

will generate sales of USD810m in 2022. It estimates its NPV at USD6.3b.

Global pharmaceutical R&D spending

Source: EvaluatePharma, Samsung Securities

US FDA approval count vs total US sales of drugs in their fifth year

Source: EvaluatePharma, Samsung Securities

8.5 12.7 8.3 14.1 6.4 9.2 4.3 5.6 5.4 13.5 11.4 13.6 16.0 27.1 32.4

32

26

3538

28 2926

3134

26

35

43

35

50

56

0

10

20

30

40

50

60

0

5

10

15

20

25

30

35

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US sales 5-years post launch (LHS) Number of drugs approved (RHS)

(USDb) (Number of new drugs)

132.9 129.0 130.1 137.5 136.5 138.2 143.1 149.8 153.8 159.0 163.4 167.5 172.3 177.0 182.0

(3.0)

0.9 5.7

(0.7)

1.2

3.6 4.7

2.6 3.4 2.8 2.5 2.9 2.7 2.8

(4)

(2)

0

2

46

8

10

12

1416

0

20

40

60

80100

120

140

160

180200

2008 2010 2012 2014 2016E 2018E 2020E 2022E

Pharma R&D spending (LHS) Growth (RHS)

(USDb) (% y-y)

2008-2015 CAGR: 1.7%

2015-2022E CAGR: 2.7%

Healthcare

2017. 6. 15

13

Top-20 most valuable R&D projects (ranked by net present value)

Rank

Product

Company

Phase

(current)

Pharmacological class

Global sales

in 2022E

(USDm)

New

entry?

Net present

value**

(USDm)

1 Ocrevus Roche Filed Anti-CD20 MAb 3,962 New entry 16,965

2 Dupilumab Sanofi Phase III Anti-interleukin-4 (IL-4) & interleukin-13 (IL-13) MAb 3,725 12,884

3 Ozanimod Celgene Phase III Sphingosine-1-phosphate (S1P) 1 & 5 receptor

modulator 2,112 9,458

4 Durvalumab AstraZeneca Phase III Anti-programmed death-1 ligand1 (PD-L1) MAb 1,673 8,276

5 Abemaciclib Eli Lilly Phase III Cyclin-dependent kinase (CDK) 4 & 6 inhibitor 1,619 New entry 7,919**

6 Veliparib AbbVie Phase III Poly (ADP-ribose) polymerase (PARP) inhibitor 1,714 New entry 7,502

7 Semaglutide Novo Nordisk Phase III Glucagon-like peptide 1 (GLP-1) agonist 2,356 New entry 6,889

8 Aducanumab Biogen Phase III Anti-beta-amyloid (Abeta) MAb 939 New entry 6,889

9 LEE011 Novartis Phase III Cyclin-dependent kinase (CDK) 4 & 6 inhibitor 1,410 New entry 6,370

10 Emicizumab Roche Phase III Anti-factor IXa/X bispecific MAb 1,765 New entry 6,336

11 ABP501 Amgen Filed Anti-tumor necrosis factor alpha (TNFa) MAb 810 New entry 6,273

12 Lanadelumab Shire Phase III Anti-plasma kallikrein MAb 1,064 New entry 5,915

13 Solanezumab Eli Lilly Phase III Anti-beta-amyloid (Abeta) MAb 1,556 5,577**

14 Fovista Ophthotech Phase III Anti-platelet derived growth factor (PDGF)-B aptamer 1,973 5514*

15 Apalutamide Johnson &

Johnson Phase III Anti-androgen 1,160 New entry 5,366

16 Bictegravir/

F/TAF

Gilead

Sciences Phase III

Nucleoside reverse transcriptase inhibitor (NRTI) &

HIV integrase inhibitor 3,489 New entry 5,276

17 Verubecestat Merck Phase III Beta secretase cleaving enzyme (BACE) 1 inhibitor 1,480 New entry 5,219**

18 JCAR017 Juno

Therapeutics Phase II

Anti-CD19 chimeric antigen receptor (CAR) T cell

therapy 1,086 New entry 4,836

19 Mongersen Celgene Phase III Smad7 mRNA antisense 1,205 New entry 4,719

20 Sirukumab Johnson &

Johnson Phase III Anti-interleukin-6 (IL-6) MAb 1,134 New entry 4,708

Top 20 36,232 142,893

Other 133,225 394,980

Total 169,457 537,873

Net present value of R&D projects May 2015 492,827

Change (%) 9.1

Note: * Fovista figures assume best-case scenario and do not full reflect development risk

** As of Aug 19, 2016

Forecasts for Abemaciclib, Solanezumab, and Verubecestat may have been adjusted downward due to recent announcements that those drugs failed in

clinical trials

Source: EvaluatePharma, Samsung Securities

Healthcare

2017. 6. 15

14

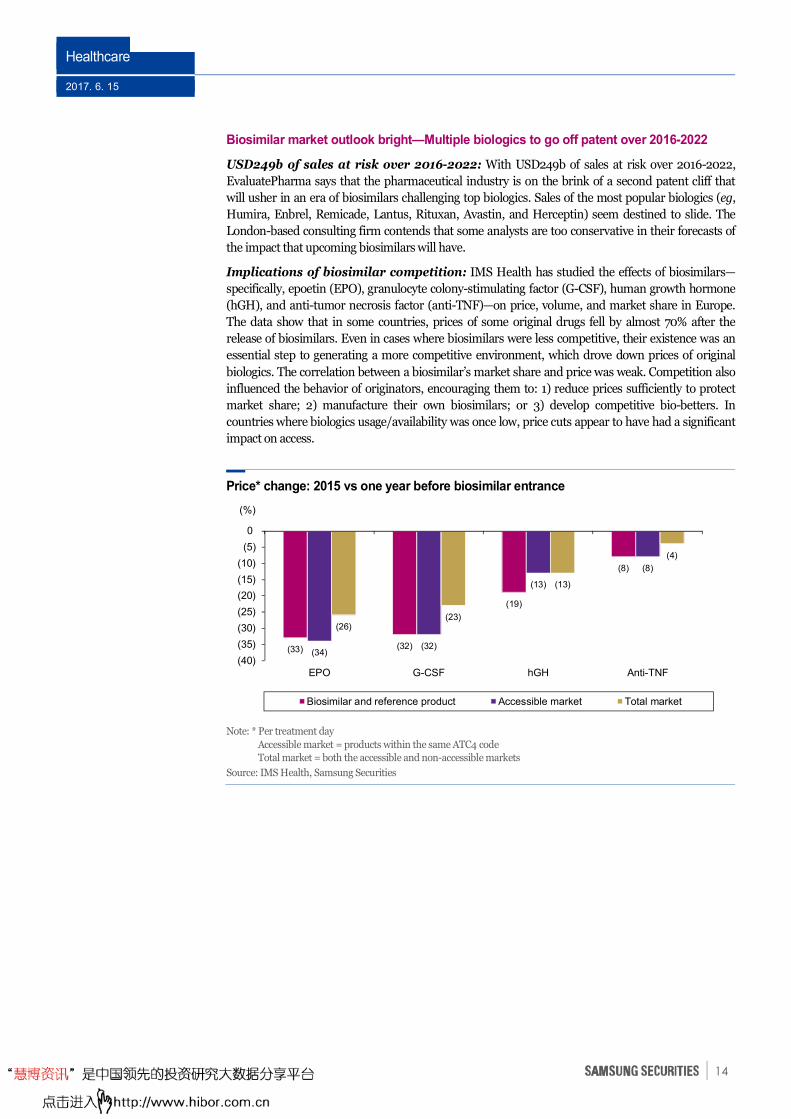

Biosimilar market outlook bright—Multiple biologics to go off patent over 2016-2022

USD249b of sales at risk over 2016-2022: With USD249b of sales at risk over 2016-2022,

EvaluatePharma says that the pharmaceutical industry is on the brink of a second patent cliff that

will usher in an era of biosimilars challenging top biologics. Sales of the most popular biologics (eg,

Humira, Enbrel, Remicade, Lantus, Rituxan, Avastin, and Herceptin) seem destined to slide. The

London-based consulting firm contends that some analysts are too conservative in their forecasts of

the impact that upcoming biosimilars will have.

Implications of biosimilar competition: IMS Health has studied the effects of biosimilars—

specifically, epoetin (EPO), granulocyte colony-stimulating factor (G-CSF), human growth hormone

(hGH), and anti-tumor necrosis factor (anti-TNF)—on price, volume, and market share in Europe.

The data show that in some countries, prices of some original drugs fell by almost 70% after the

release of biosimilars. Even in cases where biosimilars were less competitive, their existence was an

essential step to generating a more competitive environment, which drove down prices of original

biologics. The correlation between a biosimilar’s market share and price was weak. Competition also

influenced the behavior of originators, encouraging them to: 1) reduce prices sufficiently to protect

market share; 2) manufacture their own biosimilars; or 3) develop competitive bio-betters. In

countries where biologics usage/availability was once low, price cuts appear to have had a significant

impact on access.

Price* change: 2015 vs one year before biosimilar entrance

Note: * Per treatment day

Accessible market = products within the same ATC4 code

Total market = both the accessible and non-accessible markets

Source: IMS Health, Samsung Securities

(33) (32)

(19)

(8)

(34)(32)

(13)

(8)

(26)(23)

(13)

(4)

(40)

(35)

(30)

(25)

(20)

(15)

(10)

(5)

0

EPO G-CSF hGH Anti-TNF

Biosimilar and reference product Accessible market Total market

(%)

Healthcare

2017. 6. 15

15

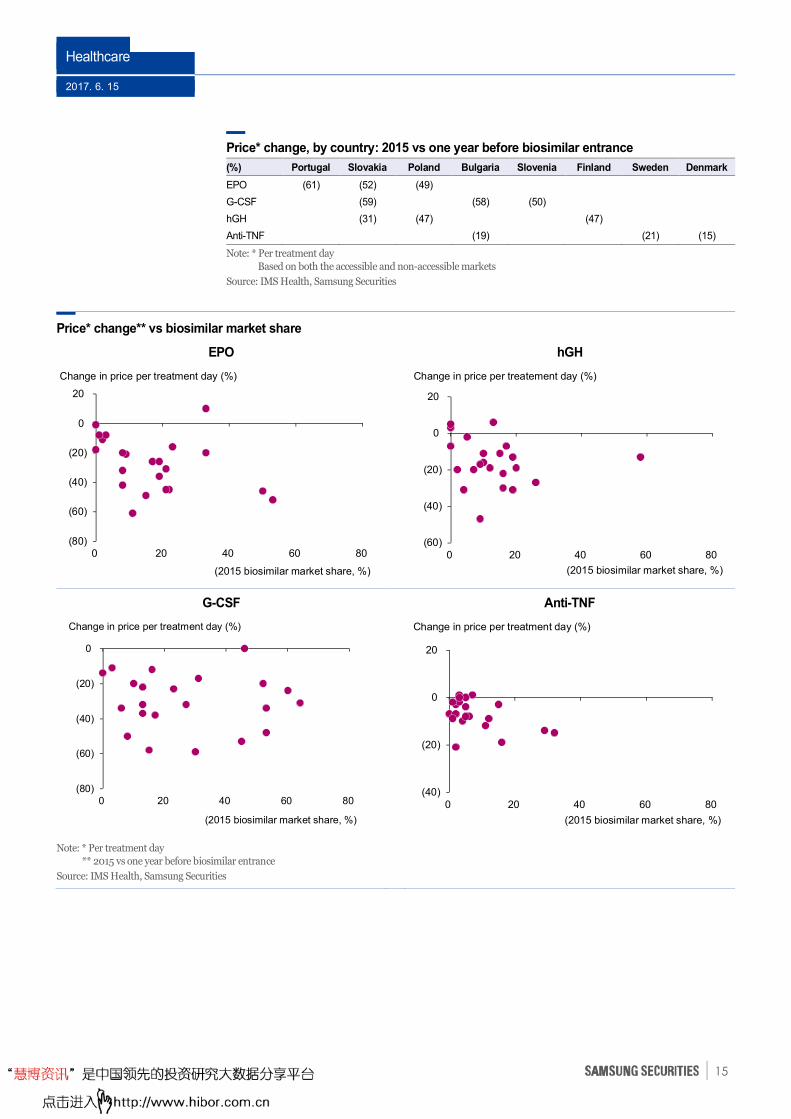

Price* change, by country: 2015 vs one year before biosimilar entrance

(%) Portugal Slovakia Poland Bulgaria Slovenia Finland Sweden Denmark

EPO (61) (52) (49)

G-CSF (59) (58) (50)

hGH (31) (47) (47)

Anti-TNF (19) (21) (15)

Note: * Per treatment day

Based on both the accessible and non-accessible markets

Source: IMS Health, Samsung Securities

Price* change** vs biosimilar market share

EPO hGH

G-CSF Anti-TNF

Note: * Per treatment day

** 2015 vs one year before biosimilar entrance

Source: IMS Health, Samsung Securities

(80)

(60)

(40)

(20)

0

20

0 20 40 60 80

(2015 biosimilar market share, %)

Change in price per treatment day (%)

(60)

(40)

(20)

0

20

0 20 40 60 80

(2015 biosimilar market share, %)

Change in price per treatement day (%)

(40)

(20)

0

20

0 20 40 60 80

(2015 biosimilar market share, %)

Change in price per treatment day (%)

(80)

(60)

(40)

(20)

0

0 20 40 60 80

(2015 biosimilar market share, %)

Change in price per treatment day (%)

Healthcare

2017. 6. 15

16

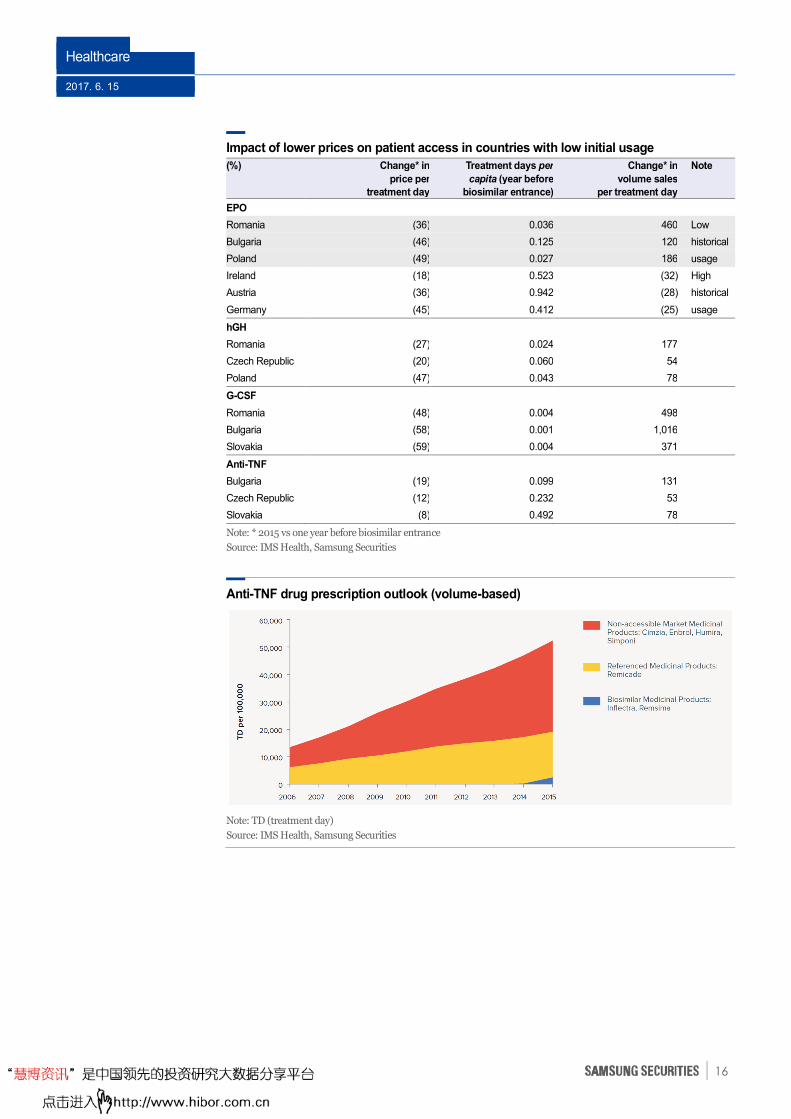

Impact of lower prices on patient access in countries with low initial usage

(%)

