Embed Size (px)

Citation preview

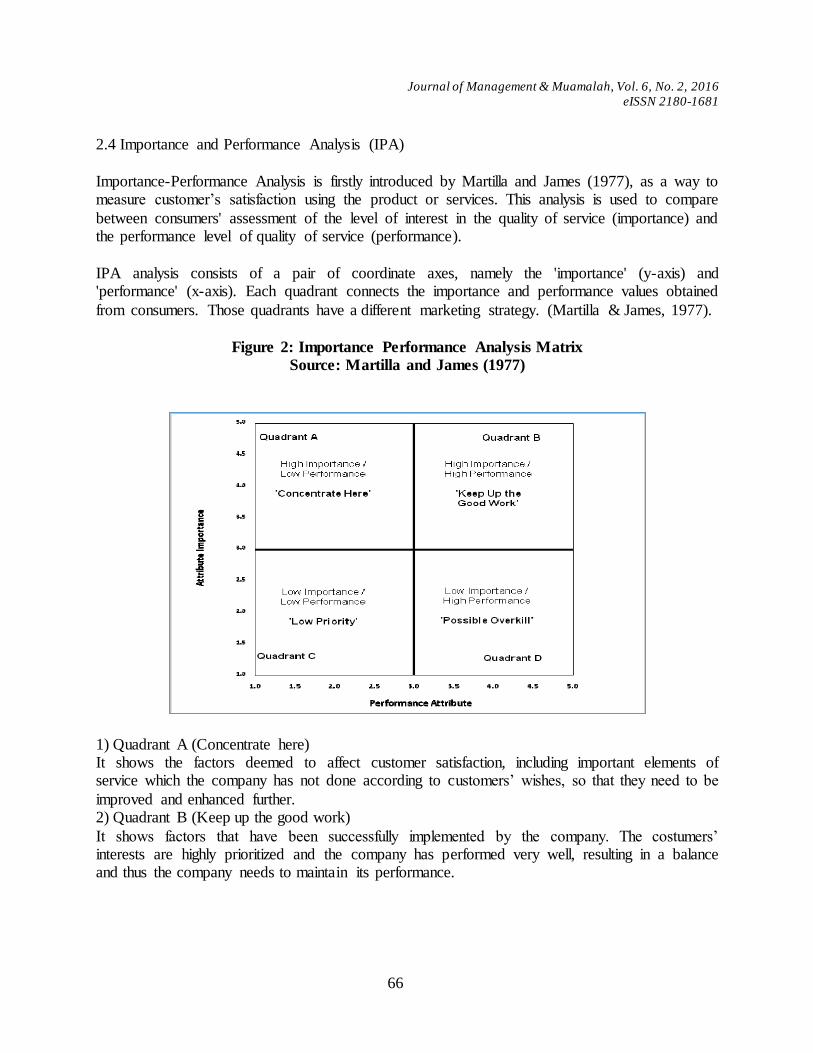

Journal of Management & Muamalah Jurnal Pengurusan & Muamalah

eISSN 2180-1681

EDITORIAL BOARD/ SIDANG EDITOR

Chief Editor / Ketua Editor Dr. SARIFAH ISMAIL

Managing Editor / Editor Pengurusan

NORFAEZAH OTHMAN NOR SUHAILY BAKAR

Executive Editor / Editor Kerja

NURNADDIA NORDIN NOR AZLA ABDUL WAHAB

Editor / Editor

NOR AIMI MUHAMAD PUAD FADILAH MAT NOR

ZAINAB AMAN RAJ ZAHID ELLEY

Secretary / Setiausaha

JUNAINAH IDRIS

Editorial Advisory Board / Sidang Penasihat Editorial DR. NOR HAKIMAH MOHD NOR

DR. NORZALINA ZAINUDIN DR. FARADILLAH IQMAR OMAR

DR. MAWAR MURNI YUNUS DR. NORMAZAINI SALEH DR. NORZIAH OTHMAN

Special thanks to all involved in the publication of this journal. Sidang Editor merakamkan ucapan jutaan terima kasih kepada semua yang terlibat

dalam menjayakan penerbitan jurnal ini.

Views expressed in this journal are not necessarily reflect views of the editor or publisher. Authors are fully responsible towards their articles.

Artikel yang diterbitkan tidak semestinya mewakili pandangan editor atau penerbit. Para penulis bertanggungjawab sepenuhnya terhadap artikel dan tulisannya.

Published by/Diterbitkan oleh:

Faculty of Management & Muamalah Kolej Universiti Islam Antarabangsa Selangor (KUIS)

Bandar Seri Putra, 43 000 Kajang,

SELANGOR, MALAYSIA

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

Jurnal Pengurusan & Muamalah

Volume / Jilid 6 November / November 2016

Number / Nombor 2 eISSN 2180-1681

No.

Articles / Artikel

Page / Halaman

1 Penipuan dan Pemalsuan Dalam Urusniaga Tanah : Kesan Terhadap Hak Milik Tidak Boleh Di Sangkal (Fraud and Forgery in Land Dealings: Effect To The

Indefeasibility of Title) Rabi’ah Muhammad Serji

1-14

2

Regulating Anti-Competitive Business conduct via completion Law in Malaysia

(Mengawal Selia Tingkahlaku Perniagaan Anti Persaingan Melalui Undang-Undang Persaingan di Malaysia) Haliza A. Shukor & Nazura Abdul Manaf

15-26

3

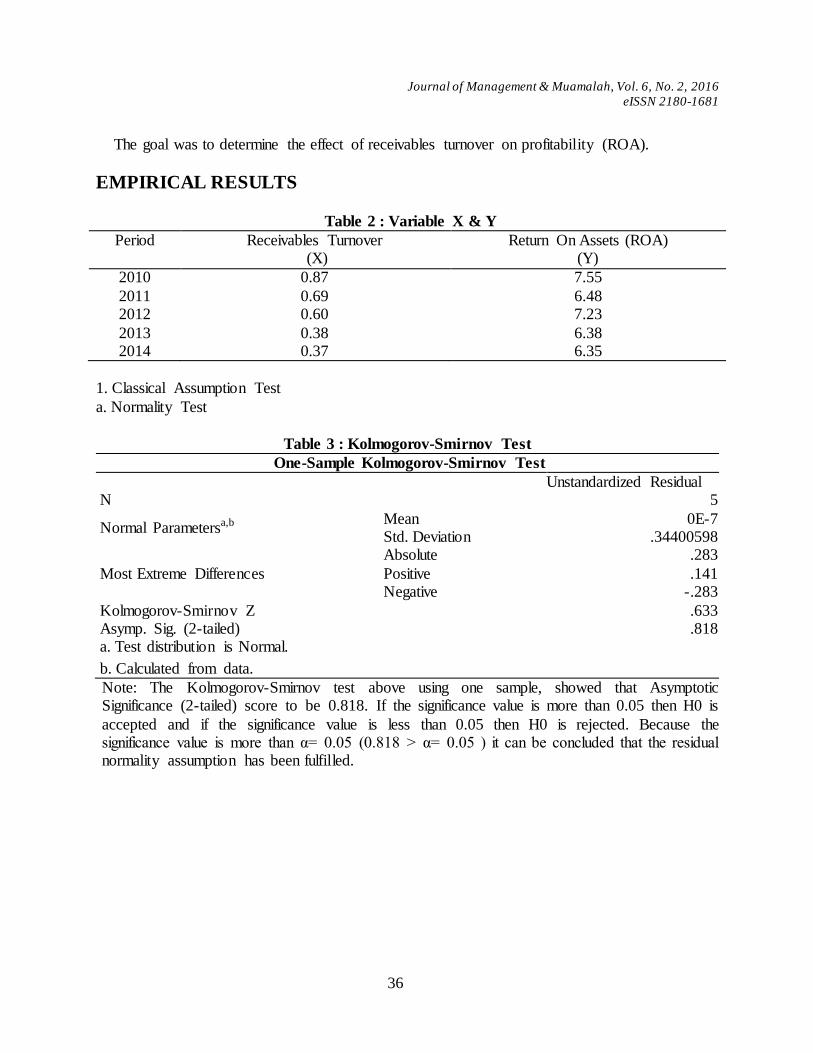

Effect of Receivable turnover to Profitability PT. Bil Finance

Center Period 2014 (Kesan Pusingganti Belum Terima Keatas Keuntungan Pt. Pusat Kewangan Tempoh 2010-2014)

Fia Dialysa

27-41

4

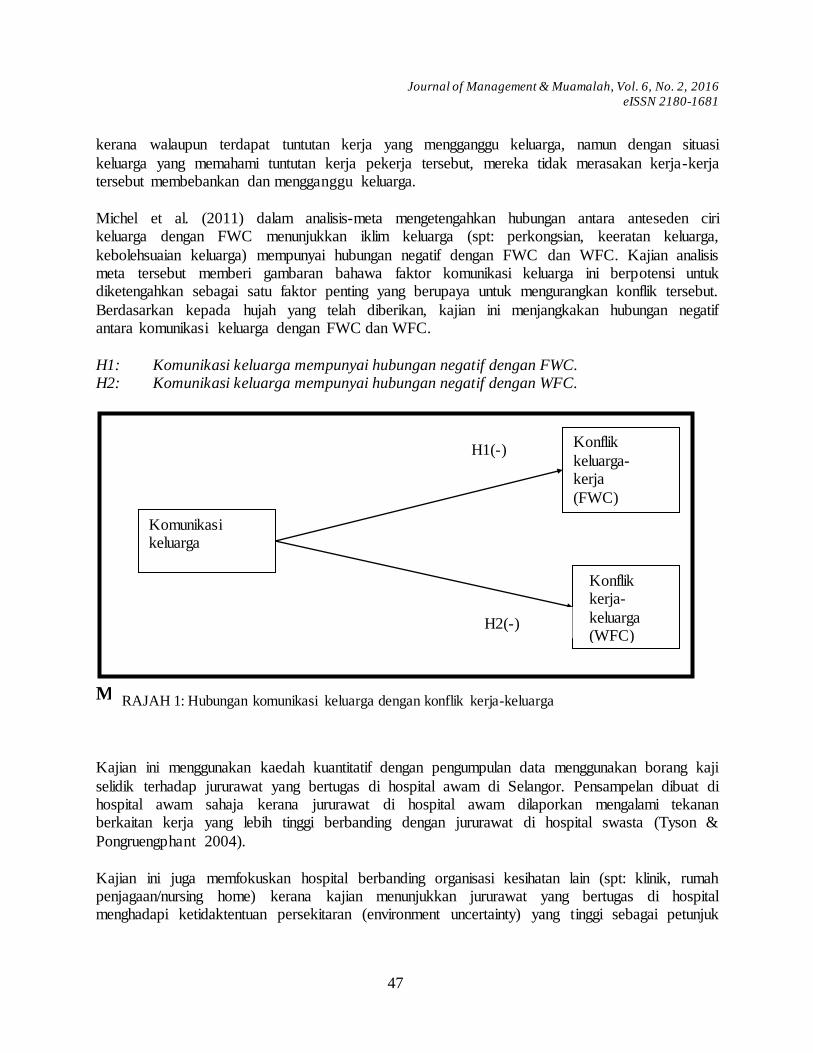

Peranan Komunikasi Dalam Mengurangkan Konflik Kerja-Keluarga: Tinjauan Ke Atas Jururawat Di Selangor (The Role of Communication in Reducing Work-Family

