Embed Size (px)

Citation preview

DEMAND RESPONSE

WHERE DO WE STAND, WHERE DO WE GO AND HOW DO WE GO

CHALLENGES, OPPORTUNITIES AND PERSPECTIVES

JOISA DUTRA

CIGRE – DEMAND RESPONSE SEMINAR

SÃO PAULO DECEMBER 15, 2016

ROADMAP

Disrupting the Use-of-Energy Markets

Demand Response Business Models

Informing DR Through Economics

Final Remarks

DISRUPTING THE USE-OF-ENERGY MARKETSFROM ASSET-BASE & ENERGY VALUE CHAIN TO USER-CHOICE SERVICES

DISTRIBUTED ENERGY RESOURCES: SETTING THE SCENE

• Emerging technologies are disrupting the energy supply chain

• Consumers’ behavior have changed and actively exercising choice

• Utilities & regulators remain applying “old framework” in how to react to DER disruptions

Key Facts

Three emerging questions in this energy landscape:

What are the new business models & players in the markets?

What are the (expected) policies guiding the market?

What to regulate: subject, role and how regulators will adapt?

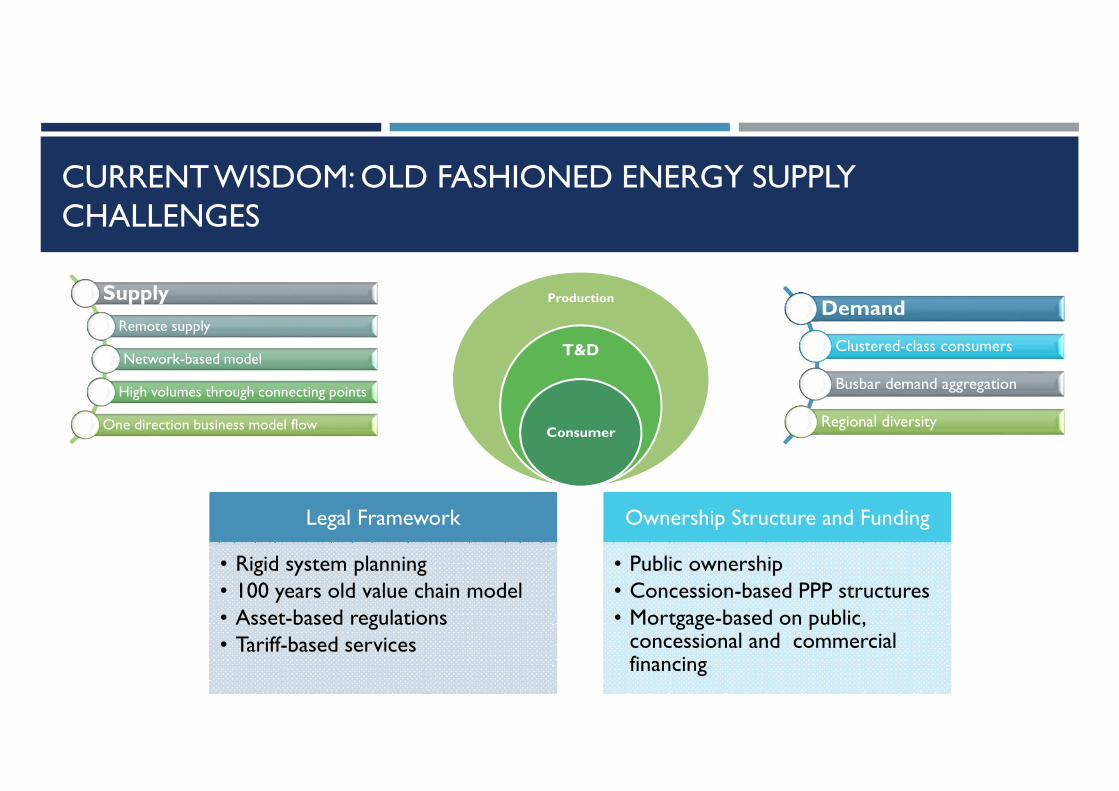

CURRENT WISDOM: OLD FASHIONED ENERGY SUPPLY CHALLENGES

Supply

Remote supply

Network-based model

High volumes through connecting points

One direction business model flow

Demand

Clustered-class consumers

Busbar demand aggregation

Regional diversity

Production

T&D

Consumer

Legal Framework

• Rigid system planning• 100 years old value chain model• Asset-based regulations• Tariff-based services

