Embed Size (px)

DESCRIPTION

Citation preview

Issues of Sustainability of Indian Rural Credit Co-operatives: A study in Kerala State, India

Jose A. MATHAI1

Introduction

The ultimate objective of the National Policy on co-operatives in India (Government ofIndia, 2002) is to provide support for the promotion and development of co-operativesas autonomous, independent and democratic organizations, so that they can play theirdue role in the socio-economic development of the country. It recognizes the distinctidentity of co-operatives and supports their values and principles by persuading statesto provide them an appropriate administrative and legislative environment in which tooperate. With the changes in the Indian economy since 1991, the co-operative sectorhas needed to focus on cost effectiveness of its operations and ensure returns frominvestments made in various economic activities in order to withstand competition.

The co-operative credit structure in India can be broadly classified into two segments.While the urban areas are served by Urban Co-operative Banks (UCBs), rural co-operatives operate in the rural parts of the country. The rural Co-operative CreditStructure (CCS) in India consists of two wings namely; Short-term and Long-term creditstructures. The Short-term co-operative credit structure is federal in character, and dealswith short- and medium-term credit for agricultural purposes. It is mostly based on athree tier pattern with the State Co-operative Banks (SCB) at the Apex level, DistrictCentral Co-operative Banks (DCCB) at the Intermediary level and Primary AgriculturalCredit Societies (PACS) at the village level. All types of primary societies are federatedinto DCCB at the district level which, in turn, are federated into the SCBs at the statelevel (i.e. Apex level).

As per the RBI (Reserve Bank of India, 2011) report at the end of March 2010, there wasa total 95,765 rural co-operative institutions operating in the country. Out of the totalnumber of rural co-operatives, short-term co-operatives constituted a majority whileonly one per cent of the total co-operatives operating in the country were long-term innature. Within the short-term structure, the ground level institutions PACS incurred hugelosses. This has severely affected their ability to provide credit in full and in time to the

The Amazing Power of Cooperatives ...179...

12-Mathai_Mise en page 1 12-09-05 14:15 Page179

rural clientele. This led to a drop in the market share of short-term credit distributed,from 77% in 1973-74 to 27% in 2008-09, while that of long-term credit by co-operatives dropped from 65% to 16% during the same period (Table 1).

The performance of short-term CCS had a different story in the State of Kerala, wherethey showed a noticeable difference in their performance; for instance, Kerala had amembership of 14,000 per PACS while at national level, it was 1,336. The Kerala co-operatives are outperforming Indian averages on indicators like owned funds, depositsand loans outstanding. This paper provides an analysis on the current state of affairs ofthe PACS in Kerala.

Statement of the problem and objective of the study

Liberalization of the co-operative movement in India sought to create commerciallyautonomous member-based co-operatives that would be democratically andprofessionally managed business ventures. The government in India viewed co-operativesas an instrument of rural development, which led to its partnership in co-operativedevelopment. In the contemporary environment of free market forces, and the vigorousdecentralization of governance in India, the importance of co-operatives is increasinglyrecognized. On both counts, co-operatives can play a major role in bringing equity andmobilizing the collective consciousness of the people. Kerala is one of the few states inthe country where the credit co-operative sector has gained considerable momentum,and has made a considerable impact on its economy. However, PACS in Kerala has shownsigns that question the co-operative character as well as its sustainability. Therefore,with the objective of exposing the performance and sustainability issues of PACS in thestate of Kerala, India, the following study was conducted.

Materials and methods

The data used in this analysis is mainly secondary data that was collected from the websitesof the following organizations: the National Federation of State Co-operative Banks Ltd.(NAFSCOB, www.nafscob.org); the National Bank for Agriculture and Rural Development(NABARD, www.nabard.org); the Reserve Bank of India (RBI, www.rbi.org.in); the Departmentof Co-operation, Government of Kerala (www.cooperation.kerala.gov.in); Kerala StatePlanning Board (www.spb.kerala.gov.in); Annual Reports of Kerala SCB; and the AnnualReports of Vellanikkara Service Co-operative Bank Ltd. The reference period for datacollected generally falls between 2003 and 2011, but due to non-availability of data insome cases, the analysis did not strictly follow the reference years stated.

The primary data collected was used to support the secondary data. Two PACS – VellanikkaraService Co-operative Bank Ltd (VSCB) and Adat Farmers Service Co-operative Bank (AFSCB)

...180... The Amazing Power of Cooperatives

12-Mathai_Mise en page 1 12-09-05 14:15 Page180

– were studied in order to elicit local/ground level realities. Focus group discussions wereheld with members, non-members, employees of the PACS and officials of Thrissur DCB andKSCB. Meetings were also held with some co-operative leaders and government officials,such as the Assistant Registrar, in order to get their views about the working of co-operativesin the State of Kerala. Simple statistical tools such as percentages, rations and compoundannual growth rates are used to analyze the data collected.