Change* in

price per

treatment day

Treatment days per

capita (year before

biosimilar entrance)

Change* in

volume sales

per treatment day

Note

EPO

Romania (36) 0.036 460 Low

Bulgaria (46) 0.125 120 historical

Poland (49) 0.027 186 usage

Ireland (18) 0.523 (32) High

Austria (36) 0.942 (28) historical

Germany (45) 0.412 (25) usage

hGH

Romania (27) 0.024 177

Czech Republic (20) 0.060 54

Poland (47) 0.043 78

G-CSF

Romania (48) 0.004 498

Bulgaria (58) 0.001 1,016

Slovakia (59) 0.004 371

Anti-TNF

Bulgaria (19) 0.099 131

Czech Republic (12) 0.232 53

Slovakia (8) 0.492 78

Note: * 2015 vs one year before biosimilar entrance

Source: IMS Health, Samsung Securities

Anti-TNF drug prescription outlook (volume-based)

Note: TD (treatment day)

Source: IMS Health, Samsung Securities

Healthcare

2017. 6. 15

17

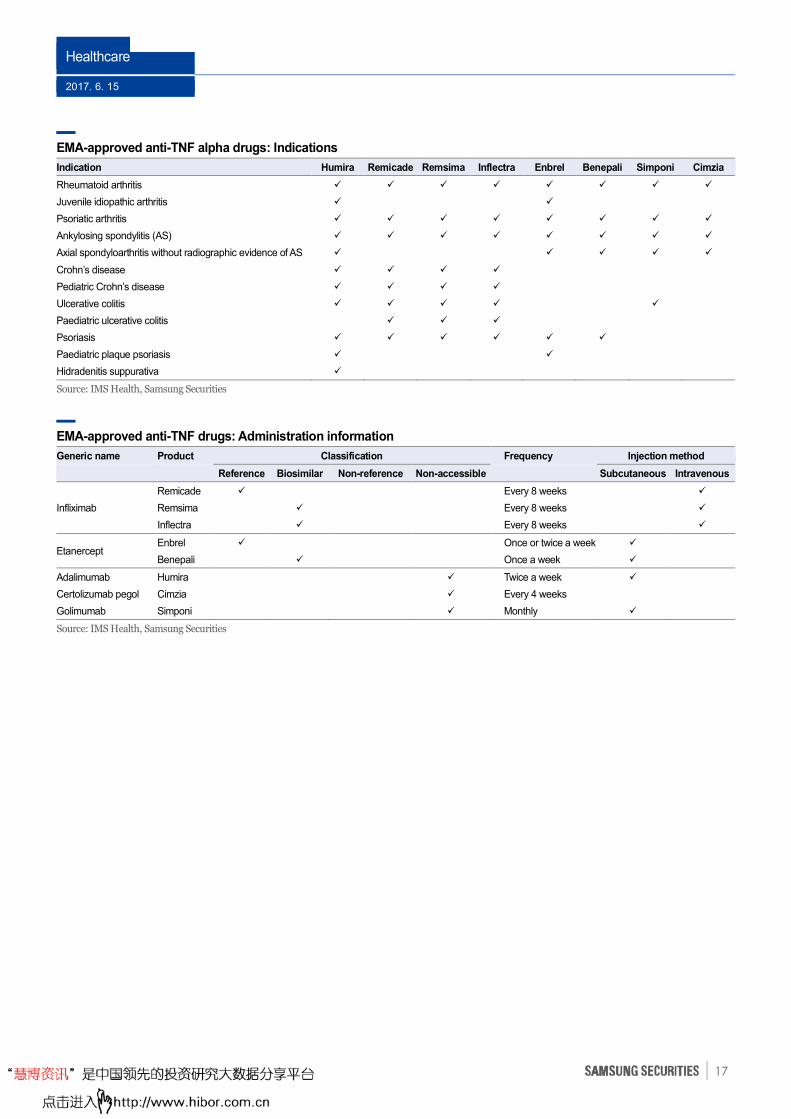

EMA-approved anti-TNF alpha drugs: Indications

Indication Humira Remicade Remsima Inflectra Enbrel Benepali Simponi Cimzia

Rheumatoid arthritis � � � � � � � �

Juvenile idiopathic arthritis � �

Psoriatic arthritis � � � � � � � �

Ankylosing spondylitis (AS) � � � � � � � �

Axial spondyloarthritis without radiographic evidence of AS � � � � �

Crohn’s disease � � � �

Pediatric Crohn’s disease � � � �

Ulcerative colitis � � � � �

Paediatric ulcerative colitis � � �

Psoriasis � � � � � �

Paediatric plaque psoriasis � �

Hidradenitis suppurativa �

Source: IMS Health, Samsung Securities

EMA-approved anti-TNF drugs: Administration information

Generic name Product Classification Frequency Injection method

Reference Biosimilar Non-reference Non-accessible Subcutaneous Intravenous

Remicade � Every 8 weeks �

Infliximab Remsima � Every 8 weeks �

Inflectra � Every 8 weeks �

Etanercept Enbrel � Once or twice a week �

Benepali � Once a week �

Adalimumab Humira � Twice a week �

Certolizumab pegol Cimzia � Every 4 weeks

Golimumab Simponi � Monthly �

Source: IMS Health, Samsung Securities

Healthcare

2017. 6. 15

18

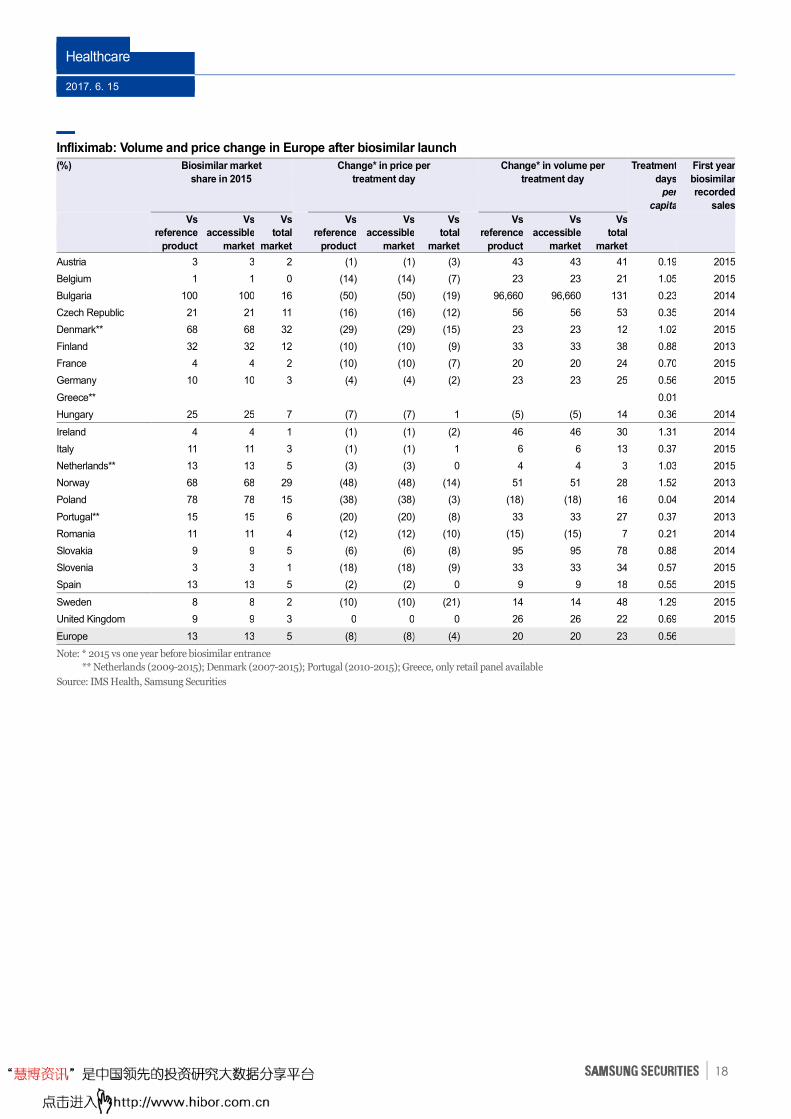

Infliximab: Volume and price change in Europe after biosimilar launch

(%)

Biosimilar market

share in 2015

Change* in price per

treatment day

Change* in volume per

treatment day

Treatment

days

per

capita

First year

biosimilar

recorded

sales

Vs

reference

product

Vs

accessible

market

Vs

total

market

Vs

reference

product

Vs

accessible

market

Vs

total

market

Vs

reference

product

Vs

accessible

market

Vs

total

market

Austria 3 3 2 (1) (1) (3) 43 43 41 0.19 2015

Belgium 1 1 0 (14) (14) (7) 23 23 21 1.05 2015

Bulgaria 100 100 16 (50) (50) (19) 96,660 96,660 131 0.23 2014

Czech Republic 21 21 11 (16) (16) (12) 56 56 53 0.35 2014

Denmark** 68 68 32 (29) (29) (15) 23 23 12 1.02 2015

Finland 32 32 12 (10) (10) (9) 33 33 38 0.88 2013

France 4 4 2 (10) (10) (7) 20 20 24 0.70 2015

Germany 10 10 3 (4) (4) (2) 23 23 25 0.56 2015

Greece** 0.01

Hungary 25 25 7 (7) (7) 1 (5) (5) 14 0.36 2014

Ireland 4 4 1 (1) (1) (2) 46 46 30 1.31 2014

Italy 11 11 3 (1) (1) 1 6 6 13 0.37 2015

Netherlands** 13 13 5 (3) (3) 0 4 4 3 1.03 2015

Norway 68 68 29 (48) (48) (14) 51 51 28 1.52 2013

Poland 78 78 15 (38) (38) (3) (18) (18) 16 0.04 2014

Portugal** 15 15 6 (20) (20) (8) 33 33 27 0.37 2013

Romania 11 11 4 (12) (12) (10) (15) (15) 7 0.21 2014

Slovakia 9 9 5 (6) (6) (8) 95 95 78 0.88 2014

Slovenia 3 3 1 (18) (18) (9) 33 33 34 0.57 2015

Spain 13 13 5 (2) (2) 0 9 9 18 0.55 2015

Sweden 8 8 2 (10) (10) (21) 14 14 48 1.29 2015

United Kingdom 9 9 3 0 0 0 26 26 22 0.69 2015

Europe 13 13 5 (8) (8) (4) 20 20 23 0.56

Note: * 2015 vs one year before biosimilar entrance

** Netherlands (2009-2015); Denmark (2007-2015); Portugal (2010-2015); Greece, only retail panel available

Source: IMS Health, Samsung Securities

Healthcare

2017. 6. 15

19

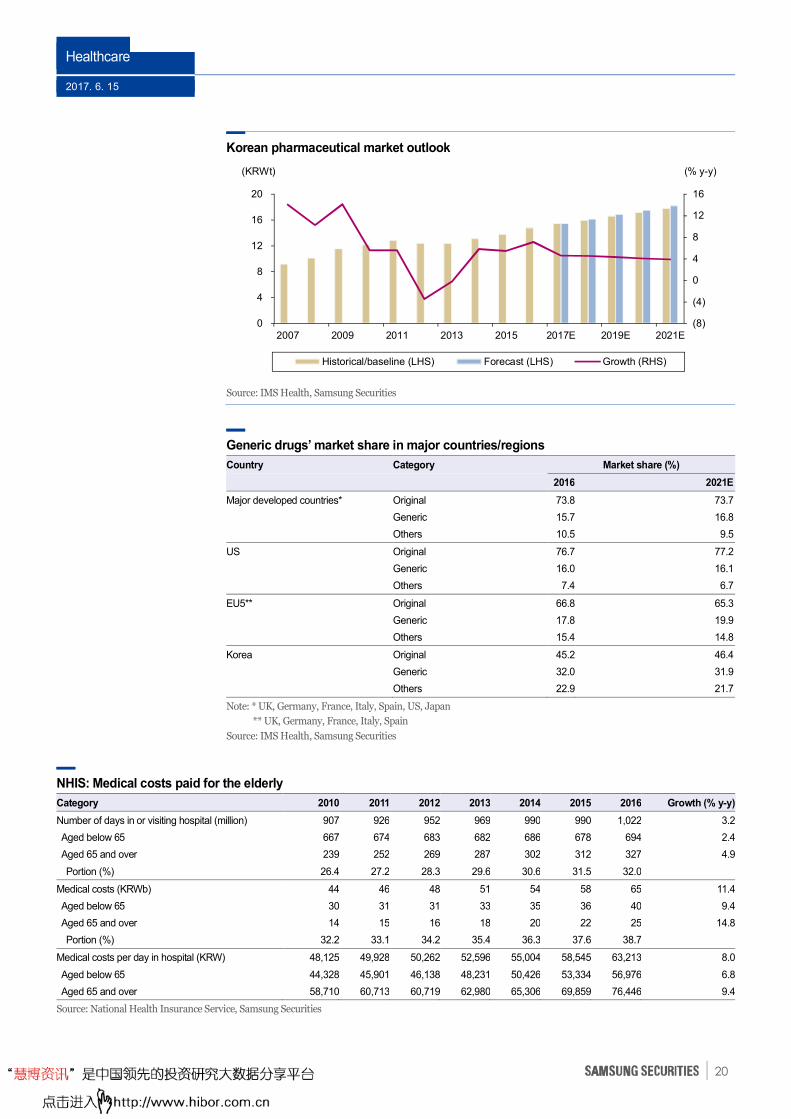

Korea’s pharmaceutical market outlook solid

Korea’s pharmaceutical sales outlook: According to IMS Health, Korea’s pharmaceutical

market should grow at a 2017-2021 CAGR of 4.4% to KRW18.58t—around twice stronger the

country’s estimated annual GDP growth of 2.3% over the same period. Cancer therapy and

immunomodulators should achieve the highest growth, averaging 8.5% pa, while anti-diabetes and

digestive-system medicines should also outpace the market’s growth, averaging 5.2% pa. Meanwhile,

sales of systemic anti-infective materials are projected fall sharply as sales of hepatitis C treatments

weaken.

