Embed Size (px)

Citation preview

IT’S ALL ABOUT MONEY, HONEY!

AnalystAshutosh Narkar 5549 1767([email protected])

DealingSandeepa Arora 5549 1776Biren Patel 5677 5900

November 2005

Crew B.O.S Products Ltd

India Infoline Research can be also accessed on Bloomberg (Code IILL), Thomson First Call and ISI Emerging markets.

In vogue

November 25, 2005 2

Crew B.O.S Products Ltd - In vogue

Share Price Chart

Shareholding pattern

Recommendation : BUY

CMP : Rs167

Target Price : Rs251Potential Upside : 50%52 Week H / L : Rs50 / 209

Market Cap : Rs2.1bn

Avg. volume : 0.8-1mn

BSE code : 532542NSE code : CREWBOSReuters code : 532542.BO

Bloomberg code : N/A

Shareholding Percentage

Promoters 57.6

Domestic Institutions 10.0

FII 7.8

Public and Others 24.6

Crew B.O.S products is one of India’s leading exporter of fashion and home

accessories. The company earns more than 95% of its revenues from the

US and the European market. Its clientele include some of world’s big

retailers namely Next, GAP, Fossil, Chico, Tesco, Laura Ashley and many

others among its clientele. The company has performed consistently in

the past with revenue CAGR of 46% and earnings CAGR of 44%over the

last five years. Post its recent GDR issue, the company is poised to expand

its operations and also enter the leather-finishing segment. We expect the

company to post revenue CAGR of 55% and earnings CAGR of 60% during

FY05-08. We initiate coverage on the company with a buy rating with a

12-15 month horizon and a price target of Rs251. This implies a potential

upside of around 50% from the current market price of Rs167.

Investment highlights

Growing fashion accessory market to drive profit CAGR of 54%(FY05-08)

Worldwide sales of fashion accessory are around 10%-12% of apparel sales.

This is up from an earlier percentage of about 6%-7% few years back. Crew

B.O.S with a strong list of major retailers in its client list is expected to benefit

from this growing trend of fashion accessories business world over. We expect

the company to post earnings CAGR of 54% during FY05-08.

Company has sustainable competitive advantage in designing capabilities

India and Crew B.O.S in particular is competing on cost competitiveness along

with strong design capabilities to keep the Chinese low cost advantage at

bay. While the Chinese score on production line, Indian companies score on

the drawing boards, helping earn a premium. Most big retailers world over

have started tapping Crew B.O.S for their fashion accessories business. The

company is also in talks with major retailers to outsource their product designing.

Leather finishing segment to give scalability to the revenue model

Acquisition of the Jalandhar unit for backward integration and expansion of

leather finishing plant to service the Chinese market is expected to give scalability

to the company’s revenue model. We expect this segment to earn operating

margins of around 15% and contribute 12-15% of revenues from FY07 onwards.

Key Financials FY04 FY05 FY06P FY07P FY08P (12) (12) (12) (12) (12)Sales (Rs mn) 554 810 1,424 2,310 3,000Growth (%) 5.3 46.3 75.7 62.2 29.9OPM (%) 12.7 15.0 16.6 16.0 15.8Net Profit (Rs mn) 42 82 172 264 335Growth (%) 27.2 95.9 109.9 53.3 26.9EPS (Rs) 6.1 7.5 13.4 20.6 26.1PE (x) 27.9 22.4 12.4 8.1 6.4P/BV (x) 8.4 5.3 2.9 2.2 1.7EV/ EBITDA 18.2 17.2 10.2 7.0 5.4ROAE (%) 34.2 33.7 32.0 31.1 29.8ROACE (%) 21.9 23.0 23.2 23.6 23.5Source: Company data, India Infoline estimates

November 25, 2005 3

Crew B.O.S Products Ltd - In vogue

Table of ContentsSr. No Particulars Page No.1 Valuation rationale 42 Industry scenario 53 Company Background 74 Management Team 75 Business profile 86 Investment rationale 9

Investment positives Investment concerns

7 Financials 14

November 25, 2005 4

Crew B.O.S Products Ltd - In vogue

Terminal GrowthRate (%)

The company has been trading in PE (x) band of 12-14 one-year forward earnings.

Crew B.O.S does not have a like comparison in the Indian market in terms of

business (Fashion Accessories). The company uses both leather (60%) and

textiles (40%) for its products and would be unfair to term it as a leather company.

As a result we refrain from valuing the company on relative basis and value it

using a two-stage DCF model. We have used a WACC of 10.5% and a terminal

growth rate of 3%. We arrive at a one-year forward value of Rs251 implying a

potential upside of 50% from the current market price of Rs167. Our target price

discounts the FY07 earnings at a multiple of 12.4x.

We feel Crew B.O.S with many inherent advantages like value added product,

niche business segment and strong earnings growth would command higher

valuations over the leather companies with vanilla products.

Since one half of the current year has already elapsed we have valued the

company from an FY07 perspective and considering FY06 as the base year.

Table: Valuation parameters

(Rs mn)High growth NPV (FY07-11) 745 Terminal growth rate Terminal growth rate 3Terminal value (NPV) 2,763 High growth NPV 745Terminal value NPV 2,763Less: Debt 454

Add: Marketable securities/Cash 155Terminal value 3,209Equity capital 128Fair price 251CMP 167Upside % 50

Price target sensitivity

Valuation Rationale

WACC (%)9.5 10.0 10.5 11.0 11.1

4.0 290 283 277 270 2643.5 276 269 263 257 2513.0 263 257 251 245 2392.5 251 245 239 234 2282.0 240 235 229 224 218

November 25, 2005 5

Crew B.O.S Products Ltd - In vogue

US$mn FY99 FY00 FY01 FY02 FY03 World Leather Accessories Imports 7,120 7,702 7,996 8,464 9,476 India Export Share % 5.8 6.3 5.5 5.5 6.2 World Leather Imports 71,701 77,330 80,784 81,877 88,182 India Exports Share % 2.2 2.5 2.4 2.3 2.5

Source: CLE

Fashion accessory- Industry scenario

Fashion accessories segment has been gaining momentum over the past few

years. The demand however, is currently concentrated in the developed regions

of US and Europe. The major markets for these fashion accessories are USA,

UK, Europe and Australia. Competition to the Indian exporters in this segment

comes from China, Korea and Turkey. However, India’s skilled resources at low

cost and its ability to provide the market with fashion accessories of different

design, feel and texture gives it a competitive advantage over its counterparts.