Conflict: A Survey on Nurses in Selangor) Normazaini Saleh

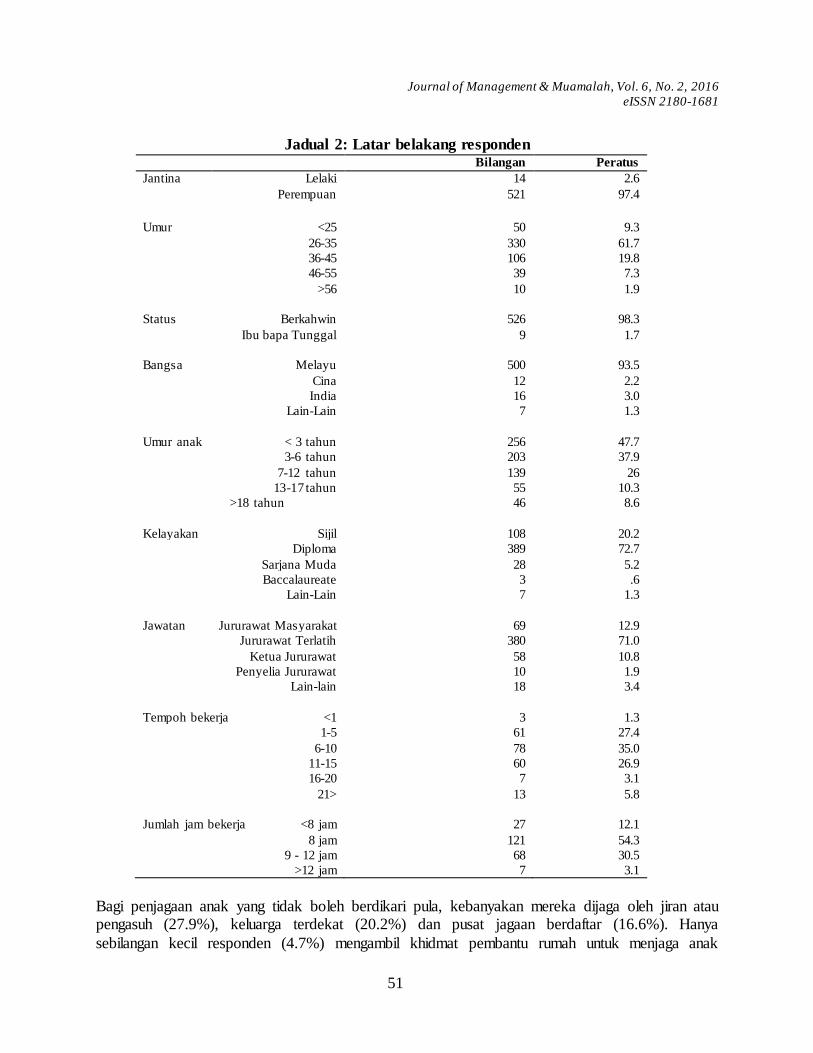

42-60

5

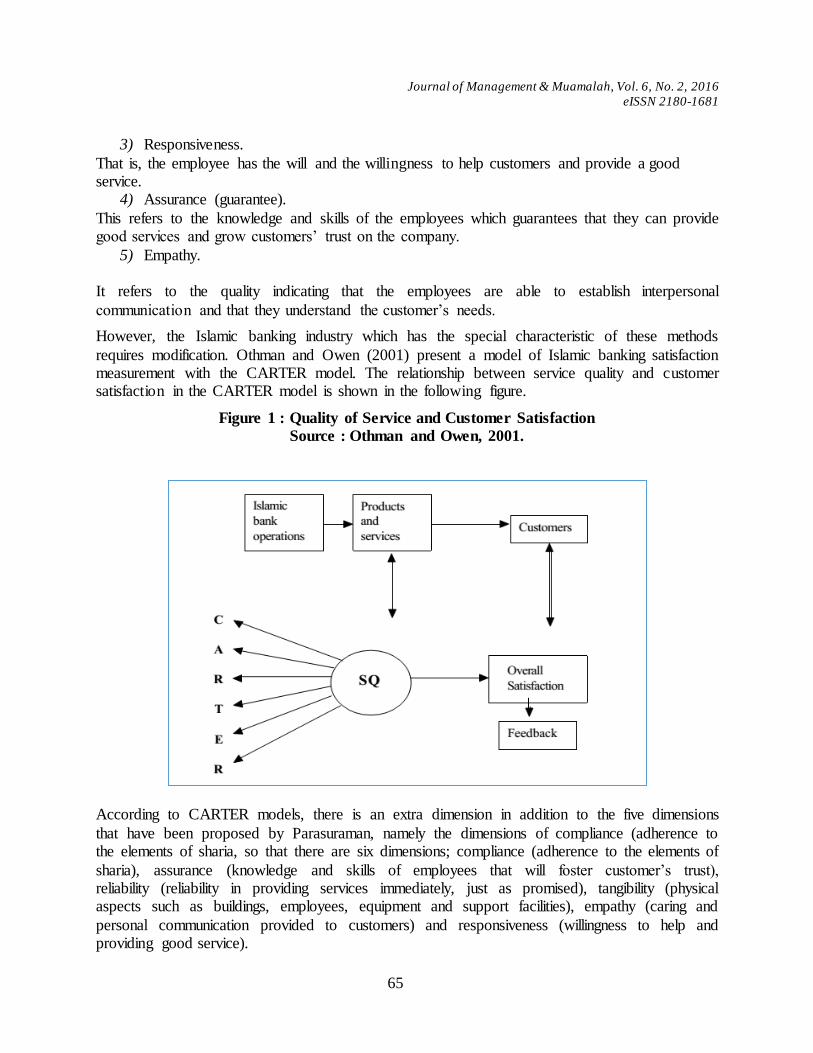

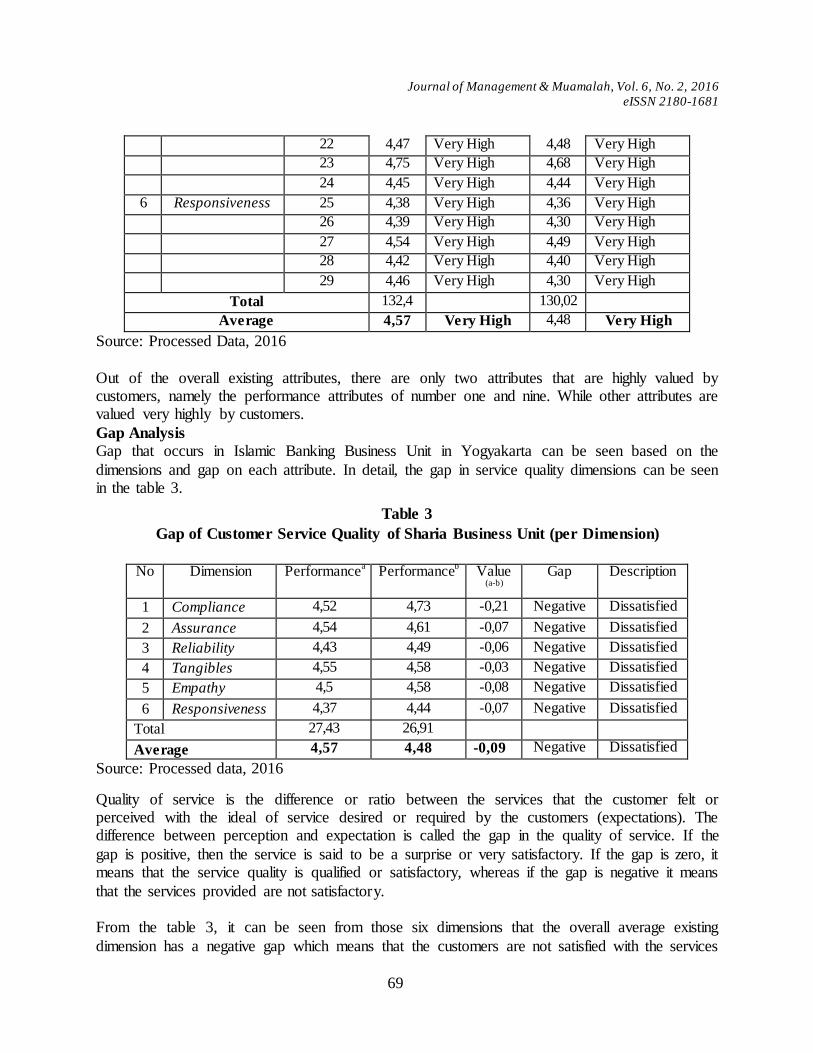

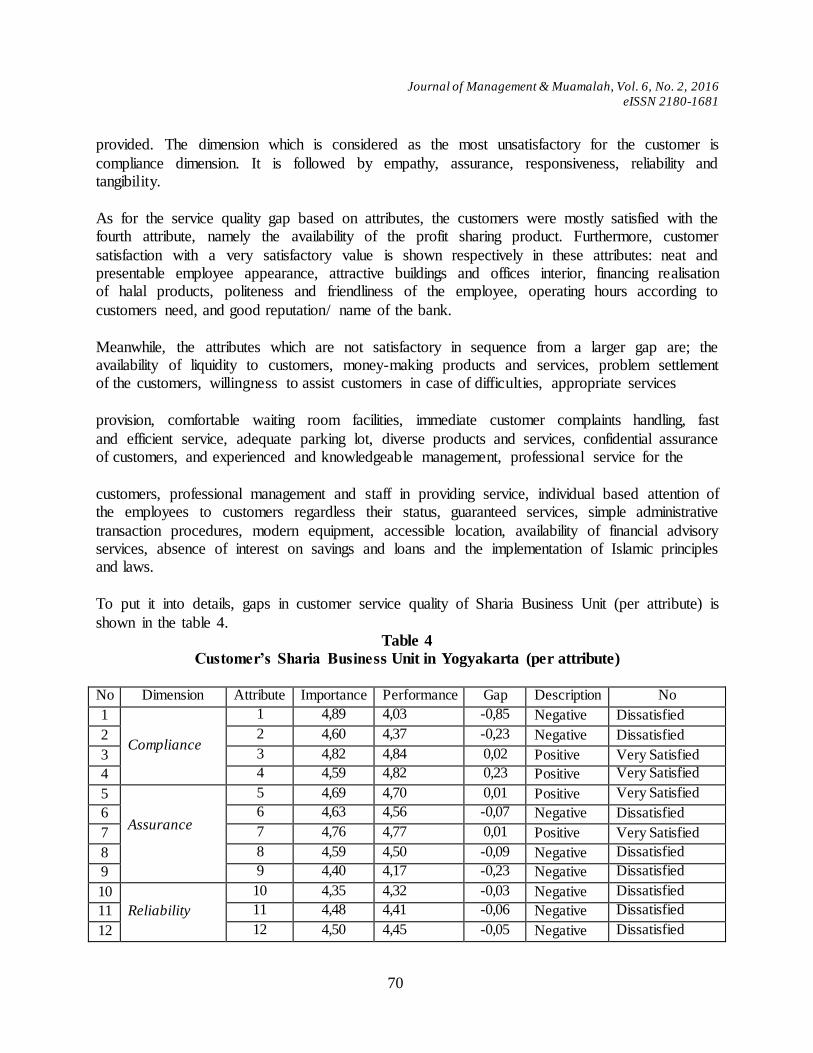

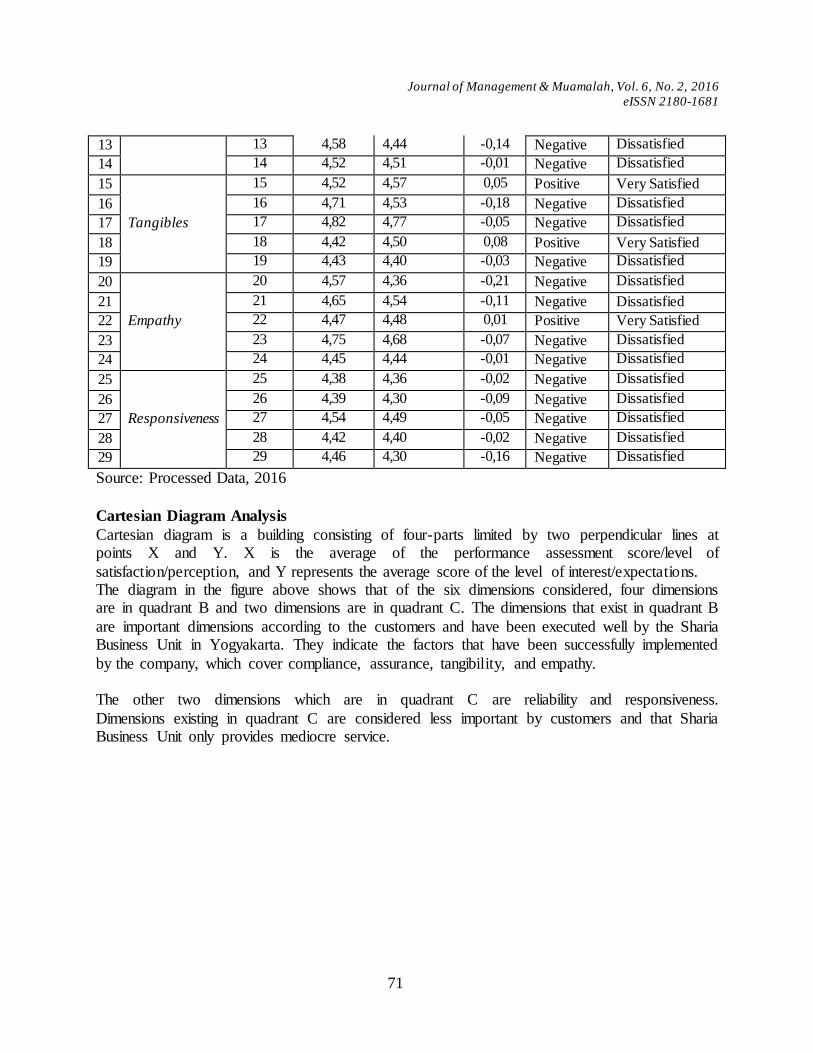

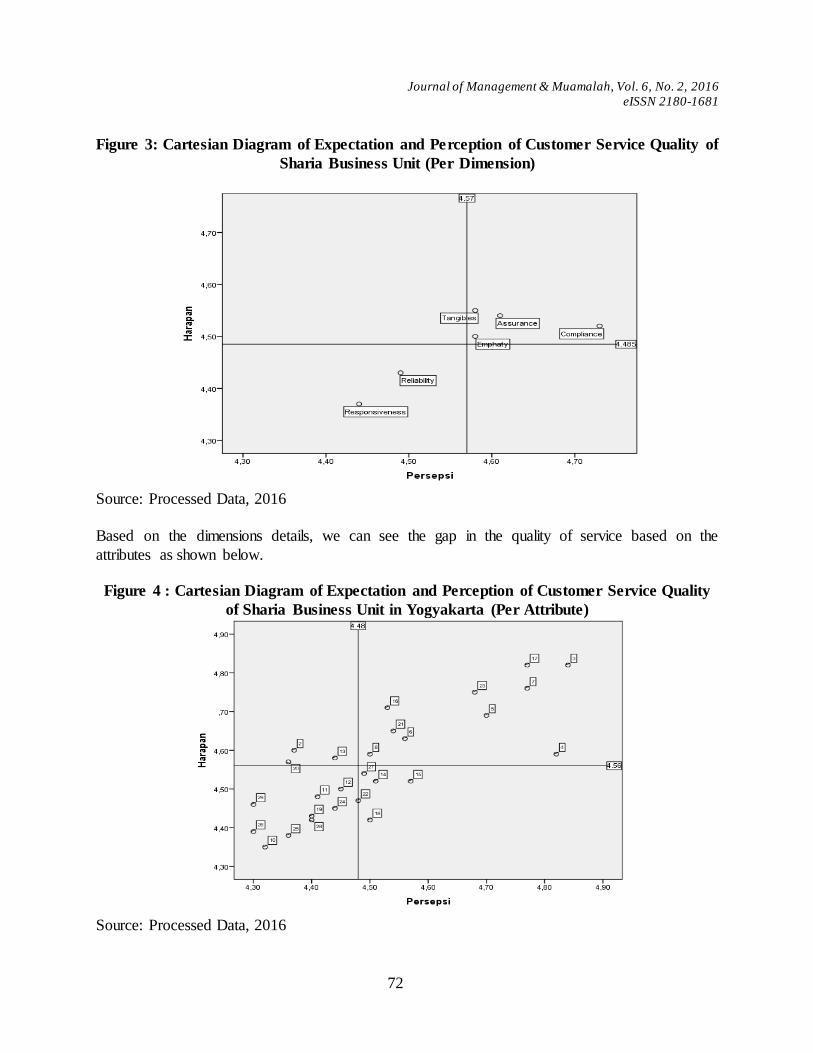

Customer Satisfaction Analysis Of Sharia Business Unit In Yogyakarta

(Analisis Kepuasan Nasabah Pada Unit Usaha Syariah Bank Di Yogyakarta)

Aidha Trisanty & Arif Darmawan

61-76

6

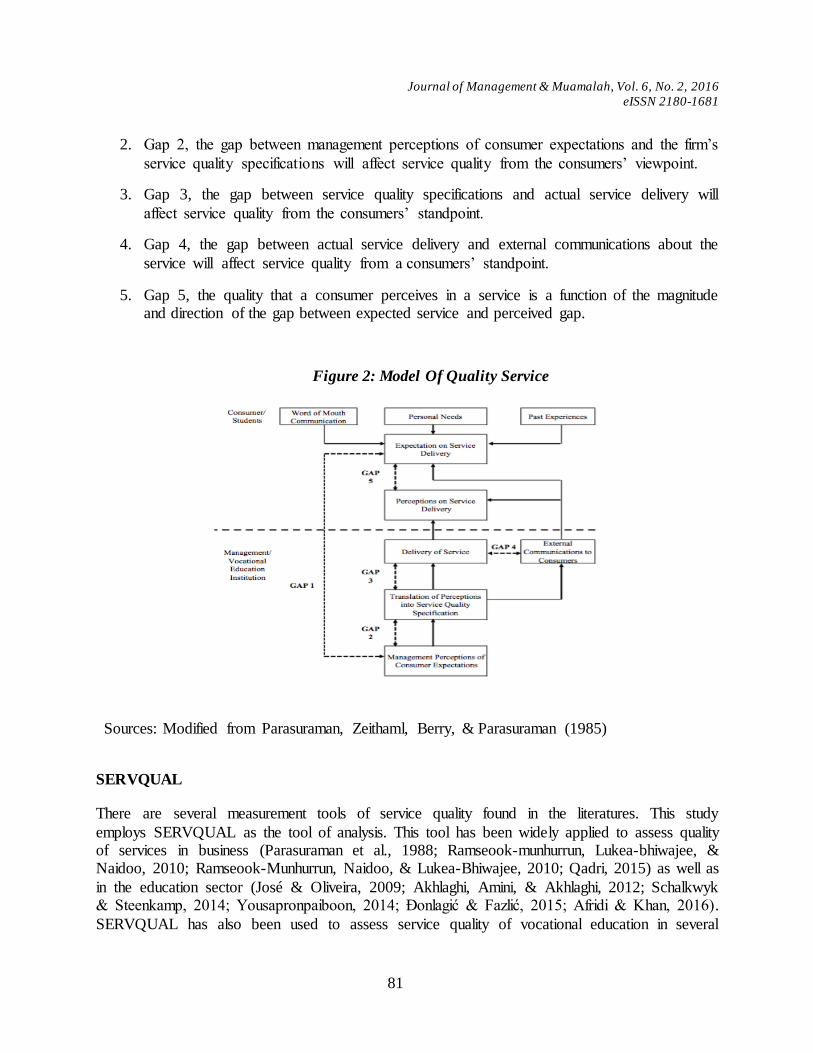

Applying SERVQUAL to Improve the Quality of Service

Delivery in Vocational Education in Indonesia (Penggunaan SERVQUAL Untuk Penambahbaikan Kualiti

