Embed Size (px)

Citation preview

Industrial Fluid PowerJoao Ramon Capital Markets Day 2004

2

• Business overview• Business overview

Agenda

• Our position

• South America

• Summary

• Markets

3

Fluid Power Products

Fluid Power global market worth $7.3bn – Hose & Connectors $1.8bn

4

Business Overview

• Part of Tomkins Industrial& Automotive division

• Accounts for 10% of Group revenue

• Balanced OE and aftermarket revenues

Hose & Connector Sales(Index: April 2002 = 100)

Operates globally in a market worth $1.8bn

123109

100

Apr 02 Dec 03 Dec 04

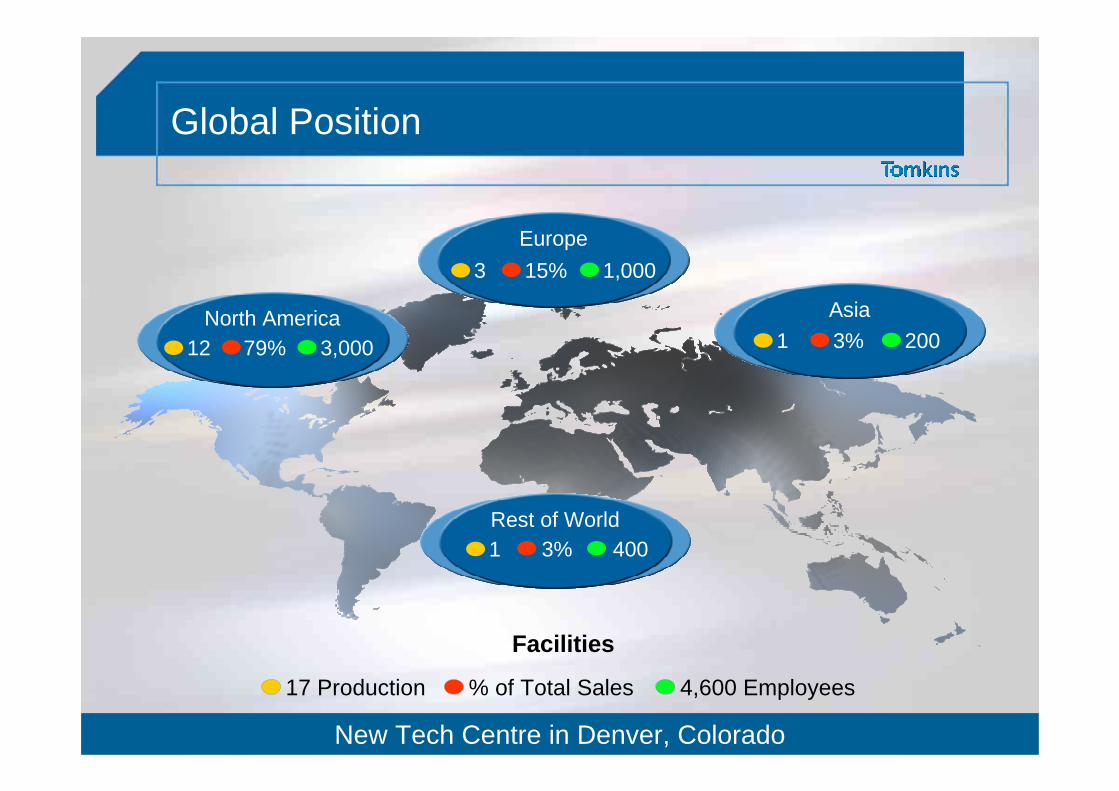

5New Tech Centre in Denver, Colorado

Global Position

Facilities

17 Production % of Total Sales 4,600 Employees

12 79% 3,000North America

3 15% 1,000Europe

1 3% 200Asia

1 3% 400Rest of World

6

• Business overview• Business overview

Agenda

• Our position

• South America

• Summary

• Markets

7

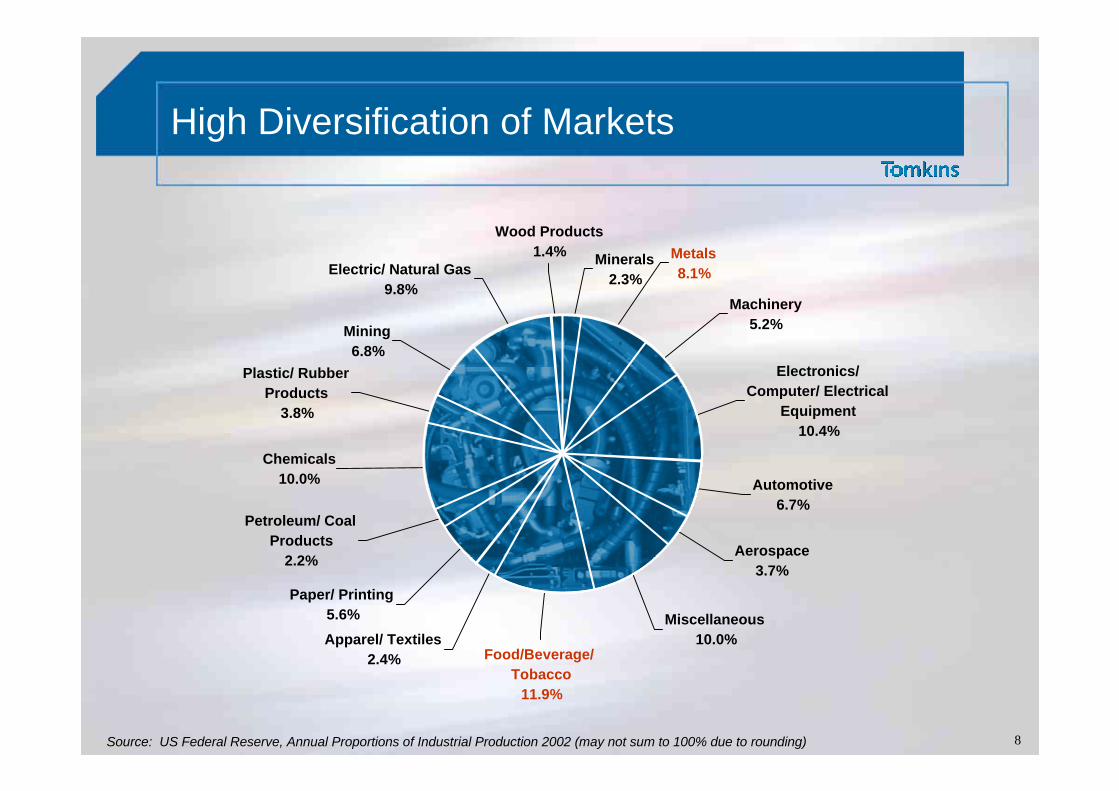

Focused on Industrial Markets

• Highly diversified

• Breadth of end-markets / customers