Growth via population aging, chronic disease, wider coverage for four big diseases:

The market expansion will be driven by population aging, according to IMS Health. In 2016, the

elderly—ie, those aged 65 and above—accounted for only 13% of people covered by the National

Health Insurance Service (NHIS), but their medical costs accounted for 39% (KRW25.2t) of the

NHIS total. The life expectancy of Korean females born in 2030 should be 90 years, up from 85.2

years in 2015, while males born in 2030 should have a life expectancy of 84.1 years (vs 79 years in

2015). The country’s medical costs should surge over 2017-2021 as: 1) more people are developing

chronic diseases due to societal aging; and 2) national health insurance coverage is expanding for

four major diseases—ie, cancers, rare diseases, cardiovascular diseases, and cerebrovascular diseases.

The government plans to improve the frameworks for drug prices and health insurance to support

the bio industry.

Generics to continue to lead market growth in Korea: IMS Health says that generics

represented 32% of Korea’s pharmaceutical market in 2016, and that figure should barely budge

through 2021, edging down just 0.1%pts. Meanwhile, the developed-market average should climb

1.1%pts to 16.8% over the same period. Why will market share stagnate in Korea? Because

penetration is already high, and prices are almost on par with those of off-patent drugs, which serves

to discourage substitution with generics. Meanwhile, original drugs accounted for 45.2% of 2016

sales in Korea, around half of which came from off-patent drugs; original drugs made up 73.8% of

sales in developed markets, while off-patent drugs accounted for around just 20%.

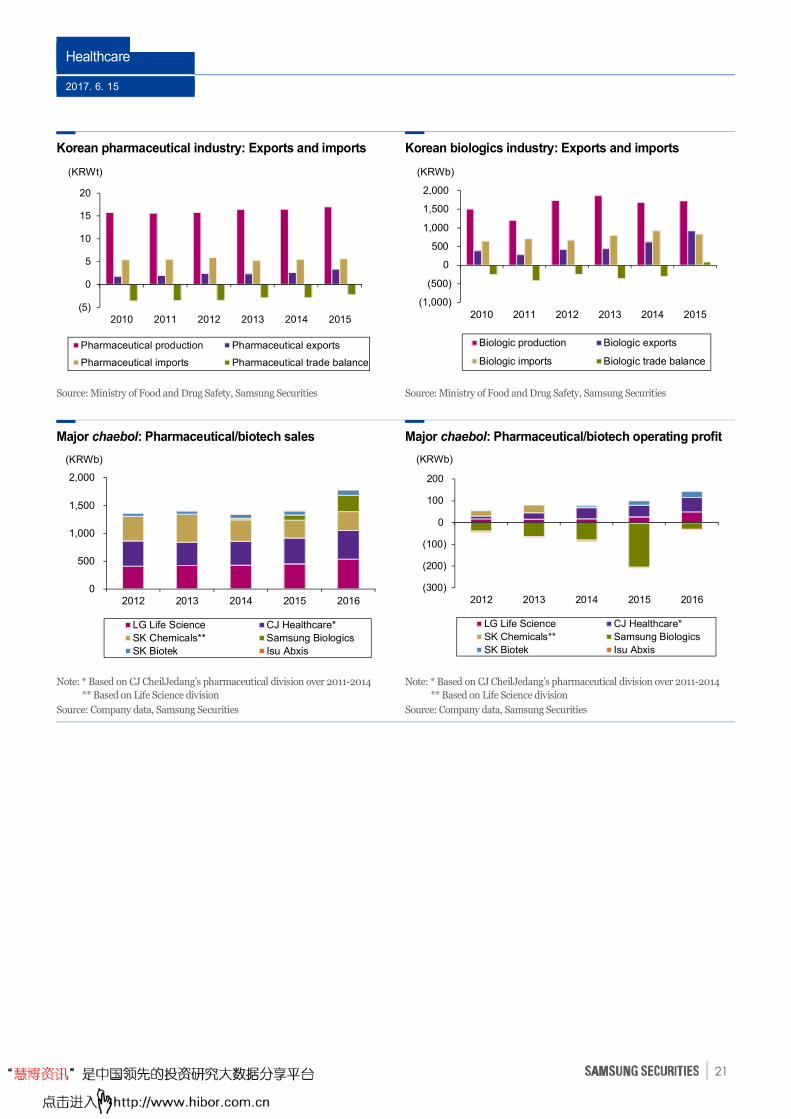

Biologics exports to keep growing strongly: According to Korea’s Ministry of Food and Drug

Safety, the pharmaceutical market grew 3.4% y-y to KRW17t in 2015, with exports leaping 31.1% y-y

to KRW3.3t and imports rising 1.9% y-y to KRW5.6t for a trade deficit of KRW2.3t. In the same year,

biologics production rose 2.3% y-y to KRW1.72t. Biologics exports leapt 47.7% y-y to KRW915.7b

while imports shrank 9.5% y-y to KRW835.3b, turning Korea to a trade surplus of KRW80.4b.

Biologics exports have accelerated, led by solid biosimilar exports, and this trend should continue as

multiple biosimilar are commercialized and exports by bio-CMO firms increase.

Chaebols’ pharmaceutical arms to thrive: Chaebols have also entered the pharmaceutical

market—eg, CJ Healthcare was established in 1984; SK Chemicals (formerly SK Pharma) in 1998;

Isu Abxis in 2001; LG Life Sciences in 2002; SK Biopharmaceuticals (spun off) and Samsung

Biologics in 2011; Samsung Bioepis in 2012; and SK Biotek (spun off) in 2015. These chaebol arms

are now emerging as growth drivers of Korea’s pharmaceutical market and, notably, enjoying rapid

earnings improvements. The combined sales of LG Life Sciences, CJ Healthcare, SK Chemicals,

Samsung Biologics, SK Biotek, and Isu Abxis leapt 27% y-y to KRW1.795t in 2016, and the group

turned y-y to a combined operating profit of KRW110.7b. We expect those companies to enjoy

sustained growth as their investments start to bear fruit.

Healthcare

2017. 6. 15

20

Korean pharmaceutical market outlook

Source: IMS Health, Samsung Securities

Generic drugs’ market share in major countries/regions

Country Category Market share (%)

2016 2021E

Major developed countries* Original 73.8 73.7

Generic 15.7 16.8

Others 10.5 9.5

US Original 76.7 77.2

Generic 16.0 16.1

Others 7.4 6.7

EU5** Original 66.8 65.3

Generic 17.8 19.9

Others 15.4 14.8

Korea Original 45.2 46.4

Generic 32.0 31.9

Others 22.9 21.7

Note: * UK, Germany, France, Italy, Spain, US, Japan

** UK, Germany, France, Italy, Spain

Source: IMS Health, Samsung Securities

NHIS: Medical costs paid for the elderly

Category 2010 2011 2012 2013 2014 2015 2016 Growth (% y-y)

Number of days in or visiting hospital (million) 907 926 952 969 990 990 1,022 3.2

Aged below 65 667 674 683 682 686 678 694 2.4

Aged 65 and over 239 252 269 287 302 312 327 4.9

Portion (%) 26.4 27.2 28.3 29.6 30.6 31.5 32.0

Medical costs (KRWb) 44 46 48 51 54 58 65 11.4

Aged below 65 30 31 31 33 35 36 40 9.4

Aged 65 and over 14 15 16 18 20 22 25 14.8

Portion (%) 32.2 33.1 34.2 35.4 36.3 37.6 38.7

Medical costs per day in hospital (KRW) 48,125 49,928 50,262 52,596 55,004 58,545 63,213 8.0

Aged below 65 44,328 45,901 46,138 48,231 50,426 53,334 56,976 6.8

Aged 65 and over 58,710 60,713 60,719 62,980 65,306 69,859 76,446 9.4

Source: National Health Insurance Service, Samsung Securities

(8)

(4)

0

4

8

12

16

0

4

8

12

16

20

2007 2009 2011 2013 2015 2017E 2019E 2021E

Historical/baseline (LHS) Forecast (LHS) Growth (RHS)

(KRWt) (% y-y)

Healthcare

2017. 6. 15

21

Korean pharmaceutical industry: Exports and imports Korean biologics industry: Exports and imports

Source: Ministry of Food and Drug Safety, Samsung Securities

Source: Ministry of Food and Drug Safety, Samsung Securities

Major chaebol: Pharmaceutical/biotech sales Major chaebol: Pharmaceutical/biotech operating profit

Note: * Based on CJ CheilJedang’s pharmaceutical division over 2011-2014

** Based on Life Science division

Source: Company data, Samsung Securities

Note: * Based on CJ CheilJedang’s pharmaceutical division over 2011-2014

** Based on Life Science division

Source: Company data, Samsung Securities

(5)

0

5

10

15

20

2010 2011 2012 2013 2014 2015

Pharmaceutical production Pharmaceutical exports

Pharmaceutical imports Pharmaceutical trade balance

(KRWt)

(1,000)

(500)

0

500

1,000

1,500

2,000

2010 2011 2012 2013 2014 2015

Biologic production Biologic exports

Biologic imports Biologic trade balance

(KRWb)

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016

LG Life Science CJ Healthcare*

SK Chemicals** Samsung Biologics

SK Biotek Isu Abxis

(KRWb)

(300)

(200)

(100)

0

100

200

2012 2013 2014 2015 2016

LG Life Science CJ Healthcare*

SK Chemicals** Samsung Biologics

SK Biotek Isu Abxis

(KRWb)

