Embed Size (px)

Citation preview

isi o.i.

mV- ^;

^ f ir

iternenis

- c

Analyzing the Reasons Behind the Trend

Bv Lynn E. Turner and Thomas R. WeiHch

Financial restatements reached tiew heights in 2005, and the first nine monthsof 2006 restatements arc ahead of last year. Just when the number of erro-neous financial reports by publicly traded companies seemed to have peaked.they have continued to climb. The results show why investors can't afford a

return to pre-Enron securities regulation.

This article analyzes financial statement restatements during 2005 and the first ninemonths of 2006 obtained from a comprehensive analysis of nearly 25,000 company fil-ings with the SEC. The article highlights the main causes of restatements, commentson restatements and securities litigation, and looks at the restatement rates of particularauditing firms.

The authors' research focused on restatements filed to correct accounting errors and,therefore, did not include restatements for changes in accounting principles (e.g., GAAP-to-GAAP changes, changes in estimates, or mandated adoptions of new accountingpronouncements). It also excluded restatements filed to add new discussion, to makeminor wording changes, or to correct typographical errors. Because SFAS 154. AccountingChanges and Error Corrections, took effect for companies with fiscal years beginningafter December 15, 2005, this study relied on the definition of an accounting error inAccounting Principles Board (APB) Opinion 20, Accounting Changes, where para-graph 13 states: "Errors in financial statements result from mathematical mistakes, mis-takes in the application of accounting principles, or oversight or misuses of facts thatexisted at the time the financial statements were prepared. A change from an account-

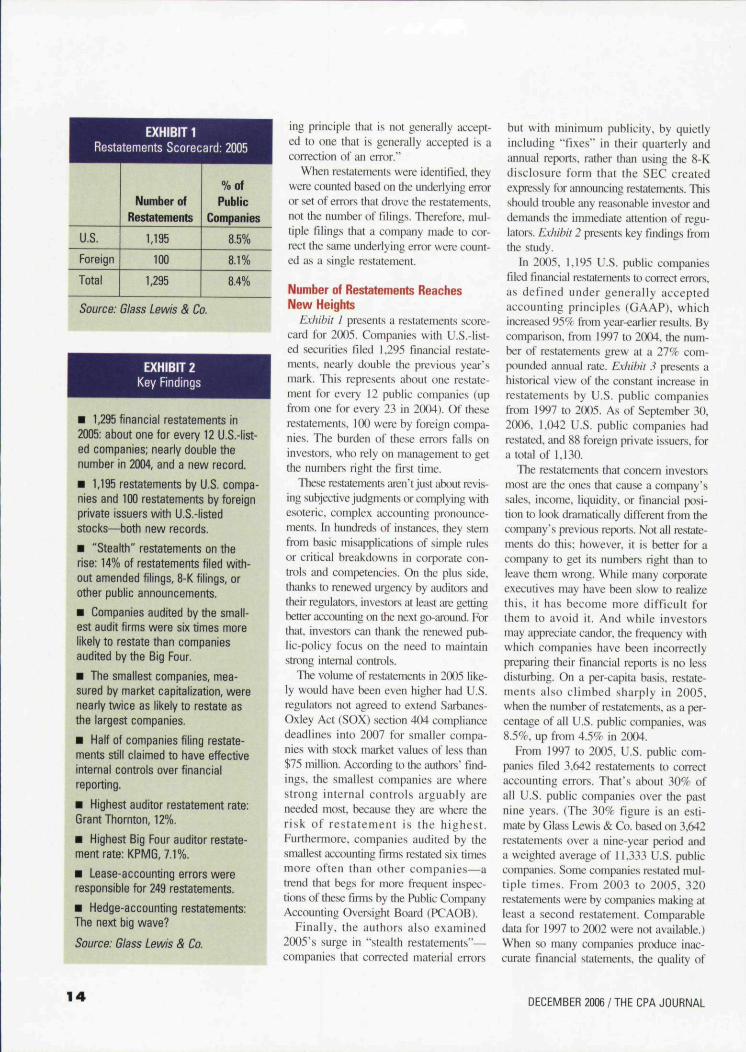

EXHIBIT 1Restatements Scorecard: 2005

U.S.

Foreign

Total

Number of

Restatements

1,195

100

1,295

%of

Public

Companies

8.5%

8.1%

8.4%

Source: Glass Lewis & Co.

EXHIBIT 2Key Findings

• 1,295 financial restatements in2005: about one for every 12 U.S.-list-ed companies; nearly double thenumber in 2004, and a new record.

• 1,195 restatements by U.S. compa-nies and 100 restatements by foreignprivate issuers with U.S.-listedstocks—both new records.

• "Stealth" restatements on therise: 14% of restatements filed with-out amended filings, 8-K filings, orother public announcements.

• Companies audited by the small-est audit firms were six times morelikely to restate than companiesaudited by the Big Four.

• The smallest companies, mea-sured by market capitalization, werenearly twice as likely to restate asthe largest companies.

• Half of companies filing restate-ments still claimed to have effectiveinternal controls over financialreporting.

• Highest auditor restatement rate:Grant Thornton, 12%.

• Highest Big Four auditor restate-ment rate: KPMG, 7.1%.

• Lease-accounting errors wereresponsible for 249 restatements.

• Hedge-accounting restatements:The next big wave?

Source: Glass Lewis & Co.

ing principle that is not generally accept-ed to one that is generally accepted is acotrection of an error."

When restatements were identified, theywere counted based on the underlying erroror set of errors that drove the restatements.not the number of filings. Therefore, mul-tiple filings that a company made to cor-rect the same underlying error were count-ed as a single restatement.

Number of Restatements ReacbesNew Heights

Exhibit I presents a restatements score-card lor 2005. Companies with U.S.-list-ed securities filed 1.295 financial restate-ments, neiirly double the previous year'smark. This represents about one restate-ment for every 12 public companies (upfrom one for every 23 in 2004). Of theserestatements. 100 were by foreign compa-nies. The burden of tbese errors falls oninvestors, who rely on management to getIhe numbers right the first time.

TTiese restatements aren't just about revis-ing subjective judgments or complying withesoteric, complex accounting pronounce-ments. In hundreds of instances, they stemfmm basic misapplications of simple lulesor critical breakdowns in corporate con-trols and competencies. On the plus side,thanks to renewed urgency by auditors andtheir regulators, investors at least are gettingbetter accounting on the next go-an^und. Eortbat, investors can thank the renewed pub-lic-policy focus on the need to maintainstrong internal controls.

Tlie volume of restatements in 2005 like-ly would have been even higher had U.S.regulators not agreed to extend Sarbanes-Oxley Act (SOX) section 404 compliancedeadlines into 2CK)7 for smaller compa-nies with stock miu'ket values of less than$75 million. According to the authors" find-ings, the smallest companies are wherestrong internal controls arguably areneeded most, because they ;ire where therisk of restatement is the highest.Furthermore, companies audited by thesmallest accounting tlmis restated six timesmore often than other companies—atrend that begs for more frequent inspec-tions of these flmis by the Public CompanyAccounting Oversight Botird (PCAOB).

Einally, the authors also examined20(}5's surge in "stealth restatements"—companies that corrected material errors

but with minimum publicity, by quietlyincluding "tixes" in their quarterly andannual reports, rather than using the 8-Kdisclosure form that the SEC createdexpressly for announcing restatements. Thisshould trouble any reasonable investor anddemands the immediate attention of regu-lators. Exhihii 2 presents key findings fromthe study.

