Embed Size (px)

Citation preview

Page 1

JAYPEE CEMENT

ALLAHABAD

Summer Internship Report On

MAPPING THE EFFECTIVENESS OF SALES AND

DISTRIBUTION CHANNEL OF JAYPEE CEMENT

Internship Report submitted as a partial requirement for the award of the two year

Master of Business Administration Program

Name: Chandra Prakash Singh

MBA 2014-16

Telephone: 9907841175

E-mail: [email protected]

Industry Supervisor

Name: Mr. S.K.P.Gupta

ALLAHABAD (Senior GM-Marketing)

Page 2

Industry Guide

Name: Mr. Janmajay Pandey & ArpitTiwari

(Salles Manager)

Start Date for Internship: 20-05-2015

End Date for Internship: 10-07-2015

Page 3

DECLARATION

I am Chandra Prakash Singh student of MBA course of Master of Business

Administration Motilal Nehru National Institute of Technology Allahabad. I hereby declared

that project report titled "Mapping the effectiveness of sales and distribution

channel of JayPee Cement" Is an original and unpublished work done in Jaypee

Allahabad Area.

Whatever I have given information in. this report that is only for support

of my project report and all information given by me are true and genuine.

I hereby declared that all the information is based on best of my

knowledge and no one had submitted this report previously for any Degree.

Guided By: Submitted To:

Janmajay Pandey General Manager –Training

Arpit Tiwari Jaypeenagar, Rewa (M.P.)

Submitted By :

Chandra Prakash Singh

M.B.A

(MNNIT Allahabad)

Page 4

ACKNOWLEDGEMENT

It is great pleasure for me to acknowledge the assistance, guidance &

supervision accorded to me by Mr. Arpit Tiwari. Their patience and strict, vigilant,

& critical supervision made this work what it is. All my efforts would be immortal

without delivering words of sincere gratitude to these honorable & eminent

personalities.

I wish to express my sincere thanks to my classmates, friend & other

members of the Department of Business Administration who directly or indirectly

helped & supported me during my research work.

I would also like to thank Prof. Geetika Goel Mam HOD SMS, Motilal

Nehru National Institute of Technology Allahabad & all the faculty members of

my department for their effort of constant co-operation, which have been a

significant factor in the accomplishment of my summer Project Report.

Chandra Prakash Singh

(M.B.A.)

Page 5

EXECUTIVE SUMMARY

While going training with Jaiprakash associates during my summer training period of 45 days, I

have come to learn lots of thing about marketing, marketing strategy of JP Cement Company,

supply chain management of JP Cement and distribution channel of JP Cement. From company I

get to learn that marketing is "Marketing is getting the right product or service in the right

quantity, to the right place, at the right time and making a profit in the process".

The Jaypee Group is a conglomerate based in Noida, India. It was founded by Jaiprakash

Gaur which is involved in well diversified infrastructure conglomerate with business interests in

Engineering & Construction, Power, Cement, Real Estate, Hospitality, Expressways, IT, Sports

& Education (not-for-profit).

After getting the opportunity to undergo my 45 days summer training in Jayprakash associates

Ltd. I carried my project on “Mapping the effectiveness of sales and distribution channel of

JP Cement”.

The first week of my training I started in getting knowledge about company profile, got the

product knowledge from the company’s marketing department, the sales and distribution

channel, and the process of making retailer, sub dealer and dealers of JP Cement.

After that I spent time on understanding the sales and pricing process of JP Cement, the existing

distribution network of JP Cement in Allahabad segmented market (area wise segmented).

My project is on mapping the effectiveness of sales and distribution channel of JP Cement, so to

find out up to which level the channel is effectively satisfying the market need and demand.

Page 6

CONTENTS

Declaration

Acknowledgement

Executive Summary

Chapter 1 Introduction of topic 07-25

Chapter 2 Company Profile 26-33

Chapter 3 Research Methodology 34-37

Chapter 4 Data Analysis & Interpretation 38-46

Chapter 5 Limitations, Recommendation,

Possible Advertisement method 47-50

Chapter 6 Findings and Conclusion 50-55

Bibliography

Annexure

Page 7

Chapter -1 Introduction to the Title

Page 8

Introduction to the Title

Today it is fashionable to talk about the new economy. We hear that the business are operating in

globalize economy, things are moving at a nano second pace our market are characterized by

hyper competition and disruptive technologies are challenging every business and so business

must adopt to empower consumer.

To become successful in such a competitive environment the business organizations have to be

customer oriented. Customers need and want must be taken care off. Customer must be

delighted. This information about the market could be collected by the way of proper market

survey.From the market survey we get the feed about the good or services of the organization.

For this purpose the said project work is undertaken.

The project was carried out for knowing prevailing market condition of jaypee cement in

Allahabad region. The second object of the project was to study the market share activities

undertaken by jaypee and its other competitors.

The project was carried out in the market of Allahabad of U.P state. There are 5 market players

in cement industry .They are jaypee, Prism, Satna, ACC and Birla Gold from these they are few

local brands selling in the market.

The information about the market was gathered by visiting retailers in the market. Interview of

retailers was taken depending upon their accessibility.

While doing the project attempt was made to collect maximum information about the maker. To

get actual and correct information, it was not told retailers that the survey is conducted by

JAYPEE cement for the obvious reasons. Numbers of retailers were visited to get the actual

picture of the market .Again the retailers of each grade were visited, to get each and every detail

about the market.

Most of the time was spent in travelling for the retailer were reluctant to give the information, as

they do not want to disclose their business details. Visit to such retailers were loss of time,

money and energy.

After collecting the detailed information about the maker analysis is done. In the analysis, the

observations recorded during the project were carefully analyzed and the results are prepared.

The findings are results of the project work are given at the later stage in the report.

Page 9

Objective of the project

The project was undertaken for two main objectives was

To carry out market survey of prevailing market condition of JAYPEE CEMENT ltd. in

Allahabad.

The second object was

To study the sales and promotion activities, undertaken by Jaypee cement and other

player in the market.

To attain these two objectives various other sub objective are needed to be achieved,

These are listed below:-

To analyze the market shares of Jaypee cement in Allahabad.

To know the customers preference for the brands of cement.

To know the preference of retailer for shorting different brands of cement.

To understand the effectiveness of various sales promotion activities of cement.

To know preference of retailers for different gift and incentives.

To analyze the sales promotion activities of various brands.

To analyze the transportation facilities of Jaypee and other cement companies.

To analyze the frequency of visits of marketing representative of various companies.

Thus it attempt to find ways to increase market share, to increase customer satisfaction and thus

increase the business prospects.

Page 10

Scope of study

The study has been done for the cement so more or less it helps in understanding the consumer

preference towards the cement market.

The study can help in analyzing certain weak point, improving on which a company can

overcome the low sales of its cement .

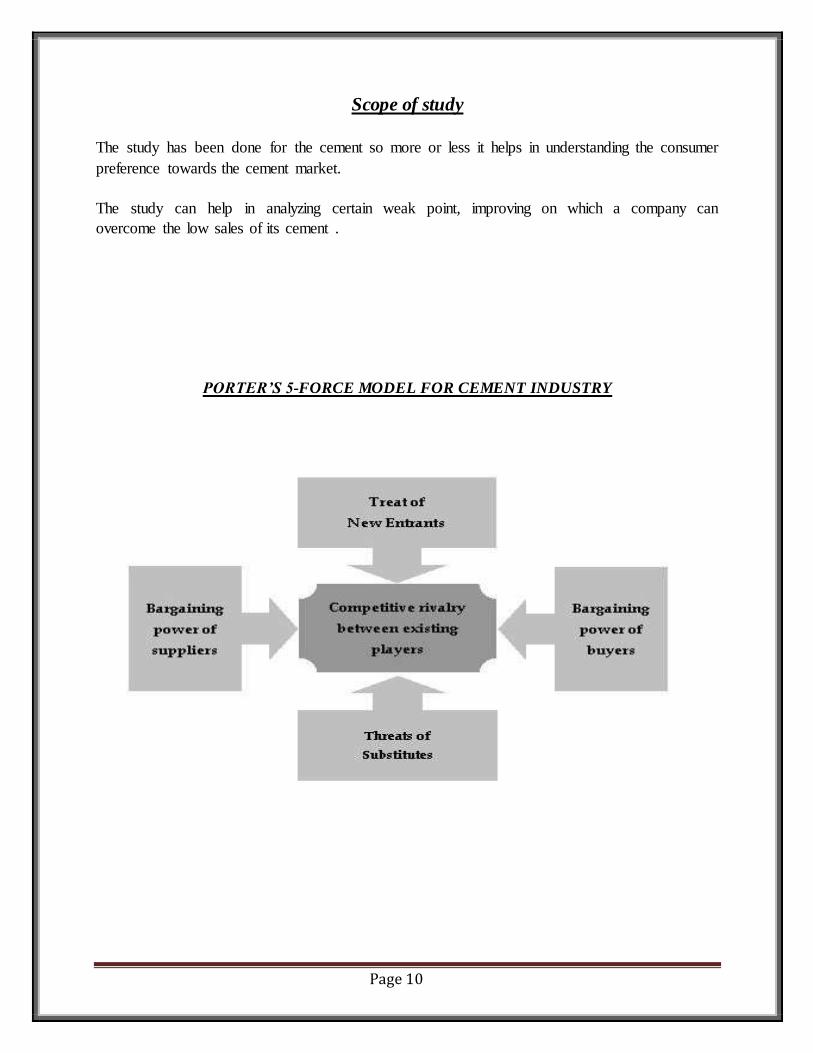

PORTER’S 5-FORCE MODEL FOR CEMENT INDUSTRY

Page 11

Threat of New Entrants:

The high capital costs acts as a major entry barrier for the entry of new players. The high freight

costs make it difficult to import cement. Cement being a high volume low value commodity

results in high freight costs, which makes cement imports economically unfeasible. Domestic

Cement industry is highly insulated from global cement markets. With Go intervention, making

cement duty free, cement is being imported from neighboring countries. However, due to

logistics issues and lack of port handling capabilities, imports of cement will remain negligible

and do not pose a threat to domestic industry.

Bargaining power of Suppliers:

The major inputs are coal and power. The Prices of both coal and power are determined by the

government. To mitigate the high costs of power the cement players have set up captive power

plants.

Competitive rivalry between existing players:

Previously the rivalry was strong among the players, as the industry was not consolidated.

During the last few years the industry has become more consolidated with the Top 3 players

having a combined market share of 49 percent in 2005-06 as compared to 32percent in 1999-

2000.

Bargaining power of Buyers:

Retail sales constitute about 80 percent of the total sales and the rest is institutional sales. The

retail buyers don’t have any bargaining power while the institutional buyers get a discount of 5 to

10 percent as they buy cement in bulk.

Threat of Substitutes:

There are no good substitutes for cement.

Page 12

INTRODUCTION

INDIAN CEMENT INDUSTRY-AN OVERVIEW

Cement production commenced in India as early as 1914. The first cement unit was set up at

Porbandar in 1914 with a capacity of 1,000 tons per annum. Cement is the preferred building

material in India. It is used extensively in household and industrial construction. Earlier,

government sector used to consume over 50% of the total cement sold in India, but in the last

decade, its share has come down to 35%. Rural areas consume less than 23% of the total cement.

Availability of cheaper building materials for non-permanent structures affects the rural demand.

Demand for cement is linked to the economic activity in any country. Broadly, it can be

categorized into demand for housing construction (homes, offices etc.) and infrastructure

creation (ports, roads, power plants etc). The real driver of cement demand is creation of

infrastructure; hence cement demand in emerging economies is much higher than developed

countries where the demand has reached a plateau. In India too, the demand for cement will be

affected by spending on infrastructure (including housing).