Healthcare

2017. 6. 15

22

Sea change for Korea’s healthcare industry over 2012-2017

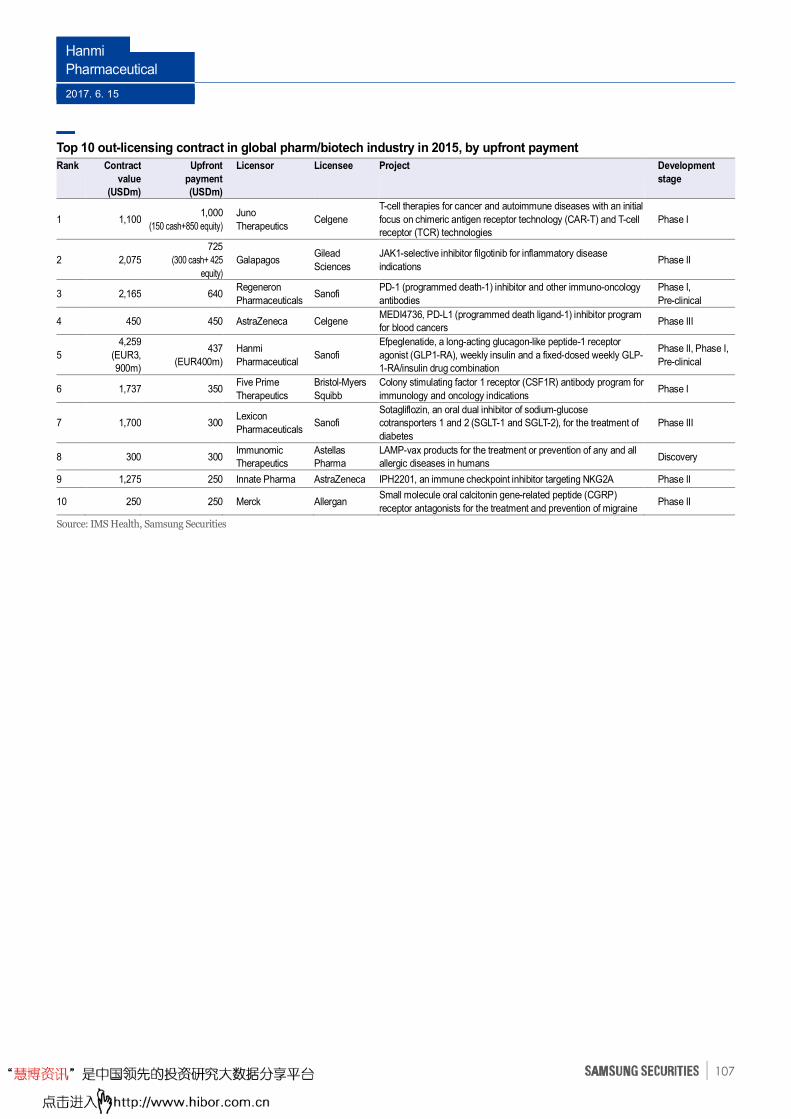

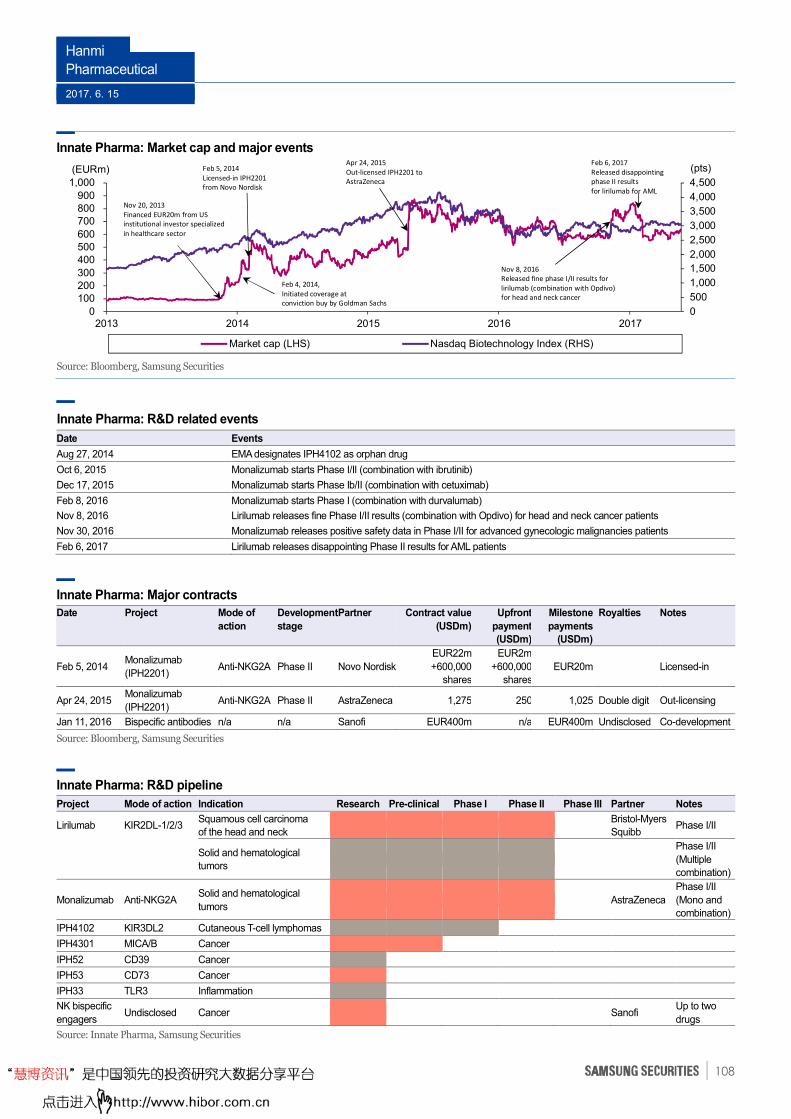

Korean players burst onto global scene via tie-ups with multinationals

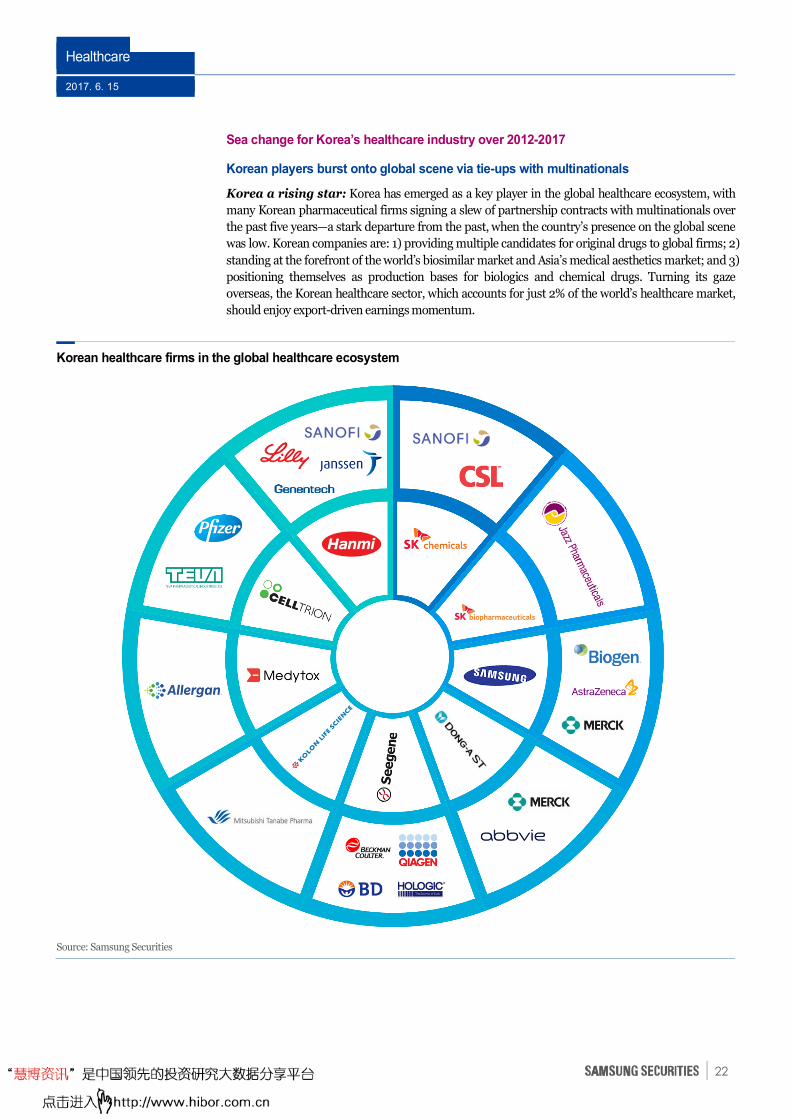

Korea a rising star: Korea has emerged as a key player in the global healthcare ecosystem, with

many Korean pharmaceutical firms signing a slew of partnership contracts with multinationals over

the past five years—a stark departure from the past, when the country’s presence on the global scene

was low. Korean companies are: 1) providing multiple candidates for original drugs to global firms; 2)

standing at the forefront of the world’s biosimilar market and Asia’s medical aesthetics market; and 3)

positioning themselves as production bases for biologics and chemical drugs. Turning its gaze

overseas, the Korean healthcare sector, which accounts for just 2% of the world’s healthcare market,

should enjoy export-driven earnings momentum.

Korean healthcare firms in the global healthcare ecosystem

Source: Samsung Securities

Healthcare

2017. 6. 15

23

Korean players out-license new drug candidates: To date, the US FDA has approved the

following Korean-made pharmaceuticals: 1) original chemical drugs by LG Life Sciences (Factive,

2003) and Donga ST (Sivextro, 2014); and 2) Afstyla biologics by SK Chemicals (2016). Most Korean

players out-license new drug candidates they discover, because: 1) the have limited capital for R&D; 2)

they lack experience in carrying out global clinical development; 3) they are unsure of the process of

gaining approval and handling health insurance providers and related authorities in developed

countries; or 4) they are weak on the marketing front. Donga ST in 2007 out-licensed Sivextro to

Trius Therapeutics, which was later acquired by Merck, which went on to commercialize the drug. SK

Chemicals’ Afstyla also hit the shelves after an out-licensing contract with CSL (Australia) in 2010.

Out-licensing contracts signed over 2013-2016: Medytox in Sep 2013 out-licensed Innotox,

the world’s first liquid botulinum toxin (BTX; a bio-better) to Allergan for USD362m. It granted

Allergan exclusive development and sales rights worldwide (save Korea and Japan). Over 2015-2016,

Hanmi Pharmaceutical agreed to export its technology for autoimmune therapy HM71224 to Eli Lilly

(in a deal worth USD690m), the Quantum Project (diabetes drugs) to Sanofi, diabetes and obesity

treatments HM12525A and JNJ-64565111 to Johnson & Johnson (USD9150m), and anti-cancer RAF

kinase inhibitor HM95573 to Genentech (USD910m). Kolon Life Science out-licensed Invossa, the

world’s first allogeneic cell therapy for degenerative arthritis, to Mitsubishi Tanabe for JPY45.7b in

2016. Donga ST in Dec 2016 said it had out-licensed DA-4501, a cancer immunotherapy candidate

targeting Mer TK, to AbbVie Biotechnology in a deal worth up to USD525m.

Healthcare

2017. 6. 15

24

Korean pharmaceutical and biologics players’ alliances

Date Exporter Importer Code/product Category Contract value Remarks

May 1997 LG Life Sciences GSK Factive Antibiotics Total: USD40.5m Cancelled in 2002, LGLS

launched the product by itself

Feb 2004 Pacific

Pharmaceuticals Schwarz PAC200030 Pain killer

Total: USD107.25m

Upfront fees: USD3.25m Stopped development

Jun 2005 Bukwang

Pharmaceutical Pharmasset

Clevudine

(Levovir)

Hepatitis

B treatment

Total: USD30m

Upfront fees: USD6m

Clinical trials stopped;

contract cancelled

Sep 2005 Ilyang

Pharmaceutical TAP

Ilaprazole

(Noltec) Antiulcer drugs

Total: USD44m

Upfront fees: USD3.5m

Phase III clinical trials

in US stopped

Feb 2007 Donga

Pharmaceutical Trius Sivextro Antibiotics

Total: USD17.2m

Royalties: 5-7% Launched globally

Nov 2007 LG Life Sciences Gilead Science LB84451 Liver disease

treatment

Total: USD200m

Upfront fees: USD20m Phase II clinical trials stopped

Dec 2008 Mezzion Warner Chilcott Udenafil

(Zydena)

Erectile dysfunction

treatment Total: USD69m Cancelled

Jun 2009 SK Chemicals CSL NBP601

(Afstyla) Hemophilia treatment n/a Launched globally

Dec 2012 Legochem Bio AstraZeneca n/a Cephalosporin

antibiotics

Total: USD140m

Upfront fees: USD2.45m Cancelled

Sep 2013 Medytox Allergan Innotox Botulinum toxin Total: USD362m

Upfront fees: USD65m

To start global Phase

III clinical trials in 2H17

Oct 2014 Olipass BMS PNA platform Gene therapy

platform n/a

Developed anti-sense gene

therapy (utilizing PNA platform)

Mar 2015 Hanmi Pharm Eli Lilly HM71224 BTK inhibitor Total: USD690m

Upfront fees: USD50m On Phase ll global clinical trials

Jul 2015 Hanmi Pharm Boehringer

Ingelheim HM61713

Molecular-targeted

cancer therapy

Total: USD730m

Upfront fees: USD50m Cancelled

Aug 2015 Legochem Bio Fosun ADC

technology

Molecular-targeted

cancer therapy Total: KRW20.8b

Signed exclusive out-licensing

deal for China

Oct 2015 Alteogen 3S Bio ADC

technology

Molecular-targeted

cancer therapy n/a

Signed exclusive out-licensing

deal for China

Oct 2015 Genexine Tasly 3 types

(incl. GX-H9) Fc-fusion protein

Total: KRW115

Upfront fees: KRW23b

Signed exclusive out-licensing

deal for China

Nov 2015 Hanmi Pharm Sanofi Quantum

project

Long-acting diabetes

treatment

Total: EUR3.9b

Upfront fees: EUR400m

To start Phase III global clinical

trials in 2H17

Nov 2015 Hanmi Pharm Johnson &

Johnson HM12525A

Diabetes/obesity

treatment

Total: USD920m

Upfront fees: USD110m

To start Phase II global clinical

trials in 2H17

Nov 2015 Hanmi Pharm ZAI Lab HM61713 Molecular-targeted

cancer therapy

Total: USD92m

Upfront fees: USD7m

Signed exclusive out-licensing

deal for China

Jan 2016 Chong Kun Dang Fuji Pharma CKD-11101 Nesp biosimilar n/a Signed exclusive out-licensing

deal for Japan

Feb 2016 Genexine Fosun GX-E2 Anemia treatment Total: USD44.5m

Upfront fees: USD2m

Signed exclusive out-licensing

deal for China

Feb 2016 Anterogen Ishin

Pharmaceutical

ALLO-ASC

-sheet

Diabetic foot ulcer

treatment

Total: USD75m

Upfront: USD1m

Signed exclusive out-licensing

deal for Japan and Taiwan

Apr 2016 Donga ST Tobira

Therapeutics DA-1229 NASH treatment Total: USD61.50m

Signed an out-licensing deal

exclusively for North America,

Europe and Australia

Jun 2016 Crystal Genomics Aptose

Biosciences CG026806

Acute myeloid

leukemia treatment

Total: KRW352.4b,

Upfront: KRW1.16b

Signed exclusive out-licensing

deal for Japan and Taiwan

Jul 2016 Yuhan Luoxin YH25448

Molecular-targeted

cancer therapy

for NSCLC

Total: USD120m

Upfront: USD6m

Signed exclusive out-licensing

deal for China, Hong Kong,

and Macao

Sep 2016 Ilyang

Pharmaceutical R-Pharm Noltec Antiulcer drugs Total: USd200m

Signed exclusive out-licensing

deal for Russia, Armenia,

and Belarus

Sep 2016 Hanmi Pharm Genentech HM95573 Molecular-targeted

cancer therapy

Total: USD910m

Upfront: USD80m Phase l in Korea (in progress)

Nov 2016 Kolon Life

Science

Mitsubishi Tanabe

Pharma Invossa

Degenerative arthritis

treatment

Total: KRW500b

Upfront fees: KRW27.3b

Signed exclusive out-licensing

deal for Japan

Dec 2016 Donga ST Abbvie

Biotechnology DA-4501

Immuno-oncology

therapy

Total: USD525m

Upfront fees: USD40m

Still in drug candidate discovery

phase

Source: Local press, Company data, Samsung Securities

Healthcare

2017. 6. 15

25

Korean biosimilar developers leading the way

Biologics turn to trade surplus for first time in 2015: Korea’s pharmaceutical market

shrank a touch in 2015, creeping down 0.7% y-y to KRW19.1b, with production, exports, and imports

up 3.4%, 31.1%, and 1.9% y-y, respectively, to KRW17t, KRW3.3t, and KRW5.6t. Meanwhile, Korea’s

biologics market contracted a sharp 17.3% y-y to KRW1.64t, with production and exports rising 2.3%

and 47.7% y-y, respectively, to KRW1.72t and KRW815.7b, and imports falling 9.5% y-y to

KRW835.3b. The biologics market accounted for 8.5% of the nation’s pharmaceutical market

(down 1.7%pts y-y), while biologics production, exports, and imports represented a respective 10.1%,

27.5% and 14.9% (down 0.1%pts, up 3.1%pts, and down 1.9%pts y-y). The nation’s biologics industry

suffered a trade deficits before turning to its first-ever surplus in 2015. Backed by solid growth in

biologics exports, the pharmaceutical trade deficit also declined rapidly.

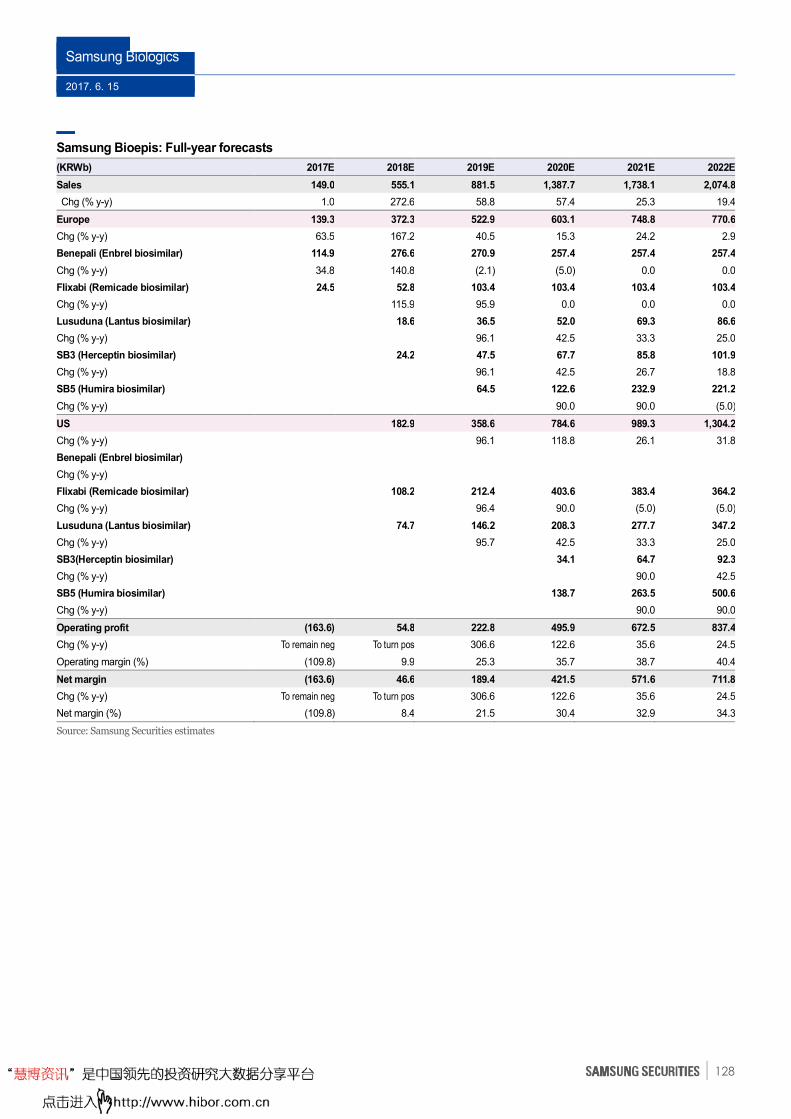

Korea’s biosimilar exports to top KRW1t in 2017: Korea’s combined biosimilar exports