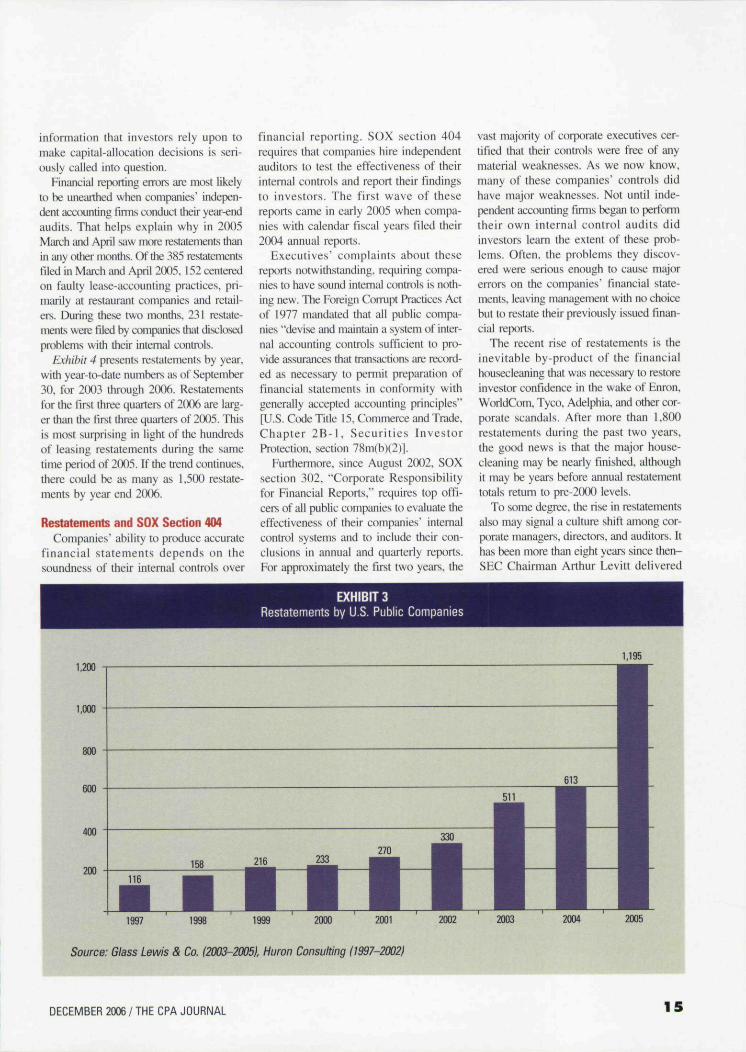

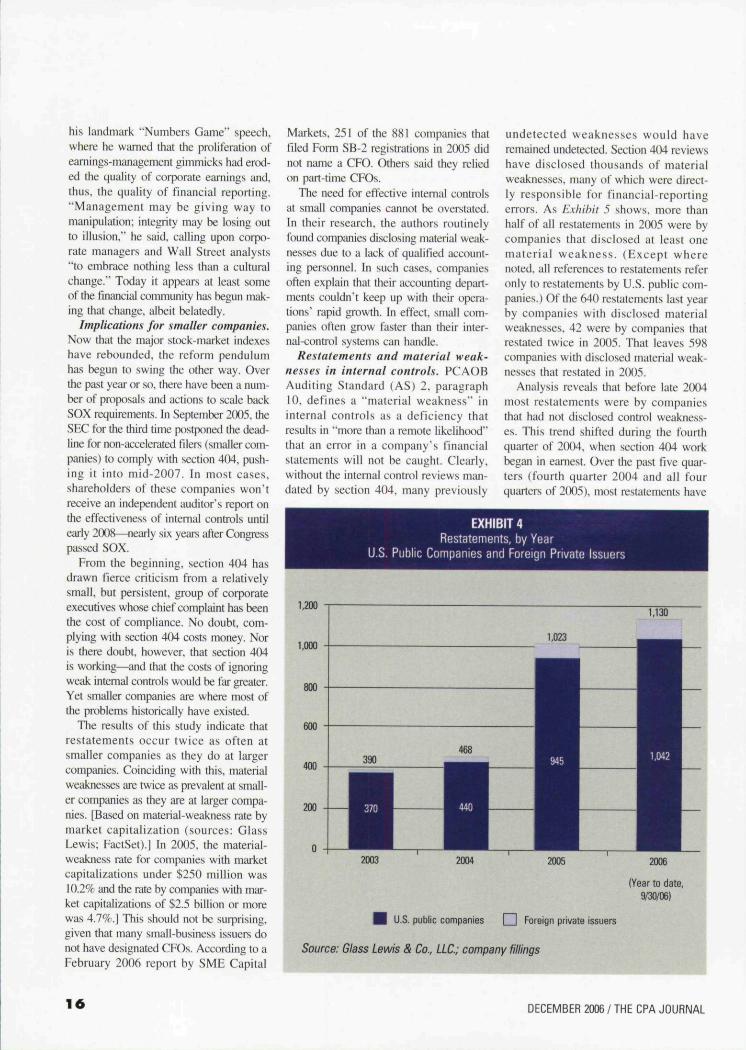

In 2(H)5, 1,195 U.S. public companiesfiled financial restatements lo correct errors,as defined under generally acceptedaccounting principles (GAAP), whichincreased 95% from year-earlier results. Bycomparison, from 1997 to 2004, the num-ber of restatements grew at a 27'/r com-pounded annual rate. Exhibit 3 presents ahistorical view of the constant increase inrestatements by U.S. public companiesfrom 1997 lo 2005. As of September 30,2006, I,(J42 U.S. public companies badrestated, and 88 foreign private issuers, fora total of 1.130.

The restatements that concern investorsmost are the ones that cause a company'ssales, income, liquidity, or financial posi-tion to look dramatically difterent from tbecompany's previous reports. Nol all restate-ments do this; however, it is better for acompany to get its numbers right tban toleave tbem wrong. While many corporateexecutives may have been slow to realizethis, it has become more difficult forthem to avoid it. And while investorsmay appreciate candor, the frequency withwhich companies have been incorrectlypreparing their financial reports is no lessdisturbing. On a per-capita basis, restate-ments also climbed sharply in 2005,when tbe number of restatements, as a per-centage of all U.S. public companies, was8.5%, up from 4.5'/c in 20(H.

Erom 1997 to 2005, U.S. public com-panies filed 3,642 restatements to correctaccounting errors. That's about MH- ofall U.S. public companies over the pastnine years. (The 30% figure is an esti-mate by Glass Lewis & Co. based on 3,642restatements over a nine-yeiir peritxl anda weighted average of \\.3^^ U.S. publiccompanies. Some companies restated mul-tiple times. Erom 2003 to 2005, 320restatements were by companies making atleast a second restatement. Comparabledata for 1997 to 2002 were not available.)When so many companies produce inac-curate financial statements, the quality of

1 4 DECEMBER 2006 / THE CPA JOURNAL

information that investors rely upon tomake capital-allocation decisions is seri-ously called into question.

Financial reporting errors are most likelyto be unearthed when companies" indepen-dent accounting finns conduct their year-endaudits. That helps explain why in 2005March and April saw more restatements thanin any otber months. Of the 385 restatementsfiled in March and April 2005, 152 centeredon faulty lease-accounting practices, pri-marily at restaurant companies and retail-ers. During these two months, 231 restate-ments were filed by companies that disclosedproblems with their intemal controls.