Indian co-operatives - a brief history

The growth of the co-operative movement in India to its present size and operating levelsis broken into different phases. The first phase takes place between 1900 and 1930. In1904, the Co-operative Societies Act was passed and “co-operation” became a provincialsubject by 1919. The second phase from 1930 to 1950 was marked by the majordevelopment of the pioneering role played by RBI in guiding and supporting the co-operatives. However, even during this phase, signs of sickness in the Indian ruralco-operative movement were becoming evident. Nevertheless, the third phase, between1950 and 1990, marked a continuation of co-operative credit society growth. The AllIndia Rural Credit Survey committee (1954) not only recommended state partnership interms of equity but also partnership in terms of governance and management. Thepreoccupation of the government with the co-operative sector and its potential forbringing about development, right up to the ’90s, resulted in an increase in the numberof co-operatives and their contribution, making the Indian co-operative movement oneof the largest movements of its kind in the world.

The fourth phase, which takes place from the early 1990s to the present, culminateswith the process of economic reforms that were initiated in 1991 in response to changesin the external and internal economic environment. The major objectives of theeconomic reforms included: market orientation of the economy, increasing private sectorinitiatives, improving efficiency in government spending, enhancing export compe -titiveness, foreign capital inflows, stabilizing balance of payments and revamping manysectors of the economy such as industry, trade, finance, infrastructure, etc. By this time,co-operatives had a much deeper reach, with nearly four times the number of accountsthan commercial (public sector) banks (Government of India, 2009). The Fourth Phasesaw an increasing realization of the disruptive effects of intrusive state patronage andpoliticisation of the co-operatives, especially financial co-operatives, which resulted inpoor governance and management and the consequent impairment of their financialhealth. A number of committees were set up to suggest reforms in the sector.

Some of the key committees that significantly contributed to the development of themovement in India were: the All India Rural Credit Survey Committee (1954); the Mirdha

The Amazing Power of Cooperatives ...181...

12-Mathai_Mise en page 1 12-09-05 14:15 Page181

Committee on co-operatives (1965); the All India Rural Credit Review Committee (1969);the Committee to Review Arrangements for Institutional Agriculture and RuralDevelopment (1981); the Agricultural Credit Review Committee (1989); the ExpertCommittee on Rural Credit (2001); the Committee on Model Co-operative Act (1991);the task force to Study the Functions of the Co-operative Credit System and to SuggestMeasures for its Strengthening (1999); the Expert Committees on Short and Long TermCredit Structures (2004 and 2006); and the High Powered Committee on Co-operatives(2009).

The expert committees had identified the following as the underlying factors responsiblefor the present state of affairs of PACS: Low motivation or involvement of members;ineffective supervision, including audits by state registrars or the co-operative department,leaving frauds or embezzlements either undetected or, if detected, not followed up. MostPACS have run into losses due to overstaffing, high cost of transactions and the high interestthey pay. PACS were also forced to undertake un-remunerative non-credit functions likepublic distribution systems, purchasing and sale of fertilizers to members, procurement offood grains and running consumer stores, etc. The co-operative credit system also suffersfrom impaired governance, management and financing. Some of the other critical problemsfaced by the PACS in India as identified by the expert committees were: failure to inculcateessential co-operative values, increasing incidence of non-viability, politicization andexcessive government intervention, lack of cost competitiveness, deficiency of efforts incapital formation, non-recognition of co-operatives as economic institutions, inability toattract and retain competent professionals and a dearth of skilled staff.

In India, there are many studies on the co-operative credit movement by eminent scholars.The studies of Baviskar (1968), Satyasai and Badatya (2000), Shivamaggi (1996),Puhazhendhi and Jayaraman (1999), Desai and Namboodiri (1993) and Urs andChitambaram (2000) have all influenced the intellectual thinking in India’s approach to co-operatives.

These studies have revealed that sustainability of co-operative credit means that the co-operatives need to increase their capital base in order to maintain further expansion of thelending business on a long-term basis. In order to be sustainable, co-operative creditinstitutions are required to have sufficient margin between lending rates and the cost offunds raised for lending to cover non-financial transaction costs. Despite the impressivegains made by the rural credit delivery system in Kerala, there has been deterioration inthe financial health of the co-operative credit institutions. It is argued that the revival ofPACS in India is in the hands of involved members, committed leaders and motivatedemployees. Together they can revive co-operative glory by making it a professional,member-centric and member-driven institution.

