Embed Size (px)

Citation preview

CIRCULATING COPYJgm L E 3 P .Y TO BE RETURNED TO REPORTS DESK

DOCUMENT OF INTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

Report No. P-1353a-BD

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

EXECUTIVE DIRECTORS

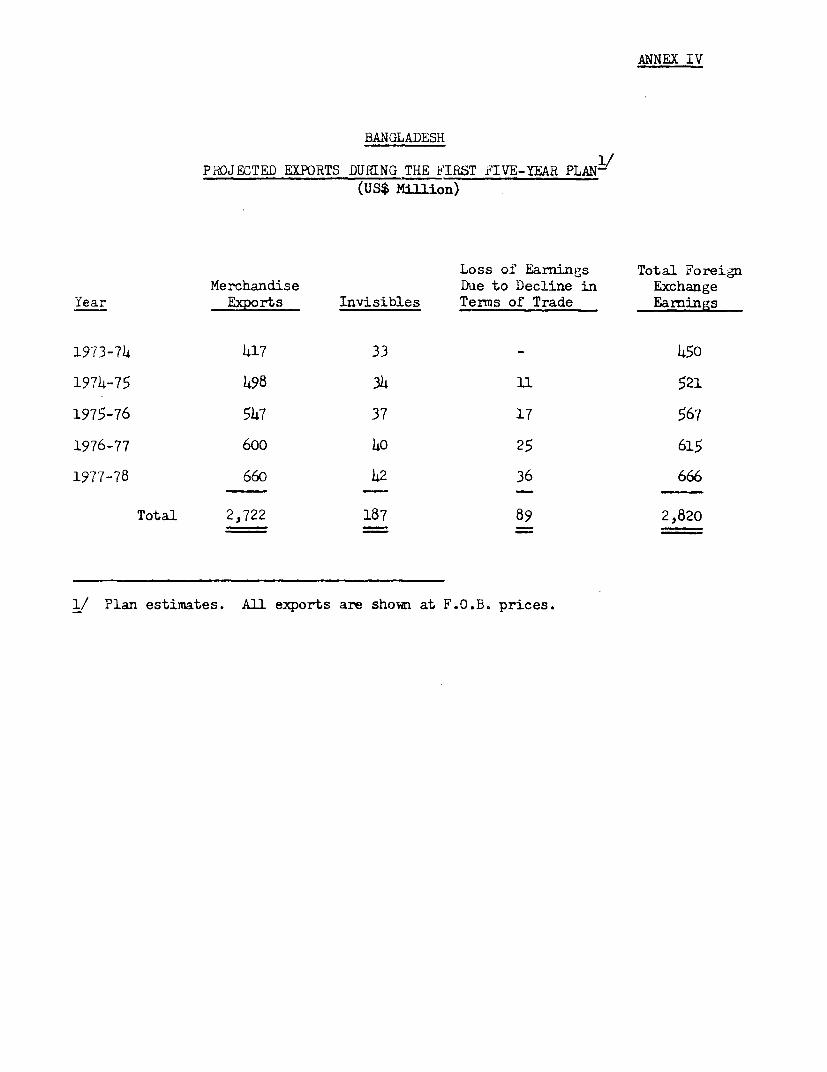

ON A

PROPOSED CREDIT

TO

THE PEOPLE'S REPUBLIC OF BANGLADESH

FOR AN

IMPORTS PROGRAM

January 15, 1974

This report was prepared for official use only by the Bank Group. It may not be published,quoted or cited without Bank Group authorization. The Bank Group does not acceptresponsibility for the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

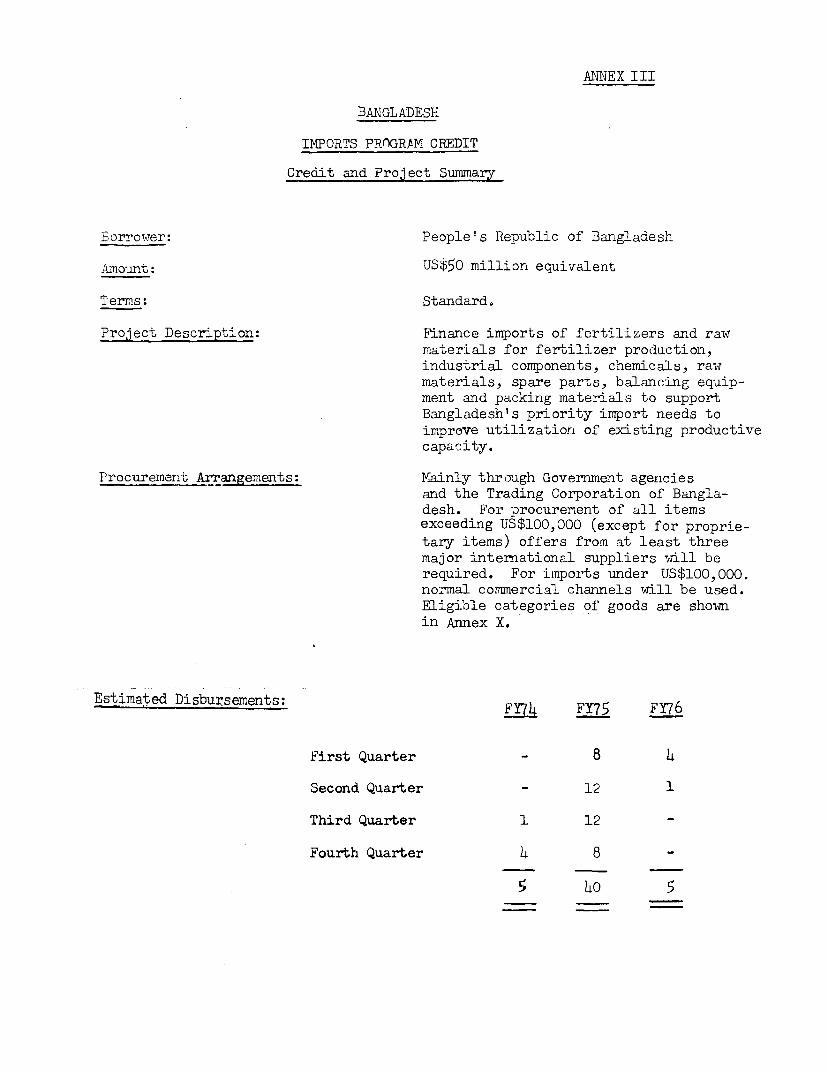

rized

Pub

lic D

iscl

osur

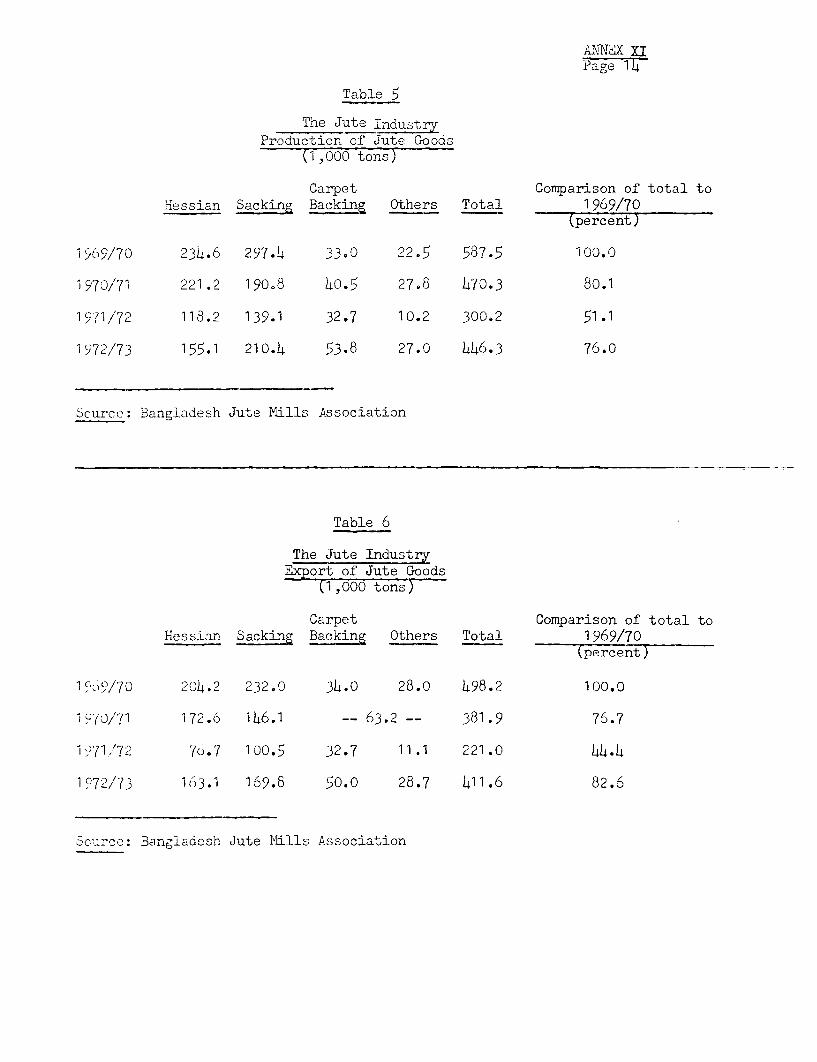

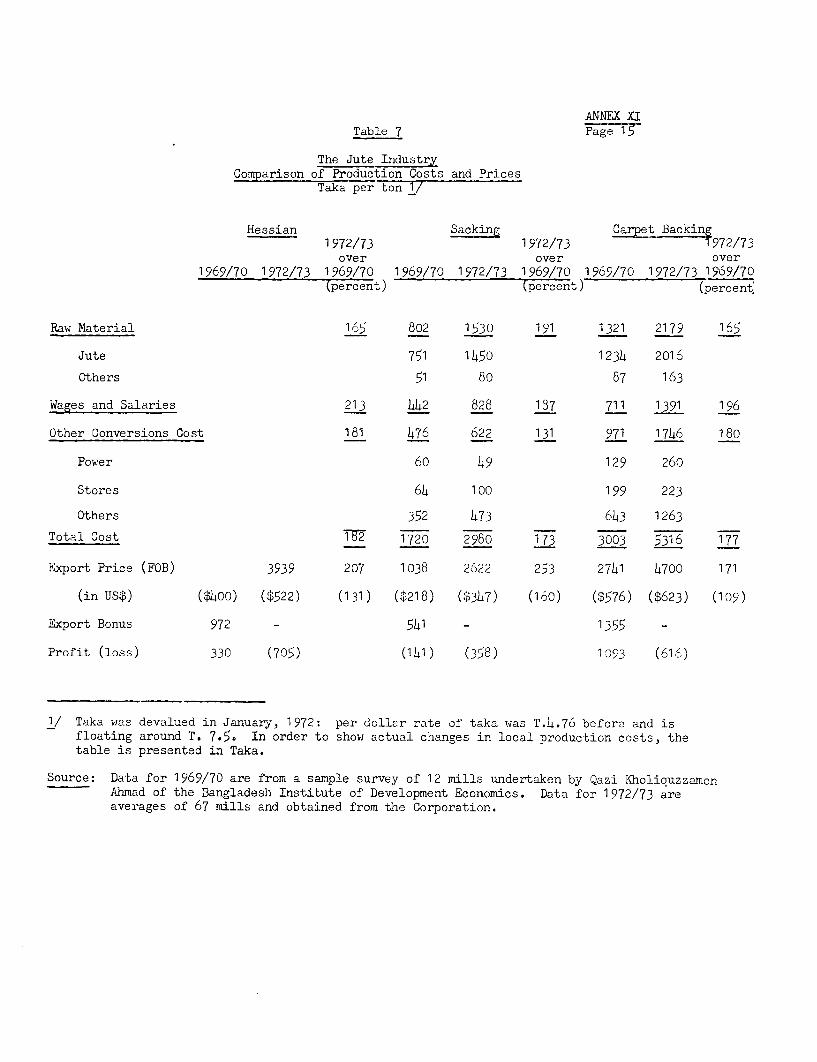

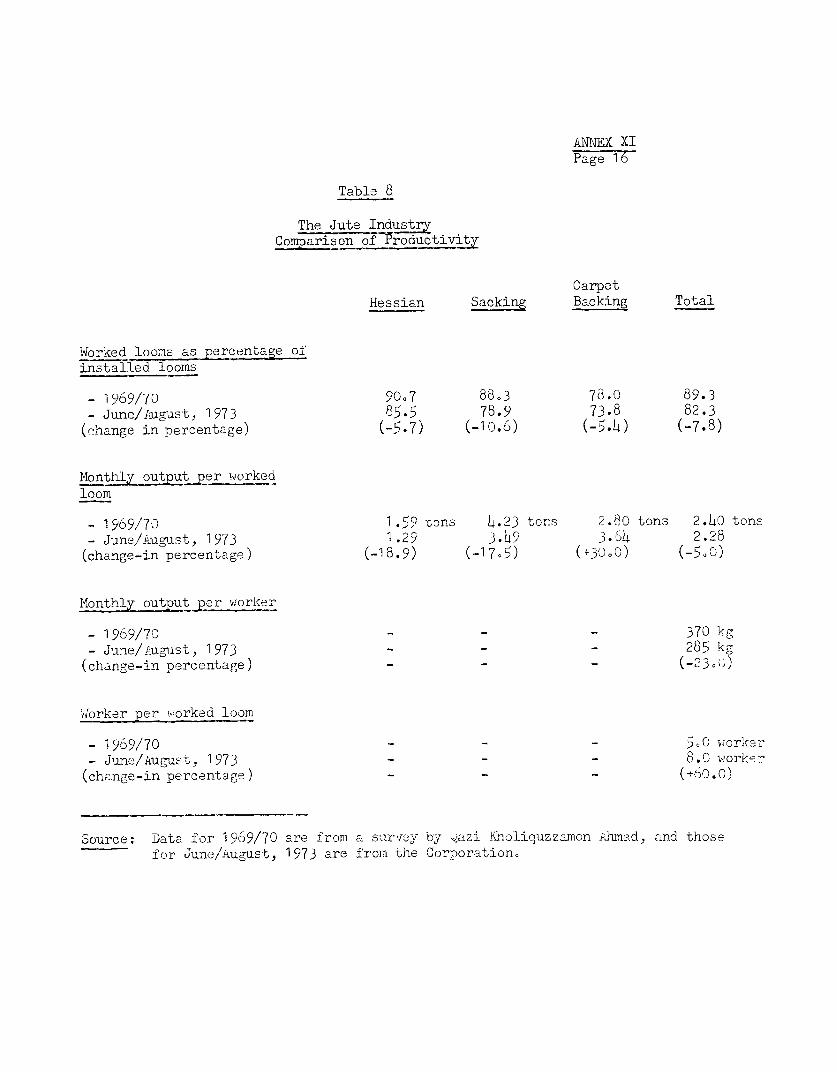

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSkas at December 28, 19i3)

Currency Unit: Taka (Tk)

US$ = Tks. 8.2 /aTk 1 = US$0.122Tks 1,uO = US$122iks 1,000,000 = US$122,000

/a The Taka is officially valued at 18.9677to the Pound Sterling. The Pound is nowfloating relative to the US dollar; con-sequently the Taka - US dollar exchangerate is subject to change. Unless otherwisestated, all currency conversions in thisreport have been made at the exchange rateprevailing at the time of appraisal inSeptember/October 1973, i.e. at Tks 7.55to US$1.