With the boost given by the government to various infrastructure projects, road network and

housing facilities, growth in the cement consumption is anticipated in the coming year. The

increase in infrastructure projects by the government coupled with the construction of the Golden

Quadrilateral and the North-South and East-West corridor projects have led to an increase in

consumption of cement. This increase is expected to continue in the future. The reduction in

import duties is not likely to affect the industry as the cement produced is at par with the

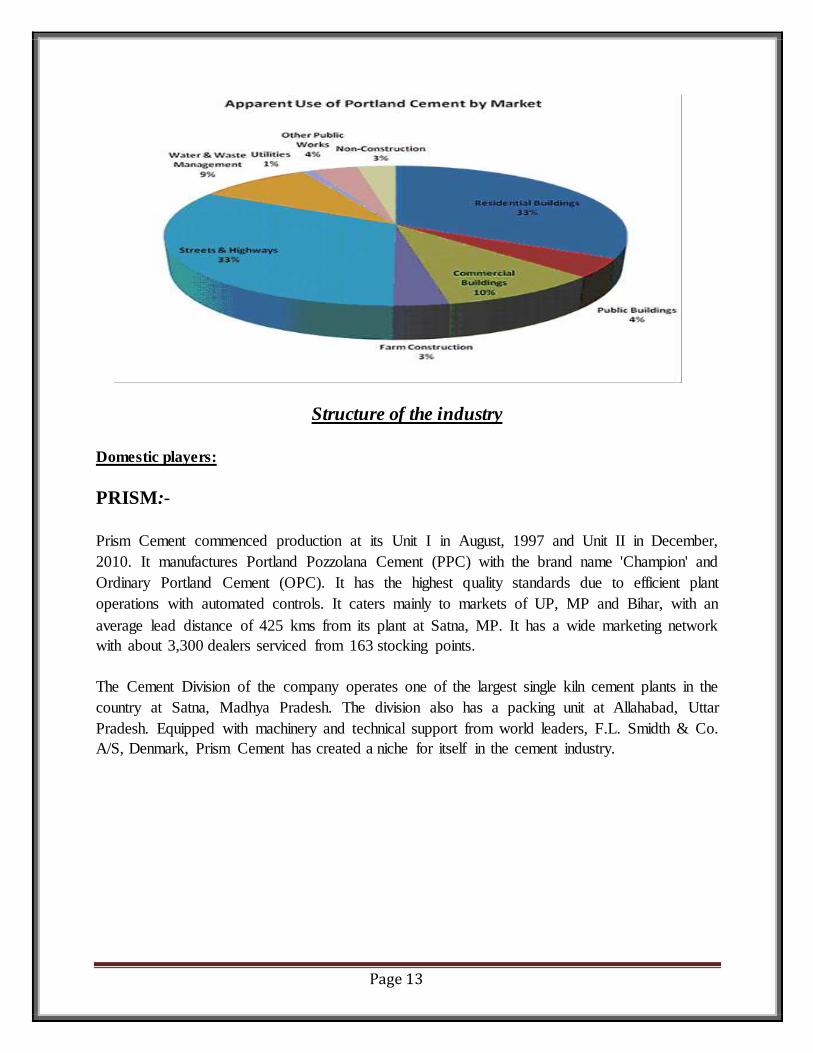

international standards and the prices are lower than those prevailing in international markets.

The graph below shows the consumption of cement in different areas of housing, infrastructure

and industries.

Page 13

Structure of the industry

Domestic players:

PRISM:-

Prism Cement commenced production at its Unit I in August, 1997 and Unit II in December,

2010. It manufactures Portland Pozzolana Cement (PPC) with the brand name 'Champion' and

Ordinary Portland Cement (OPC). It has the highest quality standards due to efficient plant

operations with automated controls. It caters mainly to markets of UP, MP and Bihar, with an

average lead distance of 425 kms from its plant at Satna, MP. It has a wide marketing network

with about 3,300 dealers serviced from 163 stocking points.

The Cement Division of the company operates one of the largest single kiln cement plants in the

country at Satna, Madhya Pradesh. The division also has a packing unit at Allahabad, Uttar

Pradesh. Equipped with machinery and technical support from world leaders, F.L. Smidth & Co.

A/S, Denmark, Prism Cement has created a niche for itself in the cement industry.

Page 14

Birla Corp:-

Birla Corp's product portfolio includes acetylene gas, auto trim parts, casting, cement, jute

goods, yarn, calcium carbide etc. The cement division has an installed capacity of 4.78 million

metric tones and produced 4.77 million metric tones of cement in 2003-04. The company has

two plants in Madhya Pradesh and Rajasthan and one each in West Bengal and Uttar Pradesh

and holds a market share of 4.1 per cent. It manufactures Ordinary Portland cement (OPC),

Portland pozzolana cement, fly ash-based PPC, Low-alkali Portland cement, Portland slag

cement, low heat cement and sulphate resistant cement. Large quantities of its cement are

exported to Nepal and Bangladesh. Going forward, the company is setting up its captive power

plant to remain cost competitive.

ACC:-

ACC Limited is India’s foremost manufacturer of cement and ready mixed concrete with a

countrywide network of factories and sales offices. Established in 1936, ACC is acknowledged

as a pioneer and trendsetter in cement and concrete technology. Among the first companies in

India to include environment protection as a corporate commitment, ACC regularly wins

accolades for best practices in environment management at its plants and mines, and for

demonstrating good corporate citizenship.

ACC Limited (Formerly The Associated Cement Companies Limited) one of the largest

producers of cement in India. It's registered office is called Cement House. It is located on

Maharishi Karve Road, Mumbai. The stock price of company contributes in calculating BSE

Sensex.

The management control of company was taken over by Swiss cement major Holcim in 2004.

On 1 September 2006 the name of The Associated Cement Companies Limited was changed to

ACC Limited. The company is only Cement Company to get Super brand status in India.

Jaiprakash Associates Limited:-

Jaiprakash Industries, now known as Jaiprakash Associates Limited (JAL) is part of the

JAYPEE Group with businesses in civil engineering, hospitality, cement, hydropower, design

consultancy and IT. It has an annual capacity of 4.6 million tonne with plants located in Rewa &

Bela (Madhya Pradesh) and Sadva Khurd (Uttar Pradesh). The company has a market share of

3.8 percent with the cement division contributing US$ 172 million to revenue in 2003-04. The

company is upgrading its capacity to 6.5 million tonne through the modernizing of the existing

units and the commissioning of a new grinding unit at Tanda (Uttar Pradesh) with an

Page 15

investment of US$ 163 million. Jaiprakash Associates has decided to concentrate on its core

business of construction and engineering and leave its cement plant to its subsidiary Jaypee

Rewa Cement Ltd. The company manufactures a widerange of world class cement of OPC

grades 33, 43, 53, IRST-40 and special Blends of pozzolana cement.

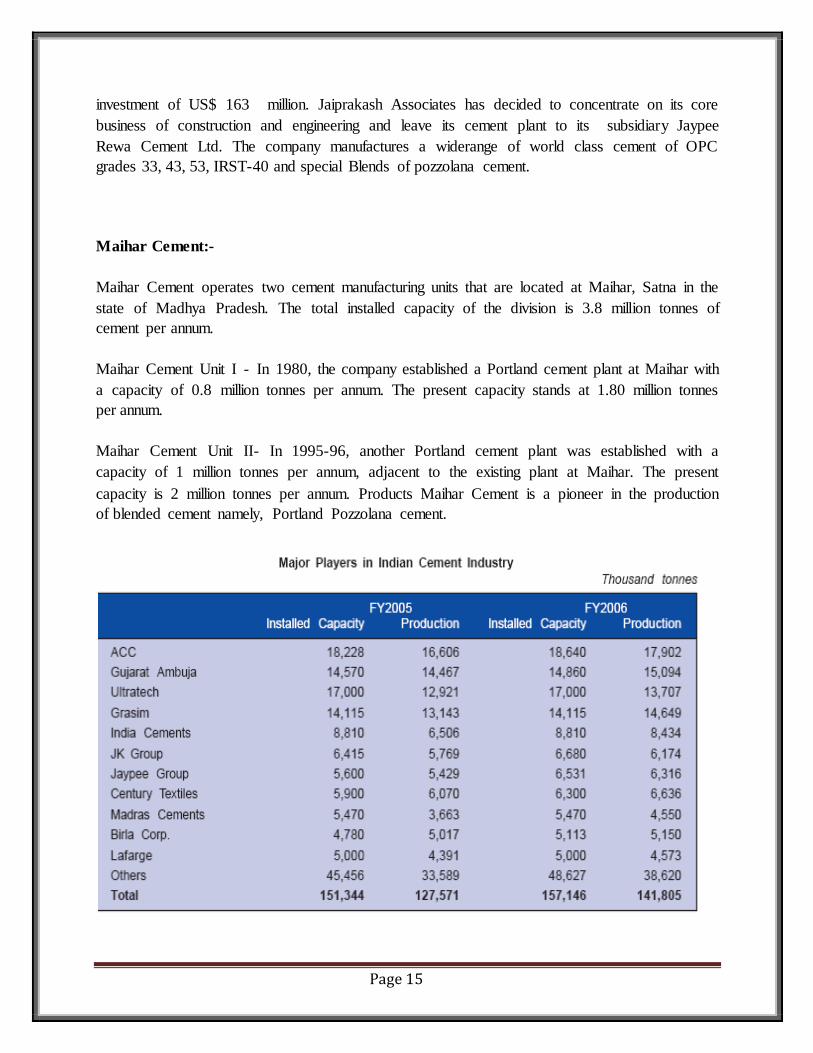

Maihar Cement:-

Maihar Cement operates two cement manufacturing units that are located at Maihar, Satna in the

state of Madhya Pradesh. The total installed capacity of the division is 3.8 million tonnes of

cement per annum.

Maihar Cement Unit I - In 1980, the company established a Portland cement plant at Maihar with

a capacity of 0.8 million tonnes per annum. The present capacity stands at 1.80 million tonnes

per annum.

Maihar Cement Unit II- In 1995-96, another Portland cement plant was established with a

capacity of 1 million tonnes per annum, adjacent to the existing plant at Maihar. The present

capacity is 2 million tonnes per annum. Products Maihar Cement is a pioneer in the production

of blended cement namely, Portland Pozzolana cement.

Page 16

State wise Capacity

As cement is a low value commodity, freight costs assume a significant proportion of the final

cost. Transporting costs render the prices of cement in distant destinations uncompetitive. For

instance, it is financially infeasible to transport cement by road over 250 kms. Railways are

mostly used to transport cement over longer distances. However, its bulky nature and

infrastructure bottlenecks render even rail transport unviable over very long distances.

Therefore, manufacturers tend to sell cement at the nearest market first and sell in distant

markets only if additional realization is greater than freight costs incurred. This is the reason for

showing regional demand rather than state demand in case of cement.

