Embed Size (px)

Citation preview

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 1 of 71

1 THE HONORABLE RICARDO S. MARTINEZ

2

3

4

5

6

7

8

9

10

11 JONATHAN REINSCHMIDT, Individually

12

and on Behalf of All Others Similarly Situated,

13

Plaintiff,

14

vs.

15

ZILLOW, INC., et al.,

16

Defendants.

17

18

19

20

21

22

23

24

25

26

No. 2:12-cv-02084-RSM

CLASS ACTION

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT

UNITED STATES DISTRICT COURT

WESTERN DISTRICT OF WASHINGTON

AT SEATTLE

852878_1

CONSOLIDATED CLASS ACTION AMENDED

I E. COMPLAINT (2:12-CV-02084-RSM)

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 2 of 71

TABLE OF CONTENTS

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

852878_1 26

V.

VI

VII

I.

II.

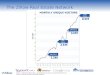

III.

IV

Page

NATURE OF THE ACTION ..............................................................................................1

JURISDICTION AND VENUE ..........................................................................................7

THEPARTIES.....................................................................................................................8

A. Lead Plaintiffs ..........................................................................................................8

B. Defendant Zillow .....................................................................................................9

C. Individual Defendants ..............................................................................................9

ZILLOW’S BUSINESS MODEL AND SWITCH IN PRICING .....................................11

A. Zillow’s IPO and Profitability Plan .......................................................................11

B. Zillow’s Limited Revenue Sources ........................................................................13

C. Zillow’s Shift to Impression-Based Pricing for Agent Advertising ......................14

D. Customers Were Cancelling or Downsizing Their Subscriptions, and Churn Was Increasing ............................................................................................16

E. Further Resistance to Zillow’s Business Practices ................................................21

F. Zillow’s Increased Expenses in Connection with Attracting and Maintaining Agent Subscriptions ..........................................................................23

G. Zillow’s Static Average Revenue Per Customer ...................................................24

H. Zillow’s Downward Trending Revenue Growth ...................................................26

I. Zillow Further Concealed the Loss of High Margin Display Advertising Business.................................................................................................................27

DEFENDANTS CONDUCT A SECONDARY OFFERING ...........................................28

DEFENDANTS’ MASSIVE INSIDER SELLING AT ARTIFICIALLY INFLATEDPRICES .........................................................................................................30

DEFENDANTS’ FALSE AND MISLEADING STATEMENTS ....................................32

A. Fourth Quarter and Full Year 2011 Misstatements ................................................32

B. First Quarter 2012 Misstatements ..........................................................................36

C. Second Quarter Misstatements ..............................................................................41

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E k

HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - i - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E k

HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE, WA 98101 - ii - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 3 of 71

Page

1

VIII. THE TRUTH IS FINALLY REVEALED .........................................................................52

2

A. Disclosures that ARPU Levels Were Flat ..............................................................53

3

B. Disclosures Regarding Loss of Display Advertising Business ..............................57

4

IX. ADDITIONAL SCIENTER ALLEGATIONS ..................................................................59

5

X. FRAUDULENT SCHEME AND COURSE OF BUSINESS ...........................................61

6

XI. LOSS CAUSATION/ECONOMIC LOSS ........................................................................62

7

XII. CLASS ACTION ALLEGATIONS ..................................................................................62

8

XIII. APPLICABILITY OF PRESUMPTION OF RELIANCE: FRAUD ON THE MARKET DOCTRINE .....................................................................................................64

9 XIV. NO SAFE HARBOR .........................................................................................................64

10 XV. CAUSES OF ACTION ......................................................................................................65

11 COUNTI ...........................................................................................................................65

12

For Violation of Section 10(b) of the Exchange Act and Rule 10b-5(a), (b) & (c) Promulgated Thereunder Against All Defendants

13 COUNTII ..........................................................................................................................66

14

For Violation of Section 20(a) of the Exchange Act Against the Individual Defendants

15 XVI. PRAYER FOR RELIEF ....................................................................................................67

16 JURY TRIAL DEMANDED .........................................................................................................67

17

18

19

20

21

22

23

24

25 852878_1

26

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 4 of 71

1

Lead plaintiffs Oklahoma Firefighters Pension and Retirement System (“Oklahoma

2

Firefighters”), State-Boston Retirement System (“State-Boston”) and James Atkinson (“Atkinson”)

3

(collectively, “Lead Plaintiffs”), individually and on behalf of all other persons and entities who

4

purchased or acquired the common stock of Zillow, Inc. (“Zillow”) during the period between

5

February 15, 2012 and November 6, 2012, inclusive (the “Class Period”) and who were damaged

6

thereby, allege the following based upon personal knowledge as to themselves and their own acts,

7

and upon information and belief as to all other matters.

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

Lead Plaintiffs’ allegations are based on Lead Counsel’s investigation, which included,

among other things: (i) a review of Zillow’s public filings with the U.S. Securities and Exchange

Commission (“SEC”); (ii) a review and analysis of research reports issued by financial analysts

concerning Zillow; (iii) a review and analysis of other publicly available information concerning

Zillow and its senior officers and directors, including Spencer M. Rascoff, Lloyd D. Frink, Chad M.

Cohen and Richard N. Barton (collectively, the “Individual Defendants”); and (iv) interviews with

former Zillow employees on a confidential basis (“Confidential Witnesses” or “CWs”), each of

whom has specific, personal knowledge of the facts alleged herein. Lead Plaintiffs believe that

substantial additional evidentiary support exists for the allegations set forth in this Complaint that

will be revealed after a reasonable opportunity for discovery.

I. NATURE OF THE ACTION

1. This is a securities class action arising from Defendants’ material misstatements and

omissions regarding the Company’s business during the Class Period.

2. Zillow is an online company that purports to offer various services to assist

consumers with real estate needs, including the buying and selling of homes, renting, borrowing and

I remodeling. Zillow operates through its website and various mobile applications, and gives

consumers access to a database of real estate listings. Zillow also offers a service called a

I “Zestimate” that estimates the value of a property based on various sources of data.

CONSOLIDATED CLASS ACTION AMENDED _____________ COMPLAINT (2:12-cv-02084-RSM)

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - 1 - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 5 of 71

1

3. Zillow is free to consumers and generates the majority of its revenue in two ways:

2

selling advertising on its website (“Display Advertising”) and selling subscription services to real

3

estate agents and mortgage lenders nationwide (“Marketplace Advertising”), whereby real estate

4

agents can get their name and contact information displayed on Zillow’s website next to a potential

5

buyer’s real estate search results. Since Zillow’s initial public offering in July 2011, Marketplace

6

Advertising has become the Company’s largest line of business and continues to grow.