India is beginning to get appreciation for its work in this industry and brand

India is gradually gaining strength world over.

Fragmented nature of the industry makes it difficult to estimate the market

size. The industry is divided into different segments like handbags, belts, wallets,

eyewear, neckwear, watches, gloves, hats, hosiery, other accessories, home

furnishing products etc. These fashion accessories are marketed through mass

merchandisers, department stores and specialty shops depending on their price

and quality. Consumers are becoming more aware of accessories as fashion

statements, and as a result, are purchasing brand name and quality items that

complement other fashion items.

Leather fashion accessory segment

Leather forms a critical component of the fashion accessory segment, with most

of the products like handbags, belts, wallets, home furnishings, fashion wear

shoes all using leather as raw material. The growth in this sector is exports

driven resulting from developed nations switching manufacturing hubs to low

cost nations like China and India. Even traditional leather producing countries

like Italy have resorted to outsource their manufacturing to India and other

developing nations, due to increasing costs and environmental concerns. Other

major leather product consuming countries like Spain, Germany and USA, have

started evaluating outsourcing their leather product requirements to the Indian

subcontinent.

Table: Indian leather industry export market share in world leather imports

November 25, 2005 6

Crew B.O.S Products Ltd - In vogue

Table: Major leather exporting countries and their market share

FY99 FY00 FY01 FY02 FY03China 15.9% 17.8% 18.2% 19.7% 21.8%Italy 16.1% 15.9% 16.3% 15.8% 15.9%Brazil 2.8% 3.1% 3.2% 3.1% 3.2%India 2.2% 2.5% 2.4% 2.3% 2.5%Korea 3.2% 3.2% 2.7% 2.2% 1.9%Indonesia 2.5% 2.5% 2.2% 1.6% 1.5%Thailand 1.8% 1.7% 1.6% 0.0% 1.4%Taiwan 2.2% 2.0% 1.6% 1.6% 1.4%Mexico 1.1% 1.1% 0.9% 0.8% 0.8%Turkey 0.6% 0.6% 0.6% 0.6% 0.6%

Source: CLE

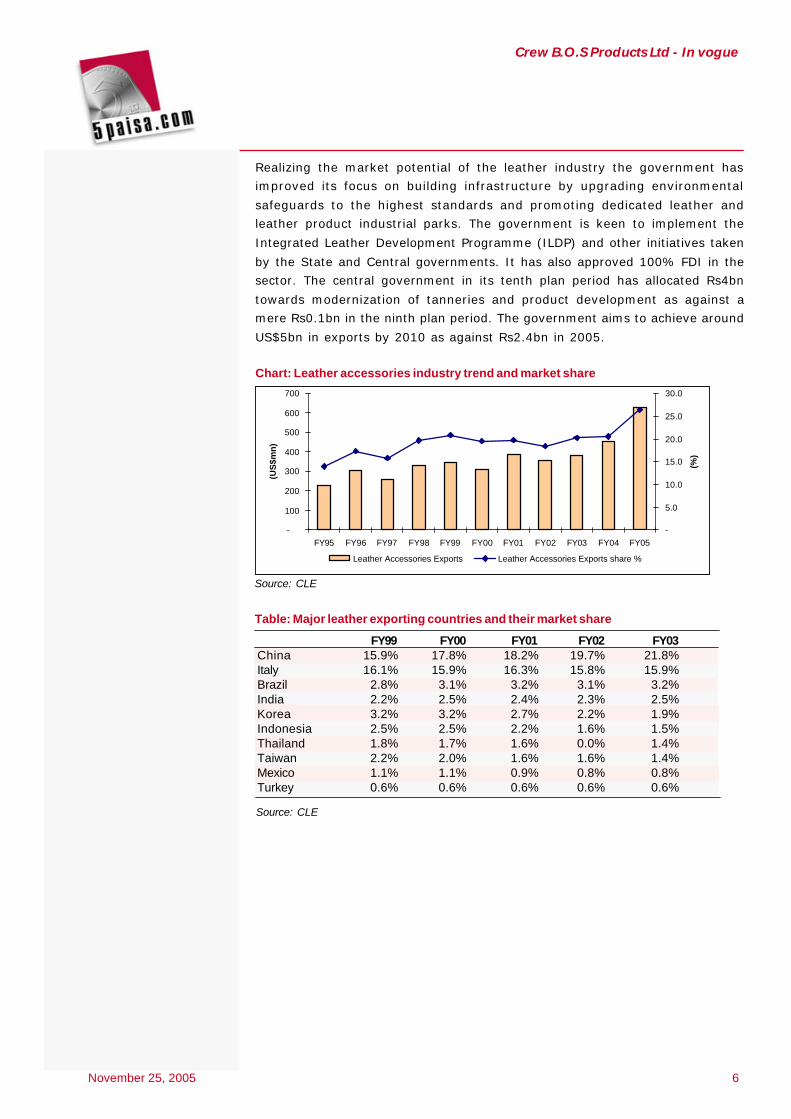

Realizing the market potential of the leather industry the government has

improved its focus on building infrastructure by upgrading environmental

safeguards to the highest standards and promoting dedicated leather and

leather product industrial parks. The government is keen to implement the

Integrated Leather Development Programme (ILDP) and other initiatives taken

by the State and Central governments. It has also approved 100% FDI in the

sector. The central government in its tenth plan period has allocated Rs4bn

towards modernization of tanneries and product development as against a

mere Rs0.1bn in the ninth plan period. The government aims to achieve around

US$5bn in exports by 2010 as against Rs2.4bn in 2005.

