Embed Size (px)

Citation preview

6/26/2012

1

IRS Issue Spotting and

Record Keeping Jed Wolcott, CPA

Sue Folkringa, CPA

Wolcott & Associates, PA

NBAA Live Webinar | June 26, 2012

6/26/2012

2

2

Are you a Certified Aviation Manager or

interested in earning points towards your initial application?

Today’s Webinar is eligible for Certified Aviation Manager (CAM)

Initial and Recertification points.

To qualify for credit you must respond to all poll questions.

Live NBAA Webinar| June 26, 2012

6/26/2012

3

Presenters

Sue Folkringa, CPA

Wolcott & Associates, PA

954.763.9363

Jed R. Wolcott, CPA

Wolcott & Associates, PA

954.763.9363

www.aviation-cpa.com

3

Live NBAA Webinar| June 26, 2012

6/26/2012

4

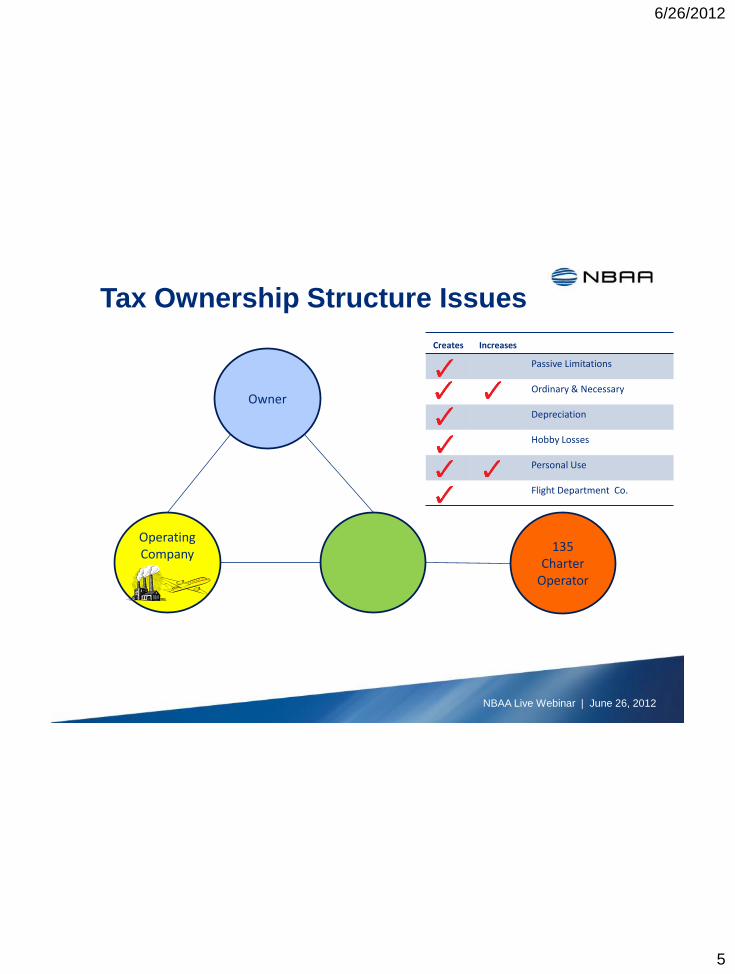

Aircraft Audit Issues

1. Passive Loss Limitations IRC §469

2. Ordinary and Necessary Use IRC §§162, 212

3. Depreciation Issues IRC §§168,167, 280F

4. Hobby Losses IRC §183

5. Personal Use of Company Aircraft IRC §274

6. Flight Department Company & FET IRC §§4261, 4262

7. Audits, Appeals, and Tax Court

8. Documentation required to support

aircraft business use deductions IRC §274(d)(4)

NBAA Live Webinar | June 26, 2012

6/26/2012

5

Creates Increases

Passive Limitations

Ordinary & Necessary

Depreciation

Hobby Losses

Personal Use

Flight Department Co.

Tax Ownership Structure Issues

Owner

Operating Company

135 Charter

Operator

NBAA Live Webinar | June 26, 2012

6/26/2012

6

Poll slide #1

Passive income could result from:

a rental activity, such as renting or leasing your aircraft

inadequate participation in the activity by the owner

can only be offset by passive income

all of the above

6/26/2012

7

Aircraft Audit Issues

Limits on deductions from leasing and activities

where there is insufficient participation by the owner

Passive Loss Limitations

IRC § 469

NBAA Live Webinar | June 26, 2012

6/26/2012

8

Passive Loss Limitations

(PAL) IRC §469

• IRS limits use of losses from:

• Rental activities

• Inadequate participation of owner

• Causes:

• Lease to 135, rental company

• Dry leases

• Aircraft owner does not participate in activity

• PAL activity can be internal or external

• Result: Passive losses can only be used to offset passive income and often can not be used by taxpayer

NBAA Live Webinar | June 26, 2012

6/26/2012

9

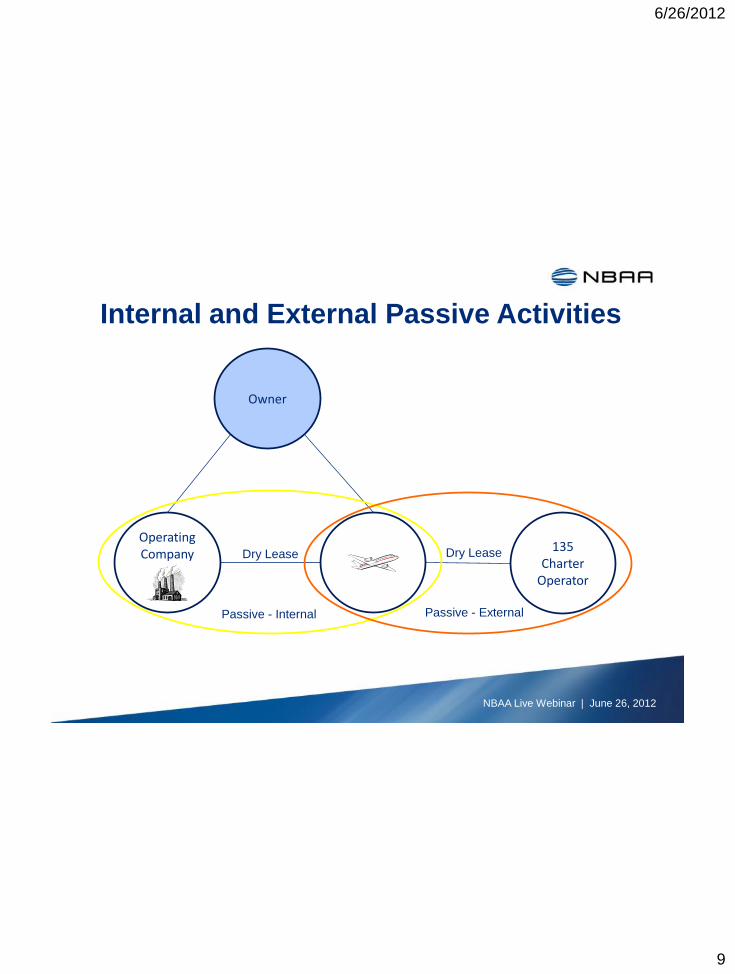

Internal and External Passive Activities

Owner

Operating Company

135 Charter

Operator

Dry Lease Dry Lease

Passive - Internal Passive - External

NBAA Live Webinar | June 26, 2012

6/26/2012

10

PAL Income

• PAL Income includes:

• Rental income

• Income from activities where owner does not have material

participation

• Gain on sale of property used in a passive activity

• Passive income generator (PIG)

• PAL Income does NOT include:

• Operating company income

• Portfolio income (interest, dividends, annuities)

• Income from working interests in oil and gas

• Royalties from self-created intangibles

NBAA Live Webinar | June 26, 2012

6/26/2012

11

PAL Rules, Exceptions,

and Grouping

• There are 6 exceptions to the PAL leasing rules. Treas. Reg. §

1.469-1T(e)(3)(ii)(A)-(F)

• There are 7 “tests” in the PAL material participation rules. Treas.

Reg. §1.469-5T(a)(1)-(7)

• PAL grouping rules provide a defense to the material participation

rules. Treas. Allows time spent in other managing other entities to

count toward the aircraft-owning entity. Reg. § 1.469-4

• Note, as of January 25, 2010, grouping election must be in

writing, filed with each tax return in the group

NBAA Live Webinar | June 26, 2012

6/26/2012

12

Tax Ownership Structure Issues

Owner

Operating Company

135 Charter

Operator

Dry Lease Dry Lease

Economic Entity – Allows

grouping to overcome material

participation concern

NBAA Live Webinar | June 26, 2012

6/26/2012

13

What to do Before the Audit

• Separate active and passive activities to limit passive effects

• Amend returns to include grouping election, restatement of

activities

• Restructure assignment of duties, prepare time logs

• Look for passive income opportunities

• Rental real estate

• Passive income generators (PIG)

• Document taxpayer’s intentions with leases and in corporate

minute books with annual meetings

NBAA Live Webinar | June 26, 2012

6/26/2012

14

Aircraft Audit Issues

IRS rules and regulations that

determine when and if use of an

aircraft is appropriate and deductible

Ordinary and Necessary IRC §§ 162, 212

NBAA Live Webinar | June 26, 2012

6/26/2012

15

Ordinary and Necessary Business Expense - IRC §162

• The IRS ordinary and necessary business expense standard requires that an expense be:

• Appropriate

• Helpful in carrying on the taxpayer’s business

• A common and accepted practice

• Reasonable in amount

• Incidental to the business

• Not “lavish” or “exorbitant”

I.R.C. § 162(a)(2):

NBAA Live Webinar | June 26, 2012

6/26/2012

16

Ordinary and Necessary Business Expense - IRC §162

• Aircraft must be ordinary and necessary to the normal course of

business

• Three hurdles must be overcome:

• Air transportation is a business requirement

• Air transportation need may only be met by private aircraft

• The aircraft is appropriate

for the company’s use

NBAA Live Webinar | June 26, 2012

6/26/2012

17

Ordinary and Necessary Business Expense - IRC §162

• IRS may try to limit deduction because aircraft was inappropriate for

specific travel requirement

• Could limit deduction to first class airfare equivalent

• May substitute reduced hourly operating rate

NBAA Live Webinar | June 26, 2012

6/26/2012

18

What to do Before the Audit

• Analyze company need for private air transportation

• Consider trading if current aircraft is inappropriate for company’s use

• Document business use with corporate minutes approving purchase

and explaining business purpose. Prepare business plan and adopt

in minutes

• Maintain logs tracking business use, non-business use, training

NBAA Live Webinar | June 26, 2012

6/26/2012

19

Aircraft Audit Issues

Rules for when and how much depreciation

can be deducted

Depreciation Issues

IRC §§168, 167, 280F

NBAA Live Webinar | June 26, 2012

6/26/2012

20

Poll Slide #2

True or False:

Generally, for depreciation purposes, Part 91 aircraft are depreciated

over 5 years and Part 135 aircraft are depreciated over 7 years.

NBAA Live Webinar | June 26, 2012

6/26/2012

21

Depreciation Audit Issues:

• Non-compliance with Listed Property rules

• Incorrect application of depreciation rates

• Failure to follow 1031 tax free exchange regulations

• Failure to follow bonus depreciation rules

• If there is leasing to +5% owner(s), business use by other

employees must exceed 25% to qualify for MACRS and

bonus depreciation

NBAA Live Webinar | June 26, 2012

6/26/2012

22

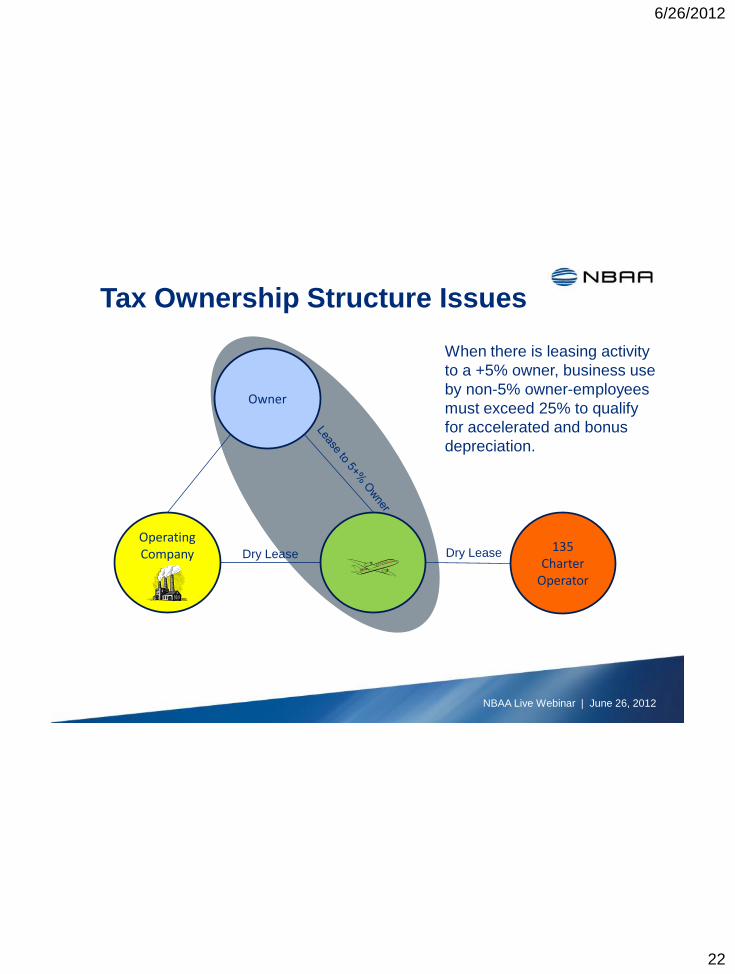

Tax Ownership Structure Issues

Owner

Operating Company

135 Charter

Operator

Dry Lease Dry Lease

When there is leasing activity

to a +5% owner, business use

by non-5% owner-employees

must exceed 25% to qualify

for accelerated and bonus

depreciation.