• Huge potential market

• Expanding globally

Growing at 6% per year

8

High Diversification of Markets

Source: US Federal Reserve, Annual Proportions of Industrial Production 2002 (may not sum to 100% due to rounding)

Wood Products1.4%

Electric/ Natural Gas9.8%

Plastic/ Rubber Products

3.8%

Mining6.8%

Chemicals10.0%

Food/Beverage/Tobacco

11.9%

Apparel/ Textiles2.4%

Paper/ Printing5.6%

Petroleum/ Coal Products

2.2%

Miscellaneous10.0%

Aerospace3.7%

Automotive6.7%

Electronics/ Computer/ Electrical

Equipment10.4%

Machinery5.2%

Metals8.1%

Minerals2.3%

9

Steel Market – Growing 6% Annually

• 1,040m tons / $ 1,200bn

• Replacement H&C - $ 98m

• Our strategy:– Focused equipment mfg– Develop specialized

distributors

Worldwide Steel Production

Source: IISI / ILAFA / IBS

Global Annual Production

Others34%

USA10%Ukraine

4%

Germany5%

South Korea

5%

Russia7%

Japan12%

Brazil3%

China20%

10

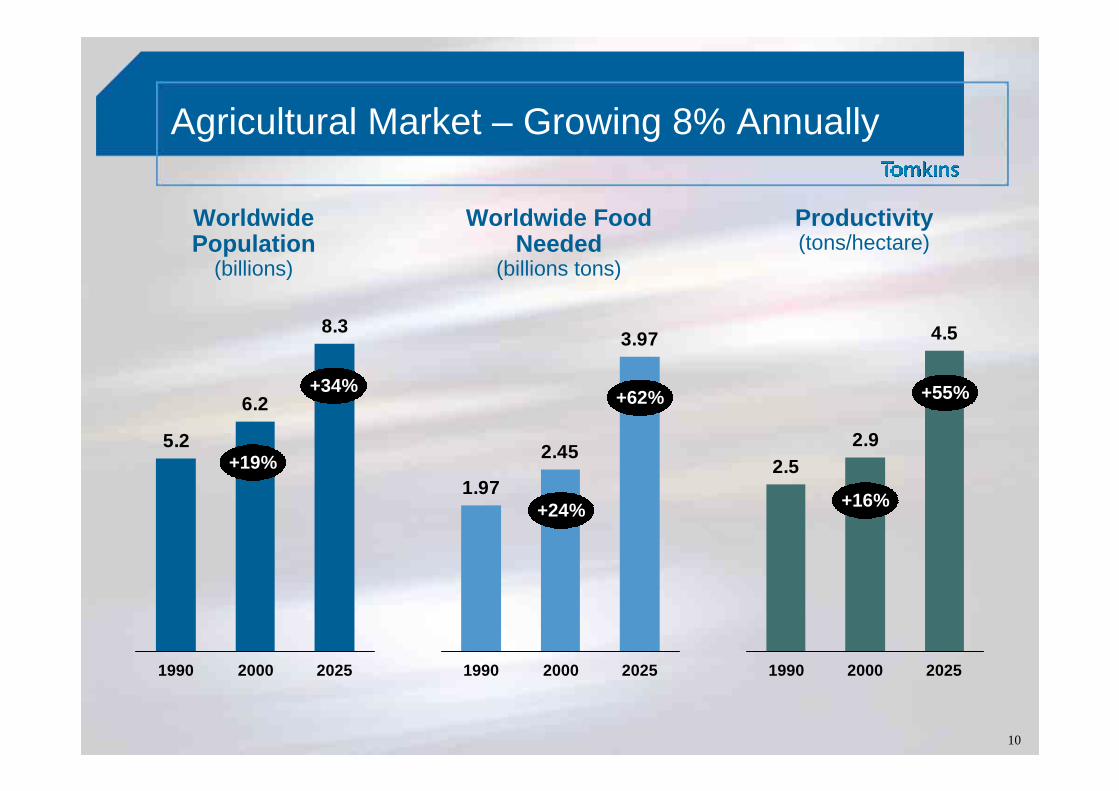

Agricultural Market – Growing 8% Annually

WorldwidePopulation

(billions)

