Embed Size (px)

Citation preview

John L. Culhane, Jr., PartnerConsumer Financial Services [email protected]

Alphabetical Compliance – “M” is for Madden v. Midland and the Military Lending Act

2015 NCHER Fall Legal Committee Meeting

September 25, 2015Minneapolis, MN

Copyright 2015 by Ballard Spahr LLP

2

Madden v. Midland

3

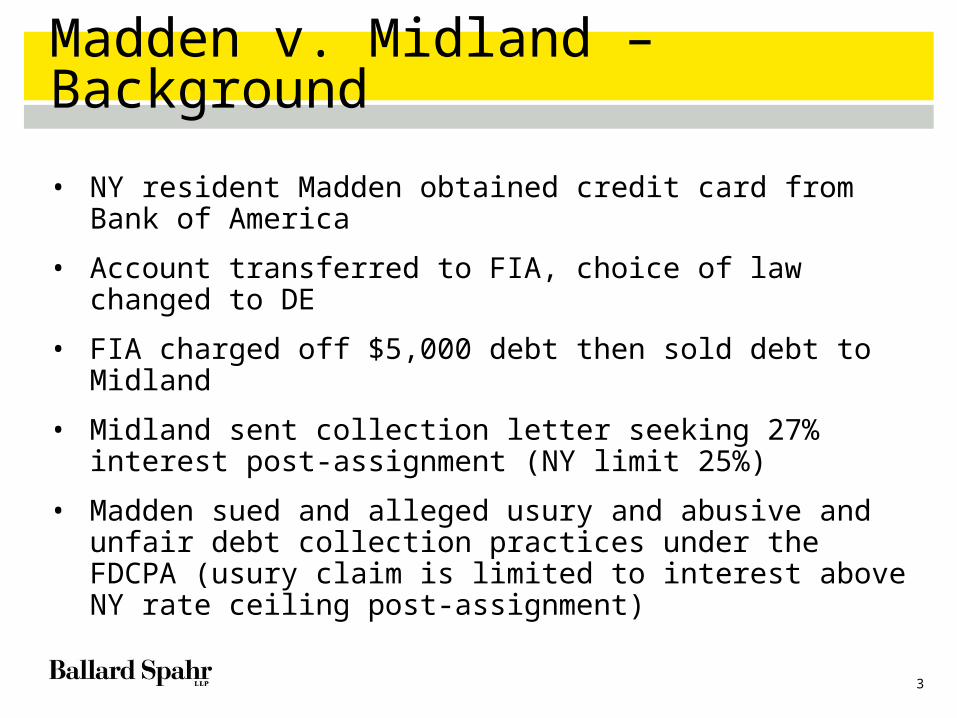

Madden v. Midland – Background

• NY resident Madden obtained credit card from Bank of America

• Account transferred to FIA, choice of law changed to DE

• FIA charged off $5,000 debt then sold debt to Midland

• Midland sent collection letter seeking 27% interest post-assignment (NY limit 25%)

• Madden sued and alleged usury and abusive and unfair debt collection practices under the FDCPA (usury claim is limited to interest above NY rate ceiling post-assignment)

