Embed Size (px)

Citation preview

Analyst Meeting

2011 Performance

23 February 2012

IRPC Public Company Limited

2

2011 Highlights

Operation Performance

Financial Performance

Industry Outlooks

Project Progress & Future

Appendix

AGENDA

2011 Highlights

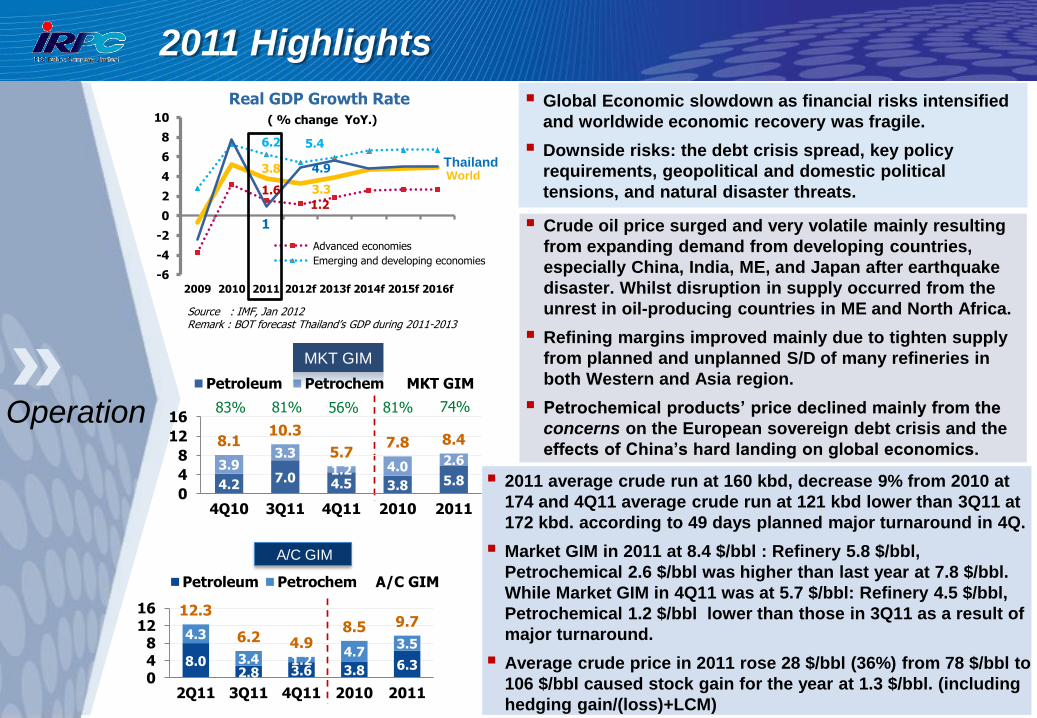

Global Economic slowdown as financial risks intensified

and worldwide economic recovery was fragile.

Downside risks: the debt crisis spread, key policy

requirements, geopolitical and domestic political

tensions, and natural disaster threats.

Crude oil price surged and very volatile mainly resulting

from expanding demand from developing countries,

especially China, India, ME, and Japan after earthquake

disaster. Whilst disruption in supply occurred from the

unrest in oil-producing countries in ME and North Africa.

Refining margins improved mainly due to tighten supply

from planned and unplanned S/D of many refineries in

both Western and Asia region.

Petrochemical products’ price declined mainly from the

concerns on the European sovereign debt crisis and the

effects of China’s hard landing on global economics.

3.8

3.3 1.6

1.2

6.2 5.4

1

4.9

-6

-4

-2

0

2

4

6

8

10

2009 2010 2011 2012f 2013f 2014f 2015f 2016f

Advanced economies

Emerging and developing economies

Real GDP Growth Rate

( % change YoY.)

World Thailand

Source : IMF, Jan 2012 Remark : BOT forecast Thailand’s GDP during 2011-2013

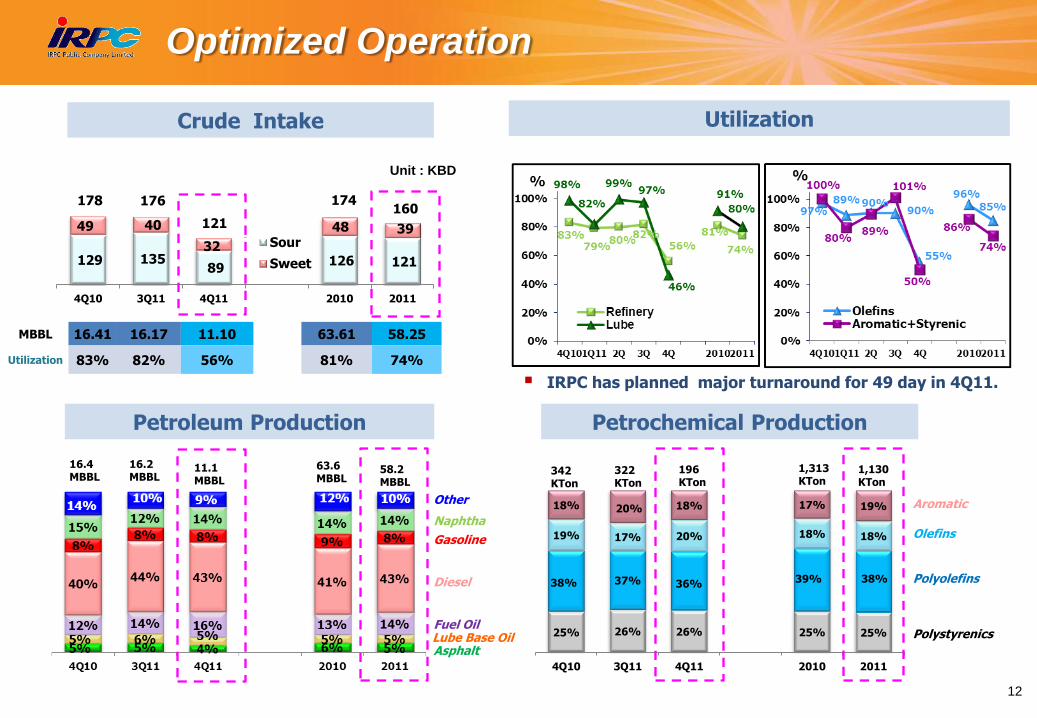

2011 average crude run at 160 kbd, decrease 9% from 2010 at

174 and 4Q11 average crude run at 121 kbd lower than 3Q11 at

172 kbd. according to 49 days planned major turnaround in 4Q.

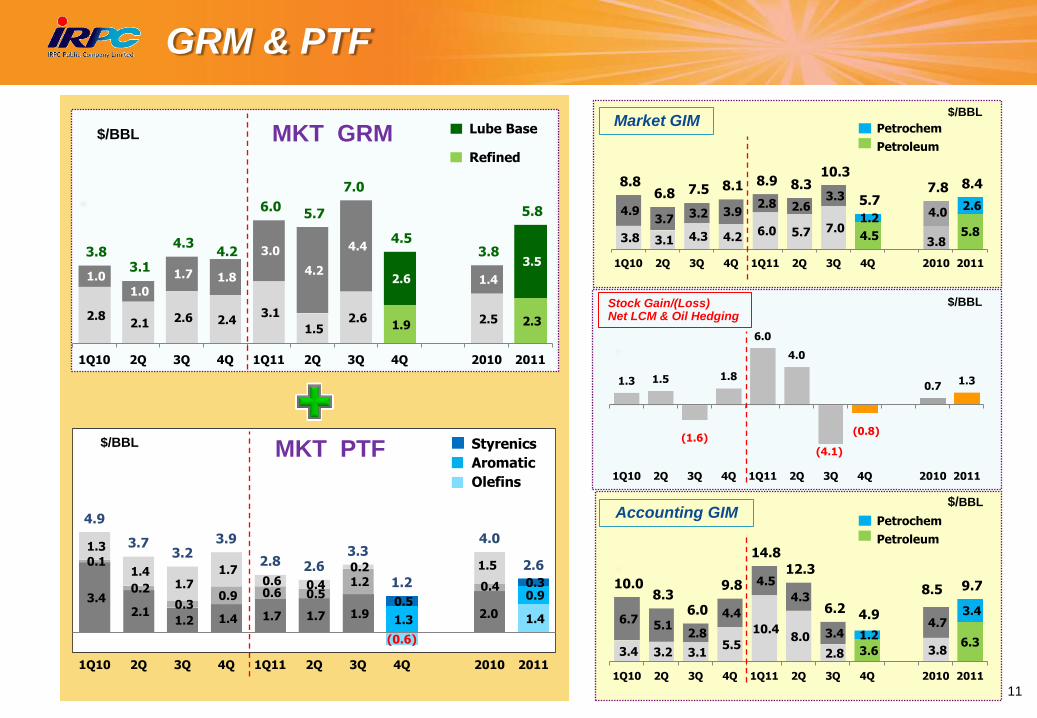

Market GIM in 2011 at 8.4 $/bbl : Refinery 5.8 $/bbl,

Petrochemical 2.6 $/bbl was higher than last year at 7.8 $/bbl.

While Market GIM in 4Q11 was at 5.7 $/bbl: Refinery 4.5 $/bbl,

Petrochemical 1.2 $/bbl lower than those in 3Q11 as a result of

major turnaround.

Average crude price in 2011 rose 28 $/bbl (36%) from 78 $/bbl to

106 $/bbl caused stock gain for the year at 1.3 $/bbl. (including

hedging gain/(loss)+LCM)

8.0 2.8 3.6 3.8 6.3

4.3

3.4 1.2 4.7

3.5

12.3

6.2 4.9 8.5 9.7

048

1216

2Q11 3Q11 4Q11 2010 2011

Petroleum Petrochem A/C GIM

A/C GIM

Operation

4.2 7.0 4.5 3.8 5.8

3.9 3.3

1.2 4.0 2.6

8.1 10.3

5.7 7.8 8.4

0

4

8

12

16

4Q10 3Q11 4Q11 2010 2011

Petroleum Petrochem MKT GIM

83% 81% 56%

MKT GIM

81% 74%

Successfully Launched “Polimaxx Green ABS” to Europe

and South America and join with Hatari in the production

of Hatari’s fans.

Achieved two awards in “Thailand ICT Excellence Awards 2010”

GIM for Core Process Improvement Project

iDEAL, iRON for Business Enabler Project and iPORT.

Developed Wood Plastic Composite for enhancing plastic properties: resistant,

toughness and environmental friendly.

Successful development of catalyst for HDPE Production in internal PTT Group

2011 Highlights (Con’t)

4

Operation

Innovation

Finance “IRPC Global Export Insured”, co-operate with Kbank to reduce financial

risk and increase capability to compete with global competitors.

IRPC announced to pay dividend of the year at 0.12 Bath/share accounted for 60%

payout. The interim dividend of 0.08 Baht/share already paid on 30 September 2011.

Successful CHP Project since 1 June 2011 with saving

benefit of 3-5 MB/day .

Overall Phoenix progress averaged at 15.5%, the benefit

of this year reached 2,152 MB, of which 85% mainly

came from Petrochemical and Petroleum Operation and

Energy efficiency.