FISCAL YEAR

July 1 - June 30

GLOSSARY OF ABBREVIATIONS

BSIC - Bangladesh Small Industries CorporationCCIE - Chief Controller of Imports and ExportsMP - Muriate of PotashTCB - Trading Corporation of BangladeshTSP - Triple Super Phosphate

INTERNATIONAL DEVELOPMENT ASSOCIATION

RFPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON A PROPOSED CREDIT

TO THIE PEOPLE'S REPUBLIC OF BANGLADESH FOR ANIMPORTS PROGRAiM

1. I submit the following report and recommendation on a proposeddevelopment credit to the People's Republic of Bangladesh for the equivalentof US$50 million on standard IDA terms, to help finance the foreign exchangecosts of an imports nrogram to sustain agricultural production and to pro-mote industrial production through higher utilization of existing capacity.

PART I - THE ECONOMY

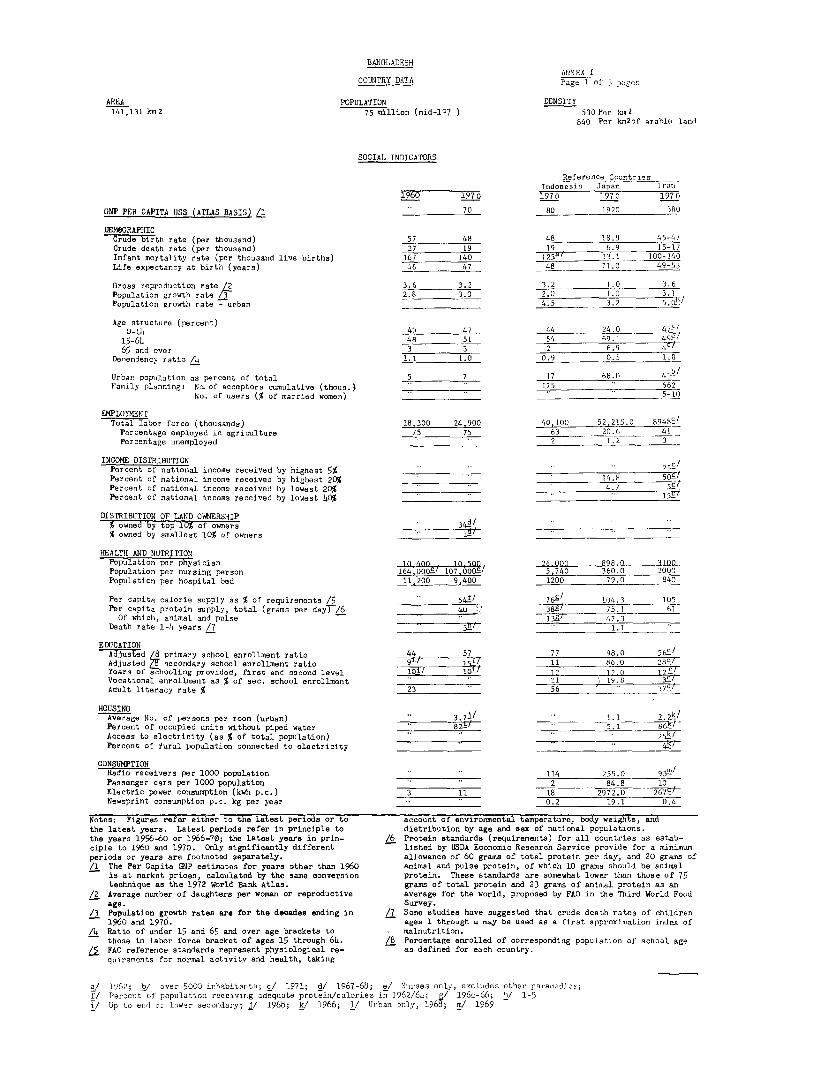

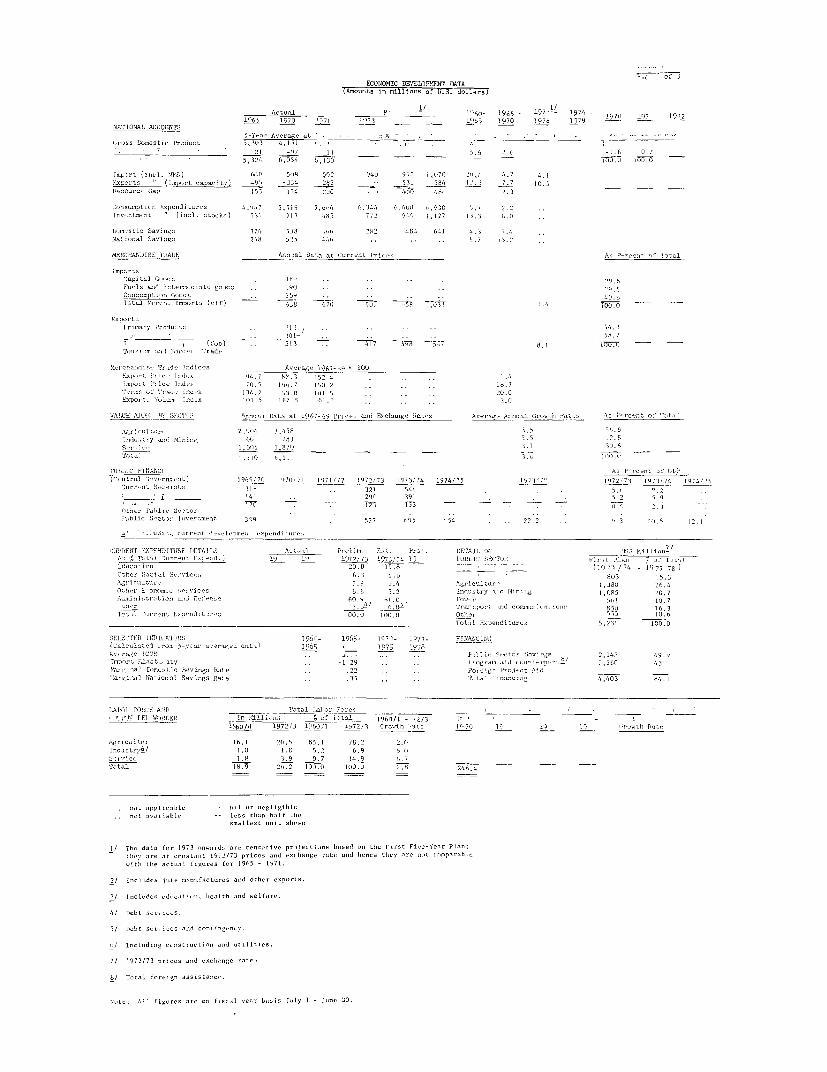

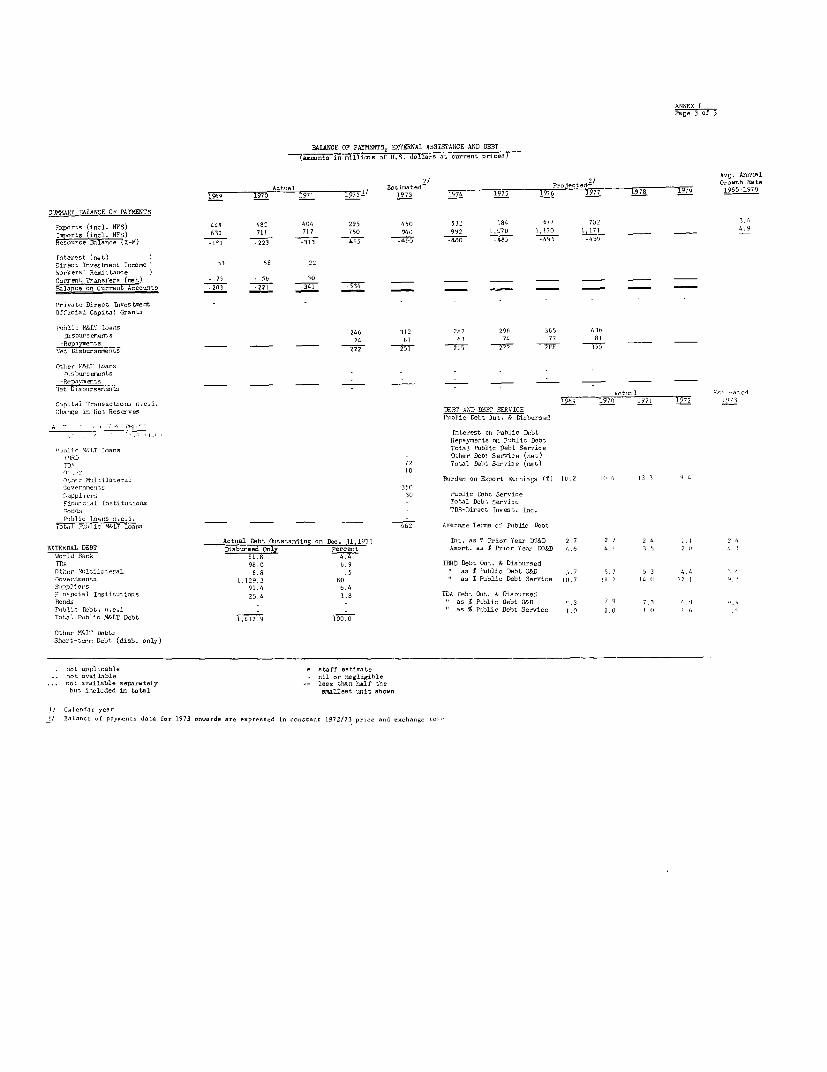

2. A report entitled "Reconstructing the Economv of Bangladesh"(R72-230) was distributed to the Executive Directors on October 13, 1Q72.A Basic Economic Mission was in the field during September/October 1973,and its report is being prepared. A country data sheet is attached asAnnex I.

Background

3. The inhabitants of Bangladesh are poor, per capita income beingonly about IJSS70. They have little opportunity to generate savings. Popu-lation is growing at about 3 percent per annum, and the immediate needs ofthe people are so great that current commitments at least to prevent percapita GDP from falling form the major focus of economic management. Thismakes it difficult to give attention to coherent longer-term programs.The country is very densely populated (1,400 per square mile), lacksnatural resources, and is consequently heavily dependent on imports. Allof these factors combine to make decisions about resource allocationexceptionally complex.

4. Independence on December 16, 1971 brought rising expectations tothe average Bengali. But the task of improving his lot had clearly beenmade much more difficult by the destruction which had taken nlace over theprevious two years, first as a result of the cyclone of late 1970 and thenfrom the political upheavals of 1971 which resulted in war and finallyindependence. The first two years during which the Government of Bangladeshhas been in control of the country have been dominated by an emergencysituation in which law and order had to be re-established, political stabilityachieved, and the administrative framework reconstituted. The millions ofrefugees who had migrated temporarily to India had to be resettled andprovided with relief. The transport system needed to be reconstructed topermit the distribution of food and other supplies.

5. Most of these urgent tasks of reconstruction were tackled speedily,although viable long-term solutions to the problems of the Bangladesheconomy are still proving elusive. The Government was aided in its efforts

-2-

in part by massive assistance initially from India and subsequently froma number of other countries and private international agencies, mostlyunder the auspices of the United Nations. United Nations relief operationshave been terminated as of December 31, 1973, after two years in which overUS$1.3 billion were disbursed, largely for emergency relief. The vital portof Chittagong was restored to 90 percent of its prewar capacity by the endof June 1972. Roads were quickly, if temporarily, repaired, and ferrieswere brought in to substitute for damaged bridges. The vital Bhairabbridge which links Chittagong to Dacca by rail was fully repaired inSentember 1973.

6. Among the principal achievements of the Government since in-dependence has been the establishment of a parliamentary democracy whichhas given the people a measure of political particination which thev felthad hitherto been denied to them. Some progress has been made towardsrestoration of law and order to the cotntryside - sufficient at leastto have permitted the first parliamentary elections to be held in March1073.

7. But these achievements nall in the face of significant anddisturbing prohlems which remain to be solved before Bangladesh can besaid to be launched on a path of stable economic development. Externalassistance has tapered off to a level below that of the initial infusionsof aid. Meanwhile the economy is empty and Government administration isfragile. Some staple consumer items are disappearing from the marketand inflationary pressures are a serious problem.

Food and Other Production

8. The gravest problem confronting the Government since independencehas been the food situation. The 1970/71 crops were poor and the crop of

December 1971 was disrupted by thle war. Record levels of food importsof about 2.5 million tons in 1972 prevented the widely feared famine fromoccuring. Nevertheless, per capita foodgrain availabilities in 1972were well below 1969/70 levels and this combined with internal transport

difficulties, widespread hoarding, and smuggling of foodgrains to India,led to a 50 percent rise in prices over the year. By October 1972 it wasapparent that the monsoon had again been poor, and the main rice crop was20 percent lower than normal. Ranid increases in population and the needto build up depleted stocks added to the crisis, and imports of approx-

imatelv 2.4 million tons of foodgrains were again necessary in 1973.

Assistance in financing, procuring, transporting and distributing these

massive imports was the United Nations' most conspicuous achievement, andalso an achievement for the Government, which has gradually taken over

this task.

9. The nresent position is still uncertain. Observers' estimatesdiffer, but there is a strong possibilitv that, due mainly to rather

favorable weather conditions, the main (aman) 1973/74 rice crop will prove

- 3 -

to be 7-S million tons and if so production for 1973/74 could well be a

record 12-13 million tons. Much now depends on the ability of the Government

to implement its announced policy of procuring large quantities of foodgrains

in the local market in surplus areas for distribution through ration shops to

low and fixed income groups. Failure to do so could have serious implications

for the level of imports of other commodities. In the absence of Government

T?rocurement, hoarding and smuggling wqill reduce the total amouints available

to the economy. Even on "optimistic" assumptions - no increase in the con-

sumPtion level or in stocks, both of which are already too low; a good harvest;

no repayment of borrowed grains - the Government will have to imDort at least

about 1 million tons for calendar 1974. The stark reality is that even with

improv,ed crop production, Bangladesh will continue to reqtuire substantia].

foodgrain imports for a number of years.

10. Elsewhere in the economy, non-agricultural sectors have been

slow to rtcover. Industrial activity came to a virtual standstill from

November 1971 to January 1972. Industrial Droduction recovered to some

degree fairly rapidly in 1972 and 1973, but 1969/70 ]evels of output

have not yet been achieved consistently (with considerable variation

among inditstv-ies). The difficulties impeding a return to full production

arise from thti lack of raw materials, spare parts, components and other

material inpuits, the lack of repair and maintenance, the inability to

replace certain' key items of machinery and equipment lost during the

disturbances, aiid power failures. These latter have resulted more

from inadequate transmission and distribution facilities, or from problems

in transporting fuel, than from lack of generating capacity. Transport

is also a bottleneck; there are still fewer trucks and buses than were

available before the war. With stocks extremelv low or non-existent,

any one of these factors can cause an enterprise to come to a complete

standstill. The productivity and profitability of industrial enterprises

are generally low wnd their financial position precarious, making their

full r-ecoverv more difficult to achieve. In addition, there are significant

pockeirs of labor unrest. The resulting low levels of output have been

a major factor in contributing towards the high levels of inflation. In

major cities the cost of living increased by 60 percent in the year ending in

June 1973.