7

4. Zillow’s Marketplace Advertising business includes the Premier Agent program,

8

through which real estate agents purchase subscription-based advertising at three levels of

9

participation. The most basic is Silver, more enhanced being Gold, and the premium, most

10

expensive and profitable level to Zillow is Platinum. Defendants publicly portrayed the market

11

opportunity for the Premier Agent program as vast ($6 billion) and largely untapped, and suggested

12

that demand for its Platinum-level of service far exceeded its capacity to deliver that service.

13

5. At the start of the Class Period, Defendants announced a change to Zillow’s business

14

purportedly to take advantage of that vast, untapped market, which included transitioning from

15

selling a finite number of Platinum subscription spaces (a maximum of 12) per zip code, to charging

16

Platinum subscribers based on the number of web site impressions Zillow delivered. Zillow

17

purportedly did this to broaden the availability of the Premier Agent program to agents who were

18

demanding the Platinum level of service, and more important to investors, so that Zillow could

19

increase the prices charged to agents. This new business model was designed to fundamentally

20

change the way in which Zillow charged for and priced subscriptions to its Premier Agent program.

21

Because Zillow generated the majority of its revenue from selling subscriptions to its Premier Agent

22

program, the status of this new development was highly material to investors.

23

6. Throughout the Class Period, Defendants represented to investors that this new

24

I impressions-based pricing for real estate agent subscriptions gave Zillow the ability to sell more

25

subscriptions at higher prices. Defendants also represented that Zillow was making good progress

26

introducing its new impressions-based pricing model, because existing customers were happy with

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 6 of 71

I the new program and were willing to pay higher prices for the advertising features that were Zillow’s

main source of revenue within the Premier Agent program.

7. Investors were focused on whether the new pricing model allowed Zillow to raise

prices, because it was a direct indicator of Zillow’s ability to grow revenue and become more

profitable. The most important information that would allow investors to accurately evaluate

whether Zillow was successfully raising prices was an internal metric called Average Revenue per

Subscriber (“ARPU”). However, Zillow did not disclose the key ARPU metric to investors during

the Class Period. As a result, investors had no quantitatively accurate means of gauging the truth of

Defendants’ Class Period representations that Zillow was successfully raising prices under to the

new pricing model.

8. Unbeknownst to investors, and directly contrary to Defendants’ Class Period

representations, Zillow was experiencing great difficulty in raising subscription prices to its Premier

Agent program, and the rollout of the new impressions-based pricing model was being resisted by

existing Platinum Premier Agents. Additionally, a number of other factors were also negatively

impacting Zillow’s Marketplace Advertising business. Zillow’s best, most profitable markets were

becoming saturated. Zillow was facing stiff competition from other online providers, and a number

of Zillow’s business practices angered and alienated customers. Those included the widespread

inaccuracy of Zestimates, Zillow’s inferior listing information, and the fact that many real estate

agents resented Zillow for how it did business (Zillow essentially takes an agent’s proprietary listing

and resells it back to the agent). Moreover, many of Zillow’s customers did not believe they were

getting a sufficient return on investment (“ROI”) from the dollars they spent advertising on Zillow.

9. All of these factors were causing Zillow serious problems in its efforts to implement

I the new pricing plan for Premier Agent subscriptions. As explained by numerous confidential

witnesses, when faced with a substantially higher price for Zillow’s new cost-per-impression based

service, many of Zillow’s Premier Agents cancelled their subscriptions causing significant churn. In

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

A 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - 'I - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 7 of 71

I addition to ARPU, churn is another important measure of subscriber health in any subscription-based

I business, and was also a metric that Zillow consistently refused to disclose.

10. In order to continue to increase its subscriber base and revenues in light of the

negative factors it faced, Zillow significantly ramped up its sales efforts during the Class Period,

which Defendants portrayed as positive for Zillow’s business. Unbeknownst to investors, however,

as Platinum-level subscribers became harder and harder to find , Zillow was forced to sell more

subscriptions at lower levels and price points. While this allowed Zillow to show an increase in the

number of reported subscribers and revenue when it reported its financial results, it also resulted in a

substantial increase in the cost of sales, and at a lower ARPU. Defendants were concealing ARPU

and churn numbers during the Class Period, because they would have revealed that Zillow was not

having success with its new pricing model.

11. In fact, had Zillow disclosed its ARPU numbers during the Class Period, investors

would have seen that as soon as Zillow began rolling out its new impressions-based pricing model, it

lost the ability to continue raising prices. In the quarters prior to the start of the Class Period, Zillow

had been able to dramatically increase its ARPU under the old pricing model, but under the new

pricing program ARPU was no longer increasing and it had become essentially flat due to churn and

agents resisting the higher pricing. A higher ARPU would signal strong demand because it would

mean that overall customers were subscribing to and paying for Zillow’s more expensive higher-tier

Platinum service. A lower ARPU, on the other hand, would mean lower demand for the higher

priced product and that subscribers were only willing to pay for Zillow’s less expensive tiers.

12. In August 2012, towards the end of the Class Period, the SEC issued comment letters

to Defendants and asked why Zillow was not disclosing ARPU. Defendants tried to persuade the

SEC that Zillow did not need to disclose its ARPU, but the SEC did not find Zillow’s arguments

persuasive. The SEC viewed the ARPU information as highly material to investors’ decision

making process, because it provided fundamentally important information regarding the trends and

conditions surrounding Zillow’s pricing of its primary product—subscriptions sold to real estate

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

- 5S 1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 8 of 71

I agents. Because the SEC continued to press for disclosure of this key information, Defendants

I eventually told the SEC in late August 2012 that Zillow would begin disclosing this information.

13. However, after Defendants told the SEC that Zillow would disclose the highly

material ARPU numbers, they delayed doing so until after they had sold over $165 million in Zillow

stock in a secondary offering. Specifically, shortly after telling the SEC that Zillow would begin

disclose ARPU, Defendants filed a prospectus with the SEC for a secondary public offering of

Zillow stock that still did not disclose that key information.

14. Because Zillow was refusing to disclose its ARPU numbers during the Class Period

and reported only its total subscriber number, and not the make-up of Platinum, Gold or Silver

subscriptions, analysts were forced to calculate their own estimates of ARPU based on the total

reported subscriber numbers and statements by management about strong demand for Zillow’s

Premier Agent products. Analysts consistently overestimated ARPU based on the belief that

demand for high-tiered services was strong, whereas Zillow’s true ARPU numbers were much lower,

reflecting the undisclosed negative factors impacting Zillow’s business described herein.

15. As a result of analysts’ attempts to calculate Zillow’s ARPU, investors had begun to

I question whether Zillow was experiencing slowing or declining ARPU growth late in the Class

Period. In particular, in early August 2012, certain stock analysts made calculations that suggested

there might be an issue with Zillow ability to increase pricing in the 2Q12.