Exhibit 4 presents restatements by year,with year-to-date numbers as of September30, for 2003 through 2006. Restatementsfor the first three quarters of 2(X)6 are larg-er than tbe fu t three quiirters of 2005. Thisis most surprising in light of the hundredsof leasing restatements during the sametime period of 2(X)5. If the trend continues,there could be as many as 1,500 restate-ments by year end 2006.

Restatements and SOX Section 404Companies' ability to produce accurate

financiai statements depends on thesoundness of their intemal controls over

financial reporting. SOX section 404requires that companies hire independentauditors to test the effectiveness of theirinternal controls and report their findingsto investors. The first wave of thesereports came in early 2005 when compa-nies with calendar fiscal years filed their2004 annual reports.

Executives' complaints about thesereports notwithstanding, requiring compa-nies to have sound intemal controls is noth-ing new. The Foreign Corrupt Practices Actof 1977 mandated that all public compa-nies "devise and maintain a system of inter-nal accounting controls sufficient to pro-vide assurances that transactions iire record-ed as necessary to pennit preparation offinancial statements in conformity withgenerally accepted accounting principles"[U.S. Ctxie Title 15, Commerce and Trade,Chapter 2B-I , Securities InvestorProtection, section 78m(b)(2)|.

Furthermore, since August 2(X)2, SOXsection 302, "Corporate Responsibilityfor Financial Reports," requires top offi-cers of all public companies to evaluate theeffectiveness of tbeir companies' intemalcontrol systems and to include tbeir con-clusions in annual and quarterly reports.For approximately the first two years, the

vast majority of corporate executives cer-tified that their controls were free of anymaterial weaknesses. As we now know,many of these companies' controls didhave major weaknesses. Not until inde-pendent accounting firms began to pertbrmtheir own internal control audits didinvestors learn the extent of these prob-lems. Often, tbe problems they discov-ered were serious enough to cause majorerrors on the companies' financial state-ments, leaving management with no cboicebut to restate their previously issued finan-cial reports.

The recent rise of restatements is theinevitable by-product of the financialhousecleaning that was necessary to restoreinvestor confidence in the wake of Enron,WorldCom, Tyco, Adelphia, and other cor-porate scandals. After more than 1,800restatements during the past two years,the good news is that the major house-cleaning may be nearly finished, althoughit may be years before annual restatementtotals return to pre-2(XX) levels.

To some degree, the rise in restatementsalso may signal a culture shift among cor-porate managers, directors, and auditors. Ithas been more than eight years since then-SEC Chairman Arthur Levitt delivered

EXHIBIT 3Restatements by U.S. Public Companies

1,200

1.000

1.195

400

200

• I , 1 , 1 , 1 , 1 • 1 I1997 1998 1999 2000 2001 2002 2003 2004 2005

Source: Glass Lewis & Co. (2003-2005}, Huron Consultitig (1397-2002)

DECEMBER 2006 / THE CPA JOURNAL 15

his landmark "Numbers Game" speeeh,where he warned that the proliferation ofeamings-managenient gimmicks had erod-ed the quality of corporate earnings and,thus, the quality of financial reporting."Management may be giving way tomanipulation; integrity may be losing outto illusion." he said, calling upon corpo-rate managers and Wall Street analysts"to embrace nothing less than a culturalchange." Today it appears at least someofthe financial eommunity has begun mak-ing that change, albeit belatedly.

Implications for smaller companies.Now that the major sttick-market indexeshave rebounded, the reform pendulumhas begun to swing the other way. Overthe past year or so. there have been a num-ber of proposals and actions to seale baekSOX requirements. In September 2(X).'i. theSEC for the third time postponed the dead-line ior non-accelerated filers (smaller com-panies) to comply with section 404. push-ing it into mid-2007. In most cases,shareholders of these companies won'treceive an independent auditor's report onthe effectiveness of internal controls untilearly 2(X)8—nearly six years after Congresspassed SOX.

From the beginning, section 404 hasdrawn fierce criticism from a relativelysmall, but persistent, group of corporateexecutives whose chief complaint has beenthe cost of compliance. No doubt, com-plying with seetion 404 costs money. Noris there doubt, however, that section 404is working—and that the costs of ignoringweak internal controls would be far greater.Yet smaller companies are where most ofthe problems historieally have existed.

The results of this study indicate thatrestatements oeeur twice as often atsmaller companies as they do at largercompanies. Coinciding with this, materialweaknesses are twice as prevalent at small-er companies as they are at larger compa-nies. [Based on material-weakness rate bymarket capitalization (sources: GlassLewis; FaetSet).] In 2(M)5, the material-weakness rate for eompanies with marketeapitalizations under $250 million was10.2% and the rate by companies with mar-ket eapitalizations of $2.5 billion or morewas 4.1%.] This should not be surprising.given that many small-business issuers donot have designated CFOs. According to aFebruary 2006 report by SME Capital

Markets, 251 of the 881 companies thatliled Form SB-2 registrations in 2(K)5 didnot name a CFO. Others said they reliedon part-time CFOs.

The need for effective internal controlsat small eompanies eannot be overstated.In their researeh, the authors routinelyfound companies diselosing material weak-nesses due to a lack of qualified account-ing personnel. In such cases, companiesoften explain that their aeeounting depart-ments couldn't keep up with their opera-tions' rapid growth. In effect, small com-panies often grow faster than their inter-nal-control systems can handle.

Restatements and material weak-nesses in internal controts. PCAOBAuditing Standard (AS) 2. paragraph10. defines a "material weakness" ininternal controls as a deficiency thatresults In "more than a remote likelihood"that an error in a eompany's financialstatements will not he caught. Clearly,without the internal control reviews man-dated by seetion 404, many previously