Trade

11. Total exports in fiscal year 1972/73 are estimated at about

US.q370 million, which compares with about US$500 million exported to

Pakistan and other countries in the prewar period. Much of this decline

is on items such as tea, matches and spices, which were formerly exported

to Pakistan. In view of the uncertain prospects for the international

prices of jute and jute goods, the 1973/74 export target of about T!SS450

million (Annex IV) will be difficult to achieve. A subsidy of 30 nercent

has been given to 79 non-jute exports since the beginning of FY1973/74,

but this is unlikely to contribute much to export earnings in the short

run becauise of sutbstantial increases in the costs of production since

indenendence, the industrial difficulties noted above, and the fact that

- 4 -

non-jute exports now represent only about 10 percent of the total value

of exports.

12. One of the major factors impeding the growth of production (and

exports), and another major cause of the rapid increase in the general

level of prices, has been the lack of imports. Non-food imports in

1972/73 were well below the 1969/70 level. In part, this is due to

failures in the administrative arrangements for the procurement of

imports, including those provided under foreign aid. The increases in

the international prices of major imported commodities such as foodgrairis,

cotton and cement have also contributed significantly to the problems

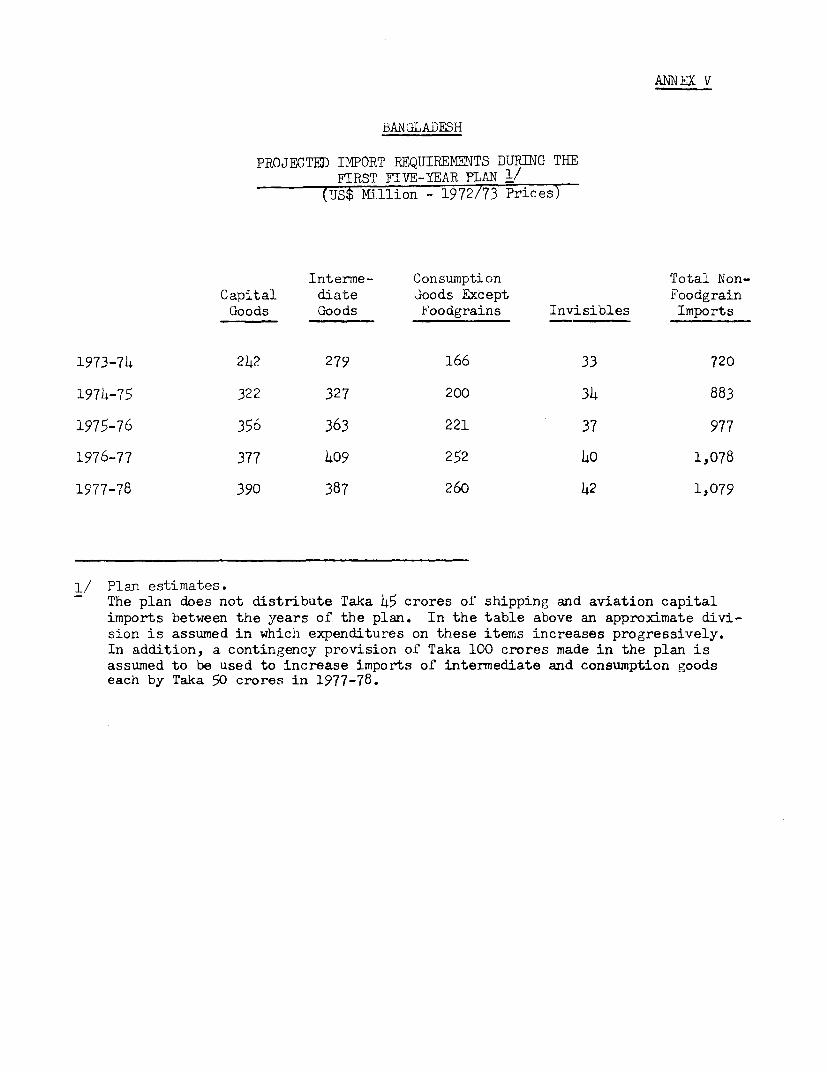

of import planning and procurement. For 1973/74, the non-food import

targets of about US$720 million (Annex V) can be achieved only if the

efficiencv of the licensing and the importing systems is improved to a

significant degree, and only if funds do not have to be diverted to

increased food imports as a result of the failure of local procurement.

Further, it is important to note that the planned target for non-food

imports alloxws for no buildup of stocks, which is a crucial factor in

the production process.

The Annual Plans of 1972/73 and 1973/74

13. In July 1972 the first budget and Annual Plan (for 1972/73)

were presented; they proposed some US$430 million of public development

expenditure and a further US$160 million for reconstruction. About half

of the development expenditure was for agriculture, rural institutions,

and water and flood control. The revised estimates for the 1972/73

Annual Plan show a 20 percent shortfall in development expenditure.

Considering the price rises during the year, the shortfall in real terms

was far higher. The need to provide substantial subsidies for public sector

enterprises led to larger than budgeted deficit financing through net credit

to the public sector. The money supply expanded by 82 percent between

January and December 1972. This combined with commoditv shortages to cause

serious price problems; because of their political implications these loom

large in the short-term economic concerns of the Government.

14. The budget and Annual Plan for 1973/74, which appeared in July

1973, show an increase in projected development expenditure of 30 per-

cent over the revised estimates for 1972/73. The priority given to

agriculture remains unchanged. The volume of aid disbursements is

estimated to be at the same level as in 1972/73 and the Plan thus places

heavy reliance on mobilizing domestic resources. Given the shortfall

on this account which took place in 1972/73, the achievement of these targets

would require improved performance both on the fiscal and project im-

plementation sides.

The First Five-Year Plan

15. The First Five-Year Plan, covering the period 1973/74 -

1l77/78, was approved by the cabinet in earlv November 1973. The Plan

aims at increasing GDP at an average annual rate of 5.5 percent in real

- 5 -

terms, and its primary strategies are to reduce dependence on imnorts

of foodgrains and to imDrove the balance of payments by imnort substitu-

tion and export promotion. Apart from self-sufficiency in foodgrains,

the Plan expects major import substitution to come from new industries,

notably fertilizer and synthetic fibers to be based on indigenous

natural gas. To achieve these targets, the Plan calls for financial

development outlay of US$5.9 billion, about US$5.3 billion of which is

allocated to the public sector. Agriculture and water resources would

receive the highest priority with a projected outlay of about 23 nercent

of total development expenditure.

16. The Plan places heavy reliance on mobilizing domestic resources.

It calls for savings generated in the public sector of about 41 percent

of public sector development spending, with foreign aid making un approx-

imately a further 43 percent. On the evidence of 1972/73, however, the

Plan targets for domestic resource mobilization now appear out of reach

in real terms, given current depressed income levels.

External Assistan e to Bangladesh

17. The preceding analysis makes it evident that Bangladesh will

reauire large and continuing external assistance on very favorable terms

for some vears, if it is to achieve an acceptable growth rate. Long-

term projections suggest that, even to maintain present per capita

income levels in the face of continued population growth, net aid dis-

bursements of between US$100 million and US$200 million per annum would

be required. Average net aid disbursements of IJSS500 million per year

over the Five-Year Plan period would be required to nermit imports

to be maintained at a level of US$0.9 to 1.0 billion and the rate of

investment at the 12-15 percent of GDP level which is needed for a 5

percent per annum growth of GDP. Net aid disbursement levels of about

US$300 million would permit imports of only about U!S$700 million which,

given a higher foodgrain component and substantiallv higher world

commodity prices, would allow for no more investment goods and raw

materials than were imported in 1969/70 into the area that became

Bangladesli.

18. Sustained growth of 5 percent per annum would produce only a

2 percent growth in per capita GDP; at this rate another two decades

would be needed before GDP per capita would pass USS100. The prospects

for achieving the required minimum import level for 1973/74, about

US$900 million including foodgrain imports, are not bright. As stated in

paragraph 11 above, the export target of US$450 million is optimistic.

Planned financing of the gap, another US$450 million, is as follows:

bilateral project aid, US$200 million; bilateral food and commodity aid,

US$150 million; IDA project aid, US$40 million; and IDA program credits

(the Reconstruction Imports Credit and the proposed Imports Progran Credit)

US$60 million.

19. The emergency phase of foreign assistance in Bangladesh has

come to an end with the termination of the United Nations relief opera-

tions. There are no large amounts of undisbursed funds left in the UN

coordinated rehabilitation program. Total aid commitments to date,

which were about US$1.4 billion as of October 1973, have been ample

and on generous terms (with suppliers' credits forming only a small

part of overall aid inflows), and indications are that the dollar amounts

of these commitments will remain at about the same annual level, about

US$450 million through FY75. Disbursements, however, are likely to be

limited by the capacity to procure and import efficiently, by world

supply shortages of some basic commodities, and by the lack of a suf-

ficient number of wmell prepared projects.

20. Bilateral programs of assistance during the immediate Post-

independence period have been flexible and oriented towards quick-

disbursing commodity and program lending both to relieve the critical

food situation and to respond to the country's immediate import needs.

All of the bilateral agencies, however, now wish to redirect their

operations program towards development projects, especially in agricul-

ture and rural develonment. 1Jowever, it is by no means certain that

project lending will be a major feature of external assistance to Bangladesh

over the next 12 months. Virtually all donors to Bangladesh have commit-

ted non-food commodity credits for 1973/74, though a good deal of this

aid is tied to designated sources of supply. (Even Sweden, which had

hitherto provided untied aid to Bangladesh, will tie 40 percent of its

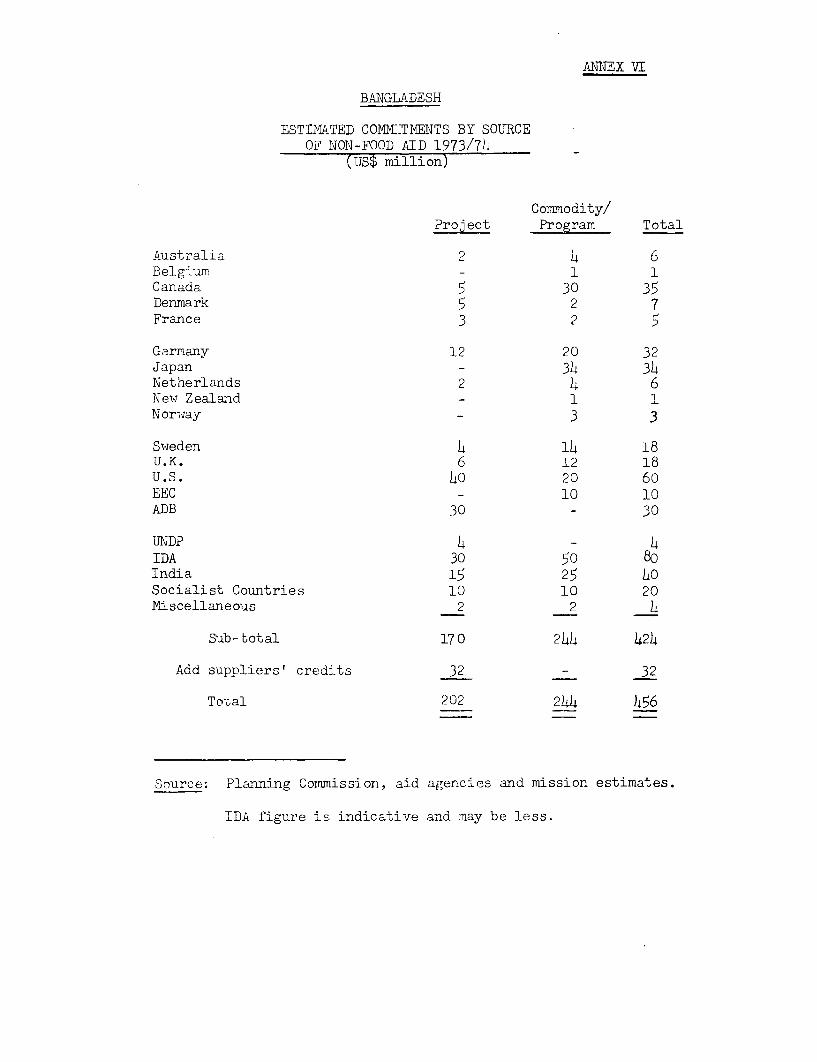

commodity assistance this vear.) Annex VI shows that, even under present

assumptions about project preparedness, only about 55 percent of total

non-food aid to Bangladesh during 1973/74 will be in the form of program

lending, compared with about 70 percent in 1971/72 and 66 percent in

1972/73. The estimated percentage of program aid for 1974/75 is inder

50 percent, which reflects donors' intentions of redirecting aid commitments

towards projects in the Five-Year Plan. Major donors are colnscious, how-

ever, that they mav be reqtlired to direct more resources than presently

contemplated towards program aid, because so few projects are ready, and

because the need for program aid persists.

The Case for Pro _gaL Tndin-

21. The case for program lending rests on tihree interrelated aspects

of the current state of economic development in Bangladesh: the urgent

need for materials, spares, components and machinerv to restore industrial

production to levels of existing canacitv: the need for rapidlv disbursing

aid to help meet the foreign exchange gap; and the lack of an adequate

p:_ 4 ect pineline. The first of these is discussed in paragraDhs 10 and 12

above and in more detail in paragraphs 37 to 39 below. The inescapable fact

is thiat, to restore existing industrial plant to good working order, equip-

ment that was destroyed, lost or worn out, Tmust be replaced and stocks of

vital spares and raw materials must be replenished. In many industries,

the priority need is simply for a steady supply of the raw materials or

components of production. UJntil the trade gap can be closed, the need for

such imports will have to be met from aid disbursements, and commitment

of aid against project requirements will only help after a year or two at

best. Finally, a number of obvious circumstances has prevented the develop-

ment of an adequate supply of projects which can ranidly absorb commitments

- 7 -

and produce disbursements. The disturbances which resulted in the warcontinued to inhibit project preparation even after independence. Theresults of earlier efforts were often vitiated, and many key personnelwere lost or displaced. It is not surnrising that the Government is onlynow finding both the time and the personnel to begin tackling this problem.

22. In circumstances of continued shortages of critical items and asevere foreign exchange constraint, program aid must continue for sometime to be a mainstay of development aid to Bangladesh, both from multi-lateral and bilateral sources. All available funds under the ReconstructionImports Credit (see paragraph 47 below) have been committed since about theend of August 1973. The Government's ability to authorize vital importsmust not be interrupted. In particular, it needs now to place orders forthe 1974/75 fiscal year. Hence the importance of the proposed credit atthis time.

PART II - BANK GROUP OPERATIONS IN BANGLADESH

23. Sklce Bangladesh became a member of the Bank and of the Associa-tion in August 1972, Bank group operations in Bangladesh have concentratedmainly on reactivation of IDA credits for uncompleted projects financedunder credits to Pakistan before the independence of Bangladesh. Elevensuch projects in an aggregate amount of USS151.4 million (including USSt44.1million for the repavment of amounts that had been disbursed under thecorresponding previous credits to Pakistan) have been made to Bangladesh.The last reactivation credit (US$25.0 million for the Highwav Project) wassigned on June 29, 1973. In addition four new credits have heen made,totalling USf65.6 million: US$50.0 million for a Reconstrtuction ImportsProgram; USS7.5 million for the Cereal Seeds Project; US$4.0 million forthe Technical Assistance Project; and US$4.1 million for the Inland WaterTransport Rehabilitation Project.

