Embed Size (px)

Citation preview

John M Cooper

Vice-President

Anthem Blue Cross and Blue Shield

Affordable Care Act

22

What we’ll cover: ▪ Insurance carrier dashboard▪ ACA Impact to individuals & employers▪ Early look at results▪ What does the future hold and key items to

monitor

Today’s topics

3

Environmental Landscape & Market Factors

Margin compression through MLR and payer tax

Unsustainable costs plus rate

shock

ACA market expansion

Strong market competitors, new entrants & disruptors

Delivery system appetite for

taking on risk

Consumer demand for

information & convenience

.com

3

4

Shifting market dynamics

Exchanges become part of the new reality

We anticipate significant change ahead …

EXPECTED MARKET CHANGES

Uninsured

Large GroupRisk and ASO

Small Group

Individual

Medicaid

Medicare

4121M

20

2010Population

296M

2015Population

306M

1261M

127

32

26

15

266M

11M

19M

6M

39

58

43 49

4

Overview of 2014 changes

Changes that affect premiums

Guaranteed issueNo one can be denied coverage

Broader benefits and limits 10 types of Essential Health Benefits* required, out-of-pocket limits and deductible restrictions

Change in rating Rates based on age and address (and tobacco use, in some states), not gender and health status

At least 60% actuarial value Plans pay at least 60% of covered services

New taxes and feesApply to certain plans

Subsidies/credits Help those with low or moderate incomes pay for coverage

Reinsurance programInsurers / TPAs / self-funded plans contribute to fund high claims

New Health Insurance Marketplace (Exchanges) Offers plans for individuals and small groups *Not required for large-group and ASO plans

Why participate in the Exchange?

8

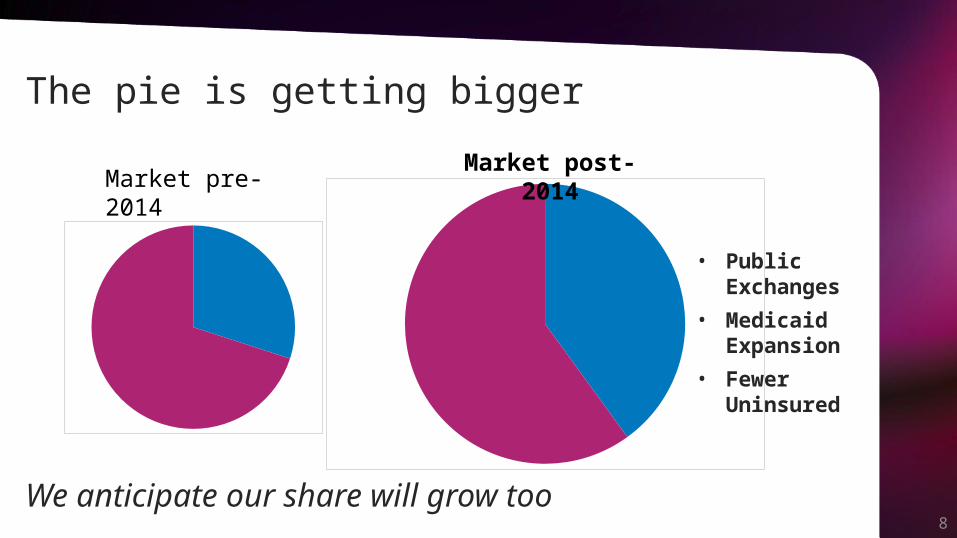

The pie is getting bigger

Market pre-2014Market post-2014

We anticipate our share will grow too

• Public Exchanges

• Medicaid Expansion

• Fewer Uninsured

9

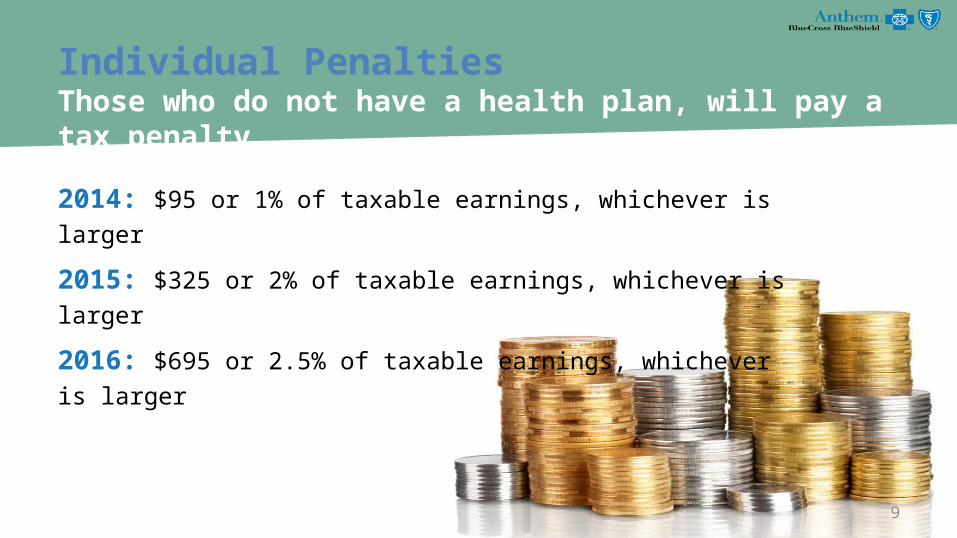

Individual PenaltiesThose who do not have a health plan, will pay a tax penalty.

