Embed Size (px)

Citation preview

The cost of University Is it worth it?

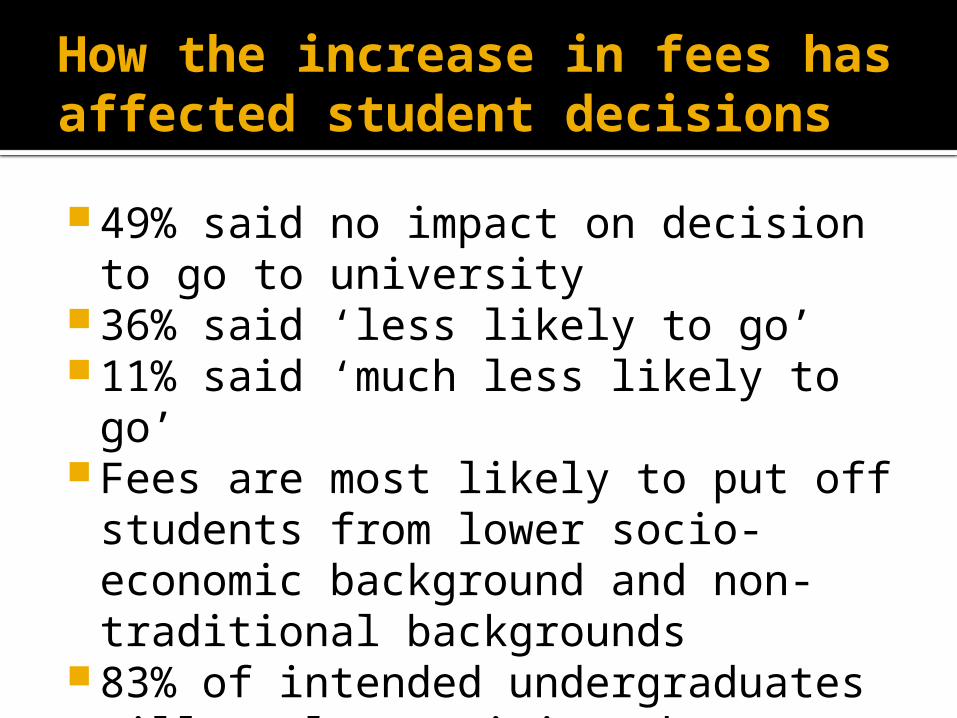

How the increase in fees has affected student decisions

49% said no impact on decision to go to university

36% said ‘less likely to go’ 11% said ‘much less likely to go’ Fees are most likely to put off

students from lower socio-economic background and non-traditional backgrounds

83% of intended undergraduates will apply to cities where living costs are lower

It depends how you see it

Should a student loan be seen as investment or graduate tax rather than debt?

There is a poor awareness of grants, bursaries and scholarships that reduce the debt

You don't need to have cash to go to university

It ISN'T a case of 'pay up or you can't go'.

Tuition fees are automatically paid by loans which you only need to start repaying in the April AFTER graduation and you are earning a reasonable salary

But you will be charged 3% above the Retail Price Index (RPI) in interest

Earn under £21,000 and you'll never repay

The loan is repaid through the income tax system. That means once you're working your employer takes it off the payroll, so you never see the money, it simply reduces the amount you receive in your pay packet

You repay 9% of everything you earn annually above £21,000.

