Embed Size (px)

Citation preview

Real Estate TransactionsReal Estate TransactionsIssues Under Income-tax Act, 1961

CA Nihar Jambusaria

◙ Tax issues relating to Real Estate Transactions under Income-tax Act, 1961

� Accounting For Revenue from Real Estate Sales

� Finance Cost, Indirect Cost and Compounding

The Focus

Page 2

� Finance Cost, Indirect Cost and Compounding Charges

� Analysing the concept “Income Derived From”

� Section 80-IB(10)-Judicial Pronouncements

� Completion Certificate

� Property V/s Business Income

� Miscellaneous

Accounting For Revenue From Real Estate Sales

� Methods Applicableo Project Completion Method permissible

» CIT v/s Bilahari Investments (P) Ltd. [(2008) 299 ITR 1 SC]

o Percentage Completion Method permissible

» CIT vs. Advance Construction Co. (P) Ltd. [(2005) 275 ITR 30 (Guj.)]

o Change of method of accounting

» Satish H. Patel [93 TTJ 458 (Pune)]

� Disclosure in the course of search – Whether Income be taxed on Completion of

Page 3

� Disclosure in the course of search – Whether Income be taxed on Completion ofProjecto Undisclosed income in the form of “on money”

» Dhanvarsha Builders & Developers (P) Ltd. Vs. DCIT [(2006) 102 ITD 375 (Pune)]

� Tax Audito Amount received as advance by builder following project completion method

whether tax audit applicable and penalty under section 271B imposable

» Gopal krishan Builders [92 TTJ 215 (Luck)]

� Interest on Borrowed Capital – Scope of Section 36(1)(iii)

» CIT vs. Lokhandwala Construction [(2003) 260 ITR 579 (Bom.)]

» Wall street Constructions Ltd. & Anr. Vs. JCIT [(2006) 101 ITD 156 (Mum) (SB)]

» JCIT vs. Raheja (P) Ltd. [(2006) 102 ITD 414 (Mum.)]

Finance Cost, Indirect Cost & Compounding Charges

- Related Developments

Page 4

� Advertisement Expenses to be capitalised as work-in-progress

» Income Tax Officer vs. Panchvati Developers [115 TTJ 139 (Mum)]

� Whether Compounding charges paid by builders allowed as a deduction

» Mamta Enterprises – [ 135 Taxman 393 (Karnataka)]

Analysing the Concept “Income derived from”

� Sale of TDR/FSI» Radhe Developers & Others V/s ITO [113 TTJ 300 (Ahmd)]

Profit earned by assessee include sale of extra FSI which was unutilized. It is held that deduction could not be denied to the assessee on the ground that profit earned by the assessee are not for developing and building housing project done but for sale of extra FSI which has not been utilized for developing and building the housing project.

� Interest earned on surplus money parked as Fixed Deposit with Bank taxed under

Page 5

� Interest earned on surplus money parked as Fixed Deposit with Bank taxed under the head income from business

» CIT vs. Lok Holdings [308 ITR 356 (Bom HC) ]» Tricom India Ltd. vs. ACIT, ITA No. 1924/Mum/08, ITAT Mumbai Bench E

� Relevance of Income derived from» Sterling Foods vs. CIT [237 ITR 579 (SC)]

There must be direct nexus between the profit and the industrial undertaking. If the nexus is not direct but only incidental, such profit cannot be treated as profit derived from export.

Section 80-IB(10) - Judicial Pronouncement

� Proportionate Deduction for eligible housing units in a project containing ineligible

housing units

» Bengal Ambuja ITA No. 1735 (cal.) (2007)

� Deduction in case of individual projects if they are part of bigger project but got

sanction separately

» Dy. CIT vs. Brigade Enterprise (P) Ltd [119 TTJ 269]

Page 6

» Dy. CIT vs. Brigade Enterprise (P) Ltd [119 TTJ 269]

� Proportionate Deduction for completed blocks in total projects

» Saroj Sales Organisation vs. ITO [(2008) 115 TTJ 485 (Mum) ]

� Ownership of Land – Whether Compulsory?

