Embed Size (px)

Citation preview

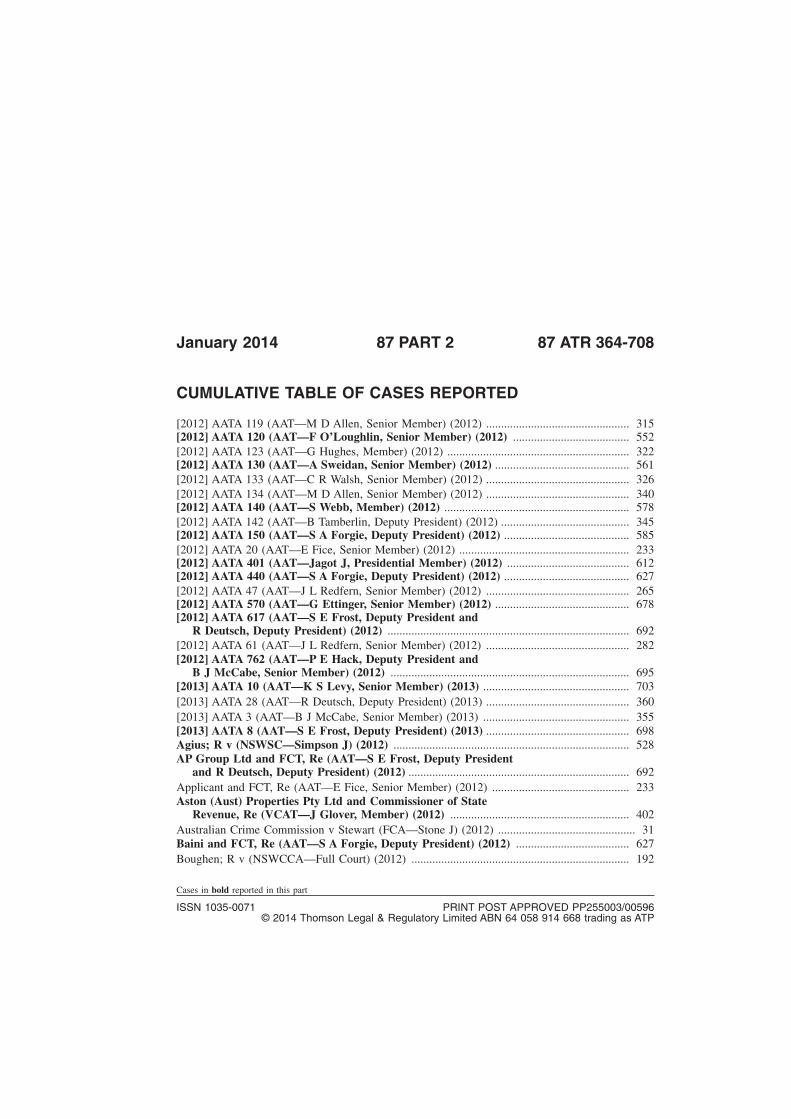

January 2014 87 PART 2 87 ATR 364-708

CUMULATIVE TABLE OF CASES REPORTED

[2012] AATA 119 (AATmdashM D Allen Senior Member) (2012) 315[2012] AATA 120 (AATmdashF OrsquoLoughlin Senior Member) (2012) 552

[2012] AATA 123 (AATmdashG Hughes Member) (2012) 322[2012] AATA 130 (AATmdashA Sweidan Senior Member) (2012) 561

[2012] AATA 133 (AATmdashC R Walsh Senior Member) (2012) 326

[2012] AATA 134 (AATmdashM D Allen Senior Member) (2012) 340[2012] AATA 140 (AATmdashS Webb Member) (2012) 578

[2012] AATA 142 (AATmdashB Tamberlin Deputy President) (2012) 345[2012] AATA 150 (AATmdashS A Forgie Deputy President) (2012) 585

[2012] AATA 20 (AATmdashE Fice Senior Member) (2012) 233[2012] AATA 401 (AATmdashJagot J Presidential Member) (2012) 612[2012] AATA 440 (AATmdashS A Forgie Deputy President) (2012) 627

[2012] AATA 47 (AATmdashJ L Redfern Senior Member) (2012) 265[2012] AATA 570 (AATmdashG Ettinger Senior Member) (2012) 678[2012] AATA 617 (AATmdashS E Frost Deputy President and

R Deutsch Deputy President) (2012) 692

[2012] AATA 61 (AATmdashJ L Redfern Senior Member) (2012) 282[2012] AATA 762 (AATmdashP E Hack Deputy President and

B J McCabe Senior Member) (2012) 695[2013] AATA 10 (AATmdashK S Levy Senior Member) (2013) 703

[2013] AATA 28 (AATmdashR Deutsch Deputy President) (2013) 360

[2013] AATA 3 (AATmdashB J McCabe Senior Member) (2013) 355[2013] AATA 8 (AATmdashS E Frost Deputy President) (2013) 698Agius R v (NSWSCmdashSimpson J) (2012) 528AP Group Ltd and FCT Re (AATmdashS E Frost Deputy President

and R Deutsch Deputy President) (2012) 692

Applicant and FCT Re (AATmdashE Fice Senior Member) (2012) 233Aston (Aust) Properties Pty Ltd and Commissioner of State

Revenue Re (VCATmdashJ Glover Member) (2012) 402

Australian Crime Commission v Stewart (FCAmdashStone J) (2012) 31Baini and FCT Re (AATmdashS A Forgie Deputy President) (2012) 627

Boughen R v (NSWCCAmdashFull Court) (2012) 192

Cases in bold reported in this part

ISSN 1035-0071 PRINT POST APPROVED PP25500300596copy 2014 Thomson Legal amp Regulatory Limited ABN 64 058 914 668 trading as ATP

Cameron R v (NSWCCAmdashFull Court) (2012) 192

DCT v Seabrooke (FCAmdashSiopis J) (2012) 217DCT v Sent (VSCmdashMukhtar AsJ) (2013) 394DCT HC Legal Pty Ltd v (FCAmdashMurphy J) (2013) 379Dickinson and FCT Re (AATmdashP E Hack Deputy President and

B J McCabe Senior Member) (2012) 695EME Productions No 1 Pty Ltd Screen Australia v (FCAmdashFull

Court) (2012) 434Ericson tas Flearsquos Concreting Hansen Yuncken Pty Ltd v

(QSCmdashMcMurdo J) (2012) 489

Esso Australia Resources Pty Ltd v FCT (FCAmdashFull Court) (2012) 124

FCT v Interhealth Energies Pty Ltd (As Trustee of the Interhealth SuperannuationFund) (FCAmdashLogan J) (2012) 164

FCT v Regent Pacific Group Ltd (FCAmdashSiopis J) (2013) 364

FCT v Unit Trend Services Pty Ltd (HCAmdashFull Court) (2013) 13

FCT Esso Australia Resources Pty Ltd v (FCAmdashFull Court) (2012) 124

FCT Sent v (FCAmdashFull Court) (2012) 223

FCT Unit Trend Services Pty Ltd v (FCAmdashLogan J) (2013) 1General Aviation Maintenance Pty Ltd and FCT Re

(AATmdashF OrsquoLoughlin Senior Member) (2012) 552

Gunawan and FCT Re (AATmdashM D Allen Senior Member) (2012) 315Hansen Yuncken Pty Ltd v Ericson tas Flearsquos Concreting

(QSCmdashMcMurdo J) (2012) 489Harbutt and FCT Re (AATmdashS E Frost Deputy President) (2013) 698HC Legal Pty Ltd v DCT (FCAmdashMurphy J) (2013) 379

Interhealth Energies Pty Ltd (As Trustee of the Interhealth Superannuation Fund) FCTv (FCAmdashLogan J) (2012) 164

Kalafatis and FCT Re (AATmdashS A Forgie Deputy President)(2012) 585

Kalomel Nominees Pty Ltd v Commissioner of State Taxation (SASCmdashGray J) (2012) 88Kolya v Tax Practitioners Board (FCAmdashFlick J) (2012) 474Lend Lease Development Pty Ltd v Chief Commissioner of State

Revenue (VSCmdashPagone J) (2012) 504

Lengyel and Tax Practitioners Board Re (AATmdashM D Allen Senior Member) (2012) 340

Ma and Estate of Late Wai Hung Ma and FCT Re (AATmdashJ L RedfernSenior Member) (2012) 265

Mason and FCT Re (AATmdashC R Walsh Senior Member) (2012) 326

Montgomery Wools Pty Ltd (As Trustee for Montgomery Wools Pty Ltd Super Fund)and FCT Re (AATmdashJ L Redfern Senior Member) (2012) 282

Naude and FCT Re (AATmdashA Sweidan Senior Member) (2012) 561Panthers Investment Corporation Pty Ltd v Chief Commissioner

of State Revenue (NSWSCmdashGzell J) (2013) 369Peaker and FCT Re (AATmdashS Webb Member) (2012) 578Penrowse Pty Ltd and FCT Re (AATmdashK S Levy Senior Member)

(2013) 703

Port Augusta Medical Centre Pty Ltd v Commissioner of State Taxation (SASCmdashFullCourt) (2012) 102

R v Agius (NSWSCmdashSimpson J) (2012) 528

R v Boughen (NSWCCAmdashFull Court) (2012) 192

(Cases in bold reported in this part)

TABLE OF CASES REPORTED

R v Cameron (NSWCCAmdashFull Court) (2012) 192R v Zerafa (NSWSCmdashSimpson J) (2012) 528Regent Pacific Group Ltd FCT v (FCAmdashSiopis J) (2013) 364Screen Australia v EME Productions No 1 Pty Ltd (FCAmdashFull

Court) (2012) 434

Seabrooke DCT v (FCAmdashSiopis J) (2012) 217

Sent v FCT (FCAmdashFull Court) (2012) 223Sent DCT v (VSCmdashMukhtar AsJ) (2013) 394State Revenue Chief Commissioner of Lend Lease Development

Pty Ltd v (VSCmdashPagone J) (2012) 504State Revenue Chief Commissioner of Panthers Investment

Corporation Pty Ltd v (NSWSCmdashGzell J) (2013) 369State Revenue Commissioner of Re Aston (Aust) Properties Pty

Ltd and (VCATmdashJ Glover Member) (2012) 402State Revenue Commissioner of Re Tate-Louery amp Dwyer Pty

Ltd (As Trustee for the Cash Wheeler Unit Trust) and(VCATmdashJudge Macnamara Vice-President) (2012) 429

State Revenue Commissioner of Re Verra Pty Ltd (As Trustee forthe Pharmacies Services Trust) and (QCATmdashP McDermottMember) (2012) 417

State Revenue Commissioner of Re Westnet Rail Holdings No 1Pty Ltd and (WASATmdashChaney J President) (2012) 448

State Taxation Commissioner of Kalomel Nominees Pty Ltd v (SASCmdashGray J)(2012) 88

State Taxation Commissioner of Port Augusta Medical Centre Pty Ltd v (SASCmdashFullCourt) (2012) 102

Stewart Australian Crime Commission v (FCAmdashStone J) (2012) 31Tate-Louery amp Dwyer Pty Ltd (As Trustee for the Cash Wheeler

Unit Trust) and Commissioner of State Revenue Re(VCATmdashJudge Macnamara Vice-President) (2012) 429

Tax Practitioners Board Kolya v (FCAmdashFlick J) (2012) 474

Taxpayer and FCT Re (AATmdashB Tamberlin Deputy President) (2012) 345

Taxpayer and FCT Re (AATmdashB J McCabe Senior Member) (2013) 355

Tom and FCT Re (AATmdashR Deutsch Deputy President) (2013) 360

Tran and FCT Re (AATmdashG Hughes Member) (2012) 322

Unit Trend Services Pty Ltd v FCT (FCAmdashLogan J) (2013) 1

Unit Trend Services Pty Ltd FCT v (HCAmdashFull Court) (2013) 13Verra Pty Ltd (As Trustee for the Pharmacies Services Trust) and

Commissioner of State Revenue Re (QCATmdashP McDermottMember) (2012) 417

Vita Hot Bread Pty Ltd and FCT Re (AATmdashG EttingerSenior Member) (2012) 678

Westnet Rail Holdings No 1 Pty Ltd and Commissioner of StateRevenue Re (WASATmdashChaney J President) (2012) 448

Yacoub and FCT Re (AATmdashJagot J Presidential Member) (2012) 612Zerafa R v (NSWSCmdashSimpson J) (2012) 528

(Cases in bold reported in this part)

TABLE OF CASES REPORTED

TABLE OF CASES JUDICIALLY CONSIDERED IN THIS PART

Adams Trustees of Estate of v Commissioner of Pay-roll Tax (Vic) (1980) 143 CLR 629

Applied [2013] AATA 10 Re Penrowse Pty Ltd and FCT 703

Karingal 2 Holdings Pty Ltd v Commissioner of State Revenue (2002) 51 ATR 190

Applied Panthers Investment Corporation Pty Ltd and Another vChief Commissioner of State Revenue 369

Lygon Nominees Pty Ltd v Commissioner of State Revenue (2007) 23 VR 474

Applied Panthers Investment Corporation Pty Ltd and Another vChief Commissioner of State Revenue 369

Nguyen and FCT Re (2011) 84 ATR 618

Applied [2012] AATA 570 Re Vita Hot Bread Pty Ltd and FCT 678

Sgardelis and FCT Re (2007) 68 ATR 963

Followed [2012] AATA 570 Re Vita Hot Bread Pty Ltd and FCT 678

Tasty Chicks Pty Ltd v Chief Commissioner of State Revenue (NSW) (2011) 245 CLR 446

Followed Re Verra Pty Ltd (As Trustee for the PharmaciesServices Trust) and Others and Commissioner of State Revenue 417

TSC 2000 Pty Ltd and FCT Re (2007) 66 ATR 945

Followed [2012] AATA 570 Re Vita Hot Bread Pty Ltd and FCT 678

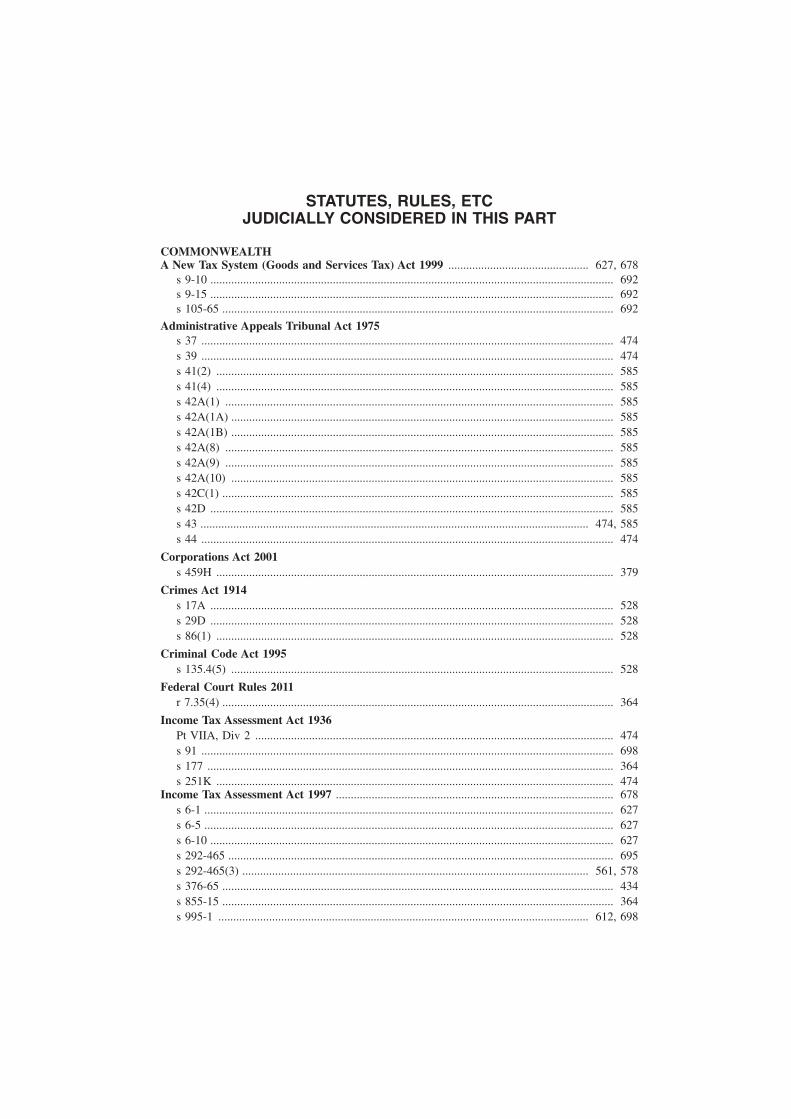

STATUTES RULES ETCJUDICIALLY CONSIDERED IN THIS PART

COMMONWEALTHA New Tax System (Goods and Services Tax) Act 1999 627 678

s 9-10 692

s 9-15 692

s 105-65 692

Administrative Appeals Tribunal Act 1975

s 37 474

s 39 474

s 41(2) 585

s 41(4) 585

s 42A(1) 585

s 42A(1A) 585

s 42A(1B) 585

s 42A(8) 585

s 42A(9) 585

s 42A(10) 585

s 42C(1) 585

s 42D 585

s 43 474 585

s 44 474

Corporations Act 2001

s 459H 379

Crimes Act 1914

s 17A 528

s 29D 528

s 86(1) 528

Criminal Code Act 1995

s 1354(5) 528

Federal Court Rules 2011

r 735(4) 364

Income Tax Assessment Act 1936

Pt VIIA Div 2 474

s 91 698

s 177 364

s 251K 474Income Tax Assessment Act 1997 678

s 6-1 627

s 6-5 627

s 6-10 627

s 292-465 695

s 292-465(3) 561 578

s 376-65 434

s 855-15 364

s 995-1 612 698

Superannuation Guarantee (Administration) Act 1992

s 11 703

s 12(1) 552

s 12(3) 552

s 12(8) 552Superannuation Guarantee Charge Act 1992 703

Tax Agent Services Act 2009

s 20-5 474

s 20-15 474

s 20-25 474

s 40-5 474

s 90-1 474

Tax Agent Services (Transitional Provisions and Consequential Amendments) Act 2009