Worldwide FoodNeeded

(billions tons)

Productivity(tons/hectare)

5.2

6.2

8.3

1990 2000 2025

+19%

+34%

1.97

2.45

3.97

1990 2000 2025

+24%

+62%

2.52.9

4.5

1990 2000 2025

+16%

+55%

11

Wheel Tractors – Large Growth Opportunity

• Worldwide OE production: 457,000 units

• Machine content: $ 70

Source: OEM customers / ANFAVEA

• Worldwide fleet (aftermarket):

Hose & Connector Potential $ 32m

Hose & Connector Potential $ 178m

Units (‘000s)

North America 5,820 Europe 11,090Asia 7,280South America 1,290

Total 25,490

12

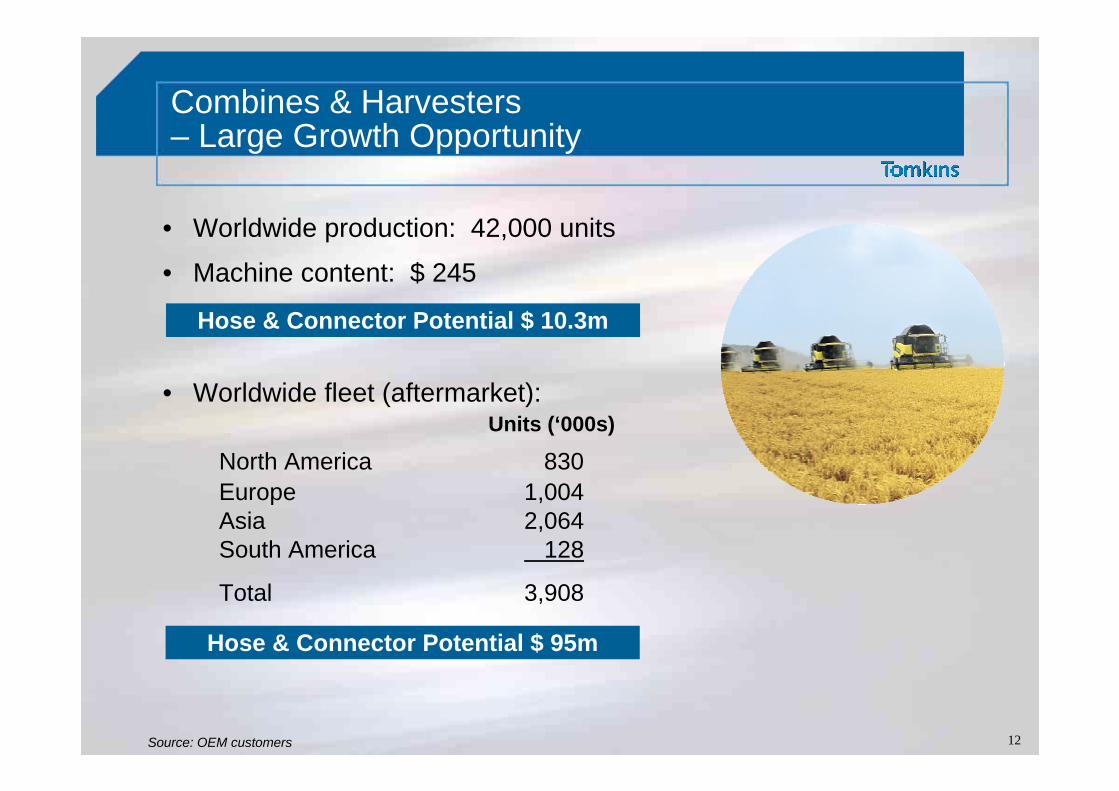

Combines & Harvesters– Large Growth Opportunity

• Worldwide production: 42,000 units

• Machine content: $ 245

Source: OEM customers

• Worldwide fleet (aftermarket):

Hose & Connector Potential $ 10.3m

Hose & Connector Potential $ 95m

Units (‘000s)