TDAE

HDPE Pipe grade

Anti-dripping

ABS powder

(Impact Modifier)

Green ABS

5

Operation Performance

6 Source: Platts, IRPC Analysis Team

20

40

60

80

100

120

140

160

180

Dubai

ULG

Gasoil

Fuel Oil

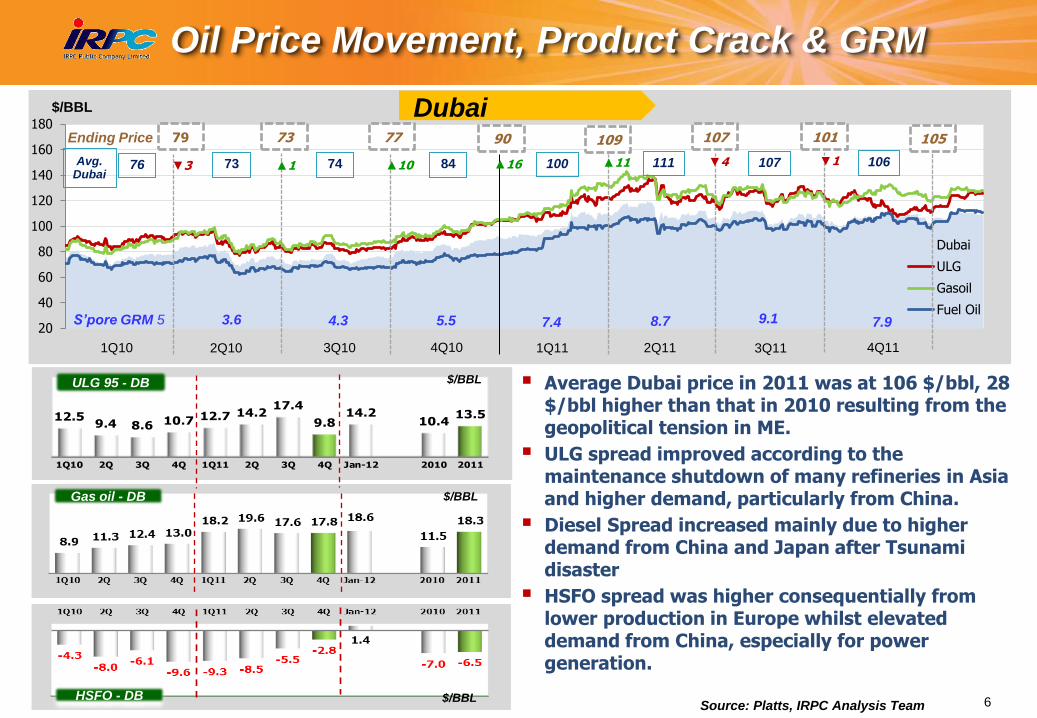

79 73 77 90 109 107 101 Ending Price

100 111 107 76 73 74 84 Avg. Dubai

Dubai $/BBL

S’pore GRM 5 3.6 4.3 5.5 7.4 8.7 7.9

▲1 ▼3 ▲16 ▲10 ▲11 ▼4

Oil Price Movement, Product Crack & GRM

9.1

▼1

105

106

4Q10 1Q11 2Q11 3Q10 2Q10 1Q10 4Q11 3Q11

$/BBL Gas oil - DB

1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q Jan-12 2010 2011

12.59.4 8.6 10.7 12.7 14.2

17.4

9.814.2

10.413.5

$/BBL ULG 95 - DB

$/BBL HSFO - DB

Average Dubai price in 2011 was at 106 $/bbl, 28 $/bbl higher than that in 2010 resulting from the geopolitical tension in ME.

ULG spread improved according to the maintenance shutdown of many refineries in Asia and higher demand, particularly from China.

Diesel Spread increased mainly due to higher demand from China and Japan after Tsunami disaster

HSFO spread was higher consequentially from lower production in Europe whilst elevated demand from China, especially for power generation.

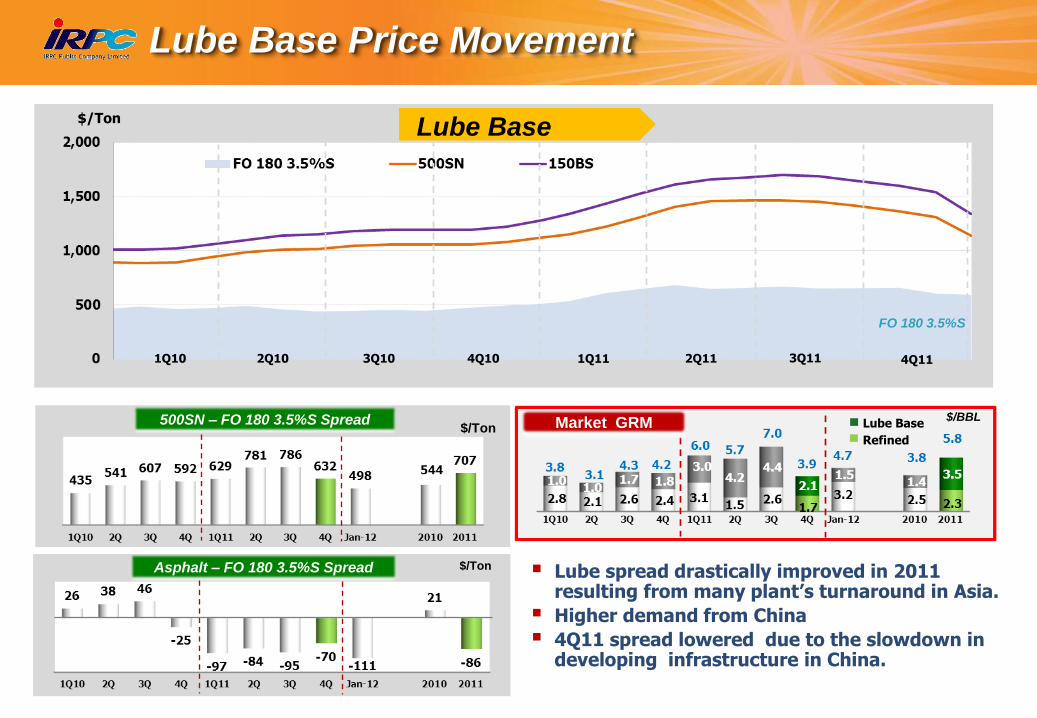

500SN – FO 180 3.5%S Spread

1Q10 3Q10 2Q10 4Q10

$/Ton

1Q11 2Q11 3Q11

Lube Base Price Movement

Lube Base

Asphalt – FO 180 3.5%S Spread

$/Ton

$/Ton

FO 180 3.5%S

4Q11

Lube Base

Refined

Market GRM $/BBL

Lube spread drastically improved in 2011 resulting from many plant’s turnaround in Asia.

Higher demand from China

4Q11 spread lowered due to the slowdown in developing infrastructure in China.

$/Ton

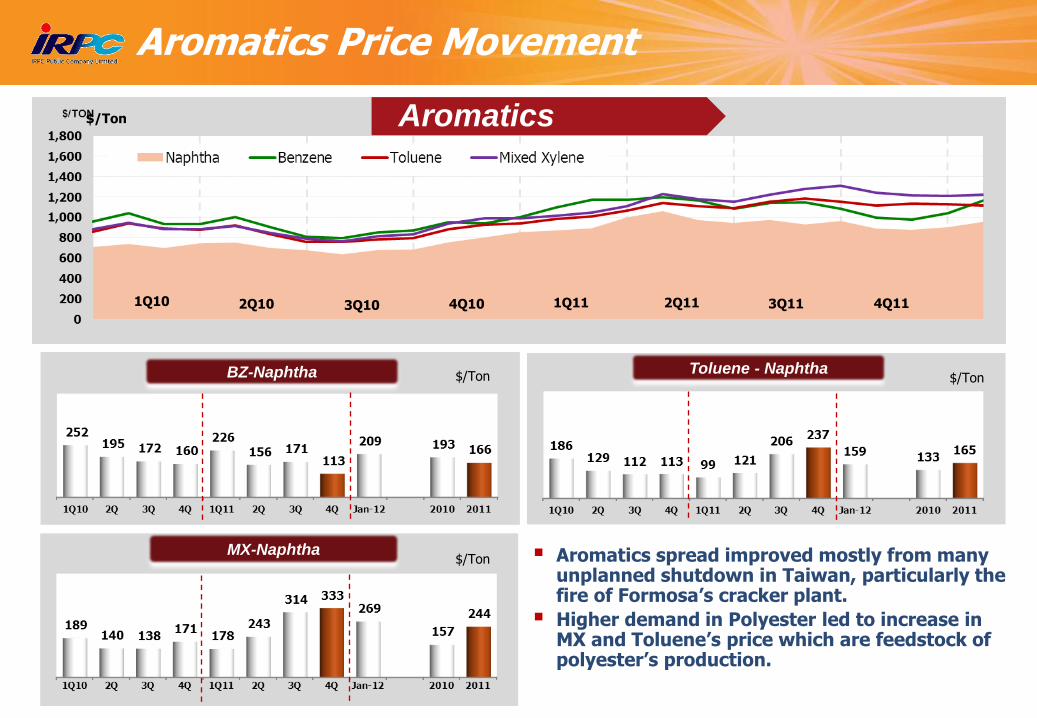

MX-Naphtha

BZ-Naphtha Toluene - Naphtha

Aromatics Price Movement

Aromatics

$/Ton $/Ton

$/Ton Aromatics spread improved mostly from many unplanned shutdown in Taiwan, particularly the fire of Formosa’s cracker plant.

Higher demand in Polyester led to increase in MX and Toluene’s price which are feedstock of polyester’s production.

1Q10 3Q10 2Q10 4Q10 1Q11 3Q11 4Q11 2Q11

0

500

1,000

1,500

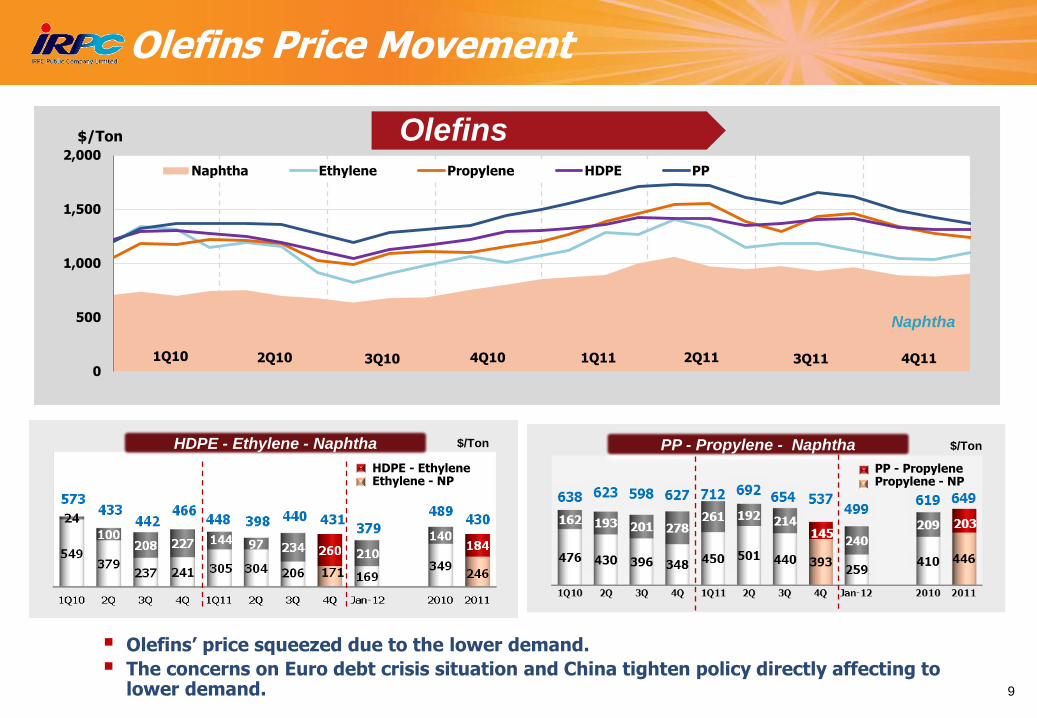

2,000Naphtha Ethylene Propylene HDPE PP

$/Ton

Olefins Price Movement

HDPE - Ethylene - Naphtha $/Ton $/Ton PP - Propylene - Naphtha

Olefins

Naphtha

HDPE - Ethylene Ethylene - NP

PP - Propylene Propylene - NP

Olefins’ price squeezed due to the lower demand.