Ownership Structure and Funding

• Public ownership• Concession-based PPP structures • Mortgage-based on public,

concessional and commercial financing

Public “coordination” environment: concession and licenses to operate

CURRENT WISDOM: MORE EFFICIENT ‘100 YEARS OLD’ BUSINESS MODELS

Asset costs and energy supply management

• Large T&D networks

• Utility scale generation

• Fuel supply and retail management

+Debt costs (rates)

• Public & concessional funding

• ECA/DFI & commercial financing

+Equity returns

• Public (limited)

• Private - network (moderate)

• Private –commodities supply (moderate +)

=Cost of services & allowed revenues

• Regulatory levies and fees

• Taxes

Networks

Concession (size) rent seeking

Guaranteed revenues

Commodities

Volume & capacity rent seeking

Guaranteed entry barriers

Trading & Retail

Energy volume management mark-ups

Supplier & customer capture

Business models thrive on asset returns and

fuel/supply management mark-ups

DISRUPTING THE CURRENT WISDOM: TECHNOLOGY AND BEHAVIORAL CHANGES LEADING TO “NEW” BUSINESS MODELS

Tech

nolo

gy

Dis

ruptions Fast, reliable & Mobile

Telecoms

Web-based IT

Bounded demand systems efficiency

Smart grid-customer interface

Small size renewables generating & storage

Big data

Beh

avio

ral C

han

ges IT Services Platform

Predominance of customer’s choices, not consumer

Clustered energy services, not supply

Millennium investor approach N

ew B

usi

nes

s M

odel

s Aggregator platform (yields seeker)

Shared-asset usage (joint & part-time)