Sch 2 item 1 474

Taxation Administration Act 1953

s 14ZS(1) 585

s 14ZS(2) 585

s 14ZS(4) 585

s 14ZZ 585

s 14ZZ(a) 585

s 14ZZE 585

s 14ZZJ 585

s 14ZZK 585

s 14ZZO 585

s 14ZZP 585

Sch 1 s 260-5 489

Sch 1 s 260-20 489

Sch 1 s 284-75 678

Sch 1 s 284-75(1) 627

Sch 1 s 284-90 678

NEW SOUTH WALES

Land Tax Management Act 1956

s 3 369

s 10(1)(g)(iii) 369

s 10(1)(h) 369

QUEENSLAND

Payroll Tax Act 1971

s 68 417

s 69 417

s 71 417

VICTORIADuties Act 2000 402 504Land Tax Act 1958 429

s 44(3) 402

Land Tax Act 2005

s 46A 402

s 47 402

s 50 402

STATUTES RULES ETC JUDICIALLY CONSIDERED

Taxation Administration Act 1997

s 20 402

WESTERN AUSTRALIA

Interpretation Act 1984

s 5 448

Stamp Act 1921

s 76(1) 448

s 76AP 448

STATUTES RULES ETC JUDICIALLY CONSIDERED

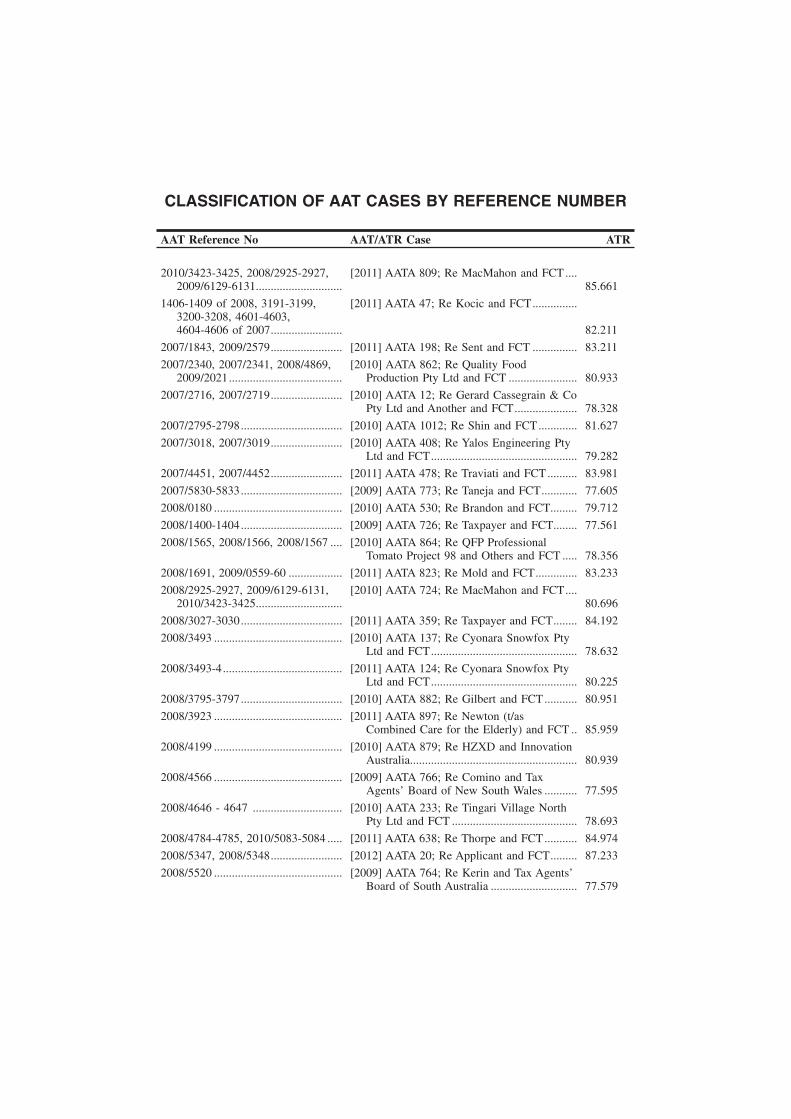

CLASSIFICATION OF AAT CASES BY REFERENCE NUMBER

AAT Reference No AATATR Case ATR

20103423-3425 20082925-292720096129-6131

[2011] AATA 809 Re MacMahon and FCT85661

1406-1409 of 2008 3191-31993200-3208 4601-46034604-4606 of 2007

[2011] AATA 47 Re Kocic and FCT

82211

20071843 20092579 [2011] AATA 198 Re Sent and FCT 83211

20072340 20072341 2008486920092021

[2010] AATA 862 Re Quality FoodProduction Pty Ltd and FCT 80933

20072716 20072719 [2010] AATA 12 Re Gerard Cassegrain amp CoPty Ltd and Another and FCT 78328

20072795-2798 [2010] AATA 1012 Re Shin and FCT 81627

20073018 20073019 [2010] AATA 408 Re Yalos Engineering PtyLtd and FCT 79282

20074451 20074452 [2011] AATA 478 Re Traviati and FCT 83981

20075830-5833 [2009] AATA 773 Re Taneja and FCT 77605

20080180 [2010] AATA 530 Re Brandon and FCT 79712

20081400-1404 [2009] AATA 726 Re Taxpayer and FCT 77561

20081565 20081566 20081567 [2010] AATA 864 Re QFP ProfessionalTomato Project 98 and Others and FCT 78356

20081691 20090559-60 [2011] AATA 823 Re Mold and FCT 83233

20082925-2927 20096129-613120103423-3425

[2010] AATA 724 Re MacMahon and FCT80696

20083027-3030 [2011] AATA 359 Re Taxpayer and FCT 84192

20083493 [2010] AATA 137 Re Cyonara Snowfox PtyLtd and FCT 78632

20083493-4 [2011] AATA 124 Re Cyonara Snowfox PtyLtd and FCT 80225

20083795-3797 [2010] AATA 882 Re Gilbert and FCT 80951

20083923 [2011] AATA 897 Re Newton (tasCombined Care for the Elderly) and FCT 85959

20084199 [2010] AATA 879 Re HZXD and InnovationAustralia 80939

20084566 [2009] AATA 766 Re Comino and TaxAgentsrsquo Board of New South Wales 77595

20084646 - 4647 [2010] AATA 233 Re Tingari Village NorthPty Ltd and FCT 78693

20084784-4785 20105083-5084 [2011] AATA 638 Re Thorpe and FCT 84974

20085347 20085348 [2012] AATA 20 Re Applicant and FCT 87233

20085520 [2009] AATA 764 Re Kerin and Tax AgentsrsquoBoard of South Australia 77579

AAT Reference No AATATR Case ATR

20085586 20085587 20085588 [2010] AATA 311 Re BRMJCQ Pty Ltd andFCT 79220

20085702-5704 [2009] AATA 881 Re Jendahl InvestmentsPty Ltd and FCT 77971

200859335935 [2011] AATA 386 Re Cameron and FCT 83928

20085986 [2011] AATA 296 Re Wynnum Holdings No1 Pty Ltd and FCT 83444

20086172 [2010] AATA 1058 Re Bartercard AustraliaPty Ltd and FCT 81836

20090060 [2010] AATA 140 Re Mortimer and TaxAgentsrsquo Board of South Australia 78640

20090062-63 [2011] AATA 682 Re Applicant and FCT 85561

20090228 - 37 [2010] AATA 289 Re Mano and FCT 78981

20090590-591 [2010] AATA 215 Re Cooper and FCT 78669

20090663 [2010] AATA 148 Re Andriopoulos and FCT 78654

20090803-0805 [2009] AATA 775 Re Soubra and FCT 77946

20090851 [2010] AATA 420 Re Willis and FCT 79287

20090976-977 [2009] AATA 890 Re Caller and Another andFCT 77975

20091153 [2010] AATA 758 Re QFL Photographics PtyLtd and FCT 80760

20091456 [2011] AATA 303 Re Carberry and FCT 83773

20092014-15 [2010] AATA 392 Re Clark and FCT 79262

20092075 20092077-9 [2010] AATA 473 Re Victorian HealthcareAssociation Ltd and FCT 79890

20092253 2254 4008 [2010] AATA 398 Re Manne and FCT 79272

20092404 [2009] AATA 981 Re Surana and TaxAgentsrsquo Board of New South Wales 771003

20092548 [2012] AATA 350 Re Climo and FCT 83248

20092614 [2010] AATA 149 Re Proh and Tax AgentsrsquoBoard of Victoria 78663

20092940-2941 [2010] AATA 843 Re Sills and FCT 80908

20092965 [2010] AATA 819 Re Taxpayer and FCT 80885

20092970 [2010] AATA 549 Re Tanti and FCT 79740

20093384-87 [2011] AATA 657 Re Helbers and FCT 85550

20093404 [2011] AATA 281 Re Clothing Importer andFCT 79707

20093486 [2012] AATA 61 Re Montgomery Wools PtyLtd (As Trustee for Montgomery WoolsPty Ltd Super Fund) and FCT 87282

20094082-4085 [2010] AATA 782 Re Optimise Group PtyLtd and FCT 79953

CLASSIFICATION OF AAT CASES BY REFERENCE NUMBER mdashcontinued

AAT Reference No AATATR Case ATR

20094777 [2010] AATA 858 Re France and FCT 80927

20094778 [2010] AATA 829 Re Brown and FCT 80783

20094890 [2011] AATA 479 Re Greenhatch and FCT 80480

20094899-901 20094921 [2011] AATA 593 Re Mackay and FCT 82256

20095232 [2011] AATA 390 Re A amp C Sliwa Pty Ltdand FCT 83455

20095295 [2010] AATA 455 Re Taxpayer and FCT 79510

20095308 [2011] AATA 512 Re Krishnamurti AustraliaInc and FCT 84322

20095321 [2010] AATA 622 Re Allen J Middlebrook ampAssociates Pty Ltd and Tax PractitionersrsquoBoard 80244

20095513 [2010] AATA 977 Re Qantas Airways Ltdand FCT 81170

20095568 [2011] AATA 39 Re Beyond Productions PtyLtd and Screen Australia 82194

20095626 20102838 [2010] AATA 591 Re Cannavo and FCT 79756

20095672 [2010] AATA 902 Re Sinclair and FCT 80972

20095680 [2010] AATA 912 Re Employee and FCT 80999

20095695 20100543 [2010] AATA 526 Re Pleno and Tax AgentsrsquoBoard 79533

20095721-5722 [2010] AATA 576 Re Smith and FCT 79934

20095748 [2010] AATA 876 Re Trustee of the FamilyTrust and FCT 78364

20095838 20095839 [2010] AATA 573 Re McMennemin andFCT 79898

20096010 [2010] AATA 749 Re Ristevski and TaxPractitioners Board 80742

20096044 [2010] AATA 367 Re Coker and FCT 79258

2010 3506 [2011] AATA 110 Re SXGX and FCT 79882

20100011 20100012 20100013 [2011] AATA 399 Re Ng and FCT 83948

20100186 [2010] AATA 679 Re Elcano Capital LP andInnovation Australia 80495

20100431 [2010] AATA 1065 Re Clontarf DevelopmentPty Ltd and FCT 79540

20100599-0601 20100965-0967 [2011] AATA 785 Re Yip and FCT 82761

20100843 [2011] AATA 439 Re EME Productions No 1Pty Ltd and Screen Australia 83965

20100950 20100951 [2011] AATA 940 Re Shail SuperannuationFund and FCT 86339

20101005 [2011] AATA 48 Re Kakavas and FCT 82234

2010119-120 2010121-122 [2011] AATA 431 Re Antonopoulos andFCT 84311

CLASSIFICATION OF AAT CASES BY REFERENCE NUMBER mdash continued

AAT Reference No AATATR Case ATR

20101310 [2011] AATA 264 Re Perfrement and FCT 83737

20101378 [2011] AATA 588 Re Venturi and FCT 84905

20101437 20110405 20110406 [2011] AATA 698 Re Buggins and FCT 85590

20101721 20101723 [2011] AATA 444 Re Bicycle VictoriaIncorporated and FCT 81924

20101764 [2011] AATA 16 Re Heinrich and FCT 81903

20101912 [2011] AATA 589 Re Syttadel Holdings PtyLtd and FCT 84683

20101994 20103764 20103765 [2011] AATA 766 Re National Jet SystemsPty Ltd and FCT 82740

20102220-2221 [2011] AATA 69 Re Hunt and FCT 82248

20102360-2371 [2011] AATA 628 Re Areffco and FCT 84924

20102378 [2011] AATA 672 Re Badaoui and Konigand FCT 81385

20102430 [2011] AATA 160 Re Taxpayer and FCT 79701

20102462 [2011] AATA 607 Re Inglewood andDistricts Community Enterprises Ltd andFCT 84688

20102473 [2011] AATA 35 Re Player and FCT 82184

20102559-2560 [2010] AATA 846 Re Waters and FCT 80919

20102657-62 20102663-65 [2012] AATA 47 Re Ma and Estate of LateWai Hung Ma and FCT 87265

20102689-92 [2011] AATA 539 Re Mynott and FCT 84594

20102821 [2011] AATA 298 Re Retirement Village Coand FCT 83757

20102841-2844 [2011] AATA 906 Re Knox and FCT 86838

20102895-98 [2011] AATA 847 Re Crown InsurancesServices Ltd and FCT 85905

20103083 [2011] AATA 769 Re MTAA SuperannuationFund (R G Casey Building) Property PtyLtd and FCT 84334

20103136 [2011] AATA 839 Re Rinaldo and FCT 85682

20103311-3317 [2010] AATA 1069 Re Taxpayer and FCT 81864

20103649 20103650 [2011] AATA 318 Re Taxpayer and FCT 83788

20103728 [2011] AATA 693 Re Turner and FCT 85582

20103737 20105022 [2012] AATA 3 Re Ohl and FCT 85798

20103760-3761 [2011] AATA 725 Re Fardell and FCT 85812

20104083 [2011] AATA 545 Re Taxpayer and FCT 84659

20104217-4219 20104223-422520112792-2795

[2012] AATA 119 Re Gunawan and FCT 87315

20104239-4240 [2011] AATA 567 Re Park and FCT 84672

CLASSIFICATION OF AAT CASES BY REFERENCE NUMBER mdashcontinued

AAT Reference No AATATR Case ATR

20104592 [2011] AATA 555 Re Print AppliedTechnology Pty Ltd and FCT 81992

20104609 [2011] AATA 508 Re Taxpayer and FCT 83994

20104695 20110005 [2011] AATA 804 Re Kolya and TaxPractitioners Board 85635

20105064 20105065 [2011] AATA 480 Re Kaley and FCT 85311

20105166 [2011] AATA 445 Re Education Pty Ltd andFCT 81380

20105243 [2011] AATA 563 Re Smith and FCT 84667

20105287 [2011] AATA 499 Re Taxpayer and FCT 83986

20110005 [2011] AATA 73 Re Kolya and TaxPractitioners Board 81912

20110057 20110061 [2012] AATA 11 Re Fortune Corporation PtyLtd and Another and Tax PractitionersBoard 85805