...182... The Amazing Power of Cooperatives

12-Mathai_Mise en page 1 12-09-05 14:15 Page182

Unique features of Kerala State and scope for interventionby co-operatives

The Kerala State has an area of 38, 863 sq. kms with a population of 33.4 million, oneof the highest population densities (859/sq.km) among the less developed countries ofthe world. The “Kerala model of development” has been under much discussion indevelopment literature as it has the highest Human Development Index in India, but withmuch lower per-capita income (Government of Kerala, 2012a). Kerala reduced thepercentage of people living below the poverty line from approximately 60% to less than15% during the last three and half decades (1973/74 to 2004/05; Reserve Bank of India,2012: Table 162). Now the task at hand is addressing the remaining 15% of people inneed and below the poverty line, in addition to assuring better services to people in alloccupations. Co-operatives do have scope as the harbingers in helping the governmentto achieve its development goals in the state. The Approach to Agriculture in the12th Five Year Plan (2012-17) from the Government of Kerala focuses on raising incomesfor farmers through increasing productivity, subsidiary occupations, better marketingand thorough promotion of value added products (Government of Kerala, 2012b). Nodoubt, these are the projects that the PACS can do for the farmers of Kerala who wereprone to vagaries of the market mechanism.

Profile of credit co-operatives in Kerala

There are 13,478 co-operatives under the control of Registrar of Co-operative Societiesand another 12,000 co-operatives under the control of Industries Department. Out ofthe 25,478 co-operatives in the state, credit co-operatives have a share of 13% (KSCB,2012).

As of March 31, 2012, there were 1,607 PACS in Kerala with 12.74 million members.About 51.3% of them were making a profit while 45.1% were operating at a loss and1.5% were dormant and the remaining 2.1% were defunct (KSCB, 2012). Thecomparative performance of PACS in Kerala with respect to their counterparts in the restof the country is remarkable. Kerala had the highest rank with regard to membership,population coverage, borrowing members, loans and advances, deposits mobilisationand share capital contribution. With respect to short-term co-operative credit structures,the state has around 4,807 co-operative bank branches/outlets. This elaborate networkof branches/outlets made Kerala credit co-operatives quite distinct from that of rest ofIndian credit co-operatives.

The operational details of PACS as presented by the Economic Review of the Kerala StatePlanning Board, during the period from 2004 to 2011, have been quite impressive(Government of Kerala, 2012a). For the last seven years, the societies in Kerala are

The Amazing Power of Cooperatives ...183...

12-Mathai_Mise en page 1 12-09-05 14:15 Page183

performing well according to indicators such as average membership, average sharecapital and deposits per society. The CAGR – compound annual growth rate – for theseindicators was 12.01%, 11.95%, and 19.58% respectively. Per member depositsincreased by 6.76% per annum – while that of per society was 19.58%, as seen above– which shows that non-members also deposit at PACS in Kerala. It should be noted that,in Kerala, the percentage of borrowing membership is 151.3% of the total membershipof 19.26 million (NAFSCOB, 2011) meaning that even non-members get loans from co-operatives. The percentage of over-dues to demand was 19.18 % in 2009-10, whichwas less than the national average of 21.93% (NAFSCOB, 2012c: Table XIV).

Kerala’s PACS are unique in many ways as is evident from operational details shown. Inspite of all these strong points, some issues need urgent attention.

Issues of sustainability of PACS in Kerala State

Despite the phenomenal outreach and volume of operation, the health of a very largeproportion of Kerala’s PACS has deteriorated significantly. Let us see these issues in itsdetail:

Membership of co-operatives

The Indian co-operative movement has many co-operative principles that the ICApropagates; the core principles of user-owner, user-benefit and user-managed have beensubdued by the Kerala model of the credit co-operative movement. Essentially, a memberorganisation like PACS could work for the betterment of members in many ways. EachPACS has to decide – based on its members’ needs and its own opportunities andresources – on the services that could be provided by it to the members. Unfortunately,this is not happening as depositors and borrowers of the PACS are not necessarilymembers. Even non-members do more business with co-operatives than the members;as demonstrated above, the borrower percentage against membership is as high as 150%in Kerala; also the major depositors of co-operatives are non-members in Kerala.

Co-operatives lost their ‘voluntary and open membership’ principle and becameinstruments in the hands of the local politicians for maintaining their hold on institutionsthat can provide a sojourn to a multitude of party cadres who aspire to obtain positionsin public institutions to enhance their popularity as a leader. Those who get onto theBoard of Directors need not be actual users of the service because the co-operatives inKerala are the bedrocks of party politics.

As far as co-operative membership is concerned, it has become a situation where thefundamental philosophy of the co-operative – organisation of the weak – is beingquestioned as seen from Table-2. During the period between 2003 and 2011, the shareof weaker sections of the society was getting reduced in India as well as in Kerala. In

...184... The Amazing Power of Cooperatives

12-Mathai_Mise en page 1 12-09-05 14:15 Page184

Kerala, the situation is quite serious as the percentages of the weaker sections– Scheduled Caste (SC), Scheduled Tribe (ST), Rural Artisans (RA) and Small Farmers (SF) –in the co-operative membership were as low as 6.94%, 1.56%, 4.81% and 34.18%respectively.