Convergence of services trading

Blending financing

INTRODUCING “NEW” BUSINESS MODELS WRAPPED BY BIG DATA AND THE INTERNET OF THINGS: NAVIGATING IN UNCHARTERED WATERS

Customer

Choice of services Data ownership Data leasing

Big Data Platform Host

Multisector Multi-Customer Origination Storage

Matching Providers & Customers

Data Rights Management

IT Infrastructure Enablers

Telecoms Distributed ServersProviders and Customers

Data Acquisition

Energy Providers

Services Aggregators

Multi-sectors

Competition and

Regulations

Platform & Data

Challenges: Ownership,

Rights, Obligations and Civil Liberties Threats

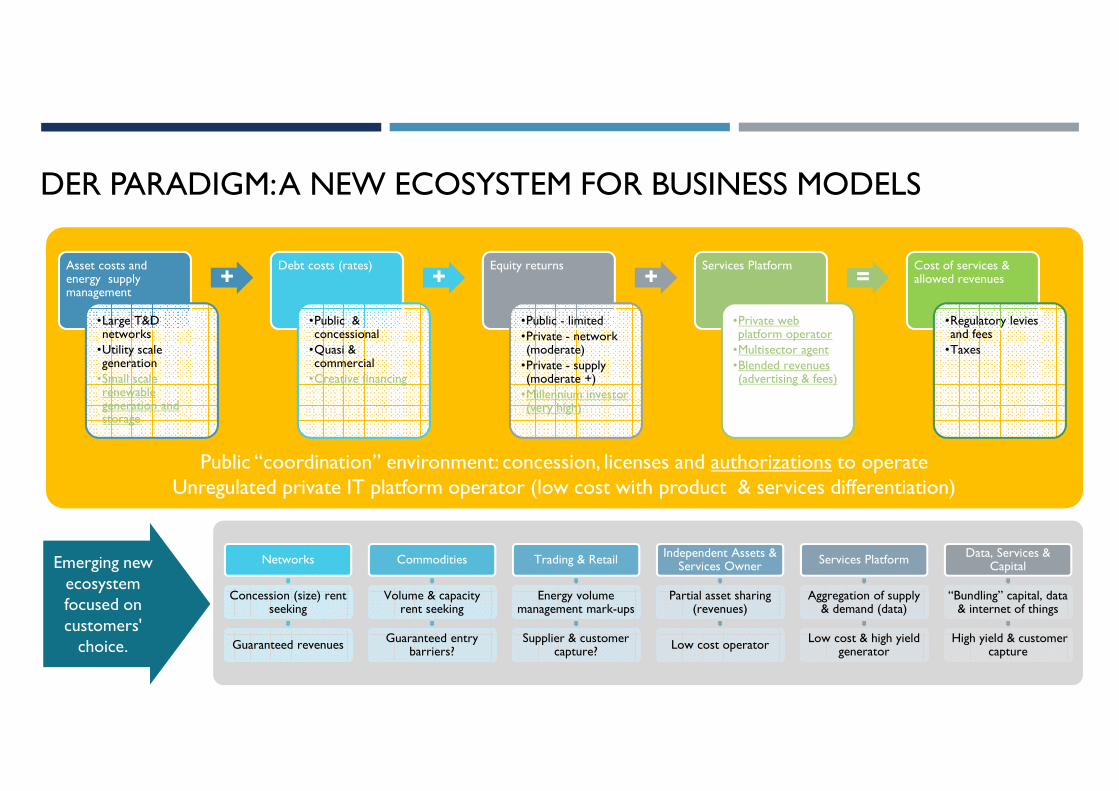

Public “coordination” environment: concession, licenses and authorizations to operateUnregulated private IT platform operator (low cost with product & services differentiation)

DER PARADIGM: A NEW ECOSYSTEM FOR BUSINESS MODELS

Networks

Concession (size) rent seeking

Guaranteed revenues

Commodities

Volume & capacity rent seeking

Guaranteed entry barriers?

Trading & Retail

Energy volume management mark-ups

Supplier & customer capture?

Independent Assets & Services Owner

Partial asset sharing (revenues)

Low cost operator

Services Platform

Aggregation of supply & demand (data)

Low cost & high yield generator

Data, Services & Capital

“Bundling” capital, data & internet of things

High yield & customer capture

Asset costs and energy supply management

•Large T&D networks

•Utility scale generation

•Small scale renewable generation and storage

+Debt costs (rates)

•Public & concessional

•Quasi & commercial

•Creative financing

+Equity returns

•Public - limited

•Private - network (moderate)

•Private - supply (moderate +)

•Millennium investor (very high)

+Services Platform

•Private web platform operator

•Multisector agent

•Blended revenues (advertising & fees)

=Cost of services & allowed revenues

•Regulatory levies and fees

•Taxes

Emerging new ecosystem focused on customers'

choice.

COEXISTENCE OF BUSINESS MODELS?

Energy chain supplier

Authorized revenues

RoE – 10%

Equity costs

Debt costs

Asset-base

Services Platform

Market-driven fee

Blended yields (25%+)

Platform costs

Aggregated asset-base & usage

Retailer” & Trader Yields seeker

Regulated asset rent seeker

Product & Services Costs and

Differentiation advantage

DEMAND RESPONSE (BUSINESS MODELS)

DEMAND RESPONSE BUSINESS MODELS

Demand Response Encompasses a Large Category of Technologies and Applications

Different BM emerge in each category

Automatically activated in response to price signals

Manually in response to requests from the DR business

Via alternative dispatch signals.

PRICE - BASED DEMAND RESPONSE

(TOU, CPP, RTP)

Does not requirethe load to be

verifiable.

Dynamic Pricing(CPP, RTP):

technological constraints

institutional constraints (absence of spot prices

reflecting short-run marginal costs on a real-time basis).

Trade-off: more accurate prices

Complexity, higher

transaction costs

Efficiency

Pilot programs

How reliable it is as a dispatchableload?

Pilot programs tailores to criticalareas?

INCENTIVE-BASED DR

INCENTIVE-BASED

Demand-sidebidding, interruptibledemand, and direct

load

More fit to deal withsudden contingencies.

How to define the value of reduction?