24. Annex II contains a summary statement of (i) IDA credits madeto Bangladesh, (ii) the loan and credits to Pakistan for completed projectslocated wholly in Bangladesh for which a new loan and new credits have notbeen made to Bangladesh, and (iii) notes on the status of execution ofongoing projects. There are no IFC investments in Bangladesh.

25. Previous IDA lending and prospects for FY74 reflect the inter-runtion of project preparation efforts in 1971 and the precedence takensince then by reconstruction efforts. Two earlier IDA projects, theReconstruction Imnorts Credit and the Inland Water Transport Rehabilitationproject, therefore concentrated on program-type lending to meet the mosturgent short-term needs of the economy. This proposed imports programcredit also falls into this category.

26. Although program lending will continue for some time to be anecessary feature of IDA assistance to Bangladesh, the proportion of projectlending wil]. increase year by year, beginning with this fiscal year. Two

- 8 -

other projects are likely to be presented to Executive Directors shortly.

One, a telecommunications project, benefits from preparation work already

done and will support part of the Five-Year Plan for telecommunications.

The second, the Barisal irrigation project, has been preDared by the

FAO/IBRD cooperative program. Two further projects should be ready for

presentation in early FY75. They are a population planning project, for

which IDA missions did considerable preparatory work, and a fertilizer

production project, for which IDA preparation missions supplemented work

already done in Bangladesh.

27. For the longer term, IDA has provided funds under the Technical

Assistance Project to assist the Government with studies and technical

assistance needed in overcoming the hiatus in project preparation and thus

help to develop a stream of projects which would serve longer-term develop-

ment objectives. Several proposals are being prepared; subprojects are

expected to be approved shortly which will prepare for a second inland

water transport project and a second Dacca water supply project.

28. The Association recognizes the prime importance of the agricultural

sector (on which the livelihood of about 80 percent of the population

depends) and accordingly plans to allocate to agriculture a much higher

percentage of lending than before. Before 1971 only one-third of Bank

Group lending to the area of Bangladesh went to agriculture. This was the

result both of the difficulties encountered in the formulation and execution

of agricultural projects - difficulties arising from Bangladesh's river

dominated terrain and a climate that brings devastating floods as well as

drought - and of inadequate appreciation of possible alternative investment

strategies for agriculture. A review of alternative strategies for the

development of the agriculture and water resource sector was undertaken

by the Association during 1971 and 1972. It suggested the need for a

stronger emphasis - especially during the next few years - on proiects

designed to yield results rapidly. This view of priorities is set forth in

detail in the Bank's nine volume "Land and W4ater Resource Sector Study"

(Report No. PS-13, dated December 1, 1972). With this in mind, a number of

agricultural projects are being prepared or will be prepared under the

Technical Assistance Project. Projects already under preparation include

minor irrigation works and supporting agricultural inputs in the Mluhuri

and Karnafuli river areas, an inland fisheries project, an integrated rural

development project, an agricultural training project, and a second food-

grain storage project.

29. Growth of sectors other than agriculture will require attention

as well, particularly the development of the transportation system to

improve the distribution of agricultural inputs and bring farm output and

food imports to market, and the development of industries, especially those

serving the rural areas (such as fertilizer) and those based on agricultural

materials. The scope for further transportation projects should be defined

by the Bangladesh Transportation Sector Survey now being completed with

tUnited Kingdom assistance. In industry, the Association has completed a

survey of the small-scale sector (Report No. 154a-BD, July 23, 1973) and a

second small-scale industries project is expected to carry on the work of

the first, reactivated project. It may also help rural-based industries

such as cottage and handloom industries.

- 9 -

PART III - THE PROJECT

30. The proposed Imports ProgLam credit, like its predecessor thi..Reconstruction Imports Program Credit, i. intended to provide thc Governmentwith the abiAty to finance priority imports of raw materials and equipmentnecessary to make use of existing productive capacity. In July 1973, theGovernment requested a second program credit. An Association missionappraised the proposed credit from September 13 to October 17, 1973, andnegotiations were held in Washington on December 17-z1. The Governmentwas represented by Mr. M. Syeduzzaman, the Secretary of the Planning Com-mission, Mr. A. H. Choudhury, an Executive Director of the Bangladesh Bank,and Mr. N. Islam, First Secretary (Economic) at the Bangladesh Embassy inWashington. A Cre.it and Project summary is attacned as Annex III.

31. The Reconstruction Imports Program Credit covered a broad, multi-sectoral range of goods. I_ is proposed in the second, or Imports Programcredit,to concentrate primarily on the revival of production in certaintpriority industries. As noted in detail in paragraphs 58 to 60 below,this will enable tht AssociaLion to monitor more closely the use of theproceeds of the credit, and to measure more effectively the benefitsachieved. It is appropri--e, therefore, to provide as background a briefpicture of the industrial sector in Bangladesh, and the conditions underwhich it has operated since independence. The forthcoming basic economicreport will provide a more exhaustive treatment of the sector, but it isimportant for the purposes of the proposed credit to provide a view of thebottlenecks preventing the fuller utilization of existing capacity.

The Industrial Sector

32. General - Historically, the manufacturing sector of Bangladeshhas been greatly influenced by the scarcity of natural resources. Today,industry is a small but important segment of the emerging national economy.It accounts for some 8 percent of GDP, and 6 percent of total employment.Perhaps two-thirds of all industry is agro-based, and the textile sectoralone (that is, jute and cotton processing) accounts for more than two-fifthsof total industrial value added, and for more than a half of total industriallabor force. At the other end of the industrial spectrum is the small-scale sector composed mostly of cottage-type units. Between these twoextremes are industries processing food, tobacco, skins and hides, wood,metals, oil, and natural gas. Bangladesh has among the lowest levels ofper capita production and consumption of industrial goods of any country.

33. Compared with other sectors, the direct physical damage to in-dustries caused by the war was not very sizeable, but the sector as awhole was seriously affected by the disruption of vital material linkagesof enterprises, and by general uncertainty. The new Government nationalizedmost medium- and large-scale industrial units and the public sector nowcovers the units that belonged to the public sector previously under tnemanagement of the East Pakistan Industrial Development Corporation,the units that were owned by West Pakistani entrepreneurs and abandoned

- 10 -

by them during the war, and all the units in the jute, cotton textile andsugar industries. The public sector now comprises about 350 units withabout 250,UO0 workers and about 70 percent of the fixed assets of modernmanufacturing, that is, excluding cottage industries. These are organizedunder several industrial "corporations" called the Public Sector Corpora-tions, under a ministerial body.

34. The private industrial sector now consists mostly of small-scaleenterprises. Private medium- and large-scale units exist to a significantextent only in the pharmaceutical (three foreign owned units), edible oiland steel re-rolling industries. New enterprises with assets of aboveUS$333,000 must be in the public sector. Existing private sector unitsbelow the US$333,000 benchmark may not grow past US$465,000 without beingabsorbed into the public sector.

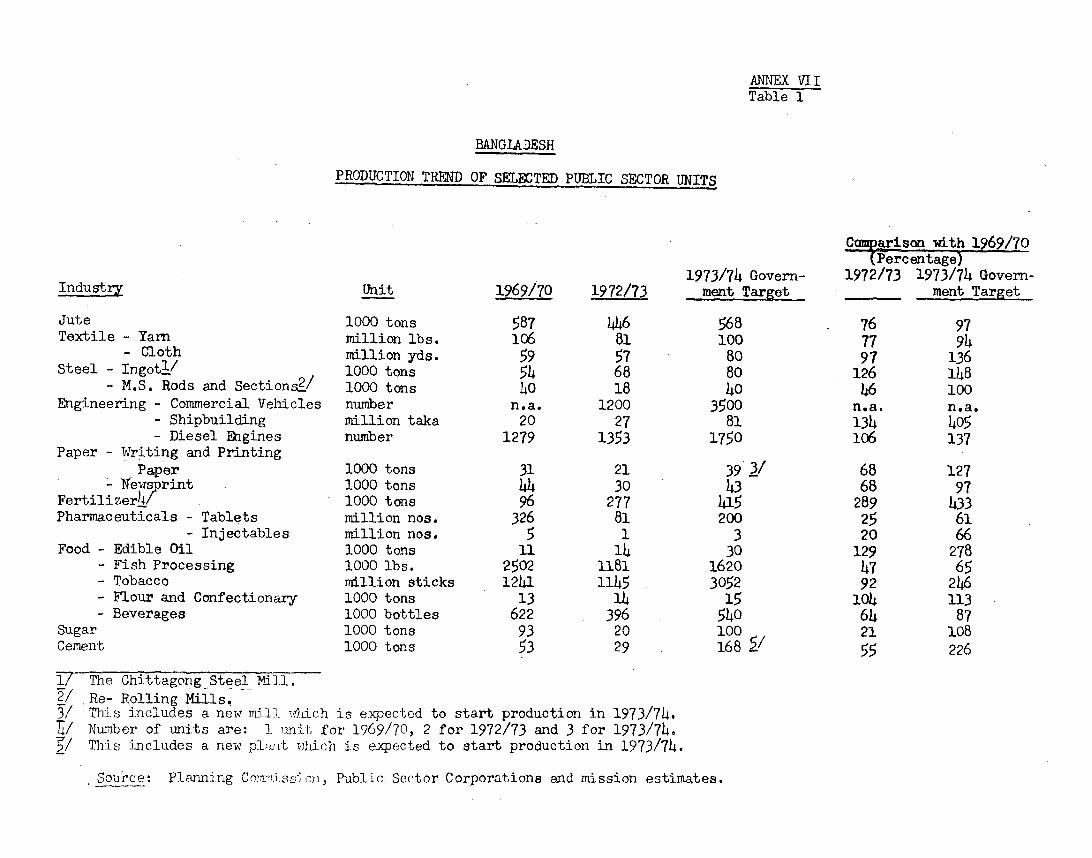

35. Industrial Production and Constraints in 1972/73 - Industrialproduction in 1972/73 showed some improvement over the previous year, butwas still unable to return to the prewar (1969/70) level in most enterprises.Production of most items (see Annex VII, Table 1) returned to about 70 percentof the 1969/70 levels, and only a few items surpassed the 1969/70 levels.

36. Problems derived from the transition into the public sector, whichstarted in April 1972 and continued through 1972/73, or inherited by thepublic sector from past conditions, affected industrial production in 1972/73.To resume production in these units, the Government and the Corporations oftenhad to rehabilitate physical production facilities and re-establish manage-ment structures. More important, they sometimes found that enterpriseslacked working capital. This problem was not solved until the Governmentdirected nationalized banks to meet the requirements. The problems oftransition still exist. Experienced management staff is scarce. Anefficient division of responsibilities among the Government, the Corporationsand the individual firms has not yet been worked out.

37. Other familiar major problems were sometimes aggravated in 1972/73.In general, shortages of imported inputs, labor troubles, and power failuresprevailed throughout all industries, while loss of markets in the former1West Pakistan and shortages of local raw materials hampered production insome industries.

Short-Term Prospects for the Industrial Sector - The prospects-ior z',7J/74 Industrial production depena on o-vercoming the shortages ofimported inputs and spare parts, and also the .cwer and labor problems.Regarding electric powe. some mechanical difficultie3 affecting powergsneration have been repaired; however, general shortages due to the in-adequate transmission network, small technical troubles and scarcity offuel are likely to continue. The future of labor problems is more difficultto foresee, and positive measures to deal with them must be a first prio-rity for the Government. Trantsportation bottlenecks for local and importedmaterials have been partly but not completely removed.

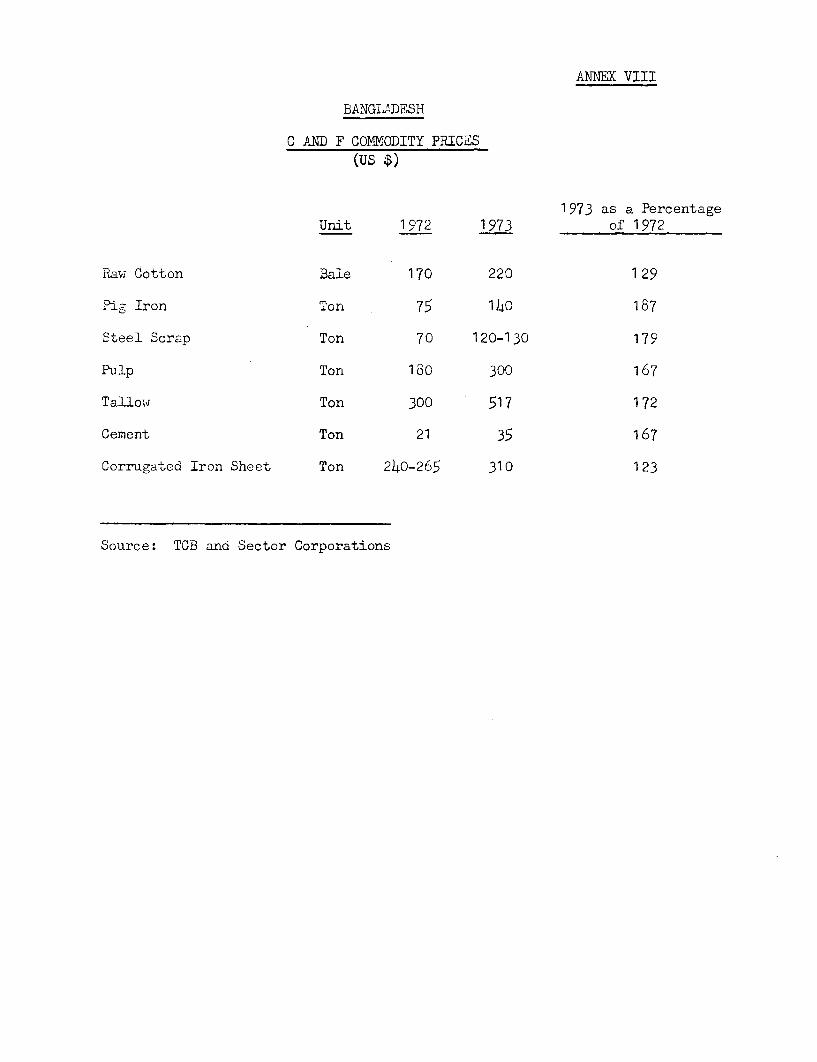

39. Availability of imported raw ma.erials and parts continues to bea major constraint. The scarcity of foreign exchange is of course themain factor. Against an estimated import requirement of about US$630 millionneeded to run industries on a single-shift basis only during the periodfrom independence to June 1973, the Government was able to issue onlyUS$265 million of import licenses. An ever worsening international com-modity price situation has further aggravated the problem and will surelyaffect production in 1973/74 and beyond (see Annex VIII). The supply situationof a few items has become so tight that Bangladesh is not able to importthem at any cost because goods simply are not available in the internationalmarket. As a result, most industrial units have kept very low stocks ofmaterials and parts, or none at all, whereas six months of stocks aredesirable for most items due to the long time needed for importing. Pro-vision of imported materials is the most crucial problem which the Govern-ment faces in increasing industrial production.