North America 830 Europe 1,004Asia 2,064South America 128

Total 3,908

13

• Business overview• Business overview

Agenda

• Our position

• South America

• Summary

• Markets

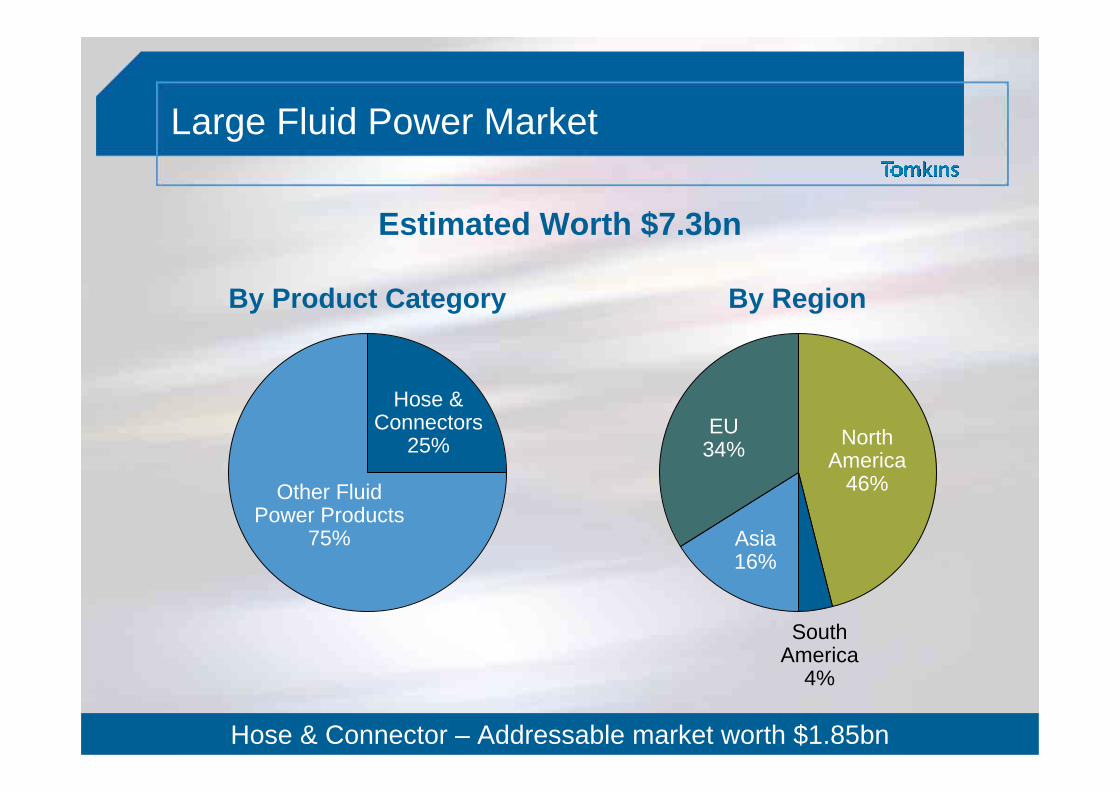

14Hose & Connector – Addressable market worth $1.85bn

Large Fluid Power Market

Estimated Worth $7.3bn

Other FluidPower Products

75%

Hose & Connectors

25%

By Product Category By Region

Asia16%

NorthAmerica

46%

EU 34%

South America

4%

15

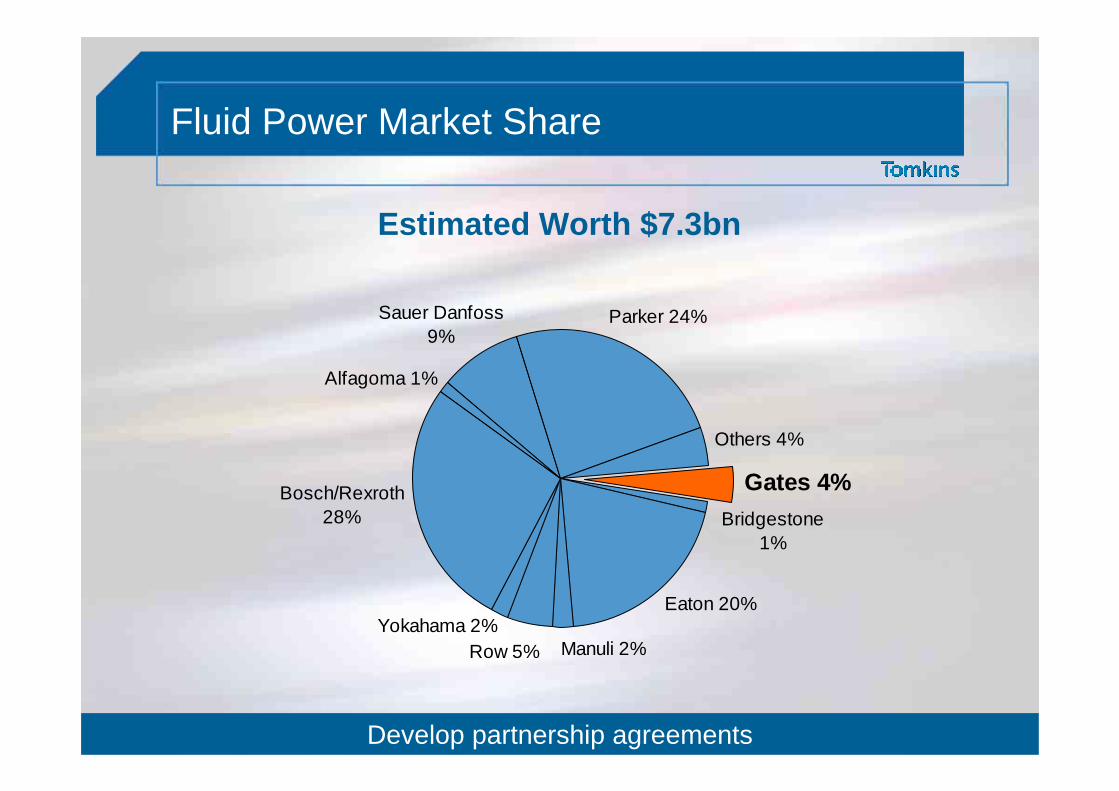

Eaton 20%

Manuli 2%

Gates 4%Bridgestone

1%

Others 4%

Parker 24%Sauer Danfoss 9%

Alfagoma 1%

Row 5%Yokahama 2%

Bosch/Rexroth28%

Fluid Power Market Share

Develop partnership agreements

Estimated Worth $7.3bn

16

Eaton 20%Manuli 6%

Gates 17%

Bridgestone4%

Others 18%

Parker 29%

Alfagomma 6%

Hose & Connector Market Share

Third largest player – acting in all regions

Estimated Worth $1.85bn

17

• Business overview• Business overview

Agenda

• Our position