The concerns on Euro debt crisis situation and China tighten policy directly affecting to lower demand.

431

9

1Q10 3Q10 2Q10 4Q10 1Q11 3Q11 4Q11 2Q11

$/Ton

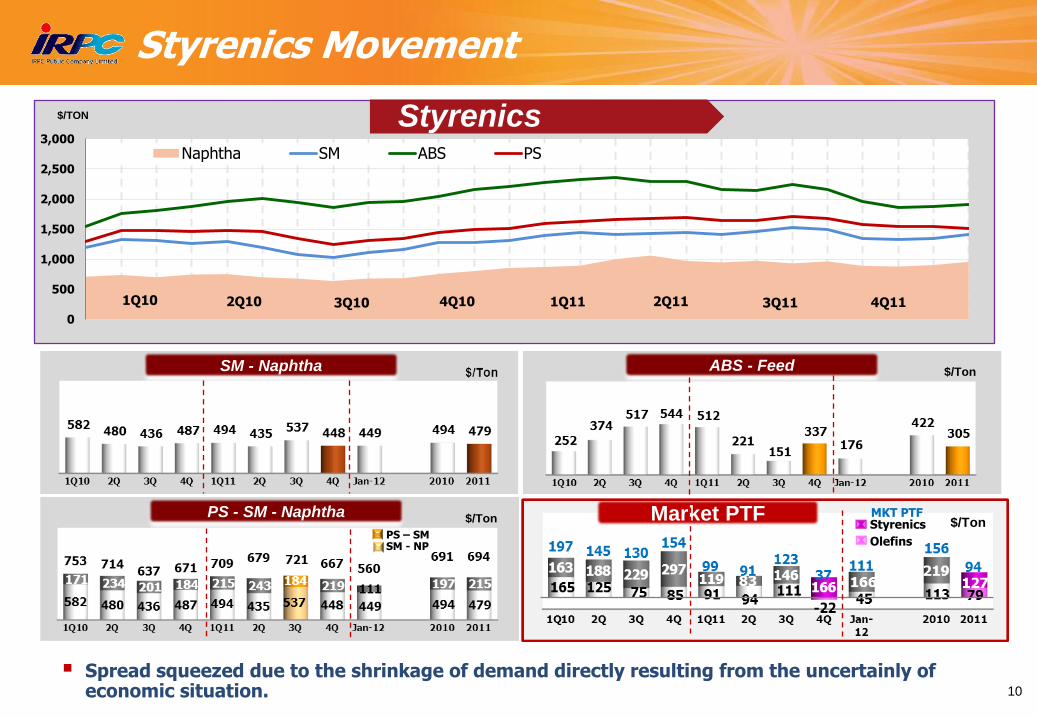

Styrenics Movement

1Q10 3Q10 2Q10 4Q10 1Q11 2Q11 3Q11

10

$/Ton

$/Ton PS - SM - Naphtha

ABS - Feed

PS – SM SM - NP

Styrene

$/Ton Market PTF Styrenics

Olefins

MKT PTF

SM - Naphtha

Spread squeezed due to the shrinkage of demand directly resulting from the uncertainly of economic situation.

0

500

1,000

1,500

2,000

2,500

3,000

$/TON

Naphtha SM ABS PS

Styrenics

1Q10 3Q10 2Q10 4Q10 1Q11 3Q11 4Q11 2Q11

GRM & PTF

11

2.8 2.1 2.6 2.4

3.1

1.5 2.6

1.9 2.5 2.3

1.0

1.0

1.7 1.8

3.0

4.2

4.4

2.6 1.4

3.5 3.8

3.1

4.3 4.2

6.0 5.7

7.0

4.5 3.8

5.8

1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q 2010 2011

3.4 2.1

1.2 1.4 1.7 1.7 1.9

(0.6)

2.0 1.4

0.1

0.2

0.3 0.9 0.6 0.5

1.2

1.3

0.4 0.9

1.3

1.4 1.7

1.7 0.6 0.4

0.2

0.5

1.5

0.3

4.9

3.7 3.2

3.9

2.8 2.6 3.3

1.2

4.0

2.6

1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q 2010 2011

Lube Base

Refined

$/BBL

3.8 3.1 4.3 4.2 6.0 5.7 7.0

4.5 3.8

5.8

4.9 3.7 3.2 3.9

2.8 2.6 3.3

1.2 4.0 2.6

8.8 6.8 7.5 8.1 8.9 8.3

10.3

5.7 7.8 8.4

1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q 2010 2011

Market GIM $/BBL

3.4 3.2 3.1 5.5

10.4 8.0

2.8 3.6 3.8 6.3

6.7 5.1

2.8

4.4

4.5

4.3

3.4 1.2 4.7

3.4

10.0 8.3

6.0

9.8

14.8

12.3

6.2 4.9

8.5 9.7

1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q 2010 2011

Accounting GIM $/BBL

MKT GRM

MKT PTF

Petrochem

Petroleum

1.3 1.5

(1.6)

1.8

6.0

4.0

(4.1)

(0.8)

0.7 1.3

1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q 2010 2011

Styrenics

Aromatic

Olefins

Petrochem

Petroleum

Stock Gain/(Loss) Net LCM & Oil Hedging

$/BBL

$/BBL

Optimized Operation

129 135 89

126 121

49 40

32

48 39

178 176

121

174 160

4Q10 3Q11 4Q11 2010 2011

Sour

Sweet

Crude Intake

Petroleum Production Petrochemical Production

MBBL 16.41 16.17 11.10 63.61 58.25

Utilization 83% 82% 56% 81% 74%

16.4 MBBL

16.2 MBBL

11.1 MBBL

Other

Naphtha

Gasoline

Diesel

Fuel Oil Lube Base Oil

Asphalt

Unit : KBD

63.6 MBBL

58.2 MBBL

Utilization

IRPC has planned major turnaround for 49 day in 4Q11.

12

25% 26% 26% 25% 25%

38% 37% 36% 39% 38%

19% 17% 20% 18% 18%

18% 20% 18% 17% 19%

4Q10 3Q11 4Q11 2010 2011

Aromatic

Olefins

Polystyrenics

342 KTon

322 KTon

196 KTon

1,313 KTon

1,130 KTon

Polyolefins

13

Revenue Structure

Sale Volume (MBBL) 2011 2010

1. Gasoline 4.72 5.45

2. Gas Oil 24.79 26.11

3. Fuel Oil 8.41 7.55

4. Lube Base Oil & Asphalt 6.11 6.38

5. Others 5.34 4.85

Petroleum 49.37 50.34

1. Aromatics 1.86 2.05

2. Olefins 5.07 5.24

3. Styrenics 1.64 2.52

4. Polyol 0.11 0.12

Petrochem 8.69 9.92

Total 58.06 60.26

Refinery 62%

Lube 10%

Olefins 3%

Polyolefins

12%

Polyol

0.5%

Aromatics

4%

Polystyrenics

7%

Power & UT 1.2% Port & Tank

0.2%

Land & Others 0.4%

2010 200,744 MB

Refinery 66%

Lube 10%

Olefins 3%

Polyolefins 10%

Polyol 0.5%

Aromatics 4%

Polystyrenics 5%

Power & UT 1.3%

Port & Tank 0.2%

Land & Others 0.3%

2011 237,757

MB

76% of revenue came from refineries’ product.

Average 35% of both businesses were exported.

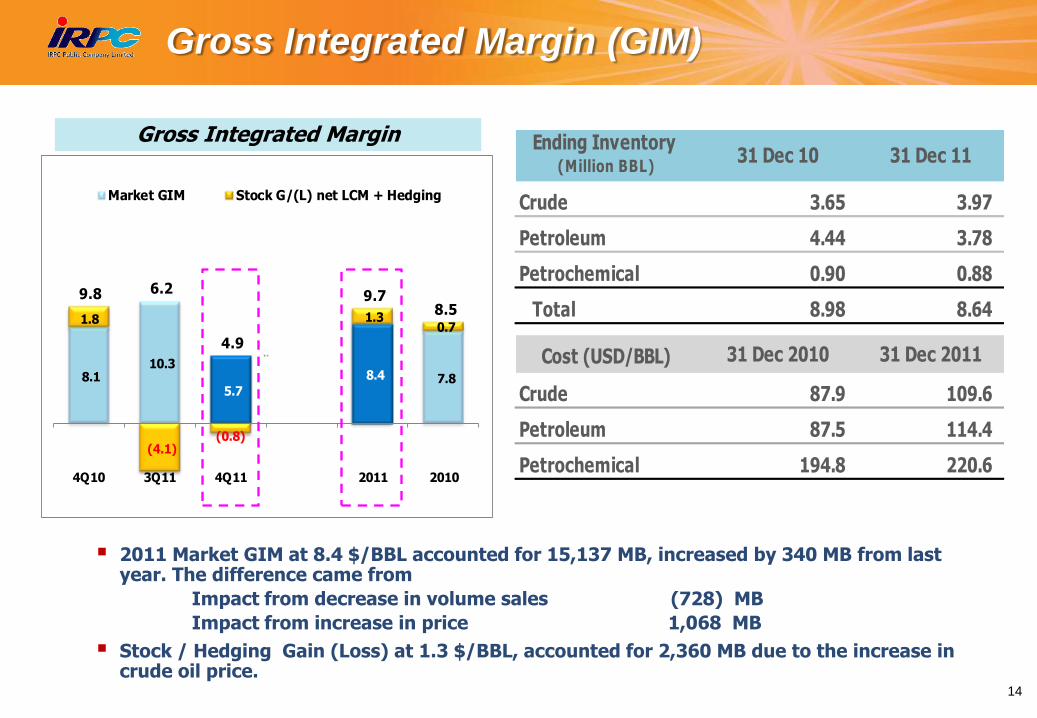

Gross Integrated Margin (GIM)

8.1 10.3

5.7

8.4 7.8

1.8

(4.1)(0.8)

1.3 0.7

9.8 6.2

4.9

9.7 8.5

4Q10 3Q11 4Q11 2011 2010

Market GIM Stock G/(L) net LCM + Hedging

Ending Inventory (Million BBL)

31 Dec 10 31 Dec 11

Crude 3.65 3.97

Petroleum 4.44 3.78

Petrochemical 0.90 0.88

Total 8.98 8.64

Cost (USD/BBL) 31 Dec 2010 31 Dec 2011

Crude 87.9 109.6

Petroleum 87.5 114.4

Petrochemical 194.8 220.6

2011 Market GIM at 8.4 $/BBL accounted for 15,137 MB, increased by 340 MB from last year. The difference came from

Impact from decrease in volume sales (728) MB

Impact from increase in price 1,068 MB

Stock / Hedging Gain (Loss) at 1.3 $/BBL, accounted for 2,360 MB due to the increase in crude oil price.