4

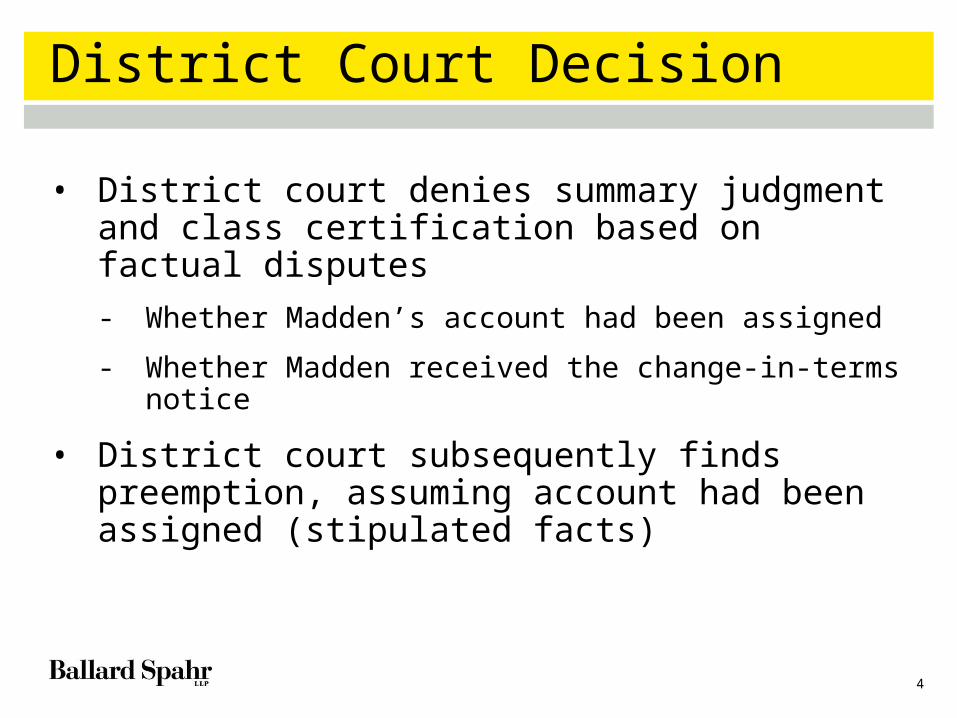

District Court Decision

• District court denies summary judgment and class certification based on factual disputes

- Whether Madden’s account had been assigned

- Whether Madden received the change-in-terms notice

• District court subsequently finds preemption, assuming account had been assigned (stipulated facts)

5

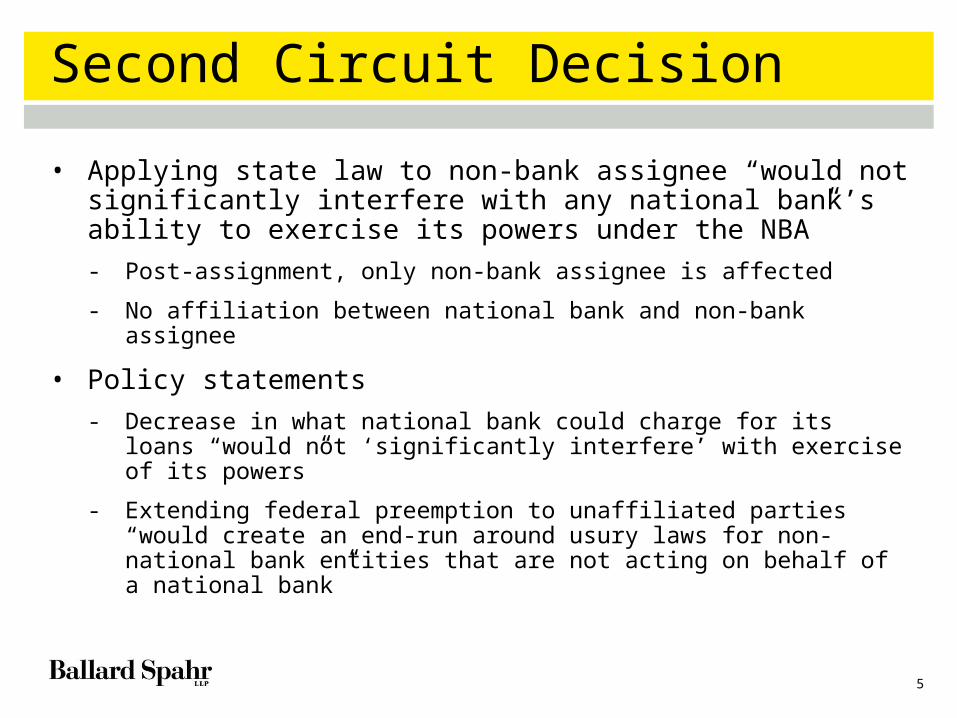

Second Circuit Decision

• Applying state law to non-bank assignee “would not significantly interfere with any national bank’s ability to exercise its powers under the NBA”

- Post-assignment, only non-bank assignee is affected

- No affiliation between national bank and non-bank assignee

• Policy statements

- Decrease in what national bank could charge for its loans “would not ‘significantly interfere’ with exercise of its powers”

- Extending federal preemption to unaffiliated parties “would create an end-run around usury laws for non-national bank entities that are not acting on behalf of a national bank”

6

Second Circuit Decision (cont.)