It is also noted that the percentage of borrowing SF members among members is 20.80%in 2010-11, down from 22.28% in 2002-03. The percentage of SC borrowing membersin total among total borrowing members was just 5.55% and among ST, it was 2.21%.All weaker sections’ share in borrowing membership declined during 2002-03 and2010-11 (see Table-2). It is to be noted that the percentage of other weaker sectionsthat utilise the service of the co-operative is less than proportionate to their size in themembership of co-operative. This is an area of concern as the percentage of the weakersections who make use of cooperative services is less and it is, in fact, an aberrationfrom the original idea of the co-operative movement, which is meant to empowerdowntrodden sections of society. This shows that co-operatives in Kerala became notnecessarily the institutions that serve the interest of poor.

Another issue of membership is related to member participation in management of theco-operatives. Though Kerala co-operatives did succeed in mobilizing deposits, thedepositors were not given a hand in the management of the co-operatives. Theobservation from the membership data of the VSCB (Vellanikkara Service Co-operativeBank) showed that during the period from 2001-02 to 2010-11, the annual growth rateof the PACS membership was just 2.65% while deposits of the co-operative increasedat the rate of 11.65%. Most of the depositors – in spite of their major share in thebusiness of the co-operative – are not members of the co-operative and do not haveroles in the management of the institution. The committee headed by ProfessorVaidyanathan has observed the same at the all-India level and has made suggestions togive representation to depositors in the management of the co-operatives in India.

High cost of borrowed funds

It is well established that the rise in the average interest cost on deposits is due to thepresence of a higher portion of fixed deposits in the aggregate deposits. In addition, theincrease in interest income from advances has not been commensurate with the rise inthe interest cost. The PACS are unable to make new investments that would maximizethe interest spread and contribute to their viability. In fact, this has another dimension;the government’s insistence that PACS should deploy their funds as deposits at DCBs didcontribute to their financial ill health. This is because the PACS savings deposits at theDCBs yield much less than what they pay to the fixed deposits account holders.

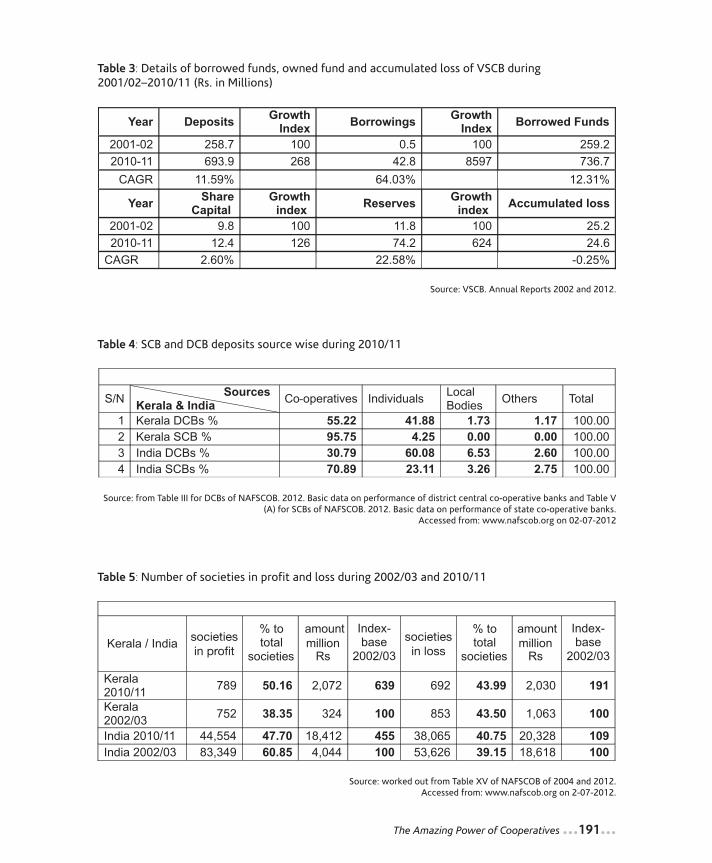

The field data from the VSCB showed that the fixed deposits of the bank, whichconstitutes 71% of the total deposits, have increased at a rate of 28.05% per annum

The Amazing Power of Cooperatives ...185...

12-Mathai_Mise en page 1 12-09-05 14:15 Page185

during 2001-02 to 2010-11 and total deposits at the rate of 11.59% per annum (seeTable-3). The borrowings grew at 64.03% per annum during the same period. There was12.31% growth in borrowed funds at VSCB during the same period. As a result of thehigh cost of borrowed funds, the VSCB could not make a significant dent on accumulatedloss as it declined only at -0.25% per annum during the same period. This is mainlybecause of the low interest margin that the co-operatives receive from their operations.

It has been noticed that there was a continuous decline in the share of owned funds in thetotal resources of the PACS. Both at the national level as well at Kerala level, the percentageof owned funds to working capital have declined during 2001-02 and 2010-11. In Kerala,the percentage was 7.26% in 2010-11 while it was 10.09% in 2001/02 (NAFSCOB, 2004and 2012: Table I and Table IV).