40. Production targets for 1973/74 for selected industries are givenin Annex VII, Table 1. These targets, based on Government estimates, havebeen adjusted downwards by the appraisal mission in some cases where theywere clearly a.ealistic. The resulting targets are still very optimistic;they do not reflect, for instance, the recent and expected increases inprices of imported materials. Even if these targets were achieved, pro-duction for about one third of the industries selected for illustrationwould still be below 1969/70 levels.

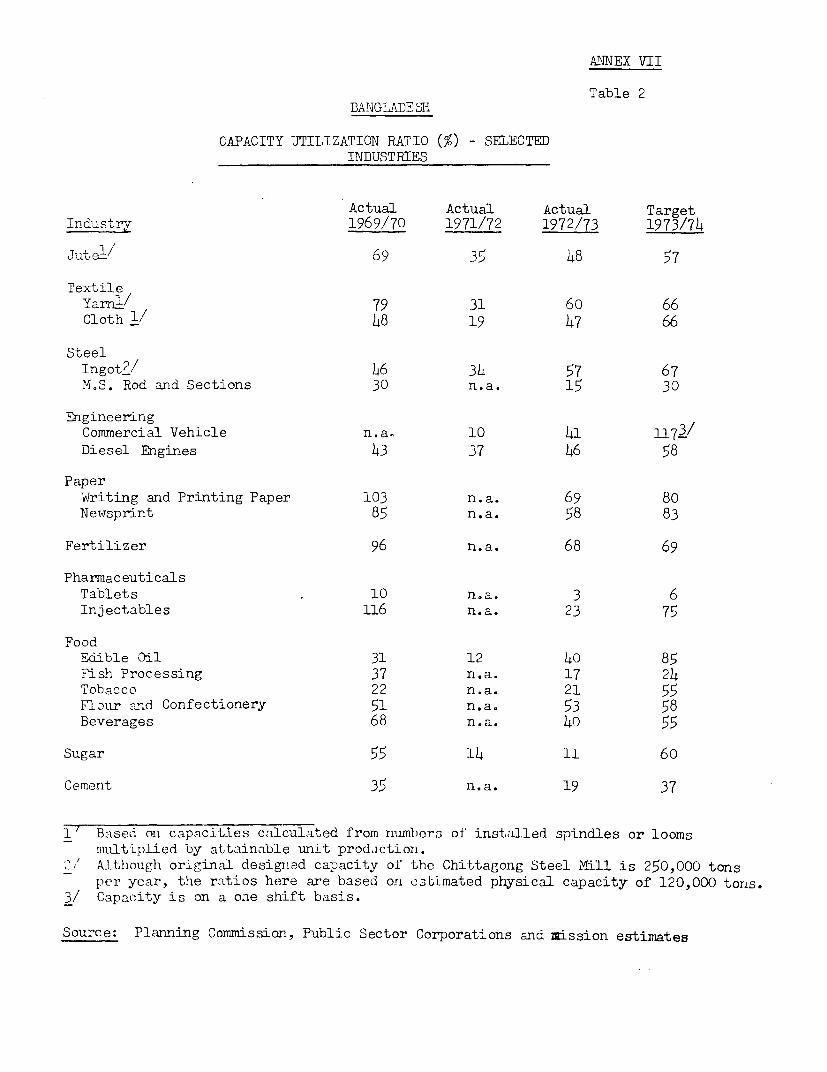

41. More important, production targets are not high enough to utilizeexisting capacity fully. If the targets were reached, capacity utilizationratios in 1973/74 would still b- less than 70 percent for the majority ofthe industries (see Annex VII, Table 2). These levels would be considerablylower were it not for the expected disbursements of large amounts of programlending by th.- Association and by bilateral donors. Utilization of existingcapaciry must continue to enjoy a top priority in the Government's industrialpolicy, and for external assistance to Bangladesh.

42. The Import Control System - Another important factor presents aserious obstacle to efficient industrial production in Bangladesh: thesystem of import controls. Some of the problems of the system, as theyhave affected the rate of utilization of the Reconstruction Imports ProgramCredit, are discussed, with suggestions for improvement, in paragraphs45-48 below. The system is summarized briefly in Annex IX, which indicatesthe considerable scope for delay which is inherent in the system. The systemis in need of a thorough review by competent analysts who should be asked forrecommendations for a complete overhaul. During negotiations, the Governmentagreed to conduct such a study, to be comupleted on a timetable and with termsand conditions to be agreed with the Association.

43. Supervision of the Reconstruction Imports Program Credit hasshown that although the system can lead to long and costly delays, constantvigilance of each transaction can greatly speed up the process. Accordingly,as an interim measure, the Government also agreed at negotiations to thestrengthening of the unit in the Planning Commission already established

- 12 -

to monitor the progress of the credit, especially to expedite actions inall concerned agencies in the import process up to the time of shipment ofgoods.

The Reconstruction Imports Credit (345-BD)

44. The Reconstruction Imports Credit w7as signed in November 1972 forthe purnose of assisting the Government in meeting the most pressing importrecuirements of an economy in the early stages of recovery from the severesetbacks caused by cyclone damage in 1970 and the war of 1971. The listof goods agreed between the Government and IDA as eligible for financingwas broad, covering all major sectors - agriculture, transport and com-munications, and industrv - and two major categories of needs: (i) equip-ment and snares to replace or repair capital goods destroyed or damagedin 1970 and 1971 in order to restore the economy's prewar capacity, and(ii) materials, components and intermediate goods needed as inputs toutilize existing production capacity in agriculture and industry.

45. Utilization of the Credit suffered immediately from delays by theGovernment in organizing imports to be financed. The Government wasreluctant to issue licenses against the Credit until the Credit becameeffective. It did not even begin the process of allocating the funds topotential end-users tntil late February 1973. Given the time necessaryunder the import control system for the notification of end-users and thepreparation, review and approval of license anplications, the majority oflicenses were issued only in the June - August 1973 period. Of course,further time'was required for tendering, ordering, and shipping, beforedisbursements could begin.

46. Another cause of slow utilization of the Credit was the Govern-ment's reluctance to issue import licenses for goods to be financed outof the proceeds of the Credit, in amounts greater than the total amount ofthe Credit. Thus, delavs by individual users, or cauised by the importcontrol svstem, or arising from the need to reallocate funds to higherpriority uses, have not been balanced by more rapid utilization elsewhere.

47. As a result of these delays, only a small portion of the goodsto he imported under the Credit has arrived and been utilized so far.Accordingly, the Credit had no impact on production in 1972/73, althoughit will contribute substantiallv to production in 1973/74. As of November30 the Government had issued licenses against the proceeds of the Credit fora total value of US$49 million. Of this amount letters of credit havebeen opened for UtS$37 million, including IJS$21 million against which theAssociation has issued agreements to reimburse. In addition, the Governmentrequested reimbursement for an additional UJS$11 million of eligible goodsor(lered before, hutt paid for from the Covernment's cash resources after,the signing of the Credit. Disbursements as of December 31, 1973 amountto US$21.7 million.

48. After the initial slow start, progress in accelerating letter ofcredit openings and disbursements has been rapid and heartening in recentmonths, and it now appears that the Credit should be almost fully disbursed

- 13 -

bv the end of June 1974. However, the Government has been urged to adoptpractices xwhich will prevent repetition of the kind of delays experiencedunder the Credit. The Government has realized the cost of excessive cautionin issuiing licenses under the Reconstruction Imports Credit and confirmedat negotiations that it planned substantial advance licensing (US$25 millionbefore December 31, 1973) against the funds to be made available under theproposed Imports Program credit. Further, the Government agreed atnegotiations to issue licenses well in excess of the amount of the credit.

49. The Government's allocation of the proceeds of the ReconstructionImports Credit reflected the availability of alternative financing andthe feasibility of importing goods rapidly, as well as the Government'soverall priorities and development objectives. The initial pattern ofallocation was changed from time to time as the Government withdrew allo-cations from enterprises whose utilization of their share of credit wasslow and reallocated the funds to those whose utilization had been moreexpeditious. Difficulties in procuring some eligible items, suchas rock phosphate, were also a cause of license reallocation. The presentexpected pattern of utilization of the proceeds of the Credit, by sector,is: agriculture, 10 percent; transport and communications, 20 percent;industry, 61 percent; and construction, 9 percent.

50. The beneficiaries which have been able to act most expeditiouslyin utilizing their allocations have been the Public Sector Corporations andthe Trading Corporation of Bangladesh (TCB), a Government owned organiza-tion which, at the direction of the Government, procures certain items,e.g. bulk commodities where large orders may get better prices, for bothpublic and private sector firms. Imports administered by the eight majorPublic Sector Corporations, together with raw cotton imported through theTCB (but used exclusively by public sector mills), account for 68 percent ofletters of credit opened. A few major items - vehicle spare parts, cottony:-rl, cement - were directed towards specific industrial units in both thepublic and private sectors. Apart from those items, private industrialunits have used only a small portion of the credit.

51. The TCB utilized its licenses fairly rapidly for most items forwhich it was the sole importer through bulk procurement (which includedcaustic soda, cotton yarn, raw cotton, and cement). It encounteredproblems, however, in procurement and distribution of certain items. Inthe case of rock phosphate, TCB was not able to cope with rising pricesand a difficult stupply situation, and the stubstantial purchases necessaryto keep up fertilizer production were not made.

52. In the case of cement and corrugated iron sheet delays and confusionoften resulted from the complicated distribution system, although it wasdesigned to meet priority needs first. Because of their importance - con-struction is almost at a standstill - these items are included in the proposedlist of goods for the proposed Imports Program credit. However, given thecritical, shortages, there is need for a clearer definition of priorities,anl(l better adlministration of distrihtition arrnngements to see that essentialconcstruction needs are met. Accordingly, the Government has discussed1 withthe Association plans for the distribution of the amounts of these goods to

- 14 -

be financed under the proposed credit, and the Government and the Associationalso have agreed to keep these plans under continuous review.

53. Cotton yarn also had distribution problems. Both raw cotton andfinished yarn were imported under the Reconstruction Imports Credit, andboth are includee again in the proposed list of goods for the proposed ImportsProgram credit. As with the construction items, future distribution plansand continuous review were agreed at negotiations.

54. Parts of the small-scale industries allocation also have beenslow to be used. Two agencies, the Ministry of Industry and the BangladeshSmall Industries Corporation (BSIC), were each allocated $1 million. TheMinistry was able to find takers for only 20 percent of its allocation.BSIC recommended to the Chief Controller of Imports and Exports (CCIE) theissuance of licenses to 237 small units on the basis of an extensive assess-ment of applicants' requirements. However, because of differences of opinionon division of responsibility for administration of the credit beLween BSICand CCIE, issuing the licenses took nearly six months. The Government agreedat negotiations that BSIC should have sole responsbility for distributing theproceeus of the proposed Imports Program credit to the Small-Scale Industriessector.

55. There are many difficulties within the national banking system.It took some time for the nationalized banks to establish sufficientcorrespondent banking relationships in some countries wnere goods were tobe procured under the Credit. A further problem has been that many keyposts in the foreign departments of the banks had been occupied by WestPakistanis before independence, resulting in a lack of adequately trainedstaff and administrative continuity after independence.

56. Mlany of these difficulties might have been expected in a newstate. Specific remedies 'or some have been suggested and agreed, and forothers it is hoped that the general review of the import system (paragraph42 above) will suggest methods of improvement. However, as mentionedabove, progress has already been much improved in recent months. TheGovernment has shown its concern for rapid utilization by reallocatingfunds to other priority users, and it is acting to license ahead for theproposed Imports Program credit. 'Tle Government's concern, and the arrange-ments made during negotiations should go a long way towards assuring thatthe purpose of the proposed credit, rapid provision of vital imports, willbe n<

TEh; Proposed Thports Progrym Credit

57. The Reconstruction Imports Program Credit was designed to meetthe needs of an emergency situation, and it truerefore financed inputsfor several sectors - industry, agriculture, power, and the transportsystem - with agriculture and transportation receiving large allocations.It is now appropriate to provide a sharper focus to the uses of theproposed credit by concentrating more resources on the highest priorityindustries. Broadly defined, these are the industries that (a) produce

- 15 -

goods for export, (b) serve the essential requirements of consumers, and(c) serve the key transportation and construction sectors. The need forexports, transportation and construction is obvious; essential consumergoods also must be given high priority in order to reduce the scarcity ofnecessity items contributing to the high rate of inflation and the generalfeeling among the public that the living standard is deteriorating.

58. Narrowing the range of industries will make it easier to monitortheir progress and to follow and supervise the use of Association funds.It will also make it possible to meet their needs more systematically.For many industries, raw materials were not provided under the ReconstructionImports Credit. For others, replacement machinery was not covered. Forthe proposed Imports Program credit, the industrial part of the list ofgoods has been arranged on an industry-by-industry basis. The industrialcategory provides for components, spare parts, balancing equipment, rawmaterials, chemicals and packing materials for each of the eleven sub-sectors covered.

59. Another reason for sharpening the focus of the proposed creditis that, for many of the items financed under the existing ReconstructionImports Credit, it is now appropriate to consider project lending. Finishedtugs and barges for the inland water transport system and telecommunicationsitems are examples for which projects are already in the pipeline. (Theproposed credit does, however, include a small amount of steel in theshipbuilding industry which will make tugs and barges in Bangladesh.) Foritems such as tubewells and low lift pumps, which were included in theReconstruction Imports Credit, the need is still urgent and the potentialbenefits great, but there are problems in utilization which should properlybe dealt with in the context of a project credit. These include such issuesas proper location for pumps and wells and their integration withcomplementary programs in agriculture and rural development.