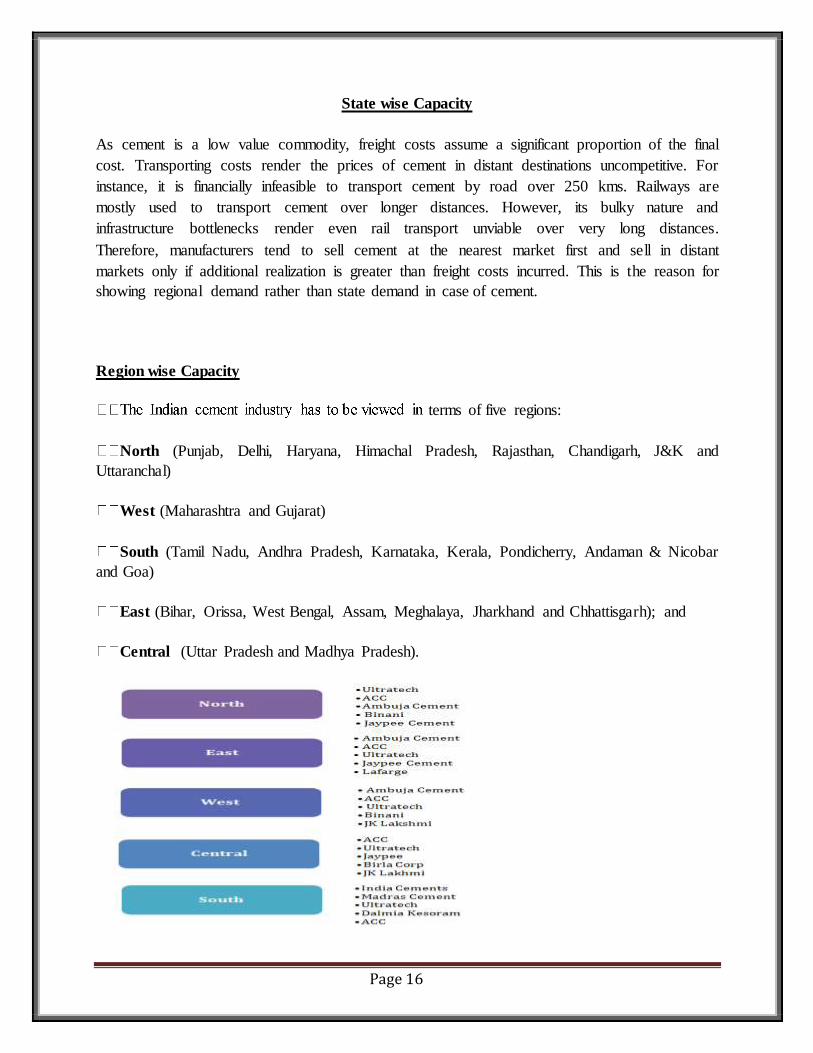

Region wise Capacity

terms of five regions:

North (Punjab, Delhi, Haryana, Himachal Pradesh, Rajasthan, Chandigarh, J&K and

Uttaranchal)

West (Maharashtra and Gujarat)

South (Tamil Nadu, Andhra Pradesh, Karnataka, Kerala, Pondicherry, Andaman & Nicobar

and Goa)

East (Bihar, Orissa, West Bengal, Assam, Meghalaya, Jharkhand and Chhattisgarh); and

Central (Uttar Pradesh and Madhya Pradesh).

Page 17

South accounts for 33.03% of cement production capacity of the country, with Andra Pradesh

accounting for 15.27% of the total production capacity of India. It has an installed capacity of

around 20mn tons of cement and ranks first in the country, followed by Tamil Nadu with 9.94%

of the total production capacity. North accounts for 18.02% of the total production capacity, with

Rajasthan at 12.55% of the total production capacity of the country. West accounts for 16.85% of

the total production capacity. Maharashtra and Gujarat have production capacity of 6.89% and

9.96% respectively. East and Central Regions account for 16.33% and 15.77% of the total

production capacity of the country respectively.

Trade between these regions is on a very low scale mainly because of the transportation

bottlenecks and uncompetitive cost of transportation. The Southern region dominated the cement

consumption at 44.5 mn tonnes in FY 07, accounting for about 30% of total domestic cement

consumption. During FY 03-07, Southern region has witnessed highest CAGR of cement

demand growth at 10.4% followed by Northern and Eastern regions at 8.9% and 9%

respectively.

Mechanics of Distribution Channels of Sector

Companies invariably hire agents or transport cements to own or government warehouses either

via roadway or railways. In case of exports, cement reaches the nearest port via roadways or

railways and is then transferred to the importing country. Domestically, from agents or

warehouses the cement is transported to the dealers/distributors and in turn to sub dealers who

finally sell it to the end users. There may or may not be physical ownership of goods. In the

second case, dealers and sub dealers take order from buyers and place it to the companies, co

ordinate and monitor the timely dispatch of said orders.

ENERGY AND TRANSPORT REQUIREMENTS

The cement industry is dependent on three major infrastructural sectors of the economy: coal,

power and transport. The inputs from these three sectors account for roughly 50% of the cost of

cement. Both the availability and the cost of these inputs have a vital bearing on the fortunes of

the cement players. All these sectors are largely in the State sector, and, historically cement

companies have had virtually no control on the cost or availability of these inputs.

Hence, the industry response has largely been in the form of achieving efficiency gains and

finding alternatives (captive power, use of water ways). One additional external influencer of the

cement industry performance is the taxes and levies imposed by the Central and State

Governments. The shortage in domestic coal production coupled with the poor quality has

resulted in cement companies resorting to importing coal, or going in for open market purchase

of coal, or using alternative fuel such as lignite or pet coke.

Page 18

Use of imported coal has become an essential feature of the Indian cement industry and has

shown a rising trend during the last few years. Power and Fuel cost form the largest proportion of

the cost structure. This reflects the effects of the trend in rising global oil and fuel prices. On the

other hand Employee costs from the smallest proportion of overall cost.

This is essentially because cement industry is a very capital intensive industry. This also

accounts for the huge depreciation and interest costs which accrue on the plant and machinery.

Moreover, the labour employed is essentially semi-skilled excluding the top management which

brings down labour costs.

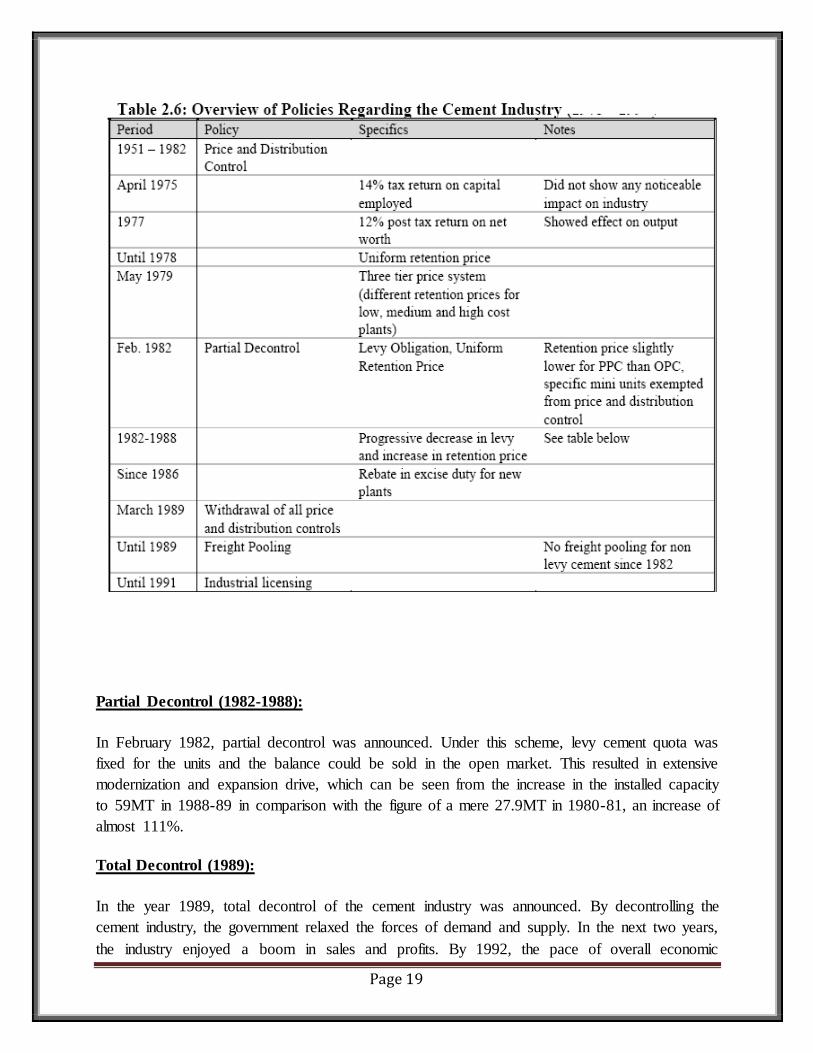

GOVRNMENT POLICIES

Government policies have affected the growth of cement plants in India in various stages. The

control on cement for a long time and then partial decontrol and then total decontrol has

contributed to the gradual opening up of the market for cement producers. The stages of growth

of the cement industry can be best described in the following stages

Price and Distribution Controls (1940-1981):

During the Second World War, cement was declared as an essential commodity under the

Defense of India Rules and was brought under price and distribution controls which resulted in

sluggish growth. The installed capacity reached only 27.9 MT by the year 1980-81.

Page 19

Partial Decontrol (1982-1988):

In February 1982, partial decontrol was announced. Under this scheme, levy cement quota was

fixed for the units and the balance could be sold in the open market. This resulted in extensive

modernization and expansion drive, which can be seen from the increase in the installed capacity

to 59MT in 1988-89 in comparison with the figure of a mere 27.9MT in 1980-81, an increase of

almost 111%.

Total Decontrol (1989):

In the year 1989, total decontrol of the cement industry was announced. By decontrolling the

cement industry, the government relaxed the forces of demand and supply. In the next two years,

the industry enjoyed a boom in sales and profits. By 1992, the pace of overall economic

Page 20

liberalization had peaked; ironically, however, the economy slipped into recession taking the

cement industry down with it. For 1992-93, the industry remained stagnant with no addition to

existing capacity. The things that primarily control the price of cement are coal, power tariffs,

railway, freight, royalty and cess on limestone. Interestingly, all of these prices are controlled

by government.

Coal:

The consumption of coal in a typically dry process system ranges from 20- 25% of clinker

production. This means for per ton clinker produced 0.20- 0.25 ton of coal is consumed. This

contributes 35-40% of the production cost. The cement industry consumes about 10mn tons of

coal annually. Since coalfields like BCCL supply a poor quality of coal, NCL and CCL the

industry has to blend high-grade coal with it. The Indian coal has a low calorific value (3,500-

4,000 kcal/kg) with ash content as high as 25-30% compared to imported coal of high calorific

value (7,000-8,000 kcal/kg) with low ash content 6-7.

Electricity:

Cement industry consumes about 5.5bn units of electricity annually while one ton of cement

approximately requires 120-130 units of electricity. Power tariffs vary according to the location

of the plant and on the production process.

The state governments supply this input and hence plants indifferent states shall have different

power tariffs. Another major hindrance to the industry is severe power cuts. Most of the cement

producing states like AP, MP, experience power cuts to the tune of 25-30% every year causing

substantial production loss.

Limestone:

This constitutes the largest bulk in terms of input to cement. For producing one ton of cement,

approximately 1.6 ton of limestone is required. Therefore, the cement plant location is

determined by the location of limestone mines. The major cash outflow takes place in way of

royalty payment to the central government and cess on royalties levied by the state government.

The total limestone deposit in the country is estimated to be 90 billion tons. AP has the largest

share -- 34%, Karnataka 13% Gujarat 13%, M.P 8%, and Rajasthan 6.5%. The plants near the

limestone deposit pay less Transportation cost than others.

Page 21

Transportation:

Cement is mostly packed in paper bags now. It is then transported either by rail or road. Road

transportation beyond 200 kms is not economical therefore about 55% cement is being moved by

the railways. There is also the problem of inadequate availability of wagons especially on

western railways and southeastern railways. Under this scenario, manufacturers are looking for

sea routes, this being not only cheap but also reducing the losses in transit. Today, 70% of the

cement movement worldwide is by sea compared to 1% in India. However, the scenario is

changing with most of the big players like L&T, ACC and OCL having set up their bulk

terminals

Incentives in States:

Most state governments, in order to attract investments in their respective states, offer fiscal

incentives in the form of sales tax exemptions/deferrals. In some states, this applies only to

intrastate sales, like Madhya Pradesh and Rajasthan. States like Haryana offer a freeze on power

tariff for 5 years, while Gujarat offers exemption from electric duty.