14

Gross Integrated Margin

15

Financial Performance

16

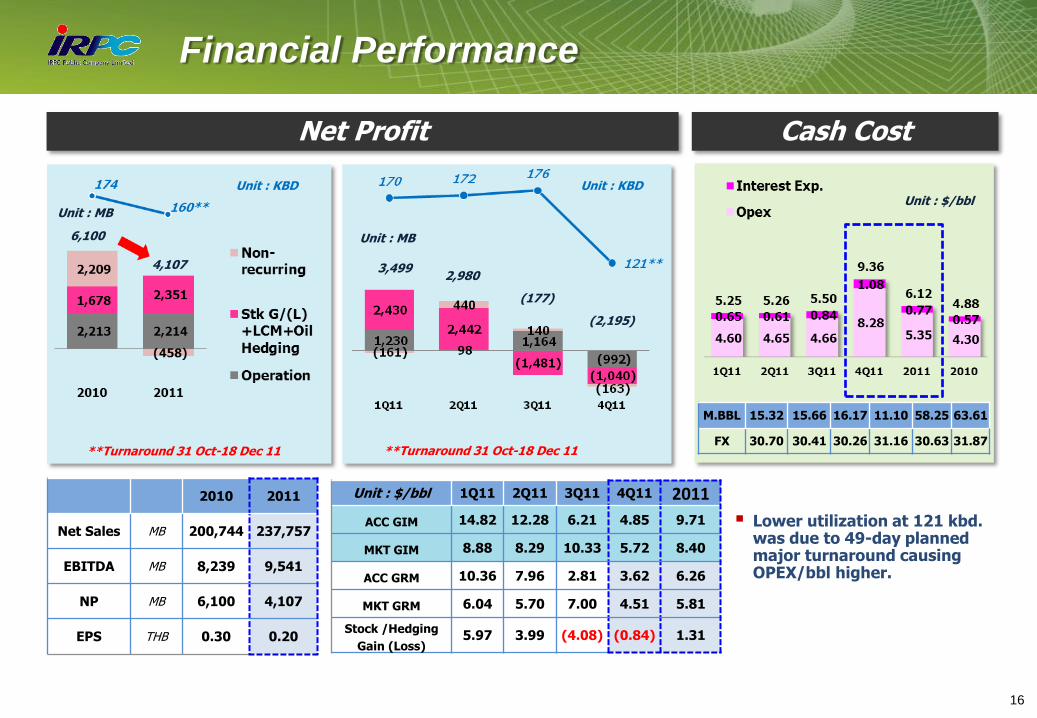

Financial Performance

Unit : $/bbl 1Q11 2Q11 3Q11 4Q11 2011

ACC GIM 14.82 12.28 6.21 4.85 9.71

MKT GIM 8.88 8.29 10.33 5.72 8.40

ACC GRM 10.36 7.96 2.81 3.62 6.26

MKT GRM 6.04 5.70 7.00 4.51 5.81

Stock /Hedging

Gain (Loss) 5.97 3.99 (4.08) (0.84) 1.31

Net Profit

2010 2011

Net Sales MB 200,744 237,757

EBITDA MB 8,239 9,541

NP MB 6,100 4,107

EPS THB 0.30 0.20

**Turnaround 31 Oct-18 Dec 11

Cash Cost

Unit : MB

Unit : MB

Unit : KBD Unit : KBD Unit : $/bbl

**Turnaround 31 Oct-18 Dec 11

M.BBL 15.32 15.66 16.17 11.10 58.25 63.61

FX 30.70 30.41 30.26 31.16 30.63 31.87

6,100

4,107 3,499 2,980

(177)

(2,195)

Lower utilization at 121 kbd. was due to 49-day planned major turnaround causing OPEX/bbl higher.

17

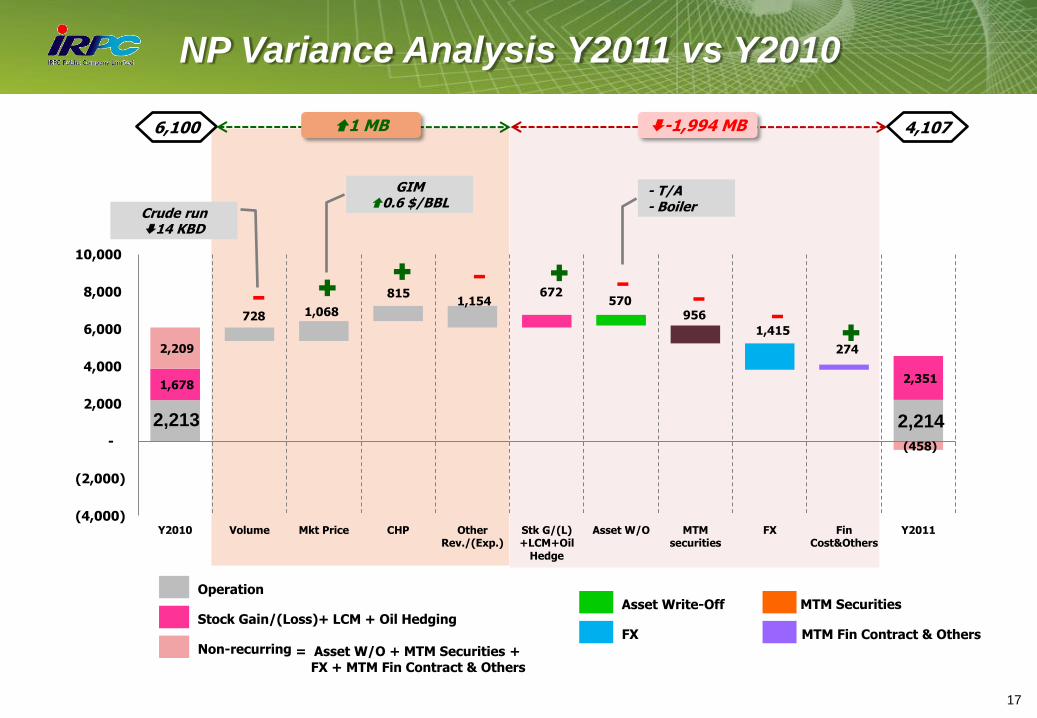

NP Variance Analysis Y2011 vs Y2010

2,213 2,214

728 1,068

815 1,154

1,678

672

2,351

2,209

570

(458)

956

1,415

274

(4,000)

(2,000)

-

2,000

4,000

6,000

8,000

10,000

Y2010 Volume Mkt Price CHP OtherRev./(Exp.)

Stk G/(L)+LCM+Oil

Hedge

Asset W/O MTMsecurities

FX FinCost&Others

Y2011

6,100 4,107 -1,994 MB

Asset Write-Off MTM Securities

FX MTM Fin Contract & Others

Crude run 14 KBD

GIM 0.6 $/BBL

- T/A - Boiler

1 MB

Operation

Non-recurring

Stock Gain/(Loss)+ LCM + Oil Hedging

= Asset W/O + MTM Securities + FX + MTM Fin Contract & Others

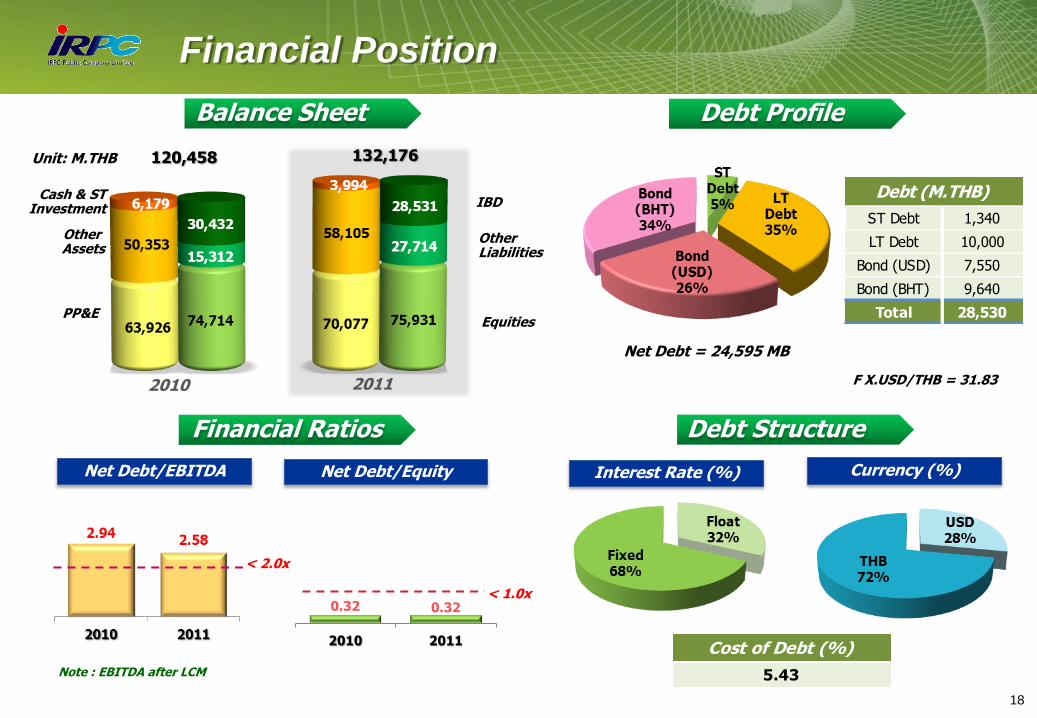

0.32 0.32

2010 2011

< 1.0x

Note : EBITDA after LCM

Cost of Debt (%)

5.43

18

Net Debt/EBITDA Net Debt/Equity

Financial Ratios

Balance Sheet

Debt Structure

Debt Profile

Interest Rate (%) Currency (%)

Cash & ST Investment

PP&E

IBD

Other Liabilities

Equities

2010 2011

120,458 132,176

Other Assets

Unit: M.THB

ST Debt 1,340

LT Debt 10,000

Bond (USD) 7,550

Bond (BHT) 9,640

Total 28,530

Debt (M.THB)

Net Debt = 24,595 MB

Fixed

Float USD

THB

Financial Position

< 2.0x

F X.USD/THB = 31.83

19

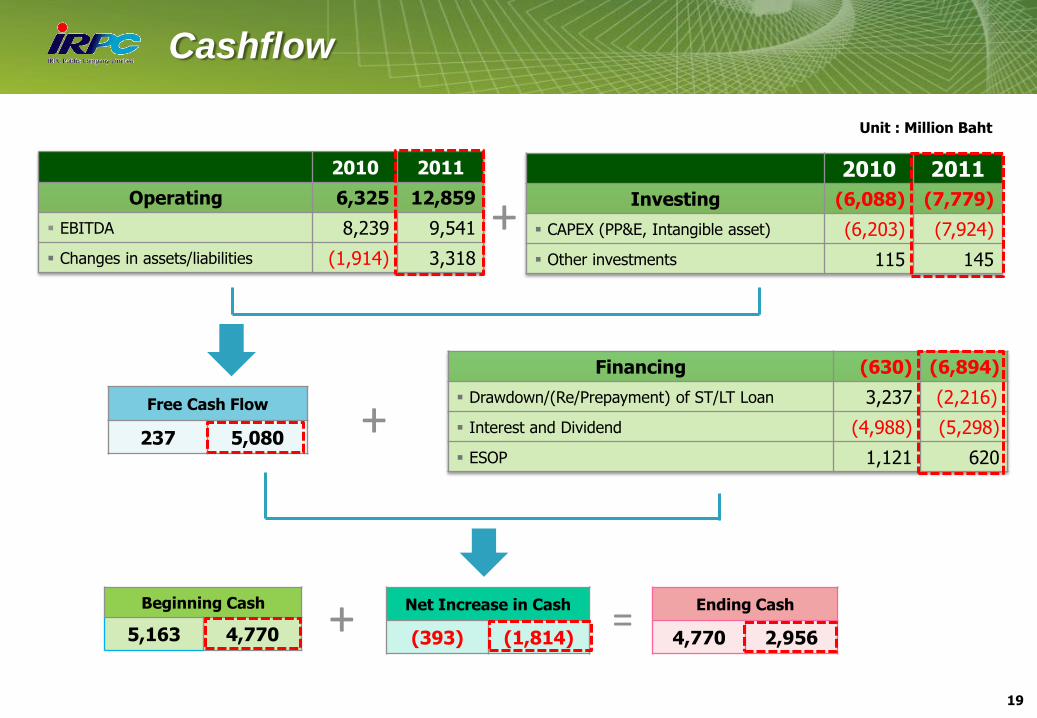

Cashflow

Unit : Million Baht

2010 2011

Operating 6,325 12,859

EBITDA 8,239 9,541

Changes in assets/liabilities (1,914) 3,318

+

+ =

Financing (630) (6,894)

Drawdown/(Re/Prepayment) of ST/LT Loan 3,237 (2,216)