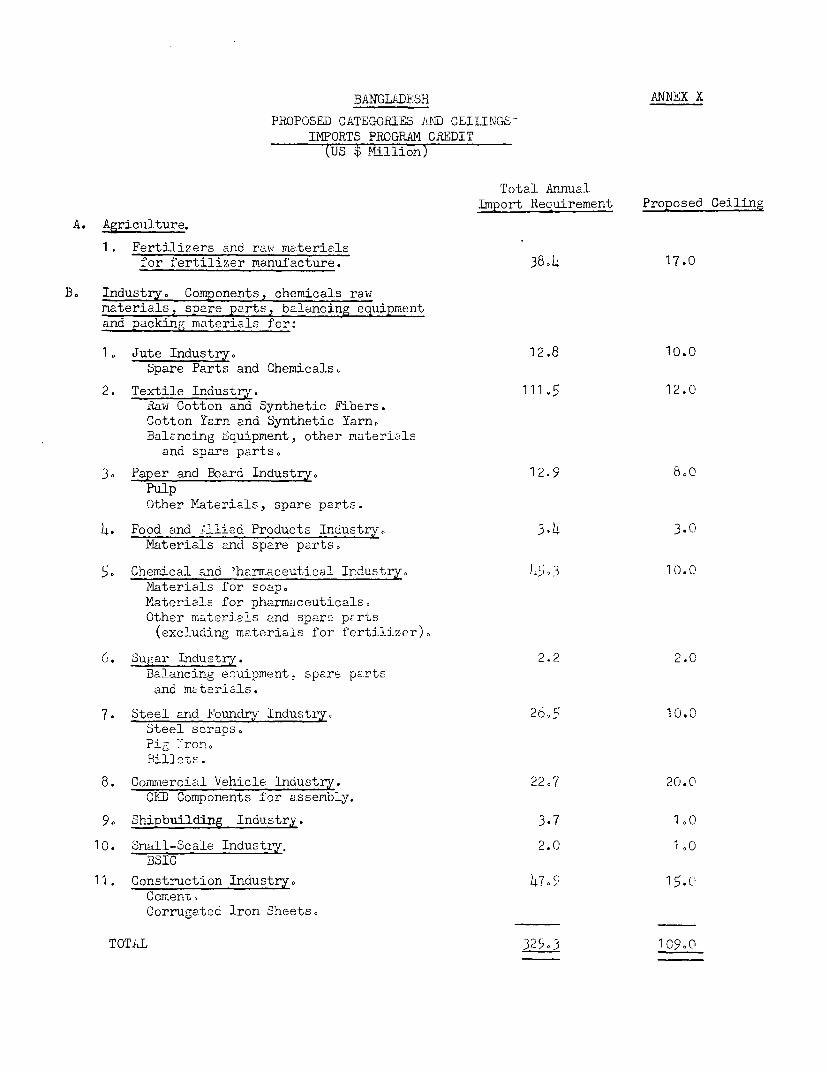

60. Proposed Uses of the Proceeds of the Credit - The categories ofitems which would be eligible for financing out of the proceeds of thecredit are set out in Annex X which also shows the main items expectedto be imported for each industry, the estimated total annual import require-ment for each and the proposed ceiling for expenditures under the credit(see paragraphs 17 and 78 below). The proposed Development Credit Agree-ment will contain only the major headings ana tht. propostd ceilings. Thecategories are discutsed in detail in the paragraphs which follow.

bl. A. Agriculture. FertilizeL is one of the key inputs in the agri-cultural technology bas-d on hig.i yielding seeds for agricultural production.In Bangladesh, increased use of fertilizer along with other agriculturalinputs is of immense significance as, due to limited possibilities forexpansion of cultivated land, increased production must come from landalready being farmed.

62. Th_ proposed credit would help meet remaining import needs for1973/74 and the requirement to build up stocks by July 1974 to meet theneeds of the 1974 aman rice crop. The total requirement for 1973/74 isthus estimated at 716,000 tons of urea, triple super phosphate (TSP) and

- 16 -

muriate of potash (MP). Allowing for estimated local production of ureaand TSP, and expected arrivals from the aid pipeline, there are uncoveredimport requirements of 84,000 tons of urea, 17,000 tons of TSP, and29,000 tons of MP.

63. The actual requirements may differ from the above figures asbetween urea, TSP and MP, because distribution of fertilizers may differfrom the planned programs. More important, it may be necessary to importmore finished TSP if rock phosphate cannot be procured. The two local TSPfactories did not produce any TSP in 1972/73 because imported rock phosphatewas not available. The ceiling proposed in Annex X would meet the needs forrock phosphate imports and the uncovered import requirements listed above,less an estimate of new aid commitments from other sources. Given thepossible need for importing a different mix, the Government should be allowedto use the funds flexibly for any fertilizer or material for the manufactureof fertilizer.

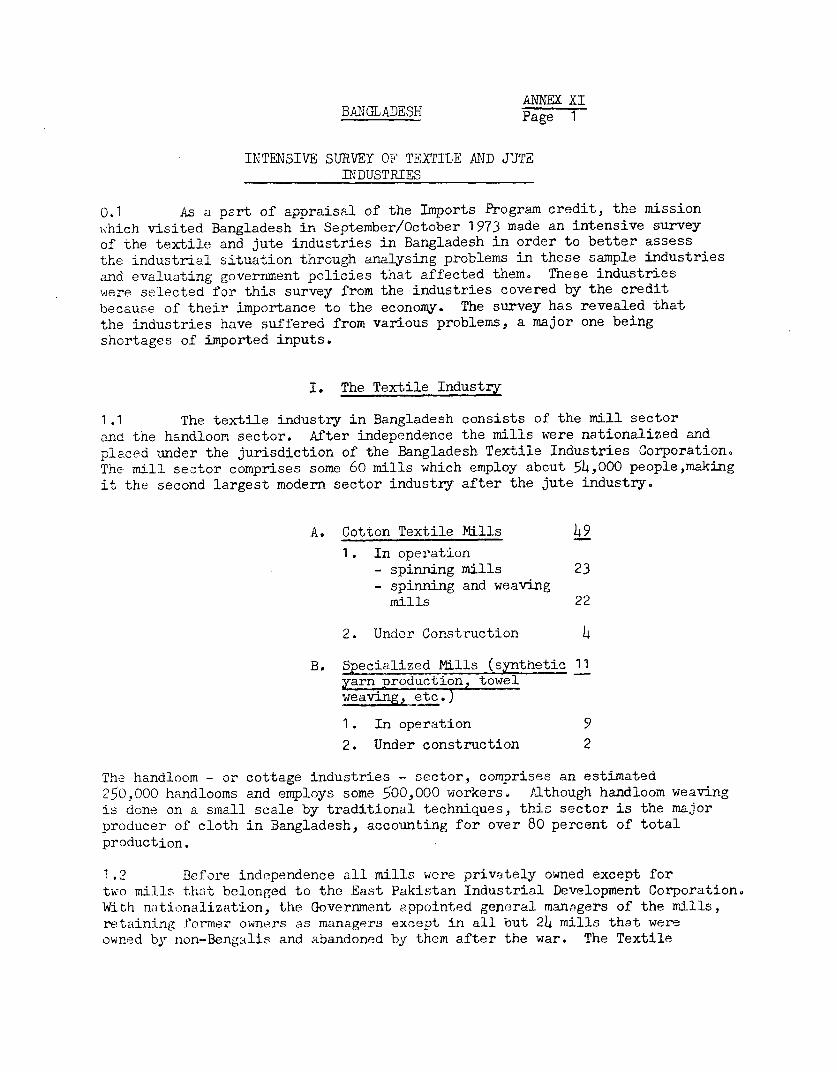

64. B. Industry. Eleven priority industrial sub-sectors have beenselected to be recipients of the proceeds of the proposed credit. Althoughprivate sector firms in these industries will be eligible, it is expectedthat public sector units, because they dominate these industries, willutilize the majority of the industry portion of the proposed credit. Themost important private sector users would be handloom weavers, small-scaleinduatries and construction businesses. Tute first two sub-sectors discussedbelow, the textile and jute industries, were the subject of an intensivereview during appraisal and are discussed in more detail in Annex XI. If

there are further program credits to Bangladesh, there will be furtheradditional inteiLsive surveys of industries selected as recipients of

Association funds.

b5. The jute industry is the major foreign exchange earner of Bangladesh.Export of jute manufactures (i.e. excluding raw jute) amounted to aboutUS$185 million in 1972/73. In addition, the industry is important for employ-ment, with 160,000 workers. It depends on imports for consumable andmechanical spare parts, dyes and chemicais.

66. The textile industry is comprised of mills and handloom weavingshops, and also is a major employer in the country. Because of inabilityto import sufficient quantities of cotton (much of which formerly came fromPakistan), the industry has not been able to meet local demand and thereforethe country has had to import finished products. Even so, there is drasticshortage of finished cloth. The industry can utilize the large and presentlypartly unused capacity in mills and handlooms shops only by securing impurtsof raw cotton, cotton yarn or synthetic substitutes. These latter areincluded as eligible items under the proposed credit because of the worldwide shortage of cotton and cotton yarn. The industry has demonstrated thatit can effectively use synthetics as a substitute. This industry needs alarge amount of spare parts because most equipment is old ana has been poorlymaintainea.

- 17 -

o7. The paper and board industry, utilizing locally available bamboo,jute waste and bagasse pulp, not only supplies writing and printing paper,newsprint and board to the local market, but also has export potential.It has already been exporting newsprint, and is trying to develop exportsof other items. Imported wood pulp is required to mix with local pulp soas to attain better quality, which is particularly important for export,and to fill the supply gap from local sources.

68. Among food and allied products, the proposed credit would coverspare parts and chemicals for processing shrimp, which is mostly exported,and other packaged food goods.

69. The chemical industry includes such important products as fertilizer,pharmaceuticals and soap. Both pharmaceuticals and soap are in short supplyin Bangladesh. For pharmaceuticals, the Government estimates annual importrequirement of finished goods at US$13 million, which accounts for about60 percent of the country's total requirement. The industry saves foreignexchange by importing raw materials and processing them locally. Currentutilization of overall local capacity is estimated at about only 4U percent.The credit would cover materials and spare parts required by the industry.

70. The sugar industry has not been able to satisfy local demand,although it has sufficient production capacity. Raw materials are locallyavailable. The industry would use the proceeds of the proposed credit forimportation of spare parts and balancing equipment.

71. The steel and foundry industry consists of the Chittagong SteelMill, re-rollers and foundries. The products of the Mill and re-rollers(the Mill also supplies materials for the re-rollers) are used mainly forconstruction and partly for shipbuilding. Foundries are important insupplying small local works producing simple spare parts, which would takei4`ustrial units a long time and cost a great deal to import. The industryrequires imported pig iron, steel scraps and billets.

72. The commercial vehicle industry assembles completely knocked-downcomponents into trucks and buses with less cost than that of importingfinished vehicles. Because an estimated 5,000 trucks alone were damagedduring the war, out of about 9,000 private trucks on the road previously,the Government has imported about 3,000 trucks and buses. However, morevehicles are clearly necessary to meet the road transport requirement. Theneed for buses for public transport, where there are both public and privatesector firms, is particularly urgent.

/3. The shipbuilding industry supplies barges, tugs and ferries andtankers for inland-water transportation which assumes the largest trafficburden in Bangladesh. After independence the Government established a planto reconstruct the war-damaged inland-water fleet, and nationalized a majorpart of it. There are at present two large shipyards in the pub±ic sector,and two more are under construction. These yards are technically capable ofmeeting the demand for these vessels though the industry is heavily dependenton imports of steel materials and equipment to be installed in the vessels.

- 18 -

74. The construction industry is hard pressed to meet demands for newand rehabilitated houses and facilities for essential government and businessactivities. Shortages of cement and corrugated iron sheets have constrainedconstruction, and, at the same time, endangered jobs for many constructionworkers. Shortages in cement, which were more severe than in corrugated ironsheets, have brought the price per bag up from US$2 just after independenceto US$7. Recently cement has virtually disappeared from the market.

75. small-scale industry units cover a wide sDectrum both in types ofindustry and in geographic L-ocations. They have close links with local marketsand local material sources.

76. The Public Sector Corporations will continue to be responsiblefor administering most imports under portions of the proposed credit tobe utJl±zed by their subsidiar1 units. TCB or CCIE will be responsiblefor importing textile yarns, foundry grade pig iron, cement and corrugatediron sheets to be used by both the private public sectors.

7X. Ceilings - Annex X shows the estimated annual import requirementsfor fertilizer and the selecl.'t.d industries. These amounts were based uponthe import requirements for 1973/74, but the levels are not expected tochange significantly from one year to the next. The proposed credit willin fact cover imports largely to be made in 1974/75, although some goodsare expected to arrive in 1973/74, and all of the licenses are expectedto be issued in 1973/74. The ceilings have been determined in most cases bytaking the estimated annual import requirement and subtracting amountsexpected to be filled by other foreign assisLance or normally covered bycash licenses against Bangladesh's foreign exchange earnings. In some cases,e.g. the textile industry, the ceilings have been further reduced in order toassure that the proceeds of the credit will be spread over all of the vitalsubsectors selected.

78. The ceilings which were agreed with the Government during negotia-tions have been incorporated into the Credit Agreement. However, theGovernment and the AssociaLion will keep these ceilings under continuingreview.

79. Procuremenrt - The bulk of the imports to be financed under theproposed credit, including some of the goods to be used by the privatesector, will be imported through Government agencies. Normal Governmentpz-r-urement procedures require international competitive bidding or atleast requesti-ag offers frovi a minimum of t}.-ae international suppliers.These procedures will be foliowed ror all procurement under the creditexcept for (a) goods cos,:ing less thaa US$100. )00C, and (b) special casesin which proprietary items, compatible spares and components, or deliveryon an emergency basis are required. Imports of goods costing less thanUS$1U0,000 will be made through normal commercial channels.

80. These procedures follow those of the Reconstruction Imports Creditwith the exception that the exemption from international bidding or shoppingfor goods costi.g less than US$100,000 would now be applied to the public

as well as the private sector. This will simplify and expedite Association

approval of disbursement applications.

81. Disbursement - Under the Reconstruction Imports Credit, there

were disbursement delays which arose because of the IDA disbursement pro-

cedure chosen by the Government in all cases over US810,000: the issuance

by the Association of agreements to reimburse. The Government had not wished

to first make payment to suppliers from its an foreign exchange resources,

and then be reimbursed by the AssociLation, giving as its reason the temporary

loss of reserves in a very tight foreign exchange position. This position

is still precarious, but because the Government recognizes the need for

rapid utilization of this proposed Credit, it was agreed to raise the amount

below which the Government would first make payment from its own foreign

exchange reserves to US$20,000.

82. The Bangladesh Bank would be responsible for obtaining disburse-

ment from IDA and arranging with banks to obtain the necessary shipping

documents. The Bangladesh Bank would also assure, and certify, in each case

that the goods have been supplied by IBRD member countries or Switzerland

and that they have not been previously financed by any bilateral or other

multilateral source. These documents would then be forwarded by the

Bangladesh Bank to the Association in support of withdrawal applications.

All items included in the list of goods and paid for after the date of the

credit would be eligible for financing under the Credit. It is expected

that all contracts under this credit would be placed by September 1974

and that the bulk of disbursements will be made within 18 months of the

date of the credit. The credit should be fully disbursed within 24 months,

i.e. by about January 1976.

PART IV - LEGAL INSTRUMENTS AND AUTHORITY

83. The draft Development Credit Agreement between the People's

Renublic of Bangladesh and the Association and the Recommendation of the

Committee provided for in Article V, Section 1 (d) of the Articles of

Agreement, and the text of a resolution approving the proposed credit are

being distributed to the Executive Directors separately. The draft Credit

Agreement contains no unusual provisions and is similar to the Credit

Agreement for the Reconstruction Imports Program Credit.

84. I am satisfied that the proposed development credit would comply

with the Articles of Agreement of the Association.

PART V - RECOMMENDATION

85. T recommend that the Executive Directors approve the proposed

credit.