20110058 [2011] AATA 860 Re Allan and FCT 85700

20110421 [2011] AATA 910 Re Trustee for NaiduFamily Trust and FCT 82807

20110781 [2011] AATA 729 Re Arogun and TaxPractitioners Board 85600

20110819-21 [2011] AATA 400 Re Griffith and FCT 83960

20111227-1228 [2011] AATA 758 Re Vaughan and FCT 85608

20111351 [2011] AATA 790 Re Craddon and FCT 81395

20111465 [2011] AATA 856 Re Iyengar and FCT 85924

20111594 [2011] AATA 878 Re Fitzgerald and FCT 85950

20111761 [2011] AATA 779 Re Applicant and FCT 85612

20111981 [2012] AATA 409 Re AP Group Ltd andFCT 83493

20112356 [2012] AATA 142 Re Taxpayer and FCT 87345

20112706 [2013] AATA 3 Re Taxpayer and FCT 87355

20112852 [2011] AATA 801 Re Luke and FCT 85626

20113905 [2012] AATA 133 Re Mason and FCT 87326

20114154 [2012] AATA 134 Re Lengyel and TaxPractitioners Board 87340

20114442 [2012] AATA 123 Re Tran and FCT 87322

20114699 [2013] AATA 28 Re Tom and FCT 87360

AT200323-27 [2004] AATA 1073 Re Taxpayer and FCT 85791

No 20103362 [2012] AATA 45 Re Bell and FCT 86692

No 20104319 [2012] AATA 44 Re Trustee for the R AliSuperannuation Fund and FCT 86826

NT2002198 [2004] AATA 202 Re Isaacs and FCT 80785

NT2002225-227 [2004] AATA 753 Re Ryan and FCT 82140

CLASSIFICATION OF AAT CASES BY REFERENCE NUMBER mdash continued

AAT Reference No AATATR Case ATR

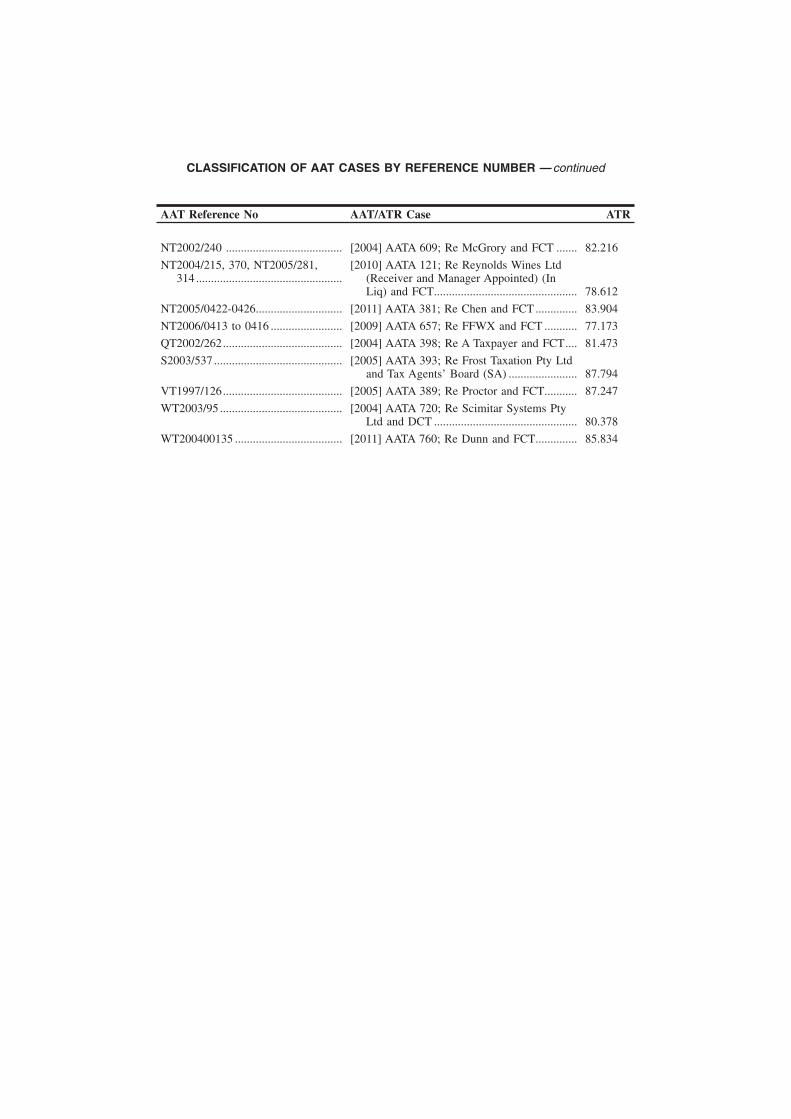

NT2002240 [2004] AATA 609 Re McGrory and FCT 82216

NT2004215 370 NT2005281314

[2010] AATA 121 Re Reynolds Wines Ltd(Receiver and Manager Appointed) (InLiq) and FCT 78612

NT20050422-0426 [2011] AATA 381 Re Chen and FCT 83904

NT20060413 to 0416 [2009] AATA 657 Re FFWX and FCT 77173

QT2002262 [2004] AATA 398 Re A Taxpayer and FCT 81473

S2003537 [2005] AATA 393 Re Frost Taxation Pty Ltdand Tax Agentsrsquo Board (SA) 87794

VT1997126 [2005] AATA 389 Re Proctor and FCT 87247

WT200395 [2004] AATA 720 Re Scimitar Systems PtyLtd and DCT 80378

WT200400135 [2011] AATA 760 Re Dunn and FCT 85834

CLASSIFICATION OF AAT CASES BY REFERENCE NUMBER mdashcontinued

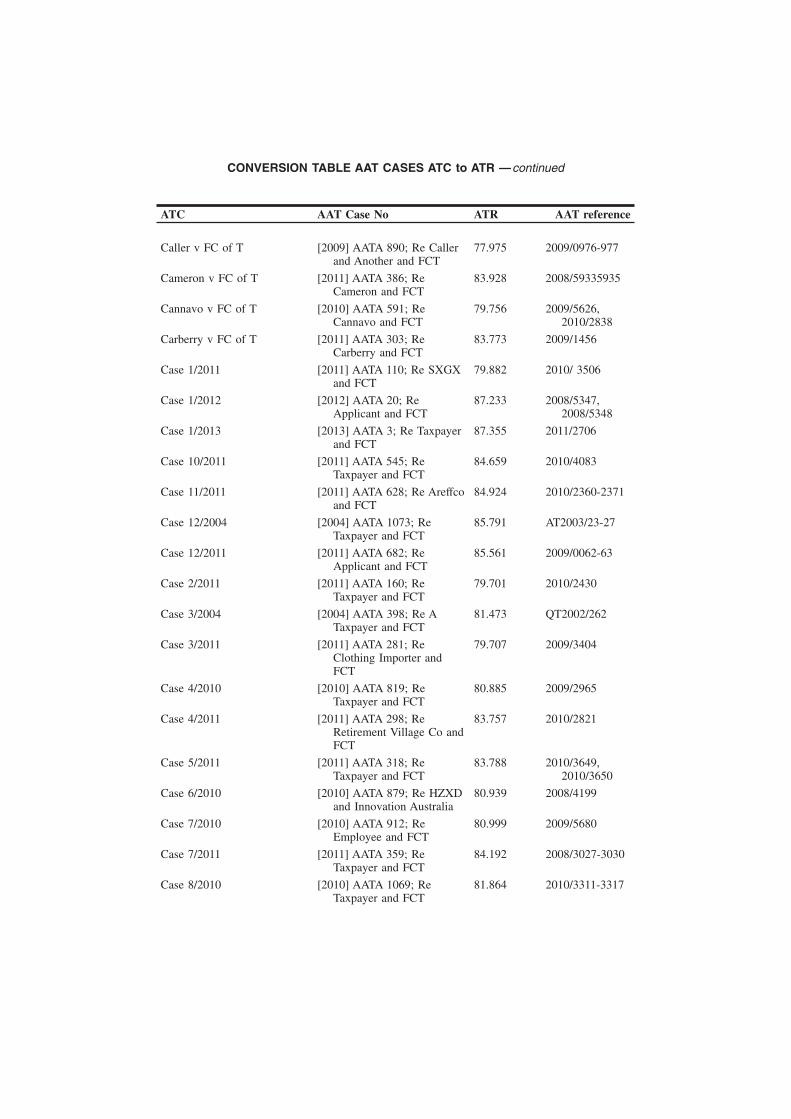

CONVERSION TABLE AAT CASES ATC to ATR

ATC AAT Case No ATR AAT reference

A amp C Sliwa Pty Ltd v FC ofT

[2011] AATA 390 Re A amp CSliwa Pty Ltd and FCT

83455 20095232

AP Group Ltd v FC of T [2012] AATA 409 Re APGroup Ltd and FCT

83493 20111981

Allan v FC of T [2011] AATA 860 Re Allanand FCT

85700 20110058

Allen J Middlebrook ampAssociates Pty Ltd v TaxPractitionersrsquo Board

[2010] AATA 622 Re Allen JMiddlebrook amp AssociatesPty Ltd and TaxPractitionersrsquo Board