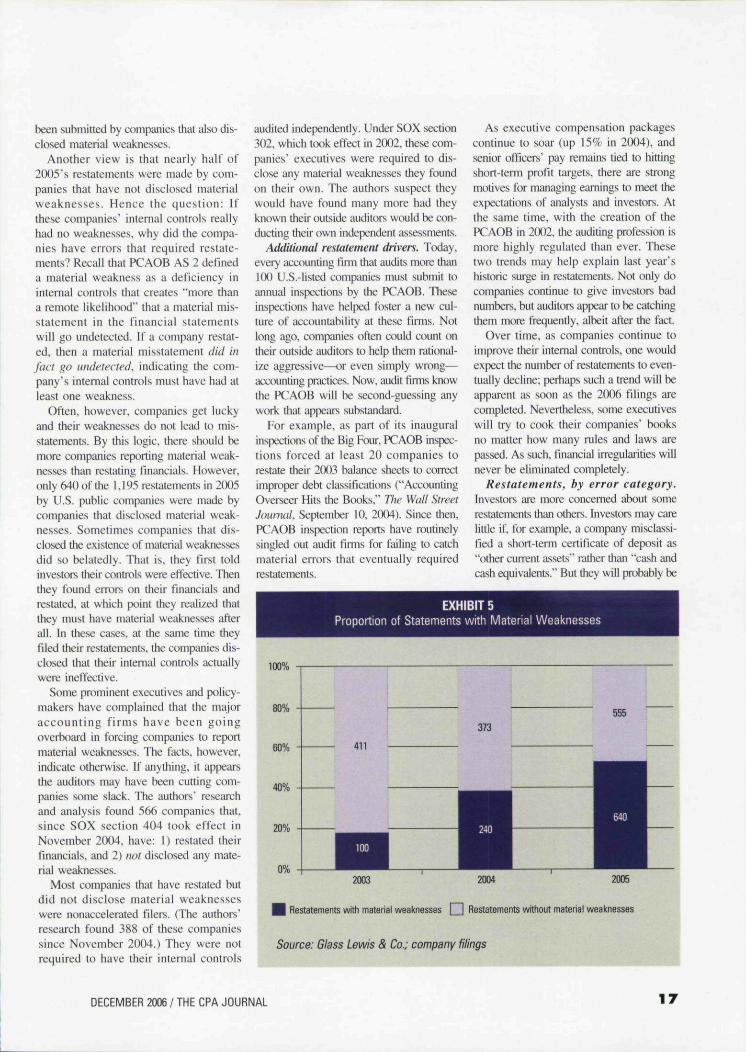

undetected weaknesses would haveremained undetected. Section 404 reviewshave diselosed thousands of materialweaknesses, many of which were direet-ly responsible for financial-reportingerrors. As Exhibit 5 shows, more thanhalf of all restatements in 2005 were bycompanies that disclosed at least onematerial weakness. (Except wherenoted, all references to restatements referonly to restatements by U.S. public com-panies.) Ofthe 640 restatements last yearhy companies with diselosed materialweaknesses, 42 were by companies thatrestated twice in 2005. That leaves 598companies with disclosed material weak-nesses that restated in 2005.

Analysis reveals that before late 2004most restatements were by companiesthat had not disclosed eontrol weakness-es. This trend shifted during the fourthquiuler of 2004, when seetion 404- workbegan in earnest. Over the past five quar-ters (fourth quarter 2004 and all fourquarters of 2(X)5). most restatements have

EXHIBIT 4Restatements, by Year

U.S. Public Companies and Foreign Private Issuers

1,200

1,000

800

600

2003 2004 2005 2006

(Year to date,9/30/06)

H U.S. public companies Q Foreign private issuers

Source: Glass Lewis & Co., LLC; company fillings

1 6 DECEMBER 2006 / THE CPA JOURNAL

been submitted by companies that also dis-closed material weaknesses.

Another view is that nearly half of2CX)5's restatements were made by com-panies that have nol disclosed materialweaknesses. Hence the question: Ifthese companies' internal controls reallyhad no weaknesses, why did the compa-nies have errors that required restate-ments? Recall that PCAOB AS 2 defineda material weakness as a deficiency inintemal controls thai creales "more thana remote likelihood" that a material mis-statement in the financial statementswill go undetected. If a company restat-ed, then a material misstatcment did infact go undetected, indicating the com-pany's internal controls must have had atleast one weakness.

Often, however, companies get luckyand their weaknesses do not lead to mis-statements. By this logic, there should bemore companies reporting material weak-nesses than restating tinancials. However,only 640 of the 1. 195 restatements in 2(K)5by U.S. public companies were made bycompanies that disclosed material weak-nesses. Sometimes companies that dis-closed the existence of material weaknessesdid so belatedly. That is. they first toldinvestors their controls were effective. Thenthey found errors on their financials andrestated, at which point they realized thatthey musi have material weaknesses afterall. In these cases, at the same time theyfiled their restatements, the companies dis-closed that their intemal controls actuallywere ineffective.

Some prominent executives and policy-makers have complained that the majoraccounting firms have been goingoverboard in forcing companies to reportmaterial weaknesses. The facts, however,indicate otherwise. If anything, it appearsthe auditors may have been cutting com-panies some slack. Thc authors' rese;m:hand analysis found 566 companies that,since SOX section 404 took effect inNovember 2004. have: I) restated theirfinancials, iuid 2) not disclosed any mate-rial weaknesses.

Most companies that have restated butdid not disclose material weaknesseswere nonaccelerated filers. (The authors"research found 388 of these companiessince November 2004.) They were notrequired to have their intemal controls

audited independently. Under SOX section302. which took effect in 2002. these com-panies' executives were required to dis-close any material we;iknesses they foundon their own. The authors suspect theywould have found many more had theyknown their outside auditors would be con-ducting their own independent assessments.

Additional restatement drivers. Today,every accounting finn that audits more than100 U.S.-iisted companies must submit toannual inspections by the PCAOB. Theseinspections have helped foster a new cul-ture of accountability at these firms. Notlong ago, companies often could count ontheir outside auditors to help them rational-ize aggressive—or even sitnply wrong—acc(5unting practices. Now, audit finm knowthe PCAOB will be second-guessing anywork that appears substandani.

For example, as part of its inauguralinspections of the Big Four, PCAOB inspec-tions forced at least 20 companies torestate their 2(K)3 balance sheets to correctimproper debt classifications ("AccountingOverseer Hits the Books." The Wall StreetJournal. September 10. 2004). Since then,PCAOB inspection reports have routinelysingled out audit firms for failing to calchmaterial errors that eventually requiredrestatements.

As executive compensation packagescontinue to soar (up 15% in 2004), andsenior officers" pay remains tied to hittingshort-term profit targets, there are strongmotives for managing earnings to meet theexpectations of analysts and investors. Atthe same time, with the creation of thePCAOB in 2(X)2, the auditing profession ismore highly regulated than ever. Thesetwo trends may help explain la.st year"shistoric surge in restatements. Not only docompanies continue to give investors badnumbers, but auditors appear to be catchingthem more frequently, albeit after the fact.

Over time, as companies continue toimprove their intemal controls, one wouldexpect the number of restatements to even-tually decline; perhaps such a tn;nd will beapparent as soon as the 2006 filings arecompleted. Nevertheless, some executiveswill try to cook their companies' booksno matter how many rules and laws arepassed. As such, financial irregularities willnever be eliminated completely.

Restatements, by error category.Investors are more concemed about somerestatements than others. Investors may carelittle if. for example, a company miscla.ssi-fied a short-temi cenillcate of deposit as"other current assets"" rather than "cash andcash equivalents.'" But they will probably be

EXHIBIT 5Proportion of Statements with Material Weaknesses

100%

0%2003 2004 2005

B Restatements witti material weaknesses Q Restatements without material weaknesses

Source: Glass Lewis & Co.; company filings

DECEMBER 2006 / THE CPA JOURNAL 17

EXHIBIT 6Accounting-Error Categories

Category

Revenue recognition

Expense recognition

Misclassification

Equity

Other comprehensive

income (OCI)

Tax accounting

Ac q uisltions/i n vestme nts

Capital assets

Inventory

Reserves/allowances

Liabilities/contingencies

Other

Description

Restatements due to improper revenue accounting.

This category includes instances in which revenue was

improperly recognized, questionable revenues were

recognized, or any other related errors that led to

misreported revenue.

Restatements due to improperly recording expenses in

the incorrect period or for an incorrect amount. This

category includes restatements due to improper lease

accounting.

Restatements due to improperly classifying accounting

items on the balance sheet, income statement, or

statement of cash flows. These include restatements

due to misclassification of short- or long-term accounts

or misclassification of cash flows.

Restatements due to improper accounting for earnings

per share (EPS), stock-based compensation plans, stock

options, warrants, convertible securities, and other equity

instruments,

Restatements due to improper accounting for OCI

transactions, including foreign-currency items, unreal-

ized gains and losses on investments in debt and equity

securities, derivatives, other financial instruments, and

pension-liability adjustments.

Restatements due to errors involving correction of taxprovisions, improper treatment of tax liabilities,

deferred-tax assets and liabilities, tax contingencies,

sales tax, and other tax-related items.