Perkhidmatan Di Pendidikan Vokasional Di Indonesia) RR Sita Dewi Kusumaningrum

77-90

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

7

Financial Literacy of Youths: A Case Study of Islamic Banking

and Finance Students in Kolej Universiti Islam Antarabangsa Selangor (Belia Celik Kewangan: Kajian Kes Pelajar Perbankan Islam

dan Kewangan di Kolej Universiti Islam Antarabangsa Selangor)

Nurul Wajhi Ahmad, Murni Yunus Mawar & Norazlina

Ripain

91-103

8

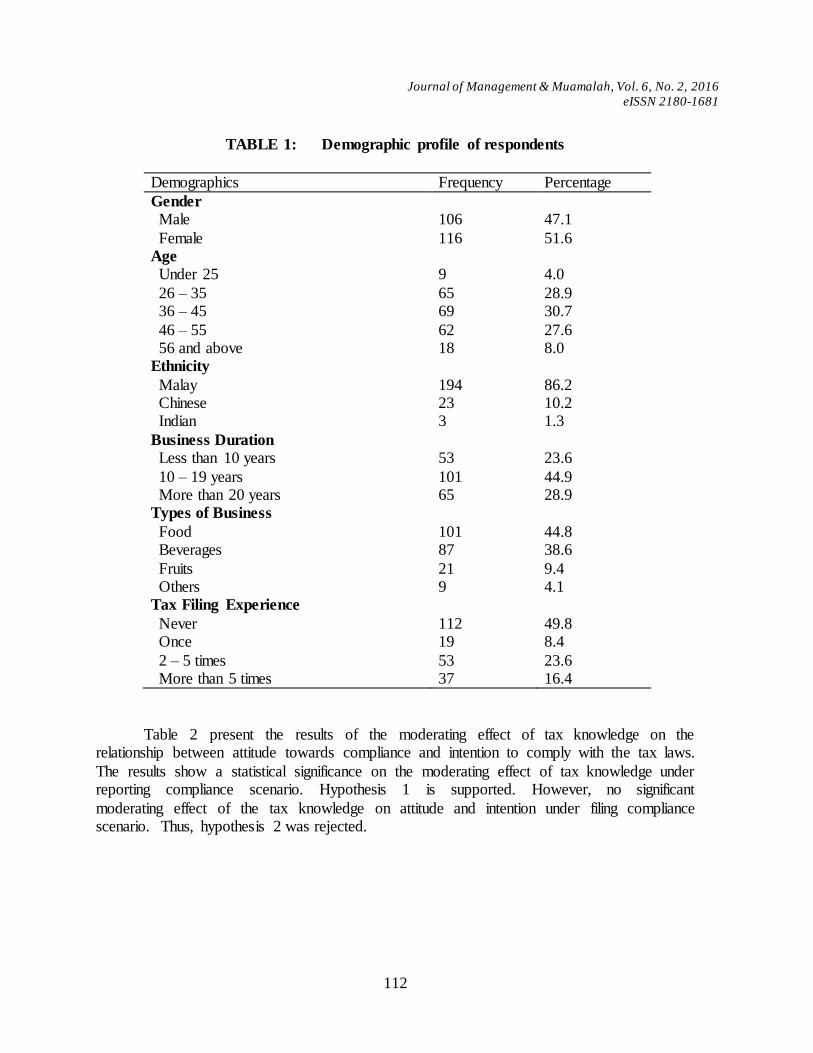

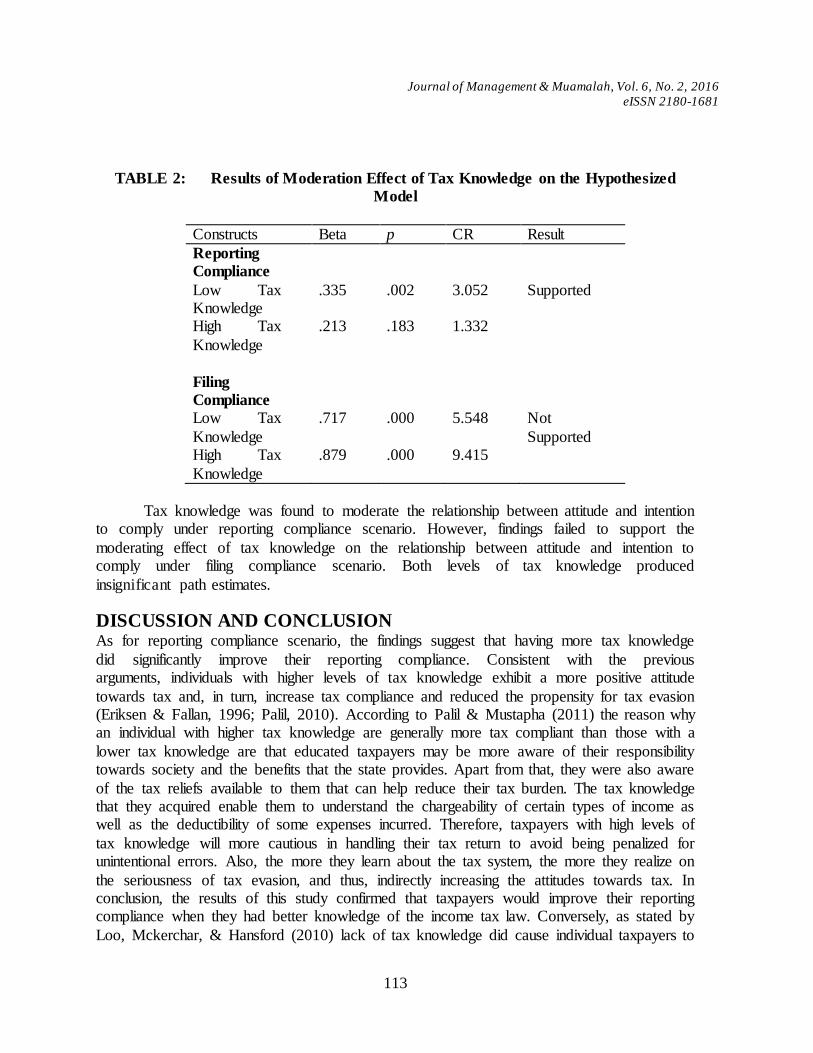

Attitudes, Tax Knowledge and Education Towards Compliance Behaviour

(Sikap, Pengetahuan Cukai dan Pendidikan Terhadap Tingkahlaku Pematuhan) Noor Suhaila Shaharuddin & Mohd Rizal Palil

104-115

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

4

Penipuan dan Pemalsuan Dalam Urusniaga Tanah: Kesan

Terhadap Hak Milik Tidak Boleh Di Sangkal

(Fraud and Forgery in Land Dealings: Effect to the Indefeasibility of Title)

Rabi’ah Muhammad Serji

Kolej Universiti Islam Antarabangsa Selangor Selangor, Malaysia

ABSTRAK

Prinsip undang-undang Tanah yang diguna pakai di Malaysia ialah prinsip undang-undang Tanah Torrens yang berasal dari Australia Selatan. Prinsip Torrens ini mementingkan

pendaftaran dalam setiap urusniaga tanah yang dijalankan. Setiap urusniaga tanah yang dilakukan mengikut prosedur yang telah ditetapkan oleh undang-undang akan memberikan pemilik berdaftar hak milik dan kepentingan yang tidak boleh disangkal dan disoal oleh sesiapa

pun. Jaminan hak milik ini telah diperuntukkan dengan jelas di dalam seksyen 340 Kanun Tanah Negara 1965. Namun begitu, peruntukan yang sama menyenaraikan pengecualian statut

terhadap perkara ini dan antara pengecualian yang diperuntukkan terhadap hak tidak boleh disangkal ialah sekiranya berlakunya penipuan dan pemalsuan dalam urusniaga tanah tersebut. Kertas kerja ini akan mengenalpasti penipuan dan pemalsuan bagaimanakah yang dimaksudkan

oleh seksyen 340 KTN dan kesannya terhadap hak milik tidak boleh disangkal di bawah sistem Torrens. Kajian kepustakaan dan analisis kes merupakan kaedah yang akan digunakan dalam

kertas kerja ini. Kata kunci: Prinsip Torrens, Kanun Tanah Negara 1965, Hak Tidak Boleh Disangkal,

Penipuan dan Pemalsuan, Urusniaga Tanah

ABSTRACT

Land law principle which was applied in Malaysia was Torrens system originated from South

Australia. According to the Torrens principle, registration of land dealings was very important. Every land dealing which follow all the procedures of law will gave the registered owner the

indefeasibility of title and interest. The guaranteed title to the registered owner was clearly enacted in section 340 of the National Land Code 1965. This section however listed out the statutory exceptions to the principle of indefeasibility such as fraud and forgery in land

dealings. This paper will studied what kind of fraud and forgery as mentioned in the exceptions of section 340 NLC and its impact to the principle of indefeasibility of title under the Torrens

system. The method of library research and case analysis was used in this paper. Keywords: Torrens Principle, National Land Code 1965, Indefeasibility of Title, Fraud and