Rate of adhesion

policy

Complementary

technologies

Market mechanisms

Consumerengagement

EFFECTIVENESS

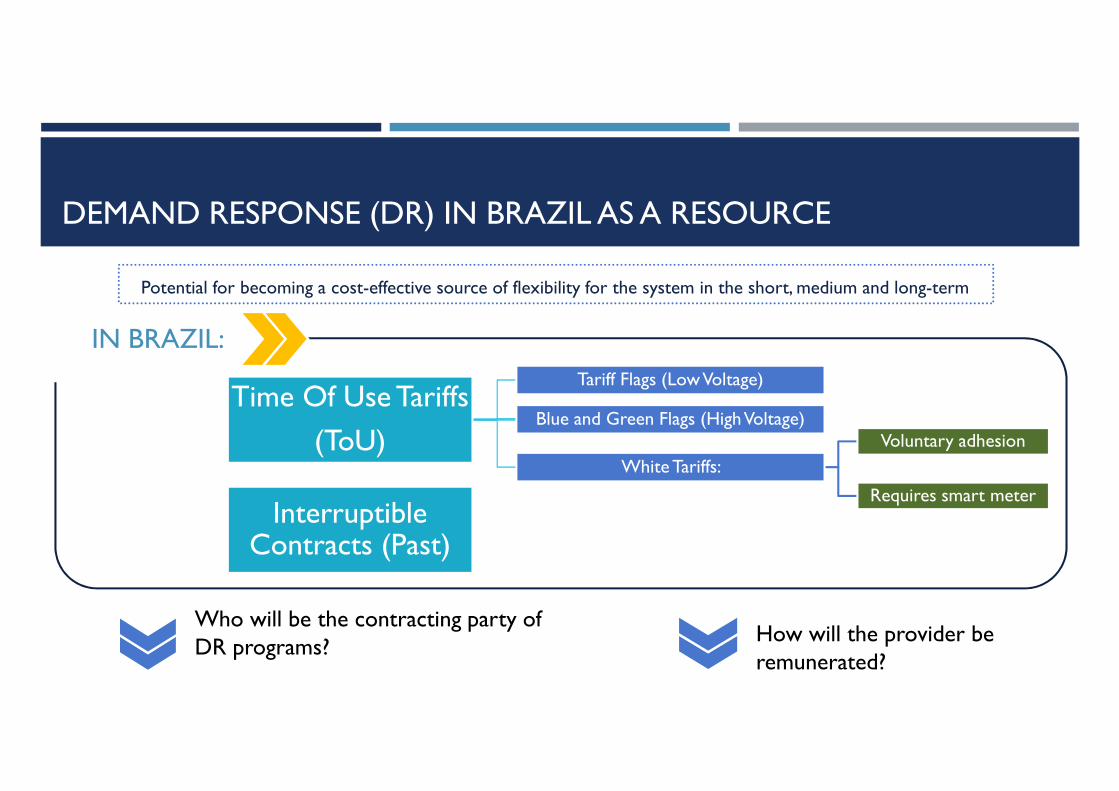

DEMAND RESPONSE (DR) IN BRAZIL AS A RESOURCE

Potential for becoming a cost-effective source of flexibility for the system in the short, medium and long-term

IN BRAZIL:

Time Of Use Tariffs

(ToU)

Tariff Flags (LowVoltage)

Blue and Green Flags (High Voltage)

White Tariffs:

Voluntary adhesion

Requires smart meterInterruptible

Contracts (Past)

Who will be the contracting party ofDR programs?

How will the provider beremunerated?

THE NEED OF A NEW REGULATORY FRAMEWORK TO LAUNCH DEMAND RESPONSE AS A RESOURCE

Need for new Business Models

Competition and new players in retail.

Requires the provisionof comparable (to

generation) opportunity

More Accurate PriceSignals

CONTRACTINGFRAMEWORK?

Aggregators:

• Transaction costs (specially for smallconsumers).

• Customer interface management.

• Portfolio of residential consumers hasincreased value

Enablers: technology.

Access to markets

Compensation

Demand growth for electricity grows

sales and revenue growth.

DG: Net metering scheme

DR: ToU tariffs

Transitional Arrangements

Consumer empowerment

New revenue streams for Utilities: more focused onelectric service provisions

DERs: comparableopportunities to those of

generation

More accurate price signals

Customer-side business models

Market design

• Energy• Capacity• Ancillary• Services

OUR APROACH

GOVERNANCE OF THE TRANSITION

Challenge: disruptive changes, pace of technology innovation, a new paradigm.

A dynamic framework for assessing priorities and recommendations, and

acting on them to provide a sound regulatory and competitive

environment must be drawn.

Requires a comprehensive and

integrated strategy

• active engagement of external stakeholders.

• interagency dialogue

The executive power: leadership role in orchestrating the interaction of

multiple stakeholders

• Acknowledge all stakeholders as strategic players.

Integrated view of short, intermediate, and long-term

objectives involving various actors and sectors.

Aneel “Chamada 20” R&D is animportant step in this direction –

necessary but not sufficient.

QuadriennialEnergy Review

(QER): An interagency Task Force,

which includes members from all relevant executive departments and

agencies (agencies) to develop an integrated

review of energy policy that integrates

all of these perspectives.