NBAA Live Webinar | June 26, 2012

6/26/2012

23

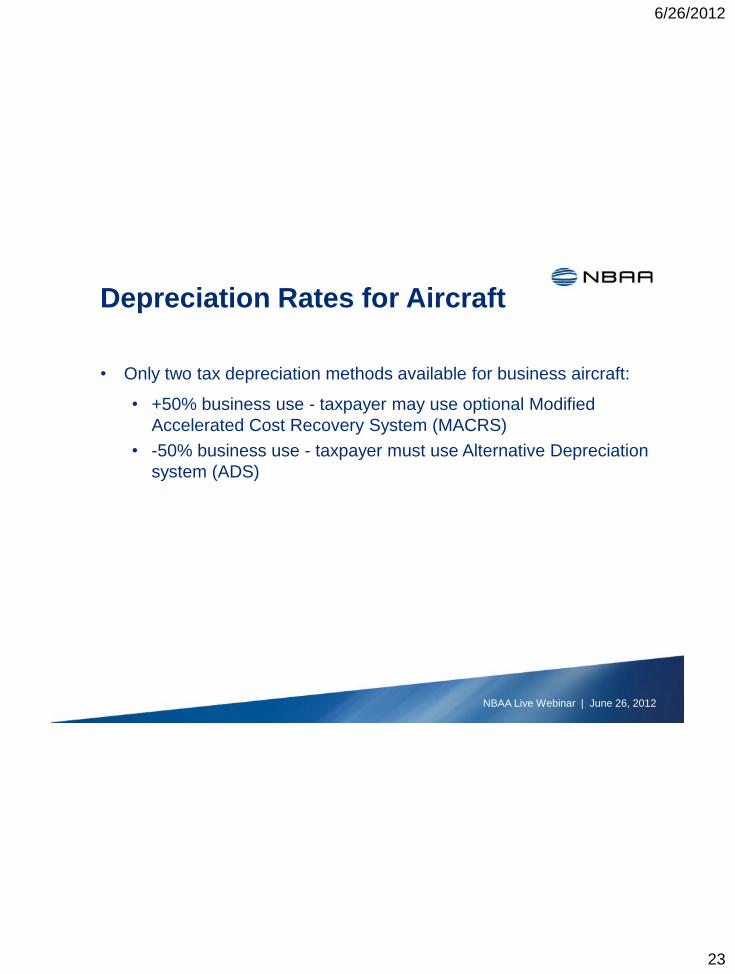

Depreciation Rates for Aircraft

• Only two tax depreciation methods available for business aircraft:

• +50% business use - taxpayer may use optional Modified

Accelerated Cost Recovery System (MACRS)

• -50% business use - taxpayer must use Alternative Depreciation

system (ADS)

NBAA Live Webinar | June 26, 2012

6/26/2012

24

Depreciation Rates for Aircraft –

MACRS

• Modified Accelerated Cost Recovery System (MACRS)

• 5 Year rate for Part-91 aircraft

• 7 Year rate for Part-135 aircraft

• Depreciation rate must reflect predominant use each

year if use is split between Part-91 andPart-135

• BIG GOTCHA: If MACRS is adopted and business use falls

below 50% taxpayer must recapture previous year’s excess

depreciation

NBAA Live Webinar | June 26, 2012

6/26/2012

25

Depreciation Rates for Aircraft –

ADS

• Alternative Depreciation System (ADS) Straight Line Depreciation

• 6 Year rate for Part-91 aircraft

• 12 Year rate for Part-135 aircraft

• Once straight line depreciation is elected, taxpayer cannot change

NBAA Live Webinar | June 26, 2012

6/26/2012

26

Bonus Depreciation Issues

• Typical bonus depreciation audit issues:

• Not meeting contract requirements

• Not meeting deposit requirements

• Incorrect application of 1st year business-use requirements

• Purchasing existing contracts

• Failure to meet +50% business use in all subsequent years

• If you claim bonus depreciation, EXPECT TO BE AUDITED

NBAA Live Webinar | June 26, 2012

6/26/2012

27

Poll slide #3

Does the use of the aircraft in the acquisition year have a bearing on

the amount which could be deducted for bonus depreciation?

Yes/No

6/26/2012

28

1031 Tax-Free Exchange

Regulations IRC §1031

• Rules for “Forward” and “Reverse” exchanges are complex

• Planning must take place prior to signing any documents;

1031’s transactions cannot be done “after the fact”

• Completing the transactions within the specified deadlines is crucial

• Failure to meet stat deadlines will cause gain on the relinquished

aircraft to be recognized in the year of sale

• Suggestion: Use exchange company

NBAA Live Webinar | June 26, 2012

6/26/2012

29

Single-Purpose Companies

Have High Audit Exposure

• SPC’s are companies formed to only own an aircraft

• Often used to shelter from potential liability, lease aircraft back to

owner

• Typically S-Corps and multi-member LLC’s

• Cash in equals cash out

• Depreciation expense remains, very prominent

• Very high audit selection rate

NBAA Live Webinar | June 26, 2012

6/26/2012

30

What to do Before the Audit

• Consider restructuring SPC

ownership to limit audit exposure

• Review 91 vs. 135 use to see if rate is

appropriate;

• if bonus or accelerated depreciation is

claimed, be sure that business use

exceeds 50%

• If leasing, review use by 5% owners;

amend if necessary

• Consider the “visibility” of bonus

depreciation; be sure documentation

is adequate

NBAA Live Webinar | June 26, 2012

6/26/2012

31

Aircraft Audit Issues

IRS rules for companies considered

not in business to make a profit

Hobby Losses IRC §183

NBAA Live Webinar | June 26, 2012

6/26/2012

32

Poll Slide #4

The IRS presumes an activity is not a hobby if income is earned in

1 of 10 years

2 of 3 years

3 of 5 years

Aircraft are never considered to be hobbies

NBAA Live Webinar | June 26, 2012

6/26/2012

33

Hobby Loss Rules – IRC §183

• Restricts use of losses against other taxable income if activity is not

“for profit”

• IRS presumes activity is not a hobby if company has profits in 3 out

of 5 years

• If not 3 profitable years, IRS applies facts and circumstances test

• Hobby Loss Rules are dangerous because they allow IRS to

disallow all operating costs, ownership costs, and depreciation.