16. In response to these concerns, Defendants made public statements that attempted to

reassure investors that Zillow was continuing to successfully roll out the new pricing model and it

was generating increased pricing. As a result of these misrepresentations, Zillow’s stock price

reached a Class Period high of over $46 per share on September 20, 2012—shortly after the

secondary stock offering where Zillow had again chosen not to disclose its ARPU numbers.

17. Defendants’ false and misleading statements during the Class Period failed to disclose

a known trend—that the new impressions-based pricing model had not allowed Zillow to materially

increase its pricing. Moreover, Zillow’s increased prices resulted in low ROI for subscribers and

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 9 of 71

1

resulted in significant churn. Defendants failed to disclose that it was only able to report increases in

2

subscriber numbers and revenues through high-pressure sales tactics that resulted in subscribers

3

being signed at lower tiers and at lower ARPU than analysts were estimating. Defendants also failed

4

to disclose that by the start of the Class Period, Zillow decided to drop Foreclosure.com , a major

5

advertiser and contributor to its Display Advertising business, as a customer.

6

18. Then, on October 1, 2012, the SEC’s inquiry into Zillow’s financial reporting was

7

reported by news outlets. Once investors learned that Zillow failed to disclose the ARPU numbers in

8

its most recent SEC filings in connection with the September 7, 2012 secondary offering, even after

9

the SEC had insisted on disclosure, and even after Defendants had expressly acknowledged to the

10

SEC that “the average monthly Premier Agent revenue per Premier Agent subscriber may be

11

meaningful to investors and also meaningful as a performance indicator in managing the Company’s

12

business,” investors became concerned that the Zillow was concealing its ARPU numbers because

13

of what those numbers might reveal to investors. As a result of those concerns, Zillow’s stock price

14

immediately declined in value. On October 2, 2012, following the widespread dissemination of the

15

SEC’s comment letters, Zillow’s stock price dropped sharply, initially falling 10.2% and eventually

16

closing down 4.2% for the day.

17

19. Finally, on November 5, 2012, Zillow issued a press release and held a conference

18

call after the market closed announcing significantly reduced financial guidance for the coming

19

quarter, and finally revealing what Defendants knew since the start of the Class Period: Zillow’s

20

revenues would be further impacted during the quarter by the loss of Foreclosure.com . During the

21

conference call with analysts Defendants also revealed the existence of churn that had been caused

22

by real estate agents whose ROI was insufficient to justify the higher pricing that Zillow was

23

attempting to impose on its customers.

24

20. Zillow filed its 3Q 2012 Form 10-Q with the SEC the next day in which Zillow

25

I reported ARPU for the first time. Those numbers revealed, contrary to Defendants’ prior

26

representations, that the new impressions-based pricing model had not allowed Zillow to materially

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - 6 - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E i

HAGENS BERMAN

'.7 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - I - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 10 of 71

increase its pricing. Rather, ARPU had been essentially flat during the Class Period. It also showed

that while ARPU had been substantially increasing during 2011, it stopped increasing once the new

impression based pricing was introduced in 1Q12, and had remained stuck in the $258 to $270

range. Moreover, those disclosures showed that actual ARPU during the Class Period was far lower

than analysts’ estimates caused by Defendants’ misstatements regarding and concealment of this

highly material information.

21. Zillow’s stock price reacted strongly to the news falling $6.22 per share on

November 6, 2012, a one-day decline of almost 18% on very heavy volume of 7.4 million shares

traded. Lead Plaintiffs have brought this case to recover their losses caused by purchasing Zillow

stock at artificially inflated prices during the Class Period as a result of Defendants material

misstatements and omissions.

22. Indeed, Defendants had a duty to disclose its actual ARPU during the Class Period

because: (i) it was highly material to investors, as the SEC told Defendants in August 2012;

(ii) Defendants acknowledged the materiality of ARPU when they told the SEC that “the average

monthly Premier Agent revenue per Premier Agent subscriber may be meaningful to investors and

also meaningful as a performance indicator in managing the Company’s business,” and told the SEC

that Zillow would begin disclosing it; (iii) Defendants were publicly speaking about purported price

increases in Premier Agent subscriptions throughout the Class Period and thus needed to disclose the

ARPU numbers in order to make their statements not misleading; and (iv) Defendants sold millions

of dollars in Zillow stock during this time period, thus they needed to disclose the ARPU before

trading on the inside information that showed Zillow had not and could increase subscription prices

under its new impressions-based pricing model.

II. JURISDICTION AND VENUE

23. The federal law claims asserted herein arise under Section 10(b) and Section 20(a) of

the Exchange Act, 15 U.S.C. §78j(b) and §78t(a), and Rule 10b-5 promulgated thereunder by the

SEC, 17 C.F.R. §240.10b-5.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 11 of 71

1

24. This Court has subject matter jurisdiction over this action pursuant to 28 U.S.C.

2

I §1331 and §27 of the Exchange Act, 15 U.S.C. §78aa.

3

25. This Court has jurisdiction over each defendant named herein because each defendant

4

I is an individual who has sufficient minimum contacts with this District so as to render the exercise of

5

I jurisdiction by the District Court permissible under traditional notions of fair play and substantial

6

I justice.

7

26. Venue is proper in this District pursuant to §27 of the Exchange Act and 28 U.S.C.

8

§1391(b). Many of the false and misleading statements were made in or issued from this District.

9

Zillow is headquartered in this District, with its principal place of business located at 1301 Second

10

Avenue, Floor 31, Seattle, Washington 98101.

11

III. THE PARTIES

12

A. Lead Plaintiffs

13 27. On April 24, 2013, this Court appointed James Atkinson, Oklahoma Firefighters and

14 State-Boston to serve as Lead Plaintiffs for the Class in this consolidated class action pursuant to the

15 Private Securities Litigation Reform Act of 1995 (the “PSLRA”)

16 28. Atkinson purchased Zillow common stock in reliance on Defendants’ false and

17 misleading statements and omissions of material facts and/or the integrity of the market for Zillow

18 securities at artificially inflated prices during the Class Period and suffered economic loss and

19 damages when the truth about Zillow that was misrepresented and omitted during the Class Period

20 was revealed to the market. The certification for Atkinson with a detailed listing of transactions was

21 filed with this Court on January 28, 2013 and is adopted by reference herein. (Dkt. No. 24-1.)

22 29. Oklahoma Firefighters is a qualified governmental retirement plan that provides

23 retirement benefits to firefighters in the State of Oklahoma. Oklahoma Firefighters purchased

24 Zillow common stock in reliance on Defendants’ false and misleading statements and omissions of

25 material facts and/or the integrity of the market for Zillow securities at artificially inflated prices

26 during the Class Period and suffered economic loss and damages when the truth about Zillow that

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E i

HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE, WA 98101 - 8 - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 12 of 71

1

was misrepresented and omitted during the Class Period was revealed to the market. The

2

certification for Oklahoma Firefighters with a detailed listing of transactions was filed with this

3

Court on January 28, 2013 and is adopted by reference herein. (Dkt. No. 26-2.)