Restatements due to improper purchase accounting for

business combinations, other merger- or acquisition-

related errors, and errors related to the appropriate

accounting method for significant investments in other

companies.

Restatements due to asset impairments, asset place-in-

service dates, write-downs, and depreciation and

amortization.

Restatements associated with inventory-costing valua-

tions, quantity issues, and cost-of-sales adjustments.

Restatements due to errors involving bad-debt reserves

for accounts receivable, reserves for inventory, valua-

tion allowances, provision for loan losses, or other

types of allowances and reductions of assets.

Restatements due to errors in estimated liability claims,

loss contingencies, litigation matters, commitments,

certain accruals, or other types of obligations.

Any restatement not covered by the listed categories.

Source: Glass Lewis 8t Co.

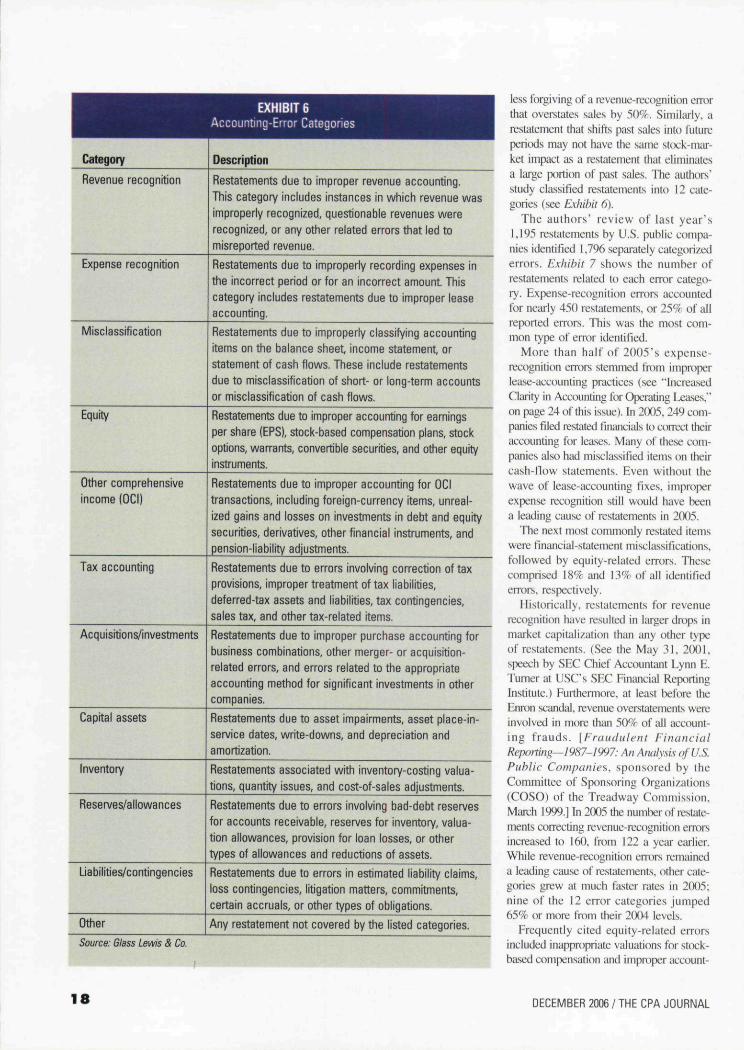

less forgiving of a rcventie-recognition errorthat overstates siilcs by 5O*7f. Similarly, arestatement that shifts past sales into futureperiods may not have the same stock-mar-kei impact as a t estateincnt that eliminatesa Ijirge portion of past sales. The authors'study classified restatements into 12 cate-gories (see Exiiibil 6).

The authors' review of lasl year's1.195 restatements by U.S. public compa-nies identified 1,796 separately categorizederrors. Exhibit 7 shows the number ofrestatements related to each error catego-ry. Expense-recognition errors accountedfor nearly 450 restatements, or 25% of allreported errors. This was the most com-mon type of error identified.

More than half of 2()05's expense-recognition errors stemmed fk)m improperlease-accounting practices (see "IncreasedClarity in Accounting for Operating Ixases."on page 24 ol" this issue). In 2(K)5. 249 com-panies filed restated financials to correct theiraccounting for leases. Many of these com-panies also had misclassified items on theircash-flow statements. Even without thewave of lease-accounting fixes, improperexpense recognition still would have beena leading cause of restatements in 2005.

The next most commonly restated itemswere financial-statement misclassifications,followed by equity-related errors. Thesecomprised 18% and 13% of all identifiederrors, respecfively.

Historically, restatements for revenuerecognition have resulted in hirger drops inmarket capitalization than any othei" typeof restatements. (See the May 31. 2(X)I.speech by SEC Chief Account;mt Lynn E.Tumer at USC's SEC Financial ReportingInstitute.) Furthennore. at least before IheEnron .seandal, revenue overstatements wereinvolved in mi re than 50% of all accoiint-ing frauds. [Fraudulent FinancialReporting—1987'm7: An Analysis of as.Public Companies. sp{)nsored by theCommittee of Sponsoring Organizations(COSO) of the Treadway Commission.March 1999.] In 2005 the number of restate-ments correcting revenue-recognition errorsincreased to 160. from 122 a year e:irlier.While revenue-recognition errors remaineda leading cause of restatements, other cate-gories grew at mueh faster rates in 2{X)5;nine of the 12 error categories Jumped65% or more from their 2(K)4 levels.

Frequently cited equity-related errorsincluded inappropriate valuations for stock-based compensation and improper account-

18 DECEMBER 2006 / THE CPA JOURNAL

ing for warrants and convertible debt.Restatements in the equity error categoryrose 77% in 2005, fueled by an Increasein errors related tt) sttx:k options and con-vertible instruments. Errors in other com-prehensive income (OCI) jumped 198%,the highest percentage increase of anycategory in 2005. Improper hedge-account-ing practices, primarily at financial insti-tutions and service companies, led to 57 ofthe 122 OCl-related restatements.

Restatements related to acquisitionsand investments more than doubled in2005. Common errors included improperpurchase accounting for business combi-nations. Some companies used the equitymethod of accounting for investmentsthat they should have consolidated, andvice versa.

From January to September 2006, 145(I77() of the restatements were for mis-classifications with 100 related to cash flowmisciassifications and 28 related to hedgeaccounting. Interestingly, the January Ithrough September 30, 2006. reviewshowed an increase in equity-type restate-ments, with 179 restatements (21 %). Theseappear to have been driven by convertible-debt eiTors where companies have had torestate the proportions they allocated todebt and equity. Smaller companies con-tinue to restate more often thiin larger com-panies. Approximately two-thirds of thc2006 restatements so far were made bycompanies with a market capitalization ofless than $1(X) million.

Lease-accounting restatements. After20()5's wave of lease-accounting restate-ments, one lesson should be drilled intothc minds of accountants: Just becauseeverybody"s doing it doesn"t make itright. In a February 2{X)5 open letter tothe AICPA. then-SEC Chief AccountantDonald Nicolaisen noted the large num-ber of companies improperly accountingfor lease transactions. The letter, whichMr. Nicolaisen issued at the request ofthe accounting profession, laid out theSEC staffs view on the correct way todo things—a view that FASB happenedto share. As it turned out. hundreds ofcompanies simply hadn"t been follow-ing GAAP.