Chart: Leather accessories industry trend and market share

Source: CLE

-

100

200

300

400

500

600

700

FY95 FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05

(US

$mn

)

-

5.0

10.0

15.0

20.0

25.0

30.0

(%)

Leather Accessories Exports Leather Accessories Exports share %

November 25, 2005 7

Crew B.O.S Products Ltd - In vogue

Background

Crew B.O.S. Products Limited (formerly known as Motherson Unimetex Private

Limited) was established in 1988. The company has grown from being a fashion

bag and belt manufacturer initially to a manufacturer of multiple products in the

fashion accessories segment. It is primarily engaged in the manufacturing and

marketing of lifestyle fashion accessories and premium home decoration

products to reputed retailers like GAP, Next PLC, Fossil, Esprit etc in US and

Europe. It currently operates its manufacturing facilities from seven factories,

all in India.

The company in August 2004 tapped the capital markets to fund its expansion

plans. The company raised Rs140mn through the initial public offer. The company

recently concluded its GDR offering in August 2005 and raised around Rs220mn

to further expand its existing capacities.

Management Team

Mr.Tarun Oberoi, Managing Director (Age 44 years)

Mr.Oberoi is the founding promoter of Crew B.O.S. He holds a bachelors degree

in Commerce from the Delhi University along with a management diploma through

the Oberoi School of Hotel Management. Before promoting the company he had

a 4-year experience in East India Hotels at various positions both in India and

abroad.

Mr.Robin Bartholomew, Whole time Director (Age 45 years)

Mr.Bartholomew is the co promoter of the company. He holds a post-graduate

diploma in Sociology from the Delhi School of Economics. He holds a Diploma in

Hotel Management from the Oberoi School of Hotel Management. He worked

with East India Hotels Limited for 4 years at various positions in India. He

joined Crew BOS in June 1991 as promoter director

Mr.Puneet Nikore, Director Finance (Age 41 years)

Mr.Nikore is chartered accountant by profession and heads the commercial and

finance function of the company. He has been associated with the company

since inception in various capacities as auditor, Vice-President Finance and

currently as Director finance. His areas of specialization are project financing,

company law matters, audit and direct tax matters.

Company Profile

November 25, 2005 8

Crew B.O.S Products Ltd - In vogue

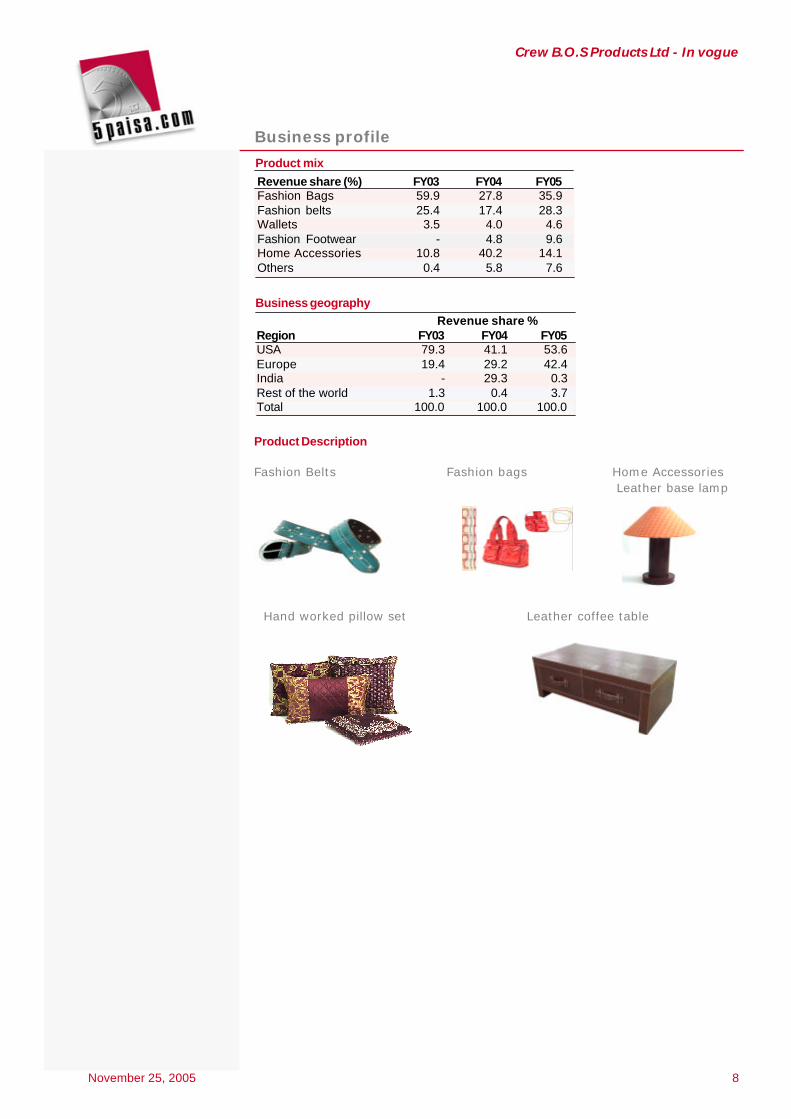

Business profile

Product mix

Revenue share (%) FY03 FY04 FY05Fashion Bags 59.9 27.8 35.9Fashion belts 25.4 17.4 28.3Wallets 3.5 4.0 4.6Fashion Footwear - 4.8 9.6Home Accessories 10.8 40.2 14.1Others 0.4 5.8 7.6

Business geography Revenue share %

Region FY03 FY04 FY05USA 79.3 41.1 53.6Europe 19.4 29.2 42.4India - 29.3 0.3Rest of the world 1.3 0.4 3.7Total 100.0 100.0 100.0