4

30. State-Boston is an institutional investor that provides retirement benefits for the

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

employees of the City of Boston, Massachusetts. State-Boston purchased Zillow common stock in

reliance on Defendants’ false and misleading statements and omissions of material facts and/or the

integrity of the market for Zillow securities at artificially inflated prices during the Class Period and

suffered economic loss and damages when the truth about Zillow that was misrepresented and

omitted during the Class Period was revealed to the market. The certification for State-Boston with

a detailed listing of transactions was filed with this Court on January 28, 2013 and is adopted by

reference herein. (Dkt. No. 26-2.)

B. Defendant Zillow

31. Zillow purports to operate the leading real estate information marketplace through its

website and mobile applications. Zillow is a Washington corporation with its principal place of

I business located at 1301 Second Avenue, Floor 31, Seattle, Washington 98101.

C. Individual Defendants

32. Spencer M. Rascoff (“Rascoff”) was one of Zillow’s founding employees. He joined

the Company in 2005, has been the CEO since September 2010 and a Director since July 2011.

Rascoff previously served as the Company’s Vice President of Marketing, Chief Financial Officer

(“CFO”) and Chief Operating Officer. During the Class Period, Rascoff sold 54,500 shares of his

Zillow stock for proceeds of over $2.1 million.

33. Lloyd D. Frink (“Frink”) co-founded Zillow and is, and at all relevant times has been,

the Company’s Vice Chairman, a position he has held since March 2011. Frink has been a member

of the Board since the Company’s inception in December 2004, and served as President since

February 2005. Frink previously served as the Company’s Vice President from December 2004 to

February 2005, as Treasurer from December 2009 to March 2011, and as Chief Strategy Officer

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E i

HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 13 of 71

1

from September 2010 to March 2011. As of April 5, 2012, Frink owned or controlled approximately

2

4,841,227 shares of Zillow Class A common stock, and 3,781,222 shares of Zillow Class B common

3

stock, representing 35.3% of the total voting power of the Company. During the Class Period, Frink

4

sold over 1.3 million shares of his Zillow stock for proceeds of over $48.0 million.

5

34. Chad M. Cohen (“Cohen”) is and at all relevant times has been the Company’s CFO,

6

a position he has held since March 2011. Cohen previously served as Zillow’s Controller from June

7

2006 to March 2011, and as Vice President of Finance from September 2010 to March 2011. During

8

I the Class Period, Cohen sold 50,791 shares of his Zillow stock for proceeds of over $1.76 million.

9

35. Richard N. Barton (“Barton”) co-founded Zillow and is, and at all relevant times has

10

been, the Company’s Executive Chairman of the Board, a position he has held since September

11

2010. Barton has been a member of the Board since its inception in December 2004 and served as

12

Company’s Chief Executive Officer (“CEO”) until September 2010. As of April 5, 2012, Barton

13

owned or controlled approximately 5,487,333 shares of Zillow Class A common stock, and

14

4,910,404 shares of Zillow Class B common stock, representing 45.9% of the total voting power of

15

the Company. During the Class Period, Barton sold over 1.1 million shares of his Zillow stock for

16

proceeds of over $42.2 million.

17

36. Rascoff, Frink, Cohen and Barton are collectively referred to hereinafter as the

18

I “Individual Defendants.”

19

37. The Individual Defendants were involved in drafting, producing, reviewing and/or

20

disseminating the false and misleading statements, information and omissions alleged herein, were

21

aware of, or recklessly disregarded, the fact that the false and misleading statements and omissions

22

were being issued by the Company, and approved or ratified these statements, in violation of the

23

federal securities laws

24

38. Moreover, facts critical to Zillow’s “core operations” are presumably known by its

25

I key officers, including the Individual Defendants. Further, the Individual Defendants, because of

26

I their senior management positions within the Company, and as to Barton and Frink, their substantial

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

- 1i 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 0 - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 14 of 71

stock ownership, possessed the power and authority to control the contents of Zillow’s quarterly

reports, press releases, and presentations to securities analysts, money and portfolio managers, and

institutional investors, i.e. , the market. They were provided with copies of the Company’s reports

and press releases alleged herein to be misleading prior to or shortly after their issuance and had the

ability and opportunity to prevent their issuance or cause them to be corrected. Because of their

positions with the Company, and their access to material, non-public information available to them

but not to the public, the Individual Defendants knew that the adverse facts specified herein had not

been disclosed to and were being concealed from the public, and that the positive representations

being made were then materially false and misleading. The Individual Defendants are liable for the

false and misleading statements alleged herein.

39. As officers and/or controlling persons of a publicly-held company whose shares are

registered with the SEC and traded on NASDAQ, the Individual Defendants also had a duty to

disseminate prompt, accurate and truthful information with respect to Zillow, and to correct any

previously issued statements that had become materially misleading or untrue, so that the market

price of the Company’s common stock would be based upon truthful and accurate information. The

Individual Defendants each violated these specific requirements and obligations during the Class

Period.

IV. ZILLOW’S BUSINESS MODEL AND SWITCH IN PRICING

A. Zillow’s IPO and Profitability Plan

40. Barton and Frink co-founded Zillow in December 2004. The Company’s stated

mission was “to build the most trusted and vibrant home-related marketplace to empower consumers

with information and tools to make smart decisions about homes.” The Company operates a

website, Zillow.com, and Zillow Mobile, a suite of mobile applications, through which it purports to

offer various online services to assist consumers with their real estate needs, including Zillow

Mortgage Marketplace, where borrowers connect with lenders to find loans and get competitive

mortgage rates, Zillow Digs, a home improvement marketplace where consumers can find visual

852878_1

CONSOLIDATED CLASS ACTION AMENDED

I E. COMPLAINT (2:12-cv-02084-RSM)

- 1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 11 - (206) 623-7292 • FAX (206) 623-0594

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 15 of 71

I inspiration and local cost estimates, and Zillow Rentals, a marketplace for rental professionals.

Zillow also offers services and applications to real estate professionals including Postlets, Diverse

Solutions, Buyfolio, Mortech and HotPads.

41. Zillow purportedly maintains a “living” database of over 110 million U.S. homes,

whether for rent or for sale, and includes homes that are not even on the market. This database

includes properties that have been listed by real estate agents representing sellers on various multiple

listing services (“MLS”) around the country. Zillow also obtains information regarding homes

offered for sale from a number of other sources, including third party syndicators who compile and

aggregate real estate listings from MLS around the country. Zillow offers a free valuation service

known as “Zestimates,” whereby the Company calculates the estimated value of the properties listed

in the database based on the properties’ physical attributes, tax assessments, prior sales prices and

other factors.