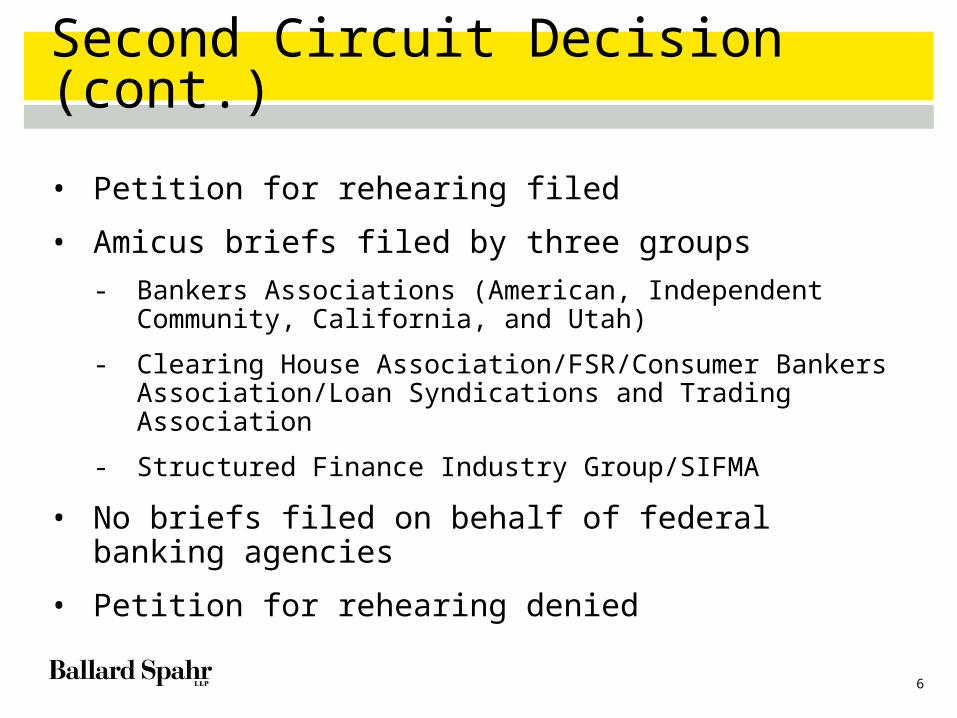

• Petition for rehearing filed

• Amicus briefs filed by three groups

- Bankers Associations (American, Independent Community, California, and Utah)

- Clearing House Association/FSR/Consumer Bankers Association/Loan Syndications and Trading Association