The infractions centered on fairly black-and-white violations of well-establishedaccounting rules. (SFAS 13, Accountingfor Leases, was issued in 1976. andFASB Technical Bulletin ^5-3. Accountingfor Operating Leases with Scheduled

Rent Increases., issued in 1985, clarifies themisapplied rules.) Typically, the viola-tions—most of which occurred in therestaurant and retail industries—had theeffect of understating rental expenses orimproperly keeping lease obligations offthe balance sheet. These violations, whichhad gone on for decades, ultimately led to249 restatements in 2005 to correct improp-er lease accounting.

This may sound familiar, because in1999, FASB Staff Accounting Bullcrin(SAB) 99, Materiality, debunked the wide-ly held but incorrect notion that companiescould let accounting misstatements slide aslong as they fell below certain quantita-tive benchmarks. (Some accountants usedto call this the 5% rule of thumb.) Somecompanies made one-time adjustments inthe fourth quarter of 2004 to correct theirlease accounting but avoided restatementsby citing immateriality.

Hedge-aceounting restatements. Almosta year to the day after the lease-accountingrestatement frenzy began, a new but famil-iar wave of restatements took its place. Afteran initial surge in March, hedge-account-ina restatements started to roll in one after

another. Perhaps it was the highly publicizedhedge-accounting woes at Fannie Mae thatprompted both Fannie Mae's auditor at thetime, KPMG, and other companies toreassess their own practices. Whatever theease, by year end, 57 companies hadrestated due to hedge-accounting errors.Because the outbreak of hedge-accountingrestatements started in late 2005, this issuewill probably continue well into the 2006financial statements.

The 57 hedge-accounting restatementsdoes not include restatements by federalhome-loan banks that do not file reportswith the SEC, although some of thesebanks also restated in the wake of irregu-larities at Fannie Mae and its govern-ment-chartered cousin. Freddie Mac.

As with the lease-accounting restate-ments, the hedge-accounting problemsstemmed from companies abiding by asupposed industry norm, notwithstandingthat the norm ran counter to GAAPrequirements. Once one company has beenscolded publicly, everybody else doing thesame thing has to face up to the fact thattheir accounting isn't GAAP either. Thenthey. ttx). must restate.

EXHIBIT 7Number of Restatements, by Error Category

Expense recongnition

Misclassification

Equity

Revenue recognition

Tax accounting

OCI

Acquisitions/investments

Capita! assets

Inventory

Liabilities/contingencies

Reserves/allowances

Other

50 100 150 200 250 300 350 400 450

• 2004 I 2005

Source: Glass Lewis

Note: The total number of errors exceeds the total number of restatements, because sotnerestatements contained multiple errors.

DECEMBER 2006 / THE CPA JOURNAL 19

Stock-Option restatements. The adop-tion of SFAS I23(R), Share-BasedPaynieni, prompted many companies toreview their accounting for slockoptions and other stock-based compen-sation. As a result, dozens of companiesrestated their financial statements, evenif only their footnote disclosures. Auditorsand corporate managers in the past maynot have given footnotes their full atten-tion in the past, but they must be audit-ed ttx). Over thc past few years especially,investors began relying heavily on com-panies' stock-option footnotes, becausethey knew the expenses disclosed therewould be harbingers of things to comeonce SFAS I23(R) took effect. Theauthors" analysis found 71 stock-options-reiated restatements in 2005, comparedto 39 in 2004,

"Steatth" RestatementsOne of Wall Street"s biggest open secrets

is that, increasingly, companies ai-e keep-ing their restatements under thc radar bymaking it difficult for shareholders to findout about them. As a result, many investorsperusing companies* financial reports aresurprised to discover I'estatements that thecompanies never previously announcai; thatis. if the investors discover them at all. Theauthors call these "stealth"" restatements.

"Stealth" means that companies restat-ed: 1) without filing an amended quarter-ly or annual report; 2) without firstannouncing the restatement in a pressrelease, filed on Fonii 8-K Item 4.02; and3) without citing the restatement as the rea-son for a late quarterly or annual report,disclosed in a Form 12b-25 "NT"" filing.The authors use the term "obscure" if acompany filed either iui amended report oran 8-K, but not both; also for a companythat disclosed a restatement in an NT fil-ing but filed neither an 8-K nor anamended report.

Trick I: Restate., but don't amend.When a company files a restatement, it typ-iciiily does so by filing an amended reportfor the period affected (for example, aForm lU-K/A for a year period, a Form10-Q/A for a quarter). The "A" alertsinvestors that something has changed.Upcjn reading the tiling, an investor usu-ally will find an expkinatory note describ-ing the reason for the amended filing; inthis case, a resliitement of previously issuedresults. While the majority of 2005'srestatements used amended reports, 45%

of restatements did not. In 2004. 9%' ofrestatements were filed without amendedreports; in 2003. just 5%' were.

Many companies avoid using amendedfilings by restating previous peritxls in theirnext regularly scheduled quarterly or annu-al filings. For example, many companiesrestated amounts for their 2003 fiscal yearsin their fiscal 2004 annual reports, filedon Form 10-K. Had these companiesinstead filed separate, amended annualImports for fiscal 2(K)3. using Form [O-K/A.their restatements would have been farmore transparent to investors.

Companies that file restatements with-out amending their prior filings often leaveinvestors unaware that prior periods havebeen restated. The authors suspect this isby design. Investors reading a compiiny"scurrent financial reports simply may notnotice the small print. They may dismissa restatement as relatively minor, becausethe company was able to tuck it awayquietly in the cuirent peri(Ki"s results.

Trick 2: Restate, but don V announce.Another way for companies to avoid draw-ing attention to restiitements is fairly obvi-ous: They don"t file press releases announc-ing them. In 2(X)4. the SEC created a sec-tion in the Form 8-K Current Report (com-monly used to file press releases) to beused by companies to warn investors thatthey shouldn't rely on previously issuedfinancial statement (SEC Release No. 33-8400, Additional Form 8-K DisclosureRequirements and Acceleration of FilingDate, effective August 23, 2(K)4). SinceAugust 23. 2004. companies have been

"required" to file Forni 8-K, Item 4.02, toannounce restatements and alert investors notto rely on the previously issued financialstatements affected by the i-estatcment. (SeeForm 8-K, Current Report GeneralInstructions, Item 4,02.) An Item 4.02 mustbe Illed if: a) "the registrant's board of direc-tors, a committee of tlie boaid of directorsor the officers ... concludes that any previ-ously issued financial statements, coveringone or more years or interim [leriods forwhich thc Registrant is required to providefinancial statements ... should no longer berelied upon because of an error in such finan-cial statements as addressed in |APBOpinion 20|." or b) "the regi.strant is advisedby, or receives notice from, its independentaccountjuit that disclosure should be miidcor action should be taken to prevent futurereliiuice on a pieviously issued audit reportor completed interim review related to pre-viously issued financial statements." Theauthors put "required" in quotes becausethere are some big Icxipholes.

Shortly after the new reporting require-ments were issued, the AICPA"s SECRegulations Committee explicitly asked theSEC if all restatements needed to be report-ed on Fomi 8-K pursuant to Item 4.02. TheSEC staff said they would support the viewofthe profession and not require all restate-ments to be announced in a Eonn 8-K,Item 4,02. The decision has led to signif-icantly less transparency surrounding thereporting of restatements.