Opening up the FDI channel:

The impact of government policies on cement demand has been steadily decreasing with the

sector being gradually deregulated. At present , 100 per cent foreign direct investment (FDI) is

permitted in the cement industry. Lafarge was the first foreign company toenter the Indian

market in 1999.

Declining Role of Public Sector:

Historically, cement has been one of the most important areas of operations for the Indian private

sector. Unlike much of heavy industry and utilities, cement was not deemed to be the exclusive

preserve of the State sector in the post-independence development strategy. Cement was also the

industry of choice of many corporate diversifying away from the troubled traditional areas of jute

and textiles. Over the years, the share of the public sector in cement production has declined.

While the private sector (large companies) accounts for around 95% of the total installed

capacity, the share of public sector companies has declined from a level of 11% in FY1996 to

around 4.4% in FY2006. The share in production of the public sector companies is even lower at

1.2% in FY2006 as compared to 6.5% in FY1996.

Page 22

Export of cement from India

The Indian cement industry exported around 6 mt of cement during FY2006, accounting for

around 4% of the total production. There has been a significant year on year variation in the

export trend, implying that Companies rely on cement exports to balance out the domestic

demand supply situation. As seen from above there is excess production, so the difference in

supply and demand is met by exporting. The export of Indian cement has increased over the

years, giving a boost to the Indian cement industry. The demand for cement in the foreign

countries is a derived demand, for it depends on industrial activity, real estate, and construction

activity. Since growth is taking place all over the world in these sectors, Indian export of cement

is also increasing.

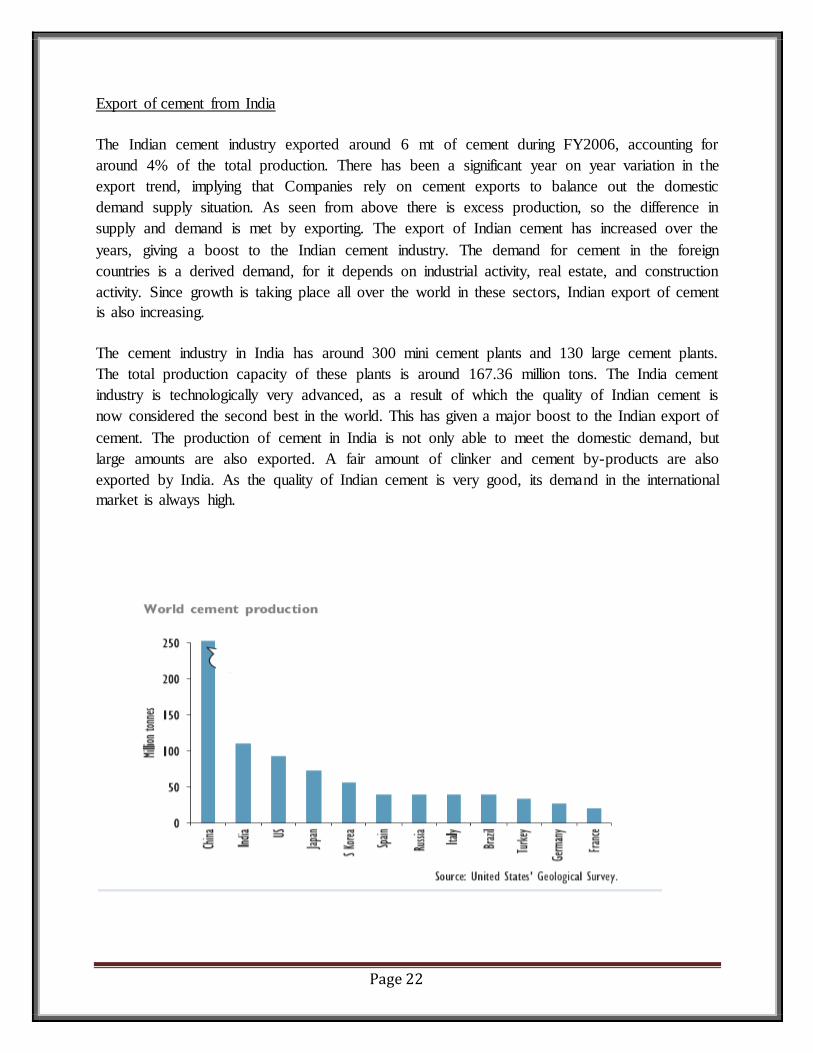

The cement industry in India has around 300 mini cement plants and 130 large cement plants.

The total production capacity of these plants is around 167.36 million tons. The India cement

industry is technologically very advanced, as a result of which the quality of Indian cement is

now considered the second best in the world. This has given a major boost to the Indian export of

cement. The production of cement in India is not only able to meet the domestic demand, but

large amounts are also exported. A fair amount of clinker and cement by-products are also

exported by India. As the quality of Indian cement is very good, its demand in the international

market is always high.

Page 23

The graph shows that the production of cement in India is at 2nd place after China, this higher

production is a good reason for exporting cement.

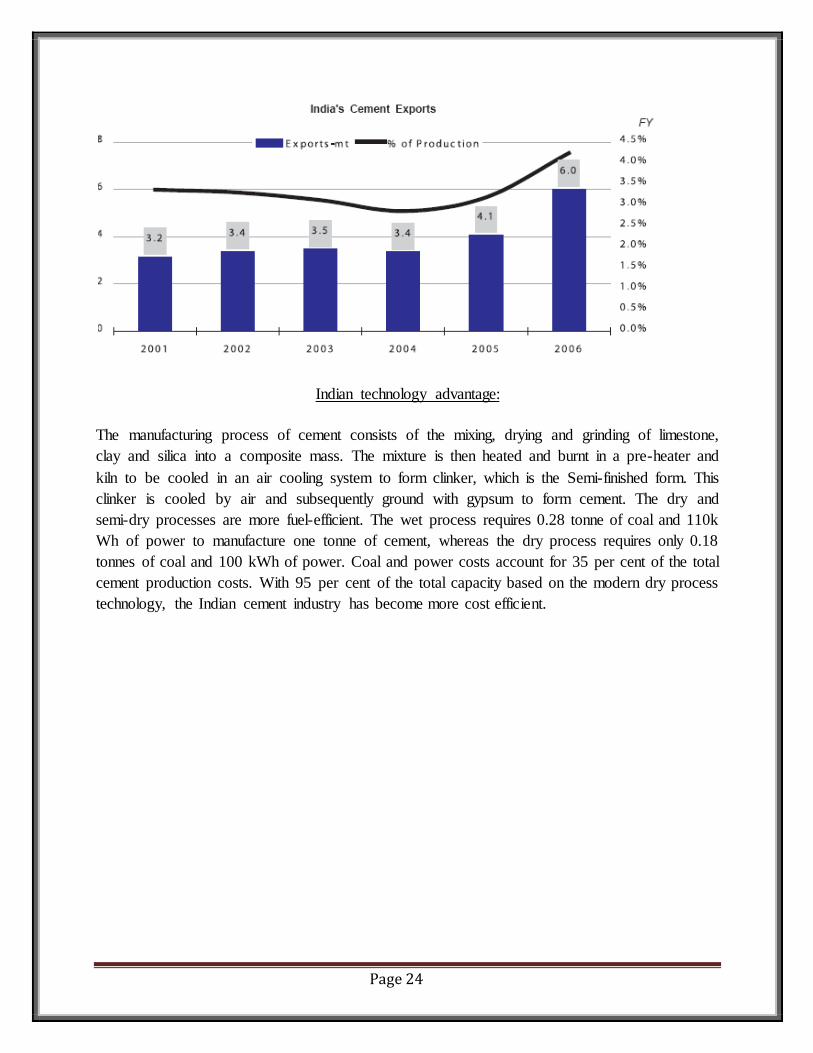

In 2001-2002, 3.38 million tons of cement was exported from India. That figure stood at 3.47

million tons in 2002-03, and 3.36 million tons in 2003- 04. In 2001-2002, 1.76 million tons of

clinker was exported from India.

In 2002- 2003 clinker exports amounted to 3.45 million tons, and in 2003- 2004 the figure stood

at 5.64 million tons. This shows that the export of Indian cement has been increasing at a steady

pace over the years.

The major companies exporting Indian cement are:

Export of Indian cement has registered growth a fair amount of growth, giving a boost to the

Indian economy. India has an immense potential to tap cement markets of countries in the

Middle East and South East Asia due to its strengths of location advantage, large-scale limestone

and coal deposits, Adequate cement capacity and world-class cement production, with the latest

technology. India has an estimated total of 90 billion tonnes of limestone deposit in the country.

Page 24

Indian technology advantage:

The manufacturing process of cement consists of the mixing, drying and grinding of limestone,

clay and silica into a composite mass. The mixture is then heated and burnt in a pre-heater and

kiln to be cooled in an air cooling system to form clinker, which is the Semi-finished form. This

clinker is cooled by air and subsequently ground with gypsum to form cement. The dry and

semi-dry processes are more fuel-efficient. The wet process requires 0.28 tonne of coal and 110k

Wh of power to manufacture one tonne of cement, whereas the dry process requires only 0.18

tonnes of coal and 100 kWh of power. Coal and power costs account for 35 per cent of the total

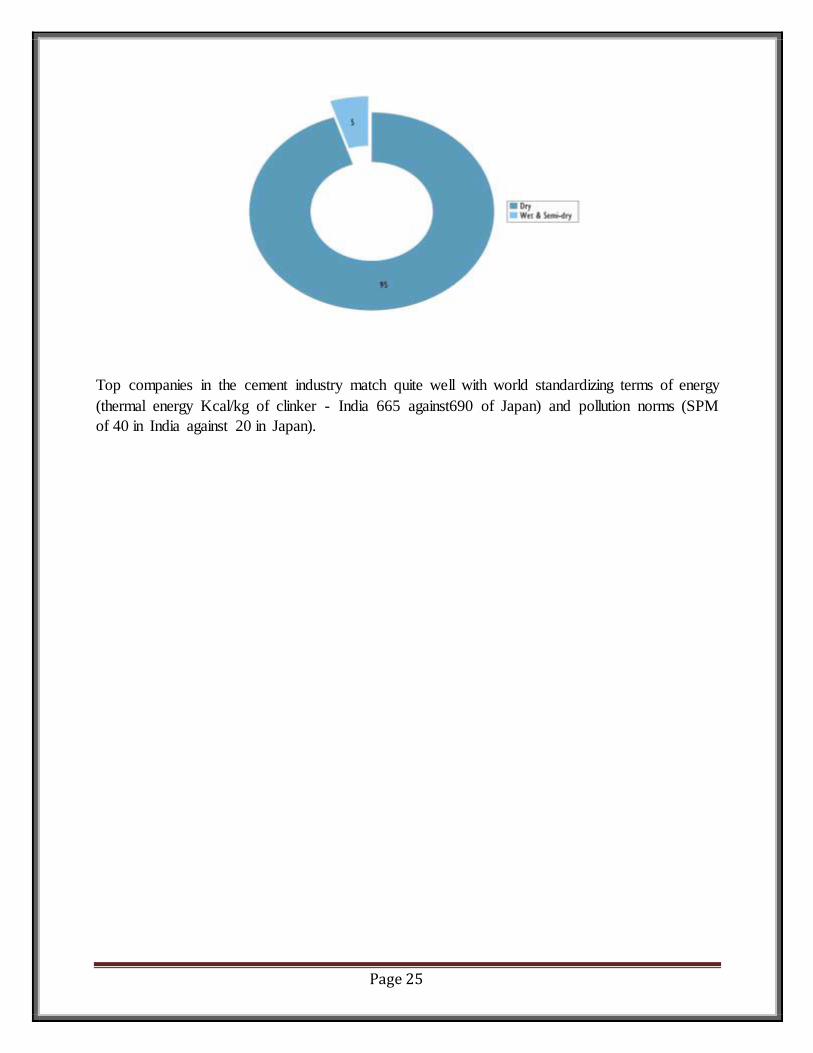

cement production costs. With 95 per cent of the total capacity based on the modern dry process

technology, the Indian cement industry has become more cost efficient.