• South America

• Summary

• Markets

18

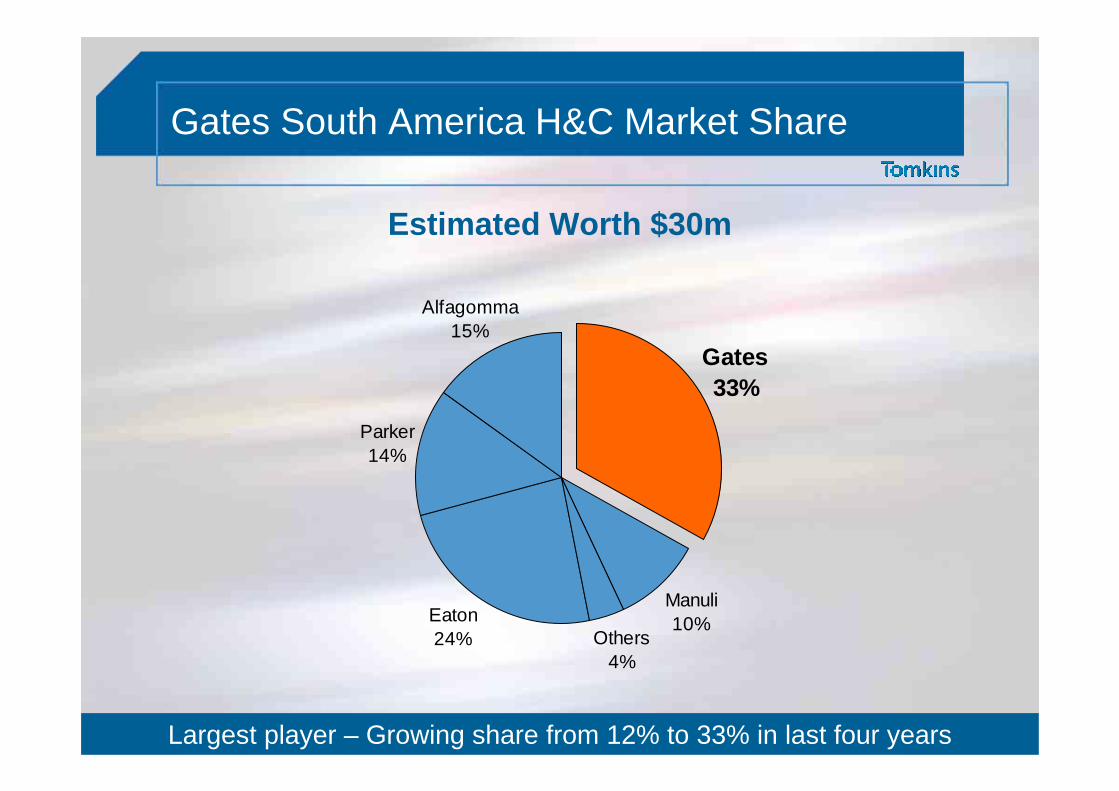

Others4%

Gates33%

Manuli10%

Alfagomma15%

Parker14%

Eaton24%

Gates South America H&C Market Share

Largest player – Growing share from 12% to 33% in last four years

Estimated Worth $30m

19

Brazilian Agricultural Market

• Huge potential

• Massive territory

• Favourable weather– Selected crop harvested

twice per year

• Agricultural production– Y03/04: 119m tons– Y04/05: 128m tons– Growth 7.6%

Austria Romania Holland Lithuania Italy PolandEstonia

Greece

UkraineBosnia

Croatia

Macedonia

Iceland

Serbia/ Montenegro

NorwayFinlandSwitzerlandBelarus

Czechoslovakia

Hungary

France

Ireland

Belgium

Albania

Portugal

Spain Bulgaria

UK

Germany

Denmark

Sweden

Latvia

20

Large, Growing Brazilian Agricultural Markets

SoybeanHarvest

CottonHarvest

Sugar CaneHarvest

Production: 53m tonsGrowth: 6.1%

Note: Production CY04/05 vs. CY03/04

Production: 0.89m tonsGrowth: 5.9%