Forgery, Land Dealings

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

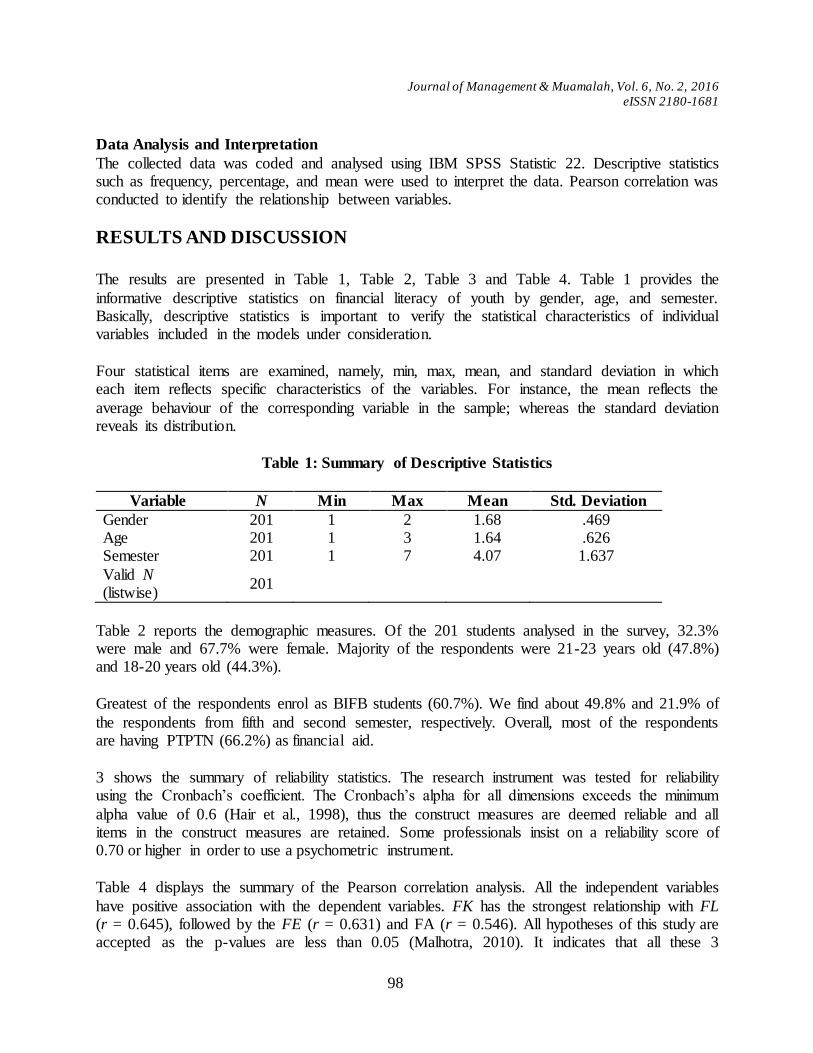

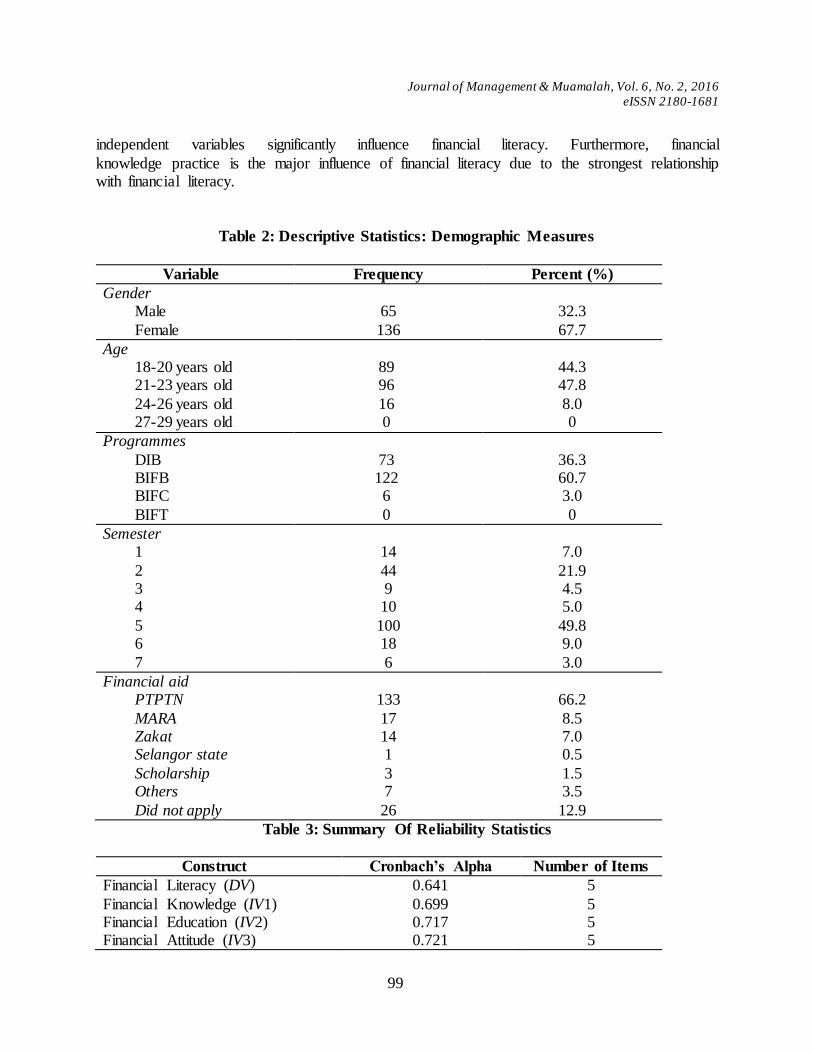

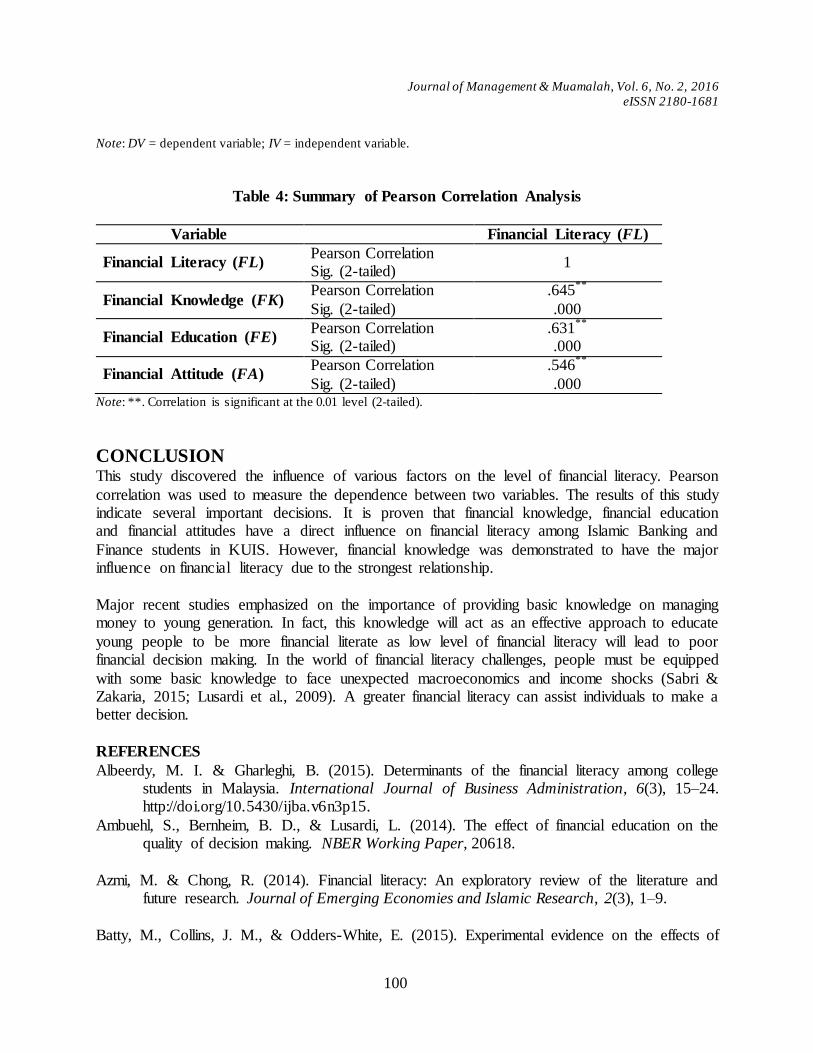

5

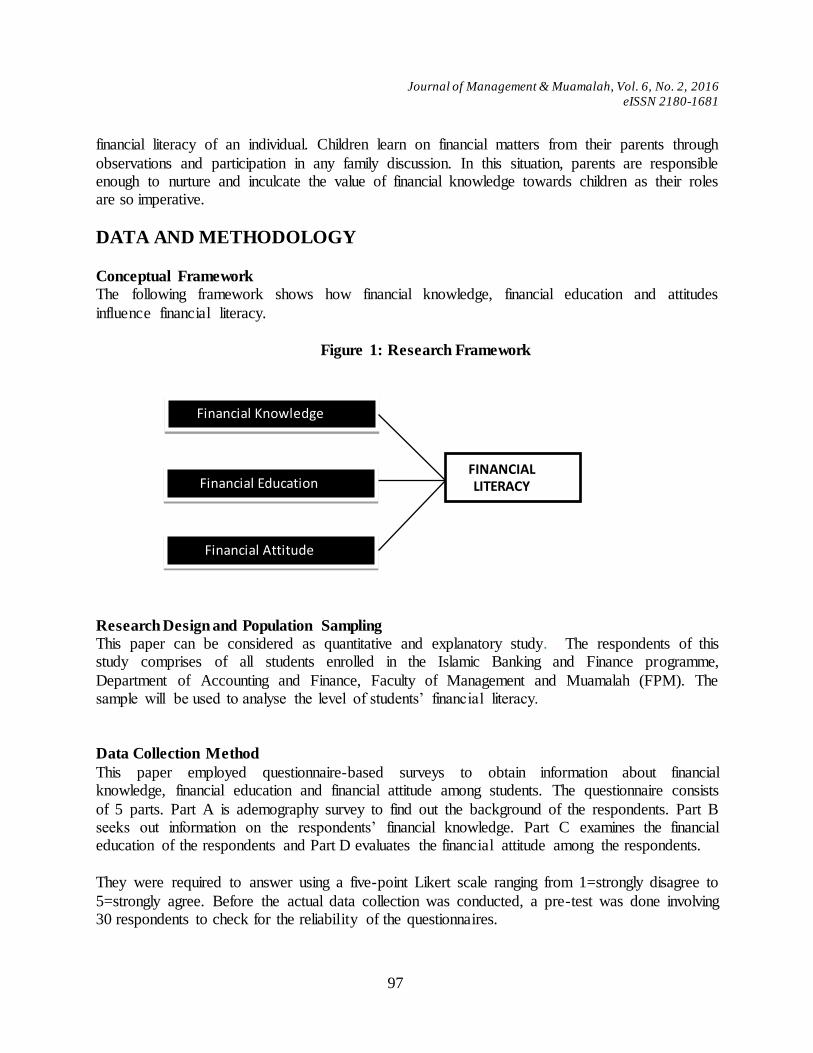

PENGENALAN Undang-undang tanah di Malaysia khususnya negeri-negeri di semenanjung Malaysia terkandung dalam undang-undang tanah utama iaitu Kanun Tanah Negara 1965. Pemakaian undang-undang ini adalah berasaskan kepada prinsip kemuktamadan daftar yang dikenali

sebagai sistem Torrens. Sistem ini pada permulaannya telah diperkenalkan di Australia Selatan oleh pengasasnya iaitu Sir Richard Robert Torrens. Prinsip asas undang-undang Torrens ialah

semua urusniaga berkaitan tanah yang dilakukan perlu didaftarkan bagi memastikan urusniaga tersebut diiktiraf oleh undang-undang dan boleh dikuatkuasakan. Mengikut prinsip Torrens, setiap urusniaga berkaitan dengan tanah perlu menggunakan borang-borang berkaitan yang telah

ditetapkan dan didaftarkan bagi menjamin kesahan setiap urusan tanah yang dilakukan. Pendaftaran yang dilakukan mengikut prosedur yang telah ditetapkan akan memberikan hak

yang tidak boleh disangkal kepada pemilik. Ini bermakna mengikut sistem Torrens, hak pemilik berdaftar adalah mutlak dan tidak boleh dipersoalkan oleh sesiapa pun. Individu yang namanya didaftarkan sebagai pemilik berdaftar bagi sesuatu tanah dikatakan mempunyai hak milik yang

tidak boleh dicabar atau dipersoalkan (Visu Sinnadurai, 1984). Hak pemilik mengikut Torrens adalah dijamin oleh pihak berkuasa negeri (Ainul Jaria, 2008).

Namun, hak tidak boleh disangkal yang diberikan oleh undang-undang kepada pemilik berdaftar ini akan menimbulkan masalah apabila sesuatu urusniaga dilakukan dengan kewujudan fraud

dan pemalsuan. Selepas beberapa pindaan dan penambah baikan terhadap undang-undang tanah Torrens semenjak diperkenalkan, peruntukan dalam undang-undang utama berkaitan tanah di

Malaysia iaitu Kanun Tanah Negara 1965 memperuntukkan pengecualian terhadap prinsip tidak boleh sangkal ini di dalam seksyen 340(2).

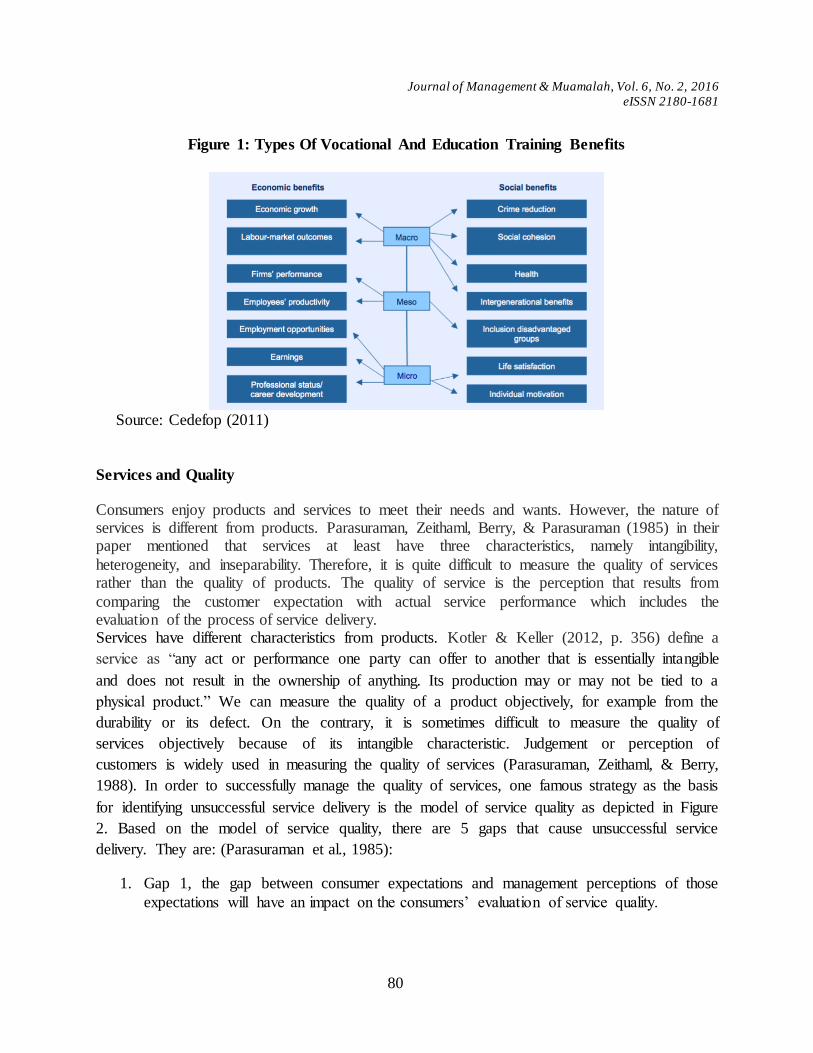

SISTEM TORRENS Sistem Torrens merupakan sistem pentadbiran tanah yang diguna pakai di Malaysia pada hari ini. Sistem ini mula diperkenalkan di Semenanjung Tanah Melayu oleh British pada tahun 1864

dan seterusnya berkembang dan diamalkan oleh semua negeri di semenanjung melalui undang-undang tanah yang sama iaitu Kanun Tanah Negara 1965 yang mula berkuat kuasa mulai Januari 1966. Sistem Torrens mementingkan pendaftaran yang mana ianya menghendaki semua

urusniaga berkaitan tanah yang dilakukan perlu direkod dan didaftarkan bagi menjamin kesahannya. Pendaftaran akan memudahkan bakal pembeli untuk mengenal pasti hak milik,

kepentingan dan juga bebanan sekiranya ada terhadap tanah yang disiasat (Jerald Gomez, 2008). Secara umumnya, terdapat dua prinsip utama sistem Torrens iaitu prinsip Cermin dan prinsip

Tabir. Di bawah prinsip Cermin, pendaftaran mencerminkan segala fakta material berhubung hak milik seseorang ke atas tanahnya. Hak milik itu tidak boleh disangkal serta selamat, terang

dan mudah (Ridzuan Awang, 1994). Fakta material berkenaan adalah termasuk nama pemilik, butir-butir mengenai tanah, luas kawasan dan lokasinya, pelan ukur dan had sempadannya. Dengan kata lain, prinsip ini mencerminkan dalam rekod apa yang ada di atas tanah dengan

daftar hak milik. Daftar hak milik adalah seperti satu cermin yang mampu menunjukkan segala maklumat yang penting mengenai tanah yang mungkin dikehendaki oleh seorang bakal pembeli

atau bakal pemegang gadaian (Das, Sk, 1963). Prinsip ini telah diperuntukkan di dalam seksyen

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

6

340 Kanun tanah Negara 1965, bahawa pendaftaran sesuatu tanah atas nama seseorang atau

badan sebagai tuan punya, memberi hak milik dan kepentingan yang tidak boleh disangkal kecuali dalam keadaan-keadaan tertentu sahaja seperti penipuan, salah nyataan, pemalsuan atau instrumen yang tidak sah.

Prinsip kedua sistem Torrens iaitu prinsip Tabir yang membawa maksud daftar yang

mempunyai sifat sebagai satu tabir yang mana dalam setiap transaksi antara pemilik berdaftar dengan bakal pembeli, bakal pembeli hanya dikehendaki memberi perhatian kepada daftar dan tidak lebih daripada itu. Adalah memadai bagi pembeli untuk bergantung pada maklumat yang

ada dalam daftar dan tidak perlu, malahan tidak boleh melihat lebih jauh daripada itu (Salleh Buang, 2007). Di dalam kes Gibbs V Messer [1891] A.C. 248, Majlis Privy telah menjelaskan

bahawa tujuan utama sistem Torrens adalah:

“….untuk menyelamatkan orang-orang yang berurusan dengan pemilik tanah daripada

kesulitan dan perbelanjaan kerana terpaksa menyiasat latar belakang hak milik berkenaan untuk memuaskan hati mereka mengenai kesahihannya”.

Prinsip Tabir ini menitik beratkan tujuan pembeli dengan turut diberi perhatian terhadap pendaftaran yang dianggap sebagai suatu sumber maklumat berhubung dengan hak milik yang

sah dari segi undang-undang. Prinsip ini mementingkan maklumat yang tercatat di dalam rekod daftar dan tidak perlu melihat di sebalik tabir seperti sejarah tanah dan sebagainya.

Pendaftaran yang sah akan memberikan hak dan kepentingan yang tidak boleh disangkal kepada individu yang namanya tercatat dalam daftar. Objektif utama sistem Torrens ialah untuk

menjadikan pendaftaran dokumen hak milik sebagai bukti konklusif terhadap pemilikan sesuatu hartanah (Ainul jaria, Hunud, 2010).

HAK TIDAK BOLEH DISANGKAL Hak milik dan kepentingan yang tidak boleh disangkal merupakan kesan penting kepada pendaftaran urusniaga. Apabila hak milik dan kepentingan seseorang individu didaftarkan

mengikut prosedur pendaftaran yang telah ditetapkan oleh undang-undang, ianya akan direkodkan di dalam dokumen pendaftaran hak milik. Kesannya, individu yang mendaftarkan uruniaga tanah itu akan menjadi pemilik mutlak yang tidak boleh disangkal. Ini bermakna hak

pemilik berdaftar tidak boleh dipersoalkan atau ditarik balik. Semua urusniaga yang didaftarkan akan mendapat pengiktirafan dan perlindungan hak tidak boleh disangkal. Di dalam kes Teh Bee

v K Maruthamuthu [1977] 2 MLJ 7, Mahkamah Persekutuan mengesahkan bahawa di bawah sistem Torrens, daftar adalah segala-galanya dan membenarkan siasatan dilakukan ke atas hak seorang pemilik berdaftar merupakan amalan yang salah kerana ianya akan menjejaskan

maksud dan matlamat pendaftaran. Di dalam kes ini mahkamah memutuskan bahawa, fakta pendaftaran dokumen hak milik atas nama appelan merupakan satu bukti konklusif bahawa hak

milik ke atas tanah itu adalah terletak kepada appelan.