From the differential growth in the funds of different tiers - DCBs and SCBs - it appearsthat higher-level tiers are thriving at the cost of lower-level institutions but withouttaking any positive responsibility for the growth of the primary units. For instance, thedeposits mobilized by higher tiers (see Table-4) in the short-term structure are mobilizedby way of statutory deposits from lower tiers, rather than deposits mobilized throughtheir own efforts. In Kerala, about 55.22% of the deposits at DCB are from PACS, while95.75% of the deposits at SCB are from DCBs. It is further observed that SCBs are notlending to DCCBs in net terms other than passing on the refinance amount, as shown bythe decline in the ratio of involvement of SCBs to the DCCB deposits kept with SCB overtime. There is a serious imbalance in the growth of resources vis-à-vis lending amongdifferent tiers.

Internal resources of PACS in Kerala are relatively less – 6.84% compared with thenational average of 9.23% (NAFSCOB, 2012c). Government contributions in share capitalof PACS (13.7%) are very high compared to the national average of 9.2%. The share ofborrowings, 10.7%, and deposits, 80.6%, to working capital of PACS in Kerala indicatesthe higher cost of funds that the Kerala PACS have in their operations – the percentagesfor these variables at the national level were 38.3% and 26.1% respectively (NAFSCOB2012c). The VSCB data show that among deposits, fixed deposits, which are very costlyfor the society as the rate of interest paid was around 10%, constituted about 72% ofthe deposits.

Mounting losses of PACS and poor loan recovery

The mounting losses of PACS are threatening their very existence. As NAFSCOB dataindicate, 692 societies (44%) are incurring losses (see Table-5) and another 92 societieswere dormant in Kerala in 2011. The loss totalling Rs. 2,030 million had a growth indexof 191 over 2003. There was no change in the percentage loss in Kerala in 2011, as itwas the same 44% even eight years before. The fact is that nearly half of the PACS,

...186... The Amazing Power of Cooperatives

12-Mathai_Mise en page 1 12-09-05 14:15 Page186

including the dormant ones, are in trouble as they have to pay back the huge depositscollected from the public. Since PACS do not come under the Banking Regulation Act,non-performance of the PACS add to the risk of the depositors.

Compared to the national scenario, Kerala co-operatives are doing better as the shareof profit increased from 38.35% to 50.16% during 2003-2011. At the all India level,there was a decline in the percentage of profit making societies from 60.85% to 47.70%during 2003-2011.

Further, the PACS are poor in loan recovery – the overdue loans among Kerala PACS were25.09% for agricultural loans, 25.95% for non-agricultural loans and 19.18% for others(NAFSCOB, 2012c). The poor loan recovery rate is a concern in Kerala as a fourth of theloans issued are not available for the societies to recycle. There are many reasons behindthese overdue loans, but the major one is due to political interference in banking businessby way of writing-off of loans in the name of agricultural debt relief. In Kerala, thescapegoat of political populism has been the co-operative movement and it bears thisburden by way of borrower apathy to repay the loan on time. This has been happeningfor many years and it has created a negative psychological feeling regarding timely loanrepayments, as the people who repay the loan in a timely manner are deemed foolish.

Unwillingness to make agricultural loans

The share of agricultural credit in the total credit disbursed by co-operatives in Keraladeclined considerably between 1981-82 and 2010-11 from 53% to 17.45%. It shouldbe noted that the percentage of loans issued to agriculture by PACS at the all-India levelwas 50.90% in 2010-11 (NFSCOB, 2012c). These percentages are inflated as there areusually adjustments in which non-agricultural loans are also reckoned as farm loans(generally done to avail interest subsidies as well as for the banks to attain priority sectorlending targets). The fact is that the Kerala PACS are not financing agriculture as in otherstates. This is a serious issue in the background of agricultural stagnation in the stateand they are not justifying their name as ‘agricultural’ co-operatives.

Failure to diversify

Over the years, the number of PACS that have undertaken non-credit business activityhas not increased significantly. The percentage of agricultural produce marketed throughPACS was just 1.35% of its total working capital during the period 2005-07. In addition,the value of fertilizers sold through PACS remained very low at 2.28% of its workingcapital (Government of Kerala, 2012a). Limited operations and mounting over-dues havecontributed to their financial non-viability. For various reasons, particularly poorgovernance and management, members of PACS have disowned the institution eventhough they have an equity stake in it. The affairs of PACS have not improved to thedesired extent, despite recommendations by various committees. On the other hand, the

The Amazing Power of Cooperatives ...187...

12-Mathai_Mise en page 1 12-09-05 14:15 Page187

increase in overdues has choked the available credit lines to PACS, bringing down theirliquidity and lending ability. The share of co-operatives at grassroot level credit foragriculture declined from 2/3 to less than 1/5 of ground level credit over the last decade.