Product Description

Fashion Belts Fashion bags Home Accessories Leather base lamp

Hand worked pillow set Leather coffee table

November 25, 2005 9

Crew B.O.S Products Ltd - In vogue

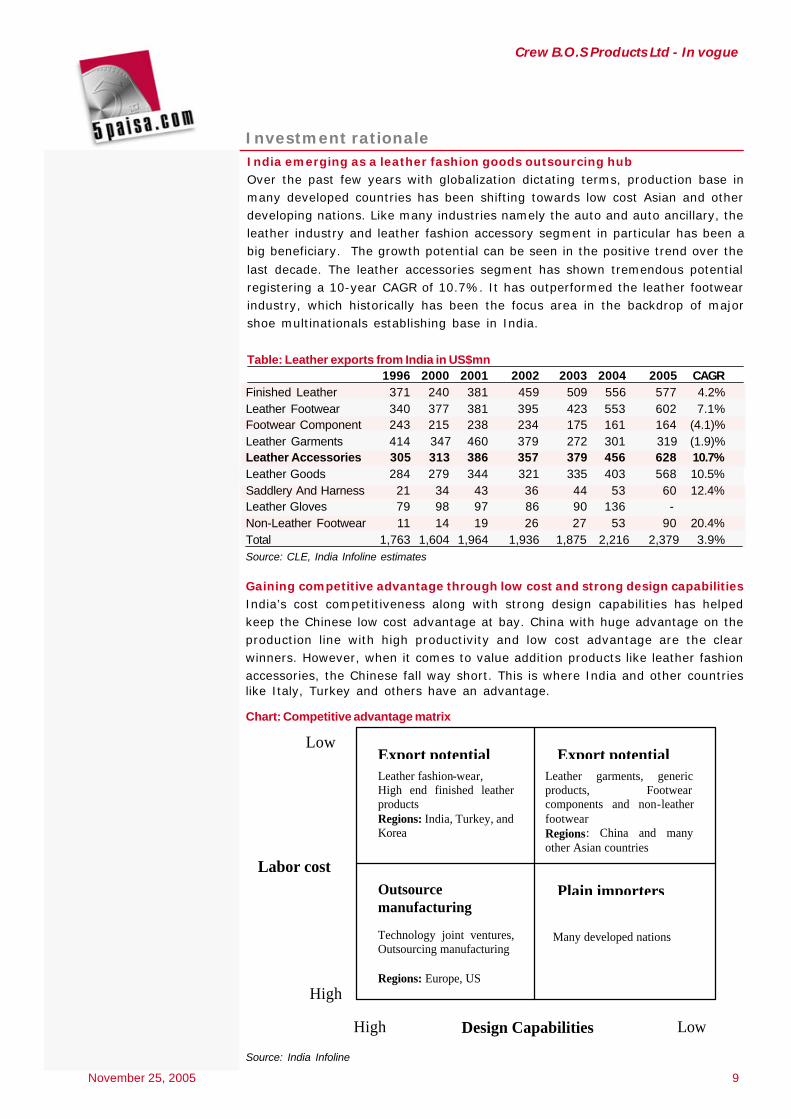

Investment rationaleIndia emerging as a leather fashion goods outsourcing hubOver the past few years with globalization dictating terms, production base inmany developed countries has been shifting towards low cost Asian and otherdeveloping nations. Like many industries namely the auto and auto ancillary, theleather industry and leather fashion accessory segment in particular has been abig beneficiary. The growth potential can be seen in the positive trend over the

last decade. The leather accessories segment has shown tremendous potentialregistering a 10-year CAGR of 10.7%. It has outperformed the leather footwearindustry, which historically has been the focus area in the backdrop of majorshoe multinationals establishing base in India.

Table: Leather exports from India in US$mn1996 2000 2001 2002 2003 2004 2005 CAGR

Finished Leather 371 240 381 459 509 556 577 4.2%Leather Footwear 340 377 381 395 423 553 602 7.1%Footwear Component 243 215 238 234 175 161 164 (4.1)%Leather Garments 414 347 460 379 272 301 319 (1.9)%Leather Accessories 305 313 386 357 379 456 628 10.7%Leather Goods 284 279 344 321 335 403 568 10.5%Saddlery And Harness 21 34 43 36 44 53 60 12.4%Leather Gloves 79 98 97 86 90 136 - Non-Leather Footwear 11 14 19 26 27 53 90 20.4%Total 1,763 1,604 1,964 1,936 1,875 2,216 2,379 3.9%Source: CLE, India Infoline estimates

Gaining competitive advantage through low cost and strong design capabilitiesIndia’s cost competitiveness along with strong design capabilities has helpedkeep the Chinese low cost advantage at bay. China with huge advantage on theproduction line with high productivity and low cost advantage are the clearwinners. However, when it comes to value addition products like leather fashionaccessories, the Chinese fall way short. This is where India and other countrieslike Italy, Turkey and others have an advantage.

Chart: Competitive advantage matrix

Leather fashion-wear, High end finished leather products Regions: India, Turkey, and Korea

Technology joint ventures, Outsourcing manufacturing Regions: Europe, US

Leather garments, generic products, Footwear components and non-leather footwear Regions: China and many other Asian countries

Many developed nations

Export potential Export potential

Outsource manufacturing

Plain importers

Low

High

High

Low

Labor cost

Design Capabilities

Source: India Infoline

November 25, 2005 10

Crew B.O.S Products Ltd - In vogue

While the Italians have developed this art and still are a force to reckon in this

business, high manufacturing cost is slowly moving the manufacturing base from

the European countries to the Asian countries and especially India. Most big

retailers world over have started tapping Crew B.O.S for their fashion accessories

business. The company boasts of clients like Next, GAP, Fossil and many others.

In house design capabilities and advanced Italian technology providing a

competitive edge

Crew B.O.S. is in a unique position where more than 50% of its turnover comes

from manufacture of products researched and designed in house. The company

has an in-house design team of 18 people. The company is exploring opportunities

to outsource the designing capabilities of its major customers. Designing

capabilities sets the company apart from most of its Chinese counterparts, who

are more into generalized product manufacturing like belts and bags. This has

also helped the company get better realizations on its products.