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

7

Namun begitu, untuk memperolehi hak ketidak boleh sangkalan, individu yang berurusniaga

hendaklah mendaftarkan kepentingannya mengikut kehendak Kanun Tanah Negara dan memastikan agar dokumen yang ingin didaftarkan adalah sah dan dapat diterima mengikut undang-undang. Jika pendaftaran kepentingan gagal dilakukan, adalah agak mustahil untuk

memperolehi hak tidak boleh disangkal (Joshua, 2006). Peruntukan undang-undang berkenaan hak tidak boleh disangkal terdapat pada bahagian dua

puluh, Kanun Tanah Negara 1965. Seksyen 340 kanun tersebut memperuntukkan, pendaftaran untuk memberi hak milik atau kepentingan yang tak boleh disangkal, kecuali dalam keadaan-keadaan tertentu. Klausa (1) seksyen 340 memperuntukkan seperti berikut:

(1) Hak milik atau kepentingan mana-mana orang atau badan buat masa itu sebagai tuan punya mana-mana tanah, atau atas nama siapa apa-apa pajakan, gadaian atau esmen

adalah buat masa itu terdaftar, hendaklah, tertakluk kepada peruntukan –peruntukan berikut seksyen ini, tidak boleh disangkal.

Seksyen 340(1) ini menyebut perkataan hak milik atau kepentingan. Terdapat perbezaan di antara hak milik dan kepentingan di dalam peruntukan ini iaitu hak milik merujuk kepada hak

milik seseorang terhadap tanah yang telah didaftarkan. Manakala kepentingan pula bukan merujuk kepada hak milik tetapi hanya kepada kepentingan yang diperolehi daripada tanah tersebut. Sebagai contoh kepentingan pemegang gadaian (pihak bank), penerima pajakan atau

pun pemilik tanah dominan dalam urusniaga esmen.

Secara mudahnya bolehlah disimpulkan bahawa hak milik mutlak akan diberikan oleh undang-undang kepada individu yang namanya tercatat dalam daftar. Sebagai contoh sekiranya berlaku pertikaian terhadap hak milik tanah antara A dan B, mahkamah akan melihat kepada daftar hak

milik. Sekiranya hak milik atau kepentingan didaftarkan atas nama A, maka A adalah pemilik sebenar menurut undang-undang dan hak A ke atas tanah tersebut tidak boleh disangkal atau

dipersoalkan oleh sesiapa pun. PENIPUAN DAN PEMALSUAN SERTA KESANNYA TERHADAP HAK MILIK

TIDAK BOLEH DISANGKAL

Perbincangan sebelum ini menunjukkan bahawa sistem Torrens sangat mementingkan

pendaftaran dan kesan kepada pendaftaran ialah hak dan kepentingan pemilik berdaftar menjadi tidak boleh disangkal dan dipersoal. Namun begitu, seksyen 340(2) kanun Tanah Negara 1965 sendiri memperuntukkan pengecualian kepada prinsip ini. Secara mudahnya, prinsip hak milik

tidak boleh disangkal dalam undang-undang tanah yang diamalkan di Malaysia bukanlah diberi secara mutlak. Namun, ianya masih tertakluk kepada pengecualian-pengecualian tertentu.

Klausa (2) seksyen 340 KTN 1965 memperuntukkan: (2) Hak milik atau kepentingan mana-mana orang atau badan sedemikian hendaklah

menjadi tak boleh sangkal –

(a) Dalam mana-mana kes penipuan atau salahnyata yang kepadanya orang atau badan itu, atau mana-mana ejen orang atau badan itu, adalah suatu pihak atau

privy; atau (b) Jika sekiranya pendaftaran diperolehi secara pemalsuan, atau dengan cara suatu

instrument yang tidak mencukupi atau tak sah; atau

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

8

(c) Jika sekiranya hakmilik atau kepentingan itu adalah diperolehi secara tidak sah

oleh orang atau badan dalam pergunaan berupa apa-apa kuasa atau autoriti yang diberi oleh mana-mana undang-undang bertulis.

Seksyen ini memperuntukkan keadaan-keadaan yang membolehkan hak milik atau kepentingan seseorang atau badan disangkal. Adalah penting untuk difahami bahawa tindakan bagi

menyangkal hak milik akan hanya dapat dilakukan setelah pendaftaran hak milik itu dilaksanakan. Sekiranya pendaftaran tidak dilakukan, adalah agak mustahil bagi sesuatu pihak untuk menyangkal hak milik pihak yang namanya didaftarkan sebagai pemilik (Joshua, 2006).

PENIPUAN DAN SALAH NYATA SEKSYEN 340(2)(a)

Klausa (a), seksyen 340(2) memperuntukkan bahawa sekiranya sesuatu hak milik atau kepentingan diperolehi secara penipuan atau salah nyataan, ia boleh menjadikan hak milik atau kepentingan itu sebagai boleh disangkal. Maksud peruntukan ini ialah, mana-mana orang atau

badan yang telah mendaftarkan hak milik atau kepentingannya setelah memperolehinya melalui penipuan atau istilah lain disebut sebagai fraud, maka pemilik asal akan dapat mengenepikan

kepentingan tersebut. Pemilik asal juga harus membuktikan bahawa penipuan itu telah dilakukan oleh pihak yang namanya telah didaftarkan sebagai pemilik baru yang hak miliknya ingin disangkal oleh pemilik asal.

Kanun Tanah Negara tidak mentakrifkan penipuan (fraud), oleh itu rujukan perlu dibuat kepada

keputusan kes-kes yang berkenaan. Di dalam kes Assets Co v Mere Roihi [1905] AC 176, mahkamah telah menyatakan bahawa fraud bermaksud fraud yang sebenar (actual fraud) iaitu kelakuan tidak jujur. Di dalam kes Waimiha Sawmilling Company Limited v Waione Timber

Company Limited [1926] AC 101, Lord Buckmaster menyatakan bahawa: ― Jika tujuan sesuatu pindah milik itu adalah untuk menipu seseorang supaya hilang

haknya yang telah pun wujud, itu juga merupakan fraud dan begitu juga halnya perbuatan memperdayakan orang lain dengan sengaja dan dengan itu menyebabkan sesuatu kepentingan itu tidak didaftarkan…..‖

Adalah penting bagi pemilik asal membuktikan bahawa pemilik baru yang memperolehi hak

milik melalui penipuan adalah merupakan pihak atau pun privy kepada penipuan. Dengan kata lain, hendaklah ada bukti bahawa penipuan berkenaan telah dilakukan oleh orang yang didaftarkan menjadi pemilik tanah berkenaan atau oleh wakilnya (Salleh Buang, 1993).

Contoh kes berkaitan actual fraud ialah kes Haji Aishah v Yah binti Taib (1949) 15 MLJ 128. Di

dalam kes ini, seorang wanita yang buta huruf telah diberitahu bahawa dokumen hak milik yang ditandatanganinya itu ialah borang gadaian. Sebenarnya dokumen itu ialah suratcara pindah milik. Suratcara itu kemudiannya telah digunakan untuk memindah milik tanah wanita itu

kepada Haji Musa. Haji Musa kemudiannya telah memindah milik tanah itu kepada defendan. Defendan menyedari penipuan yang telah dilakukan ke atas pemilik asal tanah itu. Mahkamah

memutuskan bahawa hak milik defendan hendaklah diketepikan.

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

9

Di dalam kes lain yang diputuskan oleh mahkamah Persekutuan iaitu kes Tai Lee Finance Co

Sdn Bhd v Official Assignee & Ors [1983] 1 MLJ 81, sebuah syarikat pemaju perumahan telah menjual beberapa lot tanah dalam projeknya kepada beberapa orang pembeli. Keseluruhan tanah itu kemudian telah digadaikan oleh pemaju kepada sebuah syarikat kewangan yang merupakan

pemegang gadaian, sebagai sekuriti pinjaman yang diperolehi daripada syarikat tersebut. Setelah masa berlalu, pemaju perumahan menghadapi kesulitan membayar balik pinjamannya kepada

pemegang gadaian. Pemegang gadaian kemudiannya telah mengambil tindakan melelong tanah yang digadai untuk mendapatkan balik wang pinjaman. Pada masa ini lah beberapa orang pembeli lot tanah itu telah mencelah.

Isu di dalam kes ini ialah, sama ada pemegang gadaian dianggap terlibat dalam perbuatan fraud

terhadap pencelah kerana apabila gadaian didaftarkan dia mengetahui bahawa lot-lot tanah berkenaan telah pun dijual kepada pencelah. Mahkamah telah menolak hujah ini dan menegaskan bahawa fraud bermaksud kelakuan atau perbuatan yang ‗tidak jujur‘ dan bukan

hanya sekadar fraud konstruktif atau fraud ekuiti. Berkenaan dengan salah nyata, tiada sebarang tafsiran berkaitan di bawah KTN 1965. Maka

adalah penting untuk menentukan sama ada salah nyata yang dimaksudkan di bawah kanun adalah salah nyata penipuan atau pun tidak. Di dalam kes Datuk Jaginder Singh v Tara Rajaratnam [1983] 2 MLJ 196, mahkamah memutuskan bahawa salah nyata di bawah seksyen

340(2)(a) adalah merupakan salah nyata penipuan (fraudulent misrepresentation). Oleh itu, salah nyata di bawah peruntukan ini boleh dianggap sebagai salah satu jenis fraud (Teo dan Khaw,

1995). Hakim Lee hun Hoe di dalam kes ini telah merujuk kepada perkataan ‗fraud atau salah nyata‘ dalam seksyen 340(2)(a) dan menyatakan bahawa perkataan ‗atau‘ di situ ialah sesuatu yang disjunktif, oleh itu istilah ‗fraud atau salah nyata‘ bermaksud fraud yang sebenar atau salah

nyata fraud atau kedua-duanya.

PEMALSUAN SEKSYEN 340(2)(b)

Mengikut peruntukan seksyen 340(2)(b) Kanun Tanah Negara 1965, hakmilik atau kepentingan mana-mana orang atau badan sedemikian janganlah menjadi tak boleh disangkal jika

pendaftaran diperolehi secara pemalsuan. Ini bermakna, jika terdapat pemalsuan dokumen dalam proses pindah milik, maka hak milik berdaftar yang diperolehi kemudiannya boleh

disangkal. Pemalsuan boleh wujud dalam keadaan seseorang yang menyalahgunakan nama pemilik

berdaftar dan tandatangannya untuk melaksanakan satu pendaftaran hak milik yang baru. Mengikut seksyen 340 (2)(b), apabila pendaftaran sesuatu urusniaga itu diperolehi secara

pemalsuan, maka hak milik yang didaftarkan itu boleh disangkal. Di dalam kes Ong Lock Choo v Quek Shin & Sons Ltd (1941) MLJ 88, seorang pemilik tanah telah memberikan dokumen hak miliknya kepada seorang peguam untuk urusan pendaftaran gadaian. Kerani peguam itu

kemudiannya telah memalsukan suratcara berkenaan dan menggadai tanah itu kepada orang lain. Mahkamah memutuskan bahawa gadaian yang didaftarkan itu tidak sah. Apa yang perlu

dibuktikan di dalam seksyen ini adalah tindakan pemalsuan itu sendiri dan tidak perlu membuktikan bahawa pemilik berdaftar yang baru telah menjadi ahli atau pun privi kepada pemalsuan seperti yang dikehendaki di bawah penipuan atau fraud (Joshua, 2006).

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

10

Di dalam kes Quah Hong Lian Neo v Seow Teong teck [1936] MLJ 203, seseorang telah

mendapat pindah milik sebidang tanah daripada pemiliknya menerusi tipu helah dan pemalsuan. Berikutnya sebagai seorang pemilik berdaftar, dia telah menggadai tanah itu kepada pihak ketiga. Mahkamah di dalam kes ini telah menjadikan kes Gibbs v Messer (1891)AC 248, sebagai

rujukan dan memutuskan bahawa pindah milik itu tidak sah. Oleh sebab dia tidak memperolehi hak yang sah menerusi pindah milik itu, dia tidak mempunyai apa-apa hak untuk mewujudkan

satu gadaian berasaskan maksim undang-undang nemo dat quod non habet. Di dalam kes OCBC Bank (M) Bhd v Pendaftar Hak milik Negeri Johor Darul Takzim [1999] 2 MLJ 511, mahkamah telah menyatakan bahawa untuk menyangkalkan hak milik atas alasan pemalsuan, pemalsuan itu

tidak perlu dikaitkan dengan pihak yang hak miliknya ingin disangkalkan. Hanya perlu buktikan bahawa terdapat pemalsuan di dalam pemindahan hak milik.

PIHAK KETIGA YANG BERTINDAK SECARA BONA FIDE

Namun begitu, masalah timbul dalam situasi jika sesuatu dokumen hak milik dipalsukan dan

kemudiannya pemilik berdaftar yang memperolehi hak milik melalui pemalsuan dokumen itu menjual tanah tersebut kepada pembeli yang membeli secara bona fide. Sama ada pemindahan

hak milik kepada pihak ketiga yang membeli secara bona fide itu boleh disangkal atau pun tidak. Perkara ini ada diperuntukkan di dalam seksyen 340(3) KTN 1965 seperti berikut:

(3) Jika sekiranya hakmilik atau kepentingan mana-mana orang atau badan adalah

boleh disangkal oleh sebab apa-apa keadaan yang dinyatakan dalam subsekyen(2)-

(a) Maka ia hendaklah tertanggung untuk diketepikan dalam tangan mana-mana orang atau badan yang kepadanya ia mungkin dipindahmilik kemudiannya; dan

(b) Apa-apa kepentingan yang diberi kemudiannya hendaklah tertanggung untuk

diketepikan dalam tangan mana-mana orang atau badan dalam mana ia adalah buat masa itu diletakhak:

Dengan syarat bahawa tiada apa jua dalam subseksyen ini hendaklah menyentuh apa-apa hak atau kepentingan yang diperolehi oleh mana-mana pembeli dengan suci hati dan untuk balasan

yang berharga, atau oleh mana-mana orang atau badan yang menuntut melalui atau di bawah seorang pembeli sedemikian.