Page 25

Top companies in the cement industry match quite well with world standardizing terms of energy

(thermal energy Kcal/kg of clinker - India 665 against690 of Japan) and pollution norms (SPM

of 40 in India against 20 in Japan).

Page 26

Chapter 2

Company

Profile

Page 27

JAYPEE CEMENT INTRODUCTION

Jaiprakash Associates Limited is the flagship company of Jaypee Group & is one of the

cement producer in the country. Its cement division currently operates modern,

computerized process control cement plants with an aggregate capacity of 28.80 MTPA.

The company is in the midst of capacity expansion of its cement business and is slated to be

a 41.40 MTPA cement producer by the year 2013 with Captive Thermal Power plants

totaling 672 MW.

The Jaypee group is the 3rd largest cement producer in the country. The group's cement facilities

are located in the Satna Cluster (U.P), which has one of the highest cement production growth

rates in India.

The group produces special blend of Portland Pozzolana Cement under the brand name ‘Jaypee

Cement’ (PPC). Its Cement Division currently operates modern, computerized process control

cement plants with an aggregate capacity of 28.8 MTPA. The company is in the midst of

capacity expansion of its cement business in Northern, Southern, Central, Eastern and Western

parts of the country and is slated to be 41.40 MTPA cement producer by 2013 with

Captive Thermal Power Plants totaling 672MW.

JAYPEE PRODUCTION UNITS:

The Cement Division of the Jaypee Group has10 state-of-the-art, fully computerized

integrated Cement Plants(ICPs),6 Grinding Units & 2 Blending Units with an aggregate

capacity of 28.46 millions tonnes per annum(MTPA) at present. The Group is in the process of

setting up new capacities across the nation and is targeting a capacity of 37.55

MTPAby 2012.alongwith Captive Thermal Power Plants(CPPs) totalling 702MW.Once the

expansion plans have been implemented, the Group will have 12 ICPs supported by 702

MW of captive thermal power, 9split location plants, 11Railway sidings and a jetty, giving

the former a pan-India presence in cement sector.

Page 28

Page 29

JAYPEE CEMENT ADVANTAGE

JAYPEE Cement Ltd is one of the l premium quality cement producer in India. JAYPEE Cement

is manufactured in the state of the art dry process plant at BAGA (H.P) and grinding unit at

Bagheri (H.P). Advanced instrumentation systems, computerized process control and online

quality control through X-ray ensure consistently high quality product at Himachal Jaypee

Cement plant. The quality of Jaypee Cement has been globally accepted and is India's largest

exporter of clinker and cement.

JAYPEE Cement due to its consistently superior quality has become the first choice amongst

discerning users and construction professionals.

Raw Material:

Careful selection and scientific proportioning of raw material with the use of latest technology

enables manufacturing of high quality cement. Rigorous hourly tests are conducted on raw

material. Laboratories at all plants are equipped with sophisticated facilities.World Class process

Technology ensures Quality and Consistency:

Quality Assurance is an integral part of Jaypee’s manufacturing Philosophy. The quality

attributes are consistently ensured through rigorous application of advanced technology. Key

features include:

careful selection of other raw material

limestone

QCX (Quality Control through X-ray)

CCR (Computerized Control Room)

-quality clinkerisation and close-circuit grinding for optimum particle size distribution

Jaypee Cement plants have been accredited with ISO 9001, 14001, 18001 Certifications by DNV

of Netherlands.

Page 30

Distinct Features:

h

-level of Chloride

-soundness

Advantages:

Customer Care and Guidance:

Jaypee Cement offers customers a range of "product plus" services. A full- fledged Technical

Services Network has been set up exclusively for technical advice and guidance in usage of

cement

Jaypee Cement is marketed nationwide through large network of stockist's, sales officers and

representatives. Cement dumps have also been established at strategic locations to facilitate

faster delivery of cement.

Page 31

Value Added Services:

rvices (Concrete cube testing facilities)

Construction practices

Material and construction

-destructive testing of concrete

Applications:

1. All Kinds of constructions including precast and pre stressed concrete, masonry works

2. Slip form constructions

3. Rehabilitation and retrofitting works

4. Cement based products such as pipes, tiles, blocks, poles,etc.

5. Roads, runways, bridges and flyovers

6. Water retaining structures

Page 32

Jaypee Rewa Plant

Unit-I: It was commissioned in 1988 with a capacity of 1.0 million MT.

Unit – II: It was commissioned in 1991 with a capacity of 1.5 million MT.

Japee Rewa Cement Unit-I was fully engineered by Holtec Engineer’s Pvt. Ltd. and for Jaypee

Rewa Cement Unit-II, the engineering and consultancy services were provided jointly by Holtec

Engineers and Holder bank management and consulting ltd. Switzerland. The choice of

machinery from equipment manufactures of world reputed and the extent of sophistication and

modernity incorporated – in the cement plant reflect the concern of the management to

customers. The JAYPEE REWA plant with two units has a capacity of 3 MTPA and grinding &

blending units of 1.6 MTPA are in Uttar Pradesh.

Jaypee Rewa Plant, Rewa (M.P.)

Page 33

AWARDS BY JAYPEE CEMENT

Cement Division of Jaiprakash Associates Limited with its Plants at Jaypee

Rewa Plant (JRP), Jaypee Bela Plant (JBP), JAAGO & JCBU has been

awarded the Integrated Management System comprising of ISO-9001:2000,

Rewa Plant, Jaypee

Bela Plant,

ISO-14001:2004 & OHSAS-18001:1999 by the world renowned Bureau Veritas Certification. ISO-

9001:2000 covers Quality Management System. ISO-14001:2004 covers all Environmental Issues

including conservation of Natural Resources and Reduction of Emissions and Wastes. OHSAS-

18001:1999 covers Operational Safety and reduces Risk to People, Plant & Machinery.

Page 34

Chapter 3

Research Methodology

Objective of the

study

Page 35

RESEARCH METHODOLOGY

The research methodology is the way systematically solve the systematically solve the research

problems. The main objective of the product was to know the market condition of Jaypee

Cement to study the sales promotion activities undertaken by various cement companies. For

this, right at the beginning the research plan was prepared. This includes all the detail of how to

go about research work of Jaypee Cement.

RESEARCH PLAN

Definition of research problem, The research problem can be defined as follows:-

1. What are the cement being used by various customer in the region of Allahabad and what are

their expectation from the cement.

2. What the market trend is of cement and brand awareness of jaypee Cement.

DATA COLLECTION

The descriptive nature of research necessitates collection of primary data from retailers through

market survey, personal interview technique was used and interviews were conducted through

structured questionnaire the questions were asked in prearranged manner. The market research

was conducted over a period of 45 days. Data was tabulated, analyzed and suggestion and

recommendation were given.

RESEARCH INSTRUMENTATS

The Research instrument chosen for conducting the survey was structured questionnaire was

prepared as show as in the annexure. The questionnaire includes open ended as well as close

ended question, few open ended question were included to obtain the perception of the retailers.

The questionnaire designed and a pilot survey was made with the questionnaire and then changes

were made accordingly with the questionnaire.

SAMPLE PLAN

Page 36

A sampling technique was chosen for the study was Random Sampling Technique. This is the

most common method of selecting the sample. This is because the retailers are localized

indifferent part of the marker a group of retailers are chosen are random from large group. It

gives all retailers in a group and equal chance of being selected for the purpose of the survey.

SAMPLE SIZE

Out of nearly 250 retailers in cement market of Allahabad region around randomly50% of total

population was considered as the sample size.

CONTACT METHOD

Both personal and telephonic interview methods were used for conducting the market survey.

Personal interview had the benefit one to one communication between the researcher and the

respondent. If the respondent is having any doubt or queries in their mind, they can get heir

doubts clarified from the researcher on the spot and so superior of data was collected from the

survey was collected from the survey.

Tele – interview was conducted with the structured questionnaire. Tele-interview was less costly

and less time consuming but the data could not be collected in detail from the respondents. Also

any doubt or queries of respondent could not be clarified.

ANALYSIS AND INFORMATION

Detailed information was collected for the project marker survey for retail marketing and sales

promotion activities of Jaypee Cement for the area of Allahabad market. The information was

collected by visiting the retailers of cement present in Allahabad market. The interview of

retailer was taken in a friendly atmosphere so as to encourage them to give right information,

without any hesitation. Because of some inherent limitation of telephonic interview, the method

of personal interview was mostly used.

ANALYSIS:-

The analysis of the collection information was made in scientific manner. Different manner rank

was given to each alternative of particular questions, in the questionnaire. A particular rank was

given in the following manner,

Rank-1For the most favorable alternative

Rank-2For the moderately favorable alternative

Rank-3For unfavorable alternative

Page 37

Rank-4For most unfavorable alternative

Rank-5Unfavorable

To come at the conclusion, total of each alternative of all the sample size retailers was made.

Thus the “sum of an alternative” having least score considered to be most favorable. In this

manner, result is prepared for various important parameters of the survey. With the help of

results so obtained, the findings are recorded in the form of graphs. The market of cement

Changes as the area changes. The demand for particular cement for particular cement is much

less. This is because of the crazier Trend of particular market.

Thus the demand for the cement is not that price sensitive. Price is not the criterion for selection

of rejection of particular brand is adapted on the type of application of cement and the brand

name in market. Thus the awareness among the customers about the particular cement plays a

vital role.

The major types of customers are the builders and masons. The individual customers are there,

but their demand is not more. The customers are ready to give slightly high price, but he wants

quality cement, thus he is quality conscious. The customer perceives quality of cement as good

quality because of effective marketing. So effective marketing is necessary. The retailer in the

marker plays an important role in the sale of the cement. They have some expectation from the

cement companies; they expected credit facility, good sales promotion schemes, and timely

delivery of cement, etc. Among the plastic bag and paper bag of cement, Customer prefer bag.

This is because the paper bag prevents it from moisture and quantity remains intact.

In brief cement market is sensitive to marketing. The better & more the marketing the more is

possibility of sales. The observations and findings of the market survey about market share and

sales promotion activities are given at the next stage, in the report.

Page 38

Chapter-4 Data Analysis and

Interpretation

Page 39

Data Analysis and Interpretation

DATA ANALYSIS AND FINDINGS

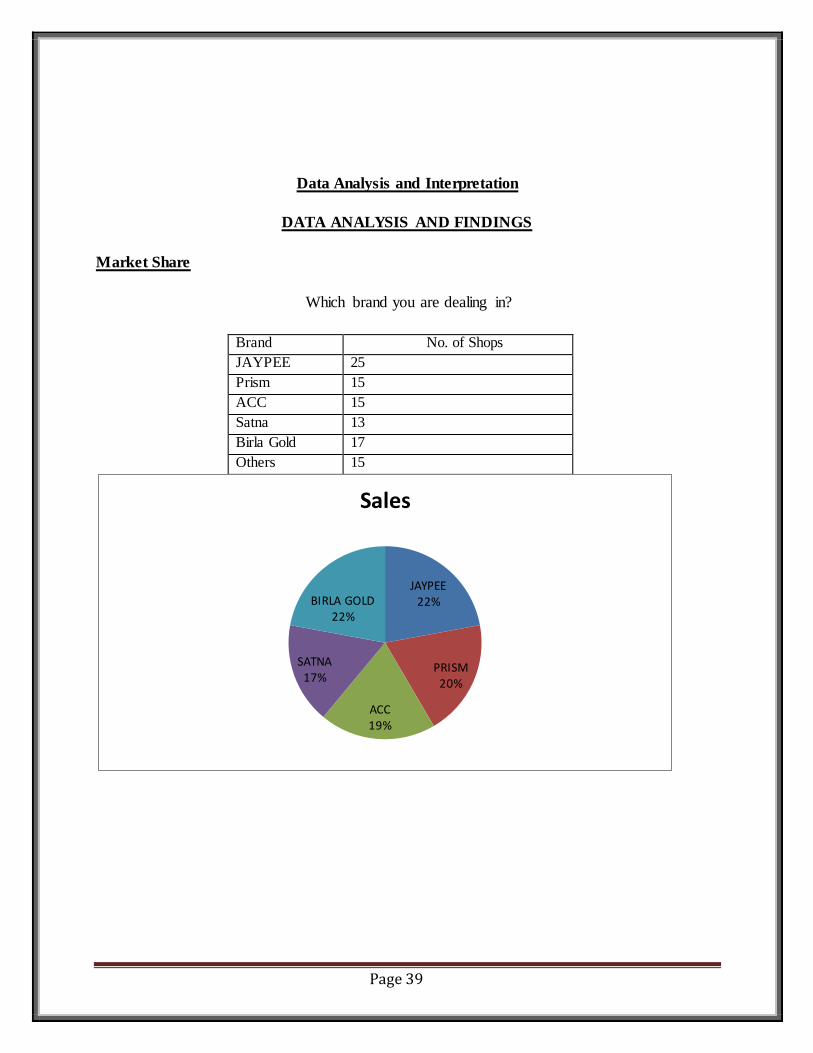

Market Share

Which brand you are dealing in?