INFORMING (AND IMPROVING EFFECTIVENESS OF) DR THROUGH ECONOMICS

CONSUMER ENGAGEMENT CAN BE FOSTERED BY INSIGHTS COMING FROM ECONOMICTHEORY

� Understanding ConsumerElasticity is key for unlockingthe potential of DRs and SG Technologies.

� Behavior Science can shedsome (a lot!) light.

Economic Theory

can provide insights on

Economic Theory

can provide insights on

Market Mechanisms Market Mechanisms

Pricing IncentivesPricing Incentives

Empirical techniques Empirical techniques

Field Experiments Field Experiments

CONSUMER ENGAGEMENT CAN BE FOSTERED BY INSIGHTS COMING FROM ECONOMICTHEORY

Economic Theory

can provide insights on

Economic Theory

can provide insights on

Market Mechanisms Market Mechanisms

Pricing IncentivesPricing Incentives

Empirical techniques Empirical techniques

Field Experiments Field Experiments

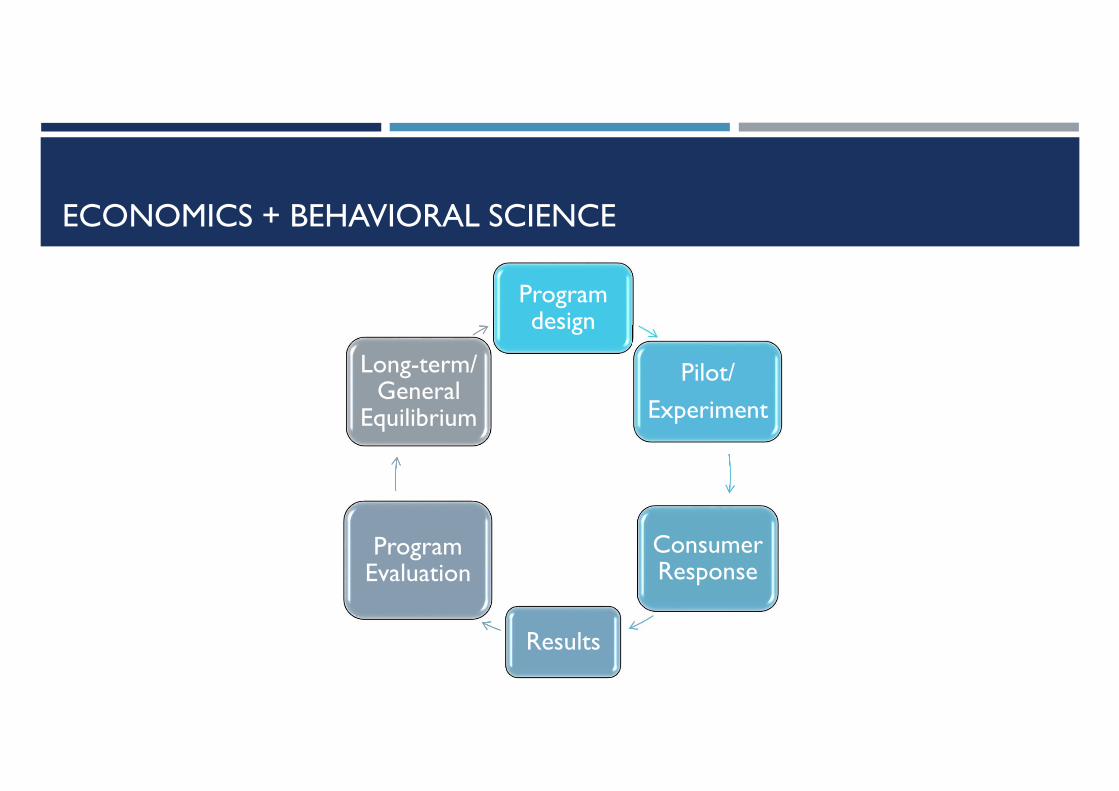

Experiments are Key to Inform the Implementation and Learning From It

ECONOMICS + BEHAVIORAL SCIENCE

Programdesign

Pilot/

Experiment

ConsumerResponse

Results

ProgramEvaluation

Long-term/ General

Equilibrium

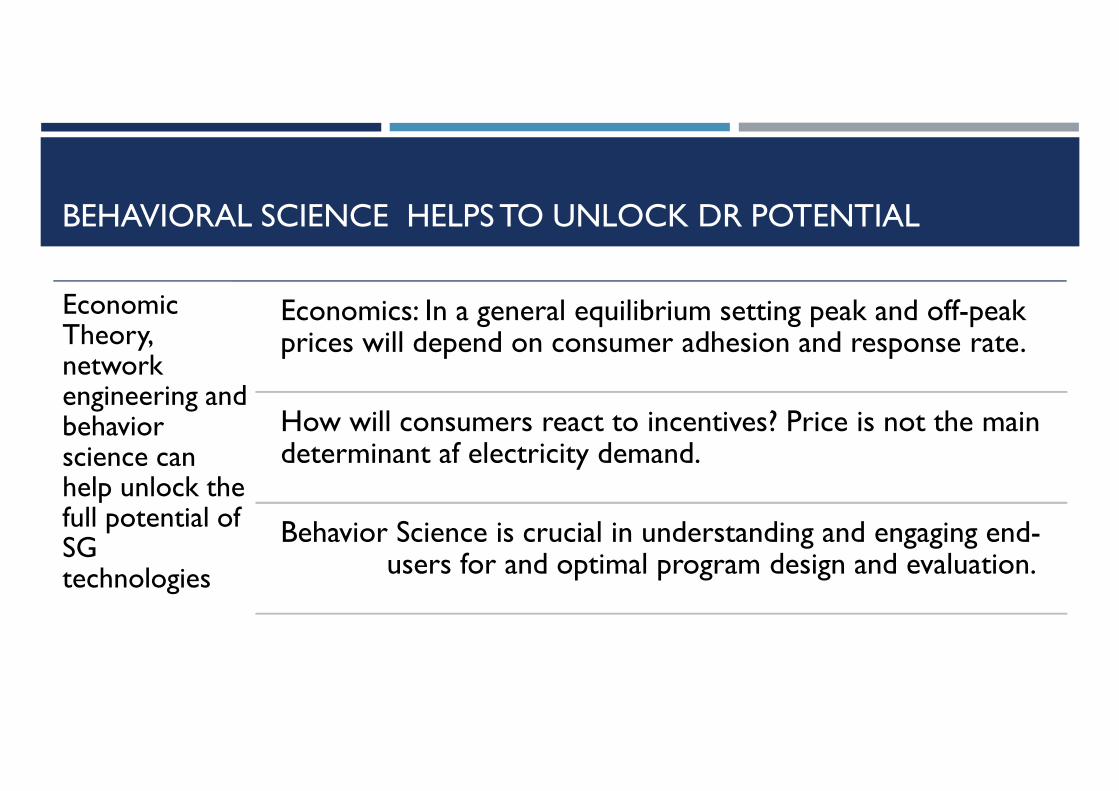

BEHAVIORAL SCIENCE HELPS TO UNLOCK DR POTENTIAL

EconomicTheory, network engineering andbehaviorscience canhelp unlock thefull potential ofSG technologies

Economics: In a general equilibrium setting peak and off-peakprices will depend on consumer adhesion and response rate.

How will consumers react to incentives? Price is not the maindeterminant af electricity demand.