Poor service

The social objective assigned to co-operative banks also brought in uncongenial factorssuch as bureaucracy, high non-performing assets, capital inadequacy, dependence ongovernment and resistance to automation. All these held back the PACS while financialsector reforms initiated in 1991 paved the way for transformation of the bankingindustry. The cornerstone of reform was increased competition, thus acceleratingproduct innovations and enriching the quality of customer service, which co-operativeshave failed to achieve thus far. This may be the reason why credit co-operatives losttheir market share in India. Only 55% of the societies had computer facilities in 2007,and weak MIS added to the worries of the sector. The limitations of the co-operativesystem have to be overcome. These include their restricted area of operation andactivities; their inability to cater to credit needs for all purposes from a single outlet;their low level of professionalism and their inability to offer all types of financial servicesthat commercial banks/RRBs offer (money transfer through drafts/MT, etc.). Real successcomes when co-operatives take full advantage of their ability to operate at a closeinterface with their clientele. This ability almost matches similar ability of non-institutional rural lenders and can possibly never be acquired by other institutionalagencies.

Commitment of management and workforce

Staff skills are still very low, as there is lack of professionalism as can be seen from theNAFSCOB data (2012). In Kerala, about 6% of societies are without a paid secretary. Thepercentage of untrained staff at Kerala as well as at the national level is very high – 39%and 55% respectively. All these facts indicate that there is lack of professionalism in thecredit co-operative sector, which naturally affects the efficiency of operations of co-operatives. Another issue that has surfaced is that too many staff are at lower levels ofthe organisation but at the top level, very few were available, implying that professionalsare not interested in co-operative sector jobs in India. In Kerala, persons who gotdeputation from the IAS (Indian Administrative Service) cadre of the governmentbureaucracy head most of the apex co-operatives, as the government stake is higher inthose co-operatives.

Cost cutting by co-operatives

The co-operatives urgently need organizational reforms to cut the cost of operations –like the 3-tier structure of the credit co-operatives which adds to the cost of funds thatwere available to primaries; separate ST and LT structures which tend to increase the

...188... The Amazing Power of Cooperatives

12-Mathai_Mise en page 1 12-09-05 14:15 Page188

cost of management; and merging of the primary-level non-viable co-operative banks;and winding up of defunct institutions. The state co-operative federations need toassume more responsibilities including promotion, guidance, information sharing and soon, instead of competing with their affiliate members. The co-operative structure shouldtry to look as an integrated whole, ensuring timely conduct of elections, generalmeetings and audits (currently the audit is delayed on average by seven years, asobserved in the field).

Conclusions and policy implications

As 2012 is the International Year of Co-operatives, this should make co-operativeenterprises a key to transforming small-holder agriculture into a profitable business byenhancing market-oriented farm practices. As the clout of agri-business grows, foodinflation rises and informal work becomes the norm, challenging dominant structuresof ownership and power is the central challenge of the co-operative movement. In India,no amount of tinkering can make growth ‘inclusive,’ unless people have a say in howthat growth is driven.

Mounting losses, high cost of deposits and deteriorating margins, increasing overheadcosts, declining financial discipline, lack of professional management, poor service,fading member centrality and ignoring weaker sections of society are some of the urgentconcerns of the PACS in Kerala. Co-operatives in Kerala should function as economicenterprises and not as an extended arm of the state. They require an entrepreneurialapproach and competitive edge through a suitable enterprise focus and strategicalliances with private and public sector units. Appropriate mechanisms would be put inplace so that farmers have greater control of the market channels and improve profitopportunities through co-operatives and SHGs. The management of the co-operativesneeds to be made professionally competent, with clear demarcation of functions of theelected members and the managers. The audit and accounting systems would beimproved and made transparent so as to give greater confidence to all the members ofco-operatives. Good governance of co-operatives requires well-organized performancereporting, powerful internal control mechanisms backed up with good externalsupervision, along with training for the boards of directors and elected representatives.

There is a need to inculcate the values of self-help and member centrality in Kerala co-operative organisations so that they can function as ‘co-operative enterprises.’ If thephilosophy of co-operation is an important parameter to measure the success of co-operative development, there is lot more for Kerala to achieve. The co-operative principleenables the most marginalised people to mobilise their most abundant resource: theirproductive power and their solidarity. The choice is between two different worlds: onedriven by hyper-profit and mass distress, the other holding out the promise of shared

The Amazing Power of Cooperatives ...189...

12-Mathai_Mise en page 1 12-09-05 14:15 Page189

prosperity and well-being. As observed by Shivajirao G. Patil, the Chairman of the Highpowered Committee on Co-operatives, “it cannot be ignored that while the co-operativeroute is a dignified way of growth for all, it is particularly so for the marginalizedsegments of the country, offering the small man as it does the chance to enter a ‘worldof bigness’” (Government of India, 2009: ii).