In this case, the niles themselves maybe to blame. Where a company"s board.officers, or outside auditor concludes that

EXHIBIT 8Restatement Rate, by Audit Firm

KPMG

PwC

E&Y

O&T

Grant Thornton

BDO Seidman

- T

1

1

I•

J—0,0% 2.0% 4,0% 6.0% 8.0% 10,0% 12.0%

• 2004 B 2005

Source: Glass Lewis; Public Accounting Report

DECEMBER 2006 / THE CPA JOURNAL

any previously issued financial statementsshould not be relied upon, the company hasfour days to tile a report disclosing thatsuch an event has occurred. However, ifthe company includes that same informa-tion in a quarterly or annual report beforethe four-day period ends, the informationneed not be repeated in an 8-K.

When that four-day period begins, how-ever, is in the eye of the restater. For exam-ple, a company's auditor and board mem-bers may haggle for months about whethera restatement is necessary—before theyfiniilly "conclude" that it is. In that case.the conclusion date may fall convenientlywithin four days of when the company wasscheduled to file its next quarterly or annu-al report. Outsiders can do little to chal-lenge the company's judgment. And so therestatement announcement gets buried.

Prior to the effective date of Item 4.02,some companies did announce restatementsin Eomi 8-K tilings. In 2(K)5. 66% of com-panies that restated announced their restate-ments using Form 8-K, Item 4.02. Theauthors believe this number probably

would have been closer to 10()% had theSEC not given companies such broad dis-cretion in filing Item 4,02 disclosures.

That said, the revised 8-K reportingrequirements have improved transparencyfor investors. In 2003, just one-third ofrestatements were announced using 8-K fil-ings; in 2(X)5, two-thirds were. Still, therewere 406 restatements in 2005 where, inthe authors' view, the companies did notproperly alert investors.

Trick 3: File late, keep quiet, thenrestate. The majority of companies thatrestate postpone at least one annual or quar-terly report before they complete theirrestatements. For 64% of 2005's restate-ments, the company also was late in fil-ing either a quarterly report or an annualreport during the year. This was up fromabout 54% in both 2003 and 2004.

Assuming they become aware of a com-pany's intention to restate, investors mayinterpret a late tiling as an indication of therestatement"s severity, ll also may signalthe depth of the control weaknesses thatprecipitated the restatement. Companies

typically wait to tile restatements until theydetermine the correct amounts andbelieve they have fixed the problem thatcaused the restatement in the tlrst place.If a company is in the process of restat-ing—and unable to file financials ontime—one would expect it to explain justthat in the late-filing notices. This isn'talways the case, however: Many compa-nies fail to provide adequate explanationsin their NT filings.

In the authors' study, ofthe 191 com-panies restating in 2005 that didn't use8-K forms or amended financial reportsto disclose their restatements. 107 filed NTnotices before they restated. Of those 107.76 did not explain in their NT notices thattheir filings were late because they werebusy restating their previous periods.

Stealth restatements—the trifeeta. Torecap. 535 of 2005's restatements did notuse amended returns. There were 406restatements that weren't announced in8-Ks. As for the 760 restatements thatcame less than a year after NT notices,the vast majority of those NT notices

We think we're MicrosoftGOLD CERTIFIED

Partner

at business solutions

ivbat Microsoft thinks

Microsoft Dynamics SL, Dynamics GPand Dynamics AX

sociates42 Broadway, Suite 1814,

New York, New York 10004212-269-1313-phone

2l2-42.V405.Vrax

Microsoft Microsoft Mkrosoft2004-200b 2004-2005 1995 2005

Solomon fcxcollcncc MBS Partner of President's ClubAward the Vear for NV/NJ Award

33 Wood Avenue South, ."jth floor,iselin. New Jersey 08830

732-205-1660-phone732-205-l

5, St. John's LaneLondon England ECIM 4BH

Main Line: 020 7549 1606

www.queueassoc.com • [email protected]

DECEMBER 2006 / THE CPA JOURNAL

didn't cite the companies' forthcomingrestatements as the reason the companies'filings were late.

About 14% of 2005's restatementswere "stealth'" restatements that com-pleted the trifeeta. That is, they were: I)not filed via an amended filing, 2) notannounced in an 8-K. and 3) not men-tioned in any lale-filing notices. Thefirst time that readers of the companies"filings had thc opportunity to learn ofthese restatements was when the compa-nies filed their regularly scheduledannual or quarterly reports, in which theytucked the restated periods behind their

Assessing what it means

for an auditor to have a high

or low restatement rate is

d icu l t for outsidefs.

latest periods' numbers. There were 160stealth restatements in 2005. up from 13in 2004 and just two in 2(K)3.

Last year. 21 stealth restatements weredue to lease accounting issues. Companieswith market capitalizations of less than $75million accounted for 102 of last year" s 160stealth restatements. For companies filingrestatements, the authors believe the bestpractice is to file an 8-K, Item 4.02, as soonas they know they will restate, warninginvestors that they no longer should relyon previously issued financial statements.Companies should also file their restate-ments using amended filings that explainexactly what was corrected. And if therestatements delay their filings, they shouldexplain st) in their tate-filing notices.

Restatements and Securities LitigationContrary to what one might expect^

a corresponding rise in the number ofinvestor lawsuits seeking to recoup loss-es through class actions—the number ofsecurities class actions has gone down.mainly due to a decline in investor loss-es tied to such suits. While restatementsby U.S. public companies in 2005 set anall-time record of 1.195. securities classactions fell 17% to 176, according to aCornerstone Research study that alsofound that 89% of these lawsuits in 2(X)5alleged misrepresentations in financialdocuments, compared with 78% a yearearlier.

Because not ail restatements trigger sub-stantial market-capitalization losses, restate-ments don't necessarily lead to securitiesclass actions. Investors are more likely tosuffer large losses—and in turn tile law-suits—if a company discloses revenueoverstatements, as opposed to. say, a bal-ance-sheet misclassification.

Consider last year's 249 lease restate-ments. A few of these restatements mayhave increased expenses materially. Still,investors perceived most—but not all ofthem—to be mere technicalities, with lit-tle impact on companies' fundamentals.Such restatements aren't likely to lead toinvestor lawsuits when there are no corre-sponding drops in stock prices.

In its review of 2005 lawsuits.Cornerstone found the three most fre-quently mentioned accounting allegationswere revenue overstatements (40 cases),overstatements of accounts receivable (17cases), and understatements of liabilities(14 cases). Because these accounting issuesare the ones most likely to result in adrop in share price, they are more likely tolead to litigation.

Surprisingly, only five of the 176shiveholder suits filed in 2005 named com-panies' outside auditors as defendants,down from eight in 2(X}4, according toCornerstone. That's less than one case foreach of the six largest accounting firms—Deloitte & Touche, Pricewaterhouse-Coopers. KPMG. Ernst & Young. GrantThornton, and BDO Seidman. By com-parison, companies audited by these flrnisfiled 782 restatements in 2(X)5.

Auditor AnalysisThe first resptmsibility of auditors is to

protect the investing public. Their job isto ensure that companies' financial state-

ments are presented fairly and comply inall material respects with GAAP.Unfoitunatcly for investors, too often audi-tors fall short of their objectives.