» Radhe Developers & Ors Vs. ITO [113 TTJ 300 (Ahmd)]

� Restriction on commercial area – Prospective or Retrospective?

» Arun Excello Foundation Vs. ACIT 108 TTJ 71

� One Acre Area interpretation where eligible & ineligible projects are constructed

» Vandana Properties ITA No. 1253/Mum/2007

Section 80-IB(10) - Judicial Pronouncement

contd

Page 7

� Beneficial Interpretation of Provision

» Dy. CIT vs. Brigade Enterprises (P) Ltd 119 TTJ 269

Completion Certificate

� Occupation Certificate – Whether Sufficient Compliance ?

» Dy. CIT vs. Ansal Properties & Industries Ltd. [(2008) 22 SOT 45 (Del.)]

It is held that occupation certificate given by BMC would be sufficient proof that the

Housing project is completed. But, these certificates are sometimes given building wise. If all the buildings

are constructed by the developer having occupation certificate before 31/03/08, it may be sufficient

compliance

Page 8

compliance

Property V/s Business Income

With several malls and business centres emerging, taxability of rental income arising therefrom is an important issue.

� Shambhu Investment Private Ltd v/s CIT [263 ITR 143 (SC)] - held that income derived from letting, assessable as income from property and not business income.

� PFH Mall & Retail Management Ltd v/s ITO [110 ITD 337(Kol)]

After considering Shambhu Investment Pvt Ltd it was held that income derived from shopping mall

Page 9

After considering Shambhu Investment Pvt Ltd it was held that income derived from shopping mallbusiness center was assessable as business income and not income from House Property.

� Mumbai Tribunal in the case of M/s Omsagar Engg. Pvt Ltd v/s ACIT, ITA no. 2989/Mum/03, Bench-K,dated 30/11/2006, - held that income from service center is to be treated as business income.

� CIT v/s Sarabhai Pvt Ltd[263 ITR 197(Guj)]

When property has been let out not only as property but with services which is complex letting, the income cannot be said to be derived from mere ownership of house property but may be assessable as income from business.

Miscellaneous� Transfer of Development Rights – whether constitutes transfer u/s 2(47)

» Chaturbhuj Dwarkadas Kapaidia V/s CIT [260 ITR 491 (Bom.)]

�Conversion of Stock in trade into Capital Asset – what will be the holding period

» CIT v/s Bright Star Investments (P) Ltd. [24 SOT 288 (Bom.)]

» Splendor Constructions (P) Ltd. V/s ITO [27 SOT 39(Delhi)]

� Exemption u/s 54E cannot be denied for depreciable assets

Page 10

� Exemption u/s 54E cannot be denied for depreciable assets

» CIT V/s ACE Builders (P) Ltd. [281 ITR 210 (Bom.)]

» CIT V/s Assam Petroleum Industries (P) Ltd.[262 ITR 587 (Gau.)

» CIT V/s Legal Heirs of late Dr Mrs S.R. Pandit, ITA No. 144/2007 dt.30.08.2005 [Bombay HC]

�Conversion of Tenancies into ownership – subsequent sale thereof is short term capital

gain

» Dr. D.A. Irani V/s First ITO [7 ITD 160 (Bom.)]

�Stamp Duty Valuation – when income from transfer is business income

» M/s Inderlok Hotels Pvt. Ltd. V/s ITO, ITA No. 4376/M/2008, Bench “I”, dt. 5/2/2009

THANK YOU

Page 11

Accounting for Revenue from Real Estate Sales

- Gist of Cases

� CIT vs. Bilahari Investments (P) Ltd. (2008) 299 ITR 1(SC)

It is held that Recognition/identification of income under the Act, is attainable by several methods of

accounting. It may be noted that the same result could be attained by any one of the accounting methods.