- Structured Finance Industry Group/SIFMA

• No briefs filed on behalf of federal banking agencies

• Petition for rehearing denied

7

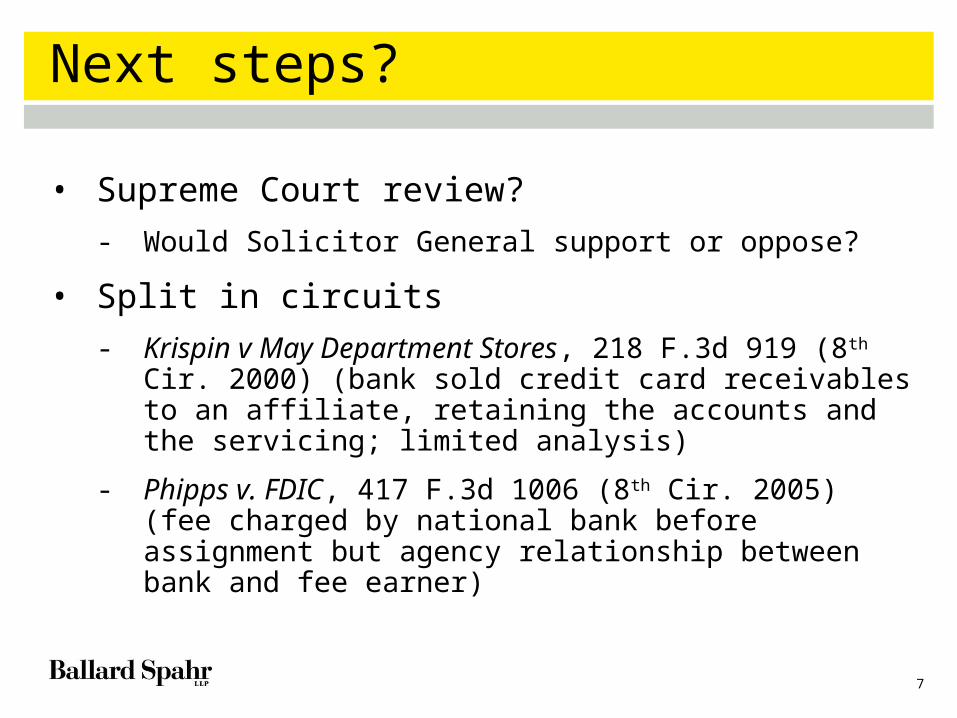

Next steps?

• Supreme Court review?

- Would Solicitor General support or oppose?

• Split in circuits

- Krispin v May Department Stores, 218 F.3d 919 (8th Cir. 2000) (bank sold credit card receivables to an affiliate, retaining the accounts and the servicing; limited analysis)

- Phipps v. FDIC, 417 F.3d 1006 (8th Cir. 2005) (fee charged by national bank before assignment but agency relationship between bank and fee earner)

8

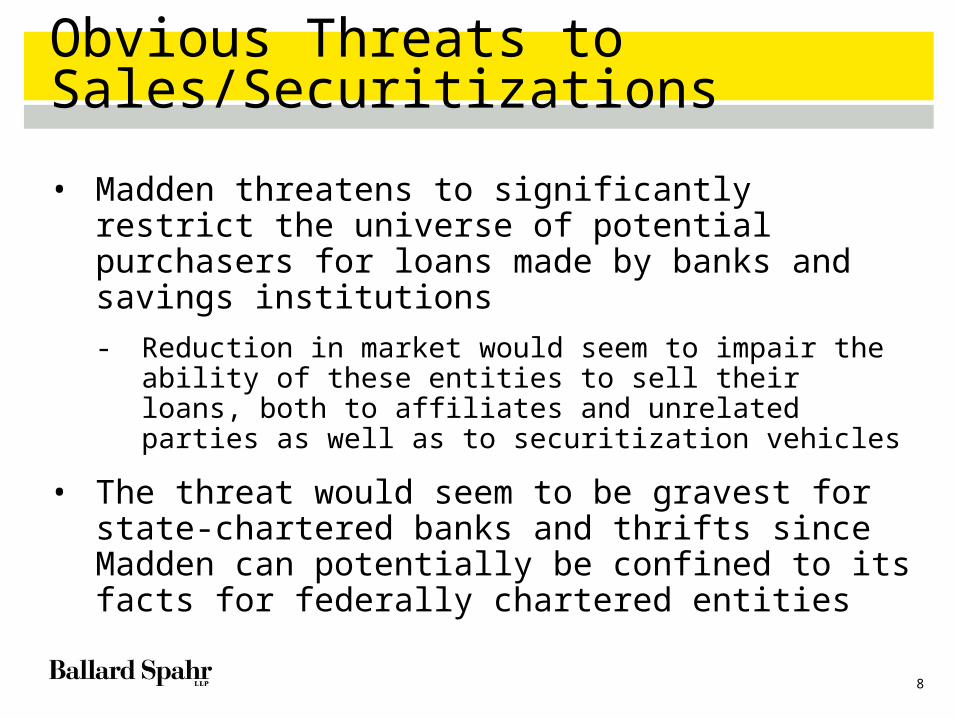

Obvious Threats to Sales/Securitizations

• Madden threatens to significantly restrict the universe of potential purchasers for loans made by banks and savings institutions

- Reduction in market would seem to impair the ability of these entities to sell their loans, both to affiliates and unrelated parties as well as to securitization vehicles

• The threat would seem to be gravest for state-chartered banks and thrifts since Madden can potentially be confined to its facts for federally chartered entities