Production: 390m tonsGrowth: 14.7%

21

Agricultural OEMs – Gates Customers

22

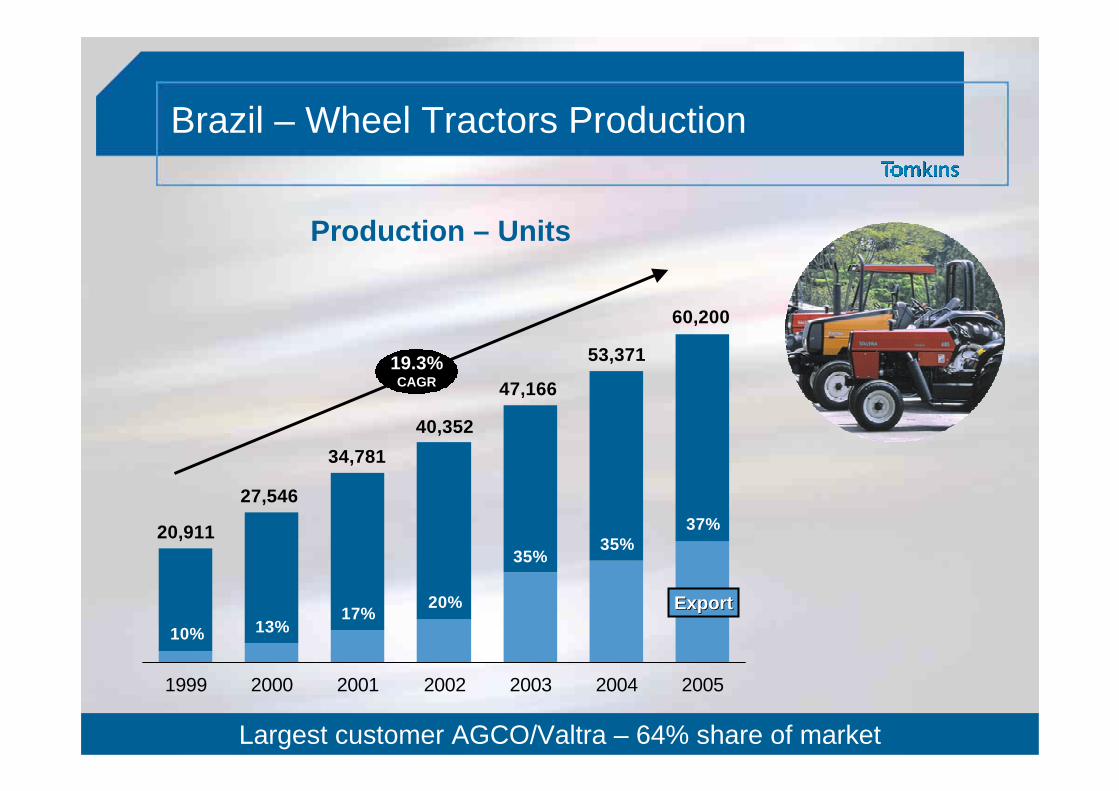

Brazil – Wheel Tractors Production

37%35%

35%

20%17%13%10%

60,200

53,371

47,166

40,35234,781

27,546

20,911

1999 2000 2001 2002 2003 2004 2005

ExportExport

Production – Units

19.3%CAGR

Largest customer AGCO/Valtra – 64% share of market

23

Brazil – Combines Production

42%35%

35%

18%23%16%18%

10,97710,515

9,195

6,851

5,1964,296

3,760

1999 2000 2001 2002 2003 2004 2005

ExportExport

Production – Units

19.5%CAGR

Largest customer John Deere – 40% share of market

24

John Deere

• 2003 sales of $13.3bn worldwide and $0.7bn in Brazil

• Investing $250m in new Brazilian wheel tractor plant

93%$2.0mBelts78%$2.6mHose & Connector

ShareSales

25

Case New Holland

• 2003 sales of $8.7bn worldwide and $1.0bn in Brazil

• The biggest agriculture equipment manufacturer in Brazil

94%$2.9mBelts18%$1.3mHose & Connector

ShareSales

26

AGCO (Massey Ferguson)