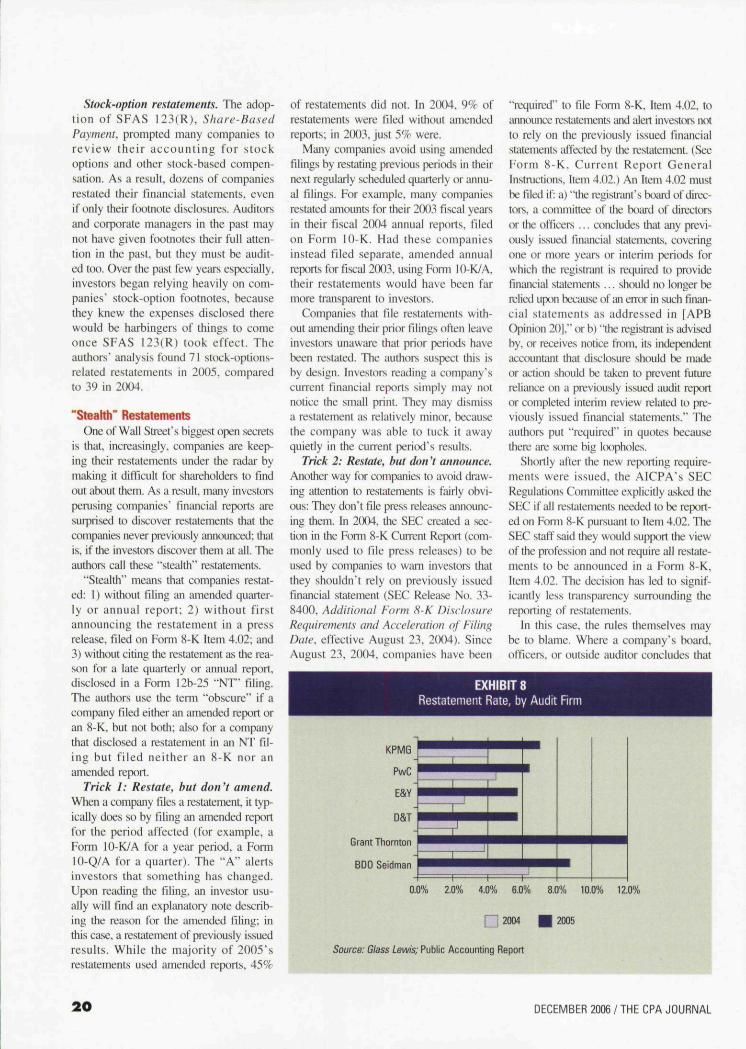

Exhibit fi shows that Grant Thomton hadthe highest restatement rate (number ofrestatements divided by total iiumber ofpublic companies audited) during 2(X)5, fol-lowed by BDO Seidman. Of ail the com-panies audited by Gram Tliornton, 12%restated during 2(K)5. compared with 3.8%in Km. Among the Big Four. KPMG's2005 restatement rate was highest: 7.1%;Deloitte & Touche's 5.6% rate was thelowest.

Assessing what it means for an auditorto have a high or low restatement rate isdifficult for outsiders. An accounting firmwith a low restatement rate may be pro-viding high-quality audits; or a low ratemay signal that the auditor seldom forcescompanies to correct mistiikes. Although ahigh restatement rate could indicate ptwraudit quality, it may also indicate thai afirm is more willing than others to requirecorrections.

PricewaterhouseCoopers and Deloittehad the largest volume of restatements inboth 2005 and 2(X)4. Both had 2(X) or morerestatements last year. While Deloitte hadthe lowesf restatement rate among the BigFour, its volume of restatements increasedby 130% in 2rK)5, the largest increase ofthe Big Four.

Companies audited by the six largestaccounting firms, including GrantThomton and BDO Seidman, accountedfor about two-thirds of 2005's restate-ments. The number of restatements atcompanies audited by other firms morethan doubled: 413 in 2005, comparedwith 189 in 2004.

Audit flniis with less than $100 millionin annual revenue had the highest restate-ment rate by far. In 2(K)5, 37.2%' of thecompanies audited by smaller firmsrestated. The authors view this rate as intol-erable. By comparison, the Big Four'scombined rate was 6.1%; the second-tierfirms' combined rate was 8.4%.

Under SOX, annual PCAOB inspectionsare required only for firms that auditmore than 100 companies with U.S.-listedsecurities. Smaller auditors must be inspect-ed once every three years. The authors'study, which found the restatement rate forsmaller flmis extraordinarily high, demon-strates that triennial inspections may not befrequent enough for some firms.

DECEMBER 2006 / THE CPA JOURNAL

While companies audited by smallerfirms restate more frequently, compa-nies audited by the Big Four still accountfor the largest volume of restatements. In2005. 706 restatements were at compa-nies audited by the Big Four, comparedwith 389 at companies audited by smallfirms. The number of Big Four restate-ments increased ^\% during 2005.while the number of restatements at smallfirms jumped 114%.

The auditor-turnover rale for companieswilh rcslatemcnts was twice as high asthe overall auditor-turnover rate. From2(X)3 to 2(XJ5, the average turnover rate forall companies was about \2^/c. The aver-age auditor-turnover rate lor companieswitli restatements during the same Ehree-year pericxi was about 24^^

Smaller Companies RestateMore Often

More than 1 \9c of U.S. public compa-nies with market capitalization of less than$250 million restated during 2(K)5. com-pared with about 6% of companies withmarket capitalizations of $2.5 billion ormore. Restatement rates increased acrossall size categories in 2005; the rates dou-bled among companies with market capi-talizations of more than $250 million.About one of every 19 companies in thelargest category ($7.5 billion or more)restated financials in 2005. comparedwith just one of every 46 in 2(X)4.

Even with the high growth in restate-ments by larger companies, what standsout is that one of every eight small com-panies (market capitalization under $75million) restated in 2(X)5. More than halfof last year's restatements were filed byIhe smallest companies, which registered6()4 restatements. The number of restate-ments declines frotn there as mtirket cap-italization rises.

The trend in 2004 was clear: Thesmaller the market capitalization or annu-al revenue, the more likely a company wasto restate. However, the trend in 2005was more mixed. Higher annual revenuesin 2(K)5 didn't necessarily translate intolower re.statement rates, although highermarket eapitalizations did.

Sarbanes-Oxley Was Notan Overreaction

Financial statement restatements contin-ue to rise. But according to a relative haiid-lul of senior executives and policy mak-

ers, the big problem isn't that investors gotbad information the first time: rather, theycontend that Congress overreacted when itpassed SOX and tliat. for the gcxxl of glob-al capitalism. Congress should now relaxthe scrutiny it imposed on corporate boardsand executives after the collapses of Enronand WorldCom.

After surveying the accountingmishaps and do-overs that were report-ed in 2(X)5 and first nine months of 2(X)6.the authors couldn't disagree more. It'sprecisely because of the heightenedaudit ing s tandards mandated by

Sarbanes-Oxley that investors are final-ly getting a true sense of how much workremains to be done before they c:ui feelconfident about the accuracy of the finan-ciai statements prepared by corporatemanagers. •

Lynn E. Turner, CFA, i.s managing direc-tor of research al Glass Lewis & Co.. LLC.and senior advisor to KroU. Inc. ThomasR. Weirich, PhD, CPA, i\ a professor ofaccounting at Central Michigan University,Mt. Pleasant, Mich.

And so is datamining with IDEA.

IDEAData Analysis Sofcwsre

IDEiA IS a regiEiiered tradBmailinf CaaaWsra intfimst.ional. Inc.

With IDEA, doing extractionsis an easy ride.IDEA also quickly and accuratelyimports, joins, analyzes andsamples data from almost anysource. Learning this powerful,easy to use, productivity tool isa breeze. And, IDEA'S free firstyear of customer support helpsyou lose the training wheels fast.For a free demo, ride up to ourweb site at www.audimation.com.

DECEMBER 2006 / THE CPA JOURNAL