Completed contract is one such method. Similarly, percentage of completion is another such method.

� CIT vs. Advance Construction Co. (P) Ltd. (2005) 275 ITR 30 (Guj)

Page 12

It is held that Assessee-contractor having offered profits for tax on the basis of percentage completion

method which is a standard accounting practice and has been constantly followed by the assessee in

subsequent years, the same could not be rejected.

� Satish H. Patel 93 TTJ 458 (Pune)

It is held that the assessee having changed his method of accounting from work-in- progress in original returnto project completion method in revised return, assessment had to be made as per revised return.

Accounting for Revenue from Real Estate Sales

- Gist of Cases

� Dhanvarsha Builders & Developers (P) Ltd vs. DCIT (2006) 102 ITD 375 (Pune)

It is held that Undisclosed income in the form of ‘on money’ stood established by

seizure of document r/w statement recorded under s. 132(4); however in computing undisclosed income,

expenditure incurred has to be allowed; income discovered has to be taxed in assessment years as per method

of accounting followed by assessee.

Page 13

� Gopal Krishan Builders, 92 TTJ 215 (Luck.)

It is held that amounts received as advance by the assessee-builder from customers

had an element of profit and same were to be adjusted towards the cost of flats booked by each customer and

thus, the amounts of advance have to be included in "gross receipts" for the purpose of s. 44AB; assessee being

under obligation to get its accounts audited under s. 44AB. It cannot be contended that the assessee following

project completion method would get the books of account audited in the last year and not in earlier years

when he is debiting the expenses and other items and showing different types of receipts penalty under s. 271B

was imposable for its failure to get the same done

Finance Cost, Indirect Cost & Compounding Charges

- Gist of Cases� CIT vs. Lokhandwala Construction, (2003) 260 ITR 579 (Bom)

� Wallstreet Constructions Ltd. & Anr. Vs. JCIT 2006 101 ITD 156 (Mum) (SB)

It is held that construction project undertaken by the assessee-builder constituted

its stock-in-trade and the assessee was entitled to deduction under s. 36(1)(iii) in respect of interest on

loan obtained for execution of said project.

Page 14

� JCIT vs. Raheja (P) Ltd. (2006) 102 ITD 414 (Mum.)

It is held that the assessee following project-completion method of accounting,

the interest identifiable with that project should be allowed only in the year when the project is

completed and the income from that project is offered for taxation. The same cannot be deducted as

period cost from year to year. True profits in such a case can be determined only when entire cost of the

project, direct or indirect, including finance cost is added to the value of work-in progress

It is held that even though assessee was following competed contract method for

returning its income, its claim of finance cost as a period cost in nature of interest was allowable in the

year in which it was incurred or accrued, in accordance with AS – 7 issued by the ICAI.