80244 20095321

Andriopoulos v FC of T [2010] AATA 148 ReAndriopoulos and FCT

78654 20090663

Antonopoulos and Anor v FCof T

[2011] AATA 431 ReAntonopoulos and FCT

84311 2010119-120 2010121-122

Applicant 1761 of 2011 v FCof T

[2011] AATA 779 ReApplicant and FCT

85612 20111761

Arogun v Tax PractitionersBoard

[2011] AATA 729 Re Arogunand Tax PractitionersBoard

85600 20110781

BRMJCQ Pty Ltd v FC of T [2010] AATA 311 ReBRMJCQ Pty Ltd andFCT

79220 200855862008558720085588

Badaoui v FC of T [2011] AATA 672 ReBadaoui and Konig andFCT

81385 20102378

Bartercard Australia Pty Ltd vFC of T

[2010] AATA 1058 ReBartercard Australia PtyLtd and FCT

81836 20086172

Bell v FC of T [2012] AATA 45 Re Bell andFCT

86692 No 20103362

Beyond Productions Pty Ltd vScreen Australia

[2011] AATA 39 Re BeyondProductions Pty Ltd andScreen Australia

82194 20095568

Bicycle Victoria Inc v FC ofT

[2011] AATA 444 Re BicycleVictoria Incorporated andFCT

81924 2010172120101723

Brandon v FC of T [2010] AATA 530 ReBrandon and FCT

79712 20080180

Brown v FC of T [2010] AATA 829 Re Brownand FCT

80783 20094778

Buggins v FC of T [2011] AATA 698 ReBuggins and FCT

85590 201014372011040520110406

ATC AAT Case No ATR AAT reference

Caller v FC of T [2009] AATA 890 Re Callerand Another and FCT

77975 20090976-977

Cameron v FC of T [2011] AATA 386 ReCameron and FCT

83928 200859335935

Cannavo v FC of T [2010] AATA 591 ReCannavo and FCT

79756 2009562620102838

Carberry v FC of T [2011] AATA 303 ReCarberry and FCT

83773 20091456

Case 12011 [2011] AATA 110 Re SXGXand FCT

79882 2010 3506

Case 12012 [2012] AATA 20 ReApplicant and FCT

87233 2008534720085348

Case 12013 [2013] AATA 3 Re Taxpayerand FCT

87355 20112706

Case 102011 [2011] AATA 545 ReTaxpayer and FCT

84659 20104083

Case 112011 [2011] AATA 628 Re Areffcoand FCT

84924 20102360-2371

Case 122004 [2004] AATA 1073 ReTaxpayer and FCT

85791 AT200323-27

Case 122011 [2011] AATA 682 ReApplicant and FCT

85561 20090062-63

Case 22011 [2011] AATA 160 ReTaxpayer and FCT

79701 20102430

Case 32004 [2004] AATA 398 Re ATaxpayer and FCT

81473 QT2002262

Case 32011 [2011] AATA 281 ReClothing Importer andFCT

79707 20093404

Case 42010 [2010] AATA 819 ReTaxpayer and FCT

80885 20092965

Case 42011 [2011] AATA 298 ReRetirement Village Co andFCT

83757 20102821

Case 52011 [2011] AATA 318 ReTaxpayer and FCT

83788 2010364920103650

Case 62010 [2010] AATA 879 Re HZXDand Innovation Australia

80939 20084199

Case 72010 [2010] AATA 912 ReEmployee and FCT

80999 20095680

Case 72011 [2011] AATA 359 ReTaxpayer and FCT

84192 20083027-3030

Case 82010 [2010] AATA 1069 ReTaxpayer and FCT

81864 20103311-3317

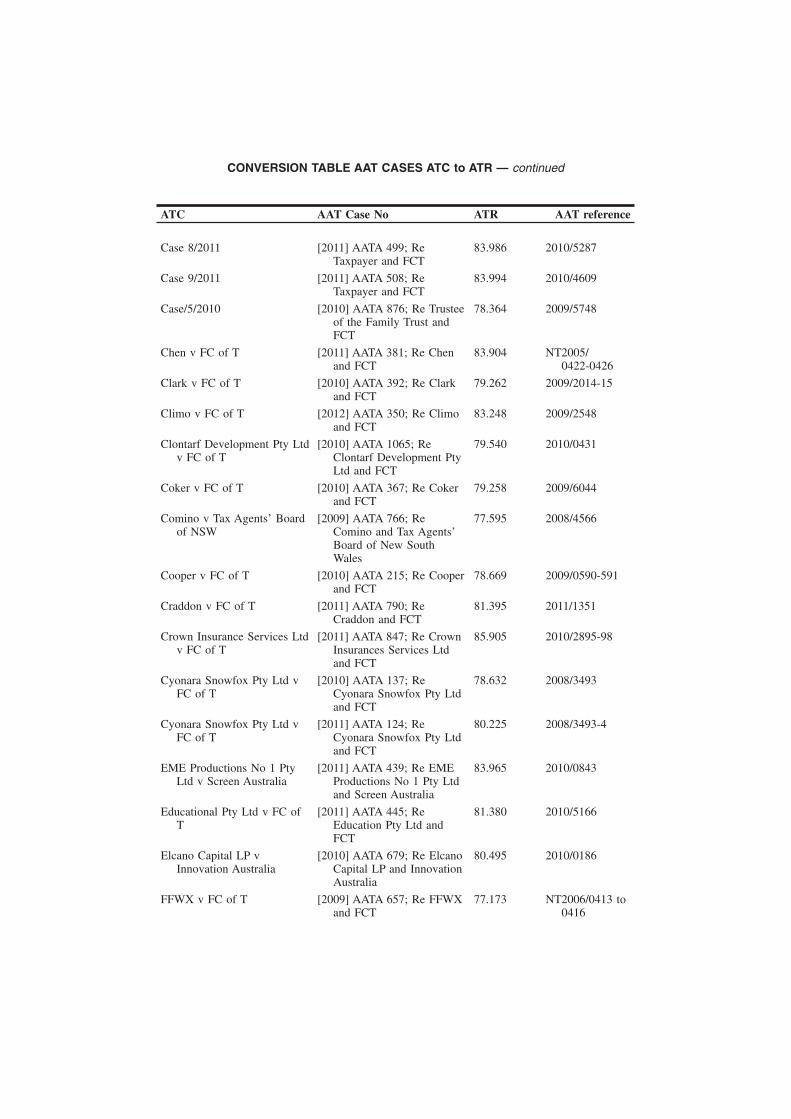

CONVERSION TABLE AAT CASES ATC to ATR mdashcontinued

ATC AAT Case No ATR AAT reference

Case 82011 [2011] AATA 499 ReTaxpayer and FCT

83986 20105287

Case 92011 [2011] AATA 508 ReTaxpayer and FCT

83994 20104609

Case52010 [2010] AATA 876 Re Trusteeof the Family Trust andFCT

78364 20095748

Chen v FC of T [2011] AATA 381 Re Chenand FCT

83904 NT20050422-0426

Clark v FC of T [2010] AATA 392 Re Clarkand FCT

79262 20092014-15

Climo v FC of T [2012] AATA 350 Re Climoand FCT

83248 20092548

Clontarf Development Pty Ltdv FC of T

[2010] AATA 1065 ReClontarf Development PtyLtd and FCT

79540 20100431

Coker v FC of T [2010] AATA 367 Re Cokerand FCT

79258 20096044

Comino v Tax Agentsrsquo Boardof NSW

[2009] AATA 766 ReComino and Tax AgentsrsquoBoard of New SouthWales

77595 20084566

Cooper v FC of T [2010] AATA 215 Re Cooperand FCT

78669 20090590-591

Craddon v FC of T [2011] AATA 790 ReCraddon and FCT

81395 20111351

Crown Insurance Services Ltdv FC of T

[2011] AATA 847 Re CrownInsurances Services Ltdand FCT

85905 20102895-98

Cyonara Snowfox Pty Ltd vFC of T

[2010] AATA 137 ReCyonara Snowfox Pty Ltdand FCT

78632 20083493

Cyonara Snowfox Pty Ltd vFC of T

[2011] AATA 124 ReCyonara Snowfox Pty Ltdand FCT

80225 20083493-4

EME Productions No 1 PtyLtd v Screen Australia

[2011] AATA 439 Re EMEProductions No 1 Pty Ltdand Screen Australia

83965 20100843

Educational Pty Ltd v FC ofT

[2011] AATA 445 ReEducation Pty Ltd andFCT

81380 20105166

Elcano Capital LP vInnovation Australia

[2010] AATA 679 Re ElcanoCapital LP and InnovationAustralia

80495 20100186

FFWX v FC of T [2009] AATA 657 Re FFWXand FCT

77173 NT20060413 to0416

CONVERSION TABLE AAT CASES ATC to ATR mdash continued

ATC AAT Case No ATR AAT reference

Fardell v FC of T [2011] AATA 725 Re Fardelland FCT

85812 20103760-3761

Fitzgerald v FC of T [2011] AATA 878 ReFitzgerald and FCT

85950 20111594

Fortune Corporation Pty Ltdand Another v TaxPractitionersrsquo Board

[2012] AATA 11 Re FortuneCorporation Pty Ltd andAnother and TaxPractitioners Board

85805 2011005720110061

France v FC of T [2010] AATA 858 Re Franceand FCT

80927 20094777

Frost Taxation Pty Ltd v TaxAgentsrsquo Board (SA)

[2005] AATA 393 Re FrostTaxation Pty Ltd and TaxAgentsrsquo Board (SA)

87794 S2003537

Gerard Cassegrain amp Co PtyLtd v FC of T

[2010] AATA 12 Re GerardCassegrain amp Co Pty Ltdand Another and FCT

78328 2007271620072719

Gilbert v FC of T [2010] AATA 882 Re Gilbertand FCT

80951 20083795-3797

Greenhatch v FC of T [2011] AATA 479 ReGreenhatch and FCT

80480 20094890

Griffith v FC of T [2011] AATA 400 Re Griffithand FCT

83960 20110819-21

Gunawan v FC of T [2012] AATA 119 ReGunawan and FCT

87315 20104217-421920104223-422520112792-2795

Heinrich v FC of T [2011] AATA 16 Re Heinrichand FCT

81903 20101764

Helbers v FC of T [2011] AATA 657 Re Helbersand FCT

85550 20093384-87

Hunt v FC of T [2011] AATA 69 Re Huntand FCT

82248 20102220-2221

Inglewood and DistrictsCommunity EnterprisesLtd v FC of T

[2011] AATA 607 ReInglewood and DistrictsCommunity EnterprisesLtd and FCT

84688 20102462

Isaacs v FC of T [2004] AATA 202 Re Isaacsand FCT

80785 NT2002198

Iyengar v FC of T [2011] AATA 856 Re Iyengarand FCT

85924 20111465

Jendahl Investments Pty Ltd vFC of T

[2009] AATA 881 Re JendahlInvestments Pty Ltd andFCT

77971 20085702-5704

Jungim Shin v FC of T [2010] AATA 1012 Re Shinand FCT

81627 20072795-2798

CONVERSION TABLE AAT CASES ATC to ATR mdashcontinued

ATC AAT Case No ATR AAT reference

Kakavas v FC of T [2011] AATA 48 Re Kakavasand FCT

82234 20101005

Kaley v FC of T [2011] AATA 480 Re Kaleyand FCT

85311 2010506420105065

Kerin v Tax Agentsrsquo Board ofSouth Australia

[2009] AATA 764 Re Kerinand Tax Agentsrsquo Board ofSouth Australia

77579 20085520

Knox v FC of T [2011] AATA 906 Re Knoxand FCT

86838 20102841-2844

Kocic amp Anor v FC of T [2011] AATA 47 Re Kocicand FCT

82211 1406-1409 of20083191-31993200-32084601-46034604-4606 of2007

Kolya v Tax PractitionersBoard

[2011] AATA 73 Re Kolyaand Tax PractitionersBoard

81912 20110005

Kolya v Tax PractitionersBoard (No 2)

[2011] AATA 804 Re Kolyaand Tax PractitionersBoard

85635 2010469520110005

Krishnamurti Australia Inc vFC of T

[2011] AATA 512 ReKrishnamurti Australia Incand FCT

84322 20095308

Lengyel v Tax PractitionersBoard

[2012] AATA 134 ReLengyel and TaxPractitioners Board

87340 20114154

Luke v FC of T [2011] AATA 801 Re Lukeand FCT

85626 20112852

MTAA Superannuation Fund(R G Casey Building)Property Pty Ltd v FC ofT

[2011] AATA 769 Re MTAASuperannuation Fund (R GCasey Building) PropertyPty Ltd and FCT

84334 20103083

Ma and Anor v FC of T [2012] AATA 47 Re Ma andEstate of Late Wai HungMa and FCT

87265 20102657-6220102663-65

MacMahon v FC of T [2010] AATA 724 ReMacMahon and FCT

80696 20082925-292720096129-613120103423-3425

MacMahon v FC of T [2011] AATA 809 ReMacMahon and FCT

85661 20103423-342520082925-292720096129-6131

CONVERSION TABLE AAT CASES ATC to ATR mdash continued

ATC AAT Case No ATR AAT reference

Mackay v FC of T [2011] AATA 593 ReMackay and FCT

82256 20094899-90120094921

Manne v FC of T [2010] AATA 398 Re Manneand FCT

79272 20092253 22544008

Mano v FC of T [2010] AATA 289 Re Manoand FCT

78981 20090228 - 37

Mason v FC of T [2012] AATA 133 Re Masonand FCT

87326 20113905

McGrory v FC of T [2004] AATA 609 ReMcGrory and FCT

82216 NT2002240

McMennemin v FC of T [2010] AATA 573 ReMcMennemin and FCT

79898 2009583820095839

Mold v FC of T [2011] AATA 823 Re Moldand FCT

83233 2008169120090559-60

Montgomery Wools Pty Ltd vFC of T

[2012] AATA 61 ReMontgomery Wools PtyLtd (As Trustee forMontgomery Wools PtyLtd Super Fund) and FCT

87282 20093486

Mortimer v Tax AgentsrsquoBoard (SA)

[2010] AATA 140 ReMortimer and Tax AgentsrsquoBoard of South Australia

78640 20090060

Mynott v FC of T [2011] AATA 539 Re Mynottand FCT

84594 20102689-92

National Jet Systems Pty Ltdv FC of T

[2011] AATA 766 ReNational Jet Systems PtyLtd and FCT

82740 201019942010376420103765

Newton v FC of T [2011] AATA 897 ReNewton (tas CombinedCare for the Elderly) andFCT

85959 20083923

Ng v FC of T [2011] AATA 399 Re Ng andFCT

83948 201000112010001220100013

Ohl and Anor v FC of T [2012] AATA 3 Re Ohl andFCT

85798 2010373720105022

Optimise Group ProprietaryLtd v FC of T

[2010] AATA 782 ReOptimise Group Pty Ltdand FCT

79953 20094082-4085

Park v FC of T [2011] AATA 567 Re Parkand FCT

84672 20104239-4240

Perfrement v FC of T [2011] AATA 264 RePerfrement and FCT

83737 20101310

Player v FC of T [2011] AATA 35 Re Playerand FCT

82184 20102473

CONVERSION TABLE AAT CASES ATC to ATR mdashcontinued

ATC AAT Case No ATR AAT reference

Pleno v Tax Agents Board [2010] AATA 526 Re Plenoand Tax Agentsrsquo Board

79533 2009569520100543

Print Applied Technology PtyLtd v FC of T

[2011] AATA 555 Re PrintApplied Technology PtyLtd and FCT

81992 20104592

Proctor v FC of T [2005] AATA 389 Re Proctorand FCT

87247 VT1997126

Proh v Tax Agents Board(Vic)

[2010] AATA 149 Re Prohand Tax Agentsrsquo Board ofVictoria

78663 20092614

QFL Photographics Pty Ltd vFC of T

[2010] AATA 758 Re QFLPhotographics Pty Ltd andFCT

80760 20091153

QFP Professional TomatoProject 98 v FC of T

[2010] AATA 864 Re QFPProfessional TomatoProject 98 and Others andFCT

78356 200815652008156620081567

Qantas Airways Ltd v FC ofT

[2010] AATA 977 Re QantasAirways Ltd and FCT

81170 20095513

Quality Food Production PtyLtd v FC of T

[2010] AATA 862 Re QualityFood Production Pty Ltdand FCT

80933 20072340200723412008486920092021

Reynolds Wines Ltd v FC ofT

[2010] AATA 121 ReReynolds Wines Ltd(Receiver and ManagerAppointed) (In Liq) andFCT