42. Initially, Zillow’s business model and marketing efforts were largely based around its

Zestimates service, which allowed visitors to its website to obtain property value estimates by

entering a property address. More recently, however, Zillow’s primary source of revenue has come

from selling “subscriptions” to real estate agents, which Zillow markets as a vehicle for agents to

advertise their services to potential home buyers. Zillow’s business model has been subject to

criticism because the Company essentially acts as a middleman, collecting the valuable property

listings of real estate agents, obscuring the identity of the original listing agent, and then attempting

to sell back to agents advertising space, alongside with the listings that were originally generated by

the agents themselves.

43. After operating as a start-up business for about six years, Zillow had its initial public

offering (“IPO”) in July 2011 at a price of $20 a share. At the time of its IPO, Zillow had never

turned a profit. Defendants told investors that Zillow’s relatively near-term plan was to become a

profitable business with over $200-$250 million in annual revenue and profit margins of 30-35%. In

order to generate such profitability, Zillow needed to dramatically increase its sales, while

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

i 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - I2 - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 16 of 71

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

I controlling costs. As alleged below, Zillow faced numerous undisclosed obstacles standing in the

I way of its business plan.

B. Zillow’s Limited Revenue Sources

44. Because the online services offered by Zillow are free to the consumer looking to

buy, sell or rent a property, the Company derives its revenue from online advertisements by real

estate agents, housing and mortgage professionals, and brand advertisers. Most of the Company’s

advertising revenue is generated primarily on a subscription basis from local real estate professionals

(the “Premier Agent subscribers” or “subscribers”).

45. Zillow categorizes its advertising revenue into two lines of business—Marketplace

Advertising and Display Advertising. Marketplace Advertising consists of subscriptions sold to real

estate agents under the Company’s Premier Agent program and cost-per-click (CPC) advertising

sold to mortgage lenders under the Zillow Mortgage Marketplace program. According to the

Company’s Form 10-K for the year ended December 31, 2012 (“2012 Form 10-K”), Marketplace

Advertising revenue comprised 64% of total revenue in 2011, and increased to 74% of revenue for

2012.

46. Zillow’s second line of business, Display Advertising, primarily consists of graphical

mobile and web advertising sold on a cost per thousand impressions (“CPM”) basis to advertisers in

the real estate industry, including real estate brokerages, home builders, mortgage lenders and home

services providers. Such revenue is recognized according to the number of impressions made and

delivered to users interacting with the website or mobile applications. According to the Company’s

2012 Form 10-K, display advertising revenue comprised 36% of total revenue in 2011, and

decreased to 26% in 2012.

47. Because the majority of Zillow’s revenue is derived from its Premier Agent program,

Zillow’s existing and future profitability depended on its ongoing ability to sell Premier Agent

I subscriptions. Defendants conveyed to investors that the market for its Premier Agent program was

vast and largely untapped, as only a fraction of the total number of real estate agents in the United

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

i ,, 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - I j - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 17 of 71

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

States were subscribers to the program. For instance, during a February 15, 2012 analyst conference

call, Rascoff represented that Zillow was trying to “capture” the 1.8 million real estate agents in the

United States and the $6 billion spent by them on marketing services. Rascoff explained:

We see agents in the United States collecting about $60 billion in commissions and turning around and spending 10% of that, or $6 billion or so, advertising themselves in their listings. Much of that $6 billion spend is still offline. What we’re doing is, through the Premier Agent program, we’re going after that $6 billion TAM [total aggregate market], but then they actually spend a bunch of other money on other services such as CRM and agent websites and a number of other technology things. By moving in a direction of providing a full suite of services to these agents, we’re trying to become more relevant to those agents and therefore garner a greater portion of that $6 billion TAM, of which today we have a less than 1% wallet share. It’s a little bit mind boggling, if you think about it. As the largest real estate Company on the Web, we have less than 1% wallet share of what all agents spend on advertising. It’s a bit of an embarrassment, quite frankly. Despite, our massive revenue growth, we’ve just scratched the surface of the opportunity in terms of how big this market is.

48. Unbeknownst to investors, Zillow was experiencing great difficulty in capturing and

retaining the market for real estate agents, due to the Company’s transition to a new, more expensive

impressions-based pricing system for the Premier Agent program, along with various competitive

factors and concerns about Zillow’s business practices.

C. Zillow’s Shift to Impression-Based Pricing for Agent Advertising

49. Under the Premier Agent program, real estate agents purchase ad listings on the

Company’s web and mobile platforms, whereby the agent’s contact information appears next to the

search results for homes in the purchased zip code. The Premier Agent program was previously

offered at a single “Platinum” level, but Zillow eventually transitioned the Program into three

escalating levels of agent participation—Silver, Gold and Platinum—thus offering agents more

purported features and more listing exposure at increasing price points.

50. The Company charges different rates to agent subscribers based on the zip code in

which they operate according to market forces in the relevant market. For example, a subscriber

operating in higher demand, higher price areas such as Manhattan or San Francisco would pay

substantially higher rates than a subscriber who was operating in areas like upstate New York,

Tennessee, or other parts of the country where housing prices are less competitive. Therefore, it was

I A 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - I 'I - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

- 15I S- 1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 18 of 71

I critical that Zillow focus its marketing and sales efforts on retaining agents in high-end, major

I metropolitan markets with high housing prices.

51. Prior to the Class Period, Zillow sold advertising based on a percentage of all viewers

within a given zip code (which it calls “percentage of voice” or “share of voice”). Under the

percentage of voice pricing model, Zillow offered real estate agents 25%, 50%, 75%, or 100% of all

web traffic for the search results on its website and mobile platforms for homes in a given zip code.

Due to space limitations, however, no more than three advertisements could be displayed on

Zillow’s website. Thus, there was a theoretical limit of 12 on the number of subscriptions that

Zillow could sell within any zip code; if each agent purchased 25% of the voice, there would be a

total of 12 agents advertising within a given zip code (4 agents each with 25% of the voice times 3

advertising slots on the website).

52. In an effort to overcome this limitation, Zillow implemented a new pricing model in

which advertising would no longer be sold based on percentage of views, but rather upon the number

of impressions ( i.e. , the number of times potential home buyers viewed the webpage for a given zip

code) that occurred within any given month. Thus, Zillow’s existing Premier Agents who had

Platinum subscriptions would no longer receive 25% to 100% of the impressions within a given zip

code (depending on what percentage they had purchased). Rather, they would be transitioned to the

new pricing model where they would pay for the number of impressions delivered each month.