Multiple factors should contribute to robust revenue growth over the next

few years

The growing fashion accessories business world over and Crew B.O.S’s established

brand in servicing world’s big retailers is expected to place the company in a

strong position to tap the outsourcing business of these big retailers. The company

has also leveraged well on its existing client relationship to increase its revenues

from Fossil for export of leather watchstraps. The company is also entering the

leather finishing business through expansion of its existing plant, which is

expected to give scalability to the revenue model. This will help the company

serve the Chinese market with its finished leather products. We expect all these

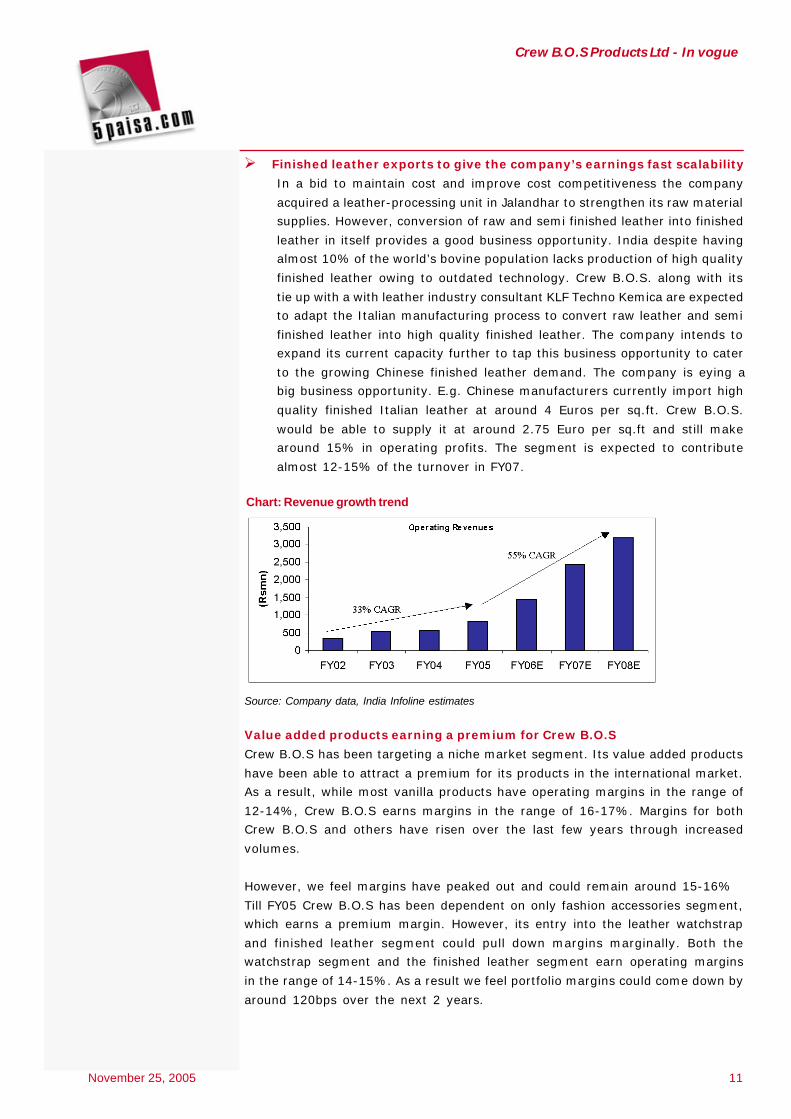

to help the company to post revenue CAGR of 58% during FY06-08.

Ø Growing fashion accessories business world over

Worldwide sales of fashion accessory are around 10%-12% in comparison

to apparel sales. This is up from an earlier percentage of about 6%-7% few

years back. Accessories besides giving a differentiation and increasing the

product line also offer high margins compared to apparel. This is now making

accessory a much larger segment than it has been historically and therefore

offers significantly more opportunities with lesser competition in comparison

to apparel.

Ø Fashion accessory major Fossil’s stake in the company could lead to

more business

The company has a good client relationship with Fossil. Fossil has also

acquired around 3% of the company’s equity in the latest GDR offering.

Fossil sources majority of its requirements from Asia and China and Hong

Kong in particular. We see Fossil’s stake in the company as a move towards

increasing it’s sourcing from India and Crew B.O.S. in particular. Most other

retailers world over have been looking at other Asian markets to reduce

their exposure to China. This is expected to benefit Crew Bos positively as

the company has now proved itself on the international stage for its product

variety and design capabilities.

November 25, 2005 11

Crew B.O.S Products Ltd - In vogue

Ø Finished leather exports to give the company’s earnings fast scalability

In a bid to maintain cost and improve cost competitiveness the company

acquired a leather-processing unit in Jalandhar to strengthen its raw material

supplies. However, conversion of raw and semi finished leather into finished

leather in itself provides a good business opportunity. India despite having

almost 10% of the world’s bovine population lacks production of high quality

finished leather owing to outdated technology. Crew B.O.S. along with its

tie up with a with leather industry consultant KLF Techno Kemica are expected

to adapt the Italian manufacturing process to convert raw leather and semi

finished leather into high quality finished leather. The company intends to

expand its current capacity further to tap this business opportunity to cater

to the growing Chinese finished leather demand. The company is eying a

big business opportunity. E.g. Chinese manufacturers currently import high

quality finished Italian leather at around 4 Euros per sq.ft. Crew B.O.S.

would be able to supply it at around 2.75 Euro per sq.ft and still make

around 15% in operating profits. The segment is expected to contribute

almost 12-15% of the turnover in FY07.

Chart: Revenue growth trend

Source: Company data, India Infoline estimates

Value added products earning a premium for Crew B.O.S

Crew B.O.S has been targeting a niche market segment. Its value added products

have been able to attract a premium for its products in the international market.

As a result, while most vanilla products have operating margins in the range of

12-14%, Crew B.O.S earns margins in the range of 16-17%. Margins for both

Crew B.O.S and others have risen over the last few years through increased

volumes.

However, we feel margins have peaked out and could remain around 15-16%

Till FY05 Crew B.O.S has been dependent on only fashion accessories segment,

which earns a premium margin. However, its entry into the leather watchstrap

and finished leather segment could pull down margins marginally. Both the

watchstrap segment and the finished leather segment earn operating margins

in the range of 14-15%. As a result we feel portfolio margins could come down by

around 120bps over the next 2 years.