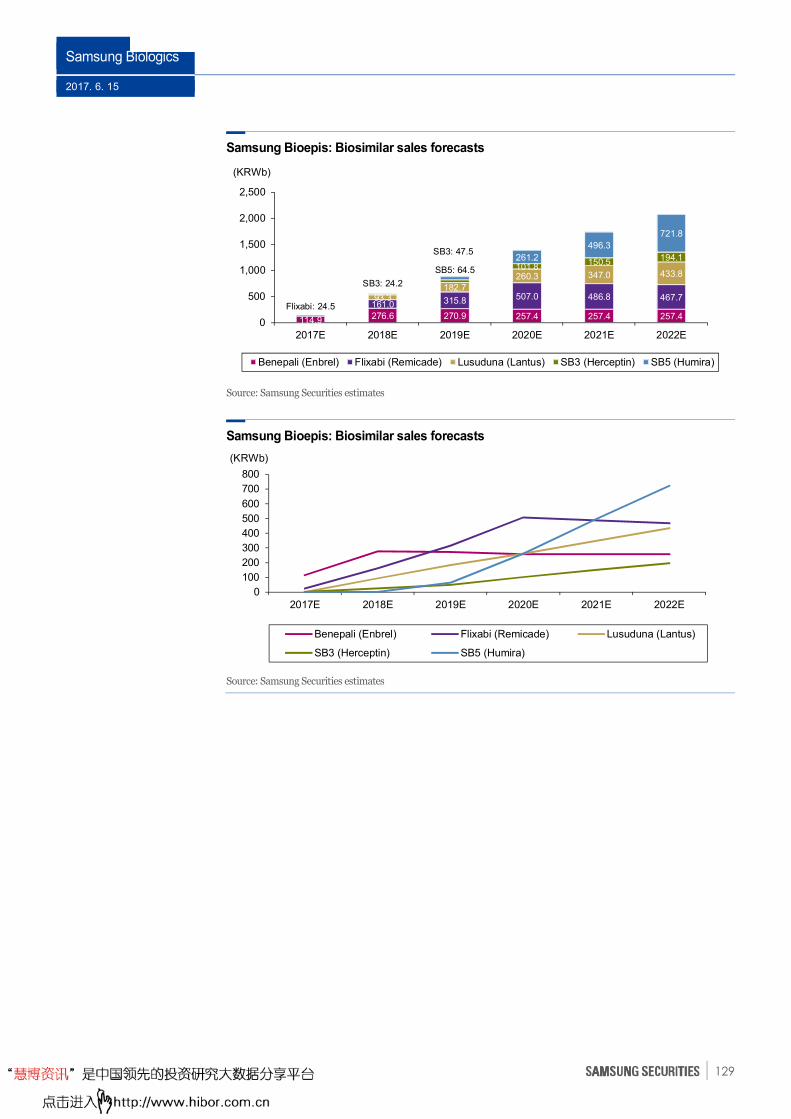

climbed 112.3% y-y to KRW905.2b in 2016, which figure includes consolidated sales from Celltrion

Healthcare (up 88.3% y-y to KRW757.7b) and Samsung Bioepis (up 517% y-y to KRW147.5b).

According to PR Newswire, Celltrion Healthcare’s Remsima (a Remicade biosimilar) and Samsung

Bioepis’ Benepali (an Enbrel biosimilar) boast volume-based market shares of 40% and 25%,

respectively, in Europe. Celltrion’s partner, Pfizer, announced that 1Q sales of Remsima leapt 116.7%

y-y to USD78m. Remsima is called Inflectra in the US. Samsung Bioepis’s partner, Biogen, said 1Q

sales of Benepali skyrocketed 3,200% y-y to USD66m. Celltrion Healthcare launched Inflectra in the

US on Dec 5, 2016 and plan to release Rituxan biosimilar Truxima in Europe soon. Samsung Bioepis

is planning a US launch for Remicade biosimilar Flixabi (Renflexis in Korea) and an European

launch for Lantus biosimilar Lusduna. Accordingly, Korea’s biosimilar exports (including those of

Celltrion Healthcare and Samsung Bioepis) should exceed KRW1t in 2017.

Healthcare

2017. 6. 15

26

Pfizer (Hospira): Remsima/Inflectra quarterly sales Biogen: Benepali quarterly sales

Note: Pfizer (Hospira) has exclusive marketing rights for Remsima/

Inflectra in the US and some parts of Europe

Source: Company data, Samsung Securities

Source: Company data, Samsung Securities

Remsima/Inflectra: Market share in Europe Benepali: Market share in Europe

Note: Volume-based

Source: PR Newswire, Samsung Securities

Note: Volume-based

Source: PR Newswire, Samsung Securities

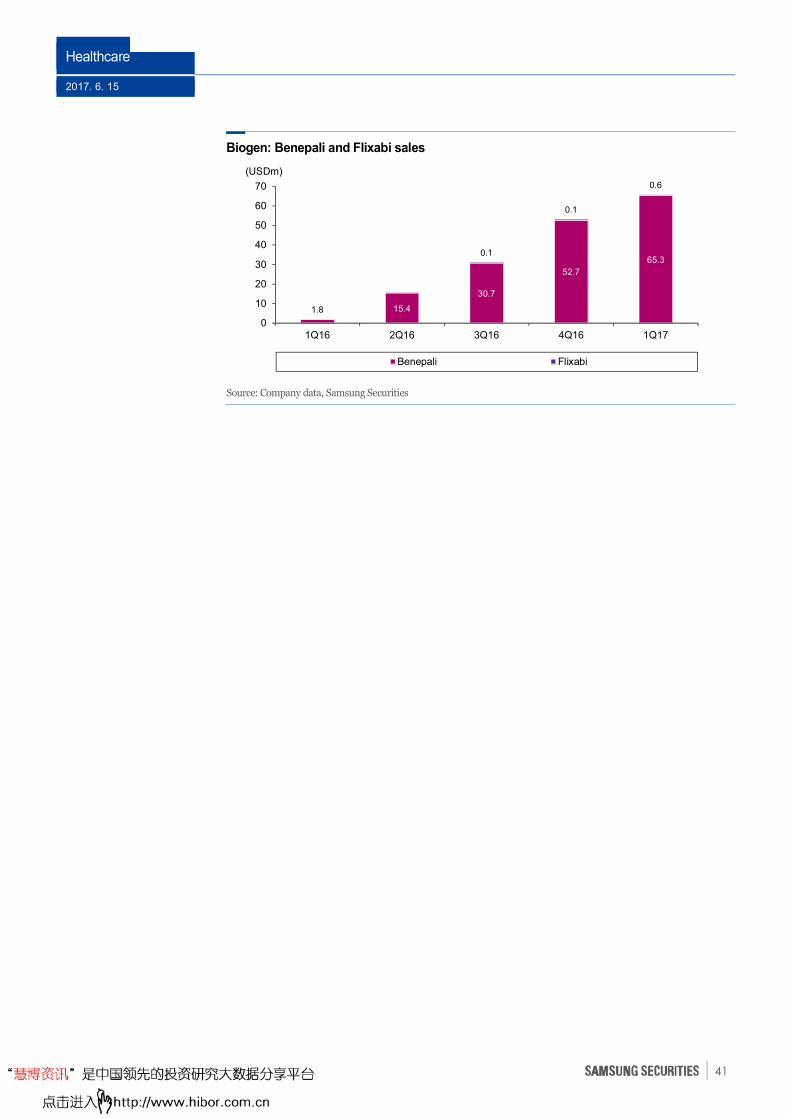

Celltrion Healthcare and Samsung Bioepis: Annual sales

Source: Company data, Samsung Securities

3036

40

5561

78

0

10

20

30

40

50

60

70

80

90

4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

(USDm)

1.8

15.4

30.7

52.7

65.3

0

10

20

30

40

50

60

70

1Q16 2Q16 3Q16 4Q16 1Q17

(USDm)

Remsima/Inflectra:

40%

Remicade:60%

Benepali:25%

Enbrel:75%

34 145 165

402

758

44

76

24

147

0100200300400500600700800900

1,000

2012 2013 2014 2015 2016

Celltrion Healthcare Samsung Bioepis

(KRWb)

Healthcare

2017. 6. 15

27

Korean medical-aesthetic firms penetrate global BTX and filler markets

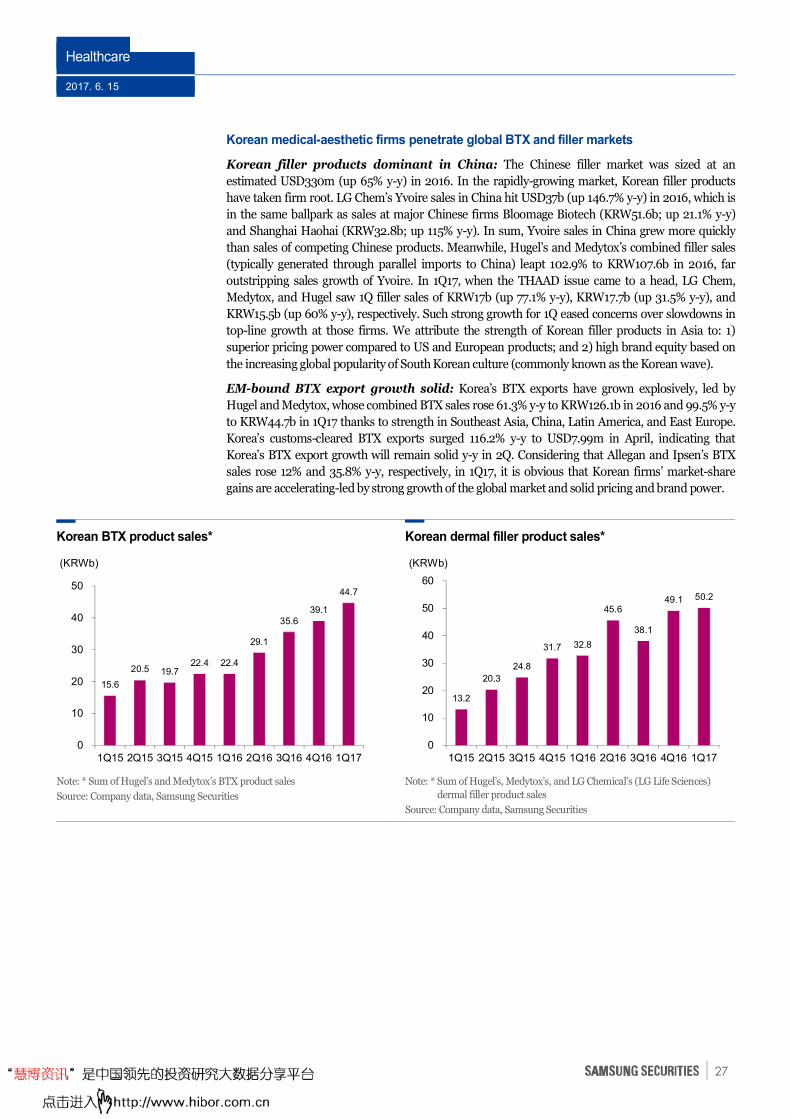

Korean filler products dominant in China: The Chinese filler market was sized at an

estimated USD330m (up 65% y-y) in 2016. In the rapidly-growing market, Korean filler products

have taken firm root. LG Chem’s Yvoire sales in China hit USD37b (up 146.7% y-y) in 2016, which is

in the same ballpark as sales at major Chinese firms Bloomage Biotech (KRW51.6b; up 21.1% y-y)

and Shanghai Haohai (KRW32.8b; up 115% y-y). In sum, Yvoire sales in China grew more quickly

than sales of competing Chinese products. Meanwhile, Hugel’s and Medytox’s combined filler sales

(typically generated through parallel imports to China) leapt 102.9% to KRW107.6b in 2016, far

outstripping sales growth of Yvoire. In 1Q17, when the THAAD issue came to a head, LG Chem,

Medytox, and Hugel saw 1Q filler sales of KRW17b (up 77.1% y-y), KRW17.7b (up 31.5% y-y), and

KRW15.5b (up 60% y-y), respectively. Such strong growth for 1Q eased concerns over slowdowns in

top-line growth at those firms. We attribute the strength of Korean filler products in Asia to: 1)

superior pricing power compared to US and European products; and 2) high brand equity based on

the increasing global popularity of South Korean culture (commonly known as the Korean wave).

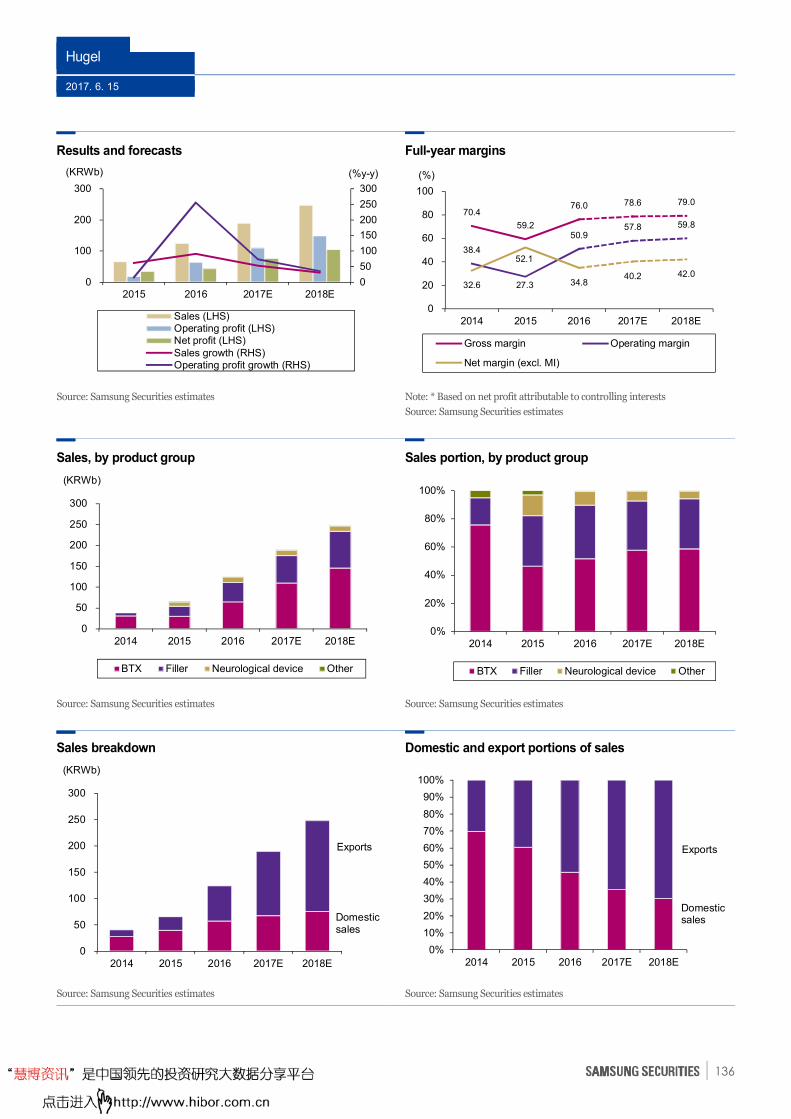

EM-bound BTX export growth solid: Korea’s BTX exports have grown explosively, led by

Hugel and Medytox, whose combined BTX sales rose 61.3% y-y to KRW126.1b in 2016 and 99.5% y-y

to KRW44.7b in 1Q17 thanks to strength in Southeast Asia, China, Latin America, and East Europe.

Korea’s customs-cleared BTX exports surged 116.2% y-y to USD7.99m in April, indicating that

Korea’s BTX export growth will remain solid y-y in 2Q. Considering that Allegan and Ipsen’s BTX

sales rose 12% and 35.8% y-y, respectively, in 1Q17, it is obvious that Korean firms’ market-share

gains are accelerating-led by strong growth of the global market and solid pricing and brand power.