53. This new impressions-based pricing model could allow Zillow to expand the number

of agents who were purchasing advertising within any given zip code, for as long as traffic to

Zillow’s website grew, there would be more product to sell. By the start of the Class Period, Zillow

was in the process of rolling out this new impressions-based pricing model, and investors were most

interested in whether or not Zillow was having success with its new pricing plan. Investors wanted

to know whether existing Platinum subscribers were renewing their subscriptions and whether

Zillow was obtaining greater revenue per subscriber. Zillow tracked this performance metric in the

form of ARPU, but did not disclose ARPU to investors until the end of the Class Period, and only at

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 19 of 71

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

the behest of the SEC. As alleged below, Defendants publicly represented that Zillow was having

great success during the Class Period with its new impression-based pricing model, when in fact

large numbers of existing Platinum subscribers were objecting to the new plan, and either renewing

their subscriptions at a lower tier or cancelling their subscriptions. The high rate of existing-

subscriber turnover was forcing Zillow to incur greater costs to replace, retain and expand

subscription membership. This had the effect of reducing Zillow profitability at the same time

Zillow’s revenue growth rate was slowing (as was its ARPU), which meant Zillow’s earnings would

be at risk and, in fact, the Company would soon be incurring losses.

D. Customers Were Cancelling or Downsizing Their Subscriptions, and Churn Was Increasing

54. Zillow’s new impression-based pricing model was not popular with existing

subscribers, because it gave them less advertising exposure, was considerably more expensive, and

increased competition on the website. As a result, Zillow was experiencing problems with its rollout

of impression-based pricing, as a large number of existing agents, who had already purchased

subscriptions to its Premier Agent program, were cancelling these subscriptions. Also, other existing

agents with subscriptions that were up for renewal were refusing to renew at the new pricing and

were subscribing at a lower price point. As a result, contrary to the Company’s public disclosures

during the Class Period, Zillow was experiencing waning subscriber retention throughout the Class

Period, resulting in significant “churn.” Churn is the rate of attrition, or rate at which Zillow’s

subscribers leave during a given period of time. The Company was losing customers at a rapid rate,

which put pressure on its sales force to begin aggressively attracting new customers from less

competitive, untapped markets.

55. The shift in Platinum pricing was not well-received by subscribers who were up for

renewal of their subscriptions. As more subscriptions came up for renewal, more and more

subscribers were shocked by the drastically increased cost, causing a large number of them to

terminate their Premier Agent subscriptions altogether, or switch to the lower-cost Gold and Silver

subscriptions. During the Class Period, the rate of agents who were cancelling their subscriptions, or

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM)

- 1 0 - (206) 623-7292 • FAX (206) 623-0594 i ,- 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101

E L . HAGENS BERMAN

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 20 of 71

I churn, reached very high levels as the Company attempted to promote its switch to the new Platinum

I subscriber model. The Company was forced to increase its sales efforts to rapidly replace the steady

stream of outgoing subscribers.

56. The CWs, former sales consultants and back office administrators at Zillow’s Seattle

and Irvine offices, confirm that Zillow was having problems rolling out its new pricing plan and the

resulting churn in agent subscriptions. CW1 is a former marketing and sales consultant who worked

at Zillow’s Seattle headquarters from February through June 2012. CW1’s supervisor reported to

Doug Slotkin (“Slotkin”), Vice President of Local Advertising Sales. CW1 was responsible for

selling Zillow subscriptions to real estate agents. CW1 indicated that due to the switch to the new

pricing plan, agents who had been clients of Zillow for 2-3 years were ending their subscriptions.

CW2 is a former employee of Zillow who worked as a sales consultant in the Seattle office from

July 2010 to March 2013. CW2’s primary responsibilities included signing contracts with “big

money” agents and real estate companies to place their listings on Zillow’s website. CW2 stated that

existing agent customers were “freaking out” at the pricing increase, and that Zillow’s churn rate

was high. CW3 is a former inside sales consultant who worked at Zillow’s Irvine office from June

2012 through September 2012. CW3 reported to Jon Boller, Sales Director, and then Cody Fagnant,

Sales Manager, who in turn both reported to Slotkin. CW3’s responsibilities included selling

Premier Agent subscriptions to real estate agents. CW3 stated that several sales consultant’s

customers were similarly “furious” about the switch, in large part because they believed it

diminished their exposure and ROI.

57. With the transition to the more expensive impression-based pricing plan, many

existing real estate agents expressed their dissatisfaction with the ROI on their purchase of Platinum-

level ad listings. These agents either discontinued their Platinum subscriptions altogether, or opted

to purchase less page views (at the same or lower price), or switched to less costly Silver or Gold

subscriptions. CW4 is a former account executive who worked at Zillow’s Seattle office from June

2010 through July 2012. CW4 reported to Team Manager Jeremiah Flocchini, who in turn reported

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

1 '.7 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - I I - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 21 of 71

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

to Slotkin. Slotkin reported to Chief Revenue Officer, Greg Schwartz (“Schwartz”), who in turn

reported to Rascoff. CW4’s responsibilities included selling Zillow’s services to new subscribers

(real estate agents and agencies) and maintaining existing relationships. CW4 confirmed that many

Premier agents were renewing at the least expensive Silver rate because they did not feel that Gold

and Platinum subscriptions met their ROI requirement. CW5 is a former inside sales a consultant

who worked at Zillow’s Seattle office from February 2012 through June 2012. CW5 stated that

some agents felt that they were paying a lot of money for the new pricing structure and not getting

enough return on investment.

58. CW4 confirmed that there was a trend towards lower tier subscribers throughout

CW4’s tenure, both when selling share of voice and selling impressions. CW4 noticed this trend

when Zillow added the Silver and Gold tiers to the Premier Agent program. CW4 explained that

even when the impressions model was instituted, many subscribers who wanted to remain as

Platinum Agents did so, but would buy fewer impressions because they deemed it too expensive and

did not recognize enough ROI to keep up the same percentage of the zip code that they had when

buying shares of the zip code. CW4 added that many other customers switched to the Silver and

Gold programs after the impressions model was instituted.

59. Zillow’s management, including the Individual Defendants, was well aware of

Zillow’s churn rate. CW6 is a former executive assistant who worked for Zillow from July 2012

through March 2013. CW6 worked as an executive assistant for certain executives including

defendant Cohen. CW6 also assisted in preparing Cohen and Raymond “RJ” Jones for investor

presentations and analyst calls. According to CW6, Rascoff held monthly company-wide meetings

where churn was regularly discussed. During these meetings, Rascoff provided an “executive

overview,” which always includes churn rate data. CW7 is a former inside sales representative who

worked at Zillow from August 2012 through February 2013. CW7 reported to Blake Lester, Sales

Manager, who in turn reported to Slotkin. CW7 was responsible for selling advertising. CW7

i 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - I 8 - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

- 19i g' 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 ) - (206)623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 22 of 71

I attended meetings with Zillow’s executive management, including Rascoff, during which they would

I brainstorm ideas on how to decrease churn.