• 2003 sales of $3.5bn worldwide and $0.6bn in Brazil

• Transferred combine product development to Brazil

73%$1.5mBelts12%$0.3mHose & Connector

ShareSales

27

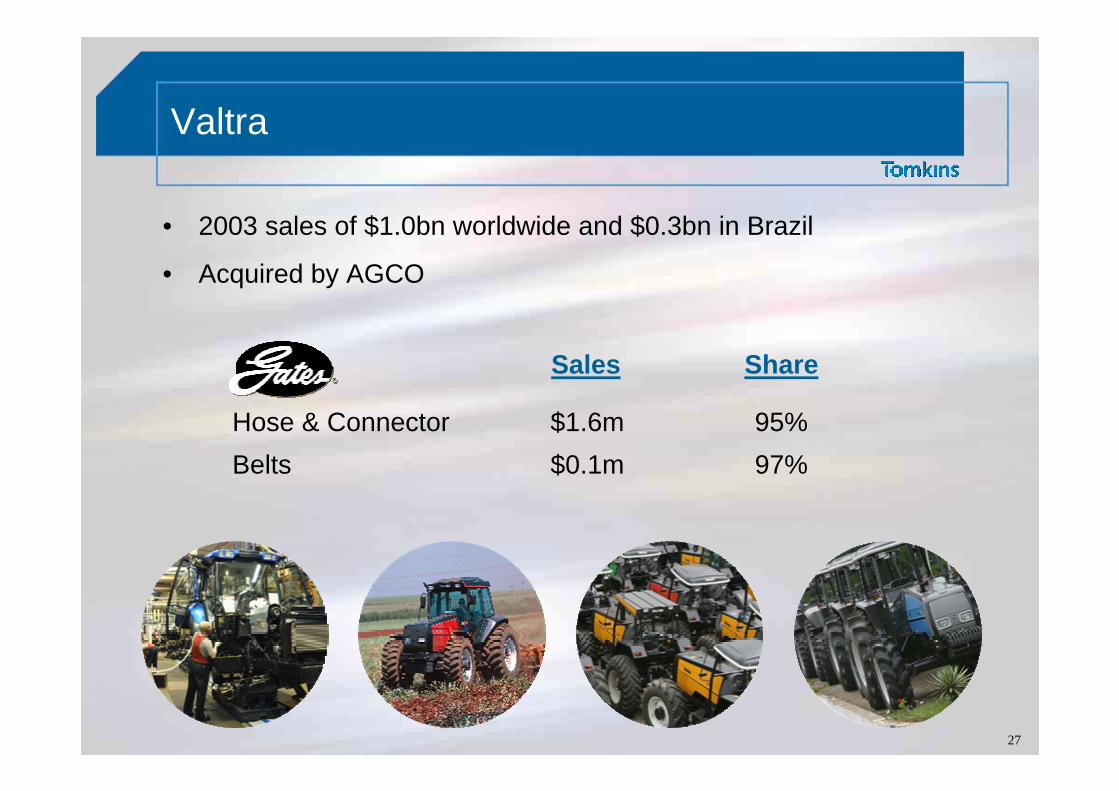

Valtra

• 2003 sales of $1.0bn worldwide and $0.3bn in Brazil

• Acquired by AGCO

97%$0.1mBelts95%$1.6mHose & Connector

ShareSales

28

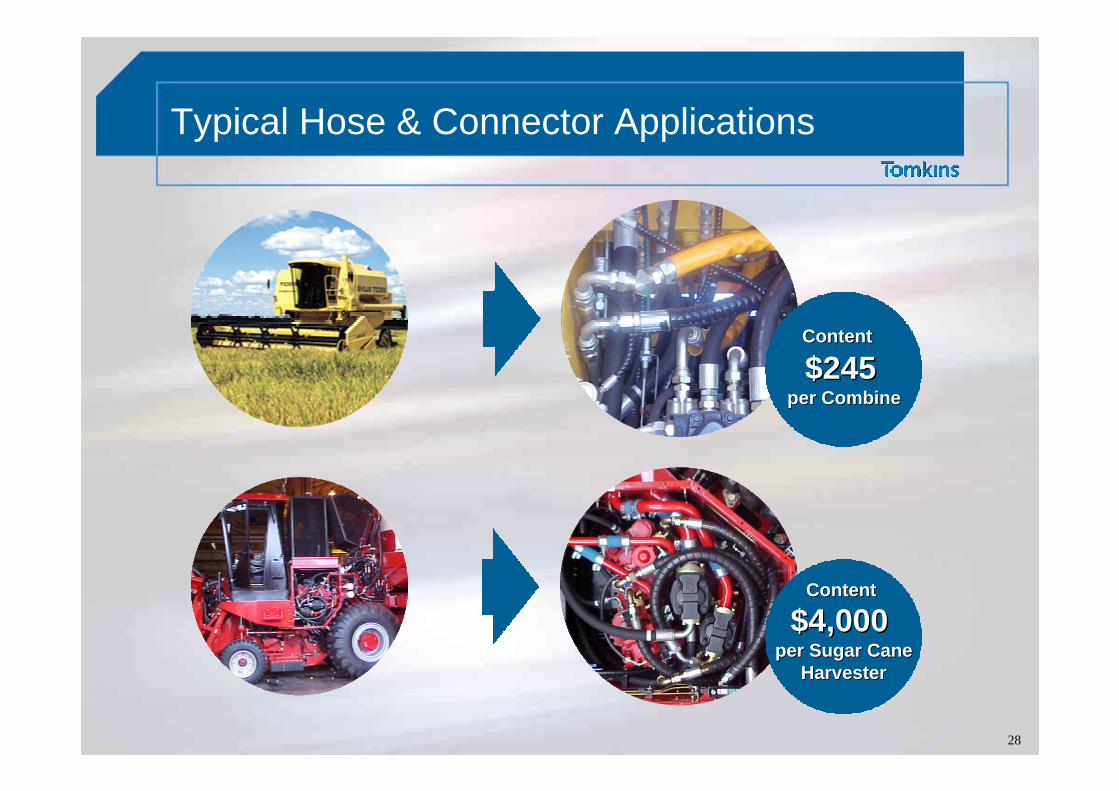

Typical Hose & Connector Applications

ContentContent

$245$245per Combineper Combine

Content Content

$4,000 $4,000 per Sugar Caneper Sugar Cane

HarvesterHarvester

29

Hydraulic Assemblies – Market Trends

TraditionalAssemblies

Gates InnovationKit Assemblies

Gates CreativitySub-Systems

$42 $47 $238

Five times value increase

30

Sub-Systems: Expand Content Five-Fold

John DeereWheel Tractor MR TOP

Creativity increasing machine content & business potential

BUSINESS POTENTIALTractors over 100hp

Actual Future

Machine content $47 $238

Brazil $1.3m $6.4m

Global $11m $56m

31

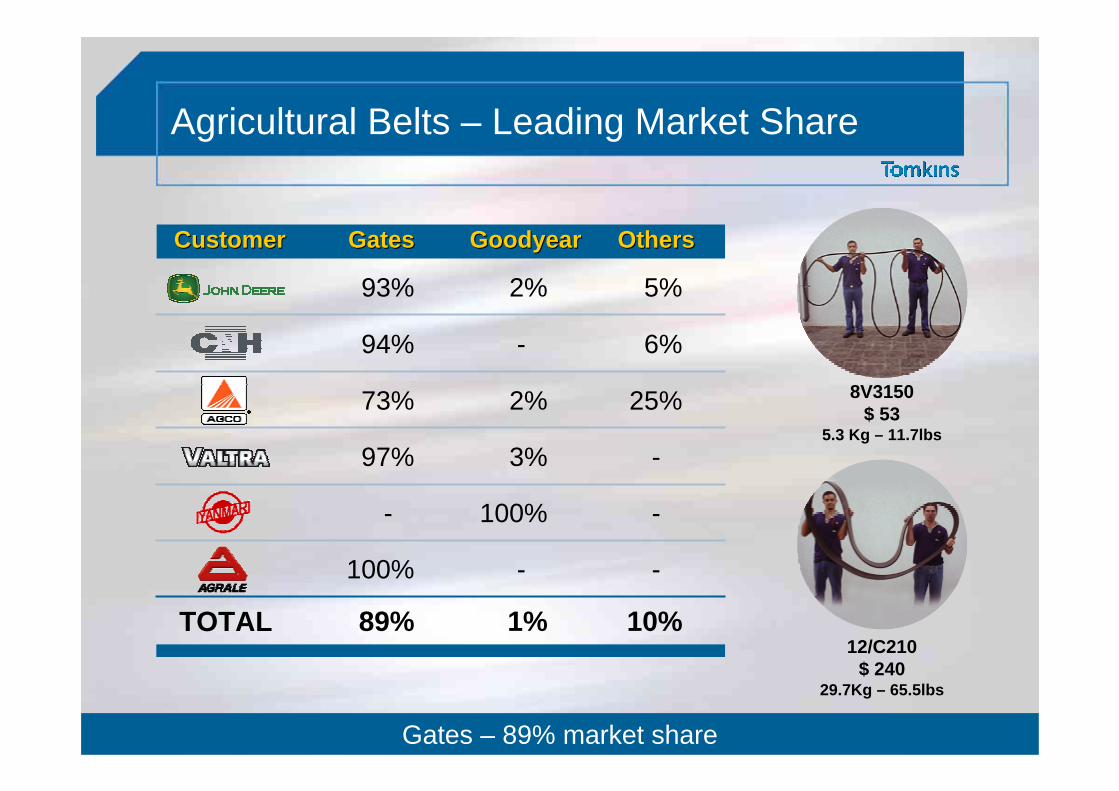