Korean BTX product sales* Korean dermal filler product sales*

Note: * Sum of Hugel’s and Medytox’s BTX product sales

Source: Company data, Samsung Securities

Note: * Sum of Hugel’s, Medytox’s, and LG Chemical’s (LG Life Sciences)

dermal filler product sales

Source: Company data, Samsung Securities

15.6

20.5 19.7 22.4 22.4

29.1

35.6 39.1

44.7

0

10

20

30

40

50

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

(KRWb)

13.2

20.3

24.8

31.7 32.8

45.6

38.1

49.1 50.2

0

10

20

30

40

50

60

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

(KRWb)

Healthcare

2017. 6. 15

28

Korean firms to lead global biologics CMO and chemical-drug CMS markets

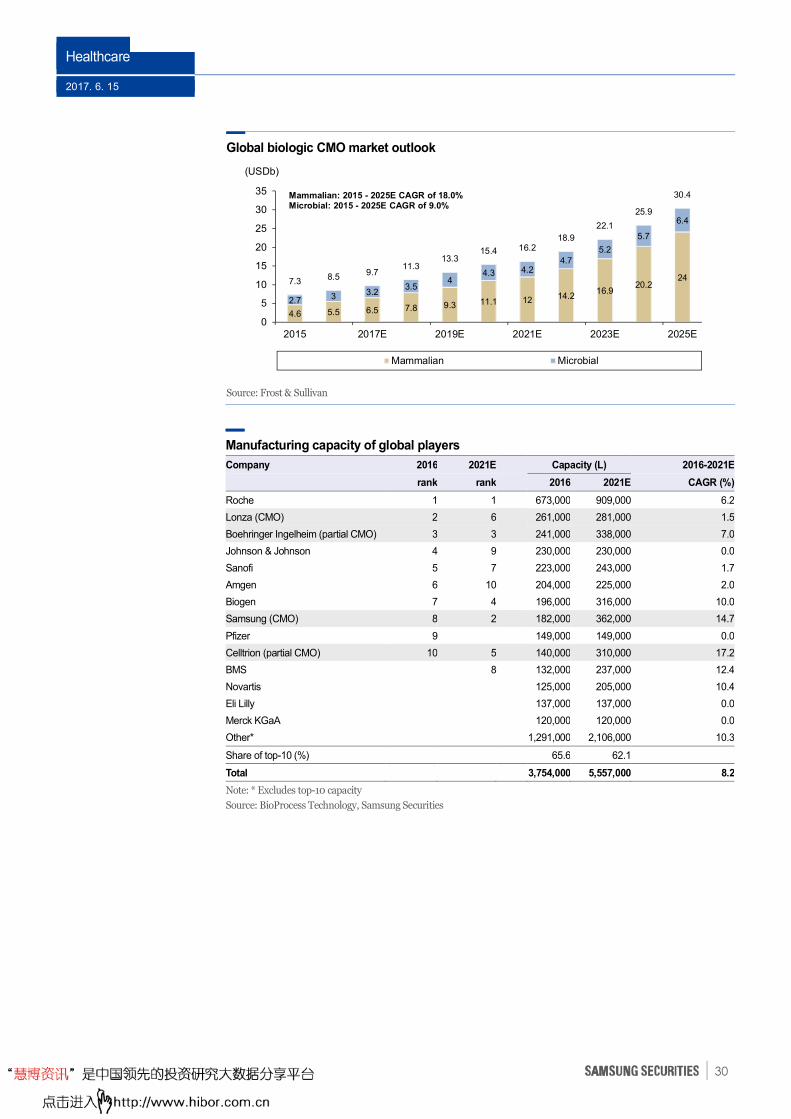

Global market for contracted manufacturing growing: The global market for chemical-

drug contract manufacturing services (CMS) is projected to grow at a 2015-2020 CAGR of 6.3% to

USD84b as pharmaceutical firms increasing outsource manufacturing as they strive to improve cost

competitiveness and amid rising demand for selective manufacturing technology. The global market

for biologics contract manufacturing organizations (CMOs) should grow at a 2015-2025 CAGR of 15.1%

to USD30.3b given the needs for capacity management, cost savings, risk control, rapid production,

and efficient use of resources.

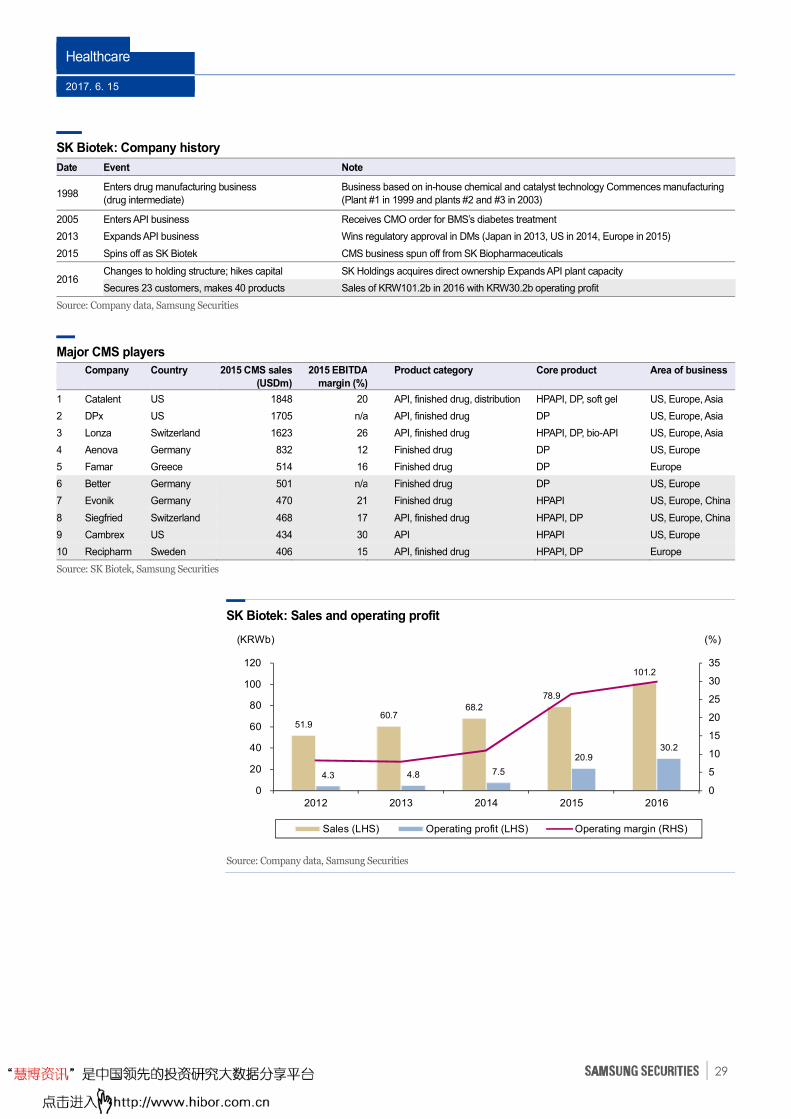

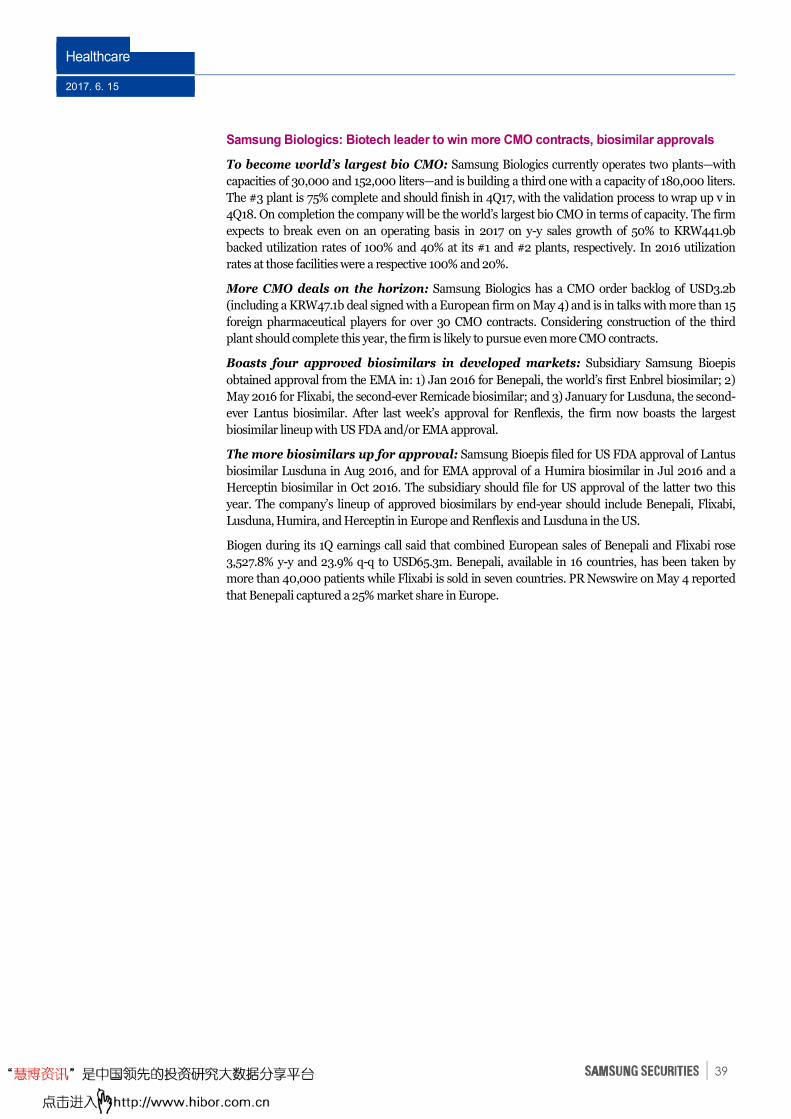

Korea potentially home to a global top-ten CMS and the top CMO: SK Biotek entered the

CMS business in 1998 and was incorporated as an SK Group subsidiary in 2016 after being spun off

from SK Biopharmaceuticals in 2015. SK Biotek has accumulated a wide range of experience and

knowhow thanks to its group’s five decades of operating refineries and petrochemicals facilities. Of

note is the firm’s ability to meet customer demand for high-tech manufacturing, backed by its world-

class technology in continuous organic synthesis and systems that enable it to make over 50 types of

chemical synthesis technology. The firm’s factory in Daeduk has an annual production capacity of

158m cubic meters, while its factory in Sejong will open this year with a capacity of 318m cubic

meters, and this latter should rise to 798

m in 2020. Meanwhile, Samsung Biologics is Samsung Group’s biotech holding company established

in 2011 as a subsidiary of Samsung C&T and Samsung Electronics. Samsung Biologics is expanding

capacity efficiently by leveraging the group’s: 1) competitiveness in design, engineering, procurement,

construction, and validation (DEPC-V); and 2) ability to construct plant and install equipment

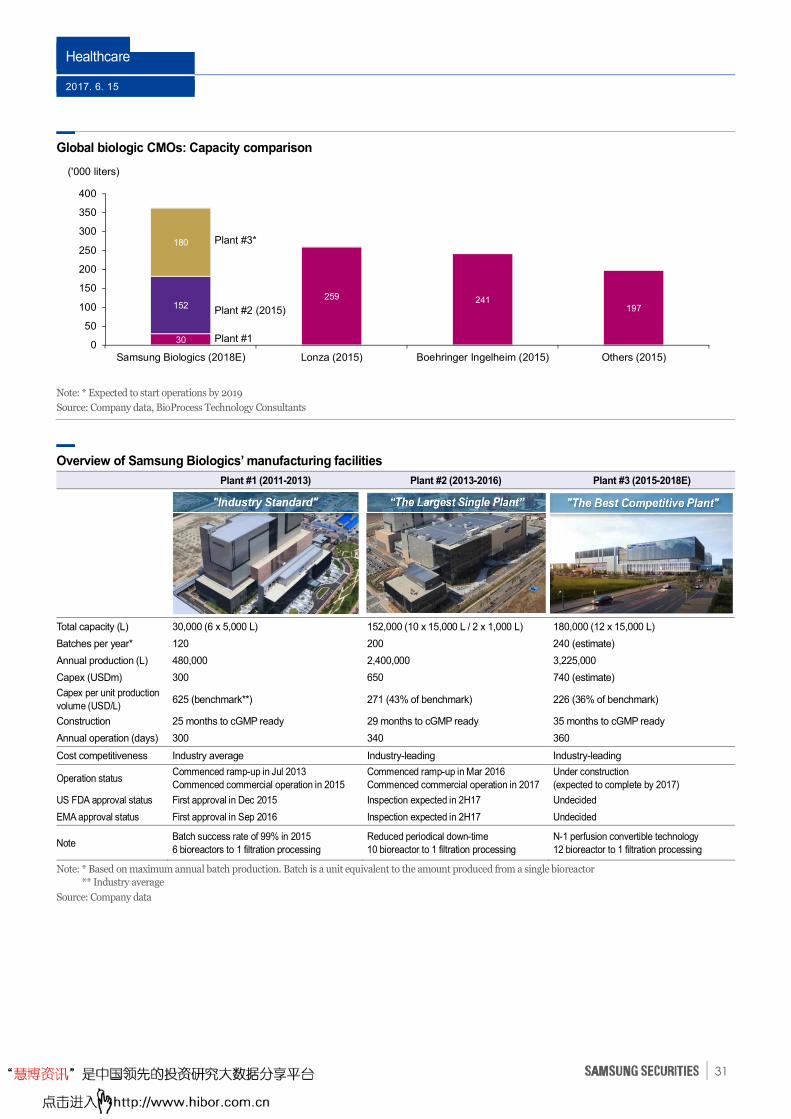

concurrently (based on its experience in the semiconductor industry). Swiss firm Lonza currently has

the world’s largest bio-CMO capacity at 259,000 liters, followed by Boehringer Ingelheim’s 241,000

liters and Samsung Biologics’ 182,000 liters. By 2018, however, Samsung Biologics should top the list

with 362,000 liters of capacity, followed by Boehringer Ingelheim’s 319,000 liters and Lonza’s

265,000 liters.