Di dalam kes Adorna Properties Sdn. Bhd v Boonsom Boonyanit [2001] 2 CLJ 133, fakta secara ringkasnya ialah seseorang telah memalsukan tandatangan Boonsom dan telah memindah milik

suatu tanah yang asalnya hak milik Boonsom kepada Adorna. Adorna tidak mengetahui langsung tentang pemalsuan dan dokumen yang telah dipalsukan. Telah dihujahkan bahawa

urusan penjualan dan pendaftaran tanah telah dilakukan mengikut prosedur yang telah ditetapkan oleh undang-undang. Mahkamah Tinggi telah memutuskan kes ini berpihak kepada Adorna berdasarkan kepada proviso seksyen 340(3). Namun begitu, Mahkamah Rayuan telah

membuat keputusan sebaliknya dengan memutuskan bahawa hak yang didaftarkan atas nama Adorna adalah boleh disangkal berdasarkan kepada peruntukan seksyen 340(2) dan proviso

seksyen 340(3) tidak terpakai. Walau bagaimana pun, apabila rayuan dibuat ke Mahkamah Persekutuan, mahkamah memutuskan bahawa proviso seksyen 340(3) adalah terpakai dan memberikan hak milik yang tidak boleh disangkal kepada Adorna. Di dalam kes ini mahkamah

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

11

menganggap Adorna sebagai pembeli yang membeli secara suci hati (bona fide) sebagai mana

yang peruntukkan di dalam proviso seksyen 340(3). Associate Professor Teo Keang Sood ketika mengkritik penghakiman kes Adorna menyatakan

bahawa mahkamah telah tersilap dalam mentafsir peruntukan seksyen 340. Seksyen 340(1) digubal untuk memberikan pemilik berdaftar hak milik dan kepentingan yang tidak boleh

disangkal melainkan hak milik dan kepentingan itu diperolehi dengan cara yang dinyatakan di dalam sub seksyen (2) dan (3), seksyen 340. Salah satu keadaan yang dinyatakan di dalam seksyen 340(2) yang menjadikan hak milik dan kepentingan pemilik berdaftar boleh disangkal

ialah sekiranya pendaftaran hak milik itu diperolehi dengan cara pemalsuan. Pendaftaran hak milik yang diperolehi dengan cara pemalsuan menjadikan hak milik itu boleh disangkal dan

kesannya hak milik itu boleh diketepikan sebagaimana yang diperuntukkan di dalam seksyen 340(3). Walau bagaimana pun, terdapat proviso kepada seksyen 340(3) seperti yang telah diterangkan di atas (Teo Keang Sood, 2004).

Associate Professor Teo seterusnya meringkaskan kritikannya terhadap kes ini kepada 6 perkara

penting iaitu: i. Bersetuju dengan tafsiran mahkamah terhadap seksyen 340(1). ii. Seksyen 340(2) menjadikan pendaftaran hak milik dan kepentingan boleh

disangkal dalam kes pemalsuan walau pun pemilik berdaftar yang baru itu bukanlah pihak atau pun privy kepada perbuatan pemalsuan itu. Dengan kata

lain, walau pun sekiranya pemilik berdaftar bertindak secara suci hati, hak milik dan kepentingannya masih boleh disangkal jika terbukti wujudnya pemalsuan.

iii. Di dalam kes Boonsom, pihak yang melakukan pemalsuan tidak mendaftar tanah

itu atas namanya sendiri tetapi menjualnya terus kepada appelan iaitu Adorna. Dengan kata lain, Adorna membeli tanah itu terus daripada pihak yang

melakukan pemalsuan. Di dalam kes ini, situasi appelan itu termasuk di dalam peruntukan seksyen 340(2)(b) dan oleh itu menjadikan hak miliknya boleh disangkal. Kes ini bukanlah berkaitan pembeli yang membeli dengan suci hati

dan untuk balasan yang bernilai dan oleh itu seksyen 340(3) tidak terpakai. iv. Adalah penting untuk difahami bahawa seksyen 340(3) tidak terpakai melainkan

jika didapati hak milik dan kepentingan pemilik berdaftar boleh disangkal disebabkan wujudnya perkara-perkara yang dinyatakan di dalam seksyen 340(2). Sekiranya perkara itu berlaku, ianya hanya akan terpakai kepada pembeli yang

membeli daripada pemilik berdaftar yang mana hak milik dan kepentingannya boleh disangkal berdasarkan seksyen 340(2). Sekiranya perkara ini berlaku,

barulah seksyen 340(3) terpakai. v. Di dalam kes Boonsom, tiada ruang kepada pemakaian seksyen 340(3) kerana

tiada pembelian sebagaimana yang dinyatakan di dalam seksyen 340(3) berlaku.

Oleh itu hak milik dan kepentingan appelan masih boleh disangkal berdasarkan peruntukan seksyen 340(2).

Walau bagaimana pun harus difahami di sini bahawa kritikan Associate Professor Teo itu hanyalah pendapatnya dan tidak mengikat mana-mana pihak. Tafsiran seksyen 340 yang

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

12

mengikat boleh dilihat dalam keputusan mahkamah di dalam kes Tan Ying Hong v Tan Sian San

& Ors [2010] 2 MLJ 1. Di dalam kes ini, isu yang perlu diputuskan oleh mahkamah ialah sama ada pemilik berdaftar suatu gadaian di bawah Kanun Tanah Negara 1965 yang memilikinya melalui suatu dokumen yang telah dipalsukan akan memperolehi secara serta merta hak milik

dan kepentingan yang tidak boleh disangkal.

Fakta dalam kes ini ialah, perayu merupakan pemilik berdaftar tanah seluas Sembilan ekar yang terletak di Kuantan, Pahang. Tanpa pengetahuan perayu, responden pertama telah bertindak dengan menggunakan surat kuasa wakil yang telah dipalsukan untuk memeterai dua gadaian

bagi mendapatkan pinjaman untuk responden kedua. Responden kedua telah gagal membayar balik pinjaman dan pihak bank telah menuntut bayaran pinjaman tersebut daripada perayu.

Perayu membuat permohonan kepada mahkamah untuk mengisytiharkan bahawa gadaian itu tidak sah dan batal atas alasan surat kuasa wakil yang digunakan untuk proses gadaian itu telah dipalsukan. Mahkamah Tinggi menolak permohonan perayu atas alasan perayu bukan pemilik

sebenar tanah dan seksyen 340(3) KTN dan proviso telah melindungi responden ketiga. Mahkamah Rayuan mengekalkan keputusan Mahkamah Tinggi. Dalam rayuan ke Mahkamah

Persekutuan, mahkamah berpuas hati bahawa gadaian telah dimeterai dengan menggunakan instrument yang batal dan oleh itu secara automatik boleh diketepikan oleh perayu yang merupakan pemilik berdaftar. Mahkamah Persekutuan menegaskan, fakta bahawa hak atau

kepentingan itu diperolehi secara suci hati dan untuk balasan yang bernilai bukanlah persoalannya kerana sekiranya mahkamah berpuas hati bahawa gadaian itu diwujudkan dengan

menggunakan dokumen yang tidak sah, maka ia secara automatik menjadikan hak dan kepentingan yang didaftarkan itu boleh diketepikan. Mahkamah di dalam kes ini mengiktiraf prinsip hak milik tidak boleh disangkal secara tertunda dan bukannya serta merta seperti yang

biasa diamalkan di bawah sistem Torrens. Mahkamah Persekutuan di dalam kes ini menyatakan bahawa Mahkamah Persekutuan di dalam Kes Boonsom Bonyanit telah salah faham dalam

mentafsir seksyen 340(1) atau telah melakukan kesilapan dalam memutuskan kes tersebut. Keputusan kes Tan Ying Hong ini menunjukkan bahawa mahkamah telah mengubah prinsip

yang telah dibuat di dalam kes Boonsom.

KESIMPULAN Kesimpulannya daripada perbincangan ini jelas menunjukkan bahawa sistem Torrens

memberikan hak milik dan kepentingan yang tidak boleh disangkal kepada pemilik berdaftar suatu tanah. Namun sekiranya pendaftaran hak milik dan kepentingan itu diperolehi dengan cara

fraud atau pemalsuan, peruntukan seksyen 340(2) Kanun Tanah Negara 1965 seperti yang dinyatakan di atas, secara jelas menyatakan bahawa, yang bermaksud sekiranya terdapat fraud dan pemalsuan dalam sebarang urusniaga tanah, maka pendaftaran tidak akan memberikan hak

milik dan kepentingan yang tidak boleh disangkal kepada pemilik yang namanya tercatat di dalam daftar. Hak serta kepentingan yang didaftarkan itu boleh diketepikan. Ini bermaksud,

kesan terhadap kewujudan urusniaga tanah secara fraud dan pemalsuan ialah hak milik dan kepentingan pemilik berdaftar masih boleh disangkal dan persoalkan.

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

13

Kes-kes pemalsuan yang dibincangkan di atas menunjukkan pihak-pihak yang memalsukan

dokumen sebenarnya juga secara tidak langsung melakukan penipuan terhadap urusniaga yang dilakukan. Oleh itu penulis menyimpulkan bahawa seksyen 340(2) itu secara umumnya adalah berkaitan urusniaga yang melibatkan fraud dan kesannya adalah menjadikan hak milik dan

kepentingan yang didaftarkan itu boleh disangkal menurut undang-undang. Tafsiran terhadap seksyen 340 Kanun Tanah Negara 1965, yang telah dibuat oleh Mahkamah Persekutuan di

dalam kes Tan Ying Hong mampu memberi perlindungan hak milik kepada pemilik asal suatu tanah, selari dengan matlamat utama Sistem Torrens yang menjadikan pendaftaran sebagai asas perlindungan hak milik.

RUJUKAN

Ainul Jaria Maidin & Hunud Abia Kadouf. Weaknesses in The Registration of Land Dealings

System in Malaysia: Suggestions for Improvements for Enhancing the System. [2010] 1

LNS 1.

Ainul Jaria Maidin, Sharifah Zubaidah Syed Abdul Kader, Bashiran Begum Haji Mobarak Ali, Nor Asiah Mohamad, Azlinor Sufian, Ratna Azah Rosli & Fauziah Md. Nor. (2008) Principles of Malaysian Land Law. Lexis Nexis, Singapore.

Das, SK (1963) The Torrens System in Malaya. MLJ, Singapore.

Jerald Gomez. Section 340 of the National Land Code, Before and After Boonsom Boonyanit.

[2008] 1 MLJ lxxii.

Joshua Kevin Sathiaseelan (2006) Prinsip-prinsip Penting Perundangan Tanah di Malaysia.

Lexis Nexis, Malaysia. Noraida Harun, Jady@Zaidi Hassim dan Noor ‗Ashikin Hamid, Penipuan, Rasuah dan

Pencurian Maklumat dalam Urus Niaga Tanah: Cabaran dan Penyelesaian, [2013] 25

KANUN (2), 160.

Ridzuan Awang (1994) Undang-undang Tanah Islam; Pendekatan Perbandingan. Dewan Bahasa dan Pustaka, Kuala Lumpur.

Salleh Buang (1993) Undang-undang Tanah di Malaysia. Dewan Bahasa dan Pustaka, Kuala Lumpur.

Salleh Buang (2007) Malaysian Torrens System. Second Edition, Dewan Bahasa dan Pustaka,

Kuala Lumpur.

Teo Keang Sood, Khaw Lake Tee (1995) Land Law in Malaysia, Cases and Commentar.

Second Edition, Butterworths Asia, Malaysia.

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

14

Teo Keang Sood (2004) Demise of Deferred Indefeasibility under the Malaysian Torrens

System? Infoline. SENARAI KES

Adorna Properties Sdn. Bhd v Boonsom Boonyanit [2001] 2 CLJ 133 Assets Co v Mere Roihi [1905] AC 176

Datuk Jaginder Singh v Tara Rajaratnam [1983] 2 MLJ 196 Gibbs V Messer [1891] A.C. 248 Haji Aishah v Yah binti Taib (1949) 15 MLJ 128

OCBC Bank (M) Bhd v Pendaftar Hak milik Negeri Johor Darul Takzim [1999] 2 MLJ 511 Ong Lock Choo v Quek Shin & Sons Ltd (1941) MLJ 88

Quah Hong Lian Neo v Seow Teong teck [1936] MLJ 203 Tai Lee Finance Co Sdn Bhd v Official Assignee & Ors [1983] 1 MLJ 81 Tan Ying Hong v Tan Sian San & Ors [2010] 2 MLJ 1

Teh Bee v K Maruthamuthu [1977] 2 MLJ 7 Waimiha Sawmilling Company Limited v Waione Timber Company Limited [1926] AC 101

Rabi’ah Muhammad Serji

Faculty of Islamic Study and Civilization

Selangor International Islamic University College SELANGOR, MALAYSIA [email protected]

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

15

Regulating Anti-Competitive Business Conduct via Competition

Law in Malaysia

(Mengawal Selia Tingkahlaku Perniagaan Anti Persaingan Melalui Undang-Undang

Persaingan di Malaysia)

Haliza A.Shukor Prof Dr Nazura Abdul Manap

Universiti Kebangsaan Malaysia

Selangor, Malaysia

ABSTRACT

The introduction of the competition law in Malaysia via Competition Act 2010 has brought a

tremendous shift in business practices. Common practice in businesses such as collusion to exploit quantity and price of goods in the market is no longer permitted with the coming into force the Competition Act 2010 in 2012. Hence, it is the aim of this paper to identify roles of

Malaysia competition law in regulating anti-competitive business conduct in Malaysia. The result indicated that while competition law in Malaysia plays its role in combating anti-

competitive business conduct, improvements of the provisions such as inclusion of specific merger provisions in the Competition Act 2010 and specific guidelines for intellectual property matters are needed in order to further support implementation of competition law in Malaysia.

This paper employs library based approach which collects data from statutes, decided cases, journals and books.

Keywords: Anti-Competitive Business Conduct, Competition Law, Competition Act 2010,

Competition Commission Act 2010

ABSTRAK

Pengenalan Undang-Undang Persaingan di Malaysia melalui Akta Persaingan 2010 membawa perubahan besar dalam amalan perniagaan. Amalan biasa dalam perniagaan

seperti pakatan sulit untuk mengeksploitasi kuantiti dan harga barangan di pasaran adalah tidak lagi dibenarkan dengan mula berkuatkuasanya Akta Persaingan 2010 pada tahun 2012.

Oleh itu, tujuan artikel ini ialah untuk mengenal pasti peranan Undang-Undang Persaingan di Malaysia dalam mengatur kelakuan perniagaan yang bersifat anti-persaingan. Hasilnya menunjukkan bahawa,walaupun Undang-Undang Persaingan di Malaysia memainkan peranan

dalam memerangi perlakuan perniagaan yang bersifat anti-persaingan, namun penambahbaikan peruntukan seperti kemasukan peruntukan khusus berkaitan penggabungan

dalam Akta Persaingan 2010 dan garis panduan khusus bagi perkara-perkara berkaitan harta intelek adalah diperlukan dalam usaha untuk terus menyokong pelaksanaan Undang-Undang Persaingan di Malaysia. Artikel ini menggunakan pendekatan kepustakaan yang mengumpul

data dari statut, kes-kes yang telah diputuskan, jurnal-jurnaldan buku-buku.

Kata kunci: Anti-persaingan, Undang-Undang Persaingan, Akta Persaingan 2010

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

16

INTRODUCTION Competition law concerns with practices that bring harm to the competitive process (Whish, R. 2009). Some of the practices which bring harm to the competitive process may include participating in agreements which have their objects or effects to restrict competition and

improper monopolist behavior in the market. Agreement between competitors who agree to group together with the objective to reduce competition in the market by either fixing prices or

sharing information may result to society losing the benefit from the competition law, simply because it will restrict the choice of prices for the same product and services from entrepreneurs.

Apart from that, for the purpose of protection or obtaining power in the market, monopolists tend to behave in such a way which may harm the competition process in the market. The aim to

obtain market power is evidenced when a dominant supplier in the market buys all raw materials in order to exclude his competitor which amounts to market foreclosure, resulting harm in the competition process.

Thus, this article attempts to discuss the roles of Malaysia competition law in regulating anti-

competitive behavior in business practices. The first part of this article highlights the meaning and types of anti-competitive practices, followed by a brief overview of competition law in Malaysia. This article will further provide discussion on the roles of competition law in

regulating business conducts and highlight several issues which may be relevant for consideration by the competition authority in order to encourage fair business practices in the

market.