9

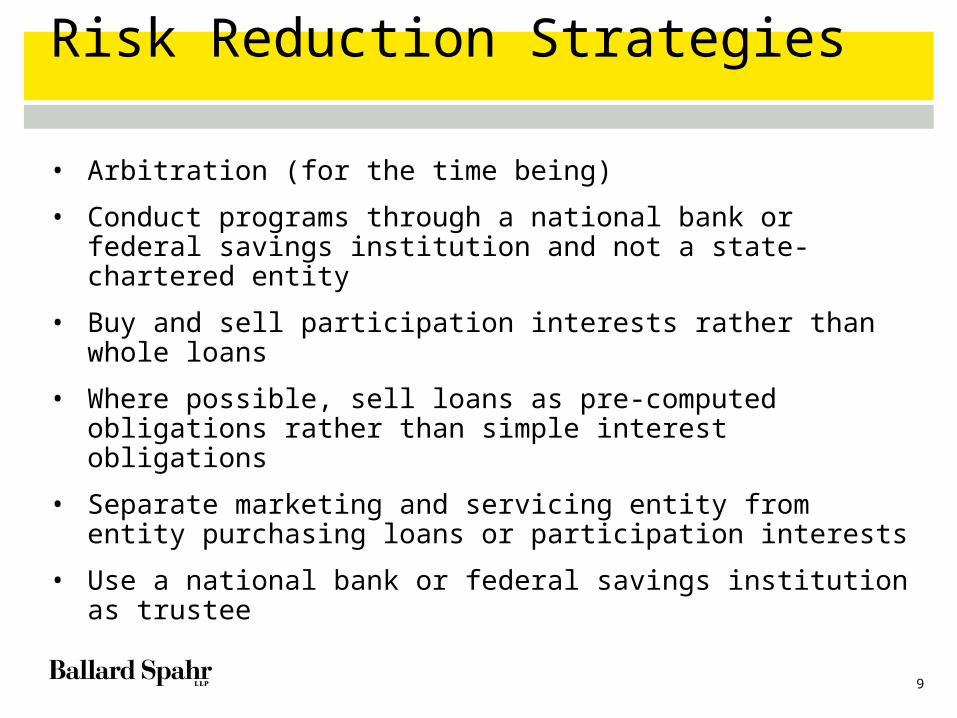

Risk Reduction Strategies

• Arbitration (for the time being)

• Conduct programs through a national bank or federal savings institution and not a state-chartered entity

• Buy and sell participation interests rather than whole loans

• Where possible, sell loans as pre-computed obligations rather than simple interest obligations

• Separate marketing and servicing entity from entity purchasing loans or participation interests