78612 NT2004215370NT2005281314

Rinaldo v FC of T [2011] AATA 839 ReRinaldo and FCT

85682 20103136

Ristevski v Tax PractitionersBoard

[2010] AATA 749 ReRistevski and TaxPractitioners Board

80742 20096010

Ryan v FC of T [2004] AATA 753 Re Ryanand FCT

82140 NT2002225-227

Scimitar Systems Pty Ltd vDeputy FC of T

[2004] AATA 720 ReScimitar Systems Pty Ltdand DCT

80378 WT200395

Sent v FC of T [2011] AATA 198 Re Sentand FCT

83211 2007184320092579

Shail Superannuation Fund vFC of T

[2011] AATA 940 Re ShailSuperannuation Fund andFCT

86339 2010095020100951

Sills v FC of T [2010] AATA 843 Re Sillsand FCT

80908 20092940-2941

CONVERSION TABLE AAT CASES ATC to ATR mdash continued

ATC AAT Case No ATR AAT reference

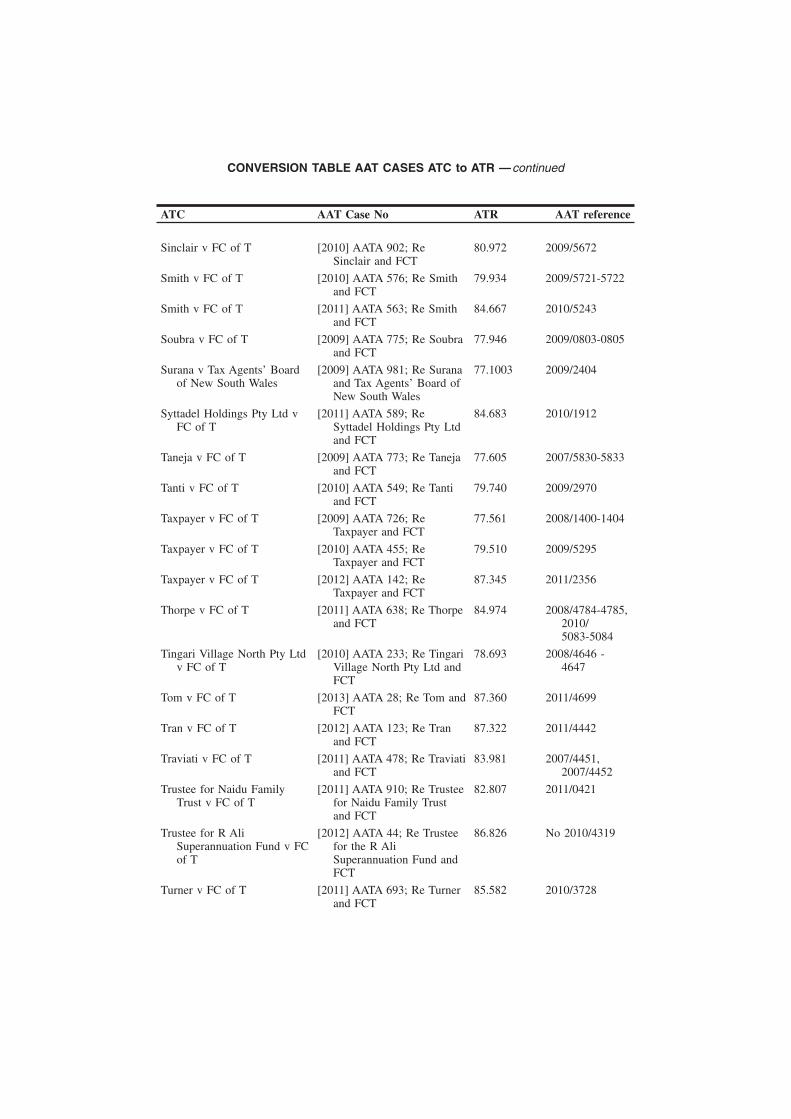

Sinclair v FC of T [2010] AATA 902 ReSinclair and FCT

80972 20095672

Smith v FC of T [2010] AATA 576 Re Smithand FCT

79934 20095721-5722

Smith v FC of T [2011] AATA 563 Re Smithand FCT

84667 20105243

Soubra v FC of T [2009] AATA 775 Re Soubraand FCT

77946 20090803-0805

Surana v Tax Agentsrsquo Boardof New South Wales

[2009] AATA 981 Re Suranaand Tax Agentsrsquo Board ofNew South Wales

771003 20092404

Syttadel Holdings Pty Ltd vFC of T

[2011] AATA 589 ReSyttadel Holdings Pty Ltdand FCT

84683 20101912

Taneja v FC of T [2009] AATA 773 Re Tanejaand FCT

77605 20075830-5833

Tanti v FC of T [2010] AATA 549 Re Tantiand FCT

79740 20092970

Taxpayer v FC of T [2009] AATA 726 ReTaxpayer and FCT

77561 20081400-1404

Taxpayer v FC of T [2010] AATA 455 ReTaxpayer and FCT

79510 20095295

Taxpayer v FC of T [2012] AATA 142 ReTaxpayer and FCT

87345 20112356

Thorpe v FC of T [2011] AATA 638 Re Thorpeand FCT

84974 20084784-478520105083-5084

Tingari Village North Pty Ltdv FC of T

[2010] AATA 233 Re TingariVillage North Pty Ltd andFCT

78693 20084646 -4647

Tom v FC of T [2013] AATA 28 Re Tom andFCT

87360 20114699

Tran v FC of T [2012] AATA 123 Re Tranand FCT

87322 20114442

Traviati v FC of T [2011] AATA 478 Re Traviatiand FCT

83981 2007445120074452

Trustee for Naidu FamilyTrust v FC of T

[2011] AATA 910 Re Trusteefor Naidu Family Trustand FCT

82807 20110421

Trustee for R AliSuperannuation Fund v FCof T

[2012] AATA 44 Re Trusteefor the R AliSuperannuation Fund andFCT

86826 No 20104319

Turner v FC of T [2011] AATA 693 Re Turnerand FCT

85582 20103728

CONVERSION TABLE AAT CASES ATC to ATR mdashcontinued

ATC AAT Case No ATR AAT reference

Vaughan v FC of T [2011] AATA 758 ReVaughan and FCT

85608 20111227-1228

Vaughan v FC of T [2011] AATA 760 Re Dunnand FCT

85834 WT200400135

Venturi v FC of T [2011] AATA 588 Re Venturiand FCT

84905 20101378

Victorian HealthcareAssociation Ltd v FC of T

[2010] AATA 473 ReVictorian HealthcareAssociation Ltd and FCT

79890 2009207520092077-9

Waters v FC of T [2010] AATA 846 Re Watersand FCT

80919 20102559-2560

Willis v FC of T [2010] AATA 420 Re Willisand FCT

79287 20090851

Wynnum Holdings No 1 PtyLtd v FC of T

[2011] AATA 296 ReWynnum Holdings No 1Pty Ltd and FCT

83444 20085986

Yalos Engineering Pty Ltd vFC of T

[2010] AATA 408 Re YalosEngineering Pty Ltd andFCT

79282 2007301820073019

Yip v FC of T [2011] AATA 785 Re Yipand FCT

82761 20100599-060120100965-0967

CONVERSION TABLE AAT CASES ATC to ATR mdash continued

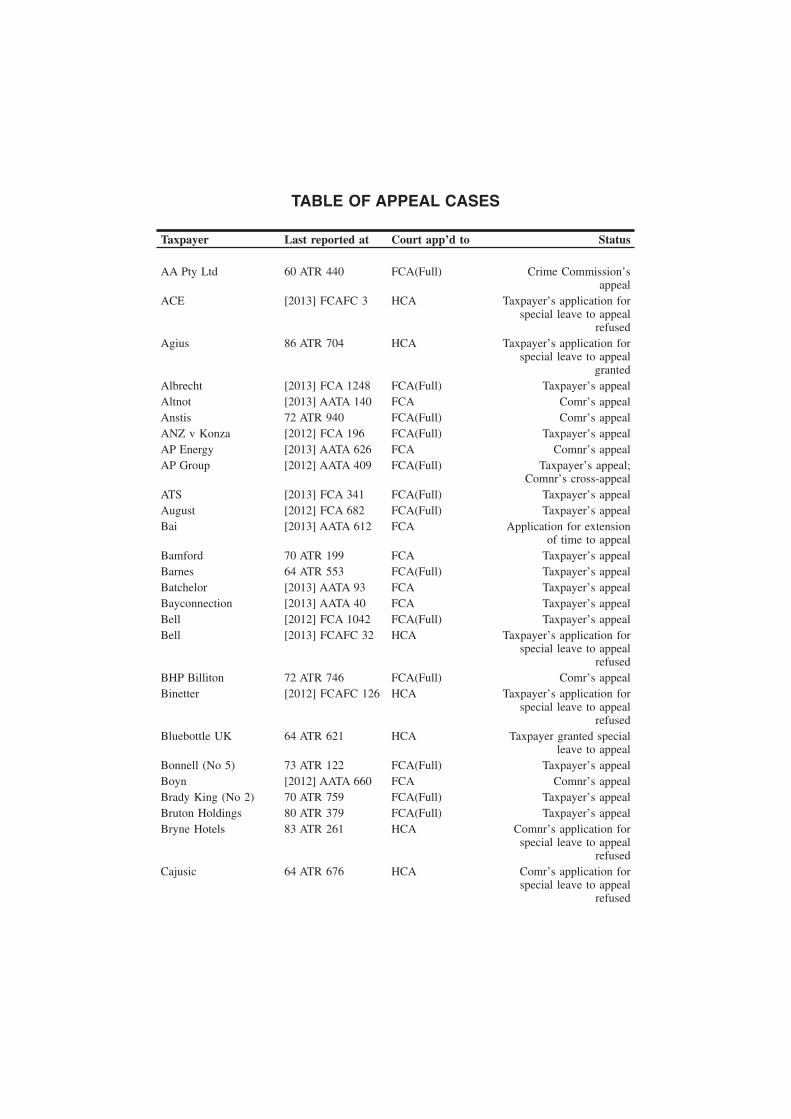

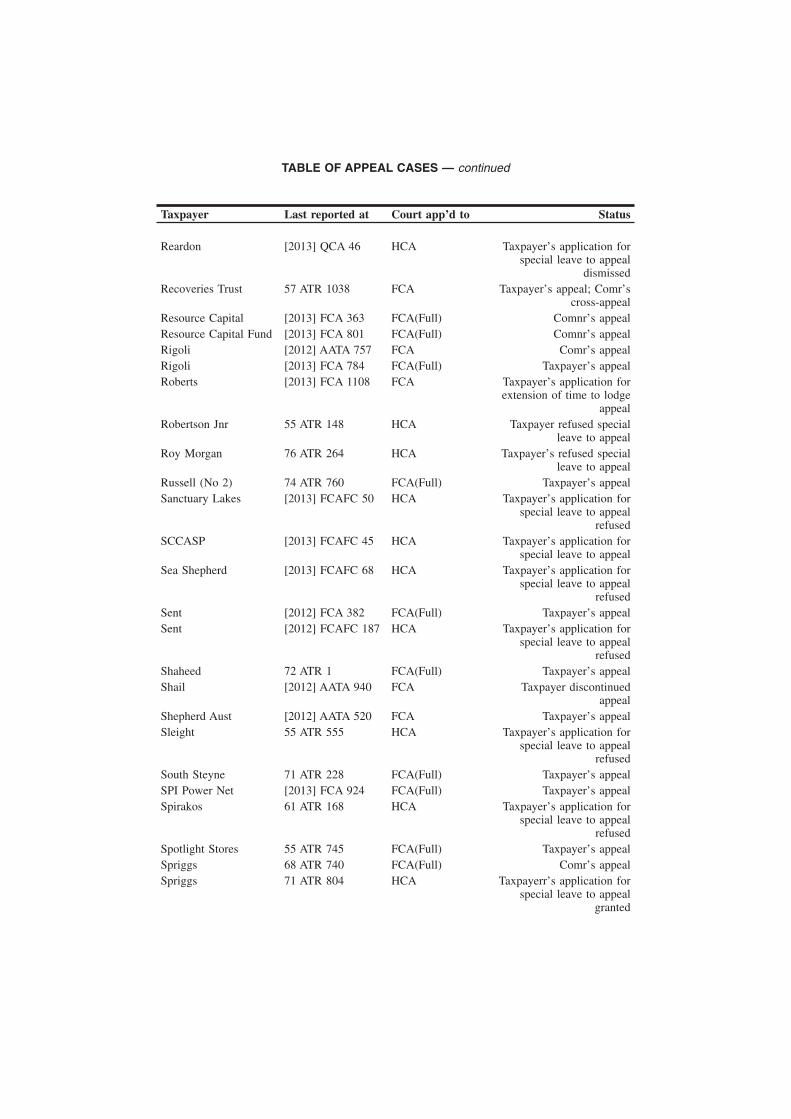

TABLE OF APPEAL CASES

Taxpayer Last reported at Court apprsquod to Status

AA Pty Ltd 60 ATR 440 FCA(Full) Crime Commissionrsquosappeal

ACE [2013] FCAFC 3 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Agius 86 ATR 704 HCA Taxpayerrsquos application forspecial leave to appeal

granted

Albrecht [2013] FCA 1248 FCA(Full) Taxpayerrsquos appeal

Altnot [2013] AATA 140 FCA Comrrsquos appeal

Anstis 72 ATR 940 FCA(Full) Comrrsquos appeal

ANZ v Konza [2012] FCA 196 FCA(Full) Taxpayerrsquos appeal

AP Energy [2013] AATA 626 FCA Comnrrsquos appeal

AP Group [2012] AATA 409 FCA(Full) Taxpayerrsquos appealComnrrsquos cross-appeal

ATS [2013] FCA 341 FCA(Full) Taxpayerrsquos appeal

August [2012] FCA 682 FCA(Full) Taxpayerrsquos appeal

Bai [2013] AATA 612 FCA Application for extensionof time to appeal

Bamford 70 ATR 199 FCA Taxpayerrsquos appeal

Barnes 64 ATR 553 FCA(Full) Taxpayerrsquos appeal

Batchelor [2013] AATA 93 FCA Taxpayerrsquos appeal

Bayconnection [2013] AATA 40 FCA Taxpayerrsquos appeal

Bell [2012] FCA 1042 FCA(Full) Taxpayerrsquos appeal

Bell [2013] FCAFC 32 HCA Taxpayerrsquos application forspecial leave to appeal

refused

BHP Billiton 72 ATR 746 FCA(Full) Comrrsquos appeal

Binetter [2012] FCAFC 126 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Bluebottle UK 64 ATR 621 HCA Taxpayer granted specialleave to appeal

Bonnell (No 5) 73 ATR 122 FCA(Full) Taxpayerrsquos appeal

Boyn [2012] AATA 660 FCA Comnrrsquos appeal

Brady King (No 2) 70 ATR 759 FCA(Full) Taxpayerrsquos appeal

Bruton Holdings 80 ATR 379 FCA(Full) Taxpayerrsquos appeal

Bryne Hotels 83 ATR 261 HCA Comnrrsquos application forspecial leave to appeal

refused

Cajusic 64 ATR 676 HCA Comrrsquos application forspecial leave to appeal

refused

Taxpayer Last reported at Court apprsquod to Status

Cameron [2012] FCAFC 76 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Cancer amp BowelResearch

[2013] AATA 336 FCA Comrrsquos appeal

Carter [2013] AATA 141 FCA Application for extensionof time to appeal

discontinued

CCM [2013] NSWSC1072

NSWCA Comnrrsquos appeal

CC Pty Ltd 68 ATR 834 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Central Equity 83 ATR 550 FCA(Full) Taxpayer discontinuedappeal

Centro 86 ATR 28 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Challenger 84 ATR 576 HCA Comnrrsquos application forspecial leave to appeal

refused

City Link 57 ATR 316 HCA Comrrsquos appeal

Clarke 69 ATR 724 HCA Taxpayerrsquos application forspecial leave to appeal

granted

Coal Developments 68 ATR 869 FCA(Full) Taxpayerrsquos appeal

Colby 71 ATR 62 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Coleambally Irrigation 57 ATR 104 FCA(Full) Taxpayerrsquos application forspecial leave to appeal

Coleambally Irrigation 57 ATR 104 HCA Taxpayer refused specialleave to appeal

Collection Point [2012] FCA 720 FCA(Full) Taxpayerrsquos appeal

Commonwealth Bank 75 ATR 273 FCA(Full) Taxpayerrsquos appeal

Condell 63 ATR 514 FCA(Full) Taxpayerrsquos appeal

ConnectEast 72 ATR 84 FCA(Full) Taxpayerrsquos appeal

Consolidated Media 83 ATR 793 HCA Comnrrsquos application forspecial leave to appeal

granted

Crown Insurance [2012] FCAFC 153 HCA Comnrrsquos application forspecial leave to appeal

dismissed

Cumins 68 ATR 39 HCA Taxpayerrsquos application forspecial leave to appeal

refused

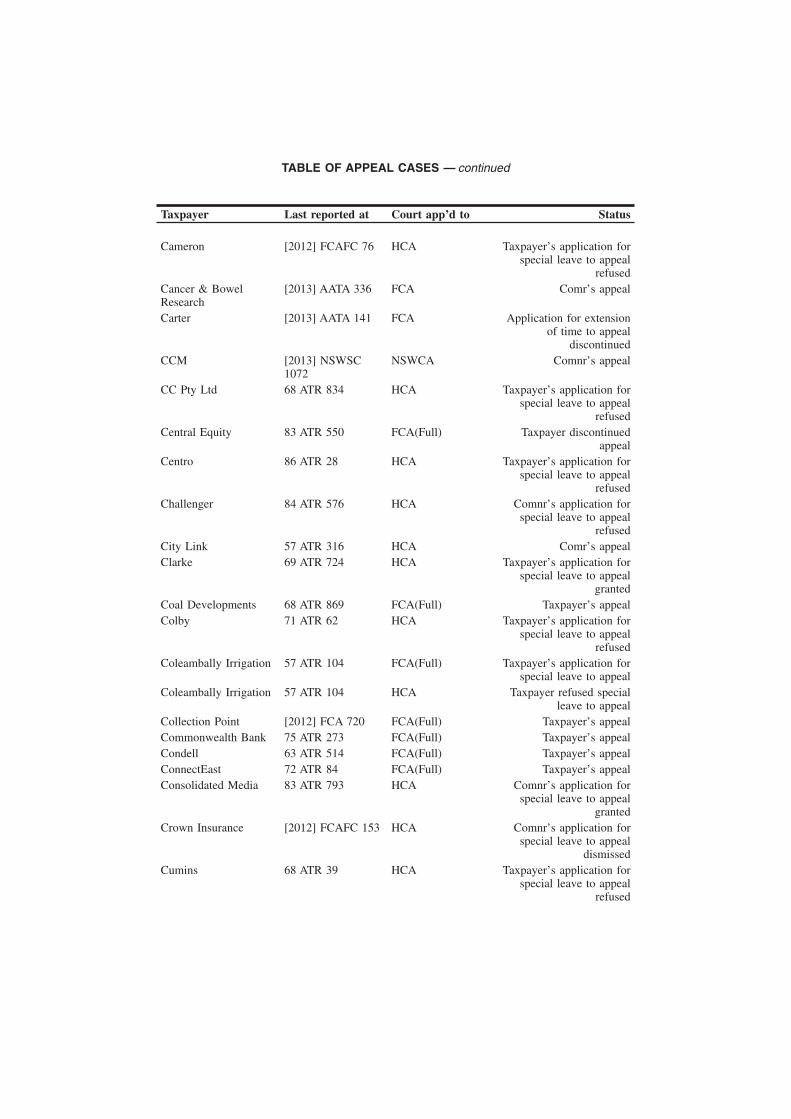

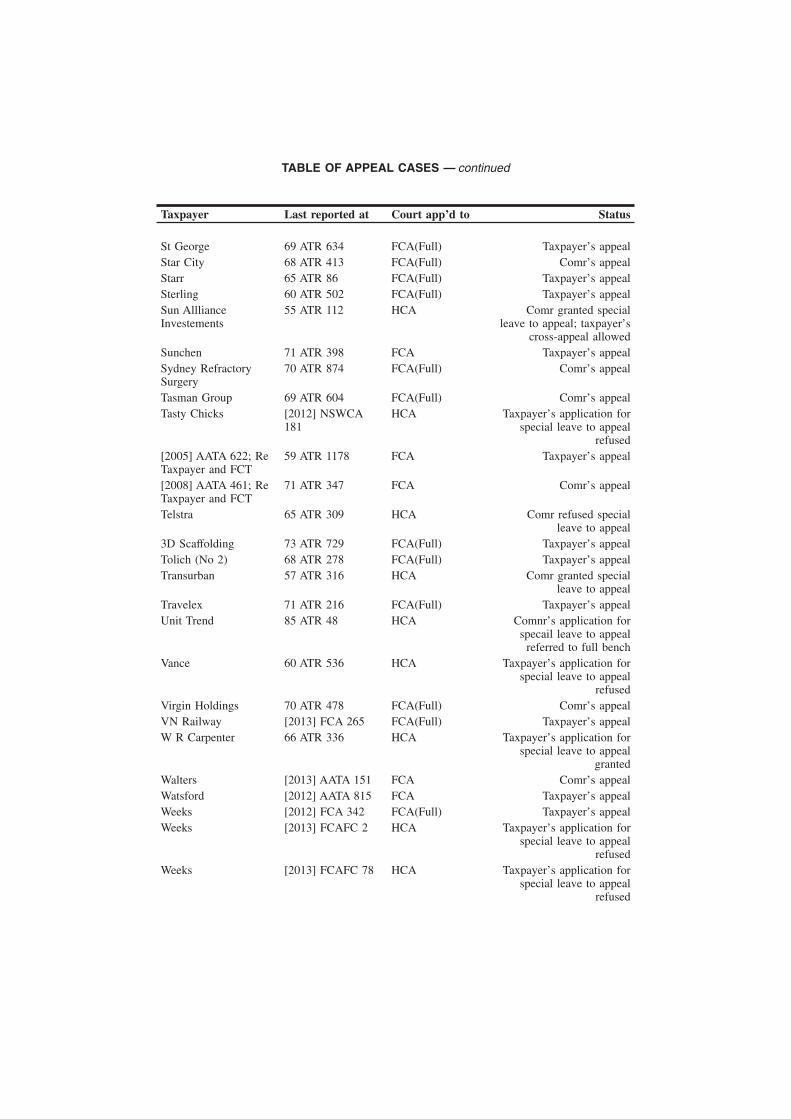

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

Cumins 70 ATR 855 FCA(Full) Taxpayerrsquos application forleave to appeal

Cyonara Snowfox [2012] FCAFC 177 HCA Taxpayerrsquos application forspecial leave to appeal

dismissed

Day 62 ATR 530 FCA(Full) Comrrsquos appeal

DB Rreef 59 ATR 388 FCA(Full) Comrrsquos appeal

DB Rreef 62 ATR 699 HCA Comrrsquos application forspecial leave to appeal

Day 67 ATR 936 HCA Comr granted specialleave to appeal

DesalinationTechnology

[2013] AATA 846 FCA Comrrsquos appeal

Devereaux 66 ATR 691 FCA(Full) Taxpayerrsquos appeal

Dick v DCT 67 ATR 762 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Dickinson [2013] AATA 25 FCA Comnrrsquos appeal