ANTI-COMPETITIVE PRACTICES: ITS DEFINITION AND TYPES

Definition

Anti competitive practices or also known as restrictive business practices (Goode, W., 2007) refers to a wide range of business practices in which a firm or group of firms may engage in order to restrict inter-firm competition to maintain or increase their relative market position and

profits without necessarily providing goods and services at a lower cost or of higher quality (https://stats.oecd.org/glossary/detail).

Generally, anti-competitive practices relate to business practices which aim to restrict fair competition in the market for the purpose of maintaining market power. However, in

determining which types of business practices are considered as anti-competitive varies by jurisdictions because each jurisdiction sets its own legal criteria in determining anti-competitive

practices. Anti-competitive practices as indicated by the Competition Act 2010 refer to two kinds of conducts, which are participating in anti-competitive agreement and abuse of dominant position.

Types of anti-competitive practices

According to Walter Goode, competition law in most jurisdictions deals with the following kinds of firm behavior; horizontal arrangement, vertical arrangement, misuse of market power by monopolies and control of mergers and acquisitions (Goode, W., 2007). As such, it can be

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

17

said that anti-competitive practices commonly relate to three kinds of conducts namely, cartels

which may occur between firms operating at the same level of production (horizontal arrangement) or firms operating at a different level of production (vertical arrangement), abuse of dominant position by an enterprise which is dominant in the market and merger.

Cartels exist as a result of formal or informal agreement between firms which agree to manage

the markets in order to eliminate competition (Goode, W., 2007) while abuse of dominant position occurs when an enterprise which possesses the market power abuses its dominant position in the market by behaving in such a way which restrict competition in the market. For

example, limiting production in order to foreclose the market, refusal to deal or supply or excessive pricing.

On the other hand, mergers relate to combination of operations between two groups of companies. Mergers can take place via different ways such as horizontal mergers, vertical

mergers or conglomerate mergers. Horizontal mergers happen when two competing companies join together and vertical mergers refer to combination of two companies in which one of the

company is a supplier to the other. Another type of merger, known as the conglomerate merger occurs when two companies in different industries combine together (Mushera Ambaras Khan, 2013)

In Malaysia, the Competition Act 2010 includes only two kinds of anti-competitive practices

namely prohibition from participating in anti-competitive agreement and abuse of dominant position (Part II of the Competition Act 2010). These two conducts which are declared as anti-competitive demands fulfillment of several criteria under the Competition Act 2010 before

enterprises can be declared as engaging in anti-competitive practices. For example, under Section 4 (1) of the Competition Act 2010, it requires enterprises to engage in ―horizontal or

vertical agreement‖ which has ―the object or effect of significantly preventing, restricting or distorting competition in any market for goods or services.‖ On the other hand, an enterprise is regarded as abusing its dominant position in the market if the dominant enterprise carry its

conduct in any ways listed under Section 10(2)(a) – (g) of the Competition Act 2010, namely, imposition of unfair trading condition to suppliers or customers, limiting production, market

outlets, technological development or investment to the prejudice of consumers, refusal to supply to a particular enterprise, applying different conditions to equivalent transactions with other trading partners, tying or bundling, predatory pricing and market foreclosure.

Provisions relating to mergers are excluded from the Competition Act 2010 due to the needs to

―promote global corporate competition and to further strengthen the economy of Malaysia.‖ The decision to exclude mergers from the Competition Act 2010 was highlighted by the Minister, Dato‘ Sri Ismail Sabri bin Yaakob during the presentation of the competition bill after ―taking

into account views from various agencies such as Bank Negara Malaysia and Securities Commission Malaysia‖ (Penyata Rasmi Parlimen Dewan Rakyat, 20 April 2010).

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

18

COMPETITION LAW IN MALAYSIA The competition regulation in Malaysia was initially regulated by sectors - the energy and the communication sectors. The provisions relating to competition rules are incorporated in their respective legislations, indicating prohibitions relating to anti-competitive practices. For

example, the Communications and Multimedia Act 1998 prohibits a licensee from “engaging in any conduct which has the purpose of substantially lessening competition in a communications

market” (Section 133 of the Communications and Multimedia Act 1998) while Section 135 Communications and Multimedia Act 1998, prohibits a licensee from entering into any understanding, agreement or arrangement which provides for rate fixing, market sharing,

boycott of a supplier of apparatus or boycott of another competitor. On the other hand, the energy sector provides a general provision relating to competition which can be seen in Section

14(1) (h) of the Energy Commission Act 2001. Section 14(1) (h) of the Energy Commission Act 2001 gives power to the Energy Commission to “promote and safeguard competition and fair and efficient market conduct or, in the absence of a competitive market, to prevent the misuse of

monopoly or market power in respect of the generation, production, transmission, distribution and supply of electricity and the supply of gas through pipelines.” It is pertinent to note that,

although competition law has been regulated by the abovementioned sectors, it does not cover other kinds of commercial activities.

Hence, a bill known as Fair Trade Practices Bill was introduced and approved on the 26th of October 2005 in the Parliament, the purpose of which is to accommodate the growth of trade

and business and encourage fair competition in business. The Fair Trade Policy seeks to accomplish several policy objectives which, among others include; to promote and protect market competition, produce active and competitive entrepreneurs, create fair and competitive

market prospects as well as to hinder anti-competitive practices that affect domestic market in order to prevent unjust trade practices.

Competition laws in Malaysia refer to the following; the Competition Act 2010 and the Competition Commission Act 2010 including any subsidiary legislation made under the

abovementioned laws (Section 2 of the Competition Commission Act 2010). The Competition Act 2010 mainly consists of provisions relating to the application of competition law in

Malaysia. The Competition Act 2010 mainly highlights the coverage of the Competition Act 2010 including commercial practices prohibited by the competition law, procedures relating to investigation, imposition of penalty and appeal procedures.

On the other hand, the Competition Commission Act 2010 provides provisions relating to the

establishments, powers and functions of the MyCC as well as other matters connected therewith. In brief, the Competition Commission Act 2010 elaborates on the establishment of the MyCC including the functions and powers of the MyCC as well the financial aspect of the MyCC such

as establishments of the Competition Commission Fund and the management of the fund.

Apart from the abovementioned legislations on competition law, it is also worth mentioning that the application of the competition laws in Malaysia is assisted by soft laws, which takes the form of guidelines. At present, the guidelines issued by the competition authority in Malaysia

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

19

are Guidelines on Leniency Regime, Guidelines on Financial Penalties, Guidelines on the

Market Definition, Guidelines on Complaints Procedures, Guidelines on Abuse of Dominant Position and Guidelines on Anti-Competitive Agreement. These guidelines are general in nature, applicable to all commercial activities, their main function being to provide clarification relating

to existing provisions in the Competition Act 2010 for the purpose of implementing and deciding issues in competition law.

ROLES OF MALAYSIA COMPETITION LAW IN REGULATING ANTI-

COMPETITIVE BUSINESS PRACTICES The roles of competition law varies depending on the aims and objectives of the competition

law in a particular jurisdiction. In relation to Malaysia, the primary objectives of the competition law can be deduced from the preamble of the Competition Act 2010 which provides for the promotion of economic development and protection of consumer‘s interest. The

Competition Act 2010 further provides that, for the purpose of promoting economic growth, the process of competition is to be protected because such process encourages efficiency,

innovation and entrepreneurship which will promote competitive prices, improvement in the quality of products and services as well as serving wider choices for consumers (Preamble of the Competition Act 2010).

The application of the Competition Act 2010 covers all commercial activities within and outside

Malaysia regardless of the status of the entity that carries them out. This is an indication that associations, government-linked companies (GLCs) as well as SMEs are not excluded from the coverage of Competition Act 2010 as expressly provided under Section 3 of the Competition

Act 2010. By virtue of Section 3(4) of the Competition Act 2010, commercial activity refers to ―any activity of a commercial nature‖ but does not include activities authorized by the

government whether direct or indirect, activities which are based on solidarity principles and purchase and offering of goods and services which are not part of any economic activity.

The discussion below attempts to highlight the roles of competition law in regulating anti-competitive business practices.

(i) Preventing collusion in the market under Section 4 of the Competition Act 2010

In order to prevent collusion in the market, Section 4(1) of the Competition Act 2010 prohibits enterprises from participating in horizontal or vertical agreement which has the object or effect

of significantly preventing, restricting or distorting competition in any market for goods or services. The term ‗enterprise‘ as referred to in Section 4 (1) of the Competition Act 2010 means ‗any entity carrying on commercial activities relating to goods or services‘. The term

‗agreement‘ as employed by Section 4(1) of the Competition Act 2010 refers to the following: any form of contract, arrangement or understanding, whether or not legally enforceable and

includes a decision by an association and concerted practices. The term ‗concerted practice‘ refers to secret co-operation made among enterprises, usually between competitors. Section 2 of the CA 2010 elaborates the meaning of ‗concerted practice‘:

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

20

any form of coordination between enterprises which knowingly substitutes practical

co-operation between them for the risks of competition and includes any practice which involves direct or indirect contact or communication between enterprises, the object or effect of which is either—

(a) to influence the conduct of one or more enterprises in a market; or

(b) to disclose the course of conduct which an enterprise has decided to adopt or is contemplating to adopt in a market,

in circumstances where such disclosure would not have been made under normal conditions of competition.

It is therefore submitted that the usage of the term ‗agreement‘ under the Competition Act 2010 is broad. The inclusion of contract under the term ‗agreement‘ signifies that it may be a written

or unwritten agreement since contract may exist regardless whether it is made orally or in writing. Other conducts such as arrangement, understanding, decisions by associations as well as

secret cooperation indicate that informal arrangements are not excluded from the ambit of ‗agreement‘ under the Competition Act 2010. Further, the Competition Act 2010 expressly mentions that contract, arrangement and understanding need not be legally enforceable in order

to fall within the meaning of ‗agreement‘ under the Section 2 of the Competition Act 2010.

Section 4(1) of the Competition Act 2010 expressly provides that agreements which have the object or effect of significantly preventing, restricting or distorting competition in any market for goods or services are prohibited, regardless whether such agreement is horizontal or vertical.

Horizontal agreement is agreement between enterprises operating at the same level of production. In contrast, vertical agreements refer to agreement concluded between enterprises

functioning at different levels of production.

The significant role of competition law in combating collusion in the market can be seen when the Competition Act 2010 declares that horizontal agreement whose objectives are either to fix price, to allocate markets between competitors, to limit or control production and bid rigging as

anti-competitive. Some of the instances in which this provision is violated can be seen when entrepreneurs agree among themselves to enter into price fixing agreement. As in the case

involving four container depot operators and an information technology service provider, the MyCC was of the opinion that these entrepreneurs engaged in price fixing which may result to financial penalty (Case Number: MyCC.700.2.005.2013).

Although scholars such as Mark Furse suggests that horizontal agreement is prone to distort

competition in the market rather than vertical agreement (Furse,M, 2008), vertical agreement is not excluded from the provision of anti-competitive agreement under the Competition Act 2010.

In fact, it is also recognized by the Malaysia Guidelines on Chapter 1 Prohibition under paragraph 3.11 which expressly provides that ‗vertical agreements in general are less harmful to competition than horizontal agreements‘. According to Tilottama Raychaudhuri, vertical

agreement may to a certain extent be anti-competitive when the firm imposing a vertical restraint

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

21

possesses market power which will consequently limit competition from other firms products.

For example, in an exclusive supply agreement, a manufacturer usually restricts distributors from acquiring products from other manufacturers. This kind of restriction might harm competition in the market because of its ability to foreclose the market and encourage collusion (Tilottama

Raychaudhuri, 2011).

This may be the reason why vertical agreement is included in the prohibition under Section 4(1)

of the Competition Act 2010. However, the determination of whether vertical agreement is anti-competitive is rather flexible since it employs rule or reason approach. In contrast, assessment of horizontal agreement is based on the deeming provision under Section 4(2) of the Competition

Act 2010, commonly known as per se rule. Once a horizontal agreement contains objects indicated under Section 4(2) of the Competition Act 2010, it is highly regarded as anti-

competitive. (ii) Preventing abuse of market power under Section 10 of the Competition Act 2010

Abuse of dominant position is another restriction provided in the Competition Act 2010 which

aims to control enterprises from abusing their dominant position in the market. Dominant position occurs when ―one or more enterprises possess such significant power in a market‖ so as to enable them to ―adjust prices or outputs or trading terms, without effective constraint from

competitors or potential competitors.‖ The above definition on dominant position as referred to by the Competition Act 2010 suggests that it does not prohibit entrepreneurs from possessing

dominant positions in the market. This is supported by the provision in Section 10 (1) of the Competition Act 2010 which provides that only those dominant enterprises which engage in conducts listed under Section 10(2) (a) to (g) would amount to abuse of dominant position.

Section 10(2) (a)-(g) of the CA 2010 provides a non-exhaustive list of abusive behavior by

dominant position which include excessive pricing, market foreclosure, refusal to deal or license, tying and bundling, and predatory pricing. Excessive pricing relates to a situation in which entrepreneurs would raise prices by restricting output. As a result, consumers who

purchase the goods would have to pay more due to the absence of competitive condition (Graham,C, 2013). Market foreclosure occurs when a supplier who is in a dominant position

buys all raw materials in order to exclude his competitor from the market while refusal to deal may occur when entrepreneurs set unacceptably high price in order to refuse request of supply (Liyang Hou, 2011).

Tying, on the other hand refers to a situation where the customer is forced to buy a second

product from the seller, failing which the seller would refuse to sell the first product to the customer while predatory pricing refers to entrepreneurs who excludes rivals from the market by setting prices below cost.

Recent examples can be seen in the case where MyCC proposed to impose financial penalty to

My EG Services Bhd (MyEG) for infringing Section 10 of the Competition Act 2010.

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

22

According to MyCC, MyEG contravenes Section 10 (2) of the Competition Act 2010 by

applying different conditions to equivalent transactions with other trading parties to the extent that may harm competition (Case Number: MyCC (ED) 700-1/1/2/2015).

Enforcement of provisions of the Competition Act 2010

The MyCC is an independent body under the Ministry of Domestic Trade, Co-operatives and Consumerism whose function is to enforce provisions contained in the Competition Act 2010. At present, the chairperson of the MyCC is YBhg Tan Sri Dato‘ Seri Siti Norma Yaakob who

was formerly a Chief Judge of Malaysia. The MyCC consists of a Chairman, four representatives from the government and three to five members made up of those

knowledgeable in commerce (Section 5 of the Competition Commission Act 2010). MyCC is vested with powers to enforce competition law (Section 16(d) of the Competition

Commission Act 2010) including imposition of penalty for infringement of competition law provisions ( Section 17(2)(b) of the Competition Commission Act 2010 ), organizing competition

law awareness programs among the public (Section 16(i) (j) of the Competition Commission Act 2010 )giving advices and alert the Minister in matters relevant to competition law especially when dealing with international agreements (Section 16(a),(b),(k) of the Competition

Commission Act 2010), perform studies in relation to issues relevant for competition law in Malaysia (Section 16(g) of the Competition Commission Act 2010) and to act as an advocate for

competition matters under Section 16(f) of the Competition Commission Act 2010. Enforcement of competition law in Malaysia takes two approaches, namely soft and hard

approaches. Soft approach refers to enforcement of competition law by the MyCC without imposing financial penalty to infringers. For example, the case of Cameron Highland

Floriculturist Association (CHFA) which was the earliest case decided by the MyCC relating to infringement of Section 4 (2) (a) of the Competition Act 2010 on price fixing. In that case, the MyCC decided that no financial penalty will be imposed to CHFA because the competition law

at that time was still in its infancy. Hence, the MyCC decided that stern warnings and advises to CHFA were sufficient to educate CHFA to comply with the competition rules. The MyCC

required the CHFA to perform the following act: to cease and stop the act of fixing prices of flowers; to provide responsibility on its members to refrain from any anti-competitive practices in the relevant market and to publish the remedial actions taken by them in the mainstream

newspapers (Case Number: MyCC/0003/2012(ACA).