• Use a national bank or federal savings institution as trustee

10

Military Lending Act

11

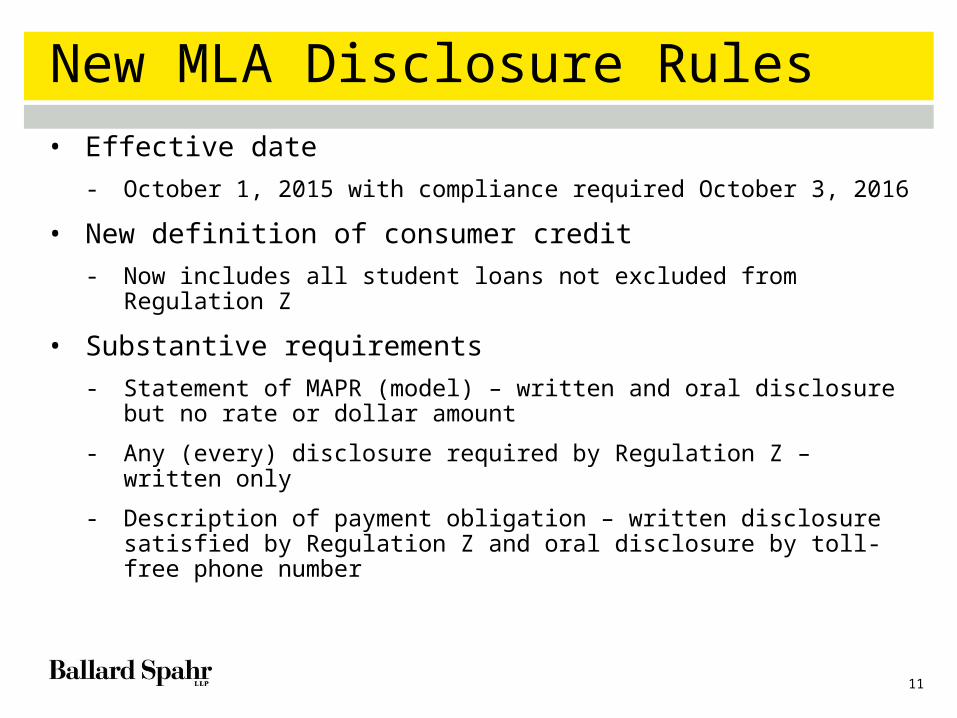

New MLA Disclosure Rules

• Effective date

- October 1, 2015 with compliance required October 3, 2016

• New definition of consumer credit

- Now includes all student loans not excluded from Regulation Z

• Substantive requirements

- Statement of MAPR (model) – written and oral disclosure but no rate or dollar amount

- Any (every) disclosure required by Regulation Z – written only

- Description of payment obligation – written disclosure satisfied by Regulation Z and oral disclosure by toll-free phone number

12

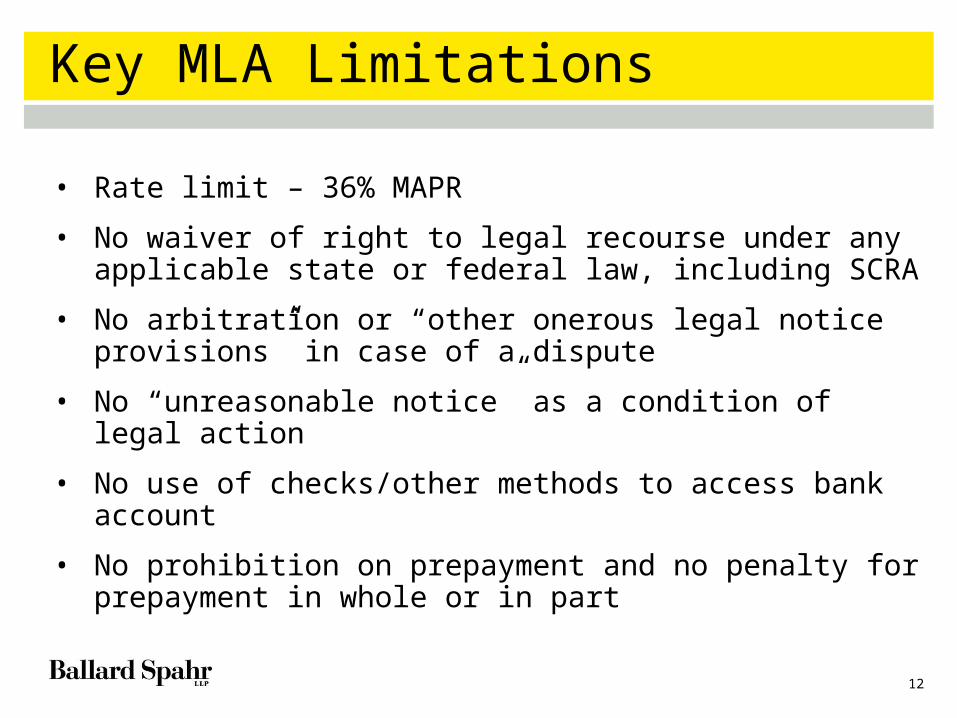

Key MLA Limitations

• Rate limit – 36% MAPR

• No waiver of right to legal recourse under any applicable state or federal law, including SCRA