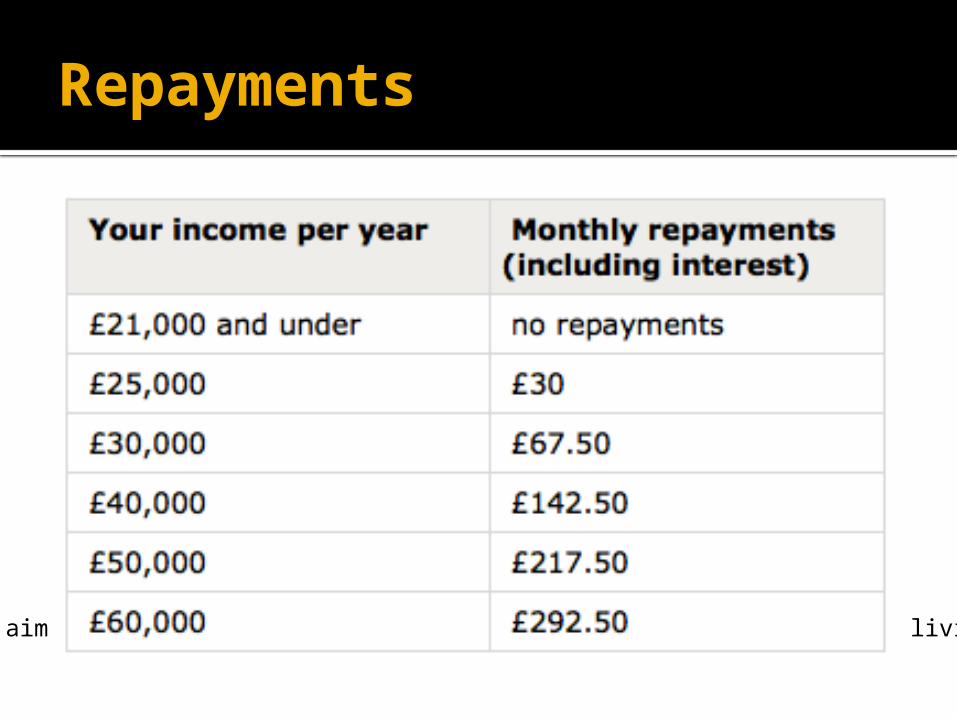

Repayments

The aim is to reduce the impact of higher fees on your standard of living

Monthly repayments are the same whether fees are £6,000 or £9,000

So you will not have more money taken from your salary when you start earning £21,000 if you went to a high fee University

But it will take longer to pay off.

Student loans and grants also cover living costs

Full-time students aged under 60 at the start of their course can also take a loan to pay for their living costs, eg food, books, accommodation and travel. These are usually paid in three termly instalments direct to students' bank accounts.

The amount is dictated by two elements: The Guaranteed bit. Up to 65% of the maximum living