Brand No. of Shops

JAYPEE 25

Prism 15

ACC 15

Satna 13

Birla Gold 17

Others 15

JAYPEE22%

PRISM20%

ACC19%

SATNA17%

BIRLA GOLD22%

Sales

Page 40

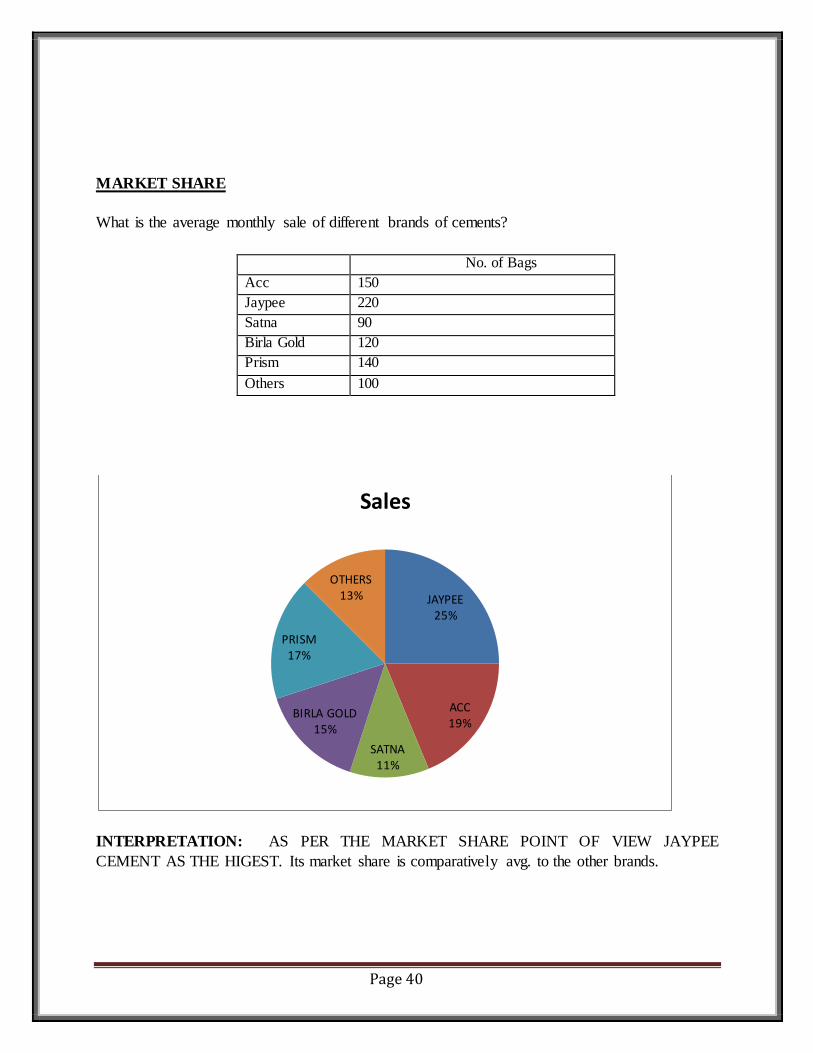

MARKET SHARE

What is the average monthly sale of different brands of cements?

No. of Bags

Acc 150

Jaypee 220

Satna 90

Birla Gold 120

Prism 140

Others 100

INTERPRETATION: AS PER THE MARKET SHARE POINT OF VIEW JAYPEE

CEMENT AS THE HIGEST. Its market share is comparatively avg. to the other brands.

JAYPEE25%

ACC19%

SATNA11%

BIRLA GOLD15%

PRISM17%

OTHERS13%

Sales

Page 41

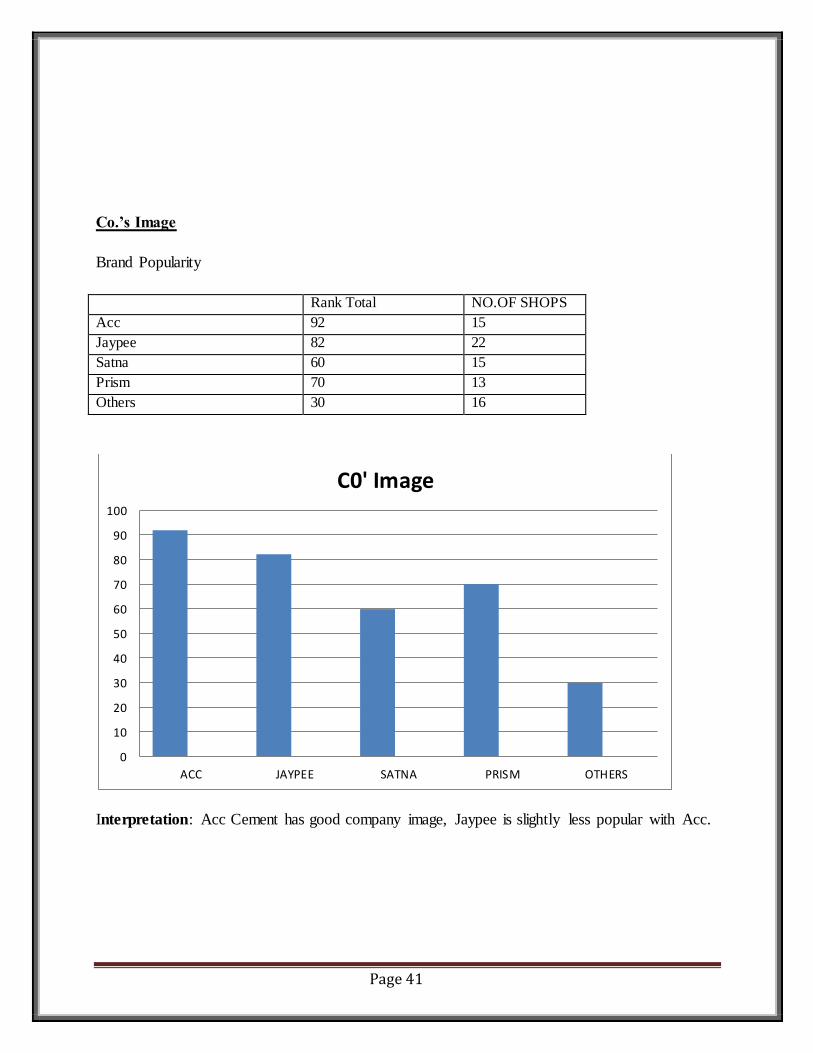

Co.’s Image

Brand Popularity

Rank Total NO.OF SHOPS

Acc 92 15

Jaypee 82 22

Satna 60 15

Prism 70 13

Others 30 16

Interpretation: Acc Cement has good company image, Jaypee is slightly less popular with Acc.

0

10

20

30

40

50

60

70

80

90

100

ACC JAYPEE SATNA PRISM OTHERS

C0' Image

Page 42

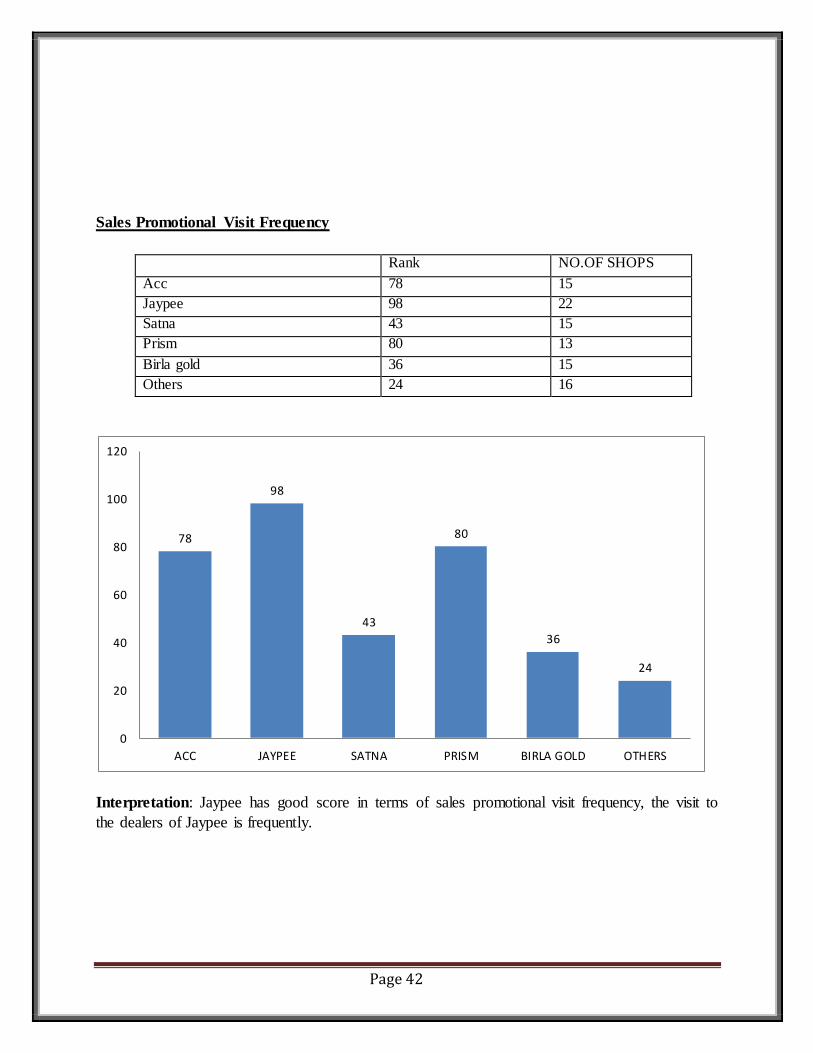

Sales Promotional Visit Frequency

Rank NO.OF SHOPS

Acc 78 15

Jaypee 98 22

Satna 43 15

Prism 80 13

Birla gold 36 15

Others 24 16

Interpretation: Jaypee has good score in terms of sales promotional visit frequency, the visit to

the dealers of Jaypee is frequently.