Can be big win for IRS

NBAA Live Webinar | June 26, 2012

6/26/2012

34

Hobby Loss Rules

• IRS often cites Hobby Loss rules when aircraft is owned by a

single-purpose company (SPC)

• Includes S-corps, multi-member LLC’s, and Schedule C’s

for individually-owned aircraft

• Cash in often equals cash out, meaning no profit from day-

to-day operations

• SPC’s often have consistent loss years due to depreciation

NBAA Live Webinar | June 26, 2012

6/26/2012

35

Single Purpose Companies –

Audit Targets

Owner

Operating Company

135 Charter

Operator

Example of Single-Purpose Company

SPC

Reports Losses

Files Tax Return

NBAA Live Webinar | June 26, 2012

6/26/2012

36

Hobby Loss Rules

Treas. Reg. §1.183-2(b)

IRS regulations provide a list of nine factors to test if an activity is

for profit, such as

1. Manner in which taxpayer carries on the activity

2. Expertise of the taxpayer or advisors

3. Time and effort expended

4. Expectation of future profits

5. Expectation that assets will appreciate in value

IRS also permits grouping of “hobby” activity with other profitable

activity Treas. Reg. § 1.469-4(d)

NBAA Live Webinar | June 26, 2012

6/26/2012

37

What to do Before the Audit

• Change ownership structure to place aircraft in a profitable operating company, or

• In analyzing profitability, depreciation can be ignored

• Change ownership to make company a disregarded SM-LLC

• Amend returns to include grouping election

• Create business plan, record

• in Corporate Minute Book

• Document, document, document

NBAA Live Webinar | June 26, 2012

6/26/2012

38

Aircraft Audit Issues

Rules for reporting the non-business use of company

aircraft

Personal Use of Company Aircraft

IRC § 274, Reg. § 1.61-21

NBAA Live Webinar | June 26, 2012

6/26/2012

39

Personal Use of

Company Aircraft

• For aircraft owned by a Corporation, S-Corp or Partnership and

provided with pilot(s):

• Employees must report SIFL1 taxable income for non-business

flights

• Separate rates for “control” and “non-control” employees

• Cash reimbursements may satisfy this requirement

• Company must apply cost limitation rules for entertainment

flights by “specified individuals” and guests

1Standard Industry Fare Level rates published by DOT

NBAA Live Webinar | June 26 , 2012

6/26/2012

40

Personal Use of

Company Aircraft

• For individual-owned aircraft, including aircraft in a single-member

LLC owned by an individual:

• Apply primary purpose test, similar to how individual-owned

autos are reported

• Deduct pro-rata portion of direct costs, ownership costs and

depreciation for non-business flight use

• No distinction between non-business and entertainment

flights; use is either business or non-business

NBAA Live Webinar | June 26, 2012

6/26/2012

41

Personal Use Of Company

Aircraft – Defenses (continued)

• Entertainment Cost Limitations

• No “safe harbor” rules

• Follow Notice 2005-45

• Follow proposed Reg. 1.274-10

• No cases yet (legislation is too recent)

NBAA Live Webinar | June 26, 2012

6/26/2012

42

What to do Before the Audit

• Personal Use of Company Aircraft:

• If SIFL has been overlooked, amend employee personal

tax returns to include SIFL

• If entertainment disallowance has been overlooked,

amend company returns to recognize the entertainment

cost disallowance rules for aircraft-owning entity

• Amend returns for unapplied non-business use deduction

for individually-owned and flown aircraft

• Document business flights; make sure flight logs support

business and non-business use

NBAA Live Webinar | June 26, 2012

6/26/2012

43

Aircraft Audit Issues

Flight Department Company

IRC §§4261, 4262

NBAA Live Webinar | June 26, 2012

6/26/2012

44

Flight Department

Company Issue – IRC § 4261

• Entity only owns and operates the aircraft

• Pays DOC’s including pilots

• Only purpose is to provide air transportation

• Commercial says IRS!!!! – Excise tax owed:

• 7.5% of all costs, plus

• $3.80 per passenger (2012)

• 6.25% for freight

• See Notice 2005-62 for IRS examples

NBAA Live Webinar | June 26, 2012

6/26/2012

45

Typical Flight Department

Company Structure

Owner

Operating Company

Wet Lease

Pilot (paid by aircraft

company)

IRS says: “You are

providing air transportation services. FET

applies”

Owner says: “I’m simply

providing my company with an aircraft”

NBAA Live Webinar | June 26, 2012

6/26/2012

46

Flight Depart. Co. –

How to Restructure – Pros and Cons

• Convert “wet lease” to “dry lease”

• Create separate management company to employ pilots?

• OK, providing the lessee pays the pilots

• Note potential problem: This strategy could convert activity to passive

• Key issue – who controls the pilot?

• Caution: It is too late to restructure after the audit has commenced

NBAA Live Webinar | June 26, 2012

6/26/2012

47

Affiliated Group Exemption

as a Flight Dept. Company Audit Defense

– IRC 4282

• Allows large company with many subsidiaries to form an “aircraft operations” entity to operate the company aircraft without incurring FET liability

• Must be a common parent owning at least 80% of each includable subsidiary

• Certain entities are not includable, including S-corporations (IRC Sec. 1504)

• Exemption does not apply to flights provided to third parties outside of the affiliated group

NBAA Live Webinar | June 26, 2012

6/26/2012

48

Poll slide #5

If an operating company owns an aircraft, pays the pilots and

provides transportation to its employees, will there be an FET

liability?

Yes or No

6/26/2012

49

What to do Before the Audit

• Convert wet leases to dry leases (can be as simple as

changing which checkbook is used)

• Have written leases making clear who pays the pilots

• Hire a management company to provide pilots

• A company may create their own crew management

company; it only has to be an entity separate from the

aircraft-owning company

• If claiming affiliated group exemption, be sure all

entities using the aircraft qualify

NBAA Live Webinar | June 26, 2012

6/26/2012

50

The Audit Process

NBAA Live Webinar | June 26, 2012

6/26/2012

51

IRS Audits: A Three-Step Process

Audit (sometimes called the field audit).

Auditor is on-site examining book and records

Should be handled by qualified company personnel

Best done away from the company offices

IRS Appeals.

Conducted by specially-trained senior IRS agents

Requires written protest listing all the taxpayer arguments

U.S. Tax Court

Requires qualified representation

Each step progressively takes longer, and is more costly to defend

NBAA Live Webinar | June 26, 2012

6/26/2012

52

Every Issue Won at Field Audit

Level is a Victory!

• Consider the field auditor the “Traffic Cop”

• Easier to argue a ticket on the street than in Traffic Court

• Any issue eliminated at the audit level is gone

THE FIELD EXAMINATION IS THE MOST

CRUCIAL PORTION OF THE AUDIT

NBAA Live Webinar | June 26, 2012

6/26/2012

53

During the Field Audit:

EVERYTHING IS NEGOTIABLE

If you can’t settle the case at the audit level, then someone is being unreasonable

NBAA Live Webinar | June 26, 2012

6/26/2012

54

Supervisor Negotiations

• Negotiations become more difficult as the audit progresses

• Taxpayer can always request a supervisor meeting

• Supervisor is obligated to attend final meeting if taxpayer

requests

• Strategy: Probably nothing to lose to demand meeting

• Make auditor and supervisor aware by your actions that you are

prepared to take the case to court if a settlement can’t be reached

at Appeals

• Always request that supervisor abate penalties

NBAA Live Webinar | June 26, 2012

6/26/2012

55

30-Day Letter

• Notifies taxpayer of right to appeal to proposed adjustments within

30 days

• Package will include a copy of auditor’s examination report and

Notice of Proposed Adjustments

• For individual - Form 4549-E and Letter 3605-A

• For corporation or partnership - Letter 1085

• If Taxpayer intends to take case to Appeals, IRS rules permit 30

days to file Protest Letter

• Note that the 30-day period is strictly enforced

NBAA Live Webinar | June 26, 2012

6/26/2012

56

90-Day Letter

• If taxpayer does not respond to 30-day letter, IRS sends 90-day

letter

• Also known as Statutory Notice of Deficiency

• Gives taxpayer 90 days (150 days if out of country) to file a petition

with Tax Court

• If taxpayer still does not respond, the case is closed, and the Notice

of Deficiency is sent to Collections

Note that the 90-day period is strictly enforced

NBAA Live Webinar | June 26, 2012

6/26/2012

57

Documentation

IRS Regulations for Documenting the Use of

Business Aircraft IRC § 274(d)(4)

Documentation to keep in the event of an audit.