60. CW1 stated that churn rate got “really bad” during his time at Zillow. Based on

conversations he had with friends still employed at Zillow, CW1 attributed the churn rate to the

changes in billing practices from a percentage-based plan to a page-use plan. CW1’s description of

the billing practices demonstrated the difficulty sales consultants faced when attempting to renew

subscribers under the new plan. CW1 provided the following example: Suppose a zip code has

10,000 page uses, or impressions. Under the percentage plan, if a realtor paid for 25% of that zip

code, that realtor would be guaranteed to be viewed 2,500 per month for that particular zip code.

Under the impression-based plan, the realtor pays based on the total monthly impressions, or the

amount of times a zip code was viewed per month. So a realtor that was previously paying for 25%

of a zip code now has to pay more due to increased impressions. To reflect this cost, Zillow told its

customers that if their impressions went from 10,000 to 40,000, their fee to advertise on Zillow

would increase 400%, directly proportional to the increased views of their ads.

61. CW1 stated that by the time he left Zillow in early July 2012, Zillow had upset its

I client base and that realtors began leaving Zillow. CW1 stated: “ There are not that many agents in

high-end markets, and when Zillow screws over one of them, they all talk about it .” 1

62. CW2 described Zillow’s churn rate as “high” based on the level of turnover not only

in his accounts, but also based on meetings where subscriber metrics were a topic. CW2 stated that

I subscriber “metrics were getting worse in 2012,” and notes that it was discussed in internal meetings

I with department managers.

63. For example, CW2 mentioned one meeting held sometime between June and

I September 2012 where Rascoff stated that retention was down, as was the signing up of new

I subscribers. According to CW2, other meetings held by department managers throughout 2012 were

1 All emphasis is added.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 (206) 623-7292 • FAX (206) 623-0594 - 20 -

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 23 of 71

I held to discuss how to deal with the problem of sagging demand and how to bring in new

I subscribers. In order to retain the subscribers and reduce churn, the Company resorted to offering

I significant discounts.

64. CW2 stated that due in large part to the “churn aspect,” subscription contracts were

reduced from 12 months to six months to blunt the total price increase over the term of the contract.

CW2 noted that these six-month subscriptions still came at significantly higher monthly prices,

however. According to CW2, a subscriber who was grandfathered in at a rate of $150 per month

prior to the switch would still have to pay $500 per month after the switch. Observing that it was a

“battle” to convince subscribers to accept more than double their prior monthly rates, CW2 stated

that the Company hired an entire new team in 2012 dedicated to calling subscribers when their six-

month contract was up and informing them of the price increase. Even so, CW2 noted that

customers were “freaking out” at the increased pricing.

65. CW8 is a former inside sales representative at Zillow in its Irvine, California office,

employed from October 2012 to March 2013. CW8 reported to Cody Fagnant, Sales Manager, who

reported to a floor manager that in turn reported to Slotkin. CW8 stated that when a subscriber from

highly desirable areas such as Malibu, Laguna Beach, Santa Monica and Silicon Valley left, it was

very hard to replace them because the costs were much greater, sometimes as much as $2,000 per

month per zip code. CW2 was also responsible for the larger accounts and corroborated CW8’s

account, noting the difficulty with which he kept his large customers satisfied and that “it was taking

everything that I had to keep them onboard, including discounts.” CW2, CW8 and CW9 corroborate

that the Company replaced these Premier Agents during the Class Period with agents from smaller

markets at greatly reduced subscription rates. Hence, even if the Company was able to renew the

large customers during the Class Period it was forced to offer greatly reduced rates, and the more

expensive contracts were replaced with customers from less expensive locales.

66. CW9 is a former real estate marketing specialist with Zillow, was employed by the

I Company from June 2010 to June 2012 ,and was one of the top 15 out of 180 sales representatives at

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 24 of 71

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

the Company. CW9 reported to Robert Dietz, who in turn reported to Doug Slotkin. CW9’s

responsibilities included selling Zillow’s services to new subscribers (real estate agents and

agencies) and maintaining existing relationships. According to CW9, due to the increase in pricing,

Zillow was having trouble selling Platinum-level listings for high profile, expensive residential

areas. To make up for the high rate of churn in these areas, Zillow’s sales staff had to aggressively

sell subscriptions to agents in new areas that were less in demand and did not generate high margins.

Zillow’s expansion into these new, lower demand areas, while it increased the number of new

Premier Agent subscribers, also drove down the ARPU, as revealed at the end of the Class Period.

67. CW9 also noted that it was very difficult to retain old customers due to a low ROI.

CW9 advised that for every 10 new clients that were added per month, Zillow would probably lose

8 or 9 of them in a few months . CW9 stated that while the customer base at Zillow was expanding,

it was moving to less profitable areas and away from more profitable areas such as Manhattan and

northern and southern California.

68. Faced with an increasing rate of churn that was being exacerbated by the transition to

the more expensive impression-based pricing plan, Zillow was forced to aggressively sell lower

priced Silver and Gold subscriptions to make up for agents who were cancelling their Platinum

subscriptions. Thus, while Defendants represented a significant increase in the number of new

Premier Agent subscribers each successive quarter in 2012, they did not disclose that a substantial

portion of these new subscribers were lower margin Silver and Gold-level agents. Moreover, Zillow

did not disclose ARPU until the end of the Class Period after being compelled by the SEC, so

investors and analysts had no way of determining if the new pricing plan allowed the Company to

increase pricing or of knowing the composition of Zillow’s Premier Agent subscriber base during the

Class Period.

E. Further Resistance to Zillow’s Business Practices

69. In addition to real estate agents’ resistance to the roll out of the new impression-based

I pricing model, Zillow was facing a number of other challenges that were interfering with the success

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

-i i 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 - L I - (206) 623-7292 • FAX (206) 623-0594

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 25 of 71

I of this new program. Zillow was facing increased competition from other online real estate portals

I offering similar services such as Realtor.com , Housevalues.com, Move.com, Redfin.com, and

Trulia.com, which filed for its initial public offering during the Class Period.

70. Moreover, many in the real estate industry held the view that Zillow simply wanted to

charge agents for their own intellectual property and hard work in creating property listings. Zillow

was seen as disruptive to the traditional real estate brokerage business model because it provided

potential buyers and sellers with many of the same services that agents provided. Accordingly, there

were agents that viewed Zillow as a direct competitor and were not interested in the ad subscriptions

or other services the Company offered.