Dickinson [2013] AATA 26 FCA Comnrrsquos appeal

Dickinson [2013] FCAFC 99 HCA Application for specialleave to appeal

Dowling [2013] AATA 49 FCA Comnrrsquos appeal

Dreamtech 78 ATR 532 FCA(Full) Taxpayerrsquos appeal

Egglishaw 68 ATR 822 FCA(Full) Applicantrsquos appeal

Egglishaw (No 2) 71 ATR 570 FCA(Full) Applicantrrsquos appeal

Eldersmede 56 ATR 1179 FCA(Full) Taxpayerrsquos appeal

Ell 61 ATR 661 FCA(Full) Taxpayerrsquos appeal

Elsinora 61 ATR 482 FCA(Full) Comrrsquos appeal

Epov 65 ATR 399 FCA(Full) Taxpayerrsquos appeal

Ergon Energy 61 ATR 366 FCA(Full) Taxpayerrsquos appeal

Esso AustraliaResources

87 ATR 124 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Experienced Tours 63 ATR 1147 Comrrsquos appeal Taxpayerrsquosappeal

Fabig [2013] FCAFC 99 HCA Application for specialleave to appeal

Fardell 85 ATR 812 FCA Comnr discontinuedappeal

Fortescue [2013] HCA 34 HCA Taxpayerrsquos appeal

Fowler [2012] FCA 1040 FCA(Full) Taxpayerrsquos appeal

Frugtniet [2013] AATA 188 FCA Taxpayerrsquos appeal

Futuris 63 ATR 562 FCA (Full) Taxpayerrsquos appeal

Futuris 66 ATR 719 HCA Application for specialleave to appeal granted

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

Gail Freeman 66 ATR 763 FCA(Full) Taxpayerrsquos appeal

Gashi [2013] FCAFC 30 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Gem Plant Hire [2012] AATA 852 FCA Comnrrsquos applicationdiscontinued

Gloxinia 75 ATR 806 HCA Comnrrsquos application forspecial leave to appeal

refused

Greenhatch [2012] FCAFC 84 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Guss 61 ATR 135 FCA(Full) Taxpayerrsquos appeal

HampR Super [2012] FCA 1052 FCA(Full) Taxpayerrsquos appeal

Hancox [2012] AATA 836 FCA Taxpayerrsquos appeal

Hart 86 ATR 476 HCA Taxpayerrsquos application forspecial leave to appealComnrrsquos application for

special leave to appealrefused

Hastie Group 70 ATR 353 FCA(Full) Taxpayerrsquos appeal

HC Legal [2013] FCA 45 FCA(Full) Taxpayerrsquos appeal

Healey [2012] FCA 269 FCA(Full) Taxpayerrsquos appeal

Healey [2012] FCAFC 194 HCA Taxpayerrsquos application forspecial leave to appeal

Hogan (No 4) 72 ATR 107 FCA(Full) Applicantrsquos appeal

Hornibrook 61 ATR 573 FCA(Full) Comrrsquos appeal

Howard [2012] FCAFC 149 HCA Taxpayerrsquos application forspecial leave to appeal

granted on one ground andrefused on the other

Hua Wang BankBerhad

80 ATR 449 FCA(Full) Taxpayerrsquos appeal

Hua Wang BankBerhad

[2012] FCA 938 FCA(Full) Taxpayerrsquos appeal

Hunger Project [2013] FCA 693 FCA(Full) Comnrrsquos appeal

Interhealth Energies 87 ATR 164 FCA(Full) Taxpayerrsquos appeal

International Finance 74 ATR 125 HCA Applicantrsquos application forspecial leave to appeal

granted

IOOF Holdings [2013] AATA 239 FCA Taxpayerrsquos appeal

IOOF Holdings [2013] FCA 1189 FCA(Full) Taxpayerrsquos appeal

Jewiss 61 ATR 254 HCA Taxpayer refused specialleave to appeal

JMA Accounting 56 ATR 327 FCA(Full) Taxpayerrsquos appeal

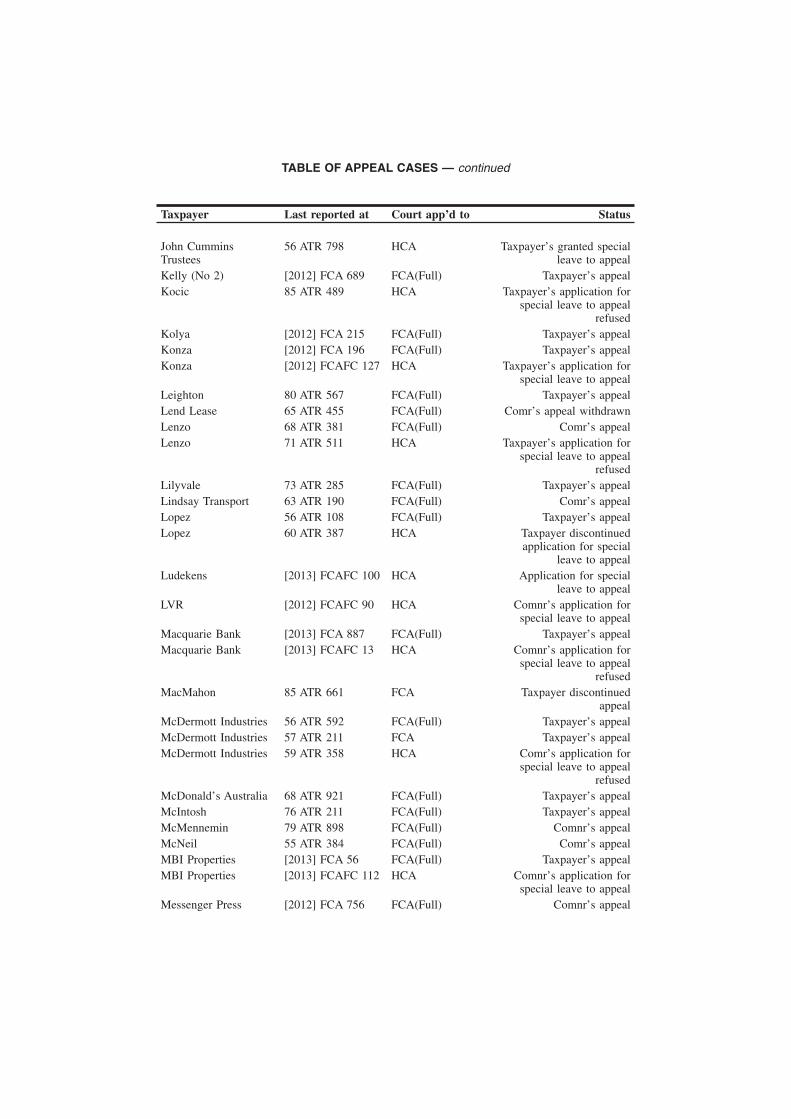

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

John CumminsTrustees

56 ATR 798 HCA Taxpayerrsquos granted specialleave to appeal

Kelly (No 2) [2012] FCA 689 FCA(Full) Taxpayerrsquos appeal

Kocic 85 ATR 489 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Kolya [2012] FCA 215 FCA(Full) Taxpayerrsquos appeal

Konza [2012] FCA 196 FCA(Full) Taxpayerrsquos appeal

Konza [2012] FCAFC 127 HCA Taxpayerrsquos application forspecial leave to appeal

Leighton 80 ATR 567 FCA(Full) Taxpayerrsquos appeal

Lend Lease 65 ATR 455 FCA(Full) Comrrsquos appeal withdrawn

Lenzo 68 ATR 381 FCA(Full) Comrrsquos appeal

Lenzo 71 ATR 511 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Lilyvale 73 ATR 285 FCA(Full) Taxpayerrsquos appeal

Lindsay Transport 63 ATR 190 FCA(Full) Comrrsquos appeal

Lopez 56 ATR 108 FCA(Full) Taxpayerrsquos appeal

Lopez 60 ATR 387 HCA Taxpayer discontinuedapplication for special

leave to appeal

Ludekens [2013] FCAFC 100 HCA Application for specialleave to appeal

LVR [2012] FCAFC 90 HCA Comnrrsquos application forspecial leave to appeal

Macquarie Bank [2013] FCA 887 FCA(Full) Taxpayerrsquos appeal

Macquarie Bank [2013] FCAFC 13 HCA Comnrrsquos application forspecial leave to appeal

refused

MacMahon 85 ATR 661 FCA Taxpayer discontinuedappeal

McDermott Industries 56 ATR 592 FCA(Full) Taxpayerrsquos appeal

McDermott Industries 57 ATR 211 FCA Taxpayerrsquos appeal

McDermott Industries 59 ATR 358 HCA Comrrsquos application forspecial leave to appeal

refused

McDonaldrsquos Australia 68 ATR 921 FCA(Full) Taxpayerrsquos appeal

McIntosh 76 ATR 211 FCA(Full) Taxpayerrsquos appeal

McMennemin 79 ATR 898 FCA(Full) Comnrrsquos appeal

McNeil 55 ATR 384 FCA(Full) Comrrsquos appeal

MBI Properties [2013] FCA 56 FCA(Full) Taxpayerrsquos appeal

MBI Properties [2013] FCAFC 112 HCA Comnrrsquos application forspecial leave to appeal

Messenger Press [2012] FCA 756 FCA(Full) Comnrrsquos appeal

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

Mills 83 ATR 384 HCA Taxpayerrsquos application forspecial leave to appeal

granted

Milne [2012] NSWCCA24

HCA Application for specialleave to appeal granted

Miniello 70 ATR 843 FCA(Full) Comrrsquos appeal

Multiflex 81 ATR 347 FCA(Full) Comnrrsquos appeal

Murray [2012] AATA 557 FCA Taxpayerrsquos appeal

Nash [2012] AATA 719 FCA Comnrrsquos appeal

National Mutual 74 ATR 173 FCA(Full) Taxpayerrsquos appeal

National Mutual Life [2011[ SASCFC106

HCA Taxpayerrsquos application forspecial leave to appeal

refused

Nelson [2012] AATA 579 FCA Taxpayerrsquos appeal

Nicholls 74 ATR 381 FCA(Full) Applicantrsquos appeal

Oswal [2013] FCA 745 FCA(Full) Taxpayerrsquos appeal

Pacific National 69 ATR 857 HCA Taxpayerrsquos application forspecial leave to appeal

granted

Parks Holdings 56 ATR 210 FCA(Full) Taxpayerrsquos appeal

Parliamentary Trustee [2012] FCA 720 FCA(Full) Taxpayerrsquos appeal

Pratt Holdings [2012] FCA 1075 FCA(Full) Taxpayerrsquos appeal

Pratt Holdings [2013] FCAFC 82 HCA Taxpayerrsquos application forspecial leave to appeal

Pre-Paid ProfessionalAssoc

73 ATR 779 FCA(Full) Taxpayerrsquos appeal

Price Street 66 ATR 1 FCA(Full) Taxpayerrsquos appeal

Pryke 64 ATR 152 QCA Comrrsquos appeal

PTTEP [2013] FCA 1175 FCA(Full) Taxpayerrsquos appeal

Purvis [2013] AATA 58 FCA Taxpayerrsquos application forextension of time to

appeal

Qantas 81 ATR 816 HCA Comnrrsquos application forspecial leave to appeal

granted

Rafland 62 ATR 49 FCA(Full) Taxpayerrsquos appeal

Rafland 65 ATR 336 HCA Taxpayer granted specialleave to appeal

Ramsden 56 ATR 42 FCA(Full) Comrrsquos appeal

Ramsden 58 ATR 485 HCA Taxpayerrsquos special leaveto appeal refused

Rawson [2012] FCA 753 FCA(Full) Taxpayerrsquos appeal

RCI 80 ATR 122 FCA(Full) Taxpayerrsquos appeal

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

Reardon [2013] QCA 46 HCA Taxpayerrsquos application forspecial leave to appeal

dismissed

Recoveries Trust 57 ATR 1038 FCA Taxpayerrsquos appeal Comrrsquoscross-appeal

Resource Capital [2013] FCA 363 FCA(Full) Comnrrsquos appeal

Resource Capital Fund [2013] FCA 801 FCA(Full) Comnrrsquos appeal

Rigoli [2012] AATA 757 FCA Comrrsquos appeal

Rigoli [2013] FCA 784 FCA(Full) Taxpayerrsquos appeal

Roberts [2013] FCA 1108 FCA Taxpayerrsquos application forextension of time to lodge

appeal

Robertson Jnr 55 ATR 148 HCA Taxpayer refused specialleave to appeal

Roy Morgan 76 ATR 264 HCA Taxpayerrsquos refused specialleave to appeal

Russell (No 2) 74 ATR 760 FCA(Full) Taxpayerrsquos appeal

Sanctuary Lakes [2013] FCAFC 50 HCA Taxpayerrsquos application forspecial leave to appeal

refused

SCCASP [2013] FCAFC 45 HCA Taxpayerrsquos application forspecial leave to appeal

Sea Shepherd [2013] FCAFC 68 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Sent [2012] FCA 382 FCA(Full) Taxpayerrsquos appeal

Sent [2012] FCAFC 187 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Shaheed 72 ATR 1 FCA(Full) Taxpayerrsquos appeal

Shail [2012] AATA 940 FCA Taxpayer discontinuedappeal

Shepherd Aust [2012] AATA 520 FCA Taxpayerrsquos appeal

Sleight 55 ATR 555 HCA Taxpayerrsquos application forspecial leave to appeal

refused

South Steyne 71 ATR 228 FCA(Full) Taxpayerrsquos appeal

SPI Power Net [2013] FCA 924 FCA(Full) Taxpayerrsquos appeal

Spirakos 61 ATR 168 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Spotlight Stores 55 ATR 745 FCA(Full) Taxpayerrsquos appeal

Spriggs 68 ATR 740 FCA(Full) Comrrsquos appeal

Spriggs 71 ATR 804 HCA Taxpayerrrsquos application forspecial leave to appeal

granted

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

St George 69 ATR 634 FCA(Full) Taxpayerrsquos appeal

Star City 68 ATR 413 FCA(Full) Comrrsquos appeal

Starr 65 ATR 86 FCA(Full) Taxpayerrsquos appeal

Sterling 60 ATR 502 FCA(Full) Taxpayerrsquos appeal

Sun AlllianceInvestements

55 ATR 112 HCA Comr granted specialleave to appeal taxpayerrsquos

cross-appeal allowed

Sunchen 71 ATR 398 FCA Taxpayerrsquos appeal

Sydney RefractorySurgery

70 ATR 874 FCA(Full) Comrrsquos appeal

Tasman Group 69 ATR 604 FCA(Full) Comrrsquos appeal

Tasty Chicks [2012] NSWCA181

HCA Taxpayerrsquos application forspecial leave to appeal

refused

[2005] AATA 622 ReTaxpayer and FCT

59 ATR 1178 FCA Taxpayerrsquos appeal

[2008] AATA 461 ReTaxpayer and FCT

71 ATR 347 FCA Comrrsquos appeal

Telstra 65 ATR 309 HCA Comr refused specialleave to appeal

3D Scaffolding 73 ATR 729 FCA(Full) Taxpayerrsquos appeal

Tolich (No 2) 68 ATR 278 FCA(Full) Taxpayerrsquos appeal

Transurban 57 ATR 316 HCA Comr granted specialleave to appeal

Travelex 71 ATR 216 FCA(Full) Taxpayerrsquos appeal

Unit Trend 85 ATR 48 HCA Comnrrsquos application forspecail leave to appeal

referred to full bench

Vance 60 ATR 536 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Virgin Holdings 70 ATR 478 FCA(Full) Comrrsquos appeal