• No arbitration or “other onerous legal notice provisions” in case of a dispute

• No “unreasonable notice” as a condition of legal action

• No use of checks/other methods to access bank account

• No prohibition on prepayment and no penalty for prepayment in whole or in part

13

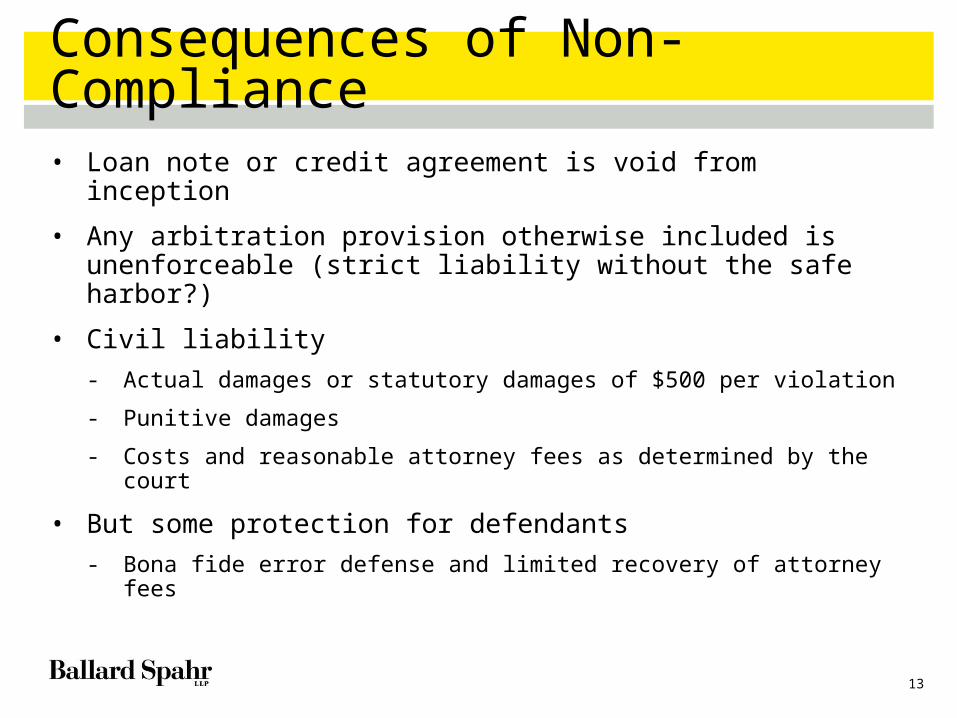

Consequences of Non-Compliance• Loan note or credit agreement is void from inception

• Any arbitration provision otherwise included is unenforceable (strict liability without the safe harbor?)

• Civil liability

- Actual damages or statutory damages of $500 per violation

- Punitive damages

- Costs and reasonable attorney fees as determined by the court

• But some protection for defendants

- Bona fide error defense and limited recovery of attorney fees

14

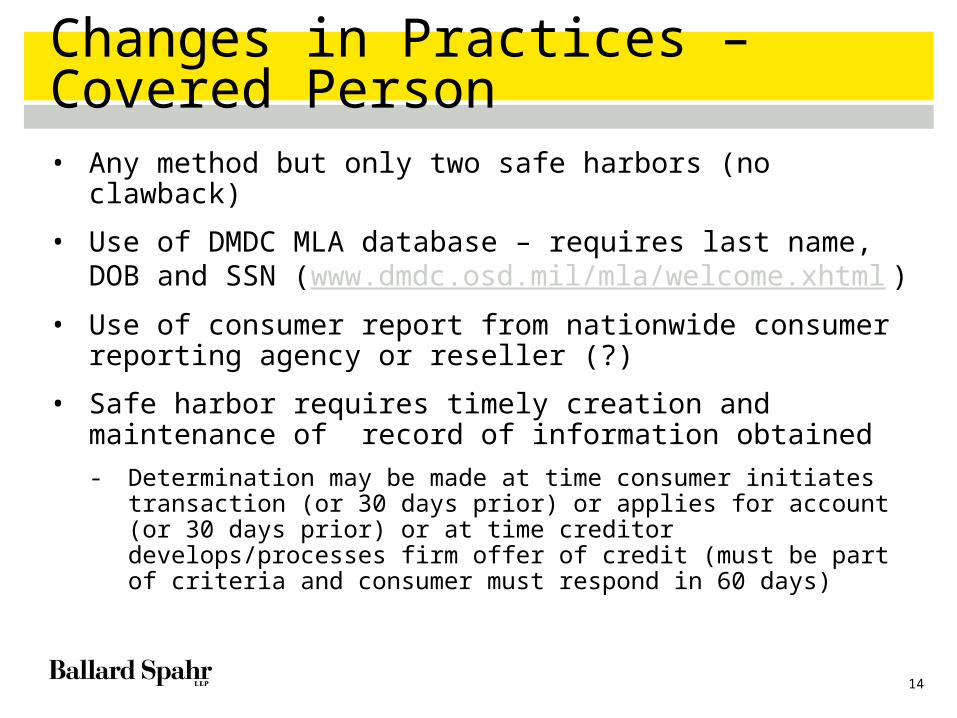

Changes in Practices – Covered Person• Any method but only two safe harbors (no clawback)