November 25, 2005 12

Crew B.O.S Products Ltd - In vogue

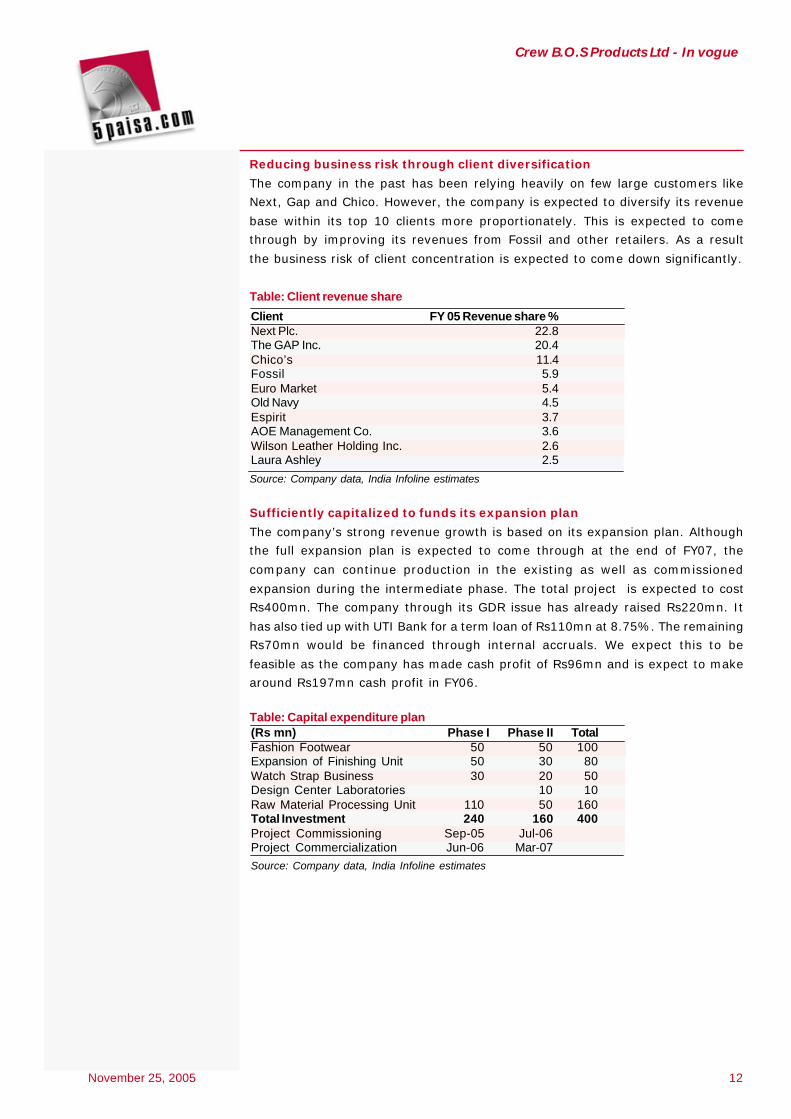

Reducing business risk through client diversification

The company in the past has been relying heavily on few large customers like

Next, Gap and Chico. However, the company is expected to diversify its revenue

base within its top 10 clients more proportionately. This is expected to come

through by improving its revenues from Fossil and other retailers. As a result

the business risk of client concentration is expected to come down significantly.

Table: Client revenue share

Client FY 05 Revenue share %Next Plc. 22.8The GAP Inc. 20.4Chico’s 11.4Fossil 5.9Euro Market 5.4Old Navy 4.5Espirit 3.7AOE Management Co. 3.6Wilson Leather Holding Inc. 2.6Laura Ashley 2.5

Source: Company data, India Infoline estimates

Sufficiently capitalized to funds its expansion plan

The company’s strong revenue growth is based on its expansion plan. Although

the full expansion plan is expected to come through at the end of FY07, the

company can continue production in the existing as well as commissioned

expansion during the intermediate phase. The total project is expected to cost

Rs400mn. The company through its GDR issue has already raised Rs220mn. It

has also tied up with UTI Bank for a term loan of Rs110mn at 8.75%. The remaining

Rs70mn would be financed through internal accruals. We expect this to be

feasible as the company has made cash profit of Rs96mn and is expect to make

around Rs197mn cash profit in FY06.

Table: Capital expenditure plan(Rs mn) Phase I Phase II TotalFashion Footwear 50 50 100Expansion of Finishing Unit 50 30 80Watch Strap Business 30 20 50Design Center Laboratories 10 10Raw Material Processing Unit 110 50 160Total Investment 240 160 400Project Commissioning Sep-05 Jul-06 Project Commercialization Jun-06 Mar-07 Source: Company data, India Infoline estimates

November 25, 2005 13

Crew B.O.S Products Ltd - In vogue

Effective tax rate to remain around 5% till FY10The company derives more than 95% of the revenues from the export market.This it does by exporting through the Export Oriented Units (EOU). This presentsthe company a 100% tax holiday till FY10. As a result the effective tax rate forthe company has been around 3%. Post expansion of the leather finishing plant,the company is expected to derive some revenues from the Indian market. Toremain conservative we have estimated only 85% of the revenues to come fromthe export market. In effect the company would continue to enjoy a 100% taxholiday on 85% of the revenues, while pay a 33% tax rate on the remaining15% earnings. This results in an effective tax rate of 5% till FY10.

Investment concerns

Successful and timely completion of the expansion plan critical for growthAlthough the company’s future growth exudes confidence, the incremental highgrowth is expected to trickle down post expansion. The company has alreadyraised resources for the same. However, business growth would hinge on thecompany successfully completing the expansion in time.

Business growth dependent on understanding dynamic fashion trendsFashion trends being dynamic in nature, pose business risk to the company. Thecompany has an experienced team of 18 designers with rich experience in thefashion business. The company recruits new designers from reputed fashioninstitutes like National Institute of Fashion Technology (NIFT) and other fashioninstitutes. This has helped the company to maintain its competitive advantagein the international market. Future business growth would depend on thecompany maintaining this competitive edge.

Scaling up and retaining design team crucial to business successThe company derives a big competitive advantage in design capabilities. Itcurrently has a design team of 18 people. We feel the company would have toramp up its existing design team to shoulder the increasing workload. Expandingits existing team and successful retention policy to hold on to the existing teamwould be would be crucial for the company’s progress.