VN Railway [2013] FCA 265 FCA(Full) Taxpayerrsquos appeal

W R Carpenter 66 ATR 336 HCA Taxpayerrsquos application forspecial leave to appeal

granted

Walters [2013] AATA 151 FCA Comrrsquos appeal

Watsford [2012] AATA 815 FCA Taxpayerrsquos appeal

Weeks [2012] FCA 342 FCA(Full) Taxpayerrsquos appeal

Weeks [2013] FCAFC 2 HCA Taxpayerrsquos application forspecial leave to appeal

refused

Weeks [2013] FCAFC 78 HCA Taxpayerrsquos application forspecial leave to appeal

refused

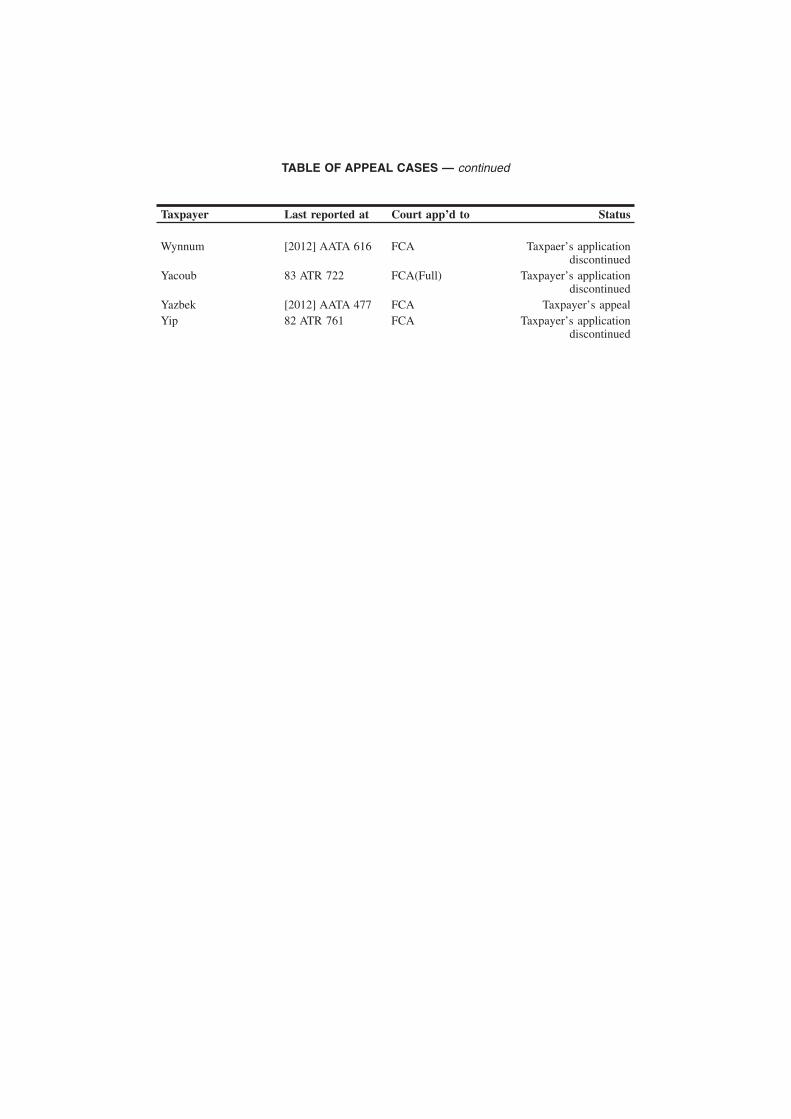

TABLE OF APPEAL CASES mdash continued

Taxpayer Last reported at Court apprsquod to Status

Wynnum [2012] AATA 616 FCA Taxpaerrsquos applicationdiscontinued

Yacoub 83 ATR 722 FCA(Full) Taxpayerrsquos applicationdiscontinued

Yazbek [2012] AATA 477 FCA Taxpayerrsquos appeal

Yip 82 ATR 761 FCA Taxpayerrsquos applicationdiscontinued

TABLE OF APPEAL CASES mdash continued

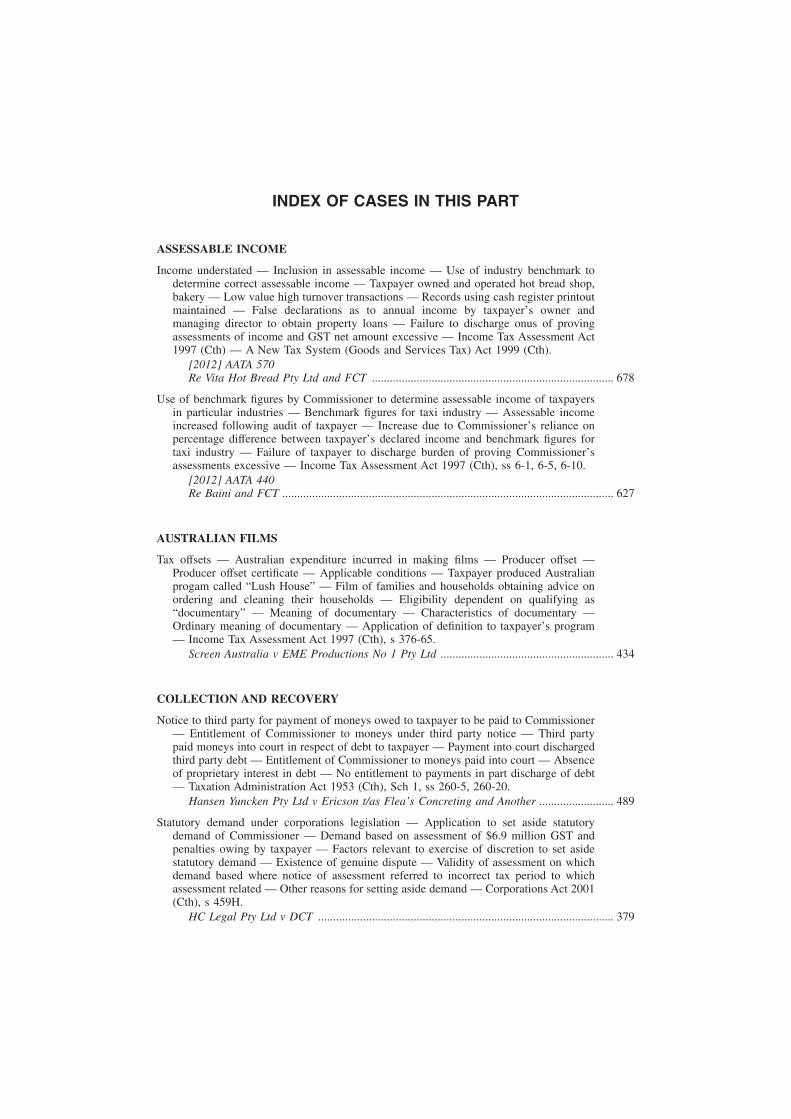

INDEX OF CASES IN THIS PART

ASSESSABLE INCOME

Income understated mdash Inclusion in assessable income mdash Use of industry benchmark todetermine correct assessable income mdash Taxpayer owned and operated hot bread shopbakery mdash Low value high turnover transactions mdash Records using cash register printoutmaintained mdash False declarations as to annual income by taxpayerrsquos owner andmanaging director to obtain property loans mdash Failure to discharge onus of provingassessments of income and GST net amount excessive mdash Income Tax Assessment Act1997 (Cth) mdash A New Tax System (Goods and Services Tax) Act 1999 (Cth)

[2012] AATA 570Re Vita Hot Bread Pty Ltd and FCT 678

Use of benchmark figures by Commissioner to determine assessable income of taxpayersin particular industries mdash Benchmark figures for taxi industry mdash Assessable incomeincreased following audit of taxpayer mdash Increase due to Commissionerrsquos reliance onpercentage difference between taxpayerrsquos declared income and benchmark figures fortaxi industry mdash Failure of taxpayer to discharge burden of proving Commissionerrsquosassessments excessive mdash Income Tax Assessment Act 1997 (Cth) ss 6-1 6-5 6-10

[2012] AATA 440Re Baini and FCT 627

AUSTRALIAN FILMS

Tax offsets mdash Australian expenditure incurred in making films mdash Producer offset mdashProducer offset certificate mdash Applicable conditions mdash Taxpayer produced Australianprogam called ldquoLush Houserdquo mdash Film of families and households obtaining advice onordering and cleaning their households mdash Eligibility dependent on qualifying asldquodocumentaryrdquo mdash Meaning of documentary mdash Characteristics of documentary mdashOrdinary meaning of documentary mdash Application of definition to taxpayerrsquos programmdash Income Tax Assessment Act 1997 (Cth) s 376-65

Screen Australia v EME Productions No 1 Pty Ltd 434

COLLECTION AND RECOVERY

Notice to third party for payment of moneys owed to taxpayer to be paid to Commissionermdash Entitlement of Commissioner to moneys under third party notice mdash Third partypaid moneys into court in respect of debt to taxpayer mdash Payment into court dischargedthird party debt mdash Entitlement of Commissioner to moneys paid into court mdash Absenceof proprietary interest in debt mdash No entitlement to payments in part discharge of debtmdash Taxation Administration Act 1953 (Cth) Sch 1 ss 260-5 260-20

Hansen Yuncken Pty Ltd v Ericson tas Flearsquos Concreting and Another 489

Statutory demand under corporations legislation mdash Application to set aside statutorydemand of Commissioner mdash Demand based on assessment of $69 million GST andpenalties owing by taxpayer mdash Factors relevant to exercise of discretion to set asidestatutory demand mdash Existence of genuine dispute mdash Validity of assessment on whichdemand based where notice of assessment referred to incorrect tax period to whichassessment related mdash Other reasons for setting aside demand mdash Corporations Act 2001(Cth) s 459H

HC Legal Pty Ltd v DCT 379

COLLECTION AND RECOVERY mdash continued

Summary judgment mdash Application by Commissioner in respect of income tax assessmentsmdash Defence by taxpayer mdash Application to stay judgment pending taxpayerrsquosapplication for special leave to appeal to High Court on challenge to assessments mdashFactors relevant to applications mdash Summary judgment granted

DCT v Sent 394

CORPORATIONS

Tax liability mdash Tax debt for over $12000000 mdash Capital gain from sale of shares inAustralian mining company mdash Taxpayer company resident in Cayman Islands mdashInterlocutory application for freezing orders mdash Jurisdiction mdash Grounds for substitutedservice mdash Income Tax Assessment Act 1997 (Cth) s 855-15 mdash Income TaxAssessment Act 1936 (Cth) s 177 mdash Federal Court Rules 2011 (Cth) r 735(4)

FCT v Regent Pacific Group Ltd and Others 364

CRIMINAL LAW

Conspiracy to defraud the Commonwealth mdash Conviction mdash Sentencing mdash Accusedinvolved in overseas tax minimisation scheme mdash One accused promoter of scheme mdashOther accused employee of accountant implementing scheme mdash Sentencingconsiderations mdash Appropriate sentences mdash Crimes Act 1914 (Cth) ss 17A 29D 86(1)mdash Criminal Code Act 1995 (Cth) s 1354(5)

R v Agius R v Zerafa 528

GOODS AND SERVICES TAX

GST net amount mdash Reliance on benchmark figures by Commissioner for assessment mdashTaxi industry mdash A New Tax System (Goods and Services Tax) Act 1999 (Cth)

[2012] AATA 440Re Baini and FCT 627

Partnership at general law mdash Partnership for taxation purposes mdash Non-entity joint venturemdash Indicia of existence of partnership mdash Taxpayers entered into agreement withcompany to purchase and develop property mdash Agreement provided for sharing equallyof all costs liabilities mortgages and proceeds derived from any sale arising from theproperty mdash Characterisation of relationship mdash Liability for GST unpaid by other partymdash Date for deregistration of registered entity mdash Income Tax Assessment Act1997 (Cth) s 995-1 definition of ldquopartnershiprdquo ldquonon-entity joint venturerdquo

[2012] AATA 401Re Yacoub and Another and FCT 612

Supply mdash Consideration mdash Taxable supply mdash Incentive payments by manufacturers tomotor vehicle dealers mdash Taxpayer group representative for GST purposes mdash Whetherpayments consideration for supply by taxpayer to manufacturer mdash Whetherconsideration for supply by taxpayer to customer mdash Meaning of supply mdash Meaning ofconsideration mdash Availability of refund to taxpayer for overpaid GST mdash A New TaxSystem (Goods and Services Tax) Act 1999 (Cth) ss 9-10 9-15 105-65

[2012] AATA 617Re AP Group Ltd and FCT 692

INDEX

LAND TAX

Exemptions mdash Land owned by or held in trust for club not carried on for profit mdashRequirements for trust mdash Whether met mdash Whether owner included ldquolesseerdquo mdash Landnot exempt mdash Land Tax Management Act 1956 (NSW) ss 3 10(1)(g)(iii) (h)

Panthers Investment Corporation Pty Ltd and Another v Chief Commissioner ofState Revenue 369

Exemptions mdash Ordinary land tax mdash Special land tax mdash Land ldquoavailable for occupation assupported residential servicerdquo mdash Taxpayer owned land on which registered supportedresidential accommodation provided by lessee of land mdash Registration ceased mdash Lesseedeparted mdash Land sold 5 years later mdash Exemption for land granted as supportedresidential service mdash Re-assessments following discovery of termination of registrationmdash Availability of exemption mdash Meaning of ldquoavailable for occupationrdquo mdash Land TaxAct 1958 (Vic)

Re Tate-Louery amp Dwyer Pty Ltd (As Trustee for the Cash Wheeler Unit Trust) andCommissioner of State Revenue 429

Grouping provisions mdash Determination by Commissioner mdash Validity of determination mdashChallenge by taxpayers to grouping mdash Failure by Commissioner to makedetermination as to grouping mdash Availability of challenge to failure to makedetermination mdash Determination encompassed within consideration of objection mdashChallenge to determination only by way of appeal against assessment of land taxliability mdash Conclusiveness of assessment mdash Prejudice to taxpayers where failure tomake determination mdash Land Tax Act 1958 (Vic) s 44(3) mdash Land Tax Act 2005 (Vic)ss 46A 47 50 mdash Taxation Administration Act 1997 (Vic) s 20

Re Aston (Aust) Properties Pty Ltd and Others and Commissioner of StateRevenue 402

PARTNERSHIP

Tax law partnership mdash Elements of tax law partnership mdash Taxpayer registered proprietorof a rental property mdash Received rental income into account in his name alone mdash Paidexpenses for property from same bank account mdash Income returned on basis thatincome derived jointly by taxpayer and wife mdash No written partnership agreement mdashAbsence of evidence from wife mdash No partnership tax returns lodged mdash Existence oftax law partnership not proven mdash Assessments attributing whole rental income totaxpayer not excessive mdash Income Tax Assessment Act 1997 (Cth) s 995-1 definition ofldquopartnershiprdquo mdash Income Tax Assessment Act 1936 (Cth) s 91

[2013] AATA 8Re Harbutt and FCT 698

PAY-ROLL TAX

Grouping of taxpayers mdash Discretion to de-group taxpayers mdash Taxpayer service companyof 2 groups of pharmacies owned by the individual or her mother mdash Some ldquowhollyownedrdquo pharmacies mdash Others ldquoindependentrdquo pharmacies operated under partnershipagreements with third parties mdash Correctness of Commissionerrsquos decision not tode-group wholly owned and independent pharmacies mdash Relevant factors mdash Degree ofcontrol under partnership agreements mdash Banking financial employment control mdashSignatory to leases and other agreements between partnerships and third parties mdashOwnership interests including 50 per cent share of profits mdash Payroll Tax Act 1971(Qld) ss 68 69 71

Re Verra Pty Ltd (As Trustee for the Pharmacies Services Trust) and Others andCommissioner of State Revenue 417

INDEX

PENALTIES AND OFFENCES

Penalty for recklessness mdash Remission of penalty mdash Taxpayer reckless in understatingincome and GST mdash Test of recklessness mdash Limit on remission in cases of recklessnessmdash Taxation Administration Act 1953 (Cth) Sch 1 ss 284-75 284-90

[2012] AATA 570Re Vita Hot Bread Pty Ltd and FCT 678

Statements false and misleading in a material particular mdash Failure to keep records bytaxpayer mdash Tax returns of taxpayer led to assessments of lower taxation liability mdash Noremission of penalty warranted mdash Taxation Administration Act 1953 (Cth) Sch 1s 284-75(1)