Robert S. McNamaraPresident

Januarv 15, 1974

BANGLADESHAlMEXS

COUNTRY DATA Page 1 of 3 pz~geo

AREA POPULATION DENSITY

141,131 kIsM 75 million (mid-197 )530Pe3r Ice2

840 Per leot2o arahle land

SOCIAL INDICATORS

Reference Countries

___________________Indonesia Japan _ Ira1960 197o 1970 197 0 19706

GNP PER CAPITA US$ (ATLAS BASIS) LI08 12 8

DEMOGRAPI{ICCrd7 7hrate (per thoeusand) 57 48 48 18.9 45-47

Crude death rate (per thousand) 27~ 19 19 6.9 15417

Infant mortality rate (per thousand live births) 167 140 125k 13.0 100O-140

Life expectancy at birth (years) -46 47 48 71.0 49-53

Gross reproduction rate! 321.6 3.2 32 1.0 3.6

Population growth rate 13 2.8 3.0 2.0 1.0 3.1

Population growth rate - urban _________4.5 3.25G-

Age structure (percent)2407Ž0_1~~~~~~~~ ~~~547 44 2. 7

15-6b _48 51 54 69.1 4E

65 and over 3 3 2 6.9

Derzendency ratio /5 1.1 1.0 0.9 0.5 1.8

Urban Population as percent of total 5 7 17 68.0 41--

Family Planning: Noa of acceptors cumulative (thoujs.) L7_______15 662

No. of uasers (% of carried women) ________ _____________5-10

EILf OYMENTTotal labor force (thousands) 18,300 24,900 40.100 52,215.0 894BE/

Percentage employed in agriculture 75 75 63 20.6 41

Percentage unemployed _________2 1.2 3

INJCOME DISTRIBUTION .

Percent of national income received by highest 5% soP'ercent of national Thrcone received by highest 20% ________ 14.85O

Percent of national income received by lowest 20% 455'

Percent of national income received by lo'west 40% _________

DISTRIBUTION OF L.AND OWNERS1IIP%owned by top 10% of -ownr 34________ I

% owned by smallest 10% of owners . .1________________

HEALTH AND UUTRITIONIPopulation per physician io400L 10SQ 6 000 898- 0 --- 3100D

Population per nursing person 164 ,00 107.005 5.740 300 20

Population per hospital bed 11.200 9,400 1200 79.0 842

Per capita calorie supply as % of requirements /5 54-E/ 76,/ 104.3 0

Per capita protein supply, total (grams per dayTL/6 3.&9' gS 75.1 hi

Of which, animal and pelse ____3_______iA 47.3

Death rate 1-bi years /7 3.0/ 2.1-

EDUCATIONAdJusted /d primary school enrollment ratio 44. 57 77 98.0 56E/

Adjusted 7W secondary school enrollment ratio 9±' '/1 86.0 285-/

Years of achoolieg provided, first and second level 10.1 10--c-

Vocational enrollment as % of see. school enrollment _________ 20 9.

Adult literacy rate % 23 56 ~ y

HOUSINGAverage No. of persons per room (urban) 3 1f'11 2. 2,

Percent of occupied units without piped water 82.1' 5 1

Access to electricity (as % of total population) .

Percent of dural population connected to electricity _________ 4lik

CONSUMPTIONRadio receivers per 1000 population _________ 114 255.0 9 3-2

Passenger cars per 1000 population _ _______ 2 84.8 20

Electric power consumption (kwh p.c.) 3 11 18 2972.0 267S'

Newsprint consumption p.c. kg per year... 0.2 19.1 0.4

Notes: Figures refer either to the latest periods or to account of environimental temperature, body weights,an

the latest years. Latest periods refer in principle to distribution by age and sex of national populations.

the years 1956-60 or 1966-70; the latest years in prin- /6 Protein standards (requirements) for all countries as ectab-

ciple to 1960 and 1970. On'ly significantly different lished by USDA Economic Research Service provide for a minimum

periods or years are footnoted separately. allowance of 60 gramns of total protein per day, and 20 grazes of

/I The Per Capita GNIP estimates for years other than 1960 animal and pulse protein, of which 10 grams should be animal

is at market prices, calculated by the same conversion protein. These standards are somewhat lower than those of 75

teohunique as the 1972 World Bank Atlas. grams of total protein and 23 grams of animal protein as an

/2 Average nu.mber of daughters per woman or reproductive average for the world, proposed by FAO in the Third World Food

age. Survey.

/3 Population growth rates are for the decades ending in /7 Some studies have suggested that crude death rates of children

- 1960 and 1970. ages 1 through S may be used as a first approximation index of

/A Ratio of under 15 and 65 and over age brackets toI malnutrition.

those in labor force bracket of ages 15 through 65. /8 Percentage en~rolled of corresponding population of school age

15 FAG reference standards represent physiological re- as defined for each counitry.

qairerents for normal activity and health, taking

2/ 1962; b/ aver 5020 inhabitants; c/ 1971; d/ 1967-68; a! Nurses only, excludes otlher psranedi2-;

f/ Percent of population receiving ad-equate protein/calories in 1962/64; V/ 1964 -66; 5/ 1-5

i/ Up to eind ci lower secondary; J/ 1968; k/ 1966; 1/ Urban only, 19681 Ln/ 1969

010110MIC DWEMPEU30TJf 21T0(A.Ounots in, rallc f U.S. dollars)

A~~t-l p '961 ~~/197Actual 9P~1 71 - 'H 1909O -197r- 1797 - 7ii 19 1972

53210181. 3013121115~~~~~~ I -q72 3-3.-a4 A0--r4 at ____ - --

iCcolt. (ccot capacity --.8 33' -5I 5 7 1.

Pecat ,lp I 5 I'- 12 3

'oaip.-p-occdit-ccco iii -,33,1 I9302

lc' nta (ia- clt 7~ I P'. 1.11 7 13

Ucoocc cO r5e. 3 384 3 2 6I .1

Nat io-l Savlwng 7a 5 -

OPP.ClJ.011-"i all Auci oP 01cc at ourect~~~~~~~~F cArct i- If ctcl-

lispt~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~4

Cap to] flcc - ~~~~~ -1 - -1 -7 .7 -7

CcaoeIcl I ,0 V--- T- -t

Tota T.c r Ompu c(i0)i-45 TTI31.

l>rcnaey ic clot .- 'I i -- --~~~~~~,2 .

It -70 2Icod it-I Ii.2

7313 Al '--t --- ] ex,i I i 7- )9 1 31B i -oi oloog ioe oo Grc3 c-.5 co

A "r.i-I z. n- 2~,50 3o45P t.5 531.0

Mi.ni- )fO2 7~L -3 3.1 303 -

o 1 iC T-rootict 1 935 I773) I07 07 117 1 7 2 I9272U3 1 73/4! 19174/ S 1517 15727 3 191 73i10 9

-i 31e - -- ~~~~ ~~~~~~~~~~3 2' 4 3> 07

_____ IA-~ ~~ ~ ~~~~~~~ 4 - i1 391 2 -5 50

7 3 --- 742 23

dcc 3-'coil- Iit"orcacilt 379 - - 527 055 - 72.2 -- 03 0.0 12.1~~~~~~~~4 2 2 3 1

ladir-c.o I-i len I; cp-cIcd IIuc

-Il;r FmXP-r13T)1515r 'EP )i T33 A, c.ca 1T00 I cl.. ho). l JfT,l -YI-[sAmI I 3 1 Z

A o Tc, LI ar -c -.ri.( __9 I, 1-7 2i73 ia 3I- 13ul00 I .i 3 i To :OFic

lootec ~~~~~~~~~~~~~~~ ~ ~~~20. 0 19.0 --8 1 71 /74 -7i(. 7-,

01,h 0- 010 -i-c-sl 6.3 b3. 103 1 5 3

Hiirr,odotiic '.er'icOl ~~~~ ~~~~~~~6.6 52 nd fc-tryso) 1711c81,05 20,7

D-: W M~~~~~~~~00 10 Ri.-I lu.7

3.i. C 6002-. fuT- ;- jo stilt t 8 t lo 1 6.3

PoILC~TLo 1121 1008.35 1967- 1965 - 10721- 1973- - H)li3tii liii

-tlcce Iou --ceoo-edIdci Q360 - __ 5.75 3970

Ovra4eIr 01-7 - -l -- 2 9 211 -t crSetg 2,12 609.0

i-Yor 3lur--ty 2 - 29 ro-geed P-t- AtOltrccd728 4

- Nrccrc iujucI Savinga Rotc! 3 5 -- -. I ttoc--443 0.

CIli7 1 F I Wt101?01t It -ll7s3etlo! 901 - 23 I

iSao/-l 1972/ 3 IC9uI 139711 roosth cot- 1Ž7 12i Ii It 'Ir-Lt Pat-i

t.-ttiOotitc-c ~~~~~~~~~~~16.1 20 .5 o5I 20. 32.1.I

),sJcti6/ 1. 1.08 5.2I 6.9 5 - cc 1.0 ~~~~ ~~~~ ~~~~3.9 9.2 134. 9 3

Total 16.9 ~~~~~~~~~~~~2tc.m2 1 0-0 100.3oo 721128

-ooc opplicoblo - cii croopl~~~Ii;i 0blc -- not t.coilaclc . 1.-to hea hlE cii.-

tolIt ia t o oi-o

I/ IThe, dote fcc 1973 --wadc or tootc c tii-p,je 00- booed on thcc Fira 88c-Y-ur P1-

tihe, or iteoa ot1972/23 prli- -ed -h-iagt rot -od herni cli.-yor - tecto.p-rble

oPt cliceh a--,io oioca tcr 1965 - l9ll.

2/ includes ate~ ii-of,c-r- a-d lobe r-pocca.

3/ioldocd 1- co,Iioth -od -ulfare

4/ DebL -atri,.-s.

5/ Oobt atri-it -nd coigo

'I7/,t colodieg c , lcccoc ~t) cod aciIcos

7/1922/73 pri- -c cd echoerat-

0/ T-1a Fe--adaitoe

c-tt 311I fig-c- fce cc iao couc botia J,oy 1 J1- J 30.

ANNEX IPage 3 of 3

EALANCE OF PAYMENTS, EXTTiFNAL ASSISTANCE AIID DEBTmaaoentn in millicns of 11.7. do1lars at c-rrent pricea

2a 2/ Ag oonActual Estimated Pro loted Growth Fits19-69 19710 1971 l71 1973 177. 197 5 1976 197 18 17965-1970

SUMMARY BALANCE OF PAYMENTS

7portn (in1. NFS) 449 48^ 404 295 450 532 384 677 702 12Tmporta (incl. 6FS) h30 711 717 _750 3IA 992 1,970 1,170 1, 17L 4.9anonurcels 1-8) 101 -223 313 -661 -A90 -4;3 -7.1 -GIl .467

Foteorot (set)3ireot -ntnet T-onco 53 58 22i torlerS Bni4tan )

CurreDt Trasosfor (rst) 75 56 50Ra10n00 00 Corrent A.o-ootS -203 2 21 T-361 -53W

Private Lirsot Ecnoetloent- -OffYsi.a1 Capital Graoto

Publir 14< Loans

msTb..ren2ertn 426 112 282 296 365 416-800' Sten 24 61 61 74 77 AlST~~~~~~~n~~~~~stn - - i'a~~~~~~~~~~~~~~~~---r W78 -let Drusnn 222 21223

Otl1el P-i-T 14ac-DIo 94ur41 oars

lot DioborsnernDts

-rital Trslisoatolns n.e.i. 1999 19970 19 1972 1971;Re.e9Chanre in lint Fesorvo- 10R1 AlD DEbT 3SRVICEPubli c Debt 3u t . P Di3 b-s dP t;r_tNbt 4 -io .ome.

!'-. *., : ' '__Inotoreot ss Public DebtTRepeyments 00 PDblit Debt

_:Ilis 11.1. 1.7000 Total Public Bobs Bonbon1015 - Othbr D0b Serion (0.t)

ID9 72 Total Dbo S-rvio (st)1- :.-r 10I'll Ir MlltilatoI l oTrdes on Export O-oroogns (f) 11.2 1 b f 13.1.l,ovorsmnmets 151lopPl or:s 30 Pu510c Itbt SnrvicnF-niX.roarl Institataora - Total Dobt so-si-o10000 - T BDSDiro-t 3nveat. Ice.Public boos n.e.i.

T1t,IA :, 4..1 loan 662 Aver.go To-so of PfbliT DBbt

Acturl Debt NOtatanding 00 Dos. 31,1913 Iot. a- Prior Year W&D 2.7 2.7 2 . I 2X7TE'RNAL DEBT Dishbesed Only P-rreot AMort. 00 f Pr-ar Year W&D 41 .6 4.1 1.s 2 (. 1World BAko 61.8 4.4TIDA 98.G 6.9 IbRD DBbt CDt. & DibuhrnedOtber 0:ltilstoral 6.8 .5 as f .ublic Dlbt OB.D 5.7 5.7 5.3 4.1loosroansnets 1,129.3 fl a 0 Public Debt Snrvicn 10.7 11.2 14.( '2 1suppliors 91.4 0.4.-os7.:oi.ai Institutions 25.4 1.0 NDA Debt Ot. & DinburoedBonds as ji% bli DebtAGU 3. 7.9 7.3 h,' 6.10lbli5 Debts s.o.i -as b POle3 Debt Sorvioo I.0 1.1 1.0 1Total Plblit M< Debt t,412.9 100.0

Oth0r M< D0bt5Shaot-t.ro DBet (diNb. only)

. sot eppltoable e ntaff -estirtesot avAilablo - nil or negligible00- rasilable separately -- leen thoo half thsbht included io tatal smallest uoit shoes

If Col-ndap ypor/ Bab1oon of poy-enns deco for 1973 oo.erdc are eop-ees-d i0 -on-ta-t 1972/73 pBios end .ooheno.g