cost loan will be available The Income Assessed bit. The amount you can

borrow is means-tested, in other words it depends on you or your parents’ income

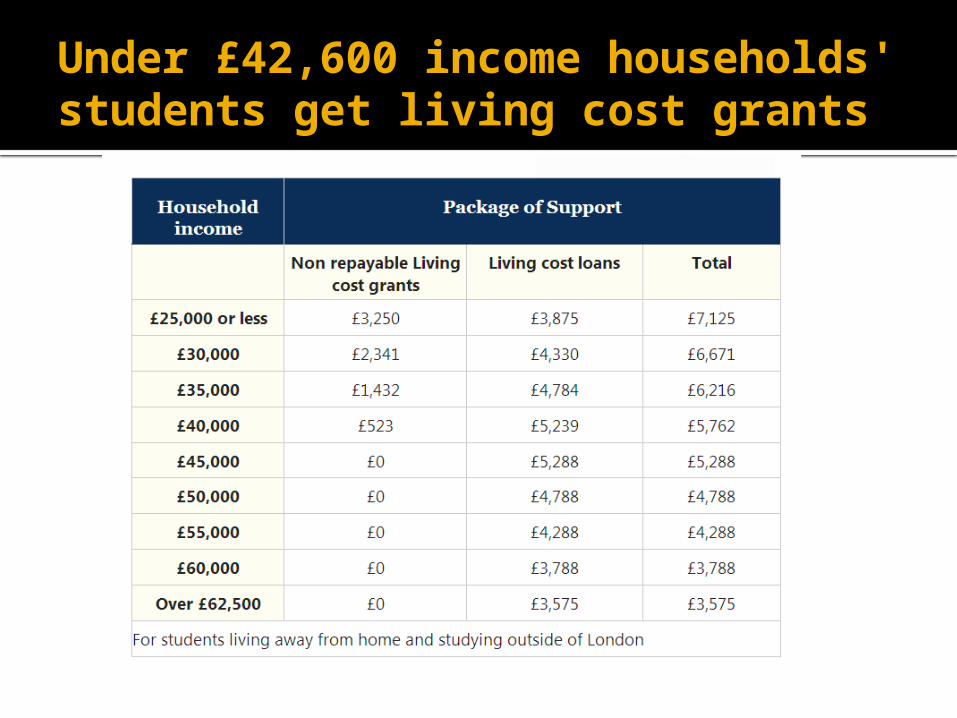

Under £42,600 income households' students get living cost grants

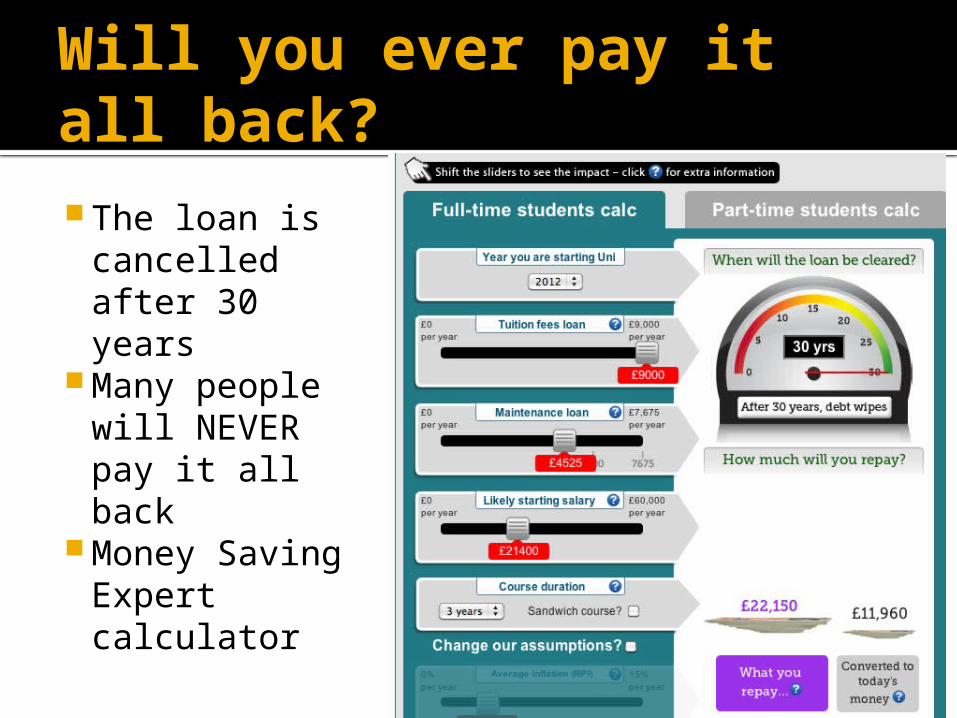

Will you ever pay it all back? The loan is

cancelled after 30 years

Many people will NEVER pay it all back

Money Saving Expert calculator

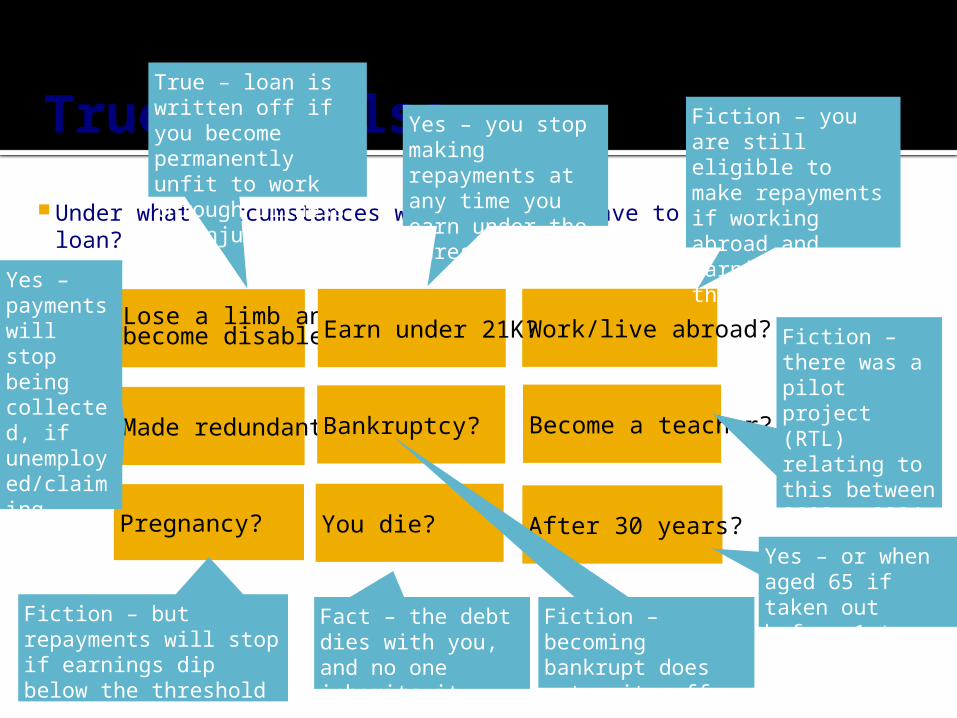

True or False

Under what circumstances would you not have to repay your loan?

Lose a limb and become disabled?

You die?Pregnancy?

Made redundant?Bankruptcy? Become a teacher?

Work/live abroad?Earn under 21K?

After 30 years?

True – loan is written off if you become permanently unfit to work through illness or injury

Yes – you stop making repayments at any time you earn under the threshold

Fiction – you are still eligible to make repayments if working abroad and earning above the threshold