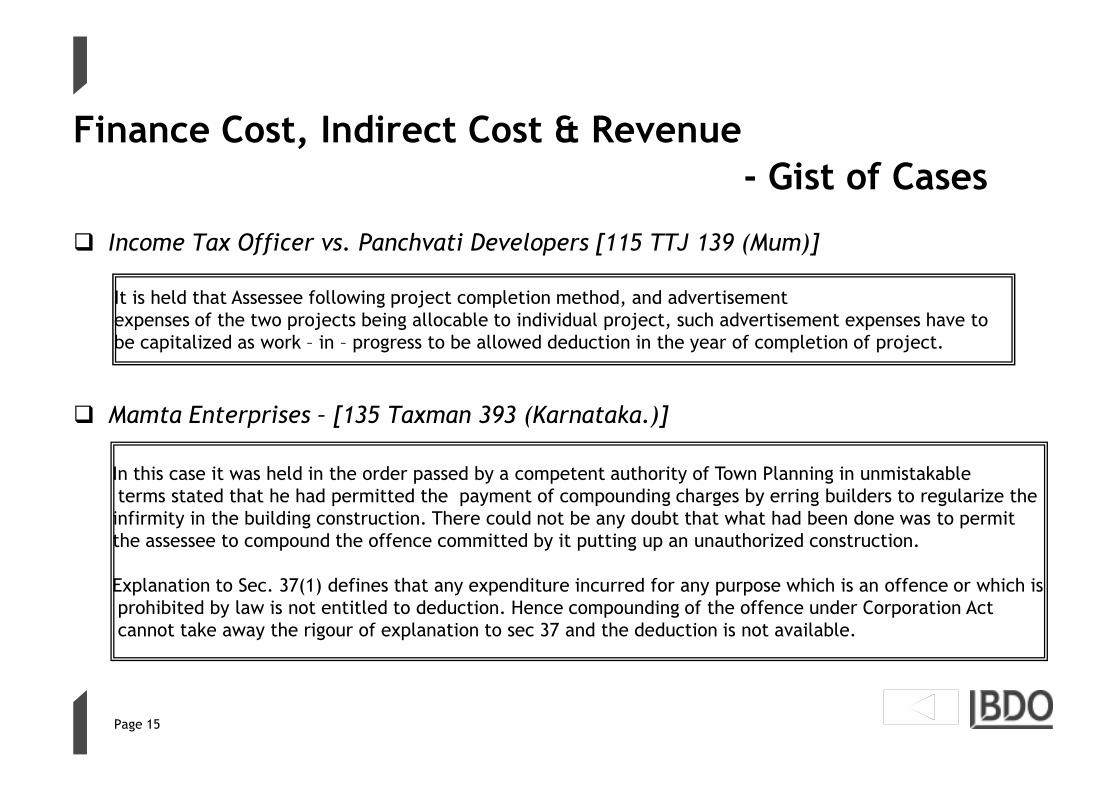

� Income Tax Officer vs. Panchvati Developers [115 TTJ 139 (Mum)]

It is held that Assessee following project completion method, and advertisement

expenses of the two projects being allocable to individual project, such advertisement expenses have to

be capitalized as work – in – progress to be allowed deduction in the year of completion of project.

Finance Cost, Indirect Cost & Revenue

- Gist of Cases

Page 15

� Mamta Enterprises – [135 Taxman 393 (Karnataka.)]

In this case it was held in the order passed by a competent authority of Town Planning in unmistakable

terms stated that he had permitted the payment of compounding charges by erring builders to regularize the

infirmity in the building construction. There could not be any doubt that what had been done was to permit

the assessee to compound the offence committed by it putting up an unauthorized construction.

Explanation to Sec. 37(1) defines that any expenditure incurred for any purpose which is an offence or which is

prohibited by law is not entitled to deduction. Hence compounding of the offence under Corporation Act

cannot take away the rigour of explanation to sec 37 and the deduction is not available.

Analyzing the Concept “Income derived from”

- Gist of Cases

� CIT vs. Lok Holdings 308 ITR 356 (Bom.)

� Tricom India Ltd. V. ACIT, ITA No. 1924/Mum/08, ITAT Mumbai Bench E

It is held that advances from customers intending to purchase Flats, deposit of surplus

Money with bank in course of business – the accrued interest arises out of Business activity hence such interest

Income assessable as Business Income and not as income from other sources.

Page 16

� Tricom India Ltd. V. ACIT, ITA No. 1924/Mum/08, ITAT Mumbai Bench E

It is held that merely because the income has been assessed as business income , it will

not automatically confer the benefits of a particular deduction once there is a rider provision that such

income should be derived from a particular source.