Interest and Dividend (4,988) (5,298)

ESOP 1,121 620

Free Cash Flow

237 5,080

2010 2011

Investing (6,088) (7,779)

CAPEX (PP&E, Intangible asset) (6,203) (7,924)

Other investments 115 145

Ending Cash

4,770 2,956

Net Increase in Cash

(393) (1,814)

Beginning Cash

5,163 4,770

+

20

Outlook Industry

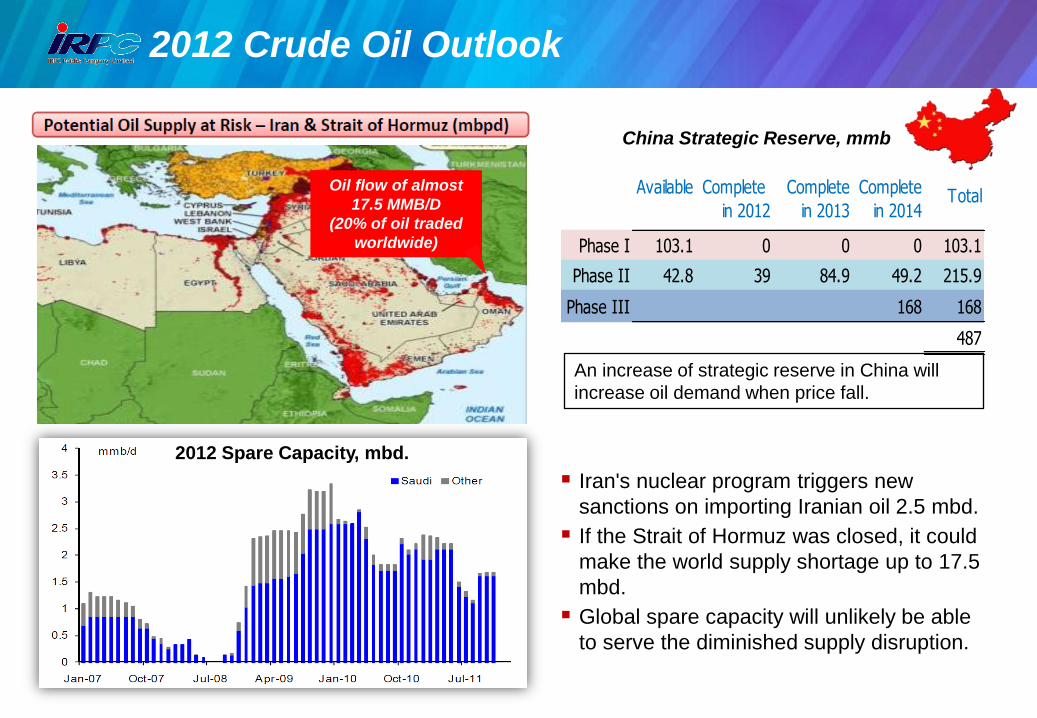

2012 Crude Oil Outlook

Available Complete

in 2012

Complete

in 2013

Complete

in 2014Total

Phase I 103.1 0 0 0 103.1

Phase II 42.8 39 84.9 49.2 215.9

Phase III 168 168

487

China Strategic Reserve, mmb

An increase of strategic reserve in China will

increase oil demand when price fall.

China Strategic Reserve, m.bbl. Available Complete

in 2012

Complete

in 2013

Complete

in 2014Total

Phase I 103.1 0 0 0 103.1

Phase II 42.8 39 84.9 49.2 215.9

Phase III 168 168

487

2012 Spare Capacity, mbd.

Iran's nuclear program triggers new

sanctions on importing Iranian oil 2.5 mbd.

If the Strait of Hormuz was closed, it could

make the world supply shortage up to 17.5

mbd.

Global spare capacity will unlikely be able

to serve the diminished supply disruption.

Oil flow of almost

17.5 MMB/D

(20% of oil traded

worldwide)

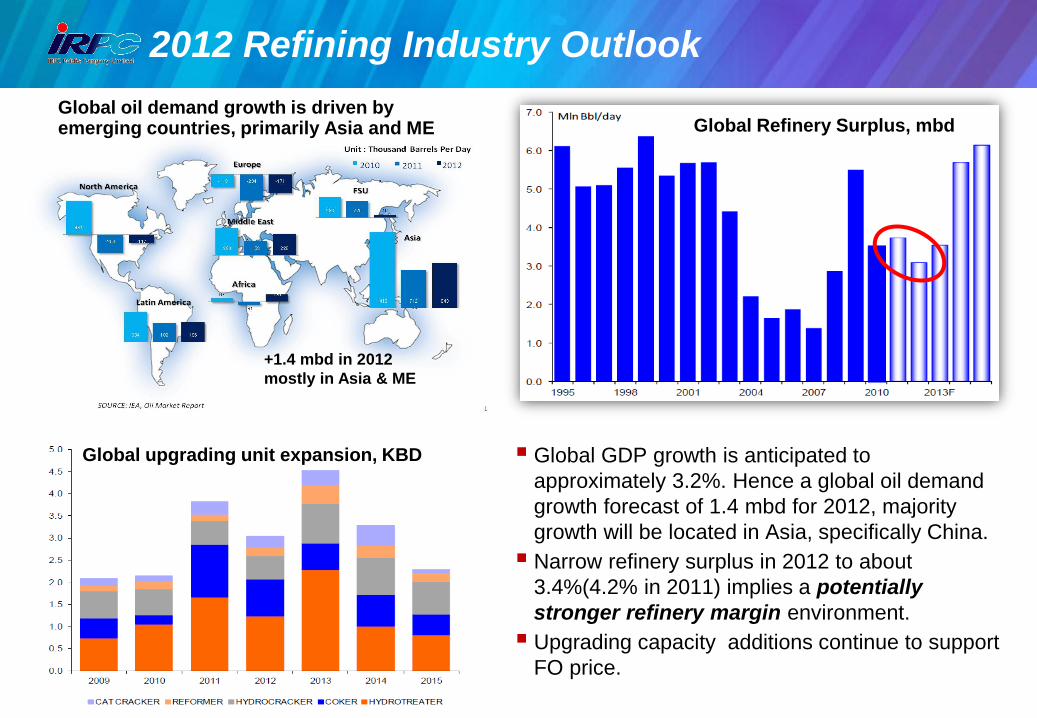

2012 Refining Industry Outlook

Global Refinery Surplus, mbd

Global upgrading unit expansion, KBD Global GDP growth is anticipated to

approximately 3.2%. Hence a global oil demand

growth forecast of 1.4 mbd for 2012, majority

growth will be located in Asia, specifically China.

Narrow refinery surplus in 2012 to about

3.4%(4.2% in 2011) implies a potentially

stronger refinery margin environment.

Upgrading capacity additions continue to support

FO price.

Global oil demand growth is driven by emerging countries, primarily Asia and ME

+1.4 mbd in 2012

mostly in Asia & ME

23

50%

60%

70%

80%

90%

100%

0.0

1.0

2.0

3.0

4.0

5.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

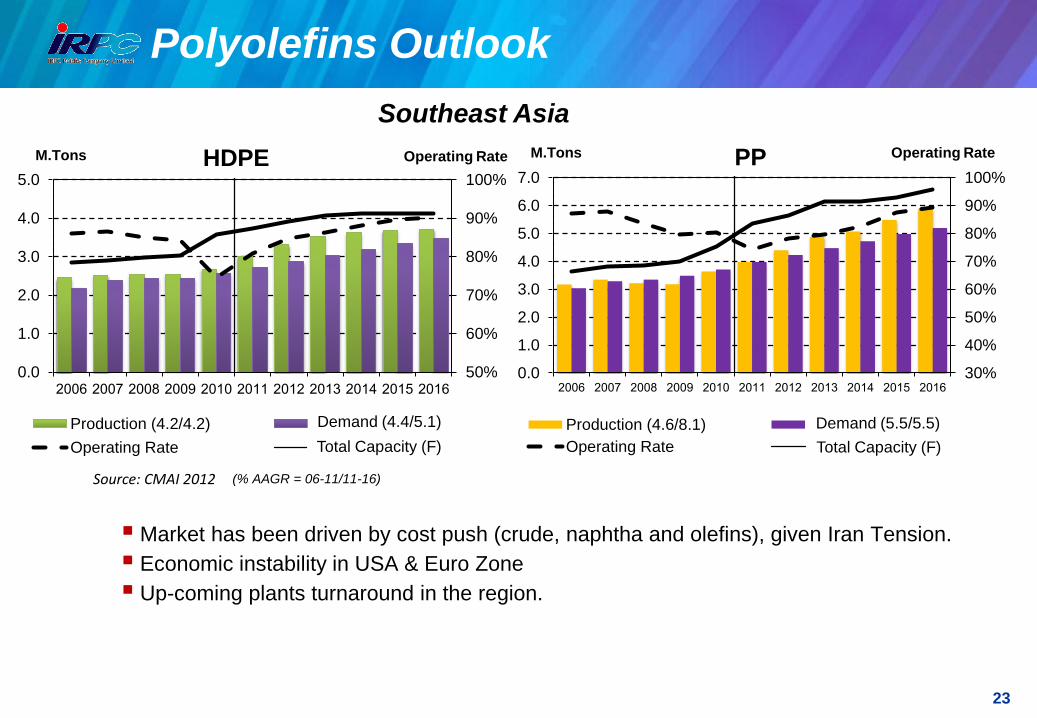

Production (4.2/4.2) Domestic Demand (4.4/5.1)

Operating Rate Forecast

Polyolefins Outlook

Source: CMAI 2012 (% AAGR = 06-11/11-16)

30%

40%

50%

60%

70%

80%

90%

100%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (4.6/8.1) Domestic Demand (5.5/5.5)

Operating Rate Forecast

Southeast Asia

Market has been driven by cost push (crude, naphtha and olefins), given Iran Tension.

Economic instability in USA & Euro Zone

Up-coming plants turnaround in the region.

M.Tons HDPE PP Operating Rate Operating Rate

Demand (4.4/5.1) Demand (5.5/5.5)

M.Tons

Total Capacity (F) Total Capacity (F)

24

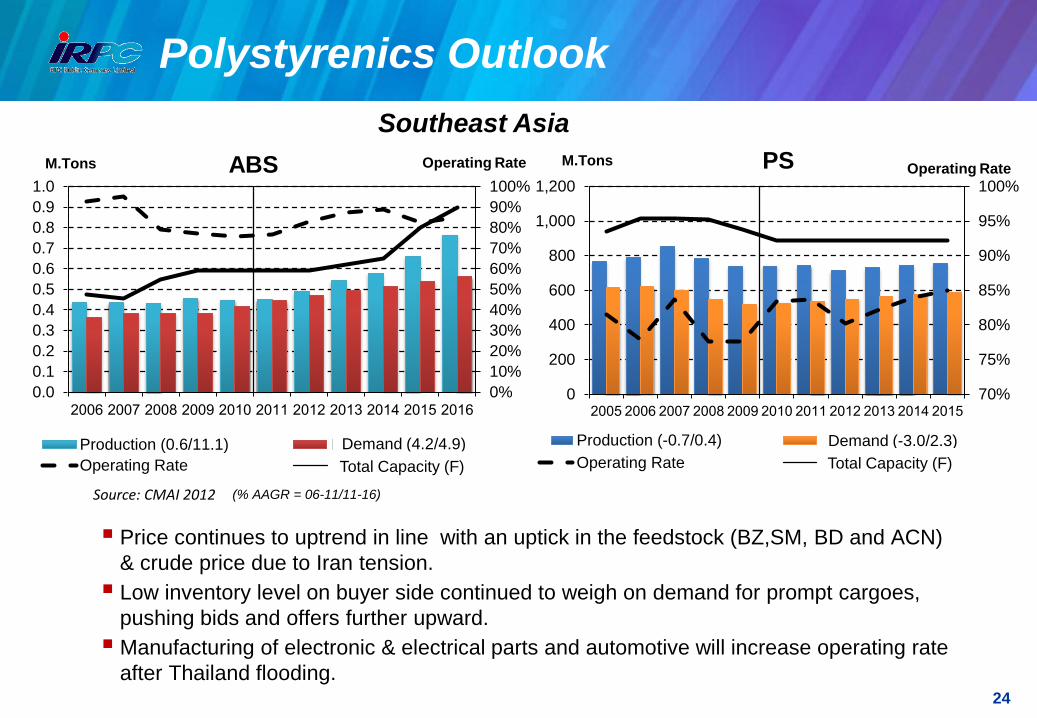

Polystyrenics Outlook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Production (0.6/11.1) Domestic Demand (4.2/4.9)

Operating Rate Forecast

70%

75%

80%

85%

90%

95%

100%

0

200

400

600

800

1,000

1,200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Production (-0.7/0.4) Domestic Demand (-3.0/2.3)

Operating Rate Forecast

Price continues to uptrend in line with an uptick in the feedstock (BZ,SM, BD and ACN)

& crude price due to Iran tension.