Fiction – there was a pilot project (RTL) relating to this between 2002 – 2004. It is discontinued

Yes – or when aged 65 if taken out before 1st September 2006

Fact – the debt dies with you, and no one inherits it

Fiction – becoming bankrupt does not write off your student loan

Yes – payments will stop being collected, if unemployed/claiming jobseekers allowance

Fiction – but repayments will stop if earnings dip below the threshold if, say, working part-time

Other grants and bursaries will be available

Universities are only allowed to charge fees if they have a system to support poorer students

On top of the official financial support, other funding sources are also available from scholarship sites such as Scholarship-search, Family-action, Turn2us, StudentCashPoint and UniGrants

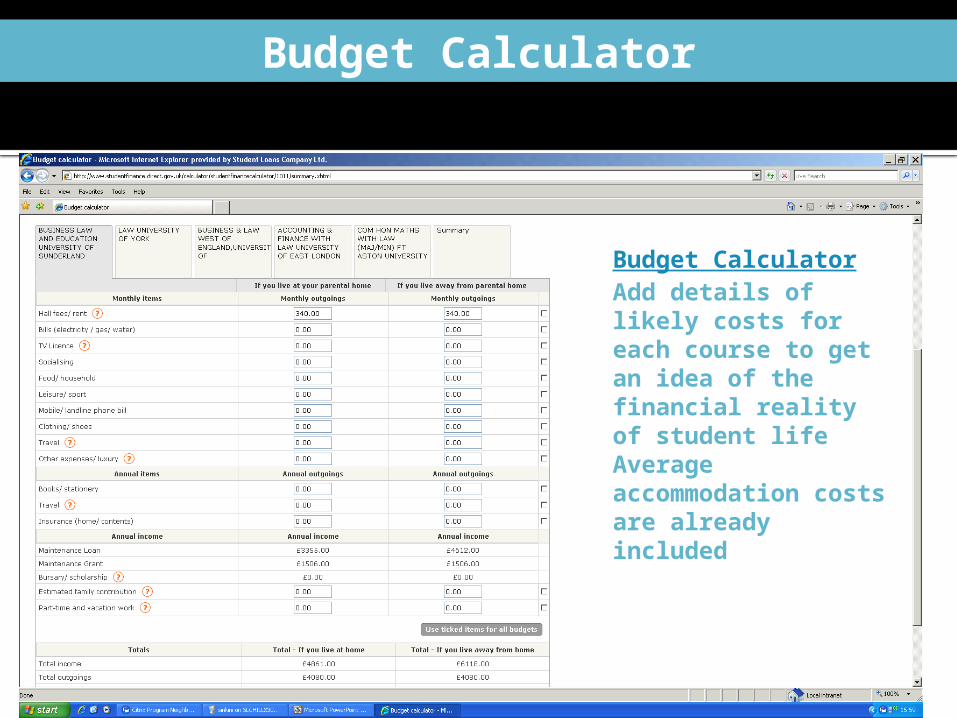

Budget CalculatorAdd details of likely costs for each course to get an idea of the financial reality of student lifeAverage accommodation costs are already included

Budget Calculator

So – is it worth it?

COSTS BENEFITS