2014: $95 or 1% of taxable earnings, whichever is larger

2015: $325 or 2% of taxable earnings, whichever is larger

2016: $695 or 2.5% of taxable earnings, whichever is larger

10

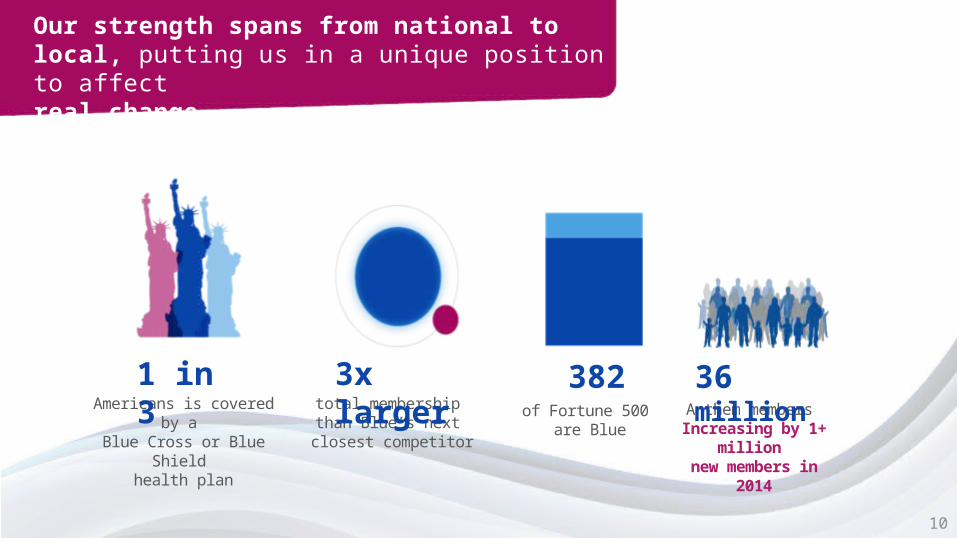

Our strength spans from national to local, putting us in a unique position to affect real change

Americans is covered by a Blue Cross or Blue Shield

health plan

total membership than Blue’s next

closest competitor

of Fortune 500 are Blue

Anthem members Increasing by 1+

million new members in 2014

1 in 3 3x larger 382 36 million

11

The health insurance market is evolving from traditional “wholesale” to a more consumer-oriented retail paradigm

Health insurance exchanges

Guaranteed issue

Essential health benefits/benefit standardization

Cost containment

Transparency

Defined contribution /private exchanges

Small group “dumping” to public exchanges

Increasing cost-sharing

New coverage models & alternatives

Increased desire for health & wellness

Tech-savvy consumers and improved connectivity (mobile, social)

Value seeking

Emerging health care consumerism

Retail Marketplace

Macro-Trends

Employer Coverage Changes

Changing Consumer Behavior

ACA Market Reforms

1212

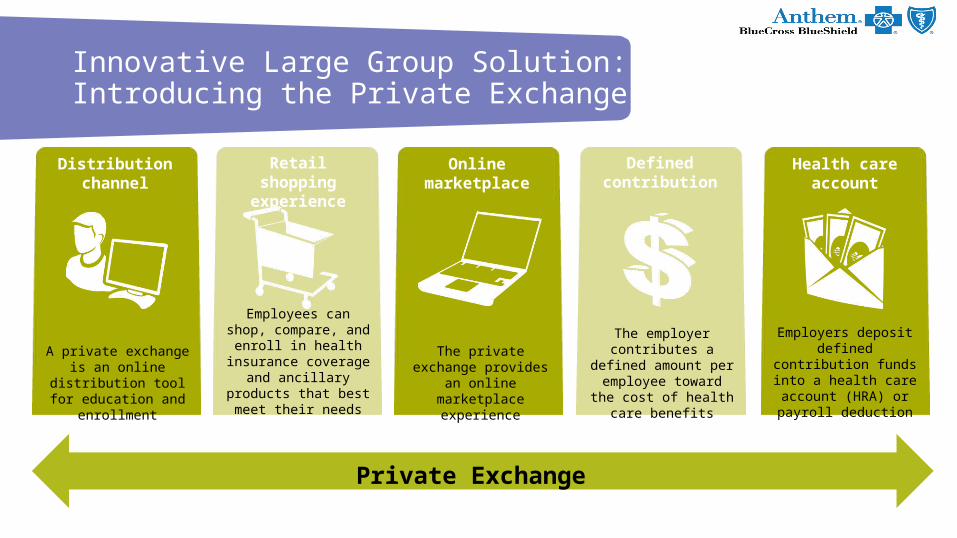

Innovative Large Group Solution:Introducing the Private Exchange

A private exchange is an online distribution tool for education and enrollment

Employees can shop, compare, and enroll in

health insurance coverage and ancillary products that best meet

their needs

The private exchange provides an online

marketplace experience

The employer contributes a defined amount per employee

toward the cost of health care benefits

Employers deposit defined contribution

funds into a health care account (HRA) or payroll

deduction

Distribution channel

Retail shopping experience

Online marketplace

Defined contribution

Health care account

Private Exchange

![Anthem Blue Cross and Blue Shield Hospital Assessment Fee [Insert image of members] January 2015](https://img.pdfslide.us/doc/110x75/56649cac5503460f9496e1f2/anthem-blue-cross-and-blue-shield-hospital-assessment-fee-insert-image-of.jpg)