ANNEX IIPage 1

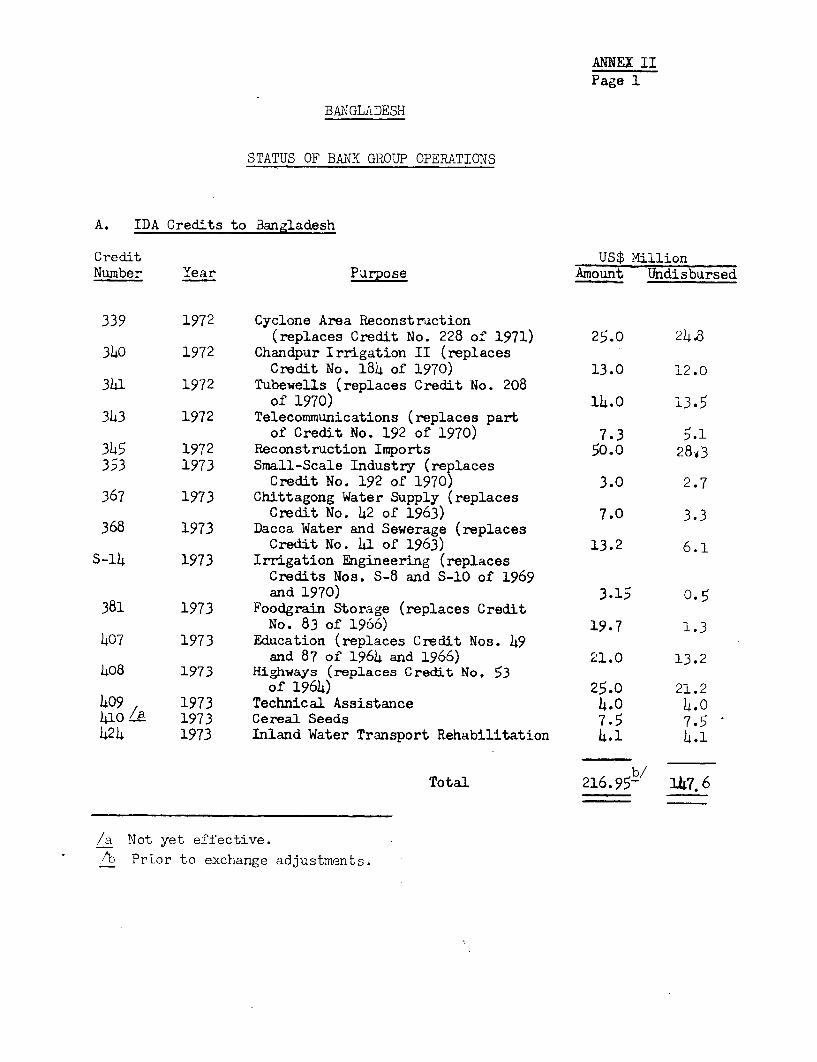

BANGLADESH

STATUS OF BANK GROUP OPERATIONS

A. IDA Credits to Bangladesh

Credit US$ MillionNumber Year Purpose Amount Undisbursed

339 1972 Cyclone Area Reconstruction(replaces Credit No. 228 of 1971) 25.0 24.8

340 1972 Chandpur Irrigation II (replacesCredit No. 184 of 1970) 13.0 12.0

341 1972 Tubewells (replaces Credit No. 208of 1970) 14.0 13.5

343 1972 Telecommunications (replaces partof Credit No. 192 of 1970) 7.3 5.1

345 1972 Reconstruction Imports 50.0 2803353 1973 Small-Scale Industry (replaces

Credit No. 192 of 1970) 3.0 2.7367 1973 Chittagong Water Supply (replaces

Credit No. 42 of 1963) 7.0 3.3368 1973 Dacca Water and Sewerage (replaces

Credit No. 41 of 1963) 13.2 6.1S-14 1973 Irrigation Engineering (replaces

Credits Nos. S-8 and S-10 of 1969and 1970) 3.15 0.5

381 1973 Foodgrain Storage (replaces CreditNo. 83 of 1966) 19.7 1.3

407 1973 Education (replaces Credit Nos. 49and 87 of 1964 and 1966) 21.0 13.2

408 1973 Highways (replaces Credit No. 53of 1964) 25.0 21.2

409 1973 Technical Assistance 4.0 4.0410 1973 Cereal Seeds 7.5 7.5424 1973 Inland Water Transport Rehabilitation 4.1 4.1

Total 216.95- b k147.6

/a Not yet effective.

1 Ab Prior to exchange adjustments.

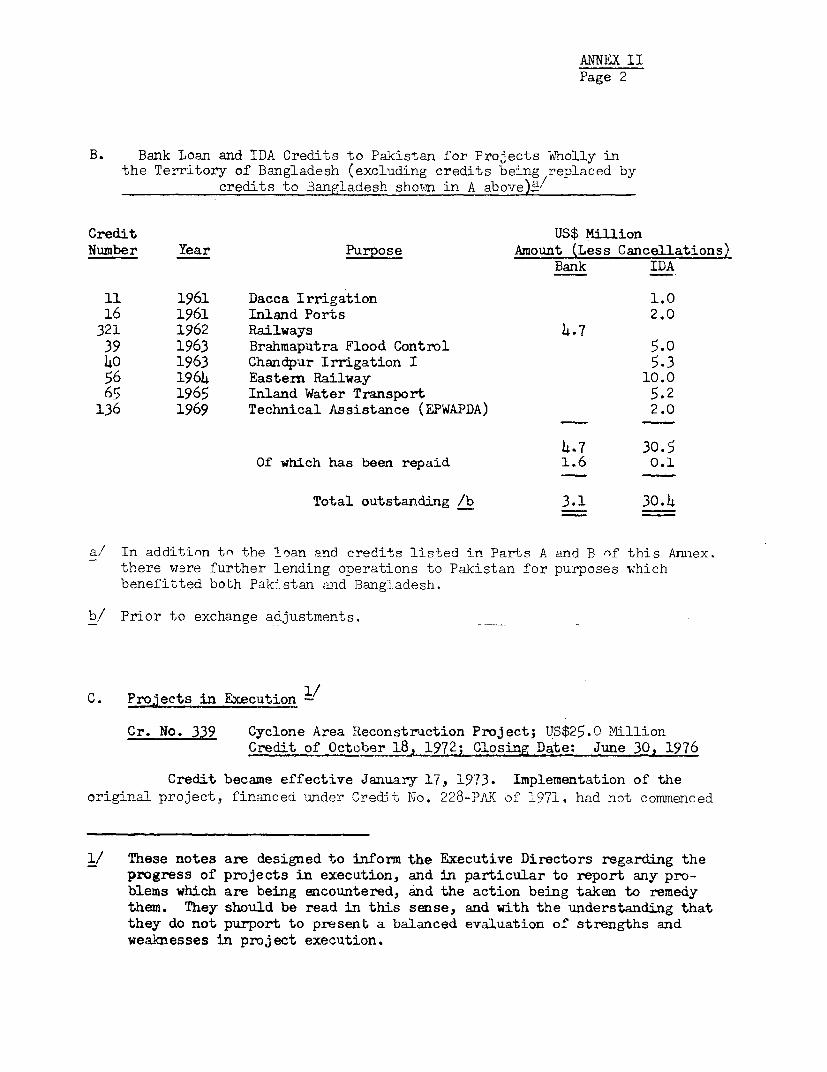

ANNEX IIPage 2

B. Bank Loan and IDA Credits to Pakistan for Projects Wholly inthe Territory of Bangladesh (excluding credits being replaced by

credits to Bangladesh showJn in A abovea/

Credit US$ MiUionNumber Year Purpose Amount (Less Cancellations)

Bank IDA

11 1961 Dacca Irrigation 1.016 1961 Inland Ports 2.0

321 1962 Railways 4.739 1963 Brahmaputra Flood Control 5.040 1963 Chandpur Irrigation I 5.3

56 1964 Eastern Railway 10.065 1965 Inland Water Transport 5.2

136 1969 Technical Assistance (EPWAPDA) 2.0

4.7 30.5Of which has been repaid 1.6 0.1

Total outstanding /b 3.1 30.14

a/ In addition tn the loan and credits listed in Parts A and B of this Annex.

there were further lending operations to Pakistan for purposes whichbenefitted both Pakistan and Bangladesh.

b/ Prior to exchange adjustments.

C. Prjects in Execution

Cr. No. 339 Cyclone Area Reconstruction Project; US$25.0 MillionCredit of October 18, 1972; Closing Date: June 30, 1976

Credit became effective January 17, 1973. Implementation of the

original project, financed under Credit No. 228-PAK of 1971, had not commenced

1/ These notes are designed to inform the Executive Directors regarding theprogress of projects in execution, and in particular to report any pro-blems which are being encountered, and the action being taken to remedythem. They should be read in this sense, and with the understanding thatthey do not purport to present a balanced evaluation of strengths andweaknesses in project execution.

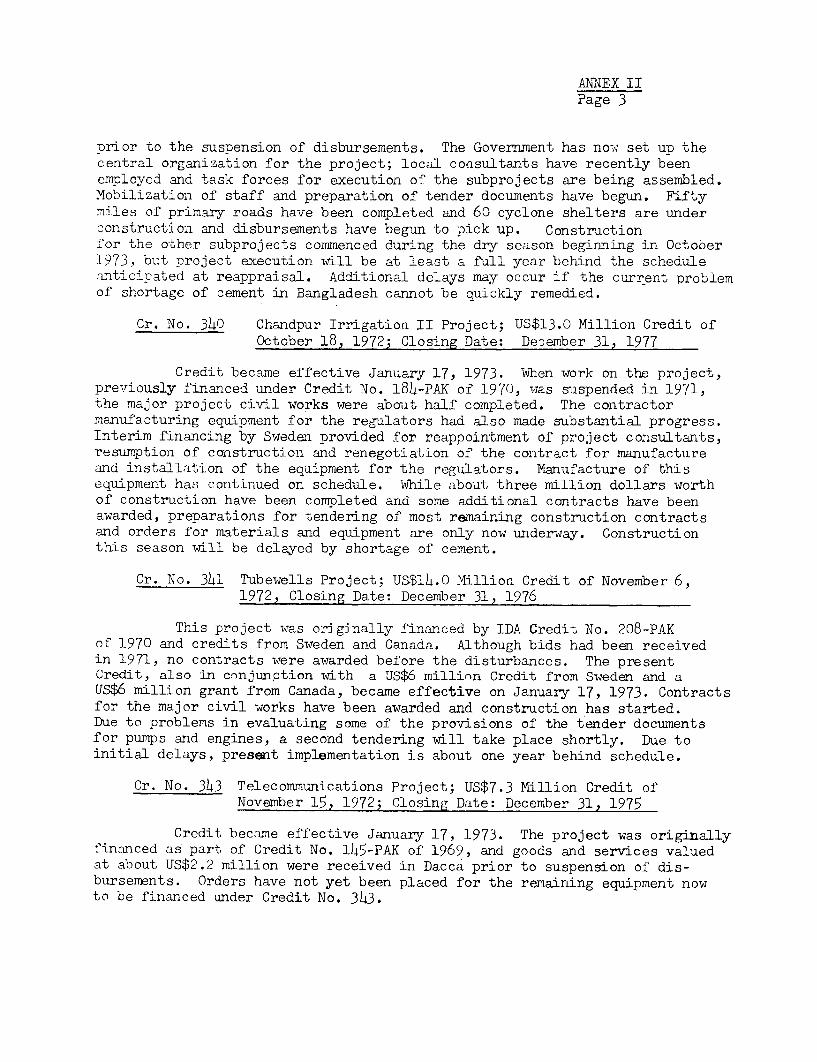

ANNEX IIPage 3

prior to the suspension of disbursements. The Government has now set up thecentral organization for the project; local consultants have recently beenemployed and task forces for execution of the subprojects are being assembled.Mobilization of staff and preparation of tender documents have begun. Fiftymiles of primary roads have been completed and 60 cyclone shelters are underconstruction and disbursements have begun to pick up. Construction-or the other subprojects commenced during the dry season beginning in Octooer1973, but project execution will be at least a full year behind the scheduleanticipated at reappraisal. Additional delays may occur if the current Problemof shortage of cement in Bangladesh cannot be quickly remedied.

Cr. No. 340 Chandpur Irrigation II Project; US$13.0 Million Credit ofOctober 18, 1972; Closing Date: December 31, 1977

Credit became effective January 17, 1973. WAhen work on the project,previously financed under Credit No. 184-PAK of 1970, was suspended in 1971,the major project civil works were about half completed. The contractormanufacturing equipment for the regulators had also made substantial progress.Interim financing by Sweden provided for reappointment of project consultants,resumption of construction and renegotiation of the contract for manufactureand installation of the equipment for the regulators. Manufacture of thisequipment has continued on schedule. While about three million dollars worthof construction have been completed and some additional contracts have beenawarded, preparations for tendering of most remaining construction contractsand orders for materials and equipment are only now underway. Constructionthis season will be delayed by shortage of cement.

Cr. No. 341 Tubewells Project; US,$14.0 Million Credit of November 6,1972, Closing Date: December 31, 1976

This project was originally financed by IDA Credit No. 208-PAKof 1970 and credits from Sweden and Canada. Although bids had been receivedin 1971, no contracts were awarded before the disturbances. The presentCredit, also in conjunption with a US$6 million Credit from Sweden and aUS$6 million grant from Canada, became effective on January 17, 1973. Contractsfor the major civil works have been awarded and construction has started.Due to problems in evaluating some of the provisions of the tender documentsfor pumps and engines, a second tendering will take place shortly. Due toinitial delays, present implementation is about one year behind schedule.

Cr. No. 343 Telecommunications Project; US$7.3 Million Credit ofNovember 15, 1972; Closing Date: December 31, 1975

Credit became effective January 17, 1973. The project was originallyfinanced as part of Credit No. 145-PAK of 1969, and goods and services valuedat about US$2.2 million were received in Dacca prior to suspension of dis-bursements. Orders have not yet been placed for the remaining equipment nowto be financed under Credit No. 343.

ANNEX IIPage 4

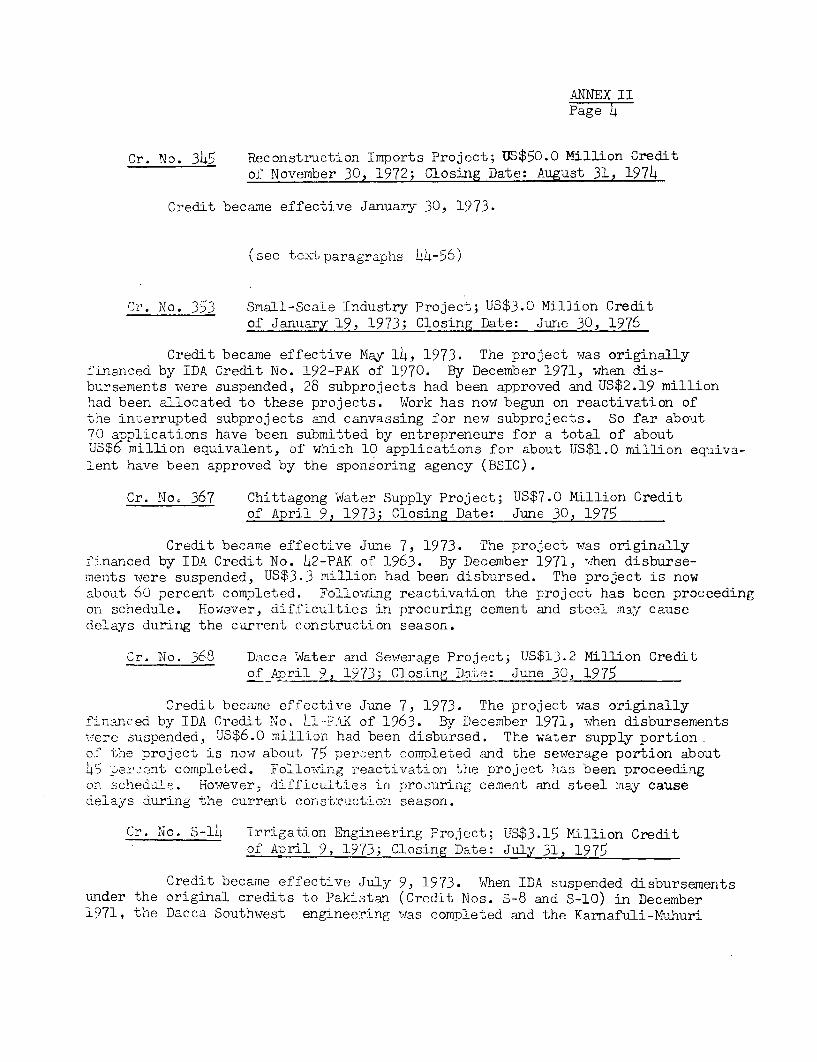

Cr. No. 345 Reconstruction Imports Project; US$50.0 Million Creditof November 30, 1972; Closing Date: August 31, 1974

Credit became effective January 30, 1973.

(see text paragraphs 4)4-56)

Cr. No. 353 Small-Scale Industry Project; US$3.0 Million Creditof January 19, 1973; Closing Date: June 30, 1976