...190... The Amazing Power of Cooperatives

Table 1: Direct Institutional Credit for Agriculture and Allied activities in India –Short-termand Long-term

Source: RBI. 2012. Handbook of Statistics on the Indian Economy RBI: Mumbai, worked out from Tables 55 and 56.Note: In parentheses percentages are given

CAGR: Compound Annual Growth Rate

Table 2: Total and Borrowing Membership of Primary Agricultural Credit Societies in Kerala andIndia during 2002/03 and 2010/11 (in %)

Source: NFSCOB. 2012. Accessed from www.nafscob.org/pacs_f.htm on 31-06-2012Note: Figures in parentheses are borrowing membership.

12-Mathai_Mise en page 1 12-09-05 14:15 Page190

The Amazing Power of Cooperatives ...191...

Table 3: Details of borrowed funds, owned fund and accumulated loss of VSCB during2001/02–2010/11 (Rs. in Millions)

Source: VSCB. Annual Reports 2002 and 2012.

Table 4: SCB and DCB deposits source wise during 2010/11

Source: from Table III for DCBs of NAFSCOB. 2012. Basic data on performance of district central co-operative banks and Table V(A) for SCBs of NAFSCOB. 2012. Basic data on performance of state co-operative banks.

Accessed from: www.nafscob.org on 02-07-2012

Table 5: Number of societies in profit and loss during 2002/03 and 2010/11

Source: worked out from Table XV of NAFSCOB of 2004 and 2012.Accessed from: www.nafscob.org on 2-07-2012.

12-Mathai_Mise en page 1 12-09-05 14:15 Page191

Note1 Associate Professor, College of Co-operation, Banking and Management,Kerala Agricultural University (KAU), Thrissur-680656, Kerala State, India, E-mail: [email protected],phone: +9194 9588 4527

BibliographyBAVISKAR, B.S. (1968). "Co-operatives and Politics", Economic and Political Weekly, Vol. 3, No. 12 (Mar. 23),

pp. 490-495, accessed from www.jstor.org/stable/4358403 on 11-06-2012.DESAI, B. M and N. V. NAMBOODIRI (1993). Rural Financial Institutions: Promotion and Performance, New Delhi,

Oxford and IBH Publishing Co.GOVERNMENT OF KERALA (2006). Human Development Report 2005, Thiruvananthapuram, Centre for

Development Studies.GOVERNMENT OF KERALA (2012a). Economic Review 2011, Thiruvananthapuram, Kerala State Planning Board,

accessed from www.spb.kerala.gov.in on 11-06-2012.GOVERNMENT OF KERALA (2012b). 12th Five Year Plan (2012-17), Approach Paper, accessed from

www.spb.kerala.gov.in/images/pdf/ape.pdf on 24-07-2012GOVERNMENT OF INDIA (1991), Report of the Committee on the Financial System, New Delhi, Ministry of

Finance.GOVERNMENT OF INDIA (1998), Report of the Committee on the Banking Sector Reforms, New Delhi, Ministry

of Finance.GOVERNMENT OF INDIA (2006). Report of the Task Force on Revival of Rural Co-operative Credit Institutions (long

term), New Delhi, Ministry of Finance. GOVERNMENT OF INDIA (2002). National Policy on Co-operatives, New Delhi, Ministry of Agriculture, Department

of Agriculture and Cooperation.GOVERNMENT OF INDIA (2004). Task Force on Revival of Co-operative Credit Institutions (Chairman: Prof.

Vaidyanathan), New Delhi, Ministry of Agriculture, Department of Agriculture and Cooperation.GOVERNMENT OF INDIA (2009). Report of the High Powered Committee on Co-operatives, New Delhi, Ministry

of Agriculture.KERALA STATE CO-OPERATIVE BANK, KSCB (2012). Co-operative banking scenario in Kerala, Thiruvananthapuram, KSCB.NABARD (2001). Expert Committee on Rural Credit, Mumbai, accessed from www.nabard.org/fileupload/ -

DataBank/ Newsletters/August2001.pdf on 26-06-2012.NABARD (2009). Report of the working group on human resource policy for short- term co-operative credit

structure, Mumbai, NABARD.NAFSCOB (2004). Performance of Primary Co-operative Credit Societies, (April 1, 2008 to March 31, 2009),

accessed from www.nafscob.org on 26-06-2012.NAFSCOB (2012a). Performance of District Central Co-operative Banks, (April 1, 2008 to March 31, 2009),

accessed from www.nafscob.org on 26-06-2012.NAFSCOB (2012b). Performance of State Co-operative Banks, (April 1, 2008 to March 31, 2009), accessed

from www.nafscob.org on 26-06-2012NAFSCOB (2012c). Performance of Primary Co-operative Credit Societies, (April 1, 2008 to March 31, 2009),

accessed from www.nafscob.org on 26-06-2012NATIONAL CO-OPERATIVE UNION OF INDIA (NCUI) (2009). Indian Co-operative Movement: A Statistical Profile-2009,