71. Zillow further alienated agents by offering a “Make Me Move” service on its website,

through which homeowners could post on Zillow’s website the offer price they would accept to sell

their homes. Thus, through the Make Me Move service, potential sellers could effectively cut agents

out of the sales transaction, thereby giving agents even less of an incentive to advertise through

Zillow.

72. Certain agents also considered Zillow’s listing information to be inferior and

inaccurate compared to the listing information provided by more traditional MLS sources, and they

therefore did not want to be affiliated with Zillow. A study published by the WAV Group in

October 2012 confirmed a number of deficiencies in Zillow’s home listings. The study revealed that

about 36% of the listings shown as “active” on Zillow were in fact no longer for sale, compared with

zero percent or near-zero percentage for the listings on brokerage websites using traditional MLS

information. Also, the brokerage websites surveyed contained 100% of the homes listed for sale by

MLS, while Zillow only featured 79% of the MLS listings. Further, the study found that home

listings were slower to make their way to Zillow’s website, as newly listed homes showed up a

median of seven days earlier on brokerage websites using MLS.

73. Additionally, agents, along with consumers, did not trust Zillow’s proprietary

I valuation system, Zestimates, because it was notoriously inaccurate and failed to provide a

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE , WA 98101 - - (206) 623-7292 • FAX (206) 623-0594

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM) E L . HAGENS BERMAN

1918 E IGHTH AVENUE , SUITE 3300 • S EATTLE, WA 98101 (206) 623-7292 • FAX (206) 623-0594 - 23 -

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 26 of 71

reasonable assessment of a home’s fair market value. In boom times, Zestimates overvalued home

prices, and during the recovery time ( i.e. , the Class Period), it undervalued homes in relation to

listing prices, which undercut the ability of real estate agents to close transactions based on the listed

price. It was reported that the Zestimates system was so flawed that 35 million homeowners

submitted corrections to their home estimates to Zillow.

74. In addition to the growing competition for web-based advertising, Zillow had been

marketing its Premier Agent subscriptions for years prior to the start of the Class Period and a large

percentage of real estate agents who were interested in purchasing advertising on Zillow’s website

had already done so. While Zillow was able to grow its total number of subscribers during the Class

Period, it was only able to do so at greatly increased cost, as alleged below. In addition, Zillow’s

revenue growth rate was slowing during the Class Period, and Defendants understood that this trend

was likely to continue as the market for Zillow’s product was becoming saturated.

75. All of these forces were in direct opposition to Zillow’s business model, and they

were further reasons why Zillow was experiencing problems in rolling out its new price model and

unable to raise pricing during the Class Period.

F. Zillow’s Increased Expenses in Connection with Attracting and Maintaining Agent Subscriptions

76. Zillow announced on May 2, 2012 that it would open a new sales office in Irvine,

California in the summer with 80 sales associates, in addition to the office it already operated out of

its Seattle headquarters. This increase in expenses related to sales was necessary in order to make up

for the large number of cancelling subscribers.

77. Although the Company stated the goal of the new sales force was to focus on selling

Premier Agent subscriptions across the country, as demonstrated by the chart below, the increase in

costs attributable to the new sales team did not bring a commensurate increase in marketplace

revenue. Over the Class Period, the Company increased its sales and marketing expenses by 86%—

from $7.58 million during the fourth quarter of 2011 to $14.12 million during the third quarter of

2012—whereas the Company’s marketplace revenues only increased by 71% over the same period.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 27 of 71

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

I The following chart shows that sales and marketing expenses nearly doubled during the Class

I Period, and further demonstrates the diminishing revenue returns throughout the Class Period

I relative to expenses:

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

Marketplace Revenue 13,746 16,593 19,623 23,616 26,838

Sales and Marketing Expenses 7,576 8,315 12,153 14,118 14,519

G. Zillow’s Static Average Revenue Per Customer

78. ARPU, or average revenue per user, is a performance metric used by web-based

companies like Zillow to track and measure the revenue generated by single, average customer per

quarter. Prior to and throughout the Class Period, investors and analysts wanted Zillow to disclose

ARPU because it would show the average subscription revenue generated by each Premier Agent,

and thus whether Zillow was successfully implementing its new Premier Agent pricing plan.

Because Zillow did not disclose ARPU during the Class Period, investors had no real insight into the

“mix” of agents in the Premier Agent program ( i.e. , whether they skewed toward higher price

Platinum subscriptions or lower price Silver/Gold subscriptions) and could not accurately determine

the profitability of the Premier Agent program. Zillow further obfuscated the profitability of the

Premier Agent program because it only reported Marketplace Advertising revenue, which combined

both Premier Agent subscription revenue and Zillow Mortgage Marketplace revenue.

79. Because ARPU was an important indicator of Zillow’s revenue mix, revenue growth

and profitability, analysts tried to calculate ARPU themselves, but with little success. For example,

the day after the August 7, 2012 analyst conference call, an analyst from PAA Research issued a

report on Zillow’s financial performance in 2Q12, in which he estimated ARPU for that quarter, as

well as future quarters. The PAA analyst calculated ARPU in 2Q12 as $316.70 and estimated

ARPU for 3Q12 as $307.20. Similarly, an analyst with ThinkEquity issued a report on August 8,

2012, which estimated ARPU in 2Q12 as $317. As would be revealed at the end of the Class Period,

these analyst calculations were far off base, as Zillow disclosed that ARPU in 2Q12 and 3Q12 were

$263 and $270, respectively.

CONSOLIDATED CLASS ACTION AMENDED COMPLAINT (2:12-cv-02084-RSM)

- - (206) 623-7292 • FAX (206) 623-0594 4 1918 E IGHTH AVENUE SUITE 3300 • S EATTLE , WA 98101 E L . HAGENS BERMAN

Case 2:12-cv-02084-RSM Document 52 Filed 06/24/13 Page 28 of 71

1

80. Although ARPU was a material performance metric, the Company adamantly refused

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

852878_1

to disclose the numbers to investors. It was only after the SEC sought disclosure of Zillow’s ARPU

in the third quarter of 2012 that the Company finally decided to disclose the metric. On August 20,

2012, Kathleen Collins, Accounting Branch Chief at the SEC, wrote to Rascoff and requested

additional disclosure of financial information for Zillow’s 2012 Form 10-K, filed with the SEC on

March 2, 2012. In response to the SEC’s inquiry, Cohen stated in a letter dated August 23, 2012,

that Zillow did not disclose ARPU because it was not “meaningful” to investors: “[T]he average

subscription price per Premier Agent subscriber is not meaningful because Premier Agent

subscribers are not limited in the amount or nature of inventory they may purchase ( i.e. , agents may

purchase multiple zip codes).”

81. In a subsequent letter dated August 30, 2012, the SEC disagreed with Cohen’s

assessment and indicated that ARPU was indeed meaningful to investors: