Embed Size (px)

Citation preview

6 NOVEMBER 2014

Islamic Investment in Asia:

New Pockets of Growth

Excellence in Islamic Finance Research

Siti Rosina Attaullah,

Head of Islamic Capital Markets,

KFH Research Ltd, Kuwait Finance House

Global Islamic Finance Assets

MENA (ex-GCC)• Banking assets (593.9)

• Sukuk outstanding (0.3)

• Islamic funds (0.4)

• Takaful assets (7.7)

• Total assets (602.4)

Sub-Saharan

Africa• Banking assets (22.9)

• Sukuk outstanding (0.3)

• Islamic funds (1.7)

• Takaful assets (0.2)

• Total assets (25.1)

GCC• Banking assets (530.8)

• Sukuk outstanding (85.3)

• Islamic funds (32.7)

• Takaful assets (8.23)

• Total assets (657.1)

Asia• Banking assets (213.5)

• Sukuk outstanding (177.2)

• Islamic funds (25.9)

• Takaful assets (3.78)

• Total assets (420.3)

• Over the last decade, Islamic finance has gained much acceptance in the global arena as rising

awareness of Shari’a compliant propositions has prompted more countries and entities to join the

global cohort of Islamic finance stakeholders.

o The industry’s assets are expected to surpass the USD2tln mark during the 3Q2014.

o There are at least 700 Islamic financial institutions presently operating across more than

70 countries.

o MENA – and the GCC within it – and Malaysia are key jurisdictions.

*Estimated values in USD bln as of 1H14

Others (North America & Europe)

• Banking assets (71.1)

• Sukuk outstanding (6.4)

• Islamic funds (12.9)

• Takaful assets (0.01)

• Total assets (90.3)

The industry’s total

assets reached an

estimated USD1.9tln by

1H2014, having grown

by 16.94% a year during

2009-2013

INTERNATIONALISATION OF ISLAMIC FINANCE

Source: Bloomberg, IFIS, Zawya, World Islamic Insurance Directory, KFH Research

2

0

50

100

150

200

250

300

350

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

US

D b

ln

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2008 2009 2010 2011 2012 2013 2014F

US

D b

ln

GCC MENA (ex. GCC) Asia Africa (ex. North Africa) Others

STRONG GROWTH ACROSS SECTORS

Global Islamic Banking Assets

Islamic Banking

The value of global Islamic banking assets reached an estimated

USD1.53tln as at 1H2014, at a CAGR of 17.4% during 2008-2013

1

Global Sukuk Outstanding

Sukuk

Global sukuk outstanding reached USD286.41bln in 1H2014, a

6.3% expansion YTD and a 16.8% growth y-o-y

2

Global Islamic Fund Assets

Islamic Funds

The global Shari’a compliant fund management sector has reached

72.9bln in assets under management

3

Global Takaful Contributions

Takaful

Gross takaful contributions are estimated to have amounted to

USD21.5bln as at 1H2014

4

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

SaudiArabia

Malaysia GCC Asia Pacific Africa South Asia Middle East

US

D m

ln

2013E 2014F

3

0

200

400

600

800

1,000

1,200

1,400

0

10

20

30

40

50

60

70

80

2008

2009

2010

2011

2012

2013

17-S

ep-1

4

No. of fu

nds

US

D b

ln

AuM No. of funds

Source: Bloomberg, IFIS, Zawya, WIID, KFHR

4

ISLAMIC INVESTMENT IN ASIA

Banking and

financial services

penetration

Integration with

Islamic Socio

Economic Vehicles

Takaful/Insurance

Penetration

Islamic Investment in Asia:

New Pockets of GrowthCross border

funding

Trade facilities to

support intra and

inter trade activities

Infrastructure

financing

Poverty alleviation

and financial

inclusion

Entrepreneurship and

SMEs

2.0tln

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 3Q14E

US

D B

LN

S

2009-2013

CAGR = 16.94%

Global Islamic Finance Assets Growth Trend

(2009-3Q2014E)

Source: Bloomberg, United Nations Department of Economic and Social Affairs, KFHR

5

GLOBAL ECONOMIC GROWTH: ASIA IN THE BRIGHT SPOT

Global growth is projected at 3.4% in 2014 and 4.0% in 2015 (2013:

3.2%), with stronger growth in advanced economies to offset weaker

growth in emerging markets. Continued policy efforts are needed to

secure a more robust recovery.

As the most dynamic region in the world, Asia has an important

role to play in shaping the agenda for balanced and sustainable

growth.

Economic growth in Asia continues to outpace the rest of the world,

with the region rapidly increasing its importance in the global

economy, and real GDP growth will average 6.4% annually in Asia in

2014-2015.

Currently, three of the world’s four largest economies by purchasing

power parity (PPP) are Asian; China, India and Japan already

account for a quarter of the world economy, with that share

increasing to 30.0% by the end of the decade.

Asia’s GDP Growth Trend (2006-2015F)

6.4 6.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2006

2007

2008

2009

2010

2011

2012

2013

2014E

2015F

% y

-o-y

1.9 1.73.0

2013 2014E 2015F

US

-0.4

1.1 1.5

2013 2014E 2015F

Euro-zone

4.5 4.54.5

2013 2014E 2015F

GCC

0

1000000

2000000

3000000

4000000

5000000

6000000

Africa Asia Europe LatinAmerica

NorthAmerica

Oceania

Th

ou

sa

nd

s

1950

2010

2050F

More than half of the world’s population lives in

Asia, and fast growing populations will create a

demand for various goods and services

Favourable demographic structure, rising middle income segment, constitutes a huge and growing consumer

market, which can heighten the demand for a wider spectrum of Islamic financial products and services

6

Largest Muslim Population by Country: 2030

0

50

100

150

200

250

300

Pa

kis

tan

Indo

nesia

India

Ba

ng

lade

sh

Nig

eri

a

Eg

yp

t

Ira

n

Tu

rke

y

Afg

ha

nis

tan

Ira

q

Mln

Top 10 countries

total: 1.42bln

CATALYST TO IMPROVE LEVEL OF BANKING PENETRATION IN ASIA

Asia’s Sub-

regions

Average GDP per Capita at PPP (current USD)

2006 2008 2010 2012

Central and

West AsiaUSD3,738 USD4,592 USD4,867 USD5,982

East Asia USD20,205 USD22,801 USD24,661 USD27,234

South Asia USD3,032 USD3,600 USD3,717 USD4,666

Southeast Asia USD13,629 USD14,442 USD15,295 USD16,528

The Pacific USD3,678 USD4,304 USD4,266 USD4,313*

Asia: Average GDP Per Capita at PPP (2006-2012)

Source: ADB

Source: Pew Research

CAGR of Islamic and Conventional Banking Assets:

Selected Markets (2008-2013)

16.1%17.6%

11.5%13.4%

26.8%

29.9%

37.4%

29.7%

5.9% 7.4%5.2%

1.0%

15.8%17.2%

15.5%

12.2%

SaudiArabia

Malaysia UAE Kuwait Qatar Turkey Indonesia Pakistan

Islamic banking Conventional banking

• Global Islamic banking assets reached an estimated

USD1.5tln as at 1H2014, having recorded a CAGR of

17.4% between 2008 and 2013

• Asian jurisdictions cumulatively make up the third largest

domicile area for Shari’a compliant banking assets -13%

share. By 2020, more than 60% of Muslims is located in

Asian region

• During the period from 2008 to 2013, the highest CAGR in

Islamic banking assets have been recorded in Indonesia

(37.4%), Turkey (29.9%) and Pakistan (29.7%).

• The Islamic banking sector, which comprises the majority of

global Islamic finance assets, is forecasted to amount to

almost USD1.7tln by end-2014.

18.97

10.5610.549.65

8.68

6.495.62 5.45

4.5 3.93 3.82 3.23 2.89 2.881.31 1.07

0

2

4

6

8

10

12

14

16

18

20

World's average: 7.93 %

World's average: 22.42%

BANKING ACCOUNTS PENETRATION IN ASIA

7

% of Adults Who Use Account at a Financial Institution for Business

Transactions or for Both Business and Personal Transactions (% age 15+)

% of Population above 15 years that Saved at Financial Institutions in

Asian Countries

Source: World Bank database, based on Survey conducted in 2011

Region Formal

Financial

Institution

(%)

Friends and

Family (%)

World 9% 22.8%

MENA 5% 31.1%

South Asia 8.7% 19.5%

SSA 4.7% 39.9%

Access to Credit – By Source of Borrowing

Current and Projected Muslim Population

(by Region)

1,296

439 386

58 110

200

400

600

800

1,000

1,200

1,400

Asia

Pacific

ME

NA

Su

b-

Sa

hara

nA

fric

a

Eu

rope

Am

erica

s

mln

2010 2030F

10 out of 30 emerging markets have large Muslim

populations

8

STRONG POTENTIAL FOR WAQF TO BE DEVELOPED

Source: KFH Research

Islamic

microfinance

Sukuk

issuances

Project

financing

Islamic Da’wah Foundation Malaysia, issued waqf shares in

2006, to fund construction of training centre. The shares were

endowed entirely to the waqf.

Takaful

Synergies between IF and Waqf

Part of a donation (USD130mln) to the IDB, was registered as

the Fa’el Khair Waqf, and utilised to provide Qard financing to

cyclone victims in Bangladesh. Later, 1/3rd of programme funds

was repatriated into the waqf and invested in Islamic avenues

to cover administrative costs.

Majlis Ugama Islam Singapure (MUIS) issued a sukuk based

on partnership (Musharakah) with its investors, to purchase and

develop several prime properties.

All registered takaful companies in Pakistan operate on the

basis of a wakalah-waqf hybrid model.

9

ISLAMIC FINANCING FOR SMEs

Source: Various banks, KFH Research

Islamic Corporation for the Development of the Private Sector (ICD)and the World Bank have partnered with several banks and SME-related institutions in Bahrain, Tunisia, Kenya and many others

The world’s first Shari’a-compliant crowd-funding platform wasformed in 2012 in Egypt, with aim of “bridging the gap betweenmicrofinance and big venture capital while prioritising ethics”

- Driven by private sector

However, regulatory framework for crowd-funding still at nascentstages:

- Malaysia’s Securities Commission Malaysia recently releaseda public consultation paper seeking public feedback on theproposed regulatory framework for equity crowd-funding

Apart from banks, multilateral development agencies and crowd-funding platforms have leveraged on IF

Project and contract financing

Mudharabah

Musharakah

Working capital

Murabahah

Cash line facility

Tawarruq

Asset purchase

Istisna'

Murabahah

Ijarah

BBA

Diverse range of IF contracts for SMEs’ financing needs

Source: Halal Development Corporation, Thomson Reuters, KFH Research

Halal sectors worldwide were valued cumulatively at USD3.2tln in

2012 and are forecasted to reach USD6.4tln by 2018F.

• Islamic finance has a distinct competitive advantage with regard

to servicing the halal market over its conventional counterpart.

o Islamic banks can facilitate trade, SME, working capital

and leasing financing deals.

o Halal investment options may also be explored through

Islamic private equity funds.

ISLAMIC FINANCE TO SUPPORT HALAL SECTORS OPPORTUNITIES

10

Global Halal Economy by Sectors

(2012 & 2018F)

Islamic finance, USD3.91tln

Halal food, USD1.6tln

Muslim clothing, USD0.32tlnTourism,

USD0.18tln

Recreation, USD0.21tln

Pharma/cosmetics, USD0.14tln

2012 2018F

*Based on totals of expenditure of Muslim consumers

& Islamic finance assets

USD790bln

USD136bln

World Halal Demand World Halal Supply

Global Halal Demand-Supply Gap*

*For five product categories only: Food & Beverage; Industrial & Chemical;

Cosmetics and Personal Care; Pharmaceuticals; Ingredients.

The current world halal demand-supply gap is

estimated at USD654bln*.

Halal demand-

supply gap:

~80% or

USD654bln

End-to-End Shari’a Compliance:

Islamic financial services solutions are essential to

ensure the Shari’a compliance of the entire

product/service supply chain for brand integrity and

Islamic investing purposes.

SUKUKS HAVE POTENTIALS TO SUPPORT INFRASTRUCTURE NEEDS

Islamic finance could partly shoulder the region’s infrastructure financing needs, given that sukuks have

gradually emerged to be a viable alternative for infrastructure financing

11Source: KFHR, ADB

Annual Infrastructure Investment Needs in

Selected Asia Countries

USD (blns)

10,848

0

5,000

10,000

15,000

20,000

25,000

30,000

2001

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

3Q

14

US

D m

ln

Infrastructure Sukuk Issuances (USD mln per year)

Malaysia66.18%

UAE10.11%

Indonesia0.13%

Pakistan0.42%

Saudi Arabia22.39% Kuwait

0.49%

Brunei0.10%

Iran0.11%

Nigeria0.07%

Infrastructure Sukuk Issuances (by contract)

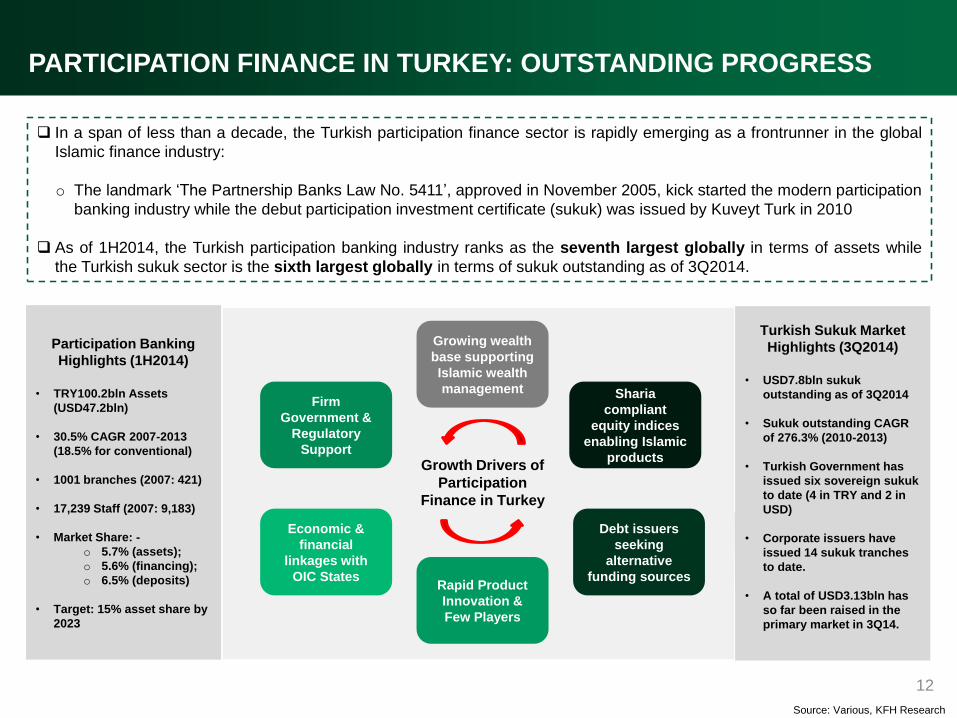

PARTICIPATION FINANCE IN TURKEY: OUTSTANDING PROGRESS

In a span of less than a decade, the Turkish participation finance sector is rapidly emerging as a frontrunner in the global

Islamic finance industry:

o The landmark ‘The Partnership Banks Law No. 5411’, approved in November 2005, kick started the modern participation

banking industry while the debut participation investment certificate (sukuk) was issued by Kuveyt Turk in 2010

As of 1H2014, the Turkish participation banking industry ranks as the seventh largest globally in terms of assets while

the Turkish sukuk sector is the sixth largest globally in terms of sukuk outstanding as of 3Q2014.

Source: Various, KFH Research

12

Firm

Government &

Regulatory

Support

Growing wealth

base supporting

Islamic wealth

management

Economic &

financial

linkages with

OIC States

Sharia

compliant

equity indices

enabling Islamic

products

Debt issuers

seeking

alternative

funding sourcesRapid Product

Innovation &

Few Players

Growth Drivers of

Participation

Finance in Turkey

Participation Banking

Highlights (1H2014)

• TRY100.2bln Assets

(USD47.2bln)

• 30.5% CAGR 2007-2013

(18.5% for conventional)

• 1001 branches (2007: 421)

• 17,239 Staff (2007: 9,183)

• Market Share: -

o 5.7% (assets);

o 5.6% (financing);

o 6.5% (deposits)

• Target: 15% asset share by

2023

Turkish Sukuk Market

Highlights (3Q2014)

• USD7.8bln sukuk

outstanding as of 3Q2014

• Sukuk outstanding CAGR

of 276.3% (2010-2013)

• Turkish Government has

issued six sovereign sukuk

to date (4 in TRY and 2 in

USD)

• Corporate issuers have

issued 14 sukuk tranches

to date.

• A total of USD3.13bln has

so far been raised in the

primary market in 3Q14.

OVERALL PROSPECTS REMAIN BRIGHT, UNDERPINNED BY STRONG

FUNDAMENTALS

13

Sukuk

Islamic

banking

Takaful

Islamic

funds

IF assets to

surpass

USD3.5tln by

end-2018

• Growing Muslim population; greater acceptance by non-Muslims

• Financial inclusion objective

• Real economic activity (expansion, working capital)

• Protection against uncertainties and crises

• Shari’a compliant and ethical investments

• Cross-border liquidity flows

• Financing for major infrastructure and corporate projects

• More high net worth individuals

Source: KFH Research

GLOBAL FINANCIAL RISKS; ISLAMIC FINANCE NOT INSULATED

Basel III & IFSB -

Capital

Risk weighted assets

&

revenue levels

Shari’a rulings &

enhanced

governance

expectations

Unique Islamic

banking

framework

Basel III & IFSB -

Liquidity

Sukuk as growth and

capital/liquidity

instrument

Cost of funds and

operational cost

Capital and funding

pressure

Key Regulatory Reforms Potential Impact

14

Source: IMF, IFSB, KFHR

Impact on Business

Model

Regulatory transformation will demand an increase in

the depth and breath of liquidity investment tools

suitable for the industry and an adaption to radically

different growth strategies.

Islamic finance is not an insulated market – increased

market and liquidity risks at global level - magnify

market shocks and liquidity risks and provide additional

challenges to global financial markets

• Emerging market economies are more vulnerable to shocks

from advanced economies as they now absorbed a much larger

share of the outward portfolio investment from advanced

economies

9 out of 10 top Islamic finance jurisdictions are classified

as emerging markets by the major financial index suppliers

• Normalization of monetary policy and interest rate adjustment

may create greater impact on asset market volatility than before

the crisis

E.g. After the potential bond tapering announcement by

the US Fed, the global sukuk market witnessed one of the

slowest quarters since 2011 and the HSBC/Nasdaq SKBI

Total Return Index in 2Q2013 witnessed a three-year

record loss due to the potential Fed taper.

News Impact to Volatility

15

ISLAMIC INVESTMENT IN ASIA: WAY FORWARD

Unlocking Growth Opportunities of Islamic Investment in Asia

Key Enablers and Stakeholders

Advancement of Islamic

finance industry globally

Framework for Shari’a

compliant value chain

Synergy and joint

marketing

Financial Regulators Financial Institutions Businesses Consumers

Growth

outlook of

Islamic

finance

Islamic banking and sukuk sectors

are likely to sustain growth

momentum in the next decade.

Islamic asset management and

takaful will grow in tandem and

continue to build mass.

Continuing sophistication in product

development and legislative &

regulatory frameworks should help

the industry harness its inherent

principles and grow sustainably.

Opportunities

in Islamic

finance

Islamic finance is a valuable source

of flexible alternative financing for

fund seekers.

The industry naturally converges

with ethical finance, and its

fundamental features are

supportive of financial inclusion

and stability.

Islamic finance acts as a conduit

enhancing trade and financial

linkages with key emerging

markets.

KFH GLOBAL INVESTMENT RESEARCH

16

THANK YOU

"Best Research in Islamic Finance”

Master of Islamic Funds Award

November 2007

“New Provider for Islamic Finance Research”

5th KLIFF Islamic Finance Awards

November 2008

“Contribution to Research in

Islamic Finance 2009”

International Islamic Finance Forum April 2009

“Best Islamic Research Company”

Islamic Finance News Awards Poll 2008

January 2009

“Best Islamic Research Company”

Islamic Finance News Awards Poll 2009

January 2010

“Best Islamic Finance Research House”

The Asset Triple A Islamic Finance Awards 2009

“Outstanding Contribution to Islamic

Finance”

Failaka-Amanie Symposium, Dubai

April 2010

“Contribution to Islamic Finance Research”

International Islamic Finance Forum, Dubai

May 2010

“Best Islamic Finance Research House 2011”

The Asset Triple A Islamic Finance Awards

2011

“Best Islamic Research Firm”

Islamic Finance News Awards Poll 2011

November 2011

“Best Islamic Finance Research House 2012”

The Asset Triple A Islamic Finance Awards 2012

“Best Islamic Consulting Service 2012”

The Asset Triple A Islamic Finance Awards 2012

“Best Islamic Finance Research House 2013”

The Asset Triple A Islamic Finance Awards 2013

“Best Islamic Consulting Service 2013”

The Asset Triple A Islamic Finance Awards 2013

“Best Islamic Research Firm 2013”

Islamic Finance News Awards Poll 2013

“Best Islamic Consulting Service 2014”

The Asset Triple A Islamic Finance Awards

2014

“Best Islamic Finance Research House 2014”

The Asset Triple A Islamic Finance Awards

2014