Low inventory level on buyer side continued to weigh on demand for prompt cargoes,

pushing bids and offers further upward.

Manufacturing of electronic & electrical parts and automotive will increase operating rate

after Thailand flooding.

Southeast Asia

M.Tons ABS PS M.Tons Operating Rate Operating Rate

Demand (-3.0/2.3)

Source: CMAI 2012 (% AAGR = 06-11/11-16)

Demand (4.2/4.9)

Total Capacity (F) Total Capacity (F)

25

Project Progress

TIME

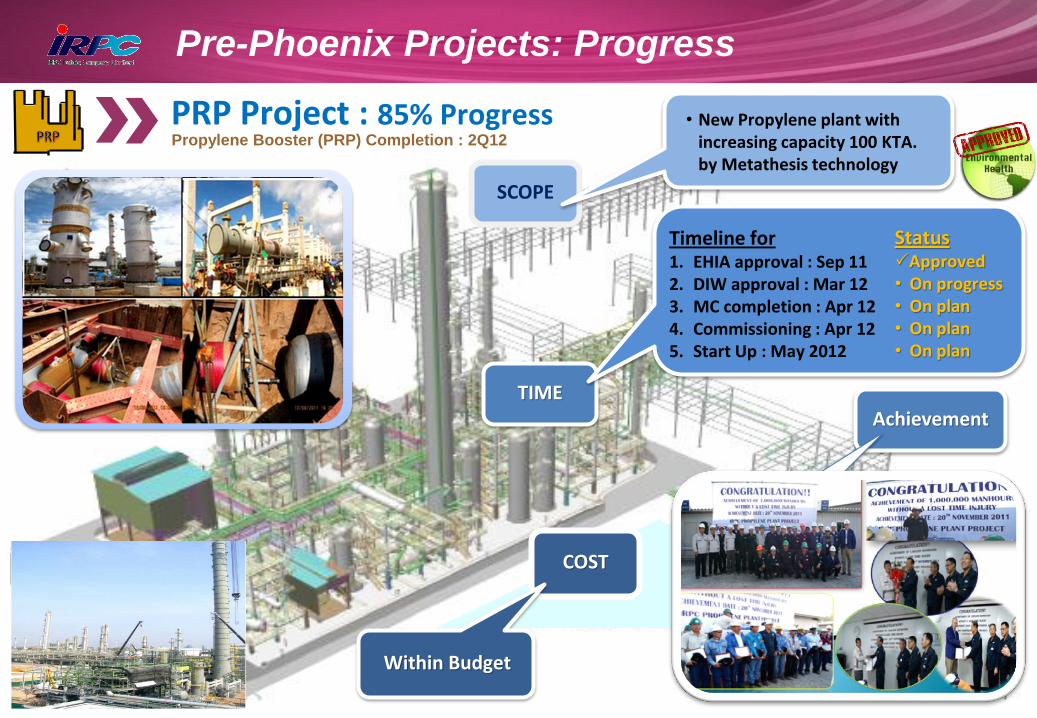

Pre-Phoenix Projects: Progress

PRP Project : 85% Progress

COST

Propylene Booster (PRP) Completion : 2Q12

Timeline for 1. EHIA approval : Sep 11 2. DIW approval : Mar 12 3. MC completion : Apr 12 4. Commissioning : Apr 12 5. Start Up : May 2012

Status Approved • On progress • On plan • On plan • On plan

Within Budget

Achievement

SCOPE

• New Propylene plant with increasing capacity 100 KTA. by Metathesis technology

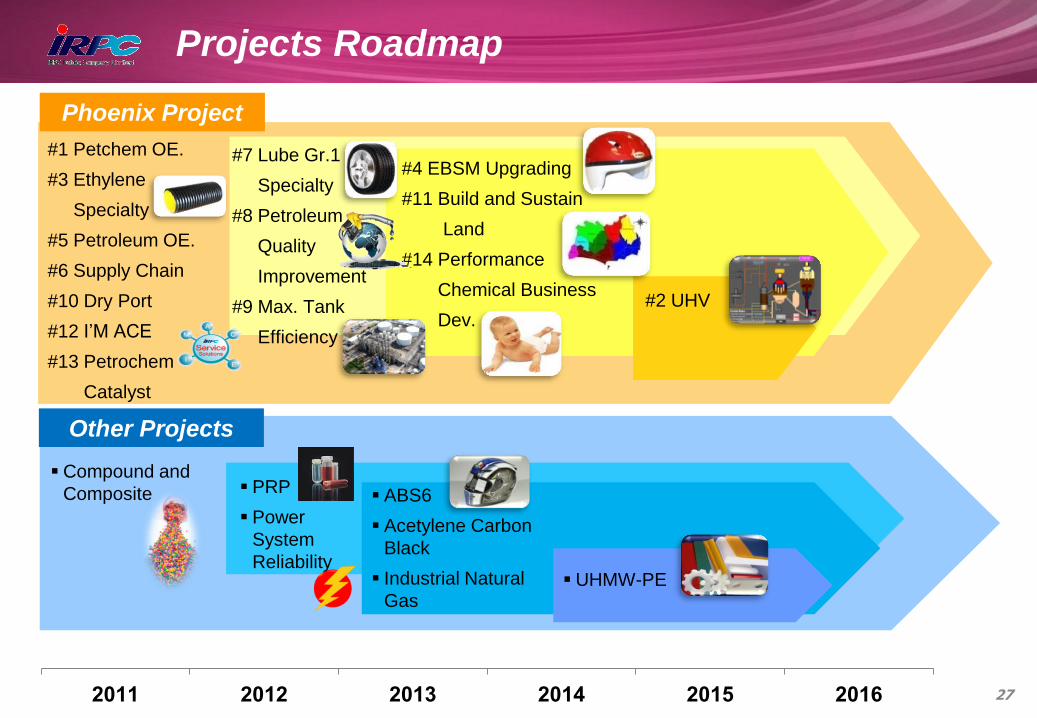

Projects Roadmap

2011 2012 2013 2014 2015 2016

#1 Petchem OE.

#3 Ethylene

Specialty

#5 Petroleum OE.

#6 Supply Chain

#10 Dry Port

#12 I’M ACE

#13 Petrochem

Catalyst

#7 Lube Gr.1

Specialty

#8 Petroleum

Quality

Improvement

#9 Max. Tank

Efficiency

#4 EBSM Upgrading

#11 Build and Sustain

Land

#14 Performance

Chemical Business

Dev. #2 UHV

Phoenix Project

ABS6

Acetylene Carbon

Black

Industrial Natural

Gas

PRP

Power

System

Reliability

Other Projects

UHMW-PE

Compound and

Composite

27

Initiative No. STATUS

#1: Petrochem Operation and

Energy Efficiency

• ETP : Under Back Pressure Turbine modification.

• HDPE : Under package preparation for Butene-1 plant

improvement .

• PP: Complete air transportation system for pellet and going on

TSA of PP Plant Improvement.

#2: Upstream Project for Hygiene

and Value Added Products (UHV)

• Licensors and EHIA consultant selected. Basic Engineering

Design is developing.

#3: Ethylene Specialty Products • DHU Phase I: Complete construction.

• DHU Phase II: Basic Engineering Design is developing.

#4: EBSM Upgrading for ABS

Specialties

• EBSM upgrading: EHIA approved by ONEP on June 2011.

• Public hearing has already been done.

#5: Petroleum Operation and

Energy Efficiency

• During selection of quick-hit projects to improve operating

condition.

• During clarification the Energy Efficiency Improvement proposal

from PTTES.

#6: Supply Chain Optimization

(Griffin and Trading)

• Complete ISC phase 1 : Orion Program for schedule control

implementation.

#7: Lube Group I Specialty

Products Focus • Under construction and expected to be completed in June 2012

Execute Study

Phoenix Projects: Progress

E

E

E

E

E

E

E

E

S

28

25%

50%

75%

100%

0%

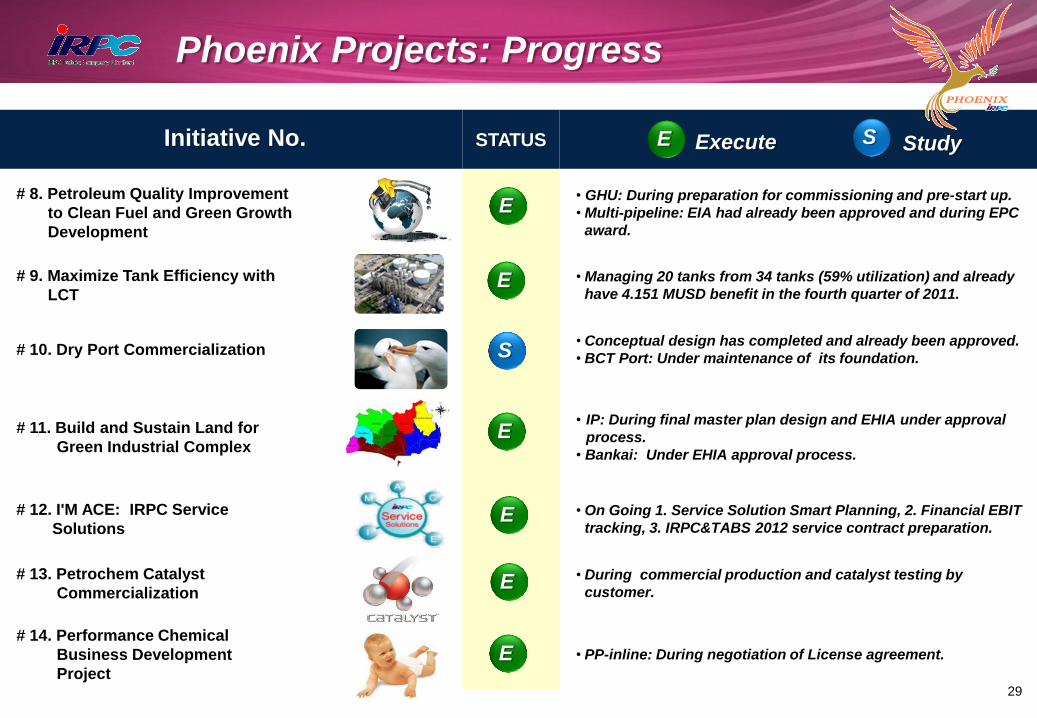

Initiative No. STATUS

# 8. Petroleum Quality Improvement

to Clean Fuel and Green Growth

Development

• GHU: During preparation for commissioning and pre-start up.

• Multi-pipeline: EIA had already been approved and during EPC

award.

# 9. Maximize Tank Efficiency with

LCT

• Managing 20 tanks from 34 tanks (59% utilization) and already

have 4.151 MUSD benefit in the fourth quarter of 2011.