NBAA Live Webinar | June 26, 2012

6/26/2012

58

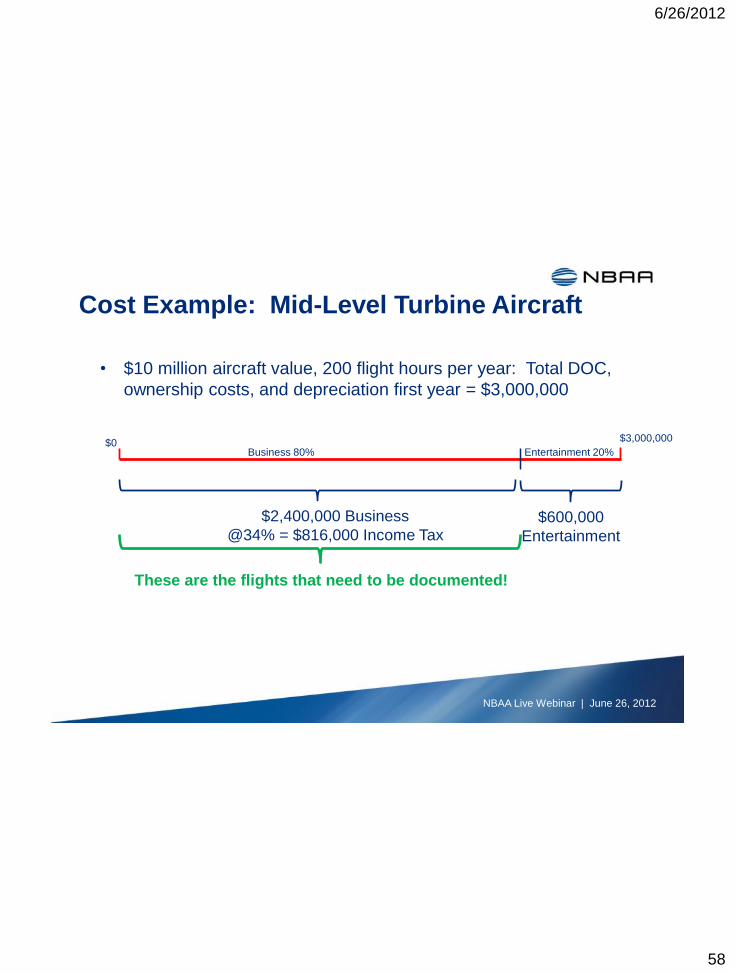

Cost Example: Mid-Level Turbine Aircraft

• $10 million aircraft value, 200 flight hours per year: Total DOC,

ownership costs, and depreciation first year = $3,000,000

Business 80% Entertainment 20% $0 $3,000,000

$2,400,000 Business

@34% = $816,000 Income Tax $600,000

Entertainment

These are the flights that need to be documented!

NBAA Live Webinar | June 26, 2012

6/26/2012

59

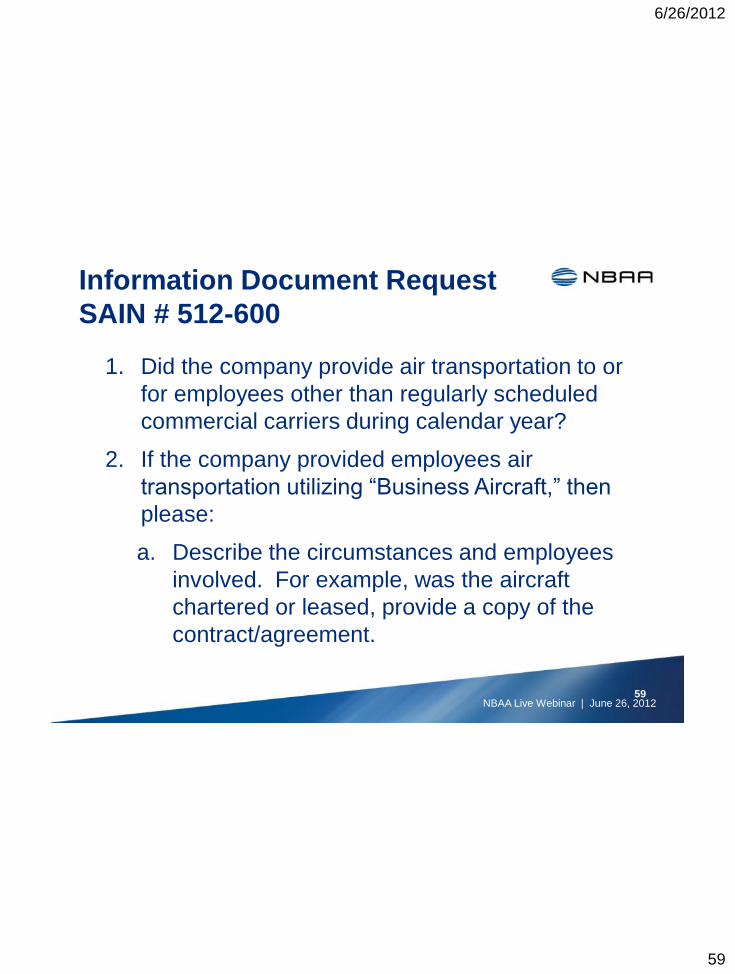

Information Document Request

SAIN # 512-600

1. Did the company provide air transportation to or

for employees other than regularly scheduled

commercial carriers during calendar year?

2. If the company provided employees air

transportation utilizing “Business Aircraft,” then

please:

a. Describe the circumstances and employees

involved. For example, was the aircraft

chartered or leased, provide a copy of the

contract/agreement.