On the other hand, hard approach takes place when the MyCC imposes financial penalty to infringers such as the case of ice manufacturers who agree among themselves to increase the

price of ice cubes. Their agreement to raise the price of ice cubes was published in the local newspapers. After due investigation by the MyCC, it was decided that the ice manufacturers

infringed Section 4(2)(a) of the Competition Act 2010 which resulted in financial penalty imposed by the MyCC (Case Number: MyCC.700.2.0001.2014).

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

23

Apart from that, the MyCC may accept undertaking from enterprises subject to the conditions

imposed by the MyCC. This is expressly provided under Section 43(1) of the Competition Act 2010. In the event the MyCC accepts an undertaking from enterprises in relation to an infringement, such enterprises will not be imposed financial penalty and the investigation will

be closed. Examples are cases involving Barbers Association (MIHSOA) and Malaysia Lorry Owners Association (PMLOA). The Chairman of Barbers Association issued media statement

relating to increase in the price of haircut. The Chairman of the Association further warns that members of the Association who fail to follow the decision will be taken action upon by the Association (http://www.mycc.gov.my/sites/default/files/Undertaking-Barbers.pdf). Similarly,

in the case involving Malaysia Lorry Owners Association (PMLOA) who agrees to fix transport charges for lorry services indicates violation of Section 4(2)(a) of the Competition Act 2010

(http://www.mycc.gov.my/sites/default/files/Undertaking-PMLOA.pdf). In both cases, the MIHSOA and PMLOA provide undertakings not to proceed with their decision to fix prices and directed their members to cease and desist from further implementing the decision. Their

undertakings have been accepted by the MyCC in accordance with Section 43 of the Competition Act 2010.

CHALLENGES AHEAD The coming into force of the Competition Act 2010 in Malaysia is seen as a step towards promoting fair competition in the market. The Competition Act 2010 is a comprehensive

legislation since it contains common provisions relating to anti-competitive practices whose purpose is to act as a legal mechanism in combating unfair business behavior in the market.

Nevertheless, there are few issues that need to be observed by the Malaysia competition authority in order to ensure competition law can be implemented effectively in Malaysia. The issues are as follows:

(i) Issues relating to mergers

Since there is absence of specific provisions controlling mergers and acquisitions under the Competition Act 2010, it indicates that there is a lack of a comprehensive regime regulating

anti-competitive mergers and acquisitions in Malaysia. At present, mergers and acquisitions in Malaysia are regulated by sectors such as Bank Negara Malaysia, Malaysia Communication and

Multimedia Commission and Energy Commission. Takeovers and mergers may infringe the competition law especially when parties in horizontal mergers decide to share information such as pricing information with competitors. Another

instance is when the merger has taken place, there is a risk of abuse of dominant position in the market because combination of two companies in the market would result in a dominant

position which may lead to abuse of dominant position and cartel. (ii) Issues relating to intellectual property

Intellectual property becomes part of the discussion under competition law when intellectual

property holders engage in practices not authorized by intellectual property law but seem to have

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

24

anti competitive effects (Hovenkamp, H.J., 2008). The main concern relating to intellectual

property is due to the fact that intellectual property is governed by laws relating to intellectual property, while the manner in which such intellectual property is to be exercised may be subject to competition law observation. Competition authority should be careful when dealing with

intellectual property matters because too strict assessment of competition law in intellectual property matters may restrict innovation.

Examples of intellectual property issue which falls within the ambit of competition law is when

intellectual property owners enter into licensing agreement. Some intellectual property licensing agreement has the possibility to create dominant market power and foreclose the market from

competitors. Other situations such as contractual restrictions contained in the intellectual property licensing agreement may be used to cover market sharing agreements which is prohibited under the competition law (Anderman, D.S. & Schmidt,H., 2009).

The current situation requires issues relating to intellectual property to be dealt by using the

provisions contained in the Competition Act 2010 and the existing general guidelines. However, based on Paragraph 4 of the Guidelines on Chapter 1 Prohibition, the MyCC endeavor to issue a separate guideline in near future to deal with intellectual property matters.

CONCLUSION AND RECOMMENDATION The foregoing discussion showed significant roles of Malaysia competition law in regulating

business conduct namely, prohibiting business operators from participating in anti-competitive practices, prevention of abuse of dominant position by dominant business

operators in the market and enforcement of competition law by a specific body regulating competition law in Malaysia, which is the MyCC.

However, specific provisions relating to mergers in the Competition Act 2010 are yet to be incorporated in the Competition Act 2010. Taking into consideration the possibilities of

infringement of competition law in the event mergers takes place, it is suggested that provisions relating to mergers be incorporated in the Competition Act 2010 so as to prevent abuse of dominant position in the market.

Another area of concern is relating to implementation of competition law in intellectual

property matters. Although the Competition Act 2010 provides provisions relating to conducts condemned by the competition law, the provisions and guidelines contain general application, which applies to all kinds of commercial activity. In the field of intellectual

property, it is suggested that specific guidelines would be helpful because guideline is able to provide a framework which can be used by the competition authority in deciding issues relating

to intellectual property (Carrier, M.A., 2002). Further, as practiced in Europe and United States of America, the existence of a specific guideline relating to intellectual property provides additional assistance to the competition authority as well as illustrative examples to solve arising

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

25

issues relating to intellectual property and competition law. As for Malaysia, the specific

guideline for intellectual property will serve as a guide to the MyCC in solving issues on competition law related to intellectual property.

REFERENCES

Anderman, D.S & Schmidt, H. (2009). EC Competition Law and IPRS in The Interface between Intellectual Property Rights and Competition Policy. United Kingdom: Cambridge University.

Carrier, M.A. (2002). Unraveling the Patent-Antitrust Paradox. University of Pennsylvania Law

Review, 150(3), 761-854. Decision of Competition Commission. (30 January 2015). Infringement of Section 4(2)(a) of the

Competition Act 2010 by TwentyFour (24) Ice Manufacturers of Kuala Lumpur, Selangor, and Putrajaya (No. MyCC.700.2.0001.2014) . Retrieved from

http://www.mycc.gov.my/sites/default/files/24IceManufacturers.pdf Decision of the Competition Commission. (24 June 2016). Infringement of section 10 of the

Competition Act 2010 by My E.G. Services Berhad (MyCC File Reference: MyCC (ED) 700-1/1/2/2015). Retrieved from http://www.mycc.gov.my/sites/default/files/Section-40-

Notice-of-Finding-of-an-Infringement-by-My-Services-Berhad.pdf Decision of the Competition Commission. (1 June 2016). Infringement of section 4(1) and 2(a)

of the Competition Act 2010 by Containerchain ( Malaysia) Sdn Bhd, AYZA Industries Sdn Bhd, ICS Depot Services Sdn Bhd, E.A.E. Depot & Freight Forwarding Sdn Bhd,

Prompt Dynamics Sdn Bhd.(MyCC File Reference: MyCC (ED) 700.2.005.2013). Retrieved from http://www.mycc.gov.my/legislation/case

Decision of the Competition Commission. (6 December 2012). MyCC/0003/2012(ACA). Retrieved from

http://www.mycc.gov.my/sites/default/files/CameronHighlandsFloriculturistAssociation.pdf

Furse, M. (2008). Competition Law of the EC and UK. Sixth Edition. United States: Oxford University Press.

Goode,W. (2007). Dictionary of Trade Policy Terms. Fifth Edition. United Kingdom:Cambridge

University Press.

Graham,C. (2013). EU & UK Competition Law. United Kingdom: Pearson.

Hovenkamp, J,H. (2008). The Intellectual Property-Antitrust Interface. University of Iowa Legal

Studies Research Paper. University of Iowa, 1979-2006.

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

26

Liyang Hou. (2011). Excessive Prices within EU Competition Law. European Competition Journal, 7, 47-70.

Musheera Ambaras Khan. (2013). A Guide to Malaysian Takeovers and Mergers Law. Malaysia: Sweet & Maxwell Asia.

OECD Glossary of statistical terms. Retrieved from https://stats.oecd.org/glossary/detail. Parlimen Malaysia. ( 20 April 2010). Penyata Rasmi Parlimen Dewan Rakyat. Retrieved

from http://www.parlimen.gov.my/hansard-dewan-rakyat.

Tilottama Raychaudhuri. (2011). Vertical restraints in Competition Law: The Need to Strike the Right Balance Between Regulation And Competition. NUJS Law Review, 4, 609-624.

Undertaking by the Malaysia Indian Hairdressing Saloon Owners Association. (2014).

Retrieved from http://www.mycc.gov.my/sites/default/files/Undertaking-Barbers.pdf. Undertaking by the Pan Malaysia Lorry Owners Association. (2014). MyCC Reference

Number 700.2.0036.2013. Retrieved from http://www.mycc.gov.my/sites/default/files/Undertaking-PMLOA.pdf.

Whish, R. (2009). Competition Law. New York: Oxford University Press.

STATUTES

Competition Act 2010 ( Act 712).

Competition Commission Act 2010 (Act 713). Communications and Multimedia Act 1998 (Act 588). Energy Commission Act 2001 ( Act 610).

Haliza A.Shukor

Faculty of Syariah & Law

Universiti Sains Islam Malaysia [email protected]

Prof Dr Nazura Abdul Manap

Faculty of Law

Universiti Kebangsaan Malaysia [email protected]

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

27

Effect Of Receivables Turnover To Profitability

Pt. Bii Finance Center Period 2010-2014

(Kesan Pusingganti Belum terima Keatas Keuntungan Pt. Pusat Kewangan Tempoh 2010-2014)

Fia Dialysa

Sekolah Tinggi Ilmu Ekonomi (STIE) EKUITAS

Bandung, Indonesia

ABSTRACT

Globalization encourages all parties to survive in the increasingly fierce competition and

business activity demanding high mobility of the business people. Society requires excess funds in order to turn around its business well. Non-bank financial institution is an alternative choice to provide funds for the community (Presidential Decree No. 61/1988 and Presidential Decree No.

9/2009). Healthy financial institutions are important in supporting the National economy (Ministry Decree No. 84/ PMK.012/2006 & Regulation FSA/POJK.05/2014). Leasing is a non-

bank financial institution that are needed at this time where the demand for vehicles is high because people mobility is increasing. The purpose of this study is to determine the effect of receivables turnover to profitability of PT. BII Finance Center in the period of 2010-2014. This

quantitative research uses simple linear regression analysis techniques with normality test, autocorrelation test, heteroscedasticity test, correlation coefficient, coefficient of determination

and t test. The method used is descriptive and verification, with data technique accumulation by documentary study and literature study. The data obtained are secondary data derived from the financial statements PT. BII Finance Center period of 2010-2014. The results of this study

indicate that Receivables Turnover has no significant effect to Profitability (ROA).

Keywords: Receivables Turnover; Profitability; Pt.Bii Finance Center

ABSTRAK

Globalisasi menggalakkan semua pihak untuk terus bertahan dalam persekitaran yang mana persaingan semakin meningkat dan permintaan yang tinggi terhadap aktiviti perniagaan

menuntut mobiliti tinggi dari ahli perniagaan. Masyarakat memerlukan lebihan dana bagi memastikan perniagaan mereka berjalan dengan baik. Institusi kewangan bukan bank adalah merupakan alternatif bagi menyediakan dana kepada masyarakat (Presidential Decree No.

61/1988 and Presidential Decree No. 9/2009). Institusi kewangan yang kukuh adalah penting dalam menyokong Ekonomi Nasional (Ministry Decree No. 84/ PMK.012/2006 & Regulation

FSA/POJK.05/2014). Pajakan adalah merupakan Institusi kewangan bukan bank yang diperlukan pada masa sekarang yang mana permintaan bagi kenderaan adalah tinggi disebabkan oleh mobiliti manusia semakin meningkat. Tujuan kajian ini dilakukan adalah untuk

menentukan kesan pusingganti belum terima terhadap keuntungan PT. BII Pusat kewangan dalam tempoh 2010-2014. Kaedah penyelidikan kuantitatif menggunakan teknik analisa regresi

linear mudah dengan ujian normaliti, penentuan „coefficient‟ dan ujian t. Kaedah yang

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

28

digunakan adalah deskriptif dan verifikasi, dengan teknik pengumpulan data melalui kajian

dokumentari dan kajian lepas. Data diperolehi dari data sekunder yang diperolehi daripada penyata kewangan PT. BII Pusat kewangan bagi tempoh 2010-2014. Hasil kajian mendapati bahawa pusingganti belum terima tidak memberi kesan signifikan keatas keuntungan (ROA).

Kata kunci: Pusingganti belum terima, keuntungan PT, pusat kewanganility Bii

INTRODUCTION

The economic crisis that occurs in Indonesia today, marks high economic competitiveness (the

era of free markets), political instability of economic conditions and commodity prices rising in the market, one of which is the economic crisis that occurred in China. According to CNBC sources on Friday (01/22/2016), China used its huge debts to stimulate economic growth in the

financial crisis. As a result, the burden of debt in local currency of each country continues to rise in the economic slowdown of countries with low economy.

The company as an economic builder also improved their business strategies to survive and help recover the national economic crisis, one of which is finance companies (leasing). Leasing as

one of the non-bank financial institutions showed uniquely ―no down payment‖. Financing can be granted up to 100% (full payout), which will help cash flow, especially for companies (lessee)

newly established or operating and growing company. Consumer finance in leasing becomes very important for a company because it can help them to increase sales of products or services.

Moreover, it is becoming important also for consumers because the consumer finance companies can help consumers to buy goods or services on credit.

Consumer financing is one of the formal financial institutions in Indonesia which is still relatively new. These institutions grow and develop along with the issuance of legal institutions

in the form of Decree (68/1988). Thus, now the existence of consumer finance shows a very good development. The rapid growth of the consumer finance business once again shows the

high public interest to buy charcoal-goods in installments along with the increasing living standard of the middle and lower layers. The development of consumer finance is also due to the constraints for low income people to access funds from other sources.

There are four reasons that encourage the development of consumer finance, namely: (1) Limited

formal financial resources (2) Difficulties in developing credit unions (3) Banks do not serve the consumer finance (4) Funding from moneylenders. Following the trend of the automotive industry, consumer finance business line of motor vehicle finance portfolio recorded a decrease

in finance receivables in the first quarter of 2015. Based on data from the Financial Services Authority cited Business (19.05.2015), consumer financing receivables in January-March

continued to fall despite the decline in numbers is still conservative. In detail, the decline in consumer financing receivables fell to 0.15% from Rp 246,54 trillion to Rp 246,16 trillion in February 2015. In March, receivables refinancing sagged a little in the position of Rp 246,14

Journal of Management & Muamalah, Vol. 6, No. 2, 2016

eISSN 2180-1681

29