• Use of DMDC MLA database – requires last name, DOB and SSN (www.dmdc.osd.mil/mla/welcome.xhtml)

• Use of consumer report from nationwide consumer reporting agency or reseller (?)

• Safe harbor requires timely creation and maintenance of record of information obtained

- Determination may be made at time consumer initiates transaction (or 30 days prior) or applies for account (or 30 days prior) or at time creditor develops/processes firm offer of credit (must be part of criteria and consumer must respond in 60 days)

15

Document Changes – Student Loans• MLA disclosure requirements and limitations apply to

student loans not excluded from Regulation Z

- Includes federal loans not made under Title IV

• Increased attention to all Regulation Z disclosures may be required because of potential for greater liability

- Any error in application disclosure and failure to obtain school certification may give rise to MLA statutory damages

- Any error in approval or final disclosure may give rise to MLA statutory damages, sometimes, in addition to TILA damages

- Some risk that error in application, approval, or final disclosure and failure to obtain school certification may also void loan

16

Document Changes – Student Loans• Regulations say Statement of MAPR (and toll-free phone

number) can be given one time, in credit agreement

- DOD is supportive but will CFPB agree?

- For private education loans, may be prudent to include this in all disclosures, perhaps adjoining Reference Notes

• Dispute resolution provisions and arbitration provisions will need to be reviewed and deleted or amended

• Best practices will include checking status of borrower before attempting to invoke arbitration or dispute resolution provisions (particularly with dependents)

17

Can You Just Say No?

• No affirmative obligation to lend, and no express prohibition on discrimination, in either MLA or in SCRA

- SCRA prohibits discrimination based on exercise of rights

- UDAAP issue under Dodd-Frank?

• Numerous states prohibit discrimination against service members but scope of protection varies greatly from state to state (some are “uniform wearing” only)

• Obvious reputational issues and risk of significant regulatory agency scrutiny

19

Panelist – John L. Culhane, Jr.• Partner at Ballard Spahr and a member of the firm’s Consumer

Financial Services, Mortgage Banking, Bank Regulation and Supervision, and Higher Education Groups as well as its Fair Lending Task Force, Collection Documentation Task Force, and TCPA Task Force

• Compliance practice emphasizes counseling clients on the development and implementation of innovative loan, leasing, and payment programs, and includes counseling on fair lending, servicing and collection issues

• Regulatory practice includes preparing clients for banking agency and CFPB targeted and full spectrum compliance examinations as well as assisting in the defense of consumer class actions, attorney general investigations, and agency enforcement actions

• Charter member of the American College of Consumer Financial Services Lawyers

• Former Chair of the Subcommittee on Fair Lending of the ABA Committee on Consumer Financial Services

20

Resources

CFPB Monitor

Subscribe to our ABA award-winning blog at www.CFPBMonitor.com.

E-Alerts

Subscribe at www.ballardspahr.com (click “subscribe” and indicate your areas of interest)

Mortgage Banking Update

Subscribe at www.ballardspahr.com (click “subscribe” and choose Mortgage Banking as your area of interest)

Questions? E-mail [email protected].

21

Upcoming Webinars

You Received a NORA Notice or PARR letter from the CFPB – Now What?

September 29

The Impact of Gomez on Class Actions – Will Rule 68 Moot Rule 23?

Anti-Money Laundering Programs in the Mortgage Banking Industry

Digital Accessibility – Looking into the Future

October 6

October 14

October 27

Register for upcoming webinars at www.ballardspahr.com or by e-mailing [email protected]. Request materials from past webinars by e-mailing [email protected].

DMEAST #22800577 V1