59 NBAA Live Webinar | June 26, 2012

6/26/2012

60

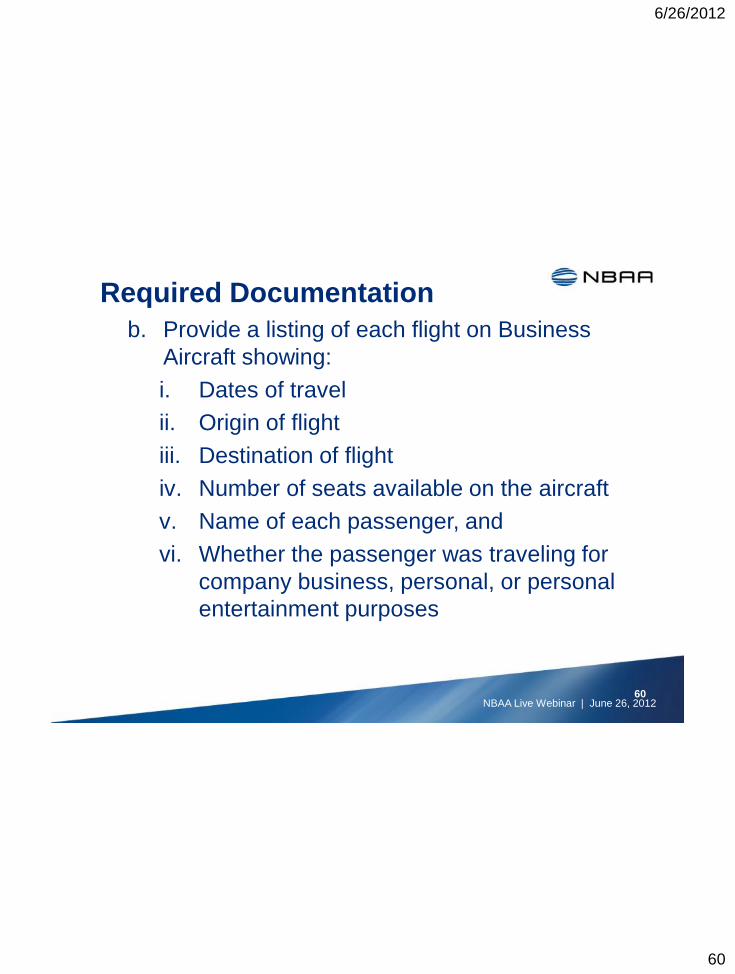

Required Documentation

b. Provide a listing of each flight on Business

Aircraft showing:

i. Dates of travel

ii. Origin of flight

iii. Destination of flight

iv. Number of seats available on the aircraft

v. Name of each passenger, and

vi. Whether the passenger was traveling for

company business, personal, or personal

entertainment purposes

60 NBAA Live Webinar | June 26, 2012

6/26/2012

61

Required Documentation

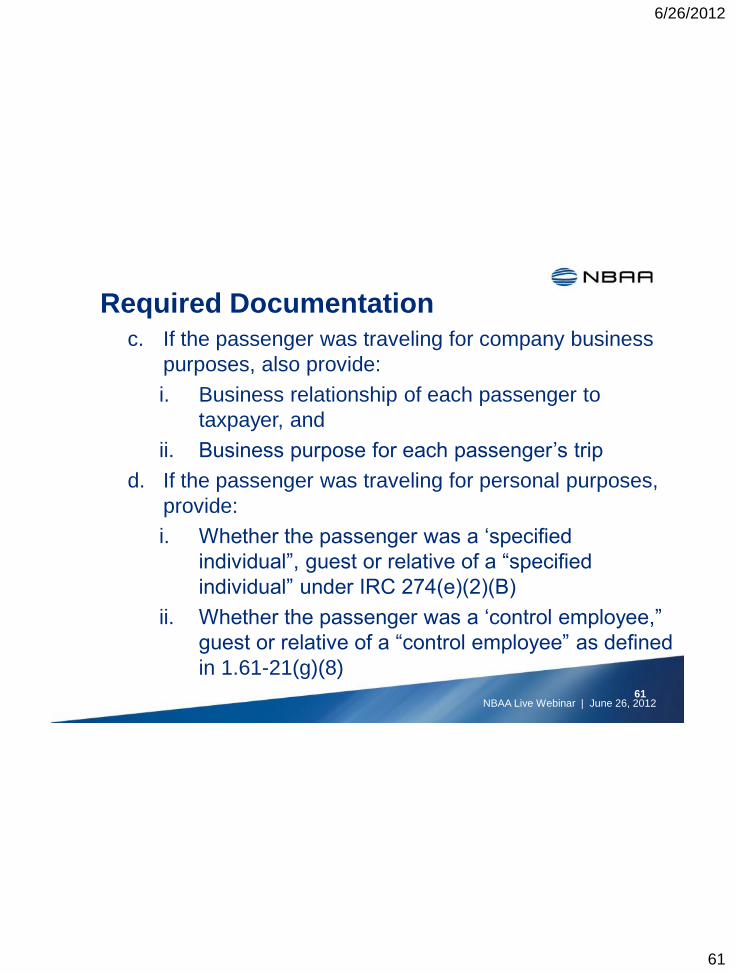

c. If the passenger was traveling for company business

purposes, also provide:

i. Business relationship of each passenger to

taxpayer, and

ii. Business purpose for each passenger’s trip

d. If the passenger was traveling for personal purposes,

provide:

i. Whether the passenger was a ‘specified

individual”, guest or relative of a “specified

individual” under IRC 274(e)(2)(B)

ii. Whether the passenger was a ‘control employee,”

guest or relative of a “control employee” as defined

in 1.61-21(g)(8)

61 NBAA Live Webinar | June 26, 2012

6/26/2012

62

Required Documentation

3. Provide all computations made under IRC 274(e),

Notice 2005-45 or proposed regulations to the

amount deductible under IRC 274(e)(2) or (9) for

personal entertainment aircraft expenses incurred

for “specified individuals”. Information must

reflect:

a. Type of Aircraft expense (fuel, interest,

depreciation, flight crews, etc.) considered in

the IRC 274(e) calculation, and

b. Flight by Flight computations

62 NBAA Live Webinar | June 26, 2012

6/26/2012

63

Required Documentation

4. Provide detailed “Fair Market Value” or “Standard

Industry Fare Level (SIFL)” computation where the

taxpayer has calculated taxable compensation of

wages for Personal Use of Business Aircraft for

employees or independent contractors

63 NBAA Live Webinar | June 26, 2012

6/26/2012

64

Required Documentation

4. (Cont’d) Additionally, provide the related Form W-2

or Form 1099 along with a computation showing

how much of the compensation on the Form is

related to personal use of aircraft

64 NBAA Live Webinar | June 26, 2012

6/26/2012

65

Required Documentation

5. Provide copies of:

a. The maintenance logs for all company aircraft

b. The aircraft logs or pilot logs for the aircraft

utilized by the company

65 NBAA Live Webinar | June 26, 2012

6/26/2012

66

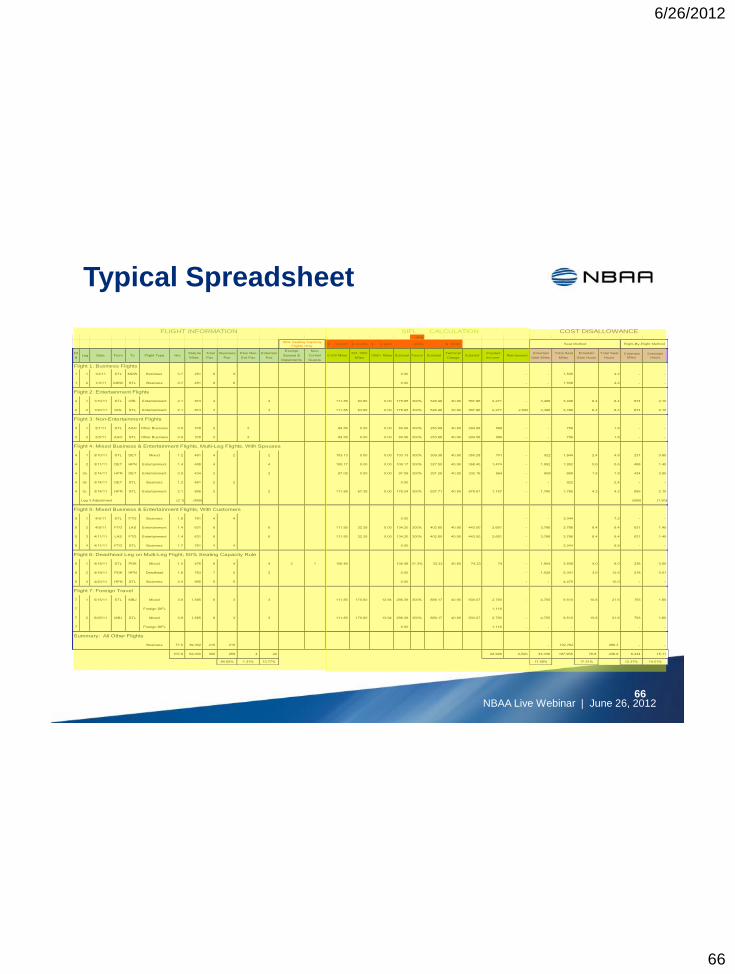

Typical Spreadsheet

31%

0.2237$ 0.1706$ 0.1640$ 300% 40.90$

Flt

# Leg Date From To Flight Type Hrs

Statute

Miles

Total

Pax

Business

Pax

Pers Non-

Ent Pax

Entertain

Pax

Exempt

Spouse &

Dependents

Non-

Control

Guests

0-500 Miles501-1500

Miles1500+ Miles Subtotal Factor Subtotal

Terminal

ChargeSubtotal

Imputed

Income Reimbursed

Entertain

Seat Miles

Total Seat

Miles

Entertain

Seat Hours

Total Seat

Hours

Entertain

Miles

Entertain

Hours

Flight 1: Business Flights

1 1 1/2/11 STL MDW Business 0.7 251 6 6 0.00 - - 1,506 4.2 - -

1 2 1/3/11 MDW STL Business 0.7 251 6 6 0.00 - - 1,506 4.2 - -

Flight 2: Entertainment Flights

2 1 1/10/11 STL ORL Entertainment 2.1 874 4 4 111.85 63.80 0.00 175.65 300% 526.96 40.90 567.86 2,271 - 3,496 3,496 8.4 8.4 874 2.10

2 2 1/20/11 ORL STL Entertainment 2.1 874 4 4 111.85 63.80 0.00 175.65 300% 526.96 40.90 567.86 2,271 2,520 3,496 3,496 8.4 8.4 874 2.10

Flight 3: Non-Entertainment Flights

3 1 2/1/11 STL AAO Other Business 0.9 378 2 2 84.56 0.00 0.00 84.56 300% 253.68 40.90 294.58 589 - - 756 1.8 - -

3 2 2/5/11 AAO STL Other Business 0.9 378 2 2 84.56 0.00 0.00 84.56 300% 253.68 40.90 294.58 589 - - 756 1.8 - -

Flight 4: Mixed Business & Entertainment Flights, Multi-Leg Flights, With Spouses

4 1 3/10/11 STL DET Mixed 1.2 461 4 2 2 103.13 0.00 0.00 103.13 300% 309.38 40.90 350.28 701 - 922 1,844 2.4 4.8 231 0.60

4 2 3/11/11 DET HPN Entertainment 1.4 488 4 4 109.17 0.00 0.00 109.17 300% 327.50 40.90 368.40 1,474 - 1,952 1,952 5.6 5.6 488 1.40

4 3a 3/14/11 HPN DET Entertainment 0.9 434 2 2 97.09 0.00 0.00 97.09 300% 291.26 40.90 332.16 664 - 868 868 1.8 1.8 434 0.90

4 3b 3/14/11 DET STL Business 1.2 461 2 2 0.00 - - 922 2.4 - -

4 3c 3/14/11 HPN STL Entertainment 2.1 895 2 2 111.85 67.39 0.00 179.24 300% 537.71 40.90 578.61 1,157 - 1,790 1,790 4.2 4.2 895 2.10

Leg 3 Adjustment (2.1) (895) (665) (1.50)

Flight 5: Mixed Business & Entertainment Flights; With Customers

5 1 4/5/11 STL FTG Business 1.8 761 4 4 0.00 - - 3,044 7.2 - -

5 2 4/8/11 FTG LAS Entertainment 1.4 631 6 6 111.85 22.35 0.00 134.20 300% 402.60 40.90 443.50 2,661 - 3,786 3,786 8.4 8.4 631 1.40

5 3 4/11/11 LAS FTG Entertainment 1.4 631 6 6 111.85 22.35 0.00 134.20 300% 402.60 40.90 443.50 2,661 - 3,786 3,786 8.4 8.4 631 1.40

5 4 4/11/11 FTG STL Business 1.7 761 4 4 0.00 - - 3,044 6.8 - -

Flight 6: Deadhead Leg on Multi-Leg Flight; 50% Seating Capacity Rule

6 1 4/18/11 STL PDK Mixed 1.0 476 8 4 4 3 1 106.48 106.48 31.3% 33.33 40.90 74.23 74 - 1,904 3,808 4.0 8.0 238 0.50

6 2 4/19/11 PDK HPN Deadhead 1.8 763 7 5 2 0.00 - 1,526 5,341 3.6 12.6 218 0.51

6 3 4/20/11 HPN STL Business 2.0 895 5 5 0.00 - - 4,475 10.0 - -

Flight 7: Foreign Travel

7 1 5/15/11 STL MBJ Mixed 3.6 1,585 6 3 3 111.85 170.60 13.94 296.39 300% 889.17 40.90 930.07 2,790 - 4,755 9,510 10.8 21.6 793 1.80

7 Foreign SIFL 1,116

7 2 5/25/11 MBJ STL Mixed 3.6 1,585 6 3 3 111.85 170.60 13.94 296.39 300% 889.17 40.90 930.07 2,790 - 4,755 9,510 10.8 21.6 793 1.80