78

98

43

80

36

24

0

20

40

60

80

100

120

ACC JAYPEE SATNA PRISM BIRLA GOLD OTHERS

Page 43

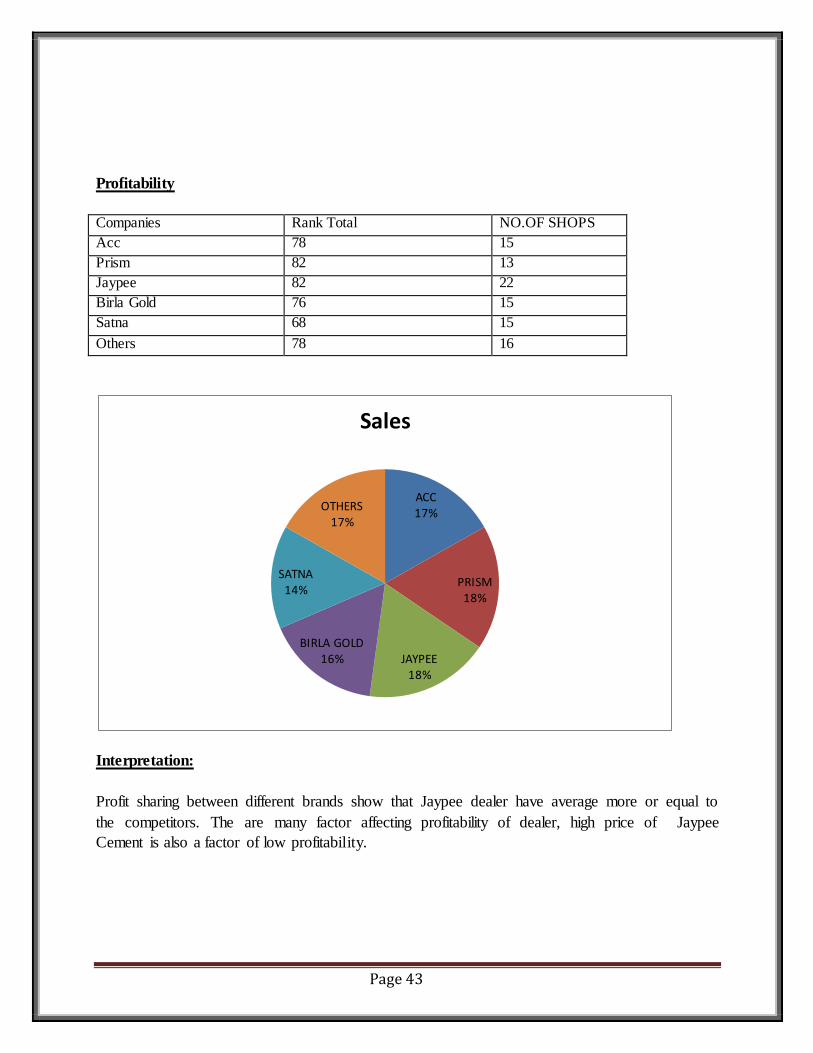

Profitability

Companies Rank Total NO.OF SHOPS

Acc 78 15

Prism 82 13

Jaypee 82 22

Birla Gold 76 15

Satna 68 15

Others 78 16

Interpretation:

Profit sharing between different brands show that Jaypee dealer have average more or equal to

the competitors. The are many factor affecting profitability of dealer, high price of Jaypee

Cement is also a factor of low profitability.

ACC17%

PRISM18%

JAYPEE18%

BIRLA GOLD16%

SATNA14%

OTHERS17%

Sales

Page 44

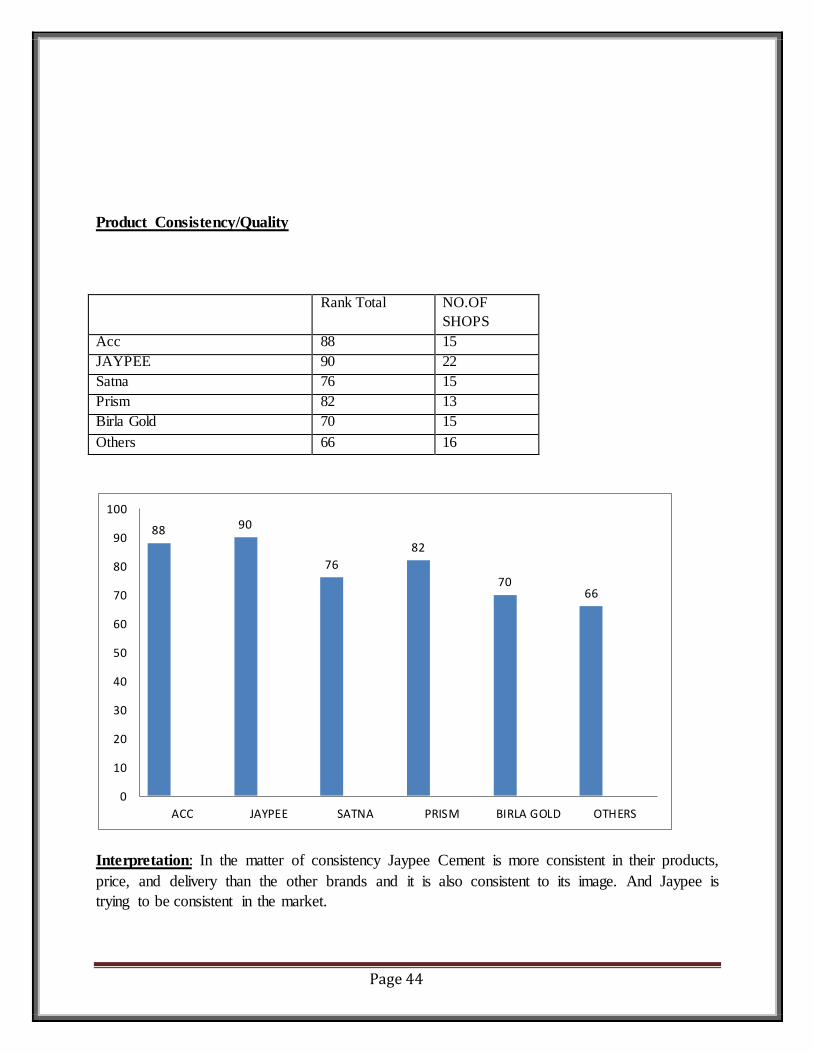

Product Consistency/Quality

Rank Total NO.OF

SHOPS

Acc 88 15

JAYPEE 90 22

Satna 76 15

Prism 82 13

Birla Gold 70 15

Others 66 16

Interpretation: In the matter of consistency Jaypee Cement is more consistent in their products,

price, and delivery than the other brands and it is also consistent to its image. And Jaypee is

trying to be consistent in the market.

88 90

76

82

7066

0

10

20

30

40

50

60

70

80

90

100

ACC JAYPEE SATNA PRISM BIRLA GOLD OTHERS

Page 45

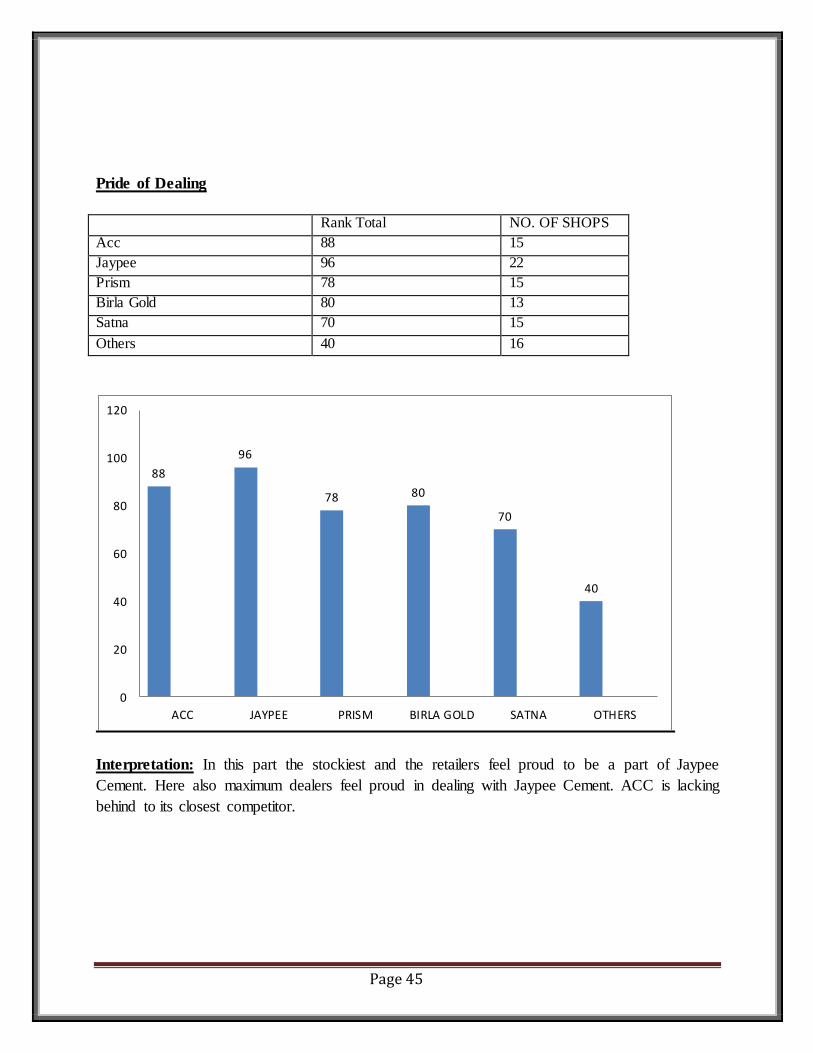

Pride of Dealing

Rank Total NO. OF SHOPS

Acc 88 15

Jaypee 96 22

Prism 78 15

Birla Gold 80 13

Satna 70 15

Others 40 16

Interpretation: In this part the stockiest and the retailers feel proud to be a part of Jaypee

Cement. Here also maximum dealers feel proud in dealing with Jaypee Cement. ACC is lacking

behind to its closest competitor.

88

96

78 80

70

40

0

20

40

60

80

100

120

ACC JAYPEE PRISM BIRLA GOLD SATNA OTHERS

Page 46

SWOT –Analysis

SWOT-analysis is done to understand the external and internal environment of the organization.

SWOT, which is acronym for strength, weakness, opportunity and threats are also known by

TOWS-analysis. Though such an analysis, is strength and weakness exist within an organization

can be matched with the opportunity and threats operating in environment, so that an effective

strategy can be formulated. An effective organizational strategy, therefore, is one that capitalizes

on the opportunity through the use of strength and neutralizes the threats by minimizing the

impact of weakness. Below is the SWOT- analysis Jaypee Cement Ltd. in cement market.

Strengths:-

World Class process Technology ensures Quality and Consistency.

People ask for bleakness in cement and jaypee has this.

Cement grade is good and people are satisfied.

Jaypee group is the 3rd largest cement producer in the country.

Higher Compressive strength.

Good customer relation.

Weakness:-

Great need of strategic way for promotion and advertisement for both dealers and

customers.

Not an easy task to overtake Prism and ACC.

Price and margins is not match with dealers and retailers expectation respectively.

The information of change in price is not properly available to the customers.

Take large time in the replacement of Cement.

Opportunity:-

Strong infrastructure requirement for the development of the country and the country is

developing in the utter pace.

No. of the medium class people is growing.

Institutional market like corporate and government offices, school society complexes are

growing in large scale, which will increase the requirement.

Threats:-

Page 47

Cheep priced brand are grabbing rapidly a large chunk of lower income customer base.

Other brands like Duncan and Grasim provide maximum profit to the both customer as

well as to the retailers.

Dealers expect more margin and gift to sell of the JAYPEE cement.

Chapter 5

Limitations,

Recommendation,

Possible

Advertisement method

Page 48

LIMITATIONS OF THE STUDY

1. The major problem of the survey was that most of the respondents being very loyal to their

brands didn’t give exact answers .like they didn’t talk much about what problems they are

facing, what are the different marketing schemes of the brand in which they deal etc.

2. Once we got the questionnaire filled, we need to restart the conversation in a very generalized

way and talk about the local market conditions. Like who is the main dealer, which cement is

mostly sold in that area etc. so this survey demands a good piece of time while talking to the

respondent. Also Allahabad is big Distict. With a number of small towns and villages. So to

complete the survey within 45 Days time seems to be a bit difficult.