Behavior Science is crucial in understanding and engaging end-users for and optimal program design and evaluation.

FINAL REMARKS

KEY MESSAGES

The (ongoing) process of weakening the traditional

value chain barriers expose incumbents and

leads to a cream skimming process

The entitlement of franchise(e) to supply

energy is ending

Isolated perspective myopia: new businesses

involving multiple sectors are evolving and capturing

profitable mark-ups/margins

New business models ecosystem is emerging as

key feature of demand response

Value is being squeezed through the emergence of

combined low cost operator and service

differentiation

Incompleteness of regulations and

unwillingness of regulators to evolve

Positioning, rivalry and tension could characterize

relationship among stakeholders

Coexistence of “Old" and “New” models are

expected to stay for a while

FGV CERI AND WORLD BANK ENERGY, LATIN AMERICA AND CARIBBEAN (LCR) PARTNERSHIP

� This presentation is part of a series of works being developed under a collaboration between FGV CERI(the Center for Studies in Regulations and Infrastructure-CERI at Fundação GetulioVargas ) and the World Bank (WB) to address key topics related to infrastructure investments in Brazil.

� The ideas discussed in these slides were presented by Prof. Joisa Dutra in São Paulo during the Demand Response event sponsored by CIGRE in São Paulo (December 15, 2016). They capture some of the thinking & perspectives current in discussions at FGV/CERI and the WB.