Order or shipment rejection can impact business significantlyMajority of Crew B.O.S’s customers are big retailers. These players have stringentproduct quality and delivery norms in addition to the strong bargaining power.Any order or shipment rejection could impact the company’s business and margins,as the goods would have to be sold at a much cheaper cost. The company so farhas not had any major order rejections. While there have been stray cases oflate shipment, which has resulted in the company having to take a haircut onthe list price depending on the delay period. While in FY05, few customersaccounted for majority of the revenues; the scene is expected to change in thecurrent and subsequent years.

High impact cost due to low paper supply in the marketThe company has small equity base of Rs128mn, out of which promoters hold57.6% and institutions hold another 17%. This leaves just 25.4% or 3.3mn sharesin the market. The average daily volumes range around 0.1-0.2mn on the NationalStock Exchange (NSE). This could result in the high impact cost, while investingas well as liquidating investment in the company.

November 25, 2005 14

Crew B.O.S Products Ltd - In vogue

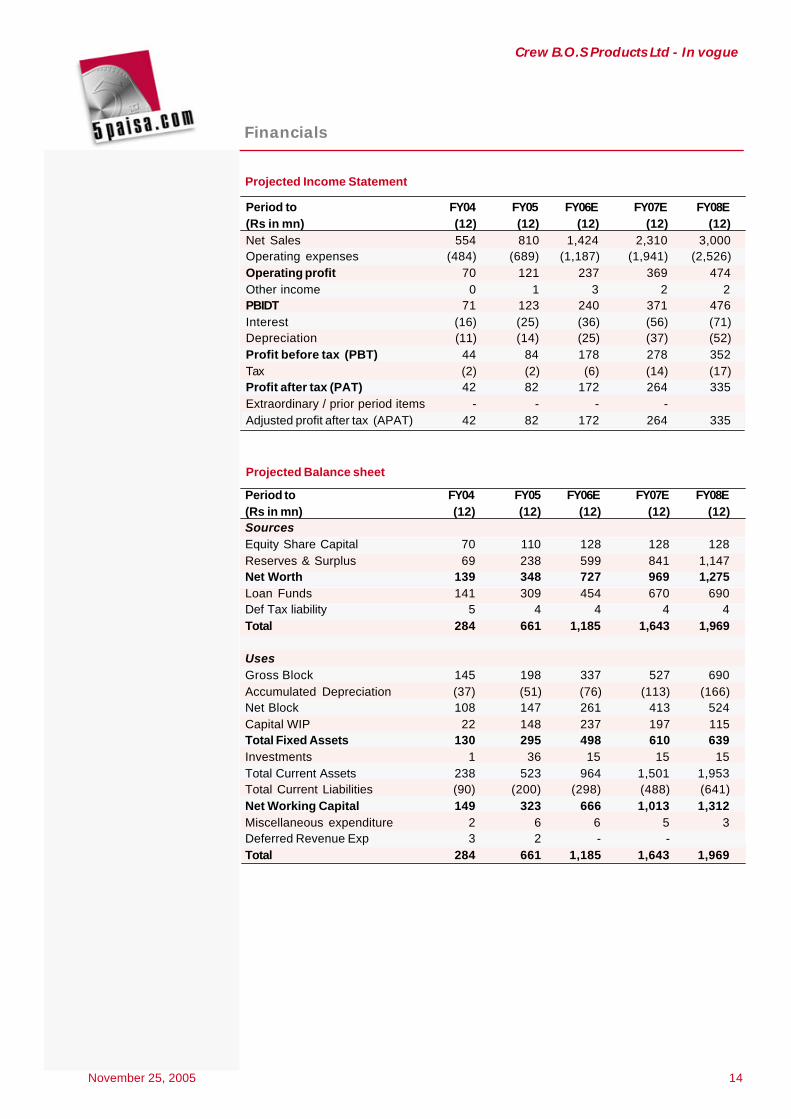

Projected Income Statement

Period to FY04 FY05 FY06E FY07E FY08E(Rs in mn) (12) (12) (12) (12) (12)Net Sales 554 810 1,424 2,310 3,000Operating expenses (484) (689) (1,187) (1,941) (2,526)Operating profit 70 121 237 369 474Other income 0 1 3 2 2PBIDT 71 123 240 371 476Interest (16) (25) (36) (56) (71)Depreciation (11) (14) (25) (37) (52)Profit before tax (PBT) 44 84 178 278 352Tax (2) (2) (6) (14) (17)Profit after tax (PAT) 42 82 172 264 335Extraordinary / prior period items - - - - Adjusted profit after tax (APAT) 42 82 172 264 335

Projected Balance sheet

Period to FY04 FY05 FY06E FY07E FY08E(Rs in mn) (12) (12) (12) (12) (12)Sources Equity Share Capital 70 110 128 128 128Reserves & Surplus 69 238 599 841 1,147Net Worth 139 348 727 969 1,275Loan Funds 141 309 454 670 690Def Tax liability 5 4 4 4 4Total 284 661 1,185 1,643 1,969 Uses Gross Block 145 198 337 527 690Accumulated Depreciation (37) (51) (76) (113) (166)Net Block 108 147 261 413 524Capital WIP 22 148 237 197 115Total Fixed Assets 130 295 498 610 639Investments 1 36 15 15 15Total Current Assets 238 523 964 1,501 1,953Total Current Liabilities (90) (200) (298) (488) (641)Net Working Capital 149 323 666 1,013 1,312Miscellaneous expenditure 2 6 6 5 3Deferred Revenue Exp 3 2 - - Total 284 661 1,185 1,643 1,969