3. Some of the respondents may have told their average monthly sale more than the actual.

Because all of them think that the monthly sale attached with the market image of their shop.

4. Many of the dealers/retailers refused to answer any question at all. So the actual figures can be

somewhat different from the one that we have found out.

5. Being new to the Distict of Allahabad, it is quite possible that I was unable to explore some of

the dealers/retailers.

Page 49

RECOMMENDATIONS

Based upon the time spent by me in the market, usefull suggestions of the dealers & retailers and

the findings from the survey, following recommendations can be suggested for increasing sales

and effectiveness of JAYPEE Cement:

are the price of the cement and then the quality.

While visiting market for cement purchase, they don’t care about which brand they are going to

buy. They simply know that X is ongoing price of the cement, if any brand costs higher than X,

they will not buy that brand. JAYPEE Cement usually costs 4-5 Rs. Higher than the other

counterparts. This extra price is the main reason behind lower sales. Therefore, JAYPEE need to

take some serious steps to reduce the selling price somehow.

rs for JAYPEE cement is very less as compared to the

main competitors ACC, Satna, Etc. They need to increase the no. of retailers as much as

possible.

dealers used to shop other type of building materials along with

cement, in the same shop. This should not be permitted by JAYPEE .Because selling of these

building materials is more profitable than cement, so the cement selling becomes less important

for these dealers. They don’t give proper attention to the company officials and also to the

various schemes of increasing sales. This in turn brings reduced sales to the company

Cement has market image of a modern cement with very good quality. It should try

to encash this image. Its mainly the younger section of people who care about quality first and

then the price. So JAYPEE needs to give proper attention to the youngsters. May be, they are

not the cement buyers at present but future possibility lies with them.

Page 50

customers loyal to their

shops, due to the high price of the cement provided by them. So at some point, the dealers are not

satisfied with the company. This need to be taken seriously by JAYPEE .Some more incentive

schemes should be introduced for the dealers and also the frequency of visits from company

officials need to be increased.

POSSIBLE ADVERTISEMENT METHODS

All of the cement brands use the similar methods of advertising like painting walls, use banners,

giving free gifts to the dealers and masons etc.There are still many possible methods of

advertisement and creating brand awareness, which are untouched. Some of these methods are as

below:

about the major

dealer/dealers in the city. Details like address, contact no. of the dealer, different schemes,

current market price etc can be shown.

are also reaching a good part of listeners. So these can also be used for

the same purpose.

ed mainly on the tractor trolleys, dealer’s shop and on walls only.

We can think about using banners on rickshaws and autos also.

and sometimes for the

masons. As a change, we can also try to attract the customers directly. For ex-discount coupons,

small free gifts, scratch cards etc can be made available for the customers.

needs some improvements.

We need to decrease the frequency of these meets. What we can do is that organize a big meet

with a no. of people, higher company officials, entertainment, and snacks for all.

The presence of company officials in the meeting is not alone sufficient. We need to call some

big personalities from that city only. The people like these masons are more impressed by the

presence of Govt.officials.

Page 51

Chapter6

Conclusion

Page 52

CONCLUSION

JAYPEE CEMENT has two major competitors- PRISM and ACC CEMENT is well established

in the markets as far as quality is concerned.

Introduction of new attractive incentive schemes can bring new dealers & retailers for JAYPEE

cement. Price is the major factor that matters for a customer while purchasing cement. Market

share increases with the increase in no. of dealers.

The market survey undertaken shows that effective marketing efforts play a vital role in creating

the goodwill for the brand. The distribution channel of cement industry must be well designed

and made effective this ensures it.

Page 53

BIBLIOGRAPHY

BOOKS

1. Research Methodology: C.K. Kothari

(Wishwa Prakashan Darayaganj New Delhi 2nd Edition-2004)

2. Marketing Management: Philip Kotler

(Prentice- hall of India Pvt. Ltd. New Delhi-110001 10 th Edition -2002)

3. WEBSITE :-

http://www.digisoft.in

www.indianexpress.com

www.google.com

www.jalindia.com

www.ibef.org

Page 54

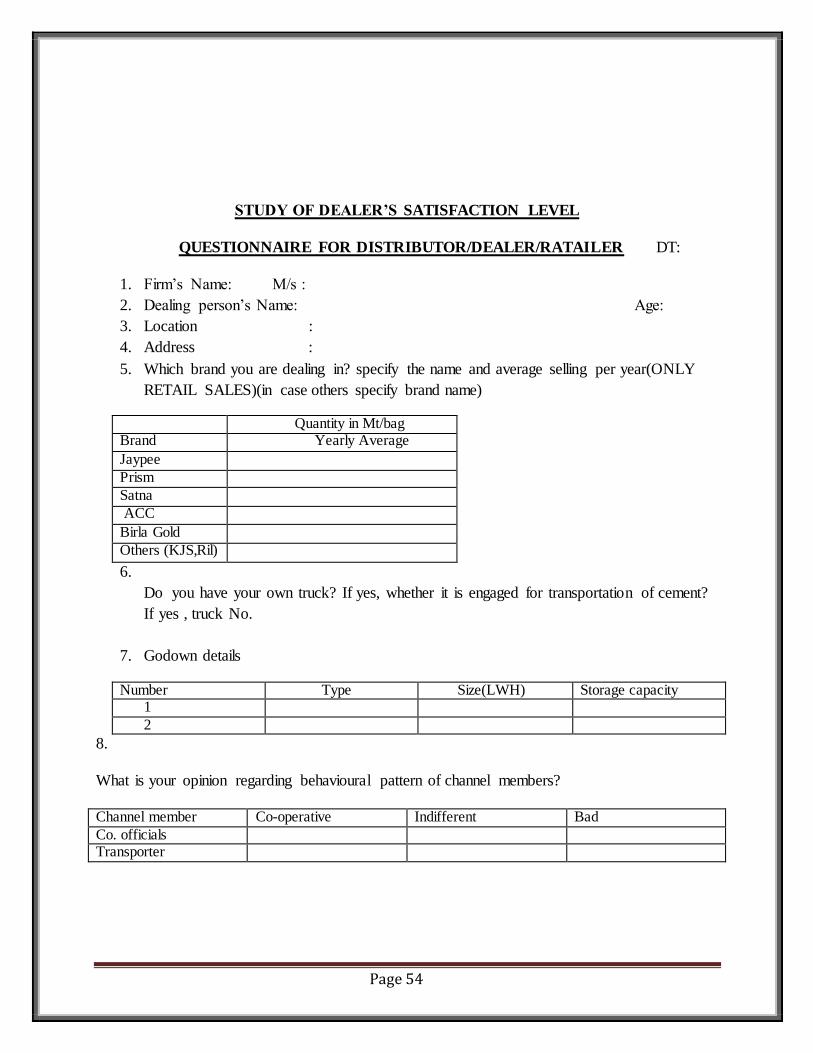

STUDY OF DEALER’S SATISFACTION LEVEL

QUESTIONNAIRE FOR DISTRIBUTOR/DEALER/RATAILER DT:

1. Firm’s Name: M/s :

2. Dealing person’s Name: Age:

3. Location :

4. Address :

5. Which brand you are dealing in? specify the name and average selling per year(ONLY

RETAIL SALES)(in case others specify brand name)

Quantity in Mt/bag Brand Yearly Average

Jaypee

Prism

Satna

ACC

Birla Gold

Others (KJS,Ril)

6.

Do you have your own truck? If yes, whether it is engaged for transportation of cement?

If yes , truck No.

7. Godown details

Number Type Size(LWH) Storage capacity 1

2

8.

What is your opinion regarding behavioural pattern of channel members?

Channel member Co-operative Indifferent Bad

Co. officials Transporter

Page 55

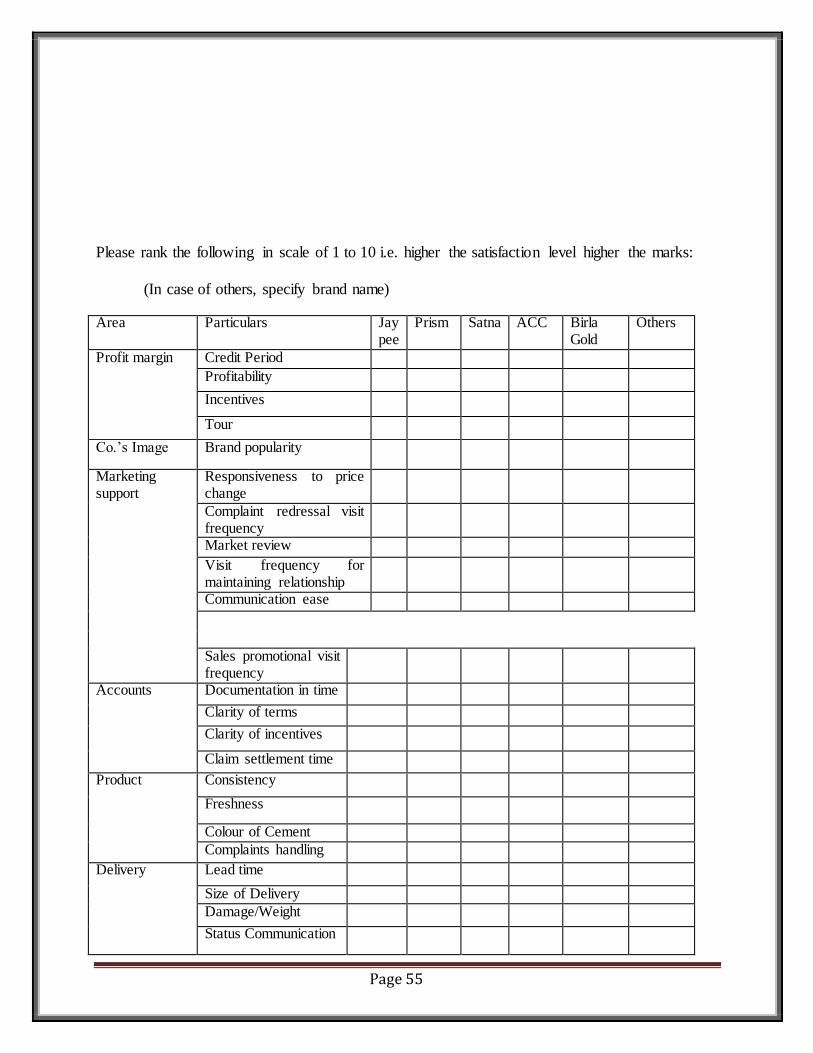

Please rank the following in scale of 1 to 10 i.e. higher the satisfaction level higher the marks:

(In case of others, specify brand name)

Area Particulars Jaypee

Prism Satna ACC Birla Gold

Others

Profit margin Credit Period

Profitability

Incentives

Tour

Co.’s Image Brand popularity

Marketing support

Responsiveness to price change

Complaint redressal visit frequency

Market review

Visit frequency for maintaining relationship

Communication ease

Sales promotional visit frequency

Accounts Documentation in time

Clarity of terms

Clarity of incentives

Claim settlement time

Product Consistency

Freshness

Colour of Cement

Complaints handling

Delivery Lead time

Size of Delivery

Damage/Weight

Status Communication

Page 56

Note: In case of low rating for any brand, ask for the expectation and note in back side of page along with brand name.

Similarly in case of high rating for any brand, ask for the best practice.

![JAYPEE CEMENT - Jaypee · PDF fileJAYPEE BALAJ] CEMENT PLANT A UNIT OF JAYPEE CEMENT CORPORATION LIMITED JCCLI IBCP t 4(t) | 201 6 t 44DL 301h November 2016 to](https://img.pdfslide.us/doc/110x75/5ab4e2e77f8b9a0f058c4119/jaypee-cement-jaypee-balaj-cement-plant-a-unit-of-jaypee-cement-corporation-limited.jpg)