7 Foreign SIFL 0.00 1,116 - - - - -

Summary: All Other Flights

Business 77.5 39,062 215 215 - 122,762 286.4 - -

107.9 52,000 305 259 4 42 22,926 2,520 33,036 187,958 76.8 438.6 6,434 15.11

84.92% 1.31% 13.77% 17.58% 17.51% 12.37% 14.01%

FLIGHT INFORMATION SIFL CALCULATION COST DISALLOWANCE

50% Seating Capacity

Flights Only Seat Method Flight-By-Flight Method

66 NBAA Live Webinar | June 26, 2012

6/26/2012

67

Typical Spreadsheet

What the typical spreadsheet often does not include:

a. Names of passengers

b. Relationship to taxpayer

i. Identifying control employees & guests

(aggregate only)

ii. Specified individuals & guests (aggregate)

c. Purpose of each passenger on the flight

d. Computations involving aircraft operating costs,

ownership costs, and depreciation

67 NBAA Live Webinar | June 26, 2012

6/26/2012

68

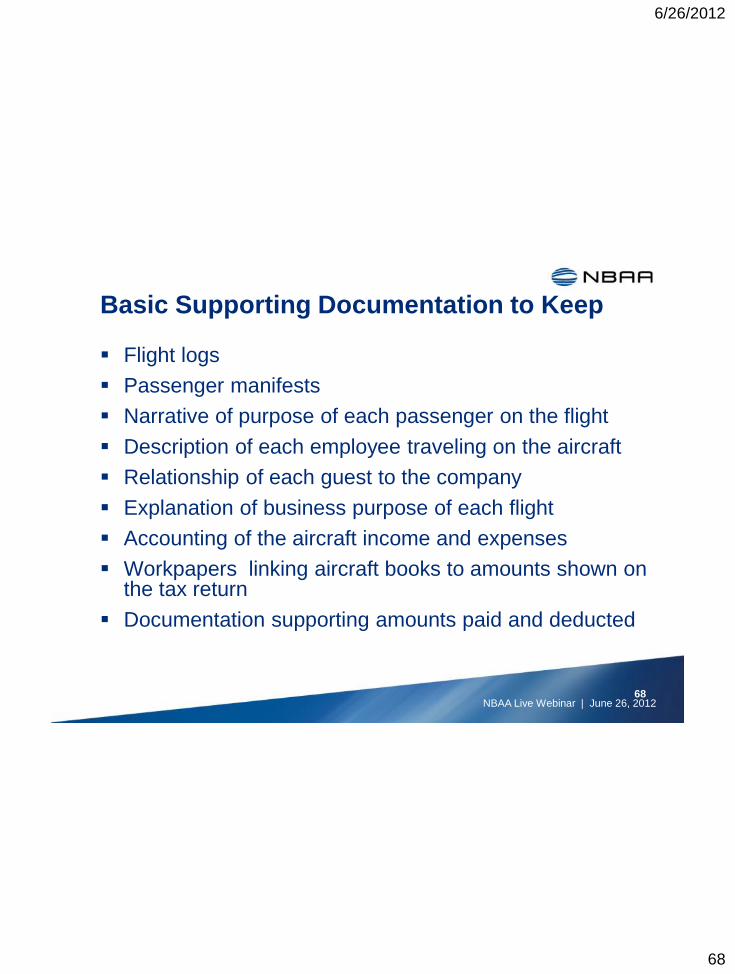

Basic Supporting Documentation to Keep

Flight logs

Passenger manifests

Narrative of purpose of each passenger on the flight

Description of each employee traveling on the aircraft

Relationship of each guest to the company

Explanation of business purpose of each flight

Accounting of the aircraft income and expenses

Workpapers linking aircraft books to amounts shown on the tax return

Documentation supporting amounts paid and deducted

68 NBAA Live Webinar | June 26, 2012

6/26/2012

69

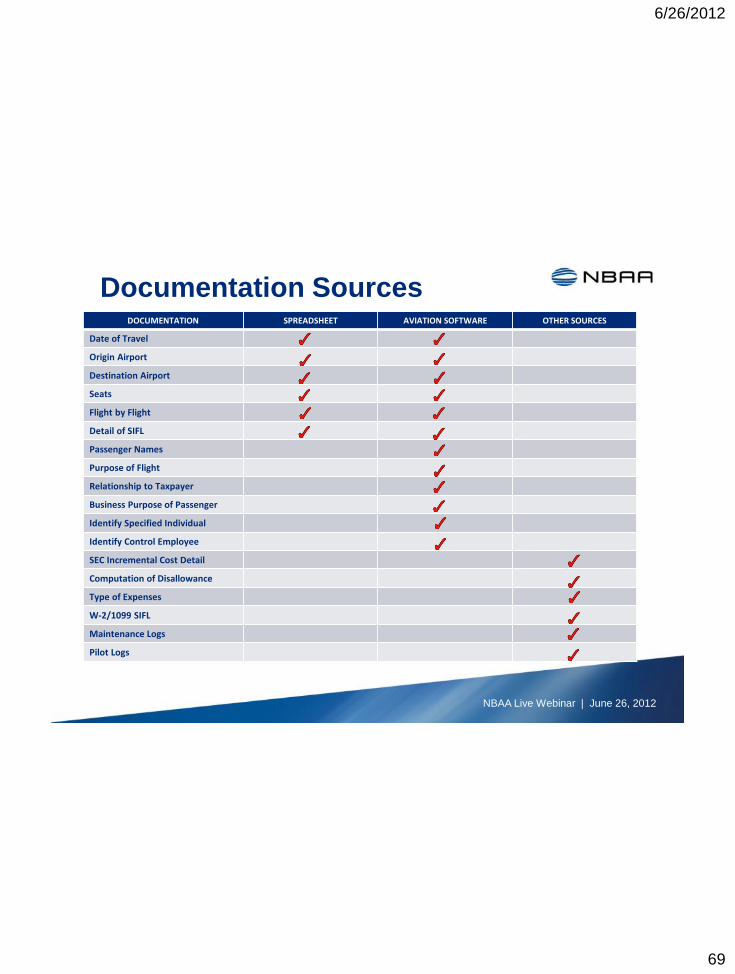

DOCUMENTATION SPREADSHEET AVIATION SOFTWARE OTHER SOURCES

Date of Travel

Origin Airport

Destination Airport

Seats

Flight by Flight

Detail of SIFL

Passenger Names

Purpose of Flight

Relationship to Taxpayer

Business Purpose of Passenger

Identify Specified Individual

Identify Control Employee

SEC Incremental Cost Detail

Computation of Disallowance

Type of Expenses

W-2/1099 SIFL

Maintenance Logs

Pilot Logs

Documentation Sources

NBAA Live Webinar | June 26, 2012

6/26/2012

70

Documentation

IRS requires tax documentation be

contemporaneous

Document the business flights, because those are

the ones you want to keep

Spreadsheets typically used for tax returns;

insufficient for documenting business use

IRS agent will often disallow all flights, then add

back business flights one-by-one

Keep records for 5 years

70 NBAA Live Webinar | June 26, 2012

6/26/2012

71

Questions for Today’s Presenters?

Sue Folkringa, CPA

Wolcott & Associates, PA

954.763.9363

Jed R. Wolcott, CPA

Wolcott & Associates, PA

954.763.9363

www.aviation-cpa.com

71

Live NBAA Webinar| June 26, 2012