Financials

November 25, 2005 15

Crew B.O.S Products Ltd - In vogue

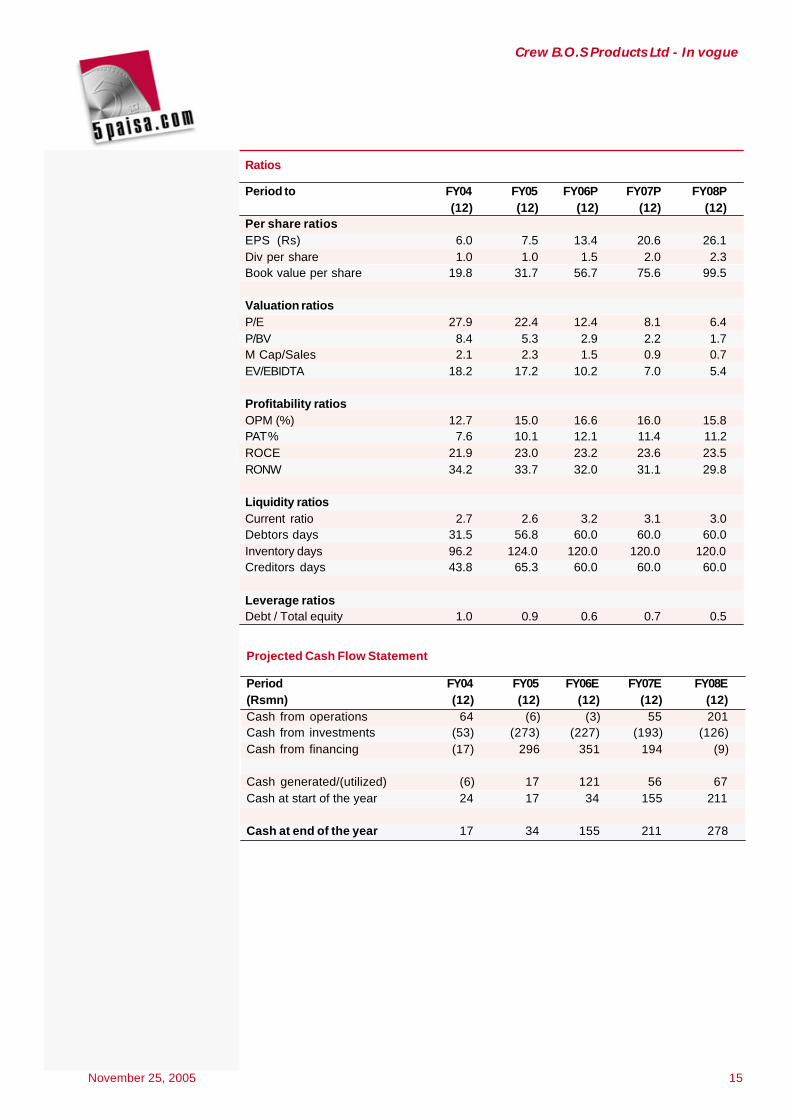

Period to FY04 FY05 FY06P FY07P FY08P (12) (12) (12) (12) (12)Per share ratios EPS (Rs) 6.0 7.5 13.4 20.6 26.1Div per share 1.0 1.0 1.5 2.0 2.3Book value per share 19.8 31.7 56.7 75.6 99.5 Valuation ratios P/E 27.9 22.4 12.4 8.1 6.4P/BV 8.4 5.3 2.9 2.2 1.7M Cap/Sales 2.1 2.3 1.5 0.9 0.7EV/EBIDTA 18.2 17.2 10.2 7.0 5.4 Profitability ratios OPM (%) 12.7 15.0 16.6 16.0 15.8PAT % 7.6 10.1 12.1 11.4 11.2ROCE 21.9 23.0 23.2 23.6 23.5RONW 34.2 33.7 32.0 31.1 29.8 Liquidity ratios Current ratio 2.7 2.6 3.2 3.1 3.0Debtors days 31.5 56.8 60.0 60.0 60.0Inventory days 96.2 124.0 120.0 120.0 120.0Creditors days 43.8 65.3 60.0 60.0 60.0 Leverage ratios Debt / Total equity 1.0 0.9 0.6 0.7 0.5

Ratios

Period FY04 FY05 FY06E FY07E FY08E(Rsmn) (12) (12) (12) (12) (12)Cash from operations 64 (6) (3) 55 201Cash from investments (53) (273) (227) (193) (126)Cash from financing (17) 296 351 194 (9) Cash generated/(utilized) (6) 17 121 56 67Cash at start of the year 24 17 34 155 211 Cash at end of the year 17 34 155 211 278

Projected Cash Flow Statement

Published in August 2005. All rights reserved. © India Infoline Ltd 2005-6.This report is for information purposes only and does not construe to be any investment, legal or taxation advice. It is not intendedas an offer or solicitation for the purchase and sale of any financial instrument. Any action taken by you on the basis of theinformation contained herein is your responsibility alone and India Infoline Ltd (hereinafter referred as IIL) and its subsidiaries orits employees or directors, associates will not be liable in any manner for the consequences of such action taken by you.We have exercised due diligence in checking the correctness and authenticity of the information contained herein, but do notrepresent that it is accurate or complete. IIL or any of its subsidiaries or associates or employees shall not be in any wayresponsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in thispublication. The recipients of this report should rely on their own investigations. IIL and/or its subsidiaries and/or directors,employees or associates may have interests or positions, financial or otherwise in the securities mentioned in this report.India Infoline Ltd , 24 Nirlon Complex, Off Western Exp. Highway, Goregaon(E). Mumbai -63. Tel 5677 5900. Fax 2685 0451

it’s all about money, honey!

Toll Free 1600-22-6555 Email [email protected] is the trade name of India Infoline Securities Pvt Ltd (IISPL), a wholly ownedsubsidiary of India Infoline Ltd. IISPL is a member of the National Stock Exchange of India(NSE) and The Stock Exchange, Mumbai (BSE). IISPL is also a Depository Participant withNSDL.

IndiaInfolinecom

Our Recent Publications

DCM Shriram Ltd - September 29, 2006

Opto Circuits (India) Ltd - Scaling Upper Circuits - September 15, 2005

Control Print India Ltd: Printing a sucess code - August 12, 2005

Finolex Cables Ltd: Get Wired - August 12, 2005

Carbon Credits : Emitting Gains - July 22, 2005

Financial Technologies Ltd : Strike it rich - July 04, 2005