TOTAL

OthersOthersGoodyearGoodyearGates Gates CustomerCustomer

Agricultural Belts – Leading Market Share

10%

-

-

-

25%

6%

5%

1%

-

100%

3%

2%

-

2%

89%

100%

-

97%

73%

94%

93%

Gates – 89% market share

12/C210$ 240

29.7Kg – 65.5lbs

8V3150$ 53

5.3 Kg – 11.7lbs

32

• Business overview• Business overview

Agenda

• Our position

• South America

• Summary

• Markets

33

Gates: South America Strategy

Focus, execution, speed and people to drive growth and profit

Value Creation

Business Intelligence

Product Innovation

Market Leader

ManufacturingExcellence

Admired CompanyReputation

34

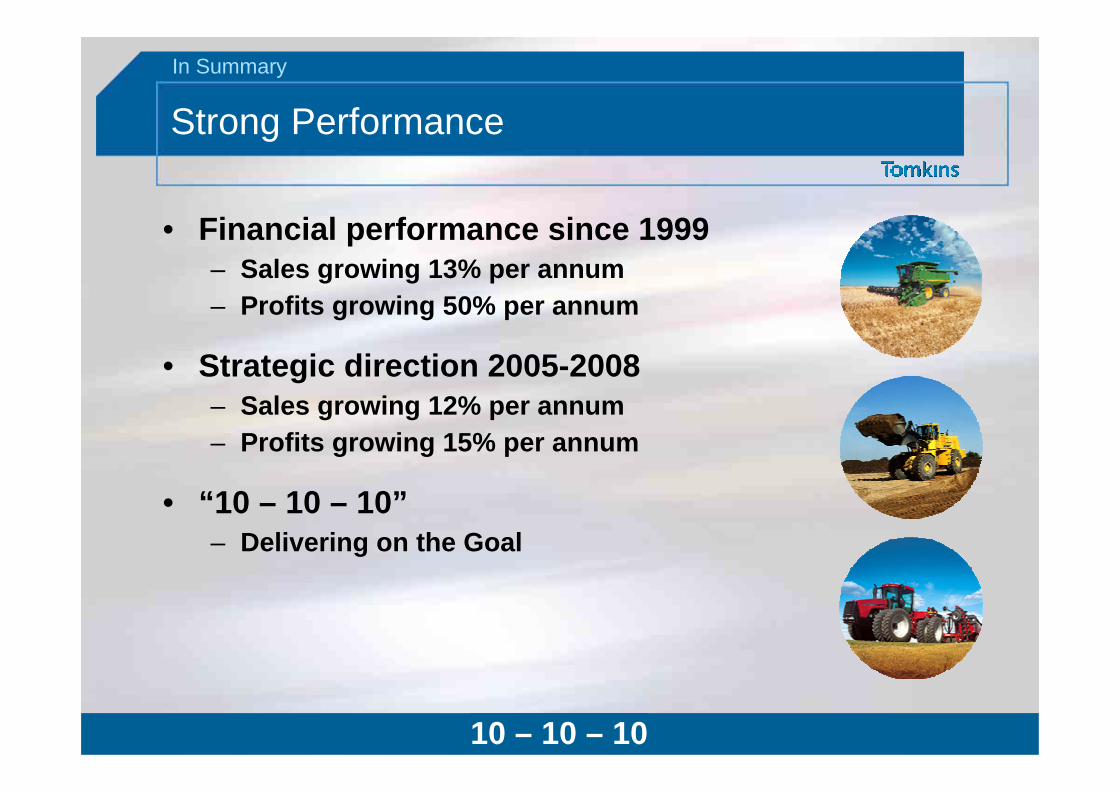

Strong Performance

• Financial performance since 1999– Sales growing 13% per annum– Profits growing 50% per annum

• Strategic direction 2005-2008– Sales growing 12% per annum– Profits growing 15% per annum

• “10 – 10 – 10”– Delivering on the Goal

In Summary

10 – 10 – 10

Industrial Fluid PowerJoao Ramon Capital Markets Day 2004