� Bengal Ambuja ITA No. 1735 (cal.) (2007)

Section 80-IB(10)

- Gist of Cases

It is held that the provisions of Sec. 80-IB(10),do not provide for denial of deduction, if

a housing complex contains both the smaller and larger residential units. It concluded that profits attributable

to eligible residential units are entitled for deduction in spite of the fact that other residential units are

greater than 1500 sq. ft. built-up area

� Dy. CIT vs. Brigade Enterprise (P) Ltd 119 TTJ 269

It is held that where some of the residential units in a bigger housing project, treated

independently, are eligible for relief u/s. 80-IB(10), relief should be given pro rata and should not be denied

by treating the bigger project as a single unit, more so, when assessee obtained all sanctions, permissions and

Page 17

by treating the bigger project as a single unit, more so, when assessee obtained all sanctions, permissions and

certificates for such eligible units separately

� Saroj Sales Organisation vs. ITO (2008) 115 TTJ 485 (Mum)

It is held that the deduction was granted for completed blocks on the ground that each

such block complied with the conditions of Sec. 80-IB(10).

� Radhe Developers & Ors Vs. ITO 113 TTJ 300 (Ahmd)

It is held in the above cited case that ownership of land is not precondition to claim the deduction.

As a result developers are allowed to get deduction u/s. 80IB(10). However, works contractors are not

allowed to claim deduction

� Arun Excello Foundation Vs. ACIT [108 TTJ 71]

Section 80-IB(10) - Gist of Cases

It is held in the above cited case that the restriction on built up area of commercial construction is effective for

projects stated after 1.4.2005. As a result projects started before 1.4.2005 will not be barred by such

limitations

� Vandana Properties ITA No. 1253/Mum/2007

It is held in the above cited case that as per clause (b) to section 80IB(10), the project should be on a size of

plot of land which has the minimum area of one acre. As a result eligible projects should be allowed deduction

even though ineligible projects are constructed on the same piece of land.

Page 18

even though ineligible projects are constructed on the same piece of land.

� Dy. CIT vs. Brigade Enterprises (P) Ltd [119 TTJ 269]

It is held in the above cited case that the cardinal rule for interpretation of any provision relating to

exempt, allowance, deduction, rebate or relief is that they should be interpreted liberally and broadly so as to

advance the object sought to be achieved and not to frustrate it. This would thus mean where there is partial

or nominal non-compliance of the requirements of law there should not be a complete disallowance of

deductions. The disallowance, if any, will have to be restricted to the extent of non-compliance of the

provisions. This rule of proportionality is well-founded in the income tax law and is recognised under various

provisions of the Act

Property V/S Business Income

- Gist of Cases

� Shambhu Investment Private Ltd vs. CIT [263 ITR 143 (SC)]

In this case assessee was letting out furnished premises on monthly rent to various parties along with furniture,

fixture, A.C., etc. for being used as “table space". Entire cost of property already recovered by way of interest free

advance by assessee. Only intention was to let out a portion of premises to respective occupant. It was held that

income derived from letting rightly held as income from property and not business income.

Page 19

� PFH Mall & Retail Management Ltd vs. ITO [110 ITD 337(Kol)]

In this case it was held that the fact that Apex court held that income earned by Shambhu Investment Pvt Ltd is

assessable as property income has no relevance in the facts and circumstances of the present case because in that

case the fact showed that the main intention was to earn rental income. That was why the entire cost of property

was recovered from tenant by way of interest free advance. In the instant case the assessee has taken bank loan to

finance his projects like any other business man. Every action of the present assessee appears to be the sole object

of commercial exploitation of the premises.

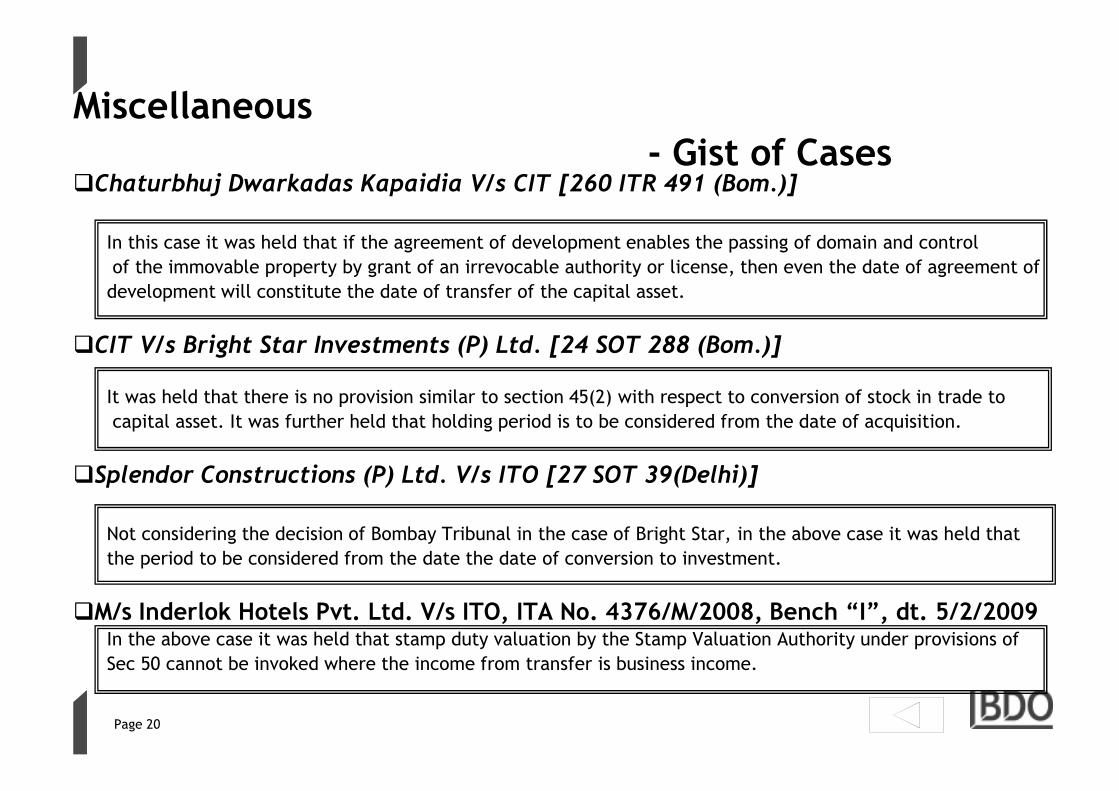

�Chaturbhuj Dwarkadas Kapaidia V/s CIT [260 ITR 491 (Bom.)]

In this case it was held that if the agreement of development enables the passing of domain and control

of the immovable property by grant of an irrevocable authority or license, then even the date of agreement of

development will constitute the date of transfer of the capital asset.

�CIT V/s Bright Star Investments (P) Ltd. [24 SOT 288 (Bom.)]

It was held that there is no provision similar to section 45(2) with respect to conversion of stock in trade to

Miscellaneous

- Gist of Cases

Page 20

It was held that there is no provision similar to section 45(2) with respect to conversion of stock in trade to

capital asset. It was further held that holding period is to be considered from the date of acquisition.

�Splendor Constructions (P) Ltd. V/s ITO [27 SOT 39(Delhi)]

Not considering the decision of Bombay Tribunal in the case of Bright Star, in the above case it was held that

the period to be considered from the date the date of conversion to investment.

�M/s Inderlok Hotels Pvt. Ltd. V/s ITO, ITA No. 4376/M/2008, Bench “I”, dt. 5/2/2009In the above case it was held that stamp duty valuation by the Stamp Valuation Authority under provisions of

Sec 50 cannot be invoked where the income from transfer is business income.