# 10. Dry Port Commercialization • Conceptual design has completed and already been approved.

• BCT Port: Under maintenance of its foundation.

# 11. Build and Sustain Land for

Green Industrial Complex

• IP: During final master plan design and EHIA under approval

process.

• Bankai: Under EHIA approval process.

# 12. I'M ACE: IRPC Service

Solutions

• On Going 1. Service Solution Smart Planning, 2. Financial EBIT

tracking, 3. IRPC&TABS 2012 service contract preparation.

# 13. Petrochem Catalyst

Commercialization

• During commercial production and catalyst testing by

customer.

# 14. Performance Chemical

Business Development

Project

• PP-inline: During negotiation of License agreement.

Execute Study

Phoenix Projects: Progress

S

E

E

E

E

E

E

E S

29

25%

50%

75%

100%

0%

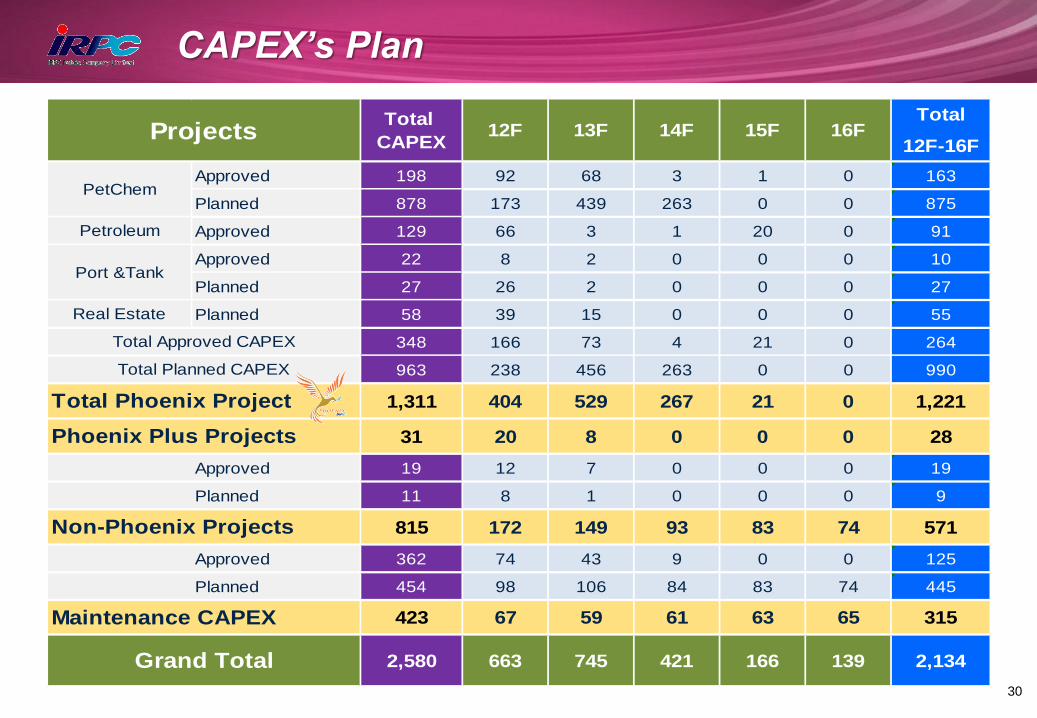

CAPEX’s Plan

30

25%

50%

75%

100%

0%

Total

12F-16F

Approved 198 92 68 3 1 0 163

Planned 878 173 439 263 0 0 875

Approved 129 66 3 1 20 0 91

Approved 22 8 2 0 0 0 10

Planned 27 26 2 0 0 0 27

Planned 58 39 15 0 0 0 55

348 166 73 4 21 0 264

963 238 456 263 0 0 990

1,311 404 529 267 21 0 1,221

31 20 8 0 0 0 28

Approved 19 12 7 0 0 0 19

Planned 11 8 1 0 0 0 9

815 172 149 93 83 74 571

Approved 362 74 43 9 0 0 125

Planned 454 98 106 84 83 74 445

423 67 59 61 63 65 315

2,580 663 745 421 166 139 2,134

15FProjectsTotal

CAPEX

Total Phoenix Project

Total Planned CAPEX

12F 13F

Petroleum

Total Approved CAPEX

Port &Tank

16F

Maintenance CAPEX

Phoenix Plus Projects

Non-Phoenix Projects

Grand Total

Real Estate

PetChem

14F

Refinery 23%

Lube 43%

Olefins 9%

Polyolefins -3%

Polyol 0.9%

Aromatics 3%

Polystyrenics 4% Power & UT

10% Port & Tank

1.9%

Land & Others 1.7%

2011

Refinery 21%

Lube 26% Olefins

32%

Polyolefins 5%

Polyol 1%

Aromatics 2%

Polystyrenics 2%

Power & UT 2%

Port & Tank 2%

Land & Others

7%

2016

Refinery 66%

Lube 10%

Olefins 3%

Polyolefins 10%

Polyol 0.5%

Aromatics 4%

Polystyrenics 5%

Power & UT 1.3%

Port & Tank 0.2%

Land & Others 0.3%

2011

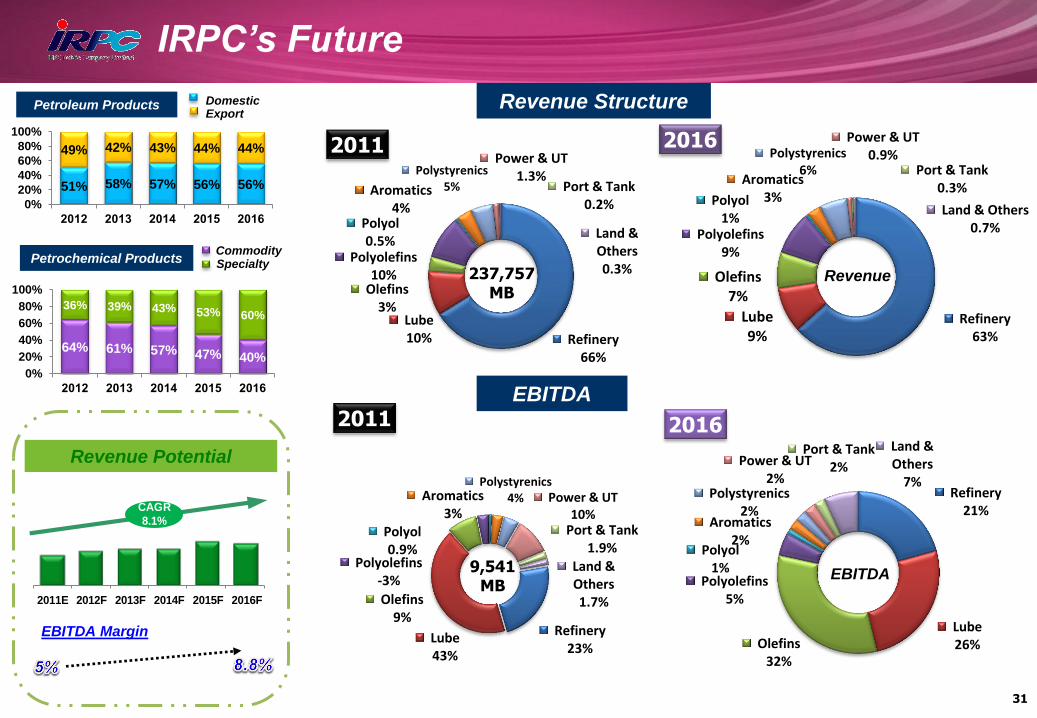

IRPC’s Future

Revenue Structure

Refinery 63%

Lube 9%

Olefins 7%

Polyolefins 9%

Polyol 1%

Aromatics 3%

Polystyrenics 6%

Power & UT 0.9%

Port & Tank 0.3%

Land & Others 0.7%

2016

EBITDA

237,757 MB

9,541 MB

31

2011E 2012F 2013F 2014F 2015F 2016F

CAGR

8.1%

Revenue Potential

EBITDA Margin

Petroleum Products

51% 58% 57% 56% 56%

49% 42% 43% 44% 44%

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016

Domestic Export

Petrochemical Products

64% 61% 57% 47% 40%

36% 39% 43% 53% 60%

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016

Commodity Specialty

Revenue

EBITDA

32

This presentation material has been prepared solely for informational purposes only. IRPC is furnishing it solely for use by prospective investors / analysts in

the proposed event. IRPC makes no representations or warranties as to the accuracy or completeness of such information. By accepting this material each

recipient agrees that IRPC shall not have any liability for any representations (express or implied) contained in, or for any omissions from this presentation.

The information contained herein does not purport to be all-inclusive or to contain all of the Information that may be material to the recipient’s decision. Each

recipient of the information and data contained herein should perform its own independent investigation and analysis of the transaction and the creditworthiness of IRPC . Reference in this Disclaimer to this shall include references to the Appendices (if any) hereto.

Investor Relations Contact : [email protected] Tel. 02-649-7384-8, Fax. 02-649-7379

presentation is available at

www.irpc.co.th Click “Presentations”

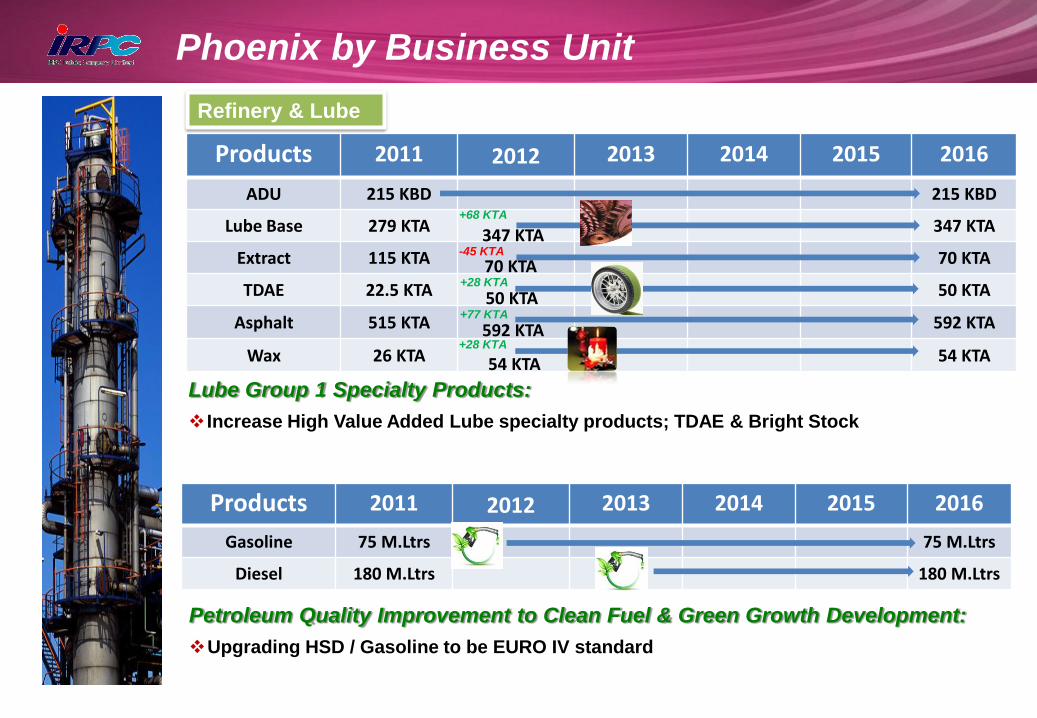

Phoenix by Business Unit

Refinery & Lube

ADU

Lube Base

Asphalt

Products 2011 2012 2013 2014 2015 2016

ADU 215 KBD 215 KBD

Lube Base 279 KTA 347 KTA

Extract 115 KTA 70 KTA

TDAE 22.5 KTA 50 KTA

Asphalt 515 KTA 592 KTA

Wax 26 KTA 54 KTA

Lube Group 1 Specialty Products:

Increase High Value Added Lube specialty products; TDAE & Bright Stock

+28 KTA

+68 KTA

Petroleum Quality Improvement to Clean Fuel & Green Growth Development:

Upgrading HSD / Gasoline to be EURO IV standard

Products 2011 2012 2013 2014 2015 2016

Gasoline 75 M.Ltrs 75 M.Ltrs

Diesel 180 M.Ltrs 180 M.Ltrs

-45 KTA

+77 KTA

347 KTA

70 KTA

50 KTA

592 KTA

54 KTA +28 KTA

Phoenix by Business Unit (Con’t)

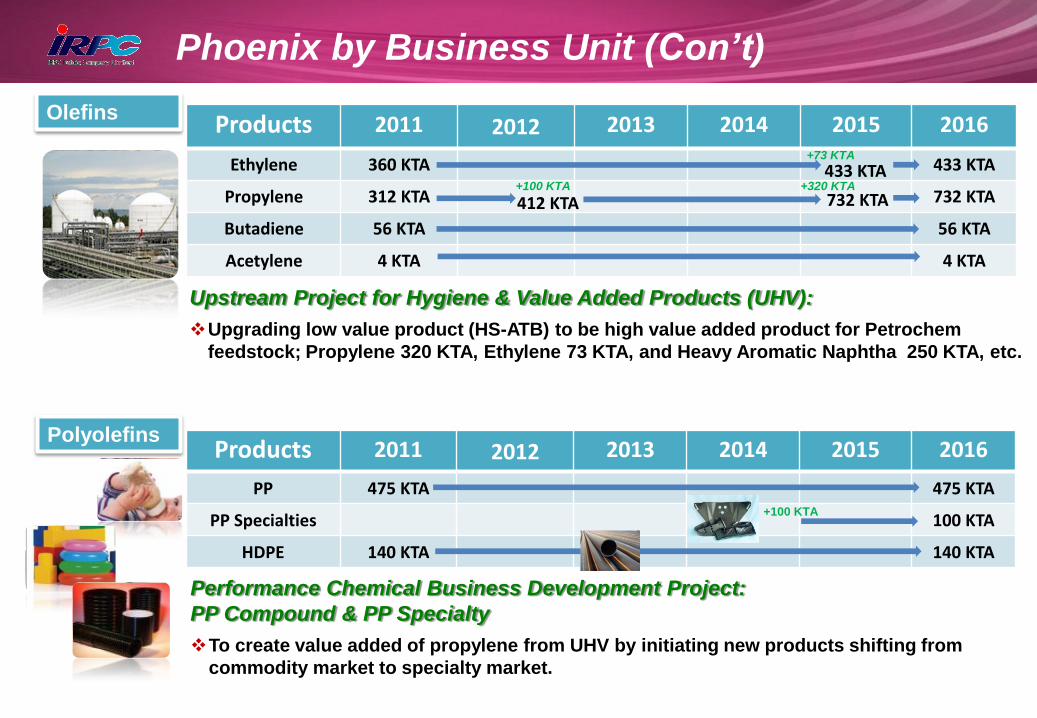

Olefins Products 2011 2012 2013 2014 2015 2016

Ethylene 360 KTA 433 KTA

Propylene 312 KTA 732 KTA

Butadiene 56 KTA 56 KTA

Acetylene 4 KTA 4 KTA

Upstream Project for Hygiene & Value Added Products (UHV):

Upgrading low value product (HS-ATB) to be high value added product for Petrochem

feedstock; Propylene 320 KTA, Ethylene 73 KTA, and Heavy Aromatic Naphtha 250 KTA, etc.

+320 KTA +100 KTA

+73 KTA

412 KTA 732 KTA

433 KTA

Polyolefins Products 2011 2012 2013 2014 2015 2016

PP 475 KTA 475 KTA

PP Specialties 100 KTA

HDPE 140 KTA 140 KTA

+100 KTA

Performance Chemical Business Development Project:

PP Compound & PP Specialty

To create value added of propylene from UHV by initiating new products shifting from

commodity market to specialty market.

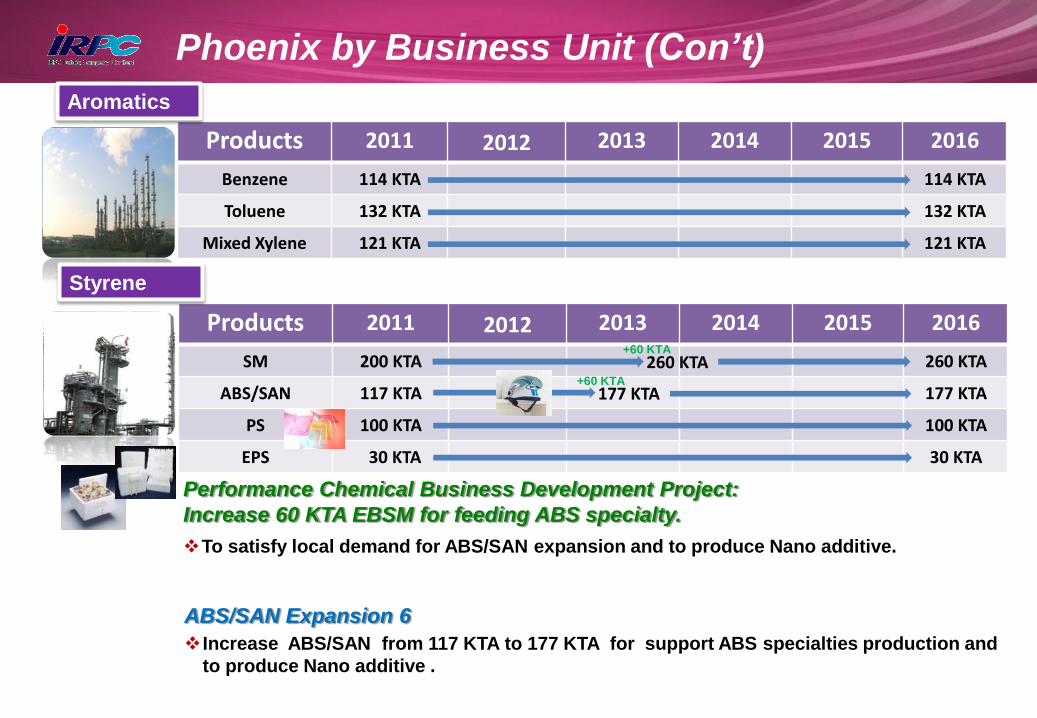

Products 2011 2012 2013 2014 2015 2016

Benzene 114 KTA 114 KTA

Toluene 132 KTA 132 KTA

Mixed Xylene 121 KTA 121 KTA

Products 2011 2012 2013 2014 2015 2016

SM 200 KTA 260 KTA

ABS/SAN 117 KTA 177 KTA

PS 100 KTA 100 KTA

EPS 30 KTA 30 KTA

+60 KTA

Performance Chemical Business Development Project:

Increase 60 KTA EBSM for feeding ABS specialty.

To satisfy local demand for ABS/SAN expansion and to produce Nano additive.

260 KTA

Styrene

Aromatics

Phoenix by Business Unit (Con’t)

+60 KTA 177 KTA

ABS/SAN Expansion 6

Increase ABS/SAN from 117 KTA to 177 KTA for support ABS specialties production and

to produce Nano additive .

Port & Tanks

Occupancy% 2011 2012 2013 2014 2015 2016

LCT 62 60 64 65 59 59

Maximize Tank Efficiency with LCT:

To increase the utilization of tanks and LCT port for service internal and external.

Phoenix by Business Unit (Con’t)

Dry Port Commercialization: Under studying process

To optimize port asset utilization and build sustainable port business.

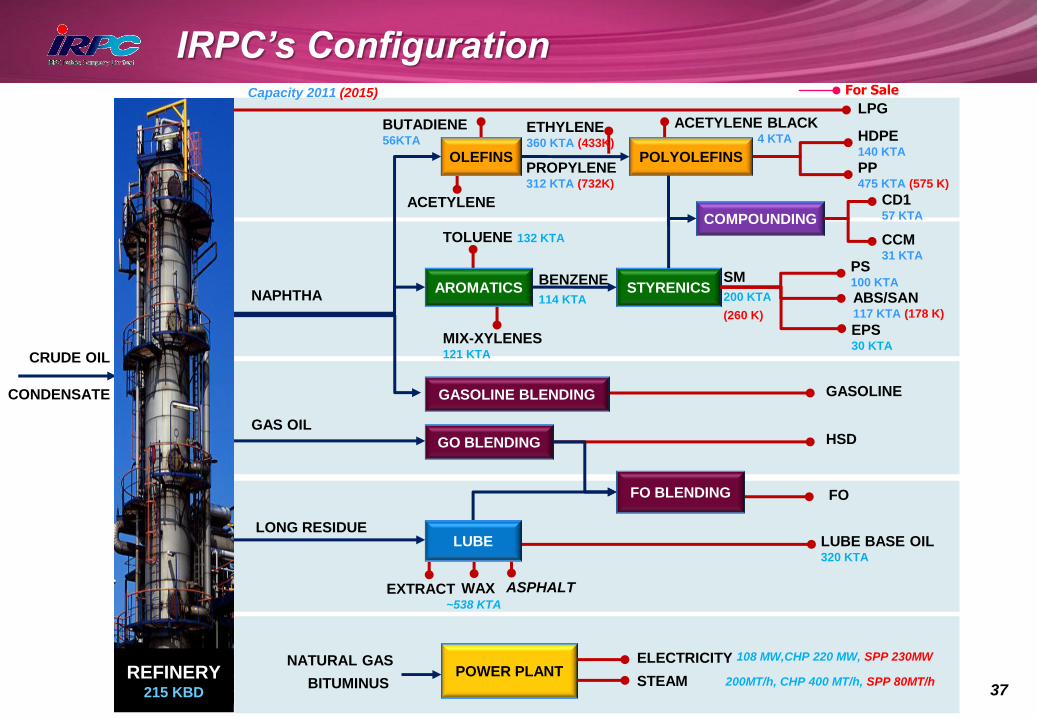

IRPC’s Configuration

37

25%

50%

75%

100%

0%

POWER PLANT NATURAL GAS ELECTRICITY

STEAM

LUBE BASE OIL 320 KTA

EXTRACT WAX

BITUMINUS

LUBE

STYRENICS

TOLUENE 132 KTA

BENZENE

114 KTA

MIX-XYLENES

121 KTA

AROMATICS

PS 100 KTA

ABS/SAN 117 KTA (178 K)

EPS 30 KTA

SM

200 KTA

(260 K)

HDPE 140 KTA

PP 475 KTA (575 K)

BUTADIENE 56KTA

ACETYLENE

ACETYLENE BLACK 4 KTA

OLEFINS PROPYLENE 312 KTA (732K)

ETHYLENE 360 KTA (433K)

POLYOLEFINS

COMPOUNDING

CD1 57 KTA

CCM 31 KTA

CRUDE OIL

CONDENSATE

NAPHTHA

LONG RESIDUE

GAS OIL

GO BLENDING HSD

GASOLINE BLENDING GASOLINE

REFINERY 215 KBD

FO BLENDING FO

LPG

ASPHALT ~538 KTA

108 MW,CHP 220 MW, SPP 230MW

200MT/h, CHP 400 MT/h, SPP 80MT/h

Capacity 2011 (2015) For Sale

![Discrete Mathematics Lecture Notes - National Taiwan …lyuu/dm/2012/20120223.pdf · · 2012-02-25Discrete Mathematics Lecture Notes ... [Harvard] college, there was not a single](https://img.pdfslide.us/doc/110x75/5ab6422e7f8b9a7c5b8d7dac/discrete-mathematics-lecture-notes-national-taiwan-lyuudm2012-mathematics.jpg)