New Delhi, NCUI.PUHAZHENDHI, V. and B. JAYARAMAN (1999). "Rural Credit Delivery: Performance and Challenges before Banks",

Economic and Political Weekly, Vol. 34, No. 3/4, (Jan.16-29,), p. 175-177+179-182, accessed fromwww.jstor.org/stable/4407579 on 26-06-2012

RESERVE BANK OF INDIA (2011). Report on trend and progress of banking in India 2010-11, Mumbai, RBI.RESERVE BANK OF INDIA (1954). All-India Rural Credit Survey Report 1951-52.RESERVE BANK OF INDIA (2000). Report of the Task Force to Study the Co-operative Credit System and Suggest

Measures for its Strengthening (chairman: Mr. Jagdish Capoor), accessed from www.rbidocs.rbi.org.in/ -rdocs/PublicationReport/Pdfs/14898.pdf on 13-7-2012.

...192... The Amazing Power of Cooperatives

12-Mathai_Mise en page 1 12-09-05 14:15 Page192

RESERVE BANK OF INDIA (2012). Handbook of Statistics on the Indian Economy, Mumbai, RBI.SATYASAI K. J. S. and K. C. BADATYA (2000). "Restructuring Rural Credit Co-operative Institutions", Economic

and Political Weekly, Vol. 35, No 5, (Jan. 29 -Feb. 4), p. 307-309+311-313+315-317+319-321+323-330,accessed from www.jstor.org/stable/4408878

SHIVAMAGGI H. B. (1996). "Future Strategy for Development of Co-operatives", Economic and Political Weekly,Vol. 31, No 20, (May 18), p. 1187-1188, accessed from www.jstor.org/stable/4404141

URS NIRANJAN RAJ, B. and K. CHITAMBARAM (2000). "Measuring the performance of District Co-operative Banks",NAFSCOB Bulletin, October-December, 2000.

Summary

Liberalization of the co-operative movement in India sought to create commercially autonomousmember-based co-operatives that would be democratically and professionally managed businessventures. Rural credit co-operative movement in India was successful in some States. Kerala is one ofthe Indian states wherein co-operative credit movement did make an impact in its socio-economiclife, however shown signs that question the co-operative character as well as its sustainability. Thispaper analyses the performance and sustainability issues of short-term credit co-operatives in KeralaState, India. The issues identified are with respect to: membership of co-operatives, borrowed funds,loan recovery, loan to agricultural sector, diversification of business, quality of service, commitmentof management and workforce, cost of operations etc. There is need to inculcate values of self-helpand member centrality in Kerala co-operative organisations to make them true ‘enterprises’.

Resumen

La liberalización del cooperativismo en India intentó crear cooperativas comercialmente autónomasbasadas en sus asociados, las que funcionarían como empresas comerciales administradas de manerademocrática y profesional. Las cooperativas de crédito rural tuvieron éxito en algunos estados de laIndia; por ejemplo, en Kerala, uno de los estados indios cuya vida socioeconómica se vio modificadapor las cooperativas de crédito, a pesar de que se cuestionó el carácter cooperativo del movimientoasí como su sustentabilidad. Este texto aborda la temática relacionada con el desempeño y lasustentabilidad de las cooperativas de crédito a corto plazo en el estado de Kerala, India. Entre lostemas identificados se encuentran: afiliación a las cooperativas, préstamo de fondos, recuperaciónde préstamos, préstamos al sector agrícola, diversificación de la empresa, calidad del servicio,compromiso de los gerentes y de los empleados, costo de las operaciones, etc. Es necesario inculcarvalores de ayuda mutua y de centralidad de los socios en las organizaciones cooperativas de Keralaa fin de convertirlas en verdaderas ‘empresas’.

Résumé

La libéralisation du mouvement coopératif en Inde visait à créer des coopératives autonomes quiétaient, en fait, des entreprises gérées démocratiquement et avec professionnalisme. Le mouvementcoopératif de crédit rural a connu du succès dans certains États indiens. Au Kerala, par exemple, lemouvement de coopératives de crédit rural a eu une incidence positive sur la vie socio-économique,malgré des signes permettant de mettre en doute le caractère coopératif et la durabilité de sesactivités. Ce texte analyse les problèmes de performance et de durabilité qu'éprouvent lescoopératives de crédit à court terme au Kerala. Voici quelques-unes des questions soulevées : lesmembres, les fonds empruntés, la récupération des prêts, les prêts au secteur agricole, ladiversification des activités, la qualité du service, l'engagement de la direction et des employés et lecoût d'exploitation. Il est important d'instaurer les valeurs d'entraide et de prépondérance desmembres dans les coopératives du Kerala afin d'en faire de véritables « entreprises ».

The Amazing Power of Cooperatives ...193...

12-Mathai_Mise en page 1 12-09-05 14:15 Page193