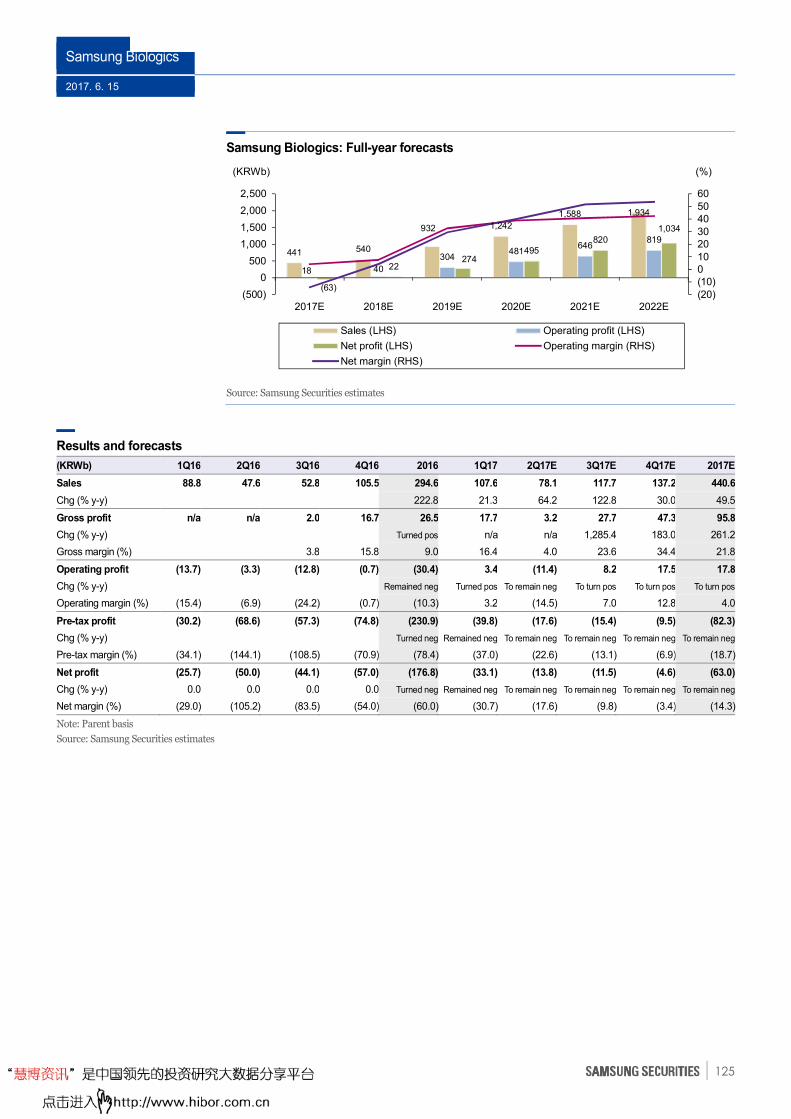

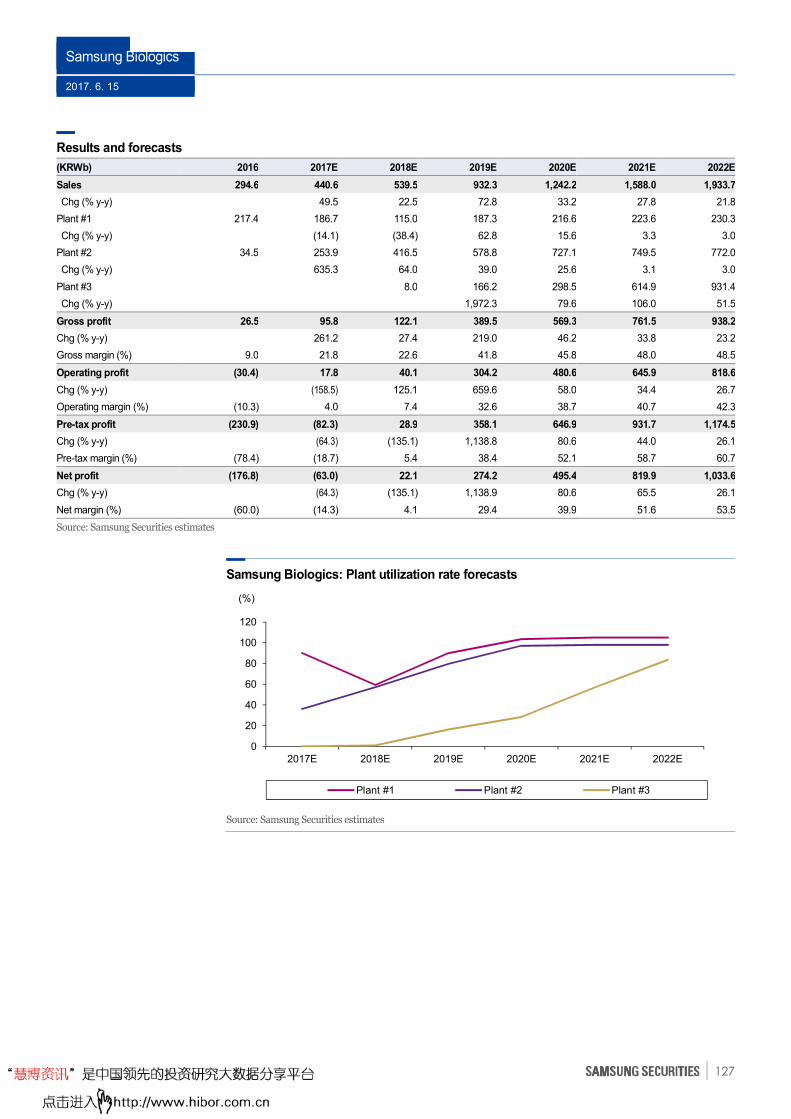

SK Biotek and Samsung Biologics pursuing ambitious 2020 targets: SK Biotek in 2016

posted sales of KRW97.1b (up 52.5% y-y) and an operating profit of KRW28.1b (up 80.1% y-y) for a

margin of 29% (up 4.4% pts y-y). The company’s 2020 vision is to become a global top-ten CMS

player with KRW1.5t in sales, KRW300b in operating profit, and an operating margin of 20%. IT will

pursue this by: 1) strengthening its competitiveness via domestic capacity expansions; and 2) seeking

M&A opportunities to rapidly secure capabilities. Samsung Biologics last year posted another

operating loss, this time to the tune of KRW30.4b on parent-based sales of KRW294.6b (up 337.3%

y-y). The company aims to be the world’s top bio-CMO player by 2020, with sales of KRW1t, an

operating profit of KRW400b, and an operating margin of 40%. The company currently has nine

CMO contracts totaling USD3.2b with six multinational pharmaceutical and biotechnology firms. It

is also negotiating with 15 such firms over around 30 biologics.

Healthcare

2017. 6. 15

29

SK Biotek: Company history

Date Event Note

1998 Enters drug manufacturing business

(drug intermediate)

Business based on in-house chemical and catalyst technology Commences manufacturing

(Plant #1 in 1999 and plants #2 and #3 in 2003)

2005 Enters API business Receives CMO order for BMS’s diabetes treatment

2013 Expands API business Wins regulatory approval in DMs (Japan in 2013, US in 2014, Europe in 2015)

2015 Spins off as SK Biotek CMS business spun off from SK Biopharmaceuticals

2016 Changes to holding structure; hikes capital SK Holdings acquires direct ownership Expands API plant capacity

Secures 23 customers, makes 40 products Sales of KRW101.2b in 2016 with KRW30.2b operating profit

Source: Company data, Samsung Securities

Major CMS players

Company

Country

2015 CMS sales

(USDm)

2015 EBITDA

margin (%)

Product category

Core product

Area of business

1 Catalent US 1848 20 API, finished drug, distribution HPAPI, DP, soft gel US, Europe, Asia

2 DPx US 1705 n/a API, finished drug DP US, Europe, Asia

3 Lonza Switzerland 1623 26 API, finished drug HPAPI, DP, bio-API US, Europe, Asia

4 Aenova Germany 832 12 Finished drug DP US, Europe

5 Famar Greece 514 16 Finished drug DP Europe

6 Better Germany 501 n/a Finished drug DP US, Europe

7 Evonik Germany 470 21 Finished drug HPAPI US, Europe, China

8 Siegfried Switzerland 468 17 API, finished drug HPAPI, DP US, Europe, China

9 Cambrex US 434 30 API HPAPI US, Europe

10 Recipharm Sweden 406 15 API, finished drug HPAPI, DP Europe

Source: SK Biotek, Samsung Securities

SK Biotek: Sales and operating profit

Source: Company data, Samsung Securities

51.9 60.7

68.2

78.9

101.2

4.3 4.8 7.5

20.9 30.2

0

5

10

15

20

25

30

35

0

20

40

60

80

100

120

2012 2013 2014 2015 2016

Sales (LHS) Operating profit (LHS) Operating margin (RHS)

(KRWb) (%)

Healthcare

2017. 6. 15

30

Global biologic CMO market outlook

Source: Frost & Sullivan

Manufacturing capacity of global players

Company 2016 2021E Capacity (L) 2016-2021E

rank rank 2016 2021E CAGR (%)

Roche 1 1 673,000 909,000 6.2

Lonza (CMO) 2 6 261,000 281,000 1.5

Boehringer Ingelheim (partial CMO) 3 3 241,000 338,000 7.0

Johnson & Johnson 4 9 230,000 230,000 0.0

Sanofi 5 7 223,000 243,000 1.7

Amgen 6 10 204,000 225,000 2.0

Biogen 7 4 196,000 316,000 10.0

Samsung (CMO) 8 2 182,000 362,000 14.7

Pfizer 9 149,000 149,000 0.0

Celltrion (partial CMO) 10 5 140,000 310,000 17.2

BMS 8 132,000 237,000 12.4

Novartis 125,000 205,000 10.4

Eli Lilly 137,000 137,000 0.0

Merck KGaA 120,000 120,000 0.0

Other* 1,291,000 2,106,000 10.3

Share of top-10 (%) 65.6 62.1

Total 3,754,000 5,557,000 8.2

Note: * Excludes top-10 capacity

Source: BioProcess Technology, Samsung Securities

4.6 5.5 6.5 7.8 9.3 11.1 12 14.216.9

20.224

2.7 3 3.23.5

44.3 4.2

4.75.2

5.7

6.4

7.38.5

9.711.3

13.315.4 16.2

18.9

22.1

25.9

30.4

0

5

10

15

20

25

30

35

2015 2017E 2019E 2021E 2023E 2025E

Mammalian Microbial

(USDb)

Mammalian: 2015 - 2025E CAGR of 18.0%Microbial: 2015 - 2025E CAGR of 9.0%

Healthcare

2017. 6. 15

31

Global biologic CMOs: Capacity comparison

Note: * Expected to start operations by 2019

Source: Company data, BioProcess Technology Consultants

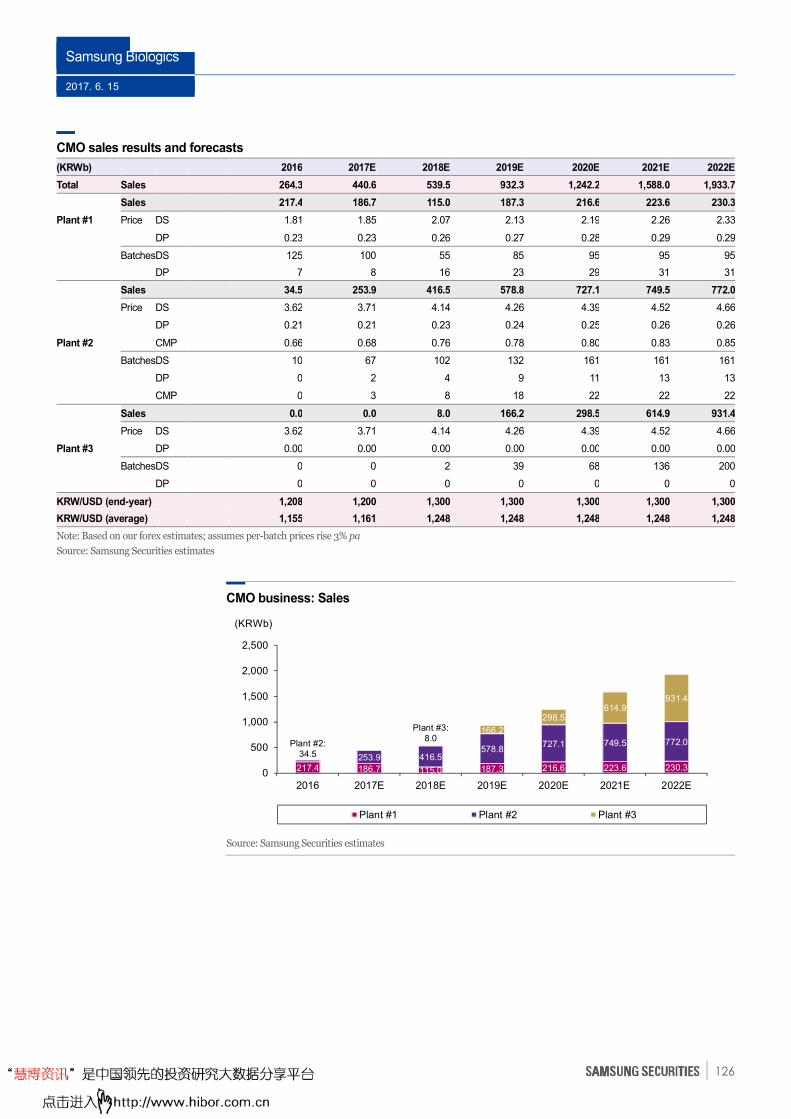

Overview of Samsung Biologics’ manufacturing facilities

Plant #1 (2011-2013) Plant #2 (2013-2016) Plant #3 (2015-2018E)

Total capacity (L) 30,000 (6 x 5,000 L) 152,000 (10 x 15,000 L / 2 x 1,000 L) 180,000 (12 x 15,000 L)

Batches per year* 120 200 240 (estimate)

Annual production (L) 480,000 2,400,000 3,225,000

Capex (USDm) 300 650 740 (estimate)

Capex per unit production

volume (USD/L) 625 (benchmark**) 271 (43% of benchmark) 226 (36% of benchmark)

Construction 25 months to cGMP ready 29 months to cGMP ready 35 months to cGMP ready

Annual operation (days) 300 340 360

Cost competitiveness Industry average Industry-leading Industry-leading

Operation status Commenced ramp-up in Jul 2013

Commenced commercial operation in 2015

Commenced ramp-up in Mar 2016

Commenced commercial operation in 2017

Under construction

(expected to complete by 2017)

US FDA approval status First approval in Dec 2015 Inspection expected in 2H17 Undecided

EMA approval status First approval in Sep 2016 Inspection expected in 2H17 Undecided

Note Batch success rate of 99% in 2015

6 bioreactors to 1 filtration processing

Reduced periodical down-time

10 bioreactor to 1 filtration processing

N-1 perfusion convertible technology

12 bioreactor to 1 filtration processing

Note: * Based on maximum annual batch production. Batch is a unit equivalent to the amount produced from a single bioreactor

** Industry average

Source: Company data

30

259 241197152

180

0

50

100

150

200

250

300

350

400

Samsung Biologics (2018E) Lonza (2015) Boehringer Ingelheim (2015) Others (2015)

('000 liters)

Plant #3*

Plant #2 (2015)

Plant #1

Healthcare

2017. 6. 15

32

Visible progress to be made on R&D and B2B fronts

Firms with R&D or B2B deals with multinationals warrant attention

Uncertainties to ease in 2H: As stated, Hanmi Pharmaceutical, Medytox, and Seegene gained

global recognition over 2013-2016 for their out-licensing and ODM supply contracts with global

pharmaceutical companies. Yet, slow R&D progress by the global firms and delays in ODM

shipments have raised concerns over contract cancellations. In 2H, we expect Hanmi and Medytox to

move to the next phase of development and Seegene to start ODM shipments. Indeed, expectations

should supplant concerns and lead to the market to reevaluate Korean firms’ R&D capabilities.