[2012] AATA 440Re Baini and FCT 627

PRACTICE AND PROCEDURE

AAT has power to make findings of fact on other matters relevant to resolution of reviewmdash AATrsquos inability to determine an issue crucial to the outcome of the review a relevantconsideration mdash Failure to defer hearing would be neither fair just economical norquick mdash AAT defers its proceedings pending determination of Supreme Courtproceedings mdash Withdrawal of application pending determination of Supreme Courtproceedings cannot be made subject to a right to have application automaticallyreinstated at a later time mdash Administrative Appeals Tribunal Act 1975 (Cth) ss 41(2)(4) 42A(1) (1A) (1B) (8) (9) (10) 42C(1) 42D 43 mdash Taxation Administration Act1953 (Cth) ss 14ZS(1) (2) (4) 14ZZ 14ZZ(a) 14ZZE 14ZZJ 14ZZK 14ZZO14ZZP

[2012] AATA 150Re Kalafatis and FCT 585

STAMP DUTY

ldquoLandholderrdquo mdash 60 per cent of value of property to which taxpayer entitled ldquolandrdquo mdashDuty payable on property mdash Taxpayer company operated freight rail services mdashSubsidiaries of taxpayer acquired rights under land use agreements with StateGovernment mdash Shares in taxpayer sold mdash Whether sale of shares in landholder subjectto duty mdash Characterisation of rights under land use agreements as contractual notproprietary rights mdash Characterisation of track infrastructure mdash Whether fixtures atcommon law mdash Whether ldquolandrdquo within definition in duties legislation mdash Whether landwithin definition in Acts interpretation legislation mdash Proper characterisation of otherleased railway infrastructure mdash Stamp Act 1921 (WA) ss 76(1) 76AP mdashInterpretation Act 1984 (WA) s 5

Re Westnet Rail Holdings No 1 Pty Ltd and Another and Commissioner of StateRevenue 448

Assessments mdash Dutiable value mdash Agreements for sale of dutiable property mdashAgreements required consideration in respect of land and other contributions includinginfrastructure and land remediation payments to be paid before transfer of land mdashCharacterisation of other amounts payable as dutiable amounts paid in respect of saleof land mdash Duties Act 2000 (Vic)

Lend Lease Development Pty Ltd and Others v Chief Commissioner of StateRevenue 504

Transfer of land by trustee of unit trusts mdash Liability to duty mdash Existence of trust notestablished mdash Duties Act 2000 (Vic)

Re Aston (Aust) Properties Pty Ltd and Others and Commissioner of StateRevenue 402

INDEX

SUPERANNUATION

Concessional contributions mdash Contributions cap mdash Excess contributions mdash Excesscontributions tax mdash Commissionerrsquos discretion to disregard or re-allocate contributionsto different income year mdash Excess concessional contributions made in financial yearfor taxpayer mdash Widespread misunderstanding of application of contributions limits infinancial services industry mdash Existence of special circumstances not satisfied mdashEveryone shared common misunderstanding mdash Nothing to suggest that taxpayerrsquos casespecial mdash Mistake in interpreting legislation not special circumstances mdash Income TaxAssessment Act 1997 (Cth) s 292-465

[2012] AATA 762Re Dickinson and FCT 695

Concessional contributions mdash Contributions cap mdash Excess contributions mdash Excesscontributions tax mdash Commissionerrsquos discretion to disregard or re-allocate contributionsto different income year mdash Salary sacrifice arrangement between taxpayer andemployer mdash Concessional contributions paid by employer in arrears mdash Contributionspaid in July related to previous June mdash Excess concessional contributions made in 2financial years mdash Control by taxpayer over amount and timing of contributions mdashForeseeability of excess contributions being made in relevant income year mdash Existenceof special circumstances mdash Unjust unreasonable or inappropriate outcome mdash IncomeTax Assessment Act 1997 (Cth) s 292-465(3)

[2012] AATA 130Re Naude and FCT 561

Concessional contributions mdash Contributions cap mdash Excess contributions mdash Excesscontributions tax mdash Commissionerrsquos discretion to disregard or re-allocate contributionsto different income year mdash Superannuation guarantee contributions paid on behalf oftaxpayer by employer mdash Concessional contributions paid by employer in arrears mdashContributions paid in July related to previous quarter mdash Excess concessionalcontributions made in financial year mdash Foreseeability of excess contributions beingmade in relevant income year mdash Existence of special circumstances mdash Unjustunreasonable or inappropriate outcome mdash Effect of Income Tax Assessment Act 1997(Cth) s 292-465(3)

[2012] AATA 140Re Peaker and FCT 578

Superannuation guarantee charge mdash Employee mdash Extended meaning of employee mdashContract principally for labour of person mdash Payments to perform or participate inentertainment or sport mdash Taxpayer paid tandem master parachutists to assist inparachute jumps of customers mdash Also required tandem masters to video jump andtransfer to CD or DVD mdash Characterisation of tandem masters as employees withinnormal usage mdash Also employees within extended meaning of term mdash Integration withcore business of taxpayer mdash Degree of control by taxpayer mdash SuperannuationGuarantee (Administration) Act 1992 (Cth) s 12(1) (3) (8)

[2012] AATA 120Re General Aviation Maintenance Pty Ltd and FCT 552

Superannuation guarantee charge mdash Meaning of ldquosalary or wagesrdquo mdash Scope of definitionmdash Reimbursements of motor vehicle expenses mdash Taxpayer paid employee driversamounts allocated 80 per cent to motor vehicle reimbursement expenses and 20 percent to wages mdash Superannuation guarantee contributions not paid on ldquoreimbursementrdquoexpenses mdash Characterisation of reimbursement expenses as salary or wages mdashSuperannuation guarantee charge underpaid mdash Superannuation Guarantee Charge Act1992 (Cth) mdash Superannuation Guarantee (Administration) Act 1992 (Cth) s 11

[2013] AATA 10Re Penrowse Pty Ltd and FCT 703

INDEX

TAX AGENTS

Registration mdash Fact finding role of the Administrative Appeals Tribunal mdash Adequacy ofreasons provided mdash Findings on material questions of fact mdash Need to identify aquestion of law mdash Jurisdiction of the court on appeal mdash Administrative AppealsTribunal Act 1975 (Cth) ss 37 39 43 44 mdash Income Tax Assessment Act 1936 (Cth)Pt VIIA Div 2 s 251K mdash Tax Agent Services Act 2009 (Cth) ss 20-5 20-15 20-2540-5 90-1 mdash Tax Agent Services (Transitional Provisions and ConsequentialAmendments) Act 2009 (Cth) Sch 2 item 1

Kolya v Tax Practitioners Board and Another 474

WORDS AND PHRASES

ldquoOwnerrdquo

Panthers Investment Corporation Pty Ltd and Another v Chief Commissioner ofState Revenue 369

INDEX

Cameron R v (NSWCCAmdashFull Court) (2012) 192

DCT v Seabrooke (FCAmdashSiopis J) (2012) 217DCT v Sent (VSCmdashMukhtar AsJ) (2013) 394DCT HC Legal Pty Ltd v (FCAmdashMurphy J) (2013) 379Dickinson and FCT Re (AATmdashP E Hack Deputy President and

B J McCabe Senior Member) (2012) 695EME Productions No 1 Pty Ltd Screen Australia v (FCAmdashFull

Court) (2012) 434Ericson tas Flearsquos Concreting Hansen Yuncken Pty Ltd v

(QSCmdashMcMurdo J) (2012) 489

Esso Australia Resources Pty Ltd v FCT (FCAmdashFull Court) (2012) 124

FCT v Interhealth Energies Pty Ltd (As Trustee of the Interhealth SuperannuationFund) (FCAmdashLogan J) (2012) 164

FCT v Regent Pacific Group Ltd (FCAmdashSiopis J) (2013) 364

FCT v Unit Trend Services Pty Ltd (HCAmdashFull Court) (2013) 13

FCT Esso Australia Resources Pty Ltd v (FCAmdashFull Court) (2012) 124

FCT Sent v (FCAmdashFull Court) (2012) 223

FCT Unit Trend Services Pty Ltd v (FCAmdashLogan J) (2013) 1General Aviation Maintenance Pty Ltd and FCT Re

(AATmdashF OrsquoLoughlin Senior Member) (2012) 552

Gunawan and FCT Re (AATmdashM D Allen Senior Member) (2012) 315Hansen Yuncken Pty Ltd v Ericson tas Flearsquos Concreting

(QSCmdashMcMurdo J) (2012) 489Harbutt and FCT Re (AATmdashS E Frost Deputy President) (2013) 698HC Legal Pty Ltd v DCT (FCAmdashMurphy J) (2013) 379

Interhealth Energies Pty Ltd (As Trustee of the Interhealth Superannuation Fund) FCTv (FCAmdashLogan J) (2012) 164

Kalafatis and FCT Re (AATmdashS A Forgie Deputy President)(2012) 585

Kalomel Nominees Pty Ltd v Commissioner of State Taxation (SASCmdashGray J) (2012) 88Kolya v Tax Practitioners Board (FCAmdashFlick J) (2012) 474Lend Lease Development Pty Ltd v Chief Commissioner of State

Revenue (VSCmdashPagone J) (2012) 504

Lengyel and Tax Practitioners Board Re (AATmdashM D Allen Senior Member) (2012) 340

Ma and Estate of Late Wai Hung Ma and FCT Re (AATmdashJ L RedfernSenior Member) (2012) 265

Mason and FCT Re (AATmdashC R Walsh Senior Member) (2012) 326

Montgomery Wools Pty Ltd (As Trustee for Montgomery Wools Pty Ltd Super Fund)and FCT Re (AATmdashJ L Redfern Senior Member) (2012) 282

Naude and FCT Re (AATmdashA Sweidan Senior Member) (2012) 561Panthers Investment Corporation Pty Ltd v Chief Commissioner

of State Revenue (NSWSCmdashGzell J) (2013) 369Peaker and FCT Re (AATmdashS Webb Member) (2012) 578Penrowse Pty Ltd and FCT Re (AATmdashK S Levy Senior Member)

(2013) 703

Port Augusta Medical Centre Pty Ltd v Commissioner of State Taxation (SASCmdashFullCourt) (2012) 102

R v Agius (NSWSCmdashSimpson J) (2012) 528

R v Boughen (NSWCCAmdashFull Court) (2012) 192

(Cases in bold reported in this part)

TABLE OF CASES REPORTED

R v Cameron (NSWCCAmdashFull Court) (2012) 192R v Zerafa (NSWSCmdashSimpson J) (2012) 528Regent Pacific Group Ltd FCT v (FCAmdashSiopis J) (2013) 364Screen Australia v EME Productions No 1 Pty Ltd (FCAmdashFull

Court) (2012) 434

Seabrooke DCT v (FCAmdashSiopis J) (2012) 217

Sent v FCT (FCAmdashFull Court) (2012) 223Sent DCT v (VSCmdashMukhtar AsJ) (2013) 394State Revenue Chief Commissioner of Lend Lease Development

Pty Ltd v (VSCmdashPagone J) (2012) 504State Revenue Chief Commissioner of Panthers Investment

Corporation Pty Ltd v (NSWSCmdashGzell J) (2013) 369State Revenue Commissioner of Re Aston (Aust) Properties Pty

Ltd and (VCATmdashJ Glover Member) (2012) 402State Revenue Commissioner of Re Tate-Louery amp Dwyer Pty

Ltd (As Trustee for the Cash Wheeler Unit Trust) and(VCATmdashJudge Macnamara Vice-President) (2012) 429

State Revenue Commissioner of Re Verra Pty Ltd (As Trustee forthe Pharmacies Services Trust) and (QCATmdashP McDermottMember) (2012) 417

State Revenue Commissioner of Re Westnet Rail Holdings No 1Pty Ltd and (WASATmdashChaney J President) (2012) 448

State Taxation Commissioner of Kalomel Nominees Pty Ltd v (SASCmdashGray J)(2012) 88

State Taxation Commissioner of Port Augusta Medical Centre Pty Ltd v (SASCmdashFullCourt) (2012) 102

Stewart Australian Crime Commission v (FCAmdashStone J) (2012) 31Tate-Louery amp Dwyer Pty Ltd (As Trustee for the Cash Wheeler

Unit Trust) and Commissioner of State Revenue Re(VCATmdashJudge Macnamara Vice-President) (2012) 429

Tax Practitioners Board Kolya v (FCAmdashFlick J) (2012) 474

Taxpayer and FCT Re (AATmdashB Tamberlin Deputy President) (2012) 345

Taxpayer and FCT Re (AATmdashB J McCabe Senior Member) (2013) 355

Tom and FCT Re (AATmdashR Deutsch Deputy President) (2013) 360

Tran and FCT Re (AATmdashG Hughes Member) (2012) 322

Unit Trend Services Pty Ltd v FCT (FCAmdashLogan J) (2013) 1

Unit Trend Services Pty Ltd FCT v (HCAmdashFull Court) (2013) 13Verra Pty Ltd (As Trustee for the Pharmacies Services Trust) and

Commissioner of State Revenue Re (QCATmdashP McDermottMember) (2012) 417

Vita Hot Bread Pty Ltd and FCT Re (AATmdashG EttingerSenior Member) (2012) 678

Westnet Rail Holdings No 1 Pty Ltd and Commissioner of StateRevenue Re (WASATmdashChaney J President) (2012) 448

Yacoub and FCT Re (AATmdashJagot J Presidential Member) (2012) 612Zerafa R v (NSWSCmdashSimpson J) (2012) 528

(Cases in bold reported in this part)

TABLE OF CASES REPORTED

TABLE OF CASES JUDICIALLY CONSIDERED IN THIS PART

Adams Trustees of Estate of v Commissioner of Pay-roll Tax (Vic) (1980) 143 CLR 629

Applied [2013] AATA 10 Re Penrowse Pty Ltd and FCT 703

Karingal 2 Holdings Pty Ltd v Commissioner of State Revenue (2002) 51 ATR 190

Applied Panthers Investment Corporation Pty Ltd and Another vChief Commissioner of State Revenue 369

Lygon Nominees Pty Ltd v Commissioner of State Revenue (2007) 23 VR 474

Applied Panthers Investment Corporation Pty Ltd and Another vChief Commissioner of State Revenue 369

Nguyen and FCT Re (2011) 84 ATR 618

Applied [2012] AATA 570 Re Vita Hot Bread Pty Ltd and FCT 678

Sgardelis and FCT Re (2007) 68 ATR 963

Followed [2012] AATA 570 Re Vita Hot Bread Pty Ltd and FCT 678

Tasty Chicks Pty Ltd v Chief Commissioner of State Revenue (NSW) (2011) 245 CLR 446

Followed Re Verra Pty Ltd (As Trustee for the PharmaciesServices Trust) and Others and Commissioner of State Revenue 417

TSC 2000 Pty Ltd and FCT Re (2007) 66 ATR 945

Followed [2012] AATA 570 Re Vita Hot Bread Pty Ltd and FCT 678

STATUTES RULES ETCJUDICIALLY CONSIDERED IN THIS PART

COMMONWEALTHA New Tax System (Goods and Services Tax) Act 1999 627 678

s 9-10 692

s 9-15 692

s 105-65 692

Administrative Appeals Tribunal Act 1975

s 37 474

s 39 474

s 41(2) 585

s 41(4) 585

s 42A(1) 585

s 42A(1A) 585

s 42A(1B) 585

s 42A(8) 585

s 42A(9) 585

s 42A(10) 585

s 42C(1) 585

s 42D 585

s 43 474 585

s 44 474

Corporations Act 2001

s 459H 379

Crimes Act 1914

s 17A 528

s 29D 528

s 86(1) 528

Criminal Code Act 1995

s 1354(5) 528

Federal Court Rules 2011

r 735(4) 364

Income Tax Assessment Act 1936

Pt VIIA Div 2 474

s 91 698

s 177 364

s 251K 474Income Tax Assessment Act 1997 678

s 6-1 627

s 6-5 627

s 6-10 627

s 292-465 695

s 292-465(3) 561 578

s 376-65 434

s 855-15 364

s 995-1 612 698

Superannuation Guarantee (Administration) Act 1992

s 11 703

s 12(1) 552

s 12(3) 552

s 12(8) 552Superannuation Guarantee Charge Act 1992 703

Tax Agent Services Act 2009

s 20-5 474

s 20-15 474

s 20-25 474

s 40-5 474

s 90-1 474