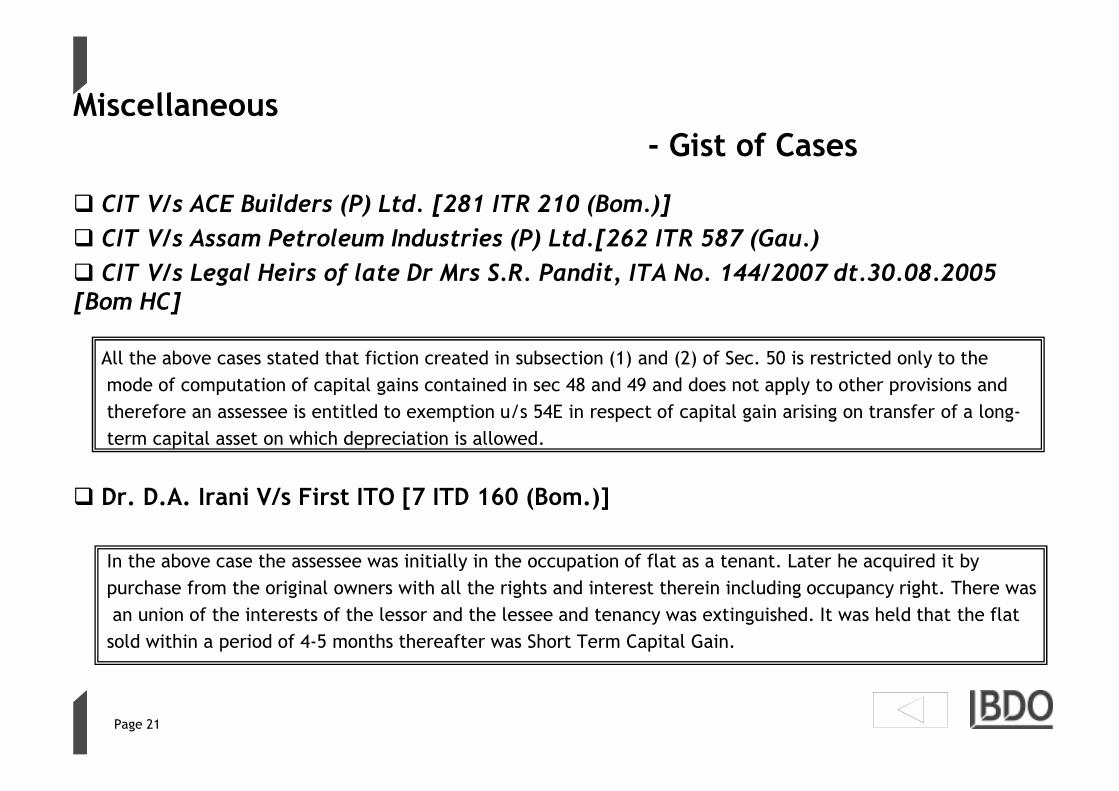

� CIT V/s ACE Builders (P) Ltd. [281 ITR 210 (Bom.)]

� CIT V/s Assam Petroleum Industries (P) Ltd.[262 ITR 587 (Gau.)

� CIT V/s Legal Heirs of late Dr Mrs S.R. Pandit, ITA No. 144/2007 dt.30.08.2005 [Bom HC]

All the above cases stated that fiction created in subsection (1) and (2) of Sec. 50 is restricted only to the

mode of computation of capital gains contained in sec 48 and 49 and does not apply to other provisions and

Miscellaneous

- Gist of Cases

Page 21

mode of computation of capital gains contained in sec 48 and 49 and does not apply to other provisions and

therefore an assessee is entitled to exemption u/s 54E in respect of capital gain arising on transfer of a long-

term capital asset on which depreciation is allowed.

� Dr. D.A. Irani V/s First ITO [7 ITD 160 (Bom.)]

In the above case the assessee was initially in the occupation of flat as a tenant. Later he acquired it by

purchase from the original owners with all the rights and interest therein including occupancy right. There was

an union of the interests of the lessor and the lessee and tenancy was extinguished. It was held that the flat

sold within a period of 4-5 months thereafter was Short Term Capital Gain.