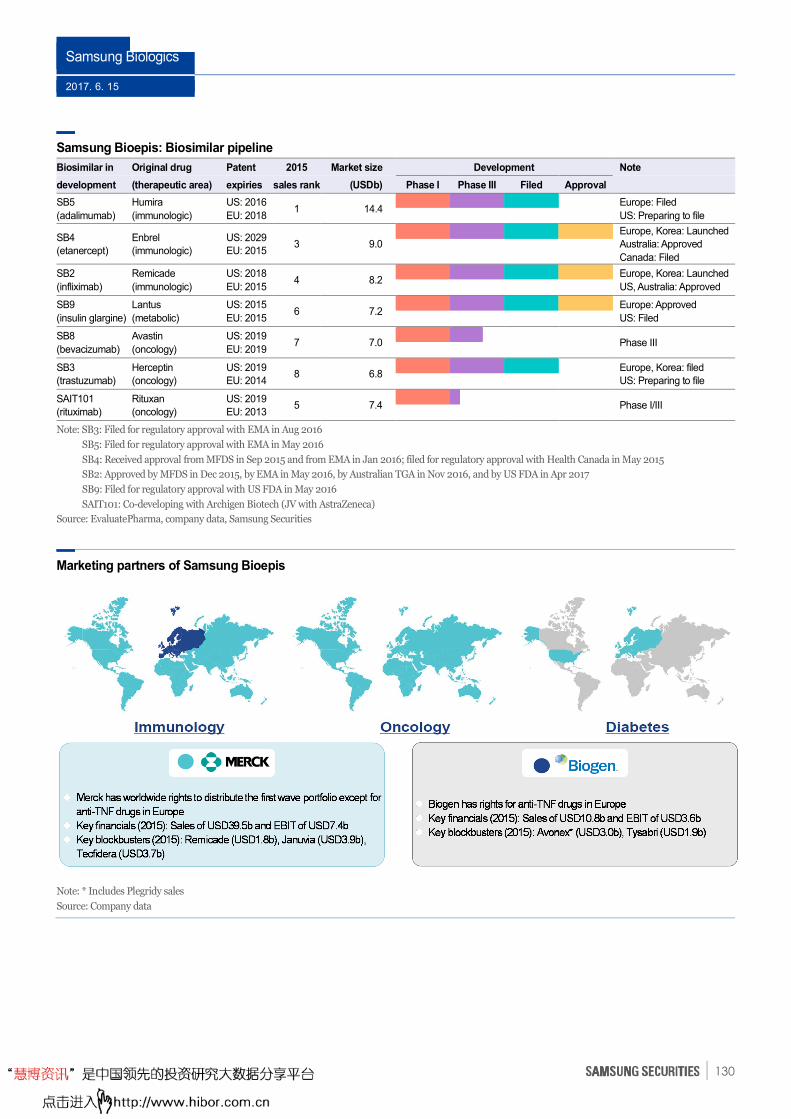

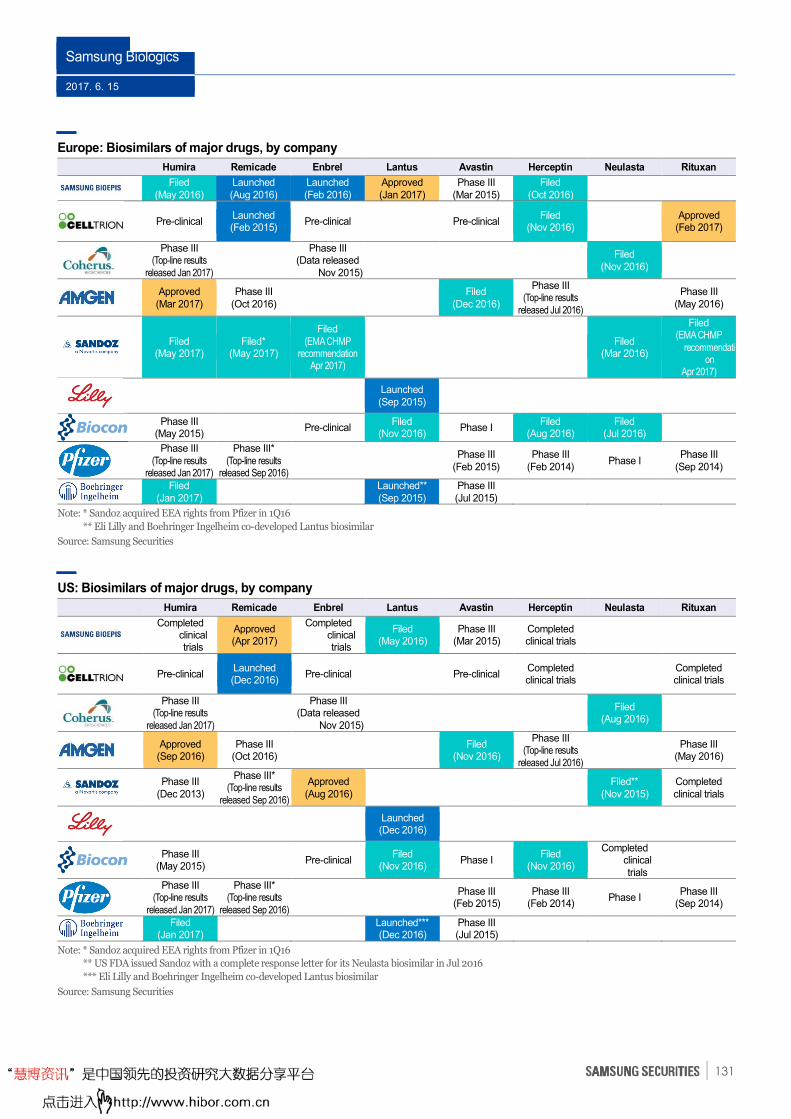

Multiple drugs up for US, European approval: Samsung Bioepis and Celltrion filed for FDA

and EMA approval of multiple biosimilars in 2016 and expect to obtain them in 2H. Also in 2H: 1)

Green Cross should reapply for US approval of its immunodeficiency drug IVIG, which was shelved

in 2016 after an FDA review; and 2) SK Biopharmaceuticals plans to file for US approval of its

epilepsy drug Cenobamate and sleep disorder drug SKL-N05/JZP-110.

R&D to regain momentum, influence shares: Sentiment on the healthcare sector soured in

late 2016 on the cancellation or revision of some of Hanmi’s out-licensing contracts, and investors

lost interest in the sector in 1H17 for a lack of R&D momentum. In 2H17, however, the sector should

show visible R&D progress, resume ODM shipments, and receive US and European approvals for

multiple drugs, boosting sentiment and making R&D a key share-price determinant once again.

Contents

1H review: Poverty in the midst of plenty

p2

Pharmaceutical market outlook

p7

Visible progress to be made on R&D and B2B fronts

p32

Government policy warrants attention

p52

Key issues in 2H p68

Solid earnings momentum in 2H

p87

Company p105

Healthcare

2017. 6. 15

33

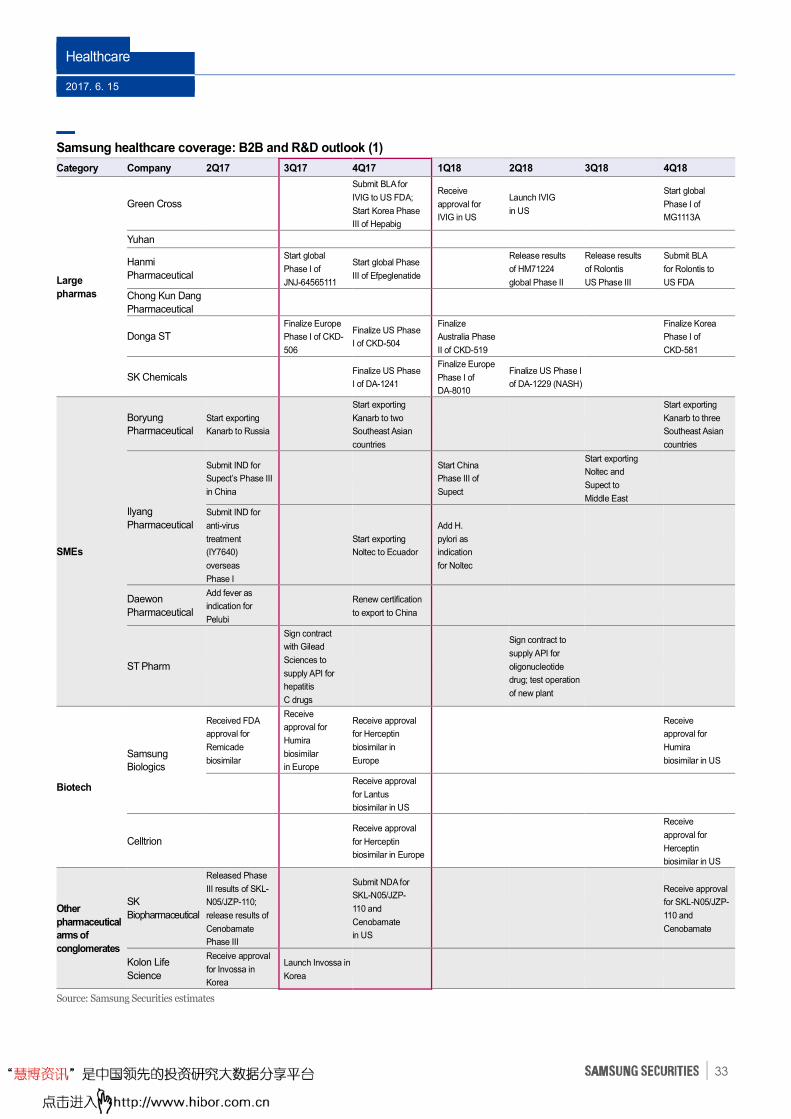

Samsung healthcare coverage: B2B and R&D outlook (1)

Category Company 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

Large

pharmas

Green Cross

Submit BLA for

IVIG to US FDA;

Start Korea Phase

III of Hepabig

Receive

approval for

IVIG in US

Launch IVIG

in US

Start global

Phase I of

MG1113A

Yuhan

Hanmi

Pharmaceutical

Start global

Phase I of

JNJ-64565111

Start global Phase

III of Efpeglenatide

Release results

of HM71224

global Phase II

Release results

of Rolontis

US Phase III

Submit BLA

for Rolontis to

US FDA

Chong Kun Dang

Pharmaceutical

Donga ST

Finalize Europe

Phase I of CKD-

506

Finalize US Phase

I of CKD-504

Finalize

Australia Phase

II of CKD-519

Finalize Korea

Phase I of

CKD-581

SK Chemicals Finalize US Phase

I of DA-1241

Finalize Europe

Phase I of

DA-8010

Finalize US Phase I

of DA-1229 (NASH)

SMEs

Boryung

Pharmaceutical

Start exporting

Kanarb to Russia

Start exporting

Kanarb to two

Southeast Asian

countries

Start exporting

Kanarb to three

Southeast Asian

countries

Ilyang

Pharmaceutical

Submit IND for

Supect’s Phase III

in China

Start China

Phase III of

Supect

Start exporting

Noltec and

Supect to

Middle East

Submit IND for

anti-virus

treatment

(IY7640)

overseas

Phase I

Start exporting

Noltec to Ecuador

Add H.

pylori as

indication

for Noltec

Daewon

Pharmaceutical

Add fever as

indication for

Pelubi

Renew certification

to export to China

ST Pharm

Sign contract

with Gilead

Sciences to

supply API for

hepatitis

C drugs

Sign contract to

supply API for

oligonucleotide

drug; test operation

of new plant

Biotech

Samsung

Biologics

Received FDA

approval for

Remicade

biosimilar

Receive

approval for

Humira

biosimilar

in Europe

Receive approval

for Herceptin

biosimilar in

Europe

Receive

approval for

Humira

biosimilar in US

Receive approval

for Lantus

biosimilar in US

Celltrion

Receive approval

for Herceptin

biosimilar in Europe

Receive

approval for

Herceptin

biosimilar in US

Other

pharmaceutical

arms of

conglomerates

SK

Biopharmaceutical

Released Phase

III results of SKL-

N05/JZP-110;

release results of

Cenobamate

Phase III

Submit NDA for

SKL-N05/JZP-

110 and

Cenobamate

in US

Receive approval

for SKL-N05/JZP-

110 and

Cenobamate

Kolon Life

Science

Receive approval

for Invossa in

Korea

Launch Invossa in

Korea

Source: Samsung Securities estimates

Healthcare

2017. 6. 15

34

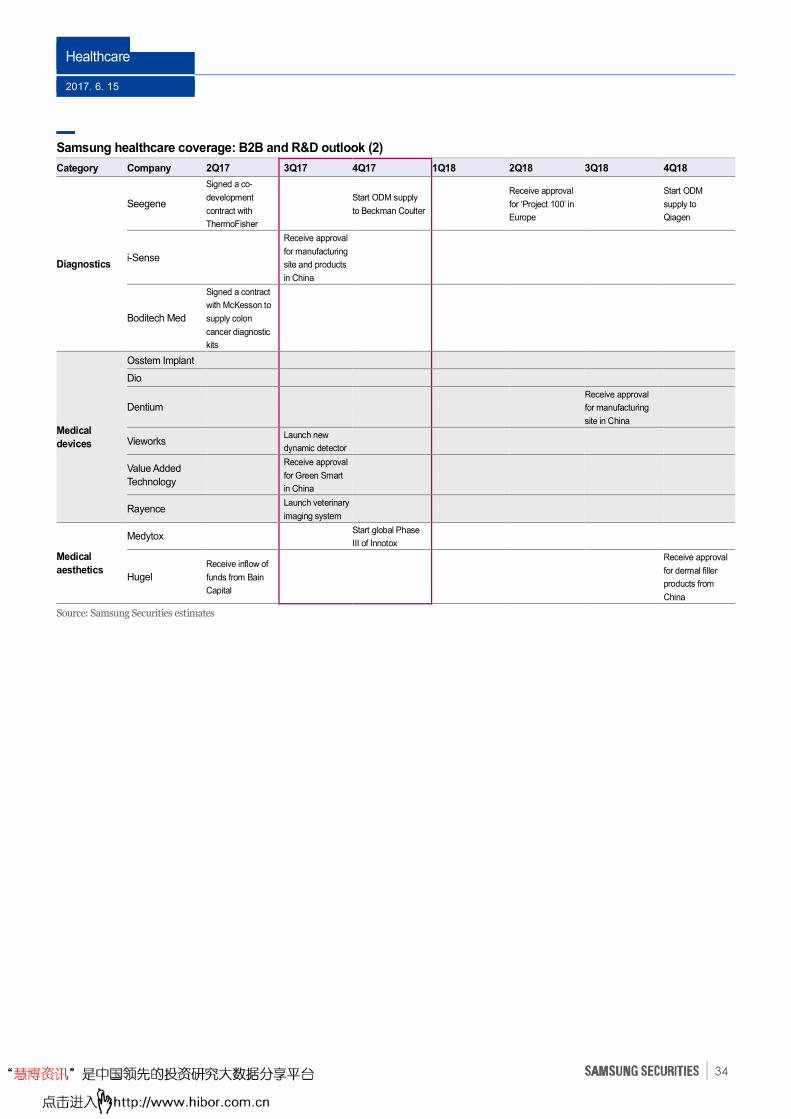

Samsung healthcare coverage: B2B and R&D outlook (2)

Category Company 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

Diagnostics

Seegene

Signed a co-

development

contract with

ThermoFisher

Start ODM supply

to Beckman Coulter

Receive approval

for ‘Project 100’ in

Europe

Start ODM

supply to

Qiagen

i-Sense

Receive approval

for manufacturing

site and products

in China

Boditech Med

Signed a contract

with McKesson to

supply colon